Asymptotic expansion of the invariant measure for Markov-modulated ODEs at high frequency

Abstract

We consider time-inhomogeneous ODEs whose parameters are governed by an underlying ergodic Markov process. When this underlying process is accelerated by a factor , an averaging phenomenon occurs and the solution of the ODE converges to a deterministic ODE as vanishes. We are interested in cases where this averaged flow is globally attracted to a point. In that case, the equilibrium distribution of the solution of the ODE converges to a Dirac mass at this point. We prove an asymptotic expansion in terms of for this convergence, with a somewhat explicit formula for the first order term. The results are applied in three contexts: linear Markov-modulated ODEs, randomized splitting schemes, and Lotka-Volterra models in random environment. In particular, as a corollary, we prove the existence of two matrices whose convex combinations are all stable but such that, for a suitable jump rate, the top Lyapunov exponent of a Markov-modulated linear ODE switching between these two matrices is positive.

1 Introduction

Let be a -dimensional compact manifold. Markov-modulated ODEs on are dynamical systems solution to

| (1) |

where is a Markov process on some space and, for all , is a vector field on .

We are interested in the high frequency regime, namely when is replaced in (1) by for some small . Provided is ergodic with respect to some probability measure , the modulated process is known to converge, as vanishes, to the solution of the averaged ODE

| (2) |

In the case where this averaged ODE has a unique global attractor , we expect the solution of (1) to be close to for large and small. In other words, the invariant measure of the Markov process converges, as vanishes, to . The goal of the present work is to provide an infinitesimal expansion in terms of for this invariant measure. This is obtained by combining a similar expansion for the law of the process for a fixed (following [22]) with a long-time convergence result for the limit process. The structure of the proof follows the work of Talay and Tubaro [23] who established a similar expansion for the invariant measure of Euler-Maruyam schemes for diffusion processes (the averaging estimates for a fixed being in that case replaced by finite-time discretization error expansions).

One of our main motivation is to get the first-order term in the expansion of the top Lyapunov exponent of systems of switched linear ODE [5, 16, 9], as detailed in Section 3.1. Our result also has applications for instance in some population models [21, 6, 4] or random splitting numerical schemes [1], cf. Section 3. More generally, Markov-modulated ODEs form a flexible class of Markov processes which appear in a variety of models, often to describe systems evolving in a randomly fluctuating environment, as in finance [12], biology [17] or fiability [19]. It is related to random ODEs, see e.g. [2, 10] and references within.

In the specific context of Piecewise-Deterministic Markov processes (PDMP; namely, when is a Markov chain on a finite set), the question of fast averaging has been addressed in [13] where a large deviation principle is proven, in [22] where the expansion of the law of the process at fixed time is given, or in [8] where the convergence of the invariant measure of the Markov process is proven. In the recent paper [15], the authors deal with the case where is not ergodic.

The paper is organized as follows. In the remaining of this introduction, we introduce our general notations and assumptions. Our main result, Theorem 1, is stated and proven in Section 2. Section 3 is devoted to exemples of applications. Finally, an appendix gathers the proofs of some intermediary results.

To conclude this section, let us clarify our settings. Denote by the semi-group associated to , namely

and by its infinitesimal generator.

Denote by the set of bounded measurable functions from to which are in their first variable and such that all their derivatives in are bounded over , and which moreover are such that for all and all multi-index , is in the domain of . We consider on the norms

Assumption 1.

We assume that:

-

1.

Almost surely, the ODE (1) is well-defined for all times, with values in . Moreover, the coordinates of are in .

-

2.

The semigroup admits a unique invariant probability measure . Moreover, there exist such that

(3) for all bounded measurable on and all .

The uniform exponential ergodicity (3) implies that the operator given by

| (4) |

is well-defined for all , with and for all . Moreover, using that for all , we get that for , namely is the pseudo-inverse of .

Example 1.

A case of interest is given by , which corresponds to where is a standard Poisson process with intensity , and is an i.i.d. sequence of random variables distributed according to . It is readily checked that, in that case, and then .

Example 2.

