On Sparse Grid Interpolation for American Option Pricing with Multiple Underlying Assets

Abstract

In this work, we develop a novel efficient quadrature and sparse grid based polynomial interpolation method to price American options with multiple underlying assets. The approach is based on first formulating the pricing of American options using dynamic programming, and then employing static sparse grids to interpolate the continuation value function at each time step. To achieve high efficiency, we first transform the domain from to via a scaled tanh map, and then remove the boundary singularity of the resulting multivariate function over by a bubble function and simultaneously, to significantly reduce the number of interpolation points. We rigorously establish that with a proper choice of the bubble function, the resulting function has bounded mixed derivatives up to a certain order, which provides theoretical underpinnings for the use of sparse grids. Numerical experiments for American arithmetic and geometric basket put options with the number of underlying assets up to 16 are presented to validate the effectiveness of the approach.

Key words: sparse grids, American option pricing, multiple underlying assets, continuation value function, quadrature

MSC classification: 65D40, 91G20

1 Introduction

This paper is concerned with American option pricing with payoffs affected by many underlying instruments, which can be assets such as stocks, bonds, currencies, commodities, and indices (e.g., S&P 500, NASDAQ 100) [51, p. 365]. Classical examples include pricing American max-call and basket options [5, 27, 30, 33, 40, 45, 46]. In practice, American options can be exercised only at discrete dates. The options that can be exercised only at finite discrete dates are called Bermudan options, named after the geographical feature of Bermudan Islands (i.e., being located between America and Europe while much closer to the American seashore) [26]. Merton [39] showed that pricing an American call option on a single asset with no dividend is equivalent to pricing a European option, and obtained an explicit solution to pricing perpetual American put. However, except these two cases no closed-form solution is known to price American options even in the simplest Black Scholes model. Thus it is imperative to develop efficient numerical methods for American option pricing.

Various numerical methods have been proposed for pricing and hedging in the past five decades, using different formulations of American option pricing, e.g., an optimal stopping problem, a variational inequality, or a free boundary problem [9, 31, 38, 49]. A finite difference method (FDM) was proposed to price American options based on variational inequalities [12], with its convergence proved in [31] by showing that the regularity of the value function with respect to the underlying price. The binomial options pricing model (BOPM) based upon optimal time stopping was developed in [17], and its convergence was shown in [4]. When the number of underlying assets is smaller than four, one can extend one-dimensional pricing methods using tensor product or additional treatment to price multi-asset options. For example, Cox-Ross-Rubinstein (CRR) binomial tree model can be extended to the multinomial option pricing model to price American options with two underlying assets [11]. However, dynamic programming (cf. (2.3) below) or variational inequalities [8] are predominant when is greater than three. Many numerical schemes have been developed based on the variational inequalities, e.g., FDMs [1, 12, 20] and finite element methods (FEMs) [33]. However, only the first order convergence rate can be achieved, since the value function has only regularity with respect to the underlying price (i.e., smooth pasting condition [42]).

There are mainly two lines of research on American option pricing based on dynamic programming, i.e., simulation based methods [5, 36, 48] and quadrature and interpolation (Q&I) based methods [44, 47]. Simulation based methods are fast and easy to implement, but their accuracy is hard to justify. One representative method is the least square Monte Carlo method [36], which employs least square regression and Monte Carlo method to approximate conditional expectations, cf. (2.3). Q&I based methods employ quadrature to approximate conditional expectations and interpolation to construct function approximators. One can use Gaussian quadrature or adaptive quadrature to approximate conditional expectations in (2.3) and Chebyshev polynomial interpolation, spline interpolation or radial basis functions to reconstruct the continuation value or the value function [44, 47]. In [24], a dynamic Chebyshev method via polynomial interpolation of the value functions was developed, allowing the generalized moments evaluation in the offline stage to reduce computational complexity. Although Q&I based methods are efficient in low-dimensional settings, the extensions to high-dimensional cases are highly nontrivial, and there are several outstanding challenges, e.g., curse of dimensionality, unboundedness of the domain and the absence of natural boundary conditions. For example, if the domain is truncated and artificial boundary conditions are imposed, then one is actually pricing an American barrier option with rebate instead of the American option itself. Accurate boundary conditions can be obtained by pricing a -dimensional problem [40], which, however, is still computationally challenging.

The sparse grids technique has been widely used in option pricing with multiple underlying assets, due to its capability to approximate high-dimensional functions with bounded mixed derivatives, for which the computational complexity for a given accuracy does not grow exponentially with respect to [14]. It has been applied to price multi-asset European and path-dependent Asian options, by formulating them as a high-dimensional integration problem [7, 13, 28], and also combined with the FDMs [45] and FEMs [15] to price options with . In the context of Q&I methods, adaptive sparse grids interpolation with local linear hierarchical basis have been used to approximate value functions [46].

In this work, we propose a novel numerical approach to price American options under multiple underlying assets, which is summarized in Algorithm 1. It crucially draws on the regularity of the continuation value function, cf. (2.4), and uses sparse grid Chebyshev polynomial interpolation to alleviate the curse of dimensionality. This is achieved in several crucial steps. First, we transform the unbounded domain into a bounded one, which eliminates the need of imposing artificial boundary conditions. Second, to further improve the computational efficiency, using a suitable bubble function, we obtain a function that can be continuously extended to the boundary with vanishing boundary values and with bounded mixed derivatives up to certain orders, which is rigorously justified in Theorem 1. This construction enables the use of the standard sparse grid technique with much fewer sparse grids (without adaptivity), and moreover, the interpolation functions fulfill the requisite regularity conditions, thereby admitting theoretical convergence guarantees. The distinct features of the proposed method include using static sparse grids at all time steps and allowing deriving the value function on the whole domain , and thus can also be used to estimate important parameters, e.g., hedge ratio.

Extensive numerical experiments demonstrate that Algorithm 1 can break the curse of dimensionality in the sense that high accuracy is achieved with the associated computational complexity being almost independent of the dimension. Furthermore, our experiments can significantly enrich feasible dimensionality, e.g., pricing American arithmetic basket put options up to (versus from the literature), and pricing American geometric basket put options up to . In both cases, we consistently observe high accuracy of the approximation, with almost no influence from the dimension. Further experimental evaluations show that the method is robust with respect to the choice of various algorithmic parameters and the specifics of the quadrature scheme. In sum, our proposed algorithm significantly improves over the state-of-the-art pricing schemes for American options with multiple underlying assets and in the meanwhile has rigorous theoretical guarantee.

The remainder of our paper is structured as follows. In Section 2, we derive the continuation value function for an American basket put option with underlying assets following the correlated geometric Brownian motion under the risk-neutral probability. In Section 3, we develop the novel method. In Section 4, we establish the smoothness of the interpolation function in the space of functions with bounded mixed derivatives. In Section 5, we present extensive numerical tests for American basket options with up to 16 underlying assets. Finally, we conclude with future work in Section 6.

2 The mathematical model

Martinagle pricing theory gives the fair price of an American option as the solution to the optimal stopping problem in the risk-neutral probability space :

| (2.1) |

where is a -stopping time, is the expiration date, , is a collection of -dimensional price processes, and is the payoff function depending on the type of the option. The payoffs of put and call options take the following form and , respectively, where , and is the strike price.

