Approximating Nash Equilibria in Normal-Form Games via Stochastic Optimization

Abstract

We propose the first, to our knowledge, loss function for approximate Nash equilibria of normal-form games that is amenable to unbiased Monte Carlo estimation. This construction allows us to deploy standard non-convex stochastic optimization techniques for approximating Nash equilibria, resulting in novel algorithms with provable guarantees. We complement our theoretical analysis with experiments demonstrating that stochastic gradient descent can outperform previous state-of-the-art approaches.

1 Introduction

Nash equilibrium (NE) famously encodes stable behavioral outcomes in multi-agent systems and is arguably the most influential solution concept in game theory. Formally speaking, if players independently choose , possibly mixed, strategies ( for ) and their joint strategy () constitutes a Nash equilibrium, then no player has any incentive to unilaterally deviate from their strategy. This concept has sparked extensive research in various fields, ranging from economics [Milgrom and Weber, 1982] to machine learning [Goodfellow et al., 2014], and has even inspired behavioral theory generalizations such as quantal response equilibria which allow for more realistic models of boundedly rational agents [McKelvey and Palfrey, 1995].

Unfortunately, when considering Nash equilibria beyond the -player, zero-sum scenario, two significant challenges arise. First, it becomes unclear how independent players would collectively identify a Nash equilibrium when multiple equilibria are possible, giving rise to the equilibrium selection problem [Harsanyi et al., 1988]. Secondly, even approximating a single Nash equilibrium is known to be computationally intractable and specifically PPAD-complete [Daskalakis et al., 2009]. Combining both problems together, e.g., testing for the existence of equilibria with welfare greater than some fixed threshold is NP-hard and it is in fact even hard to approximate [Austrin et al., 2011].

From a machine learning practitioner’s perspective, such computational complexity results hardly give pause for thought as collectively we have become all too familiar with the unreasonable effectiveness of heuristics in circumventing such obstacles. Famously, non-convex optimization is NP-hard, even if the goal is to compute a local minimizer [Murty and Kabadi, 1985], however, stochastic gradient descent (SGD) and variants succeed in training billion parameter models [Brown et al., 2020].

Unfortunately, computational techniques for Nash equilibrium have so far not achieved anywhere near the same level of success. In contrast, most modern NE solvers for -player, -action, general-sum, normal-form games (NFGs) are practically restricted to a handful of players and/or actions per player except in special cases, e.g., symmetric [Wiedenbeck and Brinkman, 2023] or mean-field games [Pérolat et al., 2022]. For example, when running the suite of all applicable methods from the hallmark gambit library [McKelvey et al., 2016] on a 4-player Blotto game, we find only brute-force pure-NE enumeration is able to return any NE within a hour time limit. Scaling solvers to large games is difficult partially due to the fact that an NFG is represented by a tensor with an exponential entries; even reading this description into memory can be computationally prohibitive. More to the point, any computational technique that presumes exact computation of the expectation of any function sampled according to similarly does not have any hope of scaling beyond small instances.

This inefficiency arguably lies at the core of the differential success between ML optimization and equilibrium computation. For example, numerous techniques exist that reduce the problem of Nash computation to the minimization of the expectation of a random variable (Section 3). Unfortunately, unlike the source of randomness in ML applications where batch learning suffices to easily produce unbiased estimators, these techniques do not extend easily to game theory which incorporates non-linear functions such as maximum and best-response. This raises our motivating goal:

| Can we solve for Nash equilibria via unbiased stochastic optimization? |

Our results. Following in the successful steps of the interplay between ML and stochastic optimization, we reformulate the approximation of Nash equilibria in an NFG as a stochastic non-convex optimization problem admitting unbiased Monte-Carlo estimation. This enables the use of powerful solvers and advances in parallel computing to efficiently enumerate Nash equilibria for -player, general-sum games. Furthermore, this re-casting allows practitioners to incorporate other desirable objectives into the problem such as “find an approximate Nash equilibrium with welfare above ” or “find an approximate Nash equilibrium nearest the current observed joint strategy” resolving the equilibrium selection problem in an effectively ad-hoc and application tailored manner. Concretely, we make the following contributions by producing:

-

•

A loss function 1) whose global minima well approximate Nash equilibria in normal form games, 2) admits unbiased Monte-Carlo estimation, and 3) is Lipschitz and bounded.

-

•

An efficient randomized algorithm for approximating Nash equilibria in a novel class of games. The algorithm emerges by employing a recent -armed bandit approach to and connecting its stochastic optimization guarantees to approximate Nash guarantees. For large games, this enables approximating equilibria with high probability faster than the game can even be read into memory.

-

•

An empirical comparison of SGD against state-of-the-art baselines for approximating NEs in large games. In some games, vanilla SGD actually improves upon previous state-of-the-art; in others, SGD is slowed by saddle points, a familiar challenge in deep learning [Dauphin et al., 2014].

Overall, this perspective showcases a promising new route to approximating equilibria at scale in practice. We conclude the paper with discussion for future work.

2 Preliminaries

In an -player, normal-form game, each player has a strategy set consisting of pure strategies. These strategies can be naturally indexed, so we redefine as an abuse of notation. Each player also has a utility function, , (equiv. “payoff tensor”) that maps joint actions to payoffs in the unit-interval . We denote the average cardinality of the players’ action sets by and maximum by . Player may play a mixed strategy by sampling from a distribution over their pure strategies. Let player ’s mixed strategy be represented by a vector where is the -dimensional probability simplex embedded in . Each function is then extended to this domain so that where and denotes player ’s component of the joint action . For convenience, let denote all components of belonging to players other than player .

The joint strategy is a Nash equilibrium if and only if, for all , for all , i.e., no player has any incentive to unilaterally deviate from . Nash is typically relaxed with -Nash, our focus: for all .

As an abuse of notation, let the atomic action also denote the -dimensional “one-hot" vector with all zeros aside from a at index ; its use should be clear from the context. We also introduce as player ’s utility gradient. And for convenience, denote by the bimatrix game approximation [Janovskaja, 1968] between players and with all other players marginalized out; denotes all strategies belonging to players other than and and separates out ’s strategy from the rest of the players . Similarly, denote by the -player tensor approximation to the game. Note player ’s utility can now be written succinctly as for any where we use Einstein notation for tensor arithmetic. For convenience, define as the function that places a vector on the diagonal of a square matrix, and as a 3-tensor of shape where .

| Loss | Function | Obstacle |

|---|---|---|

| Exploitabilty | of r.v. | |

| Nikaido-Isoda (NI) | of r.v. | |

| Fully-Diff. Exp | of r.v. | |

| Gradient-based NI | NI w/ | of r.v. |

| Unconstrained | Loss + Simplex Deviation Penalty | sampling from |

Following convention from differential geometry, let be the tangent space of a manifold at . For the interior of the -action simplex , the tangent space is the same at every point, so we drop the subscript, i.e., . We denote the projection of a vector onto this tangent space as and call a projected-gradient. We drop when the dimensionality is clear from the context. Finally, let denote a discrete uniform distribution over elements from set .

3 Related Work

Representing the problem of computing a Nash equilibrium as an optimization problem is not new. A variety of loss functions and pseudo-distance functions have been proposed. Most of them measure some function of how much each player can exploit the joint strategy by unilaterally deviating:

| (1) |

As argued in the introduction, we believe it is important to be able to subsample payoff tensors of normal-form games in order to scale to large instances. As Nash equilibria can consist of mixed strategies, it is advantageous to be able to sample from an equilibrium to estimate its exploitability . However none of these losses is amenable to unbiased estimation under sampled play. Each of the functions currently explored in the literature is biased under sampled play either because 1) a random variable appears as the argument of a complex, nonlinear (non-polynomial) function or because 2) how to sample play is unclear. Exploitability, Nikaido-Isoda (NI) [Nikaidô and Isoda, 1955] (also known by NashConv [Lanctot et al., 2017] and ADI [Gemp et al., 2022]), as well as fully-differentiable options ([Shoham and Leyton-Brown, 2008], p. 106, Eqn 4.31) introduce bias when a over payoffs is estimated using samples from . Gradient-based NI [Raghunathan et al., 2019] requires projecting the result of a gradient-ascent step onto the simplex; for the same reason as the , this is prohibitive because it is a nonlinear operation which introduces bias. Lastly, unconstrained optimization approaches ([Shoham and Leyton-Brown, 2008], p. 106) that instead penalize deviation from the simplex lose the ability to sample from strategies when each iterate is no longer a distribution (i.e., ). Table 1 summarizes these complications.

4 Nash Equilibrium as Stochastic Optimization

We will now develop our proposed loss function which is amenable to unbiased estimation. Subsections 4.1-4.4 provide a warm-up in which we assume an interior (fully-mixed) Nash equilibrium exists. Subsection 4.5 then shows how to relax that assumption allowing us to approximate partially mixed equilibria as well (including pure equilibria). Our key technical insight is to pay special attention to the geometry of the simplex. To our knowledge, prior works have failed to recognize the role of the tangent space . Proofs are in the appendix.

