Estimation and convergence rates in the

distributional single index model

Abstract

The distributional single index model is a semiparametric regression model in which the conditional distribution functions of a real-valued outcome variable depend on -dimensional covariates through a univariate, parametric index function , and increase stochastically as increases. We propose least squares approaches for the joint estimation of and in the important case where and obtain convergence rates of , thereby improving an existing result that gives a rate of . A simulation study indicates that the convergence rate for the estimation of might be faster. Furthermore, we illustrate our methods in an application on house price data that demonstrates the advantages of shape restrictions in single index models.

Keywords monotone regression, isotonic distributional regression, single index model

1 Introduction

Consider the classical regression framework in which one aims to predict a response variable with covariates . The popular generalized linear models (GLMs) assume that

where follows an exponential family distribution, is unknown, and is a monotone transformation known up to a dispersion parameter that does not depend on the covariates. Balabdaoui et al., 2019a study a semiparametric variant of this model, the monotone single index model, where the function is replaced by an unknown monotone function that is estimated nonparametrically, jointly with . The focus of this article is an extension of the monotone single index model introduced by Henzi et al., (2023), called the distributional single index model, which aims at estimating conditional cumulative distribution functions (CDFs) of given rather than only its conditional expectation. The model assumes that

| (1) |

where is an unknown conditional distribution function for all fixed , a mapping of the -dimensional covariates to , and monotonicity of is replaced by the assumption of stochastic monotonicity. Stochastic monotonicity means that is non-increasing in for all fixed , so graphically, the conditional CDFs shift to the right as increases, or in simple words, tends to attain larger values when is large. In this article, we are interested in the special case where is a linear function. The most popular families in generalized linear models — Gaussian, Binomial, Poisson, Gamma, Inverse Gaussian — satisfy the stochastic monotonicity assumption of the distributional single index model, save for a change of sign of for decreasing link functions. Thus, the model can be regarded as a semiparametric, distributional extension of GLMs. If has finite expectation, then

is increasing in , so the assumption of stochastic monotonicity is stronger than monotonicity of the conditional expectation in this case. When is binary, the distributional single index model becomes a special case of the monotone single index model. Both the monotone single index model and the distributional single index model build on the idea of single index model introduced by Härdle et al., (1993), and we refer the interested readers to the literature reviews in Balabdaoui et al., 2019a and Henzi et al., (2023) for a comprehensive discussion of related work.

Rates for the estimation of the conditional CDFs in the distributional single index model have already been obtained by Henzi et al., (2023). They showed that for an independent and identically distributed (i.i.d.) sample from model (1), if is a uniformly consistent estimator for converging at a rate of and if is computed on the data with isotonic distributional regression (Mösching and Dümbgen,, 2020; Henzi et al.,, 2021), then

| (2) |

under certain regularity conditions. Here for an interval on which has density bounded away from zero and infinity, and is a certain sequence converging to zero. When and are computed on independent samples, a faster rate of is achieved, if converges to at least at this rate. Henzi et al., (2023) provide no theoretical results on the estimation of the index function, and the rate of is likely to be suboptimal, because if it should be by Theorem 3.3 of Mösching and Dümbgen, (2020), or if is binary the results of Balabdaoui et al., 2019a yield for the estimation of and when the latter is linear.

In this article, we focus on the linear case , and propose to estimate by minimizing weighted least squares criteria of the form

| (3) |

where is a Borel measure. We obtain a rate of when has a finite support or it is compactly supported Lebesgue continuous with a bounded density. Furthermore, we investigate an approach with equal to the empirical distribution of , which has favorable invariance properties under transformations of the response variable, but the consistency and convergence rates of which remain an open challenge.

The article is structured as follows. In Section 2 we describe the estimation method in detail. Convergence rates are derived in Section 3. In Section 4, we present the invariance property result which holds when is taken to be the empirical distribution function of the responses. In Section 5 we discuss computational aspects and present a simulation study and an application on house price data. We conclude with a discussion in Section 6, and the proofs are deferred to Section A. Throughout the article, we denote the joint distribution of by , the marginals by and , and the conditional distributions by and , respectively. The empirical distributions of independent observations are denoted by , , . We denote by the support of a probability measure , and by the interior of a set . The expectation operator is understood to be with respect to , unless explicitly defined differently.

2 Estimation

Let be a sample of covariates and response variable from model , where from now on we always assume that . Define , and let be the class of bivariate functions for which is a CDF for all fixed , and is non-increasing for all fixed . The function and the parameter in (1) are not identifiable, since and for yield the same conditional distributions. Hence, we assume that , and define the class of candidate functions for estimation by

To estimate , we propose to minimize the least squares criteria of the form given in (3). The following proposition describes the solutions of this minimization problem.

Proposition 1.

Assume that is locally finite.