Now we describe a detailed mathematical model for pricing an American put option on underlying assets with a strike price and a maturity date , whose numerical approximation is the main objective of this work. One classical high-dimensional example is pricing American basket options. Let be its payoff function, and assume that the prices of the underlying assets follow the correlated geometric Brownian motions

| (2.2) |

where are correlated -Brownian motions with , for , and , and are the riskless interest rate, dividend yields, and volatility parameters, respectively. The payoffs of an arithmetic and a geometric basket put are respectively given by

In practice, the -stopping time is assumed to be taken in a set of discrete time steps, , with . This leads to the pricing of a -times exercisable Bermudan option that satisfies the following dynamic programming problem

| (2.3) |

where is called the value function at time and is the discretized price processes. Throughout, for a stochastic process , we write , . Note that by the Markov property of Itô process, we can substitute the conditional expectation conditioning on to . The conditional expectation as a function of prices is called the continuation value function, i.e.,

| (2.4) |

Below we recast problem (2.3) in terms of the continuation value function

| (2.5) | ||||||

Given an approximation to , the price of Bermudan option can be obtained by

| (2.6) |

The reformulation in terms of is crucial to the development of the numerical scheme.

Next we introduce the rotated log-price, which has independent components with Gaussian densities. We denote the correlation matrix as , the volatility matrix as a diagonal matrix with volatility on the diagonal, and write the dividend yields as a vector . Then the log-price with each component defined by follows a multivariate Gaussian distribution

with . The covariance matrix admits the spectral decomposition . Then the rotated log-price follows an independent Gaussian distribution

Therefore, to eliminate the correlation, we introduce the transformation

and denote the inverse transformation by

where and represent component-wise division and multiplication.

Finally, by defining as the continuation value function with respect to the rotated log-price for , we obtain the following dynamic programming procedure

| (2.7) | ||||||

The main objective of this work is to develop an efficient numerical method for solving problem (2.7) with a large number of dimension . The detailed construction is given in Section 3.

3 Methodologies

In this section, we systematically develop a novel algorithm, based on quadrature and sparse grids polynomial interpolation (SGPI) [6] to solve problem (2.7) so that highly accurate results can be obtained for moderately large dimensions. This is achieved as follows. First, we propose a mapping (3.1) that transforms the domain from to , and obtain problem (3.3) with the unknown function defined over the hypercube in Section 3.1. The mapping enables utilizing identical sparse grids for all time stepping , which greatly facilitates the computation, and moreover, it avoids domain truncation and artificial boundary data when applying SGPI, which eliminates extra approximation errors. However, the partial derivatives of may have boundary singularities, leading to low-efficiency of SGPI. To resolve this issue, we multiply with a bubble function (3.4), and derive problem (3.5) with unknown functions defined over the hypercube . Second, we present the SGPI of the unknown in Section 3.2. Third and last, we provide several candidates for quadrature rules and summarize the algorithm in Section 3.3, and analyze its complexity.

3.1 Mapping for unbounded domains and bubble functions

A direct application of the SGPI to problem (2.7) is generally involved since the problem is formulated on . For , quadrature and interpolation-based schemes can be applied to problem (2.7) with domain truncation and suitable boundary conditions, e.g., payoff function. However, for , the exact boundary conditions of the truncated domain requires solving -dimensional American option pricing problems [40]. Therefore, the unboundedness of the domain and the absence of natural boundary conditions pose great challenges to develop direct yet efficient interpolation for the continuation value function , and there is an imperative need to develop a new approach to overcome the challenges.

Inspired by spectral methods on unbounded domains [10], we propose the use of the logarithmic transformation , defined by

| (3.1) |

where is a scale parameter controlling the slope of the mapping. The logarithmic mapping is employed since the transformed points decay exponentially as they tend to infinity. Asymptotically the exponential decay rate matches that of the Gaussian distribution of the rotated log-price . Then by Itô’s lemma, the new stochastic process satisfies the stochastic differential equations

| (3.2) |

where , are diagonal elements of , and are independent standard Brownian motions. Note that the drift and diffusion terms in (3.2) vanish on the boundary . Thus, (3.2) fulfills the reversion condition [52], which implies for provided .

Then we apply the mapping to the dynamic programming procedure (2.7). Let be the continuation value function of the bounded variable . Then problem (2.7) can be rewritten as, for any ,

| (3.3) | ||||||

Below we denote by the payoff function with respect to the bounded variable .

Note that problem (3.3) is posed on the bounded domain , , which however remains challenging to approximate. First, the function may have singularities on the boundary due to the use of the mapping . Second, the Dirichlet boundary condition of is not identically zero, which is undesirable for controlling the computational complexity of the algorithm, especially in high dimensions. Thus, we employ a bubble function of the form

| (3.4) |

where the parameter controls the shape of . Note that for and on . Let

Then the dynamic programming problem (3.3) is equivalent to

| (3.5) | ||||||

Remark 1.

The term appearing in (3.5) is well-defined for . Nevertheless, since the bubble function approaches zero as , in the numerical experiments, one should guarantee that evaluated on the computational grid will be greater than the machine epsilon, e.g., in MATLAB. This will be established in Proposition 1.

3.2 Approximation by sparse grids polynomial interpolation (SGPI)

Next, we apply SGPI [6] to approximate the zero extension of iteratively backward in time. By choosing suitable bubble functions , we shall prove in Theorem 1 below the smoothness property of up to order . Thus the SGPI enjoys a geometrical convergence rate with respect to the number of interpolation points , which depends only on the dimension in a logarithm term, i.e. as stated in Proposition 2. In addition, thanks to the zero boundary condition of , the required number of interpolation data is greatly reduced when compared with the full grids.

SGPI [6] (also called Smolyak approximation) is a powerful tool for constructing function approximations over a high-dimensional hypercube. Consider a function . For , we denote by the set of nested Chebyshev-Gauss-Lobatto (CGL) points, with the nodes given by

The cardinality of the set is

The polynomial interpolation of over the set is defined as follows. For , consider the midpoint rule, i.e., . For , is given by

where are Lagrange basis polynomials. Then we define the difference operator

For , Smolyak’s formula approximates a function by the interpolation operator

with the index set and [6]. Equivalently, the linear operator can be represented as [50, Lemma 1]

| (3.6) |

with the index set , where the tensor product of the univariate interpolation operators is defined by

i.e., multivariate Lagrange interpolation. With the set (i.e., one-dimensional nested CGL points), the formula (3.6) indicates that computing only requires function evaluations on the sparse grids

We denote the cardinality of by . Usually, the interpolation level is defined by

Then for fixed and , the following asymptotic estimate of holds [41]

| (3.7) |

The sparse grid has much fewer grid points than the full grid generated by the tensor product. Furthermore, in high-dimensional hypercube, a significant number of sparse grids lie on the boundary. We will compare the number of CGL sparse grids and the number of inner sparse grids in Section 3.3. In Remark 1, we require that evaluated on the computational grid be greater than the machine epsilon. Note that for all inner sparse grids of the interpolation level , each coordinate satisfies

| (3.8) |

where .

3.3 Numerical algorithm

We interpolate the function on CGL sparse grids in the dynamic programming (3.5), where the interpolation data can be formulated as high-dimensional integrals. Since for , only function evaluations on the inner sparse grids are required. This greatly reduces the computational complexity, especially for large . Indeed, since with ,

| (3.9) |

For a fixed interpolation knot , we denote

| (3.10) |

and the probability density of as . Following (3.5), the interpolation data is given by

where the last integral can be computed by any high-dimensional quadrature methods, e.g., Monte Carlo (MC), quasi-Monte Carlo (QMC) method, or sparse grid quadrature.

-

1.

The Monte Carlo method approximates the integral by averaging random samples of the integrand

(3.11) where are independent and identically distributed (i.i.d.) random samples drawn from the distribution .

