theoremTheorem[section] \newtheoremreplemmaLemma[section] \newtheoremrepcorollaryCorollary[section]

Robust Trading in a Generalized Lattice Market

Abstract

This paper introduces a novel robust trading paradigm, called multi-double linear policies, situated within a generalized lattice market. Distinctively, our framework departs from most existing robust trading strategies, which are predominantly limited to single or paired assets and typically embed asset correlation within the trading strategy itself, rather than as an inherent characteristic of the market. Our generalized lattice market model incorporates both serially correlated returns and asset correlation through a conditional probabilistic model. In the nominal case, where the parameters of the model are known, we demonstrate that the proposed policies ensure survivability and probabilistic positivity. We then derive an analytic expression for the worst-case expected gain-loss and prove sufficient conditions that the proposed policies can maintain a positive expected profits, even within a seemingly nonprofitable symmetric lattice market. When the parameters are unknown and require estimation, we show that the parameter space of the lattice model forms a convex polyhedron, and we present an efficient estimation method using a constrained least-squares method. These theoretical findings are strengthened by extensive empirical studies using data from the top 30 companies within the S&P 500 index, substantiating the efficacy of the generalized model and the robustness of the proposed policies in sustaining the positive expected profit and providing downside risk protection.

1 Introduction

The robustness of algorithmic trading systems has been a focal point of numerous studies such as dokuchaev1998asymptotic, dokuchaev2002dynamic, korajczyk2004momentum, barmish2008trading. Among the various aspects of robustness, the Robust Positive Expectation (RPE), a trading policy capable of generating a positive expected profit across various market conditions, is particularly sought after. Notably, among the strategies targeting RPE, the so-called Simultaneous Long-Short (SLS) strategy, proposed by barmish2011arbitrage, barmish2015new, has proven to be a significant advancement. This strategy involves investors holding both long and short positions simultaneously, with equal weights, that leverages market movements in either direction.

Subsequently, several extensions have been proposed to the SLS strategy, including generalization for Merton’s diffusion model in baumann2016stock, geometric Brownian motion (GBM) model with time-varying parameters in primbs2017robustness, and any linear stochastic differential equation (SDE) in baumann2019positive. Additionally, the SLS strategy has also been extended to the proportional-integral (PI) controller in malekpour2018generalization, to latency trading in malekpour2016stock, and coupled SLS strategy on pair trading for two correlated assets was studied in deshpande2018generalization, deshpande2020simultaneous. Recent contributions to the SLS theory include the work by baumann2023theoretical.

Other innovative approaches have focused on robust stock trading. For example, maroni2019robust proposed a robust design strategy for stock trading via feedback control. primbs2018pairs, tie2018optimal studied the stochastic control-theoretic approach in a pair trading framework, vitale2018robust investigated robust trading for ambiguity-averse insider, o2020generalized proposed a generalized SLS with different weight settings on long and short positions. Recently, hsieh2022robust introduced a new variant of the SLS strategy, termed the double linear policy, which assigns equal weights to long and short positions in a discrete-time setting, creating a mean-variance criterion to determine optimal weights. This work was later extended by wang2023robustness to involve time-varying weights, under the assumption of serially independent returns.

Despite numerous contributions to the robust trading systems, a crucial gap persists in the existing literature. Most existing strategies, including SLS or double linear policy, are limited to single or paired assets, and often model asset correlation within the trading strategy, rather than considering it as a characteristic of the market. More importantly, they often overlook serial dependence in asset returns, a notable empirical phenomenon fielitz1971stationarity, officer1972distribution, campbell1993trading, christoffersen2006financial. While the work by balvers1997autocorrelated investigated autocorrelated returns and optimal intertemporal portfolio choice, it primarily focuses on short-term memory, and more importantly, it does not address the robustness of the strategy in various market conditions. These omissions pose a significant challenge in robust trading strategies, as emphasized by recent work that highlights the impact of tick-size reductions on various stocks and the influence of competing crossing networks werner2023tick.

In response to these gaps, this paper introduces an extension to the double linear policy, termed multi-double linear policies. We rigorously investigate its stochastic robustness in a generalized lattice market that involves both serial and asset correlations, as detailed in Section 2. Then we demonstrate that the proposed policies ensure survivability and probabilistic positivity. Following this, we establish a detailed gain-loss analysis and derive an analytic expression of the worst-case expected gain-loss function. We then prove that the proposed policies offer a form of downside risk protection in comparison to the pure long-only and pure short-only strategies. We demonstrate an “approximate” RPE in Section 3 and establish sufficient conditions under which the positive expected profit is upheld, even within a symmetric lattice market, thereby underscoring the theoretical foundations of our approach. We further show that the parameters used in the proposed generalized lattice model form a convex polyhedron, which facilitates efficient estimation through a constrained least-squares approach; see Section 4. These theoretical findings are substantiated by extensive empirical studies, lending practical relevance to the developed framework; see Section 5.

2 Preliminaries and Notations

This section provides an overview of the formulation, including the generalized lattice market with binomial serially correlated returns and asset correlation, the multi-double linear policies, and the robust positive expectation property.

2.1 Generalized Lattice Market with Serial and Asset Correlations

Consider a lattice market consisting of distinct assets. For each asset, say Asset with , the per-period returns are represented by the sequence . These returns exhibit two possible outcomes, with , where represents the upward movement factor333When working with price data on a daily based or shorter timescale, the values of the movement factors are generally observed to be small, i.e., and for all ; see granger2004occasional. and represents the downward movement factor. In combination, this holds for all stages satisfying for . The generalization of the model stems from the assumption that there are asset correlations and serial correlations in the probability of returns, signifying that a positive return at each stage depends on the previous stages and other assets.

In particular, we assume that the return process with , exhibits Markov memory with serial autocorrelation and asset correlation. Specifically, take the vector of returns at stage as , the vector of upward movement factors as , and the vector of downward movement factors as . Henceforth, we use the shorthand . Denote the matrix of autocorrelation coefficients as where and and the matrix of asset correlation coefficients as where . Let be the vector of conditional probabilities of positive returns at stage , affected by the previous stages and asset correlations. The th component of this vector is given by . Hence,

| (1) |

where is the first column of the matrix . Therefore, for Asset , the conditional probability

| (2) |

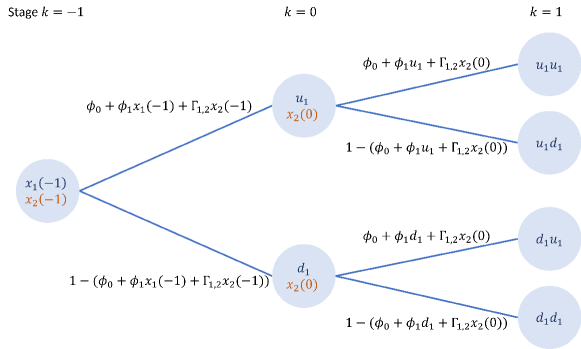

where are the elements of the th row of the matrix and represents the th row and th column of the matrix and the conditional probabilities include initial conditions for . Figure 1 illustrates the idea of the generalized lattice model with Markov memory, specifically for (indicating one memory length) and (representing two distinct assets). The figure includes the initial realized return for the two assets, demonstrating the probability for Asset 1 at each stage is dependent on the realized returns from the preceding stage.

Our analysis assumes that the trades incur zero transaction costs and that the underlying asset has perfect liquidity. Fractional shares are allowed. This setting serves as an appropriate starting point for building the model and aligns closely to the standard frictionless market framework in finance; see cvitanic2004introduction, luenberger2013investment. While not analyzed in theory, later in Section 5, some of the assumptions such as transaction costs are relaxed in empirical studies.

Remark 2.1.

Returns often exhibit serial correlation, see fielitz1971stationarity, campbell1993trading, christoffersen2006financial, with past returns over several periods. This can be due to factors like momentum, mean reversion, or other market dynamics, allowing the model to capture long-term dependencies in the return process. The correlation matrix can be extended to time-dependent correlations where is a function that captures the dependence of the correlation on past returns.

2.2 Multi-Double Linear Policies

Building upon hsieh2022robust, hsieh2022robustness, we generalize the single double linear policy, initially constructed for the single asset case, to multi-double linear policies for multi-asset portfolio case. This generalization allows for trading a portfolio consisting of distinct assets. Beginning with an initial account value of an investor, , which is to be allocated across the assets using the fractions for satisfying . That is, the initial account value for Asset is given by and the initial account is a convex combination of .

Thereafter, we strategically divide it into two parts for each asset, representing long and short positions. Superficially, take a fraction , such that the initial account value for the long position of Asset is , and the value for the short position is . The trading policy for Asset , denoted by , is constructed as the sum of the policies for long and short positions, i.e., where and are in double linear forms: and where is the weight444The choice of assures that the account is always survival, i.e., the investor who adopts the double linear policy with the weight never goes broke with probability one; see Lemma 3.1. for Asset . Here, and represent the account value for the long and short positions of Asset at stage , respectively. The long-short account value dynamics for Asset are given by

where is the risk-free rate.555 Note that the risk-free rate is included in the dynamics of the long position to signify the opportunity cost of holding the asset; conversely, in the short position, where the asset is borrowed rather than invested, this leads to the absence of in the short position dynamics. The overall account value at stage is given

where , , and with and . Note that if , the policies correspond to a pure long-only position, while corresponds to a pure short position. Therefore, one immediately sees that the proposed policies greatly generalize the common trading strategies.

Remark 2.2.

It should be noted that the notations or or , which implicitly depend on various parameters and variables, are suppressed for the sake of simplicity. In particular, the overall account value at stage can be expressed as where is the triple for the proposed polices with , is the risk-free rate, and denote the sequence of asset returns vectors up to stage .

