Semidiscrete optimal transport with unknown costs

Abstract

Semidiscrete optimal transport is a challenging generalization of the classical transportation problem in linear programming. The goal is to design a joint distribution for two random variables (one continuous, one discrete) with fixed marginals, in a way that minimizes expected cost. We formulate a novel variant of this problem in which the cost functions are unknown, but can be learned through noisy observations; however, only one function can be sampled at a time. We develop a semi-myopic algorithm that couples online learning with stochastic approximation, and prove that it achieves optimal convergence rates, despite the non-smoothness of the stochastic gradient and the lack of strong concavity in the objective function.

1 Introduction

In the semidiscrete optimal transport problem (Peyré & Cuturi, 2019), we are given a continuous random vector with known density , and a discrete random variable with known probability mass function . Our task is to choose a joint distribution for to minimize an expected cost. Formally, we write

| (1) |

subject to

| (2) | |||||

| (3) |

where is the support of and is the support of . The marginal distributions are fixed by the problem inputs and . The objective function can also be written as under the assumption that . In other words, is the mixed joint likelihood of .

The name “optimal transport” has the same origin as the well-known “transportation problem” in linear programming (Ford & Fulkerson, 1956), which can be interpreted as a special case of (1) where both and have finite support. In that case, the joint distribution of is described by a finite set of probabilities , whose cost coefficients are given by for all possible values of . The optimization problem then reduces to a linear program, whose solution can be interpreted as a minimum-cost plan for matching supply from one set of locations (or facilities) indexed by with demand at a different set of locations indexed by . Such plans have numerous applications in logistics. In semidiscrete optimal transport, remains discrete but becomes continuous, which makes the problem more difficult and generally not solvable using LP methods. The semidiscrete version also has applications in logistics, specifically in geographical partitioning problems (Carlsson et al., 2016; Hartmann & Schuhmacher, 2020) where demand can arise anywhere on the map, and the goal is to design service zones that assign spatial regions to supply facilities.

The optimal transport literature universally assumes that the cost function is known. In fact, most papers only work with some particular form for , most commonly a Euclidean distance or -norm (Santambrogio, 2015). In this paper, we study a semidiscrete optimal transport problem where is unknown, but can be estimated in a sequential manner from data. As is common in the contextual learning literature (Shen et al., 2021), we assume the linear model , where each value has a different, unknown . We observe i.i.d. samples from the density , which is also unknown. For each sampled value, we choose some and collect an observation of the form , where is an additive noise. We use linear regression to estimate from the observations for that value. Only one can be observed at a time, creating a tradeoff: one more observation of the th cost function means one less for the others.

To motivate this setting, consider the following application to online advertising. An advertising platform has clients. A guaranteed contract (Bharadwaj et al., 2010) ensures that client receives a certain number of impressions through the platform, which can be expressed as a proportion , agreed upon ahead of time, of the platform’s total user base. The vector represents the attributes of an individual user, and represents the conditional expected revenue (or another measure of performance such as clickthrough rate) earned by client from a user with those attributes. The platform requires a strategy for assigning users to clients to maximize expected revenue subject to the target proportions. The revenue function is unknown, but if user is assigned to client , we may obtain a noisy observation based on the user’s subsequent behaviour; we will not, however, collect any information pertaining to other clients.

This is essentially the same tradeoff that arises in classical optimal learning problems, such as ranking and selection (Chen et al., 2015) and multi-armed bandits (Gittins et al., 2011), where one similarly observes noisy samples of the values of various “alternatives” with the goal of efficiently identifying the best. In contextual learning, the value of an alternative additionally depends on a random vector ; see, e.g., Han et al. (2016), Alban et al. (2021) and Keslin et al. (2022) from the ranking and selection literature, or Abbasi-Yadkori et al. (2011) and Bastani et al. (2021) from the bandit community. Semidiscrete optimal transport with unknown costs can also be viewed as a contextual learning problem, but the presence of the target constraint (2) is a significant departure from those models. In optimal learning, there is a clear notion of “correct selection,” when the alternative with the smallest true value also has the smallest estimated value, and of “regret” when it does not. The proportional assignments in those problems vary between algorithms (Glynn & Juneja, 2004), and many papers aim to learn proportions that maximize the probability of correct selection (Russo, 2020; Chen & Ryzhov, 2023). However, under (2), we sometimes have to make choices that do not achieve the lowest cost, even if the costs are known. Thus, the standard definitions of correct selection or regret do not apply in this setting.

In this paper, we bridge optimal transport theory and optimal learning to formalize a notion of correct selection, and we create a sampling algorithm that makes correct selections at an optimal rate. In the process, we also obtain new results for the more standard setting of semidiscrete optimal transport with known costs. Although the known-cost setting is not the main focus of this research, the results are of some interest, and they lay the groundwork for the analytical technique that we eventually use to handle unknown costs. It is therefore necessary to discuss both settings for a clear understanding of how our analysis proceeds.

1.1 Results for known costs

When is known, the theory of semidiscrete optimal transport characterizes an optimal policy , a decision rule that maps an observed to some , in the presence of probabilistic targets. This characterization gives us a notion of correct selection that we will later use in the unknown-cost setting: given , we want to choose the same as the optimal policy.

Even under known costs, however, the correct selection is non-trivial to compute (unlike in classical learning problems). It can be shown that is characterized by a vector of parameters, namely, the shadow prices of (2) that optimally solve the Kantorovich dual of (1)-(3). As long as we know and are able to observe samples from , we can learn these parameters using stochastic approximation (SA) techniques (Genevay et al., 2016). The actual SA procedure is very simple, but there are some important nuances when it comes to performance guarantees.

Modern research in SA, surveyed by Newton et al. (2018), focuses on convergence rates; the analytical tools for deriving such results were established by the seminal work of Bach & Moulines (2011). The strongest possible guarantee is that the sequence of SA iterates converges in at the canonical rate , where is the number of samples drawn from . In general, however, this rate is only achievable with Polyak averaging (Polyak & Juditsky, 1992) included into the SA procedure and with the assumption of strong convexity (concavity) on the SA objective function. Even in later work (e.g., Bach & Moulines, 2013), which has yielded sharper rates, strong convexity is still needed to bound the error of the SA iterates. In our case, however, the objective of the Kantorovich dual is concave, but not strongly concave. The optimal transport literature is well aware of this difficulty, and has a developed a workaround (see, e.g., Genevay et al., 2016 or Taşkesen et al., 2023) that replaces the objective by a smoothed approximation. This approach recovers the canonical rate, but may no longer converge to the solution of the original problem.

In marked contrast, we do not modify the problem. Instead, we adopt a perspective from the recent bandit literature (e.g., Goldenshluger & Zeevi, 2013, Bastani & Bayati, 2020, and Bastani et al., 2021), which has found that convergence rates improve when the data-generating distribution exhibits a sufficient degree of random variation (“richness”). With comparable assumptions on the distribution of , the objective is still not strongly concave, but it has a kind of “local” strong concavity that enables us to prove the canonical rate, without smoothing or averaging. This property of the objective is also used in our analysis of unknown costs.

