Cross-Prediction-Powered Inference

Abstract

While reliable data-driven decision-making hinges on high-quality labeled data, the acquisition of quality labels often involves laborious human annotations or slow and expensive scientific measurements. Machine learning is becoming an appealing alternative as sophisticated predictive techniques are being used to quickly and cheaply produce large amounts of predicted labels; e.g., predicted protein structures are used to supplement experimentally derived structures, predictions of socioeconomic indicators from satellite imagery are used to supplement accurate survey data, and so on. Since predictions are imperfect and potentially biased, this practice brings into question the validity of downstream inferences. We introduce cross-prediction: a method for valid inference powered by machine learning. With a small labeled dataset and a large unlabeled dataset, cross-prediction imputes the missing labels via machine learning and applies a form of debiasing to remedy the prediction inaccuracies. The resulting inferences achieve the desired error probability and are more powerful than those that only leverage the labeled data. Closely related is the recent proposal of prediction-powered inference [1], which assumes that a good pre-trained model is already available. We show that cross-prediction is consistently more powerful than an adaptation of prediction-powered inference in which a fraction of the labeled data is split off and used to train the model. Finally, we observe that cross-prediction gives more stable conclusions than its competitors; its confidence intervals typically have significantly lower variability.

1 Introduction

As data-driven decisions fuel progress across science and technology, ensuring that such decisions are reliable is of critical importance. The reliability of data-driven decision-making rests on having access to high-quality data on one hand, and properly accounting for uncertainty on the other.

One frequently discussed issue is that acquiring high-quality data often involves laborious human labeling, or slow and expensive scientific measurements, or overcoming privacy concerns when human subjects are involved. Machine learning offers a promising alternative: sophisticated techniques such as generative modeling and deep neural networks are being used to cheaply produce large amounts of data that would otherwise be too expensive or time-consuming to collect. For example, tools to predict protein structure are supporting wide-ranging research in biology [22, 45, 9, 27]; large language models are being used to generate difficult-to-aggregate information about materials that can be used to fight climate change [53]; predictions of socioeconomic and environmental conditions based on satellite imagery are being used for downstream policy decisions [20, 43, 4, 35]. This increasingly common practice, marked by supplementing high-quality data with machine learning outputs, calls for new principles of uncertainty quantification.

In this work we study this problem in the semi-supervised context, where labels are scarce but features are abundant. For example, precise measurements of environmental conditions are difficult to come by but satellite imagery is abundant. Due to its volume, satellite imagery is routinely used in combination with computer vision algorithms to predict a range of factors on a global scale, including deforestation [18], poverty rates [20], and population densities [33]. These predictions provide a compelling substitute for resource-intensive ground-based measurements and surveys. However, it is crucial to acknowledge that, while promising, the predictions are not infallible. Consequently, downstream inferences that uncritically treat them as ground truth will be invalid.

We introduce cross-prediction: a broadly applicable method for semi-supervised inference that leverages the power of machine learning while retaining validity. Assume a researcher holds both a small labeled dataset and a large unlabeled dataset, and they seek inference—i.e., a p-value or a confidence interval—about a population-level quantity such as the mean outcome or a regression coefficient. Cross-prediction carefully leverages black-box machine learning to impute the missing labels, resulting in both valid and powerful inferences. The validity is a result of a particular debiasing step; the power is a result of using sophisticated predictive techniques such as deep learning or random forests. We show that the use of black-box predictions on the unlabeled data can lead to a massive improvement in statistical power compared to using the labeled data alone.