2.3 Robust Positive Expected Profits

For , let be the cumulative gain-loss function up to stage where is the account value at stage . Note that, for the sake of simplicity, we express . Then the expected cumulative gain-loss function is denoted by . The primary stochastic robustness to be studied in this paper is the so-called robust positive expectation (RPE) property, see the definition below.

Definition 2.1 (Robust Positive Expectation).

For stage , let be the initial account value, and be the account value at stage . Define the expected cumulative gain-loss function up to stage as A trading policy is said to have a robust positive expectation (RPE) property if it ensures that for all , with nonzero trend and finite variance.

2.4 Notation

We denote by the nonnegative reals and the strictly positive reals. For a set , the indicator is defined as if ; otherwise . For and and a positive integer, a set or with refers to the Cartesian product of the interval or with itself -times.

3 Stochastic Robustness of the Policies

In this section, we analyze the stochastic robustness of the multi-double linear policies within the generalized lattice market with both serial and asset correlations. To facilitate our analysis, we use the vector notations where the set , and . With these notations, the multi-double linear policies, as described in Section 2, are characterized by the triple It is important to note that our analysis in this section assumes a nominal case in the sense that the generalized lattice model’s parameters and are known. Subsequently, in Section 4, we provide an efficient least-square-based approach to estimate these parameters in a practical context.

3.1 Survivability and Probabilistic Positivity

The first result indicates that, for each Asset , the multi-double linear policies assure survival trades; i.e., bankruptcy is avoided.

[Survivability] For multi-double linear policies with triple for , we have , for all and all with probability one, and hence the overall account for all with probability one. Moreover, if for some , , and , then and and for all with probability one.

Proof. See Appendix A.

With the aid of Lemma 3.1, we can prove a general result akin to the Paley-Zygmund inequality, regarding probabilistic positivity.

Lemma 3.1 (Probabilistic Positivity).

Fix . For multi-double linear policies with triple , it follows that

| (3) |

for all .

Proof. See Appendix A.

3.2 Gain-Loss Analysis

For , let be the account value at stage . Then the corresponding cumulative gain-loss function, as defined in Section 2, is given by and the expected cumulative gain-loss function as . Note that with this notation, we can rewrite Inequality (3) in terms of the cumulative gain-loss function. Indeed, observe that

Moreover, noting that and , Lemma 3.1 becomes

which characterizes the probability of cumulative gain-loss larger than the weighted sum of and . Note that the variance of the cumulative gain-loss function, , is given by Although the analytic expression for this variance may be intractable within the generalized lattice market framework, it can be computed numerically; e.g., see later in Section 5. The next lemma indicates gain-loss under zero weight.

[Zero Weight Gain-Loss] Consider the multi-double linear policies with triple . If for all , we have for all with probability one. Moreover, if the risk-free rate is zero, i.e., , then the gain-loss function simplifies to for all .

Proof. See Appendix A.

To prove our first main result, Theorem 3.1, the following two auxiliary lemmas are useful. The first one states that the probability of receiving a positive return can be characterized by a recursion formula, and the second one expresses a sum of expected logarithmic functions using the probability recursion.

[A Recursion Formula of Probability] For , assume that are returns characterized by the generalized lattice model as described in Section 2.1. For , let be the probability of receiving a positive return of Asset at stage with initial conditions for with . Then satisfies the following recursion

| (4) |

Proof. See Appendix A.

Remark 3.1.

Let and consider assets , each associated with a weight . Assume that are returns characterized by a generalized lattice model as described in Section 2.1. Then the following equality holds:666The notation used here represents the positive and negative variations in Equation (5). If on the left-hand side of Equation (5) is , then all instances of on the right-hand sides are . Likewise, if the left-hand side is , then all instances of on the right-hand side becomes .

| (5) |

where is the expected number of receiving positive returns up to stage , and is stated in Lemma 3.2.

Proof. See Appendix A.

Theorem 3.1 (The Worst Expected Gain-Loss).

Proof.

For , fix The expected cumulative gain-loss function is given by

Note that the expectation term can be written as

where the last inequality holds by Jensen’s inequality on strictly convex function , i.e., for some random variable . Subsequently, applying Lemma 3.2, we have

where and The positivity holds since , , and for all . ∎

[Some Special Cases] Consider the multi-double linear policies with triple . We have the following conclusions:

-

(i)

If , then for all .

-

(ii)

If and for all , then for all .

Proof. See Appendix A.

Remark 3.2 (Approximate RPE).

Consider the special case where the risk-free rate , and let both and . Then, for each Asset and fixed , we have and , which implies that the lower bound in Theorem 3.1 is given by for . This leads to the inequality for all , provided that and are sufficiently small. Said another way, we observe an “approximate” RPE property. As seen later in the next section, the multi-double linear policies proposed in this paper can result in a positive expected profit. This holds true even in markets with a seemingly unprofitable symmetric lattice market. See also Section 5 for analysis of positive expected profits in practice.

3.3 Positive Expected Profits When Market has Clear Trends

The main result of this section indicates that if the assets in the market have clear trends; i.e., and (or and ), then it is possible to establish sufficient conditions for the multi-double linear policies to ensure the positive expected profits. To prove such a result, the following lemma is useful.

Lemma 3.2 (A Strict Convex Auxiliary Function).

Consider a function with where with . Then is strictly convex in . Moreover, if either and or and , then has a unique minimum at some satisfying .

Proof. See Appendix A.

Theorem 3.2 (Positive Expected Profits).

Consider multi-double linear policies with triple within the generalized lattice market. Then the following two statements hold true.

Suppose for all and for with and satisfying

then .

Suppose for all and for with and satisfying

then .

Proof.

We shall only give proof for part since an almost identical argument would work for part . To prove part , let . Then there exists such that . With the triple , Theorem 3.1 indicates that the expected gain-loss function satisfies where

and

Therefore, we have

where is an auxiliary function with and . Since and , it follows that and and . Therefore, by Lemma 3.2, the auxiliary function is strictly convex in and has unique minimum at satisfying

Moreover, the strict convexity implies that for any , the function is strictly increasing; therefore, inverse exists and is still strictly increasing for . Using the assumed hypothesis,

it follows that To complete the proof, we must show that . Indeed, proceeds a proof by contradiction by assuming that . Within this range, is strictly decreasing, therefore, it follows that

| (6) |

However, note that Hence, it follows that

This implies that which contradicts to Inequality (6). Therefore, we must have and the proof is complete. ∎

3.4 Gain-Loss Analysis in Symmetric Lattice Market

An important subclass of the lattice market framework is the symmetric market. In this type of market, the factors governing upward and downward movement have the same magnitude, creating a unique structure. It should be noted that since the multi-double linear policies earn positive profits when either an upward or downward trend is clear, it is arguable that the robustness of the symmetric lattice market needs to be further scrutinized. Below, we first provide a corollary for the lower bound of the expected gain-loss of the proposed policies in the symmetric market. Then we prove the conditions under which the RPE may hold for such a symmetric lattice market.

[Limitation of the Polices in Symmetric Lattice Market] For , consider the multi-double linear policies with triple in a lattice market with and for all .

-

(i)

If for all , then

for some

-

(ii)

If for all , then

Proof. See Appendix A.

Remark 3.3.

[An Strictly Increasing Auxiliary Function] Fix with . Define a function with . Then is a strictly increasing and .

Proof. See Appendix A.

Theorem 3.3 (RPE in Symmetric Lattice Market).

For , consider the multi-double linear policies with triple in a generalized lattice market with and for all . If either or for all satisfying where , then

Proof.

Suppose either or for all and for some . Recalling part of Corollary 3.4, we have

| (7) |

where . Note that the ratio and . Lemma 3.3 implies that is strictly increasing; hence, the inverse exists. By the hypothesis, we have which implies . Applying this inequality on the right-hand side of Inequality (7), a simple algebraic manipulation leads to the desired immediately. To complete the proof, we must show that In particular, for seeing that we proceed a proof by contradiction by supposing that Taking on both sides and applying the strict increasingness of , it leads to , which implies that

| (8) |

However, since and , it follows that . Raising both sides to the power leads to , which contradicts to the fact (8). Therefore, we must have Lastly, for seeing that , we must show that

It is equivalent to show that Simplifying the expression, we obtain which holds true for any for all and all ∎

Remark 3.4.

It is essential to note that the condition on in Theorem 3.3 is not an overly restrictive condition, and it can be easily satisfied. For illustration, within a daily basis scale, , with one common value being , as can be seen in Section 5. If we consider using multi-double linear policies and trading with one year comprising days, then the ratio for all . Then the RPE holds if the condition in Theorem 3.3 is met for some . More details about these findings will be presented in Section 5 using historical data.

4 Parameters Estimation

In practice, the parameters of the generalized lattice model, as developed in previous sections, are typically unknown to the trader and must be estimated. This constitutes the primary goal of this section. Specifically, for each Asset with , we shall discuss how to estimate the required parameters, e.g., , and for and .

4.1 Estimating the Upward and Downward Factors

To estimate the upward and downward movement factors of returns, we work with a data-driven geometric mean described as follows: Let be the per-period returns obtained from the data. Then, for each asset, we partition the return data into two separate series, positive and negative series, denoted by and consisting of positive values and negative values in the series, respectively. Now we solve to find the upward movement estimate for Asset , denoted by . Likewise, by solving , we get the downward movement estimate, denoted by , for Asset .777Given , the geometric mean of , call it , is the solution of the nonlinear equation ; for more details on this topic, we refer to casella2021statistical. On the other hand, one can also compute the upward and downward movement factors by the standard Cox-Ross-Rubinstein (CRR) method in finance; e.g., see cox1979option, luenberger2013investment.