4.1 Stationarity on the Simplex Interior

Lemma 1.

Assuming player ’s utility, , is concave in its own strategy , a strategy in the interior of the simplex is a best response if and only if it has zero projected-gradient111Not to be confused with the nonlinear (biased) projected gradient operator in [Hazan et al., 2017]. norm.

In NFGs, each player’s utility is linear in , thereby satisfying the concavity condition of Lemma 1.

4.2 Projected Gradient Norm as Loss

An equivalent description of a Nash equilibrium is a joint strategy where every player’s strategy is a best response to the equilibrium (i.e., so that ). Lemma 1 states that any interior best response has zero projected-gradient norm, which inspires the following loss function

| (2) |

where represent scalar weights, or equivalently, step sizes to be explained next.

Proposition 1.

The loss is equivalent to NashConv, but where player ’s best response is approximated by a single step of projected-gradient ascent with step size : .

4.3 Connection to True Exploitability

In general, we can bound exploitability in terms of the projected-gradient norm as long as each player’s utility is concave (this result extends to subgradients of non-smooth functions).

Lemma 2.

The amount a player can gain by exploiting a joint strategy is upper bounded by a quantity proportional to the norm of the projected-gradient:

| (3) |

This bound is not tight on the boundary of the simplex, which can be seen clearly by considering to be part of a pure strategy equilibrium. In that case, this analysis assumes can be improved upon by a projected-gradient ascent step (via the equivalence pointed out in Proposition 1). However, that is false because the probability of a pure strategy cannot be increased beyond . We mention this to provide further intuition for why our “warm-up” loss is only valid for interior equilibria.

Note that because is a projection. Therefore, this improves the naive bounds on exploitability and distance to best responses given using the “raw” gradient .

Lemma 3.

The exploitability of a joint strategy , is upper bounded by a function of :

| (4) |

4.4 Unbiased Estimation

As discussed in Section 3, a primary obstacle to unbiased estimation of is the presence of complex, nonlinear functions of random variables, with the projection of a point onto the simplex being one such example (see in Table 1). However, , the projection onto the tangent space of the simplex, is linear! This is the key that allows us to design an unbiased estimator (Lemma 5).

Our proposed loss requires computing the squared norm of the expected value of the gradient under the players’ mixed strategies, i.e., the -th entry of player ’s gradient equals . By analogy, consider a random variable . In general, . This means that we cannot just sample projected-gradients and then compute their average norm to estimate our loss. However, consider taking two independent samples from two corresponding identically distributed, independent random variables and . Then by properties of expected value over products of independent random variables. This is a common technique to construct unbiased estimates of expectations over polynomial functions of random variables. Proceeding in this way, define as a random variable distributed according to the distribution induced by all other players’ mixed strategies (). Let be independent and distributed identically to . Then

| (5) |

| Exact | Sample Others | Sample All | |

|---|---|---|---|

| Estimator of | |||

| Bounds | |||

| Query Cost | |||

| Bounds | |||

| Query Cost |

where is an unbiased estimator of player ’s gradient. This unbiased estimator can be constructed in several ways. The most expensive, an exact estimator, is constructed by marginalizing player ’s payoff tensor over all other players’ strategies. However, a cheaper estimate can be obtained at the expense of higher variance by approximating this marginalization with a Monte Carlo estimate of the expectation. Specifically, if we sample a single action for each of the remaining players, we can construct an unbiased estimate of player ’s gradient by considering the payoff of each of its actions against the sampled background strategy. Lastly, we can consider constructing a Monte Carlo estimate of player ’s gradient by sampling only a single action from player to represent their entire gradient. Each of these approaches is outlined in Table 2 along with the query complexity [Babichenko, 2016] of computing the estimator and bounds on the values it can take (derived via Lemma 20).

We can extend Lemma 3 to one that holds under samples with probability by applying, for example, a Hoeffding bound: .

4.5 Interior Equilibria

We discussed earlier that captures interior equilibria. But some games may only have partially mixed equilibria, i.e., equilibria that lie on the boundary of the simplex. We show how to circumvent this shortcoming by considering quantal response equilibria (QREs), specifically, logit equilibria. By adding an entropy bonus to each player’s utility, we can

-

•

guarantee all equilibria are interior,

-

•

still obtain unbiased estimates of our loss,

-

•

maintain an upper bound on the exploitability of any approximate Nash equilibrium in the original game (i.e., the game without an entropy bonus).

Define where the Shannon entropy is -strongly concave with respect to the -norm [Beck and Teboulle, 2003]. It is known that Nash equilibria of entropy-regularized games satisfy the conditions for logit equilibria [Leonardos et al., 2021], which are solutions to the fixed point equation . The softmax makes clear that all probabilities have positive mass at positive temperature.

Recall that in order to construct an unbiased estimate of our loss, we simply needed to construct unbiased estimates of player gradients. The introduction of the entropy term to player ’s utility is special in that it depends entirely on known quantities, i.e., the player’s own mixed strategy. We can directly and deterministically compute and add this to our estimator of : . Consider our refined loss function with changes in blue:

| (6) |

As mentioned above, the utilities with entropy bonuses are still concave, therefore, a similar bound to Lemma 2 applies. We use this to prove the QRE counterpart to Lemma 3 where is the exploitability of an approximate equilibrium in a game with entropy bonuses.

Lemma 4.

The entropy regularized exploitability, , of a joint strategy , is upper bounded as:

| (7) |

Lastly, we establish a connection between quantal response equilibria and Nash equilibria that allows us to approximate Nash equilibria in the original game via minimizing our modified loss .

Lemma 14 ( Scores Nash Equilibria).

Let be our proposed entropy regularized loss function with payoffs bounded in and be an approximate QRE. Then it holds that

| (8) |

where is the Lambert function: .

This upper bound is plotted as a heatmap for a familiar Chicken game in the top row of Figure 1. First, notice how pure equilibria are not visible as minima for zero temperature, but appear for slightly warmer temperatures. Secondly, notice that NashConv in the bottom row is unable to capture the interior Nash equilibrium because of its high bias under sampled play. In contrast, our proposed loss is guaranteed to capture all equilibria at low temperature .

5 Analysis

In the preceding section we established a loss function that upper bounds the exploitability of an approximate equilibrium. In addition, the zeros of this loss function have a one-to-one correspondence with quantal response equilibria (which approximate Nash equilibria at low temperature).

Here, we derive properties that suggest it is “easy” to optimize. While this function is generally non-convex and may suffer from a proliferation of saddle points (Figure 2) , it is Lipschitz continuous (over a subset of the interior) and bounded. These are two commonly made assumptions in the literature on non-convex optimization, which we leverage in Section 6. In addition, we can derive its gradient, its Hessian, and characterize its behavior around global minima.

Lemma 15.

The gradient of with respect to player ’s strategy is

| (9) |

where and for .

Lemma 17.

The Hessian of can be written

| (10) |

where , , and we augment (the -player approximation to the game, ) so that .

At an equilibrium, the latter term disappears because for all (Lemma 1). If was , then we could simply check if is full-rank to determine if . However, is a simplex product, and we only care about curvature in directions toward which we can update our equilibrium. Toward that end, define to be the matrix that stacks on top of a repeated identity matrix that encodes orthogonality to the simplex:

| (11) |

where subtracts the mean from each column of and is shorthand for . If for a nonzero vector , this implies there exists a that 1) is orthogonal to the ones vectors of each simplex (i.e., is a valid equilibrium update direction) and 2) achieves zero curvature in the direction , i.e., , and so is not positive definite. Conversely, if is of rank for a quantal response equilibrium , then the Hessian of at in the tangent space of the simplex product () is positive definite. In this case, we call polymatrix-isolated: polymatrix because we only require information of the local polymatrix approximation of the game (i.e., the matrices) to construct and isolated because it implies it is not connected to any other equilibria.

Definition 1 (Polymatrix-Isolated Equilibrium).

A Nash equilibrium is polymatrix-isolated iff is isolated according to its local polymatrix game approximation.

By analyzing the rank of , we can confirm that many classical matrix games including Rock-Paper-Scissors, Chicken, Matching Pennies, and Shapley’s game all induce strongly convex ’s at zero temperature (i.e., they have unique mixed Nash equilibria). In contrast, a game like Prisoner’s Dilemma has a unique pure strategy that will not be captured by our loss at zero temperature.

6 Algorithms

We have formally transformed the approximation of Nash equilibria in NFGs into a stochastic optimization problem. To our knowledge, this is the first such formulation that allows one-shot unbiased Monte-Carlo estimation which is critical to introduce the use of powerful algorithms capable of solving high dimensional optimization problems. We explore two off-the-shelf approaches.

