Conservative Predictions on Noisy Financial Data

Abstract.

Price movements in financial markets are well known to be very noisy. As a result, even if there are, on occasion, exploitable patterns that could be picked up by machine-learning algorithms, these are obscured by feature and label noise rendering the predictions less useful, and risky in practice. Traditional rule-learning techniques developed for noisy data, such as CN2, would seek only high precision rules and refrain from making predictions where their antecedents did not apply. We apply a similar approach, where a model abstains from making a prediction on data points that it is uncertain on. During training, a cascade of such models are learned in sequence, similar to rule lists, with each model being trained only on data on which the previous model(s) were uncertain. Similar pruning of data takes place at test-time, with (higher accuracy) predictions being made albeit only on a fraction (support) of test-time data. In a financial prediction setting, such an approach allows decisions to be taken only when the ensemble model is confident, thereby reducing risk. We present results using traditional MLPs as well as differentiable decision trees, on synthetic data as well as real financial market data, to predict fixed-term returns using commonly used features. We submit that our approach is likely to result in better overall returns at a lower level of risk. In this context we introduce an utility metric to measure the average gain per trade, as well as the return adjusted for downside-risk, both of which are improved significantly by our approach.

1. Introduction

Machine-learning (especially deep learning) techniques have achieved close to human-level performance in many domains such as image processing and natural language understanding. However, the same cannot be said in the case of trading in financial markets: It has been observed that expert human traders consistently outperform others, thus in some sense negating the efficient market hypothesis, and also indicating that there is expertise involved, presumably at recognizing and acting on recurring patterns, even if ephemeral.

There have been many reports of attempts to apply machine-learning and deep-learning techniques for prediction and trading in financial markets, as we shall review later in Section 6. Nevertheless, in practice these are all plagued by the fact that financial markets are noisy. Thus, even if there are ephemeral patterns in the data that are discovered by machine-learning techniques in spite of this noise, when applied the models still often result in erroneous predictions, again due to noise. If one were to believe the efficient market hypothesis, there would be no signal and only noise, and no model could succeed consistently.

Some techniques to deal with noisy data in deep-learning have relied on custom loss functions (Qin et al., 2019), (Patrini et al., 2017), as well as training procedures such as bootstrapping’ (Reed et al., 2014), where data points that train slowly are presumed to be noisy and their labels replaced with predictions of other similar but likely less noisy points.

The problem of noise in the data has been recognized historically in machine-learning: The CN2 rule-learning algorithm (Clark and Niblett, 1989) was developed to combat noise by learning a sequence of high accuracy rules that would apply only on a fraction of data, i.e., some data points would have no applicable rule. Such cases could be handled in a domain-specific manner, e.g., by predicting the majority class, making a random choice, or, more appropriate to risky situations such as trading in financial markets, by refraining from making a prediction. In the context of a trading system relying on such a model, no trade would be taken if the model refused to make a prediction.

The relative benefits of relying on simple rules when dealing with financial market data has been highlighted in (Dhar, 2011), where it is argued that more complex models only end up fitting the noise in such data.

We are motivated by the following ideas from the above prior works: (i) using simpler rule-based models as advised in (Dhar, 2011), (ii) learning a sequence of models trained on recursively smaller subsets of data as in CN2 and (iii) refraining from making a prediction any of the sequence of models are inapplicable.

Our approach involves learning a cascade of models in sequence, with each successive model being trained on data on which the previous models are under-confident, as measured by the Gini index of the predicted class distribution for each data point. Cascaded training continues as long as the accuracy obtained on data where the model is confident are above a minimum desired value. We use a three level cascade in our experiments that appears to work well. Finally, we report accuracy on the remaining ‘un-pruned’ data points as well as the support, i.e., fraction of data that the model makes confident predictions on.

Since we found that hard-decision rule-based models as learned by RIPPER performed poorly on our datasets, we employ differentiable decision trees (DDT) as introduced in (Suarez and Lutsko, 1999) and used in a deep-learning context by (Silva et al., 2020). We also used traditional MLPs in our cascaded learning approach, and compare these with DDTs.

We report experimental results on real market data as well as synthetic data created to mimic a simplistic mean-reverting market behavior using sine waves. Varying levels of noise are added to this synthetic data to study whether using a cascade of models improves accuracy with acceptable support.

Note that in a financial market scenario, it is preferable to have a model with 70% or even 60% accuracy on say 20% or even 10% of the data, on which it makes confident predictions, and abstains on the balance, as this serves to minimise risk in any decisions taken based on the model’s predictions. Further, it is more useful to have confident predictions at the extremes of the target attribute’s distribution: Such predictions are actionable (as opposed to confidently predicting placid market behaviors), and we define utility of predictions as a metric to measure actionability in the above sense.

Utility measures the average gain per trade; thus, higher utility model recommends fewer, albeit successful, as well as less risky trades. We also compute a measure of the return adjusted for downside risk. Our experimental results show that using a cascade of models indeed achieves this effect especially on synthetic data, with DDTs resulting in higher support at comparable accuracy to MLPs, and higher utility as well as risk-adjusted return. On real-data, while both models perform relatively poorly with respect to the final support, we observe that their predictions, however rare, nevertheless exhibit higher utility and risk-adjusted return, and are therefore actionable with lower level of risk. Finally we discuss how this behaviour can be exploited in the context of financial trading strategies.

