Variance Reduction of Resampling for Sequential Monte Carlo

Abstract

A resampling scheme provides a way to switch low-weight particles for sequential Monte Carlo with higher-weight particles representing the objective distribution. The less the variance of the weight distribution is, the more concentrated the effective particles are, and the quicker and more accurate it is to approximate the hidden Markov model, especially for the nonlinear case. We propose a repetitive deterministic domain with median ergodicity for resampling and have achieved the lowest variances compared to the other resampling methods. As the size of the deterministic domain (the size of population), given a feasible size of particles, our algorithm is faster than the state of the art, which is verified by theoretical deduction and experiments of a hidden Markov model in both the linear and non-linear cases.

Keywords Markov chain Monte Carlo Hidden Markov models Riesz

1 Introduction

Sequential Monte Carlo (SMC) or Particle Filter [1] is a set of Monte Carlo methods for solving nonlinear state-space models given noisy partial observations, which are widely used in signal and image processing [2], stock analysis [3, 4], or robotics [5]. It updates the predictions recursively by samples composed of weighted particles to infer the posterior probability density. While the particles will be impoverished as the sample forwards recursively, it can be mitigated by resampling where the negligible weight particles will be replaced by other particles with higher weights [6].

In the literature, several resampling methods and corresponding theoretical analysis [7, 8, 9, 10] can be found. The frequently used algorithms are residual resampling [11], multinomial resampling [1], stratified resampling [12], and systematic resampling [13, 14]. A justified decision regarding which resampling strategies to use might result in a reduction of the overall computation effort and high accuracy of the estimations of the objective. However, for resampling, most of these strategies traverse repetitively from the original population, the negligible weight particles fail to be discarded completely, although the diversity of the particle reserve, causes unnecessary computational load and affects the accuracy of estimations of the posterior distribution. From the perspective of complexity and variance reduction with promising estimation, we propose a repetitive deterministic domain ergodicity strategy, where more concentrated and effective particles are drawn to approximate the objective. Our proposal can be widely used in large-sample approximations.

In this paper, we concentrate on the analysis of the importance sample resamplings built-in SMC for the hidden Markov model. In Section 2, we present a brief introduction to SMC. Here, a brief introduction to the hidden Markov model and the sequential importance sampling method will be given. Our method will be introduced in Section 3, where we introduce the origin of our method, and how to implement each step in detail, and then the theoretical asymptotic behavior of approximations using our method is provided. The practical experiments will be validated by Section 4, where performance and complexity analysis are presented. The summary of our contributions is outlined in Section 5.

2 Resampling in SMC for Hidden Markov Model

Consider the state-space model, which is also known as a hidden Markov model, described by

| (1) |

The initial state follows probability density distribution , is a latent variable to be observed, the measurements are assumed to be conditionally independent given , the most objective is to estimate .

The recursive Bayesian estimation can be used and it is described as:

(a) Prediction

| (2) |

(b) Update

| (3) |

From (2) and (3) the integral part is unreachable, especially, for high-dimensional factors involved, we fail to get the close form of [15, 16].

Sequential Monte Carlo is a recursive algorithm where a cloud of particles is propagated to approximate the posterior distribution . Here, we describe a general algorithm that generates at time , particles with the corresponding empirical measure , a discrete weighted approximation of the true posterior , denotes the delta-Dirac mass located at , equals to . The particles are drawn recursively using the observation obtained at time and the set of particles drawn at time , accordingly, where . The weights are normalized using the principle of importance sampling such that . If the samples are drawn from an importance density , we have

| (4) |

Suppose at time step , we have existed samples to approximate the current posterior distribution , if we get a new observation at time , a recursive approximation to with a new set of samples can be obtained by importance sampling, the corresponding factorization [14] is described by

| (5) |

Then, we can get the new samples by propagating each of the existing samples with the new state . To derive the weight update equation, we follow the ergodic Markov chain properties of the model, the full posterior distribution can be written recursively in terms of , and [14]:

| (6) |

| (7) |

We assume the state is ergodic Markovian, thus, , from this point, we only need to store the , and obtain the thinning recursively update weight formula [17]:

| (8) |

The corresponding empirical posterior filtered density can be approximated as

| (9) |

It can be shown that as , converges to .

Ideally, the importance density function should be the posterior distribution itself, . While the variance of importance weights increases over time, which will decrease the accuracy and lead to the degeneracy that some particles make up negligible normalized weights. The brute force approach to reducing the effect of degeneracy is to increase as large as possible. However, as the size of the sample increases, the computation of the recursive step will also be exponentially costly. Generally, we can try two ways to improve: (I) suitable importance density sampling; (2) resampling the weights. Here we focus on the latter. A suitable measure of the degeneracy of an algorithm is the effective sample size introduced in [14]:, , while the close solution is unreachable, it could be approximated [18] by . If the weights are uniform, for each particle , ; If there exists the unique particle, whose weight is , the remaining are zero, . Hence, small easily lead to a severe degeneracy [17]. We use as an indicator to measure the condition of resampling for our experiments in section 4.