Stochastic gradient descent is the workhorse of high-dimensional stochastic optimization. It comes with guaranteed convergence to stationary points [Cutkosky et al., 2023], however, it may converge to local, rather than global minima. It also enjoys implicit gradient regularization [Barrett and Dherin, 2020], seeking “flat” minima and performs approximate Bayesian inference [Mandt et al., 2017]. Despite the lack of global convergence guarantee, in the next section, we find it performs well empirically in games previously examined by the literature.

We explore one other algorithmic approach to non-convex optimization based on minimizing regret, which enjoys finite time global convergence rates. -armed bandits [Bubeck et al., 2011] systematically explore the space of solutions by refining a mesh over the joint strategy space, trading off exploration versus exploitation of promising regions. Several approaches exist [Bartlett et al., 2019, Valko et al., 2013] with open source implementations (e.g., [Li et al., 2023]). Applying -armed bandits to our can be thought of as a stochastic generalization of the exclusion method and other bandit approaches for Nash equilibria [Berg and Sandholm, 2017, Zhou et al., 2017].

6.1 High Probability, Polynomial Convergence Rates

We use a recent -armed bandit approach called BLiN [Feng et al., 2022] to establish a high probability global convergence rate to Nash equilibria in -player, general-sum games under mild assumptions. The quality of this approximation improves as , at the same time increasing the constant on the convergence rate via the Lipschitz constant defined below. For clarity, we assume users provide a temperature in the form with which ensures all equilibria have probability mass greater than for all actions (Lemma 9). Lower corresponds with lower temperature.

The following convergence rate depends on bounds on the exploitability in terms of the loss (Lemma 14), bounds on the magnitude of estimates of the loss (Lemma 8), Lipschitz bounds on the infinity norm of the gradient (Corollary 2), and the number of distinct strategies ().

Theorem 1 (BLiN PAC Rate).

This result depends on the near-optimality [Valko et al., 2013] or zooming-dimension (Theorem 2) where and denote the degree of the polynomials that lower and upper bound the function locally around an equilibrium. For example, in the case where the Hessian is positive definite, and . Here, is any function that maps from the unit hypercube to a product of simplices; we analyze two such maps in the appendix.

Note that Theorem 1 implies that for games whose corresponding has zooming dimension , NEs can be approximated with high probability in polynomial time. This general property is difficult to translate concisely into game theory parlance. For this reason, we present the following more interpretable corollary which applies to a more restricted class of games.

Corollary 1.

Consider the class of NFGs with at least one polymatrix-isolated QRE(). Then by Theorem 1, BLiN is a fully polynomial-time randomized approximation scheme (FPRAS) for QREs().

To convey the impact of these guarantees more concretely, assume we are given that an interior polymatrix-isolated NE exists. Then for a -player, -action game, it is cheaper to compute a -NE with probability 95% than it is to just list the payoffs that define the game.

6.2 Empirical Evaluation

Figure 3 shows SGD is competitive with scalable techniques to approximating NEs. Shapley’s game induces a strongly convex (see Section 5) leading to SGD’s strong performance. Blotto reaches low, but nonzero , demonstrating the challenges of saddle points.

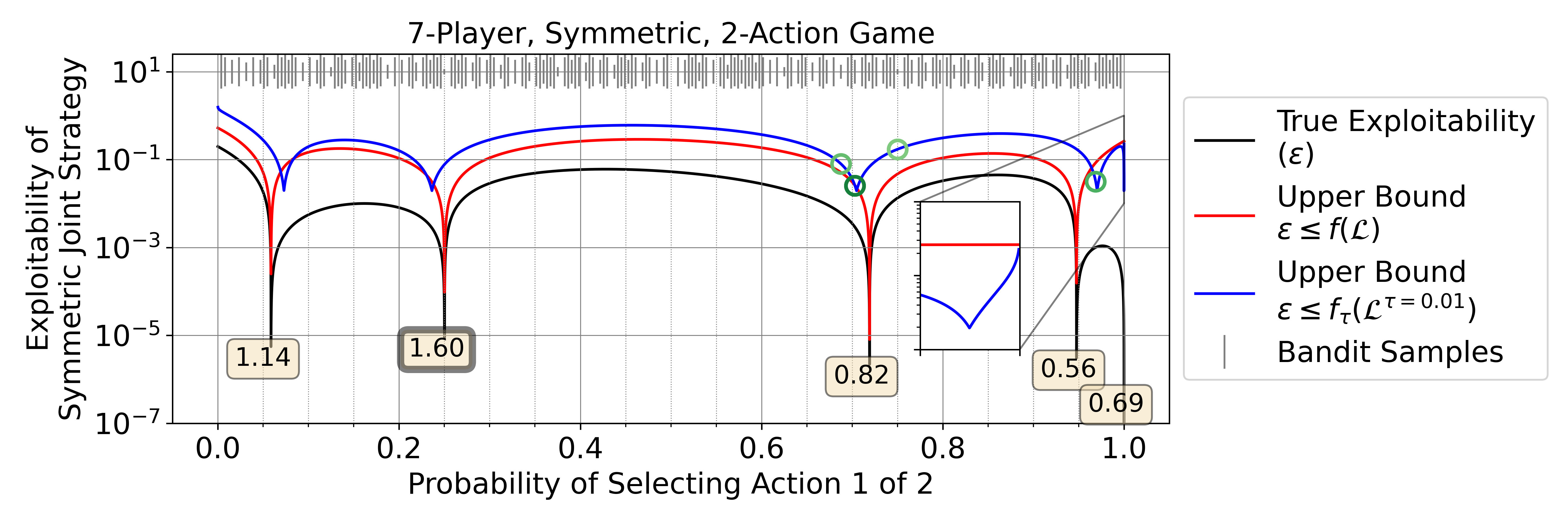

We demonstrate BLiN (applied to ) on a -player, symmetric, -action game. Figure 4 shows the bandit algorithm discovers two equilibria, settling on one near with a wider basin of attraction (and higher welfare). In theory, BLiN can enumerate all NEs as .

7 Conclusion

In this work, we proposed a stochastic loss for approximate Nash equilibria in normal-form games. An unbiased loss estimator of Nash equilibria is the “key” to the stochastic optimization “door” which holds a wealth of research innovations uncovered over several decades. Thus, it allows the development of new algorithmic techniques for computing equilibria. We consider bandit and vanilla SGD methods in this work, but theses are only two of the many options now at our disposal (e.g, adaptive methods [Antonakopoulos et al., 2022], Gaussian processes [Calandriello et al., 2022], evolutionary algorithms [Hansen et al., 2003], etc.). Such approaches as well as generalizations of these techniques to extensive-form, imperfect-information games are promising directions for future work. Similarly to how deep learning research first balked at and then marched on to train neural networks via NP-hard non-convex optimization, we hope computational game theory can march ahead to make useful equilibrium predictions of large multiplayer systems.

References

- Antonakopoulos et al. [2022] K. Antonakopoulos, P. Mertikopoulos, G. Piliouras, and X. Wang. Adagrad avoids saddle points. In International Conference on Machine Learning, pages 731–771. PMLR, 2022.

- Austrin et al. [2011] P. Austrin, M. Braverman, and E. Chlamtáč. Inapproximability of NP-complete variants of Nash equilibrium. In Approximation, Randomization, and Combinatorial Optimization. Algorithms and Techniques: 14th International Workshop, APPROX 2011, and 15th International Workshop, RANDOM 2011, Princeton, NJ, USA, August 17-19, 2011. Proceedings, pages 13–25. Springer, 2011.

- Babichenko [2016] Y. Babichenko. Query complexity of approximate Nash equilibria. Journal of the ACM (JACM), 63(4):36:1–36:24, 2016.

- Barrett and Dherin [2020] D. Barrett and B. Dherin. Implicit gradient regularization. In International Conference on Learning Representations, 2020.

- Bartlett et al. [2019] P. L. Bartlett, V. Gabillon, and M. Valko. A simple parameter-free and adaptive approach to optimization under a minimal local smoothness assumption. In Algorithmic Learning Theory, pages 184–206. PMLR, 2019.

- Beck and Teboulle [2003] A. Beck and M. Teboulle. Mirror descent and nonlinear projected subgradient methods for convex optimization. Operations Research Letters, 31(3):167–175, 2003.

- Berg and Sandholm [2017] K. Berg and T. Sandholm. Exclusion method for finding nash equilibrium in multiplayer games. In Proceedings of the AAAI Conference on Artificial Intelligence, volume 31, 2017.

- Brown et al. [2020] T. Brown, B. Mann, N. Ryder, M. Subbiah, J. D. Kaplan, P. Dhariwal, A. Neelakantan, P. Shyam, G. Sastry, A. Askell, et al. Language models are few-shot learners. Advances in neural information processing systems, 33:1877–1901, 2020.

- Bubeck et al. [2011] S. Bubeck, R. Munos, G. Stoltz, and C. Szepesvári. -armed bandits. Journal of Machine Learning Research, 12(5), 2011.

