Evaluating machine learning models in non-standard settings: An overview and new findings

Abstract

Estimating the generalization error (GE) of machine learning models is fundamental, with resampling methods being the most common approach. However, in non-standard settings, particularly those where observations are not independently and identically distributed, resampling using simple random data divisions may lead to biased GE estimates. This paper strives to present well-grounded guidelines for GE estimation in various such non-standard settings: clustered data, spatial data, unequal sampling probabilities, concept drift, and hierarchically structured outcomes. Our overview combines well-established methodologies with other existing methods that, to our knowledge, have not been frequently considered in these particular settings. A unifying principle among these techniques is that the test data used in each iteration of the resampling procedure should reflect the new observations to which the model will be applied, while the training data should be representative of the entire data set used to obtain the final model. Beyond providing an overview, we address literature gaps by conducting simulation studies. These studies assess the necessity of using GE-estimation methods tailored to the respective setting. Our findings corroborate the concern that standard resampling methods often yield biased GE estimates in non-standard settings, underscoring the importance of tailored GE estimation.

1 Introduction

In supervised machine learning (ML) applications, the fitted models and their predictions on new data are of primary interest, but it is also generally crucial to quantify the expected predictive performance. While performance estimation of ML models is a well-discussed topic in the literature, most works are confined to simple data structures. They often rely on the i.i.d. assumption, which posits that each data point is drawn independently from the same probability distribution. However, in practice, analysts frequently face non-standard settings, like spatial data. While the existing literature has highlighted certain concerns about performance estimation (for references, see the corresponding sections below) in this context, simulation studies in this paper aim to address gaps not previously covered. Standard resampling approaches can produce performance estimates that are either excessively variable or optimistically biased in non-standard settings. It is worth noting that such optimistic biases are generally more problematic than pessimistic ones, as outlined by (Roberts et al., 2017). In typical resampling processes, based on the i.i.d. assumption, the observations are randomly allocated to any of the data subsets during the division into training and test sets. In many non-standard settings, however, more advanced resampling techniques may be required.

The main contribution of this paper is that it offers a unifying overview and guidance on using such techniques in various non-standard settings. While substantial literature exists on coping with most frequently encountered non-standard settings per se, for most of them, there is a shortage of results how to estimate performance as unbiasedly and accurately as possible. Hence, we complement, where appropriate, existing literature by our own insights derived from systematic simulation studies.

All non-standard settings considered in this paper are commonly found in official statistics, which makes it a prototypical field in need of the methods we discuss and evaluate. This importance is further underscored by the fact that a comprehensive quality assessment is constitutive in this field (Yung et al., 2022). Therefore, the application examples included are influenced to some extent by this field. Nevertheless, the described methods and our simulation study results claim general validity across all areas where these settings occur.

Concretely, we consider the following five common non-standard settings: clustered data, spatial data, unequal sampling probabilities, concept drift, and hierarchically structured outcomes, which are described in detail in the subsections of Section 3. To better acquaint the reader with these settings and their practical manifestations, we provide here examples from official statistics for each:

-

•

Clustered data (cf. Section 3.1): In the design of surveys and censuses, data are often clustered into groups, for example, households. Observations within these groups are typically more similar to each other than to observations from different groups.

-

•

Spatial data (cf. Section 3.2): Any type of data that includes geographic information can be considered spatial data. For instance, satellite imagery can be used to determine the type of land use in different areas (agricultural, urban, etc.). Here, regions close to each other are more similar in land use and other features than distant areas, leading to spatial correlations between neighbouring observations.

-

•

Unequal sampling probabilities (cf. Section 3.3): In many surveys, not all units have the same probability of being sampled. For example, oversampling is a common practice to ensure that subgroups of particular interest (e.g., minority groups or companies with exceptionally high revenues) are adequately represented in the sample. As a result of using unequal sampling probabilities, the sample does not follow the same distribution as the population from which it is sampled.

-

•

Concept drift (cf. Section 3.4): The distribution of data arriving in streams can change continuously, or even abruptly, over time. For instance, data on unemployment may be affected by steady changes in the skills required in the labour market or by economic structural breaks, respectively.

-

•

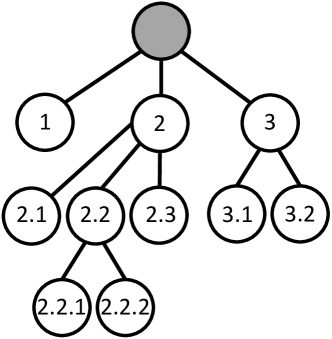

Hierarchically structured outcomes (cf. Section 3.5): In some classification problems, the observations do not belong to single classes but to a hierarchy of classes, with each class nested within a broader category. For instance, Class 1.3.2 may be a subclass within Class 1.3, which itself may be a subclass nested under the broader category of Class 1. Indeed, in official statistics, most classification systems are hierarchical. An example is the hierarchical occupational classification scheme ISCO-08 by the International Labour Organization (ILO) (International Labour Organization, 2012). The hierarchical structure of such schemes provides valuable information in statistical analyses, which has to be taken into account properly.

Several empirical studies have conducted comparisons of commonly used resampling approaches under the assumption of i.i.d. situations (Kohavi, 1995; Braga-Neto and Dougherty, 2004; Molinaro et al., 2005). For non-standard settings, however, literature on choosing appropriate approaches for performance estimation predominantly focuses on spatial data. We close this gap and conduct simulation studies comparing different approaches to performance evaluation when other types of non-standard settings are present. In these studies, we have deliberately structured the data-generating processes to be as consistent as possible across the different settings. For instance, all simulations maintain the same number of features. By ensuring similar structures for the data-generating processes, we minimize the potential for unintended result-dependent choices or overly specific configurations, thus enhancing the generalizability of our findings.

The remainder of this paper is structured as follows. Section 2 introduces general terminology and concepts related to supervised learning and losses (Section 2.1), performance metrics (Section 2.2), generalization errors (Section 2.3) and data splitting and resampling techniques (Section 2.4). Section 3 discusses the different non-standard settings enumerated above. Depending on the specific setting, we provide varying amounts of background information, but always elaborate extensively on performance estimation. Please note that readers primarily interested in specific settings can refer to the corresponding subsections in Section 3, instead of reading the entire section. For ease of reading, we provide a summary of the principal conclusions at the end of each subsection. In Section 4 we address several topics. First, we describe how suitable performance estimation methods can be developed for non-standard settings not addressed in this paper. We then briefly address model selection and tuning parameter optimization for non-standard settings. Finally, we discuss potential limitations of the simulation studies.

2 General strategies for evaluating ML models

In this section, we present a concise introduction to evaluating the performance of a supervised machine learning model, assuming the observations are i.i.d. samples. We outline terminology, notation and fundamental concepts such as performance metrics, the generalization error and data splitting and resampling. Readers familiar with these concepts can proceed to Section 3. Notably, in the non-standard contexts covered in Section 3, where observations typically are not i.i.d., the resampling methods detailed in Section 2.4 are usually inapplicable. We describe them here because in Section 3 they will be empirically compared with the resampling methods considered for the non-standard settings.

2.1 Terminology

The subsequent notation adheres to the conventions introduced in Bischl et al. (2023). Consider a labeled data set of observations, where each observation consists of a -dimensional feature vector and its corresponding label . We make the assumption that has been sampled i.i.d. from an unknown underlying distribution, denoted as . In the case of regression, the label space is defined as , whereas in classification, is a finite and categorical space with classes, where represents the cardinality. In supervised machine learning, an ML model is represented as a function ( for regression), mapping a feature vector from to a prediction in . In the case of classification, the outputs of in are typically the predicted probabilities for the classes.

The objective of supervised machine learning is using a learner to train a model using a data set of observations sampled from , aiming for good generalization performance on new, unseen observations generated by the same underlying data process. In general, the learner identifies by minimizing the empirical risk, defined as the sum of the losses across all observations . The loss function measures the discrepancy between the predictions and the true labels.

A prevalent problem in ML is overfitting, where the model aligns too perfectly with the given data set , capturing artifacts of that do not generalize to new data. For this reason, learners are configurable by hyperparameters that moderate the extent of adjustment of to . The value(s) of are not determined in the empirical risk minimization, but instead in a tuning step—typically via resampling procedures like cross-validation (CV) (see Section 2.4). After this step, the empirical risk minimization takes place with the constraint that remains fixed to the value(s) determined during tuning. We will not delve into detail about hyperparameter optimization and the concept of nested resampling, for which the reader is referred to Bischl et al. (2023).