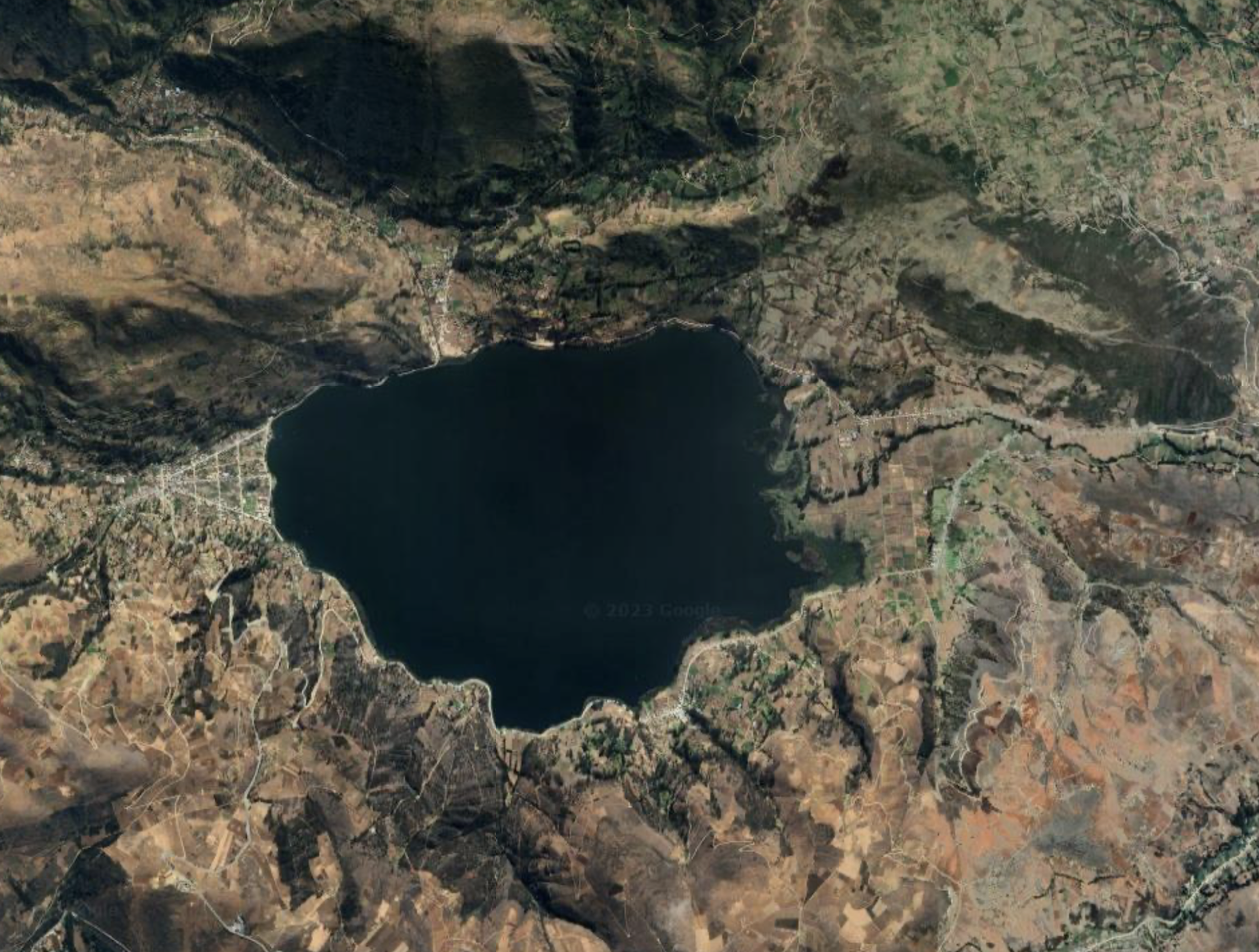

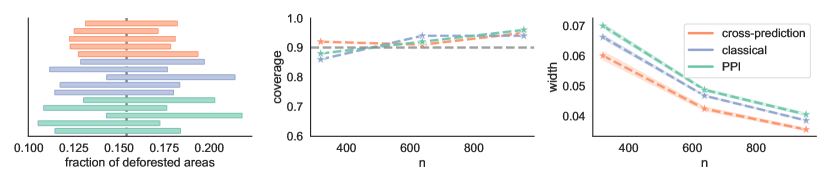

Cross-prediction builds upon the recent proposal of prediction-powered inference [1]. Unlike prediction-powered inference, we do not assume that our researcher already has access to a predictive model for imputing the labels. Rather, to apply prediction-powered inference, the researcher would need to use a portion of the labeled data to either train a model from scratch or fine-tune an off-the-shelf model. We show that this leads to a suboptimal solution. Consider the following example studied by Angelopoulos et al. [1]. The goal is to form a confidence interval for the fraction of the Amazon rainforest that was lost between 2000 and 2015. A small number of “gold-standard” deforestation labels for certain parcels of land are available, having been collected through field visits [10]. In addition, satellite imagery is available for the entire Amazon; see Figure 1 for Google Earth Engine (GEE) examples used in the deforestation study of Bullock et al. [10]. Angelopoulos et al. apply prediction-powered inference after using a portion of the labeled data and XGBoost [12] to fine-tune a regression-tree-based predictor of forest cover [41]. Our work offers an alternative: we can avoid data splitting and instead apply cross-prediction, still with XGBoost, to perform the fine-tuning. By doing so, we significantly reduce the size of the confidence interval, as seen in Figure 2. This trend will be consistent throughout our experiments: cross-prediction is more efficient than prediction-powered inference with data splitting. Figure 2 also shows that cross-prediction outperforms “classical” inference, which forms a confidence interval based on gold-standard labels only and simply ignores the unlabeled data. Additional details about these experiments can be found in Section 7.2.

Another important takeaway from Figure 2 is that cross-prediction gives more stable inferences: the confidence intervals have lower variability than the intervals computed via baseline approaches. Intuitively, classical inference has higher variability due to the smaller sample size, while prediction-powered inference has higher variability due to the arbitrariness in the data split. We will quantify the stability of cross-prediction in our experiments in Section 7, showcasing its superiority across a range of examples, see Table 4.

Our work is also related to the literature known as semi-supervised inference [51]. The main difference between existing approaches and our work is that our proposal leverages black-box machine learning methods, allowing for more complicated data modalities (such as high-dimensional imagery) and more sophisticated ways of leveraging the unlabeled data. We elaborate on the relationship to prior work in Section 2.1.

2 Problem setup

We study statistical inference in a semi-supervised setting, where collecting high-quality labels is challenging but feature observations are abundant. Formally, we have a dataset consisting of i.i.d. feature–label pairs, . In addition, we have a dataset consisting of unlabeled data points, , where denotes the marginal distribution over features according to . We are most interested in the regime where , as in the case where feature collection is far cheaper than label collection.

Our goal is to perform inference on a property of the data-generating distribution , such as the mean outcome, a quantile of the outcome distribution, or a regression coefficient. Our proposal handles all estimands defined as a solution to an M-estimation problem:

| (1) |

for a convex loss function . Here and throughout, denotes a generic sample from independent of everything else. All of the aforementioned estimands can be cast in the form (1). For example, if the target of inference is the mean outcome, , then minimizes the squared loss:

| (2) |

Note that the estimand (and thus the loss) will sometimes only depend on a subset of the features or only on the outcome , as in Eq. (2). Below, we write for short.

The main question we address is this: how should we leverage the unlabeled data to achieve both valid and powerful inference? Validity alone is an easy target: we can simply dispense with the unlabeled data and find the classical estimator , defined as

| (3) |

For all standard estimands defined via M-estimation—including means, quantiles, linear regression coefficients—there are off-the-shelf confidence intervals around that cover with a desired probability in the large-sample limit (see, e.g., [25, 46]). The classical estimator and the corresponding confidence intervals shall be the main comparison points used to evaluate the performance of cross-prediction.

2.1 Related work

We discuss the relationship between our work and most closely related technical scholarship.

Semi-supervised inference.

Our work falls within the literature known as semi-supervised inference [51]. Most existing work develops methods specialized to particular estimation problems, such as mean estimation [51, 52], quantile estimation [11], or linear regression [3, 44]. One exception is the recent work of Song et al. [42], who also study general M-estimation. Their approach uses a projection-based correction to the classical loss (3) based on simple statistics from the unlabeled data, such as averages of low-degree polynomials of the features. Unlike existing proposals, our approach is based on imputing the missing labels using black-box machine learning methods, allowing for more complicated data modalities and more intricate ways of leveraging the unlabeled data. For example, it is unclear how to apply existing methods when the features are high-dimensional images. We also note that the semi-supervised observation model has been long studied in semi-supervised learning [55, 47, 54]. However, in this literature the goal is prediction, rather than inference.

Prediction-powered inference.

The core idea in this paper is to correct imputed predictions, and this derives from the proposal of prediction-powered inference [1]. However, a key assumption in prediction-powered inference is that, in addition to a labeled and an unlabeled dataset, the analyst is given a good pre-trained machine learning model. We make no such assumption. To apply the theory of prediction-powered inference, our setting would require using a portion of the labeled data for model training and leaving the rest for inference. In contrast, cross-prediction leverages each labeled data point for both model training and inference, leading to a boost in statistical power. The distinction between having and not having a pre-trained model makes a difference even when comparing prediction-powered inference and the classical approach. Angelopoulos et al. [1] do not take into account the data used for model training when comparing the two baselines, because the model is assumed to have been trained before the analysis takes place. This makes sense when considering off-the-shelf models such as AlphaFold. In our comparisons we do take the training data into account.

Wang et al. [48] similarly study inferences based on machine learning predictions. They propose using the labeled data to train a predictor of true outcomes from predicted ones, and then applying the predictor to debias the predictions on the unlabeled data. That said, this algorithm does not come with a formal validity guarantee. Motwani and Witten [28] conduct a detailed empirical comparison of the method of Wang et al. and prediction-powered inference.

Theory of cross-validation.

Cross-prediction is based on a form of cross-fitting. Consequently, our analysis is related to the theoretical studies of cross-validation [17, 2, 7, 23, 6]. In particular, our theory borrows from the analysis of Bayle et al. [7], who prove a central limit theorem and study inference on the cross-validation test error. Our goal, however, is entirely different; we aim to provide inferential guarantees for an estimand , as defined in Eq. (1), in a semi-supervised setting.

Semiparametric inference.

Our work is also related to the rich literature on semiparametric inference [26, 19, 24, 34, 8, 29, 31, 13], where the goal is to do estimation in the presence of a high-dimensional nuisance parameter. Our debiasing strategy closely resembles doubly-robust estimators [5], such as the AIPW estimator [32, 36], and one-step estimators [30]. In this literature the estimand is typically an expected value, such as the average treatment effect. One exception is the work of Jin and Rothenhäusler [21], who study general M-estimators through a semiparametric lens. The use of cross-fitting is common in that literature as well [13, 14, 15]. While the technical arguments used in our work bear resemblance to those classically used in semiparametric inference, our motivation is different. Our focus is on showcasing how a theoretically-principled use of black-box predictors—neural networks, random forests, and so on—on massive amounts of unlabeled data can boost inference. Since the practice of leveraging unlabeled data through predictions is already prevalent in domains such as remote sensing, our goal is to ground it in statistical theory.

Inference with missing data.

Semi-supervised inference can be seen as a special case of the problem of inference with missing data [38], where missing information about the labels occurs. Our proposed method bears similarities to multiple imputation [37, 39, 40] as, at least at a high level, it is based on “averaging out” multiple imputed predictions for the labels. However, our method is substantially different from multiple imputation, most notably due to the fact that it incorporates a particular form of debiasing to mitigate prediction inaccuracies.

3 Cross-prediction

We propose cross-prediction—an estimation technique based on a combination of cross-fitting and prediction. The basic idea is to impute labels for the unlabeled data points, and then remove the bias arising from the inaccuracies in the predictions using the labeled data. We give a step-by-step outline of the construction of the cross-prediction estimator. In the following sections we will show how to perform inference with this estimator; that is, how to perform hypothesis tests or construct confidence intervals for .