-

(i)

For a fixed , let be the distinct values of , with multiplicities . The minimizer of in is uniquely defined in the first argument on and in the second argument on , and it is given by

(4) -

(ii)

Let . The minimum of is achieved for a pair with and given by (4). The minimizer is not unique.

The estimator in (4) is called the isotonic distributional regression in Henzi et al., (2021), and the fact that it is a minimizer is due to Theorem 2.1 of that article; the condition that is locally finite is only necessary to ensure uniqueness in part (i). It follows directly from (4) that is indeed a CDF for . For a fixed , the estimator depends on only through its support, as can be seen from (4). It suffices to compute it at the distinct values of , since for ,

and if . Part (ii) of the proposition follows by the same steps as Proposition 2.2 in Balabdaoui et al., 2019a . Note that the minimizers and, hence, do depend on , which appears in the criterion (3). To lighten the notation, we write in the following, and only use the subscript when it is necessary to indicate the dependence on . To define beyond the set , we let

| (5) |

for and , and

We apply these interpolation methods in our empirical studies in Section 5. For the theory, any other interpolation methods satisfying the monotonicity constraints in both arguments is admissible.

In the forecasting literature, the loss function (3) with equal to the Lebesgue measure is known under the name continuous ranked probability score (CRPS), which is a widely used proper scoring rule for the estimation of distribution functions and for forecast evaluation (Gneiting and Raftery,, 2007). The criterion with general Borel measures are the so-called threshold weighted forms of the CRPS (Gneiting and Ranjan,, 2011). At a first sight, the CRPS seems to be a natural choice for the loss function since it weighs all thresholds equally, but it has the drawback that is finite only if the conditional distributions corresponding to have finite first moment; see (21) in Gneiting and Raftery, (2007). This is an unnecessary assumption if the goal is the estimation of the conditional CDFs, rather than conditional expectations, and it complicates proofs of consistency. We therefore focus on finite measures .

3 Convergence rates

3.1 Assumptions

We proceed to establish consistency results for the bundled estimator and for the the separated estimators and . The proofs and assumptions are closely related to those by Balabdaoui et al., 2019a for the monotone single index model.

Assumption 1.

The set is bounded and convex.

Assumption 2.

The measure and the distribution of satisfy one of the following assumptions.

-

(i)

The distribution of admits a Lebesgue density which is bounded from below by and from above by , and has finite support, putting mass only on points .

-

(ii)

For all , the distribution of conditional on admits a Lebesgue density bounded from below by and from above by , with constants not depending on . The measure has support on and admits a Lebesgue density bounded from above by .

Assumption 3.

For all the function is continuously differentiable on with derivative , and for all and some .

Assumption 4.

For all , the random variable admits a Lebesgue density bounded from below by and from above by .

Assumption 5.

The density of is continuous on .

Assumptions 1, 4 and 5 correspond to (A1), (A4) and (A6) in Balabdaoui et al., 2019a , respectively, and Assumption 3 is a direct extension of their condition (A5) to our case.

In the next sections, we present one of the main convergence results of this work, derived under the assumptions above. The case would have been a natural choice. One referee raised the point of whether one can derive rates of convergence in this case when the distribution of is compactly supported. Unfortunately, compactness of the support does not solve the issue that empirical process associated with the estimation problem at hand contains a term that cannot be handled with the classical results such as Lemma 3.4.2 or Lemma 3.4.3 of van der Vaart and Wellner, (1996). The reason behind the additional difficulties is that this term in question is of the form

where is random function involving the empirical measure ; additional details are provided in Section 4. More sophisticated tools need to be used in this context. The problem is beyond the scope of this article but worth investigating in future research.

3.2 Convergence rate for the bundled estimator

The results for convergence rates for both types of in Assumption 2 are presented in a unified framework. For the bundled estimator, we obtain the following result.

The proof of Theorem 1 applies Theorem 3.4.1 and Lemma 3.4.2 of van der Vaart and Wellner, (1996), and it is given in Section A.1. In the following, we introduce empirical process notation, provide auxiliary results that are of independent interest, and discuss the techniques and problems involved in the proof.

In accordance with Assumption 1, assume for all and some , so that for . In the proofs, the following function classes appear,

where the support in the class has to be extended to for technical reasons. Non-increasing functions are considered as elements of by constant extrapolation at the boundaries. Denote the -norm of functions from to , with respect to a Borel measure , by

For integration with respect to the Lebesgue measure over a set , we write . The bracketing entropy of a function class with respect to some norm is denoted by , and the bracketing integral is defined as

The following proposition, which relies on Theorem 2.7.5 of van der Vaart and Wellner, (1996) and a result of Feige and Schechtman, (2002), is crucial for all our results.

Proposition 2.

