Optimising Distributions with Natural Gradient Surrogates

Jonathan So Richard E. Turner

University of Cambridge University of Cambridge

Abstract

Natural gradient methods have been used to optimise the parameters of probability distributions in a variety of settings, often resulting in fast-converging procedures. Unfortunately, for many distributions of interest, computing the natural gradient has a number of challenges. In this work we propose a novel technique for tackling such issues, which involves reframing the optimisation as one with respect to the parameters of a surrogate distribution, for which computing the natural gradient is easy. We give several examples of existing methods that can be interpreted as applying this technique, and propose a new method for applying it to a wide variety of problems. Our method expands the set of distributions that can be efficiently targeted with natural gradients. Furthermore, it is fast, easy to understand, simple to implement using standard autodiff software, and does not require lengthy model-specific derivations. We demonstrate our method on maximum likelihood estimation and variational inference tasks.

1 INTRODUCTION

Many problems in scientific research require the optimisation of probability distribution parameters. Such problems are of fundamental importance in the fields of machine learning and statistics. The goal of these optimisations is to minimise a function where is the parameter vector of a probability distribution . Notable examples include maximum likelihood estimation (MLE) and variational inference (VI).

When is differentiable, the archetypal optimisation method is gradient descent (GD). GD takes steps in the direction in parameter space that gives the greatest decrease in for an infinitesimally small step size, which is equivalent to following the direction of the negative gradient. While GD has many desirable properties, convergence can often be slow, and much effort has been spent in designing methods that offer improved convergence properties.

Natural gradient descent (NGD) is one such method for optimising probability distribution parameters (Amari, 1998). In contrast with GD, NGD moves the parameters in the direction of steepest descent on a manifold of probability distributions, where steepness is defined with respect to a divergence measure between distributions. This notion of steepness is intrinsic to the manifold, and so it is not dependent on parameterisation, dispensing with a well-known pathology of GD.

There are some distributions for which the natural gradient can be computed efficiently. However, in its most general form, computing the natural gradient involves instantiating and inverting the Fisher information matrix, defined as

| (1) |

posing several challenges.111We use, e.g. , to refer to both a distribution and its density function, with the intention made clear from context. We will use a subscript, e.g. , when we wish to make the dependence on parameters explicit. Our gradient notation is explained in Appendix A. First, for some distributions, the Fisher can become singular, in which case the natural gradient is undefined. Second, it may not be available in closed form, in which case it must be estimated using sampling or other numerical methods. Finally, instantiating and inverting it explicitly costs in memory and in computation, for the number of parameters. For even moderately large , this can be prohibitively expensive.

In this paper we propose a simple technique for tackling optimisation problems in which computing the natural gradient is problematic. Namely, we reframe the problem as an optimisation with respect to a surrogate distribution , for which computing natural gradients is easy, and perform the optimisation in that space. With a judiciously chosen surrogate, convergence can be rapid.

We find that a number of existing methods can be interpreted as applications of this technique: the natural gradient VI method of Lin et al. (2019) for exponential family mixtures, stochastic natural gradient expectation propagation (Hasenclever et al., 2017), a fixed-point iteration scheme for optimising elliptical copulas (Hernández et al., 2014), as well as the typical use of natural gradients in large-scale supervised learning settings. We also describe a new method for applying the technique to a wide variety of problems, using exponential family (EF) surrogate distributions. Our method is easy to understand, simple to implement using standard autodiff software, and does not require the use of lengthy model-specific derivations.

We present a number of experiments in which we find that our method typically either matches or outperforms the convergence speed of existing best-practice methods, both in number of iterations and wall-clock time. Our experiments consist of a variety of MLE and VI tasks, but we note that the method is applicable more generally to optimisations involving probability distributions, or indeed to any optimisation in which we think a manifold of probability distributions may serve as a useful surrogate for the solution space.

Our main contributions can be summarised as follows:

-

1.

We propose a novel technique for optimising probability distribution parameters.

-

2.

We prove the validity of this technique under stated conditions.

-

3.

We find several examples of existing methods that can be viewed as applying this technique.

-

4.

We describe a simple new method for applying it, using known properties of EF distributions.

-

5.

We present a variety of MLE and VI experiments in which our method significantly outperforms existing best-practice methods.

This paper is structured as follows. In Section 2 we provide a brief overview of NGD and EF distributions. Section 3 covers items 1 and 4 of the contributions above, as well as an overview of item 2 (details found in Appendix B). Sections 4 and 5 cover items 5 and 3 respectively. Finally, in Section 6, we discuss limitations of our method, and avenues for future research.

2 BACKGROUND

In this section we begin with an overview of NGD. We then briefly describe a class of distribution families for which we can efficiently compute natural gradients, namely exponential families. NGD and EF distributions will serve as the foundation for the method we introduce in Section 3.

2.1 Natural Gradient Descent

NGD updates the parameters of a distribution by taking a step proportional to the gradient of the objective , preconditioned by the inverse of the Fisher matrix of . That is, the update in parameters at step of the optimisation is given by

| (2) |

where is given by (1). The step size may follow some pre-defined schedule, or be found by line search. It can be shown that as , update (2) moves in the direction of steepest descent in , on the manifold of probability distributions spanned by , where steepness is defined with respect to a divergence measure between distributions (Ollivier et al., 2017). Because this notion of steepness is intrinsic to the manifold, NGD is locally invariant to parameterisation.

When NGD is applied to MLE objectives, it is Fisher-efficient (Amari, 1998), and can be seen as a robust approximation to Newton’s method (Martens and Grosse, 2015). These properties do not, in general, apply outside of this setting. Nevertheless, natural gradient methods have been applied in several other settings, often resulting in rapidly converging procedures (Kakade, 2001, Hoffman et al., 2013, Khan et al., 2017, Hasenclever et al., 2017).

2.2 Exponential Family Distributions

In this section we provide a brief introduction to EF distributions, whose properties support efficient natural gradient computation.

The EF of distributions defined by the vector-valued statistic function and base measure , has density

| (3) |

where is the log partition function, and are the natural parameters. When the components of are linearly independent, the family is said to be minimal.

There is an alternative parameterisation of , given by

| (4) |

where are known as the the mean parameters of . In minimal families the correspondence between and is one-to-one, and we denote the reverse map as .222Due to our overloaded use of , to denote both parameters and the map between them, we will use e.g. to disambiguate the latter if it is not clear from context. In this paper we will only consider minimal EFs.

Notable examples of EF distributions include the multivariate normal, gamma, categorical, and Dirichlet distributions to name but a few.

Let , be functions related by . It is a remarkable property of EFs that the natural gradients of , with respect to , respectively are given by

| (5) | ||||

| (6) |

That is, the natural gradient in one parameterisation is simply given by the regular gradient with respect to the other (Hensman et al., 2012). Provided that we have an efficient way of converting between natural and mean parameters, this allows us to compute the natural gradient without explicitly instantiating or inverting .

3 METHOD

The exponential families introduced in Section 2 provide us with a relatively rich set of distributions for which we can efficiently compute natural gradients. However, there are many distributions outside of this set for which computing natural gradients remains difficult. In this section, we present details of our technique, which expands the set of distributions that we can efficiently target with natural gradients.

3.1 Surrogate Natural Gradient Descent

The main idea in this paper is simple. When faced with an optimisation objective , where are the parameters of a distribution for which computing the natural gradient update is problematic, we solve the problem in two steps. First, we re-parameterise as a function of some other parameters , related by , and define the reparameterised objective

| (7) |

Second, we interpret as the parameters of a surrogate distribution , for which computing natural gradients is easy, and then perform NGD in with respect to and . That is, we perform a sequence of updates

| (8) |

where is the Fisher information matrix of . We refer to and as the target and surrogate distributions respectively. Update (8) has the straightforward interpretation of performing preconditioned GD in a reparameterised objective. Upon converging to a local minimiser of , a solution to the original problem is obtained by . We call this technique surrogate natural gradient descent (SNGD).

As a simple example, when is a multivariate Student’s distribution with parameters and known degrees of freedom , we may choose to be multivariate normal, with mean and covariance parameters . may then simply be chosen as the identity map, although alternatives are possible.333For example, we could instead equate with the variance of , which is a function of both and .

It is natural to question which properties SNGD shares with NGD under . Given that SNGD is NGD (with respect to ), it remains locally invariant to parameterisation, and performs steepest descent in a statistical manifold (that of ). What is not guaranteed, is that the statistical manifold of remains useful for the optimisation of . For example, in MLE settings, SNGD will not in general retain the asymptotic efficiency of NGD under . However, what it gains is tractability, and as we demonstrate in Section 4, the practical performance benefits can be significant. In some cases, remarkably, SNGD can actually outperform NGD under , with respect to both the original parameters , and the reparameterisation defined by .

The performance of SNGD relies crucially on appropriate choices for and . It is tempting to assume that should be an approximation to . However, as Table 1 shows, for most of the examples in this paper, and do not even have support over the same space. We defer a discussion of surrogate choice until Appendix H, with priority given here to providing examples.

3.2 Equivalence with Optimisation of

In Appendix B we prove a number of results regarding the validity of SNGD, which we summarise here.

Let , be open subsets of , respectively, with . Let be twice differentiable, with Jacobian of rank everywhere, and with . Finally, let be twice continuously differentiable, and define .

Under these conditions, optimising is equivalent to optimising in the following sense: finding a local minimiser of also gives us a local minimiser for , and all local minima of are attainable through . Furthermore, does not have any non-strict saddle points that are not also present at the corresponding points in , meaning that does not introduce any spurious attractors for GD-based methods, including NGD (Lee et al., 2016).

3.3 Exponential Familly Surrogates

In this paper we choose from the set of EF distributions described in Section 2, allowing us to perform update (8) efficiently without explicitly instantiating or inverting . Algorithm 1 provides pseudocode for an implementation of SNGD when is either the mean or natural domain of an EF. It assumes the existence of an autodiff operator grad, and an overloaded function dualparams, which maps from natural to mean parameters, or vice-versa, depending on the type of its argument. A full explanation of Algorithm 1 can be found in Appendix C.

3.4 Extension: Auxiliary Parameters

In some cases, a chosen surrogate’s parameters, , may not be sufficient to fully specify . To handle such cases, we can generalise SNGD by augmenting with an additional vector of parameters, , that are not optimised with natural gradients. Our reparameterised objective is then given by

| (9) |

We optimise (9) by updating using natural gradients as before, and using standard gradient-based techniques, either jointly or in alternation. For example, we can apply the sequence of updates

| (10) | ||||

| (11) |

where , are the step sizes for , , respectively at time . Update (11) corresponds to GD in , but we may equally use any other first-order optimiser.

Revisiting our example from Section 3.1, if is a multivariate Student’s distribution, but now with unknown degrees of freedom , its parameter vector is then . Again, we can choose to be multivariate normal with parameters . has no analogue in the multivariate normal distribution however, and so we capture this with .

4 RESULTS

| TARGET | SURROGATE | |||

|---|---|---|---|---|

| DISTRIBUTION | SUPPORT | DISTRIBUTION | SUPPORT | SECTION |

| Negative binomial | Gamma | 4.1 | ||

| Negative binomial mixture | Gamma mixture model | 4.4 | ||

| Skew-normal | Normal | 4.2 | ||

| Skew-normal mixture | Normal mixture model | 4.4 | ||

| Skew- | Normal | 4.2 | ||

| Elliptical copula | Zero-mean normal | 4.3 | ||

In this section we present a number of experiments demonstrating the utility of SNGD. Natural gradient methods have been used in a variety of settings, but perhaps most extensively for MLE (Amari, 1998, Bernacchia et al., 2018, Martens and Grosse, 2015, Ren and Goldfarb, 2019, Roux et al., 2007) and VI (Hoffman et al., 2013, Khan and Lin, 2017, Khan et al., 2017, 2018, Lin et al., 2019, Salimbeni et al., 2018). We therefore used a variety of MLE and VI tasks as test cases.

In MLE the goal is to find parameters of distribution that maximise the (log) likelihood of observed data under . That is, the objective function for MLE tasks is of the form

| (12) |

In VI we are given a generative model , and observed data , and the goal is to find parameters of distribution that minimise the Kullback-Leibler (KL) divergence from to the posterior .444The KL divergence is defined in Appendix H. The objective function for VI tasks is of the form

| (13) |

It can be shown that minimising (13) is equivalent to maximising a lower bound on the log marginal likelihood: . In the VI experiments of this section, gradients of (13) were estimated using the reparamererisation trick (Kingma and Welling, 2014).

In each experiment, we compared SNGD with a number of baselines. For tasks that were small scale, and had objectives that could be computed deterministically, we compared SNGD with two baselines: GD and BFGS (Nocedal and Wright, 2006). In these cases, we used exact line search to determine step sizes for each method, in order to compare search direction independent of hyperparameter settings. For larger tasks, or where only stochastic estimates of were available (minibatched or VI experiments), we used Adam as the standard baseline, and used grid search to determine the best hyperparameters for each method.

Further details of all experiments are given in Appendix E. A summary of surrogate-target pairs used for SNGD in these experiments can be found in Table 1, and details of parameter mappings can be found in Appendix F.

We display average training curves for each experiment, with error bars corresponding to 2 standard errors, computed across 10 random seeds. In Appendix G we plot Pareto frontiers, showing the best performance achieved by any hyperparameter setting, as a function of both iteration count and wall-clock time.

In this section we use to denote the number of training data points, and for the dimensionality of the random variable under . For brevity, we omit the conventional multivariate prefix from distribution names in this section, as this is implicit for .

4.1 Negative Binomial Distribution

The negative binomial distribution is widely used for modelling discrete data (Fisher, 1941, Lloyd-Smith et al., 2005, Lloyd-Smith, 2007, Orooji et al., 2021, Kendall et al., 2023). Maximum likelihood estimates of the negative binomial parameters are not available in closed form, and must be found numerically.

Let be the parameters of the negative binomial distribution with probability mass function

| (14) |

The gamma distribution can be seen as a continuous analogue of the negative binomial, and as it is a EF, it is a natural choice of surrogate when targeting the negative binomial with SNGD.

Let , therefore, be the gamma distribution with parameters , and probability density function