3.1 Cross-prediction for mean estimation

Before discussing the general case, we consider the problem of mean estimation to gain intuition; the object of inference is simply .

We begin by partitioning the labeled dataset into chunks, , and so on (we assume for simplicity that is divisible by ).111By removing at most data points, the size of the labeled dataset can be made divisible by . Since in our applications will typically be equal to , this truncation has a negligible effect. Here, is a user-specified number of folds, e.g. . Then, as in cross-validation, we train a machine learning model times, each time training on all data except one fold. Let denote a possibly randomized training algorithm, which takes as input a dataset of arbitrary size and outputs a predictor of labels from features. Then, for each , let be the model obtained by training on all folds but ; that is, . We note that can be quite general; it may or may not treat the training data points symmetrically, and need not come from a well-defined family of predictors. Rather, can be any black-box model; e.g. a random forest, a gradient-boosted tree, a neural network, and so on. Moreover, can be trained from scratch or obtained by fine-tuning an off-the-shelf model. Finally, we use the trained models to impute predictions and compute the cross-prediction estimator, defined as:

| (4) |

Intuitively, the first term in Eq. (4) is an empirical approximation of the population mean if we treated the predictions as true labels. The second term in Eq. (4) serves to debias this heutistic: it subtracts an estimate of the bias between the predicted labels and the true labels. We note that the estimator (4) coincides with the mean estimator of Zhang and Bradic [52] in the special case where are linear models, that is, for some . Our analysis applies more broadly, allowing for complex high-dimensional models (e.g., image classifiers).

Observe that the cross-prediction estimator is unbiased, i.e., . Indeed, since is not used to train model , we have for all . Applying this identity yields .

The classical estimator is of course the sample mean:

| (5) |

which is also unbiased. Given that both the cross-prediction estimator and the classical estimator are unbiased, it makes sense to ask which one has a lower variance. The main benefit of cross-prediction is that, if the trained models are reasonably accurate, we expect the variance of the cross-prediction estimator to be lower. To see this, first recall that, typically, . This means that the first term in should have a vanishing variance due to the magnitude of . Therefore,

As the sample mean, the remaining term is an average of terms. However, when the models are accurate, i.e. , we expect .

The closest alternative to the cross-prediction estimator is the prediction-powered estimator [1], that is, its straightforward adaptation to the setup without a pre-trained model. As discussed earlier, prediction-powered inference relies on having a pre-trained model . We can reduce our setting to this case by introducing data splitting: we use the first data points from the labeled dataset to train a model and the rest of the labeled data to compute the prediction-powered estimator:

| (6) |

The prediction-powered estimator is also unbiased: . However, this strategy is potentially wasteful because, after is trained, the training data is thrown away and not subsequently used for estimation. Cross-prediction uses the data more efficiently, by leveraging each data point for both training and estimation.

3.2 General cross-prediction

To introduce the cross-prediction estimator in full generality, recall that we are considering all estimands of the form (1). As in the case of mean estimation, we split the labeled data into folds and train a predictive model on all folds but fold . The proposed cross-prediction estimator is defined as:

| (7) |

Here, we use the short-hand notation , , and . The intuition remains the same as before: the first term is an empirical approximation of the population loss if we treated the predictions as true labels, and the second term aims to debias this heuristic. One can verify that the mean estimator in Eq. (4) is indeed a special case of the general estimator in Eq. (7), by taking to be the squared loss, as per Eq. (2).

The cross-prediction estimator optimizes an unbiased objective, since . This follows because for all , seeing that is not used to train model . Furthermore, by the same argument as before, we expect to have a lower variance than the classical objective in Eq. (3) if is large and the trained predictors are reasonably accurate. We note that may not be a convex function in general, but solving for is tractable in many cases of interest. For example, in the case of means and generalized linear models, is convex.

The prediction-powered estimator is similar to the cross-prediction estimator, but it requires data splitting and does not average over multiple model fits. It is equal to

| (8) |

where, as before, is trained on the first labeled data points. The fact that cross-prediction averages the results of multiple model fits allows it to achieve more stable inference. Indeed, in our experiments we will observe that cross-prediction is more stable than prediction-powered inference throughout.

4 Inference for the mean

We now discuss inference with the cross-prediction estimator. For simplicity we first look at mean estimation, where . We will see that much of the discussion will carry over to general M-estimation problems.

Inference with the cross-prediction estimator in Eq. (4) is difficult because the terms being averaged are all dependent through the labeled data. In contrast, the classical estimator in Eq. (5) averages independent terms, allowing for confidence intervals based on the central limit theorem. The prediction-powered estimator in Eq. (6) is similarly amenable to inference based on the central limit theorem, seeing that all the terms are independent conditional on . In this section we show that, under a relatively mild regularity condition, the cross-prediction estimator likewise satisfies a central limit theorem. This will in turn immediately allow constructing confidence intervals and hypothesis tests for .

The central limit theorem will require that, as the sample size grows, the predictions concentrate sufficiently rapidly around their expectation. Intuitively, one can think of the condition as requiring that the predictions are sufficiently stable. While the stability property is difficult to verify for complex black-box models, we empirically observe that inference based on the resulting central limit theorem nevertheless provides the correct coverage. We observe this across different estimation problems, data modalities, sample sizes, and so on.

Our analysis based on stability is inspired by the work of Bayle et al. [7], who study inference on the cross-validation test error, since the inferential challenges in cross-prediction are similar to those in cross-validation. The ultimate goals of the two analyses are, however, entirely different.

Below we state the stability condition. For all , we define ; the “average” model is the predictor we would obtain if we could train many models on independent datasets of size and average out their predictions.

Assumption 1.

We say that the predictions are stable if, as ,

If the number of folds is fixed (e.g., ), then Assumption 1 is satisfied if the variance of the difference between the learned predictions and the average predictions vanishes at any rate, . If the number of folds is allowed to grow, e.g. as in the case of leave-one-out cross-fitting, then the corresponding variance has to tend to zero sufficiently rapidly.

Equipped with Assumption 1, we can now state the central limit theorem for cross-prediction.

Theorem 4.1 (Cross-prediction CLT for the mean).

Let be the mean outcome, . Suppose that the predictions are stable (Ass. 1). Further, assume that has a limit, and that and have a nonzero limit. Then,

With this, inference on is now straightforward as long as we can estimate the asymptotic variance consistently. We will discuss strategies for doing so in Section 6.

Corollary 4.1 (Inference on the mean via cross-prediction).

Let be the mean outcome, . Assume the conditions of Theorem 4.1, and suppose that we have estimators and . Let

Then,

5 Inference for general M-estimation

We generalize the principle introduced in Section 4 to handle arbitrary M-estimation problems. Indeed, the results presented in this section will strictly subsume the results of Section 4. In the general case the estimator is no longer guaranteed to have a closed-form expression. Rather, it is implicitly defined through its variational characterization (7).

We can reduce the problem of inference for general M-estimation to one of inference on a mean parameter. Since the loss is convex, can be characterized as a zero of the gradient of the expected loss, i.e.,

Thus, to construct a confidence set for , it suffices to invert a test for the null hypothesis that . Since is an expectation, this is a hypothesis about a mean parameter.

The hypothesis test for the population gradient will follow from a central limit theorem for the gradient of the cross-prediction loss,

The main technical result of this section shows that is asymptotically normal around .

As in the case of the mean, we will require that the predictions are “stable” in an appropriate sense. Naturally, the notion of stability will depend on the loss function used to define the M-estimator.

Assumption 2.

With as before, we say that the predictions are stable if for all , as ,

Here, denotes the covariance matrix conditional on . Also, for vectors and matrices, by “” we mean convergence in mean to zero element-wise. Notice that by setting to be the squared loss, Assumption 2 reduces to Assumption 1 in the case of mean estimation.