We will be particularly concerned with the case when is a finite state space and is an irreducible continuous-time Markov chain on , with transition rate matrix . In that case, is the group inverse of , defined as the unique matrix solution333such a matrix exists and is unique since has index , meaning that and have the same rank, because is a simple eigenvalue of . See Chapter 4 in [3] for more details. to

| (5) |

In the particular case when the cardinal of is 2, then can be written as

for some . Moreover, one can easily check, using that satisfies (5), and therefore .

2 High-frequency expansion

The process is a Markov process on with generator , where is seen as a an operator on functions on acting only on the second variable and

for all . For , denote by the associated Markov semigroup, namely

We start by stating an expansion in of for a fixed (the proof is postponed to the Appendix). This is essentially the result (and proof) of [22] but written in a dual form and with more explicit functional settings. Moreover, [22] only considers the case where is a finite set, but it allows the jump rates of to depend on .

Proposition 1.

There exist two families of operators indexed by , acting on , with the following properties.

-

•

For all and , there exists such that for all ,

(6) -

•

For all , there exist such that for all and all ,

(7) -

•

For all , , , there exists such that for all and , the remainder defined by

(8) satisfies

(9) -

•

The first operators are given by

(10) and

(11) where

(12)

Next, to address the question of the long-time behaviour of the process, we work under the following condition:

Assumption 2.

There is a globally attractive for the averaged flow given in (2), and for all , there exist such that for all and ,

where is the flow associated to .

Under Assumption 2, is the unique invariant measure of given in (10). Our main result is the following expansion in terms of of any invariant measure of the process , in the spirit of Talay-Tubaro expansions in terms of the step size for discretization schemes [23].

Theorem 1.

Remark 1.

Proof of Theorem 1.

The proof is divided in two parts. In the first one, we prove (13), and we give an expression of which depends on an arbitrary time . In the second part, we obtain the announced expression of by letting vanish in this first expression.

Step 1. Fix , and let be an invariant measure of . By definition of the flow ,

Hence,

As a consequence, the function given by

| (16) |

is well-defined, in and such that, for all , for some independent from . Moreover,

Then, using this Poisson equation and that is invariant for ,

To get the convergence of to at zeroth order, we simply bound, thanks to Proposition 1,

To get the higher order expansion, write

| (17) |

From Proposition 1 and the bounds on for all ,

for some . Using that, from the convergence at order ,

for all for some , we get first with (17) at order that

| (18) |

for some . We can thus apply this first order expansion with replaced by to get

for some . Hence, considering the expansion (17) at order , we get

for some . Again, this can be used with replaced by , and a straightforward induction on concludes the proof of (13). In particular, from (18), we see that for all , can be written as

Step 2. The goal is now to let vanish in this last expression. For a fixed , denote by the function given by (12) but with replaced by . Then

with

First, by definition of , the average of with respect to , hence with respect to , is zero. At this stage, we have obtained that . Recalling that , from

integrating with respect to , we get

As a consequence,

Besides,

where we used that does not depend on and is thus in the kernel of . Hence,

where we used that and that . Indeed, thanks to Assumption 2,

and the convergence holds in all norms . The proof of (14) is concluded by letting vanish in the equality (since is independent from ).

∎

3 Applications

3.1 Top Lyapunov exponent for cooperative linear Markov-modulated ODEs

In this section, we consider linear Markov-modulated ODEs on of the form

| (19) |

where, for all , is a matrix. We work under Assumption 1 and write . Moreover, we focus on the settings of [7], given as follows:

Assumption 3.

-

1.

The Markov process is Feller.

-

2.

For all , is a cooperative matrix, in the sense that its off-diagonal coefficients are non-negative.

-

3.

The averaged matrix is irreducible in the sense that for all there exists a path with for all .

The fact that the matrices are cooperative implies that is fixed by (19) for and that Assumption 2 holds. We decompose solutions of (19) on as where with and . The ODE (19) is then equivalent to

with

It is proven in [7] that, under Assumption 3, the Markov process admits a unique invariant measure on and that for all initial conditions , almost surely,

| (20) |

where

| (21) |

is called the top Lyapunov exponent of the process. Denoting by the principal eigenvalue of (i.e., with maximal real part), Proposition 4 in [7] entails that

From Theorem 1 applied to the function , we get an expansion of for small .

Proposition 2.

Proof.