| (15) |

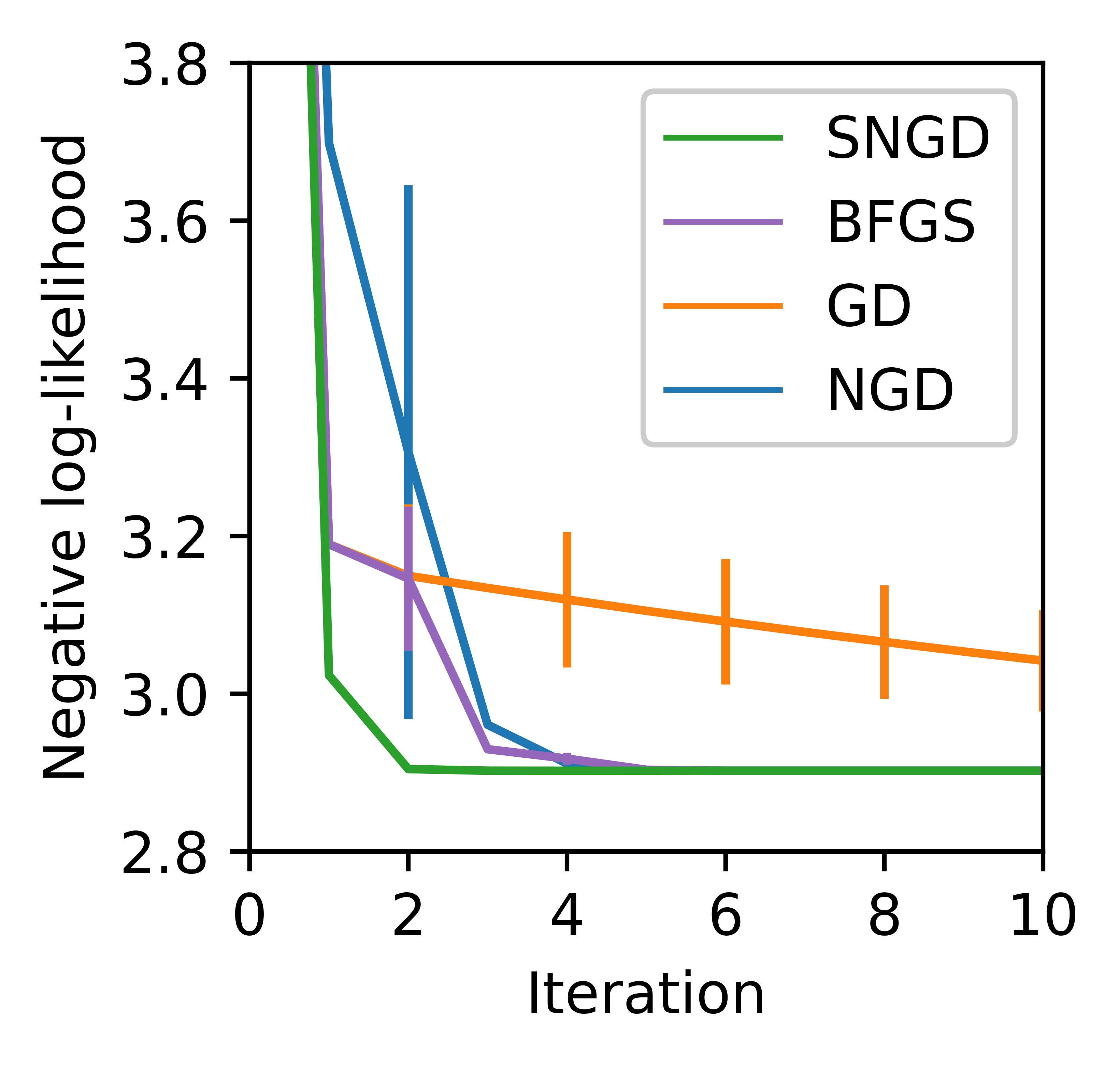

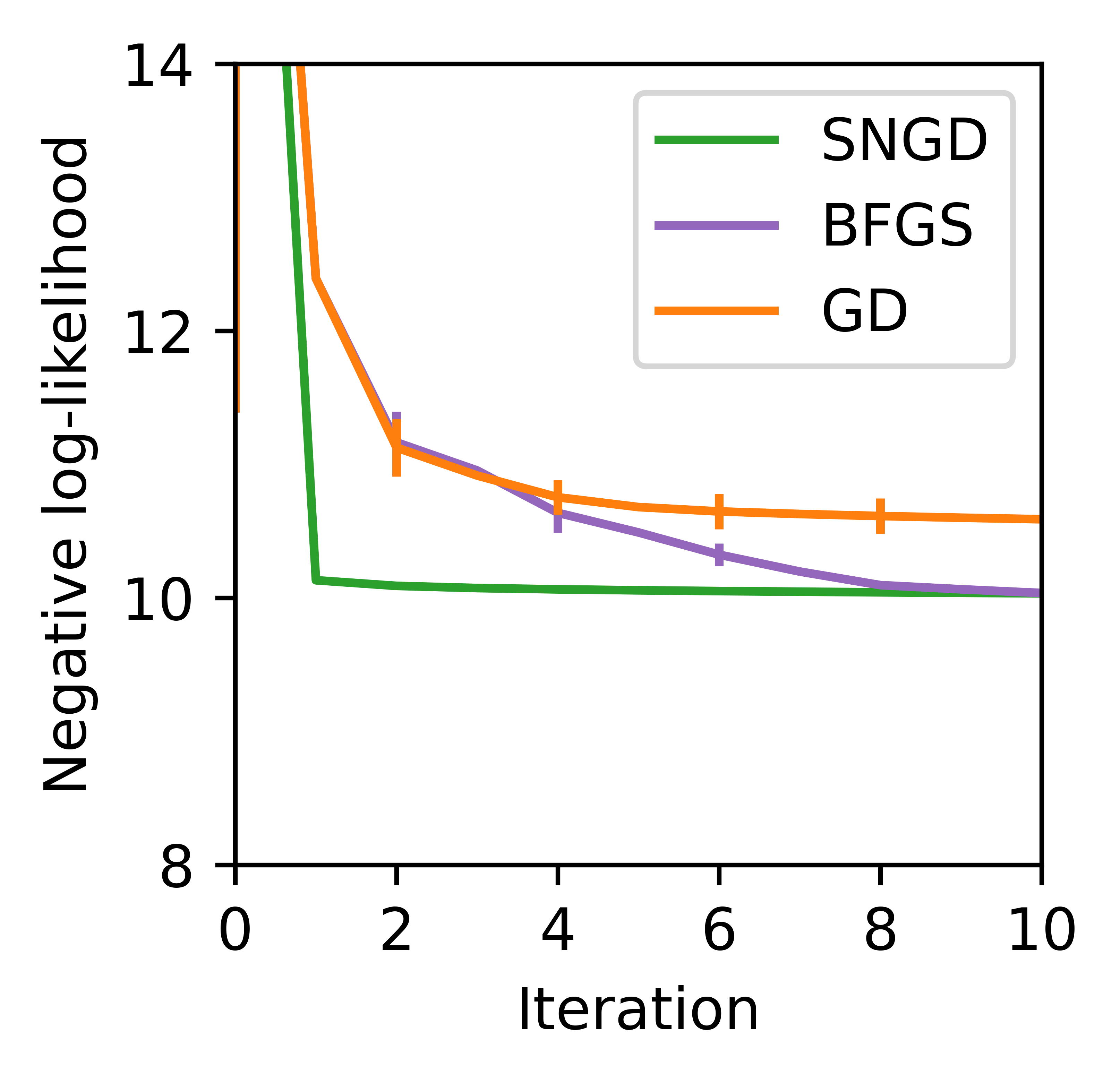

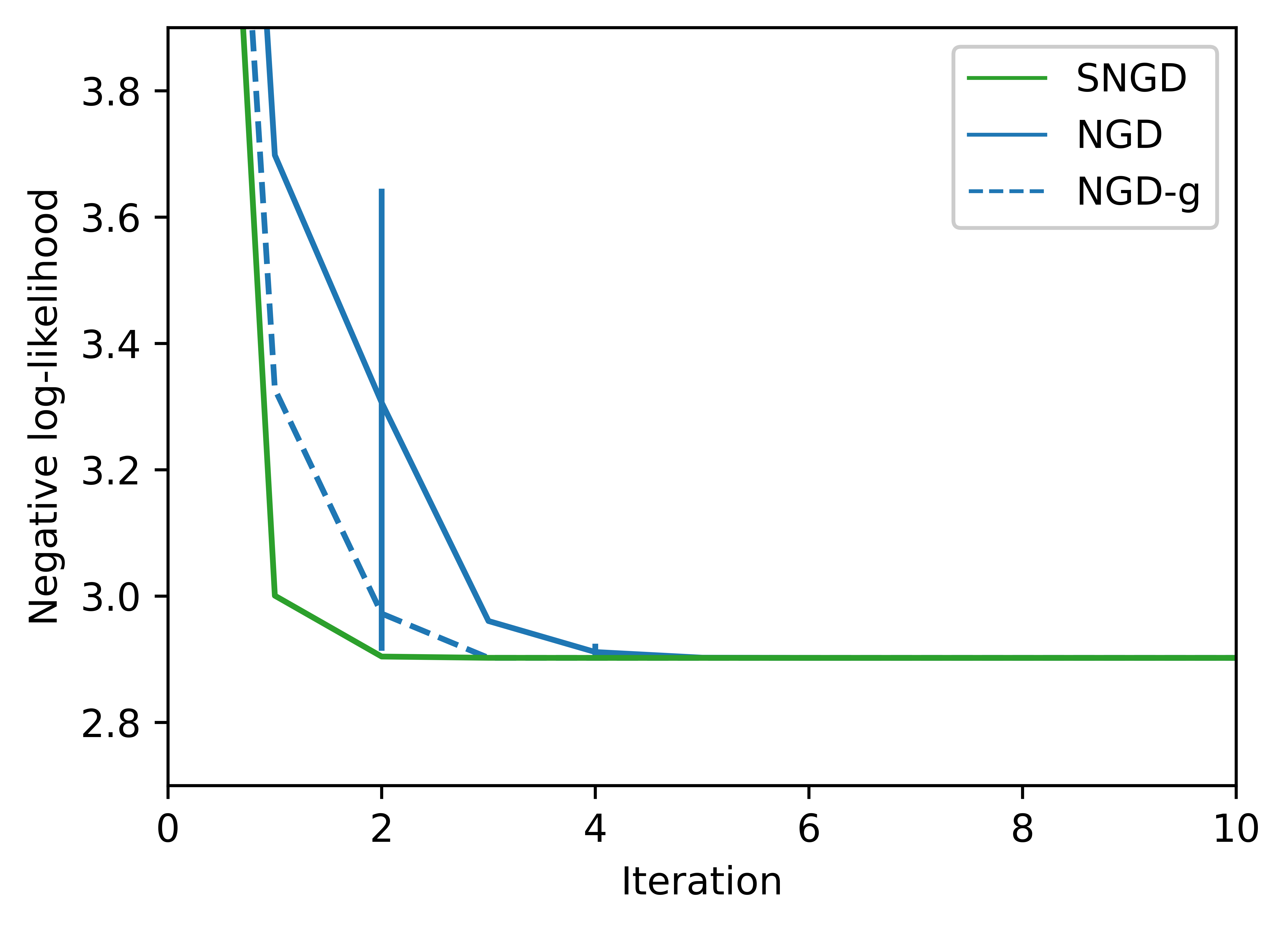

Guenther (1972) used the gamma distribution to approximate the CDF of the negative binomial, using the mapping . Let be the equivalent mapping, but defined in terms of mean parameters of . Finally, let be defined as (12), where is the dataset of Fisher (1941), consisting of counts of ticks observed on a population of sheep (=82, =1).

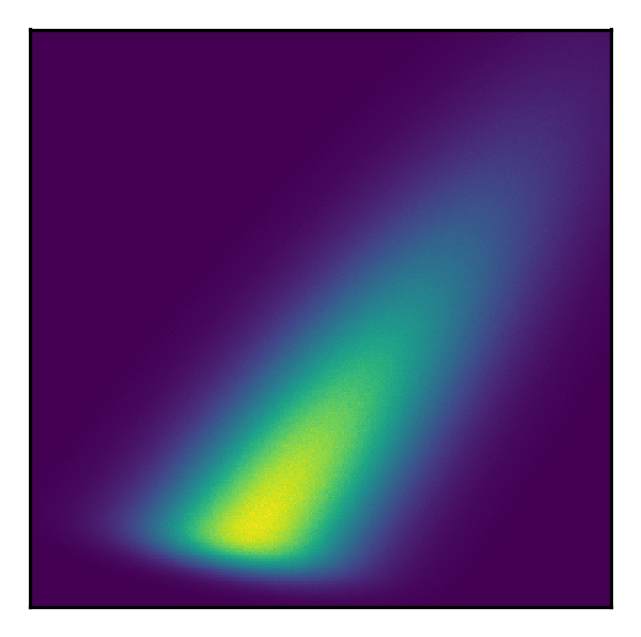

Using these definitions, we applied Algorithm 1, modified to use a line search as discussed at the start of this section. We compared SNGD with our standard baselines: GD and BFGS. Additionally, this task was sufficiently small that we were able to compare with NGD under .

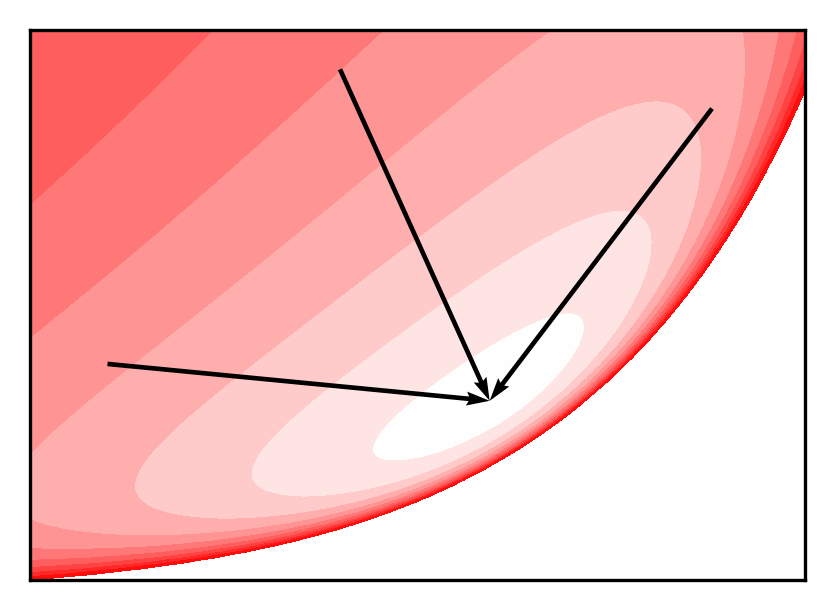

Figure 1 shows that SNGD outperformed all of the baselines. Remarkably, this included NGD under ; this surprising result is explored in detail in Appendix I. There, we show that this was true even when NGD was performed with respect to the reparameterisation defined by , implying that this is not simply an artefact of SNGD using a more effective parameterisation; rather, it is the change of parameterisation and distribution that results in such rapid convergence.

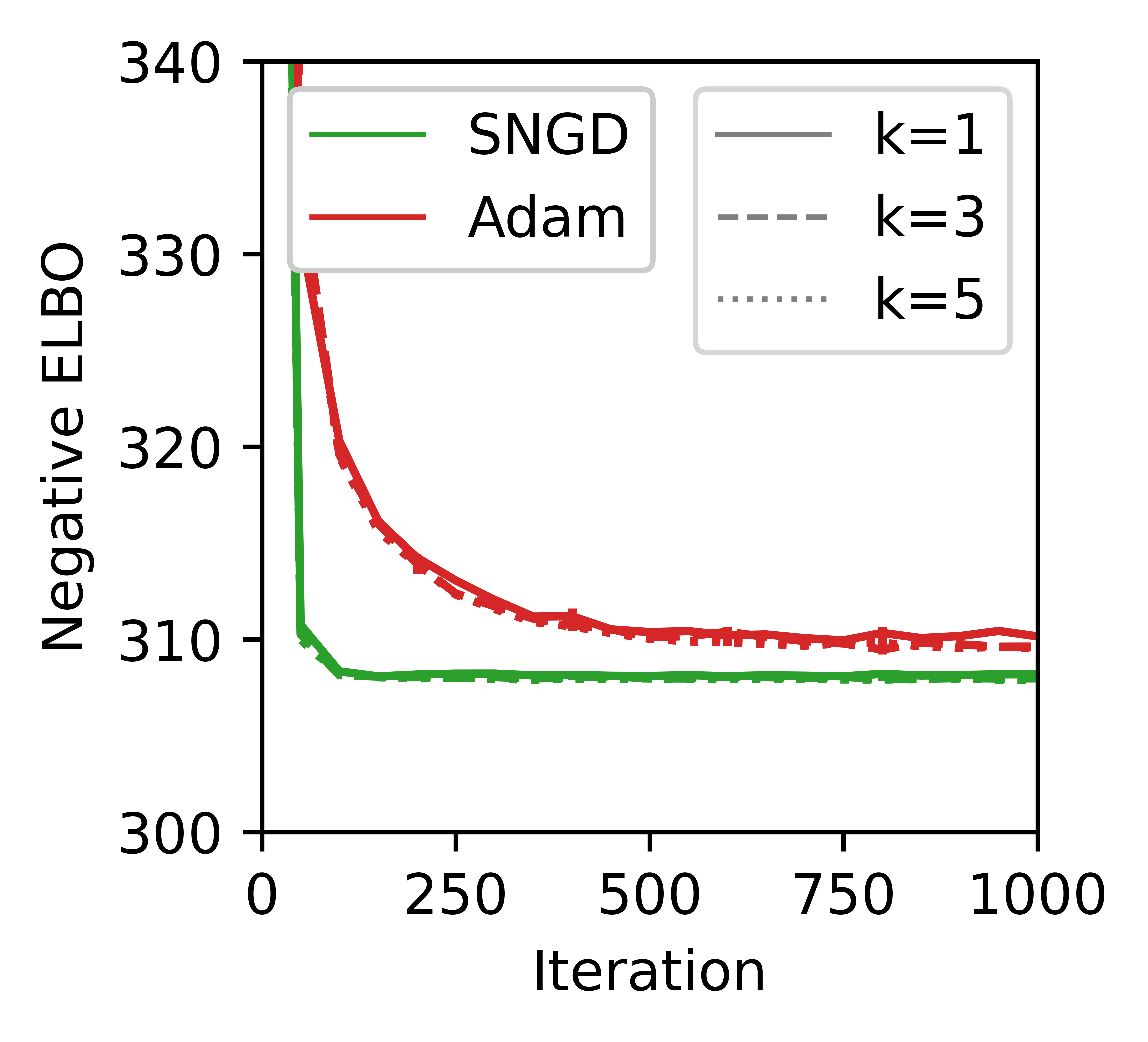

4.2 Skew-Elliptical Distributions

The skew-elliptical distributions are a flexible family of unimodal multivariate distributions, allowing for features such as asymmetry and heavy tails (Azzalini, 2013). In this section we consider in particular the skew-normal and skew- distributions. The skew-normal can be viewed as an asymmetric generalisation of the normal distribution. Similarly, the skew- can be viewed as an asymmetric generalisation of the Student’s distribution.

The normal distribution is a natural surrogate for these distributions. We used it as such in a number of experiments, mapping its mean and covariance to parameters playing similar roles in the target distributions, with any other parameters captured by as outlined in Section 3.4.

