Hidden Markov Models for Stock Market Prediction

Abstract

The stock market presents a challenging environment for accurately predicting future stock prices due to its intricate and ever-changing nature. However, the utilization of advanced methodologies can significantly enhance the precision of stock price predictions. One such method is Hidden Markov Models (HMMs). HMMs are statistical models that can be used to model the behavior of a partially observable system, making them suitable for modeling stock prices based on historical data. Accurate stock price predictions can help traders make better investment decisions, leading to increased profits.

In this article, we trained and tested a Hidden Markov Model for the purpose of predicting a stock closing price based on its opening price and the preceding day’s prices. The model’s performance has been evaluated using two indicators: Mean Average Prediction Error (MAPE), which specifies the average accuracy of our model, and Directional Prediction Accuracy (DPA), a newly introduced indicator that accounts for the number of fractional change predictions that are correct in sign.

Index Terms:

Hidden Markov Models, Stock market, forecasting.I Introduction

Prediction of the stock market, with its inherent volatility and potential for substantial financial gains, has long captivated the attention of institutional investors, hedge funds, and proprietary trading firms. These sophisticated market participants are driven by the desire to make accurate predictions about future price movements and trends in order to gain a competitive edge and maximize their investment returns.

Institutional investors, such as pension funds and insurance companies, manage large pools of capital on behalf of their clients or beneficiaries. The primary objective of these investors is to generate consistent returns over the long term to fulfill their financial obligations. Accurate predictions in the stock market allow them to identify opportunities and mitigate risks, enhancing portfolio performance and meeting their fiduciary responsibilities [1].

Hedge funds, on the other hand, are private investment partnerships that pool capital from accredited investors. Hedge fund managers seek to generate significant absolute returns, often irrespective of market conditions, by employing diverse investment strategies. Accurate predictions empower hedge funds to identify mispriced securities, exploit market inefficiencies, and construct profitable trading strategies, ultimately attracting investors and earning substantial profits [2].

These sophisticated market participants employ a wide range of quantitative and qualitative methods to make predictions in the stock market.

Algorithmic strategies rely on computer algorithms that systematically analyze vast amounts of market data, identify patterns, and generate trade signals. These algorithms are programmed to execute trades automatically, often leveraging complex mathematical models and statistical techniques. It is estimated that 50 percent of stock trading volume in the U.S. is currently being driven by algorithmic trading [3].

While algorithmic trading offers significant advantages for institutional investors, retail investors should exercise caution when relying solely on algorithmic strategies. The success of algorithmic trading is often attributed to extensive research, robust infrastructure, and substantial resources that may not be readily available to individual retail investors. Moreover, market conditions can change rapidly, rendering algorithms ineffective or even exacerbating losses. Retail investors, lacking the same level of resources and risk management capabilities, face greater risks when solely depending on algorithmic trading.

In recent years, many strategies have been developed for algorithmic trading. Since Hidden Markov Models (HMMs) have emerged as powerful tools for the prediction of time series data, we expect them to give promising results in the context of the stock market prediction.

This paper is organized as follows: in Section II, we briefly review various stock market prediction approaches; Section III outlines our theoretical approach with relevant definitions and mathematical equations; in Section IV describes our technical implementation and solutions to encountered challenges; in Section V we present our results, compare them with other models, and introduce a novel evaluation metric; finally, in Section VI we summarize key findings and suggest directions for further developments.

II Previous Works

Various approaches have been explored in the quest for reliable prediction models as accurate forecasting of stock prices and identification of trends are crucial for investors and financial institutions seeking informed decisions.

Before the emergence of artificial intelligence, probabilistic techniques formed the foundation of stock market forecasting. These theories encompassed random walk models [4], [5], correlation-based methods [6], [7], scaling properties [8], [9], stock market volatility and investor sentiment [10], [11], probability distributions of stock price returns [12], [13], and other relevant approaches.

With the advancement of machine learning and the increasing computational power of computers, several techniques utilizing big data and artificial intelligence algorithms gained popularity. Support Vector Machines (SVM) were quickly recognized as promising for time series prediction [14], and were first employed for financial forecasting in 2001 [15]. Hybrid models combining ARIMA (Autoregressive Integrated Moving Average) and SVM were introduced by Pai et al. in 2005 [16]. Neural networks, including specific types coupled with Genetic Algorithms, have been utilized to detect temporal patterns [17], [18]. Bollen et al. scraped data from Twitter to forecast the stock market based on user mood in 2011 [19].

In 2005, Hassan et al. employed Hidden Markov Models for time series prediction [20], building upon the concepts introduced in Rabiner’s influential tutorial published in 1989 [21]. Their work demonstrated the effectiveness of HMMs, leading to their widespread adoption in subsequent studies [22], [23], [24].