First, considering given by (15), we claim that for all

| (22) |

Indeed, note that, for all ,

Theorefore, using that , one has

where we have used Perron-Frobenius Theorem. From (22), we deduce that . Now, using that , we get that

and then

from which we deduce that

where we have used that As a consequence,

Using that , we see that the last line is equal to

We end up with

Integrating with respect to leads to

∎

Example 3.

When considering the switching between matrices , the following natural question arises: if all the matrices are stable (i.e. for all ), is the switched system (19) stable, in the sense that ? It is now known that this is not true. In the case of random switching between two matrices, examples of stable matrices giving an unstable system can be founded in [5] and [20]. In the first reference, for , so that fast switching leads to a unstable system. In the second reference, it is a bit more complicated, since for all , meaning that both slow and fast switching lead to a stable system. However, the authors prove in [20] that switching not too fast, nor too slowly, the system is unstable. Yet, in [20], the matrices are not cooperative in the sense of Assumption 3. This is not surprising, since it is proven in [16] that switching between cooperative matrices of size such that every matrices in the convex hull of the given matrices are stable, will always lead to a stable system. However, it is also shown in [16] that it is possible in some higher dimension to construct an example where all the matrices in the convex hull are stable, and for which there exists a periodic switching such that the linear system explodes. Later, an explicit example in dimension 3 was given by Fainshil, Margaliot and Chiganski [14]. Precisely, consider the matrices

| (25) |

It is shown in [14] that every convex combination of and is stable, and yet a switch of period 1 between and yields an explosion. In [8], the authors asked the question whether the same system but with a Markovian switching can lead to explosion. Using numerical simulations, they suggest that this is true and the Lyapunov exponent is positive for not too fast nor too slow switching. Now, using Formula (24), we prove rigorously the following assertion:

Proposition 3.

Proof.

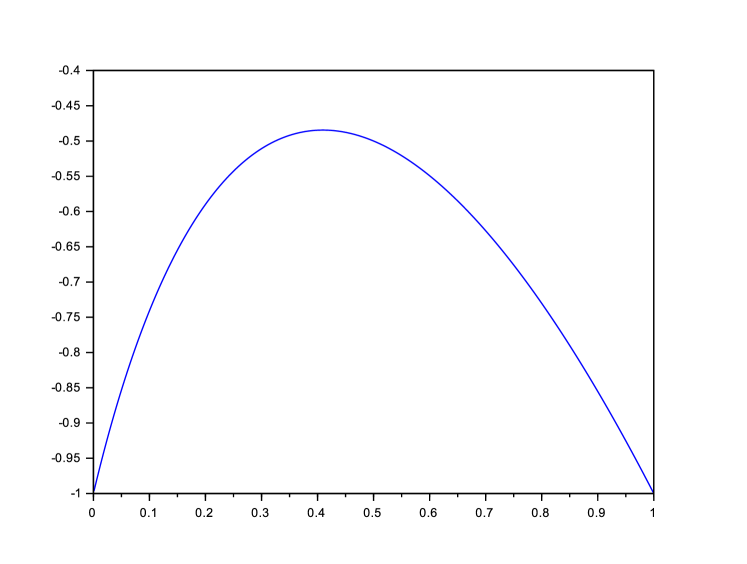

To emphasize the dependency on ,we write and for the mean matrix, the top Lyapunov exponent and the first order derivative, respectively, when the switching rates are given by the matrix in (23), and the matrices are (25). We also write for . In Figure 1(a) is plotted . One sees that the maximal value of this function is attained at some and worth . One sees on Figure 1(b), where is plotted , that on the interval , we have , so that in particular .

Let and . Replacing by in (19), we easily check that the Lyapunov exponent of the system is . Moreover, , so that , and the dynamic of the angular part of (19) is independent of . Hence, Proposition 2 entails

for some constant depending on . Choosing and yields

Letting concludes the proof, since

-

1.

-

2.

For all ,

∎

Example 4.