We will introduce our proposal based on the repetitive deterministic domain traverse in the next section.

3 Repetitive Deterministic Domain with Median Ergodicity Resampling

3.1 Multinomial Sampling

A Multinomial distribution provides a flexible framework with parameters and , to measure the probability that each class has been sampled times over categorical independent tests. It can be used to resample the location in our proposal in two steps. Firstly, we obtain the samples from a uniform generator ; secondly, we evaluate the index of samples with the generalized inverse rule, if the cumulative sum of samples larger or equal to , this index will be labeled, then the corresponding sample will be resampled, this event can be mathematically termed as .

3.2 Deterministic Domain Construction

The population of weights is divided into two parts. The first part is the weights, larger than the average , they are considered as the candidate firstly to be sampled, we keep replicates of for each , where is the renormalized unit. will be filtered one by one from the population, and the corresponding tag will be saved into an array. We find, this part also follows the multinomial distribution , We extract the samples from the population with the rule of multinomial sampling shown in section 3.1. This step is the first layer of the traverse from the population, we achieve the first subset, then, we renormalized the weights in the subset, and traverse again to differentiate the larger weights and other units, until we get the feasible size of the set to be considered as the potential deterministic domain.

We define the integer part event, , similarly for the following repetitive part, . We count the units involved in the occurrence of the event and , then extract these units based on the tags , which forms the final deterministic domain.

3.3 Repetitive Ergodicity in Deterministic Domain with Median Schema

Our goal is to retract and retain units with large weights, while the remaining ones with low weights can be effectively replaced in the populations. We set the desired number of resampled units as the size of populations under the premise of ensuring unit diversity as much as possible.

We normalized all the units to keep the same scaled level for comparison, after that, the units with higher weights above the average level will appear as real integers (larger than zero) by , the remaining will be filtered to zero. This is the prerequisite for the deterministic domain construction. In Ns subset, there exist multiple categorical units, that follow the multinomial distribution. We sample these termed large units with two loops, the outer loop is to bypass the index of the unit zero, and the inner loop is to traverse and sample the subset where different large units distribute, there more large weights will be sampled multiple times.

The last procedure is to repetitively traverse in the deterministic domain, where each unit will be renormalized and the corresponding cumulative summation is used to find the index of the unit with the rule of the inverse cumulative distribution function. Each desired unit will be drawn by the multinomial sampler to rejuvenate the population recursively. The complexity of our method is . As the size of the deterministic domain (the size of population), given a feasible size of particles, our algorithm is faster than the state of the art. The total implement schema is shown in Algorithm 1.

3.4 Theoretical Asymptotic Behavior of Approximations

3.4.1 Central limit theorem

Suppose that for each , are independent, where denotes the median of the originator particles. For others belong to the deterministic domain; the probability space of the sequence recursively changes with for sequential Monte Carlo, such a collection is called a triangular array of particles. Let . We expand the characteristic function of each to second-order terms and estimate the remainder to establish the asymptotic normality of . Suppose that both the means and the variance are finite; we have

| (10) |

Theorem 1 For each the sequence sampled from the originator particles , suppose that are independent, where denotes the median of the originator particles. For the rest belong to the deterministic domain; let be a measurable function and assume that there exists satisfying

| (11) |

and

| (12) |

If is aperiodic, irreducible, positive Harris recurrent with invariant distribution and geometrically ergodic, and if, in addition,

| (13) |

satisfies

| (14) |

Proof Let , by [19], , when , we have

| (15) |

We first assume that is bounded. From the property of characteristic function, the left-hand side can be written as

Therefore, the corresponding character function of satisfies

| (16) |

Note that the expected value exists and is finite, the right-hand side term can be integrated by

| (17) |

As , , then, , which satisfies Lindeberg condition:

| (18) |

for .

| (19) |

By [19]

| (20) |

By page358 Lemma 1 [19].

| (21) | ||||

Thus,

| (22) |

The characteristic function of is equal to , thus, (14) holds.

3.4.2 Asymptotic Variance 1

The sample median can be defined as

| (23) |

Define

| (24) | ||||

and

| (25) |

Theorem 2 Under the integrability conditions of theorem 1, suppose that , , satisfying

| (26) |

where the originator particle size and

| (27) |

Proof We decompose the original sequence in descending order into two parts, denotes the median of the originator particles, the rest belong to the deterministic domain; We solve for the variance of these estimators separately.

We assume that the population has an infinite number of individuals, The values of the variance of the median for even and odd approach the same limit, but the value for the even will be less than the value for the odd [20], Karl Pearson extended it with a more accurate estimation of the variance. Consequently, for the upper bound, here we consider the variance at the case of , denoted by . Next, we derive a more detailed expression separately.

For , we first need to find the pdf of , intuitively,

| (28) |

where is the event that of the values are less than . Because does not appear in the event , the event is the chance that if we toss a coin times, the probability of tails obtained, it can be formulated as

| (29) |

Thus, , The variance of is .