2. Methods: Algorithm & Models

2.1. Differentiable Decision Trees (DDT)

Decision Trees have long been used to generate interpretable models for tabular datasets and perform well with classification problems. However, despite the numerous algorithms developed to produce near optimal decision trees, they still are highly sensitive to their training set. Deep Neural Networks (DNN) or Multi-Layer Perceptrons (MLP), on the other hand are analytic in nature and thus can be optimised to produce good results on both regression and classification problems. However, this comes at a cost of interpretability.

Suarez and Lutsko (Suarez and Lutsko, 1999) proposed a modification to the ‘crisp’ decision trees formed by the CART algorithm. They replaced the hard decisions taken at each node with ‘fuzzy’ decisions, determined by the sigmoid function. The leaf nodes are modified to represent a probability distribution over the classes. This allows the fuzzy decision tree or ‘differentiable decision tree’ to be trained with gradient descent like a multi-layer perceptron.

Further work by Frosst and Hinton (Frosst and Hinton, 2017) introduced a regularization term to encourage a balanced split at each internal nodes. The differentiable decision tree model used in the experiments is a combination of these ideas from previous works.

2.1.1. Forward pass and optimization

The decision tree is initialized as a balanced binary tree, with the depth fixed before-hand. The model works in a hierarchical manner, with each inner node having its own weight and bias while the leaf nodes have a learned distribution . At each inner node , the probability of taking the right branch is given by the sigmoid function:

To prevent the decisions from being too soft, temperature scaling () is added to the sigmoid function as follows:

At each inner node the path probability up until that node is given by . This value is then multiplied by for the right branch and for the left branch which get passed down as the path probability for that node. The final output is calculated as a weighted sum of the probability distributions of all the leaves:

where is the path probability at leaf node . The cross-entropy loss on this output is used for the optimization of the model. Applying the softmax function on gives us the probability for each class.

denotes the probability of class while is the element in the output p. The cross-entropy is minimized by gradient descent to train the parameters as well as the scaling parameter .

2.1.2. Regularization:

The DDT tends to get stuck in a local minima quite often, with one path getting much higher probabilities than the others, which results in the model favouring one leaf over the others for most of the predictions. To solve this issue, Frrost and Hinton (Frosst and Hinton, 2017) introduced a regularization term which makes the inner nodes make a more balanced split. At each inner node an term is calculated:

The penalty summed over all the terms is:

where varies as where is the depth of the node.

2.2. Cascading Models

We introduce a method in which the model makes selective predictions, and chooses to not predict on some part of the data when it’s not confident about its prediction. We start with a classification model, which outputs probabilities of the classes, such as an MLP or DDT. The more imbalanced the probabilities, more confident the model is on it’s predictions. We use Gini Impurity to calculate the imbalance in the probabilities:

The lower the gini impurity, greater the imbalance in the probability distribution of the classes. We set a value to be the maximum admissible impurity in the predictions, and the model is confident on the ones with lower impurity.

The expectation is that the model would ideally give a much higher accuracy on the subset of the predictions (support) on which it is confident. However, in cases of very noisy data, this support can be very low. Therefore we use Cascading Models, which helps to increase support on the predictions while maintaining a high test set performance. The data-points on which we encounter high impurity values are pruned, i.e. the model doesn’t make any prediction on those points. These data-points act as the train or test set for the next model. Finally, accuracy of all the models is only calculated for data-points on which it makes a prediction. The training procedure is described in Algorithm 1:

During testing, given a sequence of models, each data-point passed through the sequence, with each model either making a prediction or passing the data-point onto the next model. The test accuracy is calculated solely on the un-pruned points. This method can be used with any classification model which can output a probability distribution over the classes. For the experiments, DDT (differentiable decision trees) and MLP were used. The inference procedure is described in Algorithm 2:

3. Materials: Data & Features

3.1. Market Data

We have used equity price data from the Indian equity market captured as five-minute candles in the standard open, high, low, close and volume form. Data for each ticker (stock) is normalized for each day by the close price of the first candle. Thus, each day starts with a normalised close price of one, with remaining values through the day recorded in multiples of this value.

Further, volume data for each symbol is normalised by its historical average 5-minute volume, computed on a prior year’s data, (i.e., discretisation is not based on volume values in the data itself). As a result, the time-series for each symbol-day pair are on the same scale for the purposes of training machine-learning models.

The OHLCV values are augmented with day information, captured as the number of days since some earlier reference date, and included as an attribute ‘era’.

3.2. Synthetic Data & Noise

Synthetic price data is generated as sine waves, with a different frequency and amplitude for each synthetic day, or ‘era’. Further, amplitude is also allowed to vary during the course of the day as a function of noise, as described later below.

Note that each wave starts at a value of one, and a phase of zero or ninety degrees chosen randomly. As noted earlier, base amplitude and frequency is also chosen randomly for each day.

Next, varying levels of noise are added to each sine-wave, parameterised by two values, base-noise and peak noise computed as follows: Each sine wave has a number of peaks, say , . Points between each zero-crossing are allocated to the intervening peak, defining intervals. Noise is added to each peak as peak noise . Thus, each noisy sine wave of amplitude and peaks is characterized by two additional noise parameters and , and computed as (for t=0 to 1, with the latter corresponding to end of day):

for . If , a noisy ascending or descending straight line is computed as:

Each (noisy) sine wave (i.e., for a day’s worth of synthetic prices) is sampled 375 times, corresponding to one-minute price samples. The time-series thus represents a synthetic trading day of about six and a half hours.