1.2 Results for unknown costs

When is unknown, we still need to use SA to learn the dual variables, but the situation becomes much more complicated because the gradient estimates are no longer unbiased (they now have to be computed using estimated costs). The problem couples optimal learning together with SA in such a way that both aspects create difficulties for each other: statistical error in the estimated costs creates bias in the gradient estimator, but the gradient estimator drives the decision rule and thus determines which alternatives are sampled.

We solve this problem using a simple, computationally efficient online algorithm with a “semi-myopic” structure. Most of the time, the algorithm approximates the optimal policy using plug-in estimators of both the costs and the dual variables, but occasionally it is forced to sample each individual cost function. These periods of forced exploration become less frequent as time goes on, to reduce their impact on performance. Semi-myopic structure has a long history in optimal learning, dating back to the work of Broder & Rusmevichientong (2012) on dynamic pricing, and followed by extensions to ranking and selection (Garivier & Kaufmann, 2016) and contextual bandits (Goldenshluger & Zeevi, 2013). Virtually all of these papers require assumptions on the richness of the data-generating distribution in order to obtain optimal rates. Semi-myopic algorithms also vary in how often they need to conduct forced exploration. The gap between exploration periods grows linearly in Broder & Rusmevichientong (2012); quadratically in Keskin & Zeevi (2014), Garivier & Kaufmann (2016), and BaKe21; and exponentially in Goldenshluger & Zeevi (2013) and Bastani & Bayati (2020). The gap for our procedure, in the more complex setting of semidiscrete optimal transport, grows sub-exponentially.

Our paper is the first to couple this type of exploration with stochastic approximation. As in SA, we update the iterates using (biased) gradient estimates; as in optimal learning, information is collected sequentially in a semi-myopic fashion. Building on our results for the known-cost setting, we prove that SA still achieves the canonical rate under this setup. As a corollary, the expected number of incorrect decisions made by the semi-myopic policy (the most relevant analog of “regret” in our setting) grows at a rate , the best possible. This performance is achieved in an online manner, without requiring the sample size to be known in advance. Numerical experiments show that, in some situations, cost uncertainty produces only minor performance loss relative to an “ideal” SA procedure with unbiased gradients.

In summary, our work bridges and contributes to three distinct streams of literature. We contribute to optimal transport by being the first to formulate and study the semidiscrete problem with unknown costs. This problem couples optimal learning and stochastic approximation in a novel and challenging way. We contribute to optimal learning by studying a novel contextual problem with probabilistic targets, and by proving that semi-myopic exploration can learn the optimal policy efficiently. We contribute to SA by showing that optimal convergence rates can be achievable without strong concavity, as long as the data-generating distribution is sufficiently rich.

2 Optimal policies in semidiscrete optimal transport

We begin by discussing the optimal solution to (1)-(3) when and are known. This solution will provide us with a performance metric for the problem that we will eventually tackle. In contextual ranking and selection (Hong et al., 2021), the main metric used to evaluate and compare algorithms is “correct selection,” which occurs when we select the alternative with the lowest cost given . This is what would happen if we removed the probabilistic target constraints (2), because then (1) would be minimized simply by setting . We require an analogous notion of correct selection that would be meaningful in the presence of (2).

It turns out that (1)-(3) is solved by a policy, or decision rule for assigning any observed to a value. In other words, should be set equal to a certain deterministic function of . The optimal transport literature has characterized this function near-explicitly using Kantorovich duality (Theorem 1.3 in Villani, 2021). To describe and explain its structure, we sketch the key steps in the derivation. The details of these arguments can be found in, e.g., Carlsson et al. (2016) or Genevay et al. (2016).

For notational convenience, we write , to visually distinguish between costs corresponding to different “alternatives,” from which we will eventually make a selection. By Kantorovich duality, the problem (1)-(3) has the same optimal value as the functional optimization problem

| (4) |

subject to the constraint

| (5) |

In (4), the marginal density of is , and the marginal pmf of is , as in the primal problem. To handle (5), we take

Letting , we can rewrite (4) as

| (6) |

The minimum of a finite number of linear functions is concave, and expectations preserve concavity, so the objective in (6) is concave in .

There are no constraints on , so we can simply take the gradient and set it equal to zero. It can be shown that, in this situation, the gradient can be interchanged with the expectation, an instance of “infinitesimal perturbation analysis,” a well-known technique in the simulation community (Fu, 2006; Kim, 2006). Formally, let . Under some conditions on the distribution of (namely, that the pairwise difference has a density for any ), one can show that , where the stochastic gradient , whose elements are given by

| (7) |

exists at any for which the argmin is unique. Combining (6) with (7), it follows that any optimal solves the system of equations

| (8) |

In words, is a vector of bonuses and penalties (since its elements can be either positive or negative) which are subtracted from the costs to ensure that each element is the smallest with precisely the target probability.

These same bonuses and penalties can be used to construct an optimal solution for the primal problem (1)-(3). By weak duality, we have

| (9) |

where is the joint likelihood of satisfying (2)-(3), as before. Now define . By (8), we have , so the joint likelihood of satisfies (2)-(3). We then write

where the last line follows by (9). Then, letting

| (10) |

it follows that the joint distribution of optimally solves (1)-(3).

The policy is a natural benchmark against which other policies may be compared. Suppose that is a sequence of i.i.d. samples from , and is a sequence of random variables taking values in . We say that a correct selection is made at time if . We may use the expected total number of incorrect selections to evaluate the performance of the sequence up to time . The probability of incorrect selection (PICS), written as , plays an important role in the analysis of this performance metric.

Many papers on optimal learning present their results in terms of the regret, which in our context would be the difference in cost achieved by vs. . However, because of (2), regret relative to can be negative, unlike in traditional bandit problems. We therefore focus on the expected number of incorrect selections, which has a very clear, straightforward interpretation.

3 Algorithms and main results

Under both known and unknown costs, our goal is to learn iteratively based on a sequence of i.i.d. samples from the data-generating density . Section 3.1 describes the algorithms that we use under both known and unknown costs. Then, Section 3.2 states our assumptions and main results for the known-cost setting, and Section 3.3 does the same for unknown costs.

3.1 Algorithms for known and unknown costs

When the cost functions are known, (8) can be approached as a stochastic root-finding problem (Pasupathy & Kim, 2011). We can straightforwardly apply the stochastic approximation (SA) algorithm

| (11) |

where is a stepsize sequence satisfying the usual conditions , . The gradient is bounded, so the convergence easily follows from classical SA theory (Kushner & Yin, 2003). The rate of convergence is discussed in Section 3.2.

Suppose now that the cost functions are unknown: in each iteration, we still observe , but we do not know . We only have access to approximate cost functions , which now have to be used to update . We can, however, select one particular and collect a noisy observation of the form , where are i.i.d. noise terms with mean zero, assumed to be independent of . Additionally, we can only observe one function at a time: if we choose at iteration , we cannot see for .

In this paper, we assume , and similarly , where is a linear regression estimator of computed using all past observations (up to the th time stage) of the th cost function. As in Bastani et al. (2021) and other papers on contextual learning, it is not particularly difficult to extend the results to other parametric statistical models (such as generalized linear models), as the most crucial component of the analysis is the choice of which cost function to observe, and not the statistical estimation procedure. We focus on linear regression in this paper because it is commonly used in the literature on contextual learning.

- Step 0:

-

Initialize , and for . Choose a deterministic stepsize sequence .

