Fast Sampling and Inference via Preconditioned Langevin Dynamics

Abstract

Sampling from distributions play a crucial role in aiding practitioners with statistical inference. However, in numerous situations, obtaining exact samples from complex distributions is infeasible. Consequently, researchers often turn to approximate sampling techniques to address this challenge. Fast approximate sampling from complicated distributions has gained much traction in the last few years with considerable progress in this field, for example, [6, 10]. Previous work [24] has shown that for some problems a preconditioning can make the algorithm faster. In our research, we explore the Langevin Monte Carlo (LMC) algorithm and demonstrate its effectiveness in enabling inference from the obtained samples. Additionally, we establish a convergence rate for the LMC Markov chain in total variation. Lastly, we derive non-asymptotic bounds for approximate sampling from specific target distributions in the Wasserstein distance, particularly when the preconditioning is spatially invariant.

1 Introduction

Sampling focuses on generating observations from a particular population for statistical analysis. Recently a lot of emphasis in literature has been on fast sampling for a large class of problems, for example, [3, 7, 9]. In this field of research, a notable trend is the observation of similarities between sampling and optimization methods. Researchers have successfully exploited this connection in numerous studies, resulting in the development of rapid sampling algorithms. These algorithms effectively generate observations from distributions characterized by densities in the form of with ; see, for example, [5, 6, 10].

In most literature the function is taken to be strongly convex with Lipschitz gradient. Recall that a function satisfies both conditions if

| (1.1) |

for all . The main intuition for this setting comes as follows; strong convexity and Lipschitz gradient are the conditions in which optimization algorithms work better. In fact, multiple algorithms in the fast sampling literature optimize the log-likelihood and use the mode as a warm start for the sampling algorithm [6]. The Langevin Monte Carlo algorithm has been studied in multiple works, for example, [5, 6, 9, 10, 21, 22] and is considered as the sampling analogue of the gradient descent algorithm.

There exist optimization algorithms that are variants of gradient descent algorithm, achieved by applying a positive definite matrix as a preconditioner to the gradient. This technique ensures faster convergence, as demonstrated in previous studies [13, 14]. Interestingly, these algorithms predate the gradient descent, with Newton’s method being one of the earliest examples following this approach. We consider a similar setup for sampling by preconditioning the LMC algorithm with a fixed positive definite matrix. Similar work in literature can be found in the use of Metropolis Adjusted Langevin Algorithm using preconditioning and in some reinforcement learning setups, for example, [12, 25, 27], which serve as the main motivation for our work. In fact, the work on preconditioned MALA [24] exhibit that preconditioning appropriately ensure a decrease in the effective sample size, which is defined as the number of samples from independent data having the same estimating power as that of a given number of correlated samples. A decrease in effective sample size in this case implies that implies that preconditioning in a “correct fashion” ensures the requirement of lesser samples for inferential purposes. In reinforcement learning, existing literature has stated that the Langevin Monte Carlo when used for the purposes of Thomson Sampling exhibit faster mixing in practice under preconditioning [25]. Taking these works to serve as our motivation we consider the problem of establishing approximate sampling and inferential guarantees for the preconditioned Langevin Monte Carlo algorithm which has not been addressed in literature previously to the best of our knowledge.

Throughout this work we shall study the Langevin Monte Carlo algorithm where the gradient and the noise are preconditioned using a function which is positive definite at each point in . The equation for the algorithm is given by

| (1.2) |

where and are the step-size and Gaussian noise, respectively. Note that the matrix is the usual square root matrix which is indeed well defined as is positive definite. Also note that when , the identity matrix, the algorithm reduces to the standard LMC algorithm. In this work we consider two problems through the preconditioned LMC algorithm: the inference and the approximate sampling from distributions. In both cases, we assume that satisfies (1.1). In the former case we establish rates of convergence of the Markov Chain (1.2) to a stationary distribution dependent on with respect to the total variation distance. We also establish a Central Limit Theorem (CLT) for the samples generated by (1.2). Note that in this regime , i.e., we may increase the number of iterations indefinitely and the approximation indeed becomes better as grows larger. In the second case, we establish that we may use (1.2) with to sample from distributions with densities proportional to . In this regime the number of iterations is bounded by some , which is the maximum number of iterations of the algorithm permissible given a fixed step size . We show that when the maximum number of iterations is large and is small such that the product , the fixed time horizon, is large, the distribution of is close to the distribution corresponding the density (which we denote by ) with respect to the Wasserstein metric.

Now we make a summary about the new features of this paper. To the best of our knowledge, these two problems have not been addressed in previous literature and hence our analysis is probably the first try. In our work, as mentioned previously, we consider the problem of inferential and approximate sampling guarantees using the preconditioned LMC algorithm. In this regard we establish a Central Limit Theorem for preconditioned LMC around the mode which may be used for the purposes of statistical inference. We also, in addition to this, establish explicit convergence bounds of the algorithm to some stationary distribution in the Total Variation norm. We also establish approximate sampling bounds, in the Wasserstein distance, given a specific target as a function of the step size and the dimension. These results seem to be new in literature and are the main theoretical contributions of our paper.

We need two probability distances to state our main results in Section 2. Recall that the total variation distance between two probability measures and is defined by

where is the set of all Borel sets in Also the Wasserstein-Monge-Kantorvich distance between and on is defined by

| (1.3) |

where the infimum is taken over all probability measure and is the set of probability measures on with and being its marginal probability measures on , respectively.

2 Main Results

As mentioned in the introduction, it has been seen in practise that preconditioning the LMC algorithm indeed speeds it up for some problems as in its optimization counterparts. Taking this to be our inspiration, we study the preconditioned Langevin Monte Carlo algorithm and consider two problems in our work. The first is analyzing the preconditioned LMC algorithm in the regime where in Section 2.1. In this case our main objective is to ascertain whether the algorithm converges to some stationary distribution (which is not the target distribution) and whether we can use samples from the algorithm for inference on the mode of the target distribution. This will allow us to construct confidence intervals and carry out hypothesis tests. The second case is treated in Section 2.2, in which we sample up to some finite , where is the set of natural numbers, and then use them as an approximate sample from the target distribution. As for preconditioning matrices appeared in both cases, in the first case we consider them to be spatially varying. In the second case, we choose them to be fixed matrices due to technical considerations.

There has been some recent work on the analysis of preconditioned algorithms [24, 11, 4]. These works mainly address the problem of establishing guarantees for fast sampling using preconditioned LMC in KL-divergence or in Wasserstein distance in the dissipative setting and also establishing geometric ergodicity conditions for the purpose of sampling using preconditioned MALA. The novelty of our results in the fast sampling case is the existence of non-asymptotic bounds in the Wasserstein distance, in the strongly convex regime, in terms of the dimension and the step size which we believe are novel. In the case of inference the novelty of our results lie in establishing a Central Limit Theorem and also obtain exact convergence bounds for the convergence of the preconditioned LMC algorithm to a stationary distribution, in total variation, dependent on the step size. Again, we believe that these results have not been established for the preconditioned algorithm and hence provide some addition to the already rich literature of fast sampling.

2.1 Inference from Preconditioned Langevin Monte Carlo

Consider the algorithm

| (2.1) |

which is the preconditioned LMC algorithm with a spatially varying preconditioning matrix . This algorithm has used predominantly in fast sampling when . We analyze this algorithm from an inferential perspective. We concentrate our efforts on three major points: a) does the algorithm have a stationary distribution and does it converge to that distribution? b) is the convergence geometric and can the rate be calculated? c) does a central limit theorem hold for the algorithm as observed in the case of SGD [20, 8]? Answering these questions is important as it allows us to know the reliability of our simulation and perform desired statistical tests. We need the following standard assumptions for the rest of the paper.

Assumption 1.

The function belongs to and is -strongly convex with -Lipschitz gradient i.e., it satisfies (1.1).

REMARK 2.1.

Note that Assumption 1 implies , where .

Here the notation for matrices and means that is non-negative definite. Remark 2.1 is well established and can be found in multiple previous works [5].

REMARK 2.2.

Note that the strong convexity of ensures that it has a minimum [2]. Let be the minimizer.

Assumption 2.

There exists such that for any .