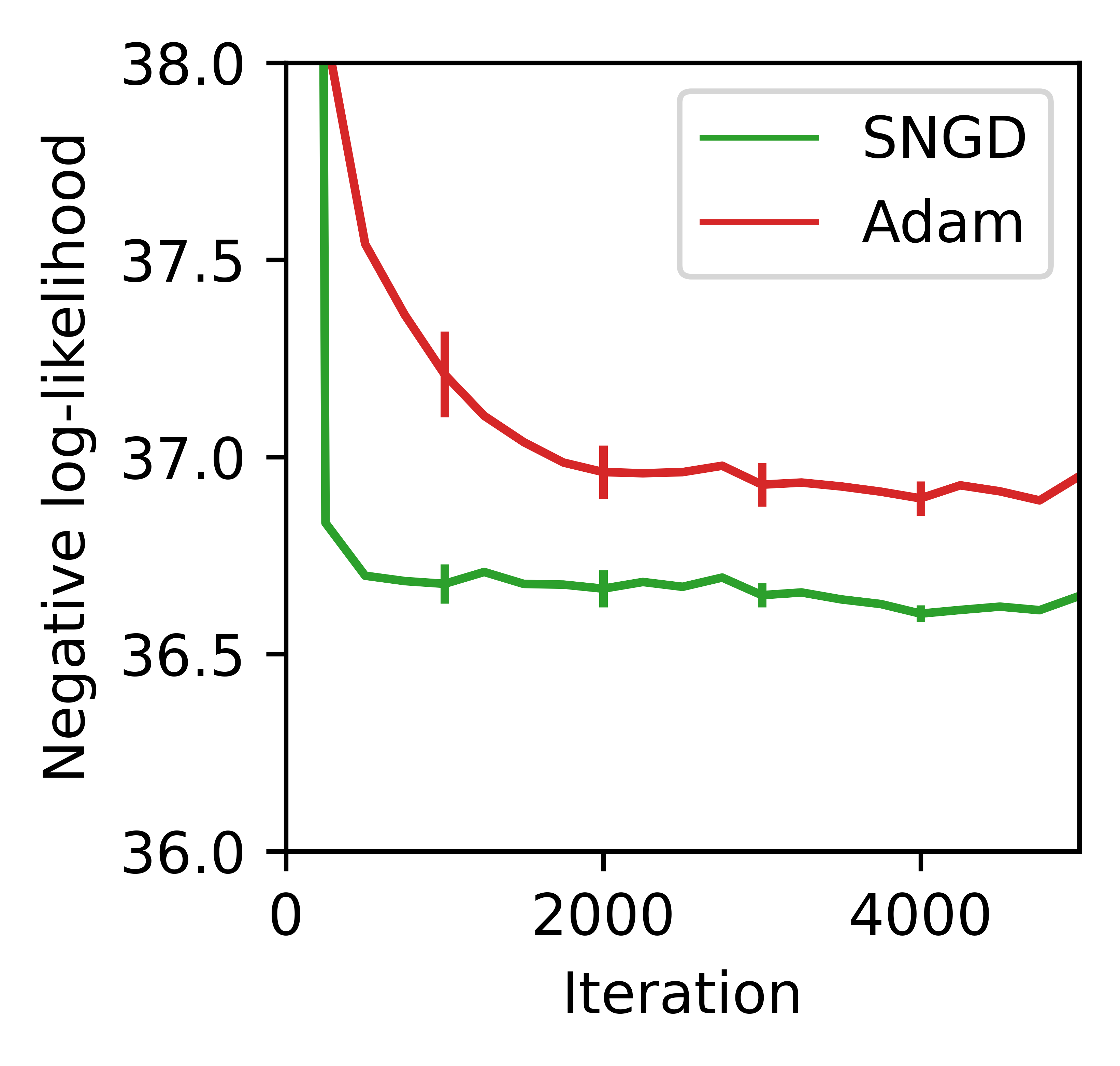

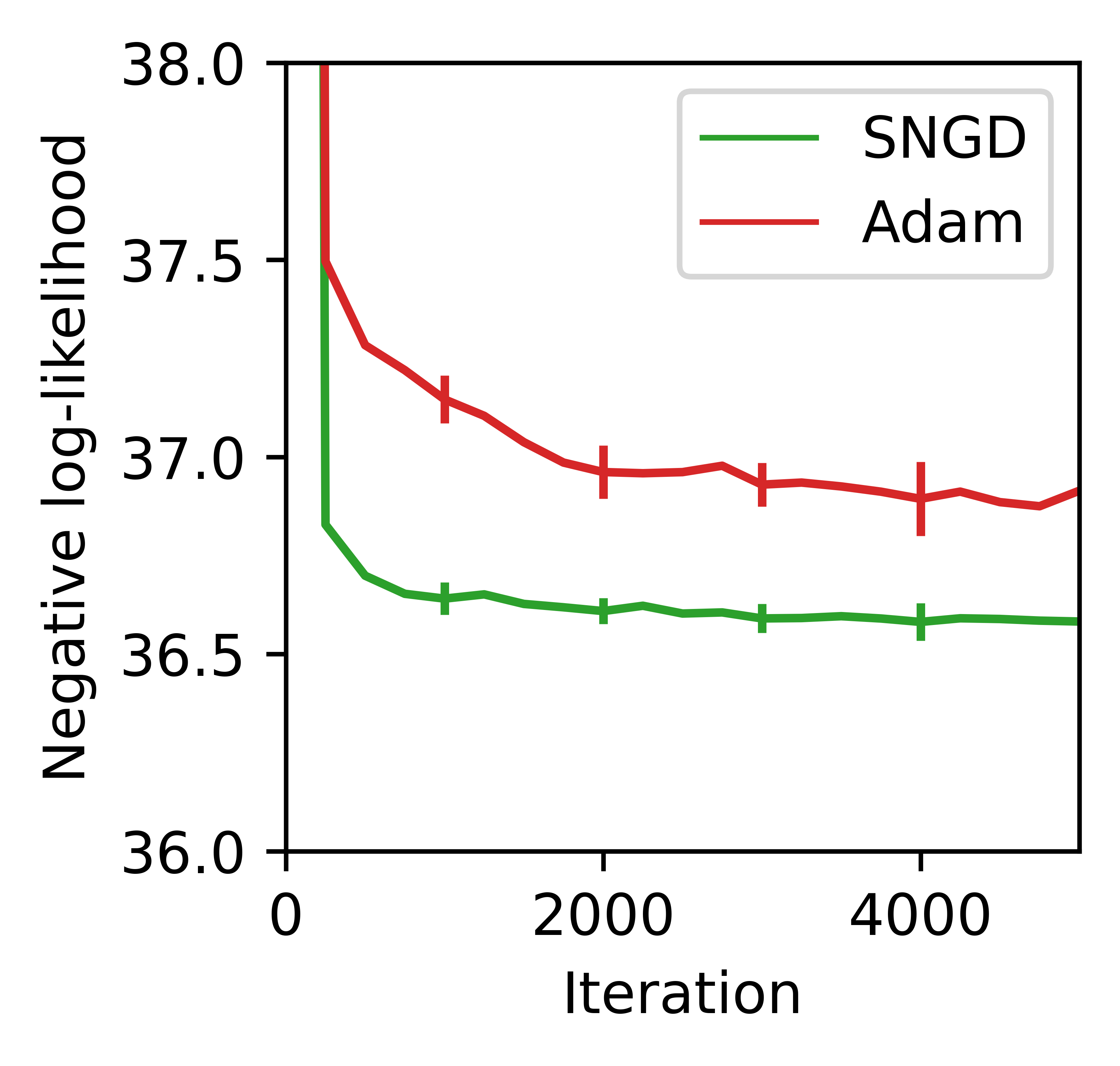

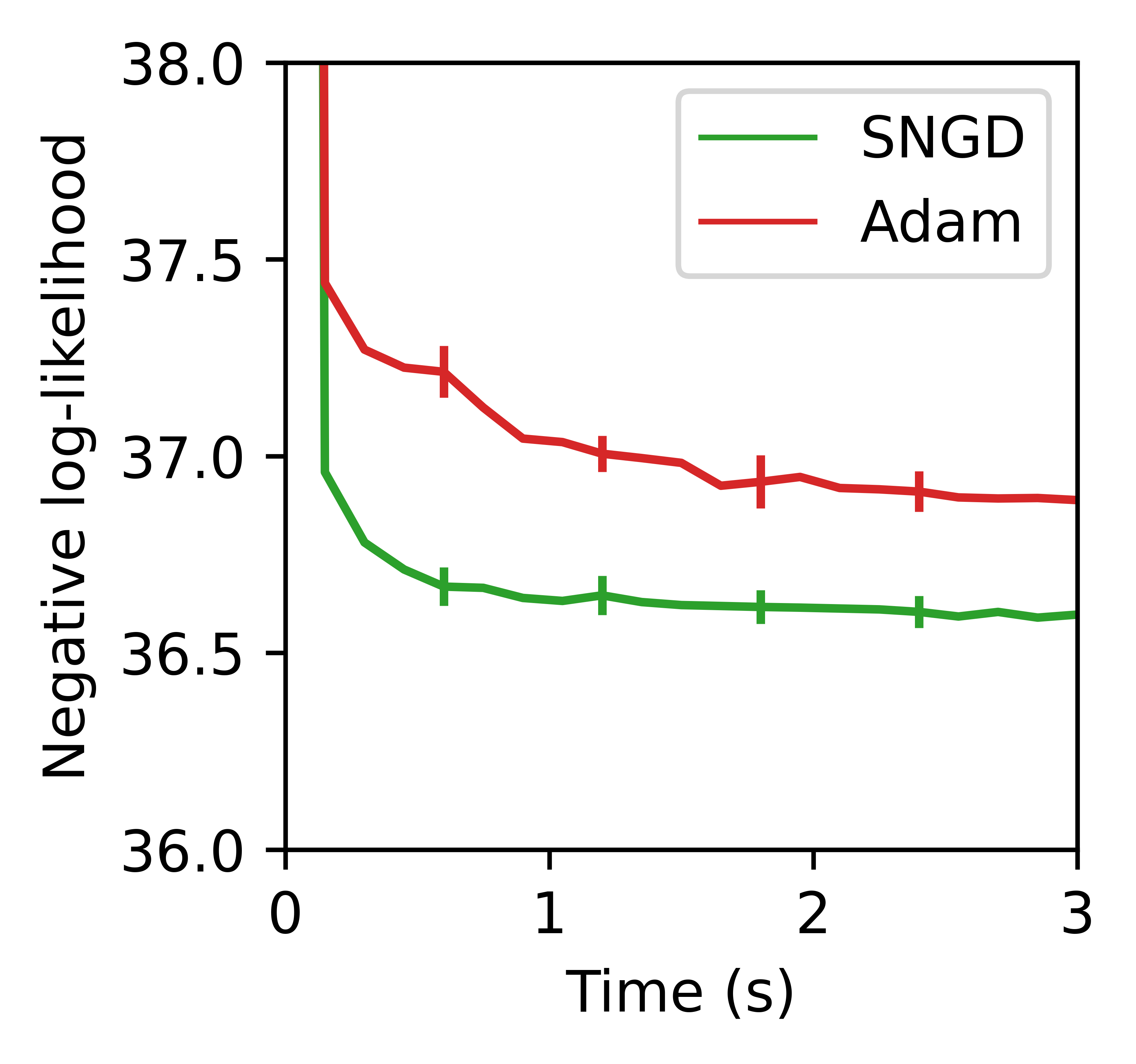

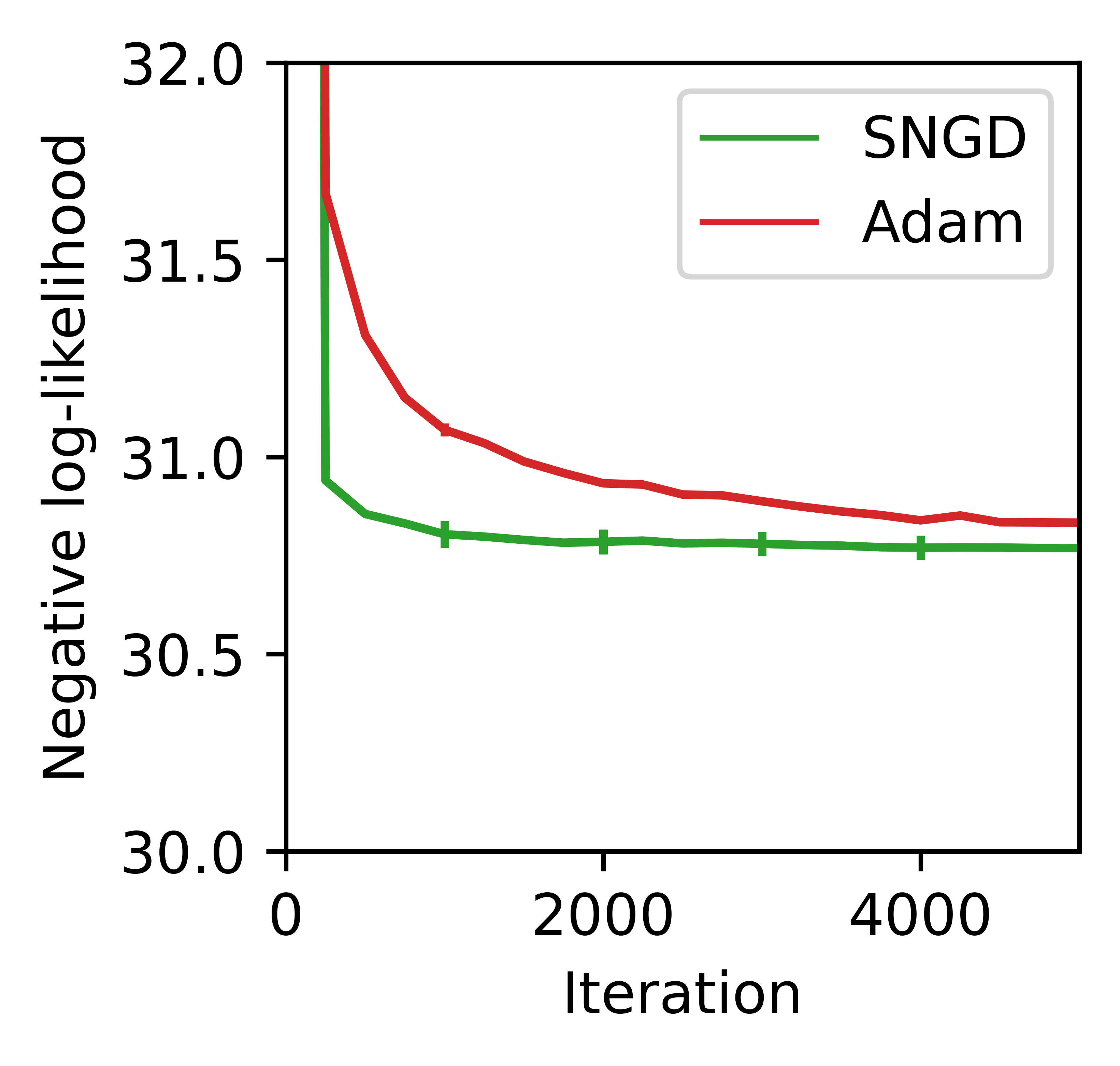

We performed two tasks in our experiments. In the first, the skew-elliptical distributions were used for density estimation on the UCI miniboone dataset (=32,840, =43) (Roe, 2010), fitting their parameters via MLE. In the second, they were used as approximate posteriors in VI for a Bayesian logistic regression model on the UCI covertype dataset (Blackard, 1998); in this task we used a small subsample of observations in order to retain some uncertainty in the posterior (=500, =53).

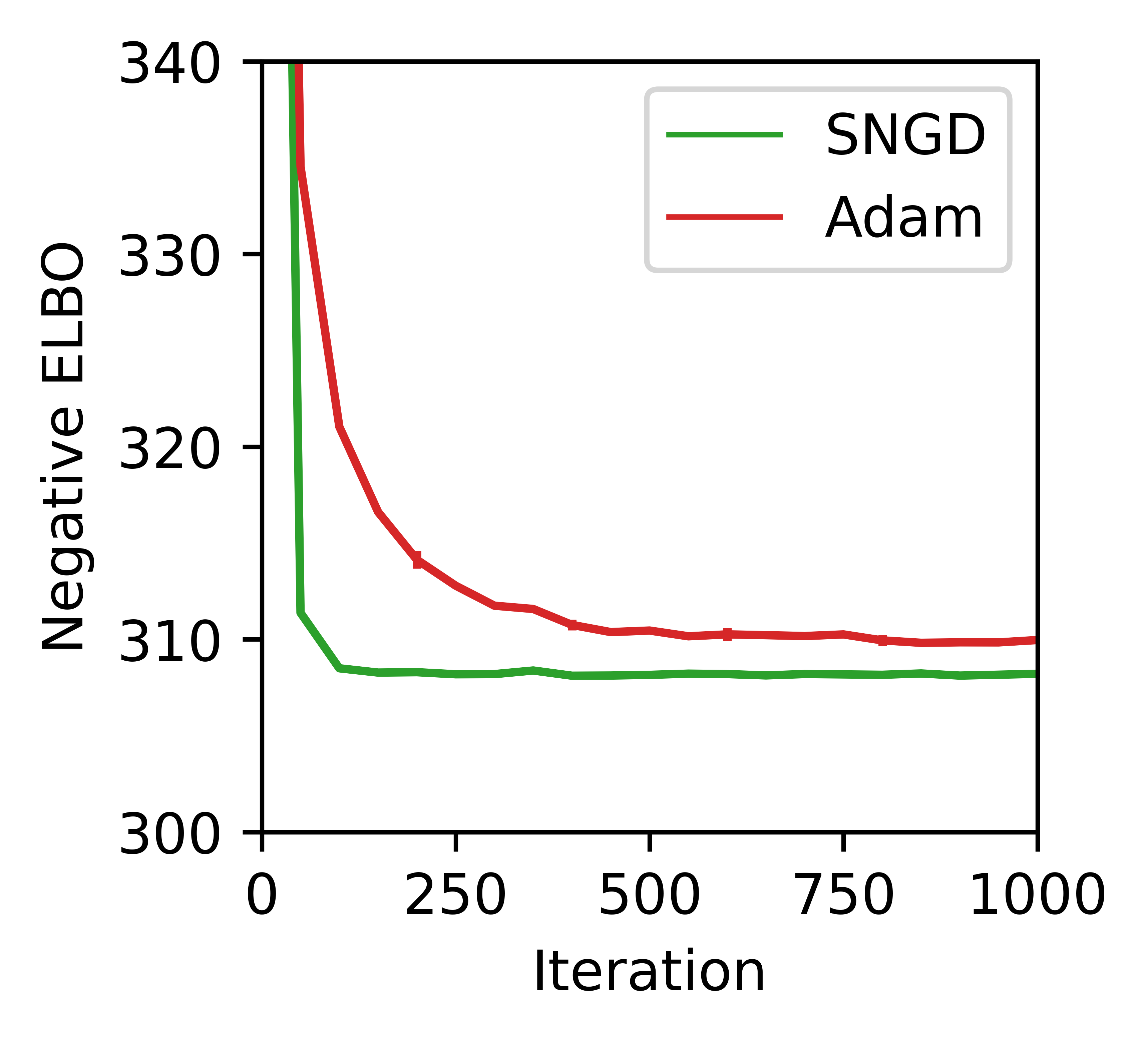

Note that the numbers of free parameters in these optimisations were due to the covariance-like parameters of the target distributions. The skew-normal distribution had 1,032 and 1,537 parameters in the miniboone and covertype experiments respectively. For the skew- distribution those numbers were 990 and 1,485.

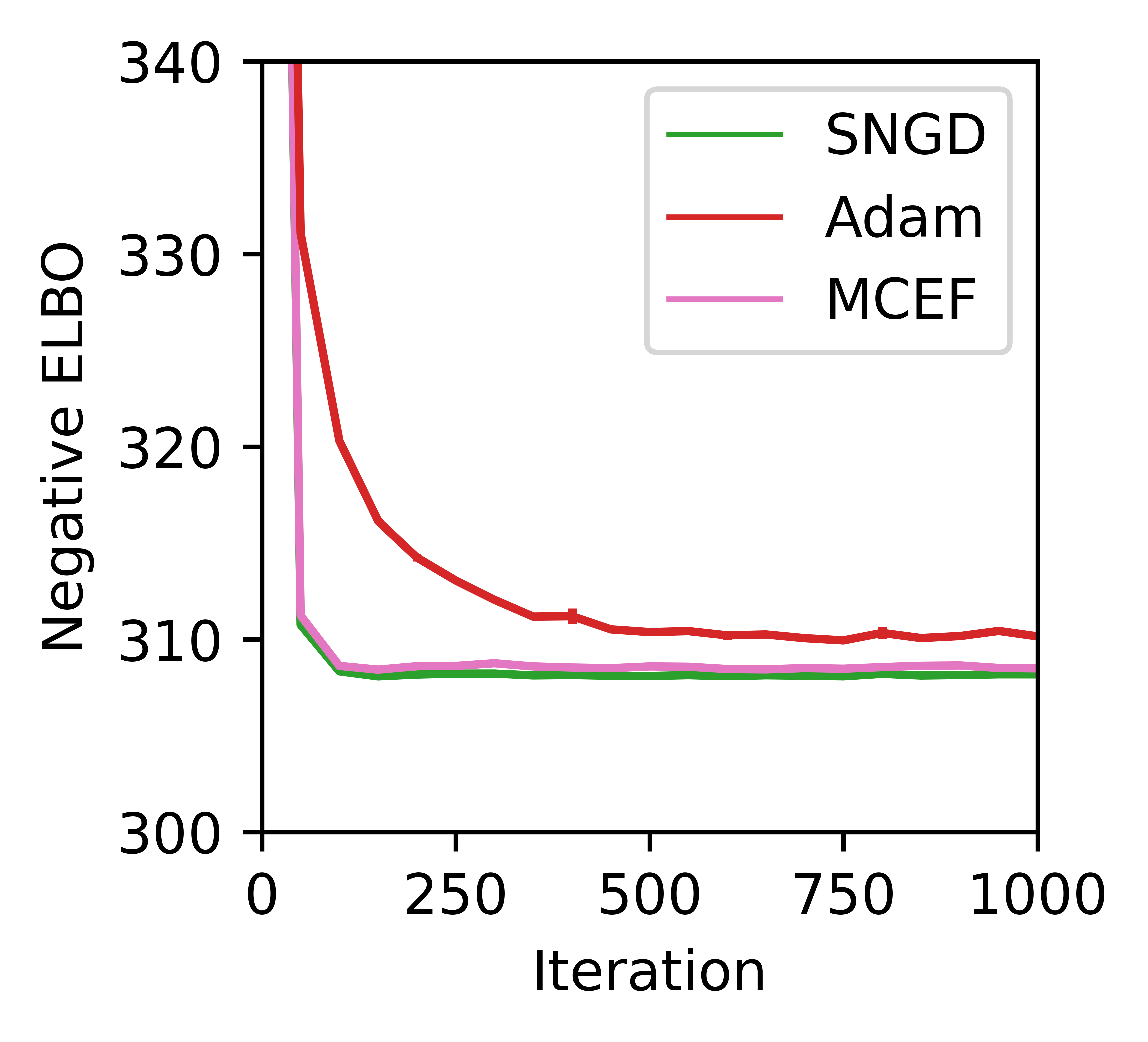

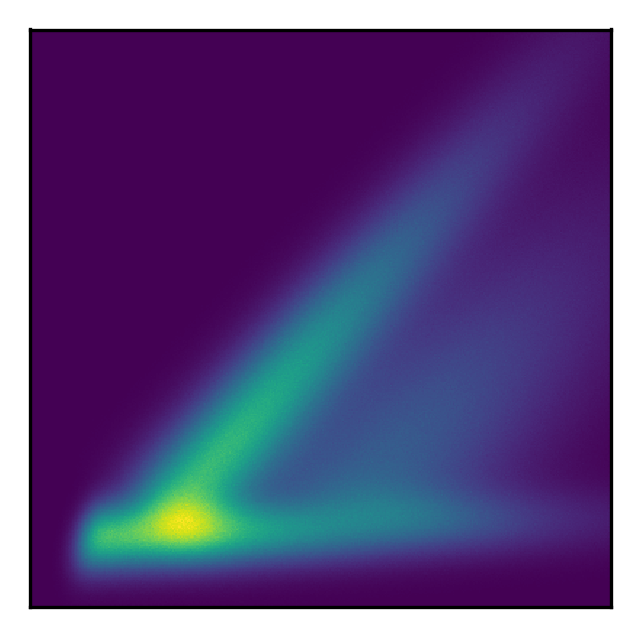

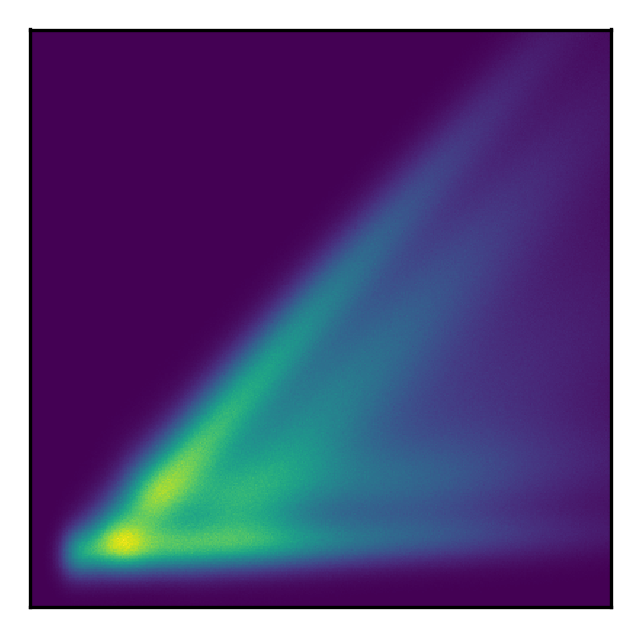

Figures 2 and 3 show training curves from the MLE and VI experiments respectively. In all cases SNGD significantly outperformed Adam. In the particular case of the skew-normal VI experiment, it was also possible to apply the natural gradient method of Lin et al. (2019) based on minimal conditional exponential family (MCEF) distributions, and so we included this as an additional baseline. Its performance was almost identical to that of SNGD. It turns out that the method of Li (2000) can, in fact, be viewed as an example of SNGD, which we discuss in Section 5.