In this project, we aimed to replicate and extend the findings reported by Gupta et al. in their 2012 study [25]. We used Mathworks Statistics and Machine Learning Toolbox™. Moreover, we decided to make our project open-sourced [26], hoping to foster collaboration and encourage the research community to build upon our work, replicate our experiments, and explore further enhancements to advance the field.

III Approach

III-A Markov Chains

A Markov chain is a stochastic model that represents a sequence of events or states. In our analysis, we will specifically focus on first-order Markov chains, which adhere to the Markov property. Let be the set of all possible states, and be the states time series. The Markov property states that for any and states :

| (1) | |||

In other words, the probability of transitioning to a certain state at time step only depends on the current state at time step and not on any previous states. This property allows us to compute the probability distribution of the Markov chain at any future time step based exclusively on its current state.

Formally, a first order Markov chain is defined by the set of states and a transition probability matrix , where represents the probability of transitioning from state to state in one step.

The elements of the transition matrix must satisfy the standard stochastic constraints:

-

•

.

-

•

.

Let be the vector containing the probabilities of being in each state at time , the system evolves according to:

| (2) |

We refer to the initial distribution of probabilities as .

III-B Hidden Markov Models

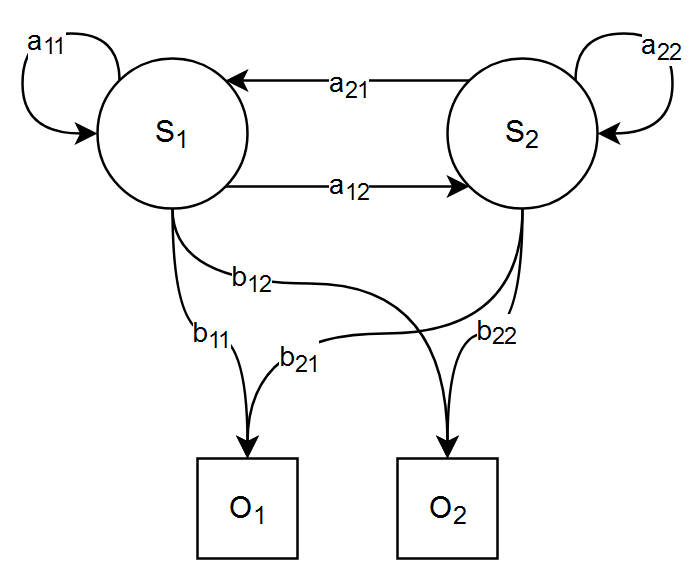

The model presented above implicitly assumes that each state corresponds to an observable (physical) event. Markov chains have proven to be valuable tools for modeling sequential data in various domains. However, many real-world scenarios involve underlying states that influence observations but are not directly observable. This limitation led to the development of Hidden Markov Models, which extend the basic Markov chain model by introducing hidden or unobservable states that affect the observed data.

The hidden state process of a HMM is a Markov chain, where each state generates an observation having a certain probability distribution that only depends on the state itself.

Let be the observed sequence, where is the set of possible observations. The hidden states are assumed to evolve according to Equation 2.

The probability of symbol being emitted by state is described by the emission probability function .

Both in the current and following sections, we refer to the emission probability matrix .

III-C Applications of HMMs: Common Problems and Solutions

The most common problems analyzed using HMMs include the evaluation problem, decoding problem, and parameter estimation problem. These problems and their corresponding solutions have been extensively studied and documented in the literature [21]. In the following paragraphs, we provide an overview of these problems and their solutions.

III-C1 Evaluation Problem

The evaluation problem in HMMs involves computing the probability of a known observation sequence, given the model. Specifically, given an HMM with the parameters , , and , and an observed sequence , we want to compute .

The procedure used to solve this problem involves computing the forward variable, denoted as , which represents the probability of being in state at time and observing the sequence up to time . It is computed recursively for each time step and state .

At the initialization step, the forward variable for the initial time step is calculated as: , where is the initial probability of being in state and is the emission probability for the first observation .

For each subsequent time step , the forward variable is computed as the sum of the probabilities of all possible paths that could have generated the observations up to time and reached state . This is expressed by the following formula:

| (3) |

By recursively calculating the forward variables for each time step, the algorithm evaluates the probability of observing the entire sequence, given the HMM parameters.

Finally, to obtain the overall probability of the observed sequence, the forward procedure computes the sum of the forward variables at the final time step :

| (4) |

III-C2 Decoding Problem

The decoding problem involves determining the most likely sequence of hidden states given an observation sequence and the model. Given an HMM with the parameters , , and , and an observed sequence , we want to find the hidden state sequence that maximizes .

The solution to the decoding problem is commonly addressed using the Viterbi algorithm.

