On Optimal Set Estimation for Partially Identified Binary Choice Models

Shakeeb Khan (Boston College)

Tatiana Komarova (University of Manchester)

Denis Nekipelov (UVA)

First Version: May 2022

This Version: October 2023111We are grateful for helpful comments from conference participants at the 2019 Asian ES meetings in Xiamen, the 2019 Chinese ES meetings in Guangzhou, the 2019 Midwest Econometric Study Group in Columbus, Ohio, the 2022 Montreal Econometrics summer conference, the 2022 Advances in Econometrics conference at Toulouse School of Economics, and seminar participants at Georgetown, UC Berkeley, UC Louvain, University of Bristol, University of Warwick, UC Riverside, Yale, Iowa. We are grateful to Ilya Molchanov for helpful comments.

Abstract:

In this paper we reconsider the notion of optimality in estimation of partially identified models. We illustrate the general problem in the context of a semiparametric binary choice model with discrete covariates as an example of a model which is partially identified as shown in, e.g. \citeasnounbierenshartog. A set estimator for the regression coefficients in the model can be constructed by implementing the Maximum Score procedure proposed by \citeasnounmanski1975. For many designs this procedure converges to the identified set for these parameters, and so in one sense is optimal. But as shown in \citeasnounkomarova2013 for other cases the Maximum Score objective function gives an outer region of the identified set. This motivates alternative methods that are optimal in one sense that they converge to the identified region in all designs, and we propose and compare such procedures. One is a Hodges type estimator combining the Maximum Score estimator with existing procedures. A second is a two step estimator using a Maximum Score type objective function in the second step. Lastly we propose a new random set quantile estimator, motivated by definitions introduced in \citeasnounmolchanov2006book. Extensions of these ideas for the cross sectional model to static and dynamic discrete panel data models are also provided.

Key Words: Maximum Score, Identified Set, Hodges estimator, Panel Data Discrete Choice.

JEL Codes: C14, C21, C25.

1 Introduction

The binary response model, as well as the more general class of monotone index models have received a great deal of attention in both the theoretical and applied econometrics literature. This is because as many economic variables of interest such as employment status or purchase decisions of a good are of a qualitative nature. The binary choice model is usually represented by some variation of the following equation:

| (1.1) |

where is the indicator function, is the observed response variable taking the values 0 or 1, and is an observed vector of covariates which affect the behavior of . Both the disturbance term and the vector are unobserved with the latter often being a parameter whose identification is to be characterized and then (point or set) estimated from a random sample of .

The disturbance term is restricted in ways that help characterize identification of . Parametric restrictions would specify the distribution of up to a finite number of parameters and would assume it is distributed independently of the covariates . Under common parametric restrictions, would be easily established to be point identified as long as the vector satisfies the usual rank condition. In these cases can be consistently point estimated (up to scale) using maximum likelihood or nonlinear least squares. However, except in special cases, these estimators are (point) inconsistent if the distribution of is misspecified or conditionally heteroskedastic. On the other hand, semiparametric or “distribution free” restrictions have also been imposed in the literature, resulting in a variety of identification results and estimation procedures for . One of the first and most influential estimation methods was the “maximum score” estimator proposed in \citeasnounmanski1975222Since this seminal work there have been many variations of it and many new inference procedures based on the original estimator. In addition to important work dating back to the 1990’s (e.g. \citeasnounhorowitz-sms) this also includes recent and important work in \citeasnounrosenura2022, \citeasnoungao2022, \citeasnouncattaneojansson2020, \citeasnounchenetal2014 and \citeasnounabrevayahuang2005.. In the case of binary choice the conditions in \citeasnounmanski1975 for the point identification of can be shown to be given by the conditional median restriction

| (1.2) |

as well as a smoothness and large support condition on the distribution of the index . \citeasnounmanski1975 proposed the estimator of which were the set of values maximizing the objective function333Alternative objective functions can be used. For example, one used in \citeasnounkomarova2013 is where denotes the conditional probability that . For implementability it would have to be estimated in a previous stage.

| (1.3) |

Under stated conditions, \citeasnounmanski1975 and \citeasnounmanski1985 established (point) identification of and consistency of the Maximum Score estimator444To be more precise, results in those papers focused primarily on what is now referred to as point identification and point consistency. This is in contrast what will be the focus of this paper which is set identification and set consistency. .

In a more general setting, the desirability of an estimator would be driven by its properties when the parameter is not point identified and, hence, so no point consistent estimator exists. In the model above, point identification can fail for a number of reasons, such as a lack of smoothness or a lack of a large support for . One empirically relevant setting is when all the covariates are discretely distributed555In the discrete regressor case, point identification also fails if we strengthen the median restriction in 1.2 to an independence restriction or exclusion restriction. See respective works in \citeasnounkhantamerjbes, \citeasnounmagnac-maurin08, \citeasnounkomarova2013. . This raises the question, which this paper will attempt to address, on how useful the Maximum Score estimation procedure as well as alternative estimation methods can be in this setting. To examine this we will be posing questions such as a) whether a given estimator converges to a set which is meaningful in the sense that it is a strict subset of the parameter space, and b) if that answer is affirmative, how does the set it converges to relate to the identified set? If the two sets (the limiting set of the maximum score estimator, and the identified set) are equal for all designs satisfying the model’s assumptions we will refer to the estimator as sharp. In contrast, if the answer is negative, we will pose the question of the existence of a sharp estimator for the problem at hand, and if the answer is affirmative, propose an estimator and establish its (set) consistency under stated regularity conditions.

The rest of the paper is organized as follows. In Section 2 we consider estimating the binary choice model under a very particular, but illustrative design – one where the disturbance term distribution is not parametrically specified and all the regressors are discretely distributed. It is well known that the regression coefficients in this model are generally not point identified – see, e.g. \citeasnounbierenshartog. The Maximum Score estimator will not be point consistent, so a natural question becomes how it performs as a set estimator. We first establish its asymptotic properties and establish (under stated) conditions that it converges to an outer region of the identified set666This result is similar to that found in \citeasnounkomarova2013.. This does not imply suboptimality of the Maximum score unless one can construct a procedure that does converge to the identified set.

Section 3 then proposes two new estimation procedures for a semiparametric binary choice model under the median restriction. The first relies on modifying the maximum score objective function by incorporating a data driven switching device. We show it is pointwise optimal in the sense that it converges to the identified set. The second estimator, analogous to that in \citeasnounkhan2001, effectively combines the objective functions used in \citeasnounmanski1975 and \citeasnounichimura1994 and is shown to also be optimal pointwise.

Section 4 then introduce the notion of uniform optimality in the sense of estimating the model in question under drifting designs, loosely analogous to that introduced in the unit root and weak iv literatures. The purpose of this is to explore notions of robustness of each of the procedures. Under such drifting designs, Section 5 compares procedures in a more refined fashion by establishing their rates of convergence under both fixed and drifting asymptotics.

Section 6 then extends the concepts, and introduces new procedures for partially identified panel data models, in both static and dynamic settings. Here, the central estimators which we focus discussion on to determine optimality are those proposed in [manski1987] and [honorekyriazidou].

Section 7 concludes by summarizing results and discussing areas for future research.

2 Identification and Estimation of Binary Choice Models

In this section we illustrate our main ideas by introducing the basic concepts of identification and set estimation of the binary choice models we will be working with. This will enable us to formally define our notion of optimality of estimators, including the maximum score estimator, for these models. We will define these basic concepts within the context of the binary choice model

Assume a random sample of observations drawn of the vector , with being an observed binary scalar and an observed vector of covariates. The scalar random variable is unobserved, and the unknown vector has the same dimension as and is to be estimated from the random sample.

Let be the set of regression coefficients that are consistent with the assumptions of the model, or, the identified set. Let be a set estimator for the target parameter .

We denote both the estimator and the target of estimation as sets as opposed to points in the parameter space. We do it for two reasons. First, estimators such as the maximum score are generally not single valued in finite samples. Furthermore, in discrete models such as the ones we consider, regression coefficients are often not point identified, in the sense that there are multiple values of the regression coefficients that could generate the observed data, even in arbitrarily large samples or in the whole population.

With these basic concepts we can immediately assess the property of an estimator by measuring its distance from the identified set. Following the standard practice in the set estimation literature, we work with the Hausdorff distance. For two sets in , we will denote this distance by . Formally,

where denotes the Euclidean distance between vectors and .

The notion of convergence in probability for a set estimator is naturally defined analogously to a point estimator converging in probability to a point in the parameter space.

Definition 1.

A set estimator converges in probability to if .

In this definition is also a probability limit of in the definition of convergence in probability in the random set theory (see [molchanov2006book], Definition 6.19). This definition naturally leads to the notion of optimality we will be using throughout this paper.

Definition 2.

Let be the identified set for a given model, as defined above. We say that estimator is optimal for a given model if .

Remark 1.

Our notion of optimality of an estimator in this paper is only based on its probability limit, and not, say its asymptotic variance, which is the metric often used for optimal point estimation. Despite this limitation, our notion will still be very useful when comparing or ranking competing estimators for parameters in a given model. For example, one set estimator will be preferable to another by our notion if its Hausdorff distance to the identified set converges to a strictly smaller number. This is an analogous to one point estimator being more efficient than another if its asymptotic variance is smaller.