We now provide a generalization of Theorem 4.1 to general M-estimation problems.

Theorem 5.1 (Cross-prediction CLT).

Suppose that the predictions are stable (Ass. 2). Further, assume that has a limit, and that and have a nonzero limit. Then,

Theorem 5.1 yields the construction of a test for the hypothesis that . Inverting the test gives a confidence set for , as stated below.

Corollary 5.1 (Inference via cross-prediction).

Assume the conditions of Theorem 5.1, and suppose that, for all , we have estimators and . Let

Then,

Above, is the -quantile of the chi-squared distribution with degrees of freedom; when (as in the case of mean estimation), is equal to .

Next, we apply Theorem 5.1 and Corollary 5.1 to two concrete problems—quantile estimation and linear regression—to get explicit confidence interval constructions.

5.1 Example: quantile estimation

Assume we are interested in a quantile of ,

The quantile can equivalently be written as any minimizer of the pinball loss,

The subgradient of the pinball loss is equal to . Plugging this expression into the confidence set from Corollary 5.1 yields

where is the average empirical CDF of the predictions on the unlabeled data, and is the difference between the empirical CDFs of the predictions and true outcomes on the labeled data. The standard errors are equal to and . The confidence set thus consists of all values such that the average predicted CDF , corrected by the bias , is close to the target level .

5.2 Example: linear regression

In linear regression, the target of inference is defined by

| (9) |

In this case, the cross-prediction estimator, equal to the solution to , has a closed-form expression. Letting (resp. ) be the unlabeled (resp. labeled) data matrix, be the vector of labeled outcomes, the solution is given by

where is the vector of average predictions on the unlabeled data, and is the vector of predictions on the labeled data: . We see that resembles the usual least-squares estimator with as the response, except for the extra debiasing factor, , that takes into account the prediction inaccuracies.

We show how to do inference with . Deriving from the general result of Theorem 5.1, we can obtain a central limit theorem for directly.

Corollary 5.2.

A confidence interval for , for some coordinate of interest , can therefore be obtained as

given an estimate of . The covariance can be estimated via the usual “sandwich” technique.

6 Variance estimation via bootstrapping

The previous inference results rely on being able to estimate the asymptotic covariance of . We herewith provide an explicit estimation strategy that we will use in our experiments.

The goal is to estimate , where and . If the average model was known, one could compute estimates of and by replacing the true covariances with their empirical counterparts. Thus, the challenge is to approximate . To achieve this, we apply the bootstrap to simulate multiple model training runs, and at the end we average the predictions of all the learned models.

In more detail, for each , we sample data points uniformly at random from the labeled dataset, and denote the indices of the samples by . Then, we use the sampled data points to train a model using the same model-fitting strategy as for the cross-prediction models . To estimate , we compute

where and denotes the empirical covariance. To estimate , we compute

Finally, we approximate the covariance by . In computing , we technically do not average out the bootstrapped models because we want to make sure that every point used to compute the gradient bias is independent of its corresponding model . Nevertheless, we show empirically that the resulting covariance estimate leads to valid coverage across a range of applications.

To give one concrete example, consider mean estimation: . We compute

and form the final interval as .

7 Experiments

We evaluate cross-prediction and compare it to baseline approaches on several datasets; the baselines are the classical inference method, which only uses the labeled data, and prediction-powered inference with a data-splitting step in order to train a predictive model. Code for reproducing the experiments is available at: https://github.com/tijana-zrnic/cross-ppi.

For each experimental setting, we plot the coverage and confidence interval width estimated over trials for all baselines. We also show the constructed confidence intervals for five randomly chosen trials. Finally, to quantify the stability of inferences, we report the standard deviation of the lower and upper endpoints of the confidence intervals for each method.

We begin with proof-of-concept experiments on synthetic data. Then, we move on to more complex real datasets.

| Mean estimation | ||||||

| Method | ||||||

| cross-prediction | 0.2694 | 0.2696 | 0.1769 | 0.1897 | 0.0591 | 0.0613 |

| classical | 0.2124 | 0.2085 | 0.1908 | 0.1885 | 0.2136 | 0.2102 |

| PPI | 0.3844 | 0.3997 | 0.2751 | 0.2684 | 0.1045 | 0.1061 |

7.1 Proof-of-concept experiments on synthetic data

To build intuition, we begin with simple experiments on synthetic data. The purpose is to confirm what we expect in theory: (a) as it gets easier to predict labels from features, cross-prediction and prediction-powered inference become more powerful and increasingly outperform the classical approach; (b) cross-prediction uses the data more efficiently than prediction-powered inference, yielding smaller intervals; (c) cross-prediction gives more stable inferences than the baselines when the predictions are useful; (d) all three approaches lead to satisfactory coverage.

In all of the following experiments, we have unlabeled data points, and we vary the size of the labeled data between and , in -point increments. We apply cross-prediction with folds. We estimate the variance using the bootstrap approach described in Section 6, with bootstrap samples. For prediction-powered inference, we use half of the labeled data for model training. To illustrate the point that cross-prediction can be applied with any black-box model, we train gradient-boosted trees via XGBoost [12] to obtain the models . We use the same model-fitting strategy for prediction-powered inference. We fix the target error level to be and average the results over trials.

| Quantile estimation | ||||||

| Method | ||||||

| cross-prediction | 0.4102 | 0.3509 | 0.3253 | 0.3242 | 0.1345 | 0.1545 |

| classical | 0.2302 | 0.3024 | 0.2569 | 0.3305 | 0.2615 | 0.2806 |

| PPI | 0.5424 | 0.4614 | 0.4141 | 0.4368 | 0.2151 | 0.3280 |

| Linear regression | ||||||

| Method | ||||||

| cross-prediction | 0.2801 | 0.2969 | 0.1875 | 0.2250 | 0.1102 | 0.1472 |

| classical | 0.2091 | 0.2098 | 0.2271 | 0.2262 | 0.1800 | 0.1809 |

| PPI | 0.4104 | 0.4870 | 0.2602 | 0.3326 | 0.1522 | 0.2530 |

Mean estimation.

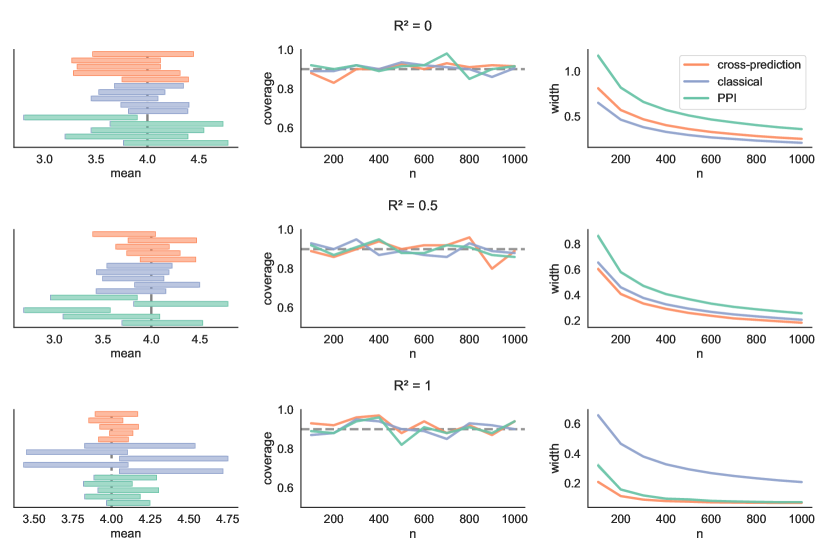

For given parameters and , the data-generating distribution is defined as , where , and is independent of . We fix and vary . The idea is to vary the degree to which the outcomes can be explained through the features: when , the outcome is independent of the features and we do not expect predictions to help, while when , the outcome can be perfectly explained through the features and we expect predictions to be helpful. Given that the variance of is kept constant regardless of , classical inference has the same distribution of widths across . The target of inference is .

