Blending gradient boosted trees and neural networks for point and probabilistic forecasting of hierarchical time series

Abstract

In this paper we tackle the problem of point and probabilistic forecasting by describing a blending methodology of machine learning models that belong to gradient boosted trees and neural networks families. These principles were successfully applied in the recent M5 Competition on both Accuracy and Uncertainty tracks. The keypoints of our methodology are: a) transform the task to regression on sales for a single day b) information rich feature engineering c) create a diverse set of state-of-the-art machine learning models and d) carefully construct validation sets for model tuning. We argue that the diversity of the machine learning models along with the careful selection of validation examples, where the most important ingredients for the effectiveness of our approach. Although forecasting data had an inherent hierarchy structure (12 levels), none of our proposed solutions exploited that hierarchical scheme. Using the proposed methodology, our team was ranked within the gold medal range in both Accuracy and the Uncertainty track. Inference code along with already trained models are available at https://github.com/IoannisNasios/M5_Uncertainty_3rd_place

keywords:

M5 Competition , Point forecast , Probabilistic forecast , Regression models , Gradient Boosted Trees , Neural Networks , Machine learning1 Introduction

Machine Learning (ML) methods have been well established in the academic literature as alternatives to statistical ones for time series forecasting [1, 2, 3, 4, 5]. The results of the recent M-competitions also reveal such a trend from the classical Exponential Smoothing and ARIMA methods [6] towards more data-driven generic ML models such as Neural Networks [7] and Gradient Boosted Trees [8, 9].

One of the most important results of the recent M5 Competition [1] was the superiority of Machine Learning methods, particularly the Gradient Boosted Trees and Neural Networks, against statistical time series methods (e.g., exponential smoothing, ARIMA etc.). This realization is in the opposite direction of the findings of previous M competitions that classical time series methods were more accurate, and establishes a milestone in the domination of Machine Learning in yet another scientific domain.

The M5 forecasting competition was designed to empirically evaluate the accuracy of new and existing forecasting algorithms in a real-world scenario of hierarchical unit sales series. The dataset provided contains hierarchical sales data from Walmart. It covers stores in three US states (California Texas and Wisconsin) and includes sales data per item level, department and product categories and store details ranging from February 2011 to April 2016. The products have a (maximum) selling history of days. The competition was divided into two tracks, one requiring point forecasts (Accuracy track), and one requiring the estimation of the uncertainty distribution (Uncertainty track). The time horizon for both tracks was 28 days ahead. For the Accuracy track, the task was to predict the sales for each one of the hierarchical time series following day . For the Uncertainty track, the task was to provide probabilistic forecasts for the corresponding median and four prediction intervals (, , , and ).

Table 1 presents all hierarchical groupings of the data. Level 12, containing unique combinations of product per store, is the most disaggregated level. Following the competition rules, only these series needed to be submitted; the forecasts of all higher levels would be automatically calculated by aggregating (summing) the ones of this lowest level. So, regardless the way we used the hierarchy information to produce 28-day ahead predictions, all we needed to actually submit was level 12 series only.

| Level | Level Description | Aggr. Level | #of series |

| 1 | Unit sales of all products, aggregated for all stores/states | Total | 1 |

| 2 | Unit sales of all products, aggregated for each State | State | 3 |

| 3 | Unit sales of all products, aggregated for each store | Store | 10 |

| 4 | Unit sales of all products, aggregated for each category | Category | 3 |

| 5 | Unit sales of all products, aggregated for each department | Department | 7 |

| 6 | Unit sales of all products, aggregated for each State and category | State/Category | 9 |

| 7 | Unit sales of all products, aggregated for each State and department | State/Department | 21 |

| 8 | Unit sales of all products, aggregated for each store and category | Store/Category | 30 |

| 9 | Unit sales of all products, aggregated for each store and department | Store/Department | 70 |

| 10 | Unit sales of product x, aggregated for all stores/states | Product | 3,049 |

| 11 | Unit sales of product x, aggregated for each State | Product/State | 9,147 |

| 12 | Unit sales of product x, aggregated for each store | Product/Store | 30,490 |

| Total | 42,840 | ||

2 Machine Learning based forecasting

Machine Learning methods are designed to learn patterns from data and they make no assumptions about their nature. Time series forecasting can be easily formulated as a supervised learning task. The goal is to approximate a function controlled by a set of parameters , which corresponds to the relation between a vector of input variables (features) and a target quantity. The machine learning setup is completed once we define: a) a (training) dataset consisting of a set of tuples containing features that describe a target (number of daily sales in the context of M5 competition) and b) a suitable loss function to be minimized . The parameters of are then tuned to minimize the loss function using the tuples of the training dataset .