The particle in the deterministic domain was resampled on the basis of the originator particle, which has been truncated, satisfying

| (30) |

For any generic function , the corresponding sample mean after resampling

| (31) |

is a consistent estimator of , whose variance is a function of the incremental weights and transition kernels encountered up to time from . Inspired by [21], the variance of this estimator under large sample sizes can be formulated as

| (32) |

where denotes expectation under the posterior distribution , denotes expectation under importance sampling distribution , and is the population size at .

Consequently, each resampling stage at contributes an additional variance component (32).

After rejuvenation, many of the previous particles will be discarded, and if we assume the whole population size of particles is stable, then the limit on the proportion of discarded particles satisfies,

| (33) |

Although the progressive impoverishment will lead to an increase in variance , the rest will maintain a common attribute when . the accumulation of variance components after each rejuvenation will be negligible.

As the simulation consistent estimator of is not available from the output samples, we consider the case from importance sampling distribution of , the variance can be reduced to

| (34) |

| (35) |

A simulation-consistent estimator of is

| (36) |

where is the index of the sample at stage that survives as sample at stage . provides an indicator of sample size whether it is adequate to resist particle impoverishment. Thus, (26) and (27) hold.

Theorem 3 Suppose that each with a strictly positive probability density function and continuity on , let be the median of each , such that the cumulative function of satisfying , then the sample median of approximates the distribution in the precise sense that, as ,

| (37) |

where .

Proof We follow (28) and let , we have

| (38) |

3.4.3 Consistency

Theorem 4 Assume that the particle set on the state space is consistent, where the convergence of Markovinian state transition holds. Then, the uniform weighted sample in the subset of drew by the repetitive ergodicity in deterministic domain with median resampler is biased but consistent.

Proof There is a special case that when the median of particles belong to the deterministic domain, the particles with weight have been totally discarded, thus, the particle set after resampling is biased.

Under the integrability conditions of theorem 1, We invoke Chebyshev’s Inequality,

,

| (42) |

As , , for , as , consequently,

| (43) |

| (44) |

for all is consistent.

As the resampling schema repetitively in a scaled domain, the total variance of our method obtained will be the lowest compared to other resampling methods, which is verified by the experiments.

4 Simulation

In this part, the results of the comparison of these resampling methods are validated from the experiments with the linear Gaussian state space model and nonlinear state space model, respectively. We ran the experiments on an HP Z200 workstation with an Intel Core i5 and an Ubuntu SMP kernel. The code is available at https://github.com/986876245/Variance-Reduction-for-SMC.

4.1 Linear Gaussian State Space Model

This linear model is expressed by:

