Finite Sample Performance of a Conduct Parameter Test in Homogenous Goods Markets

Abstract

We assess the finite sample performance of the conduct parameter test in homogeneous goods markets. Statistical power rises with an increase in the number of markets, a larger conduct parameter, and a stronger demand rotation instrument. However, even with a moderate number of markets and five firms, regardless of instrument strength and the utilization of optimal instruments, rejecting the null hypothesis of perfect competition remains challenging. Our findings indicate that empirical results that fail to reject perfect competition are a consequence of the limited number of markets rather than methodological deficiencies.

Keywords: Conduct parameters, Homogenous goods market, Monte Carlo simulation, Statistical power analysis

JEL Codes: C5, C12, L1

1 Introduction

Measuring competitiveness is important in the empirical industrial organization literature. A conduct parameter is considered to be a useful measure of competitiveness. However, the parameter cannot be directly measured from data because data generally lack information about marginal costs. Therefore, researchers endeavor to learn conduct parameters.

Researchers estimate and test structural models to understand firm conduct in both homogeneous and differentiated good markets (Nevo 1998, Magnolfi and Sullivan 2022, Duarte et al. 2023). We focus on homogenous good markets. The conduct parameters for the linear model are identified by Bresnahan (1982), and Matsumura and Otani (2023b) resolve conflicts between Bresnahan (1982) and Perloff and Shen (2012) vis-a-vis identification problems. Estimation accuracy may be improved by adding equilibrium existence conditions in the log-linear model (Matsumura and Otani 2023a). Conduct parameter testing is undertaken by Genesove and Mullin (1998), who compare estimates from the sugar industry with direct measures of market power.111Genesove and Mullin (1998) made mistakes on how to get predicted interaction terms of rotation demand instruments and endogenous quantity in the first stage regression. See Section A.3, Matsumura and Otani (2023b). When market power is around 0.1 and the number of markets is less than 100, perfect competition cannot be rejected. Clay and Troesken (2003) investigate the robustness of specifications using 38 whiskey markets and find that estimation is sensitive to model specification. Steen and Salvanes (1999) study 48 markets in the French salmon industry and Shaffer (1993) studies 25 markets in the Canadian banking industry. They also cannot reject the null hypothesis that markets are perfectly competitive. Their results raise doubts about the methodology in itself (Shaffer and Spierdijk 2017).

Recent literature on conduct parameter estimation and test in homogenous goods markets like an electricity generation industry follows Genesove and Mullin (1998) and proceeds with a comparison of estimated conduct parameters with directly measured ones through price-cost markups recovered from observed prices and marginal costs data. Wolfram (1999) studies the British electricity industry using 25,639 samples and finds that the directly measured conduct parameter is about 0.05 and the estimated conduct parameter is 0.01. So, the author cannot reject the null hypothesis of perfect competition. Kim and Knittel (2006) study California electricity markets using 21,104 samples and find that Bresnahan’s technique overstates marginal costs on average and is likely to reject the null hypothesis of perfect competition. Puller (2007) uses 163 to 573 samples and cannot reject the null hypothesis of Cournot competition for the same industry. The robustness of the data and methodology has been extensively tested in previous studies focusing on market power in the California electricity market (for example, Borenstein et al. (2002), Wolak (2003), and Orea and Steinbuks (2018)).

While popular, there is a lack of formal Monte Carlo simulations for a conduct parameter test. The lack prevents us from understanding the above comparison properly. Accordingly, we investigate the finite sample performance of the conduct parameter test in homogeneous goods markets. We analyze statistical power by varying the number of markets, firms, and strength of demand rotation instruments under the null hypothesis of perfect competition.

Our findings indicate that statistical power increases with more markets, a larger conduct parameter, and stronger demand rotation instruments. However, even with a moderate number of markets (e.g., 1000) and five firms, we cannot achieve an 80% rejection frequency (, where represents the probability of a Type II error), irrespective of instrument strength and the use of optimal instruments. While optimal instruments enhance rejection probability in large samples, they do not alter the core findings. This highlights the challenge of testing perfect competition, as recognized by Genesove and Mullin (1998), Steen and Salvanes (1999), and Shaffer (1993), primarily stemming from the limited number of markets rather than methodological flaws.

Our results and code provide a valuable reference for applied researchers examining assumptions about firm conduct in homogeneous goods markets, i.e., whether it is perfect competition, Cournot competition, or perfect collusion.

2 Model

Consider data with markets with homogeneous products. Assume that there are firms in each market. Let be the index for markets. Then, we obtain a supply equation:

| (1) |

where is the aggregate quantity, is the demand function, is the marginal cost function, and is the conduct parameter. The equation nests perfect competition (), Cournot competition (), and perfect collusion () (See Bresnahan (1982)).

Consider an econometric model integrating the above. Assume that the demand and marginal cost functions are written as:

| (2) | |||

| (3) |

where and are vectors of exogenous variables, and are error terms, and and are vectors of parameters. Additionally, we have demand- and supply-side instruments, and , and assume that the error terms satisfy the mean independence conditions, .

2.1 Linear demand and cost

Assume that linear demand and marginal cost functions are specified as:

| (4) | ||||

| (5) |

where and are exogenous cost shifters and is Bresnahan’s demand rotation instrument. The supply equation is written as:

| (6) |

By substituting (4) with (6) and solving it for , we obtain the aggregate quantity based on the parameters and exogenous variables as follows:

| (7) |

3 Simulation results

3.1 Simulation and estimation procedure

We set true parameters and distributions as shown in Table 1. We vary the true value of from 0.05 (20-firm symmetric Cournot) to 1 (perfect collusion) and the strength of demand rotation instrument, , from 0.1 (weak) to 20.0 (extremely strong) which is unrealistically larger than the price coefficient level, . For simulation, we generate 100 datasets. We separately estimate the demand and supply equations via two-stage least squares (2SLS) estimation. The instrumental variables for demand estimation are and for supply estimation are for a benchmark model. To achieve theoretical efficiency bounds, we add optimal instruments of Chamberlain (1987), used in demand estimation (Reynaert and Verboven 2014). Optimal instruments lead to asymptotically efficient estimators, as their asymptotic variance cannot be reduced via additional orthogonality conditions. See Appendix A.2 for construction details. The null hypothesis is that markets are under perfect competition, that is, . We compute the rejection frequency as the power by using t-statistics at a significance level of 0.05 over 100 datasets.

| Demand shifter | ||

|---|---|---|

| Demand rotation instrument | ||

| Cost shifter | ||

| Error | ||

Note: . Normal distribution. Uniform distribution.