Let be a Lebesgue continuous distribution with support in a bounded set contained in a ball of radius with density bounded from above by . Then,

for universal constants .

Due to Proposition 2, the entropy of the class of functions for and fixed is of the same order as the entropy of the monotone function class with values in . If has finite support, this is sufficient to obtain the cubic convergence rate. However, as one would expect, the constants in the bounds increase with the size of the support, and it is not possible to extend the same proof strategy to Lebesgue continuous . For this case, a bound for the entropy of the class

| (6) |

is required. We find such a bound by constructing a suitable discretization of the support of .

Remark 1.

One might think that a simpler way to bound the entropy of the class would be via the results of Gao and Wellner, (2007) on the entropy of multivariate monotone function. Indeed, the function is bivariate monotone, and due to Proposition 2, the fact that we have in the first argument only increases the entropy by a constant factor. However, according to Theorem 1.1 of Gao and Wellner, (2007), the entropy of the class of bivariate monotone functions is of order , which leads to a diverging entropy integral. Even with the relaxation discussed on p. 326 of van der Vaart and Wellner, (1996), which allows to integrate only from for small in the entropy integral, it is not possible to achieve the cubic rate with this entropy bound.

3.3 Convergence rate for the separated estimators

The rate for the separated estimators and relies on Theorem 1 and is proved in a similar way as in Theorem 5.2 and Corollary 5.3 of Balabdaoui et al., 2019a . Note that under our model assumptions, the parameters and are indeed identifiable. More precisely, if almost surely for a fixed , then for , and . This is shown in an analogous way as in Proposition 5.1 of Balabdaoui et al., 2019a , and it is proven in Section A.5 for completeness.

Theorem 2.

Let Assumptions 1, 2 and 4 hold true. Assume that for each the function is left-continuous, non constant and does not have discontinuity points on the boundary of . Furthermore, assume that from each subsequence we can extract another subsequence which satisfies

| (7) |

almost surely. Then,

-

(i)

converges to in probability in the euclidean norm,

-

(ii)

for all continuity points of in , we have that converges to in probability.

Theorem 3.

Part (ii) of Theorem 3 can be regarded as analogous to the result (2) derived by Henzi et al., (2023, Theorem 5.1), with the weighted -norm replacing the supremum norm. Henzi et al., (2023) do not assume a linear index function, but they impose the assumption that the index function is estimated the rate of , rather than deriving a convergence rate, which we do in part (i) of the above theorem.

4 Empirical distribution as weighting measure

The methods proposed so far require the specification of a weighting measure . An interesting variant of the criterion (3), which does not require an explicit weighting choice, arises when equals the empirical distribution ; that is,

According to the follwing lemma, for this choice of the estimator and the pointwise error of the CDFs at the observed values of the response variable do not depend on the scale of the observations .

Lemma 1.

Let be strictly increasing on the support of , and . Then, the following hold with probability one.

-

(i)

A tuple minimizes if and only if with is a minimizer of , and it holds that .

- (ii)

The above result is generally not true for in (3). The invariance property aligns well with the fact that the transformed outcome again follows a distributional single index model with the same parameter and the corresponding CDFs . However, it turns out that deriving convergence rates for this criterion is substantially more difficult than for fixed measures , because the integral in the function class in (6) is now over the random measure instead of the fixed measure . We suspect that the rate for this estimator should still be of order , and our simulations confirm this intuition in certain examples. However, a completely different strategy of proof seems necessary to prove this rate.

5 Empirical results

5.1 Simulations

| Simulation | Error type | Spherical coordinates | ||||||

|---|---|---|---|---|---|---|---|---|

| Empirical | Index | 0.49 (0.04) | 0.50 (0.04) | 0.63 (0.05) | 0.48 (0.03) | 0.47 (0.03) | 0.49 (0.03) | |

| Exponential | CDF | 0.25 (0.01) | 0.23 (0.01) | 0.36 (0.01) | 0.27 (0.01) | 0.19 (0.02) | 0.27 (0.01) | |

| Bundled | 0.36 (0.01) | 0.36 (0.01) | 0.37 (0.01) | 0.37 (0.01) | 0.37 (0.01) | 0.37 (0.01) | ||

| Index | 0.49 (0.04) | 0.50 (0.05) | 0.60 (0.05) | 0.48 (0.03) | 0.55 (0.03) | 0.48 (0.03) | ||

| Gaussian | CDF | 0.30 (0.01) | 0.30 (0.01) | 0.37 (0.02) | 0.33 (0.01) | 0.33 (0.01) | 0.34 (0.01) | |

| Bundled | 0.38 (0.01) | 0.38 (0.01) | 0.40 (0.01) | 0.39 (0.01) | 0.39 (0.01) | 0.39 (0.01) | ||