This series is then converted into 75 five-minute OHLC candles, and similarly normalised with the first close value as described earlier for market data. For synthetic data the volume is fixed at one for every candle.

As earlier, these OHLCV values are augmented with day information, in the ‘era’ attribute to distinguish each random selection of frequency and base amplitude.

Note that a synthetic price dataset, as described above, is computed for a number of days (‘eras’) for different noise levels, and each combination.

3.3. Features

We add technical analysis features such as moving averages of price and volume, relative strength index, moving-average convergence-divergence, and Bollinger-bands to the basic OHLCV attributes.

In addition to these standard technical indicators we add logical and temporal features as follows: (i) Differences of selected attributes: open - close, high - low and 20 and 10 window moving averages of price. (ii) Slopes of close values using varying window lengths (3,5,and 10). (iii) ‘Change-length’ for each of the previous logical features as well as for all the base features and technical indicators: Change-length is computed to be the number of consecutive candles, i.e., current and previous five-minute time intervals, in which a feature value is monotonically increasing or decreasing. Change-length is positive if the feature has been increasing and negative if it was decreasing.

Target values, i.e., values to be predicted by machine-learning, are computed as the 10-candle return, i.e., the difference between the normalised close value at time and time (since each candle represents a five minute interval).

Finally, all the features, i.e., OHLCV values, technical indicators as well as the logical and temporal features above, and target values are discretised into 5 bins. Thresholds for discretisation are computed using a prior year’s similar data in manner so as to result in equally populated bins, i.e., a percentile-based binning. For synthetic data, an independently sampled set is used to compute discretisation thresholds. (Thus, any potential discretisation-based information leakage is avoided during machine-learning.)

4. Experiments & Results

The models, standard as well as the cascading MLPs and DDTs are evaluated via 4 experiments for market as well as synthetic data. The experiments evaluate the models on their test set performance for given a combination of train and test data-set. The experiments are as follows:

-

(1)

Training on data from a set of eras and testing on data from the same set of eras.

-

(2)

Training on data from a set of eras but testing on data from a different set of eras.

-

(3)

Training and testing on data from a single era.

-

(4)

Training on data from a single era but testing on data from a different era.

In addition to the above experiments, two experiments were carried out solely on the synthetic data to examine the performance of the models when the noise levels in the train and test data-sets are different.

-

(1)

Training on clean data and testing on noisy data.

-

(2)

Training on noisy data and testing on clean data.

K-fold cross-validation is used to determine the optimal hyper-parameters for each model. The training set used in the first experiment is used in the cross-validation for both data and the same hyper-parameters are used for all the experiments on that set of data (synthetic and market).

4.0.1. Cascading Models:

Two types of models, DDT and MLP were trained using this method. DDT of depth 6 were trained for 500 epochs and MLP of hidden dimensions (128,64,32) trained for 1000 epochs were used. Additionally, for further investigation on the market data, DDTs of depth 4 trained for 1000 epochs and MLP of hidden layers (256,128,64,32) trained for 1000 epochs were also tested. For all the experiments, the maximum admissible impurity was 0.5 and the number of levels of cascading was 3. Using 3 levels, as observed in the experiments, improved the support by as much as 50% or more compared to using a single level.

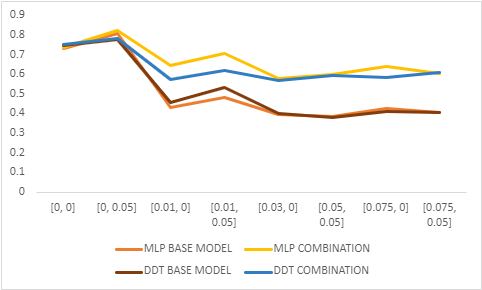

4.1. Training on data from a set of eras and testing on data from the same set of eras

The training data consists of the first 80% data points from each era in the data-set. The test set consists of the latter 20% from each era. These results are tabulated in Table 1 and Table 2.

Unsurprisingly, performances on the test data reduce with an increase in noise. The models are highly reactive to noise addition as observed by the reduction in performance from noise level [0,0.05] to [0.01,0]. However, post this drop, even though the performance decreases, it isn’t as sharp, and accuracy curves are smoother.

The cascaded models offer tangible improvement in test set performance when compared to their single model counterparts. The Cascading MLPs provide test accuracies that are as good as, if not better, than those of Cascading DDTs albeit with a substantially lower support for both train and test sets. This result, however, is reversed for the market data, where the DDTs provide greater accuracy with lower support.

On testing the DDT of depth 4 (trained for 1000 epochs) on the market data, it was found that it gave a slightly better performance with marginally higher support. The extended MLP gives significantly better results than the one used (however the base model performance is lower), albeit with much lesser support.