2.2 Performance metrics

After training an ML model , a critical consideration is how to quantitatively measure its predictive performance. We seek to use a high-quality (i.e., consistent, efficient and ideally asymptotically normal) statistical estimator, which numerically quantifies the performance of our model when it is used to predict the labels of new observations drawn from the same data-generating process of the training data.

A general performance measure for an arbitrary test set of size is defined as a two-argument function that maps the -size vector of true labels and the matrix of prediction scores to a scalar performance value. This general definition based on sets is crucial for certain performance measures, such as the area under the ROC curve (AUC), and particularly for most measures used in survival analysis. These measures are distinct in that they require consideration of the relative order or dependencies between multiple observations, as opposed to measures like the mean squared error (MSE), which also aggregate over multiple observations but treat each observation independently.

It is possible to use the loss function applied during empirical risk minimization in performance measuring. However, it is common practice to select a performance measure depending on the specific prediction task at hand. During empirical risk minimization, this metric is often approximated using a computationally more efficient and potentially differentiable version of the performance measure.

2.3 Generalization error

To mitigate the risk of overfitting, it is essential to assess the performance of every model using unseen test data, thereby ensuring unbiased estimation of its performance. We use and to symbolize specified training and test sets with sizes of and , respectively. The generalization error (GE) of a learner , trained on observations, is defined as the expectation of a performance measure , with the expectation taken over both and . Performance measures that rely on non-point-wise losses require additionally.

The generalization error corresponds to the expectation of over infinitely many models, each fitted to a different realization of of size . This quantity tells us how well the learner (e.g., random forests) performs on average when trained and evaluated on data from the same distribution . However, practitioners are generally interested in how well a fixed model performs on unseen data from the same distribution as that of the training data used to construct . This type of performance can be measured by a quantity we refer to as the prediction error (PE), obtained by holding constant and taking the expectation solely over .

The focus of this paper is on GE rather than PE due to technical considerations. Resampling techniques, such as CV (refer to Section 2.4), are regarded as more suitable estimators of the GE than of the PE (Bates et al., 2023) because resampling generates a distinct model in each iteration. However, our results are also relevant for the PE because the latter can be expected to be similar to the GE. This becomes clear when acknowledging that the PE’s expectation (taken over ) is the GE.

2.4 Data splitting and resampling

Usually, the GE must be estimated from a single given data set of size . The holdout estimator serves as a straightforward approach to this task. First, is randomly split once into a training set of size and a test set of size . Second, the learner is applied to to produce a model , which is then used on to obtain predictions that are assessed using the performance measure .

The trade-off associated with the holdout estimator can be characterized as follows within the context of estimating GE: (i) Due to the necessity of being smaller than the total number of observations , splitting induces a pessimistic bias with respect to GE, as it does not utilize the entirety of the available data for training. In essence, the estimation is performed with respect to an incorrect training set size. (ii) When the training set is large, the corresponding test set becomes small, leading to increased variance in the estimator. This trade-off is influenced not only by the relative sizes of and , but also by the absolute number of observations. Both the learning error estimation based on observations and the test error estimation based on observations exhibits a saturating effect for larger sample sizes. Nevertheless, a common heuristic consists of selecting (Kohavi, 1995; Dobbin and Simon, 2011).

Resampling methods provide a partial solution to address this dilemma. These methods involve iteratively partitioning the available data into training and test sets, applying the second step of the holdout estimator to each split, and subsequently aggregating the resulting performance values. The aggregation is often performed by taking the mean. By repeatedly averaging over multiple splits the variance in estimating the generalization error is reduced (Kohavi, 1995; Simon, 2007). Moreover, the pessimistic bias inherent in a simple holdout approach can be minimized and nearly eliminated by selecting training sets of sizes close to the total number of observations (). In general, there is little reason to prefer the holdout estimator over a resampling method except for computational efficiency reasons (Hawkins et al., 2003; Raschka, 2020).

Among the various resampling methods, -fold CV is widely employed. This technique involves partitioning the data into subsets (or “folds”) of approximately equal size, using each subset successively as a validation set while fitting a model on the remaining data. In the case of small data sets, it is advisable to repeat the CV process with multiple random partitions and average the resulting estimates to reduce variability. This approach is known as repeated -fold CV. We focus exclusively on CV, despite the existence of various other resampling methods described in various sources, such as the work of Hastie et al. (2009). This choice is primarily due to the popularity of CV and the fact that most resampling methods share a common operating principle—repeatedly partitioning the data set into training and test subsets.

The number of folds has to be selected by hand. Employing a leave-one-out strategy by choosing (i.e., fitting a model on all but one observation and evaluating the model on the left out observation and repeating this process for all observations) is not optimal as it increases the variance of the estimator [James et al., 2013, p. 179, Hastie et al., 2009, p. 242]. Contrarily, repeated CV with many folds (but fewer than ) and multiple repetitions often yields better results (Bengio and Grandvalet, 2004).

It is important to note that performance values obtained from resampling splits, especially CV splits, are not statistically independent due to the overlapping training sets, making the variance of resampling-based GE estimates notoriously difficult to estimate (Bengio and Grandvalet, 2004). Consequently, carrying out statistical tests based on resampling-based GE estimates and creating confidence intervals around these estimates become challenging tasks. There are, however, quite a number of approaches that aim to estimate the variance of resampling-based estimators of quantities similar to the GE; refer to Efron and Tibshirani (1997), Austern and Zhou (2020), Bayle et al. (2020), or Bates et al. (2023) for examples. However, it is unclear which of these estimators work well in which situations. For this reason, in an ongoing work by some of the authors, we are presently assessing these variance estimators’ effectiveness in building confidence intervals for the PE in various different contexts.

2.5 Conclusions on general strategies for evaluating ML models

Supervised ML aims to use labeled data to derive a prediction function for an outcome label, based on input features, which exhibits good predictive performance on new, unseen data. The performance of such a prediction function or model is examined using suitable performance measures. The selection of an appropriate measure depends on the nature of the outcome under consideration and the objective of the prediction.

In the context of performance evaluation, typically, two types of errors are distinguished: the GE (generalization error) and the PE (prediction error). The GE assesses the effectiveness of the learner, while the PE evaluates the performance of a specific ML model derived from the available data set at hand. Although the PE often receives more attention from practitioners, our attention is directed toward the GE due to technical considerations. Nonetheless, it is important to underline the close relationship that exists between these two.

Resampling methods, which involve repeated divisions of the data set into training and test data, are commonly used for GE estimation. These repeated divisions result in a good bias-variance trade-off of the estimate. In this paper, we exclusively focus on the most prevalent resampling method, -fold CV. If computationally feasible, the value of should be chosen as a large value, yet smaller than . Finally, estimating the variance of resampling-based GE estimators is challenging and a topic of ongoing research.

Background on supervised learning and performance evaluation is for example given in Hastie et al. (2009) and James et al. (2013). Overviews of widely used performance metrics are provided for example in Bischl et al. (2023) and Japkowicz and Shah (2011) with the latter focusing on the classification setting. Raschka (2020) provides a review of model evaluation, selection, and algorithm comparison techniques, providing recommendations for best practices in machine learning research and applications, including discussions on bootstrap methods, CV, statistical tests, and alternative approaches for small data sets. Recommendations regarding the choice of a resampling method further can be found in Bischl et al. (2012) and Boulesteix et al. (2008). Finally, details regarding the difference between the PE and GE can be found in Bates et al. (2023) and readers interested in hyperparameter optimization and nested resampling are referred to Bischl et al. (2023).