| Truncated | Index | 0.50 (0.04) | 0.53 (0.04) | 0.54 (0.05) | 0.51 (0.03) | 0.48 (0.03) | 0.46 (0.03) | |

| Exponential | CDF | 0.24 (0.02) | 0.24 (0.02) | 0.38 (0.03) | 0.29 (0.02) | 0.21 (0.02) | 0.27 (0.02) | |

| Bundled | 0.37 (0.01) | 0.37 (0.01) | 0.40 (0.02) | 0.39 (0.01) | 0.39 (0.01) | 0.40 (0.01) | ||

| Index | 0.46 (0.04) | 0.48 (0.05) | 0.55 (0.05) | 0.48 (0.03) | 0.55 (0.03) | 0.50 (0.03) | ||

| Gaussian | CDF | 0.28 (0.01) | 0.29 (0.02) | 0.37 (0.02) | 0.32 (0.02) | 0.30 (0.01) | 0.33 (0.02) | |

| Bundled | 0.38 (0.01) | 0.38 (0.01) | 0.41 (0.01) | 0.39 (0.01) | 0.40 (0.01) | 0.40 (0.01) | ||

| Uniform | Index | 0.56 (0.04) | 0.55 (0.04) | 0.61 (0.05) | 0.45 (0.03) | 0.49 (0.03) | 0.48 (0.03) | |

| Exponential | CDF | 0.21 (0.02) | 0.21 (0.02) | 0.38 (0.02) | 0.27 (0.03) | 0.19 (0.03) | 0.24 (0.03) | |

| Bundled | 0.37 (0.01) | 0.36 (0.01) | 0.39 (0.01) | 0.37 (0.01) | 0.38 (0.01) | 0.39 (0.01) | ||

| Index | 0.49 (0.04) | 0.46 (0.04) | 0.56 (0.05) | 0.48 (0.03) | 0.53 (0.03) | 0.49 (0.03) | ||

| Gaussian | CDF | 0.26 (0.02) | 0.27 (0.02) | 0.38 (0.02) | 0.29 (0.02) | 0.22 (0.02) | 0.29 (0.02) | |

| Bundled | 0.38 (0.01) | 0.38 (0.01) | 0.41 (0.01) | 0.39 (0.01) | 0.39 (0.01) | 0.39 (0.01) | ||

We investigate the convergence of our estimators in simulations. For , we simulate , , independently, and generate the response variable in two ways,

| (9) |

For the weighting measure , we consider the empirical distribution , the uniform distribution on and the Gaussian distribution with variance truncated to the interval for the simulations with Gaussian noise, and the uniform distribution on and the truncated Gamma distribution with shape and scale for the simulations with exponentially distributed noise, respectively. The rationale is that the uniform distribution over a large set provides a rather rough choice for the weighting, whereas the truncated distributions more closely follow the actual outcome distributions, up to truncation to a compact interval.

The index is parameterized in spherical coordinates with and values for , and and values for . To perform estimation, we parameterize in spherical coordinates and do a grid search followed by local numerical optimization. For , we choose equidistant points , evaluate the criterion (3) at , and perform numerical optimization of with respect to in around the for which the minimal value of the criterion is attained. The procedure for is analogous, and for the grid we take all combinations of equidistant points and points , , . Numerical optimization is performed with optimize in R (R Core Team,, 2022) for , and nmkb from the package dfoptim (Varadhan et al.,, 2020) for . Estimation of the conditional CDFs uses the isodistrreg package (Henzi et al.,, 2021). A general implementation of our estimator and replication material for Section 5 are available on https://github.com/AlexanderHenzi/distr_single_index.

To estimate the rates of convergence, we simulate realizations of the examples described above for each of the sample sizes , , and compute the the index error , the bundled error , and of the error of the CDFs . The integrals in and are estimated with the mean of the integrand evaluated at draws for and , or , respectively. We then estimate the convergence rate with the slope coefficient from regressing , for all and samples , on , for each setting and error measure. The estimates and standard errors are shown in Table 1. Naturally, there are many factors influencing the convergence rates estimates, such as noise in the estimation, different constants in different examples, and, most importantly, the fact that the rates of the errors are only estimated on a grid of finite sample sizes. Therefore, even if one might expect the same asymptotic rates in the examples that we consider, there are some deviations due to different constants and finite sample effects. However, Table 1 suggests that the rate of is faster than , as in the experiments of Balabdaoui et al., 2019a , and the rates for the bundled estimator and for the CDF are around . There are no systematic differences between the results for and for the other approaches, with average rates over all settings of , , and for the index, CDF, and bundled estimator for the empirical weighting measure, and , , and for the other weighting methods. This suggests that the same rates should hold for .

Remark 3.

