RemarkRemark \newsiamremarkDefinitionDefinition \newsiamthmCorollaryCorollary \newsiamthmAssumptionAssumption \newsiamthmTheoremTheorem \newsiamthmPropositionProposition \newsiamthmLemmaLemma \headersQMC for unbounded integrands with ISD. Ouyang, X. Wang, and Z. He

Quasi-Monte Carlo for unbounded integrands with importance sampling††thanks: Submitted to the editors DATE. \fundingThis work of the second author was funded by the National Science Foundation of China (No. 720711119). And the third author was funded by the National Science Foundation of China (No. 12071154), Guangdong Basic and Applied Basic Research Foundation (No. 2021A1515010275).

Abstract

We consider the problem of estimating an expectation by quasi-Monte Carlo (QMC) methods, where is an unbounded smooth function on and is a standard normal distributed random variable. To study rates of convergence for QMC on unbounded integrands, we use a smoothed projection operator to project the output of to a bounded region, which differs from the strategy of avoiding the singularities along the boundary of the unit cube in [24]. The error is then bounded by the quadrature error of the transformed integrand and the projection error. If the function and its mixed partial derivatives do not grow too fast as the Euclidean norm goes to infinity, we obtain an error rate of for QMC and randomized QMC (RQMC) with a sample size and an arbitrarily small . However, the rate turns out to be if the functions grow exponentially with a rate of for a constant . Superisingly, we find that using importance sampling with t distribution as the proposal can improve the root mean squared error of RQMC from to for any .

keywords:

Projection method, Growth condition, Quasi-Monte Carlo, Importance sampling1 Introduction

Quasi-Monte Calro (QMC) is an efficient quadrature method to numerically solve the integral problems on the unit cube . Unlike the Monte Carlo (MC) method, the QMC method uses low-discrepancy sequences instead of random sequences (see [3, 19, 4, 6, 26]). If the integrand has bounded variation in the sense of Hardy and Krause (BVHK), then by using the Koksma-Hlawka inequality, QMC with quadrature points yields a deterministic error of , which is asymptotically faster than the MC rate .

In many problems of financial engineering and stochastic control, the underlying solutions can be formulated as expectations of the form with respect to a standard normal distribution (see [13, 8, 27]). To estimate , QMC quadrature rule takes

| (1) |

where is a low-discrepancy point set in , is the cumulative distribution function (CDF) of satisfying

| (2) |

is the composite operator and is the inverse of acting on each component of the argument . Since unbounded functions cannot be BVHK, the Koksma-Hlawka inequality fails to provide the error rate for unbounded functions. This paper is devoted to providing comprehensive error analysis for (1), in which the integrand may have singularities along the boundary of the unit cube .

Owen [24] studied the QMC error for unbounded functions on . He found that QMC error attains a rate of if the integrand satisfies the boundary growth condition

for some , , and all , where denotes the mixed partial derivative of with respect to with and is arbitrarily small. Moreover, randomized QMC (RQMC) method yields the same rate of for the mean error. Recently, He et al. [11] found that this rate also holds for root mean squared error (RMSE) when using scrambled nets (a commonly used RQMC method [22]). It is easy to see that when are all arbitrarily small (we call it the “QMC-friendly” growth condition), the convergence rate achieves the optimal case . In this article, we propose a projection based quasi-Monte Carlo (P-QMC) method and further refine the boundary growth conditions considered in Owen [24]. Using P-QMC or RQMC method, we obtain better convergence results for different boundary growth conditions.

There are some related work on studying unbounded integrands in the context of QMC. Kuo et al. [17] studied the problem of multivariate integration over . They considered the case where the intergrand belongs to some weighted tensor product reproducing kernel Hilbert space and proved that good randomly shifted lattice rules can be constructed component by component to achieve a worst case error of order . Moreover, Kuo et al. [16] improved the results by proving that a rate of convergence close to the optimal order can be achieved with an appropriate choice of parameters for the function space. Based on this, Nichols and Kuo [18] extended the theory of Kuo et al. [16] in several non-trivial directions. In the above work, the constants in the big- bounds can be independent of dimension under appropriate conditions on the weights of the function space. Nuyens and Suzuki [20] introduced a method that scales lattice rules from the unit cube to properly sized boxes on and achieved higher-order convergence that matches the smoothness of the integrand in a certain Sobolev space. Basu and Owen [1] studied three quadrature methods for integrands on the square that may become singular as the point approaches the diagonal line .

Importance sampling (IS) is an efficient variance reduction method in the context of MC (see [9, 15, 21, 7, 28]). However, IS cannot improve the convergence rate of MC. It is natural to ask a question: “Can IS accelerate the convergence rate in QMC?”. He et al. [11] followed the framework of Owen [24] to show that using a proper IS in RQMC can retain the RMSE rate of under the “QMC-friendly” growth condition. In our framework, by employing suitable IS to slow down the growth of the integrand, the error rate of RQMC is improved from to , in which the growth condition is not necessarily “QMC-friendly”.

A key strategy in [24] is to employ an auxiliary function that has a low variation to approximate the unbounded integrand. However, the auxiliary function used in [24] is not smooth enough so that it does not meet the smoothness requirement in Owen [25] for establishing the error rate. Differently, the function constructed based on the projection method is smooth, allowing us to address this issue and obtain the desired rate of convergence when using IS.

In this paper, we prove that when the smooth integrand grows at rate of

with and , the convergence rates of the P-QMC and RQMC methods is . By Owen [24], the convergence rate of RQMC turns out to be if the integrand grows extremely fast with a rate of for a constant . However, we demonstrate that with an appropriate IS, the convergence rate of RQMC improves from to . Our work theoretically establishes that suitable IS can accelerate the convergence rate of QMC. Some integrands after pre-integration (also known as conditioning) [10, 27] arsing from option pricing and smooth loss functions in deep learning both satisfy our growth conditions. Leveraging the findings in this paper, we can obtain the convergence rates of the QMC methods for these problems.

The structure of this paper is as follows. Section 2 introduces the basic concepts of QMC and RQMC methods. Section 3 focuses on the function growth conditions as described in Owen [24], and categorizes these into specific function growth classes. In Section 4, we propose the P-QMC method and obtain the convergence results with respect to different growth classes. Section 5 discusses the P-QMC and RQMC methods using importance sampling, demonstrating that the convergence rates can be significantly improved by using a proper IS. Section 6 provides numerical experiments to confirm the theoretical results. Section 7 concludes the paper. We put lengthy but useful results about the operations of growth classes in Appendix.

2 Preliminaries

In this article, all norms that appear are Euclidean norms. In order to avoid ambiguity, bold symbols, such as and , are used to represent vectors, and normal symbols are used to represent scalars. For example, we use to represent an element of a low-discrepancy point set, and use to represent a component of a -dimensional point . Also, is always used to represent a point in and is always used to represent a point in . Denote Let be a subset of , and be the number of elements in . Let be a vector in whose -th component is if and otherwise.

2.1 Quasi-Monte Carlo methods

QMC method is a quadrature rule for approximating the integration of functions over the unit cube . Instead of using random points in Monte Carlo method, QMC method uses deterministic low-discrepancy sequences. The uniformity of a point set is measured by discrepancy defined below.

Definition 2.1.