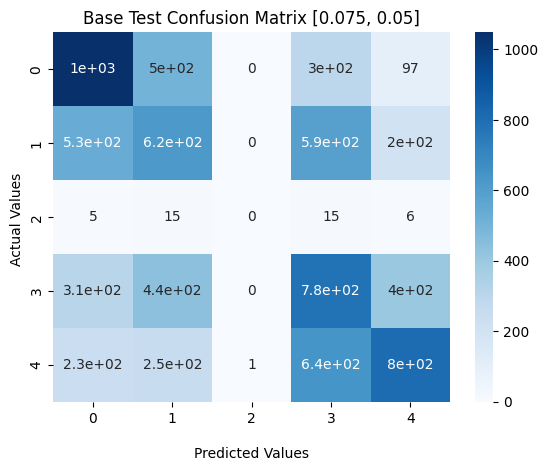

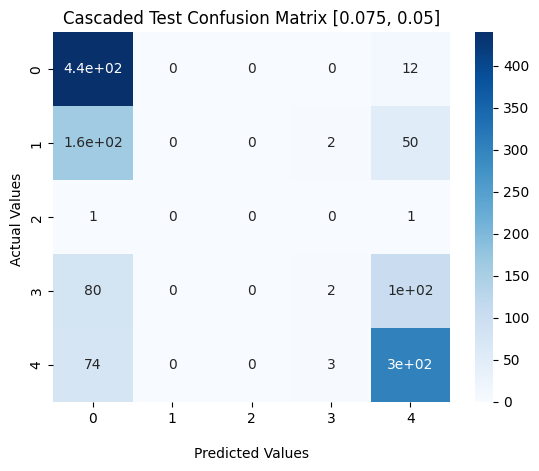

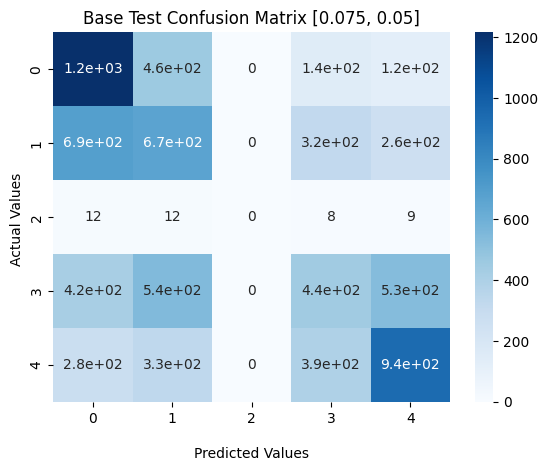

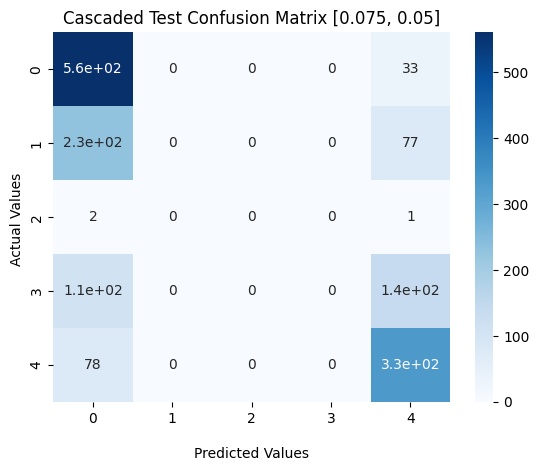

Lastly, the test-time confusion matrices revealed that the predictions made by the cascade of models i.e., predictions on the un-pruned data, lie primarily at the extremes of the target distribution. The implications of this result are further explained in experiment 2 where a similar result was observed.