2.1 Feature engineering

One of the key ingredients in any Machine Learning method is the creation of representative and information-rich input features . The task of feature engineering is a largely ad hoc procedure, considered equal parts science and art, and it crucially depends on the experience of the practitioner on similar tasks. In the context of the M5 Competition, we worked with the following feature groups:

-

1.

Categorical id-based features: This is a special type of features that take only discrete values. Their numerical encoding can take many forms and depends on the methodology chosen.

-

(a)

Categorical variables encoding via mean target value: It is a process of encoding the target in a predictor variable perfectly suited for categorical variables. Each category is replaced with the corresponding probability of the target value in the presence of this category [10].

-

(b)

Trainable embedding encoding: A common paradigm that gained a lot of popularity since its application to Natural Language Processing [11, 12] is to project the distinct states of a categorical feature to a real-valued, low-dimensional latent space.This is usually implemented as a Neural Network layer (called Embedding Layer) and it is used to compactly encode all the discrete states of a categorical feature. Contrary to one hot encoding which are binary, sparse, and very high-dimensional, trainable embeddings are low-dimensional floating-point vectors (see Fig. 1):

Figure 1: Trainable embeddings vs one hot encoding. Image taken from [13]

-

(a)

-

2.

Price related: Sell prices, provided on a week level for each combination of store and product. Prices are constant at weekly basis, although they may change through time. Using this information we calculate statistical features such as maximum, minimum, mean, standard deviation and also number of unique historical prices for each combination of store and product (level 12).

-

3.

Calendar related

-

(a)

Special events and holidays (e.g. Super Bowl, Valentine’s Day, and Orthodox Easter), organized into four classes, namely Sporting, Cultural, National, and Religious.

-

(b)

Supplement Nutrition Assistance Program (SNAP) activities that serve as promotions. This is a binary variable (0 or 1) indicating whether the stores of CA, TX or WI allow SNAP purchases on the examined date.

-

(a)

-

4.

Lag related features:

-

(a)

Lag only: These features are based the historical sales for each store/product combination (level 12) for days before a given date with ranging from to , thus spanning two weeks.

-

(b)

Rolling only: Rolling mean and standard deviation of historical sales for each store/product (level 12) ending 28 days before a given date .

-

(c)

Lag and rolling: Rolling mean and standard deviation until a lag date in the past.

-

(a)

In total we devised around input features, each one used to predict the unit sales of a specific product/store (Level 12) for one specific date.

2.2 Cross Validation

The inherent ordering of time series forecasting (i.e. the time component) forces ML practitioners to define special cross validation schemes and avoid k-fold validation [14] random splits back and forth in time. We chose the following different training/validation splits.

-

1.

Validation split 1:

-

(a)

Training days

-

(b)

Validation days (last 28 days)

-

(a)

-

2.

Validation split 2:

-

(a)

Training days

-

(b)

Validation days (28 days before last 28 days)

-

(a)

-

3.

Validation split 3:

-

(a)

Training days

-

(b)

Validation days (exactly one year before)

-

(a)

Modeling and blending was based on improving the mean of the competition metric on these splits. For each split we followed a two step modeling procedure:

-

Tuning: Use all three validation sets and the competition metric to select the best architecture and parameters of the models.

-

Full train: Use the fine-tuned parameters of the previous step to perform a full training run until day .

The biggest added value of using multiple validation sets was the elimination of any need for external adjustments on the final prediction(see Finding 5 in [1]).

3 Point Forecast Methodology

Point forecast is based on ML models that predict the number of daily sales for a specific date and a specific product/store combination. In order to forecast the complete days horizon we apply a recursive multi-step scheme [15] . This involves using the prediction of the model in a specific time step (day) as an input in order to predict the subsequent time step. This process is repeated until the desired number of steps have been forecasted. We found this methodology to be superior to a direct multi-step scheme were the models would predict at once days in the future.

The performance measure selected for this forecasting task was a variant of Mean Absolute Scaled Error (MASE) [16] called Root Mean Squared Scaled Error (RMSSE). The measure for the 28 day horizon is defined in Eq. 1

| (1) |

where is the actual future value of the examined time series (for a specific aggregation level ) at point and the predicted value, the number of historical observations, and the day forecasting horizon. The choice of this metric is justified from the intermittency of forecasting data that involve sporadic unit sales with lots of zeros.

The overall accuracy of each forecasting method at each aggregation level is computed by averaging the RMSSE scores across all the series of the dataset using appropriate price related weights. The measure, called weighted RMSSE (WRMSSE) by the organizers, is defined in Eq. 2.

| (2) |

where is a weight assigned on the series. This weight is computed based on the last observations of the training sample of the dataset, i.e., the cumulative actual dollar sales that each series displayed in that particular period (sum of units sold multiplied by their respective price) [1]. The weights are computed once and kept constant throughout the analysis.