With these definitions in hand we now can return to the binary choice model and explore the relative optimality of the maximum score (MS) estimator, \citeasnounmanski1975, focusing on situations where the regression coefficients are not point identified, such as the discrete regressors case alluded to earlier.

2.1 Maximum Score Example Discrete Design

In this section we explore the properties of the MS estimator in a simple design where the regression coefficients are not point identified. Our design is deliberately simple to illustrate the main points in this paper.

We assume a random sample of observations of the bivariate vector available to the econometrician and drawn from the model,

| (2.4) |

where are each observed binary random variables. is a fixed scalar, unknown to the econometrician and the target of estimation and inference. Further assumptions will be summarized in A1-A3 below. For now, let us make the following additional assumption which is the motivation for using the MS estimator:

Assumption A1 below will additionally imply that is strictly increasing everywhere.

In this setting the identified set, which we denote as , is the collection of such that

(The second condition uses strict monotonicty of around 0.) For this simple design we wish to establish the properties of the MS estimator for :

| (2.5) |

where denotes the parameter space.

An alternative way to define the estimator for this discrete design is as in \citeasnounkomarova2013. There, the objective function to be optimized is of the form:

| (2.6) |

where and denote, respectively, a conditional choice probability estimator and the frequency in the sample for a given :

| (2.7) |

Generally, will be a set of values, as for this design the objective function will not have a unique maximum. The question we are interested in what this set of values converges to as the sample size, denote by , gets arbitrarily large. We will also be interested in the identified set – that is, the set of values of that are consistent with the assumptions of the model, and will be the target of any estimator, including the maximum score.

To give a preview of our results, below we establish that the MS estimator is not an optimal estimator in the sense that it does not converge to the identified set in all cases. In fact, whether it does and does not depend on what the value of in the data generating process.

Before proceeding with a more technical exposition, we lay out our set of assumptions used to derive formal results.

Assumption A1.

is distributed independently of , with a positive density on the real line.

Assumption A2.

, a compact subset of the real line.

Assumption A3.

has a binary distribution and .

We now look at the identified sets and the performance of the MS estimator for various values of in DGP.

2.1.1 Case (and analogous case )

Our first theorem begins to characterize the identified set for the unknown parameter.

This result is straightforward and its proof is, therefore, omitted.

Thus, in the special case where in DGP and, hence, the conditional choice probability equals 0.5 exactly, the unknown parameter is point identified. This immediately raises two questions: 1) does the MS estimator converge to in this case, and 2) if it does not converge, is there an estimation procedure that does?

It is helpful for us define the maximum score population set , which is the set of maxima of the limiting maximum score objective function

As shown in \citeasnounkomarova2013, and are not necessarily identical and may be a superset of . In particular, this is the case for our simple design, which is shown in Theorem 2.2.

Regarding the behavior of the estimator obtained in a sample, we start with an infeasible case when are known for . A modified sample maximum score objective function then is the one where the sampling uncertainty only enters through probabilities of various values of :

| (2.8) |

Let denote the set of maximizers of (2.8). The theorem below shows that is a consistent estimator of .

Theorem 2.3 (Infeasible MS estimator).

Thus, the infeasible MS score estimator is not an optimal estimator as it converges to a superset of the identified set.

We now turn to the feasible MS estimator . Even in a large sample size will be on either side of with probabilities close to . Informally, this will result in the “fluctuations” in the values of the MS estimator. The formal result is in Theorem 2.4

Theorem 2.4 (Feasible MS estimator).

The details of what “other sets” may be are given in the proof of this theorem.

Theorem 2.4 shows that is not a consistent estimator of either or . Using the random sets theory in \citeasnounmolchanov2006book, we can find a weak limit for given in Theorem 2.5.

Theorem 2.5.

To sum up, when , the infeasible MS estimator is suboptimal and converges in probability to the superset of the identified set. The feasible MS estimator does not have either or as a probability limit. Its asymptotic behavior is best described by a distribution limit which is the random set taking the values and with equal probabilities.

While the above result shows a situation where the performance of MS estimators may be considered to be disappointing. it is important to note that this finding is only for one particular value of in the parameter space. However, by our definition of optimality even one point suffices to establish suboptimality. Nonetheless, for reasons that will be made clear later in this paper, it will prove useful to consider other values of in the parameter space.

For the situation is analogous to the case as we then have , , and where is a 0/1 binary variable taking both values with equal probability.

2.1.2 Case

It is enough to consider . We have the following result for the identified set:

The identified set is no longer a singleton. But our main question still remains – how does the maximum score estimator do? We address this in the same way as we did before.

We start by finding – the set of maxima of the limiting maximum score objective function. It is easy to see that .

Next, we establish the limit of the sequence of sets attained by the MS estimator from a finite random sample. First, we consider the case of infeasible (when conditional choice probabilities are known) and then the feasible when these probabilities have to be estimated from the sample.

For the infeasible case we have

Given that , this immediately leads to the following result.

Theorem 2.7.

Of course, we also have that as Hausdorff distance remains the same under set closures. To sum up, the infeasible maxim score converges in probability in the Hausdorff distance to the identified set, and is thus optimal in this range of parameter values.

For the feasible MS estimator we have the following result.

Theorem 2.8.

Identical arguments can be used to show optimality of the maximum score estimator for , .

Thus in one sense, maximum score is “nearly” optimal on the parameter space with and being exceptions.

3 Alternative Procedures

Results from the previous section raise the question if there exists an estimation procedure that is optimal in the sense that it converges to the identified set for all values of the parameter in the parameter space. We further explore this here by considering alternative estimation procedures to the maximum score estimator.

3.1 Two Step Closed Form Estimator

Here we consider an alternative procedure for the same binary choice model and compare its optimality properties to the Maximum Score estimator. This estimator relates directly to procedures introduced in \citeasnounichimura1994 and \citeasnounahnetal2018. They are based on the following implication of (1.1)-(1.2) (and also strict monotonicity of at 0):

Based on the above implication, their proposed estimator minimizes

where as a scale normalization, they normalized the first component of (which is the coefficient on the first regressor ) to focus on estimating remaining components denoted by . In the above equation is a weighting function estimated in first stage. This weight function assigns more weight to observations where the nonparametrically estimated choice probability is close to :

where, in a general framework, is a first stage nonparametric estimator

(in the discrete design we can simply use (2.7)).

We note this procedure is easy to implement, as it is of closed form in each stage. Thus there are no complicated optimization routines needed to construct an estimator, no matter the dimension of . Under stated conditions ensuring point identification, this estimator was shown to have desirable asymptotic properties, specifically being asymptotically equivalent to maximum score or smoothed maximum score (\citeasnounhorowitz-sms). A disadvantage compared to maximum score is that because it involves nonparametric procedures, the choice of kernel function and bandwidth sequence is required. But in this paper we are mostly concerned about its properties when the model is only partially identified as is the case when the regressors are discrete. It is this partial identification setting in which we will explore its optimality properties and compare it to the maximum score.

For expositional convenience, we focus on the simplified model (2.4) under Assumptions A1-A3. We denote the estimator obtained using the idea described above as .

We begin with the case for which we know . For this model, we have the following consistency result.

Theorem 3.1.

Suppose conditional choice probabilities are estimated as in (2.7) (or use kernel function, tuning parameter, , and a weight function where , ). Then when ,

Thus, in our simple discrete setting with the alternative estimator converges to the identified set, which is a single point. This is in contrast to the MS estimator properties in this setting described above.

Given the favorable performance of this estimator when (and analogously, when ), we are motivated to explore the performance of this estimator for cases when . Recall it was in this range of parameter values that maximum score was optimal in the sense that it converged to the identified set. Our finding is that the closed form estimator does not converge to the identified set in cases . This is formalized in the next theorem.

Theorem 3.2.

Thus, the best possible result we can achieve in these situations is for the closed form estimator to converge to a point on the boundary of the identified set. Otherwise, the limit is not defined or can be defined arbitrarily to be a point anywhere in the parameter space. To sum up, the closed form estimator is suboptimal generically – for most of the possible values in the DGP.

So far, we have shown that by our notion of optimality each of the two estimators – Maximum Score (MS) and the closed form (CF) – are suboptimal. Interestingly, their relative performances move in opposite directions of each other depending on how far the true parameter is from 0 or . It is this feature that motivates two additional approaches, discussed in the next two sections, that combine these two estimation procedures. As we will see, to make additional approaches feasible, we will need to relate the value of to the choice probability which is nonparametrically identified from the data.

3.2 Objective Function Combination

Here we consider a third procedure which combines features of the first two. Specifically, it uses the same first step nonparametric procedure of the CF estimator, but in the second step optimizes a variant of the maximum score-type objective function after replacing the dependent variable in a modified objective function with the nonparametric estimator of the choice probability. This estimator, denoted by , is defined as777An analogous 2-step rank estimator for heteroskedastic monotone index models was proposed in \citeasnounkhan2001. There assumptions were such that point identification was always attained. An estimator involving a Maximum score objective function with nonparametrically estimated regressors in the first stage was proposed in \citeasnounchenetal2014.:

| (3.1) |

where is a sequence number converging to 0 with the sample size.

