Competitive Auctions with Imperfect Predictions

Abstract

The competitive auction was first proposed by Goldberg, Hartline, and Wright. In their paper [GHW01], they introduce the competitive analysis framework of online algorithm designing into the traditional revenue-maximizing auction design problem. While the competitive analysis framework only cares about the worst-case bound, a growing body of work in the online algorithm community studies the learning-augmented framework. In this framework, designers are allowed to leverage imperfect machine-learned predictions of unknown information and pursue better theoretical guarantees when the prediction is accurate(consistency). Meanwhile, designers also need to maintain a nearly-optimal worst-case ratio(robustness).

In this work, we revisit the competitive auctions in the learning-augmented setting. We leverage the imperfect predictions of the private value of the bidders and design the learning-augmented mechanisms for several competitive auctions with different constraints, including: digital good auctions, limited-supply auctions, and general downward-closed permutation environments. We also design the learning-augmented mechanism for online auctions. For all these auction environments, our mechanisms enjoy -consistency against the strongest benchmark , which is impossible to achieve -competitive without predictions. At the same time, our mechanisms also maintain the -robustness against all benchmarks considered in the traditional competitive analysis, including , and . Considering the possible inaccuracy of the predictions, we provide a reduction that transforms our learning-augmented mechanisms into an error-tolerant version, which enables the learning-augmented mechanism to ensure satisfactory revenue in scenarios where the prediction error is moderate. We also prove a robustness ratio lower bound for mechanisms with perfect consistency. The lower bound is strictly greater than the optimal competitive ratio of digital good auctions, showing the impossibility of maintaining the optimal worst-case bound with perfect consistency.

1 Introduction

Revenue maximization is an important problem in the field of algorithmic mechanism design. Goldberg, Hartline, and Wright [GHW01] introduced the competitive analysis framework into the revenue maximization problems and they called this type of auctions the competitive auctions. In the competitive auction frameworks, there are bidders who want to buy an abstract service. Each bidder has a private value which represents his valuation of the service. The auctioneer initiates a sealed-bid auction and receives the bid of each bidder . Then the auctioneer decides whether to serve each bidder according to a given feasibility constraint and the amount should pay for the service. The bidder aims to maximize its utility, which is the difference between and its payment if he gets served and if he does not get served. Our goal is to design a mechanism that maximizes the auctioneer’s revenue while encouraging buyers to truthfully report their private valuations, i.e. . That is, the mechanism is truthful or incentive compatible.

Different from the Bayesian setting of the revenue maximization auctions, competitive auctions do not assume a prior distribution on the private values. Instead, competitive auctions take a traditional algorithmic way of worst-case analysis. In the framework, we compare the revenue of the mechanism with a revenue benchmark function and use the worst-case ratio (i.e. competitive ratio) to measure the performance of the proposed mechanisms. Let denote a benchmark function, then maps to , where denotes the set of possible value vectors and assigns a benchmark revenue to each vector. Let be a truthful mechanism and let denote the expected revenue of when the private value vector is . Then is -competitive against if for all .

The worst-case analysis of competitive ratio is a prominent mathematical framework to analyze the online algorithm and it guides the design of online algorithms for many years. However, with the development of machine learning technology in recent years, people are able to predict various unknown information. It has been found that such predictions can be applied in the design of online algorithms, resulting in better performance than worst-case bounds. There are many works that follow the line of the learning-augmented online algorithm design. Classical problems such as ski rental, caching, and scheduling are revisited in this setting [PSK18, AGP20, LV21, Roh20, JPS22, LLMV20, IKMQP21, LX21]. The idea of utilizing the imperfect prediction was naturally brought to the algorithmic mechanism design field by [XL22] and [ABG+22] independently. They show that the imperfect prediction of the private information of the selfish bidders can also be leveraged to improve the performance of truthful mechanisms.

The spirit of these learning-augmented algorithms is to leverage imperfect predictions robustly. That is, the algorithm should have a strong theoretical guarantee when the given prediction is accurate, but it does not lose much even when the prediction is arbitrarily bad. This is captured by the standard consistency-robustness analysis framework proposed in [PSK18]. Within this framework, we assess the algorithm using two metrics: the consistency ratio and the robustness ratio. The consistency ratio is the approximation ratio when the prediction is correct and the robustness ratio is the approximation ratio when the prediction is wrong.

1.1 Our Results

In this paper, we investigate the learning-augmented competitive setting where the auctioneer is given the prediction for the private value of each bidder . Based on the different feasibility constraints of the auctioneer, we have considered three specific competitive auctions, namely digital good auctions, limited supply auctions, and general downward-closed permutation environments. In the digital good auction, there is no feasibility constraint since the digital good can be duplicated infinitely and allocated arbitrarily. In limited supply auctions, the service can only be allocated to a limited number of bidders. In the general downward-closed permutation environments, the constraint is only required to be downward-closed, i.e. the subset of a feasible set is also feasible. We also consider the setting where the bidders arrive in a random order, which is called online auctions.

In the learning-augmented setting, our mechanism takes the prediction values as the input. In other words, our goal is actually to find a collection of truthful mechanisms, denoted as , where is the vector of predictions. We say is -consistent against benchmark , -robust against if is -competitive against when the prediction is perfect and -competitive against when the prediction is imperfect. That is,

| (1) |

Notice that we are allowed to use distinct benchmarks for consistent ratio and robust ratio, which is different from other works on learning-augmented mechanism design.

Throughout the paper, we take the strongest optimal revenue benchmark as the benchmark for the consistency ratio. It should be pointed out that the benchmark is not considered in the literature of competitive auctions without predictions since there is no mechanism that can achieve a constant or even non-trivial competitive ratio against it [GHW01]. Instead, several weaker benchmarks are considered in the competitive analysis, including , , maxV, and . We use these weaker benchmarks as our robustness benchmarks. is the largest revenue obtained by setting a fixed price for the service, with existing at least two bidders who can afford the price. maxV is the largest revenue obtained by a multi-unit Vickrey auction. These two benchmarks are mainly studied in digital good auctions. The benchmark was extended to more complicated settings. Actually, there are two different extensions of in the limited-supply auctions, namely and . While is more straightforward, , the optimal revenue obtained by an envy-free allocation, is more generally applicable and economically meaningful. can be further extended to the general downward-closed permutation environment.

Upper Bounds

If the prediction is perfect, the problem becomes purely an algorithm design problem rather than a mechanism design problem. Thus, it is not difficult to achieve perfect consistency alone. The challenging task is to achieve perfect consistency and constant robustness simultaneously. The main result of this paper is to achieve this goal for all the auction environments and benchmarks studied before.

Theorem 1.

For digital good auctions, limited supply auctions, and auctions with general symmetric downward-closed feasibility constraints, there are truthful auctions with perfect consistency with respect to the optimal office solution and constant robustness with respect to all the benchmarks studied for competitive auctions before.

We summarize our robustness ratio in different auction environments and for different benchmarks in Table 1. It is worth noting that the mechanisms we designed for digital good auction and downward-closed permutation environment are both black-box reductions. Let be the competitive ratio of the employed black-box mechanism, our mechanisms achieve -robust for digital good auctions and -robust for auctions with general downward-closed permutation environment.

| Auction Environment | Robustness Benchmark | Robustness Ratio (with perfect consistency) | Competitive Ratio (without prediction) |

| Digital Good Auction | [Corollary 1] | [CGL14] | |

| maxV | [Corollary 1] | [CGL14] | |

| -Limited Supply | 4.42 [Theorem 4] | 2.42 [CGL14] | |

| 5.42 [Theorem 5] | 3.42 [CGL15] | ||

| Downward-closed Permutation Environment | [Corollary 3] | [CGL15] | |

| Online Auction | [Theorem 7] | [CGL14] | |

| maxV | [Theorem 7] | [CGL14] |

Lower Bound

In the table, we can see that there is some degradation in ratio if we compare our robust ratios with the previous best-known competitive ratios without considering consistency. Is such degradation necessary? Can we achieve perfect consistency while still keeping the same robust ratio? We prove that this is impossible by the following lower bound result.