3.1 Models

Here we describe briefly the specific instances of GBM and neural network models used.

3.1.1 LightGBM models

LightGBM [17] is an open source Gradient Boosting Decision Tree (GBDT) [9, 18] implementation by Microsoft. It uses a histogram-based algorithm to speed up the training process and reduce memory. LightGBM models have proven to be very efficient in terms of speed and quality in many practical regression problems. For the Accuracy track, we trained two variations of LightGBM models:

| parameter | value |

|---|---|

| boosting_type | gbdt |

| objective | tweedie |

| tweedie_variance_power | 1.1 |

| subsample | 0.5 |

| subsample_freq | 1 |

| learning_rate | 0.03 |

| num_leaves | 2047 |

| min_data_in_leaf | 4095 |

| feature_fraction | 0.5 |

| max_bin | 100 |

| n_estimators | 1300 |

| boost_from_average | False |

| verbose | -1 |

| num_threads | 8 |

| parameters | value |

|---|---|

| boosting_type | gbdt |

| objective | tweedie |

| tweedie_variance_power | 1.1 |

| subsample | 0.6 |

| subsample_freq | 1 |

| learning_rate | 0.02 |

| num_leaves | 2**11-1 |

| min_data_in_leaf | 2**12-1 |

| feature_fraction | 0.6 |

| max_bin | 100 |

| n_estimators | see Table 4 |

| boost_from_average | False |

| verbose | -1 |

| num_threads | 12 |

| store_id | n_estimators |

|---|---|

| CA_1 | 700 |

| CA_2 | 1100 |

| CA_3 | 1600 |

| CA_4 | 1500 |

| TX_1 | 1000 |

| TX_2 | 1000 |

| TX_3 | 1000 |

| WI_1 | 1600 |

| WI_2 | 1500 |

| WI_3 | 1100 |

The target output of each LightGBM models was the sales count of a specific product. Since the target quantity (sales count) is intermittent and has a lot of zeros ( of daily sales are zeros), using the MSE loss function may lead to suboptimal solutions. For this reason, we implemented a special loss function that follows the Tweedie-Gaussian distribution [19]. Tweedie regression [20] is designed to deal with right-skewed data where most of the target values are concentrated around zero. In Figure 2 we show the histogram of sales for all available training data; it is obviously right skewed with a lot of concentration around zero.

.

The formula of the Tweedie loss function given a predefined parameter is shown in Eq. 3. In our implementation we used the default value of which is a good balance between the two terms:

| (3) |

where is a regression model controlled by a set of parameters that maps a set of multidimensional features to a target value (daily sales count). is the output of the regression model for input .

3.1.2 Neural Network models

We implemented the following two classes of Neural Network models:

-

1.

keras_nas - Keras MLP models.

Keras [13] is a model-level library, providing high-level building blocks for developing neural network models. It has been adopted by Google to become the standard interface for Tensorflow [21], its flagship Machine Learning library. Using the highly intuitive description of Keras building modules one can define a complex Neural Network architectures and experiment on training and inference.

In total we trained slightly different Keras models and we averaged their predictions. These models were grouped in slightly different architecture groups, and within each group we kept the final weights during training. This strategy helped reduce variance among predictions and stabilized the result, both in every validation split and in final training. The loss function chosen was mean squared error between the actual and predicted sale count. All model groups share the shame architecture depicted in Figure 3 and are presented in detail at https://github.com/IoannisNasios/M5_Uncertainty_3rd_place.

Figure 3: Basic Keras model architecture -

2.

fastai_cos - FastAI MLP models.

FastAI [22] is a Pytorch [23] based deep learning library which provides high-level components for many machine learning tasks. To tackle the regression task at hand, we incorporated the tabular module that implements state of the art deep learning models for tabular data. One important thing about FastAI tabular module is again the use of embedding layers for categorical data. Similarly to the Keras case, using the embedding layer introduced good interaction for the categorical variables and leveraged deep learning’s inherent mechanism of automatic feature extraction.

Our modelling approach includes implementing a special Tweedie loss function to be used during training. Roughly speaking, the FastAI tabular model is the Pytorch equivalent of Keras / Tensorflow keras_nas model with the difference of using a specially implemetned objective function. Empirical results on different regression contexts, mostly from Kaggle competitions, support this decision of using similar modelling methodology on complete different Deep Learning frameworks.

3.2 Ensembling

The final part of our modelling approach was to carefully blend the predictions of the diverge set of models. We divide our models in groups:

-

1.

lgb_cos: 1 LightGBM model, using all available data

-

2.

lgb_nas: 10 LightGBM models (1 model per store), using all available data for every store.