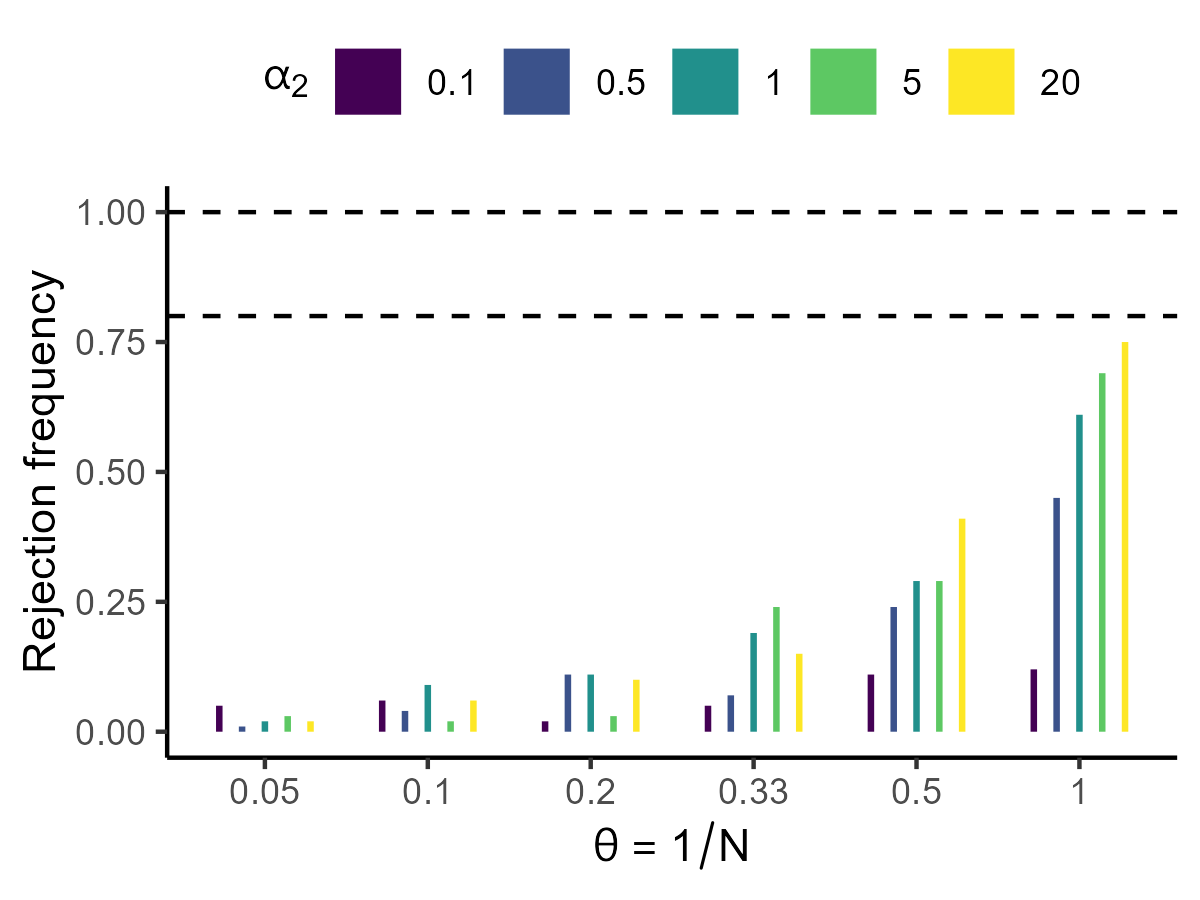

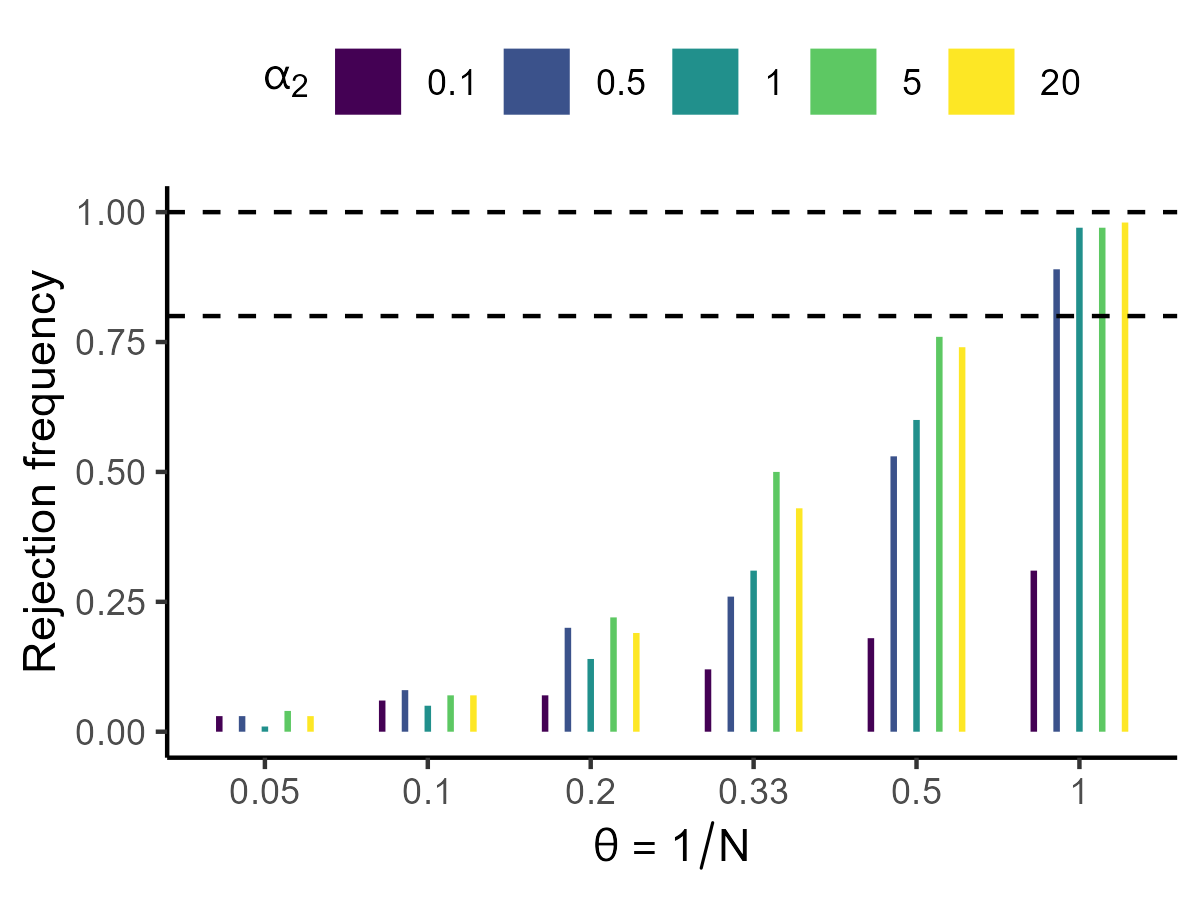

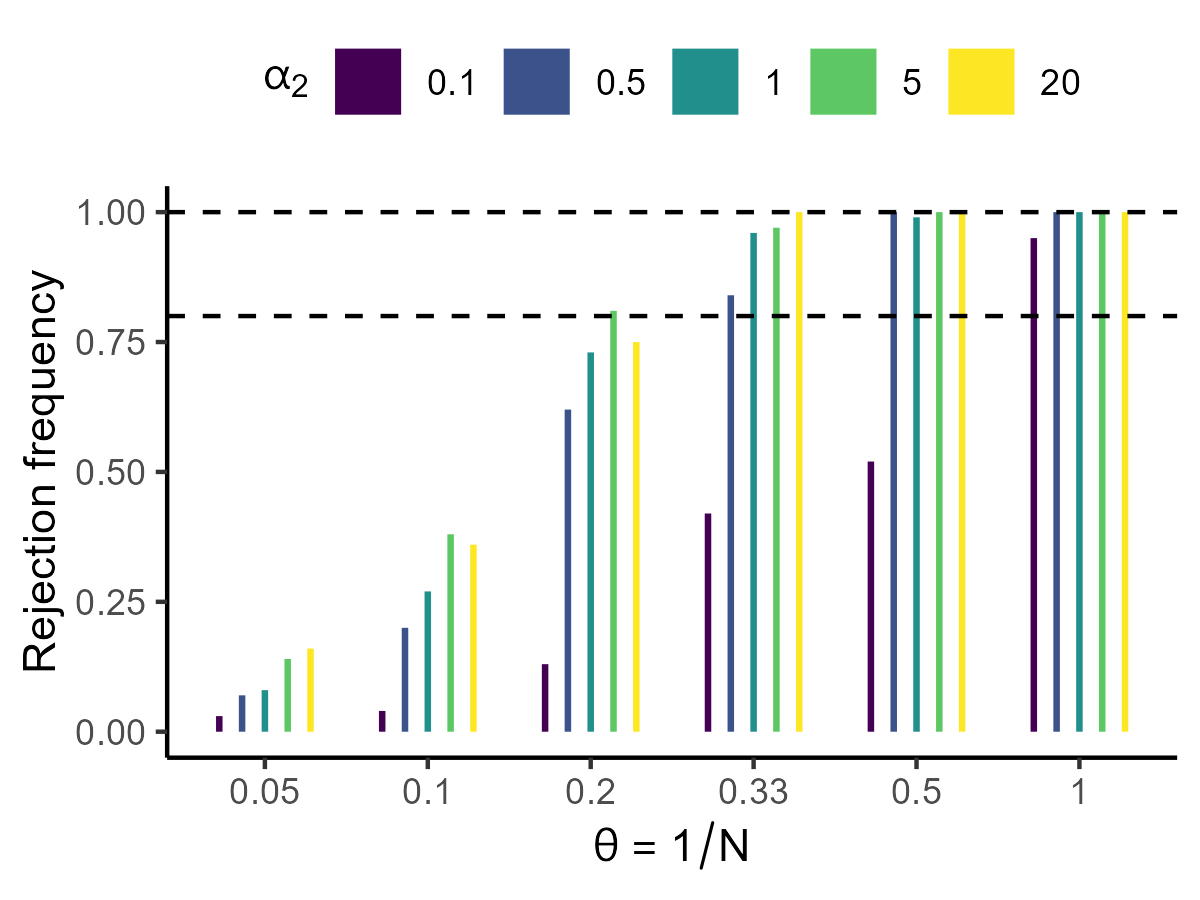

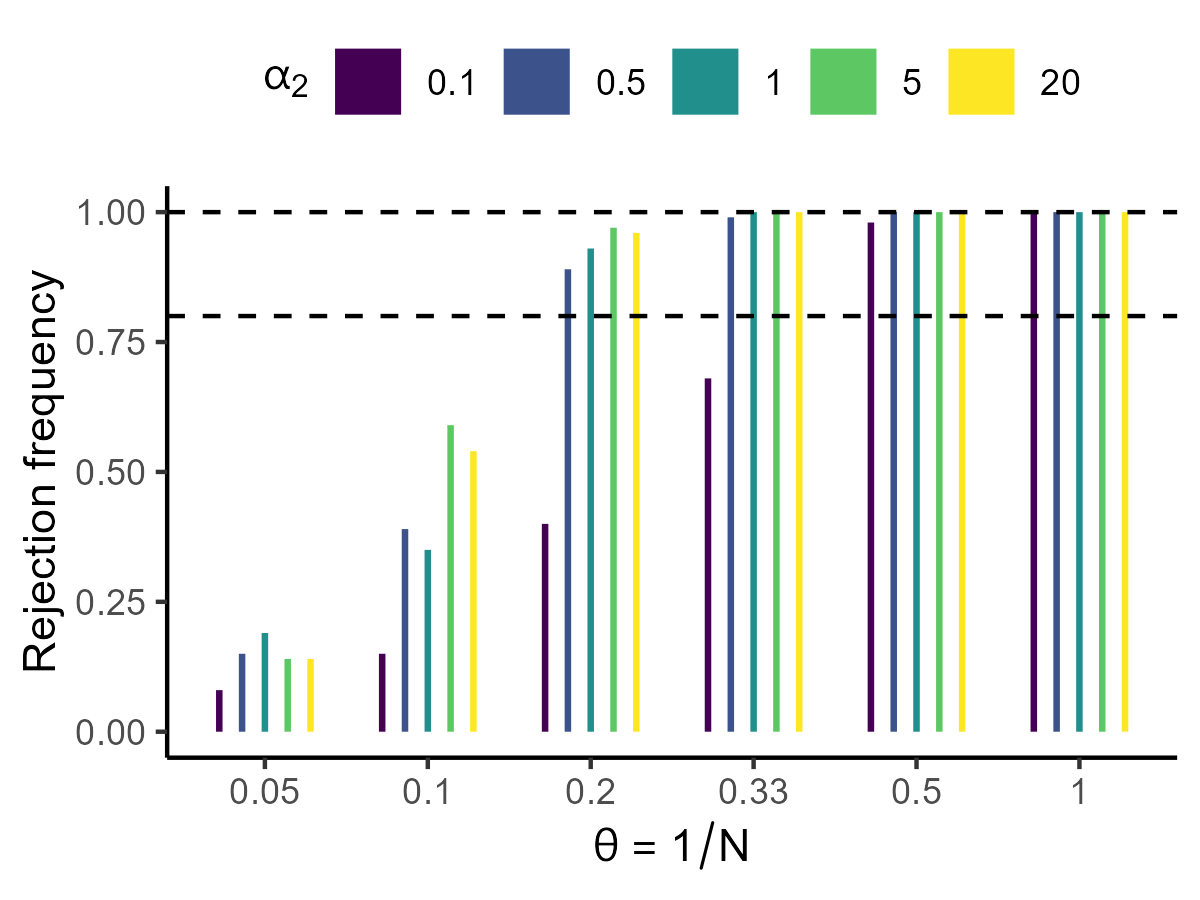

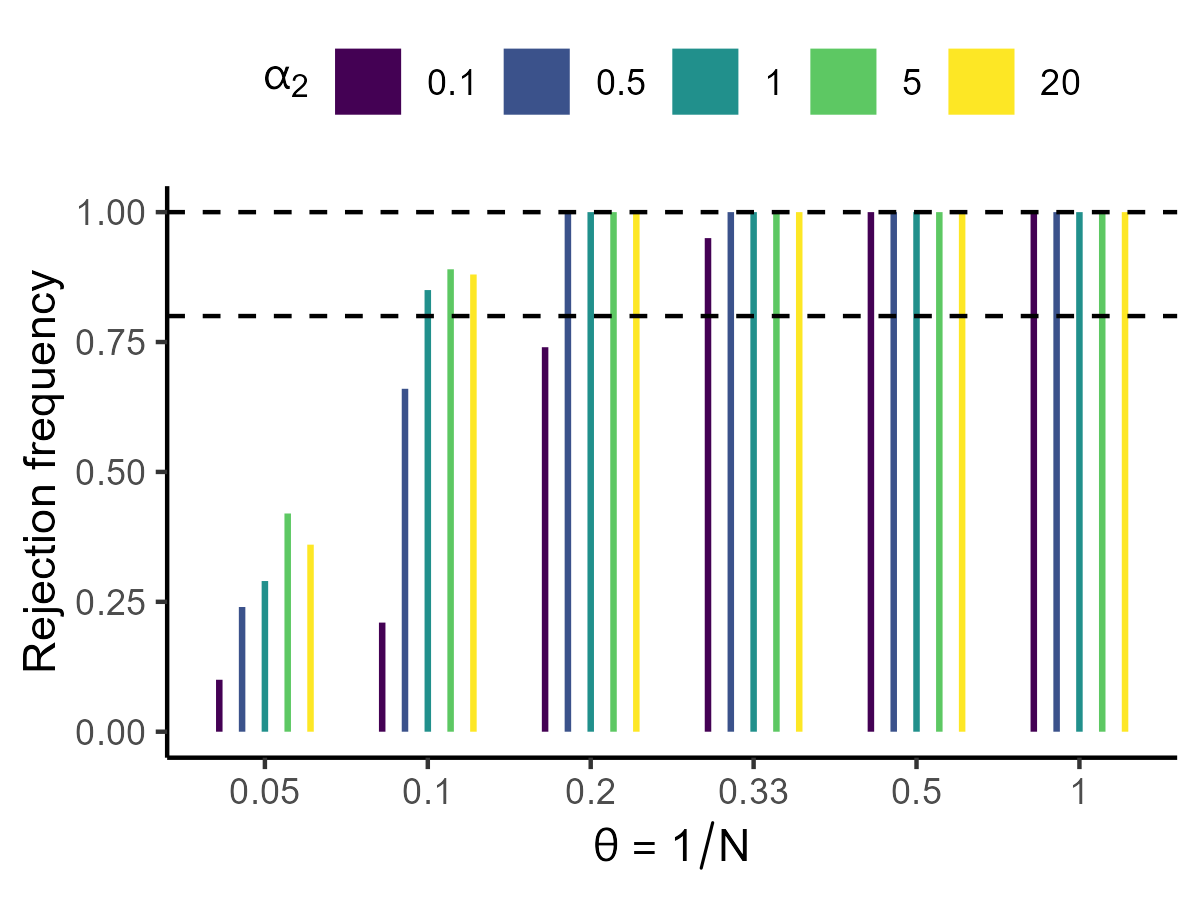

Figure 1 displays the finite sample performance results for the conduct parameter .222Simulation details and additional results for all other parameters are available in the online appendix. Rejection frequency increases under the following conditions: a large sample size (number of markets), a larger (fewer firms), and a larger (stronger demand rotation instrument). Panel (f) indicates that with 20 symmetric firms () and a sufficiently large number of markets, we achieve an approximately 70% power to reject the null hypothesis of markets operating under perfect competition. However, we cannot reject the null hypothesis with an acceptable sample size and power when markets follow 20-firm symmetric Cournot competition.

A remarkable finding is that even with a moderate number of markets (e.g., 1000 in Panel (c)) and five firms, the rejection frequency cannot achieve 80% (i.e., , where is the probability of making a Type II error), regardless of instrument strength. This implies that Genesove and Mullin (1998), using 97 markets, Shaffer (1993), using 25 markets, and Steen and Salvanes (1999), using 48 markets, fail in rejecting perfect competition due to the small sample problem.