| Noise | BASE MODEL | COMBINATION | ||||

|---|---|---|---|---|---|---|

| Accuracy | Accuracy | Support | ||||

| Train | Test | Train | Test | Train | Test | |

| [0, 0] | 0.964 | 0.964 | 0.973 | 0.972 | 0.997 | 0.993 |

| [0, 0.05] | 0.926 | 0.866 | 0.957 | 0.897 | 0.96 | 0.954 |

| [0.01, 0] | 0.659 | 0.604 | 0.899 | 0.808 | 0.43 | 0.42 |

| [0.01, 0.05] | 0.71 | 0.676 | 0.858 | 0.775 | 0.677 | 0.69 |

| [0.03, 0] | 0.554 | 0.522 | 0.83 | 0.759 | 0.317 | 0.322 |

| [0.05, 0.05] | 0.551 | 0.485 | 0.818 | 0.726 | 0.296 | 0.288 |

| [0.075, 0] | 0.516 | 0.47 | 0.808 | 0.706 | 0.221 | 0.224 |

| [0.075, 0.05] | 0.546 | 0.457 | 0.81 | 0.738 | 0.237 | 0.23 |

| Noise | BASE MODEL | COMBINATION | ||||

|---|---|---|---|---|---|---|

| Accuracy | Accuracy | Support | ||||

| Train | Test | Train | Test | Train | Test | |

| [0, 0] | 0.933 | 0.931 | 0.959 | 0.962 | 1 | 1 |

| [0, 0.05] | 0.873 | 0.844 | 0.914 | 0.865 | 0.996 | 0.994 |

| [0.01, 0] | 0.599 | 0.562 | 0.903 | 0.877 | 0.306 | 0.302 |

| [0.01, 0.05] | 0.627 | 0.597 | 0.855 | 0.824 | 0.437 | 0.444 |

| [0.03, 0] | 0.515 | 0.504 | 0.917 | 0.923 | 0.174 | 0.158 |

| [0.05, 0.05] | 0.495 | 0.479 | 0.85 | 0.793 | 0.197 | 0.195 |

| [0.075, 0] | 0.467 | 0.455 | 0.778 | 0.707 | 0.155 | 0.158 |

| [0.075, 0.05] | 0.468 | 0.456 | 0.83 | 0.824 | 0.139 | 0.142 |

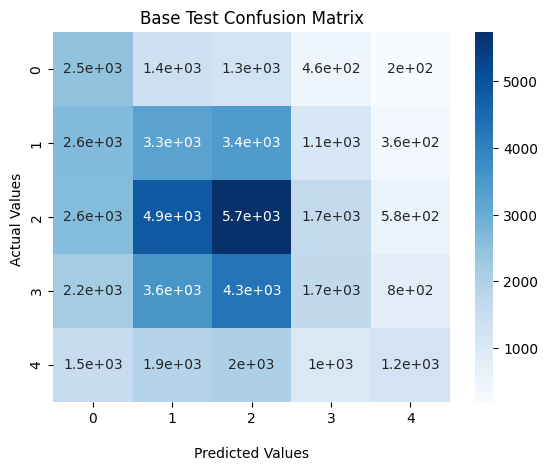

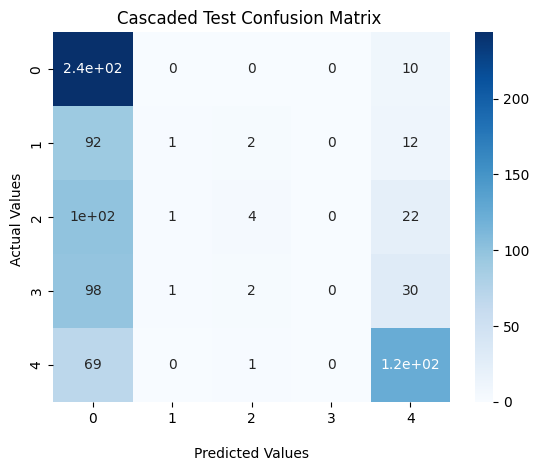

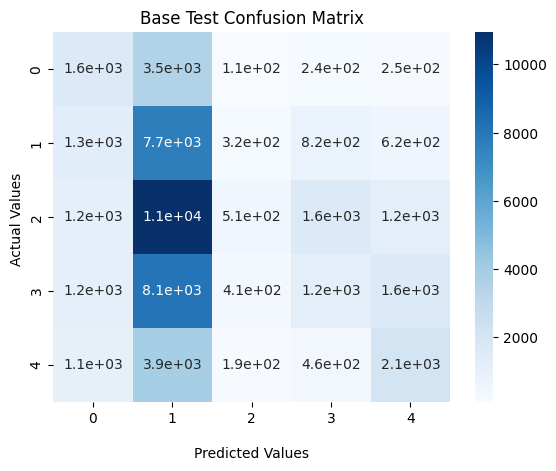

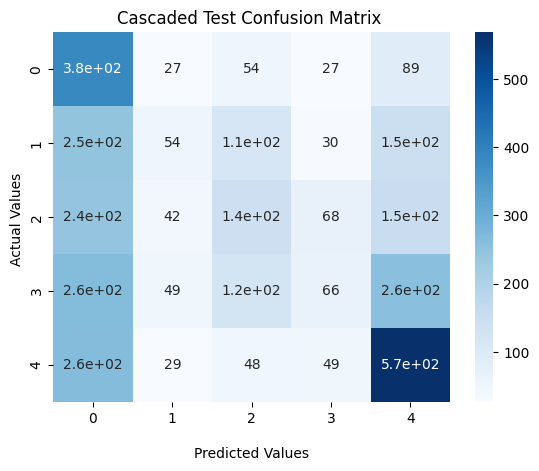

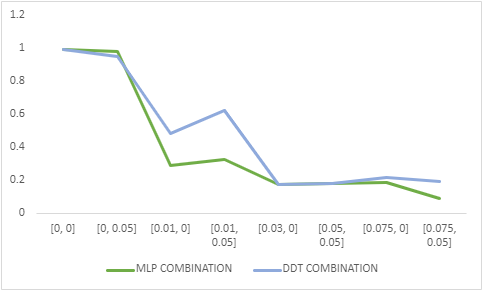

4.2. Training on data from a set of eras and testing on data from a different set of eras

The training set consists of all the data-points from every era in a set. The test set also consists of the same, however, the eras are from a different set and there is no common era between the test and training sets. The number of eras in both sets is equal.

The test accuracies and supports, in this case, are presented as line graphs in Figure 5 and Figure 6. The trend is similar to experiment 1, but the accuracy values are lower. Further, the accuracy level is better maintained across noise levels but leads to diminishing support at higher noise levels. On the real data (Tables 3 and 5), the cascading models don’t provide as much improvement in accuracy and also end up with significantly lower support. The DDT of depth 4 and the extended MLP provided improved results at the cost of lower support as shown in Tables 4 and 6.

Most importantly, observe Figures 1 and 2 that depict test-time confusion matrices for the base and cascaded models on synthetic data as well as Figures 3 and 4 which depict the same but on market data: We observe that most of the data points on which the cascaded models make a prediction, i.e., the un-pruned data, are at the extremes of the target distribution, i.e., predicting classes 0 or 4 as seen in experiment 1. It is important to note that this was not inevitable. It could well have transpired that the cascaded models only chose points in the middle of the distribution, rendering their predictions useless. As it happens, confident and accurate predictions at the extremes are exactly what is desired for making trading decisions, i.e., buy (long) for a prediction of 4 and sell (short) for 0.