Assume as in Example 1 that . Then, . Using and , we get that , which yields

Notice that, from Jensen’s inequality,

so that

3.2 Richardson extrapolation for randomized splitting schemes

In [1], in order to approximate the solution of an ODE of the form

| (26) |

the vector field is splited as , where each flow can be solved exactly. More precisely, the two main examples of interest in [1] (to which we refer for details and motivations) are the so-called Lorenz-96 model and a finite-dimensional Galerkin projection of the vorticity formulation of 2D Navier-Stokes. The trajectory is then approximated by a discrete time scheme of the form

where is the flow associated to at time and are independent random variables distributed according to the standard exponential law. More precisely, for a fixed , is approximated by with , for a small . Notice that this does not enter directly our framework. However, consider the Markov-modulated ODE

where is a cyclic chain on with rate (i.e. it is a standard Poisson Process modulo ). We can take the times to define the jump times of , and thus is exactly where is the jump time of . In particular, if , assuming that the vector fields are bounded,

and

In other words, (which can be sampled exactly if can) can be seen as an alternative variation of the scheme of [1].

The convergence of to as for a fixed , or more precisely of the corresponding Markov transition operators, is stated in [1, Theorem 4.1], which is thus similar to our Proposition 1 at order . Notice that, a priori, the ODE (26) is in but [1, Theorem 4.1] is proven by restricting the study on the orbit of the process, which is assumed to be bounded (this is Assumption 1 of [1]), so that our results apply in this context.

The higher order expansion in Proposition 1 enables the use of a Richardson extrapolation to get better convergence rates: for instance we obtain, for a fixed and ,

for some constant .

3.3 Species invasion rate in a two species Lotka-Volterra model in random environment

We consider a model of two species in interaction, in a random environment, described by the following system of Lotka - Volterra equations:

| (27) |

We assume that (intraspecific competition), the other parameters can be positive or negative. The coefficients and represents the growth rates of species 1 and 2 respectively, while the coefficients and models the interaction between the two species. If for example while , we get a prey - predator system (species 1 being the prey, and species 2 the predator). Assumption 1 is also enforced in this whole section.

In the absence of species 2 and after accelerating the dynamics of by a factor , species 1 evolves according to a logistic equation in random environment:

| (28) |

We prove in the Annex the following result:

Lemma 1.

Assume that , and . Then the process with given by (28) and will ultimately lie in and admits a unique stationary distribution on . Moreover, converges in law to when goes to infinity.

The stationary distribution represents the population of species 1 at equilibrium in the absence of species 2. The invasion growth rate of species 2 when species 1 is at equilibrium is then given by

| (29) |

Intuitively, we are interested in the sign of this quantity, since when the abundance of the second species is close to , we have roughly

where solves (28) and the right hand side converges to when goes to infinity, thanks to Lemma 1 and the ergodic theorem. It is made rigorous in [4] that, indeed, the sign of gives information on the local behaviour of (27) near the boundary . Denoting by the mean with respect to of a function defined on , it is proven in [6], in the specific case when is a two-states Markov chain, that converges as goes to 0 to . The proposition below extends this result to the general case of a process satisfying Assumption 1 and with a first order expansion:

Proposition 4.

Assume that and . Then, for any invariant probability measure of ,

Proof.

First, note that the unique equilibrium of is and Assumption 2 holds (since thanks to Lemma 1, it is sufficient to consider initial conditions in the compact set ). By Theorem 1, and since the marginal of in is independent from (so that ), one has

| (30) |

with

for . Using the formula for derived in Remark 1, we have

which yields

Then, , so that

and finally, integrating this with respect to and using that ,

| (31) |

which concludes. ∎

Let us discuss the sign of the expression (31) in some particular cases.

-

1.

If and for all , then . This is expected, since in that case, the process solution to (28) is deterministic and does not depend on , and for all . More interestingly, if and but is varying, we still have .

-

2.

If and for all , using that , we get

This is always non-negative, as it can be interpreted as an asymptotic variance. Indeed, considering with , for ,

where we used that converges to and bounded

Example 5.

We consider the two-state case, i.e., is Markov chain on , with matrices rates given by

for some . The behaviour of the solutions to (27) was studied by Benaïm and Lobry in [6], through the signs of the invasion growth rates of species 1 and 2, in the competitive case (ie, when and are negative). Their study was complemented by Malrieu and Zitt in [21], who proposed an alternative formula for the invasion growth rate which made possible for them to understand the monotonicity of . In particular, it is a consequence of the proof of Lemma 4.1 in [21] that is increasing if while it is decreasing if , where is the coefficient of the second order term of the polynomial

that is , if we assume without loss of generality that . Let us prove that our results are in accordance with the results of Malrieu and Zitt, by studying the sign of the first order term of the expansion of when . Using Example 2, we have , and if and if , from which we compute

Since we have assumed that , the sign of is indeed the same as that of (recall that ).