- Step 1:

-

Observe and select .

- Step 2:

-

Update

(12) - Step 3:

-

Observe

and use this quantity to calculate an updated . For all , let .

- Step 4:

-

Increment by and return to Step 1.

The cost function to be observed, formally denoted as , is selected in an online manner: it depends on the available estimators and , but also on the new data . Thus, affects the approximate costs in the next iteration, and through these approximations, the next gradient update as well. This algorithmic framework, laid out in Algorithm 1, can be viewed as a coupling of the SA procedure (11) with optimal learning (e.g., bandit problems). As in optimal learning, we can only sample one “alternative” (cost function) at a time, but the policy used to do this is linked to the bias of the SA update.

As discussed in Section 1.2, our analysis uses a particular construction of known as a semi-myopic policy. This approach approximates (10) using plug-in estimates of and . Most decisions are made based on this approximation, but we occasionally force ourselves to sample different to prevent the estimates from stalling. Forced exploration occurs less frequently as time goes on.

Formally, we first define to be the plug-in estimate of the optimal decision, based on estimates and . We also define, for each , the set

of time periods where we will force ourselves to explore . Any works for the theory; in practice, this value is tunable (for instance, produces fairly infrequent forced exploration). Then, the st decision is made according to the policy

| (13) |

The estimate is updated using (12), and the regression coefficients are computed using the ridge-like estimator

| (14) |

where .

It was observed, as early as Broder & Rusmevichientong (2012) and as recently as Bastani et al. (2021), that the need for forced exploration could be eliminated with very strong conditions on the data-generating process (in our case, the distribution of ). In other words, if the data inherently provide more information, a simple myopic algorithm will achieve optimal convergence rates. There is, however, no free lunch: the required assumptions are substantially stronger than anything that we will assume in our analysis.

3.2 Assumptions and main results: known costs

The results obtained here are an important prerequisite for our study of unknown costs. Because Algorithm 1 includes an SA update, we first require a detailed understanding of how SA learns under known costs before we can use it to handle the more difficult case. As mentioned in Section 1.1, the main technical obstacle in this analysis is the fact that the objective function is concave, but not strongly concave. We will explain in Section 4 how this issue is resolved; for the moment, let us state the assumptions and results.

From (10), we see that adding a constant to every component of does not change the optimal decision. Therefore, we only need to learn the differences for , so we may assume without loss of generality that . We additionally state a simple regularity condition ensuring that has a unique argmin for any choice of .

Assumption 3.1.

For any with , the random variable is absolutely continuous with respect to Lebesgue measure.

The next set of assumptions concerns the “richness” of the data-generating distribution. It is based on the recent optimal learning literature, which has found, in various settings, that desirable convergence rates require the observed values of to exhibit a sufficient degree of random variation. This is made more precise as follows.

Assumption 3.2.

Suppose that there exist constants (which may depend on ) such that:

-

i)

For any with , the random variable

has a density that is bounded within on the interval .

-

ii)

For any , we have

-

iii)

The support of is bounded, i.e., .

These assumptions are fairly typical for recent work on optimal learning. Assumptions 3.2(i) and 3.2(ii) are very similar to the margin conditions in Assumption A2 of Goldenshluger & Zeevi (2013), Assumption 2 of Bastani & Bayati (2020), and Assumption 2 of Bastani et al. (2021). Essentially, we require sufficient random variation near the decision boundary , as this is where we have the greatest difficulty identifying whether or is better. Assumption 3.2(iii) is also made by the above-cited papers and many others.

The algorithm is given by (11) using a simple stepsize with being a pre-specified constant. Our main result is a rate bound on the convergence in of the sequence , with .

Theorem 3.1.

Thus, under Assumptions 3.1-3.2, classical SA achieves the canonical rate. It is interesting to note that this does not happen in general: one usually resorts to Polyak averaging (Polyak & Juditsky, 1992) to recover the optimal convergence rate, which is indeed done in Bach & Moulines (2011). However, in the specific setting of semidiscrete optimal transport with known costs, neither averaging nor strong concavity are necessary as long as the data-generating process is rich in the sense of Assumption 3.2.

3.3 Assumptions and main results: unknown costs

As in Section 3.2, we let and . We also let . Recall the distinction between , which is the plug-in estimate of the optimal decision, and , which is the semi-myopic policy combining that estimate with forced exploration as defined in (13).

We require two additional assumptions on the data-generating distribution. The first is a standard assumption on the residual noise terms, used in virtually all proofs in contemporary learning theory. The second is very similar to Assumption A3 in Goldenshluger & Zeevi (2013), and is weaker than Assumption 3 of Bastani et al. (2021).

Assumption 3.3.

Suppose that there exist constants such that:

-

i)

The residual noise is conditionally sub-Gaussian: for any , .

-

ii)

Let be the function that returns the smallest eigenvalue of the matrix argument. For any ,

The bulk of the analysis focuses on bounding the convergence rate of the estimation error for both and . These results are stated in Theorem 3.2. Then, Theorem 3.3 obtains a rate for the accuracy of the plug-in estimate , in the sense of the PICS metric defined in Section 2.

Theorem 3.2.

Theorem 3.3.

Suppose that we are in the situation of Theorem 3.2. Then, there exists , which depends only on , such that the plug-in estimate satisfies

| (15) |

The square-root rate in (15) is due to the fact that some values can make it arbitrarily difficult to distinguish between choices. Faster rates (e.g., exponential rates, as in Gao et al., 2019) can only be obtained if one assumes some minimal amount of separation between objective values, for example by making the support of finite. If this is not the case, it will be impossible to improve on (15).

While we focus on PICS rather than regret in this work, our result is comparable to an optimal regret bound. For example, Goldenshluger & Zeevi (2013) obtains a single-period regret rate of (a known universal lower bound) from a bound that multiplies together two terms, one involving the estimation error of the regression coefficients, and one that looks similar to PICS. Individually, both terms converge at a rate of , as they do in our paper. One can view that problem as a special case of ours with known , which implies that it is not possible to guarantee faster rates than these.

A straightforward consequence of Theorem 3.3 is that the expected number of incorrect selections made by (essentially adding up (15) over ) grows according to . This rate does not change if we count incorrect selections made by the semi-myopic policy (incorporating the forced exploration periods) rather than simply the plug-in estimate, because forced exploration occurs only in time periods.

Corollary 3.1.

Suppose that we are in the situation of Theorem 3.2. Then, there exists , which depends only on , such that

4 Analysis for known costs

In this section, we prove Theorem 3.1. As was discussed previously, the main difficulty in the proof is the lack of strong concavity in the objective function. Thus, a crucial first step is the derivation (in Section 4.1) of a kind of “local strong concavity” property that is weaker than strong concavity, but still sufficient to prove (in Section 4.2) the main rate result.

4.1 Properties of the objective

We establish two technical results concerning the smoothness of the objective . The proof techniques will be used again later on, in Section 5, where these properties will be generalized to the setting of unknown cost functions.

Proof: To avoid notational clutter, we write as simply in this proof, since no other will be considered. By definition of , we can write

where

| (16) |

Clearly, . We will work toward a lower bound on , which will require some algebra on (16). Because the indices maximizing and are unique by assumption, we can write

The mapping is decreasing in . Because for any by definition, we then have

Consequently,

| (17) |

We now seek to bound the expectation of each term in (17). For convenience, let for any . Similarly, let . We write

Taking expectations, we obtain

where (4.1) follows by the tower property, and (4.1) follows because for .