3 Evaluating ML models in non-standard settings

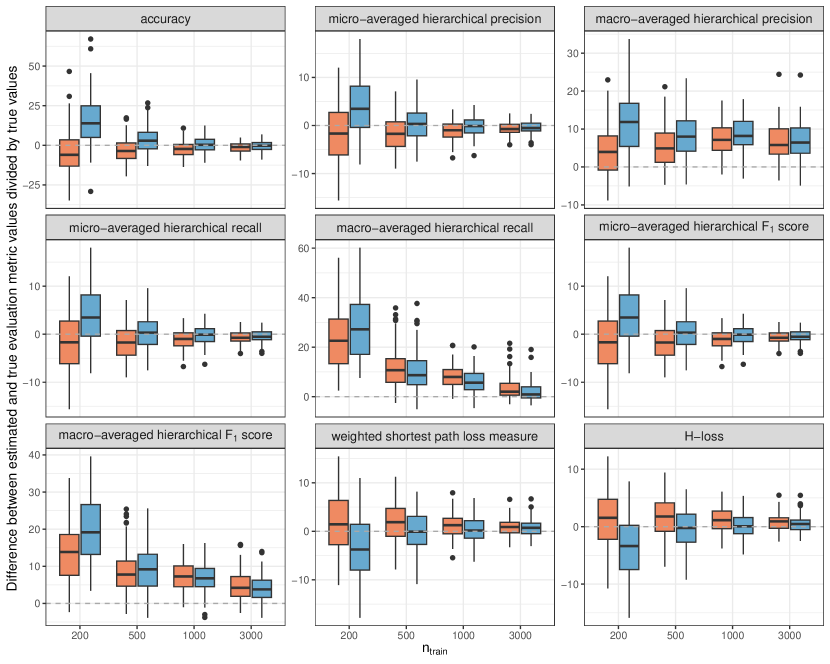

This section is structured into subsections, with each one dedicated to examining one of the five non-standard settings: clustered data, spatial data, unequal sampling probabilities, concept drift, and hierarchically structured outcomes. As mentioned in the introduction, we have carried out simulation studies for all these scenarios, except for spatial data. An abundance of empirical results for spatial data can already be found in the existing literature. The purpose of the studies presented in this section is to evaluate and compare different methods of GE estimation for each non-standard setting, with an aim to establish preliminary guidelines for conducting GE estimation in these situations. Given that the concepts of “concept drift” and “hierarchically structured outcomes” may not be familiar to many readers, we offer further background information for these settings, expanding beyond elements associated with GE estimation.

3.1 Clustered data

3.1.1 Nature and types of clustered data

In the context of clustered data, also sometimes denoted as “correlated data” in the literature, a cluster is defined as a set of observations that “belong together” and are thus expected to be more similar to each other than observations from different clusters. Here, similarity may refer to the label and/or to the vector of features . For example, if observations are individuals, households may be considered as clusters, because individuals from the same household are expected to share some characteristics. The same holds, say, for students from the same school or employees from the same company.

In this section we denote as the th observation from the th cluster and as the number of observations in cluster , with (where is the total number of clusters). In clustered data, it is generally assumed—as outlined above verbally—that is more similar to (with standing for the index of another observation from the same cluster) than to (with standing for the index of a different cluster).

As opposed to Section 3.2, there is no spatial structure, which makes the formalisation of the problem easier: the entirety of the information on the dependence structure is contained in a vector specifying which cluster each observation belongs to. Two observations are either in the same cluster or not. A special case of clustered data is obtained when clusters consist of several measurements taken from the same unit (e.g., from the same individual) at different time points. In this paper, however, we will not further consider this special case and assume data are not repeatedly collected over time.

3.1.2 GE estimation for clustered data

The first question to ask when addressing GE estimation through resampling is how the model will be used in practice. If the model will be used to predict for new observations from the clusters included in the training data set, standard resampling techniques such as those described in Section 2.4 will certainly be appropriate. Here, the observations are randomly allocated to the data subsets when splitting into training and test sets or (in the case of -fold-CV) when splitting into folds. Consequently, in the same resampling iteration, observations from the same clusters can be found in both training and test sets. However, the much more common case in practice, at least as far as small clusters such as households are concerned, is that the goal is to use the model to predict for observations from new clusters not represented in the data set used to fit the model.

In the remainder of this section, unless stated otherwise, we will assume this second case. Here, standard resampling techniques have been shown to be optimistically biased several times in the literature (Brenning and Lausen, 2008; Saeb et al., 2017; Gholamiangonabadi et al., 2020; Kunjan et al., 2021; Tougui et al., 2021). To understand that, imagine the extreme case where all observations from a cluster are identical and that this holds for all clusters, that is, . Of course, in this extreme case, one would rather collect the data at the level of clusters and not at the level of observations, but we imagine this situation for didactic purposes. Further imagine that the cluster structure is ignored when splitting the data into training and test sets. We may have observation in the training set and observation in the test set. In our extreme case, however, these observations are equal, which essentially implies that the same observation is both in the training and test sets. By ignoring the cluster structure, we thus violate the principle of separating training and test sets, which generally leads to over-optimistic performance estimations. The same mechanism is in principle at work in cases where observations from the same cluster are only similar rather than identical.

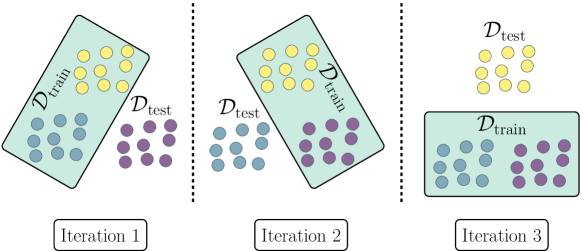

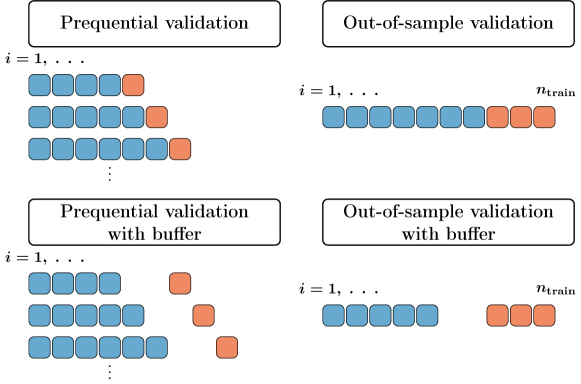

To prevent over-optimistic performance estimations, all studies cited in the last paragraph recommend ensuring that in the resampling scheme the test observations originate from clusters absent in the training data. This can be implemented by performing resampling (e.g., CV) at the cluster (or subject) level—a method we will refer to as grouped resampling or grouped CV. This differs from the resampling at the observation level, which will henceforth be termed as standard resampling or standard CV. Grouped CV was originally suggested specifically for paired data () by Brenning and Lausen (2008). A commonly used special case of this method is leave-one-subject-out CV (Gholamiangonabadi et al., 2020; Kunjan et al., 2021)—also known as leave-one-object-out CV [Bischl et al. 2024, Chapter 3]. Here, each cluster is omitted once for evaluation, while training is conducted on the remaining clusters, see Figure 1 for an illustration.

While most studies only consider grouped CV for GE estimation, Gholamiangonabadi et al. (2020) also used it for model selection. They used it to choose between different alternatives in constructing a deep learning model. However, they did not explore whether standard CV would have led to a different optimal model. In a slightly different context, Bernau et al. (2014) discovered that rankings of different ML learners can vary based on whether evaluations are performed on the same clusters or new ones. Instead of using grouped CV, Bernau et al. (2014) employed cross-study validation, which involves training on individual clusters (or studies) and evaluating on all others.

Saeb et al. (2017) conducted a simulation study to examine how variability within and across clusters impacts the GE estimated with standard and grouped CV. Note that in this simulation study, as in Tougui et al. (2021) or Kunjan et al. (2021), the clusters represented individual subjects, with each subject having consistent labels across their respective measurements. Here, as the variability across clusters increased, the error expected on new clusters also increased. However, standard CV did not reflect this trend in settings with small cluster numbers. Saeb et al. (2017) also conducted a literature review in the field of smartphone- or sensor-based prediction of clinical outcomes. They found that more than half of the included studies used grouped CV, while the rest used standard CV. Grouped CV is also prevalent in medical research, as illustrated by Pfau et al. (2020) and Künzel et al. (2020). Saeb et al. (2017) recommended the use of grouped CV not only for GE estimation but also for optimizing tuning parameter values. The choice of appropriate resampling methods for optimizing tuning parameters and model selection will be further discussed in Section 3.2 within the context of spatial prediction.