| (45) |

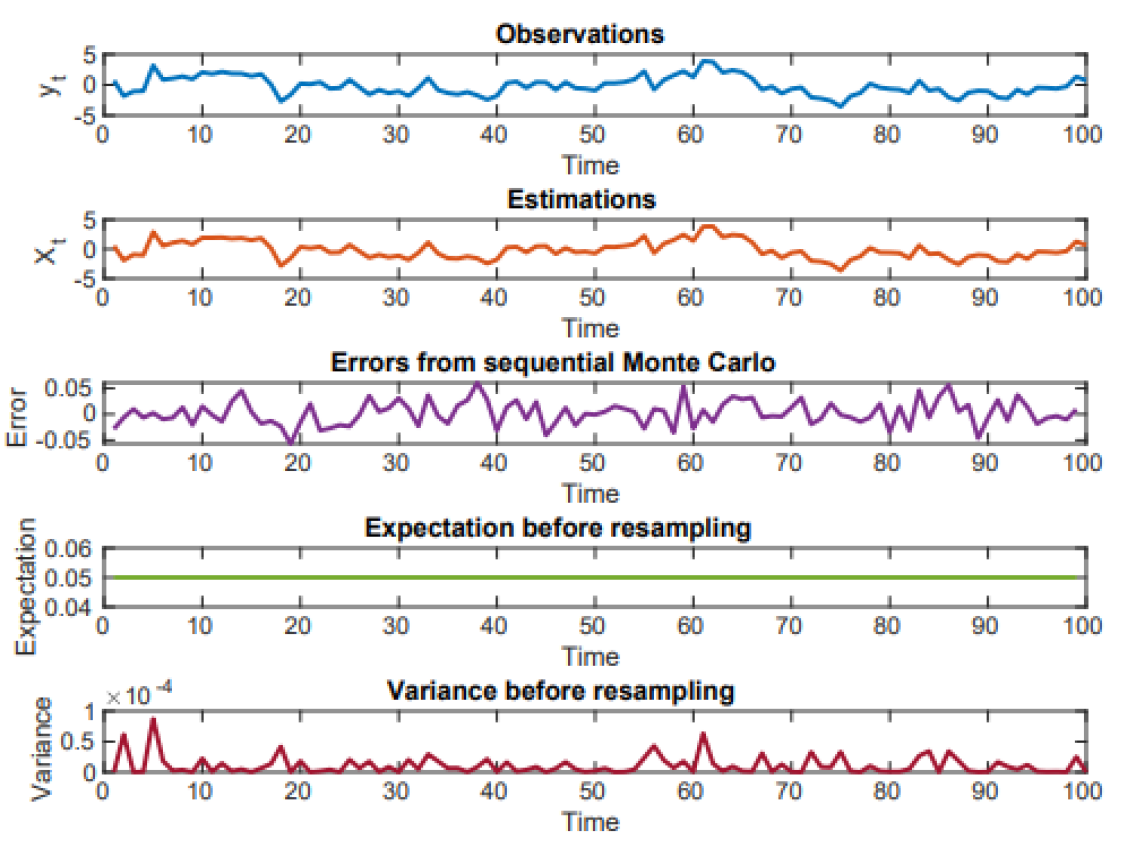

We keep parameters the same as [23] to compare with the different resampling methods. Where , describes the persistence of the state, while denote the standard deviations of the state transition noise and the observation noise, respectively. The Gaussian density is denoted by with mean and standard deviation . In Figure 1, we use 20 particles to track the probability distribution of the state, composed of 100 different times, the ground truth is from the Kalman filter [24], the error denotes the difference between the estimation by SMC and the ground truth. Initially, the expectation of weights for 20 particles is equal to , which means that these particles have equal functions to track the state.

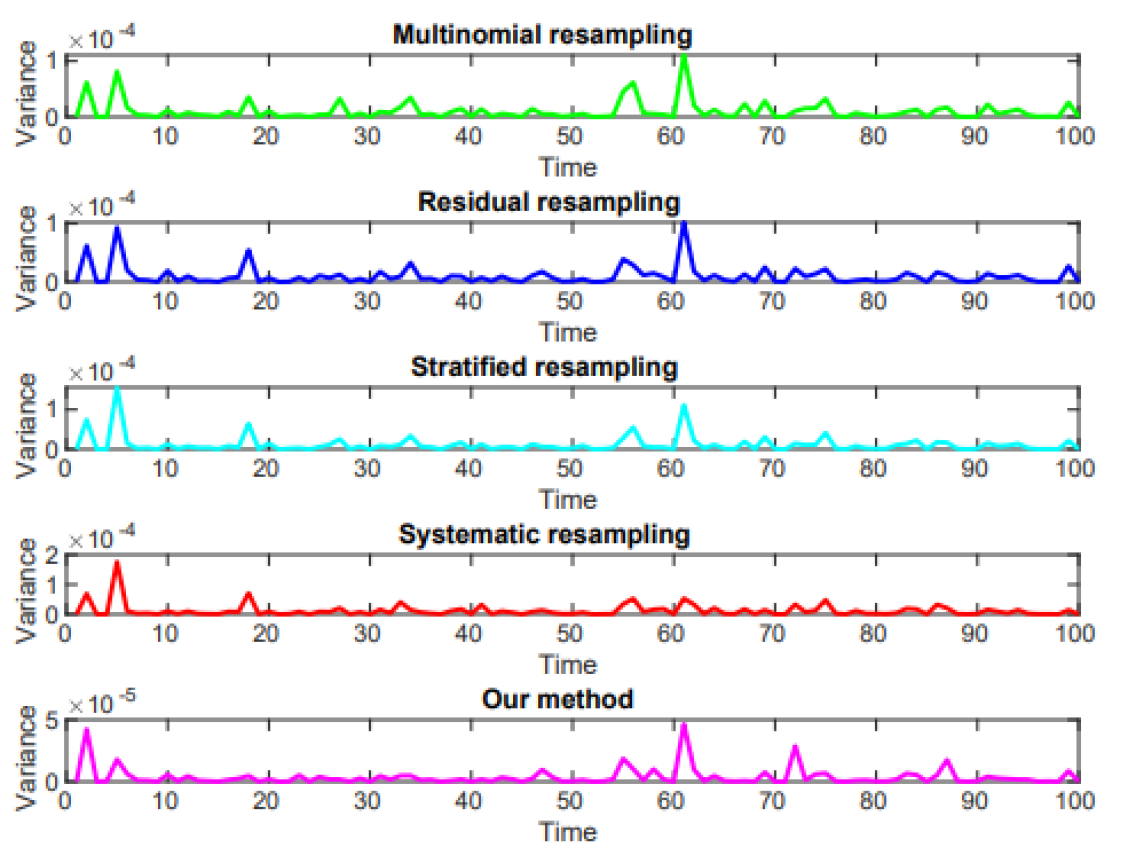

For the resampling procedure, we compare the variance from different classical resampling methods, shown in Figure 2. The variance from the deterministic traverse method is the smallest. Thus, the effective particles are more concentrated after resampling based on our proposal.

