A Comprehensive Review on Financial Explainable AI

Abstract.

The success of artificial intelligence (AI), and deep learning models in particular, has led to their widespread adoption across various industries due to their ability to process huge amounts of data and learn complex patterns. However, due to their lack of explainability, there are significant concerns regarding their use in critical sectors, such as finance and healthcare, where decision-making transparency is of paramount importance. In this paper, we provide a comparative survey of methods that aim to improve the explainability of deep learning models within the context of finance. We categorize the collection of explainable AI methods according to their corresponding characteristics, and we review the concerns and challenges of adopting explainable AI methods, together with future directions we deemed appropriate and important.

1. Introduction

Finance is a constantly evolving sector that is deeply rooted in the development of human civilization. One of the main tasks of finance is the efficient allocation of resources, with a chief example being the handling of capital flows between various entities with different needs. These entities can be divided into individuals, companies, and countries, and lead to the common categorization of personal, corporate, and government finance. The sector can be traced back to 5000 years ago, in the agrarian societies that had been established and developed for some thousand of years at the time. Indeed, one of the first examples of banking, a central institution within finance, can be attributed to the Babylonian empire. Since then, societal development and technological advances have pushed the field to undergo several changes. In the past two decades, these changes have been particularly marked, due to the accelerating pace of technological development, especially in the context of AI. The latter has started spreading across multiple segments of finance, from digital transactions to investment management, risk management, algorithmic trading, and more (Team, 2022). The use of novel AI- and non-AI technologies to automate and improve financial processes is now known as FinTech (Financial Technology), and its growth in the past two decades has been remarkable (Mroczkowska, 2020). In this review, we focus on AI-based technologies and machine learning for financial applications.s

Financial researchers and practitioners have been relying on supervised, unsupervised, and semi-supervised machine learning methods as well as reinforcement learning for tackling many different problems. Some examples include credit evaluation, fraud detection, algorithmic trading, and wealth management. In supervised-based machine learning methods it is common to use e.g., neural networks to identify complex relationships hidden in the available labeled data. The labels are usually provided by domain experts. For instance, one can think of building a stock-picking system, where a domain expert labels periods of positive and negative returns. The machine is then tasked to build the relationship between (possibly) high-dimensional data, and positive and negative returns of a given stock (or multiple stocks) and generalize to unseen data to e.g., predict the future stock’s behavior. In unsupervised-based machine learning methods, the task is instead to identify data with similar characteristics that can therefore be clustered together, without domain-expert labeling. For example, one can think of identifying all stocks that have similar characteristics into clusters using some similarity metrics, such as valuation, profitability and risk. Semi-supervised learning is a middle ground between supervised and unsupervised learning, where only a portion of the data is labeled. Finally, reinforcement learning aims to maximize, through a set of actions, the cumulative reward specified by the practitioners. Reinforcement learning is used in finance for e.g., portfolio construction. Reinforcement learning is strictly related to Markov decision processes and substantially differs from both supervised and unsupervised learning.

Among supervised, unsupervised, and reinforcement learning methods, there is vast heterogeneity in terms of complexity. Some methods are considered easier to understand, hence to interpret by practitioners (also referred to as white-box methods), while others are considered not interpretable (also referred to as black-box methods). To this end, neural networks and deep learning strategies, that underpin the majority (albeit not the entirety) of recent machine learning methods for financial applications, are considered black-box methods - i.e., the reason for a given prediction is not of easy access when available). This constitutes a critical issue, especially in risky and highly regulated sectors, such as healthcare and finance, where a wrong decision may lead to catastrophic loss of life (healthcare) or capital (finance). Hence, it was deemed important to understand the reasons (i.e., the data and patterns) the machine used to make a given decision. This aspect encompasses the broad field of AI transparency. The latter is composed of three pillars, (i) AI awareness, (ii) AI model explainability, and (iii) AI outcome explainability. The first is tasked to understand whether AI is involved in a given product. The second is responsible to provide a detailed explanation of the AI model, including its inputs and outputs. The third is responsible to provide a granular explanation of the inputs’ contributions to the AI model’s outcomes. To this last category, we find a vast array of post-hoc interpretability methods. In this review, we assume that AI awareness is achieved, i.e., we know that in a given financial process AI is involved, and focus on AI explainability, also referred to as eXplainable AI or simply XAI. A further distinction commonly made is between interpretability and explainability of an AI model. These two terms, frequently used interchangeably, have subtle differences. Interpretability refers to how and why a model works. Explainability refers to the ability of explaining the results in human terms.

While deep learning methods are considered black-boxes, many other methods in finance are considered white-box methods. The trade-off between complexity and interpretability is perhaps one of the most debated aspects in the field of financial AI. On the one hand, white-box methods are highly interpretable but lack the ability to grasp complex relationships, frequently failing to meet the desired performance. On the other hand, black-box methods are not interpretable but usually (although not always) meet the desired performance. Therefore, it is not surprising that there are significant efforts being pushed forward in recent years to render black-box methods more interpretable, where the primary example is the field of deep learning. In this paper, we provide an extensive review of XAI methods for the financial field that we name FinXAI. Although there have been a number of surveys on XAI methods (Cambria et al., 2023; Sahakyan et al., 2021; Arrieta et al., 2020; Guidotti et al., 2018; Molnar, 2020; Mueller et al., 2019; Rojat et al., 2021), these papers are targeted towards general XAI, and are not specific to finance. Hence, we conduct a review on explainability techniques exclusively related to financial use cases.

To compile this review, we took into account 69 papers, focusing mainly, though not exclusively on the third pillar, i.e., the explainability of the inputs’ contributions to the AI model’s outcomes. To this end, we considered both post-hoc interpretability methods applied to black-box deep learning models, and inherently transparent models that do not require further post-hoc interpretability. Despite the relatively small number of collected papers in the field of XAI, it is important to note that our main objective is to focus specifically on XAI techniques applicable to the financial industry. This targeted approach will provide valuable insights for researchers in related fields and will ultimately help drive innovation and progress in the financial industry. With the growing need for transparency and accountability of deep learning, the XAI community has seen increasing growth in the number of works published, we focus here instead only on works concerning financial use cases. Notably, FinXAI is but a small subset of the general field of XAI and, thus we take a holistic approach to assembling existing studies with the goal of keeping up to date with the current approaches. The papers were queried from both Google Scholar and Scopus where we searched using a set of keywords relating to works that have applied explainable AI techniques in financial use cases, the set of keywords include “XAI, explainable AI, finance, financial sector, financial field, explainable ML”. We try to collect a diverse set of papers that covers each category sufficiently well, and summarized in tables LABEL:tab:_XAI_CE, LABEL:tab:_XAI_FP, LABEL:tab:_XAI_FM. We also noticed the majority of explanation types were limited to fact-based explanations, hence we explicitly search for techniques explaining in the form of counterfactuals. Counterfactual explanations are deemed as a desirable form of explanation as the receiver tends to prefer understanding why a certain prediction was made instead of the opposing.

The main contributions of our work as such:

-

•

We provide an extensive study on consolidating XAI methods in the field of finance (FinXAI), for researchers interested in prioritizing transparency in their solutions.

-

•

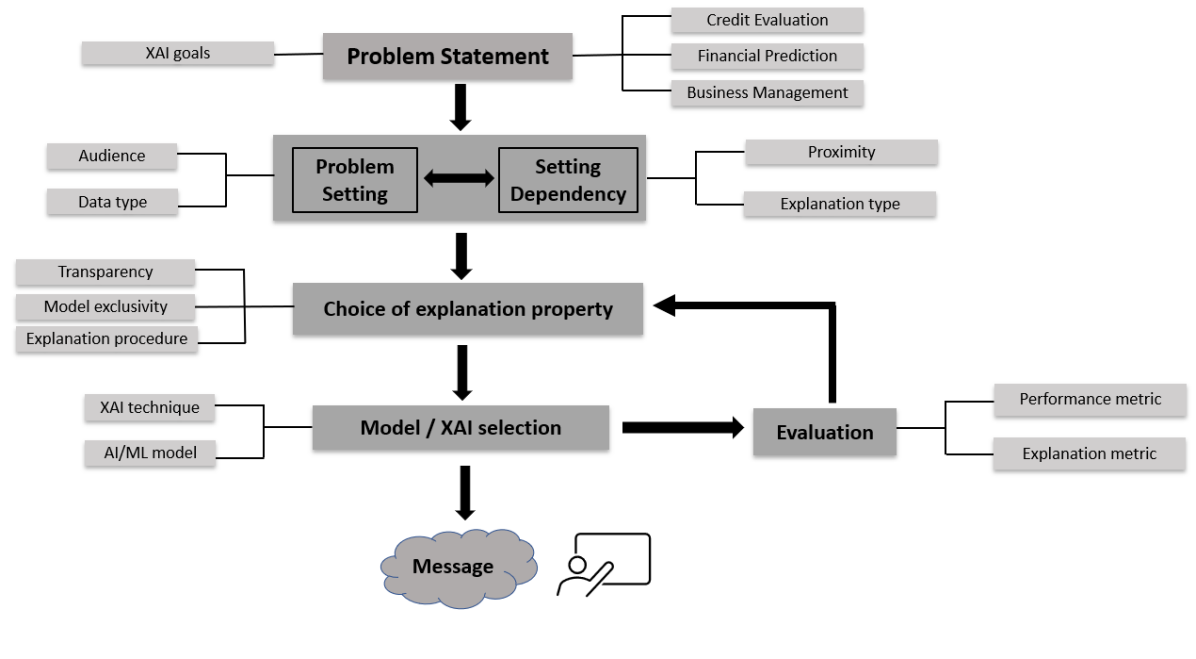

We frame the FinXAI process as a sequential flow of decision-making processes (see Fig 4), where we place importance on aligning the XAI technique with the target audience. The objective of this framework is to produce explanations that are both goal-oriented and audience-centric.