As previously mentioned, several studies have indicated that standard resampling techniques can be overly optimistic when applied to clustered data. However, many of these studies focused on specific scenarios or were based on individual data sets. For instance, Tougui et al. (2021) and Kunjan et al. (2021) considered cases where the clusters were represented by subjects with consistent labels across measurements. Gholamiangonabadi et al. (2020) limited their focus to large clusters, and as highlighted earlier, Brenning and Lausen (2008) addressed paired data. In the upcoming section, we will present a simulation study that expands upon the existing literature discussed above. We will compare grouped with standard CV for cases with varying labels within clusters and varying sizes of clusters.

3.1.3 Simulation study comparing GE estimation with and without respecting the clustering structure

Objective and simulation model

We conducted a small simulation study to compare the results of standard CV ignoring the clustering structure and grouped CV. For the simulation, we generated data from the linear model

| (1) |

where , , , and . The strength of the cluster structure is controlled by and . Apart from the standard setting in which all values were sampled i.i.d. (from ), we considered two further settings, where the or values, respectively, were constant within clusters. Examples for such features would be family income or living space. We varied the number of observations , the number of clusters , and the strength of the signal through (weak signal: vs. strong signal: ). Moreover, we considered settings with and without cluster-specific means and effects ( vs. , ). Further details about the simulation design are described in Section A.1 of the Supplementary Materials.

Study design

As a resampling technique, we used (grouped) 5-fold CV, repeated ten times. For the standard variant, we ignored the information on cluster memberships, while for grouped CV the clusters rather than the single observations were randomly assigned to the folds. Lastly, we used linear models and random forests as learners and the MSE as error measure. In this simulation study, and in all other simulation studies presented in this paper, we conducted 100 repetitions per setting.

Results

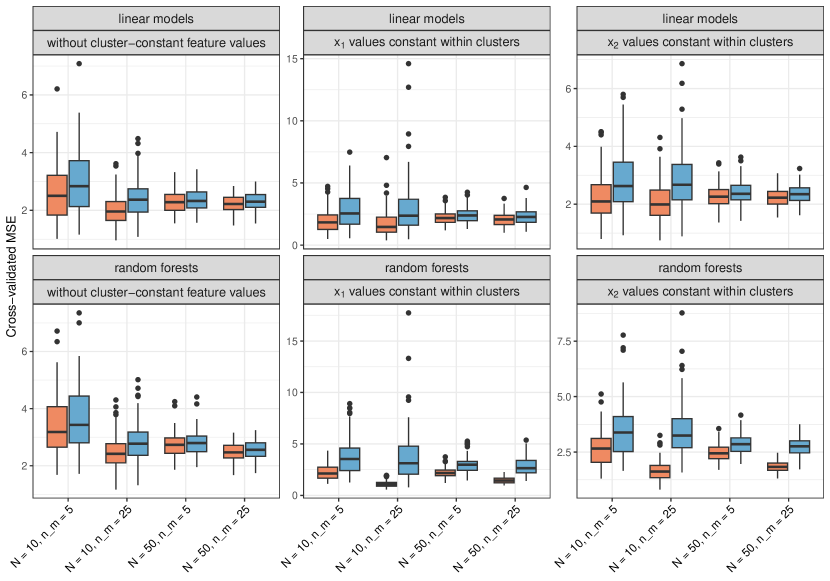

Figure 2 visually represents the primary findings of our analysis on clustered data. For the standard setting in which all are sampled i.i.d., the MSE estimates obtained by standard CV are only slightly smaller than those obtained by grouped CV and only for small numbers of clusters (). For large numbers of clusters (), there are no notable differences between the results obtained for the two CV variants in the standard setting. In contrast, for the settings for which the or values, respectively, were constant within clusters, the MSE estimates obtained with standard CV are considerably smaller than those for grouped CV in many situations. Here, the differences are again smaller for larger numbers of clusters ().

Figure 2 includes results for all settings featuring cluster-specific means, cluster-specific effects, and a strong signal. These results are representative, as we observed no substantial differences in terms of the relative differences between the MSE estimates obtained for standard and grouped CV across settings that considered cluster-specific means, cluster-specific effects, or both. The signal’s strength also did not notably impact the results in this respect.

All results are shown and described in Section A.2 of the Supplementary Materials. The R code used to produce the results shown in the main paper and in the Supplementary Materials is available on GitHub (https://github.com/RomanHornung/PPerfEstComplex).

The findings from our study somewhat diverge from those reported in the existing literature. Past research consistently reported smaller error estimates for standard CV compared to grouped CV. In contrast, our simulations only mirrored these results for certain settings. Possible explanations for this discrepancy may be found in the characteristics of the data sets used in the literature, where the labels were constant within clusters, or there were only a few clusters, each with a considerable number of observations.

The observed strong underestimation of the error in standard CV can be reasonably expected when labels within clusters are constant. In such cases, ML models can more effectively predict the labels of observations from clusters that are already represented in the training data. Additionally, it is unsurprising to witness stronger underestimation by standard CV when larger clusters are present, as the ML learner has access to more information about each cluster, enabling it to fit the clusters better.

The simulation study of Saeb et al. (2017) diverged from ours in several respects. Not only were the labels constant within clusters, but the features’ distributions were also cluster-specific. The latter also can be expected to result in more homogeneous cluster, potentially amplifying the underestimation of error via standard CV.

3.1.4 Conclusions for clustered data

When using clustered data for prediction modeling the cluster structure has to be taken into account during GE estimation. This can be performed by randomly assigning the observations to the folds on a cluster-by-cluster basis in CV, which prevents cluster overlap between training and test data. An exception is when the goal is to obtain predictions for new observations from clusters already existing in the training data. Here, standard CV should be used, that is, the observations rather than the clusters should be assigned randomly to the folds.

Our simulation study indicates that ignoring the cluster structure in GE estimation can lead to a slight, but non-negligible over-optimism. However, this effect can become stronger in the presence of features that take identical values within clusters, which is a situation frequently encountered in official statistics that is a focus of this paper. It has to be noted that the results from the existing literature consistently suggested strong over-optimism when the cluster structure is ignored. This pattern is likely attributable to the specific characteristics of the data sets and simulation designs used in these studies. Nonetheless, it underlines the importance of considering the cluster structure during GE estimation.

3.2 Spatial data

3.2.1 Nature and types of spatial data

Spatial data exhibits spatial correlation due to its nature, which necessitates similar considerations with respect to resampling and GE estimation as with other correlated data types, such as clustered data (see Section 3.1.2). Spatial data can be categorized into two types: discrete spatial data, collected, for example, at the level of federal states or other administrative units, and continuous spatial data, which includes the exact location of each observation, represented by coordinates , for example, geolocated data with , denoting longitude and latitude, respectively.

Discrete spatial data, in which observations are only known to be within a spatially defined region but without exact locations, can be considered a generalized case of clustered data. Observations in this case are grouped at state or district levels. However, such clusters exhibit not only within-cluster correlation but also spatial correlation, as data from neighboring administrative units could be more similar than data from distant units. Likewise, data collected at a finer resolution often demonstrates correlation in both features (e.g., temperature, infrastructure) and labels (e.g., unemployment rates).

3.2.2 GE estimation through spatial CV

To address the issue of spatial correlation, the literature typically recommends using resampling strategies that employ non-random allocation of observations to training and testing data sets, referred to as spatial resampling or spatial cross-validation (Schratz et al., 2019). As will be described below, there exist different variants of these strategies. All of them have in common that data used for performance evaluations are spatially separated from the training data to some extent, thereby reducing the correlation between the two. It has been frequently shown in the literature that failing to spatially separate training and testing data can lead to over-optimistic GE estimates; for examples, see Heikkinen et al. (2012), Wenger and Olden (2012), Roberts et al. (2017), Schratz et al. (2019), and Schratz et al. (2021). This bias is particularly strong when prediction in new regions is a primary goal, as opposed to prediction in the space where the training observations are found, hereafter referred to as the observation space.