4.2 Estimating the Correlation Matrix

We estimate the correlation matrix, denoted by , among the assets by determining the correlation coefficients of their realized asset returns. To achieve this, we collect historical returns data points for each Asset at stage , denoted by . Specifically, for two distinct Assets and where and for , the correlation is represented by

Notably, in contrast to the conventional setting where the diagonal elements of the correlation matrix are equal to one, we define for The departure from tradition is motivated by the fact that the correlation of the previous stage is characterized by the Markov coefficient , which will be estimated in Section 4.3. Hence, the estimated matrix can be written as

4.3 Estimating the Markov Coefficients

Having obtained the estimates of for , we then estimate the Markov coefficients for the probability model described in Section 2. Indeed, for Asset , we define the response variable Then, it follows that

where the second last equality holds by using Equality (2).

To estimate the parameters for Asset , we collect historical returns data points, , at stage satisfying , and transform it into binomial values based on the sign of per-period returns of each stage, which satisfy where is the indicator function of event . Subsequently, we compute the response values and minimize the residual sum of squares (RSS) as

Next lemma shows that the parameter space of Markov coefficients forms a convex polyhedron, which facilitates the optimization.

[Convex Constraint Set on Markov Coefficients] Let . For , the inequalities where are equivalent to

| (9) |

which forms a convex polyhedron.

Proof. See Appendix A.

For each Asset , with the aid of Lemma 4.3, the optimal estimators, call it , can be solved by the following constrained least squares optimization problem:

Note that the optimization problem above is a linear constraint quadratic convex program; see boyd2004convex, which facilitates an efficient computation.

4.4 Estimating the Time-Varying Probabilities

5 Empirical Studies

In this section, we conduct extensive empirical studies using historical price data from the top 30 holdings of the S&P 500, sorted by market capitalization. In the sequel, we shall refer to these assets as “S&P 30.”888The thirty stocks used in this paper, in terms of their tickers, are: AAPL (Apple Inc.), MSFT (Microsoft Corporation), AMZN (Amazon.com Inc.), NVDA (NVIDIA Corporation), GOOGL (Alphabet Inc. Class A), GOOG (Alphabet Inc. Class C), META (Meta Platforms Inc.), BRK.B (Berkshire Hathaway Inc. Class B), TSLA (Tesla Inc.), UNH (UnitedHealth Group Inc.), JNJ (Johnson & Johnson), JPM (JPMorgan Chase & Co.), LLY (Eli Lilly and Company), XOM (Exxon Mobil Corporation), V (Visa Inc.), PG (Procter & Gamble Co.), AVGO (Broadcom Inc.), HD (The Home Depot Inc.), MA (Mastercard Incorporated), CVX (Chevron Corporation), MRK (Merck & Co.), ABBV (AbbVie Inc.), PEP (PepsiCo Inc.), COST (Costco Wholesale Corporation), ADBE (Adobe Systems Incorporated), KO (The Coca-Cola Company), WMT (Walmart Inc.), CSCO (Cisco Systems Inc.), MCD (McDonald’s Corporation), and BAC (Bank of America Corporation). The price data were retrieved from Yahoo! Finance and the associated estimated parameters are provided in Appendix B. Our focus is twofold: The first is to demonstrate the efficacy of the generalized lattice market; the second is to illustrate the robust positive expected profits of the multi-double linear policies. Additionally, we include a comprehensive sensitivity analysis to further enhance our contributions. Toward the end of this section, a method for identifying optimal weights is discussed, accompanied by several studies of the out-of-sample trading performance of the policies.

5.1 Validation of the RPE Property

We validate the RPE property through two examples: The first example confirms the RPE versus weights; the second investigates the property via sensitivity analysis; i.e., we explore the effects of various parameters such as weights, memory length, and initial allocation constants.

Example 5.1 (RPE of S&P 30 Portfolio).

To validate our theoretical results, we consider the S&P 30 portfolio consisting of top stocks listed on the S&P 500 index. For each stock, we collect the historical daily adjusted closing prices over a one-year period from January 2022 to December 2022. Our analysis begins with the estimation of essential parameters of each asset, using the methods detailed in Section 4. Specifically, we estimate the upward and downward movement factors , , Markov coefficients , correlation coefficients , and the probability for each asset. The detailed values of these estimates can be found in Appendix B.

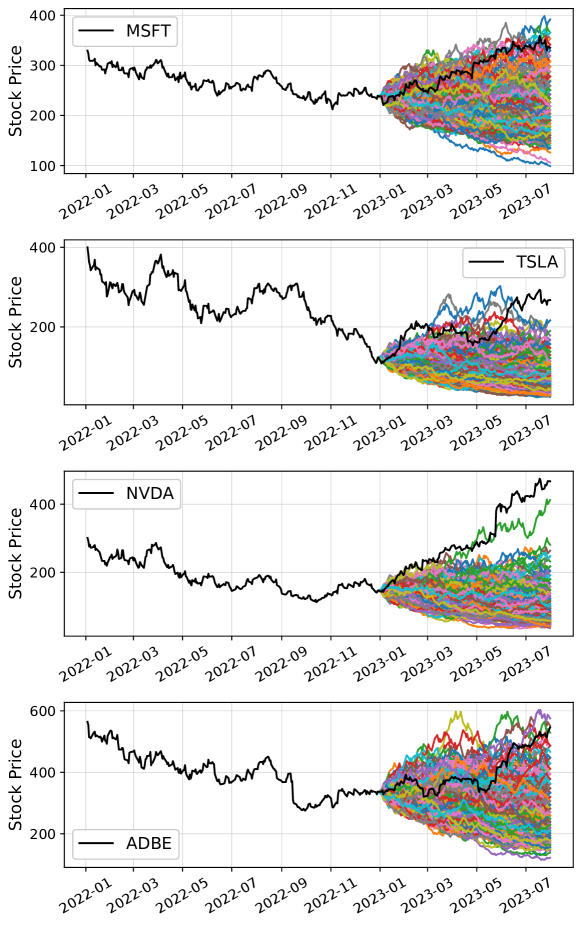

Efficacy of Generalized Lattice Market Model. With these estimations in hand, we proceeded to simulate the stock prices using the recursion for over a time horizon of days, covering the period from January 2023 to July 2023, with sample paths. Figure 2 reveals both the actual historical stock prices (in solid black lines) for 2022 and the simulated 500 paths for the first seven months of 2023. The paths were generated using the aforementioned parameter estimates. Remarkably, an examination of the figure illustrates that the simulated paths approximately encompass the real stock prices for the corresponding period in 2023, even under varying market conditions. This figure indicates the potential of our generalized lattice model to offer insights into market behavior, demonstrating that the training data might represent a bear market, while the testing data may indicate a bull market.

Initializing the Multi-Double Linear Policies. As mentioned in previous sections, to implement the multi-double linear policies, one must specify the triple and initial account value . Here, we first take , an initial account value of , and equal asset weights for all for S&P 30, using a generalized lattice model with varying memory lengths and a zero risk-free rate of . For the specification of the initial allocation vector , we consider three distinct strategies: The first one is equal-weighted allocation, denoted as . The second one is capital-weighted allocation, computed by the normalized weight of the S&P 30 index, denoted as .999The capital-weighted allocation is retrieved from Slickcharts. The third one is gain-loss-weighted allocation, calculated using the gain-loss of training data as a criterion for capital allocation. It is denoted as , forming the vector . Table 1 summarizes the choice of the relevant parameters.

| 1 | 1 | 1 | |

| 0 | 0 | {0.92, 1.51, 3.88} | |

| {1, 2, 5, 10} | 1 | 1 | |

| 0.5 | {0.1, 0.3, 0.5, 0.7, 0.9} | 0.5 | |

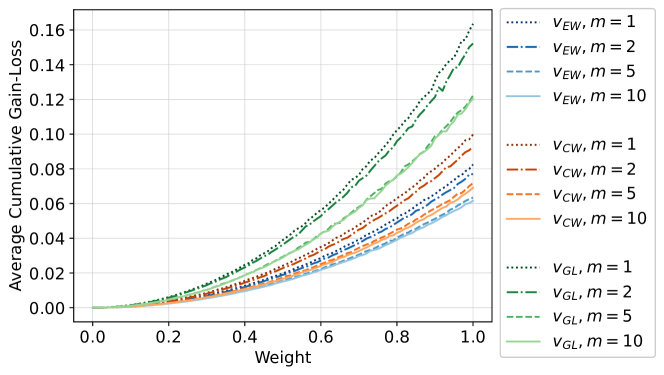

Gain-Loss Analysis. With the various settings of the triple as seen in Table 1, we implement the multi-double linear policies across the assets within the portfolio. The trading performance, as illustrated in Figure 3, depicts the average cumulative gain-loss against various weights for the parameter set in Table 1. We see that there exists a positive expected gain-loss for the given portfolio and for all parameter set combinations. Remarkably, this positivity is found to be robust across diverse choices of at .

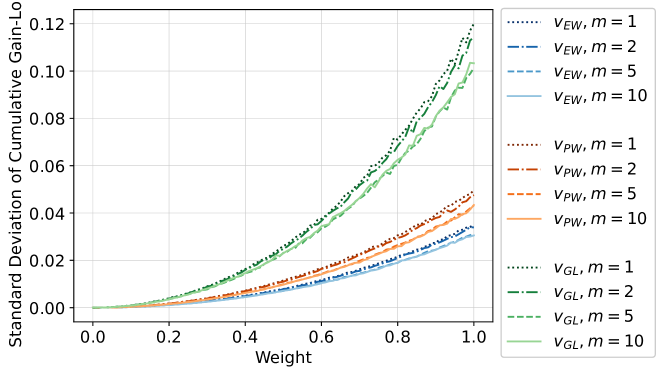

Moreover, we present the associated standard deviation of the cumulative gain-loss for the parameter set , depicted in Figure 4. Notably, both the average cumulative gain-loss and the corresponding standard deviation exhibit increasing monotonicity with respect to the weights, as shown in Figures 3 and 4. The results presented here form a foundation for practitioners aiming to explore novel trading paradigms; see Section 5.2 to follow.