-

•

We review current FinXAI techniques, analyze their technical contributions to ethical goals, and list down a number of key challenges faced in implementing XAI as well as important directions to be improved for the future.

The remainder of the review paper is organized as follows: Section 2 describes the definitions, reasons, and brief overview of FinXAI. Subsequently, we explain the methodology of FinXAI, starting from numerical in Section 3, textual in Section 4, hybrid analysis in Section 5 and ending with transparent models in Section 6. In Section 7, we analyze how the reviewed FinXAI methods contribute to ethical goals. Section 8 discusses key challenges of adopting explainable models and future directions for research. Finally, Section 9 offers concluding remarks.

2. FinXAI: Definition, Reason, Approach

This section details the definition, purpose, and approaches that have been taken in improving the transparency of AI models. A collection of existing literature reviews are analyzed and collated to give the reader a better understanding of commonly used terminologies in the XAI field, as well as the interlink between AI, linguistics, and social sciences which is essential to provide a solid understanding of the subject.

2.1. Definition of FinXAI

FinXAI or explainable AI methods in finance is inherently linked to the broader concept of AI transparency. As mentioned in section 1, this term encompasses under a single framework three key steps: AI awareness, AI model explainability, and AI outcome explainability. In this review, we focus on the latter two aspects, model and outcome explainability. Model explainability means that the inner workings of a given AI solution are interpretable, and therefore the results may be interpreted by humans. This is typically the case for models with reduced complexity (i.e., white-box models), such as linear and logistic regression, and decision trees.

Outcome explainability means that the inner workings of a given AI solution are not fully interpretable, and therefore the results may not be fully understandable by humans, unless some interpretability tools are applied to explain the AI outcomes. This is the case for complex models (i.e., black-box models), such as deep neural networks. In these cases, it is common to apply model agnostic post-hoc (and other) interpretability tools to understand the results the AI provided in human terms.

Correspondingly, XAI models may be cast into two broad categories: intrinsically explainable due to their highly interpretable nature (e.g., linear and logistic regression), and extrinsically explainable, hence requiring an external tool to make them interpretable. In turn, these two categories of models lead to different classes of model transparency: simulatability, decomposability, and algorithmic transparency (Arrieta et al., 2020). Each of these three classes inherits the preceding class’ properties, that is, if a model is decomposable, it is also simulatable, and if a model is algorithmically transparent is also decomposable and simulatable. In simple terms, simulatability refers to the model’s ability to allow a human observer to simulate a thought process over the inner workings of the model. Decomposability entails that interpretability is available at every segment of the model, including inputs, outputs as well as model inner workings and parameters. Algorithmic transparency largely deals with the human user being able to understand how the model reacts with varying inputs and more importantly the ability to reason about errors the model produces.

A transparent model is an interpretable model which exhibits the ability to provide human-understandable explanations. Areas of transparency not only lie within the region of the model but also the data and design process of the end-product (van den Berg and Kuiper, 2020). The EU High-Level Expert Group on AI (HLEG, 2019) states that the data the model interacted with should be traceable by human users at any given time. In addition, the design process of the system must be clear and explainable in a manner comprehensible to related stakeholders. The list of information types, regarded as explainable can even be extended to include principles and guidelines in the development of the AI system, as well as personnel involved in the implementation and development process (Kuiper et al., 2022).

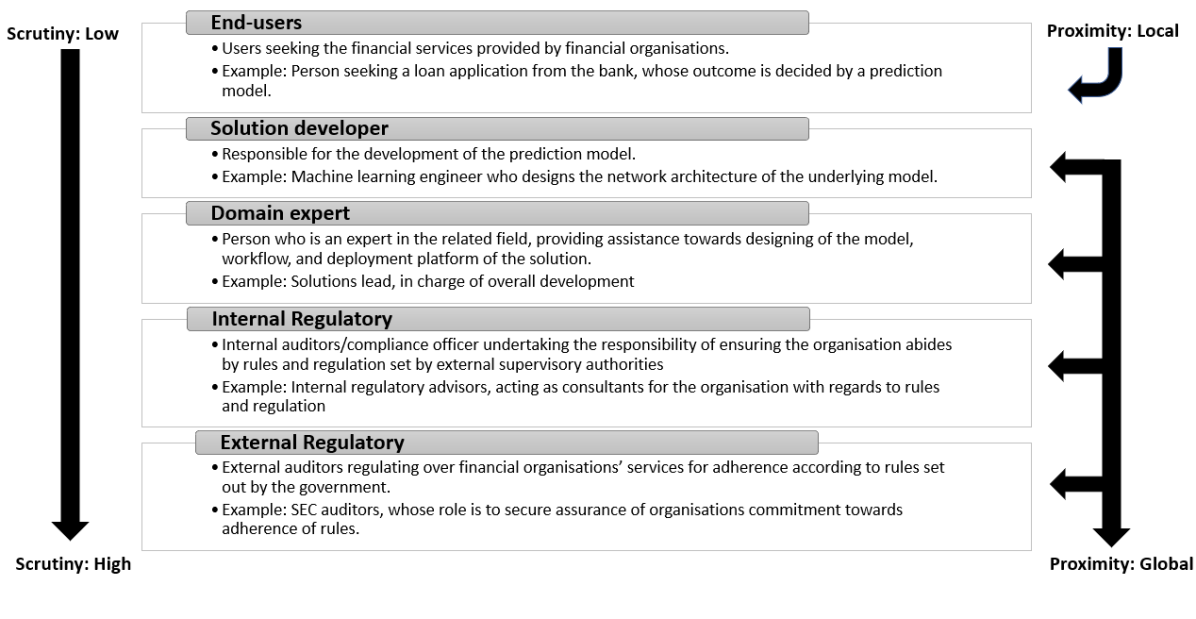

A key rationale for explainability is to gain the trust of affected stakeholders. Examples of such stakeholders include regulators, board members, auditors, end-users and developers (Yeong Zee Kin, 2023). To this end, the format and degree of explanation vary among audiences. The key message is usually conveyed in reports customized to the suitability of the receiving audience. It is common knowledge that financial service providers are regularly audited by supervisory authorities to ensure adherence to regulations and to prevent potential fraud from taking place. The level of scrutiny expected of the authorities is much higher than what the service providers expect. A study conducted by (Kuiper et al., 2022) involves a preliminary investigation to identify the types of information that are deemed necessary, in the perspective of banks and supervisory authorities. The result was that supervisory authorities identify all forms of information types as relevant while banks only consider a subset of them. As such, there exists a gap between each organization’s understanding of necessity, more often than not leading to the delay in approving the deployment of financial services.

As mentioned, the constitution of a good explanation is largely subjective. The amount of required information usually increases in a hierarchical manner starting from the audience to the regulatory authorities, as depicted in Figure 1. Here, scrutiny refers to the amount of information regarded as essential. On the one hand, end-users typically require the least amount of explanations (cause of outcome, data security) since they are usually only interested in resolving their practical concerns. On the other hand, external regulators require explanations about the end-product from head-to-toe (overall guideline in design process, accountable and involved personnel, deployment process, training structure of organization), including the end-users requirements.

Proximity refers to the region of explanation provided by the XAI technique and can be classified under local (reasons about a particular outcome) and global (view of the underlying reasoning and mechanics of the AI model). End-users tend to be concerned with how the outcome affecting them is provided (local proximity). For example, a person whose credit card application was rejected would want to know the underlying reason behind it. In contrast, the solution providers and regulators tend to focus on the internal operations and design workflow of the product, for reasons related to performance enhancement, fairness in the model’s sense of judgment, and identification of biases in the prediction (global proximity).

2.2. Reasons for FinXAI

As mentioned in the previous section, various stakeholders lean towards different forms of explanation, naturally leading to different sets of goals the explanation can provide. A paramount reason for adopting explainable models is to ensure that financial solutions adhere to ethical standards set forth in the financial sector. The Monetary Authority of Singapore (MAS) stipulates that AI solutions should be developed in accordance with the Fairness, Ethics, Accountability and Transparency (FEAT) principles (of Singapore, 2021). EU’s General Data Protection Regulation (GDPR) (Goodman and Flaxman, 2017) in 2018 announced a law referred as “right to explanation”, dictating that individuals affected by automated decision-making solutions have a right to ask for an explanation of the outcome made for them.

The rising call for explainable models is mainly influenced by the rapid advancement of AI solutions and the increasing complexity surrounding them. More importantly, public cases of AI model displaying biases in their prediction magnifies the urge for explainable solutions. A famous example is Google’s image recognition software, that accidentally labels dark-skin humans as gorillas (VINCENT, 2018). Such biases can damage the company’s reputation, and lead to profit losses.

The financial sector has its own set of ethics that should be upheld along with the desirable principles of AI ethics. These set of financial ethics often overlap with AI principles. An experiment involving 8 financial experts to investigate the relationship between the aforementioned sets was carried out in (Rizinski et al., 2022). The results show that financial ethics (integrity, objectivity, competence, fairness, confidentiality, professionalism, diligence) has significant similarities with AI ethics (growth and sustainable development, human-centered values and fairness, transparency and explainability, safety and accountability). The strength of the links between each element was assessed, with integrity and fairness having the strongest relationship with AI ethics. Indeed, this is understandable given that AI solutions should naturally embody these qualities, regardless of the industry taken into account.