Theorem 2.

Any -consistent truthful mechanism for digital good auction has a robust ratio against no less than .

The competitive ratio of the optimal mechanism for digital good auction is , thus our lower bound shows that it is impossible to maintain the optimal competitive when we require the perfect consistency of a mechanism. Since the digital good auction is a special case of other auction environments, the lower bound also applies to other auction environments considered.

Error-Tolerant Design

The original consistency-robustness analysis framework is too extreme that the consistency guarantee only works when the prediction is perfect, which makes the theoretical results not practical. To give a practical solution, we also propose an Error-Tolerant Mechanism in Section 7. A remarkable fact is that our error-tolerant mechanism is a black-box reduction, it transforms a non-error-tolerant mechanism to an error-tolerant version. The reduction is very general so it can apply to all mechanisms we proposed in this paper. The error-tolerant mechanism takes a confidence level as the input parameter. Let denote the maximal relative prediction error, if , our mechanism is competitive against the strongest benchmark. Otherwise, our mechanism is competitive against benchmark which is robust against. However, the revenue bound with respect to the benchmark is invalid immediately when . To fix this issue, we select from a certain distribution , and then we analyze the revenue bounds with respect to both benchmark and benchmark, expressing the bounds in terms of . A similar idea of selecting the confidence level parameter from a certain distribution is also used by Balcan et al. in their random expansion mechanism [BPS23]. When is set to a continuous probability distribution, the revenue bound with respect to exhibits gradual variations as the prediction error increases, and will not become invalid at some certain prediction error threshold.

1.2 Techniques and Challenges

Notice that our problem is an objective-maximization problem, such kind of problem admits a trivial random combined mechanism to leverage the predictions. The combined mechanism is, with probability we provide service and charge payment according to the optimal revenue calculated from ; with probability , we run a competitive truthful mechanism. These two mechanisms are truthful so their random combination is also truthful. With a bit of abuse of notation, we also use to represent the optimal mechanism while assuming the prediction is perfect. As an example, in the digital good auctions, mechanism is just to offer the price to each bidder . Assume that is an -competitive mechanism. The trivial random combination of and is -consistent and -robust. In a word, for the objective-maximization problem, it is trivial to obtain -consistent and -robust mechanism if the problem admits -competitive mechanism without prediction. However, such a trivial random combination is far from sufficient to achieve -consistency, since we need to obtain perfect consistency and this implies an unbounded robust ratio.

Our idea comes from another kind of combination of and a black-box competitive mechanism . At a glance at the learning-augmented competitive auction problem, one may come up with a naive combination to achieve perfect consistency. That is, to run the mechanism when , and to run when . However, the combined mechanism is not truthful since the bidder can alter the mechanism selected by misreporting its value. Let the bid vector without . To ensure truthfulness, an observation is that, if we have several truthful mechanisms and we decide which mechanism to apply to bidder only based on and , then the combined mechanism will be truthful since the bidder can not determine the mechanism applied to it. We call this type of combined mechanism a Bid-Independent Combination, which is the core technical component of our proof.

Back to the naive combination, we can modify it by using the bid-independent combination approach. If , indicating that the prediction is correct for all bidders except , we apply the mechanism to bidder . If , indicating that there is at least one incorrect prediction for the bidders other than , we apply to bidder . This combined mechanism is truthful by the Bid-Independent Combination trick. If , then , every bidder is applied with mechanism, so the mechanism actually reduces to mechanism and it gains optimal revenue in this situation. Thus, the mechanism is -consistent.

Through the above Bid-Independent Combination trick, we achieve truthfulness and perfect consistency freely. However, compared with the random combination and the naive untruthful combination, the Bid-Independent Combination has a very subtle issue that it may be the case that different mechanisms are operating simultaneously on the different bidders. Thus the robustness and feasibility guarantee of the combined mechanism can not be directly inherited from and . This is the main challenge we need to overcome in our paper.

In digital good auctions, we only face the robustness problem since the bid-independent combination of arbitrary mechanisms is feasible in this case. We notice that the combined mechanism runs two mechanisms simultaneously only when the number of wrong predictions is exactly one. It is not clear if the bid-independent combination can obtain a constant robust ratio or not. To save it, we employ another random combination outside the bid-independent combination. We find that the mechanism guarantees -robustness of the robustness benchmark when the number of wrong predictions is one which is exactly the case that bid-independent combination fails. Here we crucially use the fact that (and actually all the competitive benchmarks considered) does not depend on the highest value. Thus, one wrong prediction will not ruin the mechanism significantly.

For more complex constraints, we must deal with the robustness and the feasibility at the same time. In the limited-supply auction, we leverage a special property of the employed mechanism and show that the bid-independent combination of it and is always feasible. In the general downward-closed permutation environment, the feasibility constraint becomes very challenging. The difficulty we meet is that the downward-closed feasibility requirement is so general that we have no idea how to satisfy it if the mechanism and run simultaneously. So our idea is to incorporate a rejection mechanism into bid-independent combination to separate and . Here, the rejection mechanism means the mechanism that trivially rejects all bidders. Rigorously, we apply on bidder if ; apply on bidder if there is exactly one wrong prediction in ; apply on bidder if there is at least two wrong predictions in . We can show that it is the only possible case that mechanism and run simultaneously or mechanism and run simultaneously. On the other hand, can run concurrently with any mechanism in the downward-closed constraint. By inserting the mechanism , we solve the feasibility issue. However, the bid-independent combination of these three mechanisms can only guarantee a robustness ratio when the total number of wrong predictions is at least . So we are still left with the case that the number of wrong predictions is and . In particular, the case of two wrong predictions is very tricky since changing two values can change the benchmarks entirely. This is in strong contrast with the single wrong prediction case. We spend the vast majority of Section 5 dealing with this gap. We need to introduce new mechanisms and benchmarks to handle this. A proof sketch will be given at the beginning of the section.

1.3 Related Works

Competitive Auctions

The study of digital good auctions was initiated by [GHW01], where they propose the random sampling optimal price auction. Fiat et al. [FGHK02] and Alaei et al. [AMS09] show that the auction has a competitive ratio of and against the benchmark respectively. Fiat et al. propose the random sampling cost-sharing auction and prove that it achieves -competitive against . There is a sequence of works on improving the competitive ratio, including [GH03, HM05, FFHK05, II10]. Goldberg et al. [GHKS04] prove the competitive lower bound of the digital good auction. Chen et al. [CGL14] proved that the optimal competitive ratio is exactly and they also study the maxV benchmark and show the optimal competitive is . The online random order setting of the digital good auction is considered by Koutsoupias and Pierrakos [KP13] where the authors provide a reduction from the offline setting to the online setting.

The limited supply auction is studied with respect to the benchmark by Goldberg et al. [GHK+06], where the author shows a straightforward reduction from digital good auctions to limited supply auctions. Thus, the competitive ratio results for the digital good auctions also hold for the limited supply setting. Hartline and Yan [HY11] define the economically significant benchmark and show a constant competitive ratio against it in limited supply environments and general downward-closed permutation environments. The competitive ratio in the general downward-closed permutation environment is improved by several works [DHY15, HH12, HH13, DHH13]. So far, the best competitive ratio against is in the limited supply environment and in the downward-closed permutation environment, which are obtained in [CGL15] via the benchmark decomposition technique.

Learning-augmented Mechanisms

Xu and Lu [XL22] revisit several mechanism design problems in the learning-augmented settings, including single-item revenue maximization, frugal path auction, truthful job scheduling, and two facility location on a line. The revenue maximization auction they studied is different from ours, not only because the constraint is restricted to single-item, but also because they compete with the benchmark thus the robustness ratio is not constant and depends on the scaling of the bids. Balkanski et al. [BGT23] study truthful job scheduling independently and attain the tight asymptotic consistency-robustness trade-off. Agrawal et al. [ABG+22] design the learning-augmented mechanism for the one-facility location problem in the two-dimensional Euclidean space. Istrate and Bonchis [IB22] study the learning-augmented mechanism for the obnoxious facility location problem on several metric spaces. Gkatzelis et al. [GKST22] show the ability of imperfect predictions to improve the Price of Anarchy in games. A very recent and relevant work by Balcan et al. [BPS23] investigates the general multi-dimensional mechanism design problem with side information (predictions). The authors propose a mechanism that achieves an -consistent ratio, where represents an upper bound on any bidder’s value for any allocation.