For dimension , the computation of is a one-dimensional optimization problem, and can be approximated to a high accuracy provided that the grid for the initial grid search is fine enough. For the grid search becomes expensive, and there are no guarantees that a pair chosen by our implementation is a global minimizer of our target function, which is non-smooth and non-convex. Estimation in the monotone single index model for the mean suffers from the same optimization difficulties, and although there has been extensive research on implementation and alternative methods for estimating (Groeneboom,, 2018; Balabdaoui et al., 2019b, ; Groeneboom and Hendrickx,, 2019; Balabdaoui and Groeneboom,, 2021), the computation of remains a challenge, especially in higher dimensions.

5.2 Illustration on house price data

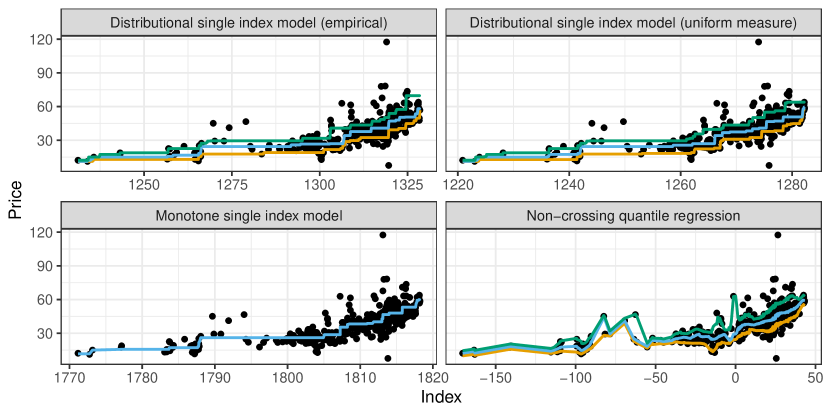

We illustrate the distributional single index model in a data example by Jiang and Yu, (2023, Section 4.4). The data set, which is available on https://doi.org/10.24432/C5J30W, contains 414 real estate transaction records from Tapiei City and New Taipei City. The dependent variable is the price per unit area, and the covariates are the number of convenience stores in the living circle on foot, the building age, the transaction year and month, and the distance to the nearest metro station. The transaction time is transformed to a numerical variable with values in between and , and it is a proxy variable which captures effects such as trends in the house prices, or different policy regimes over time that might influence the prices.

Figure 1 depicts the index values and prices , , for the distributional single index model, the monotone single index model, and for the non-crossing quantile regression estimator by Jiang and Yu, (2023); the results for the latter are equal to their Figure 3 (c) and reproduced with the code from the supplement of their article. We implemented the distributional index model with the empirical measure and with the uniform measure over a large set including all observed prices. For the distributional methods, the lines in the figure show estimated conditional quantiles at levels , which are obtained by inversion of the CDFs for our estimator. Jiang and Yu, (2023) center all covariates around their mean before estimation. With shape restricted estimation methods, such centering is not necessary since it does not change the order of the projections . As the scatterplots suggests, the order of the index values , , obtained with the three methods are very similar, and the pairwise Spearman correlations between them are indeed all above . In the given data application, all methods have advantages and disadvantages. The computation of the estimator by Jiang and Yu, (2023) is fast, but it involves several tuning parameters, namely, an initial quantile level for estimation, set to , bandwidths for kernel smoothing, and a pre-specified grid of quantiles on which the estimator is computed and evaluated, chosen to be . Estimation for our method and for the monotone single index model is slower, since we take a fine grid for the grid search over and perform local optimization in several regions to ensure a good approximation of the minimum. However, the parameters of the shape restricted methods are more easily interpretable due to the monotone dependence on . One can draw the — reasonable — conclusions that the price is increasing in the number of closely situated convenience stores and over time, and decreasing in the distance to the nearest metro station and in the age of the building; see Table 2. The interpretation is more difficult for the estimator by Jiang and Yu, (2023). Although the signs of in their estimator agree with those of the shape restricted methods, the conditional quantile curves are non-monotone and interpolate the prices for some of the observations.

| Method | Number stores | Building age | Transaction date | Distance metro |

|---|---|---|---|---|

| Distributional index model (empirical) | 0.706 | -0.263 | 0.658 | -0.013 |

| Distributional index model (uniform) | 0.750 | -0.186 | 0.634 | -0.008 |

| Monotone single index model | 0.415 | -0.122 | 0.902 | -0.006 |

| Non-crossing quantile regression | 0.152 | -0.060 | 0.987 | -0.004 |

6 Discussion

In this article, we proposed estimators for the distributional single index model, and proved a convergence rate of both for bundled and separated estimators. This greatly improves upon the -rate known so far. There are several avenues for future research. Consistency for our transformation-invariant estimator proposed in Section 4 is an open challenge, which goes beyond the techniques applied for the convergence rates in this article. A possible future research direction is to study convergence under more general weighting measures with possibly an unbounded support. This would allow analyzing whether there is an optimal choice of in terms of the estimation error for . As for the monotone single index model, our simulations also suggest that is estimated at a faster rate. Deriving this rate, as well as a comparison to the estimators for in the monotone single index model, would be an interesting direction for future work.