For the point set in the unit cube , the star discrepancy of is defined as

where the is the Lebesgue measure and is the family of all subintervals in of the form .

In this paper, we work on smooth functions, which are defined below.

Definition 2.2.

A function defined over is called a smooth function if for any , is continuous. Let be the class of such smooth functions.

For smooth functions, we have a brief definition for the variation in the sense of Hardy and Krause.

Definition 2.3.

If , then the variation of in the sense of Hardy and Krause is

The Koksma-Hlawka inequality [12] provides an error bound for QMC quadrature rule, i.e.,

Note that the error bound depends on the star discrepancy of the sequence used for QMC methods. There are several kinds of low-discrepancy sequences, such as Sobol’ sequece, Halton sequence and Faure sequence (see [19, 8]) with the star discrepancy of for the first points. Therefore, if the function is BVHK, then QMC can attain a rate of convergence , where is arbitrarily small for hiding the logarithm term. In this paper, we focus on digital nets.

Definition 2.4.

An elementary interval of in base b is an interval of the form

for nonnegative integers and .

Definition 2.5.

Let be integers with , and . A point set of points is called a -net in base b if every elementary interval in base of volume contains points of the point set and no elementary interval in base b of volume contains more than points of the point set.

If , then we use the notation -net instead. Every -net in base is a low-discrepancy point set with , whose star discrepancy becomes . We refer to Niederreiter [19] for more details.

Owen [22] provided a scrambling method to randomize the QMC points, resulting in a kind of RQMC methods. The randomized points satisfies and retain the net property. Owen [23, 25] showed that the scrambled net achieves a convergence rate of for smooth integrands, which is better than the rate for the unscrambled net. The following two propositions are taken from Owen [23].

Proposition 2.6.

If is a -net in base b and is the scrambled version of , then is a -net in base b with probability .

Proposition 2.7.

Let be a point in and is the scrambled version of . Then has the uniform distribution on .

3 Growth conditions

To drive the convergence rate of RQMC method for unbounded functions over the unit cube , Owen [24] introduced the boundary growth condition for smooth functions defined on ,

| (3) |

for some , , and all . By compositing the inverse distribution function, our target integrand is then , which is defined in . Therefore, the growth condition for function is

| (4) |

Since is a specific function, we now work out an equivalent condition on for ensuring (4). Let . Then the left hand side of (4) is

where is the Gaussian probability density. Since

the inequality (4) is equivalent to

Note that for any , if is large enough then

Consequently, for any , there exist and such that

| (5) |

As a result, the inequality (4) implies . On the other hand, if , then the inequality (4) holds, leading to a mean error rate of for RQMC [24]. To achieve the convergence rate , all must be arbitrarily small. This leads to the definition of the “QMC-friendly” condition.

Definition 3.1.

We say that satisfies the “QMC-friendly” condition if for any fixed , there exists such that

We next refine the growth conditions in Owen [24] and define some slower-growing function classes (relatively smaller), and use the P-QMC method to obtain better convergence results.

Definition 3.2.

For and , define polynomial growth class,

and define exponential growth class,

where is the class of smooth functions given in Definition 2.2. We say that has polynomial growth if there exists such that , and has exponential growth of order if there exists such that .

When the order , there are functions in the growth class that grow too fast to satisfy the “QMC-friendly” condition. This leads to the definition of fast growth class.

Definition 3.3.

If , then we call the fast growth class. We say that has fast growth, if belongs to the fast growth class.

Note that in the definition of fast growth class, we have reached the minimum restriction on . Because if , there are cases where the integral is infinity. And when , the variance can be infinity, therefore, the MC method does not converge.

The growth conditions we have defined are a further subdivision of Owen’s growth condition. If satisfies Owen’s growth condition (4), then there are three situations,

-

I)

has polynomial growth;

-

II)

has exponential growth of order ;

-

III)

has fast growth.

Note that I) and II) constitute the “QMC-friendly” condition. With the help of the projection operator defined later, if satisfies condition I) or II), P-QMC and RQMC method will yield better results.

In option pricing, under the well known Black-Scholes model [8], the payoff functions can be written as

where is a constant matrix. If and its derivatives up to order have polynomial growth, then by Theorem 7.5 in Appendix, we obtain for some and . However, the function usually has kinks or jumps in option pricing. To reclaim the efficiency of QMC, it was suggested to use the conditioning method to smooth the integrand to obtain a new function . We refer to [10, 27] for more details. From this perspective, our findings in this paper can be applied for many problems in financial engineering.

Now, we focus on the situation where satisfies the fast growth. By relation (5), if then satisfies (4) with , and therefore, by the results of Owen [24], RQMC achieves a mean error rate of . From this standpoint, is a very weak constraint; otherwise, it would not converge. In Section 5, we will prove that with a suitable IS, the P-QMC method achieves the convergence rate of and the RQMC method achieves the convergence rate of for . As a result, we can conclude that using IS accelerates the convergence rate of QMC.

4 The P-QMC method

In this section, we propose a method, called projection based quasi-Monte Carlo method (P-QMC). After composite the projection operator and inverse distribution function, the modified integrand defined on the unit cube is of BVHK, and therefore error analysis can be achieved when using QMC method to the modified integrand.

4.1 Projection operator

We introduce the concept of a projection operator, which projects the space to a bounded region for a constant .

Definition 4.1.

If , for any , we define the projection operator as

If , then acts on each component of , i.e., .

From the definition of , we can see that is a function from to the cube and that it projects each component of a vector in from to . The operator is continuous but not differentiable at some points. We next modify to make it smooth. The following lemma gives us a modification for the one-dimensional case, and the multidimensional case can be defined in the component-wise way.

Lemma 4.2.

(One-dimensional case) For any , there exists a modification of the projection operator , denoted as , which is defined on and satisfies

-

i)

;

-

ii)

has continuous derivative of order 1, i.e., ;

-

iii)

;

-

iv)

;

-

v)

and .

Proof 4.3.

There are many constructive methods for proving this lemma. For instance, we adopt a quadratic function to replace the part that , so that the piecewise function constructed is smooth. Define as:

| (6) |

It is easy to verify that the satisfies the conditions in Lemma 4.2.