-

2.

The Quasi-Monte Carlo method takes the same form as (3.11), but are the transformation of QMC points. By changing variables with being the cumulative density function (CDF) of , we have

(3.12) where are QMC points taken from a low-discrepancy sequence, e.g., Sobol sequence and sequences generated by the lattice rule. Note that other transformations are also available for designing QMC approximation [34].

-

3.

The Sparse grid quadrature approximates the integral based on a combination of tensor products of univariate quadrature rule. For the integration with Gaussian measure, several types of sparse grids are available, including Gauss-Hermite, Genz-Keister, and weighted Leja points [43]. Let be quadrature weights and points associated with an anisotropic Gaussian distribution of . Then the integral is computed by

(3.13)

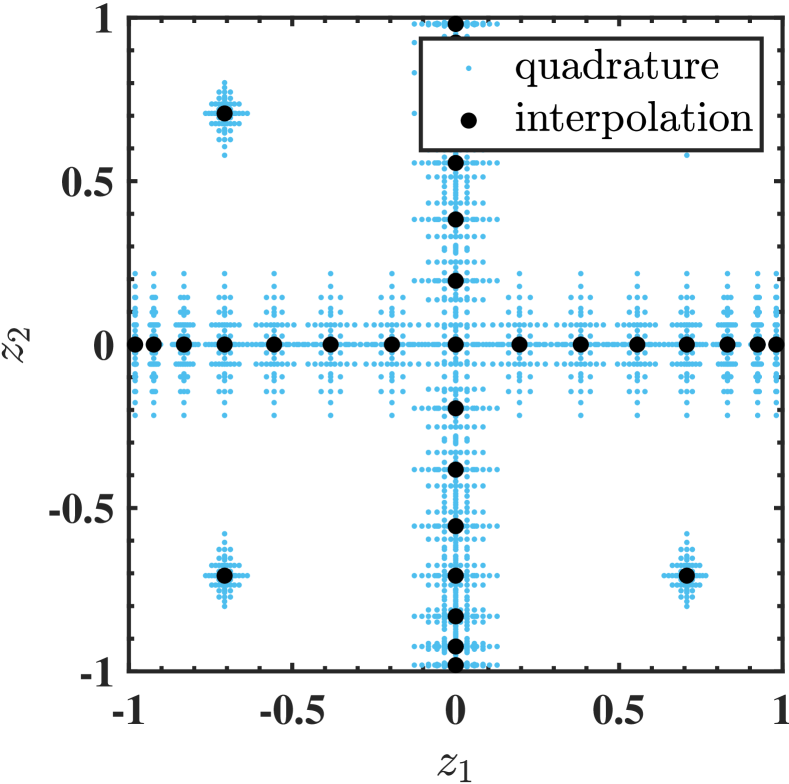

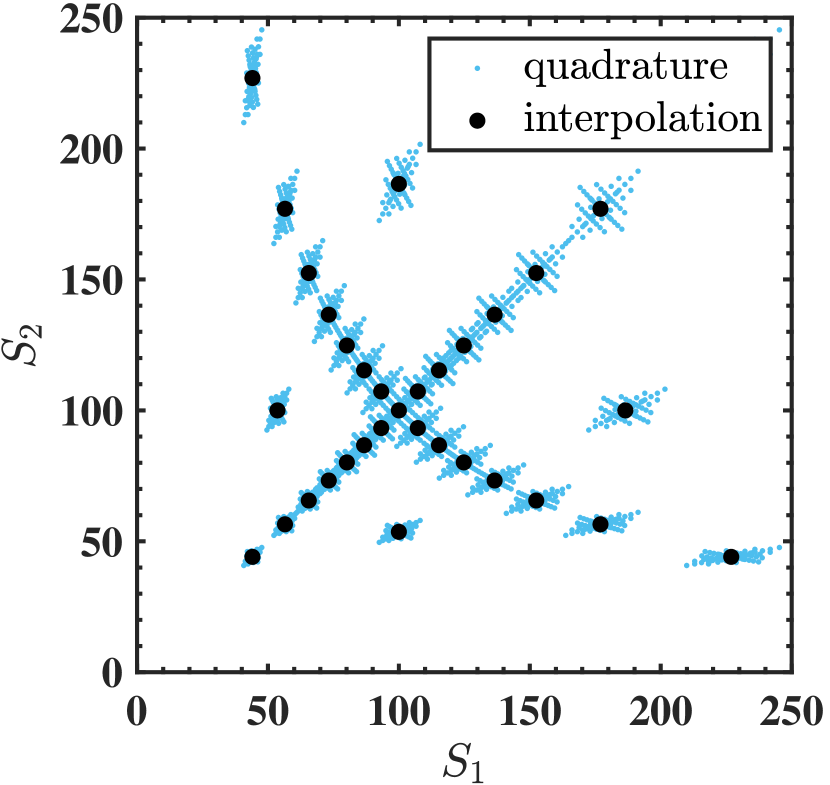

By employing the transformation between the asset price and the bounded variable , the sparse grid interpolation points and the quadrature points are shown in Fig. 1.

Now we can describe the procedure of iteratively interpolating the function in Algorithm 1.

Followed by the Remark 1, the next result gives a sufficient condition on the well-definedness of the algorithm.

Proposition 1.

Let be the machine epsilon. Assume that each coordinate of the sampling or quadrature points of the random variable satisfies

| (3.14) |

where is the -th diagonal element of , and is a constant. If and and are chosen such that

then for all sampling or quadrature points of , , we have

Proof.

Using (3.9), we have , where are inner sparse grid interpolation points and are sampling or quadrature points of . Thus the -th coordinate of is given by

For , to ensure , it suffices to prove . Without loss of generality, consider the case , i.e., . Clearly, we have

Noting that , the binomial expansion implies that it suffices to have . Using the relationship

the inequality (3.8), and the assumption (3.14), we obtain

Since , this proves the desired assertion. ∎

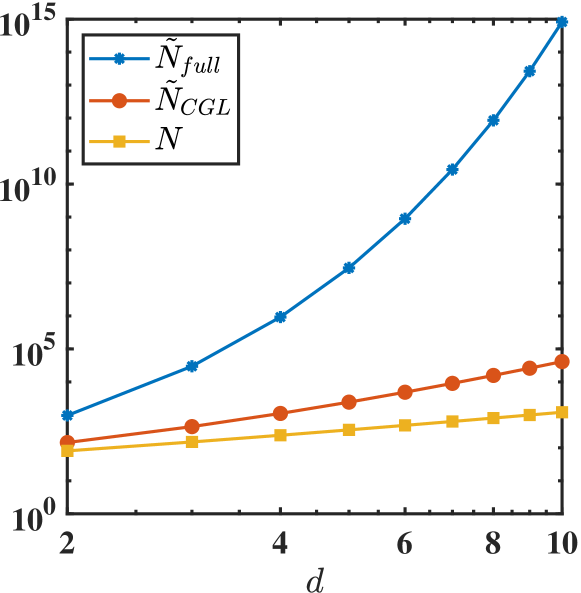

Last, we discuss the computational complexity of the algorithm. By introducing the bubble function, the interpolation functions have zero boundary values. Thus, at each time step, we require evaluations of only on the inner sparse grids, where each evaluation is approximated by equation (3.11), (3.12) or (3.13) with sampling or quadrature points. The number of inner sparse grids of level in dimension is listed in Table 2, which also shows the numbers for tensor-product full grids and CGL sparse grids with boundary points . Unlike full grids, the number of sparse grids does not increase exponentially as the dimension increases. In particular, the inner sparse grids account for less than three percent of the CGL sparse grids in . This represents a dramatic reduction of the evaluation points.

| 2 | 961 | 145 | 81 |

|---|---|---|---|

| 3 | 29791 | 441 | 151 |

| 4 | 923521 | 1105 | 241 |

| 5 | 2.8629e+7 | 2433 | 351 |

| 6 | 8.8750e+8 | 4865 | 481 |

| 7 | 2.7513e+10 | 9017 | 631 |

| 8 | 8.5289e+11 | 15713 | 801 |

| 9 | 2.6440e+13 | 26017 | 991 |

| 10 | 8.1963e+14 | 41265 | 1201 |

4 Smoothness analysis

In this section, we analyze the smoothness of the function , in order to justify the use of SGPI, thereby providing solid theoretical underpinnings of its excellent performance.