Remark 2.

The above objective function can be viewed as combining features of the objective functions from the previous two estimators. In one sense it is like the MS estimator as it involves inequalities of the index function. But it also relates to the closed form objective function as it contains estimated choice probabilities. Crucially, the inequalities are weak in both directions, giving weight to the observations where the index is equal to zero. It incorporates a “slackness” tuning parameter, to ensure consistency that is uniform in both point and set identified cases.

The importance of using the slack variable 888A related slack variables idea was used in \citeasnounkomarova2013. and non-strict inequalities stems from cases when there is a regressor value occurring with a positive probability and such that . In this case, for will fluctuate around 0.5 with a positive probability. In our objective function defining , no matter what side of 0.5 such is on, as long as it is within , for large enough sample sizes it is optimal from the optimization perspective to satisfy both inequalities and , hence giving in the limit the identified set .

We now formally establish the properties of this estimator. As we did before, we separately consider the cases when (situations related to our comment in the above paragraph) and .

Theorem 3.3.

Under Assumptions A1-A3 and random sampling of the vector , suppose conditional choice probabilities are estimated as in (2.7) (or using a kernel function and tuning parameter, , .)

If and , , then

We next turn attention to the case . Now both conditional choice probabilities are bounded away from 0.5 and, hence, only condition is required to guarantee consistency.

Theorem 3.4.

Thus, the estimator obtained by optimization of the combined objective function indeed converges to the identified set for any given a certain choice of the rate of the smoothing sequence.