Example 6.

4 Annex

4.1 Proof of Proposition 1

Proof.

This is essentially the proof of [22], in dual form since we work with rather than the law of the process. It is organized in three steps. First, assuming formally that (8) gives an expansion in of , we deduce the expression of and . With these definitions, in a second step, we establish the bounds (6) and (7) on and . Finally, from this, we obtain the bound (9) on .

Step 1. Fix . For all ,

| (32) |

Having in mind the ansatz that (8) gives an expansion in of , developing in each side of the above equality, and equating the terms of the same order (treating separately the terms and ), we end up with the following equations: for all ,

| (33) |

| (34) |

and

| (35) |

| (36) |

To shorten the notation, for , we write . Moreover, for a function , we use the notation . Equation (33) is equivalent to say that there exists such that for all , . Now, if we want Equation (34) for to have a solution , this will induce a constraint, fixing the value of . Indeed, this equation can be rewritten as

| (37) |

The left hand side averages to with respect to (for all fixed ), and thus we have to impose that

This is equivalent to

| (38) |

which is a transport equation with solution given by

In order to identify a suitable initial condition , we formally let and then go to in

which is obtained by integrating (32) and using that . This yields and as announced,

| (39) |

Now, reasoning by induction, we assume that for some , we have constructed satisfying , from which we want to define . Recalling the definition (37) of the pseudo-inverse , Equation (34) is then equivalent to the existence of a function such that

| (40) |

Once again, to find a suitable , we use Equation (34) at order that we rewrite as

| (41) |

As before, for fixed , since the left-hand side averages to with respect to , we impose

| (42) |

Notice that , so that, averaging Equation (40) with respect to and differentiating with respect to time,

| (43) |

Injecting Equations (43) and (40) in (42) yields

| (44) |

where we set

This is again a transport equation, similar to (38), but with a source term. The solution is given by

| (45) |

For now, by construction, for any choice of the function , the function defined by (40) where is given by (45) satisfies (34) and (42). It remains to specify a suitable initial condition . To do so, we need first to look at the so-called boundary layer correction terms .

Set . Then, Equations (35) and (36) read

| (46) |

and

| (47) |

Equation (46) is simply solved as

Moreover, taking and letting in (8) yields , hence we set

| (48) |

which indeed solves (46). Next, assuming by induction that has been defined for some , we can solve equation (47) to find

It remains to chose a suitable initial condition , which will be determined by the requirement of the long-time decay (7). Indeed, since , (7) can only hold if

and therefore,

| (49) |

Besides, from (8) applied with , we get that for all and, integrating (40) at with respect to , . Hence, the only choice of that is compatible with (7) is

Finally, is determined using again (40) at . At this point, we have completely determined a definition of and , which is the one that we use in the rest on the proof. It is such that (33), (34), (35) and (36) hold.

Step 2 We prove that bounds (6) and (7) on and hold true. We work by induction on , starting with . By compactness, recalling the definition (39) of , it is straightforward that for all , there exists such that for all and all ,

Let , and . Then, by Equation (48),

Using the ergodicity condition (3), we get for all , and ,

For , reasoning by induction, we assume that there exist constants and such that

and for all ,

Since and its derivatives in are uniformly bounded over , it is straightforward to check that that for any , and , there exist and such that for any ,

which we use extensively in the rest of this step. In the following, are fixed, and we denote by a constant which may change from line to line and depends only on . First, for all

by induction. Next, using that , we get that for all

by induction. Now, from (45), for all ,

To bound the derivatives in time of , instead of using (45), it is simpler to work with (44), which gives for

Reasoning by induction on yields . Gathering the previous bounds in (40) yields

This concludes the study by induction of . We now turn to the study of . Using Equation (49) and omitting the dependency in to alleviate notations, we decompose as

We have

where we used that and the previous bound on . Similarly,

where we have used the induction hypothesis on . Finally,

This proves the desired bounds on . In particular, at this stage, we have proven (6) and (7).