4.3 Elliptical Copulas

Copula models define a distribution on the unit hypercube , for which each of the marginals is uniform on . If is distributed according to copula , and , where is the inverse CDF of a distribution , then will have marginal distribution . The will be dependent in general, with dependence structure determined by .

Copula models are widely used in finance for modelling high-dimensional variables, in part because they allow marginal distributions to be modelled separately from the dependence structure (Dewick and Liu, 2022).

The class of elliptical copulas are defined as those copulas which can be used to generate elliptical distributions (Frahm et al., 2003). Common examples are the Gaussian and copulas. Elliptical copulas are parameterised by a correlation matrix , as well as a (possibly empty) set of additional parameters.

A simple way to target elliptical copulas with SNGD is to use a zero-mean normal surrogate, mapping its correlation matrix to . Any additional parameters may then be captured by , as outlined in Section 3.4.

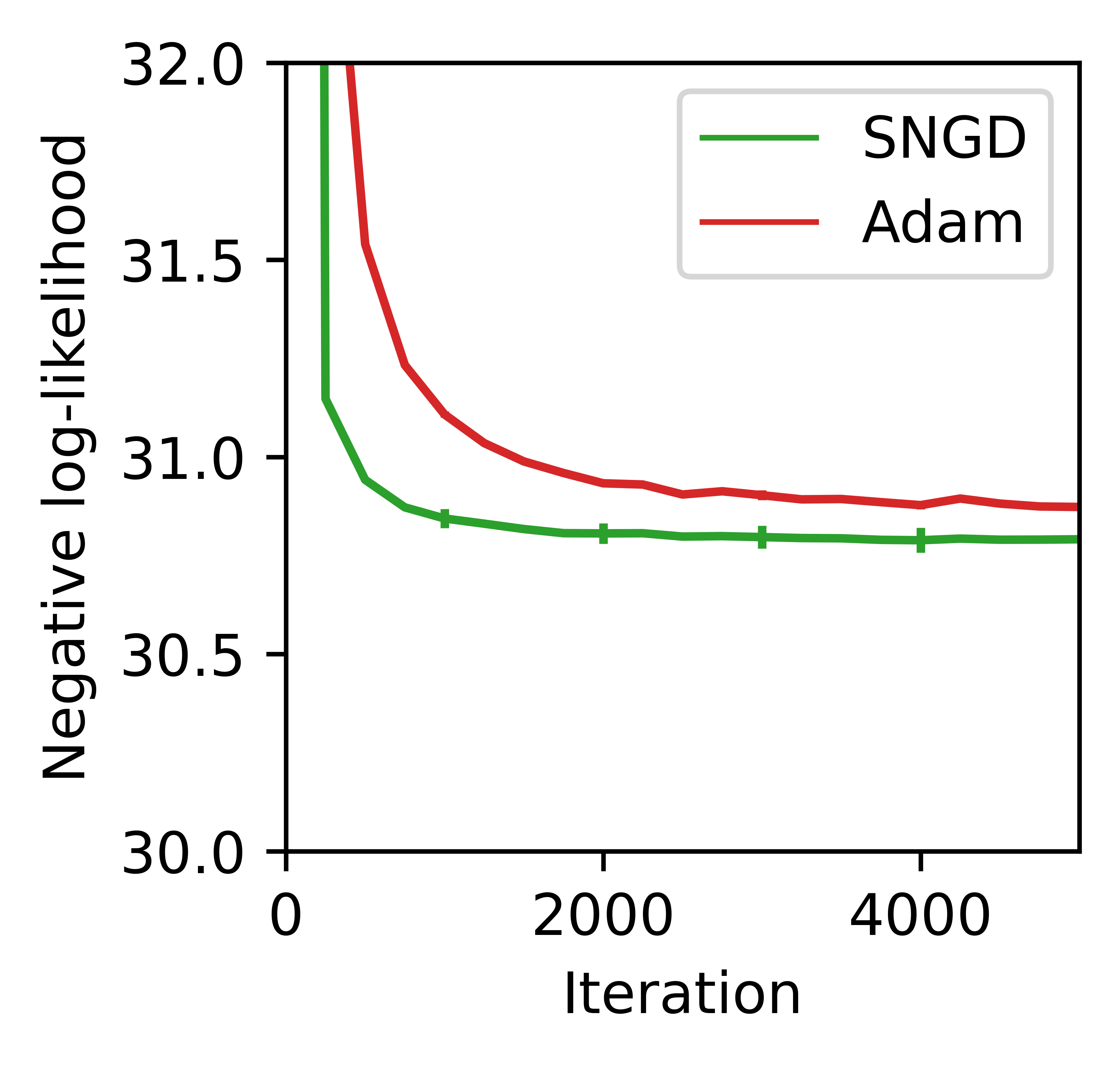

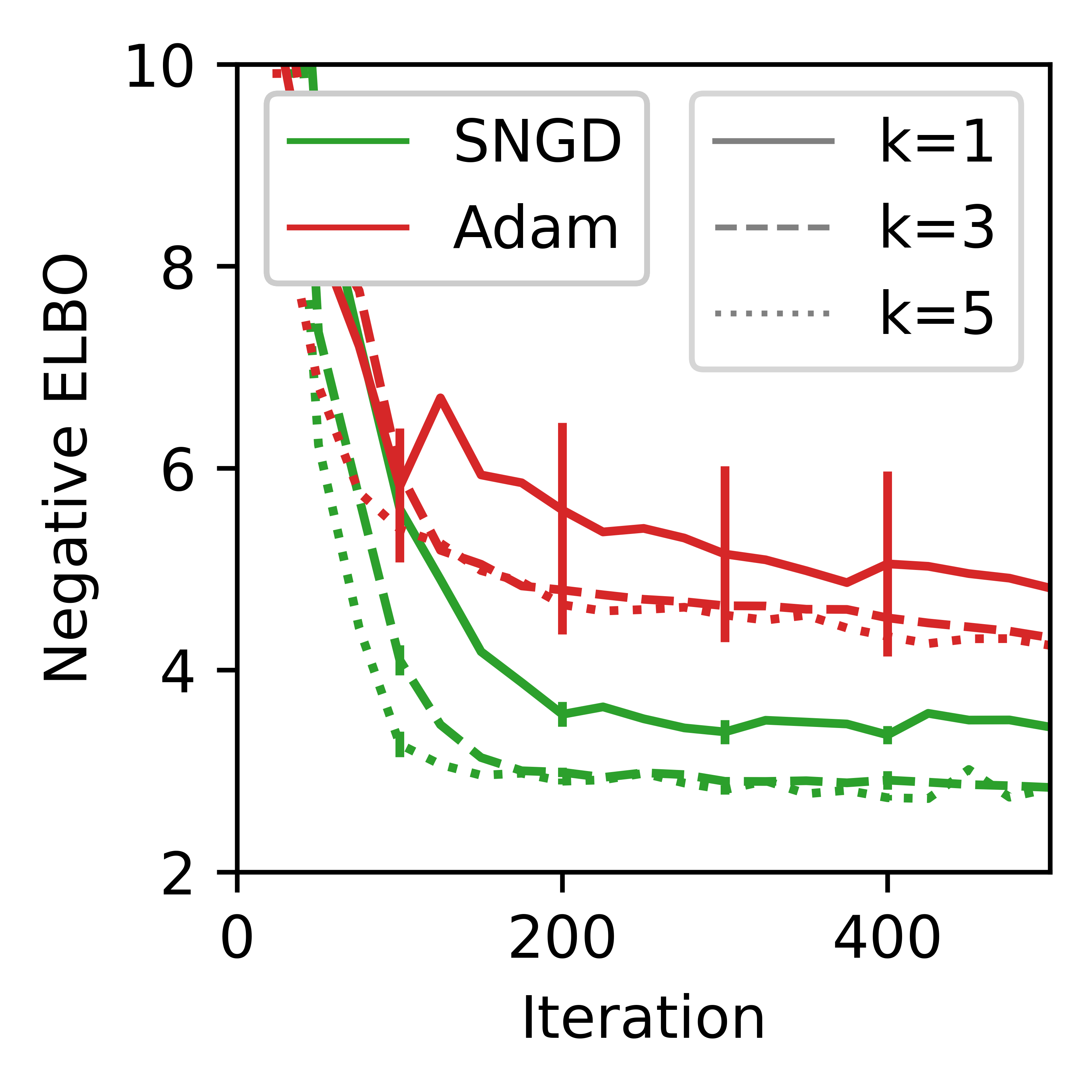

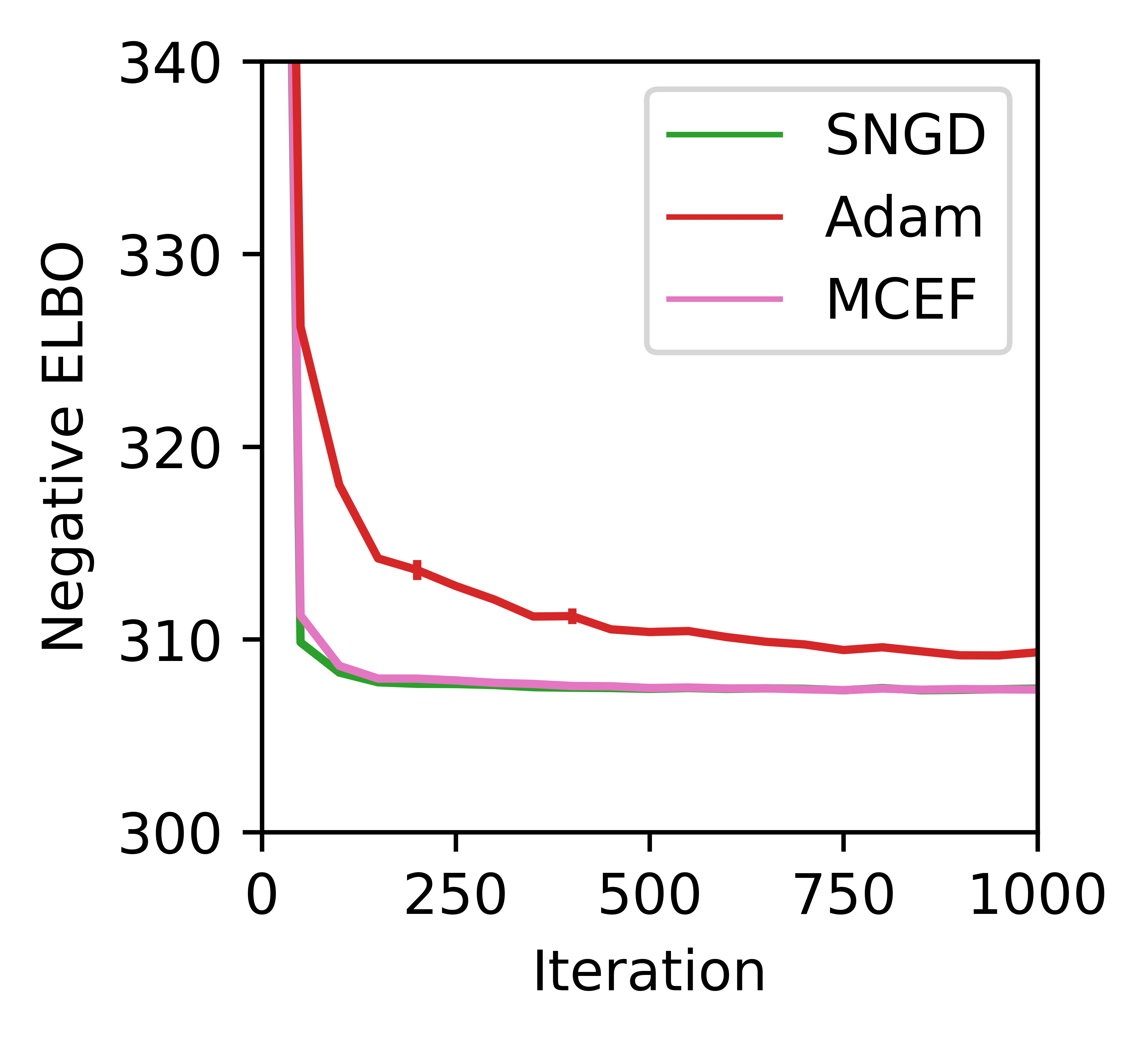

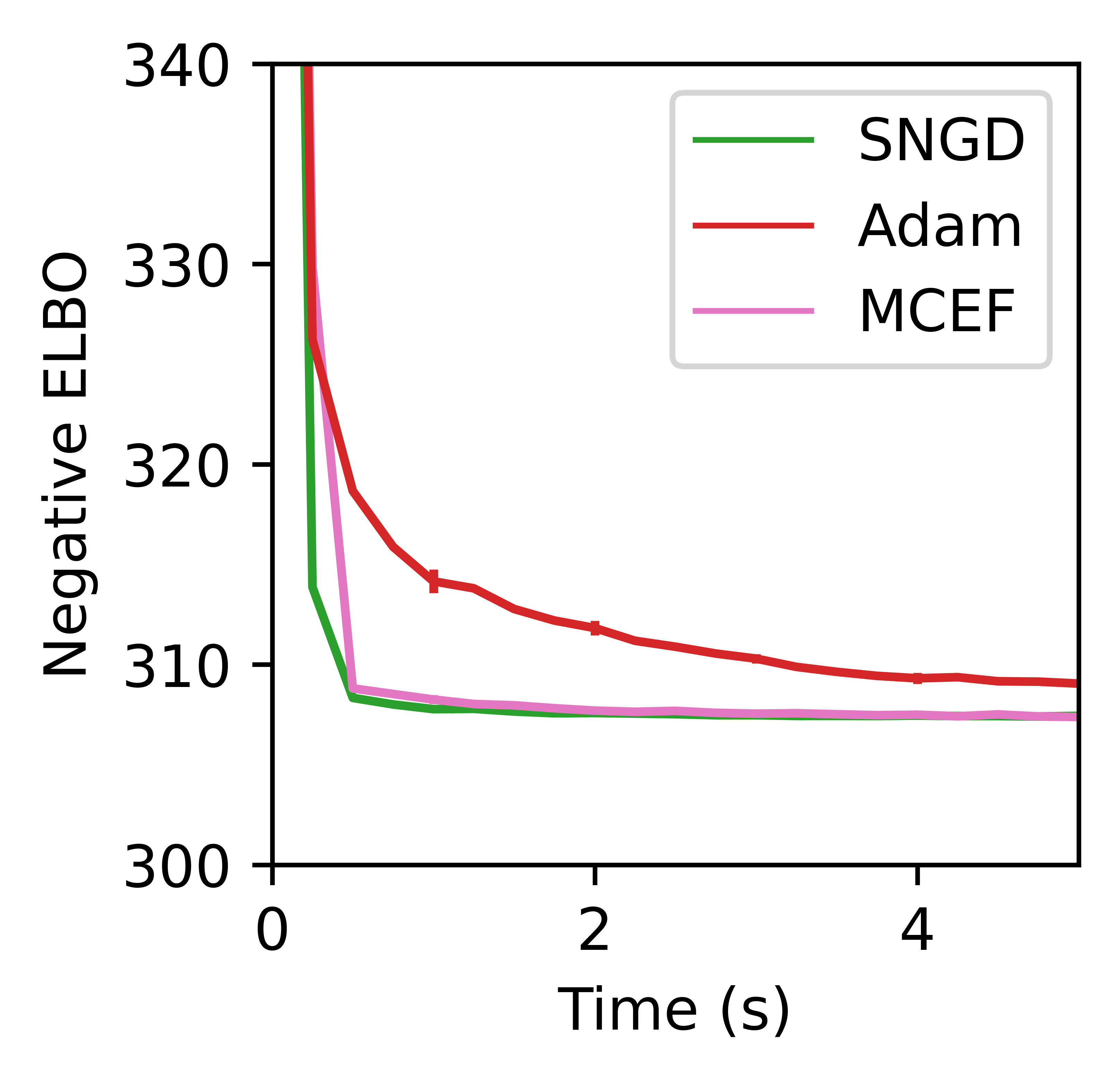

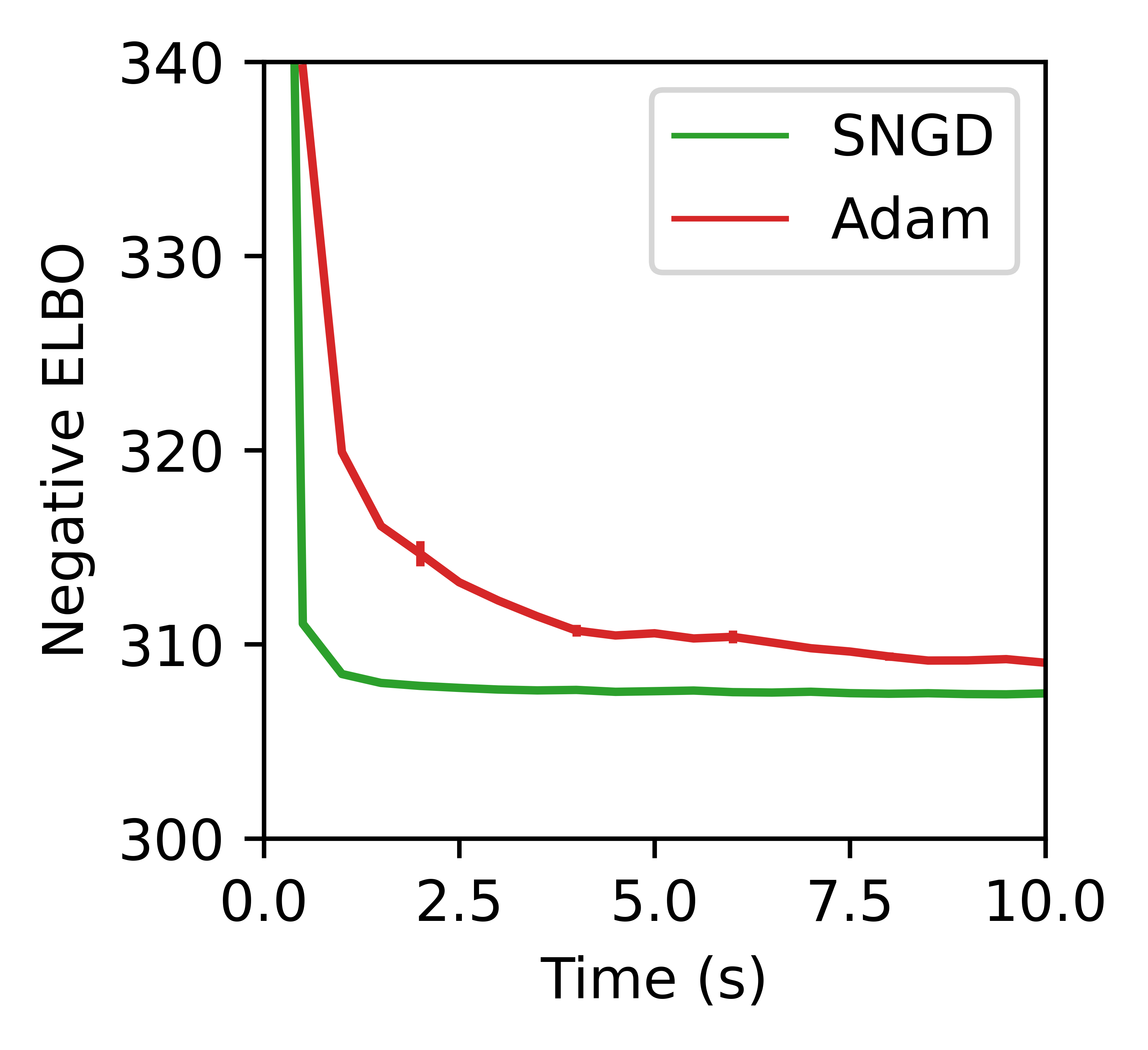

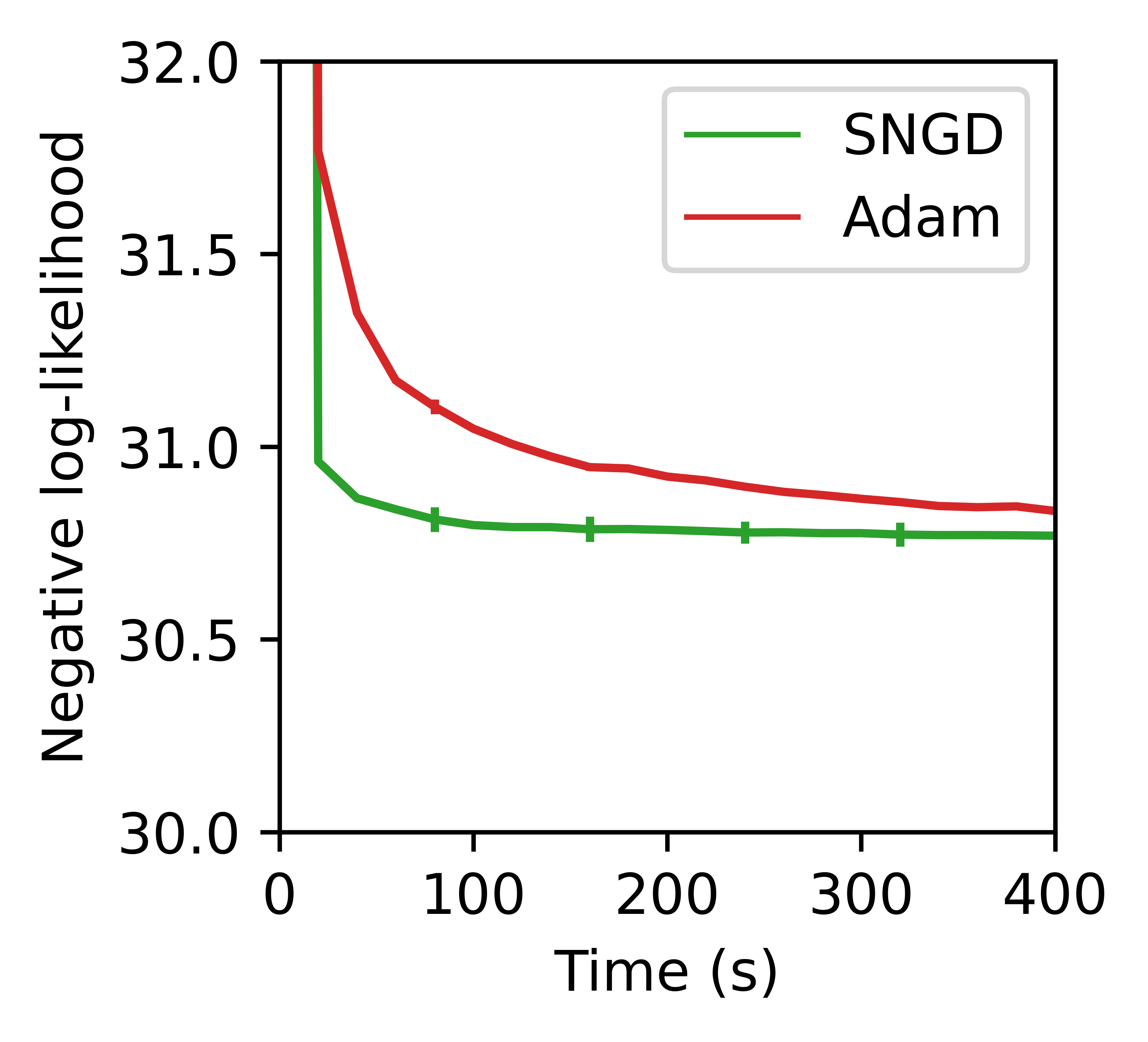

We used this approach to perform MLE of the -copula on 5 years of daily stock returns from the FTSE 100 universe (=1,515, =93), with marginals estimated as (univariate) Student’s distributions. In this experiment had 4,279 free parameters. Figure 4 shows that SNGD converged significantly faster than Adam.