Assumption 2 is standard in literature. It requires the preconditioning matrix to be bounded both above and below. This guarantees that the algorithm does not blow up or remain static at any instance. The exclusion of the two bounds means the condition number of the preconditioning matrix goes to infinity and hence the algorithm is hard to analyze. The following quantities will be needed to state our main results. Define

| (2.2) | ||||

where is any value between and and is the Lebesgue measure on . Also denote by the one-step Markov kernel for the Markov chain as defined by (1.2). This seems to abuse the notation for the probability of an event, however, it will be evident from the context.

THEOREM 1.

Proof.

The proof Theorem 1 is furnished in the Appendix A. ∎

REMARK 2.3.

Theorem 1 establishes a geometric convergence rate of the LMC Markov chain to some stationary distribution which is dependent on the step size of the algorithm.

PROPOSITION 2.1.

Proof.

The proof is provided in Appendix A. ∎

REMARK 2.4.

Note that and hence can be calculated/approximated if we can calculate or approximate and the latter of which is a hard problem.

PROPOSITION 2.2.

The statement of Theorem 1 holds with

Proof.

The proof is provided in the Appendix. ∎

REMARK 2.5.

Note that the value of may be easily calculated by drawing randomly from the ball centred at with radius and then accepting the number of samples that fall in . Multiplying the proportion of accepted by the volume of the ball should provide an estimate of .

One also notes that all values of the free parameter result in a value less than . Selecting an optimum value for is also a hard problem. One recommends practitioners to use multiple values of the free parameter in practise to find which works best. Next we present a Central Limit Theorem for the samples from (2.1) which may be used for inferential purposes.

Proof of Theorem 2.

Proof.

REMARK 2.6.

Note, this immediately implies that all one dimensional projections have a Central Limit Theorem.

2.2 Approximate Sampling from a Specified Target

In this section we focus on employing preconditioned LMC in an effort to sample from distributions with densities proportional to . For this point on we shall consider , i.e., the preconditioning is fixed. The reasoning for considering the algorithm as in (1.2) with is natural as it is the Euler discretization of the diffusion

| (2.3) |

where is the standard Brownian motion. We define and the condition number of . These quantities shall be used throughout the following this and the following chapters and are key quantities as expressed in our bounds later.

Having completed stating our assumptions, the immediate question that arises is-does (2.3) have the correct stationary distribution? The answer to the question is yes, it indeed does. Past work has indicated that diffusions of the form

| (2.4) |

have the correct stationary distribution subject to certain constraints for .

THEOREM 3.

Note that it immediately follows from Theorem 3 that we indeed have the unique stationary distribution as . This is easy to see as for (2.3), we have and hence the result follows. Note that considering a spatially varying preconditioning makes the problem much more complicated. There has been recent work [11] where the authors show convergence of LMC in a Riemannian Manifold with respect to the KL-divergence; however, the assumptions used by the authors is much stronger than what we use. Given that we indeed have the correct stationary distribution for the process (2.3), the next natural question is whether the law of the process converges to the stationary distribution. In this regard, there has been previous work for similar problems [5, 6, 9] and we follow in their footsteps.

The following proposition concludes that the continuous time Markov Chain associated with (2.3) is indeed geometrically converging in the Wasserstein distance where denotes the stationary distribution.

PROPOSITION 2.4.

Proof.

The proof of Proposition 2.4 is furnished in the Appendix. ∎

Note that this implies we converge exponentially to the stationary distribution with the rate being effected by how far away we are from the mode and there is a dependence on dimension. Also note that strong convexity is vital for our proof by noting the dependence of on the bound. Also note that the rate depends on the condition number of , .

Next we establish convergence bounds for the Euler discretization

of (2.3) to the stationary distribution of (2.3). Define the Ito process in the time interval as

| (2.5) |

Note that the marginals of (2.5) at time points have the same law as (1.2), that is, , where implies having the same law. Use to denote the measure of the random variable .

Define

and

| (2.6) |

Proof.

The proof of Theorem 4 is furnished in the appendix. ∎

REMARK 2.7.

Note that the smaller we consider , either needs to be increased or needs to be decreased. This implies that for large time horizon and small step size we shall sample from the target distribution with a small error.

REMARK 2.8.

Note that the selection of the step size is a sensitive problem for if the step-size is selected too small the algorithm needs time to explore the space. However, with the step size too large the algorithm returns incorrect results. Hence there should be an optimal step size which should vary depending the nature of the problem and preconditioning matrix used.

3 Examples and Simulations

We consider three different examples in the following sections to exhibit the properties of preconditioned LMC as espoused by us in the previous sections. In all three examples we shall consider a preconditioning as defined by

This is the first order AR(1) matrix where the value of determines it’s eigenvalues which are all positive. In our problems we consider different values of and exhibit how it affects our simulation findings. Our algorithm for each example obeys the following update rule

where for all whete is as previously espoused.