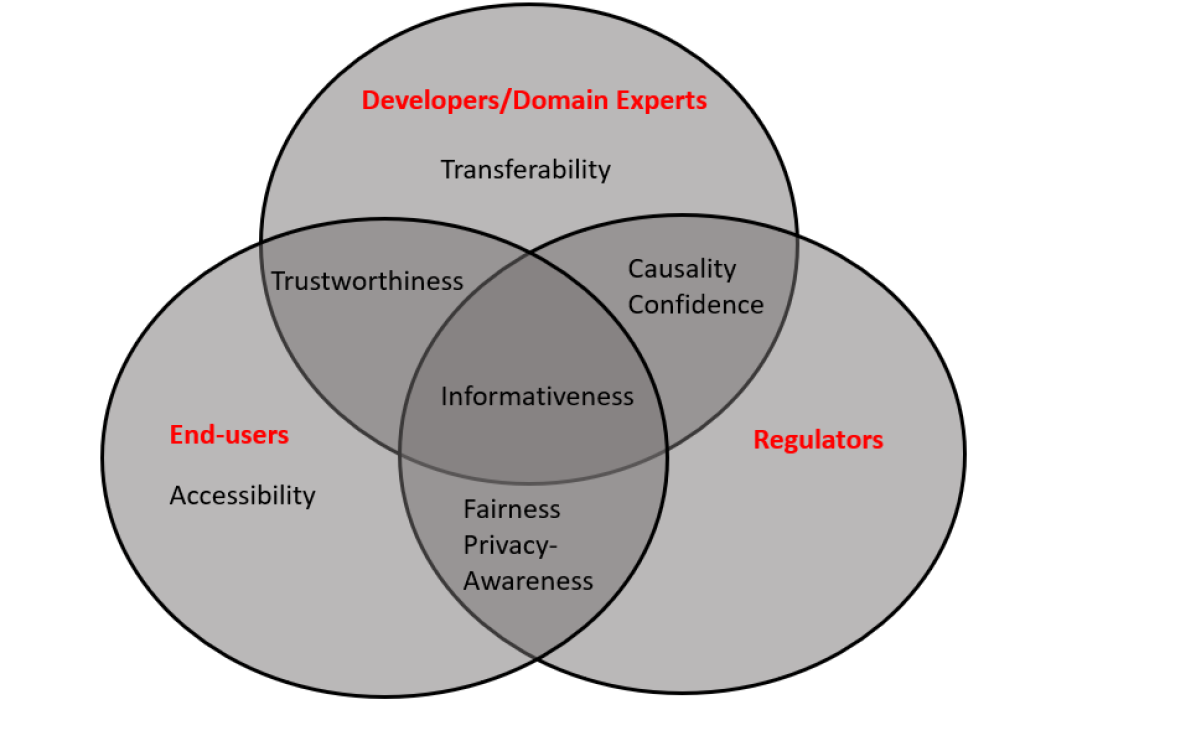

As mentioned, the ethical goals set forth by XAI solutions differ among audiences, similar to the explanation types desired. Each audience is likely to be more affected by one than the other (Arrieta et al., 2020; Mohseni et al., 2021b). Figure 2 list the ethical goals supported towards each set of audiences, and shows that there are some overlapping ethical goals across audiences. Referring to (Arrieta et al., 2020), we provide a brief explanation of each ethical goal reported in Figure 2, taking a financial perspective.

-

•

Trustworthiness: Defined as instilling trust into users affected by the decisions of the AI model. Trustworthiness can be achieved when there is a high level of confidence in the model to constantly behave in the intended manner (Ribeiro et al., 2016). Trust is also sustained if the services provided are transparent and enables affected user to maintain their faith in the service providers. However, trust is a highly subjective quality and hence difficult to quantify. Judging if an explanation instills trust is mostly subjected to the affected users’ opinions.

-

•

Fairness: Refers to delivering AI solutions and explanations to every user and stakeholder equally, removing possible biases. Indeed, bias mitigation is a key constituent of fairness. The transparency of the AI model allows for a fair and socially ethical analysis, where any form of biases existing in the product chain are eliminated. In the financial markets, users tend to use the services provided by a firm if they are assured of fair and unbiased treatment.

-

•

Informativeness: One important objective of AI models is to provide assistance to human counterparts in making decisions. Therefore, it is vital that the problem statement is made clear at all times. By providing explanations, the model benefits both from a social perspective as well as a performance standpoint, since knowing what is being done opens up opportunities for further refinement. Most of the papers in the literature dealing with this aspect aim at identifying relevant features which equates to highlighting parts of the input data the model is paying attention to. This can assist in debugging and allows pruning of unnecessary features which may cause overfitting.

-

•

Accessibility: The main personnel interacting with algorithms are usually restricted to AI developers or domain experts, providing accessibility could allow for non-experts to get involved. This can be seen as an important stepping stone for making AI prevalent and well-accepted by the general society. Likewise, complicated algorithms deter financial companies from adopting such solutions, since extensive training is required while having to fear potential repercussions in the case of any unintended wrongdoings. If a model is able to relate its mechanisms in easily understandable terms, it can ease the fear of users and encourage more organizations to adopt such practices.

-

•

Privacy Awareness: Not knowing the full limits of accessibility in the data can result in a breach of privacy. Likewise, such an issue triggers concerns within the overall design workflow. Accountable personnel in the designing process should ensure third parties are only allowed restricted access to the end-users data and prevent any misuse which can disrupt data integrity. Privacy awareness is especially important in the financial sector due to the amount and sensitivity of the information being captured.

-

•

Confidence: The AI model should provide not only an outcome but also the confidence it has in the decision-making process, allowing domain experts to identify uncertainty in both model’s results as well as the region of data captured. Stability in the prediction can be used to access a model’s confidence while explanations provided by the model should only be trusted if it produces results that are consistent across different data inputs.

-

•

Causality: It is usually in the interest of developers or experts to understand the causality between data features. However, proving it is a difficult task that requires extensive experimenting. Correlation can be involved in assessing causality, though it is frequently not representative of causality. Since AI models only discover correlations among the data they learn from, domain experts are usually required to perform a deeper analysis of causal relationships.

-

•

Transferability: Allowing for the distillation of knowledge learned from AI models is an extensive area of research, a notable benefit is that it allows for the reusability of different models and averts endless hours of re-training. However, the complexity of the algorithms limits experts from deploying trained models in different domains. For example, a model trained to forecast future stock prices can likely be used to predict other financial variables such as bond price, market volatility, or creditworthiness, if the model behavior in these circumstances is known. Delivering an intuition of the inner workings can ease the burden of experts to facilitate adapting the knowledge learned, reducing the effort required for fine-tuning. Transferability is arguably one of the essential properties for the improvement of future AI models.

2.3. Approach of XAI

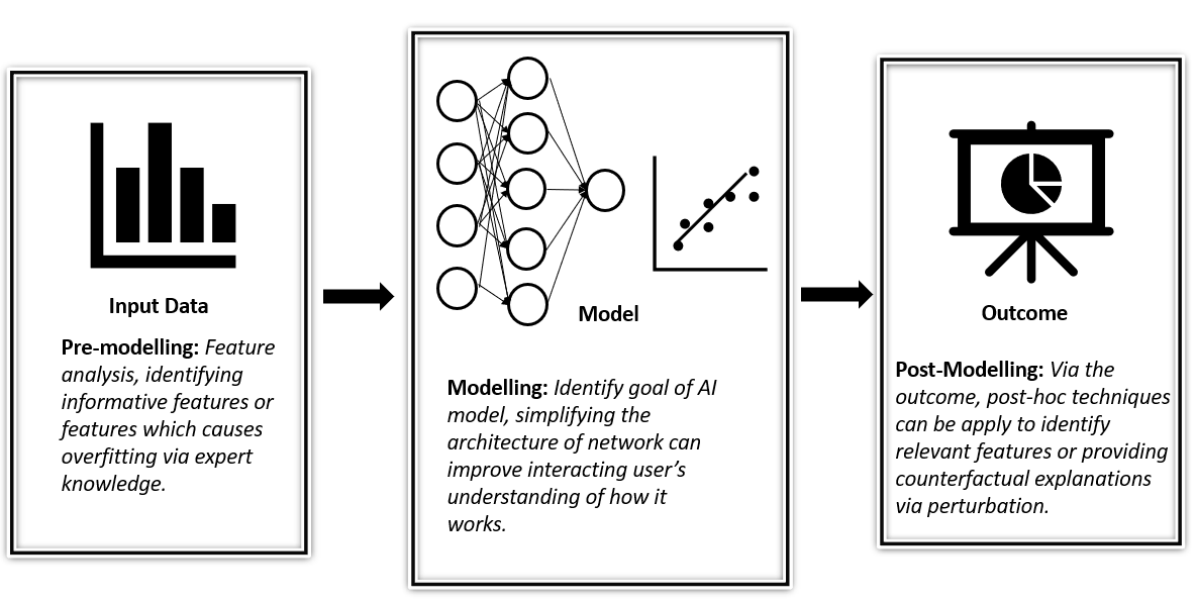

The review provided in this paper aims to give the readers an overall view of the XAI methodologies developed thus far in the financial industry. We note that explainability can be injected across different stages of the development cycle. These stages include: pre-modeling, modeling, and post-modeling (Mellon, 2021). Pre-modeling stage refers to the process chain before the designing stage of the AI model, this can include preliminary procedures which focus on identifying salient features by accessing readily available domain knowledge (Islam et al., 2019). The modeling phase includes any adjustment to the model’s architecture or optimization objective. As a start, simpler transparent models should be preferred over complex black-box models if the problem at hand is not too complicated. Most of the papers in the review focus on the post-modeling stage, mainly due to the flexibility and ease of designing explainability techniques. Since the outcome is provided, it provides developers with more information to design an appropriate explanation method towards the form of data interacted (See Figure 3). Most XAI techniques tend to focus on one stage of the modeling process, though it is possible to do so in two or more.