-

3.

keras_nas: 3 Keras models using only last days of data and simple averaging.

-

4.

fastai_cos: 1 FastAI model, using all available data

All these 4 model groups were finetuned to perform best on the average of the three validation splits described in Section 2.2 above. After fine-tuning, and using the best parameters, all 4 model groups were retrained using the information available until and then used to produce forecasts for days until .

The individual predictions were blended using geometric averaging shown in Eq. 4.

| (4) |

By reviewing several predictions by the keras_nas group of models, we noticed an unexpected large peak on the last day of the private set (day ). After confirming this behavior to be dominant in almost all cases, we decided to exclude that group’s prediction for the last day. This is the reasoning for not using keras_nas predictions on the lower branch of Eq 4. In Table 5 we present the weights for each model component as well as the validation WRMSSE score for each validation split.

| lgb_nas | lgb_cos | keras_nas | fastai_cos | Ensemble | |

|---|---|---|---|---|---|

| weights | 3.5 | 1.0 | 1.0 | 0.5 | Eq.4 |

| weight | 3.0 | 0.5 | 0.0 | 1.5 |

| lgb_nas | lgb_cos | keras_nas | fastai_cos | Ensemble | ||||||

| Val. split 1 | 0.474 | 0.470 | 0.715 | 0.687 | 0.531 | |||||

| Val. split 2 | 0.641 | 0.671 | 0.577 | 0.631 | 0.519 | |||||

| Val. split 3 | 0.652 | 0.661 | 0.746 | 0.681 | 0.598 | |||||

| Mean / std | 0.589 | 0.08 | 0.602 | 0.09 | 0.679 | 0.05 | 0.667 | 0.02 | 0.549 | 0.03 |

3.3 Post processing

We tried several post processing smoothing techniques to improve forecasting accuracy. In the final solution we employed a simple exponential smoothing () per product and store id (Level 12 - ) that lead to substantial improvement in both validation sets and the final evaluation (private leaderboard).

We notice that, although this post-processing should be performed for both competition tracks, we were able to only use it for the Uncertainty track as it was a last minute finding (2 hours before competitions closing); as it turned out, had we applied it also for the Accuracy track submissions we would have ended 3 positions higher in the Accuracy track leaderboard.

4 Probabilistic Forecast Methodology

The performance measure selected for this competition track was the Scaled Pinball Loss (SPL) function. The measure is calculated for the 28 days horizon for each series and quantile, as shown in Eq. 5:

| (5) |

where is the actual future value of the examined time series at point , the generated forecast for quantile , the forecasting horizon, is the number of historical observations, and 1 the indicator function (being 1 if Y is within the postulated interval and 0 otherwise). The values were set to , , , , , , , , and , so that they correspond to the requested median, , , , and prediction intervals.

After estimating the SPL for all time series and all the requested quantiles of the competition, the Uncertainty track competition entries were be ranked using the Weighted SPL (WSPL) shown in Eq. 6:

| (6) |

where weights were same described in Section 3.