The algorithm works by iteratively calculating the most likely path to each state at each time step, considering both the current observation and the previous states probabilities. At each time step, it computes the probability of being in each state and tracks the most probable path leading to that state.

III-C3 Parameter Estimation Problem

The parameter estimation problem in HMMs involves adjusting the model parameters to maximize the probability of an observed sequence. Given an observation sequence , we want to estimate the optimal values for the parameters , , and that maximize .

The solution to the this problem is typically addressed using the forward-backward algorithm, also known as the Baum-Welch algorithm.

The Baum-Welch algorithm is a specific implementation of the Expectation–Maximization (EM) algorithm, tailored for HMMs. It iteratively performs three main steps: forward, backward, and update step. In the forward step, the algorithm computes the probability of being in a specific state at each time step, given the observed sequence up to that point. This is the evaluation problem explained before.

In the backward step, the algorithm computes the probability of observing the remaining part of the sequence from a given state at each time step. It complements the forward procedure by computing the backward variable, denoted as , which represents the probability of being in state at time and observing the remaining sequence from time to the end. The backward variable is computed recursively for each time step and state . At the initialization step, the backward variable for the final time step is set as: .

For each time step , the backward variable is computed as the sum of the probabilities of all possible paths that can be generated from state at time to the end of the sequence. This is expressed by the following formula:

| (5) |

After computing the forward and backward variables, they are used to refine the parameters of the HMM based on the observed sequence. In fact, let be the probability of being in state at time and state at time , given the model and the observation sequence. It can be computed as:

| (6) | ||||

Let’s also define as the probability of being in state at time , given the observation sequence and the model:

| (7) |

We can relate those quantities:

| (8) |

Moreover, represents the expected number of transitions from state , and represents the expected number of transitions from state to state .

The update step involves estimating the new values for the initial state probabilities, transition probabilities, and emission probabilities. For the initial state probabilities, the updated values are calculated as the normalized forward-backward probabilities at the initial time step:

| (9) |

The transition probabilities are updated based on the expected number of transitions between states, normalized over the expected number of transitions from each state

| (10) |

The estimate for the emission probability — the probability of observing symbol from state — is calculated by evaluating the expected number of times in which is emitted from state . This value is then normalized by the expected number of transitions from state :

| (11) |

where is the Kronecker delta function that evaluates to 1 when is equal to the observed symbol , and 0 otherwise.

This process iteratively refines the model parameters until convergence, where they stabilize, meaning that the likelihood of the sequence is maximized.

Choosing the initial conditions wisely is crucial as it can significantly impact the estimation of the HMM parameters. By selecting appropriate initial conditions, the Baum-Welch algorithm is more likely to converge to some parameters that provide accurate modeling of the underlying dynamics.

III-D Gaussian Mixture Models

Gaussian Mixture Models (GMMs) are powerful probabilistic models used to represent complex probability distributions. A GMM is a weighted sum of multiple Gaussian distributions, where each component represents a subpopulation within the data.

When a single observation is composed by multiple data (multivariate data), GMMs are employed as multivariate mixture models. Each Gaussian component in a GMM represents a multivariate distribution with its own mean vector and covariance matrix. The probability density function of a multivariate GMM is given by:

| (12) |

where is the number of Gaussian components, represents the weight associated with the -th component, and denotes the multivariate Gaussian distribution with mean vector and covariance matrix .

The weights satisfy the constraint , ensuring that the probabilities sum up to one. These weights control the contribution of each Gaussian component to the overall distribution.

GMMs are particularly useful when modeling complex multivariate data that exhibit multiple modes or clusters because they can capture the inherent structure and variability present in the data.

In the context of Hidden Markov Models, GMMs are employed to initialize the emission probabilities of the hidden states. The GMM is fitted on the training dataset: the training algorithm estimates the parameters of each Gaussian component, i.e. the mean vectors and covariance matrices. These parameters are used to initialize the emission probabilities of the corresponding hidden states.

IV Technical implementation

In our study, three specific functions provided by the Statistics and Machine Learning Toolbox™ in MATLAB were utilised for the training and testing of the HMM: hmmtrain, hmmdecode and fitgmdist.

The model was trained and tested on the historical daily prices of Apple, IBM and Dell stocks that are publicly available on the web. Each observation in our dataset comprises three distinct values representing the daily fractional change, fractional high, and fractional low prices.

| (13) |

The array is a three-dimensional array consisting of real values. Since the probability of guessing any real value is mathematically zero, it was necessary to discretize the observations. The number of points used for the discretization is specified in Table I.

| Variable | Number of points |

|---|---|

| fracChange | |

| fracHigh | |

| fracLow |

We used dynamic edges for the discretization: at each train, the maximum and minimum values of fracChange, fracHigh, and fracLow are computed. We then generated three linearly spaced vectors for the edges, using as the lowest values the , and as the highest values the values. Finally, we assigned to each discrete value its corresponding index in the edges array.