| Paper | Trans -parency | Proximity | Explanation Procedure | Audience | Data Analysis | Expla -nation Type | Expl Eval | |||||||||||

| Intrinsic | Post-hoc | Local | Global | Textual | Visual | By example | Simplification | Feature relevance | End-user | Developer | Domain expert | Regulatory | Numerical | Text | Factual | Counterfactual | ||

| (Dikmen and Burns, 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Gramespacher and Posth, 2021; Chen and Ye, 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Misheva et al., 2021; Serengil et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Bussmann et al., 2021, 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Rizinski et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Müller et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Zhang et al., 2022d) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||

| (Biecek et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||

| (Crosato et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Davis et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||

| (Sudjianto and Zhang, 2021; Dumitrescu et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Bueff et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Fritz-Morgenthal et al., 2022; Tran et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Srinivasan et al., 2019) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Grath et al., 2018) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Adams and Hagras, 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Demajo et al., 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||

| (Luo et al., 2018) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Zhang et al., 2022a) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

The focused regions of finance can be broadly categorized under three sections (Bahrammirzaee, 2010): credit evaluation (peer-to-peer lending, credit assessment, credit risk management, credit scoring, accounting anomalies), financial prediction (Asset allocation, stock index prediction, market condition forecasting, volatility forecasting, algorithmic trading, financial growth rate, economic crisis forecast, bankruptcy prediction, fraud detection, mortgage default) and financial analytics (financial text classification, spending behavior, financial corporate social responsibility (CSR), customer satisfaction). Following the task classification, we further differentiate the studies based on the underlying characteristics of the XAI technique as shown in Table LABEL:tab:_XAI_CE, LABEL:tab:_XAI_FP, LABEL:tab:_XAI_FM. Specifically, we seek to answer questions such as “What form of explanation is provided?” (explanation procedure), “Who is the explanation intended for?” (audience), “What kind of explanation is provided?” (proximity, explanation type).

| Paper | Trans -parency | Proximity | Explanation Procedure | Audience | Data Analysis | Expla -nation Type | Expl Eval | |||||||||||

| Intrinsic | Post-hoc | Local | Global | Textual | Visual | By example | Simplification | Feature relevance | End-user | Developer | Domain expert | Regulatory | Numerical | Text | Factual | Counterfactual | ||

| (Zhang et al., 2020b) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Yang et al., 2018) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Deng et al., 2019) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Ghosh and Sanyal, 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||

| (Collaris et al., 2018) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||

| (Benhamou et al., 2021; Fior et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Bracke et al., 2019) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||

| (Nazemi et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Carta et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Cong et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Yasodhara et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Park and Yang, 2022; Islam et al., 2019; Weng et al., 2022; Wand et al., 2022; Vivek et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Babaei et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Lin et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Gite et al., 2021; Bandi et al., 2021) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Yan et al., 2019) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Carta et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Kumar et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Cho and Shin, 2023) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Shi et al., 2021; Kumar et al., 2017; Chen et al., 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Achituve et al., 2019) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Farzad, 2019) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||

| (Ong et al., 2023) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Yuan and Zhang, 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| Paper | Trans -parency | Proximity | Explanation Procedure | Audience | Data Analysis | Explanation Type | Expl Eval | |||||||||||

| Intrinsic | Post-hoc | Local | Global | Textual | Visual | By example | Simplification | Feature relevance | End-user | Developer | Domain expert | Regulatory | Numerical | Text | Factual | Counterfactual | ||

| (Rallis et al., 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Zhang et al., 2022c) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||

| (Maree et al., 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Maree and Omlin, 2022a) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Maree and Omlin, 2022b) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Lachuer and Jabeur, 2022) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Gramegna and Giudici, 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||

| (Liu et al., 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Yang et al., 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ||||||||||||

| (Ito et al., 2020) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||||

| (Zhang et al., 2020a) | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | ✓ | |||||||||

-

•

Transparency: As mentioned in Section 2.3, interpretability of the model is either derived via interpreting the internal mechanisms of the AI model or through external techniques aimed at delivering some form of visualization or intuition of how the model works. Most of the reviewed papers focus on post-hoc explainability techniques, which we believe are preferred for a number of reasons. Intrinsic models usually under-perform complex networks and as such, producing explanations for an inaccurate prediction is pointless. We additionally note that the method of conveying explanations for intrinsic models is by definition model-specific. This means the same method cannot be reused for a different model. While post-hoc techniques can be agnostic or specific towards any single model.

-

•

Proximity: The explanations provided by XAI tools can seek to explain either the derivation of an outcome, known as local explanation, or how the model outputs on a global scale, referred to as global explanation. Global explanations tend to provide information on how the model makes decisions globally based on the learned weights, data features, and structure of the network. Producing an acceptable global explanation tends to be difficult in most cases (Molnar, 2020) as opposed to just a region of the input data. On the other hand, local explanations focus on a specific region of the dataset and seek to assist the receiver in understanding how a particular prediction is made. Local explanation is more accurate for unique cases where the dependency on input features is rarely captured by the AI model, which can cause global explanations to ignore such dependency. End-users tend to prefer local explanations as their concern lies with the explanation surrounding their outcome. Regulators and financial experts, on the other hand, prefer global explanations in order to have a complete understanding of the model.

-

•

Explanation Procedure: According to (Arrieta et al., 2020), the various forms of post-hoc XAI techniques can be divided into several sections: text explanation (TE), visual explanation (VE), explanation by example (EE), explanation by simplification (ES) and feature relevance (FR). TE provides an explanation via text generation. Natural language tends to be easily understood by non-experts and is a common source of information in human society. VE enables visual understanding of the model’s behavior, which may be preferable for image features (Selvaraju et al., 2017), such methods comprise graphical plots for both local and global explainability. EE captures a smaller subset of examples which represents the correlations modeled by the black-box model at a high level. ES techniques build a simpler surrogate model to approximate the underlying black-box model with high fidelity yet being interpretable. FR techniques aim to identify features deemed relevant for the model’s prediction, by computing a relevance score for each feature. FR can account for explainability at both local and global levels and constitutes the largest share among the reviewed papers in our literature.

-

•

Audience: Since the quality of explanations is subjective, it is very difficult to derive a one-fit-all explanation and hence, explanations should be customized towards one’s needs. The examples of audiences are referenced from Fig 1, while we further merge internal and external regulators together. We highlight that aligning the objective of the explanation to the audience receiving it is important (Tomsett et al., 2018). Determining if an explanation is considered meaningful, is dependent on the target goals respective of each audience. Financial regulators, for example, would not be very concerned with understanding what sort of AI model or ML technique is used, but rather on the aspect of data privacy, model biases, or unfair treatment between affected end-users. It is uncommon for a single explanation to be deemed acceptable to audiences holding different positions in a financial company. An example is that the explanation produced for the developer tends to require additional customization before submitting to the immediate superior and the same applies to the proceeding higher-ups and external end-users.

-

•

Data Type: The most commonly used forms of input data among the reviewed papers consists of text, images, and numerical values. In terms of frequency among the forms of available data, numerical features are the most common source of information used in the financial industry. Images represent the least utilized source, as they tend to be storage intensive and contain a large amount of redundant information or are not applicable for most use cases. We only found a single work using image features. (Chen et al., 2020) performs classification of eight different candlestick patterns and the explanation is delivered through monitoring changes in prediction after applying adversarial attacks. Surprisingly, textual information is not used as frequently as expected, albeit being a valuable source of information for deriving market sentiment or understanding consumers’ emotions towards certain aspects of the business product. It is also possible to unify multiple sources of information, otherwise known as multi-model data. A boost in performance can be achieved, for instance by combining the patterns learned from time-series features and sentiment from textual features.

-

•

Explanation Type: A single explanation can be conveyed in various forms, including factual, contrastive, and counterfactual explanations (Miller, 2019). Factual delivers straightforward explanations that seek to answer the question “Why does X lead to Y” as opposed to contrastive “Why does X lead to Y instead of Z”. Counterfactual instead reasons how the consequent can be changed with respect to the antecedent, answering the question “how to achieve Z by changing X”. Humans tend to prefer contrastive rather than factual explanations since the latter can have multiple answers and referring to (Miller, 2019), explanations are selective. As humans tend to ignore a large portion of the explanations except for the important ones due to cognitive bias. For example, if Person A’s loan application was rejected, there could be numerous reasons for this, such as “Person A’s income was too low for the past 6 months”, “Person A’s only have 1 existing credit card”, “Person A has had a credit default 3 months ago” and so on. Whereas a contrastive explanation can instead involve comparing against another applicant whose outcome contrasts the target applicant’s and an explanation can be made, highlighting the most significant factor. As argued by (Lipton, 1990), contrastive explanations are easier to deliver as one does not have to investigate the entire region of causes but rather a subset of it. Counterfactual explanations then seek to provide solutions for the contrastive explanation, commonly done by identifying the smallest changes to the input features, such that the outcome can be altered towards the alternative.

-

•

Explanation Evaluation: Despite the extensive studies carried out to investigate what defines a good explanation, it is difficult to qualitatively compare among interpretations. The quality of an explanation is mostly subjective as a single explanation can be perceived with varying opinions among audiences. Nonetheless, there exist a number of studies that provides a quantitative approach to evaluating explanations. These measurements can be derived from human experts (Yang et al., 2020), referencing financial ethical goals (Adams and Hagras, 2020) or through statistical methods (Müller et al., 2022). (Islam et al., 2019) conducted a comparison between feature importance techniques in time series data and proposed a multivariate dataset that deals with the inability of techniques that identify salient time-series features. A vast majority of the reviewed papers focused only on evaluating the performance of the prediction model and consider it as a proxy for the quality of the explanation. We argue that such evaluation does not fully represent the quality of the explanation and even if so, it may not be suitable for every form of explanation procedure.