4.1 Quantile estimation via optimization

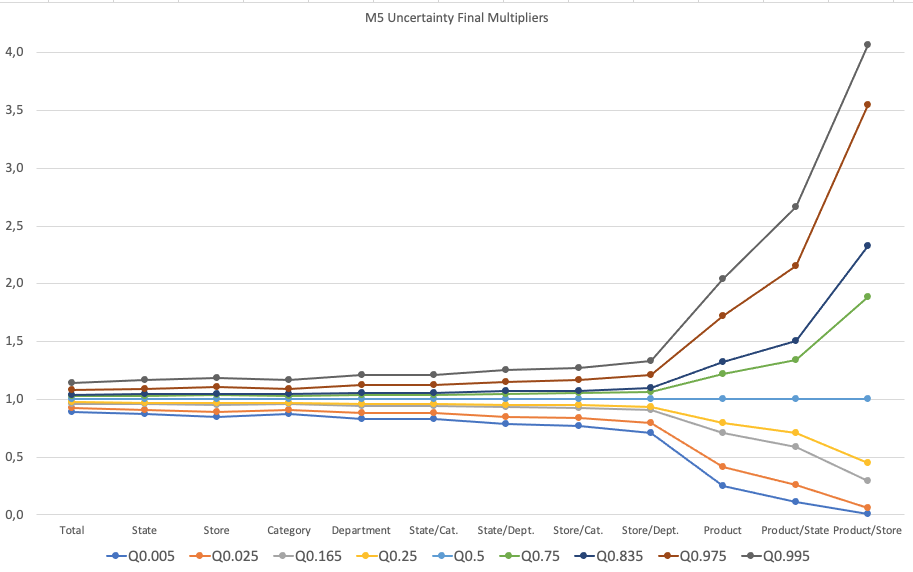

Using our best point forecast as median, we proceed on optimizing WSPL objective function on validation split 1 (last 28 days) and calculate the factors in Table 7. Due to time restrictions of the competition we could not extend our analysis to cover all three validation splits. These factors were used to multiply median solution (quantile ) and produce the remaining upper and lower quantiles. We assumed symmetric distributions on levels 1-9 and skewed distributions on levels 10-12. Furthermore, due to right-skewness of our sales data (zero-bounded on the left) for every level, on last quantile () distributions proposed factor was multiplied by either or . These factors were determined so as to minimize WSPL on validation split 1.

| Level | Aggr | # | 0.005 | 0.025 | 0.165 | 0.25 | 0.5 | 0.75 | 0.835 | 0.975 | 0.995 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | Total | 1 | 0.890 | 0.922 | 0.963 | 0.973 | 1.000 | 1.027 | 1.037 | 1.078 | 1.143 |

| 2 | State | 3 | 0.869 | 0.907 | 0.956 | 0.969 | 1.000 | 1.031 | 1.043 | 1.093 | 1.166 |

| 3 | Store | 10 | 0.848 | 0.893 | 0.950 | 0.964 | 1.000 | 1.036 | 1.049 | 1.107 | 1.186 |

| 4 | Category | 3 | 0.869 | 0.907 | 0.951 | 0.969 | 1.000 | 1.031 | 1.043 | 1.093 | 1.166 |

| 5 | Dept. | 7 | 0.827 | 0.878 | 0.943 | 0.960 | 1.000 | 1.040 | 1.057 | 1.123 | 1.209 |

| 6 | State/Cat. | 9 | 0.827 | 0.878 | 0.943 | 0.960 | 1.000 | 1.040 | 1.057 | 1.123 | 1.209 |

| 7 | State/Dept. | 21 | 0.787 | 0.850 | 0.930 | 0.951 | 1.000 | 1.048 | 1.070 | 1.150 | 1.251 |

| 8 | Store/Cat. | 30 | 0.767 | 0.835 | 0.924 | 0.947 | 1.000 | 1.053 | 1.076 | 1.166 | 1.272 |

| 9 | Store/Dept. | 70 | 0.707 | 0.793 | 0.905 | 0.934 | 1.000 | 1.066 | 1.095 | 1.208 | 1.335 |

| 10 | Product | 3.049 | 0.249 | 0.416 | 0.707 | 0.795 | 1.000 | 1.218 | 1.323 | 1.720 | 2.041 |

| 11 | Product/State | 9.147 | 0.111 | 0.254 | 0.590 | 0.708 | 1.000 | 1.336 | 1.504 | 2.158 | 2.662 |

| 12 | Product/Store | 30.490 | 0.005 | 0.055 | 0.295 | 0.446 | 1.000 | 1.884 | 2.328 | 3.548 | 4.066 |

4.2 Quantile correction via statistical information

Level 12 (the only non-aggregated one) was the most difficult for accurate estimations, and the previously calculated factors could be further improved. Statistical information on past days played a major role for this level. For every product/store id, eight statistical sales quantiles (four intervals excluding median) were calculated over the last days ( year) and over the last days. These quantiles were first averaged and then used to correct the quantile estimation of Section 4.1 for the corresponding level. For the same reason we calculated weekly sales quantiles over the last days and days. The final formula for estimating level quantiles, which led to minimum WSPL score for validation split 1, is given below:

| level 12 | ||||

Level was also corrected in a similar manner and the final formula is given below:

| level 11 | ||||

No corrections were applied for levels other than and , so the respective quantile factors for levels 1-10 remain as shown in Table 7.

The evolution of our submission attempts (SPL score / ranking) for the Uncertainty track of the competition is shown in Fig. 4. This scatter plot highlights:

-

1.

the importance of ensembling diverse models, as our rank increased by almost 90 places only by ensembling,

-

2.

the contribution of statistical correction of levels 11 and 12 that led us to a winning placement.

The overall procedure of ensembling, optimizing, and correcting for the probabilistic forecasting is depicted in Fig. 5.

5 Discussion

We have presented a Machine Learning solution for point and probabilistic forecasting of hierarchical time series that represent daily unit sales of retail products. The methodology involves two state-of-the-art Machine Learning approaches, namely Gradient Boosting Trees and Neural Networks, tuned and combined using carefully selected training and validation sets. The proposed methodology was applied successfully on the recent M5 Competition, yielding a prize position placement in the Uncertainty track.