Furthermore, compatibility with our monovariate Hidden Markov Model required mapping the three-dimensional space to a one-dimensional space. The mapping process was accomplished by enumerating the points within the discrete three-dimensional set, as described in Equation 14. The inverse mapping was achieved using Equations IV:

| (14) |

| (15) | ||||

IV-A Training

During the initial trains we assumed four underlying hidden states, where each state generates outputs represented by a GMM with four components. We then re-trained our model varying the values. The specific parameters used for each train can be found on our GitHub repository [26].

The parameters of these GMMs were estimated using the MATLAB function fitgmdist, which optimizes the model using the Expectation-Maximization (EM) algorithm. The initial parameters of the GMM are obtained through k-means clustering. The resulting probability density function served as the initial estimate for the emission matrix. Moreover, we assigned a uniform distribution of probabilities as the initial estimate for the transition matrix.

The training data for the HMM is constructed by using a rolling window approach. In this approach, each observation sequence spans a fixed duration of 10 days. We refer to this duration as latency. The window is shifted incrementally along the training period: the first sequence captures observations from the initial time point, while each following sequence incorporates new observations by sliding the window by one day. The dataset is then provided as input to the MATLAB function hmmtrain. This function utilizes the Baum-Welch algorithm to estimate the transition and emissions matrices. These estimations are initialized with the initial guesses discussed previously.

IV-B Prediction

Following the training phase, we proceeded to test our model by predicting the stock daily close prices for different time frames. For each day within the target period, the prediction process involved the following steps:

-

1.

We considered the last observations available. These observations represent the preceding 9 days.

-

2.

Next, we appended each possible output for the current day , creating a 10-day sequence. This sequence now encompasses the 9 historical observations and one potential observation for the next day. There are possibilities for the current day.

-

3.

We computed the probability for each sequence to be generated from our trained model. Finally, we selected the observation with the highest emission probability as the observation for the next day.

In certain cases, there may arise situations where the probability of emitting the historical observations, along with any hypothetical observation, becomes 0 or very close to 0. This can occur due to numerical errors or limitations inherent the model. However, we have found that incorporating a dynamic window can enhance the performance of our model.

To address the issue, we have modified the prediction algorithm as follows: if the highest probability obtained is , we repeat the prediction algorithm while gradually reducing the latency by one day. By reducing the latency, we aim to find a viable solution where the emitted probabilities are non-zero. This process of reducing latency is repeated iteratively until a solution is found, while ensuring that the historical sequence remains sufficiently long. In our case, we have set a minimum requirement of four days for the historical sequence.

V Results

We used multiple metrics to evaluate the performance of our models. Mean Absolute Percentage Error (MAPE) is calculated between the actual and predicted stock closing prices.

| (16) |

On day , is the predicted stock closing price, is the actual stock closing price, and is the total number of predictions. Table II shows our results on two different stocks, compared to the results from other papers [25], [24].

| Stock Name | Our HMM | HMM-MAP [25] | HMM + Fuzzy Model [24] | ARIMA / ANN |

|---|---|---|---|---|

| Apple Inc. | 1.50 | 1.51 | 1.77 | 1.80 |

| IBM Corp. | 0.68 | 0.61 | 0.78 | 0.97 |

Predicting the movement of stock prices for a single day is a challenging task in itself. Achieving accuracy in predicting multiple consecutive days becomes even more difficult and often approaches the realm of impossibility. Recognizing the potential utility of predicting whether the stock value will increase or decrease during the day, we introduced a novel evaluation metric called Directional Prediction Accuracy (DPA). DPA measures the percentage of correct directional predictions, providing valuable information about the accuracy of our model.

| (17) |

In Equation 17, is the total number of predictions, is the Kronecker delta function, is the predicted stock closing price, the actual closing price, and is the stock opening price. Table III demonstrates that MAPE and DPA are not equivalent measures as they are in general not correlated.