Selection Procedure: We design a framework shown in Figure 4, framing the designing of the XAI solution as a sequential decision-making process. The selection categories can be referenced from Tables LABEL:tab:_XAI_CE, LABEL:tab:_XAI_FP, LABEL:tab:_XAI_FM. The sequential structure of the framework ensures the explanation provided is tailored to the audience’s needs while achieving the goal set out with respect to the target audience. We note that certain properties of the XAI technique have inner dependencies with each other, such as the relationship between explanation proximity and target audience. The quality of the explanation is evaluated and serves as feedback for any necessary adjustment, resulting in an audience-centric explanation.

3. XAI with numerical features

Numerical features are a common source of information across all aspects of data-driven methodologies. Financial tasks such as credit scoring of individuals/firms and financial market forecasts commonly use a collection of historical numerical features, such as stock price, trade volume, and volatility, and apply various forms of data-driven models to make predictions. These data-driven models may include supervised learning approaches, e.g., classification and regression tasks, and unsupervised learning approaches, e.g., clustering tasks. The use of numerical features within the context of finance is well established, hence it is not surprising that the majority of reviewed studies focus on this area. In the following, we outline the main approaches used for explainability in this context, namely visual explanation, explanation by simplification, feature relevance, and explanation by example, and conclude with a brief summary.

3.1. Visual Explanation

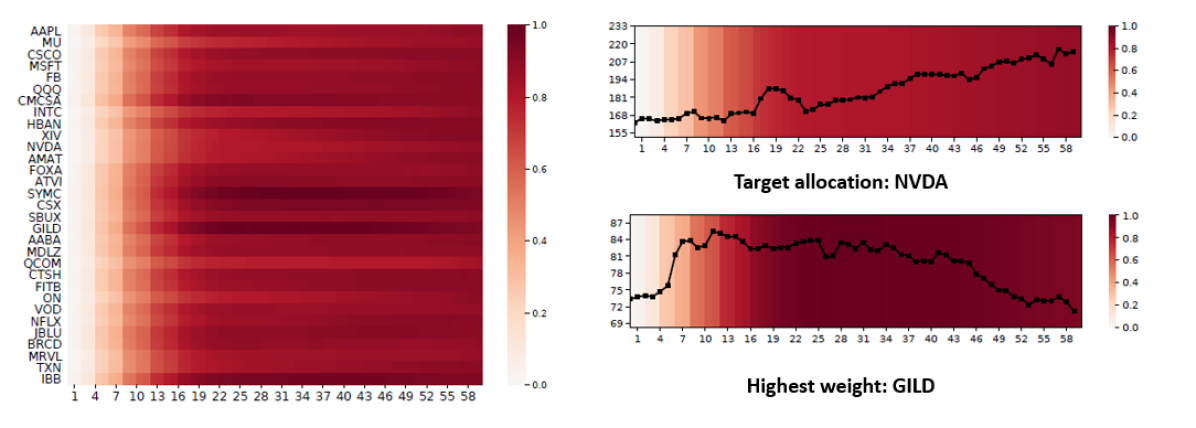

Visual explanatory (VE) techniques generate explanations of the underlying model in the form of visuals. VE techniques can be both model-specific and model-agnostic. The model-specific techniques reviewed are mainly constructed to interpret image-based networks such as convolutional neural networks (CNN). (Kumar et al., 2017) proposes to perform a deconvolution on the last layer preceding the output to extract a visual attentive map. The approach named CLass Enhanced Attentive Response (CLEAR) generates a graphical plot denoting the timeframe to which the stock-picking agent pays the most attention, along with a separate plot corresponding to the sentiment class of the stock. (Chen et al., 2020) implements a CNN network to identify 8 common candlestick patterns which are widely used for technical analysis in stock market trading. The authors then perform an adversarial attack on regions of the feature space, to demonstrate that the model is focusing on regions similar to how a human would process the candlesticks. (Shi et al., 2021) employs a reinforcement learning (RL) agent to optimize a portfolio of equities while using a temporal CNN as a feature extractor. The dynamic asset allocation is interpreted with Gradient-weighted Class Activation Mapping (Grad-CAM) (Selvaraju et al., 2017), improving over simple deconvolutions by producing class-discriminative explanations, and is applicable to any deep neural networks. The proposed technique outputs a localization map using gradients corresponding to the target label. The right plot in Figure 5 depicts a global map highlighting each asset’s importance across the trading period. Interestingly in the left plot, the agent focuses on the worst-performing stock, GLID the most, rather than the high-performing stocks. Here, the agent predicts the stock decline and reduces the allocation proportion, and indirectly increases the weights of high-performing stocks which in this case is the target stock, NVDA. (Achituve et al., 2019) proposes to use an attention mechanism (Vaswani et al., 2017) to compute similarity scores of possibly fraudulent transactions on both feature and temporal levels and in return, allows for visualization at the top contributing features accounting for the model’s prediction.

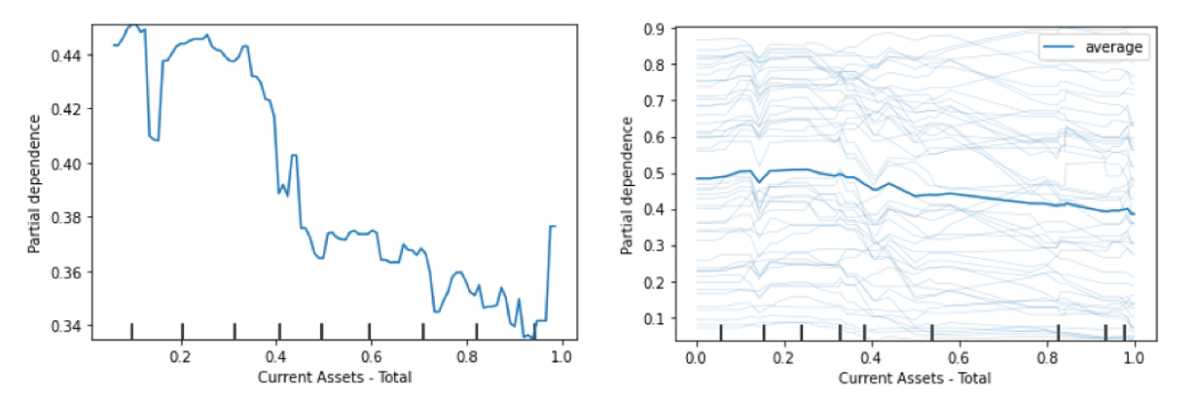

Model-agnostic VE techniques can be integrated with any form of model architecture and bear a similar resemblance with feature relevance techniques. Both investigate the effects on the model’s output by adjusting the input features. (Zhang et al., 2022d; Biecek et al., 2021; Zhang et al., 2022c; Farzad, 2019) employ Partial Dependence Plots (PDP) to visualize the marginal effects of features relating to corporate distress, credit scoring, and detecting mortgage loans defaults. The generated plots can enable a way of inferring if the underlying input-output relationship is linear or complex. However, PDP has often been criticized for its assumption of independence between features, evaluating unrealistic inputs, and also conceals any heterogeneous effects of the input features. Accumulated Local Effects (ALE) (Apley and Zhu, 2016) address the concerns of feature correlation by considering the conditional distribution rather than the marginal one. In particular, it accumulates differences between intervals within the feature set to account for individual feature effects. (Crosato et al., 2021) employs ALE on top of a tree ensemble model, XGBoost (Chen and Guestrin, 2016), as well as with global Shapley values (Shapley et al., 1953) for better scrutability. This work deduces that the increase in profit margin and solvency ratio leads to lower debt default rates of small enterprises. (Zhang et al., 2022c) evaluates across an arsenal of XAI techniques, encompassing the aforementioned, and also includes Individual Conditional Expectation (ICE) for financial auditing purposes. ICE differs subtly from PDP in that it considers instance-based effects rather than averaging across all instances, making it a local approach (see Figure 6). (Zhang et al., 2022a) generates counterfactual explanations on credit loan applications by coupling unsupervised VAE with a supervised probit regression. The combined model yields a discriminative latent state, corresponding to class labels of either delinquency or non-delinquency. The counterfactual is subsequently produced by a stepwise manipulation function towards the opposite class label. The authors evaluate the generated counterfactuals quantitatively using maximum mean discrepancy (MMD) (Zhang et al., 2022b), which measures the number of successfully flipped class labels as well as minimal feature changes.

3.2. Explanation by Simplification

The idea of Explanation by Simplification (ES) techniques is to introduce a surrogate model performing uncomplicated operations. The purpose is to allow the machine learning developer to formulate a mental model of the AI model’s behavior. The surrogate model has to be interpretable and more importantly capture the performance of the black-box model with high fidelity. The latter property should be given a higher priority since there is little use for interpreting a low-fidelity solution. ML techniques which apply linear operations and rule extraction are applicable as surrogate models in place of uninterpretable neural networks. These include decisions tree (DT) with limited depth, linear/logistic regression, K-Nearest Neighbors (KNN), and generalized linear models (GLM).