5.1 Point Forecasting score breakdown

In order to get a deeper insight on the point forecasting task, we broke down the WRMSSE calculation of Eq. 2 on each hierarchical level. The resulting per-level WRMSSE for validation split 1 is shown in Fig. 6. It is obvious that the performance varies significantly among different aggregation levels, with levels , and being the harder to predict. An interesting observation is that, although Level 1 is simply the aggregation of all Level predictions, the Level loss is less than half the magnitude of the Level loss. It would seem that aggregation cancels out the poor predictive capability on Level . This is stressed out even more by the fact that, even though mixture of traditional forecasting techniques (ARIMA, Exponential smoothing) achieved lower error on levels 10, 11, 12, than the one shown in Figure 6, the overall score was really poor.

The mean validation WRMSSE score using the final blend of Eq. 4 is , while our final submission score was - only units apart. This close tracking of the unseen test data error by the validation error is generally sought after by ML practitioners in real world problems, and it serves as an extra indication for the soundness of our methodology.

5.2 Probabilistic Forecasting Factors visualized

In Fig. 7 we present a graphical plot of the factors sorted by increasing level. We notice an unsymmetrical widening of the calculated factors as the number of series of the corresponding level increases. This delta-like shape is correlated to the increasing WRMSSE error on levels 10-12 shown in Fig. 6.

5.3 Takeaways

It is worth mentioning that our point and probabilistic forecasting results are highly correlated since we use the point forecasting as the starting point for our probabilistic analysis. It is expected that, starting from better point forecasts, will result to better probabilistic forecasts as well.

Model diversity and selected training/validation split was crucial for the overall performance and choices eliminated any need for external adjustments on the final prediction in both tracks. This is also highlighted in M5 Competition Summary [1]. After competition ended we found out that by using the magic multiplier we would end up first in Accuracy Track.

5.4 Extensions

The competition data were carefully curated and clean providing a rich variety of potential features. There were also a multitude of ML regression methods that could be tested. However we feel that the most crucial decision was not the selection of features or ML models but the selection of a representative validation sets. Although the three validation splits described in Section 2.2 were enough to stabilize our point forecasting results we believe that using more validation splits could be beneficial and would even eliminate the need of magic external multipliers () to reach the top place.

One obvious extension to the probabilistic forecast methodology was to use a weighted averaged on three validation splits instead of validation split 1 (last 28 days).

References

- Makridakis et al. [2022] S. Makridakis, E. Spiliotis, V. Assimakopoulos, The m5 accuracy competition: Results, findings and conclusions. 2020, URL: https://www. researchgate. net/publication/344487258_The_M5_ Accuracy_competition_Results_findings_and_conclusions (2022).

- Makridakis et al. [2020] S. Makridakis, E. Spiliotis, V. Assimakopoulos, The m4 competition: 100,000 time series and 61 forecasting methods, International Journal of Forecasting 36 (2020) 54–74. URL: https://www.sciencedirect.com/science/article/pii/S0169207019301128. doi:https://doi.org/10.1016/j.ijforecast.2019.04.014, m4 Competition.

- Makridakis et al. [2018] S. Makridakis, E. Spiliotis, V. Assimakopoulos, Statistical and machine learning forecasting methods: Concerns and ways forward, PloS one 13 (2018) e0194889.

- Kim et al. [2015] T. Kim, J. Hong, P. Kang, Box office forecasting using machine learning algorithms based on sns data, International Journal of Forecasting 31 (2015) 364–390.

- Crone et al. [2011] S. F. Crone, M. Hibon, K. Nikolopoulos, Advances in forecasting with neural networks? empirical evidence from the nn3 competition on time series prediction, International Journal of Forecasting 27 (2011) 635–660.

- Hyndman and Athanasopoulos [2018] R. J. Hyndman, G. Athanasopoulos, Forecasting: principles and practice, OTexts, 2018.

- Bishop et al. [1995] C. M. Bishop, et al., Neural networks for pattern recognition, Oxford university press, 1995.

- Friedman [2001] J. H. Friedman, Greedy function approximation: a gradient boosting machine, Annals of statistics (2001) 1189–1232.

- Friedman [2002] J. H. Friedman, Stochastic gradient boosting, Computational Statistics & Data Analysis 38 (2002) 367–378.

- Potdar et al. [2017] K. Potdar, T. S. Pardawala, C. D. Pai, A comparative study of categorical variable encoding techniques for neural network classifiers, International journal of computer applications 175 (2017) 7–9.

- Al-Rfou et al. [2013] R. Al-Rfou, B. Perozzi, S. Skiena, Polyglot: Distributed word representations for multilingual nlp, arXiv preprint arXiv:1307.1662 (2013).