Step 3. We now bound the remainder given by (8) for a given . Introducing for a given , we see that, thanks to (33), (34), (35) and (36), all the low order terms in vanishes (as designed) so that

The bounds obtained in the previous step yield

for some depending only on . Interpreting as the solution of the equation with yields the Feynman-Kac representation

see [11, Theorem 6.3]. The bounds on immediately yields

for some depending only on .

Now, to get similar bounds for the derivatives in space of , we work by induction on , assuming that we have already obtained that

| (50) |

for all for some and some . Indeed, then, considering a multi-index , differentiating the equation yields

| (51) |

where, for all multi-index , is a matrix whose coefficients are some derivatives in of . In other words, considering a vector whose coefficients are all the partial derivatives in of of order , then solves an equation of the form

| (52) |

where acts coefficient-wise on , the coefficients of the matrix are derivatives in of and gathers and all the terms in (51) involving derivatives of of order . In particular, thanks to the bounds (6) and (7) established in step 2 and to the induction assumption, we have

for some depending on . We use again the Feynman-Kac formula for based on Equation (52), which reads

where is the solution of the matrix-valued ODE (for completeness, we provide a proof of this formula in appendix). Since is uniformly bounded, so it over , and thus

for some depending on . Since this holds for all , this concludes the proof by induction of (50) for all . To conclude, using that

we get that, for all ,

where we used (6), (7) and (50) (for ). This concludes the proof of (9), and thus the proof of Proposition 1.

∎

4.2 Feynman Kac formula

Lemma 2.

Let be a Markov generator on a set . For , consider for , solution of

| (53) |

where is a bounded matrix field, is a bounded vector field and is to be understood component-wise. Then, for all and ,

where is a Markov process associated to with and is the solution of the matrix-valued random ODE with , provided this is well-defined almost surely.

Proof.

Fix , . Then given in the statement of the lemma is a time-inhomogeneous Markov process with generator

and thus, considering the vector-valued function , we end up with

Using that , conclusion follows from

∎

4.3 Proof of Lemma 1

We can write , and then drop the superscript to alleviate notations; in other words, without loss of generality it is sufficient to treat the case (up to replacing by in Assumption 1).

For , let . By definition of and , we have that for all , for and for , which implies that for all , there exists a time such that, for all , . Now, on the state space , we introduce the metric

and we consider on the space of probability measures on the associated Wasserstein distance defined for all by

where the infimum runs overs all the coupling measures of and . We will show that there exists such that, for all and all ,

| (54) |

where stands for , the semigroup of at time . The above inequality implies Lemma 1 by classical arguments, since the space of probability measures on endowed with the Wasserstein metric is complete.

We first prove (54) for point and such that . In that case, a coupling of and is given by the random variables , where for all ,

In other words, and denote the solution to (28) with respective initial conditions and and constructed with the same realisation of the processus starting from .

Lemma 3.

Almost surely, for all , and ,

| (55) |

where . This immediately yields

Proof.

Let and write and . Let the solution of the differential equation

| (56) |

Then, for all , and all , we have

| (57) |

Indeed, the associated variational equation is

thus

where the inequality comes from the fact that implies for all .

We now tackle the case where the initial conditions of in the two chains are distinct . Let . Thanks to Assumption 1, there exists a coupling of and with

Fix , and let be such that is distributed according to (which is possible since regular version of the conditional laws exists in Polish spaces, see e.g. [18, Theorem 5.3]), and similarly for . Then, we define as follows: under the event , we let be a Markov process associated to with initial condition , and we set for all ; otherwise, we define these processes as two independent processes associated to with respective initial conditions and . In both cases, we define as solutions to

Then is a coupling of and with, using (55) and that almost surely,

As a conclusion, we have obtained that (54) holds for all for some constants , which concludes the proof.

Acknowledgements

The research of P. Monmarché is supported by the French ANR grant SWIDIMS (ANR-20-CE40-0022).

References

- [1] A. Agazzi, J. C. Mattingly, and O. Melikechi. Random Splitting of Fluid Models: Unique Ergodicity and Convergence. Communications in Mathematical Physics, March 2023.