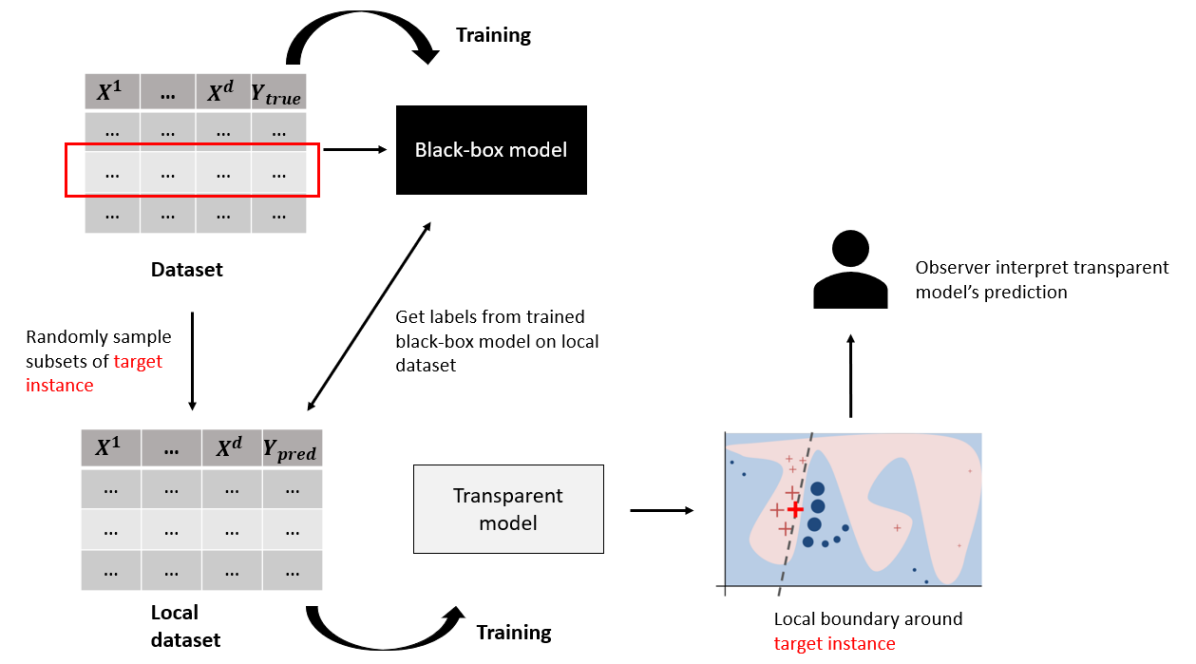

Local Interpretable Model-agnostic Explanations (LIME) (Ribeiro et al., 2016): is perhaps one of the most popular explanation techniques across various use cases, including finance. LIME is a model-agnostic method that is used to provide insight as to why a certain prediction was made and can be constituted as an outcome explanation technique. Since LIME is a local-based technique, it only has to approximate the data points within a defined neighborhood, achieving a much more realistic goal instead of capturing an interpretable representation of the entire dataset. On a high level, LIME can be implemented as follows (see Fig 7):

-

(1)

The target instance to be explained is denoted as . Uniformly sample random subsets of nonzero elements of to form local training points, , where for .

-

(2)

Derive labels for each point using the black-box model . The surrogate model, is then trained on the derived dataset, .

-

(3)

Choose a transparent surrogate model, and train it on the dataset, via Equation 1.

-

(4)

Interpret the outputs of the transparent model on the target instance, .

LIME minimizes the following loss function to optimize for both fidelity of the local model as well as minimal complexity.

| (1) |

represents the loss function of the surrogate model on the labels , weighted by proximity . represents the complexity or number of features in the surrogate model. is the set of all locally fitted models, where each explanation is produced by an individual local model. The authors additionally propose a sparse selection of features, named Submodular Pick LIME (SP-LIME), to present the observer with a global view, based on an allocated budget of maximal features to focus on. The method delivers diverse representation by omitting redundancy. (Misheva et al., 2021; Serengil et al., 2022) use LIME on top of tree ensembles to identify the contributions of individual features pushing towards predicting a specific borrower as defaulting or successfully paying off the loan. Such explanations can be useful in preventing social bias by discovering any socially discriminative features on which the model may be focused, thereby instilling trust in the model’s usability. (Yan et al., 2019) extends LIME towards financial regulators requiring commercial banks to adhere to a set of financial factors, where they propose a method named LIMER (R stands for Regtech). The authors of LIMER argue that high acceptance of financial solutions can be achieved if such factors are integrated into the explainability design of the AI model. (Collaris et al., 2018) implements model simplification by extracting logical rules from a random forest and selecting top most relevant rules. The decision rules are extracted from a local dataset, derived similarly to LIME without weighting the proximity of each drawn sample. (Maree and Omlin, 2022b) trains a recurrent neural network (RNN) to classify customer spending into five categories and an interpretable linear regression model was subsequently trained to predict the nodes formed by the RNN model. The authors then perform inverse regression which provides a mapping from output space to state space where the features responsible for categorizing customer spending can be identified.

3.3. Feature Relevance

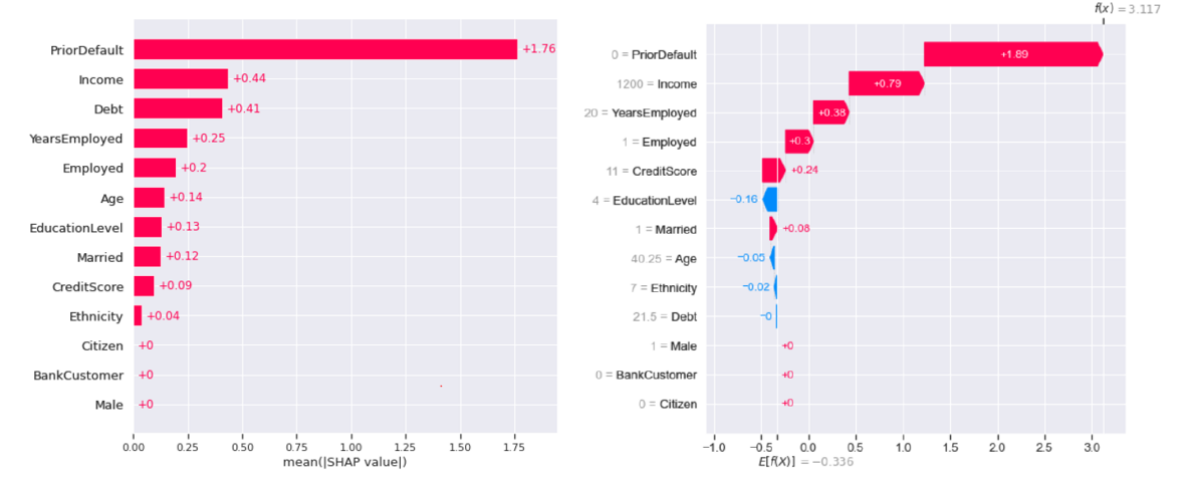

Feature relevance (FR) techniques account for the majority of the proposed explanation methodology we reviewed. FR techniques revolve around computing a relevance score for each feature, highlighting the respective contribution of the target feature either at a global or local scale. SHapley Additive exPlanations (SHAP) (Lundberg and Lee, 2017), motivated by the fair distribution among players from game theory (Shapley et al., 1953) is a highly popular FR technique, which seeks to estimate the fair value of each feature in contributing towards the outcome, . The fair value, otherwise known as shapley values are determined, based on estimating the difference between the black-box function over feature subset with and without the target feature, and respectively. The difference is then averaged across all possible coalitions within the feature set .

| (2) |

The final outcome is intuitively derived as an aggregate over all non-zero shapely values. SHAP’s popularity stems from three attractive properties: guaranteeing a complete approximation of the original model through additive feature attribution (see Equation 2), ensuring non-contributing features have no impact on model output and consistency of feature values tracking the outcome contribution. We notice a large subset of papers reviewed has utilized SHAP as an explanation approach, likely given its flexibility towards explaining the model at both local and global scales (see Figure 8). (Dikmen and Burns, 2022) incorporates SHAP with additional credit knowledge for the layperson to assess the logic of XGBoost’s decision in a peer-to-peer lending scenario. (Müller et al., 2022) introduces RESHAPE, designed for unsupervised deep learning networks, which provide explanations at the attribute level. Such explanations can assist auditors in understanding why an accounting statement is flagged as anomalous. The authors evaluated RESHAPE against other variants of SHAP, based on metrics measuring fidelity, stability, and robustness. Attributing to the recent frenzy in cryptocurrency which has led to a number of studies attempting to predict movements in the cryptocurrency market, (Fior et al., 2022) proposes an interactive dashboard providing multiple graphical tools using SHAP for financial experts. (Babaei et al., 2022) applies SHAP to explain predictions, generated by the popular mean-variance Markowitz model (Markowitz, 1952) which is an optimization model for establishing the optimal portfolio balancing between returns and risk. The generated explanation provides regulators a means of asserting compliance of algorithmic automized traders, otherwise known as robot-advisors, with established rules and regulations. (Demajo et al., 2020) incorporates Global Interpretation via Recursive Partitioning (GIRP) with SHAP as a global interpretability technique. GIRP uses the importance values generated by SHAP to further extract meaning insights from tree models, and the method is compared against a boolean rule technique in a credit scoring use case. (Bussmann et al., 2021) constructs a tree-like visual explanation with TreeSHAP (Lundberg et al., 2018), specifically designed for ensemble trees with an improvement in computational efficiency. The produced structure allows users to visualize clusters of similar outcomes describing company default risk. (Yasodhara et al., 2021) compares TreeSHAP against impurity metrics using information gain, on ensemble tree models for investment quality prediction. (Gramegna and Giudici, 2020) identifies relevant features leading to consumers’ decision on purchasing insurance and further clusters them into least to most likely groups with Shapley values. (Bussmann et al., 2020) similarly implements SHAP to explain XGBoost’s classification of credit risk, while comparing it against an interpretable logistic regression model. Other studies include discovering the relationship between corporate social responsibility and financial performance (Lachuer and Jabeur, 2022), customer satisfaction (Rallis et al., 2022), GDP growth rates (Park and Yang, 2022), stock trading (Benhamou et al., 2021; Kumar et al., 2022), financial distress (Tran et al., 2022), market volatility forecast (Weng et al., 2022) and credit evaluation (Rizinski et al., 2022; Bueff et al., 2022; Fritz-Morgenthal et al., 2022).