First we list several useful notations. Let be the standard multi-index with . Then , , and denotes that each component of the multi-index satisfies . We define the differential operator by . For an open set and , the space denotes the space of functions with their derivatives of orders up to being continuous on the closure of , i.e.,

Specially, consists of functions such that is bounded and uniformly continuous on for all [3]. We also define as the intersection of all for , i.e., .

The analysis of SGPI employs the space of functions on with bounded mixed derivatives [14]. Let be the set of all functions such that is continuous for all with for all , i.e.,

| (4.1) |

We equip the space with the norm .

For the sake of completeness, we present in Proposition 2 the interpolation error using SGPI described in Section 3.2.

Proposition 2 ([6, Theorem 8, Remark 9]).

For , there exists a constant depending only on and such that

where is the number of CGL sparse grids.

To provide theoretical guarantees of applying SGPI, we next prove in Theorem 1. This result follows by Lemma 1 111At a first glance of (4.2), the smoothness of follows directly by the fact that convolution smooths out the payoff function. However, the payoff function of the rotated log-price is not in , neither does the density function have compact support. Therefore, we provide a proof of the regularity in Lemma 1 mainly using the dominated convergence theorem. and Lemma 2.

Lemma 1 ().

Let be the payoff of a put option. Then the continuation value function defined in (2.7) is infinitely differentiable, bounded and uniformly continuous with all its derivatives up to the order for any , i.e., .

Proof.

Consider the conditional expectation without the discount factor :

| (4.2) |

where is the payoff with respect to the rotated log-price, and is the density of the Gaussian distribution , that is,

| (4.3) |

with . Since is the payoff of a put option, is bounded in . Let

Then with . The representation (4.2) is equivalent to

where denotes the convolution operator. Then an application of [19, Proposition 8.8] implies that is bounded and uniformly continuous in , and

| (4.4) |

Next, we show that has the bounded first order partial derivatives for all , and

| (4.5) |

For any fixed , ,

Since the Gaussian density has bounded partial derivatives for all and , then

| (4.6) |

As is bounded and for fixed , the function decays as at infinity, the integrand is bounded by some Lebesgue integrable function for all . Hence, by the dominated convergence theorem, one can interchange the limit and integral in the last equation of (4.6) and thus

By [19, Proposition 8.8], we obtain that is bounded and uniformly continuous in , and

Using the dominated convergence theorem, we derive the bounded second order partial derivatives

since for fixed , the function

decays as at infinity. By [19, Proposition 8.8], we obtain is bounded and uniformly continuous on , and

Repeating the argument yields the boundedness and uniform continuity of the partial derivatives of up to the order for any . Therefore, . ∎

Lemma 2 ( for ).

Let be the payoff of a put option. Then the continuation value functions defined in (2.7) are infinitely differentiable, bounded and uniformly continuous with all its derivatives up to the order for any , i.e., for .

Proof.

Let the value at be

where is bounded for a put option. By (4.4), is bounded. Hence, is bounded in . Using the argument of Lemma 1, we obtain

is infinitely differentiable, bounded and uniformly continuous with all its derivatives up to the order for any . Since , the value is bounded in . Similarly, we can obtain for all . ∎

Using the smoothness of the continuation value functions in , now we can establish the smoothness of the extended interpolation function in the bounded domain .

Theorem 1 ().

Let be the payoff of a put option. Let be the function defined in (3.5) with . Let be the bubble function of the form and be the mapping between unbounded and bounded domains defined in (3.1). If with , then can be extended to such that has bounded mixed derivatives up to the order , i.e.,

Furthermore, for with , there holds

| (4.7) | |||

where and are univariate polynomials of degrees and defined on .

Proof.

First, for the multi-index with ,

is continuous and bounded in due to the continuity and boundedness of in Lemma 2. Since approaches zero as , we can define , and for each . Then is continuous in the closure . The following argument holds for all . Thus, we drop the subscript and denote , and . For any multi-index , Leibniz’s rule implies

| (4.8) |

For any fixed , pick . Consider a multi-index with , . Let with . Then direct computation yields

| (4.9) |

where , , is a polynomial of degree . Note that depends only on through with . Then we have

| (4.10) |

where is a polynomial of degree for each . Combining the last three identities yields the assertion (4.7). Since , by Lemma 2, we deduce that is bounded. By defining the continuous extension of using (4.7), we obtain that for . ∎

To bound in the norm, we need suitable estimates of polynomials and in (4.7).

Lemma 3.

Proof.

By (4.9), . Using the identity , for , and the defining identity in (4.9), we obtain

Dividing both sides by after taking derivative over the left hand side, we obtain

By the triangular inequality, we derive

| (4.12) |

Since is a polynomial of degree defined on , a direct application of the Markov brothers’ inequality [2, p. 300] yields

Plugging this estimate into (4.12) leads to the recurrence relation

| (4.13) |

Upon noting , we derive the desired estimate on . The estimate on follows similarly. For , . For , using (4.10), we obtain

This implies

Since is a polynomial of degree , by the triangular inequality and the Markov brothers’ inequality, we obtain the recurrence relation

| (4.14) |

Together with the identity , we prove the desired assertion on . ∎

We now estimate the norms in terms of suitable mixed norms of . Here,

Theorem 2 (Upper bounds on and for ).

Proof.

Combining (4.7) with (4.11) leads to

| (4.15) | ||||

It follows from Lemma 3 that

Next, we deduce the following estimates from (4.15). If , consider the multi-index with for , then

If , consider the multi-index with for , an application of the trinomial expansion implies

This completes the proof of the theorem. ∎

In Theorem 2, we only consider the cases and , and both can overcome the curse of dimensionality by means of SGPI while maintaining a relatively small upper bound of the functional norm. Clearly, higher order mixed derivatives of the interpolation function have larger upper bounds.

5 Numerical experiments

In this section, we illustrate the efficiency and robustness of the proposed quadrature and sparse grid interpolation scheme, i.e., Algorithm 1, for pricing high-dimensional American options. We present pricing results up to dimension . The accuracy of the option price obtained by Algorithm 1 is measured in the relative error defined by

where is the reference price, either taken from literature or computed to meet a certain tolerance. The results show that the relative errors decay geometrically as the number of interpolation points increase, and the convergence rate is almost independent of the dimension . The comparison of various quadrature methods is also included. The implementation of sparse grids is based on the Sparse Grids MATLAB Kit, a MATLAB toolbox for high-dimensional quadrature and interpolation [43]. The computations were performed by MATLAB R2022b with 32 CPU cores (with 4GB memory per core) using research computing facilities offered by Information Technology Services, The University of Hong Kong. The codes for the numerical experiments can be founded in https://github.com/jiefeiy/multi-asset-American-option/tree/main.