4.4 Mixture Distributions

A mixture distribution expresses a complicated density as a convex combination of simpler densities:

| (16) |

where , and is known as the -th component distribution. For each mixture, we can also define a corresponding mixture model, a joint distribution, with density

| (17) |

where the mixture component identity, , is treated as a latent variable. Note then, that . That is, a mixture model has a mixture as its marginal. A mixture of EFs is not in general itself an EF. However, it can be shown that the corresponding mixture model (joint distribution) is an EF (see Appendix K).

When an EF is an appropriate surrogate for applying SNGD to a given target family, it is therefore straightforward to consider the extension to mixtures of that family by using an EF mixture model as a surrogate. We emphasise that in doing so, the surrogate distribution has support over more variables ( and ) than the target distribution (just ).

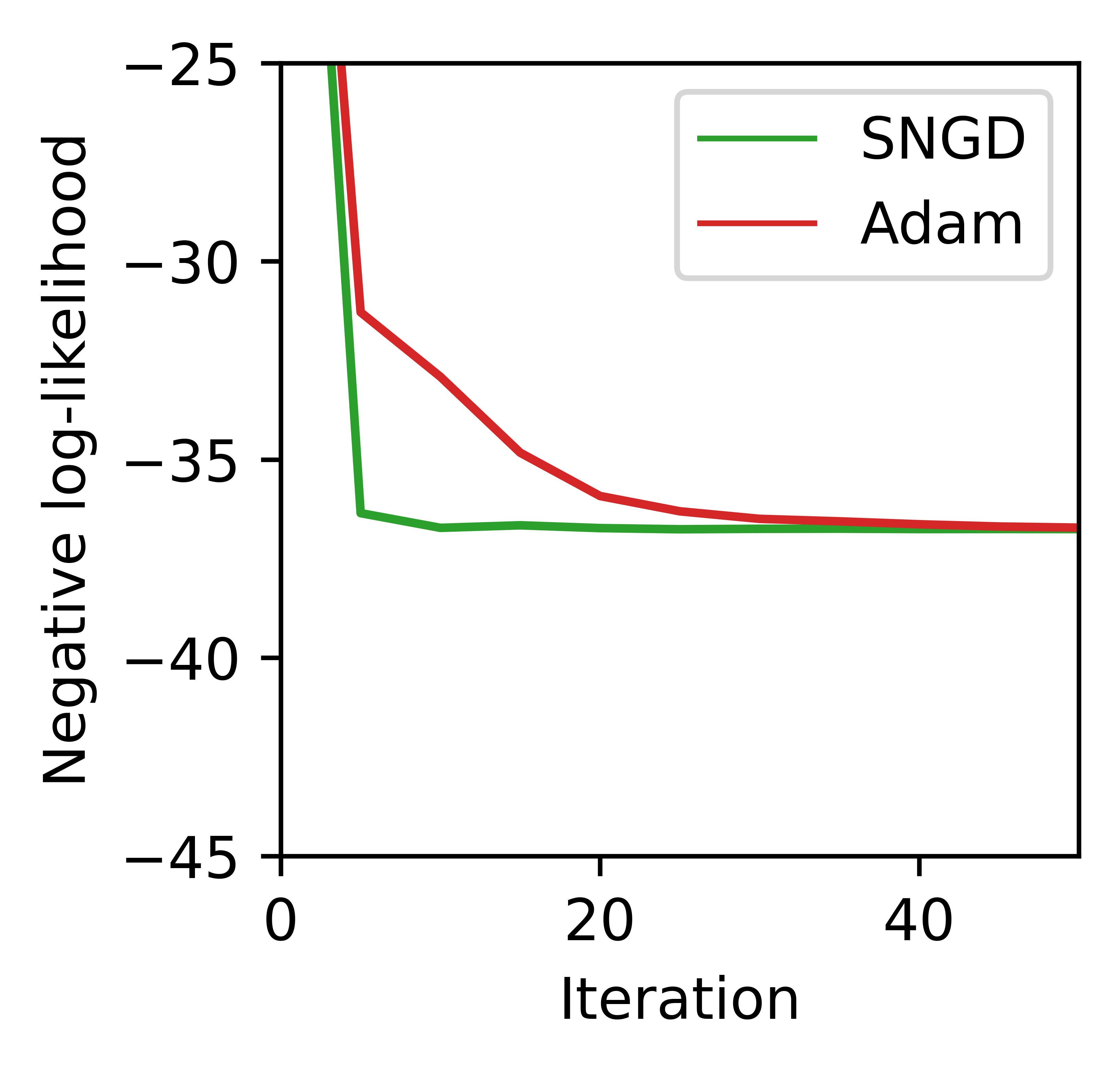

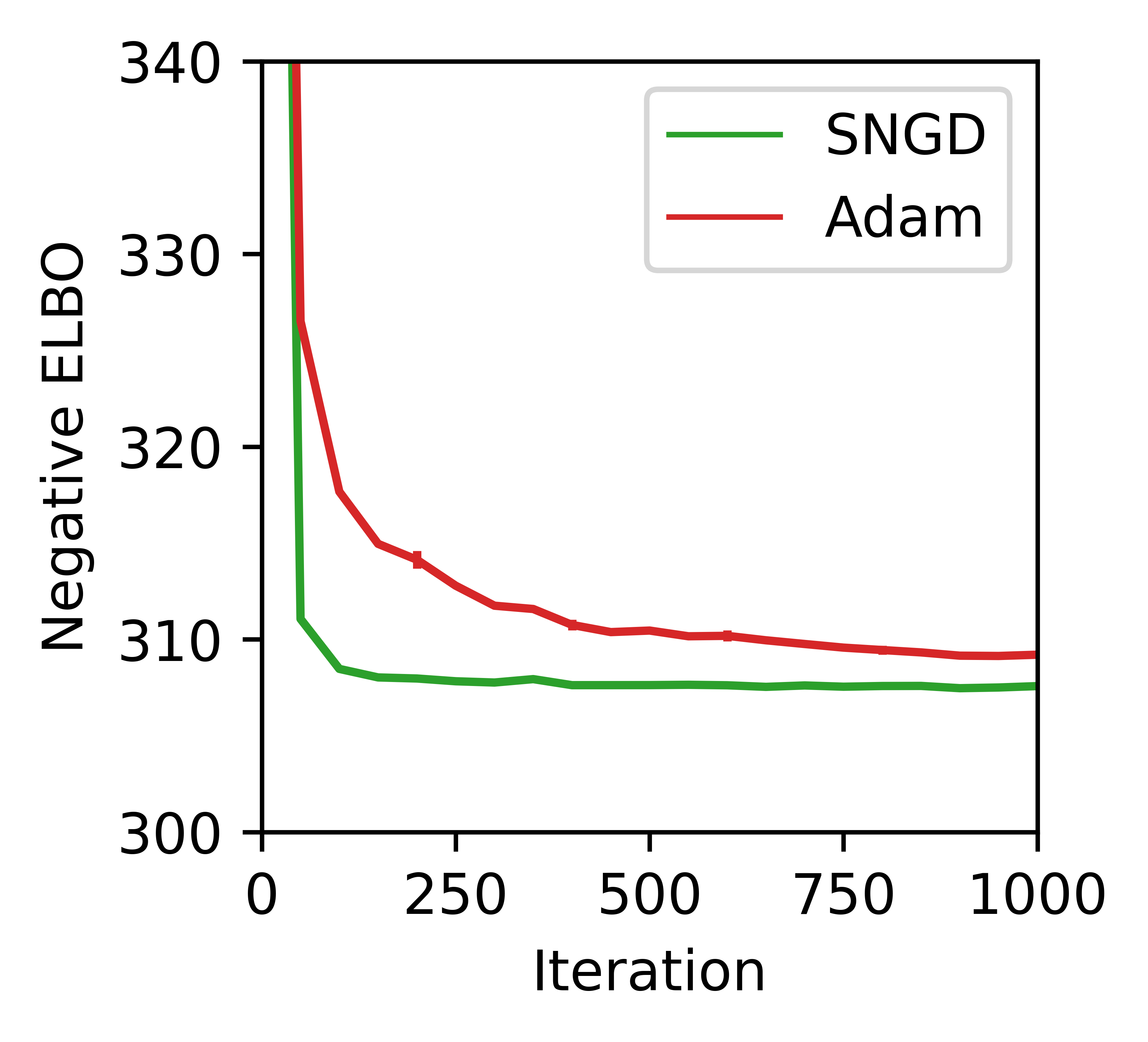

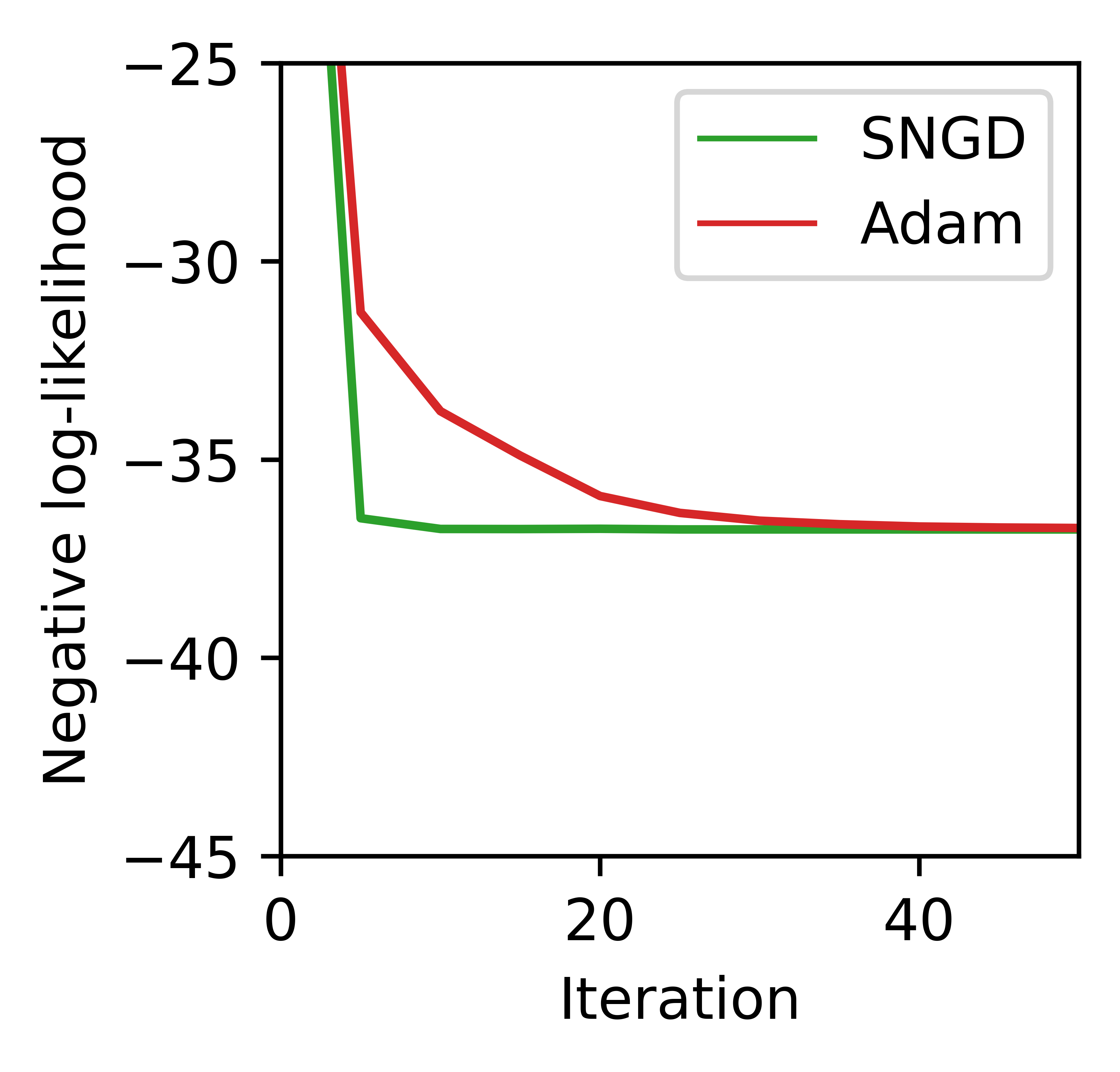

In Section 4.1 we demonstrated the use of a gamma surrogate for optimising negative binomial distribution parameters with SNGD. It is therefore straightforward to use a gamma mixture model to target a negative binomial mixture. As an experiment, we performed MLE of a 5 component negative binomial mixture, using a dataset consisting of the number of daily COVID-19 hospital admissions in the UK over a 3 year period (=1,120, =1). Figure 5 shows that SNGD significantly outperformed our baselines.