Using Assumption 3.2(ii), and taking , we write

| (20) | |||||

and, since on , (20) yields

| (21) |

Then, returning to (4.1), we consider two cases. First, suppose that . Then, (21) can be applied directly, yielding

| (22) | |||||

In the second case, we consider . The mapping

is increasing on the interval . Therefore, applying (21) again, we obtain

| (23) |

Combining (22) and (23), we have

| (24) | |||||

for any . Since the left-hand side of (24) is always positive, we have

| (25) | |||||

for any value (positive or negative) of .

We may now derive the desired result. Combining (17) and (25), we have

| (26) |

Because, in (26), all of the terms in the double sum are positive, we may take another lower bound in which we only keep those terms in which either or . However, for any , either or . Therefore, we have

whence

as required.

The second property represents, again, a kind of local strong concavity. In ordinary concavity, the right-hand side of inequality (27) below is simply zero. If we had strong concavity, the right-hand side would be . Thus, we have that property only when is small, i.e., is in a neighborhood of . For notational convenience, we let be the vector whose components are given by , noting that .

Lemma 4.2.

Suppose that we are in the situation of Lemma 4.1. Then,

| (27) |

Proof: To avoid notational clutter, we write as simply in this proof, since no other will be considered. By the concavity of the function , we have

We then apply Lemma 4.1. It remains only to show that

To see this, consider two cases. First, suppose that there is some for which . Then,

Second, suppose that for all . Then,

This completes the proof.

4.2 Proof of Theorem 3.1

We rewrite (11) in vector form as , where . We may also write a similar recursion

| (28) |

for the error sequence. Before proceeding to the convergence rate, we first prove two intermediate results: an almost sure (but non-vanishing) bound on , and a concentration inequality showing that the tail probabilities of vanish quickly outside a certain bounded range. The proofs are deferred to the Appendix (Section 9).

Lemma 4.3.

Let . Then, for .

Finally, we prove Theorem 3.1. Let . Using (28), we may write

| (29) | |||||

where (29) uses Lemma 4.2 with an appropriate . Letting be the sigma-algebra generated by , we have

On the event , we have

Therefore,

where is a constant obtained from Lemma 4.3. Taking unconditional expectations and applying Lemma 4.4, we obtain

Therefore, for some suitable , we have

Letting , we have

| (30) |

A technical lemma in the Appendix (Lemma 8.2) proves that a non-negative sequence satisfying (30) is uniformly bounded if the coefficient of on the right-hand side is positive. Thus, we obtain the desired result as long as .

5 Analysis for unknown costs

We proceed similarly to Section 4. Section 5.1 proves analogous properties to those in Section 4.1 for the case of unknown costs. Section 5.2 outlines the proof of the main rate results, with some intermediate steps moved to the Appendix.

5.1 Properties of the objective

We proceed largely the same way as in Section 4.1. This time, however, we generalize the notation to allow for different choices of the regression coefficients. Let , and let be the vector whose components are given by . Note that and .

The first two results are extensions of Lemmas 4.1-4.2. Their main purpose is to prove local strong concavity in the presence of estimation error for both and . The overall structure of the proofs closely follows that of their counterparts in Section 4.1, but some additional work is required to handle the error of the regression coefficients. The proofs are deferred to the Appendix.

Lemma 5.1.

Lemma 5.2.

The final property is completely new to the case of unknown costs, and bounds the estimation error of the vector of target probabilities in a setting where we know , but not .

Lemma 5.3.

Proof: To avoid notational clutter, we write as simply in this proof, since no other will be considered. Note, however, that we do distinguish between and .

As in the proof of Lemma 5.1, we define . For additional convenience, denote . Then, . Observe that, for any ,

| (31) | |||||

By Assumption 3.2(iii), . We focus on the first term of (31) and derive

Using very similar arguments, the same bound can be shown for the second term of (31). Thus, we have

| (32) |

Consider the case . By Assumption 3.2(i), (32) yields

At the same time, since we always have , we may continue (32) as

| (33) |

We observe the elementary inequality that, for any and ,

Applying this to (33) yields the desired result.

5.2 Proof outline for main rate results

Finally, we provide an outline of the steps made in proving Theorems 3.2-3.3. The notation from Section 5.1 is carried over. The notation will be used to denote the spectral norm (largest singular value).

The first result relates the probability of incorrect selection (for an arbitrary policy) to the estimation error of both and . It is used in several places. Theorem 3.3 will be a direct consequence of it once Theorem 3.2 is established.

Lemma 5.4.

Proof: We observe that

so it is sufficient to consider a single . Let . By repeating some arguments in the proof of Lemma 5.3 (starting from eq. (31) onwards), we obtain

| (34) | |||||

The arguments in the proof of Lemma 5.3 can then be repeated to yield the desired bound on (34).

Next, we state three intermediate technical results related to the information matrix of the observations collected using the proposed semi-myopic policy. The proofs of these results are deferred to the Appendix.

Lemma 5.5.

Lemma 5.6.

Lemma 5.7.

Let Assumptions 3.1-3.2 and 3.3 hold. Let be a sequence of random variables such that each takes values in and is measurable with respect to , the sigma-algebra generated by , , and .

Define . Similarly, let . The following statements hold:

-

1)

For any , any and any ,

(38) -

2)

For any and ,

(39)

We now begin to study the properties of the semi-myopic algorithm. We first establish concentration inequalities on the two types of estimation error (that is, the error of estimating and , respectively). The proofs are deferred to the Appendix, but we note that this is essentially the same approach as in Section 4.2; in particular, the statement and proof of Lemma 5.9 are similar in structure to Lemma 4.4. The difference is that we now require separate concentration inequalities for two interrelated objects. The result of Lemma 5.8 is used inside the proof of Lemma 5.9.

Lemma 5.8.

Lemma 5.9.

Finally, we complete the proof. Theorem 3.2 is the combination of Propositions 5.1 and 5.2 below. The proof of Proposition 5.1 is highly technical and deferred to the Appendix. Proposition 5.2 is an extension of Theorem 3.1 incorporating estimation error from regression (and using the result of Proposition 5.1). As mentioned earlier, Theorem 3.3 follows straightforwardly from these results together with Lemma 5.4.

Proposition 5.1.

Proposition 5.2.

Proof: Let . As in the proof of Theorem 3.1, we first write

| (40) | |||||

where (40) is obtained by applying Lemmas 5.2-5.3 with appropriate . Letting be the sigma-algebra generated by , , and , we write

Let , where is the constant obtained from Lemma 5.5. On the event , we obtain

by repeating arguments from the proof of Theorem 3.1. Then, in general, we have

| (41) | |||||

where in (41) is a constant obtained from Lemma 4.3. We now take the unconditional expectation, obtaining

| (43) |

where (5.2) uses Lemma 5.9, and (43) uses Proposition 5.1. We thus have

for suitable . Letting , we have

As in the proof of Theorem 3.1, we apply Lemma 8.2 and obtain the desired result as long as .