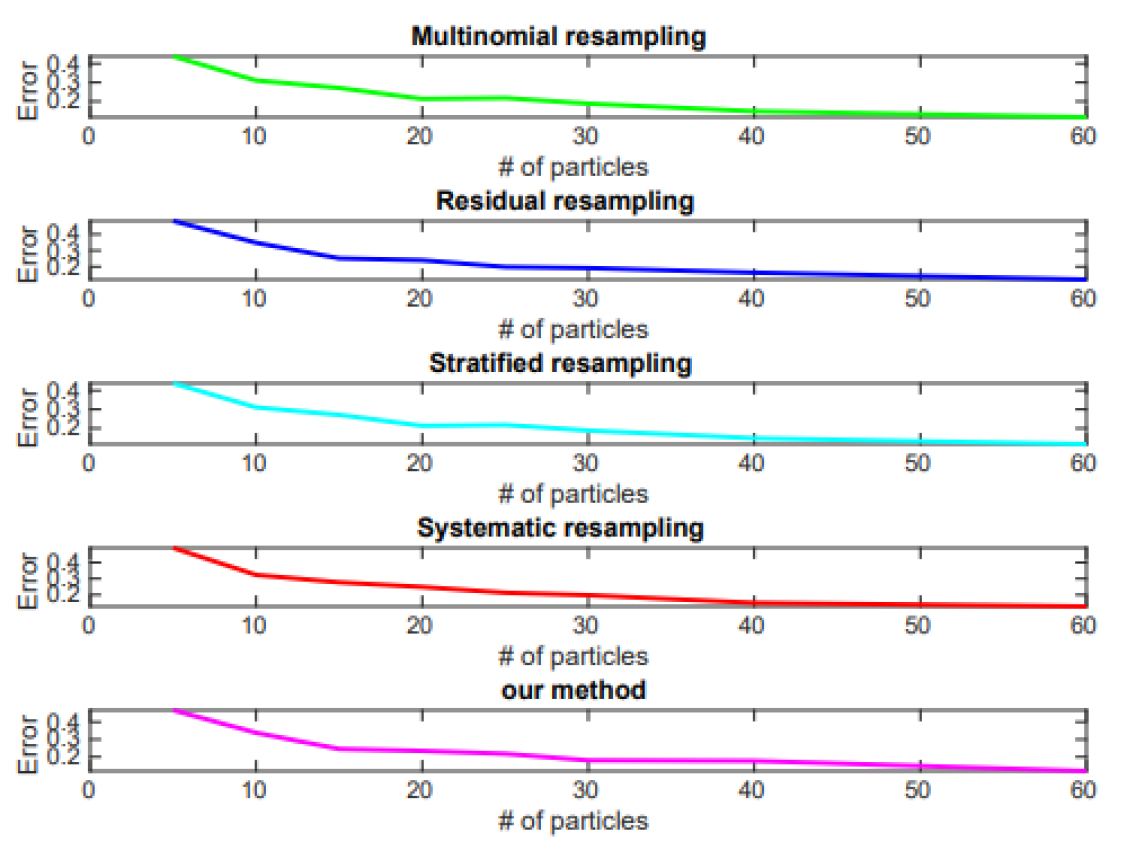

Figure 3 shows the root mean squared(RMSE) error for different resampling strategies, the decreasing rate of our method is higher than that from other methods as the particle increase, given in a feasible domain.