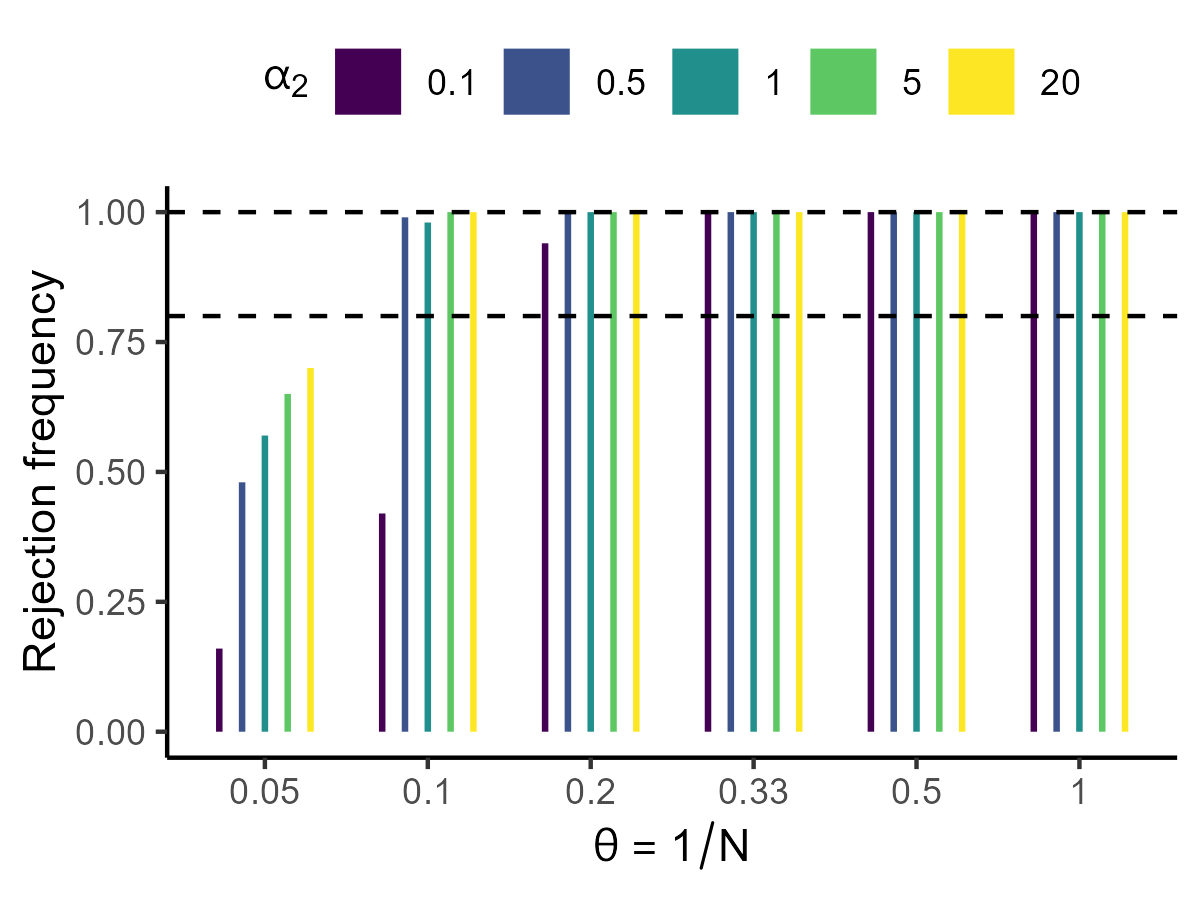

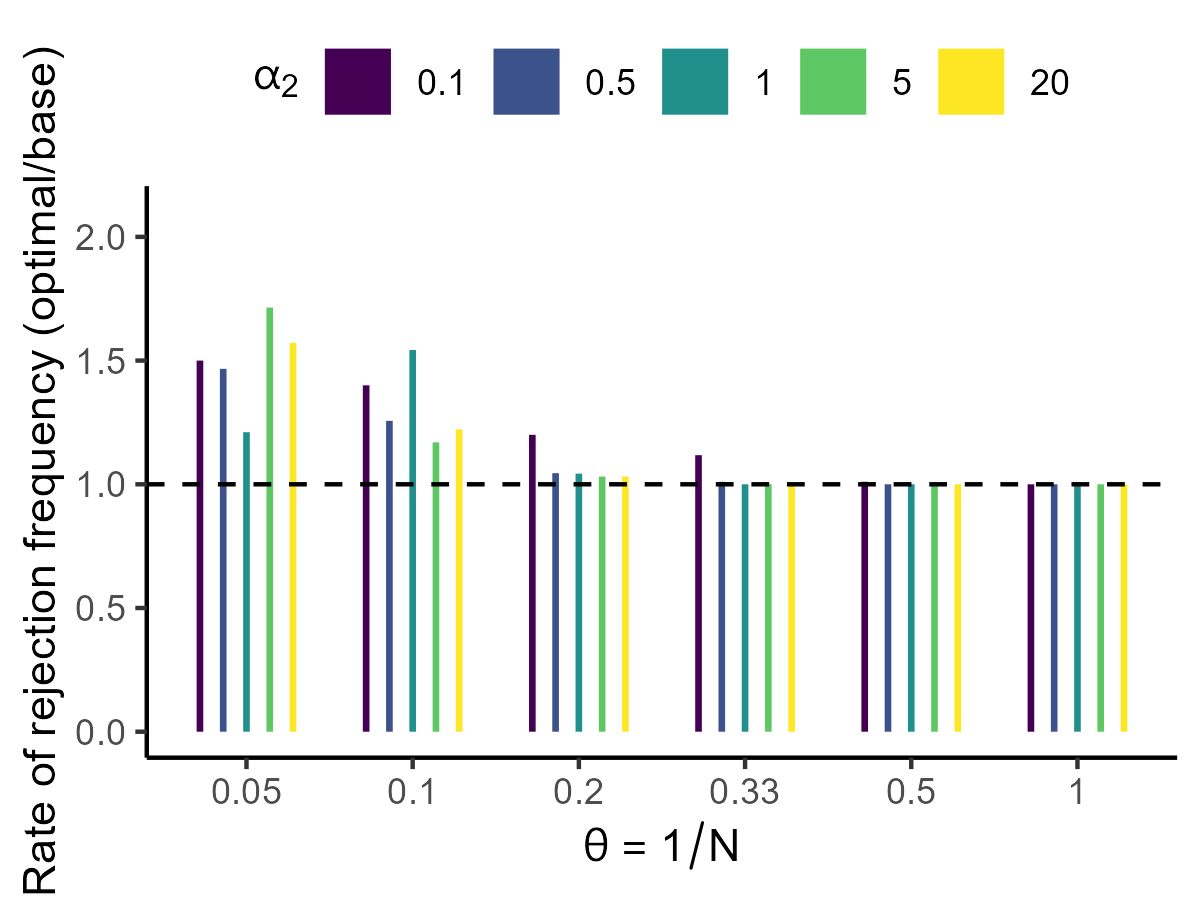

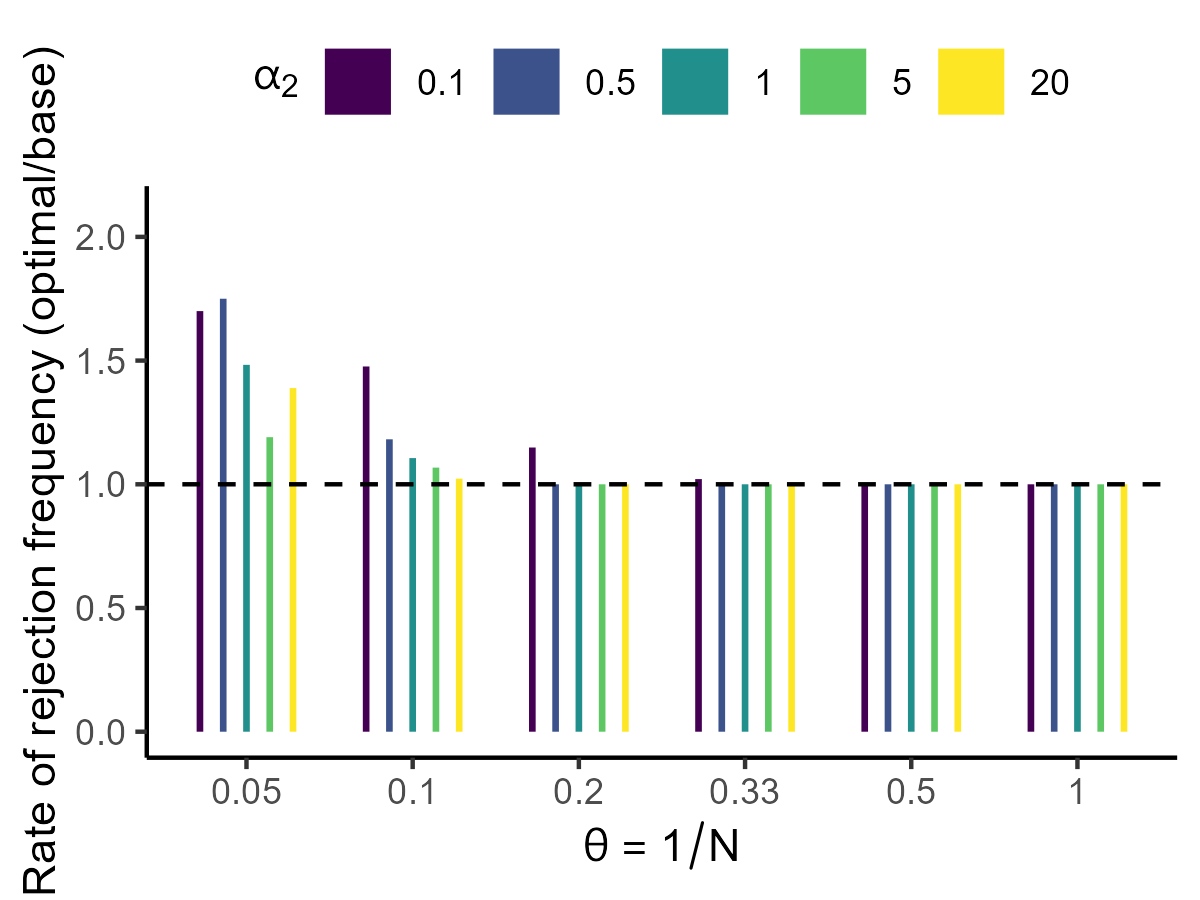

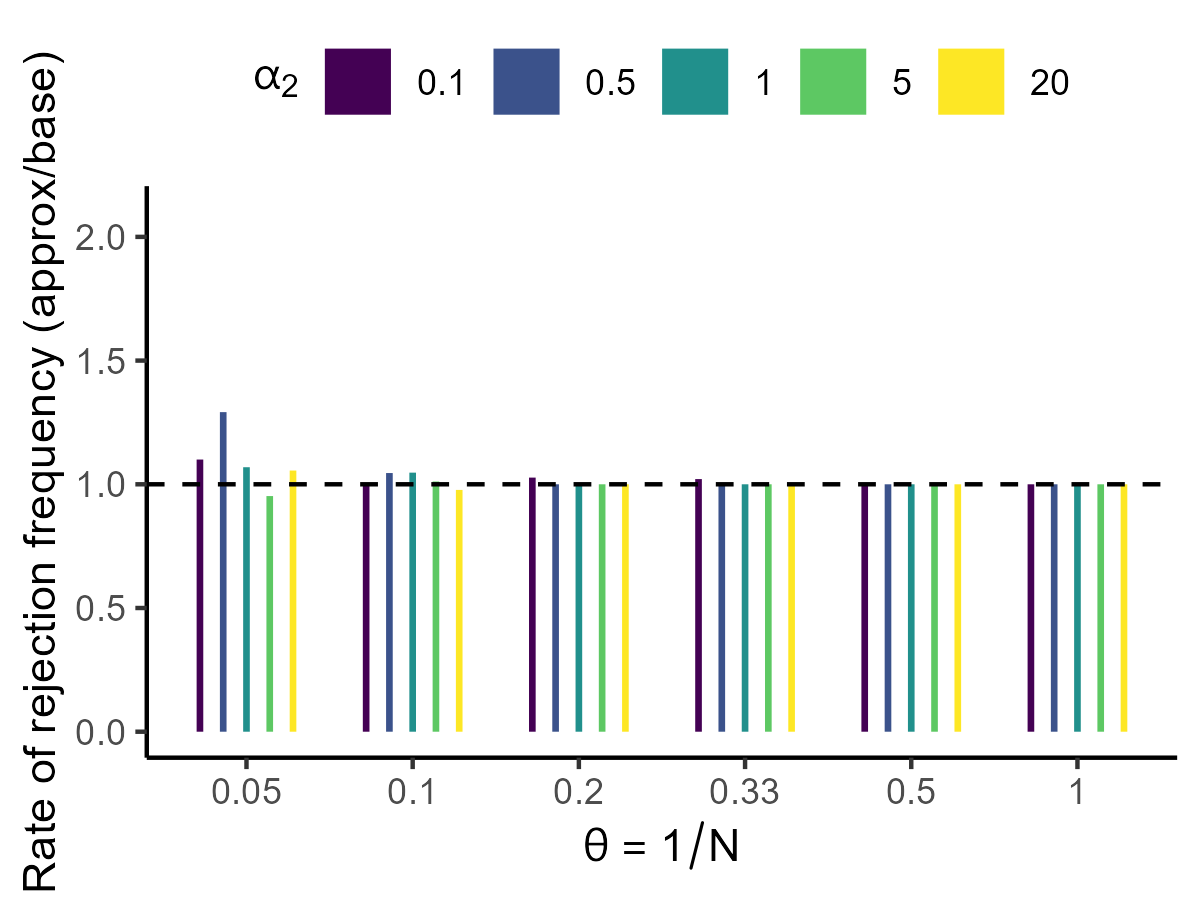

Figure 2 shows the efficiency gain of optimal instruments relative to the aforementioned benchmark model. We find that if the number of markets exceeds 1,000, optimal instruments increase the rejection probability. However, the gain does not change our benchmark results.

