Estimation of Models with Limited Data

by Leveraging Shared Structure

Abstract

Modern data sets, such as those in healthcare and e-commerce, are often derived from many individuals or systems but have insufficient data from each source alone to separately estimate individual, often high-dimensional, model parameters. If there is shared structure among systems however, it may be possible to leverage data from other systems to help estimate individual parameters, which could otherwise be non-identifiable. In this paper, we assume systems share a latent low-dimensional parameter space and propose a method for recovering -dimensional parameters for different linear systems, even when there are only observations per system. To do so, we develop a three-step algorithm which estimates the low-dimensional subspace spanned by the systems’ parameters and produces refined parameter estimates within the subspace. We provide finite sample subspace estimation error guarantees for our proposed method. Finally, we experimentally validate our method on simulations with i.i.d. regression data and as well as correlated time series data.

1 Introduction

In a variety of fields such as healthcare and e-commerce, it is often desirable to estimate parameters or provide recommendations for individuals based on data. Consider the common situation where we have different individuals, each with observations collected in . Assume the data is generated as

| (1.1) |

where is some independent noise vector, and are parameters of interest.

Such a linear model is ubiquitous in statistics, and standard least squares regression provides an estimate of based on when and is well-conditioned.

Realistically, however, while a data set may contain many individuals, the data available from each individual may be limited, especially compared to the dimension of the parameter space considered. For instance, in the healthcare setting, patient data may be fragmented and stored on different electronic health record systems, so that each record system may have many individuals but imcomplete data from each [1]. This may lead to problems of non-identifiability for individual systems, as in the case where we only have observations of a -dimensional linear model.

If there is a shared structure among individuals, however, it may be possible to leverage information from other individuals who share similar characteristics to overcome the challenge of non-identifiability of individual parameters.

In this paper, we examine this possibility and propose a method of estimating each system’s -dimensional parameter by exploiting data from other systems along with the assumption that the parameters lie in a common -dimensional subspace, where . The questions we wish to answer are: can a sufficiently large number of systems compensate for a small amount of data per system in the task of estimating all the parameters? If so, how does the sample complexity scale in the parameters and of the problem?

If we simply count the degrees of freedom of the model, we have parameters to estimate (the common -dimensional subspace of parameters plus individual factor loadings or coefficients). Intuitively, one may expect that parameters are needed to jointly identify all parameters of the system. It is not obvious how to rigorously justify this intuition, nor how to develop and implement an estimation algorithm for this setting.

To begin to tackle this complex and broad-ranging question, we propose an estimation method based on three separate least squares optimizations. The method first computes initial estimates of each system’s parameter vector, which may be significantly far from the true value, but which still contain information about the common underlying subspace spanned by the true system parameters. Next, an estimate of this low dimensional subspace is obtained by extracting the top principal subspace of the first step estimates. From this, we can obtain a refined estimate of each system’s individual parameters by solving another least squares problem, this time constrained to be over the estimated subspace. This last step requires for parameter identifiability, which can be a considerably easier condition to satisfy than the naive requirement of , as in many real world datasets.

We provide finite sample subspace estimation error guarantees for a variant of our proposed method that takes into account the possible ill-conditioning of the pseudo-inverse-based least squares solution which arises when . The analysis relies on obtaining concentration bounds for the sample covariance of the first-step estimates, and then proving that subspace estimation on these first-step estimates will obtain the true underlying subspace in expectation.

Finally, we demonstrate our method and variants on simulations with i.i.d. regression data. We also evaluate our method on time series data with correlated regressors, and find that the method is flexible enough to handle this scenario. These results suggest the applicability of the three-step estimation method for more general settings of estimation of related with a common low rank structure.

1.1 Related Work

Mixtures of linear regressions

The problem of estimating parameters from limited observations of different systems that share a common low dimensional structure is related to the problem of mixtures of linear regressions [2, 3] and multitask, or meta-learning [4, 5]. The main difference to our setting is the systems’ parameters are assumed to be clustered, rather than coming from a low dimensional subspace.

Low rank matrix regression

Furthermore, a large body of work studies the related problem of low rank matrix regression, which usually uses a least squares estimator with nuclear norm regularization to estimate a low rank matrix. We can re-express (1.1) to make the comparison with matrix regression explicit. Let be the matrix whose columns are the system parameters. Then by assumption, . However, the data generating process for observations is

| (1.2) |

where is the th coordinate vector in . While we are still trying to estimate a low rank matrix , the dimension of this matrix grows with the number of observations—unlike in matrix regression where it is assumed constant—landing us in a different regime for analysis and optimization.

Dictionary learning.

Finally, the problem of dictionary learning, also known as sparse coding, and matrix factorization, shares similar structure to the problem considered in this paper [6, 7, 8]. However, we only observe system parameters through the lens of a design matrix whose rows do not fully span the parameter space. Even if our design matrix were the identity (so ), though, we also do not impose a sparsity assumption on the dictionary coefficients, as is standard in the dictionary learning literature. The differences are further detailed in Section 4.1.

Meta-learning and transfer learning.

After the initial submission of this paper, we became aware of recent related work on this problem. In [9], the authors present a method of moments (MoM) estimator, and a similar estimator is studied under more general assumptions in [10]. We discuss the relationship between these estimators and ours and provide an empirical comparison in Section 5.3.

2 Preliminaries

2.1 General notations

We define for the set . The inequality means that there exists a universal constant such that .

For vectors , and denote the Euclidean inner product and norm, respectively.

For a matrix , , and denote its trace, transpose and Moore–Penrose pseudoinverse, respectively. The identity matrix in is written . For matrices , denotes the Frobenius or trace inner product, is the Frobenius norm of , and is its spectral norm. Let denote the orthogonal group on and denote the Stiefel manifold of orthonormal -frames in .