6 Numerical illustrations

We illustrate our framework on two numerical examples. Section 6.1 considers synthetic test instances with linear costs and Gaussian noise. Section 6.2 applies our framework to learn facility locations in a geographical partitioning problem (a common application area of semidiscrete optimal transport).

6.1 Synthetic linear costs

We consider a set of synthetic test problems. In all of these problems, the data are generated uniformly on the unit sphere in dimensions, and the residual error follows a Gaussian distribution. Each problem uses different vectors , also generated uniformly on the unit sphere, and a different generated uniformly on the -dimensional simplex.

For ease of implementation, we modified the semi-myopic policy to conduct forced exploration probabilistically: that is, in the th iteration, we select uniformly at random with probability , where we used . The rest of the time, we select a cost function according to the myopic policy . We used in the update of , and we set for simplicity, and in order to enable use of recursive least squares. At each , we evaluate the policy using the correct selection indicator . By averaging this quantity across runs, each containing iterations and starting from , , we obtain a trajectory of the probability of correct selection. We then average this trajectory over test problems.

The optimal policy for each test problem is precomputed via brute force by running (11) with the true cost coefficients for a very large number of iterations. As a benchmark, we also implement a policy that knows the true costs (and, therefore, does not need to conduct any exploration or collect any samples), but not , and runs (11) in an online manner. We also calculate the average probability of correct selection for this policy, which allows us to evaluate any loss incurred by having to learn the coefficients.

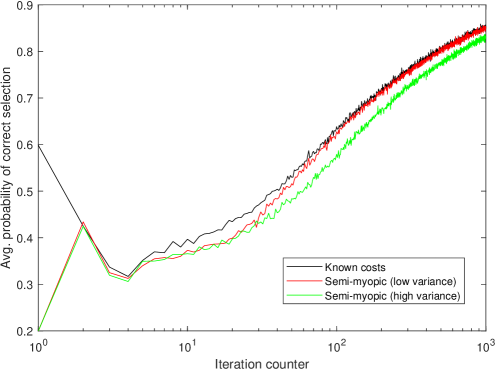

Figure 1 shows average performance for the semi-myopic policy under two levels of noise: and . Since the benchmark policy knows the costs, it is unaffected by the noise variance. We see that, when the variance is low, there is virtually no performance loss caused by unknown costs. When the variance is high, the average PCS of the semi-myopic policy lags behind that of the known-cost policy by (and has narrowed this gap relative to the earlier iterations). Performance also does not appear to be very sensitive to the frequency of forced exploration: we also tested a much higher value , for which the probability of forced exploration is only by the end of the time horizon, but obtained very similar trajectories. This also indicates that, in an online implementation, we could allow forced exploration to happen quite infrequently while maintaining good performance.

Learning appears to be the greater challenge. After iterations, the PCS is approximately even for the benchmark policy, which knows from the beginning. It is well-known in the stochastic approximation literature that the performance of SA can be sensitive to the stepsize rule. It may be possible to speed up convergence by using other choices of , many of which are surveyed in George & Powell (2006). We lightly tuned in our stepsize rule , but we do not delve deeply into this issue here because our focus in this paper is mainly theoretical.

6.2 Geographical partitioning

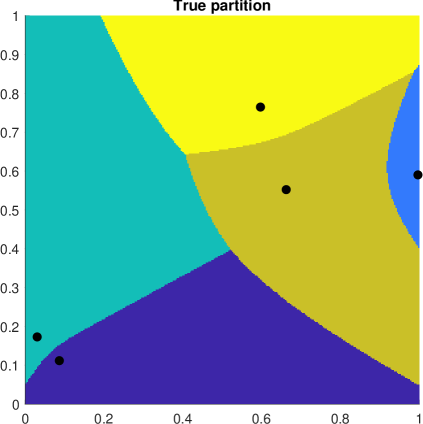

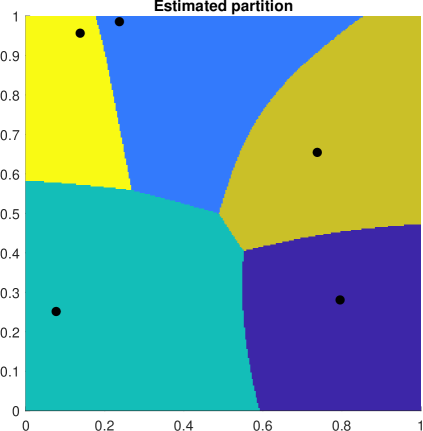

For each , let be a fixed location (“facility”) in the unit square. A user appears at some random location and is assigned to a facility. The cost incurred by assigning the user to facility is , the Euclidean distance between the facility and the user. The goal is to choose an assignment rule that minimizes the expected distance subject to the probabilistic targets (which, in this context, require each facility to serve a certain proportion of the population). It is well-known in computational geometry that the optimal policy can be visualized as an additively weighted Voronoi diagram (Carlsson et al., 2016) whose weights are the values . The diagram partitions the unit square into regions, each containing a single facility, to which all users appearing in that region are assigned.

We now suppose that the locations are unknown, but a user appearing at location can obtain a noisy observation of the distance to any one facility of his or her choice. This observation is not linear in , but we can still apply a linear regression model using the transformation

| (44) | |||||

The last two terms in (44) have zero mean and can be treated as “residual error.” Because is observed, the quantity is known. Thus, we can learn using a linear regression model in which is the vector of features, and is the response variable. The coefficients to be learned are . Clearly, is identifiable in this model.

We considered two instances of this model where and is uniformly distributed on . Note that, even with the normality assumption, the residual error in (44) is no longer sub-Gaussian. The instances used different facility locations and targets . The settings of the semi-myopic policy were the same as in Section 6.1.

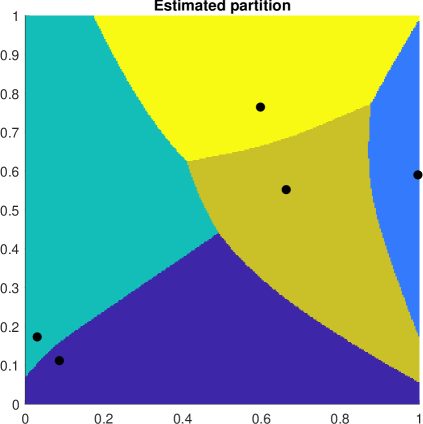

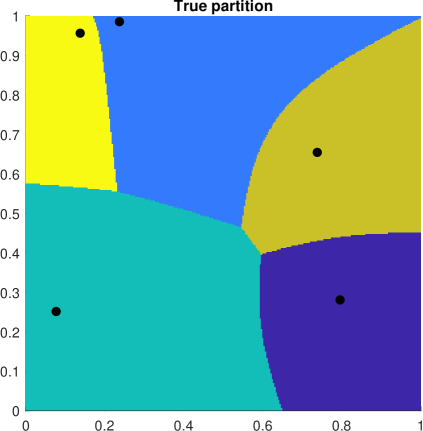

In this discussion, we aim to take advantage of the unique visual interpretation offered by the geographical partitioning setting. Thus, we do not present average trajectories of PCS over a large number of runs, as we did in Section 6.1. Rather, we will visualize the final partition learned by the semi-myopic policy after a large number of iterations, and compare this to the optimal partition induced by . Unlike in Section 6.1, we do not need to separately present a policy that knows but attempts to learn in an online manner, because the number of iterations is so large that such a policy will have converged to the true optimal partition already.