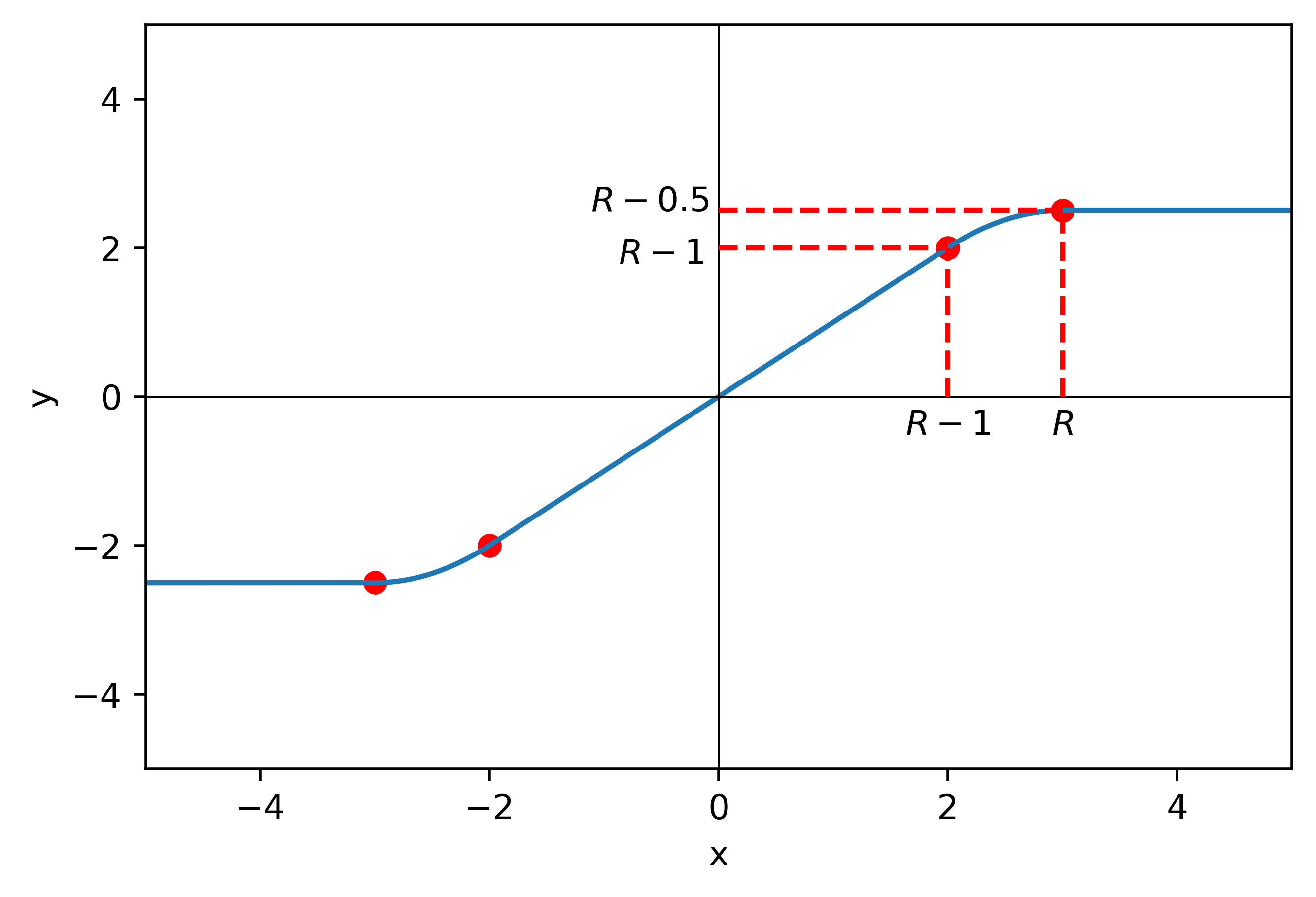

From now on, we will call the projection operator if each component of satisfies the conditions in Lemma 4.2 and with a slight abuse of terminology, call the projection radius. For convenience, we take in Lemma 4.2 and drop the dimension notation if there is no misunderstanding. Figure 1 shows the one-dimensional smoothed projection operator with .

Proposition 4.4.

Denote . If , then . If , then for any point lies on the line segment connecting points and , we have .

Proof 4.5.

It suffices to prove the second statement. There is a , such that . Let . For any , there is an index such that . Therefore,

where the second equality holds because and have the same sign.

4.2 Error analysis for the P-QMC method

In this section, we discuss how to modify the integrand through the projection operator to achieve BVHK and prove the corresponding convergence property. To this end, we modify the integrand by compositing the projection operator , and the integrand changes from to the modified integrand . The following lemma shows that the modified integrand is a smooth function on .

Lemma 4.6.

If , then the modified integrand .

Proof 4.7.

Note that our projection operator is defined on , so the modified integrand is well-defined on . For any ,

The right hand side of the above equality is well-defined on because the projection operator satisfies condition iii) of Lemma 4.2 and the derivative vanishes when approaches or . Therefore, it is continuous on .

To deal with the singularities, Owen [24] used the low variation extension due to Sobol’,

where is Sobol’s extensible with anchor . This extension is not differentiable at some points, implying . Our modified integrand is smooth, allowing to calculate the variation in the sense of Hardy and Krause simply by Definition 2.3. Furthermore, we can apply the results in Owen [25] to achieve higher convergence rate for such a smooth function.

Our P-QMC method uses the modified quadrature method

where is a low-discrepancy point set. We claim that the modified method overcomes the problem of infinite variation in the sense of Hardy and Krause, and moreover, its convergence rate is better than those in Owen [24] and He et al. [11].

The total error of the proposed P-QMC method can be decomposed into the following two parts

| (7) |

We are going to bound the error due to using the projection operator, which is called the projection error. Then, for the QMC error , we calculate the variation of the modified integrand in the sense of Hardy and Krause, and use the Koksma-Hlawka inequality to obtain an upper bound. Both of these errors depend on the projection radius . Finally, we choose an appropriate to balance the two sources of errors and obtain the convergence rate for the total error.

In contrast, if we use the original estimator defined in (1), we will have an additional term called sample error, as shown below

| (8) |

The magnitude of sample error depends on how far the low-discrepancy points we use deviate from the boundaries. In this regard, Owen [24] specifically studied the case of Halton sequences and gave several regions that avoid the origin and other corners so that the sample error vanishes. Calculating sample error is generally a cumbersome task for the P-QMC method. However, if we use the RQMC method and consider the expected error, the sample error can be bounded by the projection error, thereby avoiding the estimation of this term. The next lemma will be used several times in the following proofs.

Lemma 4.8.

If and , then

| (9) |

Proof 4.9.

With , the left hand side of (9) is equal to

where in the first inequality we use

for the case is even, and in the last inequality, we use .

When falls into different growth classes, there are corresponding worst case estimates for the projection error. Note that the mean error can be bounded by the root mean squared error.

Lemma 4.10.

Assume and . For polynomial growth class with , if , then

| (10) |

where and is the integer part of . And for exponential growth class with , if , then

| (11) |

where .

Proof 4.11.

We first prove (10). For any ,

| (12) | ||||

where we use and by Lemma 4.2. Using the polar coordinates transformation, the right hand side of (12) can be written as

where is the the integer part of , at the first inequality we use the fact that and at the second inequality we use and , and at the last inequality, we use Lemma 4.8.

The key to bound the QMC error lies in calculating the variation of the modified integrand in the sense of Hardy and Krause. For in different growth classes, corresponding upper bound estimates for the variation are given in the following lemma.

Lemma 4.12.

For every fixed and projection radius ,

| (14) |

| (15) |

Proof 4.13.

For the proof of (14), note that by Lemma 4.6, the modified integrand . Therefore, we can use the definition of the variation in the sense of Hardy and Krause for smooth functions, i.e.,

It suffices to analyze every term in the right hand side of the above equality. Recall the relation (2) for distribution function .

| (16) |

where we use and the conditions iii) and iv) in Lemma 4.2 for the smooth projection operator . Integrating both sides of (16) and changing the variable from to , we have

| (17) | ||||

where is the complement of . It follows from the above inequality that

Therefore, (14) holds. For the proof of (15), it suffices to replace the in (17) with .