2.2 Subspaces

For , denotes the Grassmanian manifold of -dimensional subspaces of and we write for the orthogonal projection onto a subspace . For an orthogonal projection of rank and , the identities and show that the map is a bijection from to the set of orthogonal projections of rank . This allows us to identify the two sets [13, Sec. 1.3.2]:

| (2.1) |

Note that the choice of an orthonormal basis of a subspace gives a representation of by an element , although the representation is non-unique. For such a matrix we have .

For any two subspaces , we can find pairs of principal vectors for , and principal angles such that , , and , for . is the smallest angle between any vector in and any vector in , which is achieved by and . The remaining principal vectors and angles are defined inductively, by restricting at each step to the orthogonal complement of the span of the previous vectors [14, 15]. We write for the diagonal matrix whose diagonal entries are the principal angles. It is possible to show that the nonzero eigenvalues of are the sines of the nonzero principal angles between and , each counted twice [16, Sec. VII.1]. This implies that and .

2.3 Random variables

Unless otherwise specified, all random variables are defined on the same probability space. We write for identically distributed variables and . We say that a random vector is sub-Gaussian with variance proxy , and write , if for all

| (2.2) |

3 Model

We consider linear systems of dimension , from each of which we have observations. Specifically, each system has observations generated according to

| (3.1) |

where is the parameter of system .

The central assumption of our model is that the system parameters lie in an -dimensional subspace of , where . An orthonormal basis of constitutes a common dictionary of atoms shared by all systems and we can write for each

| (3.2) |

for some . We are primarily interested in estimating the -dimensional subspace , from which we can easily recover , and then for , from the data.

We now describe our distributional assumptions. All the random variables , and are mutually independent. The matrices are identically distributed, each having i.i.d. standard normal entries. Coefficients and noise are centered isotropic sub-Gaussian random vectors in and , respectively, with covariance matrices and , respectively.

4 Three-Step Estimator

We propose an estimation method that follows a general three step approach. First, compute initial estimates of each system ’s parameter. Next, find the -dimensional subspace that best explains the initial estimates. In the last step, the individual system estimates are refined by leveraging the subspace learned in the second step.

Due to the linear structure of our observation model, instantiating the above approach naturally results in formulating and solving a linear least squares problem at each of the three steps. The following subsections describe these least squares problems in more details and Algorithm 1 summarizes the computation of their solution.

4.1 Initial individual estimates

We first obtain a least squares estimate of up to the null space of , which is nontrivial as we focus on the regime . Let be the pseudoinverse of . Then our initial estimates are

| (4.1) |

To gain a better understanding of our initial estimates , under our observation model (3.1), we can write

| (4.2) |

where is the projection matrix onto the -dimensional row space of . Since the distribution of the rows of is rotationally invariant, one can check that (see Lemmas A.1 and A.2). Hence, up to a rescaling by , is an unbiased estimate of . However, the noise of this estimate

| (4.3) |

is not independent of the true parameter as it includes its projection onto the null space of that was left unobserved.

Normalization.

The normalization step on line (5) ensures that the first-step estimates are all weighted equally in the subspace estimation step. As will become clear in the simulations (Section 5.2) this mitigates issues arising due to the pseudo-inverse being ill-conditioned when is close to . For tractability reasons, our theoretical analysis studies a variant of Algorithm 1 in which the normalization step is replaced with a truncation , for some predefined threshold . We also compare this variant to our main estimator in Section 5.2.

Comparison with dictionary learning.

Using (4.3) wen can write . Hence, our setting is reminiscent of the dictionary learning, or sparse coding, problem, in which we have noisy observations where , for some fixed matrix , and some vector . Both and are unknown and the goal is to learn , which in our setting then allows for a straightforward estimation of and .

However, we cannot apply dictionary learning methods straight off the shelf. First, dictionary learning models assume sparsity of the unknown coefficients , and for most sample complexity results, a degree of sparsity is necessary (i.e., the size of the support of is upper bounded) [6, 17, 18]. Meanwhile, we make no restrictive assumptions on the factor loadings . Second, the additive noise in dictionary learning is assumed to be independent of other randomness in the problem, either with standard subgaussian or bounded distributional assumptions [6, 17, 7]. However, as already mentioned, in our method is visibly not independent of the parameters to be estimated, as it contains the component of in the null space of .

4.2 Subspace recovery

The goal of the second step is to compute an estimate of the -dimensional subspace of containing the ground truth parameters . We do so by finding the -dimensional subspace that best approximates the (normalized) first step estimates , in the least squares sense. If denotes the orthogonal projection onto this optimal subspace, the residual error associated with is its distance to the subspace, that is . Consequently, the least squares problem at this step is

| (4.4) |

Note that (4.4) is exactly the problem of finding the space spanned by the first principal components of the first step estimates . Those are given by the top left-singular vectors of the matrix whose columns are .

Another interpretation of this subspace estimate can be obtained by observing that:

| (4.5) | ||||

| (4.6) | ||||

| (4.7) |

where the last equality uses that is also an orthogonal projection. This allows us to rewrite (4.4)

| (4.8) |

The matrix appearing on the last line is the sample covariance matrix of the first step estimates. Because this matrix is positive semi-definite, it admits a spectral decomposition with non-negative eigenvalues and orthogonal eigenspaces. The top left-singular vectors of are equivalently given by an orthonormal collection of eigenvectors associated with the top eigenvalues of (counted with multiplicity).