| BASE MODEL | COMBINATION | ||||

|---|---|---|---|---|---|

| Accuracy | Accuracy | Support | |||

| Train | Test | Train | Test | Train | Test |

| 0.392 | 0.273 | 0.798 | 0.375 | 0.053 | 0.046 |

| BASE MODEL | COMBINATION | ||||

|---|---|---|---|---|---|

| Accuracy | Accuracy | Support | |||

| Train | Test | Train | Test | Train | Test |

| 0.333 | 0.265 | 0.802 | 0.475 | 0.026 | 0.022 |

| BASE MODEL | COMBINATION | ||||

|---|---|---|---|---|---|

| Accuracy | Accuracy | Support | |||

| Train | Test | Train | Test | Train | Test |

| 0.314 | 0.25 | 0.847 | 0.335 | 0.067 | 0.055 |

| BASE MODEL | COMBINATION | ||||

|---|---|---|---|---|---|

| Accuracy | Accuracy | Support | |||

| Train | Test | Train | Test | Train | Test |

| 0.314 | 0.243 | 0.783 | 0.461 | 0.062 | 0.046 |

4.3. Training on a single era and testing in the same era

The training set in this experiment is the first 80% of the data from a single era and the test set is the remainder of the data. Performances on eras are averaged over the results on a noise level.

Due to lower data-set sizes, the models tend to over-fit the data, with test accuracy on the market data coming to be about 30%, which is much lower than the train accuracies.

The Cascading models also don’t provide much improvement, as the test accuracies on both, synthetic and market data, are almost the same as that of the base model. Due to over-fitting, the model gives low impurities for most of the points as observed by the supports, while pruning, it does not extract the data-points which is more helpful for increasing test accuracy.

4.4. Training on a single era and testing on a different era

In this experiment, O(N) combinations of train and test era are used, where N is the number of eras in each of the two sets in experiment 2. The entirety of the data from the eras is used in the train and test sets. While training performances are usually good, the test accuracy usually depends on the similarity in distribution between the data in the two eras.

4.5. Performance in cases where train and test set have different noise levels

The following experiments were conducted only on the synthetic data to assess the ability of models to extract patterns from the training data and effectively apply it to data at a different noise level.

4.5.1. Training on clean data and testing on noisy data

In this case, the models give low accuracies once noise is added and remain approximately the same for all noise levels. The cascading models don’t improve upon this either. For the MLP, the mean test accuracy is 32.9% and lies in the range (30.8,34.3). For DDTs, the mean is slightly higher at 37.5% and lies in a longer range of (35.1,44). This is due to the model over-fitting on the clean data, which forces it to give predictions with low impurity even with very noisy data which hampers the working of the cascading model.

4.5.2. Training on noisy data and testing on clean data

For the standard ensemble models and the base models, the training accuracy decreases with increasing noise, and the test accuracy remains significantly lower than the train. However, the cascading models offer significant improvement in this case. Here, the Cascading MLPs give significantly better results than the base models, and better results than the Cascading DDTs, which give a lower accuracy but with higher support.

4.6. Utility and Risk-adjusted Return

The confusion matrices formed by the cascading models in experiments 1 and 2 reveal that a major portion lies at the extremes of the target distribution, 0 and 4. These 2 classes generally determine the trading decision to be made at a certain point in time and are highly actionable, making these predictions very useful.

We use a metric to compare the average gain per prediction (utility) of the models before and after cascading. This value is calculated using the points where the predictions are either 0 or 4 (extreme ends of the classes). Since the ‘target’ refers to stock-specific returns, decisions to trade would mainly take place when a target of 0 or 4 is predicted, so we focus only on these two columns. Each pair of predictions and ground truth has a ‘utility’ attached to it. If the ground truth is 2, the utility is 0 regardless of the prediction as there would be no profit/loss in any case. For predictions that are 0, if the ground truth is 0, a utility of +2 is awarded, indicating a successful short sale. If the ground truth is 1, an utility of +1 is awarded, since a short sale would still have been profitable, albeit less so. For ground truths of 3 and 4, -1 and -2 are awarded to the model as the prediction would result in a loss. Predictions on class 4 award reverse. Then:

In addition to this, the downside-risk-adjusted-return is also calculated for each model, to measure the gain vs risk to capital:

as well as a ‘Traded Sharpe ratio’, as the ratio of utility to the standard deviation of returns measured across the trades actually recommended, i.e., when class 0 or 4 is predicted. We motivate utility, DRAR, and Traded Sharpe metrics further in the next Section below.

Table 7 reports utility, DRAR, and Traded Sharpe for experiments 1 and 2, and for synthetic and market data. Cascaded DDT performs better than the base model in all cases, and also better than the cascaded MLP, except for the case of market data in experiment 1. (This may be because the higher capacity MLP captures more era-specific patterns).