The projection operator plays a crucial role in computing the variation of functions in the sense of Hardy and Krause. Through compositing the projection operator, the non-zero region of the mixed partial derivative of the modified integrand is restricted by , so the variation in the sense of Hardy and Krause can be bounded. By combining the two lemmas above, we obtain the following error bounds.

Theorem 4.14.

Let be a low-discrepancy point set. The P-QMC method to approximate the integral is

| (18) |

(I) For polynomial growth class , by choosing , we obtain

| (19) |

(II) For exponential growth class with order , by choosing , we obtain

| (20) |

Proof 4.15.

For the proof of (19), note that

| (21) | ||||

| (22) |

where and are constants. The first term of (21) is obtained by Koksma-Hlawka inequality and the second term is due to (10) in Lemma 4.10. To make magnitude of the both term of (22) approximately the same, we choose , and then the second term is and the first term is . Therefore, by taking supreme at the both sides of (22), we obtain (19). The proof for (20) is straight forward.

In both cases of Theorem 4.14, the convergence rate is , and all we need to notice is that for any and , with ,

However, the results in Theorem 4.14 offer a more detailed analysis compared to the results presented in Owen [24]. These findings indicate that as the function grows faster, the performance of the QMC method becomes worse.

Corollary 4.16.

Let be an RQMC point set used in the estimator given by (1) such that each and

where is a constant independent of .

(I) For the polynomial growth class with ,

(II) For the exponential growth class with order ,

Proof 4.17.

When using the RQMC point set as samples, we can drop the projection operator and simply use as the estimator. The RMSE rate is still the same. Due to Propositions 2.6 and 2.7, a scrambled -net satisfies the condition in Corollary 4.16. Owen [24] only provided the convergence rate in the sense of mean error. He et al. [11] showed that this rate holds also for RMSE by using scrambled digital nets. But this is not true if using other randomization methods, such as digitally shifted nets. In contrast, we use a different framework to provide the RMSE rate for general RQMC point sets satisfying , including both digitally shifted nets and scrambled nets.

5 Importance sampling based methods

Importance sampling methods reduce variance and speed up convergence in Monte Carlo (MC) methods by choosing a suitable importance density. However, in QMC methods, there is no intuitive way to theoretically justify the role of importance sampling as in MC methods.

We will show theoretically how importance sampling improves QMC. We use a distribution with heavier tails than normal to achieve two things. First, as the projection radius goes to infinity, importance sampling preserves the convergence rate of the projection error to zero. Second, the heavy-tailed density slows down the QMC error divergence to infinity significantly. Moreover, by applying the importance sampling and replacing the low-discrepancy points with scrambled net, we obtain the convergence rate which is better than Owen [24] and He et al. [11].

We give a brief introduction to the importance sampling method. Suppose that and are the density functions of -dimensional random variables and , respectively, then for any is integrable under the measure induced by , we have

where

| (23) |

is the weighted function obtained after using importance sampling. Moreover, suppose that is a -dimensional random variable with each component being independent of each other, i.e., the density function of has the form

| (24) |

where is the marginal density function of . Let be the distribution function of . For , denote .

Our method is to apply the projection operator to and using the IS-based P-QMC method to obtain the quadrature rule

| (25) |

where is a low-discrepancy point set. Moreover, if is a scrambled -net, then we drop the projection operator and use IS-based RQMC method to obtain the estimator

| (26) |

We claim that our IS-based P-QMC and IS-based RQMC method can give the convergence rate for integrands in fast growth classes (see Definition 3.3), which are not “QMC-friendly”, and achieve better convergence rates of and , respectively. Note that is a larger set, so our convergence rate still holds for other growth conditions. In the following parts, we consider that has the fast growth, i.e., .

5.1 Importance sampling based P-QMC methods

In this part, we derive the projection error caused by the projection method for the integrand after importance sampling, and then we derive the upper bound of variation in the sense of Hardy and Krause. By selecting an appropriate projection radius , we obtain the convergence rate of importance sampling based P-QMC method. The following lemma provides an estimate for the derivatives of the weighted function .

Lemma 5.1.

If and , then

| (27) |

Proof 5.2.

Note that the right hand side of (27) is monotonically decreasing with respect to when and converge to 0 when . Therefore, there exists a constant depending only on , which dominates .

The following lemma estimates the mean squared error which dominates the projection error.

Lemma 5.3.

Assume and . For every and satisfying and , we have

| (30) |

Proof 5.4.

Denote . Note that by the definition of projection operator in (6), for any . Therefore,

| (31) |

where is the density function of . By the Lagrange mean value theorem, we obtain

| (32) |

where lies on the line segment connecting points and , and represents the gradient operator. Note that

| (33) |

And if , then by Lemma 5.1 and Remark 5.1, we obtain

| (34) |

In (34), note that by Proposition 4.4, for any and by Remark 5.1, the function is decreasing with respect to when . Therefore,

| (35) |

Next, we aim to demonstrate that importance sampling can decelerate the rate at which the variation, in the sense of Hardy and Krause, diverges towards infinity. Combining the results of Lemma 5.1 and Remark 5.1, we obtain the following result.

Lemma 5.5.

After using importance sampling, the variation of the modified integrand in the sense of Hardy and Krause has a uniform upper bound for every and satisfying

| (36) |

Proof 5.6.

The proof is nearly the same as in Lemma 4.12, and all we need is to note that by Lemma 5.1 and Remark 5.1, every mixed derivative of is dominated by some constant only depends on and . Therefore, for any , we can rewrite (17) as

and (36) follows from that there are at most such terms in the definition of (see Definition 2.3).

Combining Remark 5.1 and Lemma 5.5 and using the same method in the proof of Theorem 4.14, we obtain the convergence rate for importance sampling based P-QMC method.

Theorem 5.7.

Assume and . Let be a low-discrepancy point set. By choosing , we obtain

Note that this theorem tells us that by combining importance sampling, for polynomial growth classes, the degree of on the denominator of the convergence rate has been reduced from to . For exponential growth classes, there is no exponential term on the denominator of the convergence rate. Moverover, for fast growth class, without IS, the convergence rate is , and by applying IS, we achieve the convergence rate . This shows that after combining importance sampling, theoretically we obtain a faster convergence rate.

5.2 Importance sampling based RQMC methods

The results of the previous sections are based on the framework of the Koksma-Hlawka inequality, so they hold for any low-discrepancy point set. When replacing the QMC points with randomized QMC (RQMC) points, we obtain the importance sampling based RQMC method. This method can achieve a faster convergence rate of .

Owen [23, 25] gave a variance estimation of scrambled net for smooth functions on , and the variance is related to the infinity norm of the integrand. One thing to note is that the original integrand does not satisfy the condition, because it has singularities. However, when we use the projection method, that is, the original integrand is composed with the projection operator, the modified integrand or is smooth and we can estimate its infinity norm. The following result is from Owen [25], which consider the scrambled -net (see Definition 2.5).

Lemma 5.8.

Let be a smooth function. Suppose that is a -net in base with . If is the scrambled version of , then with and ,

| (37) |

where is a constant that depends only on .

Recall that . Therefore, it satisfies the condition of the Lemma 5.8. Next, we give an upper bound of the infinity norm of the modified integrand .

Lemma 5.9.