4.3 Parameter recovery

In the third stage of our algorithm we obtain revised estimates of for each given the estimate with orthogonal frame matrix :

| (4.9) | ||||

| (4.10) |

One can obtain this result by solving for where

| (4.11) |

5 Results

5.1 Sample complexity

Our main theoretical result is an upper-bound on the sample complexity of the estimator described in Algorithm 1. As already mentioned, it is easier to analyze a variant in which line (5) performs a truncation instead of a normalization. Thus, for the remainder of this section is defined as , for some predefined threshold . Equivalently, Algorithm 1 simply drops the first step estimates for which , and uses the remaining ones in the subspace estimation step.

Theorem 5.1.

Let be the subspace spanned by the columns of the output in Algorithm 1 with threshold level if , and if . Then for each , with probability at least

| (5.1) |

The proof of Theorem 5.1 is provided in Appendix B. We first show that the th principal subspace of the covariance matrix is the ground truth subspace and quantify its spectral gap. By the Davis–Kahan theorem, upper-bounding the principal subspace angle reduces to upper-bounding the spectral norm of . This follows from a standard result on the concentration of covariance matrices of sub-Gaussian random variables.

The bound in Theorem 5.1 scales as as expected when learning from independent observations. While the dimension of does not explicitly appear in the bound, it would be conventional to take , so that the norm of the ground truth parameters concentrate around , as is usually assumed in sample complexity bounds. For this choice of , our error bound scales linearly in . The first term in the bound degrades as increases and becomes when . This is due to the design matrix becoming ill-conditioned for close to , a phenomenon we inspect more closely in Section 5.2 below. When , the error bound has a rather negligible dependence on , while one would hope for a bound that decreases in . Obtaining tighter bounds is left for future work.

5.2 Simulation

We investigate by simulation the performance of the three-step estimator of Algorithm 1 that uses normalized first-step estimates, as well as the thresholding variant of Algorithm 1 analyzed in Theorem 5.1, and which uses a truncated first-step estimate for subspace estimation.

For each trial, an -dimensional subspace is fixed and i.i.d. samples , are generated according to (1.1), with , drawn uniformly from the unit ball intersected with (and thus subgaussian with variance proxy ), and with i.i.d. standard normal entries. Each plot shows the average of 30 trials and error bars indicate one standard deviation.