| Stock Name | MAPE | DPA | Training | Testing | ||||

| Apple Inc. | 1.50% | 52.11% |

|

|

||||

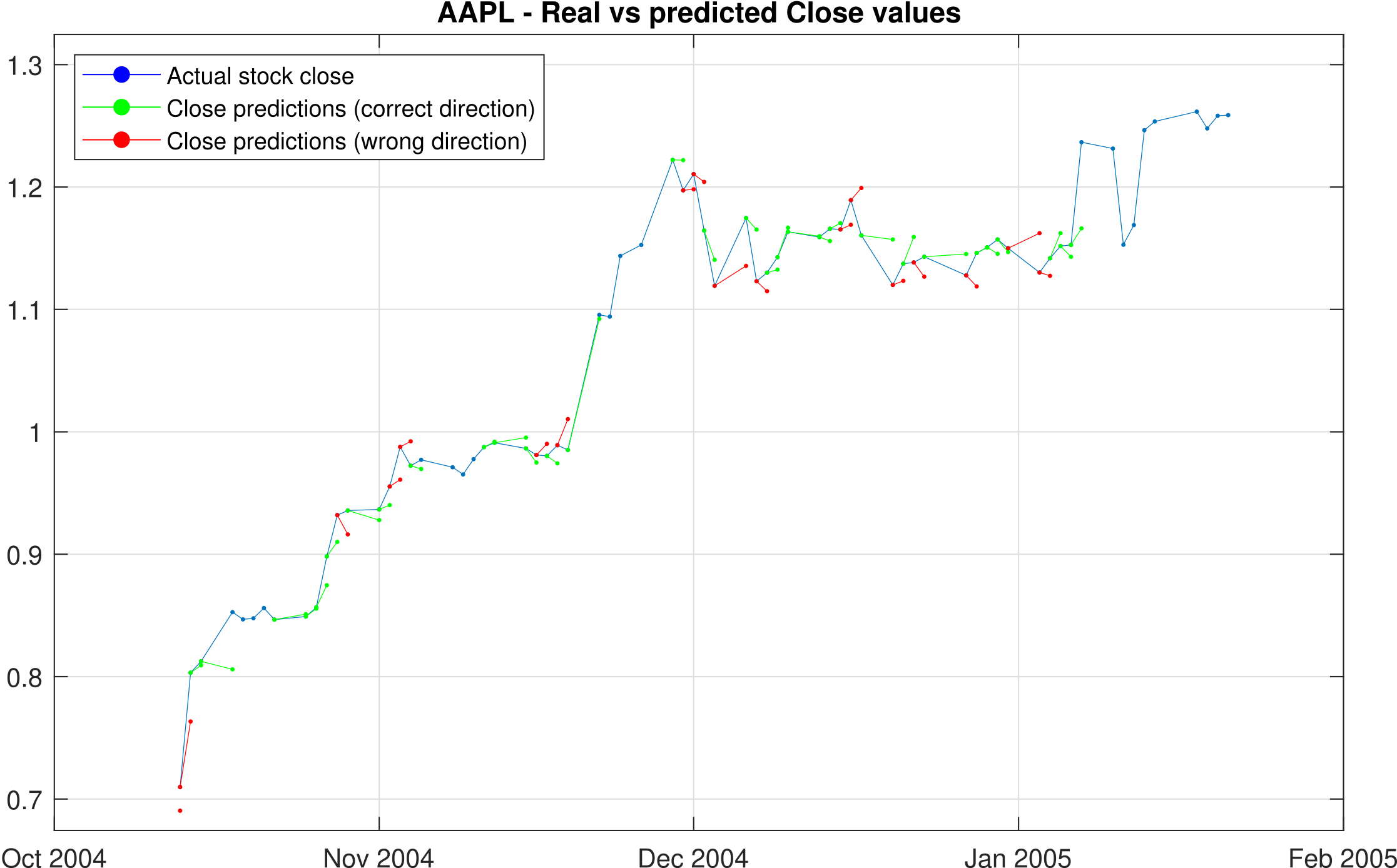

| 111Figure 3 shows predicted and actual close values for this train. Green lines indicate predictions that guessed right the sign of the fractional change with respect to the opening price. Therefore, 63.27% of the predictions are correct in sign. The high MAPE reflects the accuracy of the predictions that often deviate from the actual close value, although being correct in sign. | 1.73% | 63.27% |