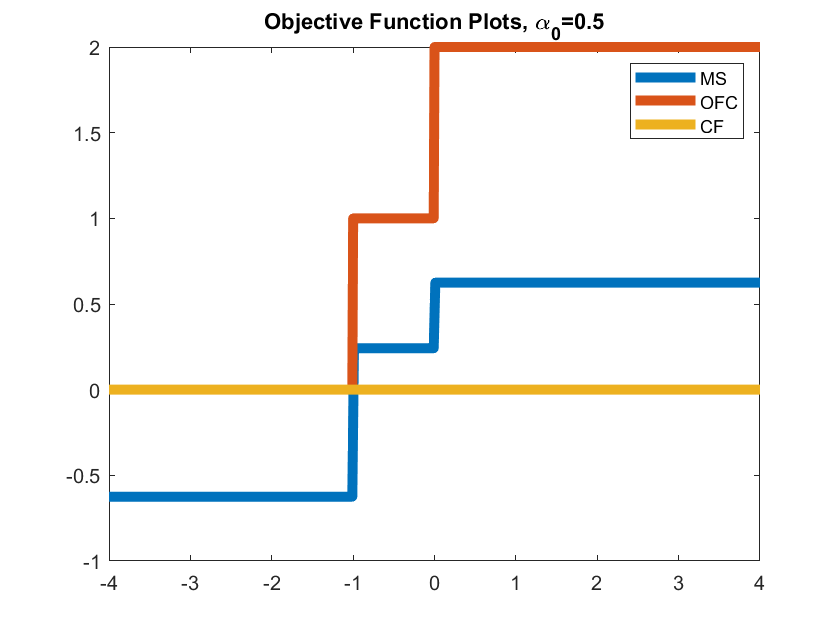

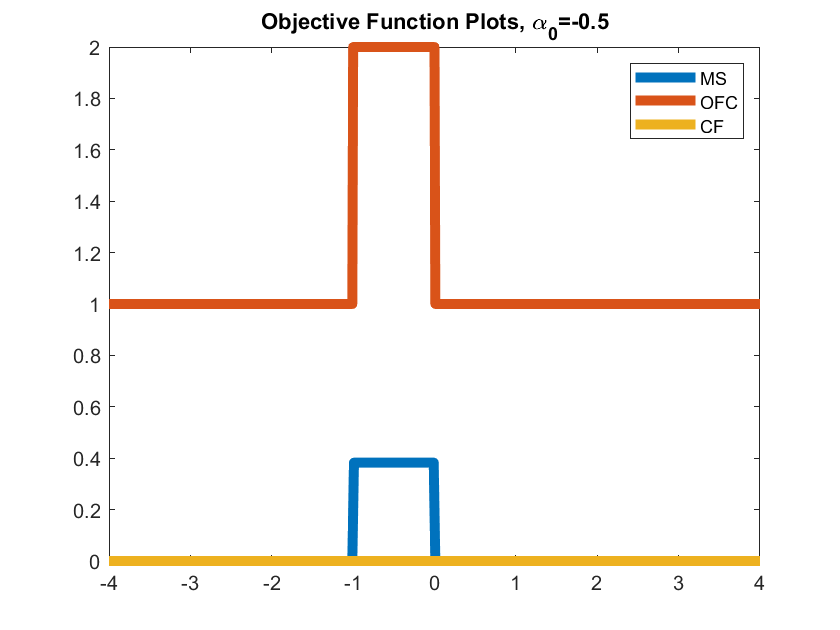

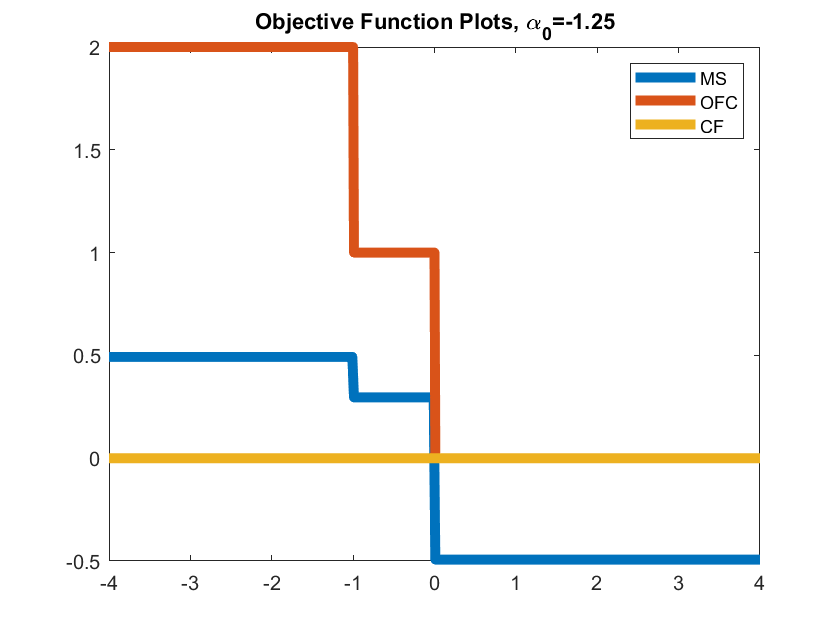

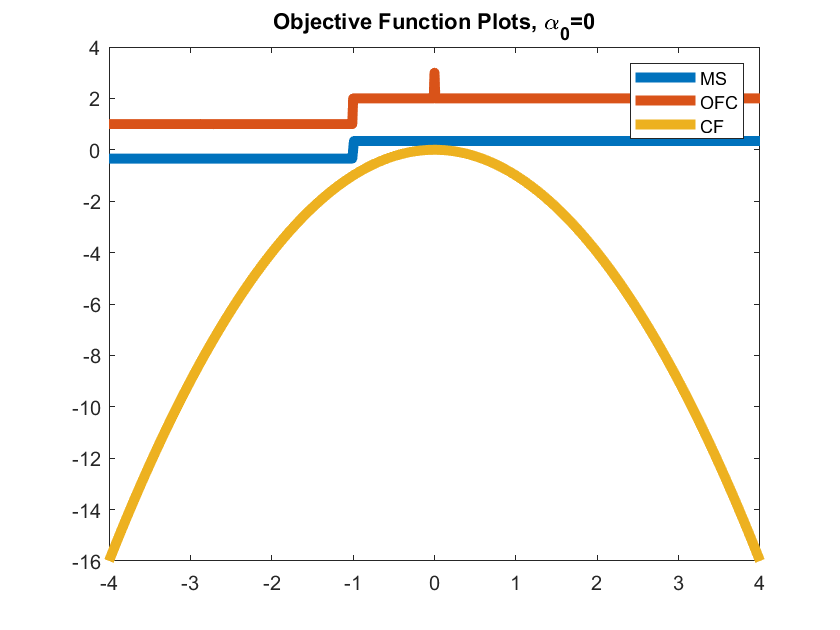

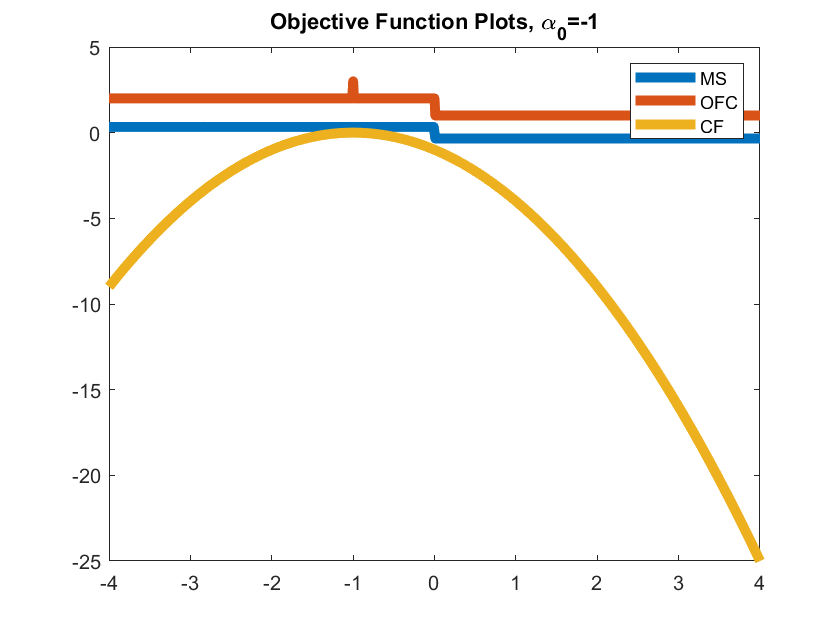

Our basic point is illustrated in Figures 1 and 2 where we plot the objective functions of the estimators discussed so far as a function of the parameter , for a series of designs which vary on how the true choice probability is from one half (and, thus, driven by what the true in DGP is). These graphs hence illustrate which procedures yield set identification and how sharp the bounds are. In the design considered, was 0/1 binomial each with probability 0.5, was standard normal, independently of . The estimators in the graphs are (infeasible) Maximum Score (MS), Closed Form (CF), and Objective Function Combination (OFC). The graphs in Figure 1 are for designs where the parameter is not point identified ( is representative of a more general , is representative of a more general , and is representative of a more general ). As we see, CF is unhelpful as it cannot even bound the parameter. The other two can, and interestingly, they both yield the same bounds, which we know are sharp from the results in \citeasnounkomarova2013.

The graphs in Figure 2 are for designs where the choice probabilities can equal one half. Here CF and OFC yield the sharpest bounds, point identifying the true parameter. MS does not, but they still provide meaningful bounds.

3.3 “Switching” Estimator

As alluded to towards the end of Section 3, the performances of the MS and CF estimators were inversely related in a certain sense. Heuristically, we found that when one performed well from the convergence in Hausdorff distance perspective, the other did not. This motivates a form of a combination estimator, that can be made feasible with a data driven selection rule.

While for now we describe it in detail only for our illustrative case with the binary regressor and the problem of identifying the intercept, the main idea will apply to the general model, as will its limiting properties.

First, from a random sample of observations of we construct nonparametric estimates of the conditional choice probabilities at each of the observations. Second, we define the minimum deviation of estimated choice probabilities from : .

Our proposed “switching” estimator is

Thus, our procedure combines the two estimators discussed in the previous sections – naturally, being far enough from zero is taken as evidence against having choice probabilities being , and being close enough from zero is supportive of the opposite case. Naturally, in the former case we can rely on the maximum score estimator and, in the latter case, on the closed form estimator. may be a point estimator or a set estimator in finite samples, depending on the data generating process. Theorem 3.5 establishes one of its desirable limiting properties.

Theorem 3.5.

Thus we see that the switching estimator is sharp in the sense that for each value of in the parameter space, it converges in probability to the identified set. As alluded to previously, we refer to this property as optimal.

3.4 Random Set Quantile Estimator

In this section we outline another approach that can potentially be used as a basis for constructing a consistent estimator of the identified set. It is based on random set theory which has been used in Econometrics since the seminal work in \citeasnounberesteanumolinari2008. Econometric papers, however, for identification analysis and subsequent estimation methodology, have primarily focused on the notion of selection (or, equivalently, Aumann) expectation from that theory and its estimators (also see further work in \citeasnounberesteanumolchanovmolinari2011) and \citeasnounBERESTEANU201217). Here for the models at hand, we work with a completely different notion.

We develop and describe our random set theory based method for our simple case of the discrete regressor design. Following the definition of the -th quantile of a random set in \citeasnounmolchanov2006book (p.176), in our simple example we propose to use a quantile of the closure of as an estimator, where . Note that this notion from \citeasnounmolchanov2006book also applies to vector settings.

To motivate this approach, consider the maximum score estimator when . As shown earlier, fluctuates mainly between two sets – and each with a probability strictly less than 1/2 in a sample but approaching 1/2 as . In a sample, other finite number of sets are possible with strictly positive probabilities which all approach 0 as (details are in the proof of Theorem 2.4).

That means that if we take the ’s quantile of the closure with , , then it consists of only for large enough and, thus, converges in probability to the identified set. If, on the other hand, we take the ’s quantile of with , , then for large enough it is which is an outer region of the identified set and, as discussed above, is the maximand of the population maximum score objective function. With , the quantile of for large enough can be shown to be the two-element set and, thus, it does not recover the identified set asymptotically.

Our formal result if given in Theorem 3.6.

Theorem 3.6.

To facilitate a deeper understanding of the concept of random set quantiles, we can draw parallels to voting rules. Let’s begin by examining the median of a random set within the context of our illustrative example.

Imagine an infinite number of random samples of a fixed size . Each sample casts votes for any number of elements of that maximize the maximum score objective function for the given sample. Equivalently, a given sample votes for its respective maximum score estimate . After the application of the closure operator , majority winners are selected – namely, those elements in that are voted for by at least 50% of the samples. The collection of those majority winners would give us . For any arbitrary index , the quantile comprises those elements from that adhere to the ’quota rule’ with a threshold of . In simpler terms, these elements within must garner votes from at least of the samples to be included.

Feasible version of the random set quantile estimator

The estimator is infeasible due to the unavailability of ’s distribution within the sample. Central to the issue is our capacity to compute a viable sample quantile for a random set. This challenge assumes heightened complexity within scenarios characterized by the estimations delineated earlier for the case . In such instances, the sample presents not fluctuating variations, but a singular set —- either or (other sets can be realized with a decreasingly small probability). Consequently, we are pressed to artificially introduce fluctuations via suitable sampling techniques. Simultaneously, these methods must be engineered in a manner that their impact on cases of where remains inconsequential.

In the context of our simple, discrete design, we rely on the interpretation of as the solution set obtained in (2.6). We propose a sampling techniques that will draw , , for each .

Of course, we know that for each ,

so it may seem natural to draw from . However, if , then this symmetric way of drawing on both sides of will give an advantage to one of the sets from or – if , then the majority of will be above as well while we need them to appear in approximately similar proportions on both sides of . This leads us to proposing an asymmetric sampling technique.

Namely, if , then

and if , then

The value of is chosen based on the design/DGP and may depend on the desired quantile index as well as probabilities of such that .

Then we consider

| (3.2) |

ids then estimated by taking a sample -quantile based on the sample of .

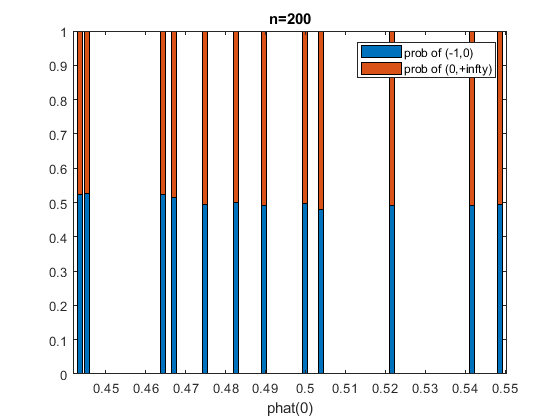

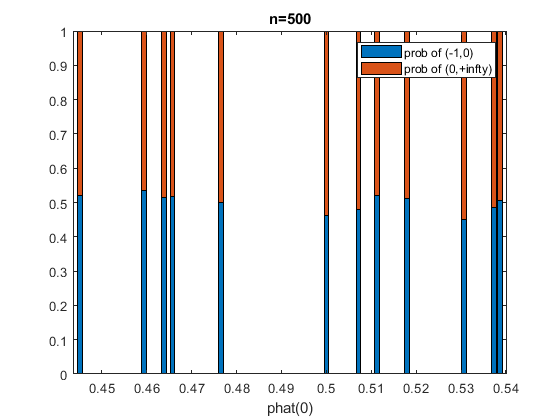

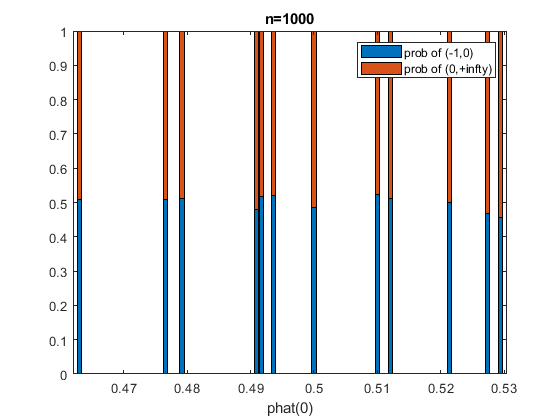

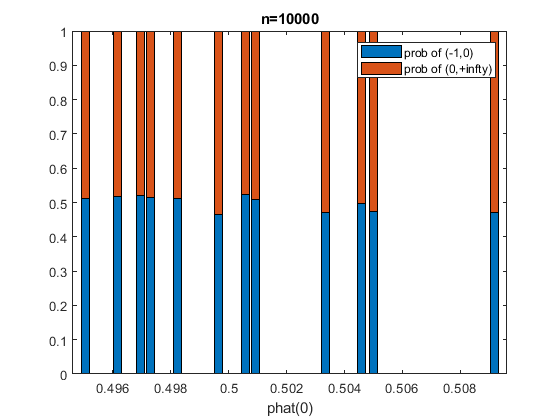

Simulation experiment for feasible quantile random set estimator.