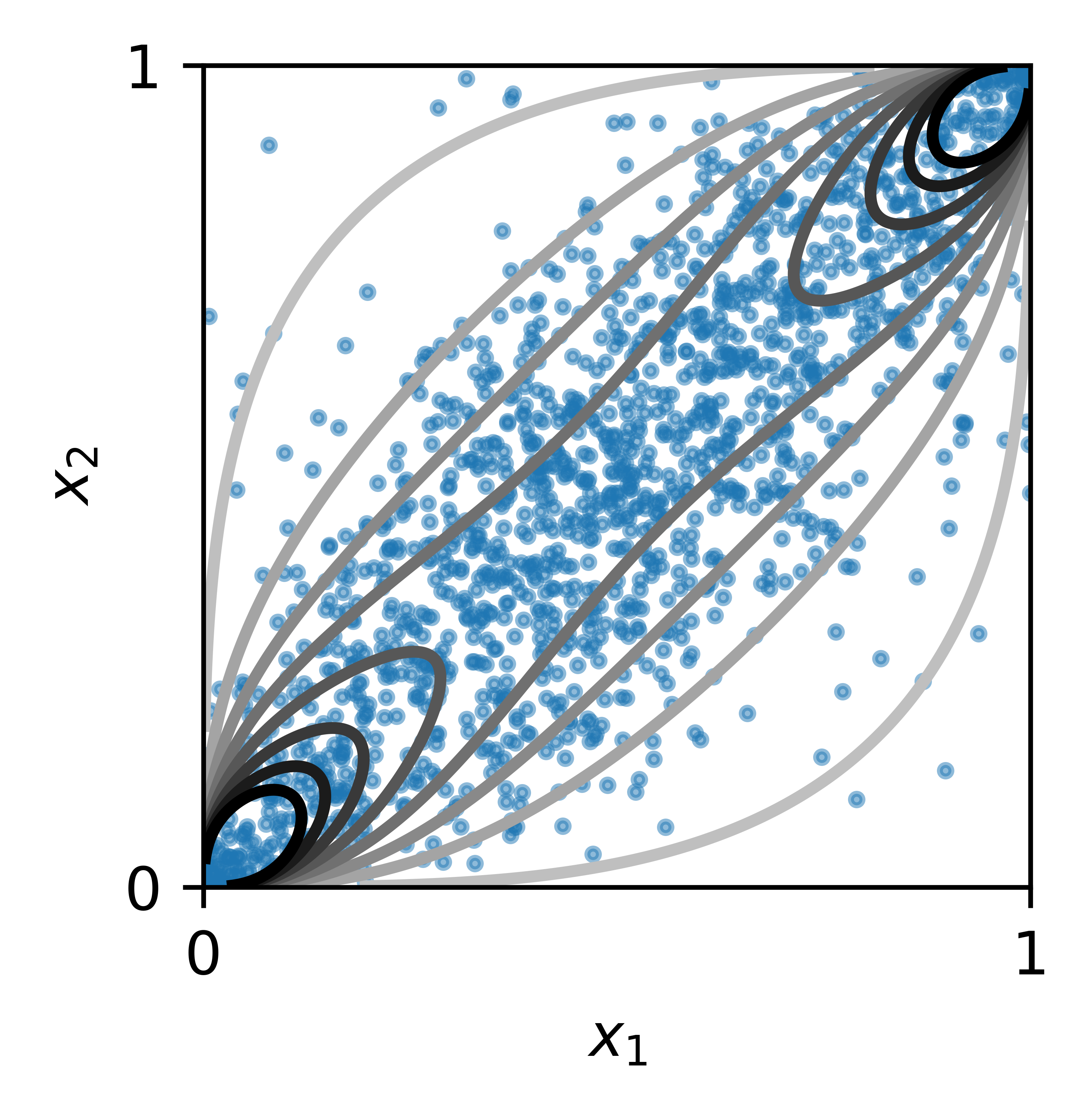

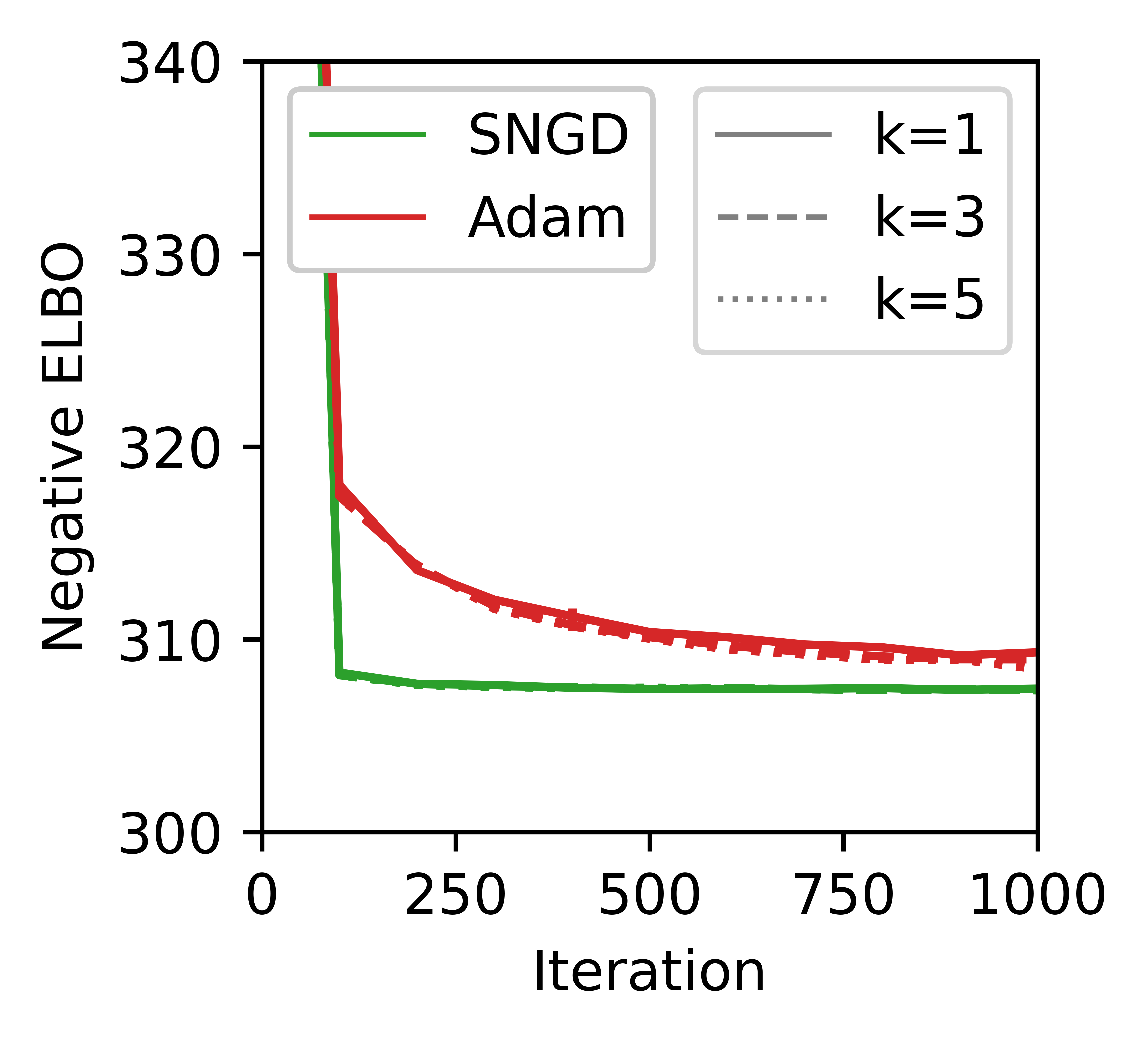

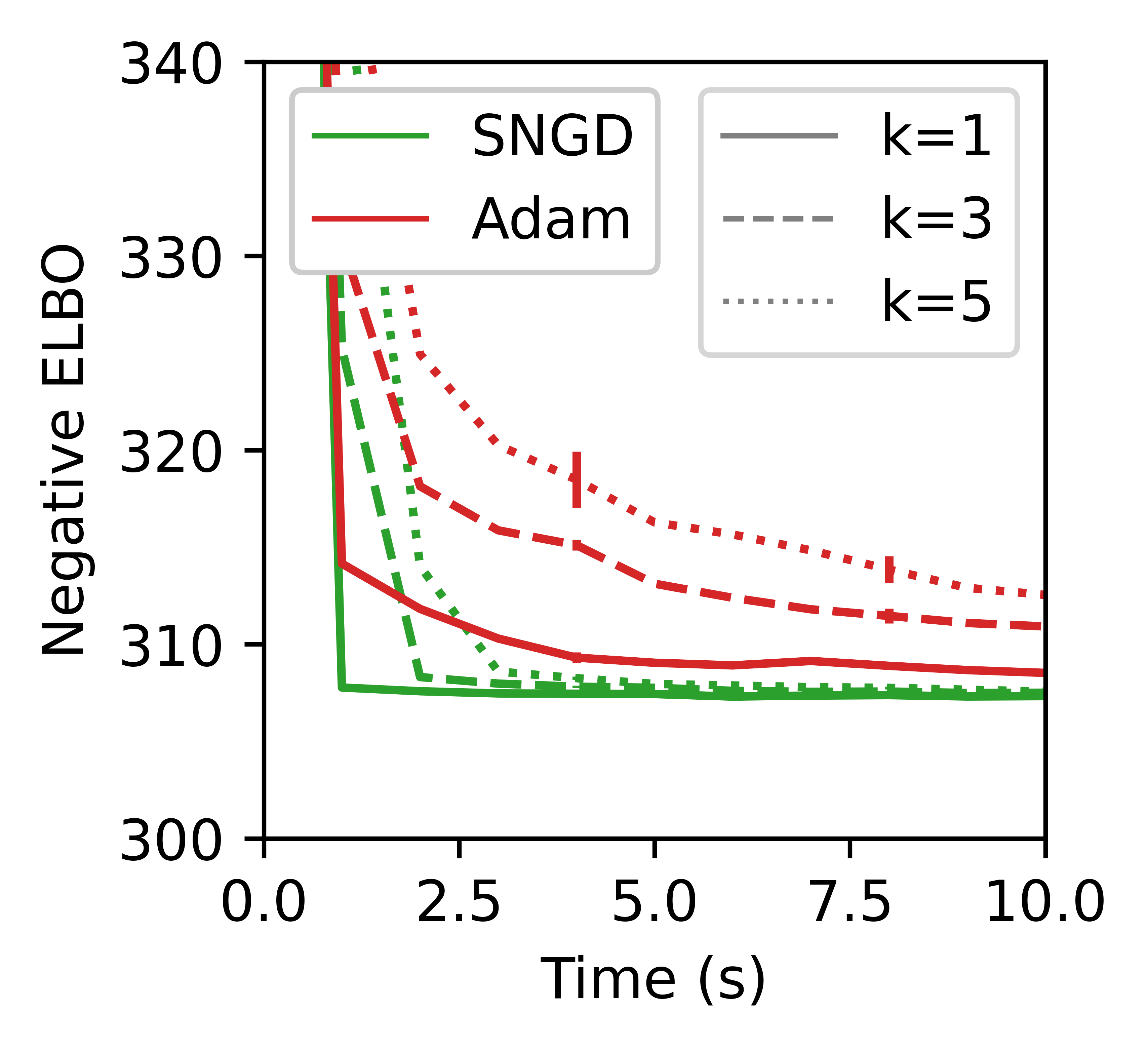

As a further example, similarly, we can use a normal mixture model as the surrogate for a skew-normal mixture. Figure 6 shows the qualitative improvement a skew-normal mixture can offer over a normal mixture on the Bayesian logistic regression VI task of Murphy (2012) (=60, =2). Figure 7 shows training curves for this task, as well as for the UCI covertype Bayesian logistic regression VI task of Section 4.2. In the latter, had 4,612 and 7,689 free parameters for =3, 5, respectively.

|

|

|

|

|

|

|

|

| GT |

5 RELATED WORK

Several existing methods can be interpreted as examples of the general technique presented in this paper.

Lin et al. (2019) introduced the class of MCEF distributions, and showed that natural gradients with respect to a particular parameterisation of MCEF distributions can be efficiently computed using an identity analogous to (5). They also showed that several standard distributions can be expressed as marginals of MCEF distributions, including the multivariate Student’s and multivariate skew-normal distributions. They then used NGD with respect to the MCEF joint as a surrogate for its marginal in a number of VI tasks. This mismatch between the surrogate and target distributions (our terminology) was not explicitly discussed by Lin et al. (2019), possibly because the two were so closely related (by marginalisation). SNGD is more general in that it makes no such assumption about the relationship between surrogate and target distributions. In particular, it is not restricted to targets that can be expressed as the marginal of a MCEF (or any other) distribution.

The stochastic natural gradient expectation propagation (SNEP) algorithm of Hasenclever et al. (2017) solves a saddle-point optimisation problem, with the inner optimisation being over a set of parameters known as the site parameters. The site parameters jointly parameterise a set of distributions for which computing natural gradients is not straightforward. SNEP instead treats each as if it were the natural parameter vector of a EF distribution in its own right, and performs NGD in the dual (mean parameter) space. These (pseudo)distributions acted as surrogates for the more problematic set of distributions that were the ultimate targets of the optimisation.

Hernández et al. (2014) devised a fixed-point iteration scheme for optimising the correlation matrix parameter of an elliptical copula. Interestingly, although their procedure was motivated in an entirely different way, the resulting updates for are identical to those performed by SNGD when applied in the manner described in Section 4.3.

In supervised learning, the goal is to model the conditional density given training data pairs . In this setting the Fisher matrix is usually defined with respect to the distribution , where is the empirical distribution of under the training data . In practice, when the data set is large, the Fisher must be computed with respect to some subset of the training inputs , such as the current minibatch. This is equivalent to using as a surrogate for , where is the empirical distribution of in . In the context of supervised deep learning, Ren and Goldfarb (2019) showed that exact natural gradients with respect to can be computed efficiently when is small.

Several works have attempted to handle intractability of the natural gradient in other ways. Some methods are based on structured approximations to the Fisher, that allow inverse vector products to be computed efficiently (Heskes, 2000, Martens and Grosse, 2015, George et al., 2018). Garcia et al. (2023) instead approximated the inverse Fisher matrix directly by expressing it in terms of the solution to an optimisation problem. The widely used Adam optimiser employs a moving average of squared gradients as a diagonal approximation to the Fisher (Kingma and Ba, 2014), although it has been cautioned that this is more accurately viewed as an approximation to the empirical Fisher (Kunstner et al., 2019).

6 DISCUSSION

In this work we proposed a novel technique for optimising functions of probability distribution parameters: reframing the objective as an optimisation with respect to a surrogate distribution for which computing natural gradients is easy, and performing optimisation in that space. We found several existing methods that can be interpreted as applying this technique, and proposed a new method based on EF surrogates. We demonstrated that our method is able to converge rapidly on a variety of MLE and VI tasks. We believe our method can be readily applied to distributions outside of the set of examples given here. We also expect that new methods can be found by applying the more general technique that motivated our method.

The main limitation of our method is the need to find a suitable surrogate and reparameterisation for a given target distribution. In some cases there is an obvious candidate, such as when an EF distribution could serve as an approximation for the target, or when the target can be viewed as an EF that has been warped or transformed in some way. However, for most of the examples in this paper, the target and surrogate distributions do not even have support over the same space (see Table 1). Our choice of surrogate for each example was largely guided by the intuition that should, in some sense, behave like with respect to . We begin to explore what this means in Appendix H. However, we leave a full characterisation of the conditions under which a surrogate will be effective to future work.

Acknowledgements

We would like to thank Runa Eschenhagen, Jihao Andreas Lin, and James Townsend for providing valuable feedback. Jonathan So is supported by the University of Cambridge Harding Distinguished Postgraduate Scholars Programme. Richard E. Turner is supported by Google, Amazon, ARM, Improbable and EPSRC grant EP/T005386/1.

References

- Amari (1998) S.-i. Amari. Natural Gradient Works Efficiently in Learning. Neural Computation, 1998.

- Azzalini (2013) A. Azzalini. The Skew-Normal and Related Families. Cambridge University Press, 2013.

- Bernacchia et al. (2018) A. Bernacchia, M. Lengyel, and G. Hennequin. Exact natural gradient in deep linear networks and its application to the nonlinear case. In Advances in Neural Information Processing Systems, 2018.

- Bertsekas (1997) D. P. Bertsekas. Nonlinear programming. Journal of the Operational Research Society, 1997.

- Blackard (1998) J. Blackard. Covertype. UCI Machine Learning Repository, 1998.

- Blondel et al. (2022) M. Blondel, Q. Berthet, M. Cuturi, R. Frostig, S. Hoyer, F. Llinares-Lopez, F. Pedregosa, and J.-P. Vert. Efficient and modular implicit differentiation. In Advances in Neural Information Processing Systems, 2022.

- Bradbury et al. (2018) J. Bradbury, R. Frostig, P. Hawkins, M. J. Johnson, C. Leary, D. Maclaurin, G. Necula, A. Paszke, J. VanderPlas, S. Wanderman-Milne, and Q. Zhang. JAX: composable transformations of Python+NumPy programs, 2018.

- Chang and Lin (2011) C.-C. Chang and C.-J. Lin. LIBSVM: A library for support vector machines. ACM Transactions on Intelligent Systems and Technology, 2011.

- Christianson (1994) B. Christianson. Reverse accumulation and attractive fixed points. Optimization Methods & Software, 1994.

- Dewick and Liu (2022) P. R. Dewick and S. Liu. Copula modelling to analyse financial data. Journal of Risk and Financial Management, 2022.

- Fisher (1941) R. A. Fisher. The negative binomial distribution. Annals of Eugenics, 1941.

- Frahm et al. (2003) G. Frahm, M. Junker, and A. Szimayer. Elliptical copulas: applicability and limitations. Statistics & Probability Letters, 2003.

- Garcia et al. (2023) J. R. Garcia, F. Freddi, S. Fotiadis, M. Li, S. Vakili, A. Bernacchia, and G. Hennequin. Fisher-legendre (fishleg) optimization of deep neural networks. In International Conference on Learning Representations, 2023.

- George et al. (2018) T. George, C. Laurent, X. Bouthillier, N. Ballas, and P. Vincent. Fast approximate natural gradient descent in a kronecker-factored eigenbasis. In Neural Information Processing Systems, 2018.

- Guenther (1972) W. C. Guenther. A simple approximation to the negative binomial (and regular binomial). Technometrics, 1972.

- Hasenclever et al. (2017) L. Hasenclever, S. Webb, T. Lienart, S. Vollmer, B. Lakshminarayanan, C. Blundell, and Y. W. Teh. Distributed bayesian learning with stochastic natural gradient expectation propagation and the posterior server. Journal of Machine Learning Research, 2017.

- Hensman et al. (2012) J. Hensman, M. Rattray, and N. Lawrence. Fast variational inference in the conjugate exponential family. In Advances in Neural Information Processing Systems, 2012.

- Hensman et al. (2013) J. Hensman, N. Fusi, and N. Lawrence. Gaussian processes for big data. In Uncertainty in Artificial Intelligence - Proceedings of the 29th Conference, UAI 2013, pages 282–290, 2013. 29th Conference on Uncertainty in Artificial Intelligence, UAI 2013 ; Conference date: 11-07-2013 Through 15-07-2013.

- Hernández et al. (2014) L. Hernández, J. Tejero, and J. Vinuesa. Maximum likelihood estimation of the correlation parameters for elliptical copulas. arXiv:1412.6316, 2014.

- Heskes (2000) T. Heskes. On “Natural” Learning and Pruning in Multilayered Perceptrons. Neural Computation, 2000.

- Hoffman et al. (2013) M. D. Hoffman, D. M. Blei, C. Wang, and J. Paisley. Stochastic variational inference. Journal of Machine Learning Research, 2013.

- Kakade (2001) S. M. Kakade. A natural policy gradient. In Advances in Neural Information Processing Systems. MIT Press, 2001.

- Kendall et al. (2023) M. Kendall, D. Tsallis, C. Wymant, A. Di Francia, Y. Balogun, X. Didelot, L. Ferretti, and C. Fraser. Epidemiological impacts of the nhs covid-19 app in england and wales throughout its first year. Nature Communications, 2023.

- Khan and Lin (2017) M. Khan and W. Lin. Conjugate-Computation Variational Inference : Converting Variational Inference in Non-Conjugate Models to Inferences in Conjugate Models. In Proceedings of the 20th International Conference on Artificial Intelligence and Statistics, 2017.

- Khan et al. (2018) M. Khan, D. Nielsen, V. Tangkaratt, W. Lin, Y. Gal, and A. Srivastava. Fast and scalable Bayesian deep learning by weight-perturbation in Adam. In Proceedings of the 35th International Conference on Machine Learning, 2018.

- Khan et al. (2017) M. E. Khan, W. Lin, V. Tangkaratt, Z. Liu, and D. Nielsen. Variational adaptive-newton method. In NeurIPS Workshop on Advances in Approximate Bayesian Inference, 2017.

- Kingma and Ba (2014) D. Kingma and J. Ba. Adam: A method for stochastic optimization. International Conference on Learning Representations, 2014.

- Kingma and Welling (2014) D. P. Kingma and M. Welling. Auto-Encoding Variational Bayes. In International Conference on Learning Representations, 2014.

- Kunstner et al. (2019) F. Kunstner, P. Hennig, and L. Balles. Limitations of the empirical fisher approximation for natural gradient descent. In Advances in Neural Information Processing Systems, 2019.

- Lee et al. (2016) J. D. Lee, M. Simchowitz, M. I. Jordan, and B. Recht. Gradient descent only converges to minimizers. In Conference on Learning Theory, 2016.

- Li (2000) D. Li. On default correlation. The Journal of Fixed Income, 9:43–54, 03 2000.

- Lin et al. (2019) W. Lin, M. E. Khan, and M. Schmidt. Fast and simple natural-gradient variational inference with mixture of exponential-family approximations. In International Conference on Machine Learning, 2019.

- Lloyd-Smith et al. (2005) J. Lloyd-Smith, S. Schreiber, P. Kopp, and W. Getz. Superspreading and the effect of individual variation on disease emergence. Nature, 2005.