Suppose that , then for and and satisfying , there exists a constant such that

| (38) |

Furthermore, we impose some specific restrictions on the importance density. Assumme is square integrable. We consider separately the cases where the importance density has polynomial and exponential growth. Define the following two sets:

As before, we can balance the errors by choosing an appropriate projection radius and drive the convergence rate for the IS-based RMQC method.

Theorem 5.11.

Let be a scrambled -net in base with , and suppose . We have

| (40) |

and

Proof 5.12.

It suffices to prove (40). Let and let be a scrambled -net. We have

| (41) | ||||

For the first term of the right hand side of (41),

| (42) | ||||

| (43) |

where in (42), we use the Cauchy–Schwarz inequality, and (43) follows from that every has the uniform distribution on (see Proposition 2.7).

Note that the second term of the right hand side of (41) is and the third term is bounded by . Therefore, we obtain

| (44) |

Using the results in Lemma 5.8 and Lemma 5.9, when is large enough so that , the first term of the right hand side of (44) has the following upper bounds.

| (45) | ||||

| (46) |

where is a constant only depends on . The inequality (45) follows from Lemma 5.9, and (46) follows from .

It is important to note that without importance sampling, the RQMC method cannot achieve a higher convergence rate of , due to the infinity norm of the derivatives of the integrand cannot be controlled by a constant and the right hand side of (38) is , thus we can not find a projection radius to make the projection error and QMC error both converge at a rate of

The conditions for Theorems 5.7 and 5.11 are about and . If we fix an appropriate importance density, the conditions of the theorems can be directly restricted to . The following section will provide a detailed discussion on this perspective. Note that, the next section uses the -distribution as an example of an IS proposal. However, our framework is highly versatile, and many distributions with heavier tails than the normal distribution may meet the conditions of Theorem 5.11 and be used as an IS proposal.

5.3 The choice of the IS density

We use a heavy-tailed distribution as the IS proposal to accelerate the convergence rate. We introduce a class of importance densities that satisfy the conditions of the above theorems. Take the -distribution as the proposal of importance sampling. The density function of is

| (48) |

Each component of is a -distribution with parameter . Let . We can easily verify that there exist and , such that

and

Therefore, for any function with , using the (3) of Theorem 7.2 in Appendix, we have that for any , there exist , such that

Note that when for all . By choosing the small enough so that and , we obtain

Therefore, it satisfies the conditions in Theorems 5.7 and 5.11, and we can drive the following theorem.

Theorem 5.13.

Assume satisfies (48) with for all and . Let .

(I) If is a low-discrepancy point set, then by choosing , we have

(II) If is a scrambled -net in base with , then

If we choose such an importance density with polynomial growth, then IS-based P-QMC or IS-based RQMC method can handle the case where the function , which is not “QMC-friendly”, and achieve the convergence rate of and , respectively. However, by the results of Owen [24], the convergence rate of QMC is without IS. This shows that, IS does accelerate the convergence rate in QMC.

6 Numerical results

In numerical experiments, we use the Sobol’ sequence, whose first points constitute a -net in base , and use the scrambled Sobol’ sequence in RQMC methods.