Acknowledgments

We are grateful to an anonymous referee for helpful comments.

References

- (1) Balabdaoui, F., Durot, C., and Jankowski, H. (2019a). Least squares estimation in the monotone single index model. Bernoulli, 25(4B):3276–3310.

- Balabdaoui and Groeneboom, (2021) Balabdaoui, F. and Groeneboom, P. (2021). Profile least squares estimators in the monotone single index model. In Advances in contemporary statistics and econometrics — Festschrift in honor of Christine Thomas-Agnan, pages 3–22. Springer, Cham.

- (3) Balabdaoui, F., Groeneboom, P., and Hendrickx, K. (2019b). Score estimation in the monotone single-index model. Scand. J. Stat., 46(2):517–544.

- Feige and Schechtman, (2002) Feige, U. and Schechtman, G. (2002). On the optimality of the random hyperplane rounding technique for max cut. Random Structures & Algorithms, 20(3):403–440.

- Gao and Wellner, (2007) Gao, F. and Wellner, J. A. (2007). Entropy estimate for high-dimensional monotonic functions. J. Multivariate Anal., 98(9):1751–1764.

- Gneiting and Raftery, (2007) Gneiting, T. and Raftery, A. E. (2007). Strictly proper scoring rules, prediction, and estimation. J. Amer. Statist. Assoc., 102(477):359–378.

- Gneiting and Ranjan, (2011) Gneiting, T. and Ranjan, R. (2011). Comparing density forecasts using threshold- and quantile-weighted scoring rules. J. Bus. Econom. Statist., 29(3):411–422.

- Groeneboom, (2018) Groeneboom, P. (2018). Algorithms for computing estimates in the single index model. https://github.com/pietg/single_index.

- Groeneboom and Hendrickx, (2019) Groeneboom, P. and Hendrickx, K. (2019). Estimation in monotone single-index models. Stat. Neerl., 73(1):78–99.

- Härdle et al., (1993) Härdle, W., Hall, P., and Ichimura, H. (1993). Optimal smoothing in single-index models. Ann. Statist., 21(1):157–178.

- Henzi et al., (2023) Henzi, A., Kleger, G.-R., and Ziegel, J. F. (2023). Distributional (single) index models. J. Amer. Statist. Assoc., 118(541):489–503.

- Henzi et al., (2021) Henzi, A., Ziegel, J. F., and Gneiting, T. (2021). Isotonic distributional regression. J. R. Stat. Soc. Ser. B. Stat. Methodol., 83(5):963–993.

- Jiang and Yu, (2023) Jiang, R. and Yu, K. (2023). No-crossing single-index quantile regression curve estimation. J. Bus. Econom. Statist., 41(2):309–320.

- Lavrič, (1993) Lavrič, B. (1993). Continuity of monotone functions. Arch. Math. (Brno), 29(1-2):1–4.

- Mösching and Dümbgen, (2020) Mösching, A. and Dümbgen, L. (2020). Monotone least squares and isotonic quantiles. Electron. J. Stat., 14(1):24–49.

- Murphy et al., (1999) Murphy, S. A., van der Vaart, A. W., and Wellner, J. A. (1999). Current status regression. Math. Methods Statist., 8(3):407–425.

- R Core Team, (2022) R Core Team (2022). R: A Language and Environment for Statistical Computing. R Foundation for Statistical Computing, Vienna, Austria.

- van der Vaart, (1998) van der Vaart, A. W. (1998). Asymptotic statistics, volume 3 of Cambridge Series in Statistical and Probabilistic Mathematics. Cambridge University Press, Cambridge.

- van der Vaart and Wellner, (1996) van der Vaart, A. W. and Wellner, J. A. (1996). Weak convergence and empirical processes. Springer Series in Statistics. Springer-Verlag, New York. With applications to statistics.

- Varadhan et al., (2020) Varadhan, R., Borchers, H. W., and Bechard, V. (2020). dfoptim: Derivative-Free Optimization. R package version 2020.10-1.

Appendix A Proofs

A.1 Proof of Theorem 1

The proof of Theorem 1 is slightly different for the two cases in Assumption 2, which involve different entropy calculations. We first give a proof for the theorem with an unspecified constant in an entropy bound, and then derive the constant for the two cases in separate lemmas.

Proof of Theorem 1.

The proof applies Theorem 3.4.1 and Lemma 3.4.2 of van der Vaart and Wellner, (1996).