5.1 American basket option pricing up to dimension 16

The examples are taken from [33], where pricing American options up to 6 assets by the FEM was investigated. For each -dimensional problem, the setting of these examples are , , , , , with for . The prices of arithmetic basket options with underlying assets are listed in Table 1, where the last column gives the reference price of American options reported in [33], where the relative error is for pricing a -d American geometric put option.

To further illustrate the efficiency of the algorithm in high dimensions, we consider pricing the geometric basket put options as benchmarks, which can be reduced to a one-dimensional problem. Thus, highly accurate prices are available using one-dimensional quadrature and interpolation scheme. Indeed, the price of the -dimensional problem equals that of the one-dimensional American put option with initial price, volatility, and dividend yield given by

respectively. The prices of geometric basket options with underlying assets are listed in Table 2, where the reference Bermudan prices with times steps with accuracy up to are calculated using one-dimensional quadrature and interpolation scheme. The last column of Table 2 are the reference prices of American options reported in [33] priced by the reduced one-dimensional problem.

| Sparse grid interpolation level | ||||||

| 3 | 4 | 5 | 6 | 7 | ||

| 2 | 2.9193 | 3.1397 | 3.1330 | 3.1269 | 3.1388 | 3.13955 |

| (7.02e-2) | (3.52e-5) | (2.07e-3) | (4.03e-3) | (2.30e-4) | ||

| 3 | 2.8649 | 2.9533 | 2.9300 | 2.9304 | 2.9463 | 2.94454 |

| (2.71e-2) | (2.96e-3) | (4.95e-3) | (4.81e-3) | (5.83e-4) | ||

| 4 | 2.8429 | 2.8547 | 2.8232 | 2.8311 | 2.84019 | |

| (9.42e-4) | (5.11e-3) | (5.98e-3) | (3.22e-3) | |||

| 5 | 2.8271 | 2.7906 | 2.7601 | 2.7710 | 2.77193 | |

| (1.99e-2) | (6.74e-3) | (4.25e-3) | (3.26e-4) | |||

| 6 | 2.8129 | 2.7455 | 2.7191 | 2.7319 | 2.71838 | |

| (3.48e-2) | (9.96e-3) | (2.60e-4) | (4.97e-3) | |||

| 7 | 2.7988 | 2.7140 | 2.6913 | 2.7052 | ||

| 8 | 2.7841 | 2.6908 | 2.6718 | |||

| 9 | 2.7720 | 2.6690 | 2.6553 | |||

| 10 | 2.7599 | 2.6498 | 2.6428 | |||

| 11 | 2.7472 | 2.6331 | 2.6334 | |||

| 12 | 2.7345 | 2.6210 | 2.6256 | |||

| Sparse grid interpolation level | |||||||

| 3 | 4 | 5 | 6 | 7 | |||

| 2 | 2.9489 | 3.1880 | 3.1880 | 3.1839 | 3.1831 | 3.18310 | 3.18469 |

| (7.36e-2) | (1.53e-3) | (1.55e-3) | (2.51e-4) | (1.43e-5) | |||

| 3 | 2.9130 | 3.0226 | 3.0060 | 3.0029 | 3.0030 | 3.00299 | 3.00448 |

| (3.00e-2) | (6.53e-3) | (9.96e-4) | (1.67e-5) | (8.59e-6) | |||

| 4 | 2.9028 | 2.9314 | 2.9103 | 2.9088 | 2.90836 | 2.90980 | |

| (1.91e-3) | (7.94e-3) | (6.75e-4) | (1.42e-4) | ||||

| 5 | 2.8963 | 2.8716 | 2.8514 | 2.8505 | 2.84994 | 2.85135 | |

| (1.63e-2) | (7.60e-3) | (5.03e-4) | (2.00e-4) | ||||

| 6 | 2.8889 | 2.8283 | 2.8110 | 2.8107 | 2.81026 | 2.81165 | |

| (2.80e-2) | (6.40e-3) | (2.74e-4) | (1.65e-4) | ||||

| 7 | 2.8810 | 2.7955 | 2.7817 | 2.7817 | 2.78155 | ||

| (3.57e-2) | (5.03e-3) | (4.95e-5) | (6.93e-5) | ||||

| 8 | 2.8725 | 2.7718 | 2.7599 | 2.75980 | |||

| (4.08e-2) | (4.34e-3) | (3.47e-5) | |||||

| 9 | 2.8631 | 2.7505 | 2.7428 | 2.74275 | |||

| (4.39e-2) | (2.84e-3) | (3.37e-5) | |||||

| 10 | 2.8525 | 2.7320 | 2.7292 | 2.72904 | |||

| (4.52e-2) | (1.08e-3) | (6.66e-5) | |||||

| 11 | 2.8412 | 2.7154 | 2.7180 | 2.71776 | |||

| (4.54e-2) | (8.79e-4) | (8.83e-5) | |||||

| 12 | 2.8294 | 2.7000 | 2.7085 | 2.70832 | |||

| (4.47e-2) | (3.09e-3) | (7.74e-5) | |||||

| 13 | 2.8175 | 2.6855 | 2.70031 | ||||

| (4.34e-2) | (5.47e-3) | ||||||

| 14 | 2.8043 | 2.6720 | 2.69342 | ||||

| (4.12e-2) | (7.95e-3) | ||||||

| 15 | 2.7910 | 2.6597 | 2.68743 | ||||

| (3.85e-2) | (1.03e-2) | ||||||

| 16 | 2.7784 | 2.6502 | 2.68218 | ||||

| (3.59e-2) | (1.19e-2) | ||||||

5.2 Convergence of interpolation for Bermudan options

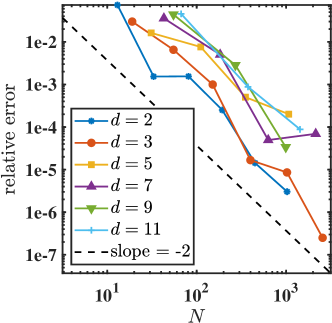

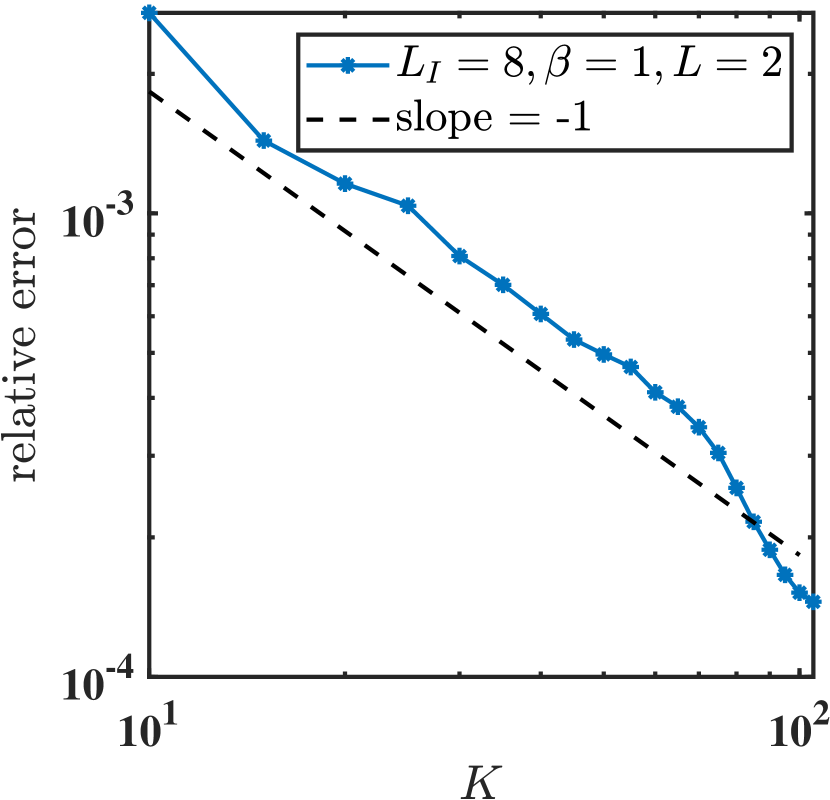

To verify the convergence rate of the SGPI, we consider -times exercisable Bermudan basket put option on the geometric average of assets. To avoid the influence of quadrature errors, sparse grid quadrature with level Genz-Keister knots is applied to ensure the small approximation errors. Fig. 3 shows the convergence for different dimension . These plots show that for a fixed number of inner sparse grids , the relative error do increase with the dimension , but the convergence rate is nearly independent of the dimension, confirming the theoretical prediction in Section 4.