Consider in our simple design. Then and . Let and with . We choose sample sizes . , and . Figure 3 is representative of the results we get for this case. The illustrations in Figure 3 are for 12 different realizations of in the sample. The blue vertical bars represent probabilities with which (or its closure or a half-closure) is , and the red vertical bars represent probabilities with which (or its closure) is . Even though for graphical quality we chose to limit our illustration to 12 different realizations of , the patterns we see in those graphs are representative of what would happen for other realizations of . In particular, we conclude that if we take , then the th sample quantile of the closure of the maximum score estimand is with an extremely high probability. Namely, for 1,000 different random sample of size (and, hence, potentially for 1,000 different realizations of ) only in 2.2% cases the sample th quantile obtained in the described above way is a strict superset of . For 1,000 different random sample of size it is 1.7%. For 1000 different random sample of size it is 2.2%. For 1,000 different random sample of size it is 2%. If we slightly increases the quantile index and take , then all these percentages for all mentioned are 0.

In the final comment we note that infrequently may be drawn outside of their natural range,. In this case, one may want to consider

instead of (3.2) but this dos not change our conclusions in any way.

4 Drifting Parameters in Binary Choice Model

An important additional desirable property of estimators is the local robustness expressed as continuity of their limit with respect to the parameter of interest and nuisance parameters. The example of the Hodges’ estimator999For important work on properties of the Hodges estimator, see for example \citeasnounLeebPots2005,\citeasnounLeebPots2006,\citeasnounLeebPots2008. when compared to MLE illustrates the role of continuity of the limit of an estimator for choice of the estimator used in practice. We use the same principle to evaluate the estimators we considered previously. We do so in the context of our simple example, with a single binary regressor whose coefficient is normalized to 1 and the parameter of interest being the intercept term.

The structure of the identified set for the parameter of interest can be viewed as determined by the probability where leads to point identification of while whenever the target parameter is partially identified. As a result, we approach the question of robustness of the estimators for the identified by analyzing their limits along the sequences of data generating processes where probability varies with the sample size and approaches in the limit.101010Alternatively, we can view this as the continuity of the limit along the sequences of values for parameter itself approaching while the distribution of the idiosyncratic error remains fixed.

An important question is the selection of the rate of drifting for the sequence For the model we consider the focal case where and the parameter of interest is point identified. We then consider the sequence of population distributions indexed by a sequence of probabilities

| (4.1) |

and we analyze the limits of our estimators along this sequence of distributions. Because , (4.1) automatically implies that

| (4.2) |

Consequently, are drifting too: .

We selected this drifting rate by using an alternative interpretation of the maximum score estimator as an ensemble of weak learners (e.g., see section 10.1 in [shalev:14]).

The maximum score objective function can be viewed as an aggregation of “votes” where each observation casts a vote for one of the sets and To see this, consider a single element of the maximum score objective function

For each possible combination the element of the objective function selects the intervals and

We can then interpret this element as a classifier (a “weak learner” in the terminology of the Machine learning literature) which can select one of the sets and or their pairwise unions. For the pairwise union, the classifier selects each set in the union.

Then a classifier corresponding to observation selects and with probability and with probability with probability and and with probability The machine learning literature calls such a classifier a “weak learner” because the probability that it classifies the object of interest correctly is not diminishing in larger samples. We consider the concept of the weak learner in context of partial identification, novel to the machine learning literature.

Let be a three-dimensional vector with elements depending on whether the corresponding set (for each of the three dimensions) was selected by observation Then produces a vector of collective “votes” of classifiers for each observation and the maximum score estimator can be written as Note that this interpretation of the maximum score estimator as an aggregator of “votes” is distinct from voting parallels in the discussion of random set quantiles. The key difference is that in case of the random set quantile the “votes” were cast by samples whereas here “votes” are cast by individual observations within a given sample.

The estimator is a function of the sample mean converging at the standard parametric rate to a normal random variable. For the analysis of continuity of distribution limit of such parameters the literature (e.g., [ibragimov], [Lecam1953]) suggest considering sequences of the population distributions of the underlying random variable with its expectation drifting at the same parametric rate. Since the expectation of the random vector is linear in the probability sequences of probabilities drifting at rate will result in an equivalent drifting of the expectation of at that rate.

One could think of other reasons to consider drifting rate for the parameter. Since the behavior of the estimators we consider is purely driven by the asymptotic behavior of (and in a lesser way by that of ), we note that the rate of is the supremum of all the monotonic rates leaving the asymptotic distribution of (and that of unchanged).

4.1 Maximum Score Estimator

We first turn attention to the MS estimator. When is the truth, the maxima of the population maximum score objective function is denoted as , the infeasible maximum score estimator from a sample of size with known is denoted as and the feasible maximum score estimator with estimated is denoted as .

Based on our results in Section 3, it is straightforward to see that under Assumption A1-A3, we have , and

An immediate consequence is that

The performance of the feasible estimator is analyzed in Theorem 4.1.

Theorem 4.1.

Under Assumptions A1-A3, random sampling, and (4.2), we have

where is a binary random variable taking the value of 0 with probability .

In particular, this implies that

One implication of Theorem 4.1 is that parameter drifting in this case can bridge two regimes. One regime is the one where asymptotically the feasible MS estimator fluctuates with equal probabilities between sets and (corresponds to ). This regime describes the behavior of the maximums score estimator without drifting which we earlier established in Theorem 2.3. The second regime is where the maximum score estimator effectively coincides with the set with probability 1 (corresponds to ) which is a desirable case from the perspective of the behavior under drifting.

To summarize, as varies from to the distribution of the random set varies from equal randomization between and to selecting a fixed set Thus, this choice of the drifting sequence indeed bridges the two cases.

Based on our results in this section, one can conclude that maximum score satisfies certain uniformity properties. Based on this, we pose the question on whether this type of uniformity should be incorporated in the definition when ranking set estimators, analogous to MLE being optimal in point estimation.

We next explore the properties of both the two-step closed form procedure and combination procedures under drifting parameter sequence.

4.2 Two-step Closed Form procedure

Let denote the closed form estimator obtained from a sample when is the truth. We have the following theorem:

4.3 Objective Function Combination Estimator

Let denote the estimator defined as in (3.1) with as the truth.

Thus, as we can see, the OFC estimator and the identified setdo not get arbitrarily close in probability in terms of the Hausdorff distance.

4.4 Switching Estimator

Let denote the “switching” estimator with as the truth:

We have the following theorem.

Proofs of this result and others pertaining to the switching estimator under drifting asymptotics can be found in Section I. The main conclusion is that the switching estimator does not get arbitrarily close to under drifting.

Remark 3.

From the perspective of the uniformity properties, the original maximum score estimator has better performance than the other three discussed. The closed form, the OFC and the “switching” estimators have poor uniform properties. Interestingly, the very attributes that enable their effectiveness in specific point-identified cases, such as , are also responsible for their weaker performance in terms of uniformity.

4.5 Random set quantile estimator

Our last result in Section 4 is on the behavior of the quantile of the closure of the MS estimator with the MS estimator being treated as a random set and, hence, with the notion of the quantile applied from the random set theory (see \citeasnounmolchanov2006book). Just as in Section 3, for simplicity we focus on the infeasible quantile estimator which under the drifting sequence (4.1) is denoted as , Theorem 4.5 below establishes the asymptotic behavior of the Hausdorff distance between and .

Theorem 4.5.

Thus, we see this estimator has desirable properties under drifting sequences in the sense that it gets arbitrarily close to . Recall that it was also optimal without drifting. While this estimator is infeasible, a consistent estimator of this quantile (see our proposed approach earlier3.6) would also have this properties.

5 Rates of Convergence

In this section, for each of the estimators introduced previously, we will establish its rate of convergence under both point and set identification and under fixed and drifting asymptotics. The purpose here is to further refine our comparison of the various procedures, as the previous section only determined if they were consistent or not. To illustrate these main points here we continue to consider the simple design with one binary regressor, only the intercept parameter to be estimated, and the disturbance term following a standard normal distribution. Recall that in that setting the the parameter was point identified when it was or and set identified otherwise.

5.1 Maximum Score Estimator

We first consider the limiting distribution theory for the maximum score estimator in our simple design. Under conditions when the parameter is point identified and the maximum score estimator is consistent, [kimpollard] established both the rate of convergence and limiting distribution of the estimator. However, that does not apply here in the simple design. Recall that even when the parameter is point identified, the maxima of the limiting maximum score objective function may be a set. Its limiting distribution theory can be characterized by Theorems 5.1-5.3, with the last one corresponding to local to zero asymptotics.

To analyze point identified cases, it is enough to consider (case is analogous), and to analyze set identified cases it is enough to consider (cases , are analogous).