| Experiment 1 | |||||

|---|---|---|---|---|---|

| Data | Metric | DDT | MLP | ||

| Dataset | Base | Cascaded | Base | Cascaded | |

| Synthetic ([0.075,0.05]) - 1571 points | Average Utility | 1.11 | 1.69 | 1.06 | 1.50 |

| Gain-Loss | 1073-202 | 303-4 | 1133-229 | 488-42 | |

| Downside-risk adjusted return | 4.31 | 74.75 | 3.95 | 10.62 | |

| Traded Sharpe ratio | 0.92 | 2.93 | 0.88 | 1.53 | |

| Market-4522 points | Average Utility | 0.50 | 1.29 | 0.79 | 1.46 |

| Gain-Loss | 1590-683 | 175-25 | 1227-327 | 107-9 | |

| Downside-risk adjusted return | 1.33 | 6 | 2.75 | 10.89 | |

| Traded Sharpe ratio | 0.38 | 1.07 | 0.63 | 1.46 | |

| Experiment 2 | |||||

| Data | Metric | DDT | MLP | ||

| Dataset | Base | Cascaded | Base | Cascaded | |

| Synthetic ([0.075,0.05]) - 7729 points | Average Utility | 0.94 | 1.18 | 0.90 | 1.12 |

| Gain-Loss | 4530-1164 | 1740-302 | 5500-1480 | 2150-409 | |

| Downside-risk adjusted return | 2.89 | 4.76 | 2.72 | 4.26 | |

| Traded Sharpe ratio | 0.73 | 0.98 | 0.70 | 0.92 | |

| Market-55450 points | Average Utility | 0.33 | 0.72 | 0.47 | 0.50 |

| Gain-Loss | 10800-5960 | 842-268 | 10300-4520 | 2410-1108 | |

| Downside-risk adjusted return | 0.81 | 2.14 | 1.28 | 1.18 | |

| Traded Sharpe ratio | 0.26 | 0.54 | 0.37 | 0.36 | |

5. Discussion

Consider an algorithmic trading scenario where a machine-learning model is being used to recommend long/short trades based on its prediction of where the market will be after a fixed number of time-steps. Consider two strategies: (a) using a model that recommends only a small number of trades each with high utility, i.e., expected gain, and (b) using a model that recommends a large number of trades but each having lower utility.

While it is conceivable that the expected total return is higher for strategy (b), as can also be seen from the figures in Table 7, in the world of financial trading minimising risk is as important as maximizing return. The standard mechanism for measuring risk-adjusted return is the Sharpe ratio, which measures the overall expected gain per time-step adjusted by the standard deviation of returns. However, since our models predict far less often than the base models, we instead measure downside-risk adjusted return and Traded Sharpe ratio as defined earlier. As we have already seen, the cascaded models, especially the DDT-based ones, are far superior in terms of these metrics as reported in Table 7.

To further motivate these metrics, consider that short-term trading often takes place in a leveraged manner, i.e., using funds borrowed from a broker and only minimal capital of the trader’s own; in practice this ratio is at least 5X and can be as high as 10X.

A strategy that incurs large draw-downs (i.e., intermediate losses) risks margin calls in the process, requiring the traders to put up extra capital that could even wipe them out if they are operating with high leverage.

On the other hand, strategies that avoid large losses at all costs, including lower overall returns, allow traders to put up more base capital and/or take higher leverage and thus increase their total return, with the risks of serious margin calls that could wipe them out being far reduced.

6. Related Work

Applying machine learning to financial markets has been and is probably continuing to be widely attempted in practice as well as in research. Apart from application of the standard data-science pipeline using off-the-shelf models, which we do not recount, some novel approaches deserve mention.

A number of prior works such as (Dhar et al., 2019) and (Cohen et al., 2020) have converted financial data into image data and thereafter applied CNN-based deep-learning models for predicting returns. While the latter directly use images of price-series, the former converts level-2 data, i.e., the limit-order book over a window into an image.

Recent works applying machine learning to trading based on price signals alone have also used reinforcement learning: ‘Deep Momentum Networks’ (Lim et al., 2019) as well as ‘Momentum Transformer’ (Wood et al., 2021) formulate the trading task as one of suggesting the position to take, e.g., 1 for a long (i.e., buy) position, -1 for a short (i.e., sell) position, and 0 for no position. Exiting a buy/sell position takes place when a 0 action follows the previous 1 actions, etc. Neural networks are trained to directly optimize volatility-adjusted expected returns, adjusted for transaction costs, over a trading period. The former paper uses MLPs and LSTMs, while the latter uses transformers. Both works are essentially applying vanilla REINFORCE to the MDP formulation of the trading problem. Deep Reinforcement Learning in Trading (Zhang et al., 2020) uses the same formulation as the above two works, but applies more refined reinforcement learning techniques, e.g., policy-gradient, actor-critic, and deep-Q-learning algorithms. Most recently, meta-reinforcement learning via the RL2 algorithm (Duan et al., 2016) was used along with logical features (including temporal ones) learned automatically via ILP (Harini et al., 2023).

The case for using logical rule-based models for financial data as an antidote to noise was made in (Dhar, 2011). More generally, the original CN2 algorithm (Clark and Niblett, 1989) was developed explicitly to deal with noisy data; RIPPER (Asadi and Shahrabi, 2016) is a modern version of the same. More modern approaches to combat noise, specifically label noise (i.e., features are assumed relatively noise-free in comparison) are represented by (Patrini et al., 2017) and (Qin et al., 2019). These use variations on novel loss functions or replace targets of suspected noisy samples with model predictions during training (‘boot-strapping’).

Dealing with noise is related to works on calibration, i.e., ensuring that predicted probabilities are close to observed frequencies on train and test datasets. One such recent approach also uses data pruning during training (as opposed to post-training, as in our proposed approach), to improve calibration error as well as improve fraction of high-confidence predictions (Patra et al., 2023).

7. Conclusions and Future Work

We have introduced cascading models as an approach to deal with noisy data and make predictions only on the fraction of data where the model cascade is confident. We have presented results using cascaded differentiable decision trees as well as MLPs on synthetic data with varying levels of noise as well as real market data.