Expanding the squares and using the fact that yields

Furthermore, we have

or, when rescaling with and using empirical process notation,

We now analyze the functions of the form

with , and denote the class of such functions by . Also, let contain all functions of type

with and for which

The elements in are obtained by shifting elements of by a fixed function, so we have . To apply Lemma 3.4.2 of van der Vaart and Wellner, (1996), we have to find an upper bound for the bracketing entropy of the class . Since is a finite measure, we have

The function above does not contribute to the entropy, and does not depend on and belongs to the class , for which we know from Assumptions 1 and 2 and Proposition 2 that for a constant . In separate lemmas below, we show that the entropy of the functions of the form above, with , is bounded from above by for some constant . Let now be an -bracket containing and an -bracket containing . We interpret as functions of which are constant in . Then the functions , form a -bracket containing , because

Consequently, the number of -brackets required to cover is bounded from above by , which yields the following bound on the entropy integral,

Lemma 3.4.2 of van der Vaart and Wellner, (1996) with implies

Consequently, with

we have

and, for , . Since maximizes by definition, Theorem 3.4.2 of van der Vaart and Wellner, (1996) implies that . ∎

For the entropy of the function class

we begin with the simpler case that has finite support.

Lemma 2.

Proof of Lemma 2.

Recall that puts all its mass on the points . Let , be -brackets covering , and let be an -bracket containing , . Then,

are an -bracket containing , because

Moreover, there are functions of the form of , corresponding to choices for and choices of . So for , we have

∎

For with Lebesgue continuous distribution, the entropy bound is as follows.

Proof of Lemma 3.

We assume that is Lebesgue continuous on with density bounded from above by . Discretize the interval with a net of suitable size, namely, let and define

The functions are contained in the class . Let , be -brackets for , such that for all . For let be an index such that , and for , define

and the functions

with for . Note that there are at most such functions for all choices of and , . By construction, we have

We show that form an -bracket. First, notice that

We separate the outer integral into three parts. The lower part, over , satisfies

since are -brackets. The upper part over equals because for . For the middle part over , let in . Then,

and we expand the integrand as follows

| (10) |

Since , are -brackets, we have

and also, because

The cross-terms can be bounded by applying the Cauchy-Schwarz inequality,

applying the bounds from above; the other cross terms are bounded in an analogous way. Hence,

where the factor is due to the fact that one obtains square terms and cross-terms from expanding the square in (A.1). So we have

Consequently, we obtain

∎

A.2 Proof of Proposition 2

Proof.

Fix . By Lemma 21 of Feige and Schechtman, (2002), we know that can be partitioned into subsets of equal size with diameter at most such that , for a universal constant . Let be points in these subsets. Furthermore, from Theorem 2.7.5 of van der Vaart and Wellner, (1996), we can find brackets with respect to the norm .

Let . Then, for some and . Let and such that and . Now, it follows from the Cauchy-Schwarz inequality that

By monotonicity of this implies that

and hence

| (11) |

Now, using the Minkowski inequality, we have that

Note that for any , there exists such that . Without loss of generality we assume that . Consider the change of variable where

Then,

where above used that for all . Using a similar reasoning, we can bound by the same constant. Now, we turn to . With the same change of variable, we have that

using monotonicity of and that for all . Now,

Thus,

If we put , then the previous calculations and the inequality (11) imply that

and hence

which in turn implies that

Finally, since the Lebesgue density of is bounded from above by , the previous bound implies

∎

A.3 Proof of Theorem 2

Proof.

For simplicity of notation, index the subsequence by , and choose an in the underlying probability space such that (7) holds true. Recall that is non increasing in the first entry and non decreasing in the second entry for every . Lemma 2.5. in van der Vaart, (1998) can be adapted to this case. Therefore converges pointwise along a subsequence to a bivariate function at each point of continuity of that lies in . The limit has the property that is left continuous and non increasing for each and non decreasing for every . Furthermore, is a sequence in a compact space and hence converges along a further subsequence to in the Eudlidean distance.

Our goal is to show that and . Recall that if the distance between two functions is zero then they coincide almost surely. We have

by applying the Cauchy-Schwarz inequality, where

We show that for the terms converge to zero almost surely, so almost surely.

Recall that converges to . Therefore, at all continuity points of we have that converges to . Note that is bounded and monotone in both variables. Lavrič, (1993) shows that the set of all discontinuity points of the bivariate, monotone function may not be countable but has Lebesgue measure . When using that both and are equivalent to the Lebesgue measure, under our assumptions, we have that by Lebesgue’s dominated convergence Theorem. The second integral converges to directly by (7). Finally, we rewrite the third integral to

where denotes the distribution of and is a random variable that is independent of the data, but has distribution . As at each point of continuity of , the function converges to and the set of discontinuity points of has Lebesgue measure 0, Assumption 4 and Lebesgue’s dominated convergence theorem imply that .