1.4 Paper Organization

In Section 2, we provide an introduction to the auction environments and benchmarks. Moving forward, in Section 3, we unveil our mechanism for digital good auctions. In Section 4, we present our mechanism designed specifically for auctions with a limited supply. In Section 5, we introduce our mechanism for general downward-closed permutation environments. In Section 6, we present our mechanism for online auctions. In order to increase the robustness of our mechanisms, we introduce modifications that enable them to tolerate small errors in prediction in Section 7. Finally, we give the lower bound for perfect consistency mechanism in Section 8.

2 Preliminary

2.1 Auction Environments

Notations and the Indices

We use and to denote the private value vector and predicted value vector respectively. We arrange the indices such that , and we define to be the order of predicted values, such that for all . When there are bidders with the same private value or predicted value, we break ties to ensure consistency between the two orders. That is, if , and , then we set , and vice versa.

In addition, we allow for random mechanisms since deterministic mechanisms have been shown to not have a non-trivial competitive ratio against some meaningful benchmarks. A random mechanism is said to be truthful if it is given by a distribution of truthful deterministic mechanisms.

We consider several different auction environments in this paper: digital good auctions, limited supply auctions, general downward-closed permutation environments, and online auctions.

Digital good auction

The auctioneer can offer an unlimited number of services and any combination of bidders can be served simultaneously (e.g., digital goods).

-limited supply auction

At most bidders can be served simultaneously. For example, the auctioneer has identical items to sell, and each bidder needs at most one item.

General downward-closed permutation environments

The feasibility constraint of the allocation is a general symmetric downward-closed set . A set is said to be downward-closed if for every and feasible, we have that is also feasible. We say that is symmetric if, for any , the entries of can be arbitrarily permuted without affecting its feasibility. We also assume that is convex since we consider randomized mechanisms and the random combination of two feasible allocations is also feasible. We focus on the symmetric constraint mainly because we can only define the envy-free optimal revenue benchmark on a symmetric constraint. Notice this auction environment includes the digital good auction and -limited supply auction as its special case. When facing an asymmetric constraint, we can symmetrize it by assuming that the roles of all bidders in the constraint are permutated uniformly at random, which is usually called a permutation environment [HY11].

Online auctions

Bidders arrive online in random order. Upon the arrival of each bidder , the prediction is revealed to the auctioneer, then the auctioneer posts an irrevocable price for the services based on the bids and predictions of previously arrived bidders. There is no feasibility constraint, which is the same as the digital good auctions.

2.2 Benchmarks

Consistency Benchmark

Throughout the paper, we employ the optimal revenue as the benchmark for consistent ratio, where represents the feasibility constraint and varies across different auction environments. Specifically, in digital good auctions, . In -limited supply auctions, . With clear context, we may omit the subscript and write .

Robustness Benchmark

Regarding the benchmark of robust ratio, we investigate several candidates who are widely considered in the competitive analysis. The first is

| (2) |

where is reordered as we have mentioned before. is the largest revenue obtained by setting a fixed price for the service, with at least two bidders can afford the price. benchmark is only meaningful in digital good auctions and online auctions which have no feasibility constraint. There is a natural extension in -limited-supply auction,

| (3) |

One may feel confused about the additional assumption that at least two bidders get served. This is because any truthful mechanism has an arbitrarily bad competitive ratio if , which makes the benchmark uninteresting without this assumption. Another common-used benchmark for digital good auctions and online auctions is

| (4) |

which is the largest revenue obtained by a multi-unit Vickrey auction.

For the more general downward-closed permutation environment, Hartline and Yan [HY11] introduced a new benchmark named , which denotes the maximum revenue that can be obtained through an envy-free allocation. Similarly to the consideration of , people actually consider the competitive ratio with respect to where is the vector obtained by replacing with . is defined on symmetric constraint set , we use the notation to specify the constraint. Given a monotone allocation where the monotone allocation means , its envy-free revenue is defined as Then is the largest possible envy-free revenue while . Hartline and Yan [HY11] also give a characterization of envy-free payment through virtual value so that we can better understand the benchmark.

Definition 1 (Virtual value).

Given a vector , we assume that the entries of have been sorted in descending order. We can calculate the virtual value of each bidder corresponding to as follows. First, we calculate the smallest non-decreasing concave function satisfying and . The formal definition is

| (5) |

Then the virtual value is,

| (6) |

Lemma 1 (Restatement of Theorem 2.4 in [HY11]).

Let be a symmetric set and is the virtual value of , then the envy-free optimal revenue over is

| (7) |

Hence, can be seen as the optimal solution to a linear maximization problem over with virtual values as linear weights. So far we always assume that is in descending order, but this is only for simplicity. If a value vector is not descending ordered, its envy-free optimal value is calculated by first ordering it and then using Lemma 1. In other words, is a symmetric function and the identification of the bidder doesn’t influence the benchmark.

2.3 Benchmark Decomposition Lemma

Another tool apart from the bid-independent combination trick is the following benchmark decomposition lemma. With this lemma, we decompose the benchmark into parts that correspond to different scenarios, then we can handle them separately.

Lemma 2 (Benchmark Decomposition with Prediction).

Let and be truthful mechanism and both with -consistent ratio against benchmark. If is -robust against benchmark and is -robust against benchmark. Then there is a truthful mechanism, which is -consistent against and -robust against benchmark.

Proof.

Consider the mechanism which runs with probability and runs with probability . Let and denote the total revenue generated by running and on instance , respectively.

If the prediction is perfect, then by the consistent ratio of them. So the revenue of the combined mechanism is . Thus the combined mechanism is -consistent.

If the prediction is not perfect, then , . So the total revenue of the combined mechanism is which means that the mechanism is -robust against benchmark. ∎

3 Digital Good Auction

In this section, we will discuss digital good auctions against and maxV benchmarks. Both and maxV enjoy a property that is key to the analysis of the robust ratio, they are both dominated by .

Definition 2 (Benchmark domination).

For two benchmark and over , we say dominates if .

Our result applies to all benchmarks dominated by , specifically, we have the following theorem.

Theorem 3.

If benchmark is dominated by and there is an -competitive truthful mechanism against , then there is a truthful mechanism, which is -consistent against and -robust against .

Let denote the number of wrong predictions. To prove the theorem, we decompose

| (8) |

We design -consistent mechanisms for the above two benchmarks respectively. Then we use Lemma 2 to obtain a mechanism for benchmark. The mechanism for is obtained via the bid-independent combination trick.

Mechanism 1.

We first run the black-box mechanism and calculate the allocation rule and payment rule of every bidder. For each bidder , if , then offer price to bidder ; if , we apply the black-box mechanism on bidder .

Mechanism 1 is a bid-independent combination of and , thus it is -consistent and truthful. Moreover, it maintains the robustness of when against the benchmark .

Lemma 3.

If is -competitive against , then Mechanism 1 is truthful, and it is -consistent against and -robust against .

Proof.

We only prove the robust ratio. When , for any bidder , there is at least one incorrect prediction other than . Therefore Mechanism 1 runs for every bidder, thus its revenue is at least by the competitive ratio of . Then Mechanism 1 is -robust against . ∎

We then use the mechanism to deal with the robustness in the case of one wrong prediction value.

Mechanism 2.

Use mechanism, that is, offer price to bidder .

Lemma 4.

Mechanism 2 is truthful and it is -consistent against and -robust against .

Proof.