- Calandriello et al. [2022] D. Calandriello, L. Carratino, A. Lazaric, M. Valko, and L. Rosasco. Scaling gaussian process optimization by evaluating a few unique candidates multiple times. In International Conference on Machine Learning, pages 2523–2541. PMLR, 2022.

- Cutkosky et al. [2023] A. Cutkosky, H. Mehta, and F. Orabona. Optimal stochastic non-smooth non-convex optimization through online-to-non-convex conversion. arXiv preprint arXiv:2302.03775, 2023.

- Daskalakis et al. [2009] C. Daskalakis, P. W. Goldberg, and C. H. Papadimitriou. The complexity of computing a Nash equilibrium. Communications of the ACM, 52(2):89–97, 2009.

- Dauphin et al. [2014] Y. N. Dauphin, R. Pascanu, C. Gulcehre, K. Cho, S. Ganguli, and Y. Bengio. Identifying and attacking the saddle point problem in high-dimensional non-convex optimization. Advances in neural information processing systems, 27, 2014.

- Deligkas et al. [2022] A. Deligkas, J. Fearnley, A. Hollender, and T. Melissourgos. Pure-circuit: Strong inapproximability for PPAD. In 2022 IEEE 63rd Annual Symposium on Foundations of Computer Science (FOCS), pages 159–170. IEEE, 2022.

- Feng et al. [2022] Y. Feng, T. Wang, et al. Lipschitz bandits with batched feedback. Advances in Neural Information Processing Systems, 35:19836–19848, 2022.

- Gemp et al. [2022] I. Gemp, R. Savani, M. Lanctot, Y. Bachrach, T. Anthony, R. Everett, A. Tacchetti, T. Eccles, and J. Kramár. Sample-based approximation of Nash in large many-player games via gradient descent. In Proceedings of the 21st International Conference on Autonomous Agents and Multiagent Systems, pages 507–515, 2022.

- Goodfellow et al. [2014] I. Goodfellow, J. Pouget-Abadie, M. Mirza, B. Xu, D. Warde-Farley, S. Ozair, A. Courville, and Y. Bengio. Generative adversarial nets. Advances in Neural Information Processing Systems, 27, 2014.

- Hansen et al. [2003] N. Hansen, S. D. Müller, and P. Koumoutsakos. Reducing the time complexity of the derandomized evolution strategy with covariance matrix adaptation (CMA-ES). Evolutionary computation, 11(1):1–18, 2003.

- Harsanyi et al. [1988] J. C. Harsanyi, R. Selten, et al. A general theory of equilibrium selection in games. MIT Press Books, 1, 1988.

- Hazan et al. [2017] E. Hazan, K. Singh, and C. Zhang. Efficient regret minimization in non-convex games. In International Conference on Machine Learning, pages 1433–1441. PMLR, 2017.

- Janovskaja [1968] E. Janovskaja. Equilibrium points in polymatrix games. Lithuanian Mathematical Journal, 8(2):381–384, 1968.

- Lanctot et al. [2017] M. Lanctot, V. Zambaldi, A. Gruslys, A. Lazaridou, K. Tuyls, J. Pérolat, D. Silver, and T. Graepel. A unified game-theoretic approach to multiagent reinforcement learning. In Advances in Neural Information Processing Systems, pages 4190–4203, 2017.

- Lanctot et al. [2019] M. Lanctot, E. Lockhart, J.-B. Lespiau, V. Zambaldi, S. Upadhyay, J. Pérolat, S. Srinivasan, F. Timbers, K. Tuyls, S. Omidshafiei, D. Hennes, D. Morrill, P. Muller, T. Ewalds, R. Faulkner, J. Kramár, B. D. Vylder, B. Saeta, J. Bradbury, D. Ding, S. Borgeaud, M. Lai, J. Schrittwieser, T. Anthony, E. Hughes, I. Danihelka, and J. Ryan-Davis. OpenSpiel: A framework for reinforcement learning in games. CoRR, abs/1908.09453, 2019. URL http://arxiv.org/abs/1908.09453.

- Leonardos et al. [2021] S. Leonardos, G. Piliouras, and K. Spendlove. Exploration-exploitation in multi-agent competition: convergence with bounded rationality. Advances in Neural Information Processing Systems, 34:26318–26331, 2021.

- Li et al. [2023] W. Li, H. Li, J. Honorio, and Q. Song. Pyxab – a python library for -armed bandit and online blackbox optimization algorithms, 2023. URL https://arxiv.org/abs/2303.04030.

- Ling et al. [2018] C. K. Ling, F. Fang, and J. Z. Kolter. What game are we playing? end-to-end learning in normal and extensive form games. arXiv preprint arXiv:1805.02777, 2018.

- Mandt et al. [2017] S. Mandt, M. D. Hoffman, and D. M. Blei. Stochastic gradient descent as approximate bayesian inference. Journal of Machine Learning Research, 18:1–35, 2017.

- Marris et al. [2023] L. Marris, I. Gemp, and G. Piliouras. Equilibrium-invariant embedding, metric space, and fundamental set of 2x2 normal-form games. arXiv preprint arXiv:2304.09978, 2023.

- McKelvey and Palfrey [1995] R. D. McKelvey and T. R. Palfrey. Quantal response equilibria for normal form games. Games and Economic Behavior, 10(1):6–38, 1995.

- McKelvey et al. [2016] R. D. McKelvey, A. M. McLennan, and T. L. Turocy. Gambit: Software tools for game theory, version 16.0.1, 2016.

- Milec et al. [2021] D. Milec, J. Černỳ, V. Lisỳ, and B. An. Complexity and algorithms for exploiting quantal opponents in large two-player games. Proceedings of the AAAI Conference on Artificial Intelligence, 35(6):5575–5583, 2021.

- Milgrom and Weber [1982] P. R. Milgrom and R. J. Weber. A theory of auctions and competitive bidding. Econometrica: Journal of the Econometric Society, pages 1089–1122, 1982.

- Murty and Kabadi [1985] K. G. Murty and S. N. Kabadi. Some NP-complete problems in quadratic and nonlinear programming. Technical report, 1985.

- Nikaidô and Isoda [1955] H. Nikaidô and K. Isoda. Note on non-cooperative convex games. Pacific Journal of Mathematics, 5(1):807815, 1955.

- Nudelman et al. [2004] E. Nudelman, J. Wortman, Y. Shoham, and K. Leyton-Brown. Run the GAMUT: A comprehensive approach to evaluating game-theoretic algorithms. In AAMAS, volume 4, pages 880–887, 2004.

- Pérolat et al. [2022] J. Pérolat, S. Perrin, R. Elie, M. Laurière, G. Piliouras, M. Geist, K. Tuyls, and O. Pietquin. Scaling mean field games by online mirror descent. In Proceedings of the 21st International Conference on Autonomous Agents and Multiagent Systems, 2022.

- Raghunathan et al. [2019] A. Raghunathan, A. Cherian, and D. Jha. Game theoretic optimization via gradient-based Nikaido-Isoda function. In International Conference on Machine Learning, pages 5291–5300. PMLR, 2019.

- Shoham and Leyton-Brown [2008] Y. Shoham and K. Leyton-Brown. Multiagent systems: Algorithmic, game-theoretic, and logical foundations. Cambridge University Press, 2008.

- Valko et al. [2013] M. Valko, A. Carpentier, and R. Munos. Stochastic simultaneous optimistic optimization. In International Conference on Machine Learning, pages 19–27. PMLR, 2013.

- Wiedenbeck and Brinkman [2023] B. Wiedenbeck and E. Brinkman. Data structures for deviation payoffs. In Proceedings of the 22nd International Conference on Autonomous Agents and Multiagent Systems, 2023.

- Zhou et al. [2017] Y. Zhou, J. Li, and J. Zhu. Identify the Nash equilibrium in static games with random payoffs. In International Conference on Machine Learning, pages 4160–4169. PMLR, 2017.

Appendix A Loss: Connection to Exploitability, Unbiased Estimation, and Upper Bounds

A.1 KKT Conditions Imply Fixed Point Sufficiency

Consider the following constrained optimization problem:

| (13) | ||||

| (14) | ||||

| (15) |

where is concave and and represent inequality and equality constraints respectively. If and are affine functions, then any maximizer of must satisfy the following KKT conditions (necessary and sufficient):

-

•

Stationarity:

-

•

Primal feasibility: for all and for all

-

•

Dual feasibility: for all

-

•

Complementary slackness: for all .

Lemma 1.

Assuming player ’s utility, , is concave in its own strategy , a strategy in the interior of the simplex is a best response if and only if it has zero projected-gradient222Not to be confused with the nonlinear (i.e., introduces bias) projected gradient operator introduced in [Hazan et al., 2017]. norm:

| (16) |

Proof.