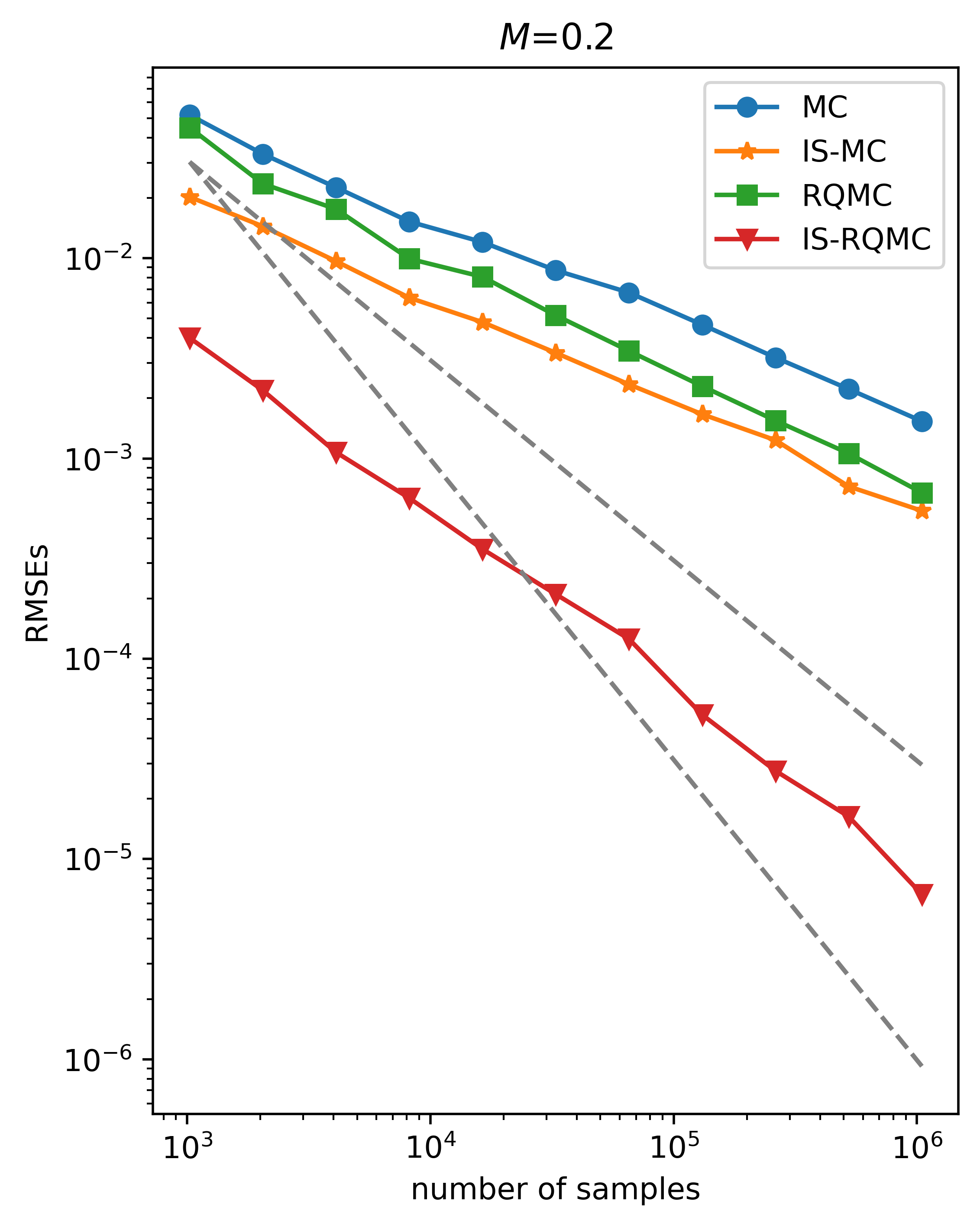

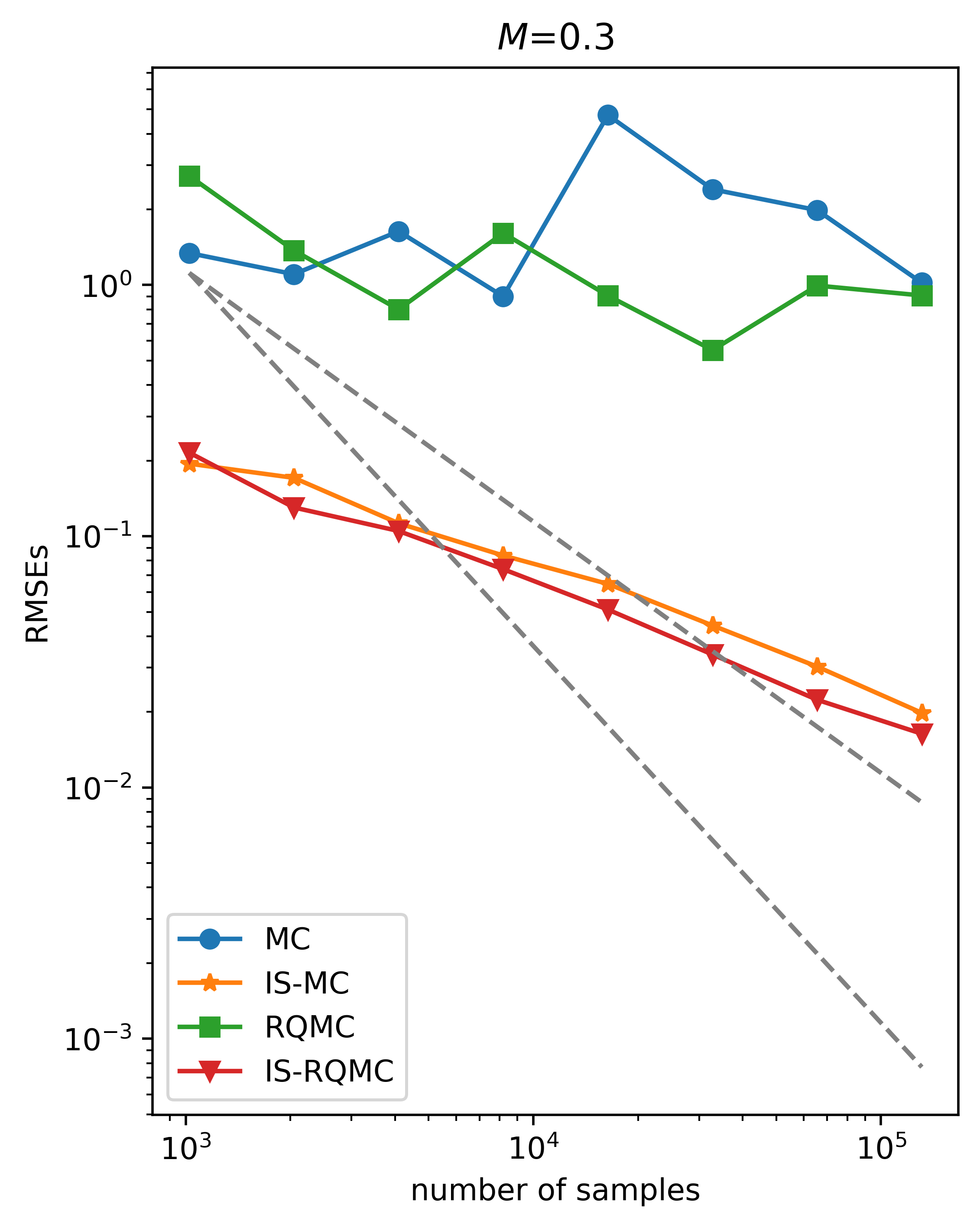

We focus on comparing the convergence results of RQMC and IS-based RQMC on the fast growth class. We use the test function

where has an impact on the boundary growth and we take to ensure for all . It is easy to verify that this function does not satisfy the “QMC-friendly” condition, and so using RQMC directly without IS will result in a convergence rate of . We take the -distribution with as the proposal of importance sampling (see details in Section 5.3). In comparison, the convergence rate of IS-based RQMC is imporved to . RMSEs in the following numerical results are computed based on 100 independent repetitions.

For , we compare the RMSEs of MC, IS-based MC, RQMC and IS-based RQMC as the sample size increases in Figure 2. The figure shows that IS-based RQMC has much smaller RMSE and better convergence rate than MC, IS-based MC and RQMC.

Note that when , the test function has fast growth and . Without importance sampling, RQMC converges at a rate and the convergence rate of MC is , while if we use importance sampling, the convergence rate will reach . This numerical result agrees with our theoretical results.