Figure 2 presents the true and estimated partitions for both instances, with the facility locations shown as black dots. The difference between locations turns out to exert a very significant impact on performance. In Instance 1, the facility close to the right edge of the unit square is also assigned a small value (specifically, ). Thus, only a small portion of observations will lead us to sample this facility, causing us to rely more on forced exploration. Even after million iterations, the PCS achieved by the semi-myopic policy (i.e., the proportion of users assigned to the correct facility) is only . In Instance 2, this is less of a concern, and the semi-myopic policy achieves a PCS of . The estimated partition is also visibly closer to the true one in Instance 2.

In general, the estimation error of is much more of an issue in the partitioning problem than it was in Section 6.1. Even after million iterations, the semi-myopic policy noticeably lags behind SA with known costs (which was used to find the true partition). We found that our policy was effective in learning the regression coefficients, with being within three decimal places of by the end of the time horizon. However, by the time this happened, the stepsize in the gradient update had become so small that had fallen behind (though it is still making progress, as PCS continues to increase if we keep running the policy). One reason may be that the regression noise in this problem is not sub-Gaussian, but has heavier tails than it did in Section 6.1, so the gradient update is more heavily biased. Even so, this example shows that the semi-myopic policy is able to learn the true partition even when some of the underlying model assumptions are violated.

7 Conclusion

We have presented a novel variant of the semidiscrete optimal transport problem in which the costs are unknown, but can be estimated through sequential observations. This process is subject to the usual tradeoff of optimal learning, where sampling one cost function means one less sample available for the others. The problem thus brings together elements of optimal transport, optimal learning, and (through the characterization of the optimal policy) stochastic approximation. We have developed a simple and provably efficient algorithm based on the well-established notion of semi-myopic exploration; however, our analysis couples this structure with stochastic approximation in a novel way. In the process, we are able to resolve several known issues with applying SA to semidiscrete optimal transport, having to do with the non-smoothness of the stochastic gradient and the lack of strong concavity in the objective function.

There are many opportunities for future work. First, it may be interesting to investigate the theoretical performance of other types of learning algorithms, such as Thompson sampling (Agrawal & Goyal, 2013), in this particular context. Second, it is worth taking a closer look at practical issues such as stepsize selection, which is known to impact the performance of SA procedures. Third, there may be potential for further connections between optimal transport and optimal learning beyond the semidiscrete version studied here. We hope that our work will spark new interest in bridging these fields.

References

- (1)

- Abbasi-Yadkori et al. (2011) Abbasi-Yadkori, Y., Pál, D. & Szepesvári, C. (2011), Improved algorithms for linear stochastic bandits, in J. Shawe-Taylor, R. S. Zemel, P. L. Bartlett, F. Pereira & K. Q. Weinberger, eds, ‘Advances in Neural Information Processing Systems’, Vol. 24, pp. 2312–2320.

- Agrawal & Goyal (2013) Agrawal, S. & Goyal, N. (2013), Thompson sampling for contextual bandits with linear payoffs, in S. Dasgupta & D. McAllester, eds, ‘Proceedings of the 30th International Conference on Machine Learning’, pp. 127–135.

- Alban et al. (2021) Alban, A., Chick, S. E. & Zoumpoulis, S. I. (2021), Expected value of information methods for contextual ranking and selection: clinical trials and simulation optimization, in S. Kim, B. Feng, K. Smith, S. Masoud, Z. Zheng, C. Szabo & M. Loper, eds, ‘Proceedings of the 2021 Winter Simulation Conference’.

- Bach & Moulines (2011) Bach, F. & Moulines, E. (2011), Non-asymptotic analysis of stochastic approximation algorithms for machine learning, in J. Shawe-Taylor, R. Zemel, P. Bartlett, F. Pereira & K. Q. Weinberger, eds, ‘Advances in Neural Information Processing Systems’, Vol. 24, pp. 451–459.

- Bach & Moulines (2013) Bach, F. & Moulines, E. (2013), Non-strongly-convex smooth stochastic approximation with convergence rate O(1/n), in C. J. Burges, L. Bottou, M. Welling, Z. Ghahramani & K. Q. Weinberger, eds, ‘Advances in Neural Information Processing Systems’, Vol. 26, pp. 773–781.

- Bastani & Bayati (2020) Bastani, H. & Bayati, M. (2020), ‘Online decision making with high-dimensional covariates’, Operations Research 68(1), 276–294.

- Bastani et al. (2021) Bastani, H., Bayati, M. & Khosravi, K. (2021), ‘Mostly exploration-free algorithms for contextual bandits’, Management Science 67(3), 1329–1349.

- Bharadwaj et al. (2010) Bharadwaj, V., Ma, W., Schwarz, M., Shanmugasundaram, J., Vee, E., Xie, J. & Yang, J. (2010), Pricing guaranteed contracts in online display advertising, in X. J. Huang, G. Jones, N. Koudas, X. Wu & K. Collins-Thompson, eds, ‘Proceedings of the 19th ACM International Conference on Information and Knowledge Management’, pp. 399–408.

- Broder & Rusmevichientong (2012) Broder, J. & Rusmevichientong, P. (2012), ‘Dynamic pricing under a general parametric choice model’, Operations Research 60(4), 965–980.

- Carlsson et al. (2016) Carlsson, J. G., Carlsson, E. & Devulapalli, R. (2016), ‘Shadow prices in territory division’, Networks and Spatial Economics 16(3), 893–931.

- Chen et al. (2015) Chen, C.-H., Chick, S. E., Lee, L. H. & Pujowidianto, N. A. (2015), Ranking and selection: efficient simulation budget allocation, in M. C. Fu, ed., ‘Handbook of Simulation Optimization’, Springer, pp. 45–80.

- Chen & Ryzhov (2023) Chen, Y. & Ryzhov, I. O. (2023), ‘Balancing optimal large deviations in sequential selection’, Management Science 69(6), 3457–3473.

- Ford & Fulkerson (1956) Ford, L. R. & Fulkerson, D. R. (1956), ‘Solving the transportation problem’, Management Science 3(1), 24–32.

- Fu (2006) Fu, M. C. (2006), ‘Gradient estimation’, Handbooks in Operations Research and Management Science, vol. 13: Simulation pp. 575–616.

- Gao et al. (2019) Gao, S., Du, J. & Chen, C.-H. (2019), Selecting the optimal system design under covariates, in ‘Proceedings of the 15th IEEE International Conference on Automation Science and Engineering’, pp. 547–552.

- Garivier & Kaufmann (2016) Garivier, A. & Kaufmann, E. (2016), Optimal best arm identification with fixed confidence, in V. Feldman, A. Rakhlin & O. Shamir, eds, ‘Proceedings of the 2016 Conference on Learning Theory’, pp. 998–1027.

- Genevay et al. (2016) Genevay, A., Cuturi, M., Peyré, G. & Bach, F. (2016), Stochastic optimization for large-scale optimal transport, in D. Lee, M. Sugiyama, U. von Luxburg, I. Guyon & R. Garnett, eds, ‘Advances in Neural Information Processing Systems’, Vol. 29, Curran Associates, Inc., pp. 3440–3448.