- [2] Ludwig Arnold, Hans Crauel, and Jean-Pierre Eckmann. Lyapunov exponents: proceedings of a conference held in Oberwolfach, May 28-June 2, 1990. Springer, 2006.

- [3] A. Ben-Israel and T. N. E. Greville. Generalized Inverses: Theory and Applications. CMS Books in Mathematics. Springer, 2 edition, 2003.

- [4] M. Benaïm. Stochastic persistence. arXiv preprint arXiv:1806.08450, 2018.

- [5] M. Benaïm, S. Le Borgne, F. Malrieu, and P.-A. Zitt. On the stability of planar randomly switched systems. Ann. Appl. Probab., 24(1):292–311, 2014.

- [6] M. Benaïm and C. Lobry. Lotka Volterra in fluctuating environment or “how switching between beneficial environments can make survival harder”. Ann. Appl. Probab., 26(6):3754–3785, 2016.

- [7] M. Benaïm, C. Lobry, T. Sari, and E. Strickler. A note on the top Lyapunov exponent of linear cooperative systems. arXiv e-prints, page arXiv:2302.05874, February 2023.

- [8] M. Benaïm and E. Strickler. Random switching between vector fields having a common zero. Ann. Appl. Probab., 29(1):326–375, 02 2019.

- [9] Y. Chitour, G. Mazanti, P. Monmarché, and M. Sigalotti. On the gap between deterministic and probabilistic Lyapunov exponents for continuous-time linear systems. arXiv e-prints, page arXiv:2112.07005, December 2021.

- [10] I. Chueshov. Monotone random systems theory and applications, volume 1779 of Lecture Notes in Mathematics. Springer-Verlag, Berlin, 2002.

- [11] M. H. A. Davis. Piecewise-deterministic markov processes: A general class of non-diffusion stochastic models. Journal of the Royal Statistical Society. Series B (Methodological), 46(3):353–388, 1984.

- [12] R. J. Elliott and T. K. Siu. On markov‐modulated exponential‐affine bond price formulae. Applied Mathematical Finance, 16(1):1–15, 2009.

- [13] Alessandra Faggionato, Davide Gabrielli, and M Ribezzi Crivellari. Non-equilibrium thermodynamics of piecewise deterministic markov processes. Journal of Statistical Physics, 137:259–304, 2009.

- [14] L. Fainshil, M. Margaliot, and P. Chigansky. On the stability of positive linear switched systems under arbitrary switching laws. IEEE Trans. Automat. Control, 54(4):897–899, 2009.

- [15] BD Goddard, M Ottobre, KJ Painter, and I Souttar. On the study of slow-fast dynamics, when the fast process has multiple invariant measures. arXiv preprint arXiv:2305.04632, 2023.

- [16] L. Gurvits, R. Shorten, and O. Mason. On the stability of switched positive linear systems. IEEE Trans. Automat. Control, 52(6):1099–1103, 2007.

- [17] Haralampos Hatzikirou, Nikos I Kavallaris, and Marta Leocata. A novel averaging principle provides insights in the impact of intratumoral heterogeneity on tumor progression. Mathematics, 9(20):2530, 2021.

- [18] O. Kallenberg. Foundations of modern probability. Probability and its Applications (New York). Springer-Verlag, New York, second edition, 2002.

- [19] JEFFREY P. KHAROUFEH and STEVEN M. COX. Stochastic models for degradation-based reliability. IIE Transactions, 37(6):533–542, 2005.

- [20] S. D. Lawley, J. C. Mattingly, and M.l C. Reed. Sensitivity to switching rates in stochastically switched ODEs. Commun. Math. Sci., 12(7):1343–1352, 2014.

- [21] F. Malrieu and P.-A. Zitt. On the persistence regime for Lotka-Volterra in randomly fluctuating environments. ALEA Lat. Am. J. Probab. Math. Stat., 14(2):733–749, 2017.

- [22] K. Pakdaman, M. Thieullen, and G. Wainrib. Asymptotic expansion and central limit theorem for multiscale piecewise-deterministic markov processes. Stochastic Processes and their Applications, 122(6):2292–2318, 2012.

- [23] D. Talay and L. Tubaro. Expansion of the global error for numerical schemes solving stochastic differential equations. Stochastic Analysis and Applications, 8(4):483–509, 1990.