(Wand et al., 2022) performs K-means clustering on historical S&P 500 stock information to identify dominant sector correlations which describe the state of the market. This work applies Layer-wise Relevance Propagation (LRP) (Bach et al., 2015), after transforming the clustering classifier into a neural network since LRP is designed to work specifically with neural network architectures. (Carta et al., 2022) prunes unimportant technical indicators using different configurations of a permutation importance technique, before implementing decision tree techniques for stock market forecasting. The proposed technique was compared with LIME and demonstrated better reliability. (Bracke et al., 2019) introduces a set of feature relevance techniques, Quantitative Input Influence (QII) (Datta et al., 2016) to compute interaction effects between influential features and additionally for each multi-class label. The authors additionally evaluated the ability of the XAI technique with five questions relating to each individual audience class. All of the XAI methods shown thus far are implemented in the post-modeling stage, while (Islam et al., 2019) is an example pertaining to pre-modeling where the identification of relevant features takes place before constructing the black-box model. This work explores the set of features relating to mortgage bankruptcy and performs feature mapping against a set of widely-used credit concepts. The utility of such an approach is confirmed through empirical evaluations.

As pointed out before, contrastive explanations are usually preferred. End-users subjected to an unfavorable AI model’s decision would prefer a solution to the problem rather than a fact-based explanation which may present multiple possible reasons, giving little use to the explanation receiver. An explanation providing changes to be made such that the outcome can be reversed towards the favorable is referred to as a counterfactual explanation. Counterfactuals are derived by computing small changes to the input features continuously until the outcome is altered to the target class. (Cho and Shin, 2023) first identifies significant features, attributing to bankruptcy through SHAP, and subsequently generates an optimal set of counterfactuals using Genetic Algorithm (GA). The loss optimized by GA composes of objectives describing desirable properties of a good counterfactual outcome, including minimizing the size of altered features and maximizing the feasibility of the outcome. (Grath et al., 2018) additionally provides positive counterfactual explanations, describing the required changes to the current inputs that would instead reverse the loan approval to rejection. Such explanations can provide some form of safety margin for the user to be mindful of. (Vivek et al., 2022) used various technique from DiCE (De Bruin et al., 2009) to generate counterfactuals under five different experimental conditions. The experiment aims to identify and study the effects of the causal variables in the fraud detection of ATM transactions.

3.4. Explanation by Example

Apart from techniques that identify feature relevance on varying scales or approximate with a surrogate model, another form of explanation exists by selecting representative samples to illustrate the model’s behavior. Such techniques can be classified as Explanation by Example (EE). One such technique includes prototype-based explanations. Prototypes can be regarded as representatives of the entire dataset, chosen based on similarity and importance in the overall decision-making of the model. (Demajo et al., 2020) implements protodash (Gurumoorthy et al., 2019), a gradient-based algorithm in a credit loan application to select top prototypes, of which the top two are selected, with being 6. The resulting outcome is a number of representative prototypes and each instance can be represented by either generated prototype in the clusters. In this case, the proportions of allocated instances were balanced between both prototypes. The number of prototypes is a hyperparameter to be fine-tuned. A higher value of is frequently used where the complexity of the problem is a concern, albeit raises the risk of overfitting, while a lower value is used in simpler scenarios but incurs the risk of underfitting. For example, in the credit loan dataset, the selection of two prototypes was considered too little by domain experts who instead prefer 3-4 as being sufficiently representative of the evaluated dataset. (Davis et al., 2022) similarly extracts representative instances using KNN and generates insights on out-of-sample instances by looking for similarities with the representative points. Additionally, the data points for computing the distance are instead replaced with Shapley values, taking into account the importance of input features. Representative samples are generally suitable if the user is interested in determining the types of patterns or behavior found in the dataset while being relatively fast and straightforward to implement.

3.5. Summary of numerical features

The above-mentioned approaches should be chosen according to the task at hand and the target audience. VE techniques, such as deconvolution and Grad-CAM, are less commonly used in the financial industry due to their limited applicability to networks other than CNNs. However, ALE, PDP, and ICE can be suitable approaches for financial analysts who might want to study the relationship between individual features and the model’s outcome. ES is a straightforward approach that delegates the interpretability problem to a less complex surrogate model, though it incurs the additional cost of ensuring the faithfulness of the surrogate model. FR techniques allow users to observe each feature’s contribution to the black-box prediction. Both global and local explanations serve different purposes for individual audiences. However, in situations where each feature equally contributes to the model outcome, such explanations might not be very helpful depending on the objective of the explanation. For example, a declined credit loan approval may have multiple features such as prior default, debt-to-income, and household capital contributing equivalently to the outcome. Such an explanation does not offer an obvious course of action for the applicant. EE techniques are particularly useful when the user wants a small set of representative samples to explain the model’s outcome. This can provide a fast and straightforward explanation, but it has limited usefulness.

4. XAI for Textual information

In this section, we review models operating with textual information. We note that the papers pertaining to this area represent the minority in the overall literature. When it comes to data preparation, textual data generally require additional pre-processing works such as stop word removal, stemming, lemmatizing, and tokenization. In terms of feature extraction, the semantics, and syntax structure around text is important and have to be learned to fully capture the information conveyed, unlike numerical features which are readily usable. Models suitable for training from textual data are also limited to a smaller subset of available techniques. Nevertheless, unstructured data such as text are in abundance. If properly processed, textual data can be used to derive informative signals such as market sentiment and emerging trends (Ma et al., 2023). Textual data are commonly classified under alternative information, which comes in a wide variety of sources including social media, online reviews, blog posts, and news headlines (Kolanovic and Krishnamachari, 2017), in contrast to non-alternative information which refers to data commonly utilized for financial analysis. Fortunately, a wide variety of explanation techniques exist which are compatible with textual information. Conveniently, textual information is applicable for XAI techniques delivering explanation via text generation, which can be preferable for the layperson as natural language provide an easier form of interpretation as compared to statistical graphs.

4.1. Text Explanation

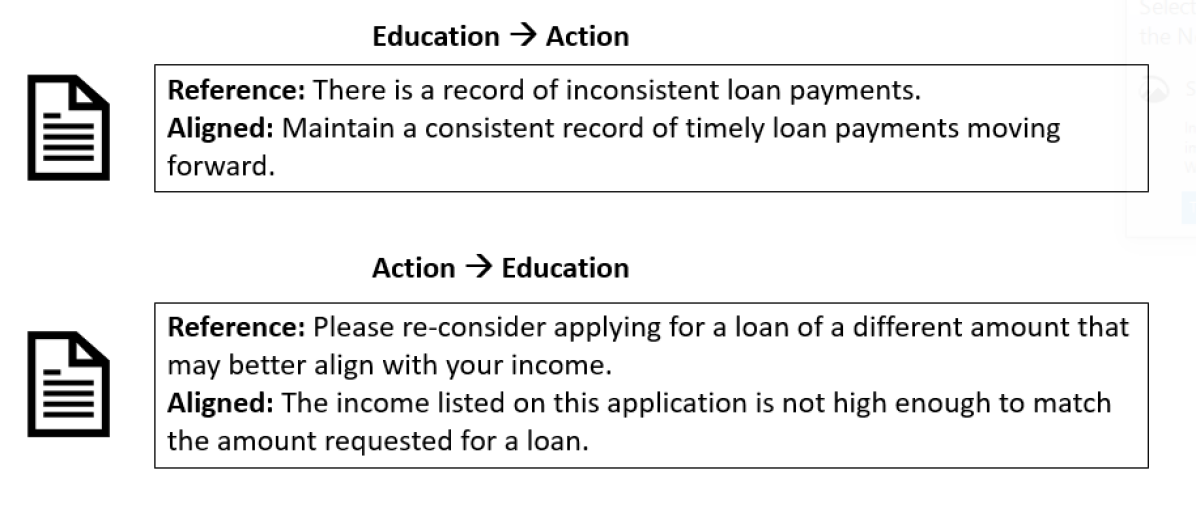

Text explanation techniques provide clarity in the form of generating informative textual statements to assist in the understanding of the model’s behavior. The generated text can either be re-generated text statements by using some form of generative model or replacing selected words in the original sentence. (Srinivasan et al., 2019) utilizes Generative Adversarial Networks (GAN) to produce text statements that seek to align with user-defined inputs. Specifically, the explanation can take two different objectives, either converting actionable text to educational text or vice versa. The actionable text briefs audiences on optimal actions to consider, based on real-world responses from human responses on multiple loan application scenarios while the latter seeks to educate the audience on reasons attributing to the response. The transfer of objectives from one to another is analogous to the implementation of style transfer on images, a popular application of GANs that translates the style of an instance to the target image while retaining the content. Figure 9 shows a snippet of an example, the proposed method can identify the semantics behind the statement and relay the relationship between consistency and time, while knowing if the current income is above or below the required threshold.