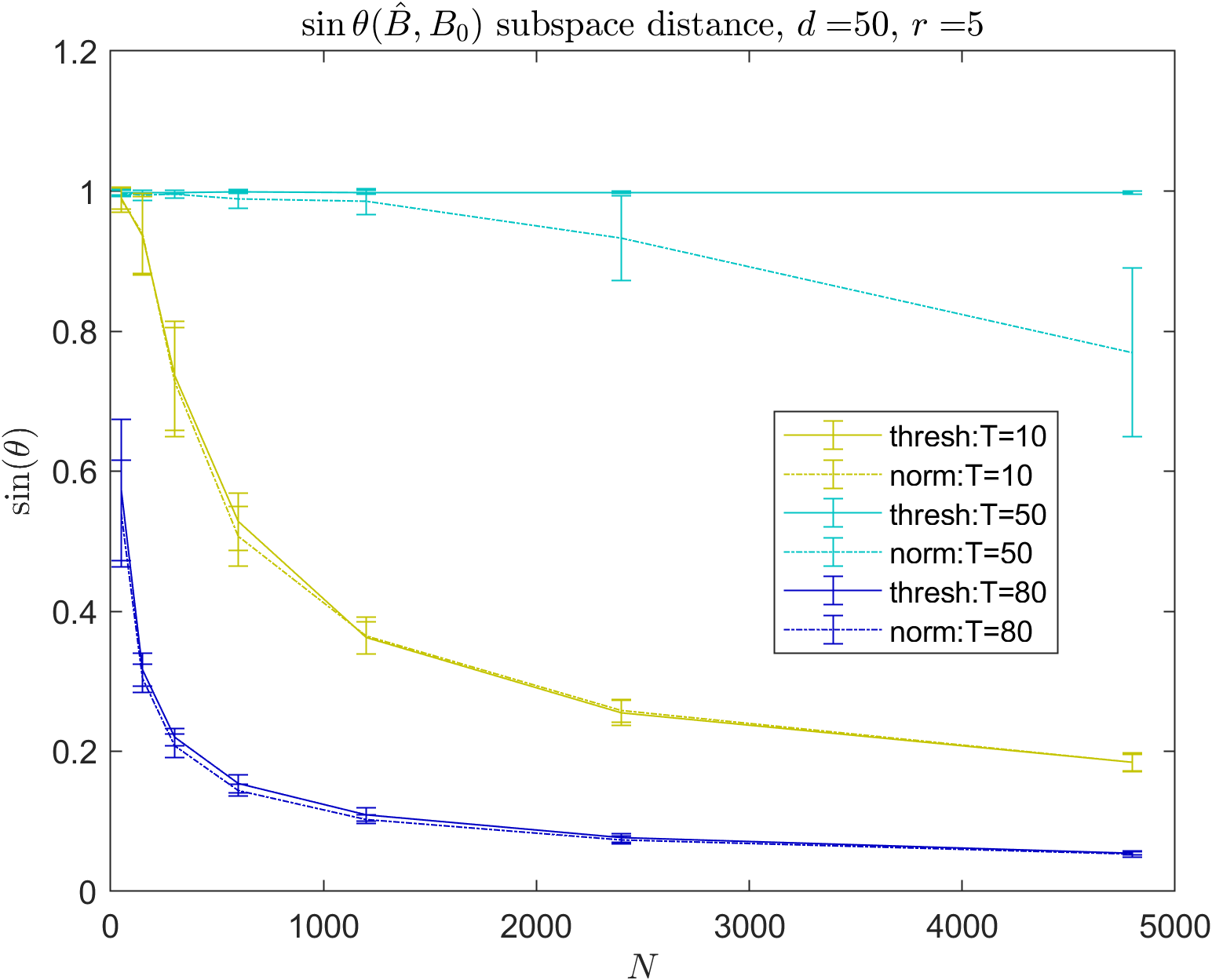

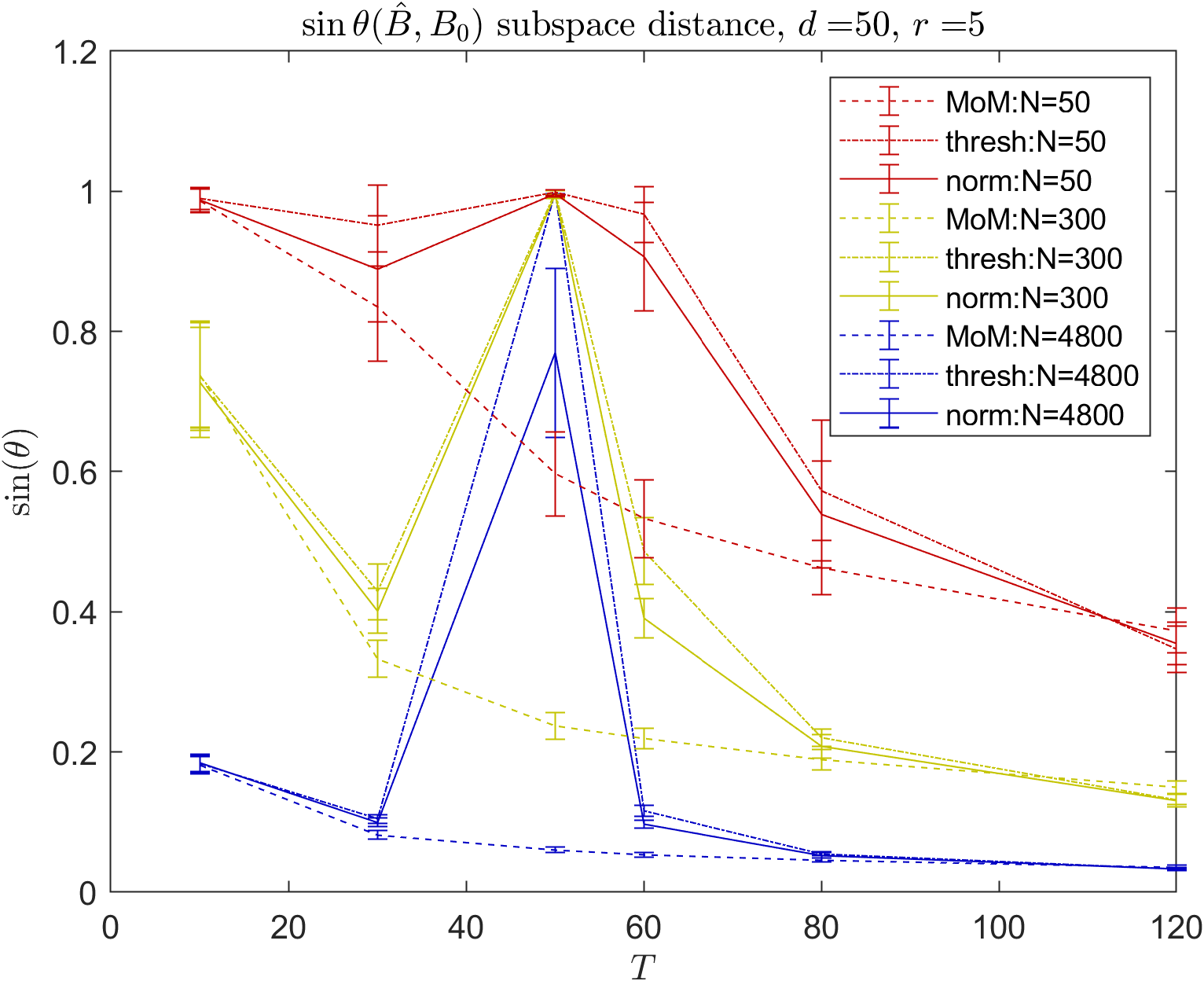

Figure 1 shows the subspace estimation error of the estimate from (1) thresh, Algorithm 1 with truncated first-step estimates, (2) norm, Algorithm 1 with normalized first step estimates. Results are shown for , in regimes , , and , as the number of systems is varied.

Both versions of the three-step estimator do well in both the and regime, though we note suboptimal performance when . This arises from the fact that the pseudoinverse of can be ill-conditioned when . As described before, we address this issue by normalizing our first step estimates to mitigate the effect of a single sample misdirecting the subspace estimator with an amplified noise term . For the truncating estimator, we chose an optimal threshold level for each and that trades off controlling the effect of possibly ill-conditioned pseudo-inverse-based least squares estimates with losses in effective sample size.