Thus, in the point identified case , the infeasible converges at an arbitrary fast rate to the maxima of the limiting maximum score objective function, which is and is an outer set of the identified set. An analogous result does not apply to the feasible maximum score estimator since, as shown before, it does not converge in Hausdorff distance in probability either to or .

Thus, in set identified cases both and converge to at an arbitrarily fast rate.

Finally, we consider what happens under the drifting sequence. The previous section focused on the case when and the drifting sequence satisfies (4.2). More generally, for any we can consider such that

| (5.1) |

Theorem 5.3 establishes the rate of convergence of for .

Theorem 5.3.

In this section instead of , we can take any function of that grows to with .

5.2 Closed Form Estimator

For the limiting distribution of the closed form estimator, we note the first step properties are particularly easy to determine in the discrete design, as regressors can simply be put into cells so there are no bandwidth conditions to consider. Recall this estimator had an “all or nothing” property pertaining to if we had point identification or not. This feature is also reflected in the limiting distribution theory, as demonstrated in Theorems 5.4-5.5, the latter of which is for drifting asymptotics.

Theorem 5.4 established that in the case of point identification the closed form estimator converges to the identified set arbitrarily fast.

When , then diverges, as established in Theorem 3.2 so there are no additional results for this case.

Finally, Theorem 5.5 considers the drifting asymptotics. It shows that for any drifting sequence (5.1), the closed form estimator constructed for as the truth, does not get close to the identified set .

The case of was considered in Theorem 4.2 (case is analogous). Theorem 5.5 considers any . Even though, for there are smoothing sequences under which , an analogous result does not hold for .

Theorem 5.5.

Let . Then

Let . Then for any ,

Thus, Theorem 5.5 confirms that the closed form estimator has poor uniformity properties and is never close to under drifting.

5.3 Objective Function Combination Estimator

In Theorem 5.6 we consider the case of no drifting and establish the arbitrary rate of convergence to the identified set for feasible .

Theorem 5.7 considers the drifting design.

Theorem 5.7.

If , then for any , .

If , then .

The result of Theorem 5.7 establish the arbitrary rate of convergence to the identified set obtained treating when parameters are drifting to the parameter resulting in a set identified case. However, as established earlier in Theorem 4.3, sets and do not get close to each other in Hausdorff distance when parameters are drifting to the value corresponding to the point identified case.

5.4 “Switching” estimator

Our first result in Theorem 5.8 is for the case of no drifting. Theorem 5.9 shows the performance of the “switching” estimator obtained when is the truth.

5.5 Random set quantile estimator

We first consider teh fixed design and establish that the random set quantile estimator , , (for simplicity, we focus on this infeasible estimator) converges to arbitrarily fast.

6 A Ranking of the estimators

After conducting a comprehensive analysis of the estimators under the influence of drift, we are now able to propose a ranking system based on their uniformity properties.

Our findings reveal that among the estimators considered —- namely, OFC, “switching”, and quantile random sets estimators – each exhibits sharp pointwise characteristics. Conversely, both the Ichimura and Maximum Score estimators lack this pointwise sharpness, and interestingly, they demonstrate poor performance in diametrically opposite scenarios.

Regarding the uniformity properties, we can rank the quantile random set estimator as most robust because for any constant in the drifting rate (4.1) we can find a range of quantile indices for which it has good uniformity properties. We can rank Maximum Score as second best because one can get arbitrarily close to good uniform properties by selecting a very large drifting constant in (4.1).

OFC and “switching” estimators are next in the ranking as they have similarly inferior uniformity properties. It is hard to craete a rank between themselves as in their pointwise behavior they have same robustness properties to mistakes made in the rates of the nuisance parameter sequences.

To clarify this point further, the OFC estimator remains informative even when fails the condition . Suppose e.g. that . Then in our focal cases the OFC estimator will behave exactly like the feasible maximum score estimator fluctuating with equal probabilities between two sets. Suppose e.g. that . Then in our focal cases the OFC estimator will behave by fluctuating among three sets – and the two sets from the asymptotic maximum score behaviors. The limiting probabilities in these fluctuations will be determine by . The choice of increasingly large will result in the probability assigned to in the fluctuations to be increasingly close to 1. The choice of increasingly small will result in the probability assigned to in the fluctuations to be increasingly close to 0 and the estimator essentially becoming the feasible maximum score estimator.

Similarly, the “switching estimator” retains its informativeness even when the choice of violates the condition . Should approach zero, the “switching” estimator becomes the feasible maximum score estimator. Conversely, if tends towards a positive finite constant designated as , and , the “switching” estimator fluctuates among three sets: and the two sets characteristic of asymptotic feasible maximum score behavior. The probabilities assigned to these fluctuations are determined by the value of , with larger values of driving the probability assigned to closer to 1, while smaller values of result in this probability approaching 0, essentially transforming the estimator into the feasible maximum score estimator in the latter case.

Lastly, we note the Ichimura (closed form) estimator occupies the lowest position in our ranking due to its complete lack of informativeness when all choice probabilities deviate from , even by an arbitrarily small amount.

7 Binary Panel Data Model

In this section we consider the identification of a binary choice model with fixed effects. \citeasnounanderson70 considered the problem of inference on fixed effects models from binary response panel data. He showed that inference is possible if the disturbances for each panel member are known to be white noise with the logistic distribution and if the observed explanatory variables vary over time. Nothing need be known about the distribution of the fixed effects and he proved that a conditional maximum likelihood estimator consistently estimates the model parameters up to scale. Interestingly, recent work demonstrates how crucial the logistic distribution assumption is for point identification and consistent estimation. \citeasnounchamberlain2010 shows that when the observable covariates have bounded support, the logistic assumption on an unobserved component is necessary for point identification.

manski1987 showed that identification of the regression coefficients remains possible if the disturbances for each panel member are known only to be time-stationary with unbounded support and if the observed explanatory variables vary enough over time and have large support.

Specifically, he considered the model:

| (7.1) |

where . The binary variable and the -dimensional regressor vector are each observed and the parameter of interest is the dimensional vector . The unobservables are , and , the former not varying with and often referred to as the “fixed effect” or the individual specific effect. \citeasnounmanski1987 imposes no restrictions on the conditional distribution of conditional on . \citeasnounmanski1987 proposed the conditional maximum score estimator to estimate up to scale. He defined this estimator as the maximizer of the objective function

| (7.2) |

In establishing its asymptotic properties, \citeasnounmanski1987 imposed the following conditions:

-

1.

for all .

-

2.

The support of is .

-

3.

Let . Then the support of does not lie in proper linear subspace of .

-

4.

There exists at least one such that and , the component of , is distributed continuously with support on the real line conditional on the other components of .

-

5.

The sample is i.i.d.

We note the 4th condition will be violated if all the regressors are discrete. This prompts an inquiry into the properties of the conditional maximum score estimator within this particular context. Notably, as we will show, in certain scenarios this estimator tends to converge towards an outer region of the identified set.

Let represent the support of , characterized by a finite set of points. To provide further clarity on the observed lack of sharpness,we reframe the population maximum score objective function as follows:

This formulation mirrors the work of Manski (1987). However, it is essential to acknowledge that the cases where , which play a vital role in pinpointing the parameter of interest in the formal identification approach

are omitted from the population maximum score objective function. Consequently, this leads to the issue of the sharpness of the maximum score estimation approach.

To follow up on our remark, let us consider an illustrative design in this panel data case.

Static panel illustrative design. Let and let , , have the support of , and have the support . Let be independent of . Take . Then

are the equalities that drive the identification of (we would have the same equalities if we additionally conditioned on ) as they imply that

where denote the first and second components of , and, together with the normalization restriction will imply that , thus indicating that the identified set (in ) is .

The population maximum score objective function will have zero entry corresponding to in Cases A and B above. It will have non-zero entries only for the following cases: (i) , , (ii) , , (iii) , , (iv) , , (v) , . This objective function will thus be maximized at that satisfy the following inequalities:

with the normalization we get the following argmax (in ) of this objective function: which is a superset of the identification set . This, once again, illustrates a lack of sharpness in the infeasible/population maximum score estimation.

As was the case in the cross sectional case, one can also consider a two- step closed form estimator for the panel data model that is analogous to \citeasnounichimura1994. To see how, construct the random variable

for , and define analogously. Let denote and define analogously. Identification and estimation of up to scale would be based on

| (7.3) |

where denotes . To construct an estimator based on 7.3, let denote kernel regression estimators of . From these kernel weights could be constructed as

where is a kernel function, and is a bandwidth. With these weights one could estimate , the last components of by weighted least squares of the first component of denoted by on the remaining components, denoted by .

With these estimators defined one can proceed to easily define estimators analogous to those defined in previous sections of this papers. For example one can define a combination (Hodges) estimator, an objective function combination estimator, and a median random set estimator, all in the panel data setting.

We are able to show analogous results for the panel data setting as those we found in the cross sectional setting. Specifically, using identical arguments, we are able to show:

-

1.

Neither the conditional maximum score nor the closed form estimator estimators are sharp, though the conditional maximum score estimator is robust.

-

2.

The combination (Hodges) estimator is sharp but not robust compared to the conditional Maximum Score estimator.

-

3.

An analogously defined combination objective function and median random set estimators are both sharp but only the latter is robust.