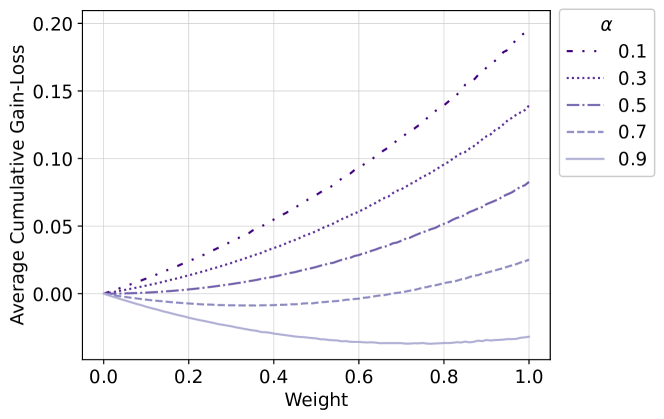

Example 5.2 (Sensitivity Analysis).

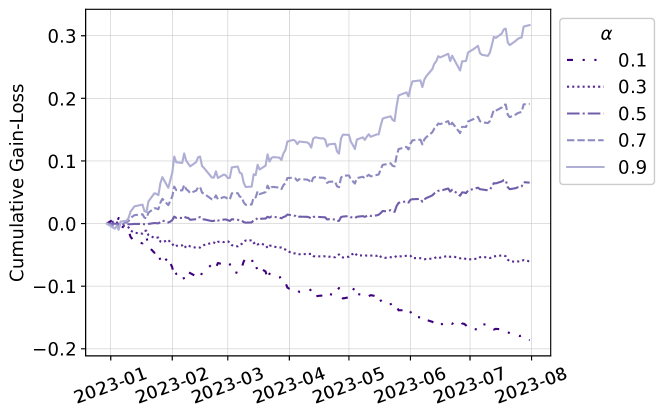

Continuing with the dataset and estimations provided in Example 5.1, we proceed further to analyze the gain-loss trading performance under different , in combination with various weights , as the parameter set listed in Table 1. The corresponding results are shown in Figure 5. We see that the average gain-loss is positive for , implying that there is a preference for initially allocating more capital to the short positions. In contrast, a negative average gain-loss is recorded for . This phenomenon might be attributable to a decreasing trend for the S&P 30 over the examined period.

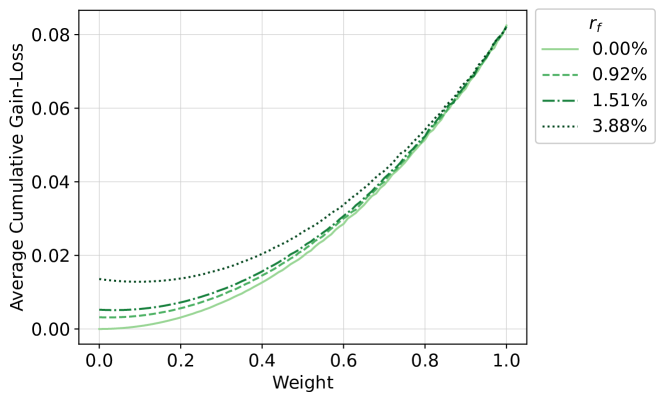

Besides, we extend our analysis to implement multi-double linear policies that incorporate a non-zero risk-free rate, },101010The three risk-free rates listed here were retrieved from the U.S. 10-year Treasury yields on the first day of the years 2021, 2022, and 2023, respectively. as outlined in the parameter set in Table 1. By comparing the performances under parameter set with , versus , represented respectively in Figure 6, we observe that incorporating a risk-free rate for long positions leads to a higher cumulative gain-loss, which is consistent with the intuition that the risk-free rate would contribute additional capital due to under-investment in each period.

5.2 Out-of-Sample Trading Performance with Costs

This section studies out-of-sample trading performance using the multi-double linear policies with triple . In the following analysis, we also consider the impact of transaction costs.

5.2.1 Identifying Optimal Weights via Mean-Variance Efficient Frontier

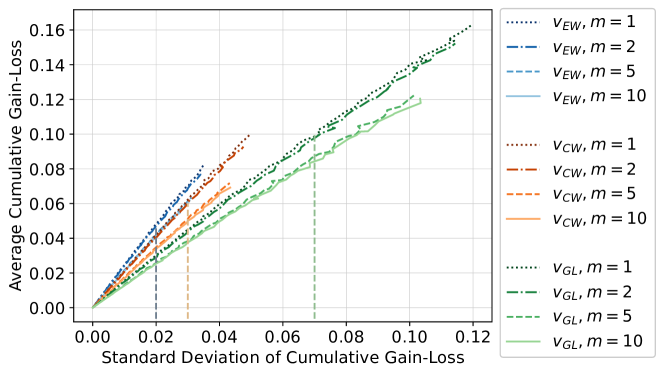

When the weight for all , Figure 3 reveals that the expected cumulative gain-loss increases as the weight increases. This is also evident in the standard deviation of the cumulative gain-loss across different weights; see Figure 4. Therefore, we then depict the mean-variance efficient frontiers using the expected cumulative gain-loss against the standard deviation , as shown in Figure 7. Based on the monotonic increasing property, one can determine an optimal weight, call it , using the mean-variance approach outlined in hsieh2022robust.

In particular, the procedure is as follows: We begin by specifying a target standard deviation, then identify the corresponding maximum expected gain-loss under the chosen target. Once this maximum expected gain-loss is decided, it can be traced back to the optimal weight due to the strictly increasing relationship between expected gain-loss and weight. Below we consider three different approaches to identifying optimal weights.

Constant Optimal Weight for S&P 30. Consider the same S&P 30 dataset from Example 5.1. Suppose we set the target standard deviation , , and for , , and , respectively, represented by the dashed line in Figure 7, for the parameter set with memory length . The maximum expected gain-loss are determined as , , and . Due to the strictly monotonic increasing relationship between expected gain-loss and weight , as seen in Figure 3, we can readily trace back the optimal weight: , , and , collectively denoted as .

Optimal Weight Determined by Top 10 Companies of S&P 30. Except for assigning the same constant weight for all assets, an alternative approach focuses solely on investing assets that exhibit the most promising performance. Here, we consider allocating the optimal constant weights to the top 10 assets of S&P 30 that exhibit the highest gain-loss, as determined by the training data. For the remaining assets that are not selected, we assign weights of zero. The corresponding weight is denoted as .

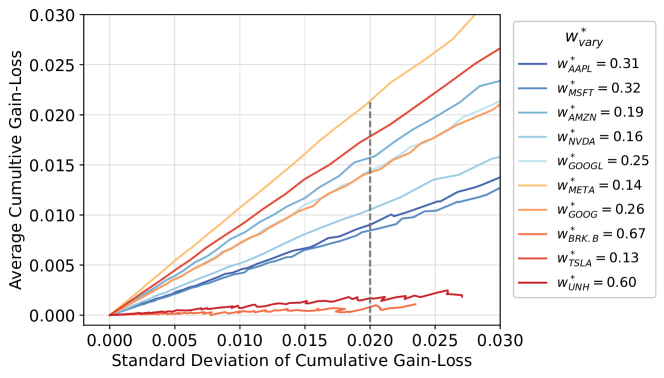

Optimal Weight Determined by Each Company. Lastly, we explore determining optimal weights for individual assets, denoted by for , using the monotonic increasing property between gain-loss function and weight. For instance, by setting a uniform target standard deviation for all assets, represented by the dashed line shown in Figure 8, we can determine the associated maximum average cumulative gain-loss for each asset, leading to a set of optimal weights called via a similar method mentioned previously.111111In the meantime, we also assign a zero weight to the assets with an average gain-loss close to zero, using a threshold of .

5.2.2 Out-of-Sample Trading Performance via Backtesting

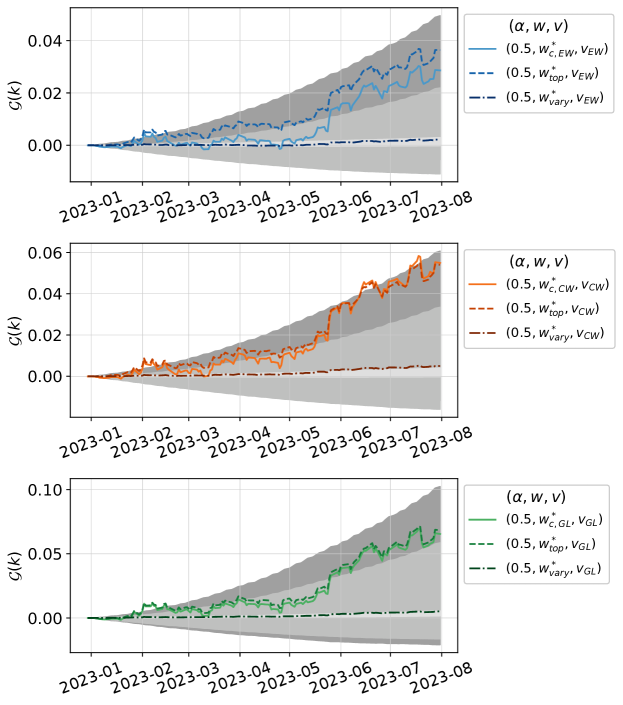

With the selected optimal weights obtained in the preceding sections, we conducted backtesting over an out-of-sample period from January 2023 to July 2023. To analyze the trading performance across distinct sets of triple parameters , we carry out three initial allocations and three types of optimal weights , the constant optimal weight, the top 10 constant optimal weight, and the optimal weight varying among assets, respectively at . The corresponding trading trajectories and performance are shown in Figure 9 and quantitatively summarized in Table 2. For these scenarios, we incorporate a non-zero risk-free rate and a transaction cost , corresponding to 1 basis point, for multi-double linear policies.