5.3 Comparison of quadrature

Now we showcase the performance of Algorithm 1 with different quadrature methods, to demonstrate the flexibility of high-dimensional quadrature rules. Since the pointwise evaluations on the inner sparse grids for interpolation are obtained via quadrature methods, cf. Section 3.3, we present the error of the pricing with three kinds of sparse grid quadrature, the random quasi-Monte Carlo (RQMC) method with scramble Sobol sequence, and the state-of-art preintegration strategy for the integrand with ’kinks’ (discontinuity of gradient).

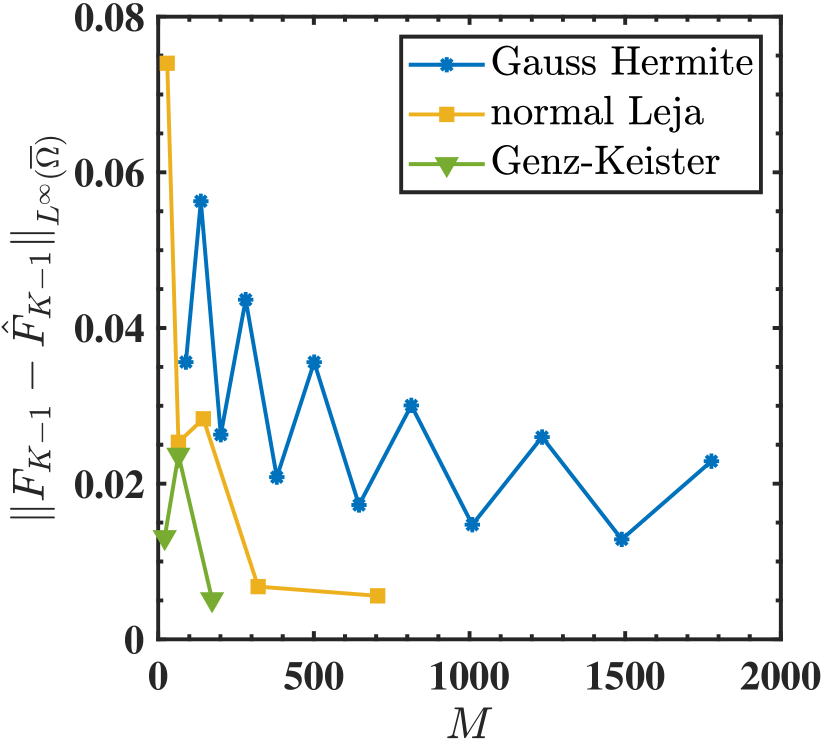

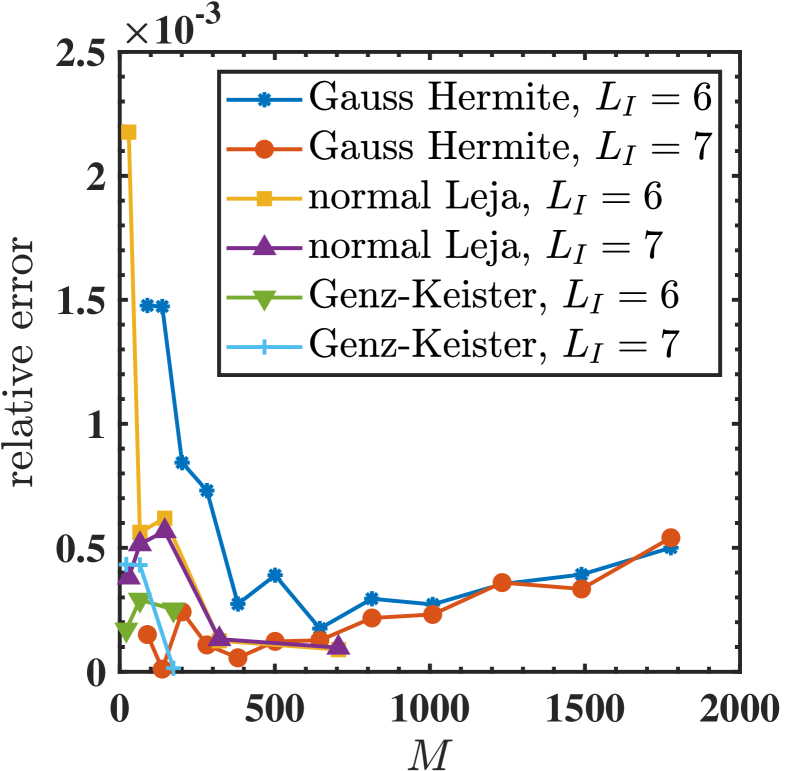

Sparse grid quadrature: We first show the relative errors of pricing using (3.13) in Fig. 4b, for three types of sparse grids, i.e., Gauss-Hermite, Genz-Keister, and normal Leja points for integration with respect to the Gaussian density. The theoretical convergence of the sparse grid quadrature are limited to functions with bounded mixed derivatives, which is not satisfied by defined in (3.10). Nonetheless, the success of sparse grid quadrature for computing risk-neutral expectations has been observed in the literatures [13, 21, 28]. Fig. 4a shows the -error of approximating by sparse grid quadrature, where the exact values correspond to the price of European options with expiration time . We observe that the quadrature errors in Fig. 4a seems much larger than the relative errors shown in Fig. 4b, which seems impausible at the first glance since the latter is poluted by many errors including the former. We find that the quadrature errors are large only near the free interface, which is a -dimensional manifold in the -dimensional problem, and hence do not result in a heavy impact on the relative errors depicted in Fig. 4b.

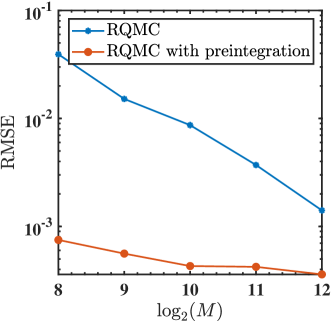

RQMC and RQMC with preintegration: To show the convergence with respect to the number of quadrature points , we use randomized quasi-Monte Carlo (RQMC) with the scramble Sobol sequence for quadrature. QMC and RQMC have been widely applied to option pricing problems for computing high-dimensional integrals [23, 32, 37]. The max function in (3.10) introduces a ’kink’, which decreases the efficiency of sparse grid quadrature or QMC. For functions with ’kinks’, the preintegration strategy or conditional sampling are developed [25, 35]. Fig. 5 shows the root mean square error (RMSE) of Bermudan option pricing with respect to the number of quadrature points in a -d problem, where we use independent replicates to estimate RMSE by .