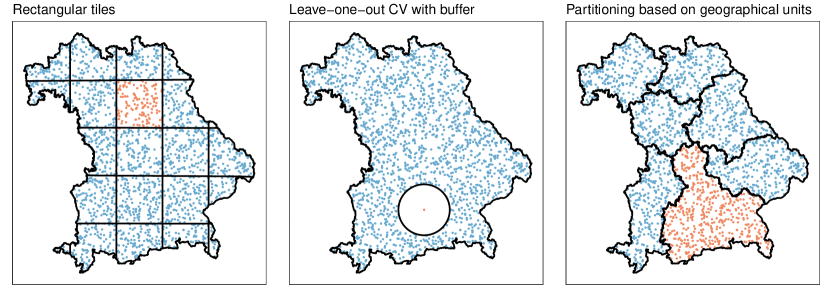

Next, we give an outline of prevalent spatial CV approaches. Figure 3 provides a visual representation of some of these methods, showcasing a single iteration of the spatial CV process in each case. Details on how to set the parameters of these approaches and how to choose between them will be provided in Section 3.2.3. This synopsis is based on the descriptions provided by Schratz et al. (2021):

-

•

Single split into training and test data: This is, arguably, the most basic method. Here, the data is spatially divided once into one training set and one test data set in such a way that a single contiguous boundary between them can be established. It also permits the establishment of a buffer zone, a spatial region surrounding the boundary between and , with data within this zone excluded from both sets (Heikkinen et al., 2012). As discussed in Section 3.2.3, this approach is suitable in situations in which the distance between the data intended for prediction and the labeled data is already known because it allows precise specification of where the test data lie relative to the training data. Despite not being a CV approach per se, it is still encompassed within the use of the term “spatial CV” in the following.

-

•

Rectangular tiles: In this approach, the observation space is divided into uniform rectangular subspaces, termed blocks (Ruß and Brenning, 2010). The first variant of this approach uses a small number of blocks, each corresponding to a fold in a -fold CV. The second variant involves a larger number of subspaces, which are randomly or systematically assigned to the folds in CV, akin to observations in a standard -fold CV. This is referred to as CV at the level of the blocks.

-

•

clustered groups: This technique is similar to the rectangular tiles approach with blocks, but with the blocks determined through a clustering algorithm such as -means clustering, rather than equally sized rectangles. Two variants exist: one with clustering based on the coordinates (Ruß and Brenning, 2010), and the other with clustering based on the features (Valavi et al., 2018), where for the latter the clustering is non-spatial (or not directly spatial).

-

•

Leave-one-out CV with buffer: This is a spatial adaptation of the conventional leave-one-out CV. Unlike the latter, where all other observations except the test observation are used as training data in each iteration, a circular buffer zone is established around the test observation in each iteration in the spatial version. Observations within this buffer zone are excluded from the training data, spatially separating the test observation from the training data (Le Rest et al., 2014). The choice of buffer zones in this and other methods will be further discussed in Section 3.2.3.

-

•

Leave-one-disc-out CV with optional buffer: This approach is analogous to the previous one. However, in contrast, individual observations are not used for testing, but all observations within discs of a fixed diameter. The use of a buffer zone is optional in this method, unlike in leave-one-out CV with buffer. The number of test data sets is fixed to , and the locations of the corresponding discs are randomly selected within the observation space (Brenning, 2005, 2012).

-

•

Partitioning based on geographical units: In certain scenarios, for example, in the case of discrete spatial data (see Section 3.2.1), pre-existing spatial units may be available. These can be used as blocks in a spatial CV, which can also be done at the level of the blocks as in the rectangular tiles approach (see above).

All of the above approaches are available in the R package “mlr3spatiotempcv” (Schratz and Becker, 2022), an extension package of the ML framework “mlr3”. The package is available online from the CRAN repository. It is important to note that the approaches described above are primarily applicable to continuous spatial data, as they necessitate the exact locations of the observations. Most of the literature presumes the presence of continuous spatial data, explaining the scarcity of resources about spatial CV methodologies for discrete spatial data. However, it should be highlighted that the same sort of spatial correlation exists in both continuous and discrete spatial data. Therefore, in the case of discrete data, we may simply use the centroids of each spatial region as substitutes for the precise locations and apply the approaches described above to these centroids.

3.2.3 Choosing and configuring spatial CV approaches

The choice and precise configuration of a suitable (spatial) CV approach should be informed by the intended use of the model and the structure of the data. More specifically, the chosen spatial CV procedure should reflect the setting in which the ML model will be applied (Schratz et al., 2021). For instance, if the objective is to fill in gaps in the observation space, the test data in the spatial CV should be closer to the training data than if the model is intended for application outside the observation space. Standard CV may suffice if predictions are to be made solely within the observation space (Wenger and Olden, 2012; Roberts et al., 2017). Predicting the prevalence of certain diseases is an example where both situations can occur. There may be applications where the goal is to fill in gaps within the observation space, as well as applications where the objective is to make predictions for new regions outside the observation space. For the former, rural areas could be underrepresented in health surveys, thus creating a need to extrapolate information from models trained on more urban areas. In the latter scenario, country A may have comprehensive disease prevalence data available, while country B may not. In this case, the aim would be to train an ML model using data from country A and obtain predictions for country B.

Key parameters that influence the difference between training and test data folds in spatial CV are block width and buffer zone width. The larger the values of these parameters are, the larger the distances between the training and the test data sets are within spatial CV. Thus, the further the prediction area is from the observation space, the larger these parameters should be for realistic error estimates (Roberts et al., 2017). The minimum width for the blocks and the buffer zone is often stipulated by the range parameter of the empirical correlogram, indicating the minimum distance between two points required for their labels to become uncorrelated (Brenning, 2005). Roberts et al. (2017) argue that larger widths may often be required due to structural features (such as temperature) causing label dependencies that extend beyond autocorrelation as measured by the correlogram. It is also crucial to measure autocorrelation in the raw data rather than in residuals from fitted models, to avoid underestimation of autocorrelation as fitted feature influences would have already accounted for some of it (Roberts et al., 2017). Particularly when the aim is to identify influential features and measure their effect, it is important to choose large block or buffer zone widths. The identification of influential features with spatial data is generally challenging, with Wenger and Olden (2012) recommending feature selection based on plausible a priori hypotheses, as the features selected in this way are likely to have influence also in new areas outside the observation space. Spatial CV is recommended by Roberts et al. (2017) even when the fitted models account for observation dependencies.

Buffer zones should only be employed when predictions are intended for new areas, where the distance to these areas exceeds the distances between neighboring observations in the training data (Schratz et al., 2021). Otherwise, spatial CV can result in GE overestimation because the sizes of the training data sets are reduced and extrapolations can occur. The latter means that feature values or combinations of feature values that are present in test data sets during spatial CV do not occur in the respective training data sets (Roberts et al., 2017). If such a scenario does not arise in the application of the prediction model—for instance, because the distance between the data used for prediction later on and the training data is less than in the spatial CV—this could lead to an overestimation of the GE. Note, however, that as already mentioned in the introduction, in most cases overestimating the GE is preferable to underestimating it (Roberts et al., 2017).

Conversely, if the observation space is small, it may be difficult to generate sufficient independence between the training and test data through spatial CV because a sufficiently large buffer zone cannot be used in that situation (Roberts et al., 2017). In such cases, obtaining a realistic error estimate from the available data may be challenging if the goal is to predict into new areas. This is because, without a sufficiently large buffer zone, the GE estimate will be overoptimistic for this goal. In these situations, Wenger and Olden (2012) recommend to keep the number of folds in spatial CV small. This leads to smaller training data sizes within CV and consequently, more conservative GE estimates. However, it can be challenging in practice to determine the optimal number of folds that yield a conservative bias sufficient to offset the over-optimism of the GE estimates. In contrast, Roberts et al. (2017) suggest as a general rule, if computationally feasible, to keep the inherent bias of CV low, training data set sizes should be maximized by including only one block in each fold during spatial CV, instead of performing the latter at the level of the blocks (see the description of the rectangular tiles approach in Section 3.2.2). If deciding a specific value in spatial CV is challenging, conducting a sensitivity analysis with varying values can be beneficial (Wenger and Olden, 2012).

Standard CV is typically repeated to reduce variability in the obtained error estimates. However, this is not usually feasible or meaningful with spatial CV, given the non-random division of data into training and test data sets that is determined by the spatial structure of the data (Schratz et al., 2021). An exception might be clustered groups approaches, where, for example, -means clustering depends on random initial values. Nevertheless, Schratz et al. (2021) found that clusters can be nearly identical with different initial values used. In general, it is noteworthy that while spatial CV provides an indication of the model’s expected performance, the actual performance can vary (Wenger and Olden, 2012). Yet, spatial CV is preferable as it generally offers more realistic error estimates than standard CV (Heikkinen et al., 2012; Wenger and Olden, 2012; Roberts et al., 2017; Schratz et al., 2019, 2021).