|

|

||||

| 1.05% | 53.06% |

|

|

|||||

| 1.01% | 40.57% |

|

|

|||||

| IBM Corp. | 0.77% | 54.55% |

|

|

||||

| 0.82% | 57.58% |

|

|

|||||

| 0.68% | 60.23% |

|

|

|||||

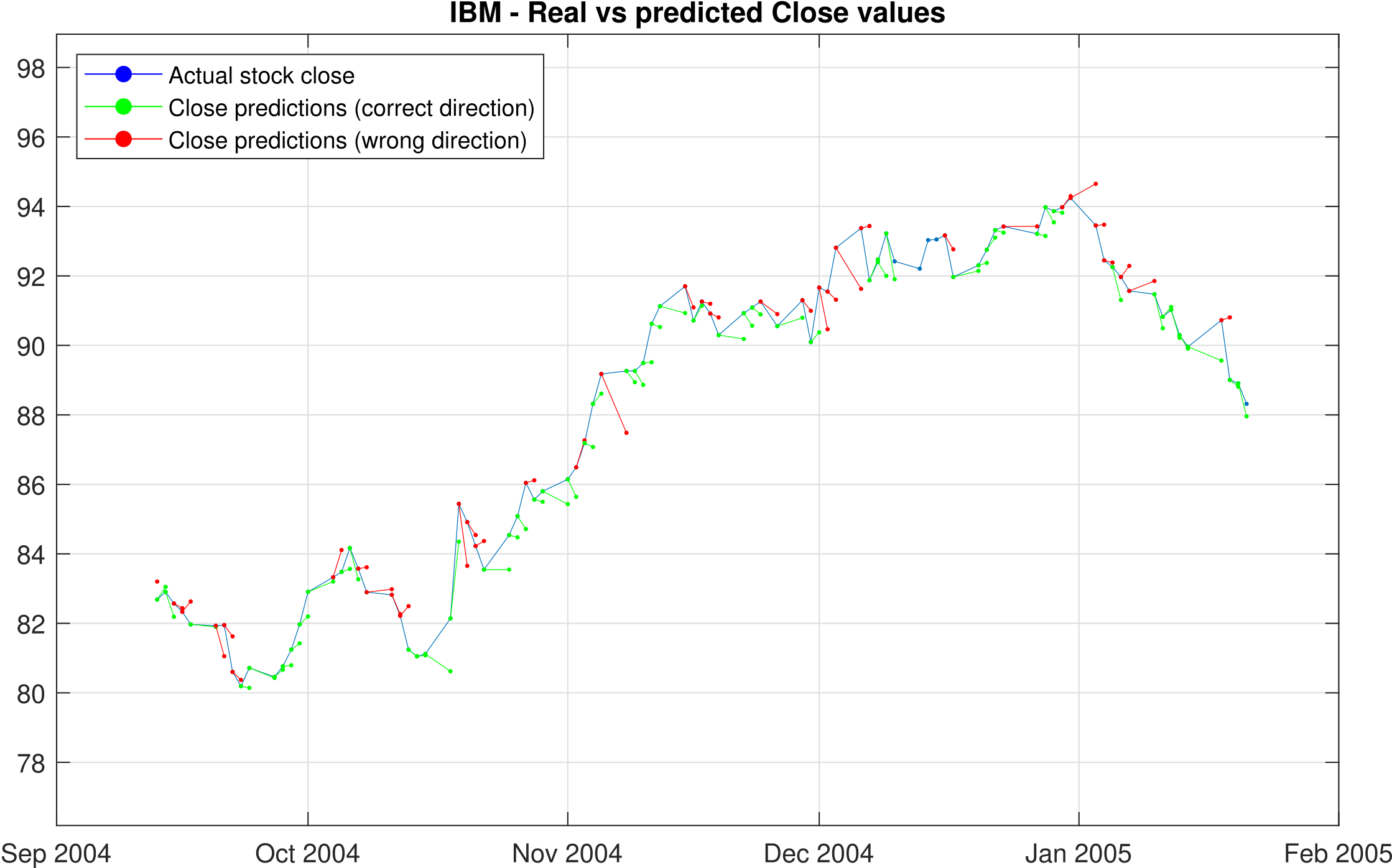

| 222The results of this train are shown in Figure 5: since the MAPE is low, predicted close values are, on average, more accurate. | 0.88% | 52.73% |