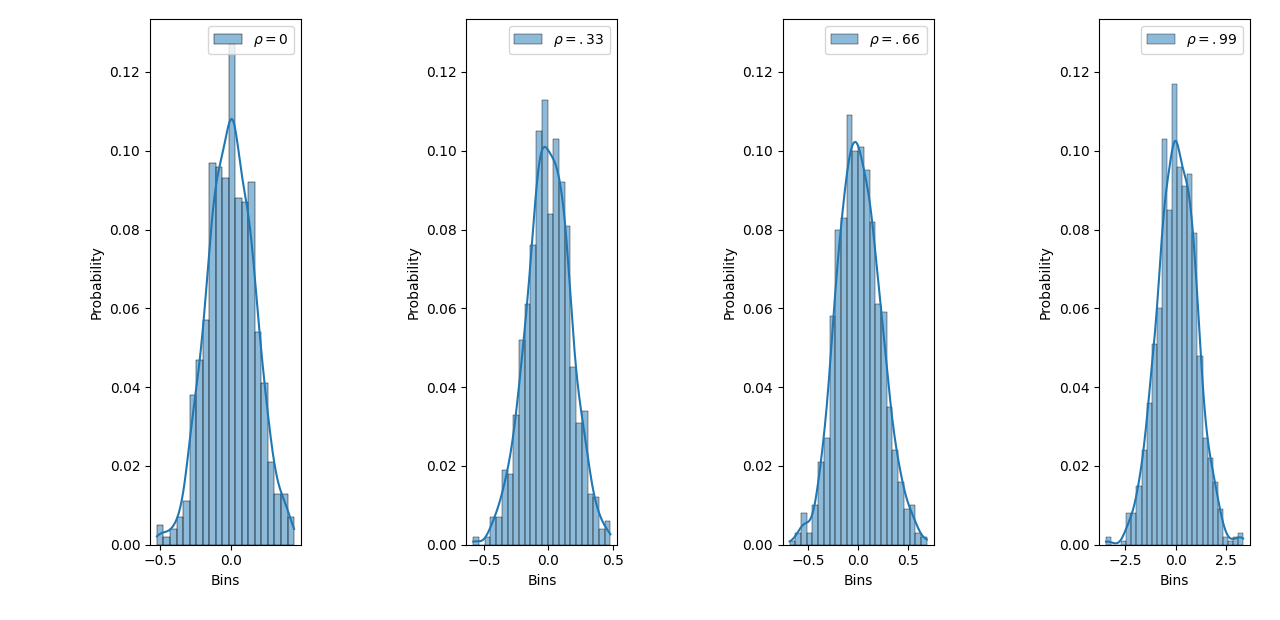

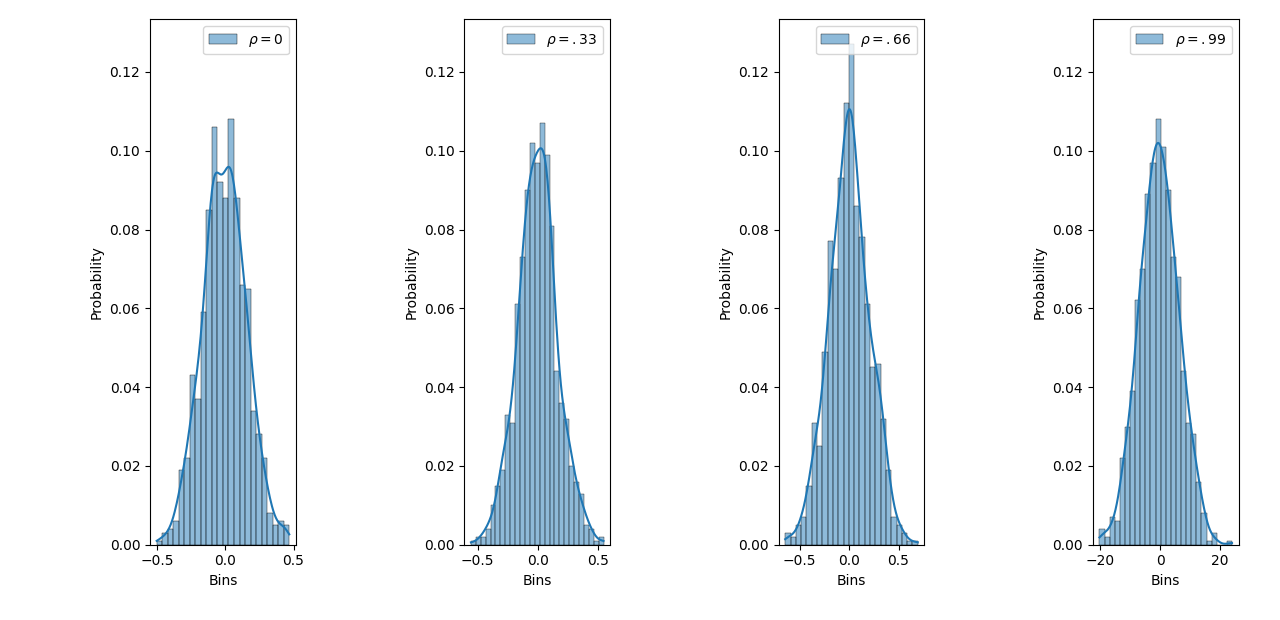

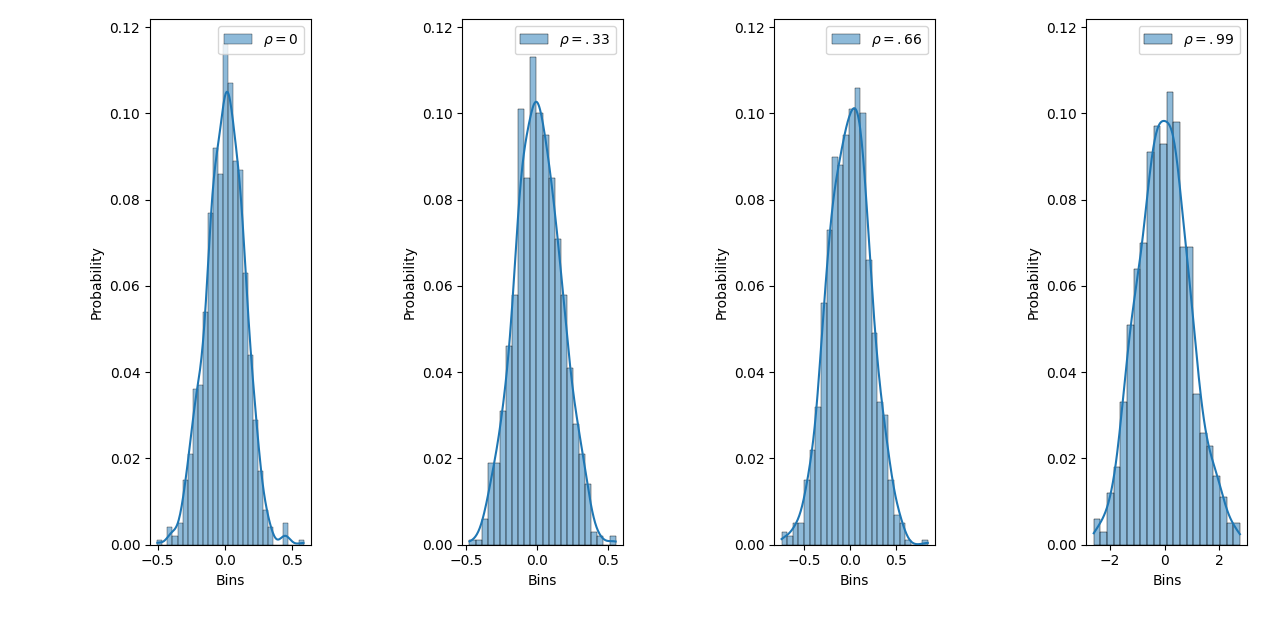

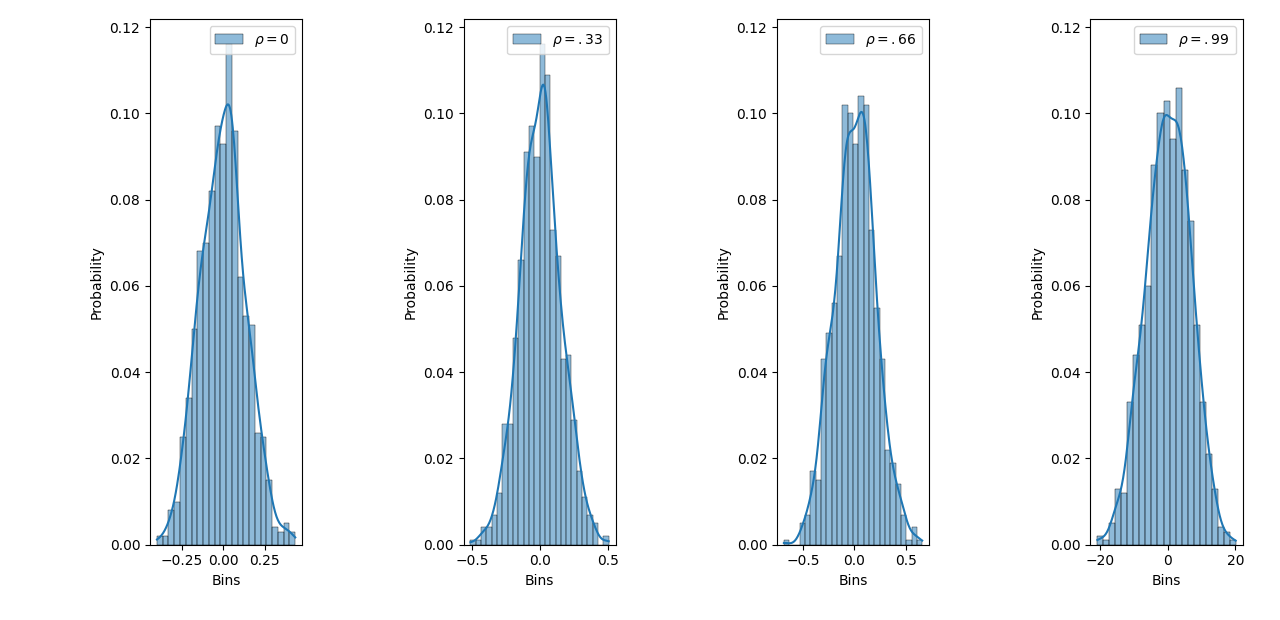

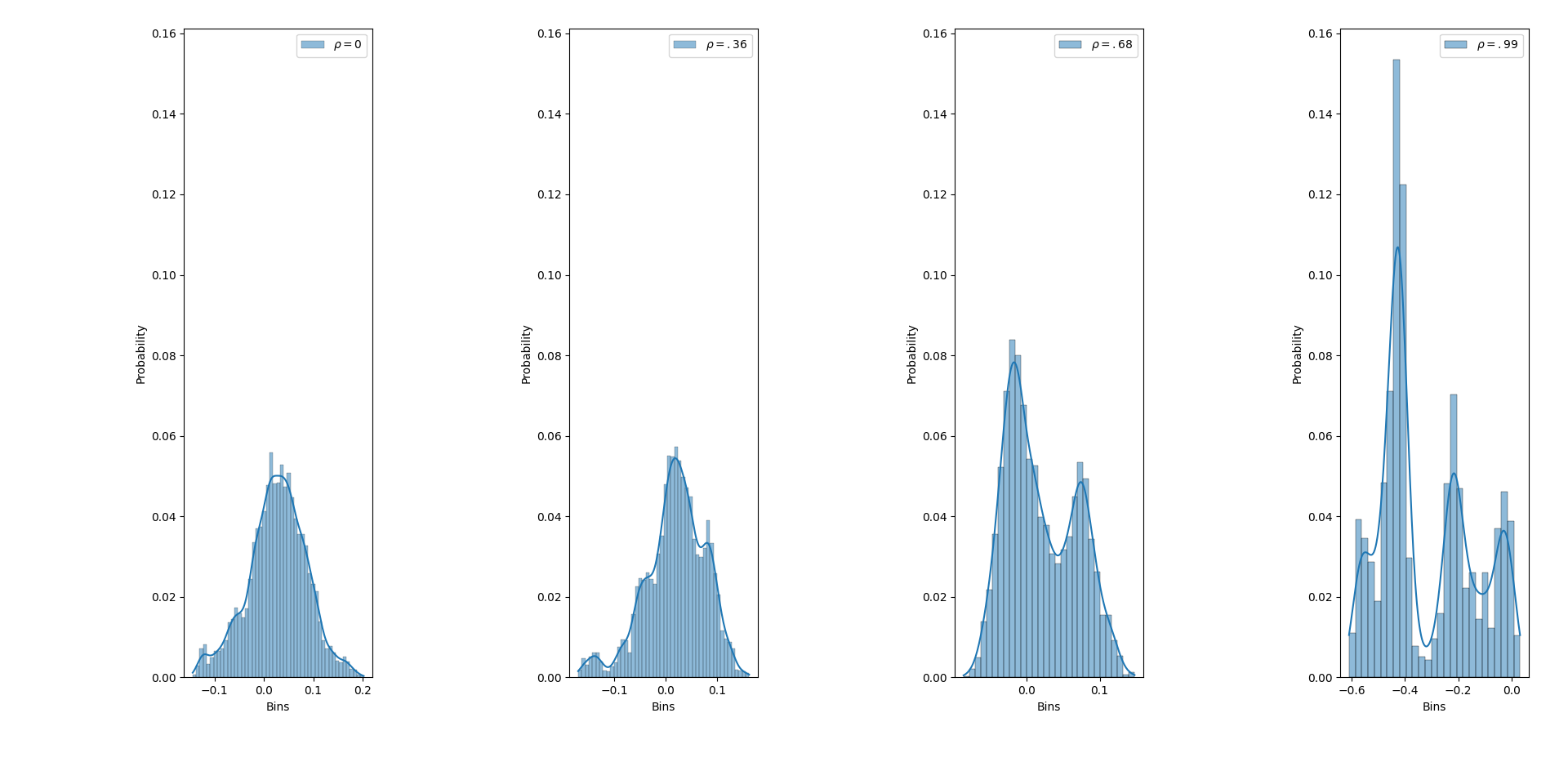

3.1 Simulating from a Mixture Gaussian

We consider the task of sampling from the density

Note that in this case

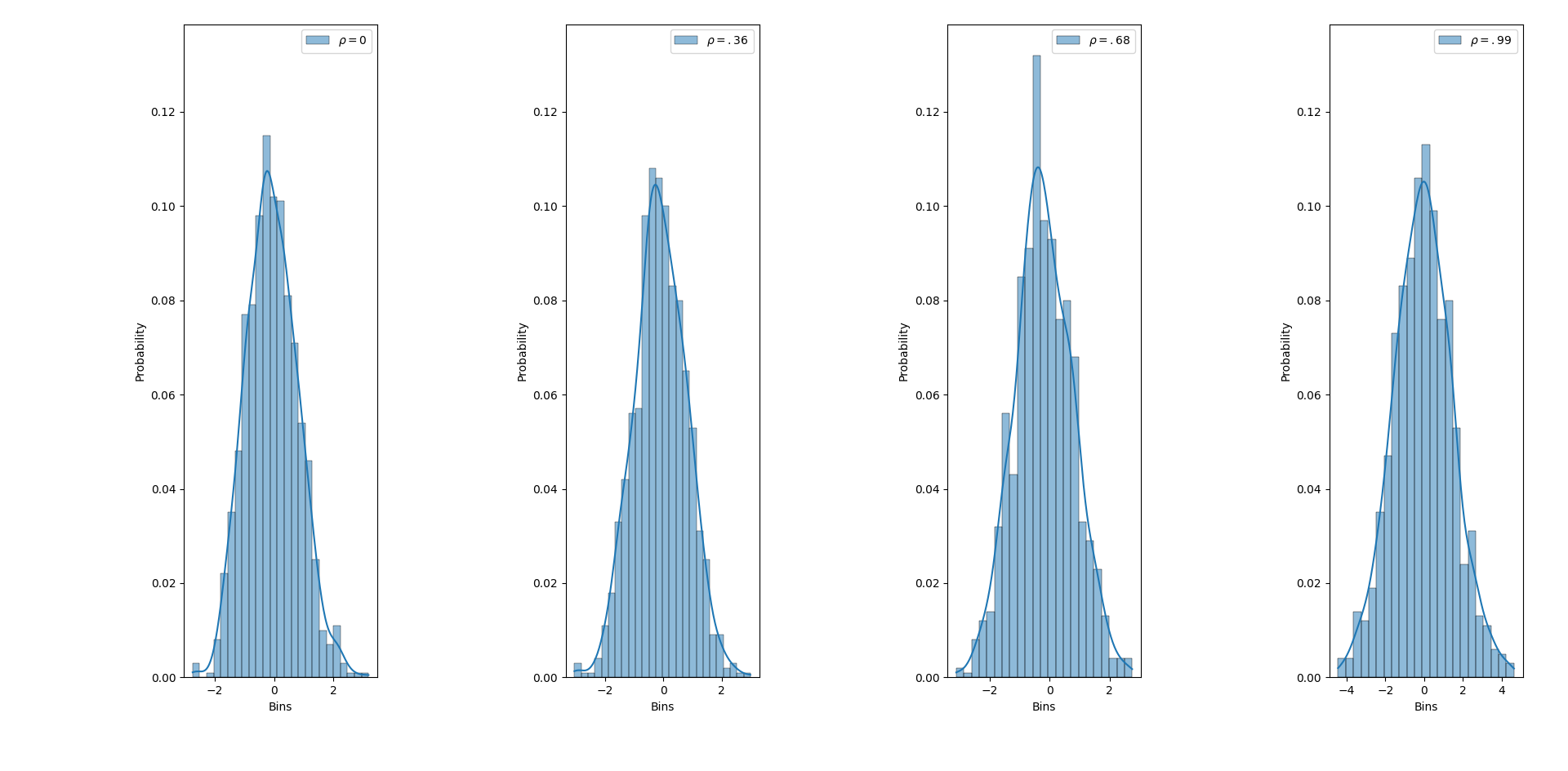

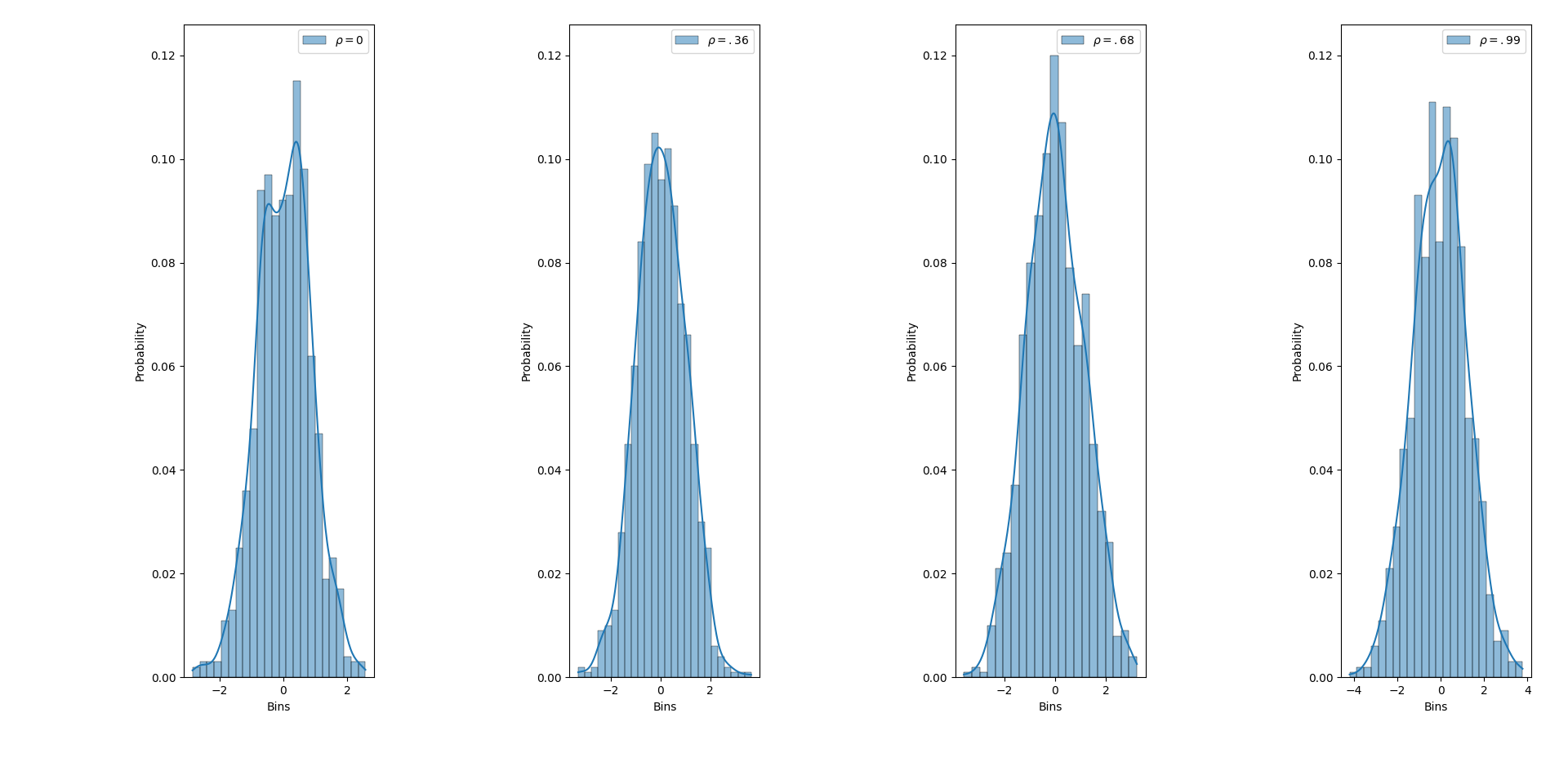

We note that is Lipschitz with Lipschitz-constant . Also, when , we have . We exhibit simulations for different values of for which we plot histograms exhibiting the Central Limit Theorem for the spatial average of the observations generated from sampling. We also plot histograms exhibiting the approximate sampling from mixture normality. We generate observations with replicates for this study.

Note that the approximate sampling of the marginal needs more samples if is taken closer to . This can be explained by observing the eigenvalues of . As can be found in previous literature [26], the spectra of matrices of the form is of the form

where . Therefore as is taken closer to , the eigenvalues of the matrix become smaller and hence more data is needed to achieve the same error.