5.4 Robustness

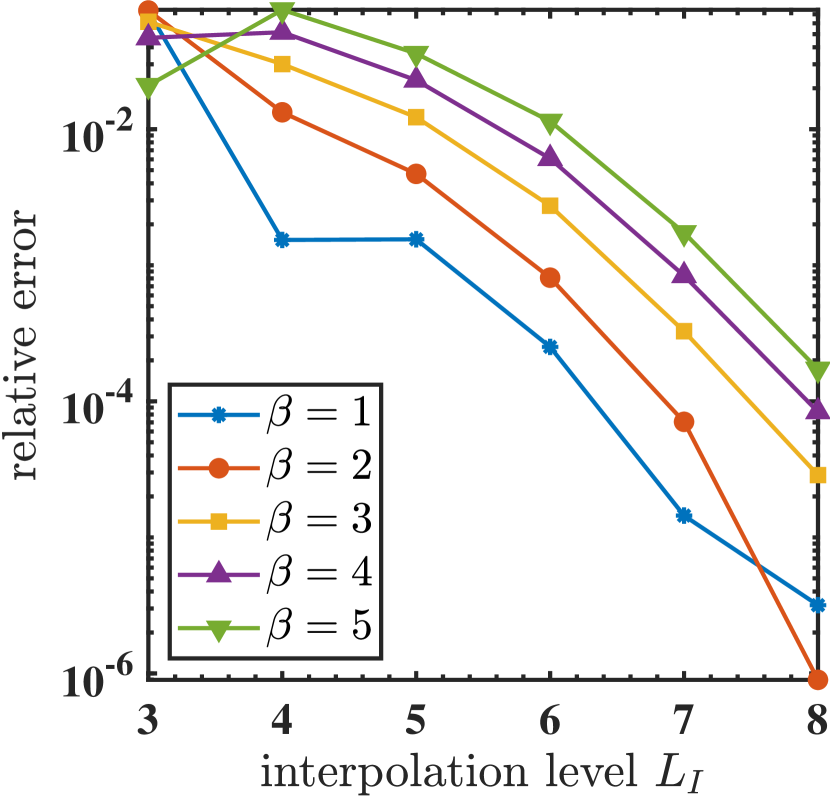

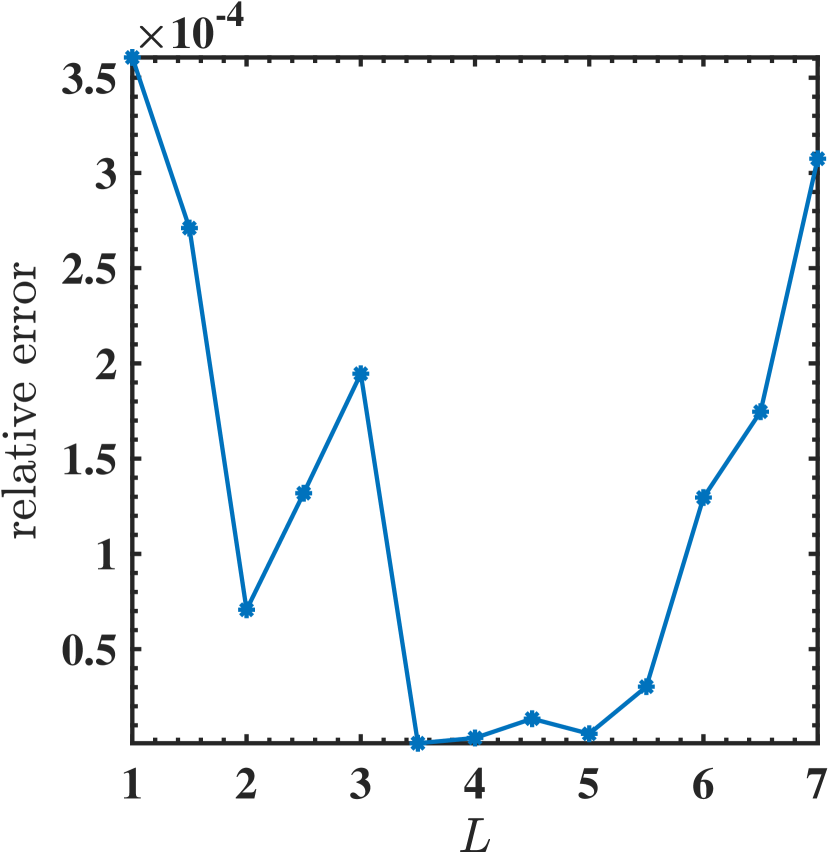

To test the robustness of Algorithm 1, we repeat the experiments for various values of the parameter occurred in the definition of the bubble function (3.4), the scale parameter introduced in the scaled map (3.1), and the number of time steps . The corresponding results are shown in Fig. 6(a), Fig. 6(b), and Fig. 6(c). We test with the example of pricing Bermudan or American geometric basket put options, where the prices are listed in Table 2.

Fig. 6(a) shows the convergence of relative errors for . Theoretically we have only provided the upper bounds of and in Theorem 2. The relative errors with respect to the chosen scale parameter are displayed in Fig. 6(b). The smallest relative error is observed for . In practice, as mentioned in Section 3.1, the parameter is determined such that the transformed interpolation points are distributed alike to the asset prices. Theorem 2 implies that the scale parameter should not be too small, and Proposition 1 implies that should not be too large.

The time discretization always arises when using the price of -times exercisable Bermudan option to approximate the American price. For the equidistant time step , it is widely accepted that the Bermudan price approaches the American price as with a convergence rate . For one single underlying asset, this convergence rate was shown in [29] for the Black Scholes model. A similar convergence rate has been observed in [44] and [18] for Lévy models. In almost all pricing schemes based upon the dynamic programming, a more accurate price can be obtained with more exercise dates (but at a higher computational cost). One general approach to alleviate the cost but still guarantee the accuracy is to apply the Richardson extrapolation [22, 16]. Fig. 6(c) present the convergence of Bermudan price to American price as increases using Algorithm 1.

6 Conclusions

In this work, we have developed a novel quadrature and sparse grid interpolation based algorithm for pricing American options with many underlying assets. Unlike most existing methods, it does not involve introducing artificial boundary data by avoiding truncating the computational domain, and that a significant reduction of the number of grid points by introducing a bubble function. The resulting multivariate function has been shown to have bounded mixed derivatives. Numerical experiments for American basket put options with the number of underlying assets up to 16 demonstrate excellent accuracy of the approach. Future work includes pricing max-call options for multiple underlying assets, which are benchmark test cases for high-dimensional American options. Max-call options pose computational challenges due to their unboundedness and thus require certain special treatment.

References

- [1] Y. Achdou and O. Pironneau, Computational methods for option pricing, SIAM, 2005.

- [2] N. I. Achieser, Theory of approximation, Courier Corporation, 2013.

- [3] R. Adams and J. Fournier, Sobolev spaces, Elsevier, 2003.

- [4] K. Amin and A. Khanna, Convergence of american option values from discrete- to continuous-time financial models, Mathematical Finance, 4 (1994), pp. 289–304.

- [5] L. Andersen and M. Broadie, Primal-dual simulation algorithm for pricing multidimensional american options, Management Science, 50 (2004), pp. 1222–1234.

- [6] V. Barthelmann, E. Novak, and K. Ritter, High dimensional polynomial interpolation on sparse grids, Advances in Computational Mathematics, 12 (2000), pp. 273–288.