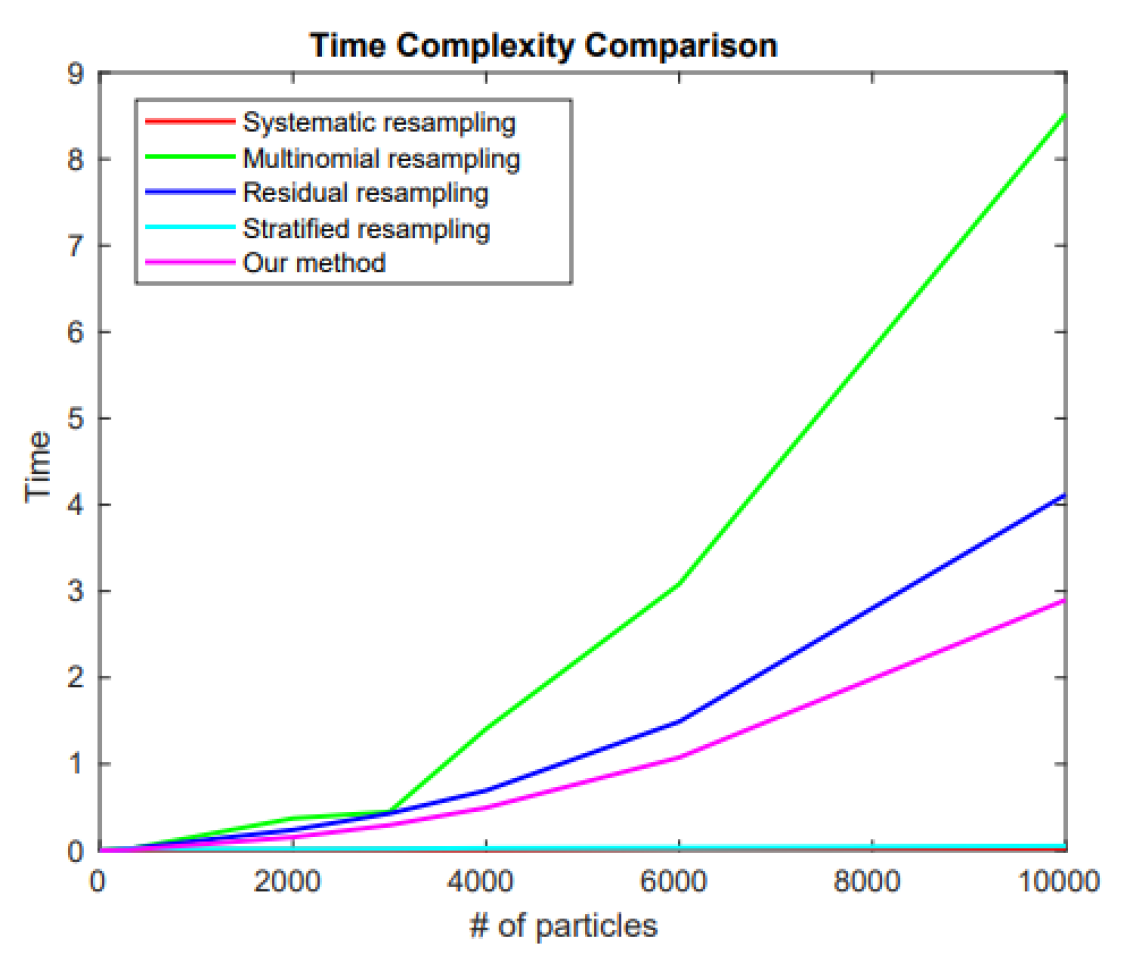

The computational complexity is another factor the resampling algorithms are compared on, Figure 4 shows the execution times for different particles distributed, generally, it depends on the machines and random generator, during our simulations, the time consumption is different under the same condition of resampling method and number of particles. Furthermore, we find under the same resampling methods, the time consumed for the small size of particles is much more than that of the larger ones. The computational stability of particles with resampling methods is very sensitive to the units from a specific population. For safety, we conduct multiple experiments to achieve the general complexity trend.

In Figure 4, all the experiments are conducted under the same conditions, for large-size particles, the stratified and systematic strategies are favorable. In Table 1, we can find under small-size particles(less than 150), our method performs best.

| # of particles | Multinomial resampling | Residual resampling | Systematic resampling | Stratified resampling | Our method |

|---|---|---|---|---|---|

| 5 | 0.0016 | ||||

| 15 | 0.0018 | ||||

| 50 | 0.0022 | ||||

| 80 | 0.0027 | ||||

| 100 | 0.0030 | ||||

| 150 | 0.0036 |

4.2 Nonlinear State Space Model

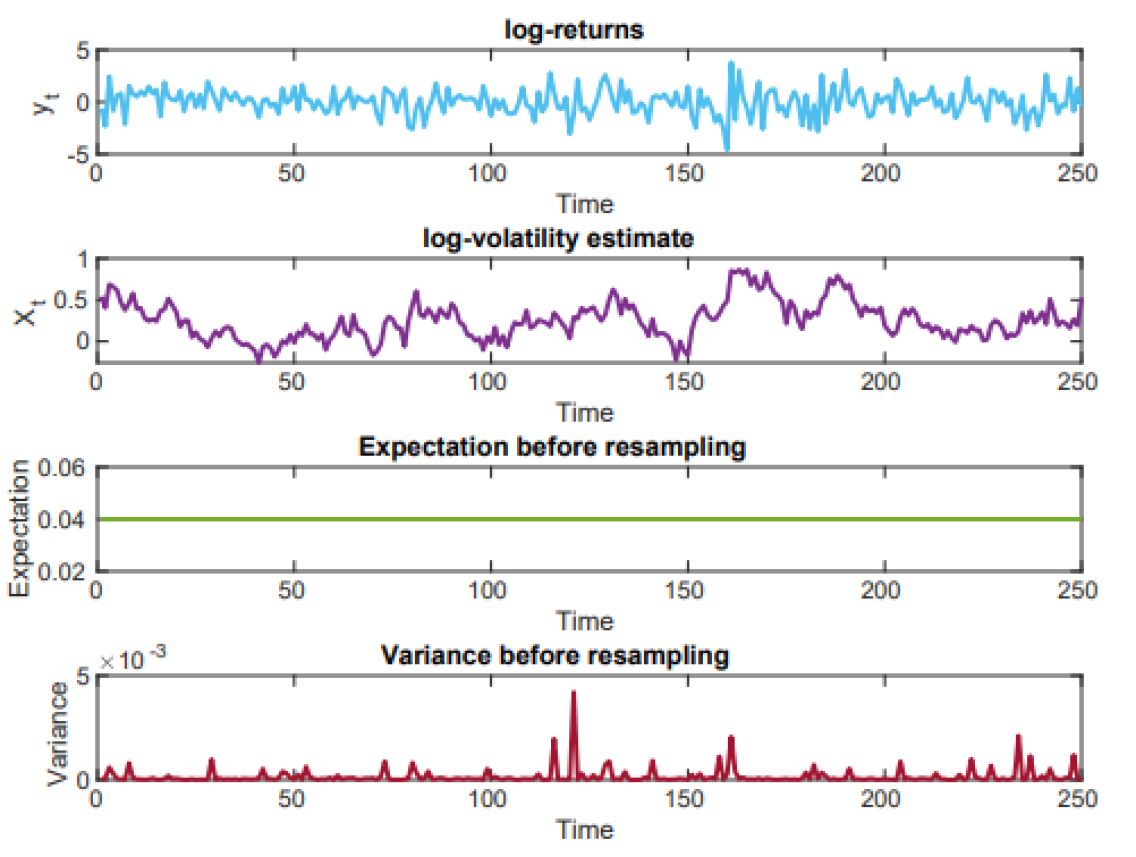

We continue with a real application of our proposal to track the stochastic volatility, a nonlinear State Space Model with Gaussian noise, where log volatility considered as the latent variable is an essential element in the analysis of financial risk management. The stochastic volatility is given by