Due to the explicit trend for the year 2023 for some assets listed in S&P 30, the multi-double linear policies assure positive gain-loss for several parameter sets even in the consideration of transaction costs. Additionally, the triple has maximium out-of-sample gain-loss, has minimum standard deviation, and has minimum maximum percentage drawdown.

Additionally, Figure 9 also presents Monte-Carlo-based 95% prediction intervals for each trading scenario in the figure. These intervals were generated via 10,000 simulated prices within the framework of the generalized lattice market model. For each path, we compute the average gain-loss and standard deviation for each day. In the figure, three distinct prediction intervals are highlighted. The dark-gray, gray, and light-gray regions correspond to the parameter triples , , and , respectively. These intervals exhibit significant positive gain-loss regions, which is consistent with our theory.

| Gain-Loss | Standard Deviation | Maximum Drawdown (%) | |

|---|---|---|---|

| 0.0286 | 0.0099 | 0.6675 | |

| 0.0364 | 0.0114 | 0.5964 | |

| 0.0021 | 0.0007 | 0.0721 | |

| 0.0549 | 0.0186 | 1.0352 | |

| 0.0540 | 0.0171 | 0.8278 | |

| 0.0050 | 0.0016 | 0.0737 | |

| 0.0654 | 0.0216 | 1.3483 | |

| 0.0683 | 0.0219 | 1.2969 | |

| 0.0051 | 0.0016 | 0.0592 |

It is worth noting that the initial allocation for long and short positions, , influences the gain-loss performance; see Figure 5. As a result, we conduct the backtesting with varying as demonstrated in Figure 10. Our analysis reveals that a positive gain-loss is attained for , while negative gain-loss is observed for , considering a transaction cost of per trade and an annual risk-free rate of . This phenomenon in gain-loss can be attributed to the bullish market trends present in the testing data for the year 2023.

6 Concluding Remark

In this paper, we investigated the stochastic robustness of a novel trading scheme called the multi-double linear policy within a generalized lattice market that accounts for both serially correlated returns and asset correlation. We proved that our policies assure survivability and probabilistic positivity. We derived a detailed gain-loss performance analysis, leading to the derivation of an analytic expression for the worst-case expected gain-loss and evidence that the proposed policies might sustain an “approximate” robust positive expected profit. Additionally, we proved sufficient conditions that multi-double linear policies can lead to positive expected profits if the market has a clear trend. This remarkable result holds true even within a symmetric lattice market. Through a conditional probabilistic model, we uncovered that the parameter space of our mode forms a convex polyhedron, estimated efficiently via a constrained least-squares method. Validated by extensive empirical studies with S&P 30 assets, we substantiate robust support for the theoretical findings.

As for future research, extending our analysis to the current findings to involve time-varying weights with time-varying movement factors and or even a return model that takes multiple outcomes, e.g., state prices duffie2010dynamic, luenberger2013investment. We envision this extension may necessitate the development of innovative mathematical tools to navigate the highly nonlinear, stochastic, and correlated nature of such models. Additionally, the impact of transaction costs could be considered to embed into the model to enhance the practicality of the proposed trading policy; see hsieh2022robustness for an initial result along this line of research. Lastly, as the generalized lattice model fits well in a daily basis time scale, it is interesting to see if the model works well in high-frequency settings, such as tick-by-tick basis; see goldstein2022high.

References

- Balvers and Mitchell (1997) Balvers RJ, Mitchell DW (1997) Autocorrelated Returns and Optimal Intertemporal Portfolio Choice. Management Science 43(11):1537–1551, URL http://dx.doi.org/10.1287/mnsc.43.11.1537.

- Barmish (2008) Barmish BR (2008) On Trading of Equities: A Robust Control Paradigm. IFAC Proceedings Volumes 41(2):1621–1626, URL http://dx.doi.org/10.3182/20080706-5-KR-1001.00276.

- Barmish and Primbs (2011) Barmish BR, Primbs JA (2011) On Arbitrage Possibilities via Linear Feedback in an Idealized Brownian Motion Stock Market. Proceedings of the IEEE Conference on Decision and Control (CDC) and European Control Conference (ECC), 2889–2894, URL http://dx.doi.org/10.1109/CDC.2011.6160731.

- Barmish and Primbs (2015) Barmish BR, Primbs JA (2015) On a New Paradigm for Stock Trading via a Model-Free Feedback Controller. IEEE Transactions on Automatic Control 61(3):662–676, URL http://dx.doi.org/10.1109/TAC.2015.2444078.

- Baumann (2016) Baumann MH (2016) On Stock Trading via Feedback Control when Underlying Stock Returns Are Discontinuous. IEEE Transactions on Automatic Control 62(6):2987–2992, URL http://dx.doi.org/10.1109/TAC.2016.2605743.

- Baumann (2023) Baumann MH (2023) On Theoretical Foundations of Mostly Model-Free Cross-Coupled Simultaneously Long-Short Stock Trading Controllers. European Journal of Control 100851, URL http://dx.doi.org/10.1016/j.ejcon.2023.100851.

- Baumann and Grüne (2019) Baumann MH, Grüne L (2019) Positive Expected Feedback Trading Gain for All Essentially Linearly Representable Prices. Proceedings of the Asian Control Conference (ASCC), 150–155.

- Boyd and Vandenberghe (2004) Boyd SP, Vandenberghe L (2004) Convex Optimization (Cambridge University Press).

- Campbell et al. (1993) Campbell JY, Grossman SJ, Wang J (1993) Trading Volume and Serial Correlation in Stock Returns. The Quarterly Journal of Economics 108(4):905–939.

- Casella and Berger (2001) Casella G, Berger RL (2001) Statistical Inference (Cengage Learning).

- Christoffersen and Diebold (2006) Christoffersen PF, Diebold FX (2006) Financial Asset Returns, Direction-of-Change Forecasting, and Volatility Dynamics. Management Science 52(8):1273–1287, URL http://www.jstor.org/stable/20110599.

- Cox et al. (1979) Cox JC, Ross SA, Rubinstein M (1979) Option Pricing: A Simplified Approach. Journal of Financial Economics 7(3):229–263, URL http://dx.doi.org/10.1016/0304-405X(79)90015-1.

- Cvitanic and Zapatero (2004) Cvitanic J, Zapatero F (2004) Introduction to the Economics and Mathematics of Financial Markets (MIT Press).

- Deshpande and Barmish (2018) Deshpande A, Barmish BR (2018) A Generalization of the Robust Positive Expectation Theorem for Stock Trading via Feedback Control. Proceedings of the European Control Conference (ECC), 514–520, URL http://dx.doi.org/10.1016/j.ifacol.2020.12.1249.

- Deshpande et al. (2020) Deshpande A, Gubner JA, Barmish BR (2020) On Simultaneous Long-Short Stock Trading Controllers with Cross-Coupling. IFAC-PapersOnLine 53(2):16989–16995, URL http://dx.doi.org/10.1016/j.ifacol.2020.12.1249.

- Dokuchaev (2002) Dokuchaev N (2002) Dynamic Portfolio Strategies: Quantitative Methods and Empirical Rules for Incomplete Information, volume 47 (Springer Science & Business Media).

- Dokuchaev and Savkin (1998) Dokuchaev N, Savkin A (1998) Asymptotic Arbitrage in a Stochastic Financial Market Model. Asymptotic Arbitrage in a Stochastic Financial Market Model, 100–104 (CESA’98 Conference Secretariat).

- Duffie (2010) Duffie D (2010) Dynamic Asset Pricing Theory (Princeton University Press).

- Fielitz (1971) Fielitz BD (1971) Stationarity of Random Data: Some Implications for the Distribution of Stock Price Changes. Journal of Financial and Quantitative Analysis 6(3):1025–1034, URL http://dx.doi.org/10.2307/2329918.

- Goldstein et al. (2022) Goldstein M, Kwan A, Philip R (2022) High-Frequency Trading Strategies. Management Science URL http://dx.doi.org/10.1287/mnsc.2022.4539.

- Granger and Hyung (2004) Granger CW, Hyung N (2004) Occasional Structural Breaks and Long Memory with an Application to the S&P 500 Absolute Stock Returns. Journal of Empirical Finance 11(3):399–421, URL http://dx.doi.org/10.1016/j.jempfin.2003.03.001.

- Hsieh (2022a) Hsieh CH (2022a) On Robust Optimal Linear Feedback Stock Trading. arXiv: 2202.02300 .

- Hsieh (2022b) Hsieh CH (2022b) On Robustness of Double Linear Trading with Transaction Costs. IEEE Control Systems Letters 7:679–684, URL http://dx.doi.org/10.1109/LCSYS.2022.3218541.

- Korajczyk and Sadka (2004) Korajczyk RA, Sadka R (2004) Are Momentum Profits Robust to Trading Costs? The Journal of Finance 59(3):1039–1082, URL https://www.jstor.org/stable/3694730.

- Luenberger (2013) Luenberger DG (2013) Investment Science (Oxford university press).

- Malekpour and Barmish (2016) Malekpour S, Barmish BR (2016) On Stock Trading Using a Controller with Delay: The Robust Positive Expectation Property. Proceedings of the IEEE Conference on Decision and Control (CDC), 2881–2887.