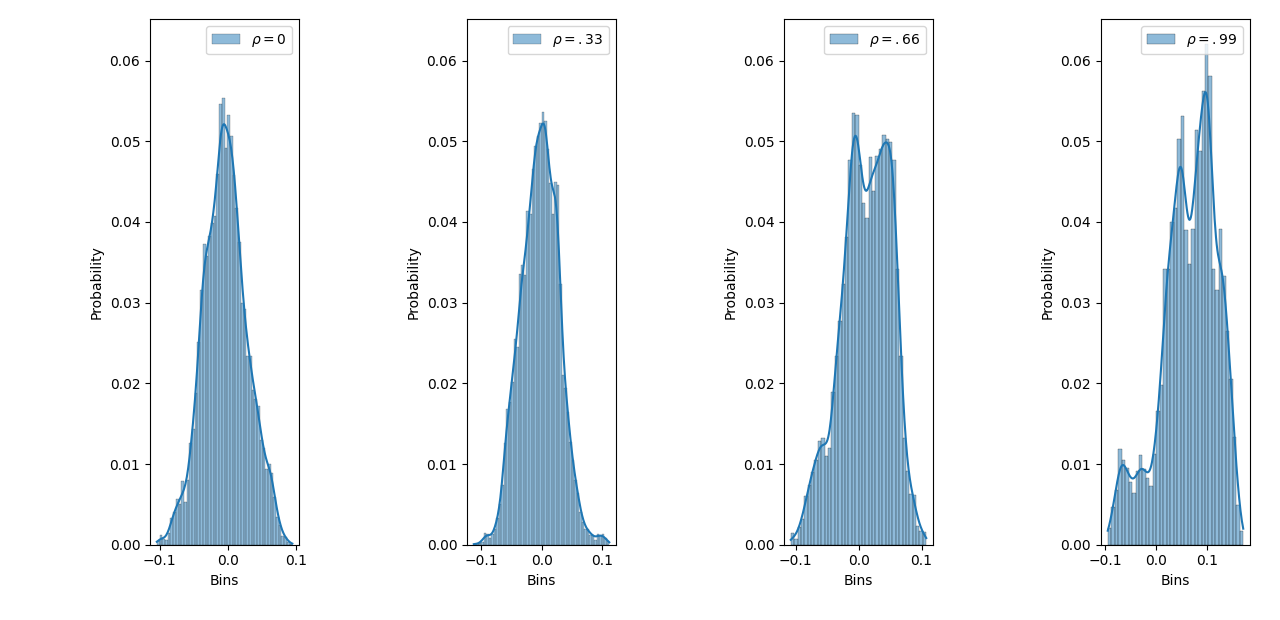

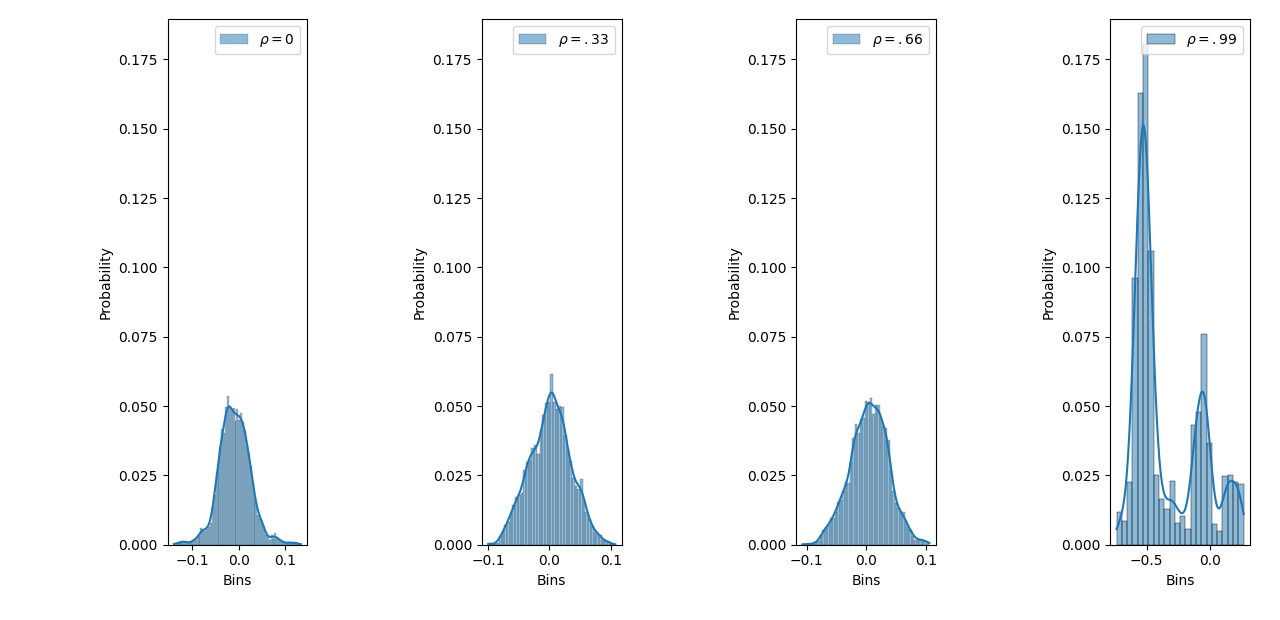

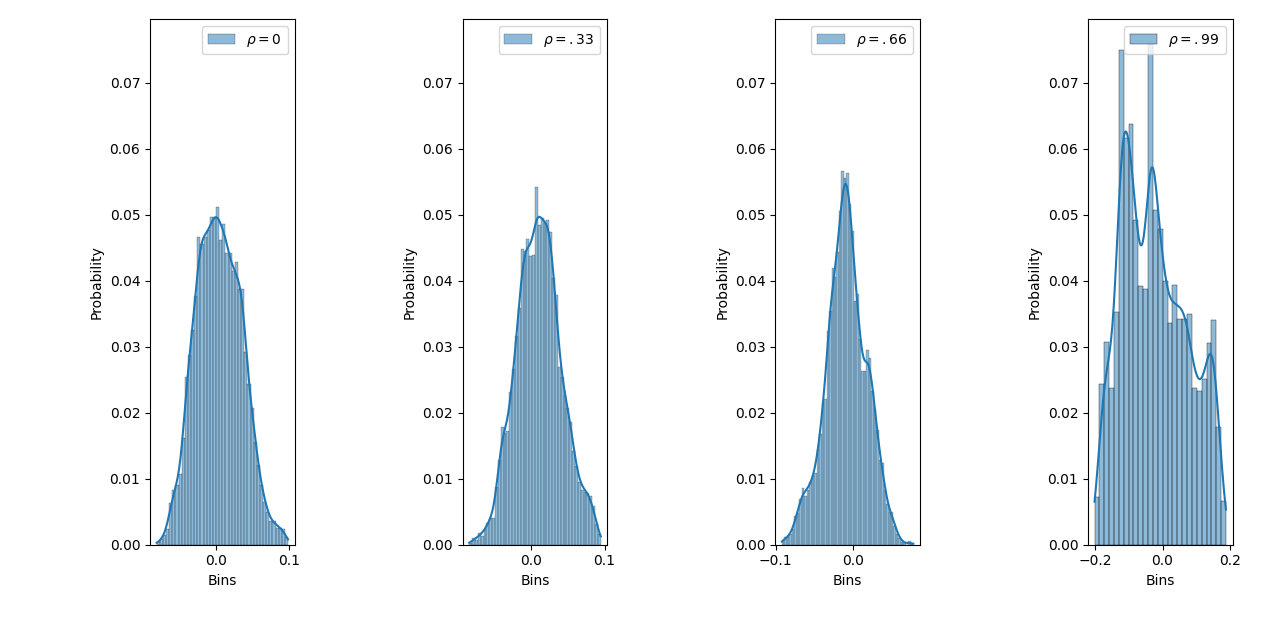

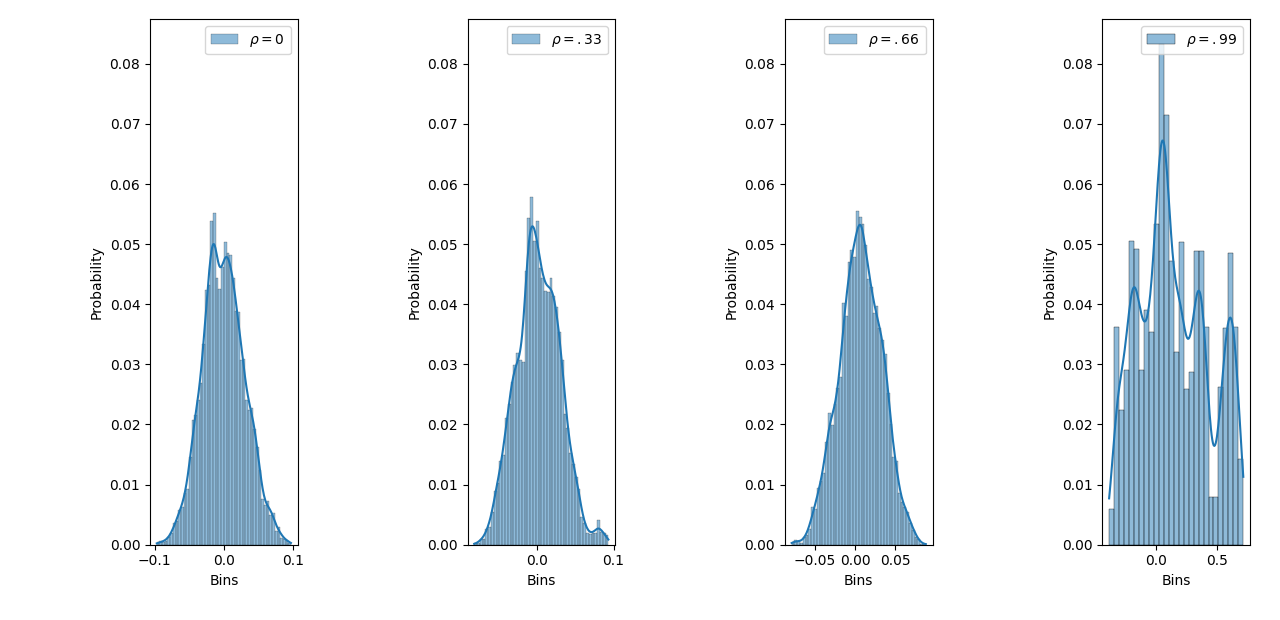

3.2 Simulating from Gaussian-Cosine distribution

Consider the problem of simulating from the density

where . Note that this distribution has no closed form expression and hence sampling from this probability measure shall require non-trivial techniques. We shall use the preconditioned LMC algorithm to sample from this distribution. Note that, for this problem,

Hence we have

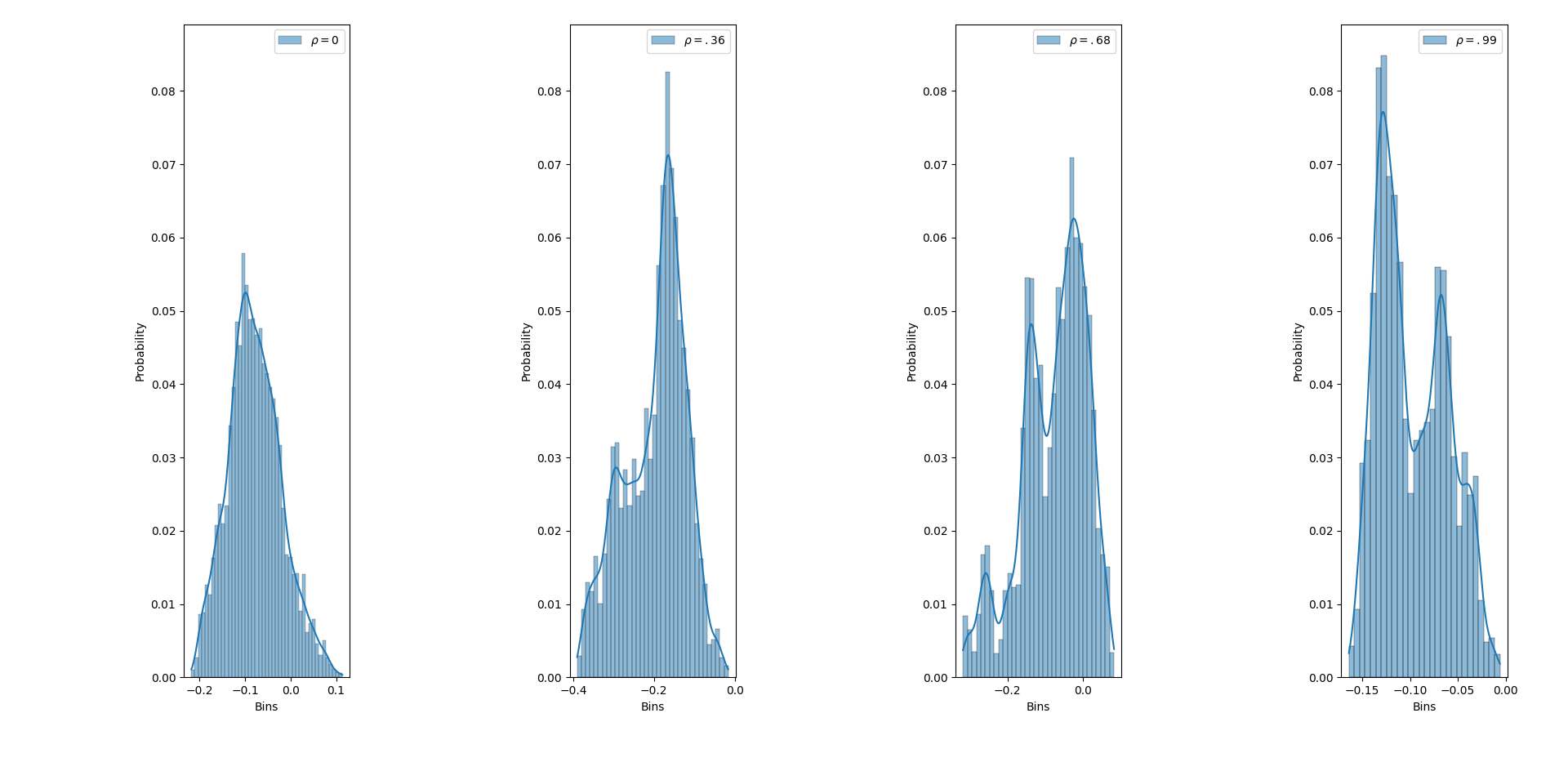

Therefore we have which is the Lipschitz constant and which is the coefficient of strong convexity. This is easy to see by finding the eigenvalues of the matrix and upper and lower bounding them. We simulate histograms of the distributions simulated for different preconditioning matrices. We consider iterations with replications for each simulation. Histograms are constructed with the average of the estimates which give the simulation results for the CLT and are plotted in Figure 3. In Figure 4 we exhibit observations which are approximately sampled from and draw histograms for the same. We note the dominant quadratic trend in the curve and also the fact that for values close to , one sees that more iterations are needed to get the desired result. This is due to the fact that as is considered closer to , the smallest eigenvalue of goes to and hence more iterations are needed to detect the small gap.