The truthfulness and consistency are obvious. We only prove the robust ratio. If , let be the bidder with the wrong prediction. Since the predictions for bidders other than are correct, they will accept the price. Thus the revenue is . Since , we have . Therefore, we have

The last inequality is because dominates . Thus Mechanism 2 is -robust against . ∎

Then Theorem 3 is a direct corollary of Lemma 3, Lemma 4, and Lemma 2. In [CGL14], the authors show the existence of a -compeitive mechanism for benchmark and a -competitive mechanism for maxV benchmark, which leads to the following corollary.

Corollary 1.

There is a truthful mechanism, which is -consistent against and -robust against -benchmark. Moreover, there is a truthful mechanism, which is -consistent against and -robust against maxV benchmark.

4 -Limited Supply Auction

In this section, we will discuss -limited supply auction against and benchmark.

For benchmark, Goldberg et al.[GHK+06] show the equivalence between digital good auctions and limited-supply auctions. The key observation is that only depends on the highest bidders, so we can throw away the bids except for the highest and runs a digital good auction on these bidders with charging the threshold bidding. This reduction maintains the competitive ratio of digital good auctions. The equivalence also exists in our setting, so the following theorem is obvious.

Theorem 4.

If there exists a digital good auction with -consistency ratio against , -robustness ratio against , then there exists a -limited supply auction with the same consistency and robustness against .

When the constraint corresponds to the -limited supply environment, we use to substitute . The benchmark depends on all bids, so we can not use the aforementioned reduction. We use the bid-independent combination techniques again to design a -consistent mechanism for this problem. Different from the unlimited supply setting, we must be careful with the feasibility here. The benchmark decomposition is the same as in the digital good auctions.

| (9) |

Our mechanism for also employs a black-box competitive mechanism of -limited supply auction.

Mechanism 3.

For each bidder , if , apply mechanism on it; if , apply the black-box mechanism on bidder .

Note that different bidders may apply different mechanisms in Mechanism 3, so it is not naturally a feasible mechanism. Fortunately, we can show the feasibility holds if the employed black-box satisfies an extra assumption.

Lemma 5.

If the winner set of is always a subset of the highest bidders and it is -competitive against , then Mechanism 3 is feasible, -consistent against and -robust against .

Proof.

Feasibility: If there are more than wrong predictions or there is no wrong prediction, Mechanism 3 reduces to and mechanism, respectively. Thus the only situation we need to investigate is when there is exactly one wrong prediction. Denote the bidder with the wrong prediction as . If or the predicted value of bidder is not the highest of all the predictions (i.e. ), we know the bidder is not served in mechanism since he will reject the price or does not in the winner set. In this case, the total number of services allocated by Mechanism 3 is at most since other bidders use the same allocation rule output by , which is feasible. If and , then bidder is allocated with one item by applying mechanism. But in this case, since the predicted value of is one of the highest predicted value, and for , , we can derive that the bidder also has the highest true value. By the assumption that the winner set of is a subset of the highest bidders, we know the union of and the winner set of is also a subset of the highest bidders. So in this case, we also have the total number of services allocated by Mechanism 3 is at most . This finalize our proof of feasibility.

Consistency: The consistency ratio is obvious .

Robustness: If there are at least wrong predictions, Mechanism 3 degenerates to . The expected revenue is at least in this case by the competitive ratio of . Then Mechanism 3 is -robust against . ∎

The mechanism for -limited supply auctions proposed in [CGL15] meets our assumption about the black-box mechanism in Lemma 5.

Lemma 6.

The winner set of the -competitive mechanism for -supply auction in [CGL15] is always a subset of the highest bidders.

Proof.

The mechanism is the random combination of the -items Vickrey auction and the optimal mechanism for -bidders digital good auction applied on the highest bidders. So the winner set is always a subset of the highest bidders. ∎

For benchmark, we use the mechanism.

Mechanism 4.

Run the mechanism. That is, offer price for and reject bidder for .

Lemma 7.

Mechanism 4 is -consistent against and -robust against .

Proof.

Truthfulness, Feasibility and Consistency are obvious.

Robustness: If there is exactly one wrong prediction, denote this bidder as . Consider bidder satisfying and , the expected revenue from is , so the total revenue is at least

which shows the -robust ratio against . ∎

Theorem 5.

There is a mechanism with -consistent ratio against and -robust ratio against .

5 Downward-Closed Permutation Environments

In this section, we propose the mechanism for the general downward-closed permutation environment auction. In this general environment, the literature only considers benchmark and we take it as our robustness ratio benchmark.

Without loss of generality, we assume that for any bidder, the allocation vector that only serves bidder with probability is feasible. When considering such a general constraint, we have not been able to identify any properties of a black-box mechanism that can be leveraged to address the feasibility issues caused by bid-independent combination, as we did in Section 4. In this section, we do not assume any additional properties of the employed black-box mechanism. Instead, we present a general approach to address the issue of feasibility.

Recall the Mechanism 1. If we use a similar version here, the outcome may be infeasible when . Let be the bidder with the wrong prediction. In this case, is applied with the mechanism, and the others are applied with the black-box mechanism. The simultaneous operation of these two different mechanisms may result in conflicts and compromise the feasibility of the allocation. However, it is inevitable to have multiple mechanisms running simultaneously. Our idea is to use a special mechanism that can run together with any other mechanism to bridge and . In the downward-closed environment, this special mechanism is to reject all the bidders. We use to denote this rejection mechanism. Then we propose the following mechanism, which is a bid-independent combination of and .

Mechanism 5.

For bidder , if , then run on bidder . If , then reject bidder (i.e. run on ). If , then run on bidder .

This mechanism is always feasible but we can only guarantee its robustness when .

Lemma 8.

Mechanism 5 outputs a feasible allocation. Under the symmetric environment, assuming that is -competitive against , Mechanism 5 is -consistent against and -robust against the benchmark .

Proof.

Feasibility: When , Mechanism 5 degenerates to mechanism, thus it is feasible. When , then , we have , the mechanism degenerates to and becomes feasible. When , only and are active, then the allocation is feasible since is downward-closed. When , only and are active, the allocation is also feasible.

Consistency: When , Mechanism 5 degenerates to mechanism, thus obtain revenue of .

Robustness: When , Mechanism 5 degenerates to , thus it is feasible and -competitive against . ∎

With Mechanism 5, the remaining case is or . In Section 3, we are only left with the case . Let’s recall what we did to handle this case. Lemma 4 shows that even though operates solely based on the predicted values , completely disregarding all bids, it still has a nice -robust ratio against benchmark. The main reason is, since there is at most one bidder with the wrong prediction, we lose at most one bidder’s revenue and is somewhat insensitive to the revenue loss of one bidder.

The insensitivity of can be shown also exist in the benchmark . In fact, we prove a stronger result showing that is insensitive to the revenue loss of fewer than bidders. Here . To be specific, let be a set of bidders, denotes the value vector by setting the value of bidders in to . Then we have

Lemma 9.

For any , symmetric , set and positive integers with , we have .

This lemma indicates that even if we ignore arbitrary bidders for , the resulting benchmark is still left with a constant proportional part compared with . We will recap and prove the lemma in Section 5.1. Another challenge that prevents us from designing the mechanism for case is, under general constraints, a single wrong prediction can significantly alter the allocation from what we want. So we do not directly use mechanism but use a new mechanism to address this issue, the mechanism is the bid-independent combination of for a different subset of bidders . See details in Section 5.1. With this approach, we can tackle the benchmark and , since is insensitive to one wrong prediction and is insensitive to two wrong predictions by Lemma 9. We call these two parts of the benchmark the Insensitive Benchmarks.

Now we focus on the remaining part of the benchmark . Note that is sub-additive and monotone, so

Then we have,

| (10) |

which is our overall benchmark decomposition. From the decomposition, the only remaining part of the benchmark is . To tackle this benchmark, we slightly modify the single-item Vickrey auction and use the bid-independent combination of the modified version and . Since we are now facing a concrete mechanism rather than a black box, we can further leverage the properties of the single-item Vickrey auction to address the feasibility issue. This part is shown in Section 5.2.