Above, we discussed aspects of configuring appropriate approaches. Going forward, we will focus on selecting the most suitable one for the application at hand, based on the characteristics of the various options available. As previously mentioned, if the data are partitioned into pre-existing spatial units, these can be directly used as folds in spatial CV by employing the partitioning based on geographical units approach (Schratz et al., 2021).

If the data are irregularly distributed in the observation space, the rectangular tiles approach can result in significant variation in sample sizes across folds (Roberts et al., 2017). In such cases, the clustered groups approach based on geographic coordinates is advisable, as here the areas associated with the folds align with the data distribution and the numbers of observations within the folds are comparable (Schratz et al., 2021). The clustered groups approach based on the features should be used if the model will be applied to data containing feature values or feature value combinations not present in the training data (Schratz et al., 2021). According to Roberts et al. (2017), although this yields less over-optimistic error estimates than standard CV, results can still be over-optimistic if spatial correlations are not considered.

Spatial leave-one-out CV with buffer, similar to standard leave-one-out CV, has the downside of being highly computationally intensive, as each observation is used once as a test observation and the model must be refitted based on the corresponding training data in each of these cases (Schratz et al., 2021). The leave-one-disc-out CV approach provides a less computationally demanding alternative.

One issue with the folds in spatial CV is that it is not possible to be performed in such a way that each fold has a similar distance to the respective training data as the area intended for prediction. Thus, examining error estimates on specific folds might be more insightful if the distance between the data intended for prediction and the training data is known (Roberts et al., 2017). We believe that in such scenarios, employing a single split into training and test data might be superior, as this allows for the specification of the test data’s distance from the training data, and thus matching it to the distance of the data intended for prediction. Table 1 provides an overview of the recommendations described above for choosing a particular approach in different situations.

Roberts et al. (2017) argue that ideally, the test data should always originate from an independent area. However, it is debatable whether this is always the best approach, as the chosen validation procedure should reflect the nature of the application. Thus, validation on independent areas would be recommended only if the model will actually be applied to completely independent areas later on.

| Application scenario | Recommended spatial CV approach(es) |

|---|---|

| pre-existing spatial units (e.g. discrete spatial data) | partitioning based on geographical units |

| irregularly distributed observations (e.g. involving clusters) | clustered groups approach based on geographic coordinates (rectangular approach is not recommended) |

| application to data containing feature values or feature value combinations not present in the training data | clustered groups approach based on the features (spatial correlations should also be considered to avoid over-optimism) |

| prediction to new regions | spatial leave-one-out CV (high computational burden); leave-one-disc-out CV with buffer (low computational burden) |

| known distance between the data intended for prediction and the training data | single split into training and test data / examining GE estimates on specific folds |

3.2.4 Model selection and tuning parameter optimization in spatial data applications

As an initial point, it should be noted that the topics treated in this subsection are also applicable to the other non-standard settings discussed in this paper, as will be elaborated in Section 4. We have already briefly touched on model selection and tuning parameter optimization in Section 3.1.2, specifically in the context of the non-standard setting “clustered data”. Given the notable number of results available on them for “spatial data”, we have decided to dedicate an entire subsection to these topics within this specific context.

Traditionally, model selection for (generalized) linear models with i.i.d. data is performed using criteria like the AIC or the BIC. However, these are typically not applicable in ML because the models in this domain are usually not obtained by maximum likelihood estimation. In addition, the structure of spatial data leads to biased AIC and BIC values (Roberts et al., 2017) and overfitting to the observation space (Wenger and Olden, 2012). When the goal is prediction within the observation space, CV may be appropriate for model selection. However, as pointed out earlier, even in this situation spatial CV is often recommended for GE estimation. More specifically, spatial CV should be used in this scenario if there are larger gaps between observations in the observation space, leading to cases for which the predicted observations have a distribution unrepresented in the training data even when predicting within the observation space.

The crucial role of choosing an appropriate validation method in spatial prediction, particularly for model selection, where the aim is to find the best-performing type of model (as opposed to, e.g., tuning parameter optimization discussed in the next paragraph), is supported by several empirical studies. These studies have suggested that different types of models can perform differently in predicting within and outside the observation space (Brenning, 2005; Heikkinen et al., 2012; Wenger and Olden, 2012; Schratz et al., 2019). These studies, however, offer some conflicting insights on the performance of various methods outside the observation space. This divergence is not unexpected, considering each study was based only on a single data set. For instance, Brenning (2005), Heikkinen et al. (2012), and Wenger and Olden (2012) reported a more pronounced decline in prediction performance outside the observation space for tree-based methods, including random forests, compared to other methods. In contrast, Schratz et al. (2019) found that random forests performed best in prediction both within and outside the observation space among the methods studied. Furthermore, while artificial neural networks showed good prediction performance outside the observation space in Heikkinen et al. (2012), according to Wenger and Olden (2012) they underperformed in this scenario. Interestingly, both Heikkinen et al. (2012) and Wenger and Olden (2012) observed that simpler model types, like linear models, generally tend to predict better outside the observation space compared to more flexible models. Schratz et al. (2019) explain that very flexible models can adapt too closely to the specific conditions of the observation space, leading to decreased performance when predicting outside this space. Despite these differences, there is a positive correlation between the methods’ performance inside and outside the observation space (Heikkinen et al., 2012). This could explain why, despite typically being associated with a strong decline in performance outside the observation space (Brenning, 2005; Heikkinen et al., 2012; Wenger and Olden, 2012), random forests also performed best outside the observation space in Schratz et al. (2019).

The selection of tuning parameters in ML models dictates the degree to which these models adapt to the given data, thereby controlling model flexibility. Since the studies of Heikkinen et al. (2012) and Wenger and Olden (2012) suggested that simpler models tend to perform better outside the observation space than more flexible models, it is logical to suggest that different tuning parameters could yield optimal performance depending on whether a model is applied within or outside the observation space. Typically, tuning parameter values are optimized by selecting those associated with the lowest CV error. To identify tuning parameter values that optimize model performance outside the observation space, spatial instead of standard CV can be used.

Schratz et al. (2019) explored this possibility based on an extensive analysis using a data set on forest disease in Spain. Here, the difference between the predictive performance (outside the observation space) of models tuned with spatial and standard CV was minor for most model types, despite notable differences in the optimized tuning parameter values between the two approaches. Nevertheless, Schratz et al. (2019) conceded the need for further validation using other data sets and model types. Based on an extensive empirical study, Ellenbach et al. (2021) demonstrated that using external data with a different distribution from the training data for tuning often results in better performing models when applied to other data with a distribution different from the training data. This setting is consistent with that of spatial models used for prediction outside the observation space. Therefore, the results of Ellenbach et al. (2021) suggest that, notwithstanding Schratz et al. (2019)’s findings, using spatial rather than standard CV for optimizing tuning parameters could potentially result in improved predictions. Regardless, for the sake of consistency, Schratz et al. (2019) recommend always using spatial CV to optimize tuning parameters if spatial CV is also employed for error estimation.

3.2.5 Conclusions for spatial data

In the GE estimation of spatial prediction models, it is most often critical to ensure a suitable spatial separation between training and test data. This is achieved by various procedures, collectively referred to as spatial CV. The choice and precise configuration of these procedures hinge on the data structure and the specific application scenario of the ML model. The primary determinant here is whether the model is intended for use within or beyond the observation space. In the former situation, and if, in addition, the training data are uniformly distributed in the observation space, standard CV without spatial separation might suffice.

Spatial CV procedures involve certain parameters, which govern the degree to which training and test data are separated. These procedures are more suitable for some types of applications than others, thus making the selection of an appropriate spatial CV method important.

When used for model selection, the choice of spatial CV method also impacts which learner is selected. Existing research indicates that simpler learners tend to be more effective when aiming for robust predictions beyond the observation space. For consistency, spatial CV should also be used in tuning parameter optimization when used for GE estimation.

3.3 Unequal sampling probabilities

3.3.1 Reasons for and examples of unequal sampling probabilities

In official statistics and other fields such as ecology (Schreuder et al., 2001), for both practical as well as principled reasons, sampling techniques that deviate from i.i.d. sampling are often used. Such designs are hereafter referred to as non-simple random sampling (NSRS), while i.i.d. sampling corresponds—for infinite populations to be sampled from—to the so-called simple random sampling (SRS). The question of how NSRS affects the estimation of the GE is, to the best of our knowledge, an unexplored but essential area of research, given its high prevalence in practice, for example, when working with survey data.