| (46) |

where the parameters , , and , denote the mean value, the persistence in volatility, the standard deviation of the state process and the instantaneous volatility, respectively.

The observations , also called log-returns, denote the logarithm of the daily difference in the exchange rate , here, is the daily closing price of the NASDAQ OMXS30 index (a weighted average of the 30 most traded stocks at the Stockholm stock exchange). We extract the data from Quandl for the period between January 2, 2015 and January 2, 2016. The resulting log-returns are shown in Figure 5. We use SMC to track the time-series persistency volatility, large variations are frequent, which is well-known as volatility clustering in finance, from the equation (42), as is close to and the standard variance is small, the volatility clustering effect easier occurs. We keep the same parameters as [23], where , , .

We use 25 particles to track the persistency volatility, the expectation of weights of particles is , shown in Figure 5, it is stable as the same with Figure 1, the variance is in orders of magnitude under random sampling mechanism.

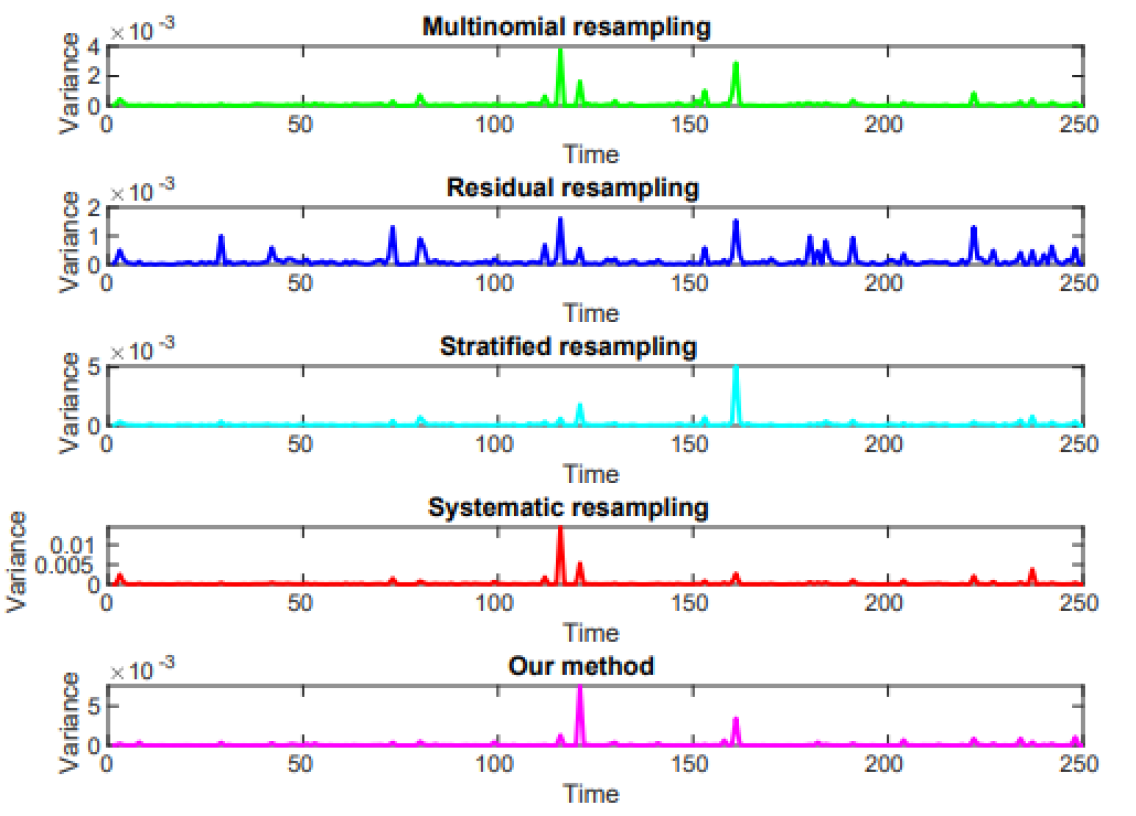

In Figure 6, the variance from our proposal shows the minimum value at different times, nearly all the plot share the common multimodal feature at the same time, it stems from the multinomial distribution that both of them have when they resample a new unit.