|

|

||||

| Dell Inc. | 1.45% | 60.32% |

|

|

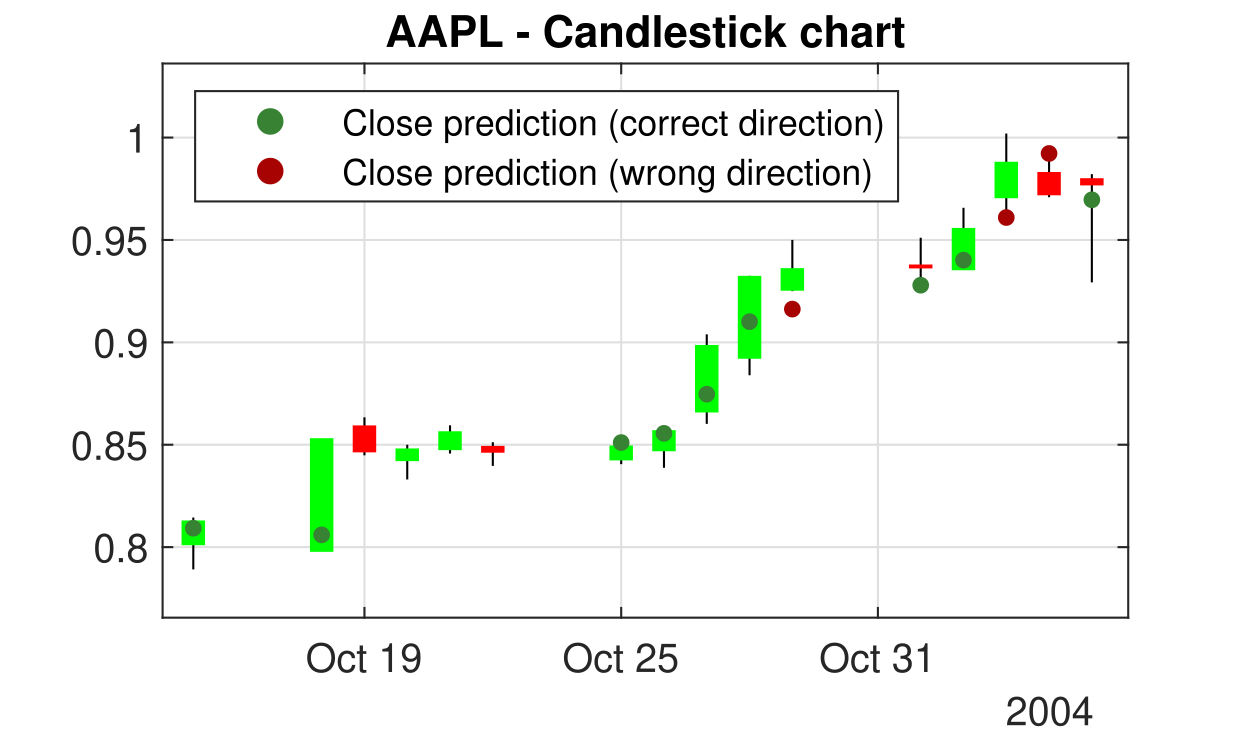

Figure 4 remarks the difference between the two indicators: the candlestick chart shows the actual prices for AAPL during the testing period 2004-10-13 to 2005-01-21. The dots show the predicted close values for the corresponding day. When the dots are green, they contribute to increasing the DPA. They only improve the MAPE when they get closer to the actual close value.

VI Conclusions and Further Developments

In this study, we have undertaken a comprehensive implementation of the Stock Prediction Hidden Markov Model originally proposed by Gupta et al. [25]. Building upon their foundational work, we aimed to assess the model’s performance on diverse datasets and explore its effectiveness in predicting stock market movements. By carefully replicating and extending their approach, we have conducted a rigorous evaluation, comparing the results with benchmark models to gain valuable insights into the model capabilities and limitations.

Our model was trained on a time period of one to two years and used to make predictions on a different time span, demonstrating its flexibility and re-usability. The complete source code, along with pre-trained models and a summary of their characteristics, is available on GitHub [26].

Our implementation underwent rigorous testing on various stocks, and we compared the results with those obtained from HMM-MAP, HMM-Fuzzy, ARIMA, and ANN models. We conducted thorough exploration of different hyperparameters, measuring their impact in search of optimal values. The outcomes demonstrated a significantly lower Mean Absolute Percentage Error compared to HMM-Fuzzy, ARIMA, and ANN models when trained on the same years as those in [25] and [24]. Furthermore, to gain additional insights into the efficiency of our model, we developed a novel evaluation metric named Directional Prediction Accuracy (DPA). The DPA allowed us to assess the accuracy of our predictions in capturing stock price movements, providing valuable information for model performance assessment.

For further improvement, we propose fine-tuning the Emission and Transmission matrices on the latest time window each day before making predictions. This approach involves training the main model on historical data, then updating the matrices with data from a more recent period just before making each prediction. For example, we could train the main model from 2021-01-01 to 2023-01-01 and fine-tune the matrices using data from 2022-06-01 to 2023-06-01 before making a prediction for 2023-06-02. This process could potentially capture more recent market trends and improve the accuracy of predictions.

In conclusion, our implementation of the Stock Prediction HMM exhibited strong predictive capabilities, outperforming other benchmark models. The proposed fine-tuning approach holds promise for enhancing future predictions and warrants further investigation to capitalize on recent market dynamics. Our work contributes to the growing field of stock market prediction and provides valuable insights for traders and financial analysts.

July 2023

References

- [1] “Institutional investors definition — nasdaq.” [Online]. Available: https://www.nasdaq.com/glossary/i/institutional-investors

- [2] “Investor bulletin: Hedge funds.” [Online]. Available: https://www.investor.gov/introduction-investing/investing-basics/investment-products/private-investment-funds/hedge-funds

- [3] “Algo or algorithmic trading definition — nasdaq.” [Online]. Available: https://www.nasdaq.com/glossary/a/algo-trading

- [4] E. F. Fama, “Random walks in stock market prices,” Financial Analysts Journal, vol. 51, no. 1, pp. 75–80, 1995, publisher: Routledge.