A common motivation for using NSRS is that these designs can be much more efficient in terms of cost. Consider, for instance, a study that wants to measure the reading ability of school children. It may be difficult to obtain a population list of all school children. In practice, it would be even more expensive to perform SRS because this would involve interviewing/testing children from numerous, potentially distant schools. A more practical approach would be first to obtain a primary sample of schools. In the second stage, a sample is taken from each selected school .111Note that the second stage sample does not have to be SRS either. This approach is typically referred to as “two-stage sampling” (Valliant et al., 2018).

To handle non-standard sample designs, it is helpful to rely on the specific perspective of sampling theory with its own terminology and notation. In this vain, one considers explicitly an unknown finite population of units with the corresponding data points and a probability measure on the subsets of specifying the sample design that determines which subset of is actually observed as a sample. For a concretely realized sample of size , the probabilities of having observed specific (pairs of) units are of particular interest: for every , one calls the inclusion probability of unit and the joint inclusion probability of and . For the NSRS designs considered in this subsection, the inclusion probabilities differ between units in the population, that is, .222Here we do not study the very special NSRS situations where the inclusion probabilities of the single units are still equal, but joint (or so-called higher order) inclusion probabilities are not.

In the school example from above, the inclusion probability for each child is given by (Haziza and Beaumont, 2017), where denotes the inclusion probability of school and the conditional probability of including unit in the sample given the inclusion of school . It is worth noting that two-stage sampling introduces a cluster structure, as discussed in Section 3.1, with the schools acting as the clusters. Consequently, based on the findings of Section 3.1, it is advisable to conduct resampling at the school level, rather than at the unit level, in scenarios akin to the one outlined above.

Even when an SRS design is possible, it may, nevertheless, be advantageous to assign higher inclusion probabilities to certain units to reduce the variance of a population parameter estimate. Consider an example where we want to estimate the average number of employees in a population using SRS of companies. Even though the simple mean estimator is unbiased, it will have a large variance. To reduce this variance, a common approach is to assign higher inclusion probabilities to large companies based on a known auxiliary variable that is approximately proportional to the label (Horvitz and Thompson, 1952; Valliant et al., 2018). This approach stabilizes the mean estimate because larger companies tend to have a greater impact on the average number of employees. Note that in this and the previous example, the fact that the observations are sampled with different probabilities must be taken into account during parameter estimation to avoid biased estimates. In our example, one could use reported revenue as and set . This approach is known as sampling proportional to size (PPS). Detailed overviews of different sampling designs can be found in Skinner and Wakefield (2017), Valliant et al. (2018), and Haziza and Beaumont (2017).

3.3.2 GE estimation under NSRS

To study the estimation of the GE of ML models, a small detour proves helpful. We first consider the estimation of the population mean under NSRS. Subsequently, the discussed concepts will be used to derive an unbiased estimator for the GE under NSRS.

Unbiased estimates of the population mean of can be obtained from the sample of size using the Horvitz-Thompson estimator of the mean

| (2) |

where . The resulting estimates typically have a much lower variance compared to the unweighted average (Horvitz and Thompson, 1952). An alternative that can be used even when the size of the population is unknown is the Hájek estimator (Hájek, 1971)

| (3) |

which has a small bias under finite sample sizes. Nevertheless, it is often preferred over (Sarndal, 1980), since, intuitively, it compensates for potential extremes in the values.

When given a sample obtained using NSRS, conventional estimates of the GE may be associated with increased bias and variance as the i.i.d. assumption is clearly violated. For example, for a given test set with a fixed model and predictions , it can easily be shown that under PPS sampling, the sampling bias for the MSE is

| (4) | ||||

| (5) | ||||

| (6) |

In the above equations, the subscripts and are used to denote that the corresponding quantities are related to the scenarios of simple random sampling and sampling proportional to size, respectively. The expressions in (5) and (6) directly imply that the bias depends on the deviation of from SRS and the dependency structure between and the error. If the inclusion probabilities vary independently from the error, no systematic bias is to be expected, although the variance will increase. If, however, the are correlated with the error, bias is to be expected, which is, for instance, the case in our example, where it is plausible that the prediction error increases with company size.

This issue has been recognized in Holbrook et al. (2020), who recommend the usage of Horvitz-Thompson estimates for the GE in the case of NSRS. However, the arising bias and unbiased estimators have not been studied extensively.

When performing CV on a sample obtained with NSRS, instead of considering a fixed model , the situation requires further consideration. The reason for this is that the model learned on an NSRS sample will also be affected by sampling bias if the differences in the sampling probabilities are ignored. However, in this paper, we focus only on the bias of the error estimation. A review of sampling-consistent learning methods under NSRS can be found in Breidt and Opsomer (2017) and applications in Toth and Eltinge (2011) and Dagdoug et al. (2021).

For point-wise losses (cf. Section 2.2), an unbiased estimator can be obtained by transferring the considerations on mean estimation via the Horvitz-Thompson estimator (2) from above, leading to

| (7) |

Proof.

The proof utilizes a classical argument handling Horvitz-Thompson-type estimators, introducing, for Bernoulli distributed random variables to denote whether or not observation is included in the sample. Then, in the finite-population setting, and can be seen as non-random (Horvitz and Thompson, 1952); the randomness solely enters via the inclusion into the sample expressed by the inclusion variables . Then

| (8) | ||||

| (9) | ||||

| (10) | ||||

| (11) |

∎

3.3.3 Simulation study comparing GE estimation with and without correcting for NSRS

To analyze the impact of NSRS on GE estimation and demonstrate the effectiveness of the Horvitz-Thompson estimator for error correction, we applied the concepts in a small simulation study based on our general simulation setting.

Simulation model

We generated data from the following linear model:

| (12) |

where , and . Additionally, we generated an auxiliary variable (approximately) proportional to the target variable used for PPS sampling via333In the rare event that a draw did not lead to a positive value it was repeated. and set . The features with effect, and , were sampled from a distribution, while the features without effect, , , and , were sampled from . The Gamma distribution for and was chosen to produce skewed label distributions, which under PPS sampling will lead to very far from underlying SRS. In this situation, based on equation (6), we expected a large bias.

Study design

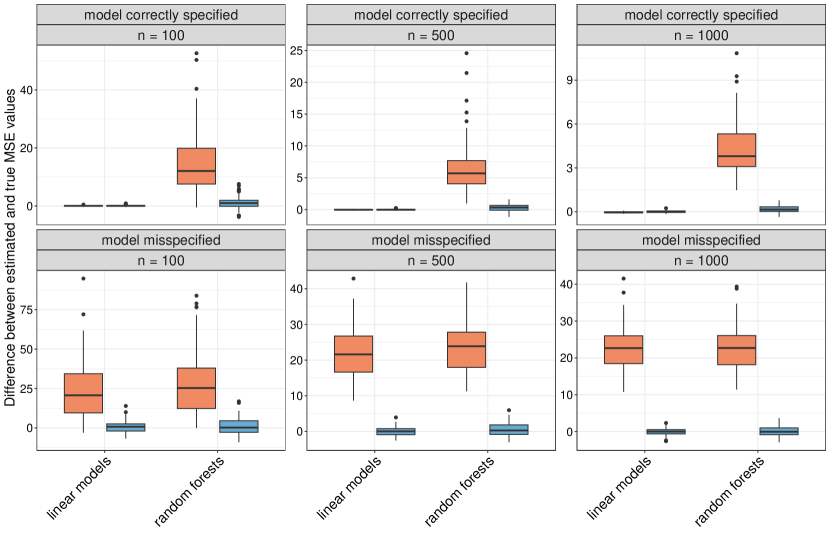

The population size was varied () and PPS samples of size were drawn from the population with probabilities . We performed 5-fold CV, repeated ten times, on each sample, with and without correcting for NSRS using the Horvitz-Thompson theorem from Equation (7). The GEs were approximated on separate test sets of size , where, for training, the entire available training data was used. Linear models and random forests were used as learners, and the MSE as error measure. We also included a variant for each simulated data set where feature was excluded after simulating the label, resulting in misspecified models.