- Lloyd-Smith (2007) J. O. Lloyd-Smith. Maximum likelihood estimation of the negative binomial dispersion parameter for highly overdispersed data, with applications to infectious diseases. PLOS ONE, 2007.

- Martens and Grosse (2015) J. Martens and R. Grosse. Optimizing neural networks with kronecker-factored approximate curvature. In International Conference on Machine Learning, 2015.

- Minka (2000) T. Minka. Estimating a dirichlet distribution. Technical report, Microsoft, September 2000.

- Minka (2002) T. Minka. Estimating a gamma distribution. Technical report, Microsoft, April 2002.

- Murphy (2012) K. P. Murphy. Machine Learning: A Probabilistic Perspective. The MIT Press, 2012.

- Nocedal and Wright (2006) J. Nocedal and S. J. Wright. Numerical Optimization. Springer, New York, NY, USA, 2e edition, 2006.

- Ollivier et al. (2017) Y. Ollivier, L. Arnold, A. Auger, and N. Hansen. Information-geometric optimization algorithms: A unifying picture via invariance principles. Journal of Machine Learning Research, 2017.

- Orooji et al. (2021) A. Orooji, E. Nazar, M. Sadeghi, A. Moradi, Z. Jafari, and H. a. Esmaily. Factors associated with length of stay in hospital among the elderly patients using count regression models. Medical Journal of the Islamic Republic Of Iran, 2021.

- Papamakarios et al. (2017) G. Papamakarios, T. Pavlakou, and I. Murray. Masked autoregressive flow for density estimation. In Advances in Neural Information Processing Systems, 2017.

- Ren and Goldfarb (2019) Y. Ren and D. Goldfarb. Efficient subsampled gauss-newton and natural gradient methods for training neural networks. arXiv:1906.02353, 2019.

- Roe (2010) B. Roe. MiniBooNE particle identification. UCI Machine Learning Repository, 2010.

- Roux et al. (2007) N. Roux, P.-a. Manzagol, and Y. Bengio. Topmoumoute online natural gradient algorithm. In Advances in Neural Information Processing Systems, 2007.

- Salimbeni et al. (2018) H. Salimbeni, S. Eleftheriadis, and J. Hensman. Natural gradients in practice: Non-conjugate variational inference in gaussian process models. In International Conference on Artificial Intelligence and Statistics, 2018.

- Sato (2001) M.-A. Sato. Online model selection based on the variational bayes. Neural Computation, 2001.

- Tatzel et al. (2022) L. Tatzel, P. Hennig, and F. Schneider. Late-phase second-order training. In Has it Trained Yet? NeurIPS Workshop, 2022.

- Wainwright and Jordan (2008) M. Wainwright and M. Jordan. Graphical Models, Exponential Families, and Variational Inference. Foundations and Trends in Machine Learning, 2008.

Appendix A GRADIENT NOTATION

In this section we introduce our notation for gradients and related quantities. We largely follow the notation of Bertsekas (1997), with one addition. For function , the gradient at , assuming all partial derivatives exist, is given by

| (18) |

Note, in particular, that this implies is the gradient of evaluated at . The Hessian of , denoted , is the matrix with entries given by

| (19) |

If is a function of and , then

| (20) |

with defined similarly.

When is a vector valued function, the gradient matrix of , denoted , is the transpose of the Jacobian of . That is, the matrix with -th column equal to the gradient of , the -th component of :

| (21) |

Finally (our addition), where is immediately followed by a bracketed expression, we use this to denote the gradient of an anonymous function, with definition given by the bracketed expression, and gradient taken with respect to the subscript, e.g.

| (22) |

and in these cases (only), evaluation of the gradient at, e.g. , is denoted

| (23) |

Appendix B EQUIVALENCE WITH OPTIMISATION OF

In this appendix we show that under certain conditions, optimising is equivalent to optimising in the following sense; finding a local minimiser of also gives us a local minimiser for (Theorem 1), and all local minima of are attainable through (Theorem 2). Furthermore, we show that does not have any non-strict saddle points that are not also present at the corresponding points in (Theorem 5, with support from Theorems 3 and 4).

Note that the results derived here are more general than those that are summarised in Section 3.2. The conditions stated in that section are sufficient to cover all of the examples appearing in this paper. In this appendix we use notation mirroring the method of Section 3.1, but the results apply equally to the extension of Section 3.4 if we replace with the product manifold below.

Let , be differentiable manifolds of dimension , respectively, where . Let be a twice differentiable submersion on , with . Let be twice continuously differentiable, and define .

Theorem 1.

has a local minimum at if and only if has a local minimum at

Proof.

First we prove the statement: has a local minimum at has a local minimum at .

From the definition of a local minimum, there exists a neighbourhood of , such that

| (24) |

Because is a continuous map, the preimage of , , is an open set which by construction contains , and is therefore a neighbourhood of . The result then follows

| (25) | ||||

Finally, we prove the statement: has a local minimum at has a local minimum at .

From the definition of a local minimum, there exists a neighbourhood of , such that

| (26) |

By assumption is a submersion and therefore a continuous open map. Because is an open set containing , must also be an open set containing . Finally, then

| (27) | ||||

∎

Theorem 2.

For any local minimiser of , that is a local minimiser of s.t.

Proof.

s.t. . The result then follows from Theorem 1. ∎

Theorem 3.

has a local maximum at if and only if has a local maximum at

Proof.

This follows from Theorem 1 by symmetric arguments. ∎

Theorem 4.

has a saddle point at if and only if has a saddle point at

Proof.

First, we prove the following statement: has a critical point at has a critical point at .

Let and be represented as co-ordinates for some charts at those points, with , , defined similarly. Then the statement about critical points can be expressed as follows

| (28) |

where is a vector of zeros. To show that , we have

| (29) |

where is the transposed Jacobian of (see Appendix A for an explanation of this notation) and has full column rank due to being a submersion, and so:

| (30) |

For the other direction, , trivially,

| (31) | ||||

Having proven correspondence of critical points, we can proceed to prove the theorem statement in two parts.

First, if has a saddle point at , then must have a critical point at . However, from Theorems 1 and 3, we know that this cannot be a local minimum or local maximum, and hence must be a saddle point.

Second, in the other direction, if has a saddle point at , then has a critical point at , which by similar reasoning must also be a saddle point. ∎

Theorem 5.

If has a non-strict saddle point at then has a non-strict saddle point at

Proof.

From Theorem 4, we know that if has a non-strict saddle point at , then must have a saddle point at . It remains to be proven that the saddle point at must be a non-strict saddle point. We do this by contradiction. Let us assume that the saddle point of at is strict.

Let , be represented as co-ordinates for some charts at those points, with , , defined similarly. Furthermore, let , be the Hessians of and , at and , respectively. Then,

| (32) | ||||

where is the Hessian of the -th component of . The second equality follows from being a critical point of .

A strict saddle point is a saddle point for which there is at least one direction of strictly negative curvature, and so given the assumption that is a strict saddle point of , such that . Let , where is any left inverse of . Then:

| (33) | ||||

| (34) | ||||

implying that is a strict saddle point, a contradiction, and so we conclude that the saddle point at cannot be strict. ∎

Appendix C ALGORITHM 1: SNGD

In Algorithm 1, restated with line numbers below, we provide pseudocode for an implementation of SNGD when is an EF distribution, and are either natural or mean parameters of that family. We assume the existence of an autodiff operator grad, which takes as input a real-valued function, and returns another function for computing its gradient. Note that when cannot be computed deterministically, such as in VI or minibatch settings, we assume grad returns a function that provides unbiased stochastic estimates of the gradient. In our VI experiments, where gradients had to be taken through samples, we used the reparameterisation trick (Kingma and Ba, 2014).

We also assume the existence of an overloaded function dualparams, which converts from mean to natural parameters of the EF, or vice-versa, depending on the type of its argument.555This is purely for convenience, as it allow us to define a single implementation handling both parameterisations. That is, in the notation of Section 2.2, dualparams resolves to either or as appropriate. We note that each dualparams pair only needs to be defined once for each EF, and is not dependent on e.g. the target distribution or loss function, meaning that if these are supplied as part of a software library, the end user is only required to supply , and . Algorithm 1 also assumes a given step size schedule, but can easily be extended to incorporate line search or other methods for choosing .

On line of Algorithm 1 we define a reparameterisation of in terms of the dual parameters. That is, if are natural parameters, is a function of mean parameters, and vice-versa. Line computes the natural gradient, given by equation (5) or (6), using automatic differentiation of the function . Note that both overloads of dualparams are called: one inside the auto-differentiated function , and the other outside (to compute its argument). It is often possible for the inner conversion to be elided; for example, the user can supply a function (instead of ) that can perform the map from dual parameters to directly, more efficiently than the composition . For example, this is often the case when depends on covariance-like parameters and the composition would otherwise involve inverting a matrix twice (a no-op).

If are mean parameters of , then the computational overhead of Algorithm 1 (relative to GD in ) is approximately , where cost returns the cost of its function argument. Similarly, if are natural parameters, then the overhead will be approximately . The factor of 3 in the second term in each case results from taking gradients through ; however, as discussed above, it is often the case the composition is almost zero cost, in which case this term can be largely eliminated by implementing directly.

We have assumed here that we can take gradients through either or efficiently, depending on the choice of parameterisation. For this is true by assumption for tractable families. For some families the ‘reverse’ map , is not available in closed form, but can be efficiently computed using an iterative optimisation procedure (Minka, 2000, 2002). In such cases, we can use implicit differentiation techniques to efficiently compute gradients (Christianson, 1994, Blondel et al., 2022).

Appendix D ALGORITHM 2: SNGD WITH AUXILIARY PARAMETERS

In Algorithm 2 we provide pseudocode for the extension of Section 3.4, in which we augment with auxiliary parameters . are optimised using natural gradients, whereas are optimised with standard first-order methods. Algorithm 2 uses GD with a fixed learning rate schedule for , but the extension to any first-order optimiser is straightforward.

The structure of Algorithm 2 is largely the same as that of Algorithm 1. One notable difference is that now has 2 arguments, and so the call to grad on line 4 returns a function that returns a 2-tuple of gradients, one for each argument.

Appendix E EXPERIMENT DETAILS

In this appendix we provide additional details about the experiments presented in the main paper.

We repeated all experiments with 10 different random seeds. In all cases this led to different random parameter initialisations. For VI experiments, this also seeded randomness in the Monte Carlo samples, and for experiments with minibatching, it also seeded randomness in the minibatch sampling. The mean and standard errors as displayed in the training curves and Pareto frontier plots were computed over the 10 runs. For VI experiments we used the reparameterisation trick to estimate gradients for each method (Kingma and Welling, 2014).

In experiments that were small scale and had objectives that could be computed deterministically, namely MLE experiments using the sheep and COVID datasets, we used exact line search to determine step sizes for each of the methods being tested. This allowed us to compare the search direction of each method without confounding results with choice of hyperparameter settings.

For all other experiments we chose hyperparameters using a grid search. The training curves in the main paper correspond to the ‘best’ hyperparameter settings for each method. The best setting was considered to be that which had the best average (across time steps) worst case (over random seeds) value of the evaluation metric (negative elbo or negative log-likelihood as appropriate). Although this choice is somewhat arbitrary, we found that it consistently chose settings with training curves that closely resembled those that we considered best for each method. In Appendix G we provide Pareto frontier plots which incorporate all of the hyperparameter settings tried, which qualitatively are very similar to the training curves in the main paper.

For SNGD we chose to be mean parameters of for all MLE tasks, and natural parameters for all VI tasks. These choices were motivated by the results of Appendix J, and we found them to consistently perform better than alternatives.

All experiments were executed on a 76-core Dell PowerEdge C6520 server, with 256GiB RAM, and dual Intel Xeon Platinum 8368Q (Ice Lake) 2.60GHz processors. Each individual optimisation run was locked to a single dedicated core. Implementations were written in JAX (Bradbury et al., 2018)

Next we provide details specific to each task featured in the experiments. In the list below, denotes the number of training observations, and denotes the dimensionality of the distribution that is being optimised in the task.

Sheep

(=82, =1) Taken from a seminal work on the negative binomial distribution by Fisher (1941), this dataset consists of the number of ticks observed on each member of a population of sheep. The task for this dataset was MLE of the negative binomial distribution.

UCI miniboone

(=32,840, =43) Taken from the MiniBooNE experiment at Fermilab, this dataset consists of a number of readings that can be used to classify observations as either electron or muon neutrinos (Roe, 2010).666Licensed under a Creative Commons Attribution 4.0 International (CC BY 4.0) license. We follow the pre-processing of Papamakarios et al. (2017). Using this dataset we performed MLE of skew-normal and skew- distributions. We used 32,840 of the observations for training, and the remaining observations for evaluation. We used a minibatch size of for each method.

UCI covertype

(=500, =53) This dataset classifies the forest cover type of pixels, based on 53 cartographic variables (Blackard, 1998).777Licensed under a Creative Commons Attribution 4.0 International (CC BY 4.0) license. We used the ‘binary scale’ preprocessing of Chang and Lin (2011). The task was to perform VI in a Bayesian logistic regression model, with regularisation parameter 1.0. We found that using anything close to the full number of observations resulted in degenerate posteriors with virtually zero uncertainty, obviating the need for variational inference, and so we used a randomly chosen subset of observations for our experiments. We used skew-normal, skew- and skew-normal mixture distributions as approximate posteriors. All methods used Monte Carlo samples for training and for evaluation.

FTSE 100 stock returns

(=1,515, =93) This dataset consists of daily stock price returns from 2017/01/01 to 2022/12/31 for the subset of FTSE 100 stocks that were members of the index during the entire period.888Downloaded from the Bloomberg Terminal. We first fitted univariate Student’s distributions to each dimension independently, and then transformed the data by converting each observed variable to its quantile value under the marginal distribution. The task was then MLE of a copula on the quantile values.

COVID hospital admissions

(=1,120, =1) This dataset consists of the number of daily COVID hospital admissions in the UK from 2020/4/1 to 2023/5/1.999Downloaded from https://coronavirus.data.gov.uk and licensed under the Open Government License v3.0. The task for this dataset was MLE of a 5-component negative binomial mixture.

Synthetic 2D logistic regression

(=30, =2) This synthetic logistic regression dataset was generated using the same procedure as Murphy (2012). The task was VI in a Bayesian logistic regression model, with regularisation parameter 1.0. We used a skew-normal mixture approximate posterior, with Monte Carlo samples for training and for evaluation.

Now we provide details particular to the distributions being optimised in the tasks above. Note that the correspondence between tasks (above) and target distributions (below) is many to many: some target distributions were applied to more than one task, and some tasks were used for several target distributions. The parameter mappings used for SNGD are given in Table 2 in Appendix F; we do not repeat them here unless additional explanation is required. When the parameter mappings make use of the auxiliary parameter extension of Section 3.4, we used Adam to optimise .

With our baseline methods, when a target distribution required a positive definite covariance matrix parameter, we tried two different parameterisations; covariance square-root (e.g. and precision square-root (e.g. (Salimbeni et al., 2018). This parameterisation choice was determined by a hyperparameter which we included in our grid search. Further parameterisation details are given below.

Negative binomial

The PMF of the negative binomial with parameters is given by (14). We initialised negative binomial parameters for all methods by drawing , . With GD, BFGS and NGD we used a log parameterisation of , and a logit parameterisation of . For SNGD we chose to be mean parameters of . In order to ensure that , we require , therefore we chose as the subset of (the mean domain of ) for which . It can be shown that this remains a convex open set.

Skew-normal

The PDF of the multivariate skew-normal with parameters is given by , where is the PDF of the -dimensional normal distribution, and is the CDF of the standard normal distribution.101010Equation (5.1) of Azzalini (2013). We used random initialisations of , , with initialised to .

Skew-

The PDF of the multivariate skew- with parameters is given by , where is the PDF of the -dimensional Student’s , is the CDF of the (univariate) Student’s , , , and .111111Equation (6.24) of Azzalini (2013). We used random initialisations of , , with and initialised to and respectively. For all methods we parameterised as .

copula

The -dimensional copula with parameters has PDF , where is the PDF of the univariate Student’s . We initialised to , and to , where , and projects a covariance matrix to its implied correlation matrix. For all methods we parameterised as .

Negative binomial mixture

The negative binomial mixture with components and parameters has PMF given by (16), where is the negative binomial PMF given by (14) with parameters . We initialised to , and the component negative binomials were initialised to have mean and variance , with and where and is the maximum value observed in the training data. With GD and BFGS, we used a softmax parameterisation of the mixture probabilities, a log parameterisation of , and a logit parameterisation of .

Skew-normal mixture

The skew-normal mixture with components and parameters has PDF given by (16), where is the skew-normal PDF with parameters . We initialised , with the remaining parameters initialised equivalently to the single-component skew-normal case. With Adam, we used a softmax parameterisation of the mixture probabilities.

Appendix F PARAMETER MAPPINGS

In Table 2 we provide parameter mappings for all of the examples appearing in this paper. For convenience, we express the mappings in terms of the standard parameterisation of . For the method described in Section 3.1, would be the mean or natural parameters corresponding to the parameters stated here, with similarly adjusted. Note that in Table 2 we also follow convention by using to denote the mean of a normal distribution, whereas in the main paper it refers to the mean parameters (expected sufficient statistics) of an EF distribution. See Appendix E for target distribution definitions.

| TARGET | SURROGATE | ||||

|---|---|---|---|---|---|

| Neg. bin. | Gamma | ||||

| Neg. bin. mix. | Gamma mix. model | ||||

| Skew-normal | Normal | ||||

| Skew-normal mix. | Normal mix. model | ||||

| Skew- | Normal | ||||

| Elliptical copula | Zero-mean normal | 121212 projects a covariance matrix to its implied correlation matrix. See Appendix E for its definition. |

Appendix G ADDITIONAL RESULTS

In this appendix we provide additional results for the experiments presented in the main paper. In several of the experiments, those not using line-search, the competing methods were dependent on hyperparameters which were chosen by grid search. For the training curves in the main paper, we used the heuristic method described in Appendix E in order to choose the ‘best’ settings for each method.

In order to provide a more complete comparison, in Figures 9 through 13 we present Pareto frontier plots that show the best (average) value of the chosen metric ( axis) attained by any learning rate setting for each method, as a function of both iteration count and wall-clock time ( axis). The displayed error bars correspond to 2 standard errors, computed for the optimal setting at the corresponding point in time.

Appendix H CHOOSING EFFECTIVE SURROGATES

In order to apply SNGD to a given target distribution , we must choose a surrogate , and reparameterisation . Appropriate choices here determine the effectiveness of SNGD.

One guiding principle that can be used is based on a view of NGD involving Kullback-Leibler (KL) divergences. The KL divergence from continuous131313The discrete KL divergence is defined similarly, with summation replacing integration. distribution to is defined as

| (35) |

The NGD direction can be motivated by a result due to Ollivier et al. (2017), restated here in our notation.

Proposition 1.

Let be a smooth function on the parameter space . Let be a point where does not vanish. Then, if

| (36) |

is the negative direction of the natural gradient of (with the Fisher norm), we have

| (37) |

where .