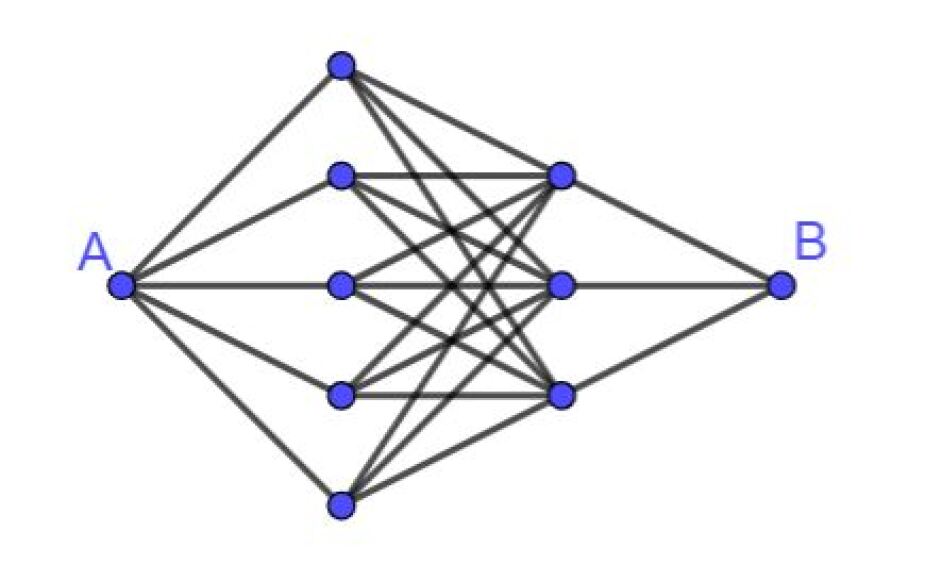

3.3 Simulating from a Reinforcement Learning Setup

For this example, we consider a reinforcement learning setup where we examine the problem of a person staring from home to reach a particular destination. He traverses multiple paths while travelling to his destination and at each path he incurs a cost. This cost can be both positive and negative. The traveller wants to select a path with a reasonable cost.

To frame the problem more mathematically consider Figure 2, where A is the stating point or home and B is the destination. Figure 2 represents a graph with vertex set and edge set . denotes the cost of traversing edge . We have a cutoff cost , which is indicative of a desired upper bound of the total cost of travel. Our problem is selection of paths with reasonable cost. Hence we consider the model

where denotes each instance and is the total number of instances. is indicative of the path from A to B at instance . denotes the set of all arranged as a vector. That is if we consider a number denoting each edge, then . Here denotes the cardinality of the edge set. Also instances are considered to be independent of each other. We consider for . This describes the distribution of the cost of traversing a path. We can also see that each path can be denoted by a vector. Let us consider with minor abuse of notation that is a vector and denote where if edge is included in the path. Hence we have

Hence this reduces to the Bayesian logistic regression setting. Now the question we are interested in is what is the distribution of the costs of traversing the edges given the data for all the instances. This enables us in finding the edge with the lowest average cost. We use to denote all the i.e., the vector of the feasibility at each instance and . We have

Thus we have

where is a constant independent of . Hence we get

and

This implies that the negative log-likelihood is strongly convex. We perform simulation studies with iterations and replications. The findings are very similar to the previous examples.

3.4 Concluding remarks.

In this paper we study the preconditioned LMC algorithm which is widely used by practitioners of fast sampling. The fast sampling bounds for the algorithm under strong conditions for KL-divergence has been settled. Also there has been numerous works in this area where there is no preconditioning. Given this, we make the following comments:

-

1.

We establish the convergence of the preconditioned LMC algorithm for general preconditioning matrices to a stationary distribution dependent on the step size in total variation. This is given in Theorem 1.

-

2.

In addition to the previous point we derive explicit convergence bounds of the algorithm to the stationary distribution dependent on the step size in total variation. This can be viewed in Proposition 2.2.

-

3.

We derive a CLT for preconditioned LMC samples which may be used for the purposes of statistical inference. This is exhibited in Theorem 2.

- 4.

-

5.

We establish a fast sampling bound of the preconditioned LMC algorithm to the target distribution when the preconditioning is spatially invariant, in the Wasserstein distance. This may be viewed in Theorem 4.

-

6.

Simulation experiments exhibit that the fast sampling and CLT accuracy is dependent on the bounds of the preconditioning. The dependence however seems somewhat robust to minor changes and fast sampling procedures seem to exhibit more sensitivity to this change than the CLT.

-

7.

One interesting question is how to extend the problem of approximate sampling in the regime of strong convexity with general preconditioning matrices. This is especially challenging in a Riemannian Manifold where the concept of convexity is non-trivial.

References

- [1] François Bolley and Cédric Villani. Weighted Csiszár-Kullback-Pinsker inequalities and applications to transportation inequalities. In Annales de la Faculté des sciences de Toulouse: Mathématiques, volume 14, 2005.

- [2] Léon Bottou, Frank E. Curtis, and Jorge Nocedal. Optimization methods for large-scale machine learning. SIAM Review, 60(2), 2018.

- [3] Nicolas Brosse, Alain Durmus, Éric Moulines, and Marcelo Pereyra. Sampling from a log-concave distribution with compact support with proximal Langevin Monte Carlo. In Conference on Learning Theory. PMLR, 2017.

- [4] Xiang Cheng, Jingzhao Zhang, and Suvrit Sra. Theory and algorithms for diffusion processes on riemannian manifolds. arXiv preprint arXiv:2204.13665, 2022.

- [5] Arnak S. Dalalyan. Further and stronger analogy between sampling and optimization: Langevin Monte Carlo and gradient descent. In Conference on Learning Theory. PMLR, 2017.

- [6] Arnak S. Dalalyan. Theoretical guarantees for approximate sampling from smooth and log-concave densities. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 79(3), 2017.

- [7] Arnak S. Dalalyan and Lionel Riou-Durand. On sampling from a log-concave density using kinetic Langevin diffusions. Bernoulli, 26(3), 2020.

- [8] Steffen Dereich and Sebastian Kassing. Central limit theorems for stochastic gradient descent with averaging for stable manifolds. Electronic Journal of Probability, 28, 2023.

- [9] Alain Durmus and Eric Moulines. Sampling from strongly log-concave distributions with the Unadjusted Langevin Algorithm. arXiv preprint arXiv:1605.01559, 2016.

- [10] Alain Durmus and Eric Moulines. High-dimensional Bayesian inference via the Unadjusted Langevin Algorithm. Bernoulli, 25(4A), 2019.

- [11] Khashayar Gatmiry and Santosh S. Vempala. Convergence of the Riemannian Langevin Algorithm, 2022, https://arxiv.org/abs/2204.10818.

- [12] Mark Girolami and Ben Calderhead. Riemann manifold Langevin and Hamiltonian Monte Carlo methods. Journal of the Royal Statistical Society. Series B (Statistical Methodology), 73(2), 2011.

- [13] Hadrien Hendrikx, Lin Xiao, Sebastien Bubeck, Francis Bach, and Laurent Massoulie. Statistically preconditioned accelerated gradient method for distributed optimization. In International Conference on Machine Learning. PMLR, 2020.