- Akbik et al. [2019] A. Akbik, T. Bergmann, D. Blythe, K. Rasul, S. Schweter, R. Vollgraf, Flair: An easy-to-use framework for state-of-the-art nlp, in: Proceedings of the 2019 Conference of the North American Chapter of the Association for Computational Linguistics (Demonstrations), 2019, pp. 54–59.

- Chollet et al. [2018] F. Chollet, et al., Deep learning with Python, volume 361, Manning New York, 2018.

- Bengio and Grandvalet [2004] Y. Bengio, Y. Grandvalet, No unbiased estimator of the variance of k-fold cross-validation, Journal of machine learning research 5 (2004) 1089–1105.

- Taieb et al. [2012] S. B. Taieb, R. J. Hyndman, et al., Recursive and direct multi-step forecasting: the best of both worlds, volume 19, Citeseer, 2012.

- Hyndman and Koehler [2006] R. J. Hyndman, A. B. Koehler, Another look at measures of forecast accuracy, International Journal of Forecasting 22 (2006) 679–688.

- Ke et al. [2017] G. Ke, Q. Meng, T. Finley, T. Wang, W. Chen, W. Ma, Q. Ye, T.-Y. Liu, Lightgbm: A highly efficient gradient boosting decision tree, in: Advances in Neural Information Processing Systems, 2017, pp. 3146–3154.

- Ye et al. [2009] J. Ye, J.-H. Chow, J. Chen, Z. Zheng, Stochastic gradient boosted distributed decision trees, in: Proceedings of the 18th ACM Conference on Information and Knowledge Management, 2009, pp. 2061–2064.

- Tweedie et al. [1957] M. C. Tweedie, et al., Statistical properties of inverse gaussian distributions. i, Annals of Mathematical Statistics 28 (1957) 362–377.

- Zhou et al. [2020] H. Zhou, W. Qian, Y. Yang, Tweedie gradient boosting for extremely unbalanced zero-inflated data, Communications in Statistics-Simulation and Computation (2020) 1–23.

- Abadi et al. [2016] M. Abadi, P. Barham, J. Chen, Z. Chen, A. Davis, J. Dean, M. Devin, S. Ghemawat, G. Irving, M. Isard, et al., Tensorflow: A system for large-scale machine learning, in: 12th USENIX symposium on operating systems design and implementation (OSDI 16), 2016, pp. 265–283.

- Howard and Gugger [2020] J. Howard, S. Gugger, Fastai: A layered api for deep learning, Information 11 (2020) 108.

- Paszke et al. [2019] A. Paszke, S. Gross, F. Massa, A. Lerer, J. Bradbury, G. Chanan, T. Killeen, Z. Lin, N. Gimelshein, L. Antiga, et al., Pytorch: An imperative style, high-performance deep learning library, arXiv preprint arXiv:1912.01703 (2019).

- Hyndman et al. [2014] R. J. Hyndman, G. Athanasopoulos, et al., Optimally reconciling forecasts in a hierarchy, Foresight: The International Journal of Applied Forecasting (2014) 42–48.

Appendix A Complete feature list

| feature category | feature name | type | meaning | lightGBM | keras | fastai |

|---|---|---|---|---|---|---|

| non trainable features | id | cat | 30490 unique ids that correspond to combination of item_id/store_id | |||

| d | integer | the increasing number of days 1-1941 | ||||

| id based categorical features | item_id | cat | 3049 distinct item ids | * | * | |

| dept_id | cat | 7 distinct departments | * | * | * | |

| cat_id | cat | 3 product categories | * | * | * | |

| store_id | cat | 10 different stores | * | * | * | |

| state_id | cat | 3 different states | * | |||

| price related features | release | integer | week when the first price was set of the product | * | * | |

| sell_price | float | current price of the product | * | * | * | |

| sell_price_rel_diff | float | relative difference between two consecutive price changes | * | |||

| price_max | float | maximum price this product ever reached | * | * | ||

| price_min | float | minimum price this product ever reached | * | * | ||

| price_std | float | standard deviation of the historical prices of the product | * | * | ||

| price_mean | float | average value of the historical prices of the product | * | * | ||

| price_norm | float | normalized price (price/price_max) for the day [0 1] | * | * | ||

| price_nunique | integer | number of unique prices for this product | * | * | ||

| item_nunique | integer | number of unique products that reached the same price in a specific store. | * | * | ||

| price_momentum | float | ratio of the previous to the current price of the product | * | * | ||

| price_momentum_m | float | mean price of the product the last month | * | * | ||

| price_momentum_y | float | mean price of the product the last year | * | * | ||