(Yang et al., 2020) generates plausible counterfactual text sentences with a transformer architecture, trained under contextual decomposition. The explanation technique, derived from Sampling and Contextual Decomposition (SCD) (Jin et al., 2019), performs different actions including inserting, removing, or replacing words that are representative of the context in the statement, based on the target objective. The high-level idea of counterfactual generation involves identifying the most relevant word and replacing it with an antonym from a reference dictionary and continues until the outcome is reversed. The proposed transformer outperforms even human experts in classifying financial articles on merger & acquisition event outcomes. (Yuan and Zhang, 2020) generates text explanations using a state-of-the-art natural language generation transformer decoder, GPT-2 (Radford et al., 2019), while fulfilling soft constraints of including keywords. The proposed technique, soft-constrained dynamic beam allocation (SC-DBA) extracts keywords corresponding to various levels of predicted market volatility using a separate network on harvested news titles. The quantitative measurement is evaluated based on the fluency and utility of the explanation produced.

4.2. Visual Explanation for Text

Besides interpreting through text, users can understand through the form of visuals, which makes the use of attention a particularly attractive option. Attention was first introduced when it was used to consider correlations between words in a sentence in a parallel fashion and is a primary component in the transformer architecture (Vaswani et al., 2017). Transformers are notably suitable for processing long sequences of text and through the use of attention. They are computationally efficient compared to RNN-based models. It so happens that, computing attention scores of each word serves as a natural form of interpretation, by allowing users to visualize how the network is capturing information from the input text (Han et al., 2022). Representative works in this area employ attention to highlight regions of text sentences that are deemed relevant for the output. (Yang et al., 2018) utilizes dual-level attention with Gated-Recurrent Units (GRU) (Chung et al., 2014), processing both inter-day and intra-day embedding of news titles relating to S&P 500 companies. The attention module assigns a relevance score to each news article and the authors additionally construct a knowledge graph conducting concept mapping between relevant entities as a visual explanation. Corresponding to dual-level attention, (Luo et al., 2018; Lin et al., 2021) propose a hierarchical attention model at both the word and sentence level and produced explanations in the form of a heatmap, highlighting relevant text. The proposed method, FISHQA was trained to detect loan arrears from financial text statements, similar to the compared baselines. The uniqueness of the proposed method lies in providing FISHQA with additional user queries. The model was able to highlight regions of the statement corresponding to the set of expert-defined concepts. This form of explanation allows users to verify if the model is focusing on the correct terms relating to the concept at hand (refer to Figure 10).

Along the lines of hierarchical attention, (Lin et al., 2021) introduces a quantitative measure to evaluate the precision and recall of captured against various lexicon dictionaries and expert annotated lists. The approach, analogous to the former study can be seen as an extrinsic process of ensuring the correctness of concept identification, by capturing words associated with financial risk. (Deng et al., 2019) implements knowledge graphs to provide a visual linkage between event entities extracted from stock news articles. The approach offers users a visual understanding between the feature’s relationship and the corresponding prediction. (Ito et al., 2020) introduces GINN, an interpretable neural network, the network is designed in a way that each layer represents different entities such as words and concepts at the node level. The approach identifies words attributing to the predicted sentiment labels, as well as the concepts it belongs to.

4.3. Summary of textual information

TE techniques aim to augment existing input text or generate new text based on given inputs. Such explanations are commonly preferred since natural language is easily understood by humans if the explanation is concise and accurate. However, textual explanations may fail to capture the nuanced relationships between input features and model decisions. This can be especially detrimental and counterproductive to domain experts whose goal is to discover further improvements based on the provided explanations. Textual explanations might also require additional processing work to ensure fluency, coherence, and unambiguity. VE techniques in these works leverage the utility of attention to provide a glimpse into how the model is representing the input text, and the use of hierarchical attention allows for a more refined analysis. However, since attention captures the relationship between each word or sentence, such explanations might be overwhelming if the set of explainable features is too large. Audiences who are not well-versed in heatmaps or attention scores may have difficulty understanding the provided visuals.

5. XAI for Hybrid information

The remaining studies implementing post-hoc explanation techniques utilize a combination of both textual and numerical/technical features. With respect to instance-level explanations, (Bandi et al., 2021) combines the sentimental analysis of text with technical analysis of historical stock prices to train a random forest stock forecasting model, explained through LIME. The resulting explanation computes a set of relevant feature values and news wording corresponding to the respective outcome. Similarly, (Gite et al., 2021) implements LIME with LSTM-CNN and accurately identifies attentive words in consonant with the target sentiment. (Liu et al., 2020) predicts the possibility of litigation on financial firms from examining 10-K financial reports and numerical indicators concerning the firm’s accounting knowledge. The author additionally carry out an ablation study on the utility of hybrid information as opposed to individual and validated the initial approach. Correspondingly, the explanation served to regulators is framed as the identification of text leading to the suspicion of insider trading, with the help of an attention mechanism. (Zhang et al., 2020a) adopted the practice of shapley values and further integrate external knowledge regarding truth factors, namely Truth Default Theory (TDT) (Levine, 2014) to detect information fraud. The explanation module incorporates both shapley values and TDT to generate a report highlighting numerical contributions of features as well as a text explanation. A union of explanation by simplification and feature relevance was proposed by (Cong et al., 2021; Ghosh and Sanyal, 2021). (Ghosh and Sanyal, 2021) implements both LIME and SHAP, offering a global and local explanation of market fear prediction in the Indian financial market. (Maree et al., 2020) uses SHAP and identifies textual information to be more important for classifying financial transactions and further performs clustering to identify top contributing keywords. (Cong et al., 2021) interprets an RL-trained agent’s behavior in algorithmic trading. The resulting explanation enables experts to focus on time-dependent variables alongside consideration of non-linearity effects, which are reduced to a small subset of initial variables. The learned policy is simplified via policy distillation, onto the space of linear regressions such that an interpretable Lasso regression model can be used as an interpretable approximation. Subsequently, -degree polynomial analysis is conducted to select salient features, with acting as an additional flexibility for the developer to decide. (Ong et al., 2023) utilizes aspect-based sentiment analysis to study the relationship between stock price movement and top relevant aspects detected in tweets. The polarity of each aspect is derived from a SenticNet-based graph convolutional network (GCN) (Liang et al., 2022). The proposed method can be seen as analogous to the feature relevance technique, aimed at deriving top contributing aspects with polarity values. The proposed work focuses on the relationship between financial variables instead of making financial predictions. Such information can allow for further analysis, leveraging the relationship between the price movement of individual stocks and individual sentiment of popular terms detected in tweets.

Hybrid information combines the utility of both numerical and textual information, which can lead to better performance and an increase in the number of compatible explanation techniques. For example, text generation techniques can be used to generate natural language explanations for non-technical audiences, facilitating ease of understanding, while feature relevance approaches can be utilized to identify top contributing factors in the feature domain for technical experts. Models working with both numerical and textual information can also benefit from a performance point of view if such information can be processed without the risk of overfitting. However, it may be difficult for models to seamlessly perform with hybrid information, as it ultimately depends on the task at hand and may require complex feature engineering. For instance, the utility of text information largely depends on the source and often requires a significant amount of preprocessing before the data can be useful. The combination of both text and numerical features may increase the complexity of the explanation and end up being counterproductive. Such issues limit the inclusion of textual information in use cases such as stock trading or market index predictions. Nonetheless, we note that leveraging hybrid information to provide explanations can be a promising approach if the aforementioned issues are addressed.

6. Explainability in Transparent models

The remaining studies look at instigating explainability from inherently transparent models. These models are typically restricted to ML models performing linear operations or rule extraction. The medium of explanation in transparent models is by nature model-specific, in the sense that the same mode of explaining how a model functions to an audience likely cannot be reused by a different model. The usability of transparent models in complicated tasks is largely restricted due to their poor predictive strength. Nevertheless, transparent models still remain an attractive option if sufficient performance can be guaranteed.

Linear/Logistic Regression: Linear regression model is among the earliest ML models to be used for quantitative analysis. The prediction outcome can be easily derived as a weighted aggregate of input features. As such, the outcome can naturally be interpreted by inferring from the coefficients, which serves as a quantitative measure of feature importance for the outcome. Attributing to the linearity assumption, the output can be derived as such:

| (3) |

One can easily interpret the outcome as “By increasing feature by one unit, the output increases by ”. On the other hand, the logistic regression model is interpreted in a slightly different manner, since the output is bounded between [0,1], a logistic function is used. Logistic regression looks at the probability ratio between both outputs: “Increasing one unit of is equivalent to increasing by ” (Molnar, 2020). (Dumitrescu et al., 2022) addresses the trade-off between accuracy and interpretability by incorporating decision trees with logistic regression acting as the main operational backbone. The technique is coined as Penalised Logistic Tree Regression (PLTR). PLTR extracts binary variables from short-depth DTs, all the while establishing sparsity through a penalized lasso operation. The proposed model is able to account for non-linear effects in a credit-scoring dataset while retaining interpretability by observing the top-selected rules.

Decision Trees: Decision trees are one of the most commonly used techniques in machine learning problems due to their simplicity and easily understandable structure. Unlike linear/logistic regression, DT can approximate nonlinear relationships and yet remain interpretable via simple if-else logic. However, the transparency of tree models diminishes with increasing depth, and popular ensemble tree models such as XGBoost or gradient-boosting tree models completely eliminate any form of interpretability. The user can interpret decision trees by traversing through the root node and upon arrival at each leaf node. The outcome can simply be explained as “if is ¿/¡ AND is ¿/¡ , , outputs ”. (Gramespacher and Posth, 2021) employs a single DT and frames the loan approval task as one which maximizes profit for the lender firm. (Carta et al., 2021) builds a lexicon dictionary associated with stock price variation, extracted from a dataset comprising both news and historical stock prices. The combined effort provides users with two forms of explanation, observed in a sequential rule-based manner as well as words correlated with the predicted market direction.