Consider the problem of formally computing :

| (17) | ||||

| (18) | ||||

| (19) |

where is some constant that captures our given assumption that the solution lies in the interior of the simplex. Note that the objective is linear (concave) in and the constraints are affine, therefore the KKT conditions are necessary and sufficient for optimality. Mapping the KKT conditions onto this problem yields the following:

-

•

Stationarity:

-

•

Primal feasibility: and for all

-

•

Dual feasibility: for all

-

•

Complementary slackness: for all .

For any point , primal feasibility will be satisfied for some . This implies each is strictly positive. By complementary slackness and dual feasibility, each must be identically zero. This implies the stationarity condition can be simplified to . Rearranging terms we find that for any , there exists a such that

| (20) |

Equivalently, at . Any vector proportional to the ones vector has zero projected-gradient norm, completing the claim. ∎

A.2 Norm of Projected-Gradient and Equivalence to NFG Exploitability with Approximate Best Responses

Proposition 1.

The loss is equivalent to NashConv, but where player ’s best response is approximated by a single step of projected-gradient ascent with step size : .

Proof.

Define an approximate best response as the result of a player adjusting their strategy via a projected-gradient ascent step, i.e., for player .

In a normal form game, player ’s utility at this new strategy is .

Therefore, the amount player gains by playing aBR is

| (21) | ||||

| (22) | ||||

| (23) | ||||

| (24) |

where the third equality follows from the fact that the projected-gradient, , is orthogonal to the ones vector. ∎

A.3 Connection to True Exploitability

Lemma 2.

The amount a player can gain by deviating is upper bounded by a quantity proportional to the norm of the projected-gradient:

| (25) |

Proof.

Let be any point on the simplex. Then by concavity of with respect to ,

| (26) | ||||

| (27) | ||||

| (28) | ||||

| (29) |

∎

Continuing, we can prove a bound on in terms of the projected-gradient loss:

Lemma 3.

The exploitability, , of a joint strategy , is upper bounded as a function of our proposed loss:

| (30) |

Proof.

| (31) | ||||

| (32) | ||||

| (33) | ||||

| (34) | ||||

| (35) | ||||

| (36) | ||||

| (37) | ||||

| (38) | ||||

| (39) |

∎

Lemma 4.

The entropy regularized exploitability, , of a joint strategy , is upper bounded as a function of our proposed loss:

| (40) |

Proof.

Recall that is also concave with respect to . Then

| (41) | ||||

| (42) | ||||

| (43) | ||||

| (44) | ||||

| (45) | ||||

| (46) | ||||

| (47) | ||||

| (48) | ||||

| (49) |

∎

A.4 Unbiased Estimation

Lemma 5.

An unbiased estimate of can be obtained by drawing two samples (pure strategies) from each players’ mixed strategy and observing payoffs.

Proof.

Define as the random variable distributed according to the distribution induced by all players’ mixed strategies. Let and represent two other independent random variables, distributed identically to . Then

| (50) | ||||

| (51) | ||||

| (52) | ||||

| (53) | ||||

| (54) | ||||

| (55) | ||||

| (56) | ||||

| (57) | ||||

| (58) | ||||

| (59) |

where is an unbiased estimator of player ’s gradient.

∎

Lemma 6.

The loss formed as the sum of the squared norms of the projected-gradients, , can be decomposed into three terms as follows:

| (60) |

where is any player other than .

Proof.

Let so that . Note that .

| (61) | ||||

| (62) | ||||

| (63) | ||||

| (64) | ||||

| (65) |

where and .

∎

A.5 Bound on Loss

By equation (50), we can also rewrite this loss as a weighted sum of -norms, where for brevity. This will allow us to more easily analyze our loss.

Lemma 7.

Assume payoffs are bounded by , then setting or or ensures for all .

Proof.

| (66) | ||||

| (67) | ||||

| (68) | ||||

| (69) | ||||

| (70) | ||||

| (71) | ||||

| (72) |

∎

The th element of the sum in the loss does not depend on agent ’s strategy. We will rewrite the loss to make its dependence on all other players’ strategies more obvious ( below).

| (73) | ||||

| (74) | ||||

| (75) | ||||

| (76) | ||||

| (77) | ||||

| (78) | ||||

| (79) |

where does not depend on .

Note this means we can also write for any .

Lemma 8.

Assume payoffs are bounded in , then

| (80) |

for any such that .

Appendix B QREs Approximate NEs at Low Temperature

Lemma 9.

Setting with ensures that all QREs contain probabilities greater than .

Proof.

Let . Then the minimum possible probability mass for any action is lower bounded as

| (86) | ||||

| (87) | ||||

| (88) | ||||

| (89) |

Let such that , then

| (90) | ||||

| (91) | ||||

| (92) | ||||

| (93) |

This implies if we set , then we are guaranteed that all QREs contain probabilities greater than . ∎

Lemma 10 (Repeated from Lemma 1 of Milec et al. [2021]).

Let be player ’s gradient () with payoffs bounded in and be a QRE at temperature . Then it holds that

| (94) |

where is the Lambert function ().

Lemma 11 (Slightly modified from Proposition 5.1a of Beck and Teboulle [2003]).

Let if else . Then is -strongly convex over w.r.t. the and norms, i.e.,

| (95) | ||||

| (96) |

for all .

Lemma 12.

Let where , , and with defined in Lemma 11. Finally, let . Then

| (97) |

Proof.

Plugging on into , we find

| (98) | ||||

| (99) |

for all . Note that is -strongly convex on , therefore, is also -strongly convex in . Continuing, this also implies is -strongly convex.

Let and note that . Strong convexity of implies

| (100) | ||||

| (101) | ||||

| (102) | ||||

| (103) | ||||

| (104) |

Rearranging the inequality achieves the desired result. ∎

Lemma 13.

[Low Temperature Approximate QREs are Approximate Nash Equilibria] Let be player ’s entropy regularized gradient with payoffs bounded in and be an approximate QRE. Then it holds that

| (105) |

where is the Lambert function ().

Proof.

First note that for . Recall that the softmax is invariant to constant offsets to its argument, i.e., for any . Then

| (106) | ||||

| (107) | ||||

| (108) | ||||

| (109) | ||||

| (110) |

where the closed-form solution to the minimization problem as a softmax formula comes from inspecting the Entropic Descent Algorithm (EDA) of Beck and Teboulle [2003].

Then, beginning with the definition of exploitability, we find

| (111) | ||||

| (112) | ||||

| (113) | ||||

| (114) | ||||

| (115) |

∎

Lemma 14.

[ Scores Nash Equilibria] Let be our proposed entropy regularized loss function with payoffs bounded in and be an approximate QRE. Then it holds that

| (116) |

where is the Lambert function ().

Appendix C Gradient of Loss

Lemma 15.

The gradient of with respect to player ’s strategy is

| (123) |

where and for .

Proof.

Recall from Lemma 6 that the loss can be decomposed as .

Then

| (124) |

where and does not depend on .

Also, letting ,

| (125) | ||||

| (126) | ||||

| (127) | ||||

| (128) | ||||

| (129) |

And

| (130) | ||||

| (131) | ||||

| (132) | ||||

| (133) |

Putting these together, we find

| (134) | ||||

| (135) | ||||

| (136) |

∎

C.1 Unbiased Estimation

In order to construct an unbiased estimate of , we will need to form two independent unbiased estimates of . Recall that is simply the expected bimatrix game between players and when all other players sample their actions according to their current strategies.

C.2 Bound on Gradient / Lipschitz Property

Lemma 16.

Assume payoffs are upper bounded by , then the infinity norm of the gradient is bounded as

| (137) |

Proof.

Recall from Lemma 15 that the gradient of with respect to player ’s strategy is

| (138) |

where and for .

For payoffs in , the entries in are bounded within with a range . Similarly, the entries in are bounded within with a range of .

The infinity norm of the gradient can then be bounded as

| (139) | ||||

| (140) | ||||

| (141) | ||||

| (142) | ||||

| (143) | ||||

| (144) | ||||

| (145) |

where the second inequality follows from Lemma 20.

∎

Corollary 2.

If is set according to Lemma 9, then the infinity norm of the gradient is bounded as

| (146) |

where and is defined implicitly for convenience in other derivations.

Proof.

As , the norm of the gradient blows up because the gradient of Shannon entropy blows up for small probabilities. As , the norm of the gradient blows up because we require infinite temperature to guarantee all QREs are nearly uniform; recall is the regularization coefficient on the entropy bonus terms which means our modified utilities blow up for large . In practice, setting to , e.g., is sufficient. ∎

Appendix D Hessian of Loss

We will now derive the Hessian of our loss. This will be useful in establishing properties about global minima that enable the application of tailored minimization algorithms. Let denote the differential operator applied to (possibly multivalued) function with respect to . For example, where is player ’s payoff tensor according to the three-way approximation between players , , and to the game at .

Lemma 17.

The Hessian of can be written

| (150) |

where , , and we augment (the -player tensor approximation to the game, ) so that and otherwise .

Proof.