5 Conclusion

Resampling strategies are effective in Sequential Monte Carlo as the weighted particles tend to degenerate. However, we find that the resampling also leads to a loss of diversity among the particles. This arises because in the resampling stage, the samples are drawn from a discrete multinomial distribution, not a continuous one. Therefore, the new samples fail to be drawn as a type that has never occurred but stems from the existing samples by the repetitive schema. We have presented a repetitive deterministic domain traversal for resampling and have achieved the lowest variances compared to other resampling methods. As the size of the deterministic domain (the size of population), our algorithm is faster than the state of the art, given a feasible size of particles, which is verified by theoretical deduction and experiments of the hidden Markov model in both the linear and the non-linear case.

The broader impact of this work is that it can speed up existing sequential Monte Carlo applications and allow more precise to estimates their objectives. There are no negative societal impacts, other than those arising from the sequential Monte Carlo applications themselves.

Acknowledgments

This was supported in part by BRBytes project.

References

- [1] Neil J Gordon, David J Salmond, and Adrian FM Smith. Novel approach to nonlinear/non-Gaussian Bayesian state estimation. In IEE Proceedings F (Radar and Signal Processing), volume 140, pages 107–113. IET, 1993.

- [2] Simo Särkkä, Aki Vehtari, and Jouko Lampinen. Rao-Blackwellized particle filter for multiple target tracking. Information Fusion, 8(1):2–15, 2007.

- [3] Roberto Casarin, Carmine Trecroci, et al. Business Cycle and Stock Market Volatility: A Particle Filter Approach. Università degli studi, Dipartimento di scienze economiche, 2006.

- [4] Thomas Flury and Neil Shephard. Bayesian inference based only on simulated likelihood: particle filter analysis of dynamic economic models. Econometric Theory, pages 933–956, 2011.

- [5] Dieter Fox. Kld-sampling: Adaptive particle filters and mobile robot localization. Advances in Neural Information Processing Systems (NIPS), 14(1):26–32, 2001.

- [6] Arnaud Doucet, Simon Godsill, and Christophe Andrieu. On sequential Monte Carlo sampling methods for Bayesian filtering. Statistics and Computing, 10(3):197–208, 2000.

- [7] Hans R Künsch et al. Recursive Monte Carlo filters: algorithms and theoretical analysis. The Annals of Statistics, 33(5):1983–2021, 2005.

- [8] Nicolas Chopin et al. Central limit theorem for sequential Monte Carlo methods and its application to Bayesian inference. Annals of Statistics, 32(6):2385–2411, 2004.

- [9] Randal Douc and Eric Moulines. Limit theorems for weighted samples with applications to sequential Monte Carlo methods. In ESAIM: Proceedings, volume 19, pages 101–107. EDP Sciences, 2007.

- [10] Walter R Gilks and Carlo Berzuini. Following a moving target—Monte Carlo inference for dynamic Bayesian models. Journal of the Royal Statistical Society: Series B (Statistical Methodology), 63(1):127–146, 2001.

- [11] Jun S Liu and Rong Chen. Sequential Monte Carlo methods for dynamic systems. Journal of the American Statistical Association, 93(443):1032–1044, 1998.

- [12] Adrian Smith. Sequential Monte Carlo Methods in Practice. Springer Science & Business Media, 2013.

- [13] Genshiro Kitagawa. Monte Carlo filter and smoother for non-Gaussian nonlinear state space models. Journal of Computational and Graphical Statistics, 5(1):1–25, 1996.

- [14] M Sanjeev Arulampalam, Simon Maskell, Neil Gordon, and Tim Clapp. A tutorial on particle filters for online nonlinear/non-Gaussian Bayesian tracking. IEEE Transactions on Signal Processing, 50(2):174–188, 2002.

- [15] Simo Särkkä. Bayesian Filtering and Smoothing. Cambridge University Press, 2013.

- [16] Arnaud Doucet and Adam M Johansen. A tutorial on particle filtering and smoothing: Fifteen years later. Handbook of Nonlinear Filtering, 12(656-704):3, 2009.

- [17] Neil Gordon, B Ristic, and S Arulampalam. Beyond the Kalman filter: Particle filters for tracking applications. Artech House, London, 830(5):1–4, 2004.

- [18] Jun S Liu. Monte Carlo Strategies in Scientific Computing. Springer Science & Business Media, 2008.

- [19] Patrick Billingsley. Measure and probability. 1995.

- [20] Tokishige Hojo and Karl Pearson. Distribution of the median, quartiles and interquartile distance in samples from a normal population. Biometrika, pages 315–363, 1931.

- [21] Carlo Berzuini, Nicola G Best, Walter R Gilks, and Cristiana Larizza. Dynamic conditional independence models and markov chain monte carlo methods. Journal of the American Statistical Association, 92(440):1403–1412, 1997.

- [22] David Williams. Weighing the odds: a course in probability and statistics. Cambridge University Press, 2001.

- [23] Johan Dahlin and Thomas B Schön. Getting started with particle Metropolis-Hastings for inference in nonlinear dynamical models. Journal of Statistical Software, 88(2):1–41, 2019.

- [24] Greg Welch, Gary Bishop, et al. An introduction to the Kalman filter. Technical report, University of North Carolina at Chapel Hill, Chapel Hill, NC, USA, 1995.