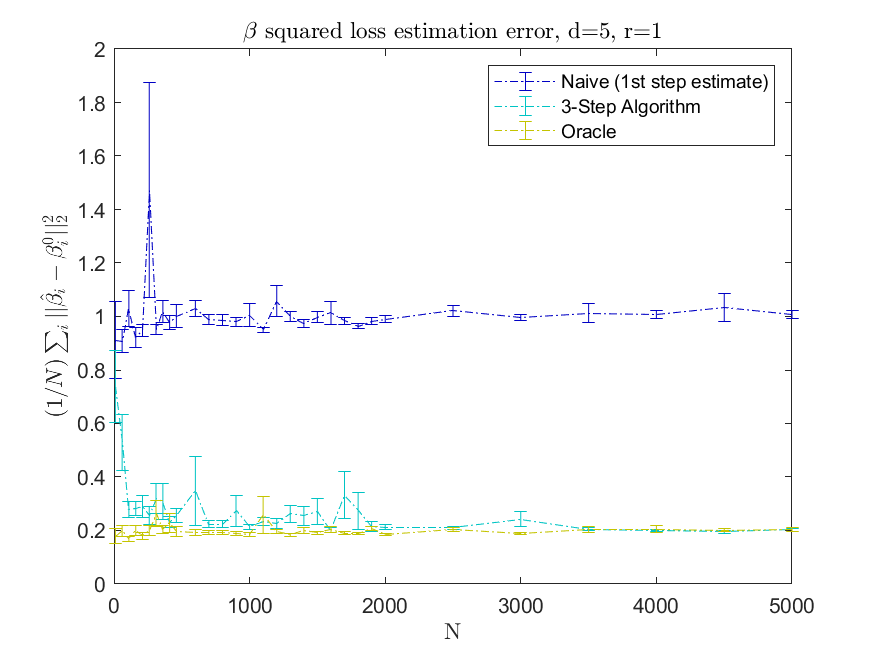

In Figure 2, we show the performance of the refined estimates from thresh in comparison with two benchmarks: (1) the “oracle” least squares estimate assuming is known, which is obtained as the minimizer of (4.9) with replaced by the true subspace , and (2) the naive least squares estimate run separately for each system , and which does not share information across systems, i.e., in (4.1). The thresh estimator is able to leverage information across systems to eventually match the performance of the oracle.