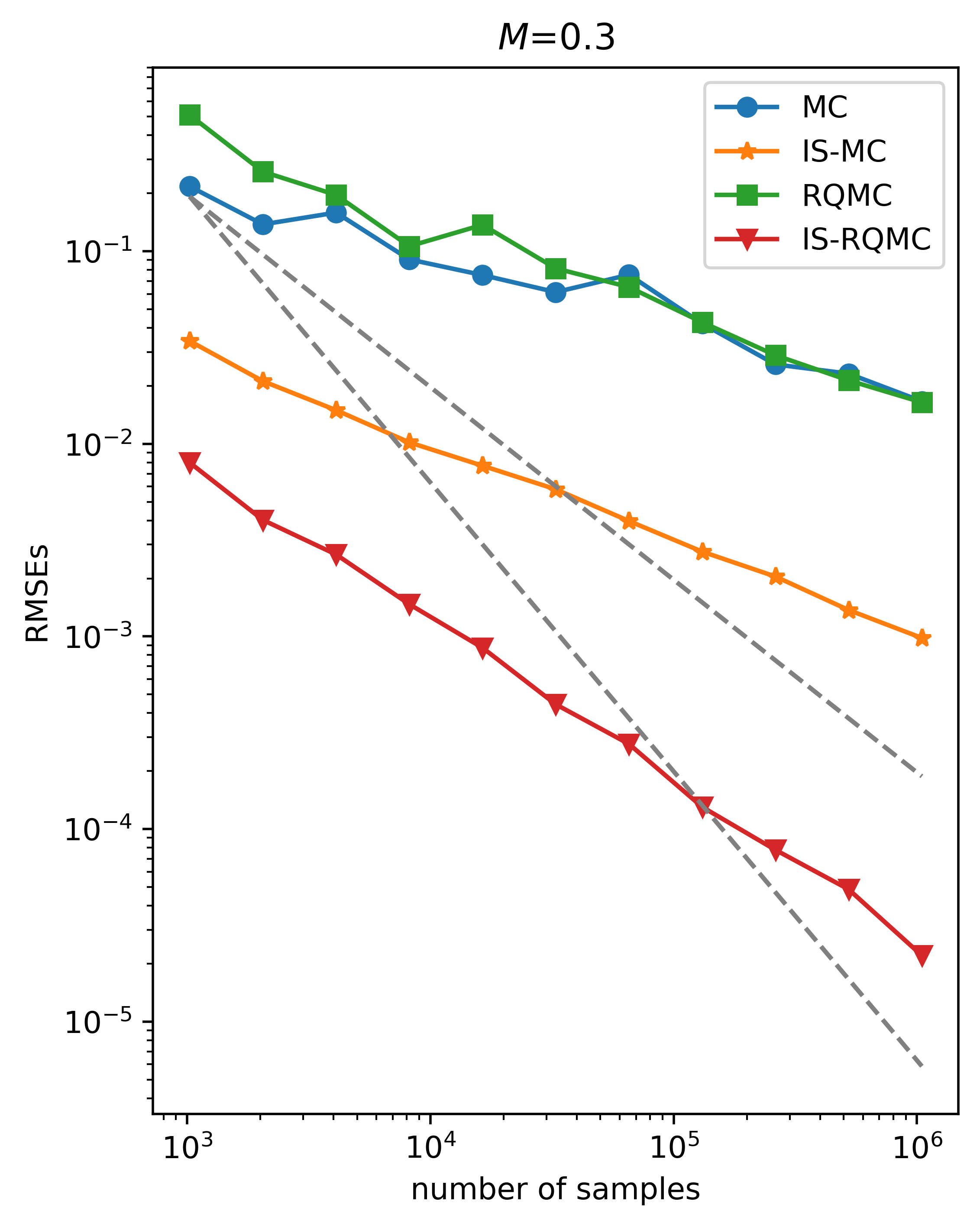

When , the variance of is infinite, so MC does not converge and RQMC has a bad performance. However, IS-based RQMC still has a good convergence rate when the sample is large enough. Note that after IS, the variance of is finite, so the IS-based MC also converges.

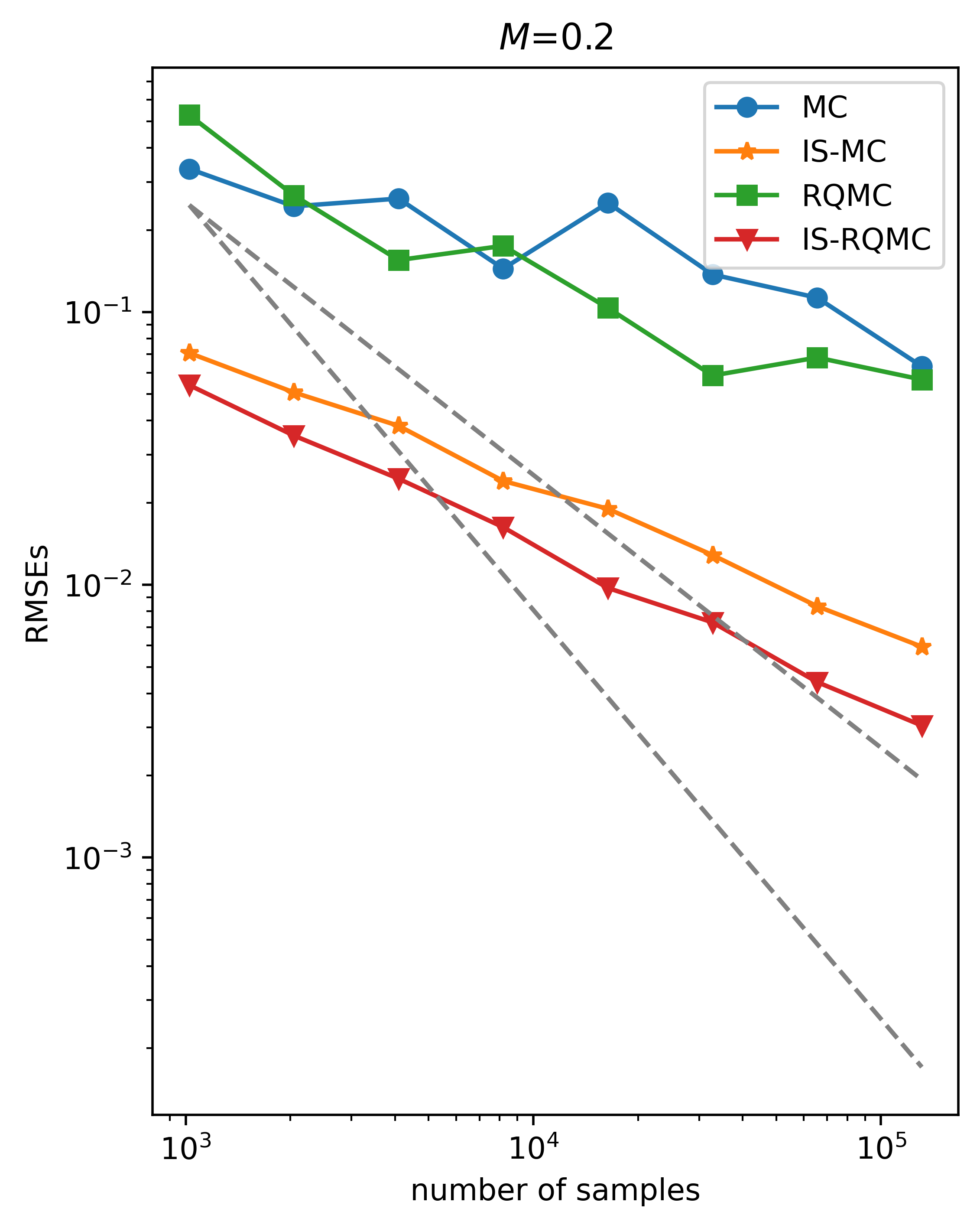

When we increase to 30, the convergence rate of IS-based RQMC in then sense of RMSE is . Therefore, with a limited number of samples, the slope of the IS-based RQMC curve may not reach . However, the numerical results in Figure 3 indicate that IS-based RQMC is still the most effective method.

Note that we only provided the -distribution as an example. In fact, any distribution that has heavier tails than the normal distribution, such as some distributions in the exponential family, may satisfy our conditions to be used as a proposal for IS and achieve a higher convergence rate of . We find that reducing variance is not the only criterion for IS in QMC. The picture on the left side of Figure 2 shows that the effect of IS-based RQMC is significantly improved when the variance is not reduced too much. How to choose an IS proposal that yields better results for a given integrand, that will be a question for our future research.

7 Conclusion

Using the projection based quasi-Monte Carlo method on various growth classes, we attained more refined results than Owen [24]’s. Our framework dictates that the convergence rate is contingent upon the growth condition of the integrand. For integrand with fast growth, both QMC and MC methods manifest inferior performance. Nevertheless, by using importance sampling with a heavy-tailed proposal, we achieved better convergence rates. This assertion is corroborated by our numerical experiments. In this paper, we do not focus on reducing the Monte Carlo variance through importance sampling. It is desirable to develop a good importance sampling to reduce Monte Carlo variance while retaining the faster convergence rate of QMC. This is left for future work.

Appendix

In many problems, the integrand that we consider, such as the loss function in deep learning, has a very complex form (it is obtained by some basic operations on different functions). We refer to Huré et al. [14] and Beck et al. [2] for details. For such a complex integrand, it is not easy to verify directly which growth class it belongs to, but the growth conditions of the functions that compose the integrand are easy to verify. Therefore, we need to discuss what kind of growth class we get after applying some operations on the basic growth classes. We use the following notation.

Definition 7.1.

If and are two function classes, then for , we define

and we define the corresponding scalar operations for the case that is a constant.

The growth classes that we defined have properties similar to those of a linear space, except that the corresponding parameters may change. From Theorem 4.14, we know that for polynomial case, the convergence rate is determined by , and for exponential case, the convergence rate is determined by and . Therefore, in the following calculations, we will focus on the changes of these coefficients, and the specific forms of other coefficients are irrelevant for our analysis.