Formal statements of these results and their proofs are delegated to the appendix, Section G.

7.1 Dynamic Binary Panel Data Model

Here we consider the binary dynamic panel data model that relates the outcome in period for individual , , to its lagged value in the following way

| (7.4) |

Here we are interested in learning about . This is treated as a fixed (but unknown) constant vector while the unobservables here take the standard form where is an individual specific and time independent “fixed effect,” and is meant to capture the systematic correlation of the unobservables over time while is an idiosyncratic error term that is both time and entity specific. The parameter is of special interest as it measures the effect of state dependence.

In econometric theory, the literature that has studied this model is vast the theoretical results we will focus on here are in \citeasnounhonorekyriazidou, who proposed an estimator based on a conditional maximum score objective function.

They assumed the the binary dependent variable is observed for 4 time periods () and the regressors are observed for 3 periods (). They defined their estimator as , the maximizer with respect to of the objective function:

| (7.5) |

where denotes a kernel function and denotes a bandwidth sequence whose properties are detailed below, and . Where, following their notation, variables with double subscripts denote time differences: e.g, , and .

To establish the (point) consistency of this estimator they imposed the following conditions

-

1.

is distributed independently of and independently across time with a cdf that is strictly increasing on the real line for all

-

2.

There exists a component of , denoted by s.t. , and the corresponding component of is continuously distributed with positive density on the real line, conditional on the remaining components of and conditional on lying in a neighborhood of 0.

-

3.

The support of conditional on in a neighborhood of zero is not contained in any proper linear subspace of

-

4.

The random vector is absolutely continuously distributed with density that is bounded from above on its support and strictly positive in a neighborhood of zero.

-

5.

For all , is continuously differentiable on its support with bounded first order derivatives.

-

6.

The kernel function is a function of bounded variation that is bounded from above and below and integrates to 1.

-

7.

The bandwidth sequence is a sequence of positive numbers that satisfies and

We note here two crucial conditions for their point identification results. One is continuity of one of the regressors in each of the time periods. This is not surprising as it was required for the static binary panel data model as well. The other is an overlap support condition- specifically they assume111111Such a condition is not necessary for identification- see recent work by \citeasnounKPT2022. that each component of has support that overlaps with the corresponding component of . To relate our results in this section to those found in previous sections of this paper we will maintain the overlap support condition in \citeasnounhonorekyriazidou, but assume has discrete support. Consequently, we will assume that and redefine the objective function as

| (7.6) |

In this dynamic panel data case we can present a illustrative design in the spirit of illustrative designs earlier to establish lack of sharpness of \citeasnounhonorekyriazidou estimator when we consider the case of discrete regressors.

Dynamic panel illustrative design. Let and let have the support , and let have the support . Let be independent of . Let be independent across time and have strictly increasing c.d.f.. Take and . Suppose the distribution of the initial is independent of .

Denote

Then

Take and . Then

and, clearly,

This implies immediately the following identifiability restriction which takes the form

| (7.7) |

Analogously,

This implies the following identifiability restriction

| (7.8) |

Together with the normalization , restrictions (7.7) and (7.8) are enough to conclude that the identified set is a singleton .

The population Honore-Kyriazidou objective function will have zero entry corresponding to cases

This is because in these cases

thus resulting in

This is analogous to what was happening in the maximum score estimation in the illustrative design there – cases driving point identification of the parameter of interest were ignored by the population maximum score objective function.

Let us now construct the set of that will maximize the population Honore-Kyriazidou objective function in our design.

Suppose, for example, that is also 0/1 variable. Then we have the following system of inequalities defining the maxmimzer of the population Honore-Kyriazidou objective function:

This set is a subset of . With the normalization we obtain

Removing redundant inequalities it is

The solution set to these inequalities can be described as

This set includes and as an interior point (take and in the description of the set). Thus, the maximizer of the population Honore-Kyriazidou objective function is a (unbounded) superset of the identified set. This maximizer is displayed in Figure 4.

If we look at the maximizer of the sample Honore-Kyriazidou objective function, then analogously to the cross sectional case, this maximizer will fluctuate among a finite number of disjoint sets with probabilities bounded away from zero and one. Each of such sets will have the truth and at the boundary and the union of all such sets will give the described above maximizer of the population objective function (again, analogous to our illustrative example in the cross sectional case). We can once again show that the random set quantile of the feasible estimator for quantile indices strictly above will give the truth and for large enough sample sizes.

We can show analogous results for the dynamic panel data setting to those found in the static panel and cross sectional setting. Specifically,

-

1.

The dynamic conditional maximum score is not sharp nor is a closed form analogous estimator, though the dynamic conditional maximum score estimator is robust.

-

2.

An analogous combination (Hodges) estimator is sharp but not robust compared to the weighted conditional Maximum Score estimator for the dynamic model that was proposed in \citeasnounhonorekyriazidou.

-

3.

An analogous dynamic combination objective function and a dynamic median random set estimator are both sharp but only the latter is robust.

Formal statements of these results and their proofs are delegated to the appendix.

8 Conclusions

In this paper we further explored the notion of optimal estimation of regression coefficients in binary choice models. Here our notion of optimality pertains to, but is a refined notion of estimating the sharp set. As pointed out in \citeasnounkomarova2013, who establishes the form of the identified set for the binary choice model introduced in \citeasnounmanski1975, the maximum score estimator introduced in that paper converges to an outer region of the identified set and is hence suboptimal. We propose several novel estimators which are optimal by that notion. Two are combination estimators- the first employs a data driven switching method to adaptively choose between the maximum score estimator and a closed form estimator introduced in \citeasnounichimura1994. The second combines the objective functions employed in the two estimators, as opposed to the estimators themselves. We prove that each procedure converges to the identified set. A third estimator we propose is referred to as a random set quantile (RSQ) estimator which we show is also optimal. Then similar ideas are used to study binary choice panel data models. Here we propose new estimators that converge to the identified sets in both static and dynamic models, in contrast to existing procedures often used in the literature.

Our work here leaves open areas for future research. There are several nonlinear models of wide interest from both theoretical and empirical perspectives which suffer from the same identification issues as the ones studied in this paper. One example is the class of discrete response models under independence restrictions, which we elaborate on in the Appendix in Section E. But there are many more which need to be explored, such as ordered, multinomial response and simultaneous discrete response models. Procedures based on maximum score or rank regression which have analogous suboptimal properties have been proposed in \citeasnounmjleeordered, \citeasnounkotmultinomial, \citeasnounabrevhaus. We aim to show in future work that our procedures introduced here can result in optimal estimation for those models as well.

References

- [1] \harvarditem[Abrevaya, Hausman, and Khan]Abrevaya, Hausman, and Khan2010abrevhaus Abrevaya, J., J. Hausman, and S. Khan (2010): “Testing for Causal Effects in a Generalized Regression Model with Endogenous Regressors,” Econometrica, 78, 2043–2061.

- [2] \harvarditem[Abrevaya and Huang]Abrevaya and Huang2005abrevayahuang2005 Abrevaya, J., and J. Huang (2005): “On the Bootstrap of the Maximum Score Estimator,” Econometrica, 73, 1175–1204.

- [3] \harvarditem[Ahn, Ichimura, Powell, and Ruud]Ahn, Ichimura, Powell, and Ruud2018ahnetal2018 Ahn, H., H. Ichimura, J. L. Powell, and P. A. Ruud (2018): “Simple Estimators for Invertible Index Models,” Journal of Business and Economic Statistics, 36, 1–10.

- [4] \harvarditem[Andersen]Andersen1970anderson70 Andersen, E. (1970): “Asymptotic Properties of Conditional Maximum Likelihood Estimators,” Journal of the Royal Statistical Society, 32(3), 283–301.

- [5] \harvarditem[Beresteanu, Molchanov, and Molinari]Beresteanu, Molchanov, and Molinari2011beresteanumolchanovmolinari2011 Beresteanu, A., I. Molchanov, and F. Molinari (2011): “Sharp Identification Regions in Models With Convex Moment Predictions,” Econometrica, 79(6), 1785–1821.

- [6] \harvarditem[Beresteanu, Molchanov, and Molinari]Beresteanu, Molchanov, and Molinari2012BERESTEANU201217 (2012): “Partial identification using random set theory,” Journal of Econometrics, 166(1), 17–32, Annals Issue on “Identification and Decisions”, in Honor of Chuck Manski’s 60th Birthday.

- [7] \harvarditem[Beresteanu and Molinari]Beresteanu and Molinari2008beresteanumolinari2008 Beresteanu, A., and F. Molinari (2008): “Asymptotic Properties for a Class of Partially Identified Models,” Econometrica, 76(4), 763–814.

- [8] \harvarditem[Bierens and Hartog]Bierens and Hartog1988bierenshartog Bierens, H., and J. Hartog (1988): “Non-Linear Regression with Discrete Explanatory Variables, with an Application to the Earnings Function,” Journal of Econometrics, 38(3), 269–299.

- [9] \harvarditem[Cattaneo, Jansson, and Nagasawa]Cattaneo, Jansson, and Nagasawa2020cattaneojansson2020 Cattaneo, M., M. Jansson, and K. Nagasawa (2020): “Bootstrap Based Inference for Cube Root Asymptotics,” Econometrica, 88, 2203–2219.