Before proceeding with the next proofs, let’s first elaborate on the tie-breaking rule of , which is crucial for the subsequent proof. Let be the allocation of , we require that for all . The following lemma ensures that we could make this requirement.

Lemma 10.

For symmetric , there exist a solution such that and for any , we have .

Proof.

Let be any allocation of . Since is symmetric, then if , we have , or we can swap and and get another feasible solution that has better revenue.

If there exist such that for any satisfying , , then we can always find new optimal allocation such that , and for and , . The new allocation has the same revenue as . After modifying all such tuple, we get the allocation we want. ∎

5.1 Handling the Insensitive Benchmarks

In this subsection, we deal with insensitive benchmarks. To address the problem that wrong prediction may significantly change the allocation, we do not directly apply to all bidders, but use the following mechanism.

Mechanism 6.

Let . For bidder , let , run on bidder .

Note that can not be changed by ’s bid and mechanism is truthful for any set . Therefore Mechanism 6 is a bid-independent combination of different and this ensures the truthfulness of the mechanism. We will see that Mechanism 6 guarantees the robustness against and at the same time. Before proving the properties of Mechanism 6, let’s first prove Lemma 9.

Proof of Lemma 9.

Let , define . Since for any set with bidders, we only need to show

Let be the non-decreasing concave envelop of , which we have introduced in Lemma 1. Similarly, let be the non-decreasing concave envelop of .

We first show that for any , , then we use this fact to prove the lemma. For , , . For , and

Next, we prove for . The formal definition of and can be written as follows and we only focus their evaluation on integer numbers,

Let be the parameter such that

It’s obvious that thus . We further require , this is because if and , we have

Replace with , we have

Which leads to a contradiction. The LHS of above inequality is a weighted average of and , and the RHS is a weighted average of and . The inequality is because and , .

With the above argument, we can find such that

Let , , , we have

Since is symmetric, there is a monotone allocation such that . We next show that , which is enough to prove .

By Abel’s lemma(a.k.a. summation by parts),

The second and third equality is because of Abel’s lemma. The first inequality is because and . ∎

Lemma 11.

Mechanism 6 outpus a feasible allocation. Moreover, it is -consistent against and -robust to the benchmark for .

Proof.

Let be the allocation of Mechanism 6.

Feasibility: Let , then . Because for any , the bidders in are applied with the same mechanism . For any bidder , , so will be directly rejected, i.e. . Let be the allocation of , we have , and , , then . Since is downward-closed, .

Consistency: When , we have and , . Thus all bidders are applied with mechanism. The mechanism degenerates to which is -consistent.

Robustness: We have proved that for . Since , , all bidders in accept the price . Let , the revenue is

The second equality is because of for and for . The first inequality is because that and is monotone. The third equality is because that . The last inequality is because of Lemma 9. Since , the revenue

This leads to the -robustness ratio against when . ∎

The following holds as a corollary of Lemma 11.

Corollary 2.

Mechanism 6 is -robust against the benchmark .

Proof.

By Lemma 11, the revenue of Mechanism 6 is at least

Since the cases and are disjoint, this expression is exactly the same as

∎

5.2 Handling Benchmark

Our last task is to find a -consistent and -robust mechanism for benchmark . Since benchmark is sensitive to two wrong predictions, we have no hope to obtain a bounded robustness ratio if we still use a bid-independent combination of mechanisms that discard all the bids. Our mechanism is based on a modified version of the single-item Vickrey auction. After the modification, it can run concurrently with , which addresses the feasibility issue of the bid-independent combination approach. Also, it guarantees at least half the revenue of the original single-item Vickrey auction.

Restricted Single-Item Vickrey Auction

Let be the allocation of and be the allocation of single-item Vickrey auction(i.e. ). Given any bidder , we slightly modify the single-item Vickrey auction by restricting the allocation of the only winner. Formally, the allocation vector of the restricted single-item Vickrey auction is defined by and . When there is no ambiguity in the context, we omit and use the notation in place of . This allocation rule is monotone and we can charge the threshold bidding (i.e. ) as the unit price, which ensures the truthfulness of the mechanism. We use the notation to refer to the restricted single-item Vickrey auction.

Our mechanism for is a bid-independent combination of , , and original single-item Vickrey auction. Therefore it is truthful.

Mechanism 7.

For each bidder , run on if . If , let be the bidder with the wrong prediction, run on . If , run single-item Vickrey auction on .

Lemma 12.

Mechanism 7 outputs a feasible allocation. Moreover, Mechanism 7 is -consistent against , -robust against the benchmark .

Proof.

Feasibility: When , let be the bidder with the wrong prediction. In this case, is applied with , and others are applied with . Let the allocation be , if , then and , we have so . In the remaining part of the feasibility proof, we assume . We have , . Note that only when . If , then thus is feasible.

If , then or . We first show that . If , then which means that , leading to a contradiction. Now we prove that is feasible when . If , we have . To prove the feasibility of , we consider . Since , we have . Then . By the symmetry of , . If , then . Therefore because of the convexity of .

When , all bidder are applied with single-item Vickrey auction or a restricted version, so the allocation and it is feasible.

Consistent ratio: If , the mechanism degenerates to . Thus the consistent ratio is .

Robust ratio: It is enough to consider the revenue when . In this situation, if , then bidder is applied with single-item Vickrey auction and pay , thus the revenue is at least . If , let be the bidder with the wrong prediction, the bidder is applied with , and pays . By Lemma 10, we have , then , thus the revenue is at least . Overall, the robust ratio is at most . ∎

5.3 Overall Mechanism

Our overall mechanism for benchmark is running Mechanism 5, Mechanism 6, Mechanism 7 with probability , , respectively where is the competitive ratio of the black-box mechanism. The following theorem holds immediately from Lemma 2.

Theorem 6.

If there is an -competitive truthful mechanism against for the downward-closed permutation environment, then there is a truthful mechanism with -consistency ratio against , -robustness ratio against for the auctions with downward-closed permutation environment.

Since there is a -competitive truthful mechanism against for the downward-closed permutation environment [CGL15], we have the following corollary.

Corollary 3.

There is a truthful mechanism with -consistency ratio against , -robustness ratio against for the auctions with downward-closed permutation environment.

6 Online Auction

Koutsoupias and Pierrakos [KP13] show a black-box reduction result that any truthful offline mechanism gives rise to an online auction in their paper. Given an offline mechanism , the reduction is conducted as follows: at each arriving bidder , we collect the bids of previously arrived bidders. Then we run a -bidders offline auction on all arrived bidders. is actually giving a price to bidder according to , we then provide this price to bidder . This reduction is called Online Sampling Auction. Koutsoupias and Pierrakos prove that the online sampling auction transforms an offline mechanism to an online one with at most twice the competitive ratio.

Lemma 13 ([KP13]).

If is -competitive against or maxV in an offline digital good auction environment. Then the online sampling auction is -competitive against or maxV in online auctions.

In our problem, we can construct a similar reduction which is named Online Sampling Auction with Predictions.

Online Sampling Auction with Predictions(OSAP)

Recall that is the random arriving order. Upon the arrival of a bidder and its prediction . We run an offline mechanism on all the arrived bidders and match each prediction with the bidder for . Specially, we always offer the predicted price to the first bidder.

We first show the consistency and truthfulness of OSAP.

Lemma 14.

If the employed is truthful and -consistent against . Then the OSAP is truthful and -consistent against .

Proof.

Truthful mechanism is equivalent to proposing a random price according to the data and , thus the OSAP runs like proposing an immediate price to each arrival bidder. This shows the truthfulness of the OSAP.

Let and , and the auction running on the first bidders and predictions. If , then for any realized random order and any arrival time , we have . Consider the -th arrival, the total revenue of the is by the perfect consistency of . Thus the bidder must pay its private value . Therefore, even for any realized , the total revenue of the OSAP is . Which shows the perfect consistency of the OSAP. ∎

Since is -robust, i.e. -competitive, we can use Lemma 13 to obtain the -robust ratio of OSAP. Then Lemma 13 leads to the following corollary.