In Figure 3 we plot the coverage and interval width of cross-prediction, classical inference, and prediction-powered inference, as well as five example intervals. All three methods approximately achieve the target coverage, and cross-prediction dominates prediction-powered inference throughout. Further, we see that the classical approach dominates the alternatives when the features are independent of the outcomes, while the alternatives become more powerful as increases. To evaluate stability, in Table 1 we report the standard deviation of the lower and upper endpoints of the confidence intervals from Figure 3, for . We observe that the classical approach is the most stable method when , which makes sense because the predictions can only introduce noise. When , cross-prediction and classical inference have a similar degree of stability, while when cross-prediction is significantly more stable. Moreover, cross-prediction is significantly more stable than prediction-powered inference throughout. These trends hold across different values of , however we only include the results for for simplicity of exposition.

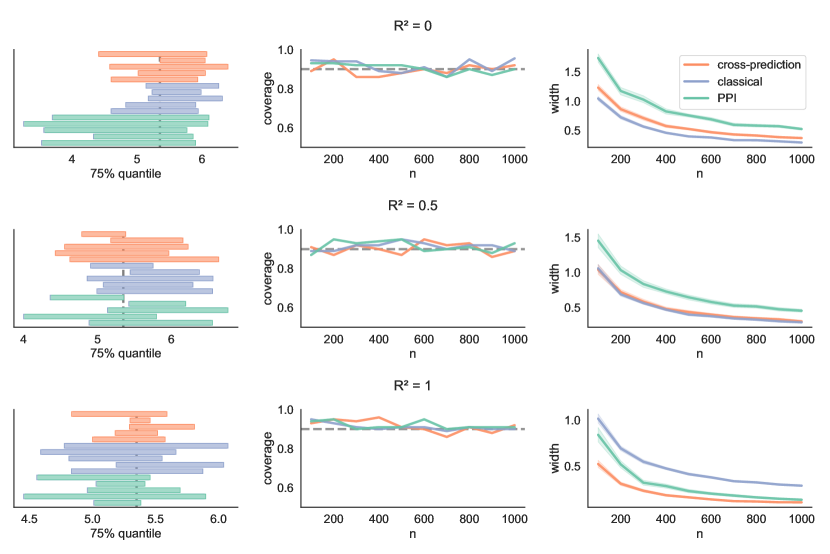

Quantile estimation.

We adopt the same data-generating process as for mean estimation. We only change the target of inference to be the 75th percentile of the outcome distribution.

In Figure 4 we plot the coverage and interval width of cross-prediction, classical inference, and prediction-powered inference, as well as five example intervals. We observe a qualitatively similar comparison as in the case of mean estimation: all three methods approximately achieve the target coverage, and cross-prediction dominates prediction-powered inference throughout. As before, the classical approach dominates the alternatives when the features are independent of the outcomes, and the alternatives become increasingly powerful as increases. In Table 2 we evaluate the stability of the methods by reporting the standard deviation of the lower and upper endpoints of the confidence intervals from Figure 3, for . As before, Table 2 shows that cross-prediction is more stable than prediction-powered inference for all values of , and when classical inference is the most stable option. When , cross-prediction has a slightly more stable upper endpoint than classical inference, while classical inference has a more stable lower endpoint. When , cross-prediction is by far the most stable method. For . Again, these trends are largely consistent across different values of , however we only include the results for for simplicity.

Linear regression.

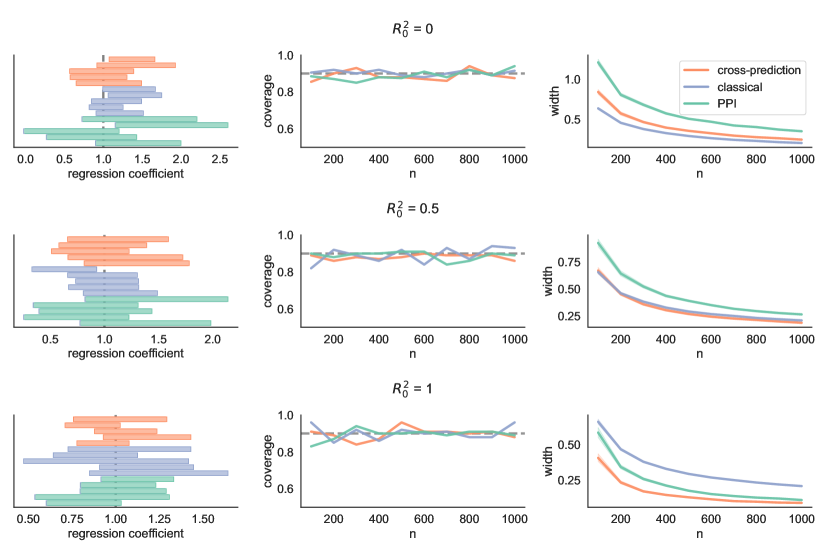

Finally, we look at linear regression. For robustness and interpretability, it is common to include only a subset of the available features in the regression. The process of deciding which variables to include is known as model selection. The variables that are not included in the model may still be predictive of the outcome of interest; we demonstrate that, as such, they can be useful for inference.

The data-generating distribution is defined as follows: we generate , , where and . Again, the idea is to vary how much of the outcome can be explained through prediction versus how much of it is exogenous randomness. We fix and vary . The target of inference is defined as the least-squares solution when regressing on , that is, the first coordinate of this solution. In this case, this is simply equal to .

In Figure 5 we plot the coverage and interval width of cross-prediction, classical inference, and prediction-powered inference. When , the classical approach outperforms the prediction-based approaches; as grows, meaning more of the randomness of the outcome can be attributed to , the prediction-based approaches dominate the classical one. As before, cross-prediction yields smaller intervals than prediction-powered inference. We remark that, even though the inference problem posits a linear model, the prediction-based approaches still use XGBoost for model training. Like in the previous two examples, we report on the stability of the three methods in Table 3. We again fix for simplicity. Cross-prediction is far more stable than prediction-powered inference throughout, and it is more stable than classical inference for nonzero values of .

7.2 Estimating deforestation from satellite imagery

We briefly revisit the problem of deforestation analysis from Section 1. As we saw in Figure 2, cross-prediction gave tighter confidence intervals for the deforestation rate than using gold-standard measurements of deforestation alone. In other words, cross-prediction can enable a reduction in the number of necessary field visits to measure deforestation. Moreover, we saw that cross-prediction outperformed prediction-powered inference.

Here we argue another benefit of cross-prediction in this problem: it is a more stable solution than the baselines. Table 4 shows the standard deviation of the endpoints of the confidence intervals constructed by cross-prediction and its competitors. Cross-prediction has a significantly lower variability of the endpoints than both classical inference and prediction-powered inference, while the latter two exhibit similar variability.

Finally, we provide the experimental details that were omitted in Section 1 for brevity. We have data points with gold-standard labels total. To simulate having unlabeled images, in each trial we randomly split the data into points to serve as the labeled data, for varying , and treat the remaining points as unlabeled. The target of inference is the fraction of deforested areas across the locations contained in the sample. We apply cross-prediction with folds. For prediction-powered inference, we use points for model tuning. We average the results over trials.