- Malekpour et al. (2018) Malekpour S, Primbs JA, Barmish BR (2018) A Generalization of Simultaneous Long–Short Stock Trading to PI Controllers. IEEE Transactions on Automatic Control 63(10):3531–3536, URL http://dx.doi.org/10.1109/TAC.2018.2799484.

- Maroni et al. (2019) Maroni G, Formentin S, Previdi F (2019) A Robust Design Strategy for Stock Trading via Feedback Control. Proceedings of the European Control Conference (ECC), 447–452.

- Officer (1972) Officer RR (1972) The Distribution of Stock Returns. Journal of the American Statistical Association 67(340):807–812, URL http://dx.doi.org/10.2307/2284641.

- O’Brien et al. (2020) O’Brien JD, Burke ME, Burke K (2020) A Generalized Framework for Simultaneous Long-Short Feedback Trading. IEEE Transactions on Automatic Control 66(6):2652–2663, URL http://dx.doi.org/10.1109/TAC.2020.3011914.

- Primbs and Barmish (2017) Primbs JA, Barmish BR (2017) On Robustness of Simultaneous Long-Short Stock Trading Control with Time-Varying Price Dynamics. IFAC-PapersOnLine 50(1):12267–12272, URL http://dx.doi.org/10.1016/j.ifacol.2017.08.2045.

- Primbs and Yamada (2018) Primbs JA, Yamada Y (2018) Pairs Trading under Transaction Costs using Model Predictive Control. Quantitative Finance 18(6):885–895, URL http://dx.doi.org/10.1080/14697688.2017.1374549.

- Tie et al. (2018) Tie J, Zhang H, Zhang Q (2018) An Optimal Strategy for Pairs Trading under Geometric Brownian Motions. Journal of Optimization Theory and Applications 179:654–675, URL http://dx.doi.org/10.1007/s10957-017-1065-8.

- Vitale (2018) Vitale P (2018) Robust Trading for Ambiguity-Averse Insiders. Journal of Banking & Finance 90:113–130, URL http://dx.doi.org/10.1016/j.jbankfin.2018.03.007.

- Wang and Hsieh (2023) Wang XY, Hsieh CH (2023) On Robustness of Double Linear Policy with Time-Varying Weights. Proceedings of the IEEE Conference on Decision and Control, forthcoming.

- Werner et al. (2023) Werner IM, Rindi B, Buti S, Wen Y (2023) Tick Size, Trading Strategies, and Market Quality. Management Science 69(7):3818–3837, URL http://dx.doi.org/doi.org/10.1287/mnsc.2022.4502.

Appendix A Technical Proofs of Sections 3 and 4

Proof of Lemma 3.1.

For , Asset has per-period returns with . Hence, the account value of the long position for the th asset is given by

where the last inequality hold since and and Similarly,

Hence, it follows that for all with probability one. To complete the proof, we note that if for some and and , then and are strictly positive. Hence, for all with probability one. ∎

Proof of Lemma 3.1.

Fix . Note that, by Lemma 3.1, for all with probability one. Observe that

where the last inequality holds by the Cauchy-Schwarz inequality. Hence, it follows that

Note that the denominator is

Therefore, we have

and the proof is complete. ∎

Proof of Lemma 3.2.

The proof is elementary. Fix for all . Note that with and . Using the fact that , it follows that Hence, the cumulative trading gain-loss function becomes for all where the last inequality hold since and ∎

Proof of Lemma 3.2.

By the law of total expectation, it can be computed by

for stage . Using the fact that and the initial conditions for , we then have the recursion for probability at stage ,

which completes the proof. ∎

Proof of Lemma 3.2.

By Lemma 3.2, the per-period returns of Asset have Bernoulli distribution with time-varying probability . Hence, the expectation of for a single stage is given by Hence, summing up stages yields

where is the expected number of the return process of Asset that receives positive returns up to stage . An almost identical proof would work for the short side, i.e.,

which completes the proof. ∎

Proof of Corollary 3.1.

To prove part , we fix . Noting that if , it would increase the ; hence, without loss of generality, we may restrict our attention to the case in the proof that follows. Begin by considering the case . We first compute the functions and in Theorem 3.1; i.e., and Substituting these two quantities to the lower bound for in Theorem 3.1, we obtain where the last inequality holds by the facts that and for all and all . An almost identical proof would work for the case of . Indeed, in this case, it is readily verified that To prove part , we note that for and take for all . Applying Theorem 3.1, it is readily verified that for all immediately. ∎

Proof of Lemma 3.2.

The strict convexity is established by invoking the second-order derivative test. That is, for any , where the last inequality holds since with and and To complete the proof, we must find the minimum, call it . Indeed, the first-order condition leads to That is, is the minimum of if and only if . Moreover, note that if and , then is increasing and is decreasing. This implies that the sum has a unique minimum . Likewise, if and , then is decreasing and is increasing, hence again has a unique minimum ∎

Proof of Corollary 3.4.

Fix . Without loss of generality, we shall give proof for the case as the methodology for proving another side follows an almost identical argument. Indeed, for , implies that there exists a constant such that . Now, take . Theorem 3.1 implies that the expected gain-loss function satisfies

| (11) |

where the two quantities and satisfy

and

Since for all , it is readily verified that and Substituting these into Inequality (11) yields

which is desired.

Similarly, for the case implies that there exists a constant such that . Following the similar method, take and , by Theorem 3.1, we have

where and . It follows that

To prove part , take in the proof above, then one immediately obtains and the proof is complete. ∎

Proof of Lemma 3.3.

Fix with . An elementary calculus proof would work for verifying the strict increasingness of the function . That is, . Proceeds with a proof by contradiction by assuming that the function was not strictly increasing. Then we have Equivalently

| (12) |

If , then . Hence Inequality (12) implies that for , which is absurd since it contradicts . On the other hand, if , then . In this case, Inequality (12) becomes for , which is again absurd. Therefore, for and the function is a strictly increasing function. To complete the proof, invoking a usual limiting argument leads to ∎

Proof of Lemma 4.3.

For and , we begin by re-expressing the products , , , and as

Hence, the conditions with holds if and only if

Therefore, it suffices to ensure that the following inequalities hold

Via a straightforward calculation, it follows that and

These conditions can be written as

To complete the proof, we note that the inequalities are linear in and , which forms a convex polyhedron. ∎

Appendix B Estimated Parameters of the S&P 30 Stocks

This appendix summarizes the estimated parameters for the S&P 30 stocks used in Section 5. Table 3 include the estimated movement factors and , Tables 4 to 7 summarize the estimated serial correlation coefficients with various memory length , and Table 8 record the asset correlation coefficient matrix . In the following tables, the symbol “mean” refers to the average of the data and“std” refers to the standard deviation of the data.