Theorem 7.2.

Assume are all positive.

-

(1)

Scalar multiplication.

Assume is a constant. For the polynomial case,

For the exponential case,

-

(2)

Addition.

The first case is the addition of two polynomial growth classes. There exist and , such that

The second case is the addition of two exponential growth classes. If , then there exists , such that

If , then

The third case is the addition of an exponential growth class and a polynomial growth class. There exists , such that

-

(3)

Multiplication.

The first case is the multiplication of two polynomial growth classes. There exist and , such that

The second case is the multiplication of two exponential growth classes. If , then for any , there exists , such that

If , then there exists , such that

The third case is the multiplication of an exponential growth class and a polynomial growth class. For any , there exists , such that

Proof 7.3.

The results of scalar multiplication are easy to verify. We briefly prove the other results. For any

it is easy to verify that the result holds by choosing appropriate for addition . For multiplication , it suffices to note that for fixed ,

As for exponential case, note that for any , there exists constant which depends on , such that

It is easy to verify the conclusion of the theorem through these calculations.

For investigating composition operations, we need additional symbols. Let be the -fold index, i.e.,

The module of is defined by

and for , we say if holds for every . We take

The derivative notation to be used is then

Definition 7.4.

For and , define

and

The function class defined here is different from Definition 3.2, since we need to take the partial derivatives of the composited function with respect to its arguments several times.

Theorem 7.5.

Assume integers . For the composition of two polynomial growth classes, there exist and , such that

For an exponential growth class compositing a polynomial growth class, there exist and , such that

For a polynomial growth class compositing an exponential growth class, there exist and , such that

Proof 7.6.

It suffices to prove the case and . For any

Note that

Similarly,

Note that for any fixed , ever term of can be written as the combination of

under the operators , and scalar multiplication. More precisely, by multivariate Faa di Bruno formula (see Theorem 2.1 in [5]), we have

| (49) |

where

The functions in (49) are all in the corresponding growth classes. Using the same method in Theorem 7.2, one can prove the desired results.

References

- [1] K. Basu and A. B. Owen, Quasi-Monte Carlo for an integrand with a singularity along a diagonal in the square, Contemporary Computational Mathematics-A Celebration of the 80th Birthday of Ian Sloan, (2018), pp. 119–130.

- [2] C. Beck, S. Becker, P. Grohs, N. Jaafari, and A. Jentzen, Solving the Kolmogorov PDE by means of deep learning, Journal of Scientific Computing, 88 (2021), pp. 1–28.

- [3] R. E. Caflisch, Monte Carlo and quasi-Monte Carlo methods, Acta numerica, 7 (1998), pp. 1–49.

- [4] R. E. Caflisch, W. J. Morokoff, and A. B. Owen, Valuation of mortgage-backed securities using Brownian bridges to reduce effective dimension, Journal of Computational Finance, 1 (1997), pp. 27–46, https://api.semanticscholar.org/CorpusID:115755914.

- [5] G. Constantine and T. Savits, A multivariate Faa di Bruno formula with applications, Transactions of the American Mathematical Society, 348 (1996), pp. 503–520.

- [6] J. Dick and F. Pillichshammer, Digital nets and sequences: discrepancy theory and quasi–Monte Carlo integration, Cambridge University Press, Cambridge, 2010.

- [7] J. Dick, D. Rudolf, and H. Zhu, A weighted discrepancy bound of quasi-Monte Carlo importance sampling, Statistics & Probability Letters, 149 (2019), pp. 100–106.

- [8] P. Glasserman, Monte Carlo methods in financial engineering, Springer, New York, 2004.

- [9] P. Glasserman, P. Heidelberger, and P. Shahabuddin, Asymptotically optimal importance sampling and stratification for pricing path-dependent options, Mathematical Finance, 9 (1999), pp. 117–152.

- [10] A. Griewank, F. Y. Kuo, H. Leövey, and I. H. Sloan, High dimensional integration of kinks and jumps—smoothing by preintegration, Journal of Computational and Applied Mathematics, 344 (2018), pp. 259–274.

- [11] Z. He, Z. Zheng, and X. Wang, On the error rate of importance sampling with randomized quasi-Monte Carlo, SIAM Journal on Numerical Analysis, 61 (2023), pp. 515–538.

- [12] E. Hlawka and R. Mück, Über eine transformation von gleichverteilten folgen II, Computing, 9 (1972), pp. 127–138.

- [13] J. C. Hull, Options futures and other derivatives, Pearson Education India, New York, 2003.

- [14] C. Huré, H. Pham, and X. Warin, Deep backward schemes for high-dimensional nonlinear PDEs, Mathematics of Computation, 89 (2020), p. 1.

- [15] A. Y. C. Kuk, Laplace importance sampling for generalized linear mixed models, Journal of Statistical Computation and Simulation, 63 (1999), pp. 143–158.

- [16] F. Y. Kuo, I. H. Sloan, G. W. Wasilkowski, and B. J. Waterhouse, Randomly shifted lattice rules with the optimal rate of convergence for unbounded integrands, Journal of Complexity, 26 (2010), pp. 135–160.

- [17] F. Y. Kuo, G. W. Wasilkowski, and B. J. Waterhouse, Randomly shifted lattice rules for unbounded integrands, Journal of Complexity, 22 (2006), pp. 630–651.

- [18] J. A. Nichols and F. Y. Kuo, Fast CBC construction of randomly shifted lattice rules achieving convergence for unbounded integrands over in weighted spaces with POD weights, Journal of Complexity, 30 (2014), pp. 444–468.

- [19] H. Niederreiter, Random Number Generation and Quasi-Monte Carlo Methods, SIAM, Philadelphia, PA, 1992.

- [20] D. Nuyens and Y. Suzuki, Scaled lattice rules for integration on achieving higher-order convergence with error analysis in terms of orthogonal projections onto periodic spaces, Mathematics of Computation, 92 (2023), pp. 307–347.

- [21] A. Owen and Y. Zhou, Safe and effective importance sampling, Journal of the American Statistical Association, 95 (2000), pp. 135–143.

- [22] A. B. Owen, Randomly permuted (t,m,s)-nets and (t, s)-sequences, in Monte Carlo and Quasi-Monte Carlo Methods in Scientific Computing, H. Niederreiter and P. J.-S. Shiue, eds., New York, NY, 1995, Springer New York, pp. 299–317.

- [23] A. B. Owen, Scrambled net variance for integrals of smooth functions, The Annals of Statistics, 25 (1997), pp. 1541–1562.

- [24] A. B. Owen, Halton sequences avoid the origin, SIAM Review, 48 (2006), pp. 487–503.

- [25] A. B. Owen, Local antithetic sampling with scrambled nets, The Annals of Statistics, 36 (2008), pp. 2319–2343.

- [26] A. B. Owen, Monte carlo theory, methods and examples, 2013.

- [27] C. Zhang and X. Wang, Quasi-Monte Carlo-based conditional pathwise method for option Greeks, Quantitative Finance, 20 (2020), pp. 49–67.

- [28] C. Zhang, X. Wang, and Z. He, Efficient importance sampling in quasi-Monte Carlo methods for computational finance, SIAM Journal on Scientific Computing, 43 (2021), pp. B1–B29.