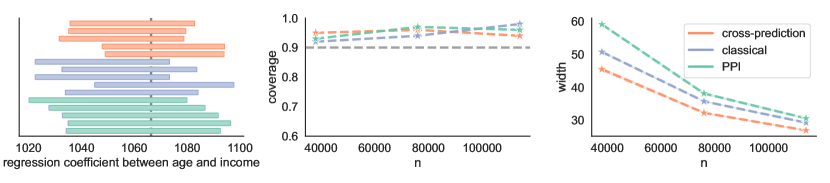

7.3 Estimating relationships between socioeconomic covariates in survey data

We evaluate cross-prediction on the American Community Survey (ACS) Public Use Microdata Sample (PUMS). We investigate the relationship between age, sex, and income in survey data collected in California in 2019 ( people total). High-quality survey data is generally difficult and time-consuming to collect. With this experiment we hope to demonstrate how, by imputing missing information based on the available covariates, cross-prediction can achieve both powerful and valid inferences while reducing the requisite amount of survey data.

We use the Folktables [16] interface to download the PUMS data, including income, age, sex, and 15 other demographic covariates. In each trial, we randomly sample data points to serve as the labeled data, for varying , and treat the remaining data points as the unlabeled data. We vary . The target of inference is the linear regression coefficient when regressing income on age and sex: , where is income and encodes age and sex, . For the purpose of evaluating coverage, the corresponding coefficient computed on the whole dataset is taken as the ground-truth value of the estimand. To obtain the models , we train gradient-boosted trees via XGBoost [12]. Note that the predictors use all 17 covariates to predict the missing labels, even though the target of inference is only defined with respect to two covariates. We apply cross-prediction with folds. For prediction-powered inference, we use points for model training, and we also train gradient-boosted trees. The target error level is and we average the results over trials.

In Figure 7 we plot the coverage and interval width for the three baselines, together with five example intervals. All three methods cover the true target with the desired probability. Moreover, as before, cross-prediction outperforms prediction-powered inference. In this example, the predictive power of the trained models is not high enough for prediction-powered inference to outperform the classical approach; cross-prediction, however, outperforms both. In Table 4 we report on the stability of the three methods for . We observe that cross-prediction is more stable than both alternatives. We also observe that prediction-powered inference has more stable intervals than the classical approach, despite the fact that they are wider on average.

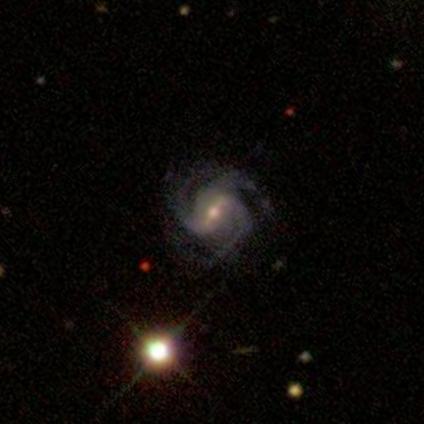

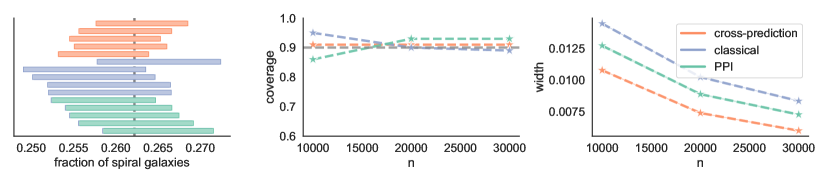

7.4 Estimating the prevalence of spiral galaxies from galaxy images

We next look at galaxy data from the Galaxy Zoo 2 dataset [49], consisting of human-annotated images of galaxies from the Sloan Digital Sky Survey [50]. Of particular interest are galaxies with spiral arms, which are correlated with star formation in the discs of low-redshift galaxies, and thus contribute to the understanding of star formation. See Figure 8 for example images of a spiral and a nonspiral galaxy. We show that, by leveraging the massive amounts of unlabeled galaxy imagery together with machine learning, cross-prediction can decrease the requisite number of human annotations for inference on galaxy demographics.

We have annotated galaxy images. In each trial, we randomly split them up into points to serve as the labeled data, for , and treat the remaining data points as unlabeled. The target of inference is the fraction of spiral galaxies in the dataset, equal to about . To compute predictions, we fine-tune all layers of a pre-trained ResNet50. We apply cross-prediction with folds. For prediction-powered inference, we use points for model training. The target error rate is and we average the results over trials.

In Figure 9 we plot the coverage and interval width of the three methods, as well as the intervals for five randomly chosen trials. Both cross-prediction and prediction-powered inference yield smaller intervals than the classical approach. Moreover, cross-prediction dominates prediction-powered inference. We observe satisfactory coverage for all three procedures. In Table 4 we evaluate the stability of the procedures for . Cross-prediction is significantly more stable than classical inference and prediction-powered inference. The latter two achieve a similar degree of stability.

| Deforestation Analysis | ACS Survey Analysis | Galaxy Analysis | ||||

| Method | ||||||

| cross-prediction | 0.0158 | 0.0182 | 11.2781 | 12.2367 | 0.0029 | 0.0029 |

| classical | 0.0195 | 0.0232 | 14.5346 | 15.6106 | 0.0037 | 0.0038 |

| PPI | 0.0200 | 0.0240 | 13.1378 | 13.8733 | 0.0036 | 0.0037 |

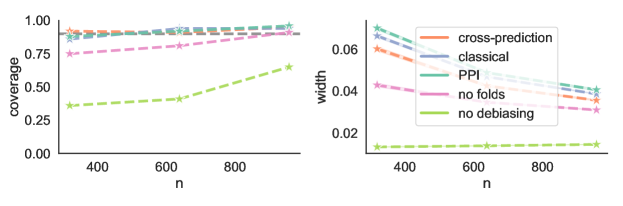

8 Evaluating heuristics

In Figure 2, we saw that cross-prediction gave tighter confidence intervals than the baseline approaches for the problem of deforestation analysis. In this section, we test two heuristic ways of reducing the variance of the classical approach and prediction-powered inference and compare the heuristics to cross-prediction.

The first heuristic removes the debiasing from the cross-prediction estimator and simply averages the predictions on the large unlabeled dataset:

| (10) |

This is akin to computing the classical estimator while pretending that the predicted labels are the ground truth. The second heuristic trains a model on all the labeled data, , and computes

This estimator is akin to the prediction-powered estimator if we treated as fixed and independent of the labeled dataset.

For both heuristics, we form confidence intervals based on the usual central limit theorem that assumes i.i.d. sampling. For the first heuristic this is done conditional on the trained models , since the terms are indeed conditionally independent given . Since the second heuristic proceeds under the assumption that can be seen as being independent of the labeled data, we apply the central limit theorem to the two sums separately, as if were fixed.

We see in Figure 10 that removing the debiasing is detrimental to coverage; removing the folds has a more moderate effect that vanishes with , but it is nevertheless significant. Cross-prediction yields wider intervals than both heuristics, and by doing so it maintains correct coverage.

Acknowledgements

We thank Anastasios Angelopoulos, Ying Jin, and Asher Spector for helpful suggestions and feedback on a draft on this manuscript, and Aditya Ghosh for catching and fixing a typo in a previous version of the manuscript. T.Z. was supported by Stanford Data Science through the Fellowship program. E.J.C. was supported by the Office of Naval Research grant N00014-20-1-2157, the National Science Foundation grant DMS-2032014, the Simons Foundation under award 814641, and the ARO grant 2003514594.

References

- Angelopoulos et al. [2023] Anastasios N Angelopoulos, Stephen Bates, Clara Fannjiang, Michael I Jordan, and Tijana Zrnic. Prediction-powered inference. arXiv preprint arXiv:2301.09633, 2023.

- Austern and Zhou [2020] Morgane Austern and Wenda Zhou. Asymptotics of cross-validation. arXiv preprint arXiv:2001.11111, 2020.

- Azriel et al. [2022] David Azriel, Lawrence D Brown, Michael Sklar, Richard Berk, Andreas Buja, and Linda Zhao. Semi-supervised linear regression. Journal of the American Statistical Association, 117(540):2238–2251, 2022.