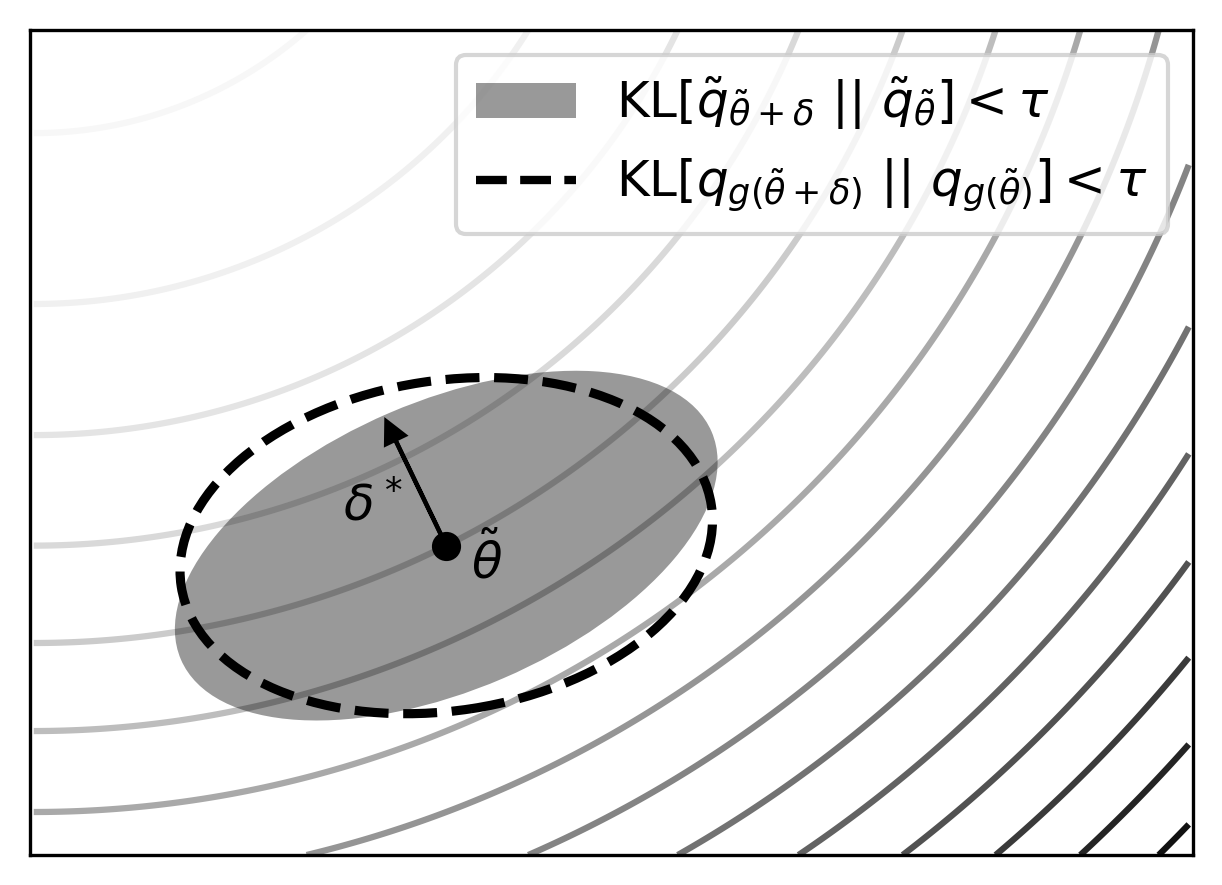

In words, this says that NGD moves in the direction in parameter space that gives the greatest decrease in the objective within an infinitesimally small KL-ball around the current point.

This suggests that we would ideally like to find and such that the KL divergence between the surrogate and a perturbed version is identical to the KL divergence from the target and its corresponding pertubation , for any small pertubation . However, because this is only required to hold in some infinitesimally small neighbourhood of , it is sufficient to satisfy

| (38) |

If equality (38) holds then SNGD will move in the same direction in as ‘exact’ NGD under (reparameterised) . While it will not typically be possible to find tractable surrogates for which equality holds exactly, this observation motivates choosing , for which it is approximately true. We illustrate this in Figure 14. This perspective also illustrates why and do not need to be distributions over the same space; all that matters is that the effect of (small) changes in on and is similar in a KL-divergence sense. If approximating NGD under is our goal, then this perspective can help guide us toward a choice of and .141414Approximating NGD under should not necessarily be our ultimate goal. We elaborate on this in Appendix I.

As a concrete example, let be a mixture distribution, with PDF given by

| (39) |

where are the component distributions, , and . Let us consider as a surrogate for the corresponding mixture model (joint distribution) with PDF

| (40) |

where , so that is simply the identity map, and . Using standard identities, we have

| (41) | ||||

| (42) | ||||

It follows that using a mixture model joint, as a surrogate for its marginal, can be viewed as using an approximate metric which includes an additional term. This term imposes an additional penalty on directions in parameter space that affect the expected responsibility distributions.151515The responsibility of component for is the probability that was generated by component having observed . In the experiments of Section 4.4 we take this approximation one step further, and use EF mixture models as surrogates for mixtures with components that are not EF distributions.

As an aside, we note that Lin et al. (2019) performed NGD with respect to a joint distribution in a VI objective for which the optimisation target was a marginal of the NGD distribution. This mismatch was not explicitly discussed by Lin et al. (2019). However, it is clear that this aspect of their method can be interpreted as an application of SNGD, and similar reasoning to that above shows that it implies making a specific approximation to the Fisher metric.

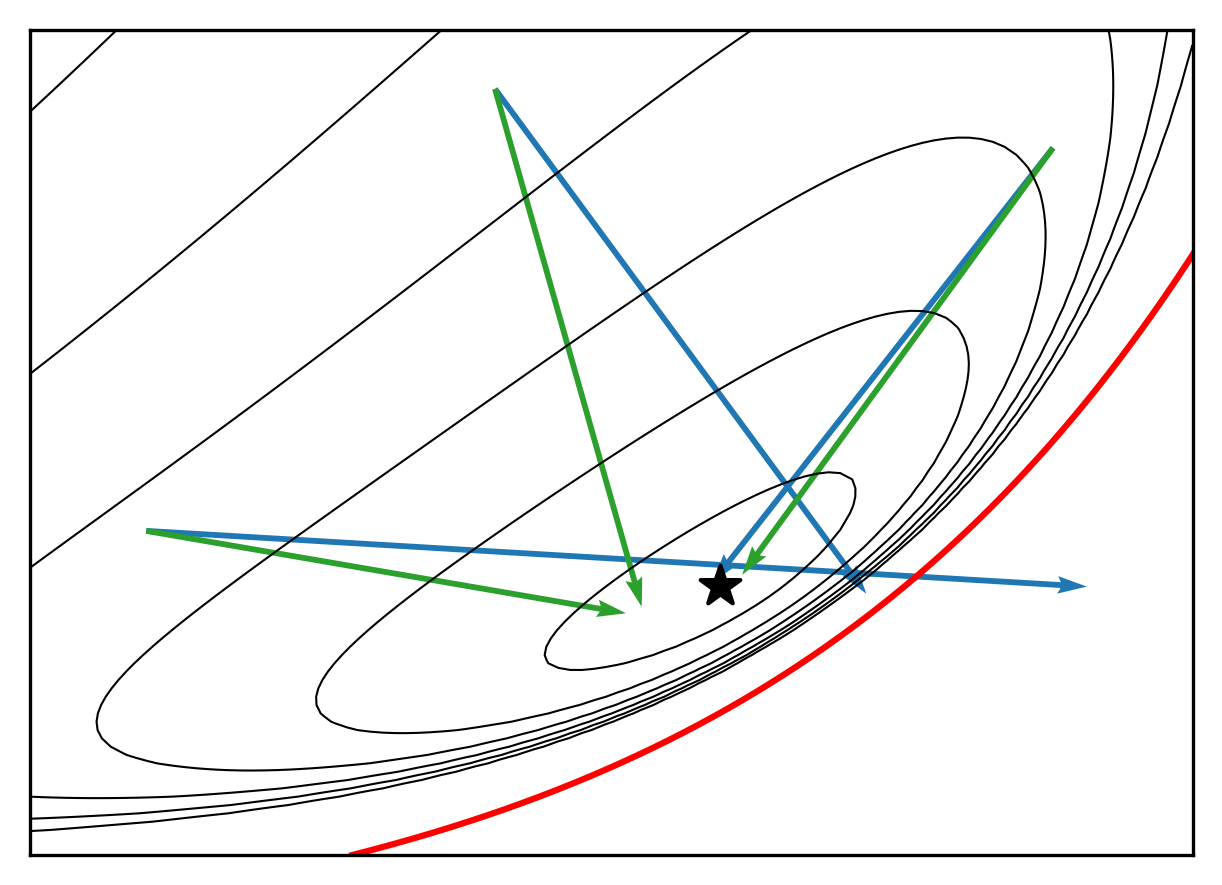

Appendix I COMPARISON WITH NGD UNDER

In Appendix H we provided a motivation for SNGD that viewed it as approximating NGD under a reparameterisation of . However, for the negative binomial MLE experiment of Section 4.1, we demonstrated that SNGD was actually able to outperform NGD under . In Figure 15, we show that this was true when NGD was performed with respect to both a standard parameterisation (also shown in Figure 1), and the reparameterisation defined by . This implies that the outperformance of SNGD is not simply an artefact of the reparameterisation. This surprising result deserves extra scrutiny.

We begin by highlighting that in fact, SNGD is NGD, but in the objective and with respect to distribution . It is helpful therefore to consider the desirable properties of NGD:

-

1.

It is locally invariant to parameterisation of the distribution being optimised.

-

2.

It follows the direction of steepest descent in the objective on the statistical manifold of the distribution being optimised.161616Where steepness is defined with respect to a KL divergence.

-

3.

For MLE objectives, it asymptotically approaches Newton’s method near the optimum.

Properties 1 and 2 apply always, and so they are necessarily inherited by SNGD. However, when is a MLE objective for (as in the experiment of Section 4.1), is not, in general, an MLE objective for , and so SNGD loses property 3. Contrast this with NGD in with respect to : although the objective function is the same as that of SNGD, it is simply a reparameterised MLE objective for , and so property 3 is retained. In other words, the asymptotic efficency of NGD is retained under change of parameterisation, but not under change of distribution.

On the face of it, then, when is a MLE objective for , SNGD appears less desirable than NGD under , inheriting only two of the properties listed above. However, none of these properties tell us anything about performance over large (or indeed, any non-inifinitesimal) steps in parameter space. But there is one special case in which we can say something about the performance of NGD over large steps in parameter space: when NGD is applied to a MLE objective of an EF distribution with respect to the mean parameters of that distribution, a single undamped step will converge straight to the optimum (see Theorem 6 in Appendix J).

When we apply SNGD with EF , and with respect to mean parameters , we meet 2 of the criteria for single-step convergence. Although is not in general a MLE for , if it behaves approximately like a MLE objective for , then SNGD can make rapid progress over large distances in parameter space, and approximately converge in a single step. And so, while SNGD loses the asymptotic efficiency of NGD under , it is possible to obtain improved performance in the early to mid stages. This is exactly what we observe in the experiment of Section 4.1, as is further illustrated in Figure 16.

The ability to make rapid progress early on is arguably more important for the overall performance of an optimiser in practice; however, if convergence to an exact (within machine precision range) optimum is required, it may be beneficial to switch to Newton-type methods during the late phase, an approach previously proposed by Tatzel et al. (2022).

We now attempt to characterise what it means for to behave approximately like a MLE for . Let be an EF with mean parameters . Furthermore, let be an MLE objective for so that

| (43) | ||||

where is the empirical density function. Using a trivial identity, we can rewrite this as

| (44) | ||||

where are optimal parameters of , and we have defined

| (45) |

and

| (46) |

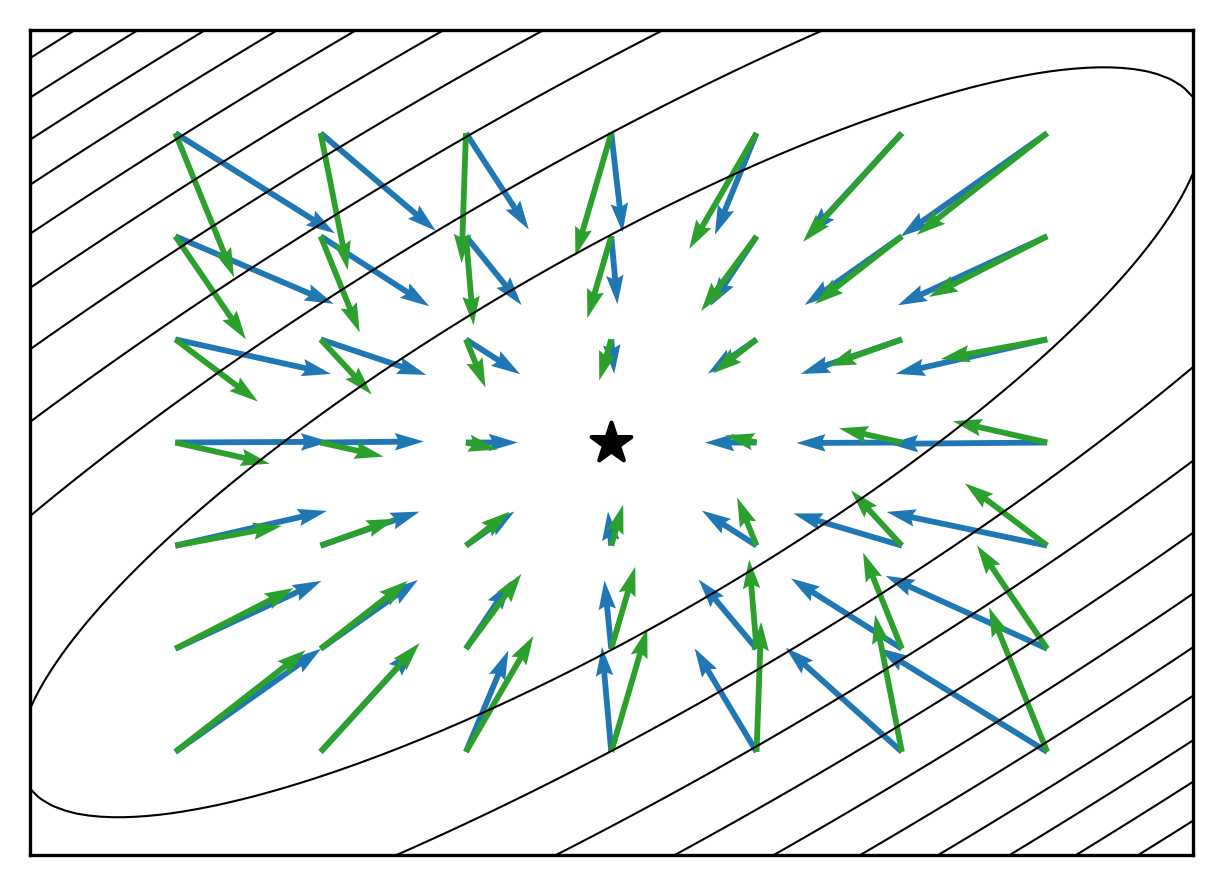

can be minimised by a single NGD step with respect to and (Theorem 6). The second term, , can then be seen as distorting the natural gradient step, acting to move it away from the optimum . If is (approximately) constant with respect to , then SNGD will (approximately) converge in a single step.

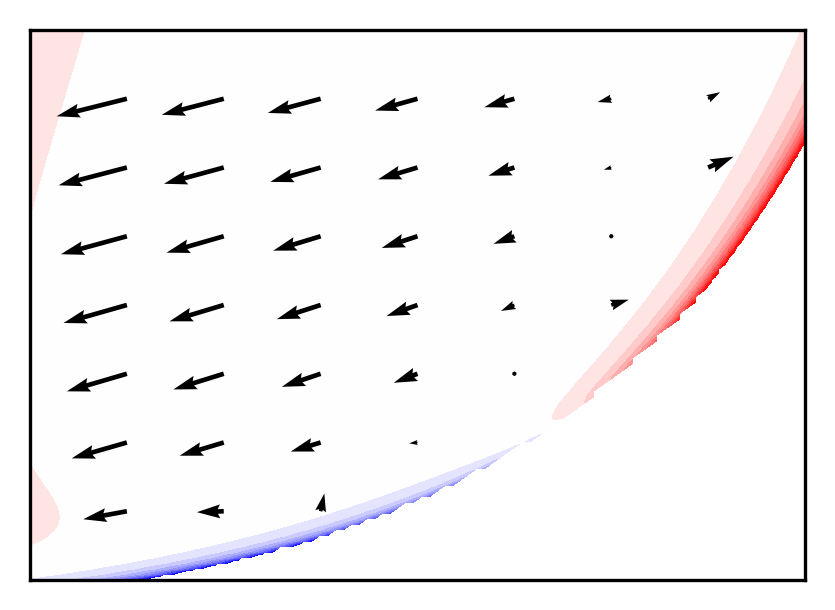

In Figure 17(a) we show that in the sheep experiment of Section 4.1, the effect of the distortion term is indeed small, even when far from the optimum, illustrating why SNGD is able to make rapid progress on this problem.

To add some intuition behind , let us assume that the data were generated from the model distribution with parameters . Furthermore, take the infinite data limit,171717We do this for convenience; for finite samples, the resulting expressions hold in expectation (over random data sets). so that

| (47) |

and . The distortion term can then be written as

| (48) | ||||

where is constant with respect to . For to be roughly constant, we then require

| (49) |

This is similar to the statement expressed by equation (38), concerning the effect of on reverse KL divergences between nearby points, whereas now we have a statement about the effect of on forward KL divergences from the (potentially distant) optimal point.

Appendix J EF NATURAL GRADIENTS

When NGD is applied to objectives involving a KL divergence (or related quantity), it has special properties when it is performed with respect to either the natural or mean parameters of an EF distribution, as the following theorems show.

Theorem 6.

For EF with mean parameters , and mean domain , let

| (50) |

where is any distribution with , and is constant with respect to . Then, , we have

| (51) |

Proof.

First, let be dually coupled with , so that . From (6), we have that

| (52) | ||||

where we have used the standard EF identity . It remains to show that . Let us reparameterise as , then

| (53) | ||||

and equating to zero, we find the unique stationary point at . To show that this is a minimum, note that

| (54) |

Given that is strictly convex and twice-differentiable (see Wainwright and Jordan (2008)), then is also strictly convex, and so must be minimised when . ∎

Theorem (6) says that (undamped) NGD with respect to the mean parameters of EF will converge in a single step when the objective is a cross entropy from any distribution to plus a constant that does not depend on . Two straightforward corollaries of this are that NGD also has single step convergence when (a forward KL divergence), or when (a MLE objective).

Typically, when performing MLE of an EF distribution, we simply think of it as ‘solving’ for the parameters, or ‘moment matching’; Theorem (6) shows that actually, this is equivalent to performing (undamped) NGD with respect to .

There is an almost-symmetry regarding NGD with respect to the natural parameters of , as the following theorem states.

Theorem 7.

For EF with natural parameters , and natural domain , let

| (55) |

where is from the same EF as with natural parameter . Then, , we have

| (56) |

Proof.

First, let be dually coupled with , so that . From (5), we have that

| (57) | ||||

where: denotes the EF distribution with mean parameter ; , the convex dual of A, is the negative entropy of ; and we have used the identity . It is clear from the properties of the KL divergence that must be the unique minimiser for . ∎

Note that Theorem 7 requires to be from the same family as , which is not the case for the corresponding result with respect to mean parameters. This is a generalisation of a result found in Hensman et al. (2013), Salimbeni et al. (2018) for sparse Gaussian process VI. It is similar to to a result given by Sato (2001) for variational Bayes. Note that an analogous result to Theorem 7 can be derived for any Bregman divergence in the same manner.

Appendix K EF MIXTURE MODELS

An EF mixture with components has density

| (58) |

where are the mixture probabilities with , and are the natural parameters of mixture component . We can also define a related mixture model, a joint distribution in which we consider the mixture identity as a latent variable, with density

| (59) |

A finite EF mixture is not, in general, an EF. However, the corresponding mixture model (joint distribution) is an EF. Consider its density,

| (60) | ||||

where is an indicator function for the singleton set . We can then recognise (60) as having the form of an EF density with: base measure ; log-partition ; and sufficient statistics and natural parameters as listed in Table 3. Note that the statistic functions are linearly independent, and so the EF defined by (59) is minimal.

| Sufficient statistic | Natural parameter |

| … | … |

| … | … |