Recall the gradient of our proposed loss:

| (151) |

where and for .

Consider the following Jacobians, which will play an auxiliary role in our derivation of the Hessian:

| (152) | ||||

| (153) | ||||

| (154) | ||||

| (155) | ||||

| (156) | ||||

| (157) | ||||

| (158) | ||||

| (159) | ||||

| (160) | ||||

| (161) | ||||

| (162) | ||||

| (163) |

We can derive the diagonal blocks of the Hessian as

| (164) | ||||

| (165) | ||||

| (166) | ||||

| (167) | ||||

| (168) | ||||

| (169) | ||||

| (170) |

and the off-diagonal blocks as

| (171) | ||||

| (172) | ||||

| (173) | ||||

| (174) | ||||

| (175) | ||||

| (176) | ||||

| (177) |

Therefore, the Hessian can be written concisely as

| (178) |

where , , and we augment (the -player tensor approximation to the game, ) so that and otherwise .

∎

Appendix E Regret Bounds

Lemma 18.

[Loss Regret to Exploitability Regret] Assume exploitability of a joint strategy is upper bounded by where is a concave function and is a loss function. Let be a joint strategy randomly drawn from the set of predictions made by an online learning algorithm over steps. Then the expected exploitability of is bounded by the average regret of :

| (179) |

Proof.

| (180) | ||||

| (181) | ||||

| (182) |

where the second inequality follows from Jensen’s inequality. ∎

Theorem 1.

[BLiN PAC Rate] Assume as defined in Lemma 2, so that all equilibria place at least mass on each strategy, and a previously pulled arm is returned uniformly at random (i.e., ). Then for any ,

| (183) |

with probability where is the Lambert function (), , and is an upper bound on the maximum sampled value from (see Lemma 8).

Proof.

Assume as defined in Lemma 2 so that is -Lipschitz with respect to . Also assume a previously pulled arm is returned uniformly at random. Starting with Lemma 14 and applying Corollary 9, we find

| (184) | ||||

| (185) | ||||

| (186) |

with probability where is the Lambert function (), , and is an upper bound on the range of sampled values from (see Lemma 8).

Recall . Therefore,

| (187) | ||||

| (188) |

Markov’s inequality then allows us to bound the pointwise exploitability of any arm returned by the algorithm as

| (189) |

with probability for any . ∎

Appendix F Complexity

F.1 Polymatrix Games

Lemma 19.

For a polymatrix game defined by the set of bimatrix games with payoff matrix for every player and , the rank of the matrix defined in equation (11) can be equivalently studied by replacing all instances of with .

Proof.

Consider the polymatrix game given by the set of matrices for every and . The polymatrix game can be equivalently written in normal form, albeit, less concisely. Note that the polymatrix approximation, , as we have defined it (see Section 2 Preliminaries) of this normal-form representation between players and with all other players’ strategies marginalized out is related to the true underlying bimatrix game between them as follows:

| (190) | ||||

| (191) | ||||

| (192) |

where is player ’s payoff matrix for the bimatrix game between players and in a polymatrix game and does not depend on player ’s strategy.

This implies that is equal to up to a constant offset of the rows, i.e.,

| (193) |

where is a matrix with constant rows.

Consider the matrix which contains blocks. Recall that the bottom rows of contain rows of ’s matching each column of blocks. Consider multiplying the th row of ’s (which contains ’s on all columns not in the th block) by and subtracting it from the block containing ,

| (194) |

Note that still remains a matrix with constant rows (the preconditioner effectively subtracts a constant matrix from ). This multiplying and subtracting a row from another is an elementary operation on the matrix, meaning it does not change its row rank. Therefore, for a polymatrix game, we can reason about the positive definiteness of the Hessian at equilibria by examining the matrix with all ’s swapped for ’s. ∎

Interestingly, at zero temperature (where QRE = Nash), is constant for a polymatrix game, so the rank of this matrix can be computed just once to extract information about all possible interior equilibria in the game. Furthermore, the Hessian is positive semi-definite over the entire joint strategy space, implying the loss function is convex (see Figure 5 (left) for empirical support). This indicates, by convex optimization theory, 1) all mixed Nash equilibria in polymatrix games form a convex set (i.e., they are connected) and 2) assuming mixed equilibria exist, they can be computed simply by stochastic gradient descent on . If is rank-, then this interior equilibrium is unique.

Complexity

Approximation of Nash equilibria in polymatrix games is known to be PPAD-hard [Deligkas et al., 2022]. In contrast, if we restrict our class of polymatrix games to those with at least one interior Nash equilibrium, our analysis proves we can find an approximate Nash equilibrium in deterministic, polynomial time (Corollary 3). This follows directly from the fact that is convex, our decision set is convex, and convex optimization theory admits polynomial time approximation algorithms (e.g., gradient descent). We consider the assumption of the existence of an interior Nash equilibrium to be relatively mild333Marris et al. [2023] shows -player, -action polymatrix games with interior Nash equilibria make up a non-trivial of the space of possible games., so this positive complexity result is surprising.

Also, note that the Hessian of the loss at Nash equilibria is encoded entirely by the polymatrix approximation at the equilibrium. Therefore, approximating the Hessian of about the equilibrium (which amounts to observing near-equilibrium behavior [Ling et al., 2018]) allows one to recover this polymatrix approximation (up to constant offsets of the columns which equilibria are invariant to [Marris et al., 2023]).

Corollary 3 (Approximating Nash Equilibria of Polymatrix Games with Interior Equilibria).

Consider the class of polymatrix games with interior Nash equilibria. This class of games admits a fully polynomial time deterministic approximation scheme (FPTAS).

Proof.

Lemma 3 relates the approximation of Nash equilibria to the minimization of the loss function . By Lemma 1, this loss function attains its minimum value of zero if and only if is a Nash equilibrium. For polymatrix games, the Hessian of this loss function is everywhere finite and positive definite (Lemma 17), therefore, this loss function is convex. The decision set for this minimization problem is the product space of simplices, therefore it is also convex. Given that we only consider polymatrix games with interior Nash equilibria, we know that our loss function attains a global minimum within this set. By convex optimization theory, this function can be approximately minimized in a polynomial number of steps by, for example, (projected) gradient descent. Gradient descent requires computing the gradient of the loss function at each step. From Lemma 15, we see that computing the gradient (at zero temperature) simply requires reading the polymatrix description of the game (i.e., each bi-matrix game between players), which is clearly polynomial in the size of the input (the polymatrix description). The remaining computational steps of gradient descent (e.g., projection onto simplices) are polynomial as well. In conclusion, gradient descent approximates a Nash equilibrium in polynomial number of steps (logarithmic if strongly-convex), each of which costs polynomial time, therefore the entire scheme is polynomial. ∎

F.2 Normal-Form Games

Corollary 1.

Consider the class of NFGs with at least one polymatrix-isolated QRE(). Then by Theorem 1, BLiN is a fully polynomial-time randomized approximation scheme (FPRAS) for QREs.

Proof.

If , an -QRE can be obtained with BLiN in a number of iterations that is polynomial in the game description length (). ∎

F.2.1 Concrete Example

The end of Section 6 stated a concrete result for a -player, -action game assuming we are given that the game has an interior Nash equilibrium. This result requires re-deriving a rate similar to Theorem 1, but for the unregularized game.

For example, revisiting Corollary 2 but for zero temperature, we find . Let as before. Now, consulting Table 2, we find that samples from are constrained to a range of size . Applying Corollary 9 to Lemma 3, we find:

| (195) |

with probability . Plugging in , , and and solving for numerically, we find that . For such large , . Again consulting Table 2, each call (arm pull) of BLiN costs , implying a total query cost of . In contrast, there exist scalar entries in the payoff tensor, which is a factor larger by .

Appendix G Helpful Lemmas and Propositions

Proposition 2.

The matrix is a projection matrix and therefore idempotent. It is also symmetric, which implies it is its own square root.

Proof.

| (196) | ||||

| (197) | ||||

| (198) |

∎

Proposition 3.

The matrix is positive semi-definite.

Proof.

Let . Then

| (199) | ||||

| (200) | ||||

| (201) | ||||

| (202) | ||||

| (203) |

∎

Proposition 4.

The matrix has rank and its -d nullspace lies along .

Proof.

Note that for matrices and of the same dimension. Let and and apply :

| (204) |

We can confirm the nullspace by inspection:

| (205) |

∎

Lemma 20.

The product for any has entries whose absolute value is bounded by where represent the minima and maxima of the matrices respectively.

Proof.