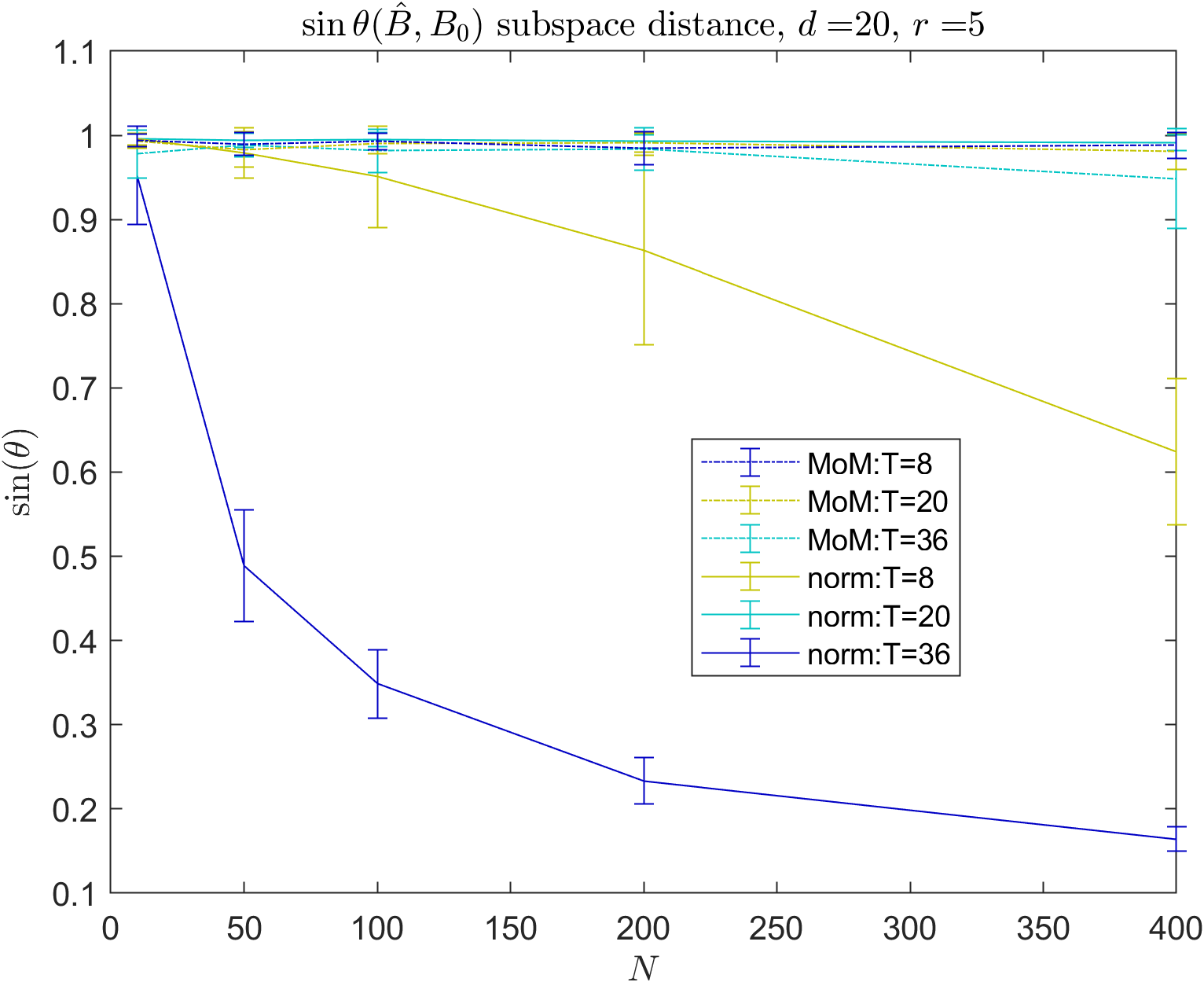

5.3 Comparison with related work

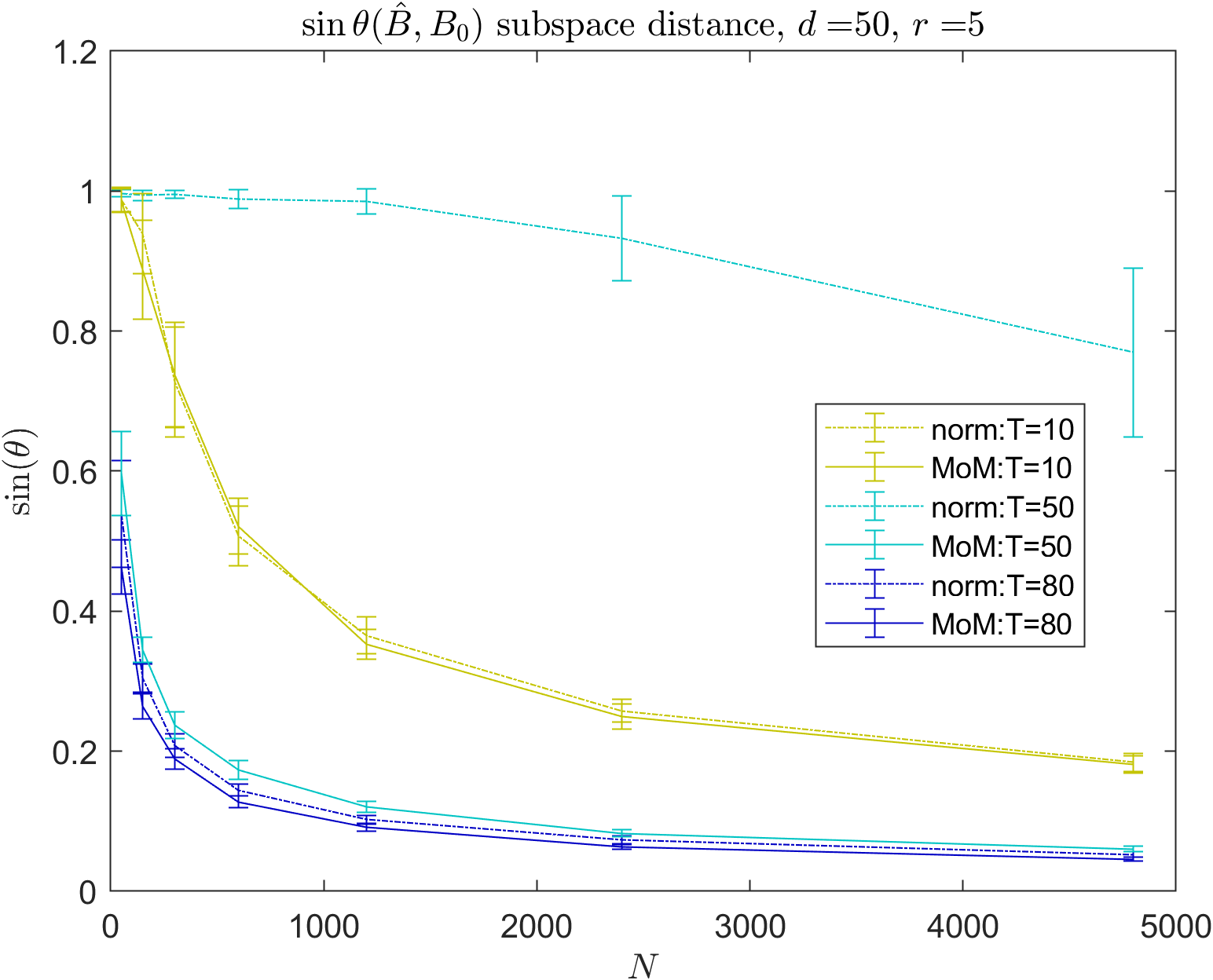

In [9], the authors present a method of moments estimator, which we refer to as MoM, for subspace estimation in the present setting. This estimator can be interpreted under our three-step method as first obtaining a first-step estimate and then estimating the subspace shared by these first-step estimators. Specifically, the matrix pre-multiplies rather than the pseudoinverse pre-multiplying as it does in the first-step least squares estimate of Algorithm 1.

Figure 3 and 4 compare the performance of norm and of MoM in terms of subspace estimation error. Results are shown for the regimes , , and . We see that both estimators perform comparably in the first and third regimes, while norm suffers in the regime where may be ill-conditioned. However, the next section on time series data suggests that norm may generalize better to settings with dependent regressors such as time-series data.

5.4 Time series estimation

We next evaluate our algorithm norm and the method of moments estimator, MoM of [9], on time series data. Specifically, consider observations generated as:

| (5.2) |

for each , with , and a sub-Gaussian random vector in . We assume each dynamics matrix is of rank and can be written in the form , where the rows of are independently distributed and rotationally invariant, and is an orthonormal -frame for a subspace . Thus, the rows of lie in , for . is normalized by its operator norm to ensure stability, since the operator norm dominates the magnitude of the eigenvalues. Unlike the setting of i.i.d. regression, the covariates are no longer independent of each other and of the collection of noise vectors .

As demonstrated in Figure 5, norm is able to generalize to this setting quite well when is not close to , as opposed to the MoM, which fails to learn even as increases. Intuitively, MoM is not robust to the non-isotropy of the regressors , while our least-squares-based first-step estimate is still able to extract useful information in this setting.

6 Conclusion

We have shown that when there is shared low-rank structure among systems, we can leverage data from other systems to help estimate individual parameters, even in the regime , in which systems would otherwise be non-identifiable from their own data alone. We have presented a method to estimate the common low dimensional subspace as well as the system parameters, by a series of three least squares optimization problems, one of which can be solved simply by singular value decomposition. We then provided finite sample estimation error guarantees of a truncating variant our proposed method. These sample complexity results are not necessarily optimal, and we seek to better understand the trade-offs in the number of systems , and the number of observations per system in the best achievable estimation error. However, experiments suggest that the three-step estimation procedure may be applied successfully to more general settings such as time-series estimation.