| AAPL | 0.0173 | -0.0175 |

|---|---|---|

| ABBV | 0.0101 | -0.0109 |

| ADBE | 0.0207 | -0.0212 |

| AMZN | 0.0229 | -0.0242 |

| AVGO | 0.0187 | -0.0182 |

| BAC | 0.0165 | -0.0146 |

| BRK.B | 0.0112 | -0.0108 |

| COST | 0.0138 | -0.0143 |

| CSCO | 0.0136 | -0.0129 |

| CVX | 0.0158 | -0.0163 |

| GOOG | 0.0183 | -0.0190 |

| GOOGL | 0.0188 | -0.0188 |

| HD | 0.0146 | -0.0153 |

| JNJ | 0.0088 | -0.0080 |

| JPM | 0.0149 | -0.0142 |

| KO | 0.0086 | -0.0099 |

| LLY | 0.0141 | -0.0127 |

| MA | 0.0156 | -0.0152 |

| MCD | 0.0099 | -0.0089 |

| META | 0.0249 | -0.0299 |

| MRK | 0.0099 | -0.0089 |

| MSFT | 0.0173 | -0.0170 |

| NVDA | 0.0305 | -0.0333 |

| PEP | 0.0088 | -0.0092 |

| PG | 0.0101 | -0.0107 |

| TSLA | 0.0291 | -0.0349 |

| UNH | 0.0108 | -0.0130 |

| V | 0.0144 | -0.0143 |

| WMT | 0.0106 | -0.0120 |

| XOM | 0.0174 | -0.0175 |

| mean | 0.0156 | -0.0161 |

| std | 0.0057 | 0.0069 |

| min | 0.0086 | -0.0349 |

| max | 0.0305 | -0.0080 |

| AAPL | 0.4743 | -7.0577 |

|---|---|---|

| ABBV | 0.5648 | -3.3926 |

| ADBE | 0.4675 | -4.5233 |

| AMZN | 0.4637 | -3.1458 |

| AVGO | 0.4934 | -7.1075 |

| BAC | 0.4425 | -1.7751 |

| BRK.B | 0.5066 | -8.0508 |

| COST | 0.4891 | -5.7026 |

| CSCO | 0.4554 | -6.9281 |

| CVX | 0.5713 | -0.4806 |

| GOOG | 0.4617 | -6.5382 |

| GOOGL | 0.4505 | -7.0812 |

| HD | 0.4898 | -4.4559 |

| JNJ | 0.4915 | -4.9624 |

| JPM | 0.4778 | -4.6107 |

| KO | 0.5666 | -6.6020 |

| LLY | 0.5287 | -0.5153 |

| MA | 0.5037 | -7.0355 |

| MCD | 0.4806 | -10.0977 |

| META | 0.4717 | -3.4837 |

| MRK | 0.5634 | -2.5778 |

| MSFT | 0.4679 | -8.2390 |

| NVDA | 0.4914 | -2.0229 |

| PEP | 0.5407 | -9.1421 |

| PG | 0.5140 | -5.9338 |

| TSLA | 0.4901 | -1.3042 |

| UNH | 0.5670 | -9.1984 |

| V | 0.5042 | -5.5996 |

| WMT | 0.5403 | -2.6996 |

| XOM | 0.5775 | 0.2417 |

| mean | 0.5036 | -5.0007 |

| std | 0.0406 | 2.8112 |

| min | 0.4425 | -10.0977 |

| max | 0.5775 | 0.2417 |

| AAPL | 0.4724 | -6.8957 | -3.2137 |

|---|---|---|---|

| ABBV | 0.5710 | -3.2523 | -4.3757 |

| ADBE | 0.4676 | -4.5708 | -1.2987 |

| AMZN | 0.4637 | -2.9836 | -0.9418 |

| AVGO | 0.4922 | -7.0590 | -0.2977 |

| BAC | 0.4406 | -1.9511 | 0.2551 |

| BRK.B | 0.5054 | -8.0853 | -3.9996 |

| COST | 0.4909 | -5.8565 | -0.9620 |

| CSCO | 0.4562 | -7.0756 | -1.4489 |

| CVX | 0.5732 | -0.4694 | -1.8346 |

| GOOG | 0.4608 | -6.3603 | -1.6429 |

| GOOGL | 0.4480 | -6.9173 | -2.4574 |

| HD | 0.4849 | -4.1834 | -4.1064 |

| JNJ | 0.4939 | -4.7201 | -1.8473 |

| JPM | 0.4776 | -4.8785 | 3.6627 |

| KO | 0.5656 | -6.7373 | -1.6632 |

| LLY | 0.5304 | -0.7643 | 0.8080 |

| MA | 0.5017 | -7.1727 | 0.0707 |

| MCD | 0.4822 | -9.7406 | 2.5554 |

| META | 0.4649 | -3.4820 | -2.1993 |

| MRK | 0.5651 | -2.7137 | -1.9016 |

| MSFT | 0.4675 | -8.3801 | -2.6249 |

| NVDA | 0.4920 | -1.8762 | -0.6963 |

| PEP | 0.5398 | -9.0190 | -1.0837 |

| PG | 0.5130 | -5.7470 | 2.9805 |

| TSLA | 0.4904 | -1.2043 | -0.5430 |

| UNH | 0.5691 | -9.0458 | -0.0528 |

| V | 0.5021 | -5.6236 | -1.9024 |

| WMT | 0.5427 | -2.9355 | 0.0720 |

| XOM | 0.5773 | 0.1968 | -0.4443 |

| mean | 0.5034 | -4.9835 | -1.0378 |

| std | 0.0417 | 2.7656 | 1.8998 |

| min | 0.4406 | -9.7406 | -4.3757 |

| max | 0.5773 | 0.1968 | 3.6627 |

| AAPL | 0.4903 | -6.0457 | -2.5566 | 1.3849 | -0.5490 | 1.6469 |

|---|---|---|---|---|---|---|

| ABBV | 0.5774 | -3.4784 | -4.6048 | -3.4273 | -0.1246 | -0.1277 |

| ADBE | 0.4706 | -4.7356 | -1.6543 | 1.4729 | -1.5489 | -1.0536 |

| AMZN | 0.4670 | -3.0835 | -0.9198 | -0.2644 | -2.0204 | 1.5314 |

| AVGO | 0.4960 | -7.2420 | -0.4197 | -0.1947 | -0.0650 | -1.7599 |

| BAC | 0.4369 | -1.8106 | 0.3323 | -0.0738 | -1.6913 | 1.8038 |

| BRK.B | 0.4974 | -8.8585 | -4.9791 | 0.6956 | -1.9145 | -2.2998 |

| COST | 0.4967 | -6.3076 | -1.1686 | -1.8999 | -2.6737 | 4.0319 |

| CSCO | 0.4513 | -7.2763 | -1.2937 | 2.1238 | -1.5100 | -1.8733 |

| CVX | 0.5620 | -0.8948 | -2.0258 | -0.1786 | 1.8117 | 1.7782 |

| GOOG | 0.4666 | -6.5287 | -1.5938 | -0.3628 | -2.0394 | 0.5425 |

| GOOGL | 0.4657 | -6.4507 | -1.9203 | 0.0000 | -2.2459 | 0.0000 |

| HD | 0.4913 | -4.2705 | -4.1762 | 0.3816 | 0.6885 | 0.5236 |

| JNJ | 0.4866 | -4.9292 | -2.8317 | 3.0761 | 3.2063 | 10.3256 |

| JPM | 0.4720 | -4.8995 | 4.0073 | 0.3229 | -1.6667 | -1.8565 |

| KO | 0.5686 | -7.1570 | -1.5807 | -0.7660 | -1.9007 | -0.2845 |

| LLY | 0.5337 | -0.8408 | 0.9450 | -0.6955 | -3.2962 | 2.9291 |

| MA | 0.5069 | -7.3545 | 0.1202 | 0.5930 | 0.2353 | 0.3416 |

| MCD | 0.4828 | -9.5574 | 2.9993 | -3.3113 | 2.2448 | 6.0217 |

| META | 0.4621 | -3.4509 | -2.1904 | -0.3271 | -0.8298 | 0.0918 |

| MRK | 0.5669 | -2.1407 | -2.0788 | -2.3531 | 3.5751 | -3.9520 |

| MSFT | 0.4835 | -7.6361 | -1.9472 | -0.6301 | 0.0000 | -1.7776 |

| NVDA | 0.4882 | -1.9375 | -0.4615 | -1.1027 | -1.0826 | 0.1271 |

| PEP | 0.5364 | -10.4331 | -1.7617 | -2.7711 | -5.2843 | -3.3639 |

| PG | 0.5139 | -5.5992 | 3.3013 | -2.0523 | 2.6299 | -2.4837 |

| TSLA | 0.4904 | -1.3581 | -0.5920 | -0.4209 | 0.4666 | -1.3029 |

| UNH | 0.5779 | -9.8296 | -0.6249 | -1.8474 | -0.2913 | -0.2166 |

| V | 0.5070 | -5.8935 | -1.8933 | -0.5778 | -1.7258 | 0.2817 |

| WMT | 0.5407 | -2.3627 | -0.1161 | 0.7031 | -2.0813 | 0.8319 |

| XOM | 0.5644 | -0.1731 | -0.7313 | 0.3908 | 2.1484 | 1.0343 |

| mean | 0.5050 | -5.0845 | -1.0806 | -0.4037 | -0.5845 | 0.3830 |

| std | 0.0402 | 2.8674 | 2.0398 | 1.5045 | 2.0326 | 2.8278 |

| min | 0.4369 | -10.4331 | -4.9791 | -3.4273 | -5.2843 | -3.9520 |

| max | 0.5779 | -0.1731 | 4.0073 | 3.0761 | 3.5751 | 10.3256 |

| AAPL | 0.4867 | -6.0468 | -2.3184 | 1.0992 | 0.0000 | 1.1757 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | -1.3424 |

|---|---|---|---|---|---|---|---|---|---|---|---|

| ABBV | 0.5722 | -3.0746 | -4.3332 | -3.2077 | -0.2310 | -0.0760 | -0.0477 | 0.2086 | 1.7399 | 0.6545 | -2.9690 |

| ADBE | 0.4714 | -4.3141 | -1.1528 | 1.1536 | -1.1368 | -0.3080 | 0.0000 | 0.0000 | -1.6589 | -0.8618 | -0.6552 |

| AMZN | 0.4787 | -2.8012 | -0.4456 | -0.3153 | -1.9531 | 1.3428 | 0.0000 | -0.7664 | -0.8991 | 0.7221 | 1.0201 |

| AVGO | 0.5082 | -6.5873 | 0.0000 | 0.0000 | 0.0000 | -1.1906 | -3.3023 | 0.0000 | -0.8407 | -0.6345 | -0.6275 |

| BAC | 0.4393 | -1.3490 | -0.0889 | -0.0362 | -1.2976 | 2.2879 | -2.7961 | 0.6335 | -2.9673 | 1.7658 | 0.1447 |

| BRK.B | 0.4964 | -8.6050 | -4.4898 | 0.0000 | -1.2611 | -2.0547 | -0.0023 | 1.7707 | -0.7803 | 1.3104 | 1.4179 |

| COST | 0.5027 | -6.3884 | -0.6677 | -1.7687 | -2.6611 | 3.6459 | 1.0455 | -0.5666 | 1.2112 | 0.5117 | 1.1456 |

| CSCO | 0.4658 | -7.1298 | -1.0377 | 2.5167 | -0.0741 | -0.5531 | -1.2505 | 2.3559 | -0.0075 | 2.6266 | -0.4315 |

| CVX | 0.5627 | -0.4194 | -2.1235 | -0.1231 | 1.8365 | 1.8130 | -2.0245 | 2.6408 | -2.5675 | 1.7544 | -0.6850 |

| GOOG | 0.4672 | -6.1960 | -1.3498 | 0.0000 | -1.7443 | 0.5515 | -0.0591 | 0.0000 | -0.0387 | 0.1627 | 0.9563 |

| GOOGL | 0.4602 | -6.3070 | -1.8457 | 0.0000 | -2.1501 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0000 | 0.0190 |