Why is it statistically challenging to differentiate between perfect and Cournot competition? In differential product markets, as demonstrated by Berry and Haile (2014), the variation in instrumental variables can aid in discerning firm behavior. Various factors such as changes in the number of products, prices in other markets, and alterations in product characteristics, can be utilized without requiring a specific functional form. In contrast, homogeneous product markets exhibit limited variation only on demand rotation instruments. Therefore, even when the number of firms is substantial, firm conduct tests may lack the necessary power to differentiate between perfect and Cournot competition.

Note: Dotted lines are 80% and 100% rejection frequencies out of 100 simulation data.

4 Conclusion

We perform a statistical power analysis for conduct parameter estimation. Power rises with an increase in the number of markets, a larger conduct parameter, and a stronger demand rotation instrument. Nevertheless, rejecting the null hypothesis of markets operating under perfect competition remains challenging, even with a moderate number of markets (e.g., 1000) and five firms, regardless of instrument strength and the use of optimal instruments. This reaffirms that the difficulty in testing perfect competition, as observed by Genesove and Mullin (1998), Steen and Salvanes (1999), and Shaffer (1993), is primarily attributed to the limited number of markets, rather than methodological shortcomings.

Acknowledgments

We thank Jeremy Fox, Isabelle Perrigne, and Yuya Shimizu for their valuable advice. This research did not receive any specific grant from funding agencies in the public, commercial, or not-for-profit sectors.

References

- (1)

- Berry and Haile (2014) Berry, Steven T and Philip A Haile, “Identification in differentiated products markets using market level data,” Econometrica, 2014, 82 (5), 1749–1797.

- Borenstein et al. (2002) Borenstein, Severin, James B Bushnell, and Frank A Wolak, “Measuring market inefficiencies in California’s restructured wholesale electricity market,” American Economic Review, 2002, 92 (5), 1376–1405.

- Bresnahan (1982) Bresnahan, Timothy F, “The oligopoly solution concept is identified,” Economics Letters, 1982, 10 (1-2), 87–92.

- Chamberlain (1987) Chamberlain, Gary, “Asymptotic efficiency in estimation with conditional moment restrictions,” Journal of econometrics, 1987, 34 (3), 305–334.

- Clay and Troesken (2003) Clay, Karen and Werner Troesken, “Further tests of static oligopoly models: Whiskey, 1882–1898,” The Journal of Industrial Economics, 2003, 51 (2), 151–166.

- Duarte et al. (2023) Duarte, Marco, Lorenzo Magnolfi, Mikkel Sølvsten, and Christopher Sullivan, “Testing firm conduct,” arXiv preprint arXiv:2301.06720, 2023.

- Genesove and Mullin (1998) Genesove, David and Wallace P Mullin, “Testing static oligopoly models: conduct and cost in the sugar industry, 1890-1914,” The RAND Journal of Economics, 1998, pp. 355–377.

- Hansen (2022) Hansen, Bruce, Econometrics, Princeton University Press, 2022.

- Kim and Knittel (2006) Kim, Dae-Wook and Christopher R Knittel, “Biases in static oligopoly models? Evidence from the California electricity market,” The Journal of Industrial Economics, 2006, 54 (4), 451–470.

- Magnolfi and Sullivan (2022) Magnolfi, Lorenzo and Christopher Sullivan, “A comparison of testing and estimation of firm conduct,” Economics Letters, 2022, 212, 110316.

- Matsumura and Otani (2023a) Matsumura, Yuri and Suguru Otani, “Conduct Parameter Estimation in Homogeneous Goods Markets with Equilibrium Existence and Uniqueness Conditions: The Case of Log-linear Specification,” Working Paper, 2023.

- Matsumura and Otani (2023b) and , “Resolving the conflict on conduct parameter estimation in homogeneous goods markets between Bresnahan (1982) and Perloff and Shen (2012),” Economics Letters, 2023, p. 111193.

- Nevo (1998) Nevo, Aviv, “Identification of the Oligopoly Solution Concept in a Differentiated-Products Industry,” Economics Letters, June 1998, 59 (3), 391–395.

- Orea and Steinbuks (2018) Orea, Luis and Jevgenijs Steinbuks, “Estimating market power in homogenous product markets using a composed error model: application to the California electricity market,” Economic Inquiry, 2018, 56 (2), 1296–1321.

- Perloff and Shen (2012) Perloff, Jeffrey M and Edward Z Shen, “Collinearity in linear structural models of market power,” Review of Industrial Organization, 2012, 40 (2), 131–138.

- Puller (2007) Puller, Steven L, “Pricing and firm conduct in California’s deregulated electricity market,” The Review of Economics and Statistics, 2007, 89 (1), 75–87.

- Reynaert and Verboven (2014) Reynaert, Mathias and Frank Verboven, “Improving the performance of random coefficients demand models: The role of optimal instruments,” Journal of Econometrics, 2014, 179 (1), 83–98.

- Shaffer (1993) Shaffer, Sherrill, “A test of competition in Canadian banking,” Journal of Money, Credit and Banking, 1993, 25 (1), 49–61.

- Shaffer and Spierdijk (2017) and Laura Spierdijk, “Market Power: Competition among Measures,” Handbook of Competition in Banking and Finance, 2017, pp. 11–26.

- Steen and Salvanes (1999) Steen, Frode and Kjell G Salvanes, “Testing for market power using a dynamic oligopoly model,” International Journal of Industrial Organization, 1999, 17 (2), 147–177.

- Wolak (2003) Wolak, Frank A, “Measuring unilateral market power in wholesale electricity markets: The California market, 1998–2000,” American Economic Review, 2003, 93 (2), 425–430.

- Wolfram (1999) Wolfram, Catherine D, “Measuring duopoly power in the British electricity spot market,” American Economic Review, 1999, 89 (4), 805–826.

Appendix A Online appendix

A.1 Details for our simulation settings

To generate the simulation data, for each model, we first generate the exogenous variables , and and the error terms and based on the data generation process in Table 1. We compute the equilibrium quantity for the linear model by (7). We then compute the equilibrium price by substituting and other variables into the demand function (4).

We estimate the equations using the ivreg package in R. An important feature of the model is that we have an interaction term of the endogenous variable and the instrumental variable . The ivreg package automatically detects that the endogenous variables are and the interaction term , running the first stage regression for each endogenous variable with the same instruments. To confirm this, we manually write R code to implement the 2SLS model. When the first stage includes only the regression of , estimation results from our code differ from the results from ivreg. However, when we modify the code to regress on the instrument variables and estimate the second stage by using the predicted values of and , the result from our code and the result from ivreg coincide.

A.2 Optimal instruments

We begin by introducing optimal instruments for a simultaneous equation model. Subsequently, we move to supply-side estimation, as the simultaneous equation model does not yield any additional efficiency advantage when the error terms in the demand and supply equations are uncorrelated, as in our scenario.

We define demand and supply residuals as follows.

where is the parameter vector. Let and . We make the assumption that is a constant matrix, defining the covariance structure of the demand and supply residuals. The optimal instrument matrix of Chamberlain (1987) is the matrix where the matrix is the conditional expectation of the derivative of the conditional moment restrictions with respect to parameters .

The conditional expectation is difficult to compute, so most applications have considered approximations. As in Reynaert and Verboven (2014), we consider two types of approximation. The first approximation for takes a second-order polynomial of for the demand side instruments (first row of ), i.e. cost shifters and , and their squares and interactions, and and for the supply side instruments (second row of ). The second approximation for implements the conditional expectation written as

where . Following the literature, we replace with the fitted values of regressions of on the second order polynomials of and the interactions.