Results

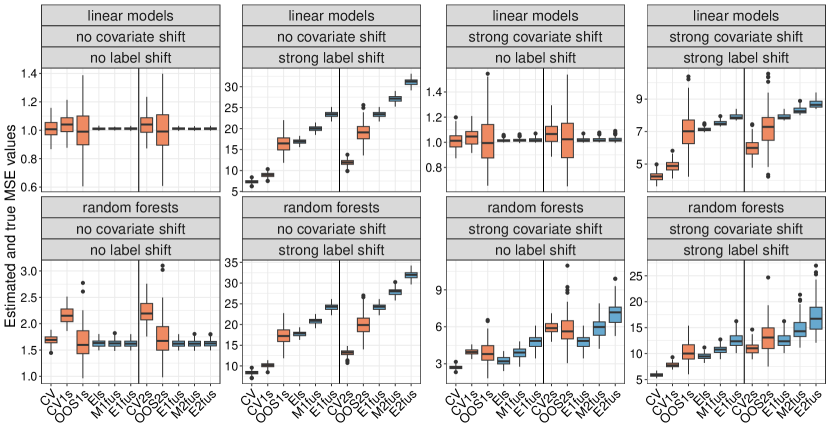

For the random forests, the GEs were overestimated when not corrected for NSRS. In contrast, for the linear models, the GEs were overestimated only when the models were misspecified. The GE estimates corrected for NSRS were unbiased across all simulation scenarios for both learners. The population size and sample size did not notably influence the bias observed in the GE estimates obtained without correcting for NSRS. The results are visualized in Figure 4.

A potential interpretation of results

The observed overestimation of the GEs for the random forests when not correcting for NSRS, even with correctly specified models, might be due to their flexibility. Random forests adapt locally to each region in the data distribution, which can lead to suboptimal performance in regions with few observations. The PPS sampling led to a higher number of observations with larger labels being sampled. However, since there were still fewer observations in this region compared to regions with smaller labels, the random forests likely performed poorly in this region. This could potentially explain the larger GE estimates for the random forests without correcting for NSRS. The (true) GEs were smaller, as the population had a greater proportion of observations with smaller label values compared to the training data. The random forests may have performed better for these smaller label values due to the higher density of observations in the region with smaller label values, both in training and test data. When correcting using the Horvitz-Thompson theorem, contributions from observations with larger labels are heavily down-weighted, which potentially led to the elimination of the upward bias in the GE estimates.

In contrast, linear models are less flexible but tend to be more robust to data sparsity in certain regions. When feature influences are linear, as in the simulation, linear models can be expected to provide accurate predictions even in areas with fewer observations. Therefore, it is conceivable that, unlike the random forests, the linear models did not perform worse in the region with larger label values; this would explain that the GE estimates for the linear models were not biased upward without correcting for NSRS. In the scenario with misspecified models, linear models exhibited similar behaviour to random forests, producing larger GE estimates without correction for NSRS. This likely occurred because, as with random forests, the prediction quality probably diminished for larger label values. A plausible reason behind this decline would be the increasing influence of in this region, which is not considered in the misspecified models as is not used, leading to erroneous slopes.

3.3.4 Conclusions for unequal sampling probabilities

There are instances in practice where observations are drawn from the population into samples with varying probabilities. As we demonstrated both analytically and through a simulation study, depending on the learner employed and the data distribution, if not accounted for, such unequal sampling probabilities can introduce bias into GE estimation. However, when the sampling probabilities are known, this bias can be corrected using the Horvitz-Thompson theorem, even if the ML model is misspecified.

3.4 Concept drift

The distribution of data arriving in streams can change over time, a phenomenon most commonly referred to as “concept drift” (Gama et al., 2014). If not taken into account, this can lead to a decline in the predictive performance of ML models on future data. This is because the data-generating process that was present during training is no longer applicable to the new data obtained after training. If this is not taken into account when estimating the GE, it can lead to bias in the resulting estimates. We will observe this effect in the simulation study presented in Section 3.4.4. A further particular practical challenge in many situations is that it is not known how and when these changes in the data-generating process occur.

3.4.1 Reasons for and types of concept drift

Naturally, the reasons for concept drift vary across different fields of application. Gama et al. (2014) provides a comprehensive review of the occurrence of concept drift in various domains. In the field of official statistics, concept drift is a particularly common phenomenon as we will illustrate by five principled examples. One prevalent reason is changes in population structure; for instance, populations can age over time (European Commission, 2023). Second, social and economic changes, such as recent technological advancements in artificial intelligence, can alter relationships between features (World Bank Group, 2019). Third, environmental factors, including climate change or natural disasters, have widespread impacts on various aspects of society (Intergovernmental Panel on Climate Change, 2022), which can also contribute to concept drift. Fourth, changes in government policies or regulations, as seen recently with the COVID-19 pandemic, can lead to shifts as well (World Bank Group, 2019). Lastly, there can be modifications in the conduct of official statistics itself, such as changes in data collection methods, definitions, or classifications (\al@un2022handbook, unece2011impact; \al@un2022handbook, unece2011impact).

There are several forms of concept drift to distinguish:

-

•

Pure feature drift, also known as virtual drift (Gama et al., 2014), occurs when only the feature distribution changes over time, while , the conditional distribution of labels given the features remains fixed.

-

•

Pure label drift (Webb et al., 2016) occurs when only the conditional distribution changes over time, but the feature distribution remains fixed.

-

•

Full concept drift refers to situations where both and change over time (this definition slightly differs from that in Webb et al. (2016)).

Pure feature drift is typically regarded as the least concerning type in the concept drift literature, because prediction models acquire knowledge on the conditional distribution (Gama et al., 2014). However, this assumes that the model is specified correctly and can successfully extrapolate to regions beyond the scope of the feature values observed in the training data. A prime example of such circumstances constitutes regression models that incorporate all influential features and linearly model their influences. Under these conditions, and importantly, if the true feature influences are also linear, the model can accurately represent even outside the range of feature values observed in the training data. This trait of regression models significantly contributes to their widespread use in the medical field, where data sets frequently deviate from representing the general population due to numerous factors, such as specific inclusion and exclusion criteria for medical studies. For instance, studies might only involve patients below a certain age (Vach, 2012). Applying a prediction model trained on these data to new data epitomizes pure feature drift, as the new data may include patients from age groups not represented in the training data. As demonstrated in the simulation study presented in Section 3.4.4 using the example of random forests, ML models, despite their impressive adaptability within the range of feature values in the training data, may struggle to extrapolate, even if the feature influences are linear. However, in the presence of nonlinear feature influences, traditional regression models are also susceptible to poor performance when extrapolating to feature values outside the training data range. These models can still reasonably depict the dependence structure in the training data, even with moderate non-linearity. However, in the case of non-linearity beyond the scope of the feature values observed in the training data, the ability of linear extrapolation to accurately represent the true dependence structure decreases as the extrapolation extends further from the range of feature values observed in the training data.

The above categorizations of concept drift are based on whether or change over time. Another way to classify concept drift is by examining how these distributions change over time:

-

•

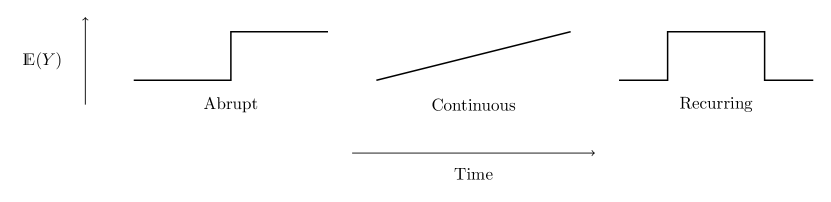

Abrupt: The distribution remains fixed until a specific point in time and then suddenly changes.

-

•

Continuous: The distribution changes continuously over time and potentially only within a specific time interval. As defined by Webb et al. (2016), the change is “incremental” if it progresses consistently in one direction, and “gradual” if it changes continuously over time without a consistent direction. Webb et al. (2016) also distinguish a related concept drift type, for which the data initially follow distribution , then transition to distribution , and in between, there are periods when the data follow either distribution or .

-

•

Recurring concepts: The distribution changes at some point but later returns to its original form (Gama et al., 2014).

Figure 5 provides an illustration of these three types of concept drifts.