References

- [1] S. B. Dewdney and J. Lachance, “Electronic records, registries, and the development of “big data”: crowd-sourcing quality toward knowledge,” Frontiers in oncology, vol. 6, p. 268, 2017.

- [2] S. Faria and G. Soromenho, “Fitting mixtures of linear regressions,” Journal of Statistical Computation and Simulation, vol. 80, no. 2, pp. 201–225, 2010.

- [3] Y. Li and Y. Liang, “Learning mixtures of linear regressions with nearly optimal complexity,” in Conference On Learning Theory. PMLR, 2018, pp. 1125–1144.

- [4] W. Kong, R. Somani, S. Kakade, and S. Oh, “Robust meta-learning for mixed linear regression with small batches,” Advances in neural information processing systems, vol. 33, pp. 4683–4696, 2020.

- [5] W. Kong, R. Somani, Z. Song, S. Kakade, and S. Oh, “Meta-learning for mixed linear regression,” in International Conference on Machine Learning. PMLR, 2020, pp. 5394–5404.

- [6] R. Gribonval, R. Jenatton, and F. Bach, “Sparse and spurious: dictionary learning with noise and outliers,” IEEE Transactions on Information Theory, vol. 61, no. 11, pp. 6298–6319, 2015.

- [7] R. Gribonval, R. Jenatton, F. Bach, M. Kleinsteuber, and M. Seibert, “Sample complexity of dictionary learning and other matrix factorizations,” IEEE Transactions on Information Theory, vol. 61, no. 6, pp. 3469–3486, 2015.

- [8] J. Mairal, F. Bach, J. Ponce, and G. Sapiro, “Online dictionary learning for sparse coding,” in Proceedings of the 26th annual international conference on machine learning, 2009, pp. 689–696.

- [9] N. Tripuraneni, C. Jin, and M. Jordan, “Provable meta-learning of linear representations,” in International Conference on Machine Learning. PMLR, 2021, pp. 10 434–10 443.

- [10] J. C. Duchi, V. Feldman, L. Hu, and K. Talwar, “Subspace recovery from heterogeneous data with non-isotropic noise,” Advances in Neural Information Processing Systems, vol. 35, pp. 5854–5866, 2022.

- [11] M. Pontil, “The benefit of multitask representation learning,” Machine Learning with Interdependent and Non-identically Distributed Data, p. 46, 2015.

- [12] S. S. Du, W. Hu, S. M. Kakade, J. D. Lee, and Q. Lei, “Few-shot learning via learning the representation, provably,” arXiv preprint arXiv:2002.09434, 2020.

- [13] Y. Chikuse, Statistics on Special Manifolds. Springer, 2003.

- [14] G. H. Golub and C. F. Van Loan, Matrix computations. JHU press, 2013.

- [15] K. Ye and L.-H. Lim, “Schubert varieties and distances between subspaces of different dimensions,” SIAM Journal on Matrix Analysis and Applications, vol. 37, no. 3, pp. 1176–1197, 2016.

- [16] R. Bhatia, Matrix Analysis, ser. Graduate Texts in Mathematics. New York, NY: Springer, 1997.

- [17] S. Arora, R. Ge, and A. Moitra, “New algorithms for learning incoherent and overcomplete dictionaries,” in Conference on Learning Theory. PMLR, 2014, pp. 779–806.

- [18] R. Gribonval and K. Schnass, “Dictionary identification—sparse matrix-factorization via -minimization,” IEEE Transactions on Information Theory, vol. 56, no. 7, pp. 3523–3539, 2010.

- [19] W. Bryc, The Normal Distribution: Characterizations with Applications. Springer, 1995.

- [20] E. S. Meckes, The random matrix theory of the classical compact groups. Cambridge University Press, 2019, vol. 218.

- [21] B. Collins, S. Matsumoto, and N. Saad, “Integration of invariant matrices and moments of inverses of Ginibre and Wishart matrices,” Journal of Multivariate Analysis, vol. 126, pp. 1–13, 2014.

- [22] R. Vershynin, “How close is the sample covariance matrix to the actual covariance matrix?” Journal of Theoretical Probability, vol. 25, pp. 655–686, Sep. 2012.

- [23] M. Rudelson and R. Vershynin, “Smallest singular value of a random rectangular matrix,” Communications on Pure and Applied Mathematics: A Journal Issued by the Courant Institute of Mathematical Sciences, vol. 62, no. 12, pp. 1707–1739, 2009.

Appendix A Uniform distribution on the Grassmanian

In this section, we collect some useful statements about the uniform distribution on the Grassmanian. We identify with the set of orthogonal projections of rank :

| (A.1) |

Under this identification, a matrix is uniformly distributed over iff and for each [13, Chap. 2]. In particular, when is uniformly distributed over the Stiefel manifold , the projection is uniformly distributed over . The following lemma shows that we also obtain a uniformly distributed element of by considering the projection onto the linear span of rotationally invariant and independent vectors.

Lemma A.1.

Let be a random matrix with and such that

-

1.

each row of has a rotationally invariant distribution over with absolutely continuous marginals111A necessary and sufficient condition for a rotationally invariant random vector to have absolutely continuous marginals is that [19, Lemma 4.1.6].,

-

2.

the rows of are mutually independent.

Then the orthogonal projection onto is uniformly distributed over .

Proof.

We first prove that is supported on , or equivalently that has full row rank almost surely. Denote by the th row of and by the remaining rows. It is sufficient to establish that for each . Since is a subspace of dimension at most , it is contained in a hyperplane of . Let be a normal vector to this hyperplane with , then we have

| (A.2) | ||||

| (A.3) | ||||

| (A.4) |

The first equality is the tower rule for conditional expectations. The second equality uses independence of the rows and the fact that by rotational invariance the distribution of does not depend on the unit norm vector (and in particular is the same as ). The last equality follows from the absolute continuity of .