- Ball et al. [2017] John E Ball, Derek T Anderson, and Chee Seng Chan. Comprehensive survey of deep learning in remote sensing: theories, tools, and challenges for the community. Journal of applied remote sensing, 11(4):042609–042609, 2017.

- Bang and Robins [2005] Heejung Bang and James M Robins. Doubly robust estimation in missing data and causal inference models. Biometrics, 61(4):962–973, 2005.

- Bates et al. [2023] Stephen Bates, Trevor Hastie, and Robert Tibshirani. Cross-validation: what does it estimate and how well does it do it? Journal of the American Statistical Association, pages 1–12, 2023.

- Bayle et al. [2020] Pierre Bayle, Alexandre Bayle, Lucas Janson, and Lester Mackey. Cross-validation confidence intervals for test error. Advances in Neural Information Processing Systems, 33:16339–16350, 2020.

- Bickel et al. [1993] Peter J Bickel, Chris AJ Klaassen, Peter J Bickel, Ya’acov Ritov, J Klaassen, Jon A Wellner, and YA’Acov Ritov. Efficient and adaptive estimation for semiparametric models, volume 4. Springer, 1993.

- Bludau et al. [2022] Isabell Bludau, Sander Willems, Wen-Feng Zeng, Maximilian T Strauss, Fynn M Hansen, Maria C Tanzer, Ozge Karayel, Brenda A Schulman, and Matthias Mann. The structural context of posttranslational modifications at a proteome-wide scale. PLoS biology, 20(5):e3001636, 2022.

- Bullock et al. [2020] Eric L Bullock, Curtis E Woodcock, Carlos Souza Jr, and Pontus Olofsson. Satellite-based estimates reveal widespread forest degradation in the Amazon. Global Change Biology, 26(5):2956–2969, 2020.

- Chakrabortty et al. [2022] Abhishek Chakrabortty, Guorong Dai, and Raymond J Carroll. Semi-supervised quantile estimation: Robust and efficient inference in high dimensional settings. arXiv preprint arXiv:2201.10208, 2022.

- Chen and Guestrin [2016] Tianqi Chen and Carlos Guestrin. Xgboost: A scalable tree boosting system. In Proceedings of the 22nd acm sigkdd international conference on knowledge discovery and data mining, pages 785–794, 2016.

- Chernozhukov et al. [2018] Victor Chernozhukov, Denis Chetverikov, Mert Demirer, Esther Duflo, Christian Hansen, Whitney Newey, and James Robins. Double/debiased machine learning for treatment and structural parameters, 2018.

- Chernozhukov et al. [2022] Victor Chernozhukov, Juan Carlos Escanciano, Hidehiko Ichimura, Whitney K Newey, and James M Robins. Locally robust semiparametric estimation. Econometrica, 90(4):1501–1535, 2022.

- Chernozhukov et al. [2023] Victor Chernozhukov, Whitney K Newey, and Rahul Singh. A simple and general debiased machine learning theorem with finite-sample guarantees. Biometrika, 110(1):257–264, 2023.

- Ding et al. [2021] Frances Ding, Moritz Hardt, John Miller, and Ludwig Schmidt. Retiring adult: New datasets for fair machine learning. Advances in neural information processing systems, 34:6478–6490, 2021.

- Dudoit and van der Laan [2005] Sandrine Dudoit and Mark J van der Laan. Asymptotics of cross-validated risk estimation in estimator selection and performance assessment. Statistical methodology, 2(2):131–154, 2005.

- Hansen et al. [2013] Matthew C Hansen, Peter V Potapov, Rebecca Moore, Matt Hancher, Svetlana A Turubanova, Alexandra Tyukavina, David Thau, Stephen V Stehman, Scott J Goetz, Thomas R Loveland, et al. High-resolution global maps of 21st-century forest cover change. science, 342(6160):850–853, 2013.

- Hasminskii and Ibragimov [1979] Rafail Z Hasminskii and Ildar A Ibragimov. On the nonparametric estimation of functionals. In Proceedings of the Second Prague Symposium on Asymptotic Statistics, volume 473, pages 474–482. North-Holland Amsterdam, 1979.

- Jean et al. [2016] Neal Jean, Marshall Burke, Michael Xie, W Matthew Davis, David B Lobell, and Stefano Ermon. Combining satellite imagery and machine learning to predict poverty. Science, 353(6301):790–794, 2016.

- Jin and Rothenhäusler [2023] Ying Jin and Dominik Rothenhäusler. Tailored inference for finite populations: conditional validity and transfer across distributions. Biometrika, page asad022, 2023.

- Jumper et al. [2021] John Jumper, Richard Evans, Alexander Pritzel, Tim Green, Michael Figurnov, Olaf Ronneberger, Kathryn Tunyasuvunakool, Russ Bates, Augustin Žídek, Anna Potapenko, et al. Highly accurate protein structure prediction with alphafold. Nature, 596(7873):583–589, 2021.

- Kissel and Lei [2022] Nicholas Kissel and Jing Lei. On high-dimensional Gaussian comparisons for cross-validation. arXiv preprint arXiv:2211.04958, 2022.

- Klaassen [1987] Chris AJ Klaassen. Consistent estimation of the influence function of locally asymptotically linear estimators. The Annals of Statistics, 15(4):1548–1562, 1987.

- Lehmann and Romano [2022] Erich L Lehmann and Joseph P Romano. Testing statistical hypotheses, volume 4. Springer Nature, 2022.

- Levit [1976] B Ya Levit. On the efficiency of a class of non-parametric estimates. Theory of Probability & Its Applications, 20(4):723–740, 1976.

- Lin et al. [2023] Zeming Lin, Halil Akin, Roshan Rao, Brian Hie, Zhongkai Zhu, Wenting Lu, Nikita Smetanin, Robert Verkuil, Ori Kabeli, Yaniv Shmueli, et al. Evolutionary-scale prediction of atomic-level protein structure with a language model. Science, 379(6637):1123–1130, 2023.

- Motwani and Witten [2023] Keshav Motwani and Daniela Witten. Valid inference after prediction. arXiv preprint arXiv:2306.13746, 2023.

- Newey [1994] Whitney K Newey. The asymptotic variance of semiparametric estimators. Econometrica: Journal of the Econometric Society, pages 1349–1382, 1994.

- Newey and McFadden [1994] Whitney K Newey and Daniel McFadden. Large sample estimation and hypothesis testing. Handbook of econometrics, 4:2111–2245, 1994.

- Robins and Rotnitzky [1995] James M Robins and Andrea Rotnitzky. Semiparametric efficiency in multivariate regression models with missing data. Journal of the American Statistical Association, 90(429):122–129, 1995.

- Robins et al. [1994] James M Robins, Andrea Rotnitzky, and Lue Ping Zhao. Estimation of regression coefficients when some regressors are not always observed. Journal of the American statistical Association, 89(427):846–866, 1994.

- Robinson et al. [2017] Caleb Robinson, Fred Hohman, and Bistra Dilkina. A deep learning approach for population estimation from satellite imagery. In Proceedings of the 1st ACM SIGSPATIAL Workshop on Geospatial Humanities, pages 47–54, 2017.

- Robinson [1988] Peter M Robinson. Root-n-consistent semiparametric regression. Econometrica: Journal of the Econometric Society, pages 931–954, 1988.

- Rolf et al. [2021] Esther Rolf, Jonathan Proctor, Tamma Carleton, Ian Bolliger, Vaishaal Shankar, Miyabi Ishihara, Benjamin Recht, and Solomon Hsiang. A generalizable and accessible approach to machine learning with global satellite imagery. Nature communications, 12(1):4392, 2021.