- [14] Xi-Lin Li. Preconditioned stochastic gradient descent. IEEE Transactions on Neural Networks and Learning Systems, 29(5), 2017.

- [15] Roberts S. Liptser and Albert N. Shiryaev. Statistics of Random Processes I: General Theory. Stochastic Modelling and Applied Probability. Springer New York, 2013.

- [16] Yi-An Ma, Tianqi Chen, and Emily Fox. A complete recipe for stochastic gradient mcmc. In C. Cortes, N. Lawrence, D. Lee, M. Sugiyama, and R. Garnett, editors, Advances in Neural Information Processing Systems, volume 28. Curran Associates, Inc., 2015.

- [17] Jonathan C. Mattingly, Andrew M. Stuart, and Desmond J. Higham. Ergodicity for SDEs and approximations: locally Lipschitz vector fields and degenerate noise. Stochastic Processes and their Applications, 101(2), 2002.

- [18] Sean P. Meyn and Richard L. Tweedie. Markov chains and stochastic stability. Springer Science & Business Media, 2012.

- [19] Bernt Oksendal. Stochastic Differential Equations: an Introduction with Applications. Springer Science & Business Media, 2013.

- [20] Herbert Robbins and Sutton Monro. A stochastic approximation method. The Annals of Mathematical Statistics, 1951.

- [21] Gareth O. Roberts and Osnat Stramer. Langevin diffusions and Metropolis-Hastings algorithms. Methodology and Computing in Applied Probability, 4(4), 2002.

- [22] Gareth O. Roberts and Richard L. Tweedie. Exponential convergence of Langevin distributions and their discrete approximations. Bernoulli, 1996.

- [23] Jeffrey S. Rosenthal. Minorization conditions and convergence rates for Markov chain Monte Carlo. Journal of the American Statistical Association, 90(430), 1995.

- [24] Vivekananda Roy and Lijin Zhang. Convergence of position-dependent mala with application to conditional simulation in glmms. Journal of Computational and Graphical Statistics, 32(2):501–512, 2023.

- [25] Daniel J. Russo, Benjamin Van Roy, Abbas Kazerouni, Ian Osband, and Zheng Wen. A Tutorial on Thompson Sampling. Foundations and Trends® in Machine Learning, 11(1), 2018.

- [26] William F. Trench. Asymptotic distribution of the spectra of a class of generalized Kac–Murdock–Szegö matrices. Linear Algebra and its Applications, 294(1-3), 1999.

- [27] Yating Wang, Wei Deng, and Guang Lin. Bayesian sparse learning with preconditioned stochastic gradient MCMC and its applications. Journal of Computational Physics, 432, 2021.

Appendix A Discrete Time Analysis on the Preconditioned Langevin Monte Carlo Algorithm

LEMMA A.1.

Proof.

It can be seen that in the expectation of the quadratic expression, the matrix is fixed given the sigma-field of . Therefore

Observe that,

and

Therefore,

and the result follows. ∎

PROPOSITION A.1.

Proof.

Our proof shall be two-fold. We shall first reduce the given problem into a simpler one and then solve the simpler problem. Note that

Now, for the first term

By using Lemma A.1, we get

We finish the proof. ∎

COROLLARY 2.

Let the conditions of Proposition A.1 hold. For the Lyapunov function , there exists the following drift condition

with .

Proof.

Note that

The proof is completed. ∎

LEMMA A.2.

Proof.

We consider three cases separately. We first tackle the question of irreducibility. Note that to establish irreducibility, we need to exhibit that

for any set with . This is trivially true as

where is of full rank for any . Thus is indeed irreducible with respect to the Lebesgue measure. Next we show that the chain is aperiodic. This can also be seen very easily as if the chain is not aperiodic, there exists a partition of as , such that and . This is impossible as

Lastly, by Corollary 4 from [17], we know a drift condition implies that the resultant chain is Harris. We then have established the Harris recurrence. ∎

COROLLARY 3.

Proof.

The proof is an immediate consequence of Lemma A.2. ∎

LEMMA A.3.

Let the conditions of Proposition A.1 hold. Consider the set

for any . For , we have

for some and probability measure .

Proof.

Define as the uniform measure restricted to , i.e., for any , we have

For and , we have

Hence we complete the proof. ∎

With the above preparation we are now ready to present the proofs of Theorem 1, Propositions 2.1 and 2.2.

Proof of Theorem 1.

Proof of Proposition 2.1.

By Lemma A.1, we know that

for any . Therefore, we have

where , , and . Note that this result holds with . This implies that the drift condition holds with in the given interval. This also implies that Lemma A.2 and Corollary 3 hold with . Hence, the proof follows by the same argument as Theorem 1. ∎

Proof of Proposition 2.2.

Note that if we can give a lower bound for

then we indeed finish the proof by Lemma A.3. In fact, by noting that

Thus, is contained in the closed ball with center at and radius . We refer to this set as . Consequently,

Now, on , we have

Therefore,

and the proof is completed. ∎

Appendix B Continuous Time Analysis of Preconditioned Langevin Monte Carlo Algorithm

B.1 Continuous Time Analysis of Preconditioned Langevin

Note that we call (2.3) a diffusion as by [19, Theorem 5.2.1]. Define as the transition semi-group of the Markov chain associated with (2.3). Also use to define the generator of . We also know that the domain of the generator is any .

Proof.

We know that

| (B.1) |

For any positive measurable function define . Using Dynkin’s formula (see Oskendal [19]), we know

Define

In this case

By strong convexity, we have . This implies

Now

The last line here again follows as . This implies

Using the Gronwall Lemma,

Therefore, by the fact , we obtain

and the desired result follows. ∎

As mentioned previously, is the Markov transition kernel and using Theorem 3 we know that the Preconditioned Langevin diffusion (2.3) has a stationary distribution, which we refer to as . Note that for the stationary measure have by definition.

Proof.

We know . This implies for a fixed constant , we have

The second line follows as is a concave function and the next line follows from Lemma B.1. Using DCT as , one has

for any . Taking , by the monotone convergence theorem, we obtain the result. ∎

Next we present a lemma which exhibits a contraction for the step markov kernel when the starting points are different. Recall the Wasserstein distance between two measures and as defined in (1.3).

Proof of Lemma B.3.

Consider the stochastic differential equations

Here the Brownian motions are the same. The starting points of and are and , respectively. Evidently,

This implies

which in turn implies

Now,

Consequently,

By the Gronwall lemma, we have

Taking expectation and using the definition of the Wasserstein distance we have

The proof is concluded. ∎

This lemma exhibits a contraction in the measures at the t-th time step starting at different point masses. Next we present the proof of Proposition 2.4 which is one of the key results presented in this work.

B.2 Discrete Time Approximation

LEMMA B.4.

Let be a Lipschitz function defined on with Lipschitz constant . Then we have

where .

Proof.

First,

By taking expectation, the previous step implies

Hence,

Therefore we have

Hence the proof is completed. ∎

Proof.

REMARK B.1.

Note that Proposition B.1 implies that for . Therefore,

where is a constant independent of . Note that we can take as

We shall connect the KL-divergence with the Wasserstein metric. Let be a Polish space and be the space of all Borel probability measures on . Recall the Wasserstein- metric between the probability measures and defined by

where denotes the set of coupling between and defined in (1.3). For the case when , this is the canonical Wasserstein-Monge-Kantorvich distance stated in (1.3).

LEMMA B.5.

[1, Corollary 3] Let be a space equipped with a metric distance . Let and let be a Borel probability measure on . Assume that there exists an and such that is finite. Then

for any , where

We shall use Lemma B.5 with , , , and . Note that to use Lemma B.5, we must establish the moment condition which is equivalent to establishing for some . Note that we can take any and as is defined as the minimum value. Define .

Proof.

Recall that

Hence by the rules of Ito differentials Again, by the rules of Ito calculus, we obtain

By using the definition of and by using the trace function on differentials, we get

Using the definition of again to see

Note that for any , we have

Here the last line follows from the strong convexity and Cauchy-Schwartz inequality. Hence

Thus

Taking expectation we find that

Noting that is a continuous time square-integrable martingale with . As a consequence,

By using the Gronwall Lemma, we obtain

The proof is completed. ∎

COROLLARY 4.

Under the setting of Lemma B.6, we have

Proof.

The proof is immediate from the inequality

∎