- [7] C. Bayer, C. Ben Hammouda, and R. Tempone, Numerical smoothing with hierarchical adaptive sparse grids and quasi-monte carlo methods for efficient option pricing, Quantitative Finance, (2021), pp. 1–19.

- [8] A. Bensoussan, On the theory of option pricing, Acta Applicandae Mathematica, 2 (1984), pp. 139–158.

- [9] A. Bensoussan and J.-L. Lions, Applications of variational inequalities in stochastic control, Elsevier, 2011.

- [10] J. Boyd, Chebyshev and Fourier spectral methods, Courier Corporation, 2001.

- [11] P. Boyle, A lattice framework for option pricing with two state variables, Journal of financial and quantitative analysis, 23 (1988), pp. 1–12.

- [12] M. Brennan and E. Schwartz, The valuation of american put options, The Journal of Finance, 32 (1977), pp. 449–462.

- [13] H.-J. Bungartz and S. Dirnstorfer, Multivariate quadrature on adaptive sparse grids, Computing, 71 (2003), pp. 89–114.

- [14] H.-J. Bungartz and M. Griebel, Sparse grids, Acta numerica, 13 (2004), pp. 147–269.

- [15] H.-J. Bungartz, A. Heinecke, D. Pflüger, and S. Schraufstetter, Option pricing with a direct adaptive sparse grid approach, Journal of Computational and Applied Mathematics, 236 (2012), pp. 3741–3750.

- [16] C.-C. Chang, S.-L. Chung, and R. Stapleton, Richardson extrapolation techniques for the pricing of american-style options, Journal of Futures Markets: Futures, Options, and Other Derivative Products, 27 (2007), pp. 791–817.

- [17] J. Cox, S. Ross, and M. Rubinstein, Option pricing: A simplified approach, Journal of financial Economics, 7 (1979), pp. 229–263.

- [18] F. Fang and C. Oosterlee, Pricing early-exercise and discrete barrier options by fourier-cosine series expansions, Numerische Mathematik, 114 (2009), p. 27.

- [19] G. Folland, Real analysis: modern techniques and their applications, vol. 40, John Wiley & Sons, 1999.

- [20] P. Forsyth and K. Vetzal, Quadratic convergence for valuing american options using a penalty method, SIAM Journal on Scientific Computing, 23 (2002), pp. 2095–2122.

- [21] T. Gerstner, Sparse grid quadrature methods for computational finance, Habilitation, University of Bonn, 77 (2007).

- [22] R. Geske and H. Johnson, The american put option valued analytically, The Journal of Finance, 39 (1984), pp. 1511–1524.

- [23] M. Giles, F. Kuo, I. Sloan, and B. Waterhouse, Quasi-monte carlo for finance applications, ANZIAM Journal, 50 (2008), pp. C308–C323.

- [24] K. Glau, M. Mahlstedt, and C. Potz, A new approach for american option pricing: The dynamic chebyshev method, SIAM Journal on Scientific Computing, 41 (2019), pp. B153–B180.

- [25] A. Griewank, F. Kuo, H. Leövey, and I. Sloan, High dimensional integration of kinks and jumps—smoothing by preintegration, Journal of Computational and Applied Mathematics, 344 (2018), pp. 259–274.

- [26] J. Guyon and P. Henry-Labordere, Nonlinear option pricing, CRC Press, 2013.

- [27] M. Haugh and L. Kogan, Pricing american options: a duality approach, Operations Research, 52 (2004), pp. 258–270.

- [28] M. Holtz, Sparse grid quadrature in high dimensions with applications in finance and insurance, vol. 77, Springer Science & Business Media, 2010.

- [29] S. Howison and M. Steinberg, A matched asymptotic expansions approach to continuity corrections for discretely sampled options. part 1: Barrier options, Applied Mathematical Finance, 14 (2007), pp. 63–89.

- [30] W. Hu and T. Zastawniak, Pricing high-dimensional american options by kernel ridge regression, Quantitative Finance, 20 (2020), pp. 851–865.

- [31] P. Jaillet, D. Lamberton, and B. Lapeyre, Variational inequalities and the pricing of american options, Acta Applicandae Mathematicae, 21 (1990), pp. 263–289.

- [32] C. Joy, P. Boyle, and K. S. Tan, Quasi-monte carlo methods in numerical finance, Management science, 42 (1996), pp. 926–938.

- [33] P. Kovalov, V. Linetsky, and M. Marcozzi, Pricing multi-asset american options: A finite element method-of-lines with smooth penalty, Journal of Scientific Computing, 33 (2007), pp. 209–237.

- [34] F. Kuo and D. Nuyens, A practical guide to quasi-monte carlo methods, 2016.

- [35] S. Liu and A. B. Owen, Preintegration via active subspace, SIAM Journal on Numerical Analysis, 61 (2023), pp. 495–514.

- [36] F. Longstaff and E. Schwartz, Valuing american options by simulation: a simple least-squares approach, The review of financial studies, 14 (2001), pp. 113–147.

- [37] P. L’Ecuyer, Quasi-monte carlo methods with applications in finance, Finance and Stochastics, 13 (2009), pp. 307–349.

- [38] H. McKean, Appendix: A free boundary problem for the heat equation arising from a problem in mathematical economics, Industrial Management Review, 6 (1965), p. 32. Last updated - 2013-02-24.

- [39] R. Merton, Option pricing when underlying stock returns are discontinuous, Journal of financial economics, 3 (1976), pp. 125–144.

- [40] B. F. Nielsen, O. Skavhaug, and A. Tveito, Penalty methods for the numerical solution of american multi-asset option problems, Journal of Computational and Applied Mathematics, 222 (2008), pp. 3–16.

- [41] E. Novak and K. Ritter, Simple cubature formulas with high polynomial exactness, Constructive approximation, 15 (1999), pp. 499–522.

- [42] G. Peskir and A. Shiryaev, Optimal stopping and free-boundary problems, Springer, 2006.

- [43] C. Piazzola and L. Tamellini, The Sparse Grids Matlab kit - a Matlab implementation of sparse grids for high-dimensional function approximation and uncertainty quantification, ArXiv, (2023).

- [44] S. Quecke, Efficient numerical methods for pricing American options under Lévy models, PhD thesis, Universität zu Köln, 2007.

- [45] C. Reisinger and G. Wittum, Efficient hierarchical approximation of high-dimensional option pricing problems, SIAM Journal on Scientific Computing, 29 (2007), pp. 440–458.

- [46] S. Scheidegger and A. Treccani, Pricing american options under high-dimensional models with recursive adaptive sparse expectations, Journal of Financial Econometrics, 19 (2021), pp. 258–290.

- [47] M. Sullivan, Valuing american put options using gaussian quadrature, The Review of Financial Studies, 13 (2000), pp. 75–94.

- [48] J. Tsitsiklis and B. Van Roy, Regression methods for pricing complex american-style options, IEEE Transactions on Neural Networks, 12 (2001), pp. 694–703.

- [49] P. van Moerbeke, Optimal stopping and free boundary problems, The Rocky Mountain Journal of Mathematics, 4 (1974), pp. 539–578.

- [50] G. Wasilkowski and H. Wozniakowski, Explicit cost bounds of algorithms for multivariate tensor product problems, Journal of Complexity, 11 (1995), pp. 1–56.

- [51] G. Zhang, Exotic options: a guide to second generation options, World scientific, 1997.

- [52] Y.-L. Zhu and J. Li, Multi-factor financial derivatives on finite domains, Communications in Mathematical Sciences, 1 (2003), pp. 343–359.