When only the supply side is estimated given fixed demand parameters as in our main results, the earlier optimal instrument matrix is modified into the matrix where

This suggests augmenting the benchmark instruments with and . To prevent redundancy, we add to the benchmark model. We verify that including in addition to does not enhance statistical power.

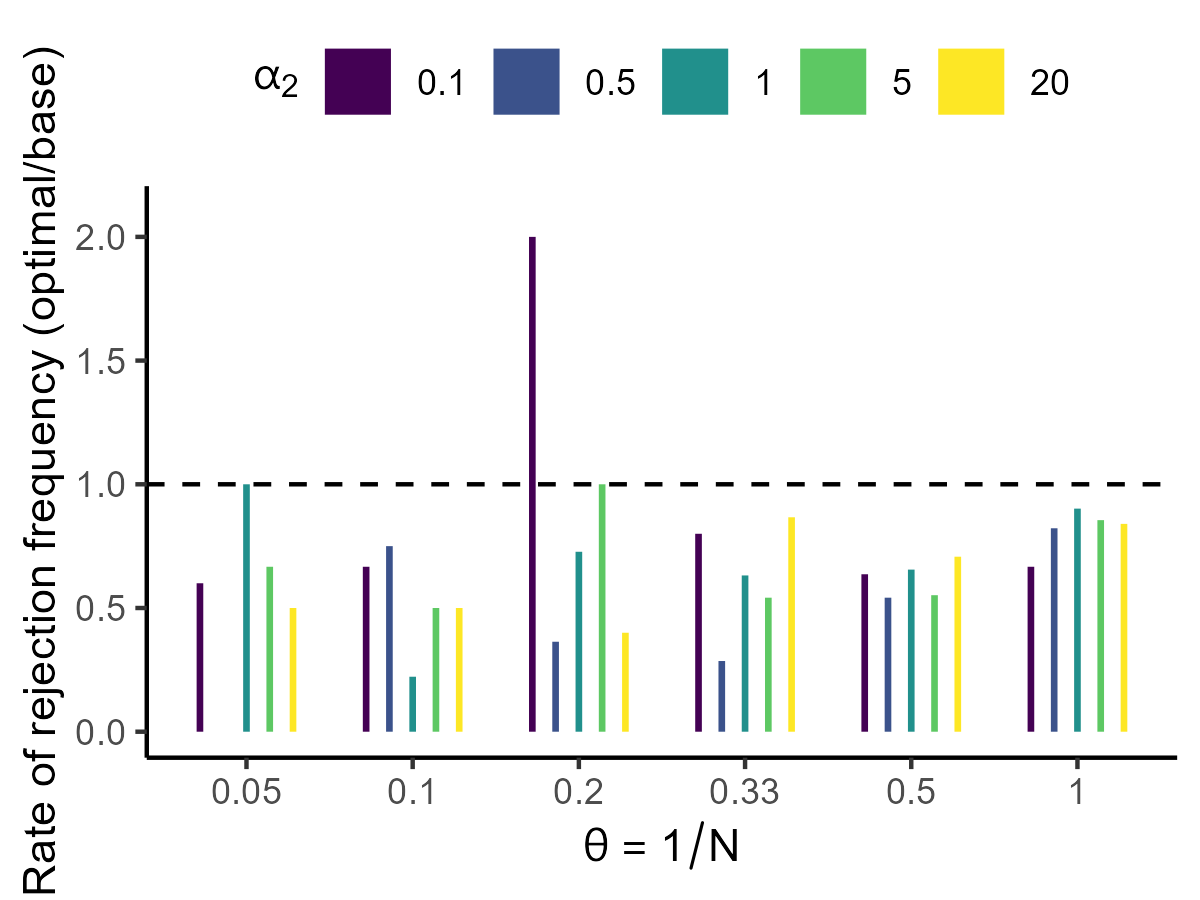

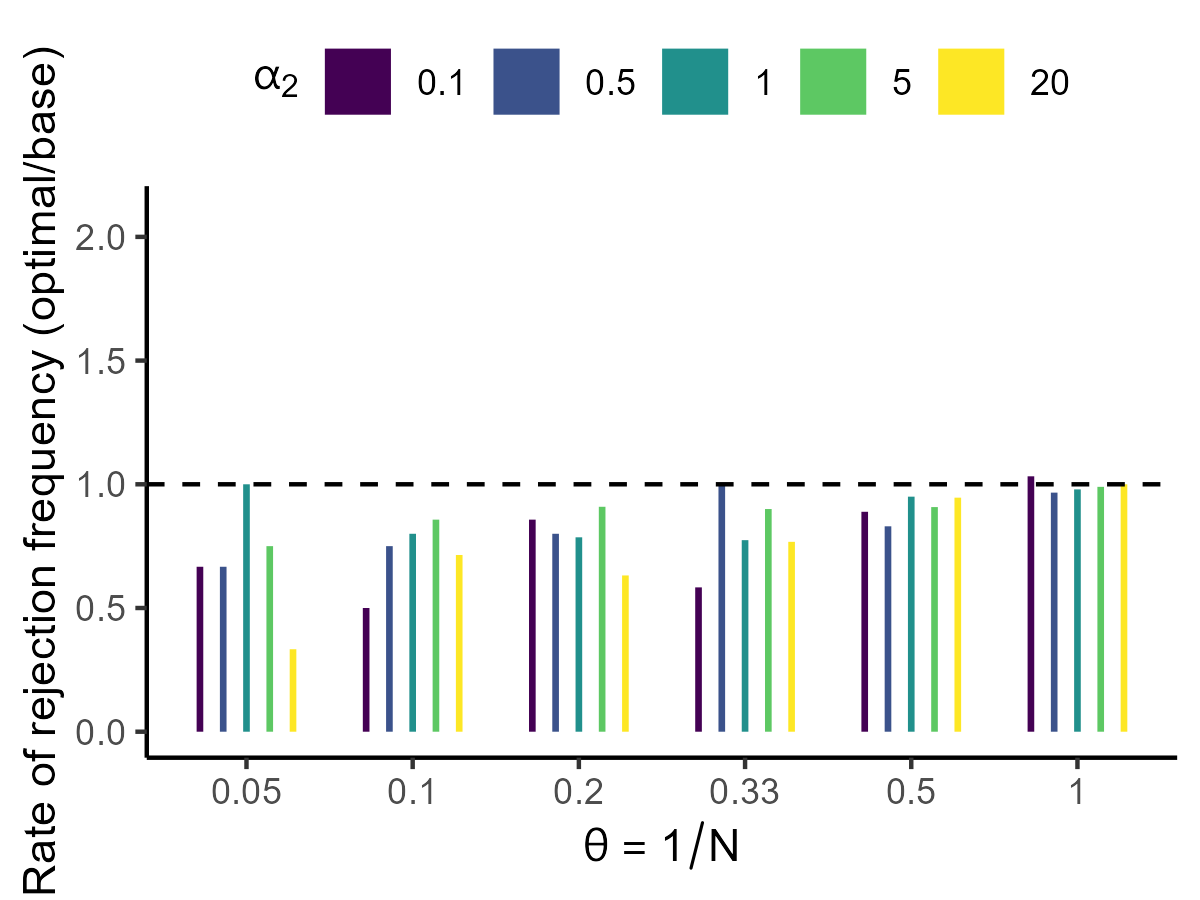

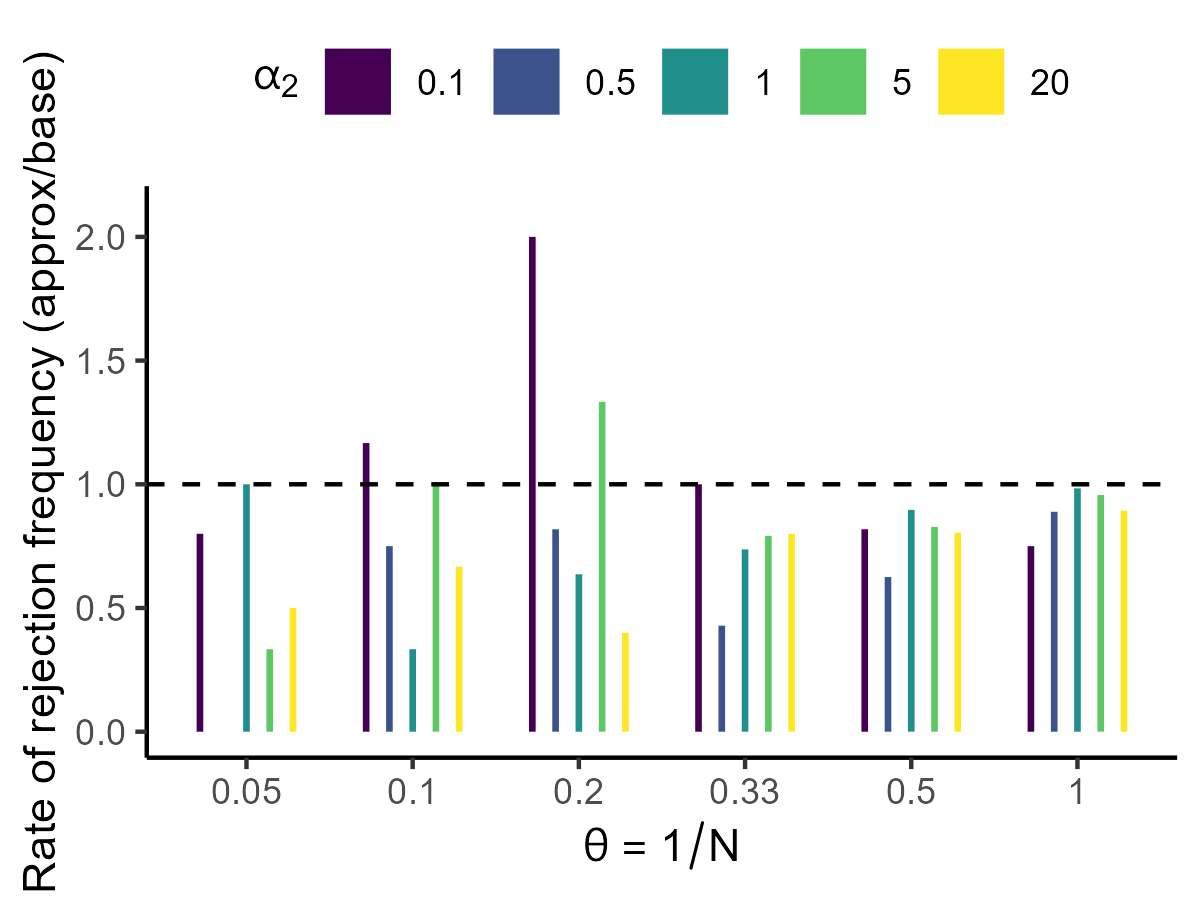

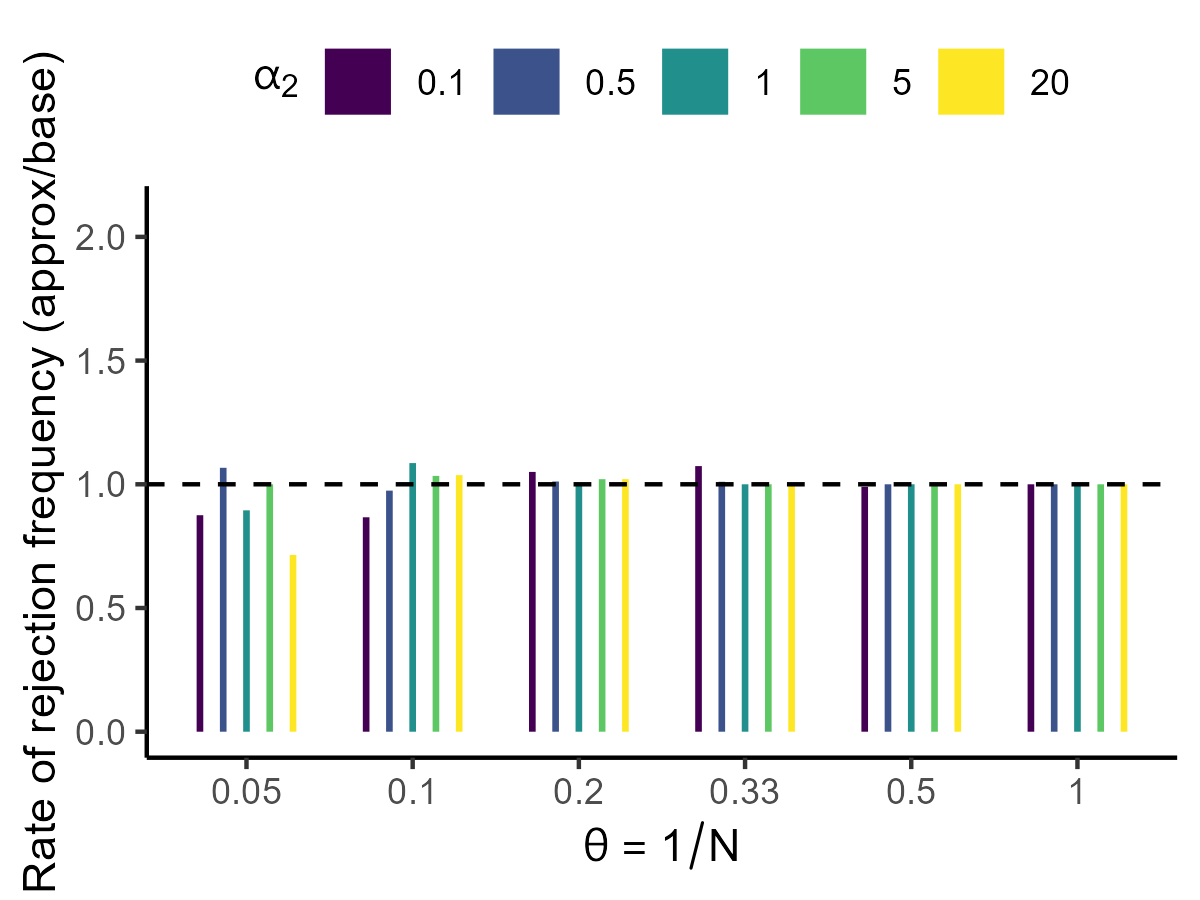

Figure 3 reports the relative efficiency gain of the first approximation approach. The efficiency gain is ignorable. Figure 2 in the main text reports the relative efficiency gain of the optimal instruments in the second approach. The efficiency gain is significant when the number of markets is more than 1,000. However, this does not change our benchmark results.

A.3 Additional results

Estimation results of all parameters except conduct parameter are shown on the author’s github. Totally, we confirm that estimation is accurate with small bias and root-mean-squared error when increasing sample size, as in Matsumura and Otani (2023b). Interested readers can modify the current data-generating process.

A.4 Statistical power on

Following chapters 5, 7, and 9 of Hansen (2022), we consider null hypothesis , i.e., markets are under perfect competition, and alternative hypothesis . Let be the t-statistics of , be the point estimator. To simplify the argument, we assume that the variance of the estimator to , is known. Then the standard error of is writen as . Then, at a significance level of 0.05, the power is

for large where is the cumulative distribution function of the normal distribution. This typical formula illustrates that the term determines the power under . For example, if , the number of markets, , must increase by 100 times compared to the case of for getting the same power. This is consistent with our findings in Figure 1. Note that this applies to all regression coefficients.