- Rotnitzky et al. [1998] Andrea Rotnitzky, James M Robins, and Daniel O Scharfstein. Semiparametric regression for repeated outcomes with nonignorable nonresponse. Journal of the american statistical association, 93(444):1321–1339, 1998.

- Rubin [1987] D Rubin. Multiple imputation for nonresponse in surveys. Wiley Series in Probability and Statistics, page 1, 1987.

- Rubin [1976] Donald B Rubin. Inference and missing data. Biometrika, 63(3):581–592, 1976.

- Rubin [1996] Donald B Rubin. Multiple imputation after 18+ years. Journal of the American statistical Association, 91(434):473–489, 1996.

- Schafer [1999] Joseph L Schafer. Multiple imputation: a primer. Statistical methods in medical research, 8(1):3–15, 1999.

- Sexton et al. [2013] Joseph O Sexton, Xiao-Peng Song, Min Feng, Praveen Noojipady, Anupam Anand, Chengquan Huang, Do-Hyung Kim, Kathrine M Collins, Saurabh Channan, Charlene DiMiceli, et al. Global, 30-m resolution continuous fields of tree cover: Landsat-based rescaling of modis vegetation continuous fields with lidar-based estimates of error. International Journal of Digital Earth, 6(5):427–448, 2013.

- Song et al. [2023] Shanshan Song, Yuanyuan Lin, and Yong Zhou. A general m-estimation theory in semi-supervised framework. Journal of the American Statistical Association, pages 1–11, 2023.

- Steele et al. [2017] Jessica E Steele, Pål Roe Sundsøy, Carla Pezzulo, Victor A Alegana, Tomas J Bird, Joshua Blumenstock, Johannes Bjelland, Kenth Engø-Monsen, Yves-Alexandre De Montjoye, Asif M Iqbal, et al. Mapping poverty using mobile phone and satellite data. Journal of The Royal Society Interface, 14(127):20160690, 2017.

- Tony Cai and Guo [2020] T Tony Cai and Zijian Guo. Semisupervised inference for explained variance in high dimensional linear regression and its applications. Journal of the Royal Statistical Society Series B: Statistical Methodology, 82(2):391–419, 2020.

- Tunyasuvunakool et al. [2021] Kathryn Tunyasuvunakool, Jonas Adler, Zachary Wu, Tim Green, Michal Zielinski, Augustin Žídek, Alex Bridgland, Andrew Cowie, Clemens Meyer, Agata Laydon, et al. Highly accurate protein structure prediction for the human proteome. Nature, 596(7873):590–596, 2021.

- Van der Vaart [2000] Aad W Van der Vaart. Asymptotic statistics, volume 3. Cambridge university press, 2000.

- Van Engelen and Hoos [2020] Jesper E Van Engelen and Holger H Hoos. A survey on semi-supervised learning. Machine learning, 109(2):373–440, 2020.

- Wang et al. [2020] Siruo Wang, Tyler H McCormick, and Jeffrey T Leek. Methods for correcting inference based on outcomes predicted by machine learning. Proceedings of the National Academy of Sciences, 117(48):30266–30275, 2020.

- Willett et al. [2013] Kyle W Willett, Chris J Lintott, Steven P Bamford, Karen L Masters, Brooke D Simmons, Kevin RV Casteels, Edward M Edmondson, Lucy F Fortson, Sugata Kaviraj, William C Keel, et al. Galaxy zoo 2: detailed morphological classifications for 304 122 galaxies from the sloan digital sky survey. Monthly Notices of the Royal Astronomical Society, 435(4):2835–2860, 2013.

- York et al. [2000] Donald G York, J Adelman, John E Anderson Jr, Scott F Anderson, James Annis, Neta A Bahcall, JA Bakken, Robert Barkhouser, Steven Bastian, Eileen Berman, et al. The sloan digital sky survey: Technical summary. The Astronomical Journal, 120(3):1579, 2000.

- Zhang et al. [2019] Anru Zhang, Lawrence D Brown, and T Tony Cai. Semi-supervised inference: General theory and estimation of means. Annals of Statistics, 47(5):2538–2566, 2019.

- Zhang and Bradic [2022] Yuqian Zhang and Jelena Bradic. High-dimensional semi-supervised learning: in search of optimal inference of the mean. Biometrika, 109(2):387–403, 2022.

- Zheng et al. [2023] Zhiling Zheng, Oufan Zhang, Christian Borgs, Jennifer T. Chayes, and Omar M. Yaghi. Chatgpt chemistry assistant for text mining and the prediction of mof synthesis. Journal of the American Chemical Society, 145(32):18048–18062, 2023.

- Zhu and Goldberg [2022] Xiaojin Zhu and Andrew B Goldberg. Introduction to semi-supervised learning. Springer Nature, 2022.

- Zhu [2005] Xiaojin Jerry Zhu. Semi-supervised learning literature survey. 2005.

Appendix A Proofs

A.1 Proof of Theorem 4.1 (CLT for mean estimation)

The proof builds on two key technical lemmas, which leverage the notion of stability in Assumption 1 to show that we can “replace” the models in the definition of the cross-prediction estimator (4) with the “average” model . Since is a nonrandom model, we can proceed with a standard CLT analysis of the two terms comprising the estimator.

We begin by stating and proving the technical lemmas, which are inspired by the analysis of cross-validation due to Bayle et al. [7]. To simplify notation, we use and to denote the expectation and variance conditional on everything but .

Lemma A.1.

Proof.

Let . We will use the fact that if and only if , as stated in Fact 1 below. See, for example, Bayle et al. [7] for a proof of the fact.

Fact 1.

Let be a sequence of random variables. Then, if and only if .

Note that is nondecreasing and satisfies for non-negative ; this yields

Notice that is also concave. Therefore, by Jensen’s inequality, we have

Invoking the stability condition shows that the right-hand side converges to zero. Note that, technically, the stability condition is stronger than what is needed for the expression above to converge to zero. In particular, stability ensures that , while for the expression above to vanish it would suffice to ensure . The stronger condition will be used in the next technical lemma, which handles the second term in the cross-prediction estimator.

Putting everything together, we get that , as desired. ∎

Lemma A.2.

Proof.

The proof follows a similar principle as the proof of Lemma A.1. As before, we let and use the fact if and only if (see Fact 1). We use the fact that for non-negative ; this yields

Next, by Jensen’s inequality, we have

Invoking the stability condition shows that the right-hand side converges to zero. Hence, . ∎

With Lemma A.1 and Lemma A.2 in hand, we can now prove Theorem 4.1. As alluded to earlier, the idea is to use Lemma A.1 and Lemma A.2 to replace the models in the definition of the cross-prediction estimator (4).

Writing , we have

| (13) |

where we define

Focusing on , we have

By an analogous argument, we have

for defined in Eq. (12). Going back to Eq. (A.1) and denoting by the limits of , respectively, we get

By the Lindeberg central limit theorem, the first term converges in distribution to , and the second term converges in distribution to . Moreover, since the two terms are independent, we finally have

A.2 Proof of Theorem 5.1 (CLT for general M-estimation)

The proof follows the same template as the proof of Theorem 4.1. We begin with two technical lemmas that allow swapping the models in the gradient of the cross-prediction loss, , with the “average” model .

Lemma A.3.

Lemma A.4.

Lemma A.3 and Lemma A.4 are proved completely analogously to Lemma A.1 and Lemma A.2; we apply the same argument as before entry-wise. Now we put the lemmas together to prove the central limit theorem:

| (16) |

where we define

We apply Lemma A.3 and Lemma A.4 to and , respectively. In particular, we can write

where is given in Eq. (14). Invoking Lemma A.3, we thus have .

Going back to Eq. (A.2) and denoting by the limits of , respectively, by the Lindeberg central limit theorem we get

The first term above converges in distribution to

and the second term converges in distribution to

Since the two terms are independent, we can add up their limiting covariance matrices and get

as desired.