Corollary 4.

If the employed is -robust against or maxV, then OSAP is -robust against or maxV.

Recall Corollary 1, combined with Lemma 14, Corollary 4, we have

Theorem 7.

There is a mechanism for online auctions with -consistent against and -robust against . Moreover, there is a mechanism for online auctions with -consistent against and -robust against maxV.

Remark 1.

In this section, our reduction is from the offline -consistent auction to the online -consistent auction, which is different from the reductions in previous sections. This makes our technique in this section independent of the one introduced in Section 1.2 and more similar to the existing reduction techniques. The reason for this difference is that online auctions have a key distinction from offline auctions. In an online auction, since we can only see the arrived bids, even if the number of wrong predictions is large, we still can not guarantee that all bidders are applied with the competitive black-box mechanism. More specifically, before the first bidder with the wrong prediction has arrived, we can only offer the predicted price to maintain perfect consistency.

7 Error-Tolerant Design

Though the mechanisms proposed in the previous sections have a perfect -consistent guarantee, it fails if the prediction is not perfect. We can not guarantee a good competitive ratio even if the error is very small. In other words, our mechanisms have very poor error-tolerant ability. Our task in this section is to present a general error-tolerant modifier that can apply to all mechanisms we have proposed. We consider the general constraints in this section, thus the modifier also applies to the digital good auction and limited supply auction. The reader can easily extend the idea to the online auction.

Let be an operator parameterized by the prediction and a confidence level . The operator acts like an attractor which changes the bid to its prediction if they are close enough. That is, for the input bid vector , output a vector where

Suppose we have a -consistent, -robust mechanism for some benchmark . To get an error-tolerant version of the mechanism, our idea is to run the learning-augmented mechanism we developed on the processed bid vector , and we allocate the services accordingly. Thus the allocation of this mechanism is also feasible. We next prove the allocation rule is monotone so that we can determine the payment rule according to Myerson’s lemma to ensure truthfulness. We denote the error-tolerant modifier , and denote the modified version of .

Lemma 15.

The allocation rule of is monotone.

Proof.

Let be the allocation rule of the bidder in and be the allocation rule of the bidder in . By the definition of , we have for all . Since is truthful, then is monotone with respect to , we then prove that is also monotone.

Consider any two bids of , which satisfy . If , then ; If , then ; If , then . If or , then . Therefore is also monotone. ∎

The lemma shows that is truthful. To bound its revenue, we consider the revenue obtained by while running on an auction where the true value vector is , denoted as . Let be the revenue of while running on the auction where the value vector is . The following inequality holds.

Lemma 16.

Proof.

For simplicity, we only prove the lemma for the case that is differentiable. But this lemma also holds for general piecewise continuously differentiable allocation rules. Let and be the payment rules of the bidder in mechanism and respectively when the private value vector is . Then it’s enough to prove for any since the revenue is the summation of payment of all bidders. Here .

By Myerson’s lemma,

For ,

The second equality is because that for and for .

For ,

The first equality is because that is a constant function in and is a jump point which has jump value . The last equality is because of when .

For ,

The first equality is because that and are two jump points of . The first inequality is because that when or . The last equality is because of when .

Overall, we have .

∎

We assume the benchmark is homogeneous, and monotone. Here is homogeneous means that for any and . These properties hold for all the benchmarks displayed in this paper. Now we prove the error-tolerant property of .

Theorem 8.

Given a -consistent, -robust mechanism where the consistent ratio is against benchmark and the robust ratio is against any monotone and homogeneous benchmark , then is an error-tolerant truthful mechanism. Define the error rate

then following holds,

-

•

If , the competitive ratio is (against ).

-

•

Else, the competitive ratio is (against ).

Proof.

-

•

If ,

Here the first inequality is because of Lemma 16 and the last equation is because that is -consistent. Since , by the monotonicity and homogeneity of , we have

Then the competitive ratio is bounded by

- •

∎

Note that the , maxV and benchmark are monotone and homogeneous, so Theorem 8 applies on all these benchmarks. Our proof does not require any extra assumption of the constraint, the feasibility of is ensured by the feasibility of the black-box mechanism.

7.1 Randomized Parameter

The competitive ratio bound is discontinuous at the confidence parameter . Xu and Lu [XL22] have shown that this discontinuity is inevitable if the mechanism is deterministic. However, we can use a parameter randomizing technique to eliminate this discontinuity easily. Concretely, we choose a continuous distribution , and let be sampled from this distribution. Let denote the resulting mechanism, denote the expected revenue of the mechanism while running on the instance .

Theorem 9.

Given a -consistent, -robust mechanism where the consistent ratio is against benchmark and the robust ratio is against any monotone and homogeneous benchmark . Assuming for all , if is sampled from distribution , we have the following two revenue bounds of , comparing to and respectively.

-

•

.

-

•

.

Proof.