- [10] \harvarditem[Chamberlain]Chamberlain2010chamberlain2010 Chamberlain, G. (2010): “Binary Response Models for Panel Data: Identification and Information,” Econometrica, 78, 159–168.

- [11] \harvarditem[Chen, Lee, and Sung]Chen, Lee, and Sung2014chenetal2014 Chen, L.-Y., S. Lee, and M. Sung (2014): “Maximum Score Estimation with Nonparametrically Generated Regressors,” Econometrics Journal, 17, 271–300.

- [12] \harvarditem[Gao and Xu]Gao and Xu2022gao2022 Gao, Y., and S. Xu (2022): “Two-Stage Maximum Score Estimator,” University of Pennsylvania Working Paper.

- [13] \harvarditem[Han]Han1987MRC Han, A. (1987): “The Maximum Rank Correlation Estimator,” Journal of Econometrics, 303-316.

- [14] \harvarditem[Hoeffding]Hoeffding1963hoeffding1963 Hoeffding, W. (1963): “Probability Inequalities for Sums of Bounded Random Variables,” Journal of the American Statistical Association, 58(301), 13–30.

- [15] \harvarditem[Honore and Kyriazidou]Honore and Kyriazidou2000honorekyriazidou Honore, B., and E. Kyriazidou (2000): “Panel Data Discrete Choice Models with Lagged Dependent Variables,” Econometrica, 68, 839–874.

- [16] \harvarditem[Horowitz]Horowitz1992horowitz-sms Horowitz, J. (1992): “A Smoothed Maximum Score Estimator for the Binary Response Model,” Econometrica, 60(3).

- [17] \harvarditem[Ibragimov and Has’ Minskii]Ibragimov and Has’ Minskii1981ibragimov Ibragimov, I. A., and R. Z. Has’ Minskii (1981): Statistical estimation: asymptotic theory. Springer.

- [18] \harvarditem[Ichimura]Ichimura1994ichimura1994 Ichimura, H. (1994): “Local Quantile Regression Estimation of Binary Response Models with Conditional Heteroskedasticity,” University of Pittsburgh Working Paper.

- [19] \harvarditem[Khan]Khan2001khan2001 Khan, S. (2001): “Two Stage Rank Estimation of Quantile Index Models,” Journal of Econometrics, 100, 319–355.

- [20] \harvarditem[Khan, Ouyang, and Tamer]Khan, Ouyang, and Tamer2021kotmultinomial Khan, S., F. Ouyang, and E. Tamer (2021): “Inference on Semiparametric Multinomial Response Models,” Quantitative Economics, 12, 743–777.

- [21] \harvarditem[Khan, Ponomareva, and Tamer]Khan, Ponomareva, and Tamer2022KPT2022 Khan, S., M. Ponomareva, and E. Tamer (2022): “Identification of Dynamic Binary Response Models,” Journal of Econometrics, forthcoming.

- [22] \harvarditem[Khan and Tamer]Khan and Tamer2018khantamerjbes Khan, S., and E. Tamer (2018): “Discussion of “Simple Estimators for Invertible Index Models” by Ahn et al.,” Journal of Business & Economic Statistics, 36, 11–15.

- [23] \harvarditem[Kim and Pollard]Kim and Pollard1990kimpollard Kim, J., and D. Pollard (1990): “Cube Root Asymptotics,” Annals of Statistics, 18, 191–219.

- [24] \harvarditem[Komarova]Komarova2013komarova2013 Komarova, T. (2013): “Binary choice models with discrete regressors: Identification and misspecification,” Journal of Econometrics, 177(1), 14–33.

- [25] \harvarditem[LeCam]LeCam1953Lecam1953 LeCam, L. (1953): “On Some Asymptotic Properties of Maximum Likelihood Estimates and Related Bayes Estimates,” University of California Publications in Statistics, 1, 277–330.

- [26] \harvarditem[Lee]Lee1992mjleeordered Lee, M. (1992): “Median Regression for Ordered Discrete Resonse,” Journal of Econometrics, 51, 59–77.

- [27] \harvarditem[Leeb and Pötscher]Leeb and Pötscher2005LeebPots2005 Leeb, H., and B. Pötscher (2005): “Model Selection and Inference: Facts and Fiction,” Econometric Theory, 21, 21–59.

- [28] \harvarditem[Leeb and Pötscher]Leeb and Pötscher2006LeebPots2006 (2006): “Performance Limits for Estimators of the Risk or Distribution of Shrinkage-type Estimators, and some General Lower Risk-bound Results,” Econometric Theory, 22, 69–97.

- [29] \harvarditem[Leeb and Pötscher]Leeb and Pötscher2008LeebPots2008 (2008): “Sparse Estimators and the Oracle Property, or the Return of the Hodges’ Estimator,” Journal of Econometrics, 142, 201–211.

- [30] \harvarditem[Magnac and Maurin]Magnac and Maurin2008magnac-maurin08 Magnac, T., and E. Maurin (2008): “Partial Identification in Monotone Binary Models: Discrete Regressors and Interval Data,” Review of Economic Studies, 75(3), 835–864.

- [31] \harvarditem[Manski]Manski1975manski1975 Manski, C. F. (1975): “Maximum Score Estimation of the Stochastic Utility Model of Choice,” Journal of Econometrics, 3(3), 205–228.

- [32] \harvarditem[Manski]Manski1985manski1985 (1985): “Semiparametric Analysis of Discrete Response: Asymptotic Properties of the Maximum Score Estimator,” Journal of Econometrics, 27(3), 313–33.

- [33] \harvarditem[Manski]Manski1987manski1987 Manski, C. F. (1987): “Semiparametric Analysis of Random Effects Linear Models from Binary Panel Data,” Econometrica, 55(2), 357–362.

- [34] \harvarditem[Molchanov]Molchanov2006molchanov2006book Molchanov, I. (2006): Theory of Random Sets. Springer Science & Business Media.

- [35] \harvarditem[Rosen and Ura]Rosen and Ura2022rosenura2022 Rosen, A., and T. Ura (2022): “Finite Sample Inference for the Maximum Score Estimand,” Duke University Working Paper.

- [36] \harvarditem[Shalev-Shwartz and Ben-David]Shalev-Shwartz and Ben-David2014shalev:14 Shalev-Shwartz, S., and S. Ben-David (2014): Understanding machine learning: From theory to algorithms. Cambridge university press.

- [37]

Appendix A Appendix

A.1 Proofs in Section 2

Proof of Theorem 2.2. In our special design limiting maximum score objective function can be rewritten as

where . Since and , only the case effectively enters the objective function. is then given as the set of that solve .

Proof of Theorem 2.3. can be descried as

with the former case being the situation when there are realizations of in the sample, and the latter case being the situation when only values are available in the sample. The fact that immediately gives that . This implies the result for the Hausdorff distance as for any .

Proof of Theorem 2.4. We obtain as when and . Set is obtained as when and . Both of these situations happen with probabilities approaching 0.5 as . Indeed,

where , . Since is the same as , and , and it is easy to establish that as , we can conclude

Other sets possible as realization of are (when ), or (when ), or (when ), or (when ), or (when ). When , then either or can be the minimand. All these situations, however, occur with the probability approaching 0 as .

For any , as

Proof of Theorem 2.5. As follows from Theorem 6.5 in \citeasnounmolchanov2006book, it is enough for us to establish in terms of the capacity functional that for any compact ,

Take such that . Then and

Take such that . Then and

Take such that . Then and .

Situations when belongs to pairwise unions of the sets , , or spans across all three these sets are considered analogously.

Proof of Theorem 2.6. Since both , the identified set is characterized by inequalities and thus giving .

Appendix B Proofs in Section 3

Proof of Theorem 3.1. For , , and for , . Hence, with probability approaching 1, or equivalently, .

Since converges to and converges to at the parametric rate with limiting normal distributions, then as , for some

The exponential bounds follow from the tail behavior of the normal distribution.121212 For example, if has standard normal distribution, we have the tail probability: .

Proof of Theorem 3.4. Taking into account that , for , note that for large enough ,

Its maximand coincides with .

The feasible estimator has the following property:

Other sets are and also all the “other sets” listed in the proof of Theorem 2.4.

This establishes our result since we have that

Earlier in the paper we also established that , which together with results obtained here implies that .

Proof of Theorem 3.5. We demonstrate our result for the simple discrete design used throughout Section 3.

For illustration purposes, we first consider the infeasible case where the choice probabilities are known. For this case, we use notation instead of . Starting with the case , we have

Hence, with a random sample of observations, is a random variable which, when , takes the value 0 with probability and takes a strictly positive value with probability . For any we then have

as gets large. This establishes the consistency of the infeasible estimator when . An identical argument can be used for when .

When , we have is bounded away from 0 for . Consequently, for some positive uniformly in , and, thus,

as gets large. Thus, for each value of in the parameter space, the infeasible analogue of converges in probability to the identified set.

We now show the same result holds in the feasible setting, when the choice probabilities are not known, but have to be estimated from the data. As before, is defined as in (2.7). First, note that from standard properties of Nadaraya - Watson estimators of the conditional choice probability for the discrete design considered here, . Second, obtain