We observe that using cascaded models results in more accurate predictions and degrade more gracefully with noise at the expense of support. Further, the predictions that are made have high utility towards making trading decisions, as well as result in better risk-adjusted returns as per the approximate metric used. We also find that the cascaded differentiable decision trees perform better than cascaded MLPs, especially in the utility of their predictions and in terms of risk-adjusted returns and traded Sharpe ratio.

Performances of all the models evaluated degrade when tested on distributions different from those they are trained on (represented by different eras in our case). Future work towards addressing this could be to employ meta-learning (Finn et al., 2017) or continual learning (Finn et al., 2019) techniques, combining these with the idea of using cascaded models via data-pruning as we have proposed. Additionally, cascaded models may use train-time pruning approaches such as in (Patra et al., 2023).

References

- (1)

- Asadi and Shahrabi (2016) Shahrokh Asadi and Jamal Shahrabi. 2016. RipMC: RIPPER for multiclass classification. Neurocomputing 191 (2016), 19–33.

- Clark and Niblett (1989) Peter Clark and Tim Niblett. 1989. The CN2 induction algorithm. Machine learning 3 (1989), 261–283.

- Cohen et al. (2020) Naftali Cohen, Tucker Balch, and Manuela Veloso. 2020. Trading via image classification. In Proceedings of the First ACM International Conference on AI in Finance. 1–6.

- Dhar (2011) Vasant Dhar. 2011. Prediction in financial markets: The case for small disjuncts. ACM Transactions on Intelligent Systems and Technology (TIST) 2, 3 (2011), 1–22.

- Dhar et al. (2019) Vasant Dhar, Chenshuo Sun, and Puneet Batra. 2019. Transforming finance into vision: concurrent financial time series as convolutional nets. Big Data 7, 4 (2019), 276–285.

- Duan et al. (2016) Yan Duan, John Schulman, Xi Chen, Peter L Bartlett, Ilya Sutskever, and Pieter Abbeel. 2016. Rl 2: Fast reinforcement learning via slow reinforcement learning. arXiv preprint arXiv:1611.02779 (2016).

- Finn et al. (2017) Chelsea Finn, Pieter Abbeel, and Sergey Levine. 2017. Model-agnostic meta-learning for fast adaptation of deep networks. In International conference on machine learning. PMLR, 1126–1135.

- Finn et al. (2019) Chelsea Finn, Aravind Rajeswaran, Sham Kakade, and Sergey Levine. 2019. Online meta-learning. In International Conference on Machine Learning. PMLR, 1920–1930.

- Frosst and Hinton (2017) Nicholas Frosst and Geoffrey Hinton. 2017. Distilling a Neural Network Into a Soft Decision Tree. (11 2017).

- Harini et al. (2023) SI Harini, Gautam Shroff, Ashwin Srinivasan, Prayushi Faldu, and Lovekesh Vig. 2023. Neuro-symbolic Meta Reinforcement Learning for Trading. arXiv preprint arXiv:2302.08996 (2023).

- Lim et al. (2019) Bryan Lim, Stefan Zohren, and Stephen Roberts. 2019. Enhancing time-series momentum strategies using deep neural networks. The Journal of Financial Data Science 1, 4 (2019), 19–38.

- Patra et al. (2023) Rishabh Patra, Ramya Hebbalaguppe, Tirtharaj Dash, Gautam Shroff, and Lovekesh Vig. 2023. Calibrating deep neural networks using explicit regularisation and dynamic data pruning. In Proceedings of the IEEE/CVF Winter Conference on Applications of Computer Vision. 1541–1549.

- Patrini et al. (2017) Giorgio Patrini, Alessandro Rozza, Aditya Krishna Menon, Richard Nock, and Lizhen Qu. 2017. Making deep neural networks robust to label noise: A loss correction approach. In Proceedings of the IEEE conference on computer vision and pattern recognition. 1944–1952.

- Qin et al. (2019) Zhen Qin, Zhengwen Zhang, Yan Li, and Jun Guo. 2019. Making deep neural networks robust to label noise: cross-training with a novel loss function. IEEE access 7 (2019), 130893–130902.

- Reed et al. (2014) Scott Reed, Honglak Lee, Dragomir Anguelov, Christian Szegedy, Dumitru Erhan, and Andrew Rabinovich. 2014. Training deep neural networks on noisy labels with bootstrapping. arXiv preprint arXiv:1412.6596 (2014).

- Silva et al. (2020) Andrew Silva, Matthew Gombolay, Taylor Killian, Ivan Jimenez, and Sung-Hyun Son. 2020. Optimization methods for interpretable differentiable decision trees applied to reinforcement learning. In International conference on artificial intelligence and statistics. PMLR, 1855–1865.

- Suarez and Lutsko (1999) Alberto Suarez and James Lutsko. 1999. Globally Optimal Fuzzy Decision Trees for Classification and Regression. IEEE Trans. Pattern Anal. Mach. Intell. 21 (01 1999), 1297–1311.

- Wood et al. (2021) Kieran Wood, Sven Giegerich, Stephen Roberts, and Stefan Zohren. 2021. Trading with the Momentum Transformer: An Intelligent and Interpretable Architecture. arXiv preprint arXiv:2112.08534 (2021).

- Zhang et al. (2020) Zihao Zhang, Stefan Zohren, and Stephen Roberts. 2020. Deep reinforcement learning for trading. The Journal of Financial Data Science 2, 2 (2020), 25–40.