Using that , we have for

| (A.5) |

where the penultimate equality uses that by rotational invariance of the rows of . This concludes the proof since the identity uniquely characterizes the uniform distribution among distributions supported on . ∎

Lemma A.2.

Let be uniformly distributed over , then . In particular, for each , and for each .

Proof.

The uniform distribution over is invariant under the conjugacy action of , so the same is true for the expectation . It is a standard fact that the only matrices that are invariant under the conjugacy action of —or equivalently, that commute with all matrices in —are the scalar matrices. Hence for some . We determine the value of by taking the trace

| (A.6) |

For the second claim

| (A.7) | ||||

| (A.8) |

where the second equality uses idempotence of . The final claim follows from the previous one by summing over the columns of . ∎

Lemma A.3.

Let be uniformly distributed over . Then for all

| (A.9) |

Proof.

Denote by the matrix in whose only non-zero entry, at , equals 1. Let be the orthogonal projection onto the first canonical basis vectors of . Writing = for some , it follows from that

| (A.10) |

Hence, it is sufficient to prove the result for the matrix . By linearity of , we focus on computing for some . We have for indices

| (A.11) |

Furthermore, we can write where is uniformly distributed over . Hence

| (A.12) |

We use [20, Lemma 2.22] to compute the summand expectations222More generally, closed-form expressions are known for arbitrary monomials in entries of a uniformly random orthogonal matrix. These can be expressed in terms of the so-called Weingarten functions [21, Proposition 2.2].. If , the expectation is always zero, so we focus on the case . If ,

| (A.13) | ||||

| (A.14) |

For we get

| (A.15) | ||||

| (A.16) | ||||

| (A.17) |

In summary,

| (A.18) |

This concludes the proof after summing the previous equality for . ∎

Appendix B Proof of Theorem 5.1

Recall the following expression for the first-step estimate:

| (B.1) |

and the truncated first-step estimate:

| (B.2) |

for some threshold that will be set at a later stage. The truncated first-step estimate provides us an upper bound on which will be used throughout our analysis.

Note that since has full row rank almost surely, we have almost surely, where is the th largest singular value of . This follows immediately from the fact that the non-zero singular values of are the inverse of the non-zero singular values of . Hence we define and express the threshold probability

| (B.3) |

The next lemma shows that the truncated first step estimates are sub-Gaussian. We will use the following standard facts about sub-Gaussian vectors.

-

•

for two independent random vectors and , we have .

-

•

for and , we have .

-

•

if , then for all and

(B.4)

Lemma B.1.

For all unit vectors and ,

| (B.5) |

with .

Proof.

Consider a unit vector and . By the law of total expectation

| (B.6) |

Conditioned on , is the sum of two independent sub-Gaussian variables, with and .

Since , we have . Hence

| (B.7) |

Whenever , the term on the right-hand side in the previous inequality is upper-bounded by , which implies by (B.6) that . Replacing with we obtain and we conclude by taking a union bound. ∎

Lemma B.2.

Let denote the empirical covariance matrix of the truncated first step estimates, and define its expectation . Defining , we have where if ,

| (B.8) | |||

| (B.9) |

and if , we have

| (B.10) | |||

| (B.11) |

In particular, and are the two eigenspaces of with spectral gap , and is the th principal subspace of .

Proof.

For notational convenience, we introduce the binary indicator variable , governing the truncation of the first step estimate. Note that and since is independent of and , we get

| (B.12) | ||||

| (B.13) |

We compute the first expectation in (B.12) as

| (B.14) | ||||

| (B.15) |

The first equality uses the definition of . We integrate out in the second equality using the law of total expectation and isotropy of .

If , (B.15) then becomes

| (B.16) | ||||

| (B.17) | ||||

| (B.18) |

where we apply the law of total expectation again in the first step. Finally, it is easy to check that the distribution of conditioned on is invariant under right multiplication by an element of , and has full row rank with probability 1. This implies by Lemma A.1, that conditioned on , is uniformly distributed over , which allows us to apply Lemma A.3.

Meanwhile, if , the rows of span almost surely, so that with probability 1. Then (B.15) becomes

| (B.19) |

For the second expectation in (B.12), for any ,

| (B.20) | ||||

| (B.21) | ||||

| (B.22) |

where we used isotropy of in the first equality and the law of total expectation for the second equality. Finally, the identity , valid for all , shows that, conditioned on , the columns of have rotationally invariant distributions, due to the rows of having rotationally invariant distributions conditioned on . ∎

Proof of Theorem 5.1.

We first apply a variant of the Davis–Kahan theorem (see e.g. [10, Thm 2.1]), to bound the maximum principal angle between subspaces and as

| (B.23) |

where we used that is the th principal subspace of by definition of our estimator, and by Lemma B.2, that is the th principal subspace of the matrix , with spectral gap . Using the expression for from Lemma B.2, we see that when and since when , we have

| (B.24) |

We then apply [22, Prop. 2.1] which provides a tail bound for the empirical covariance matrix of independent sub-Gaussian random vectors. By Lemma B.1, the truncated estimate satisfies a sub-Gaussian tail bound with variance proxy , hence

| (B.25) |

for all and with probability at least .

Finally, we set based on the following lower bound on provided by [23, Thm 1.1]. When ,

| (B.27) |

for some universal positive constants and . For , we get

| (B.28) | ||||

| (B.29) |

For this setting of when , we obtain with probability ,

| (B.30) |

When , the bound (B.27) holds with the roles of and swapped. Repeating the setting of above with and swapped, we have that when , with probability at least ,

| (B.31) |

∎