If necessary, modify to not have discontinuity points at the boundary. By Proposition 3 it follows that and everywhere on . As we have found almost sure convergence along a subsequence, we follow that the statements hold true for convergence in probability. ∎

A.4 Proof of Theorem 3

Proof.

We apply Lemma 2.5. from Murphy et al., (1999). Rewrite the integrated error as follows,

where the expectation is a shorthand notation of integrating with respect to a random variable whose distribution is the product measure of and . The functions and are and . The Cauchy-Schwarz inequality and the tower property of conditional expectations yield

where

If it follows by Murphy et al., (1999) that

| (12) |

We now prove that there exists a such that from any subsequence , there exists a subsequence along which almost surely. This shows that .

To prove the claim, consider an arbitrary subsequence. For simplicity of notation, index it with . Define and . As and is compact, converges to some along a subsequence. Recall that converges to in probability. Therefore, we can extract a further subsequence along which the convergence from to and from to happens almost surely. To make notation less cumbersome we index this subsequence again by . Fix an event in the underlying probability space such that and , so that we can consider and as non-random.

By Assumption 3, for every the map is continuously differentiable on . Extend the function such that it is bounded and continuously differentiable on and the partial derivative is bounded on . By Taylor’s Theorem we have that for and ,

| (13) |

Thus the numerator of becomes

as the mixed term can be controlled by

This is because the partial derivative is bounded. Similarly the denominator becomes

We rewrite

By Lemma 9.1 in the supplement of Balabdaoui et al., 2019a we have that almost surely. By Lebesgue’s dominated convergence theorem and the continuity of , we have that

As , it follows that and thus and . Write

Then, we have that where does not depend on the chosen path . It remains to prove that . We first expand the matrix in the denominator and get

Note that equals the numerator in the expression of . Consider some with . Define the matrix to have first row equal to and second row equal and . Since has a density that is positive on , the variable admits a density that is positive on the set , which has non-empty interior. Then,

is equal to zero if and only if almost surely or equivalently almost surely. This would mean that the distribution of is concentrated on a one-dimensional subspace. This contradicts the fact that the density of with respect to the Lebesgue measure is positive on . It follows that and thus . This proves the claim. In integral notation, it follows from (12) that

for some by the previous observations, for large enough. Note that the infimum above is strictly positive and achieved for some , as the function is continuous, is compact and the density is bounded away from zero. Thus, there exists such that

for large and almost surely.

We turn to the second part. Recall that the density of is bounded from below by , so

| (14) | ||||

with probability tending to one for , using the definition of and that . The left-hand side of (14) can be bounded from above by

The first term is bounded by Theorem 1 and the seconded term can be handled due to the fact that the absolute value of the partial derivative is bounded by ; this yields

∎

A.5 Identifiability

The identifiability result in this section is a direct adaptation of Theorem 5.1 of Balabdaoui et al., 2019a .

Proposition 3.

Assume is convex and has at least one interior point. Furthermore, assume has a density with respect to the Lebesgue measure which is strictly positive on . Suppose that for each the function is left-continuous (or right-continuous), non constant and does not have discontinuity points on the boundary of . Then is identifiable.

Proof.

We will prove the left-continuous case; the right-continuous case can be treated with the same arguments. Consider pairs having the property that for each , the functions on and are left-continuous on , non constant and do not have discontinuity points on the boundary of their domain. Assume

for almost all . Fix and define and . By assumption we have for almost every . As are left-continuous, this holds for all points in the interior of . If we prove we can follow that on the interior of . As there are no discontinuity points on the boundary, holds everywhere on and finally, so on . Therefore, it suffices to show .

As is convex, for small enough we can find an open ball of radius contained in such that is non constant and

| (15) |

for every . Without loss of generality, we assume that is centered at the origin — if necessary, replace with and with , where is the center of a ball with the desired properties. We first show and then .

Assume for a contradiction that . Then and are linearly independent and by the Cauchy-Schwarz inequality for , it holds and . Using the monotonicity of and it follows that

for each and so on . By the same arguments one shows on , and so on . Hence, for we have

| (16) |

Since is non-constant on , there exists a point of strict decrease, so one of the following two conditions must hold,

| (17) | ||||

| (18) |

The ball can be chosen in such a way that . In the case (17), if we can choose small enough such that for it holds and , since . Then, we have

which contradicts (16). If we let and choose sufficiently small such that and . Then,

which contradicts (16), again. The second case, (18), can be proven with similar ideas. Namely, if choose and small enough such that . Then,

which contradicts (16). If choose and small enough such that . Then,

which contradicts (16). This proves .

A.6 Proof of Lemma 1

Proof.

Replacing by in (4) and the fact that almost surely for imply , which also yields the statement about the minimizers in (i). Part (ii) holds by definition of , , , and . ∎