| calendar related features | event_name_1 | cat | If the date includes an event the name of this event | * | * | |

| event_type_1 | cat | If the date includes an event the type of this event | * | * | * | |

| event_name_2 | cat | If the date includes a second event the name of this event | * | * | * | |

| event_type_2 | cat | If the date includes a second event the type of this event. | * | * | * | |

| snap_CA | binary | SNAP activities that serve as promotions in California on a specific date. | * | * | * | |

| snap_TX | binary | SNAP activities that serve as promotions in Texas on a specific date. | * | * | ||

| snap_WI | binary | SNAP activities that serve as promotions in Wiskonskin on a specific date. | * | * | ||

| log_d | float | where the increasing number of days | * | |||

| tm_d | integer | day of the month for a specific date | * | * | ||

| tm_w | integer | week of the year for a specific date | * | * | ||

| tm_m | integer | month of a year for a specific date | * | * | ||

| tm_y | integer | year of the specific date (5 years total) | * | * | ||

| tm_wm | integer | number of week within a month | * | * | ||

| tm_dw | integer | number of the day within a week | * | * | * | |

| tm_w_end | binary | is weekend or not | * | |||

| target encoding features | enc_cat_id_mean | float | average value of sales for each category id | * | ||

| enc_cat_id_std | float | std value of sales for each category id | * | |||

| enc_dept_id_mean | float | average value of sales for each department id | * | |||

| enc_dept_id_std | float | std value of sales for each department id | * | |||

| enc_item_id_mean | float | average value of sales for each item id | * | |||

| enc_item_id_std | float | std value of sales for each department ids | * | |||

| enc_item_id_state_id_mean | float | average value of sales for each combination of item id and state id | * | |||

| enc_item_id_state_id_std | float | std value of sales for each combination of item id and state id | * | |||

| enc_state_id_dept_id_mean | float | average value of sales for each combination of item id and department id | * | * | ||

| enc_state_id_dept_id_std | float | std value of sales for each combination of item id and department id | * | * | ||

| enc_state_id_cat_id_mean | float | average value of sales for each combination of item id and category id | * | |||

| enc_state_id_cat_id_std | float | std value of sales for each combination of item id and category id | * | |||

| lag features | sales_lag_28 | integer | the sales value for each id and each date 28 29 30 … 42 days ago (span 2 weeks) | * | * | * |

| sales_lag_29 | integer | |||||

| sales_lag_30 | integer | * | * | |||

| sales_lag_31 | integer | * | * | |||

| sales_lag_32 | integer | * | * | |||

| sales_lag_33 | integer | * | * | |||

| sales_lag_34 | integer | * | * | |||

| sales_lag_35 | integer | * | * | |||

| sales_lag_36 | integer | * | * | |||

| sales_lag_37 | integer | * | * | |||

| sales_lag_38 | integer | * | * | |||

| sales_lag_39 | integer | * | * | |||

| sales_lag_40 | integer | * | * | |||

| sales_lag_41 | integer | * | * | |||

| sales_lag_42 | integer | * | * | |||

| rolling statistics 28 days ago | rolling_mean_7 | float | rolling means and averages for the sales of a specific product that end 28 days prior current date | * | * | * |

| rolling_median_7 | float | * | ||||

| rolling_std_7 | float | * | * | |||

| rolling_mean_14 | float | * | * | |||

| rolling_std_14 | float | * | * | |||

| rolling_mean_30 | float | * | * | * | ||

| rolling_median_30 | float | * | ||||

| rolling_std_30 | float | * | * | |||

| rolling_mean_60 | float | * | * | |||

| rolling_std_60 | float | * | * | |||

| rolling_mean_180 | float | * | * | |||

| rolling_std_180 | float | * | * | |||

| rolling means within the 28 day window | rolling_mean_tmp_1_7 | float | rolling means and averages for the sales of a specific product within 28 days prior current date. While we can train our models with these features we need to be extra careful when predicting 28 days ahead because these features need to be calculated recursively. | * | ||

| rolling_mean_tmp_1_14 | float | * | * | |||

| rolling_mean_tmp_1_30 | float | * | * | |||

| rolling_mean_tmp_1_60 | float | * | * | |||

| rolling_mean_tmp_7_7 | float | * | * | |||

| rolling_mean_tmp_7_14 | float | * | * | |||

| rolling_mean_tmp_7_30 | float | * | * | |||

| rolling_mean_tmp_7_60 | float | * | * | |||

| rolling_mean_tmp_14_7 | float | * | * | |||

| rolling_mean_tmp_14_14 | float | * | * | |||

| rolling_mean_tmp_14_30 | float | * | * | |||

| rolling_mean_tmp_14_60] | float | * | * |