Exponentially decaying

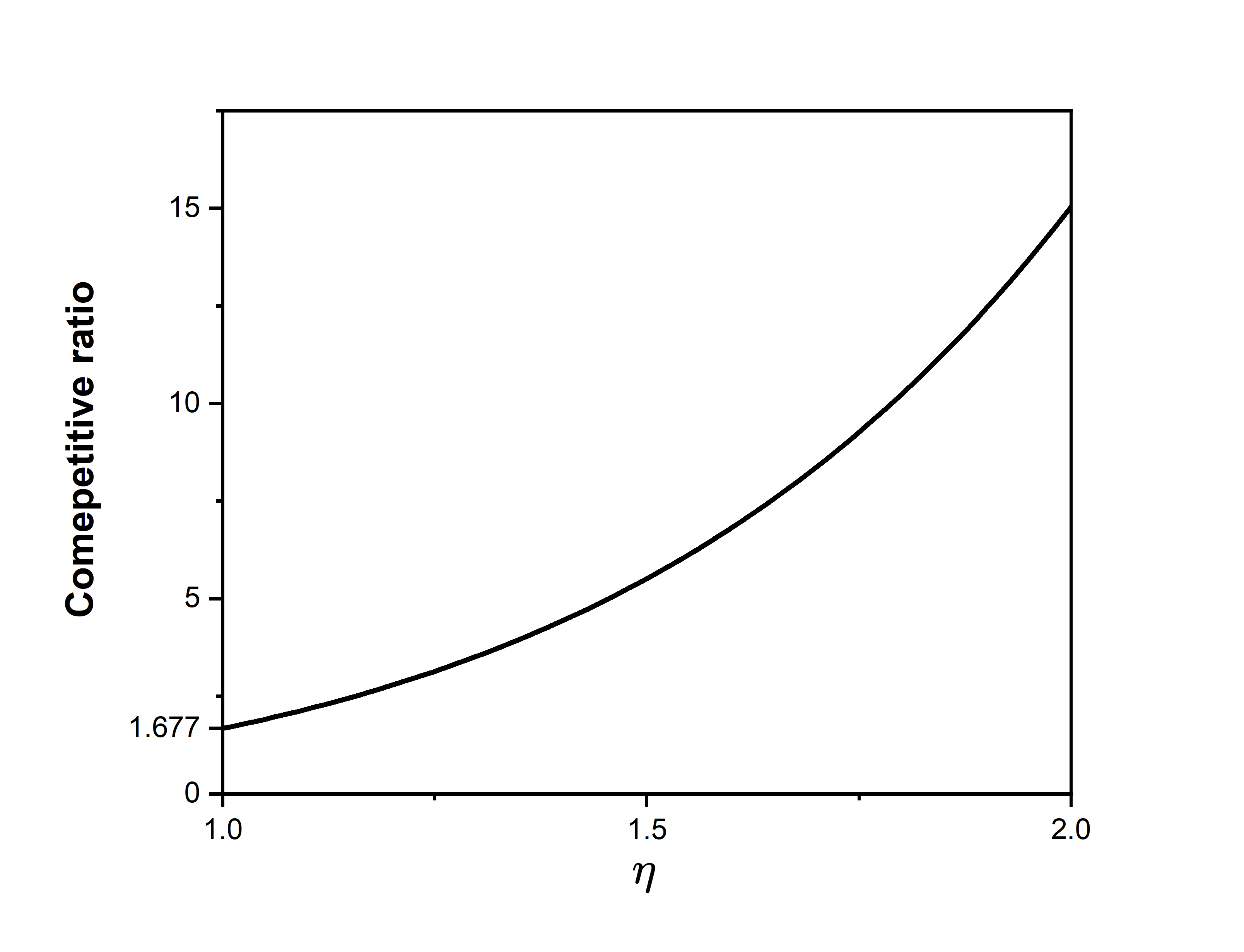

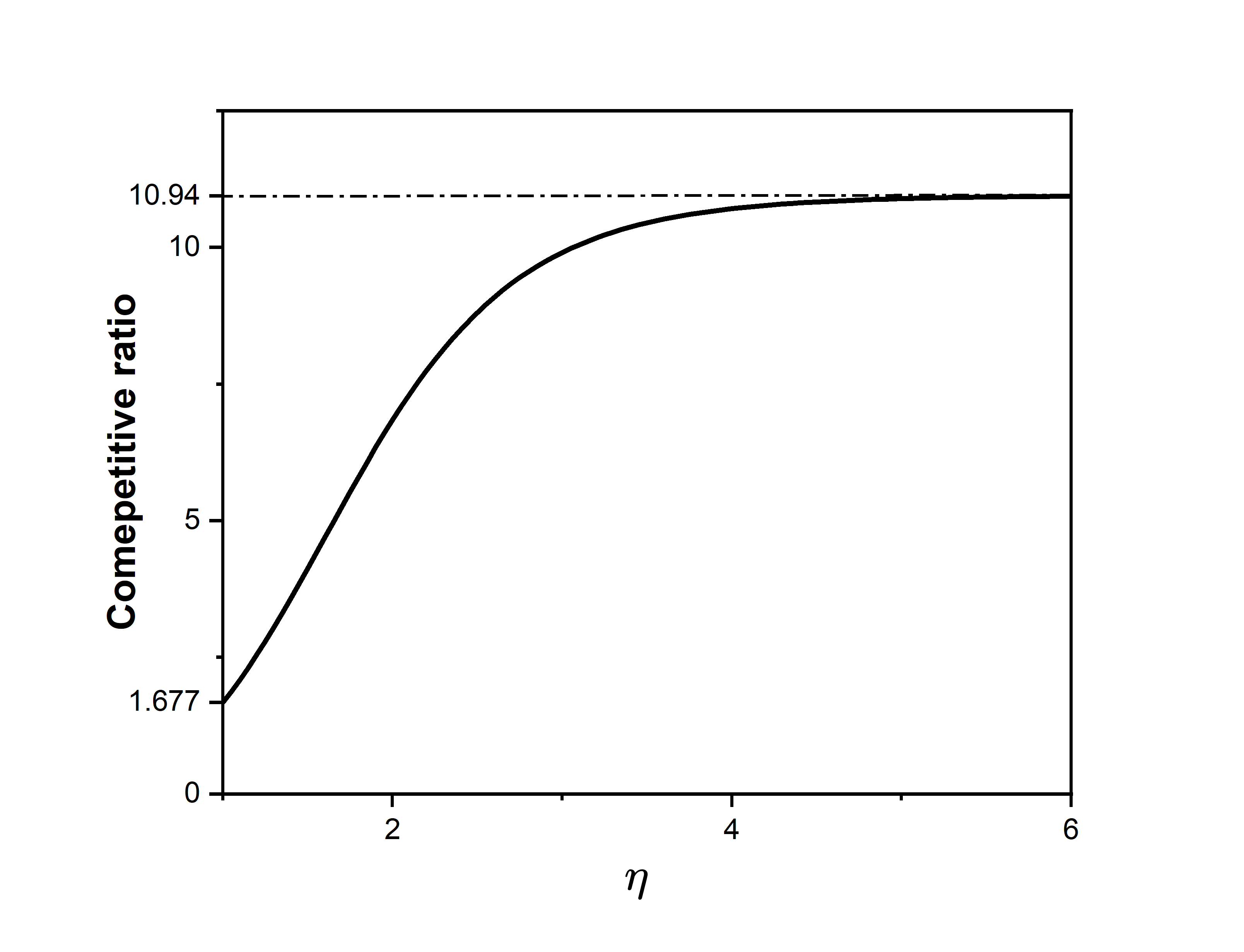

Inspired by the double search random expansion mechanism proposed in [BPS23], we calculate a specific example to exhibit the performance of Theorem 9. We reuse the notation by denoting it as the probability density, let , be the mechanism for digital good auction proposed in Section 3, . We report the competitive ratio w.r.t. and respectively in Figure 1.

Remark 2.

The example of Figure 1 presents a -consistency ratio and -robustness ratio. We point out that if we let be a distribution that concentrates around , the consistent ratio can be arbitrarily close to and the robustness ratio can be arbitrarily close to . However, the cost is that the competitive ratio of the mechanism against will converge more quickly as the prediction error increases. To be concrete, in this example, when , we can guarantee a revenue better than . But if we do not use the error-tolerant design or use a distribution more concentrated around , then it may perform worse than our example here when . The choice of provides an opportunity to balance between the theoretical consistency-robustness bound and the practical ability to tolerate the prediction error.

8 Lower Bound for Perfect Consistency Mechanism

We prove the lower bound for the digital good auction in the -bidders case and we do not order the private value vector in this section. Let be a truthful mechanism with -consistency ratio. Fix the prediction , here is a number to be determined later. We prove our lower bound by a probabilistic method argument. We consider the distribution of the private value vector of bidders. The distribution is defined as a conditional distribution of the so-called equal-revenue distribution, which is used to prove the competitive ratio lower bound of the digital good auction. The probability density function of the equal-revenue distribution is , we denote the distribution . Define , the distribution we need is simply the conditional distribution of the equal-revenue distribution given that the event happens. We denote the distribution and its probability density . Formally, since

we have

Our lower bound proof analyzes the expected revenue that the mechanism obtains from each bidder, let denote the expected revenue that obtains from the bidder when the private value vector is . There are some facts about shown in previous works [GHKS04, CGL14], and we restate them in the following lemma.

Lemma 17 ([GHKS04, CGL14]).

Let be a truthful mechanism, then

-

(i)

is non-decreasing with respect to .

-

(ii)

.

-

(iii)

.

The next lemma shows that the bidder must contribute a large revenue outside to maintain the perfect consistency.

Lemma 18.

Let be a -consistent, -robust mechanism. If we fix the prediction to be , then

Proof.

Since is -consistent, we have . By Lemma 17, , we have . Since any truthful mechanism in the digital good auction is bid-independent pricing, must offer the deterministic price to the bidder when to make sure . Similarly, must offer the deterministic price to the bidder when to make sure . Therefore, we have,

| (11) |

By Lemma 17 (iii), we have

The first equality is because of equation (11). Thus, . Let be the robust ratio of , then we have

| (12) |

Set where , we have . By Lemma 17 (i), is monotone with respect to , so we obtain the desired result. ∎

Next, we bound the expected revenue of and expectation of benchmark on instance distribution in Lemma 19 and Lemma 20. Then we use a probabilistic method argument to show the lower bound in Theorem 2.

Lemma 19.

Proof.

Lemma 20.

Proof.

Since , we have

∎

Theorem 2.

Any -consistent truthful mechanism for digital good auction has a robustness ratio against no less than .

Proof.

Thus there must exist a such that,

The expectation is on the randomness of the randomized mechanism. Note that is the robust ratio of , then

Let , we have . ∎

The optimal competitive ratio in digital good auctions is [CGL14]. Our robustness lower bound shows that it’s impossible to maintain the optimal worst-case ratio while having perfect consistency.

Remark 3.

Note that the digital good auction is a special case of the more general limited-supply auction and downward-closed permutation environments, and the benchmark is the same benchmark with or in the digital good auction. Therefore, our lower bound in this section is also the lower bound for more general limited-supply auctions and downward-closed permutation environments.