The matrix is idempotent so we can rewrite the product for any as

| (206) |

The matrix has the property that it removes the mean from every row of a matrix when right multiplied against it, i.e., removes the means from the rows of . Similarly, left multiplying it removes the means from the column. Let and represent these mean-centered results respectively. The absolute value of the th entry in the resulting product can then be recognized as

| (207) | ||||

| (208) | ||||

| (209) |

The variance of a bounded random variable is upper bounded by . Hence its standard deviation is bounded by . Plugging these bounds for and into equation (209) completes the claim. ∎

Appendix H Maps from Hypercube to Simplex Product

In this section, we derive properties of a map from the unit-hypercube to the simplex product. This map is necessary to to adapt our proposed loss to the commonly assumed setting in the -armed bandit literature Bubeck et al. [2011]. We derive relevant properties of two such maps: the softmax and a mapping that interprets dimensions of the hypercube as angles on a unit-sphere that is then -normalized.

Lemma 21.

Let . Then .

Proof.

| (210) |

∎

Lemma 22.

The -norm of the Jacobian-transpose of a transformation applied elementwise to a product space is bounded by the -norm of the Jacobian-transpose of a single transformation from that product space, i.e., for any .

Proof.

Let , and where ; denotes column-wise stacking, . Also, and for all and . Then the Jacobian of is

| (211) |

The -norm of this matrix is the max -norm of any row. This matrix is diagonal, therefore, the -norm of each elementwise Jacobian-transpose represents the max -norm of the rows spanned by its block. Given that the domains, ranges, and transformations for all blocks are the same, their -norms are also the same. The max over the blocks is then equal to the -norm of any individual . ∎

H.1 Hessian of Bandit Reward Function

Lemma 23.

Let be a function that maps the unit hypercube to the simplex product (mixed strategy space). Then the objective function . The Hessian of at an optimum in direction is where is the Hessian of and is the Jacobian of .

Proof.

| (212) | ||||

| (213) |

∎

Lemma 24.

Let be an injective function, i.e., . Also let be the Jacobian of with respect to and be a nonzero vector in the tangent space of . Then

| (214) |

Proof.

Recall that the th entry of the Jacobian represents so that the th entry of is

| (215) |

Assume . This would imply a change in results in no change in (), contradicting the fact that is injective. Therefore, we must conclude the claim that . ∎

Lemma 25.

Let be the Jacobian of the softmax operator. Then and .

Proof.

Let represent the th entry of for any . Then the -norm of row is upper bounded as

| (216) | ||||

| (217) | ||||

| (218) | ||||

| (219) | ||||

| (220) | ||||

| (221) | ||||

| (222) |

Also, the -norm of row is upper bounded similarly as

| (224) | ||||

| (225) | ||||

| (226) | ||||

| (227) | ||||

| (228) | ||||

| (229) |

The -norm of a matrix is the maximum -norm of any row. Therefore, and are both upper bounded by . ∎

Lemma 26.

Let be the Jacobian of any composition of transformations where . Then lies in the tangent space of the simplex.

Proof.

We aim to show for any and . By chain rule, the Jacobian of is . Therefore, . Consider the first product:

| (230) |

by Lemma 28. Therefore . This implies is orthogonal to for any and , therefore lies in the tangent space of the simplex for any and . ∎

For spherical coordinates, where , maps angles to the unit sphere, and .

Definition 2.

Define as the transformation to the unit-sphere using spherical coordinates:

| (231) | ||||

| (232) | ||||

| (233) | ||||

| (234) | ||||

| (235) | ||||

| (236) |

Lemma 27.

Let be the Jacobian of the transformation to the unit-sphere using spherical coordinates, i.e. where and represents an angle for each . Then .

Proof.

The Jacobian of the transformation is

| (237) |

and it square is

| (238) |

where

| (239) | ||||

| (240) |

To compute the Frobenius norm, we will need the sum of the squares of all entries. We will consider the sum of each row individually using the following auxiliary variable where and apply a recursive inequality.

| (242) | ||||

| (243) | ||||

| (244) | ||||

| (245) | ||||

| (246) | ||||

| (247) | ||||

| (248) |

Note then that . We know , therefore, by applying the inequality recursively. Finally, implies the claim . ∎

Lemma 28.

Let be the Jacobian of where . Then .

Proof.

The th entry of the Jacobian of is

| (249) |

Therefore where is a point on the unit-sphere in the positive orthant. ∎

Appendix I A2: Bounded Diameters and Well-shaped Cells

We assume the feasible set is a unit-hypercube of dimensionality where cells are evenly split along the longest edge to give new partitions and represents the center of each cell.

There exists a decreasing sequence , such that for any depth and for any cell of depth , we have . Moreover, there exists such that for any depth , any cell contains an -ball of radius centered at .

I.1 -Norm

Lemma 29 (-Norm Bounding Ball).

Let . Then where and .

Proof.

| (250) | ||||

| (251) | ||||

| (252) | ||||

| (253) | ||||

| (254) | ||||

| (255) | ||||

| (256) | ||||

| (257) | ||||

| (258) | ||||

| (259) | ||||

| (260) | ||||

| (261) |

where , , and . ∎

Lemma 30 (-Norm Inner Ball).

Let . Any cell contains an -ball of radius where .

Proof.

Any cell contains an -ball of radius equal to its shortest axis:

| (262) | ||||

| (263) | ||||

| (264) | ||||

| (265) |

∎

I.2 -Norm

Lemma 31 (-Norm Bounding Ball).

Let . Then where and .

Proof.

Any cell is contained by an -ball of radius equal to its longest axis:

| (266) | ||||

| (267) | ||||

| (268) | ||||

| (269) |

where , and . ∎

Lemma 32 (-Norm Inner Ball).

Let . Any cell contains an -ball of radius where .

Proof.

Any cell contains an -ball of radius equal to its shortest axis:

| (270) | ||||

| (271) | ||||

| (272) | ||||

| (273) |

∎

I.3 Near Optimality Dimension

This is written in terms of a maximizing .

Assumption 1.

Locally around each interior , is lower bounded by and upper bounded by where with and if . In other words, for all :

| (274) | ||||

| (275) |

where we have left the precise norm unspecified for generality.

Definition 3.

Definition 4.

Corollary 4.

.

Proof.

By Assumption 1, . Therefore, any that satisfies the requirement for an element of , , will also satisfy the requirement for an element of . ∎

Definition 5.

The -near optimality dimension is the smallest such that there exists such that for any , the maximum number of disjoint -balls of radius and center in is less than .

Theorem 2.

The -near optimality dimension of under is with constant

| (276) |

Proof.

First, let us define as in equation (287) which implies . Then apply Lemmas 33 () and 35 () which bound the number of -balls required to pack when is less than and greater than respectively:

| (277) | ||||

| (278) |

and

| (279) | ||||

| (280) | ||||

| (281) | ||||

| (282) | ||||

| (283) | ||||

| (284) |

where is the volume constant for a -sphere under the given norm. has been upper bounded for the -norm in Lemma 34. For the -norm, . We have written in terms of to clarify which is larger.

Therefore,

| (285) | ||||

| (286) |

Intuitively, if the radius for which the polynomial bounds hold () is large and the minimum curvature constant is also large, then the bound holds for large deviations from optimality . The number of -radius -balls required to cover the remaining space, , will be comparatively small. ∎

Corollary 5 (Zooming Dimension).

The zooming dimension of under is .

Proof.

Mapping the definition of zooming dimension onto -near optimality, we find and . Then we can infer . This result only effects the constant , not the zooming dimension.

If , then . ∎

Lemma 33 ().

The number of disjoint -balls that can pack into a set , , is upper bounded by where and and is the volume constant for a -sphere under the given norm .

Proof.

The number of disjoint -balls of radius and center in can be upper bounded as follows.

Rewrite by rearranging terms as

| (287) |

and recall that from Corollary 4 that . Furthermore, an -ball of radius implies

| (288) |

The number of disjoint -balls that can pack into a set , , is upper bounded by the ratio of the volumes of the two sets:

| (289) | ||||

| (290) | ||||

| (291) | ||||

| (292) | ||||

| (293) | ||||

| (294) | ||||

| (295) |

where and and is the volume constant for a -sphere under the given norm , e.g., for . ∎

Corollary 6.

If ,

| (296) |

In other words, where and .

Corollary 7.

If Assumption 1 is given in terms of the -norm, these can be translated to bounds in terms of the -norm resulting in the same -near optimality dimension but incurring an additional exponential factor in the constant .

Proof.

Recall that , therefore

| (297) | ||||

| (298) |

where and . Then

| (299) |

∎

Recall, these results apply when , i.e., when . Otherwise, we can upper bound the number of -balls by considering the entire set which has volume . First, we will bound the constant associated with the volume of a -sphere.

Lemma 34.

The volume of a -sphere with radius and even is given by where .

Proof.

First, we recall Stirling’s bounds on the factorial: . This will be useful for bounding the Gamma function: for even .

Given is even, we start with the exact formula for :

| (300) | ||||

| (301) | ||||

| (302) | ||||

| (303) | ||||

| (304) | ||||

| (305) |

∎

Lemma 35 ().

The number of disjoint -balls that can pack into a set , , is upper bounded by where and is the volume constant for a -sphere under a given norm.

Proof.

Corollary 8.