- George & Powell (2006) George, A. P. & Powell, W. B. (2006), ‘Adaptive stepsizes for recursive estimation with applications in approximate dynamic programming’, Machine Learning 65, 167–198.

- Gittins et al. (2011) Gittins, J. C., Glazebrook, K. D. & Weber, R. (2011), Multi-armed bandit allocation indices (2nd ed.), John Wiley and Sons.

- Glynn & Juneja (2004) Glynn, P. W. & Juneja, S. (2004), A large deviations perspective on ordinal optimization, in R. Ingalls, M. D. Rossetti, J. S. Smith & B. A. Peters, eds, ‘Proceedings of the 2004 Winter Simulation Conference’, pp. 577–585.

- Goldenshluger & Zeevi (2013) Goldenshluger, A. & Zeevi, A. (2013), ‘A linear response bandit problem’, Stochastic Systems 3(1), 230–261.

- Han et al. (2016) Han, B., Ryzhov, I. O. & Defourny, B. (2016), ‘Optimal learning in linear regression with combinatorial feature selection’, INFORMS Journal on Computing 28(4), 721–735.

- Hartmann & Schuhmacher (2020) Hartmann, V. & Schuhmacher, D. (2020), ‘Semi-discrete optimal transport: a solution procedure for the unsquared Euclidean distance case’, Mathematical Methods of Operations Research 92(1), 133–163.

- Hong et al. (2021) Hong, L. J., Fan, W. & Luo, J. (2021), ‘Review on ranking and selection: A new perspective’, Frontiers of Engineering Management 8(3), 321–343.

- Keskin & Zeevi (2014) Keskin, N. B. & Zeevi, A. (2014), ‘Dynamic pricing with an unknown demand model: Asymptotically optimal semi-myopic policies’, Operations Research 62(5), 1142–1167.

- Keslin et al. (2022) Keslin, G., Nelson, B. L., Plumlee, M., Pagnoncelli, B. K. & Rahimian, H. (2022), A classification method for ranking and selection with covariates, in B. Feng, G. Pedrielli, Y. Peng, S. Shashaani, E. Song, C. G. Corlu, L. H. Lee, E. P. Chew, T. Roeder & P. Lendermann, eds, ‘Proceedings of the 2022 Winter Simulation Conference’, pp. 156–167.

- Kim (2006) Kim, S. (2006), Gradient-based simulation optimization, in L. F. Perrone, F. P. Wieland, J. Liu, B. G. Lawson, D. M. Nicol & R. M. Fujimoto, eds, ‘Proceedings of the 2006 Winter Simulation Conference’, pp. 159–167.

- Kushner & Yin (2003) Kushner, H. J. & Yin, G. (2003), Stochastic approximation and recursive algorithms and applications (2nd ed.), Springer.

- Newton et al. (2018) Newton, D., Pasupathy, R. & Yousefian, F. (2018), Recent trends in stochastic gradient descent for machine learning and big data, in M. Rabe, A. A. Juan, N. Mustafee, A. Skoogh, S. Jain & B. Johansson, eds, ‘Proceedings of the 2018 Winter Simulation Conference’, pp. 366–380.

- Pasupathy & Kim (2011) Pasupathy, R. & Kim, S. (2011), ‘The stochastic root-finding problem: Overview, solutions, and open questions’, ACM Transactions on Modeling and Computer Simulation 21(3), 19:1–19:23.

- Peyré & Cuturi (2019) Peyré, G. & Cuturi, M. (2019), ‘Computational optimal transport: With applications to data science’, Foundations and Trends in Machine Learning 11(5-6), 355–607.

- Polyak & Juditsky (1992) Polyak, B. T. & Juditsky, A. B. (1992), ‘Acceleration of stochastic approximation by averaging’, SIAM Journal on Control and Optimization 30(4), 838–855.

- Russo (2020) Russo, D. (2020), ‘Simple Bayesian algorithms for best-arm identification’, Operations Research 68(6), 1625–1647.

- Santambrogio (2015) Santambrogio, F. (2015), Optimal transport for applied mathematicians, Birkhäuser, NY.

- Shen et al. (2021) Shen, H., Hong, L. J. & Zhang, X. (2021), ‘Ranking and selection with covariates for personalized decision making’, INFORMS Journal on Computing 33(4), 1500–1519.

- Shiryaev (2019) Shiryaev, A. N. (2019), Probability-2, Springer.

- Taşkesen et al. (2023) Taşkesen, B., Shafieezadeh-Abadeh, S. & Kuhn, D. (2023), ‘Semi-discrete optimal transport: Hardness, regularization and numerical solution’, Mathematical Programming A199, 1033–1106.

- Villani (2021) Villani, C. (2021), Topics in optimal transportation, American Mathematical Society.

8 Appendix: additional technical lemmas

In this section, we present two stand-alone technical results used in various proofs. The first technical lemma is used in the proof of Lemma 5.1.

Lemma 8.1.

Suppose that is a non-negative function satisfying and for , where . Let satisfy

| (45) |

Then,

| (46) |

Proof: Clearly, if , the integrand in (46) equals zero. Hence, we only need to consider or . For a lower bound, it is sufficient to consider only one case, so we pick the second, i.e., . We derive

| (47) | |||||

| (48) | |||||

| (49) | |||||

| (50) |

where is the antiderivative of with . In this derivation, (47) follows because, if , the integrand in (46) can be made to equal zero by taking . Equation (48) follows by taking the positive part of the absolute value, (49) sets , and (50) applies integration by parts.

For any , we have

| (51) |

To continue bounding (50), let us first consider the case . If this holds, then

and

where (8) follows by (51). Thus, we can continue (50) as

| (53) | |||||

| (54) | |||||

| (55) |

where (53) uses the boundedness of , and (54) follows from (45).

It remains to consider the case . If this holds, then

and

Continuing (50), we have

| (58) |

where (8) uses and , and (8) uses (45). Combining (55) and (58) yields the desired result.

Lemma 8.2.

Let be a non-negative sequence. Suppose that and are fixed constants, and that, for we have

| (59) |

Then,

Proof: Define

It is straightforward to verify that by checking the root of the quadratic equation . Hence,

where (8) follows by the elementary inequality for .

We now show by induction that for all . The inequality obviously holds for . Suppose that it holds for . We consider two cases: and . In the first case, we observe that

where the second inequality is due to the non-negativity of together with the assumption that . In the second case, we observe that

where the first inequality is due to (59) and the assumption that , and the second inequality follows by . This completes the proof.

9 Appendix: proofs

Below, we provide complete proofs for all results that were stated in the text.

9.1 Proof of Lemma 4.3

We observe that w.p. . Then,

which completes the proof.

9.2 Proof of Lemma 4.4

Fix arbitrary constants and such that . Fix and define . Let . Using (28), we derive

| (61) | |||||

Due to Lemma 4.3, we may write for some sufficiently large constant . It is also easy to show that

Combining this with (61), we have

for some suitable .

Pick any and define the event

with an additional special case

We will study the behavior of on for three possible cases representing different ranges of . Specifically, we consider 1) , 2) , and 3) .