- [5] A. W. Lo and A. C. MacKinlay, “Stock market prices do not follow random walks: Evidence from a simple specification test,” The Review of Financial Studies, vol. 1, no. 1, pp. 41–66, 2015-04.

- [6] F. Longin and B. Solnik, “Is the correlation in international equity returns constant: 1960–1990?” Journal of International Money and Finance, vol. 14, no. 1, pp. 3–26, 1995.

- [7] Z. Ding, C. W. J. Granger, and R. F. Engle, “A long memory property of stock market returns and a new model,” Journal of Empirical Finance, vol. 1, no. 1, pp. 83–106, 1993.

- [8] T. D. Matteo, T. Aste, and M. M. Dacorogna, “Scaling behaviors in differently developed markets,” Physica A: Statistical Mechanics and its Applications, vol. 324, no. 1, pp. 183–188, 2003.

- [9] R. N. Mantegna and H. E. Stanley, “Scaling behaviour in the dynamics of an economic index,” Nature, vol. 376, no. 6535, pp. 46–49, 1995.

- [10] K. R. French, G. W. Schwert, and R. F. Stambaugh, “Expected stock returns and volatility,” Journal of Financial Economics, vol. 19, no. 1, pp. 3–29, 1987.

- [11] W. Y. Lee, C. X. Jiang, and D. C. Indro, “Stock market volatility, excess returns, and the role of investor sentiment,” Journal of Banking & Finance, vol. 26, no. 12, pp. 2277–2299, 2002.

- [12] X. Gabaix, P. Gopikrishnan, V. Plerou, and H. E. Stanley, “A theory of power-law distributions in financial market fluctuations,” Nature, vol. 423, no. 6937, pp. 267–270, 2003, publisher: Nature Publishing Group UK London.

- [13] R. N. Mantegna, Z. Palágyi, and H. E. Stanley, “Applications of statistical mechanics to finance,” Physica A: Statistical Mechanics and its Applications, vol. 274, no. 1, pp. 216–221, 1999.

- [14] S. Mukherjee, E. Osuna, and F. Girosi, “Nonlinear prediction of chaotic time series using support vector machines,” in Neural Networks for Signal Processing VII. Proceedings of the 1997 IEEE Signal Processing Society Workshop, 1997, pp. 511–520.

- [15] F. E. Tay and L. Cao, “Application of support vector machines in financial time series forecasting,” Omega, vol. 29, no. 4, pp. 309–317, 2001.

- [16] P.-F. Pai and C.-S. Lin, “A hybrid ARIMA and support vector machines model in stock price forecasting,” Omega, vol. 33, no. 6, pp. 497–505, 2005.

- [17] H. jung Kim and K. shik Shin, “A hybrid approach based on neural networks and genetic algorithms for detecting temporal patterns in stock markets,” Applied Soft Computing, vol. 7, no. 2, pp. 569–576, 2007.

- [18] K. jae Kim and I. Han, “Genetic algorithms approach to feature discretization in artificial neural networks for the prediction of stock price index,” Expert Systems with Applications, vol. 19, no. 2, pp. 125–132, 2000.

- [19] J. Bollen, H. Mao, and X. Zeng, “Twitter mood predicts the stock market,” Journal of Computational Science, vol. 2, no. 1, pp. 1–8, 2011.

- [20] M. R. Hassan and B. Nath, “Stock market forecasting using hidden markov model: a new approach,” in 5th International Conference on Intelligent Systems Design and Applications (ISDA’05), 2005, pp. 192–196.

- [21] L. Rabiner, “A tutorial on hidden markov models and selected applications in speech recognition,” Proceedings of the IEEE, vol. 77, no. 2, pp. 257–286, 1989.

- [22] M. Zhang, X. Jiang, Z. Fang, Y. Zeng, and K. Xu, “High-order hidden markov model for trend prediction in financial time series,” Physica A: Statistical Mechanics and its Applications, vol. 517, pp. 1–12, 2019.

- [23] Y. Zhou and J. Zheng, “Research on stock market forecasting model based on data mining and markov chain,” in 2022 IEEE 2nd International Conference on Mobile Networks and Wireless Communications (ICMNWC), 2022, pp. 1–5.

- [24] M. R. Hassan, “A combination of hidden markov model and fuzzy model for stock market forecasting,” Neurocomputing, vol. 72, no. 16, pp. 3439–3446, 2009.

- [25] A. Gupta and B. Dhingra, “Stock market prediction using hidden markov models,” in 2012 Students Conference on Engineering and Systems, 2012, pp. 1–4.

- [26] (2023) valentinomario/HMM-stock-market-prediction. [Online]. Available: https://github.com/valentinomario/HMM-Stock-Market-Prediction