9 Discussion

In this paper, we design the perfect consistent learning-augmented mechanisms for several competitive auctions. It is worth mentioning that we consider a maximization problem that has a trivial random combination approach to design a learning-augmented mechanism. The existing works on the learning-augmented mechanism mainly focus on the deterministic mechanism. We proposed the Bid-Independent Combination trick, which significantly outperforms the random combination approach. We recognize it as a conceptual contribution that imperfect predictions can also be leveraged non-trivially in the randomized mechanism design and maximization problems.

Since our mechanisms employ mechanisms without predictions, an interesting question is whether one can improve the robustness ratio(with perfect consistency) by using non-black-box mechanisms. Specifically, let’s focus on the simplest digital good auction, what is the optimal robustness ratio with perfect consistency? We have already shown that the optimal ratio is in . An immediate idea is to revisit the proof idea of the optimal competitive ratio [CGL14]. However, the proof heavily relies on the fact that the revenue function of the optimal mechanism can be monotone. This property is inherently unachievable by mechanisms with perfect consistency.

References

- [ABG+22] Priyank Agrawal, Eric Balkanski, Vasilis Gkatzelis, Tingting Ou, and Xizhi Tan. Learning-augmented mechanism design: Leveraging predictions for facility location. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 497–528, 2022.

- [AGP20] Keerti Anand, Rong Ge, and Debmalya Panigrahi. Customizing ml predictions for online algorithms. In International Conference on Machine Learning, pages 303–313. PMLR, 2020.

- [AMS09] Saeed Alaei, Azarakhsh Malekian, and Aravind Srinivasan. On random sampling auctions for digital goods. In Proceedings of the 10th ACM conference on Electronic commerce, pages 187–196, 2009.

- [BGT23] Eric Balkanski, Vasilis Gkatzelis, and Xizhi Tan. Strategyproof scheduling with predictions. In 14th Innovations in Theoretical Computer Science Conference (ITCS 2023), volume 251, page 11. Schloss Dagstuhl-Leibniz-Zentrum für Informatik, 2023.

- [BPS23] Maria-Florina Balcan, Siddharth Prasad, and Tuomas Sandholm. Bicriteria multidimensional mechanism design with side information. arXiv preprint arXiv:2302.14234, 2023.

- [CGL14] Ning Chen, Nick Gravin, and Pinyan Lu. Optimal competitive auctions. In Proceedings of the forty-sixth annual ACM symposium on Theory of computing, pages 253–262, 2014.

- [CGL15] Ning Chen, Nick Gravin, and Pinyan Lu. Competitive analysis via benchmark decomposition. In Proceedings of the Sixteenth ACM Conference on Economics and Computation, pages 363–376, 2015.

- [DHH13] Nikhil R Devanur, Bach Q Ha, and Jason D Hartline. Prior-free auctions for budgeted agents. In Proceedings of the fourteenth ACM conference on Electronic commerce, pages 287–304, 2013.

- [DHY15] Nikhil R Devanur, Jason D Hartline, and Qiqi Yan. Envy freedom and prior-free mechanism design. Journal of Economic Theory, 156:103–143, 2015.

- [FFHK05] Uriel Feige, Abraham Flaxman, Jason D Hartline, and Robert Kleinberg. On the competitive ratio of the random sampling auction. In Internet and Network Economics: First International Workshop, WINE 2005, Hong Kong, China, December 15-17, 2005. Proceedings 1, pages 878–886. Springer, 2005.

- [FGHK02] Amos Fiat, Andrew V Goldberg, Jason D Hartline, and Anna R Karlin. Competitive generalized auctions. In Proceedings of the thiry-fourth annual ACM symposium on Theory of computing, pages 72–81, 2002.

- [GH03] Andrew V Goldberg and Jason D Hartline. Competitiveness via consensus. In SODA, volume 3, pages 215–222, 2003.

- [GHK+06] Andrew V Goldberg, Jason D Hartline, Anna R Karlin, Michael Saks, and Andrew Wright. Competitive auctions. Games and Economic Behavior, 55(2):242–269, 2006.

- [GHKS04] Andrew V Goldberg, Jason D Hartline, Anna R Karlin, and Michael Saks. A lower bound on the competitive ratio of truthful auctions. In STACS 2004: 21st Annual Symposium on Theoretical Aspects of Computer Science, Montpellier, France, March 25-27, 2004. Proceedings 21, pages 644–655. Springer, 2004.

- [GHW01] Andrew V Goldberg, Jason D Hartline, and Andrew Wright. Competitive auctions and digital goods. In Proceedings of the twelfth annual ACM-SIAM symposium on Discrete algorithms, pages 735–744, 2001.

- [GKST22] Vasilis Gkatzelis, Kostas Kollias, Alkmini Sgouritsa, and Xizhi Tan. Improved price of anarchy via predictions. In Proceedings of the 23rd ACM Conference on Economics and Computation, pages 529–557, 2022.

- [HH12] Bach Q Ha and Jason D Hartline. The biased sampling profit extraction auction. arXiv preprint arXiv:1206.4955, 2012.

- [HH13] Bach Q Ha and Jason D Hartline. Mechanism design via consensus estimates, cross checking, and profit extraction. ACM Transactions on Economics and Computation (TEAC), 1(2):1–15, 2013.

- [HM05] Jason D Hartline and Robert McGrew. From optimal limited to unlimited supply auctions. In Proceedings of the 6th ACM Conference on Electronic Commerce, pages 175–182, 2005.

- [HY11] Jason Hartline and Qiqi Yan. Envy, truth, and profit. In Proceedings of the 12th ACM conference on Electronic Commerce, pages 243–252, 2011.

- [IB22] Gabriel Istrate and Cosmin Bonchis. Mechanism design with predictions for obnoxious facility location. arXiv preprint arXiv:2212.09521, 2022.

- [II10] Takayuki Ichiba and Kazuo Iwama. Averaging techniques for competitive auctions. In 2010 Proceedings of the Seventh Workshop on Analytic Algorithmics and Combinatorics (ANALCO), pages 74–81. SIAM, 2010.

- [IKMQP21] Sungjin Im, Ravi Kumar, Mahshid Montazer Qaem, and Manish Purohit. Non-clairvoyant scheduling with predictions. In Proceedings of the 33rd ACM Symposium on Parallelism in Algorithms and Architectures, pages 285–294, 2021.

- [JPS22] Zhihao Jiang, Debmalya Panigrahi, and Kevin Sun. Online algorithms for weighted paging with predictions. ACM Transactions on Algorithms (TALG), 18(4):1–27, 2022.

- [KP13] Elias Koutsoupias and George Pierrakos. On the competitive ratio of online sampling auctions. ACM Transactions on Economics and Computation (TEAC), 1(2):1–10, 2013.

- [LLMV20] Silvio Lattanzi, Thomas Lavastida, Benjamin Moseley, and Sergei Vassilvitskii. Online scheduling via learned weights. In Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1859–1877. SIAM, 2020.

- [LV21] Thodoris Lykouris and Sergei Vassilvitskii. Competitive caching with machine learned advice. Journal of the ACM (JACM), 68(4):1–25, 2021.

- [LX21] Shi Li and Jiayi Xian. Online unrelated machine load balancing with predictions revisited. In International Conference on Machine Learning, pages 6523–6532. PMLR, 2021.

- [PSK18] Manish Purohit, Zoya Svitkina, and Ravi Kumar. Improving online algorithms via ml predictions. Advances in Neural Information Processing Systems, 31, 2018.

- [Roh20] Dhruv Rohatgi. Near-optimal bounds for online caching with machine learned advice. In Proceedings of the Fourteenth Annual ACM-SIAM Symposium on Discrete Algorithms, pages 1834–1845. SIAM, 2020.

- [XL22] Chenyang Xu and Pinyan Lu. Mechanism design with predictions. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence (IJCAI-22), pages 571–577, 2022.