Case 1: . By repeating the arguments in the proof of Lemma 4.3, we obtain

| (62) |

On the event , (62) combined with the assumption yields

Case 2: . On the event , we have

| (63) | |||||

| (64) |

where (63) uses the definition of , while (64) uses integral bounds on partial sums. At the same time, on the event , we have , meaning that

| (65) |

We will now bound for Case 2. If the condition of Case 2 holds and is sufficiently large, we have

| (66) |

whence

| (67) |

For any , Azuma’s inequality yields

| (69) |

where (9.2) is due to the inequality

and (69) follows by

for some suitable constant . Applying this result to (67) yields

| (70) |

The remainder of the proof of Case 2 focuses on showing the bound

| (71) |

Since , combining (70) and (71) yields

| (72) |

which will be used later. To show (71), we first observe that

where

We then calculate

Thus, is equivalent to , which can be rewritten as

This holds if and only if , where

It can be seen that by multiplying and dividing the expression by . On the other hand, . Since we are considering , plugging in the definition of yields , whence for large . Therefore, for large , is increasing on , and, if , is decreasing on . In any event, we have

for sufficiently large , thus establishing (71).

Case 3: . On the event , we have . By repeating the derivation of (64), we obtain

| (73) |

Recall that . Plugging in the definition of , we obtain . We also have

whence, for large , we have

Consequently, (73) becomes

| (74) | |||||

On , we have , whence (74) yields

Applying (69) yields

with the second inequality due to . Consequently, for large , we have

the same bound as in (72). Note that the same argument applies to the special case .

9.3 Proof of Lemma 5.1

To avoid notational clutter, we write as simply in this proof, since no other will be considered. Note, however, that we do distinguish between and .

Initially, we proceed exactly as in the proof of Lemma 4.1. By making the same arguments (omitted to avoid redundancy), we derive

where satisfies , and

| (77) | |||||

As in the proof of Lemma 4.1, our goal is to bound the expectation of each term in (77).

For notational convenience, we let for any . As in the proof of Lemma 4.1, let . We also introduce the new notation

and note that

In addition,

In the following, we may assume, without loss of generality, that and satisfies . The bound becomes trivial if due to the concavity of . Furthermore, for any , either or will be non-negative, and a later step in the analysis allows us to only consider one of these.

With these assumptions, we write

where the last line is due to the assumption . We now take expectations to obtain

| (78) | |||||

By repeating arguments from the proof of Lemma 4.1, we obtain

for any . We can then apply Lemma 8.1 and continue (78) as

We then repeat the arguments at the end of the proof of Lemma 4.1 (starting from eq. (26) onwards) to obtain the final bound.

9.4 Proof of Lemma 5.2

To avoid notational clutter, we write as simply in this proof, since no other will be considered. Note, however, that we do distinguish between and .

As in the proof of Lemma 4.2, we apply Lemma 5.1 and obtain

| (79) |

Let . We wish to show that, if , then

| (80) |

To show (80), we consider three cases. First, if , then the left-hand side of (80) becomes and the right-hand side becomes . Second, if , then the left-hand side of (80) becomes and the right-hand side is . Finally, if , the left-hand side of (80) is zero and the right-hand side is .

Combining (79) and (80) yields

| (81) | |||||

| (82) |

where in (81) is a suitable constant obtained by combining the two conditions on , and (82) repeats arguments in the proof of Lemma 4.2. Thus, we have shown the desired result

| (83) |

in the case . To handle the other case , we write

| (84) |

We can make large enough for the right-hand side of (84) to be negative. Since

by concavity of , this means that (83) always holds. This completes the proof.

9.5 Proof of Lemma 5.5

9.6 Proof of Lemma 5.6

Recall that, for any square matrix , . Therefore,

By Hoeffding’s inequality,

Thus,

and (36) follows by a change of variables.

9.7 Proof of Lemma 5.7

Fix and let

where is the density of the distribution. Also let . We first bound by deriving

| (87) | |||||

| (88) |

where (87) is due to

using Assumption 3.2(iii).

9.8 Proof of Lemma 5.8

We use the notation and from Lemma 5.7. Using this notation, and recalling (14), we can write

Then,

and

| (89) | |||||

where (89) follows because .

Recall that is the set of time periods in which the policy is forced to explore the th cost function. Then, for some . Letting , we obviously have . Then, (89) is continued as

| (90) |

9.9 Proof of Lemma 5.9

The overall structure of this proof is very similar to that of Lemma 4.4. We will omit those details that are identical, referring to arguments from the proof of Lemma 4.4 as necessary. As in that proof, we begin by fixing and such that . We let . Again, we use the recursion

where . Let .

Similarly to (61) in the proof of Lemma 4.4, we have

| (92) | |||||

where (92) is obtained by applying Lemmas 5.2-5.3 with appropriate .

Due to Lemma 4.3, we may write for some suitably large constant . By repeating the arguments immediately after (61) in the proof of Lemma 4.4, we have

| (93) | |||||

for some suitable .

Pick any and define two events

where is the constant from Lemma 5.8. We also define an additional special case

Similarly to the proof of Lemma 4.4, we will study the behavior of on for three possible cases representing different ranges of , namely, 1) , 2) , and 3) .

Case 2: . On the event , we continue (93) as

| (94) | |||||

The last two terms in (94) are obtained from the definition of and from the bound on .

Starting with (94), we now repeat the derivation of (64) in the proof of Lemma 4.4 and obtain

| (95) | |||||

By repeating the arguments after the derivation of (64) in the proof of Lemma 4.4, we obtain

| (96) |

for sufficiently large , by analogy with (66). In other words, the additional terms on the right-hand side of (96), which are new to this proof, can be ignored. Therefore, the remainder of Case 2 proceeds exactly as in the proof of Lemma 4.4, and we obtain

by analogy with (72).

Case 3: . On the event , we have . By repeating the derivation of (95), we obtain

Repeating the arguments in the proof of Lemma 4.4, starting with eq. (73), we obtain

| (97) |

for sufficiently large . Again, this essentially allows us to ignore the additional terms on the left-hand side of (97) that are new to this proof. Therefore, the remainder of Case 3 proceeds exactly as in the proof of Lemma 4.4, and we obtain and

Putting Cases 1-3 together. As in the proof of Lemma 4.4, we write

| (99) |

where (9.9) follows from the analysis of Case 1, and (99) is the result of the other two cases. Applying Lemma 5.8, we obtain

whence

Using similar reasoning, we also obtain , whence

| (100) |

By construction, . The coefficient in (100) can be increased to make the bound hold for all . The desired result follows.

9.10 Proof of Proposition 5.1

As in Lemma 5.7, define . Also let

where is the sigma-algebra generated by , , and . By repeating the same arguments as in the proof of Lemma 5.6 (replacing Hoeffding’s inequality with Azuma’s inequality), we can obtain

| (101) |

for any .

Recall that is the set of time periods in which the policy is forced to explore the th cost function. For any , we have where was defined in eq. (35) of Lemma 5.5. By the result of Lemma 5.5,

where . Applying Lemmas 5.8 and 5.9, we may obtain

| (102) |

for and some suitable . Since is of order , we have

| (103) |

for large .

Then, for large , we may derive

| (105) | |||||

| (106) |

In this derivation, (9.10) is due to (101), while (105) applies (103), and (106) follows by (102). Thus, we arrive at the bound

| (107) |

for some suitable .