If Assumption 1 is given in terms of the -norm, these can be translated to bounds in terms of the -norm resulting in the same -near optimality dimension but incurring an additional exponential factor in the constant .

Proof.

| (311) | ||||

| (312) | ||||

| (313) | ||||

| (314) |

∎

If we further assume , then we can bound the number of -balls required with a constant, independent of , as

| (315) | ||||

| (316) | ||||

| (317) |

where , for and for , for . dominates for large . The cross over occurs at

| (318) | ||||

| (319) | ||||

| (320) |

where was defined in equation (287). As grows and exceeds , begins to dominate, therefore we will upper bound as

| (321) |

| Locality | |

|---|---|

For convenience, we repeat the other relevant constants in Table 5.

Appendix J D-BLiN

The regret bound for Doubling BLiN [Feng et al., 2022] was originally proved assuming a standard normal distribution, however, the authors state their proof can be easily adapted to any sub-Gaussian distribution, which includes bounded random variables. This matches our setting with bounded payoffs, so we repeat their analysis here for that setting.

Definition 6 (Global Arm Accuracy).

.

Define: .

Definition 7 (Elimination Rule).

Eliminate if where .

Lemma 36.

.

Proof.

Assume with and . Applying a Hoeffding inequality gives

| (322) | ||||

| (323) | ||||

| (324) |

By Lipschitzness of we also have

| (325) |

Then consider

| (326) | ||||

| (327) | ||||

| (328) | ||||

| (329) |

with probability . The first inequality follows by triangle inequality and the second follows from equation (325) and considering the complement of equation (324).

The complement of this result occurs with probability

| (330) |

At least arm is played in each cube for , therefore, must be true given the exit condition of the algorithm. In addition, assume ( will be defined such that this is true). Then a union bound over all events gives

| (331) | ||||

| (332) | ||||

| (333) | ||||

| (334) |

Taking the complement of this event and noting that gives the desired result. ∎

Lemma 37 (Optimal Arm Survives).

Under event , the optimal arm is not eliminated after the first batches.

Proof.

Let denote the cube containing in . Under event , for any cube and , the following relation shows that avoids the elimination rule in round :

| (335) | ||||

| (336) | ||||

| (337) | ||||

| (338) |

where the first inequality follows from applying Lemma 36 to upper bound and individually. The remaining steps use the optimality of , the definition of , and the elimination rule. ∎

Lemma 38.

Under event , for any , any and any , satisfies

| (339) |

Proof.

For , recall that is the side length of a cube , therefore, holds directly from the Lipschitzness of .

For , let be the cube containing . From Lemma 37, this cube has not been eliminated under event . For any cube and , it is clear that is also in the parent of , denoted (). Then for any , it holds that

| (340) | ||||

| (341) | ||||

| (342) | ||||

| (343) | ||||

| (344) | ||||

| (345) |

where we have applied Lemma 36 similarly as in Lemma 37 and also used the definition of . The last two inequalities use the fact that and was not eliminated. ∎

Theorem 3.

With probability exceeding , the -step total regret of BLiN with Doubling Edge-length Sequence (D-BLiN) Feng et al. [2022] satisfies

| (346) |

where is the zooming dimension of the problem instance. In addition, D-BLiN only needs no more than rounds of communications to achieve this regret rate.

Proof.

Since for the Doubling Edge-length Sequence, Lemma 38 implies that every cube is a subset of . Thus from the definition of zooming number (Corollary 5 with appropriate condition), we have

| (347) |

Fix any positive number . Also by Lemma 38, we know that any arm played after batch incurs a regret bounded by , since the cubes played after batch have edge length no larger than . Then the total regret that occurs after batch is bounded by (where is an upper bound on the number of arms).

Thus the regret can be bounded as

| (348) |

where the first term bounds the regret in the first batches of D-BLiN, and the second term bounds the regret after the first batches. If the algorithm stops at batch , we define for any and inequality equation (348) still holds.

By Lemma 38, we have for all . We can thus bound equation (348) by

| (349) | ||||

| (350) | ||||

| (351) | ||||

| (352) |

where equation (350) uses equation (347), and equation (351) uses equality . Since and , we have

| (353) | ||||

| (354) |

Continuing we find

| (355) | ||||

| (356) | ||||

| (357) | ||||

| (358) | ||||

| (359) | ||||

| (360) | ||||

| (361) |

This inequality holds for any positive . By choosing , we have

| (362) | ||||

| (363) | ||||

| (364) | ||||

| (365) |

∎

Corollary 9.

Proof.

∎

Appendix K Experimental Setup and Details

Here we provide further details on the experiments.

K.1 GAMBIT

The seven methods from the gambit [McKelvey et al., 2016] library that we tested on the -player and -player Blotto games are listed below (with runtimes). Only gambit-enumpoly and gambit-enumpure are able to return any NE for -player Blotto within a hour time limit (and only pure equilibria). And only gambit-enumpure returns any NE for the -player game.

-

•

gambit-enumpoly [73 sec 3-player, timeout 4-player]

-

•

gambit-enumpure [72 sec 3-player, 45 sec 4-player]

-

•

gambit-gnm

-

•

gambit-ipa

-

•

gambit-liap

-

•

gambit-logit

-

•

gambit-simpdiv

K.2 Loss Visualization and Rank Test

Figure 5 and claims made in Section 5 analyze several classical matrix games. We report the payoff matrices in standard row-player / column-player payoff form below. All games are then shifted and scaled so payoffs lie in (i.e., first by subtracting the minimum and then scaling by the max).

RPS:

| (367) |

Chicken:

| (368) |

Matching Pennies:

| (369) |

Modified-Shapleys:

| (370) |

Prisoner’s Dilemma:

| (371) |

K.2.1 Loss on Familiar Games

K.3 Saddle Point Analysis

To generate Figure 2, we follow a procedure similar to the study of MNIST in [Dauphin et al., 2014] (Section 3 of Supp.). Their recommended procedure searches for critical points in two ways. The first repeats a randomized, iterative optimization process times. They then sample one these trials at random, select a random point along the descent trajectory, and search for a critical point (using Newton’s method) nearby. They repeat this sampling process times. The second approach randomly selects a feasible point in the decision set and searches for a critical point nearby (again using Newton’s method). They also perform this times.

Our protocol differs from theirs slightly in a few respects. One, we use SGD, rather than the saddle-free Newton algorithm to trace out an initial descent trajectory. Two, we do not add noise to strategies along the descent trajectory prior to looking for critical points. Thirdly, we minimize gradient norm rather than use Newton’s method to look for critical points. Lastly, we use different experimental hyperparameters. We run SGD for iterations rather than epochs and rerun SGD times rather than . We sample points for each of the two approaches for finding critical points.

K.4 SGD on Classical Games

The games examined in Figure 3 were all taken from [Gemp et al., 2022]. Each is available via open source implementations in OpenSpiel [Lanctot et al., 2019] or GAMUT [Nudelman et al., 2004].

We compare against several other baselines, replicating the experiments in [Gemp et al., 2022]. RM indicates regret-matching and FTRL indicates follow-the-regularized-leader. These are, arguably, the two most popular scalable stochastic algorithms for approximating Nash equilibria. is a stochastic algorithm developed in [Gemp et al., 2022].

For each of the experiments, we sweep over learning rates in log-space from to in increments of . We also consider whether to run SGD with the projected-gradient and whether to constrain iterates to the simplex via Euclidean projection or entropic mirror descent [Beck and Teboulle, 2003]. We then presented the results of the best performing hyperparameters. This was the same approach taken in [Gemp et al., 2022].

Saddle Points in Blotto

To confirm the existence of saddle points, we computed the Hessian of for SGD (), deflated the matrix by removing from its eigenvectors all directions orthogonal to the simplex, and then computed its top- eigenvalues. We do this because there always exists a -dimensional nullspace of the Hessian at zero temperature that lies outside the tangent space of the simplex, and we only care about curvature within the tangent space. Specificaly, at an equilibrium , if we compute where is formed as a linear combination of the vectors , then each block is identically zero at an equilibrium: . By Lemma 17, this implies there is zero curvature of the loss in the direction : .

K.5 BLiN on Artificial Game

To construct the -player, -action, symmetric, artifical game in Figure 4, we used the following coefficients (discovered by trial-and-error):

| (372) |

The first row indicates the payoffs received when player plays action and the background population plays any of the possible joint actions (number of combinations with replacement). For example, the first column indicates the payoff when all background players play action . The second column indicates all background players play action except for one which plays action , and so on. The last column indicates all background players play action . These scalars uniquely define the payoffs of a symmetric game.

Given that this game only has two actions, we represent a mixed strategy by a single scalar , i.e., the probability of the first action. Furthermore, this game is symmetric and we seek a symmetric equilibrium, so we can represent a full Nash equilibrium by this single scalar . This reduces our search space from variables to variable (and obviates any need for a map from the unit hypercube to the simplex—see Lemma 25).