| HD | 0.5025 | -4.7400 | -4.6531 | -0.3289 | 0.2936 | 0.4028 | -0.5937 | 1.3441 | 1.0331 | 2.0433 | 2.1760 |

| JNJ | 0.5006 | -5.7181 | -3.9292 | 3.4345 | 2.8180 | 11.8124 | 0.1560 | -0.5695 | -2.5858 | 0.3663 | -5.4969 |

| JPM | 0.4785 | -4.5622 | 3.2834 | 0.2067 | -0.6562 | -1.5361 | -0.1417 | 0.5352 | 0.7523 | 3.2933 | -2.8566 |

| KO | 0.5604 | -7.5233 | -1.6110 | -1.0146 | -2.1853 | 0.0297 | -6.1188 | 2.9035 | 0.9533 | 0.0414 | -0.2377 |

| LLY | 0.5350 | -0.8946 | 1.2286 | 0.2687 | -3.6011 | 3.1966 | 0.0389 | -1.2349 | -3.2674 | 4.8204 | -0.4896 |

| MA | 0.5014 | -8.0033 | -0.1182 | 0.5164 | 0.9363 | 0.7731 | 0.0000 | -1.4314 | -2.9440 | -0.7316 | 0.3741 |

| MCD | 0.4984 | -9.4845 | 1.8615 | -2.3841 | 1.0978 | 3.7620 | 3.7078 | 2.8442 | -3.3899 | 0.6593 | 3.6118 |

| META | 0.4688 | -3.3157 | -1.8679 | -0.5192 | -0.7732 | 0.3499 | -1.1460 | 1.1556 | 0.6323 | 0.0000 | -0.8245 |

| MRK | 0.5501 | -2.8590 | -1.1644 | -2.1002 | 2.6720 | -3.5841 | 0.2096 | 0.0355 | 6.0822 | 2.8016 | 1.7149 |

| MSFT | 0.4826 | -7.4980 | -1.6388 | -0.1095 | 0.0000 | -1.1698 | -1.2919 | 0.0000 | 0.0000 | 0.2375 | 0.0000 |

| NVDA | 0.4831 | -1.7214 | -0.4927 | -1.0516 | -1.1298 | 0.2661 | -0.4853 | 0.8280 | -0.8354 | -0.3877 | 0.3978 |

| PEP | 0.5298 | -10.4575 | -0.7566 | -1.9033 | -5.1067 | -2.7873 | -3.3101 | 2.0992 | -0.1821 | 0.4434 | -2.7524 |

| PG | 0.5165 | -5.5333 | 2.5618 | -1.9286 | 3.3486 | -2.7486 | -0.2179 | -0.9519 | -1.0760 | 0.8461 | -0.0148 |

| TSLA | 0.4973 | -0.8211 | -0.5040 | -0.2528 | 0.6465 | -1.2883 | 0.3078 | 2.3891 | -1.4361 | 1.4047 | -0.8947 |

| UNH | 0.5718 | -8.7663 | -0.0536 | -0.7555 | 0.0000 | 0.0000 | -1.1147 | 0.1035 | 0.0000 | 1.7695 | -6.8970 |

| V | 0.5082 | -6.2467 | -1.6439 | -0.7032 | -1.6754 | 0.0739 | -1.0217 | -1.6165 | -0.7638 | -2.4145 | -1.9267 |

| WMT | 0.5482 | -2.2058 | -0.5936 | 0.9173 | -2.7262 | 0.9771 | -0.7612 | 0.1939 | 1.1571 | -1.2646 | 3.2698 |

| XOM | 0.5674 | 0.5619 | -0.4573 | 0.3952 | 2.2481 | 1.3658 | -2.9903 | 2.7908 | 0.6023 | 1.5257 | -2.6165 |

| mean | 0.5071 | -4.9669 | -1.0134 | -0.2665 | -0.4822 | 0.5510 | -0.7737 | 0.5898 | -0.4026 | 0.7822 | -0.5157 |

| std | 0.0368 | 2.9305 | 1.8586 | 1.3714 | 1.9466 | 2.7760 | 1.7149 | 1.3465 | 1.8901 | 1.4626 | 2.2513 |

| min | 0.4393 | -10.4575 | -4.6531 | -3.2077 | -5.1067 | -3.5841 | -6.1188 | -1.6165 | -3.3899 | -2.4145 | -6.8970 |

| max | 0.5722 | 0.5619 | 3.2834 | 3.4345 | 3.3486 | 11.8124 | 3.7078 | 2.9035 | 6.0822 | 4.8204 | 3.6118 |

| AAPL | ABBV | ADBE | AMZN | AVGO | BAC | BRK.B | COST | CSCO | CVX | GOOG | GOOGL | HD | JNJ | JPM | KO | LLY | MA | MCD | META | MRK | MSFT | NVDA | PEP | PG | TSLA | UNH | V | WMT | XOM | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| AAPL | 0 | .24 | .71 | .70 | .76 | .57 | .69 | .63 | .64 | .29 | .79 | .80 | .60 | .37 | .55 | .52 | .36 | .75 | .51 | .59 | .28 | .82 | .76 | .55 | .46 | .64 | .49 | .70 | .34 | .28 |

| ABBV | - | 0 | .18 | .21 | .26 | .30 | .41 | .30 | .31 | .16 | .22 | .22 | .28 | .51 | .35 | .42 | .51 | .28 | .32 | .10 | .49 | .28 | .19 | .43 | .44 | .06 | .51 | .30 | .25 | .18 |

| ADBE | - | - | 0 | .65 | .71 | .42 | .52 | .54 | .54 | .22 | .72 | .73 | .61 | .20 | .43 | .35 | .30 | .66 | .37 | .60 | .15 | .77 | .72 | .39 | .33 | .50 | .29 | .62 | .27 | .20 |

| AMZN | - | - | - | 0 | .66 | .55 | .57 | .56 | .48 | .31 | .72 | .72 | .57 | .23 | .50 | .36 | .27 | .60 | .34 | .61 | .16 | .74 | .71 | .36 | .24 | .59 | .32 | .55 | .30 | .25 |

| AVGO | - | - | - | - | 0 | .56 | .62 | .57 | .66 | .30 | .73 | .74 | .59 | .25 | .56 | .42 | .32 | .67 | .44 | .56 | .18 | .76 | .83 | .43 | .39 | .59 | .41 | .61 | .22 | .27 |

| BAC | - | - | - | - | - | 0 | .71 | .41 | .50 | .36 | .54 | .54 | .43 | .31 | .90 | .44 | .25 | .60 | .47 | .42 | .26 | .56 | .55 | .40 | .36 | .41 | .42 | .59 | .23 | .31 |

| BRK.B | - | - | - | - | - | - | 0 | .55 | .60 | .47 | .62 | .63 | .57 | .48 | .71 | .62 | .43 | .65 | .50 | .43 | .37 | .64 | .58 | .55 | .46 | .41 | .49 | .62 | .36 | .43 |

| COST | - | - | - | - | - | - | - | 0 | .54 | .23 | .57 | .57 | .65 | .41 | .42 | .56 | .36 | .49 | .49 | .37 | .21 | .61 | .56 | .58 | .54 | .46 | .50 | .48 | .59 | .20 |

| CSCO | - | - | - | - | - | - | - | - | 0 | .25 | .57 | .57 | .52 | .41 | .53 | .55 | .43 | .54 | .50 | .42 | .33 | .59 | .55 | .55 | .51 | .36 | .44 | .51 | .36 | .21 |

| CVX | - | - | - | - | - | - | - | - | - | 0 | .26 | .26 | .17 | .12 | .30 | .19 | .20 | .24 | .13 | .19 | .20 | .26 | .28 | .15 | 0 | .17 | .25 | .21 | .20 | .88 |

| GOOG | - | - | - | - | - | - | - | - | - | - | 0 | 1 | .56 | .27 | .51 | .37 | .32 | .66 | .40 | .68 | .23 | .85 | .77 | .41 | .34 | .55 | .39 | .59 | .31 | .21 |

| GOOGL | - | - | - | - | - | - | - | - | - | - | - | 0 | .56 | .27 | .51 | .38 | .32 | .66 | .41 | .68 | .23 | .85 | .77 | .42 | .35 | .55 | .40 | .60 | .31 | .22 |

| HD | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .38 | .48 | .51 | .38 | .57 | .43 | .48 | .25 | .62 | .57 | .52 | .47 | .35 | .39 | .54 | .41 | .14 |

| JNJ | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .35 | .57 | .60 | .30 | .48 | .16 | .64 | .32 | .18 | .59 | .59 | .10 | .55 | .31 | .33 | .09 |

| JPM | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .46 | .31 | .60 | .52 | .39 | .29 | .53 | .53 | .43 | .39 | .37 | .44 | .58 | .23 | .28 |

| KO | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .43 | .50 | .63 | .22 | .42 | .46 | .34 | .84 | .75 | .23 | .54 | .50 | .43 | .18 |

| LLY | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .38 | .45 | .29 | .59 | .38 | .28 | .47 | .37 | .19 | .56 | .41 | .24 | .18 |

| MA | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .55 | .53 | .29 | .73 | .68 | .49 | .44 | .47 | .42 | .93 | .26 | .27 |

| MCD | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .23 | .43 | .47 | .41 | .68 | .57 | .25 | .50 | .53 | .34 | .13 |

| META | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .22 | .63 | .61 | .28 | .24 | .39 | .18 | .46 | .18 | .14 |

| MRK | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .25 | .10 | .45 | .45 | .02 | .50 | .30 | .23 | .19 |

| MSFT | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .79 | .49 | .44 | .55 | .46 | .66 | .32 | .22 |

| NVDA | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .35 | .29 | .67 | .35 | .62 | .23 | .23 |

| PEP | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .74 | .22 | .56 | .48 | .47 | .16 |

| PG | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .15 | .54 | .43 | .42 | .03 |

| TSLA | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .28 | .44 | .17 | .16 |

| UNH | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .41 | .33 | .22 |

| V | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .22 | .24 |

| WMT | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 | .17 |

| XOM | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | - | 0 |