Adaptive Pricing in Unit Commitment Under Load and Capacity Uncertainty

Abstract

The increase of renewables in the grid and the volatility of the load create uncertainties in the day-ahead prices of electricity markets. Adaptive robust optimization (ARO) and stochastic optimization have been used to make commitment and dispatch decisions that adapt to the load and capacity uncertainty. These approaches have been successfully applied in practice but current pricing approaches used by US Independent System Operators (marginal pricing) and proposed in the literature (convex hull pricing) have two major disadvantages: a) they are deterministic in nature, that is they do not adapt to the load and capacity uncertainty, and b) require uplift payments to the generators that are typically determined by ad hoc procedures and create inefficiencies that motivate self-scheduling. In this work, we extend pay-as-bid and uniform pricing mechanisms to propose the first adaptive pricing method in electricity markets that adapts to the load and capacity uncertainty, eliminates post-market uplifts and deters self-scheduling, addressing both disadvantages.

Index Terms:

Pricing, Robust Optimization, Adaptive Optimization, Unit Commitment, Energy Markets, UncertaintyI Introduction

The future of electricity markets is expected to prominently feature renewable energy sources, which bring volatility and unpredictability to the markets [1, 2]. With the increase of wind and solar power comes an increase in the price volatility, among other things, which creates issues for both the market operators and the market participants. Specifically, [3] shows that as the penetration of wind power increases, the market-clearing price becomes more volatile and uncertain, making it difficult for wind power producers to forecast and bid their power accurately. In addition, changes are also expected on the consumer side. For example, the introduction of electric vehicles could change demand patterns as well as available storage options [4, 5]. Also, consumers could simultaneously play the role of producers thereby becoming \sayprosumers [6, 7, 8].

So far, most energy markets do not directly address these challenges as they have been set up using deterministic approaches [9]. However, there has been recent work in robust and stochastic optimization with promising results in addressing the unit commitment (UC) problem under uncertainty [10, 11, 12, 13, 14]. Adaptive robust optimization (ARO) minimizes the cost under the worst-case scenario in an uncertainty set, while stochastic optimization accounts for the probability distribution of the uncertain parameters by minimizing the expected cost. In general, ARO has been used to protect against different types of uncertainty, from contingencies and demand planning to wind energy output and has lower average dispatch and total costs, indicating better economic efficiency and significantly reduces the volatility of the total costs [10]. In [10], the authors use ARO to find solutions in the UC problem that are robust to uncertain nodal injections. This work is extended in [11], which deals with multistage UC and dynamic uncertainty sets related to the capacity of renewable energy sources. The authors of [12] also address wind uncertainty. They propose a distributionally robust approach, where they define a family of wind power distributions and minimize the expected cost under the worst-case distribution. Our approach is based on ARO but there has also been promising work on stochastic optimization. See [13, 15] for an introduction to these methods.

While the previous approaches have been successful in dealing with the volatility in energy systems and markets, the pricing methods available are still mostly deterministic [16, 17]. One of the more popular schemes is uniform marginal-cost pricing or \sayIP pricing, which may result in losses for some generators [18, 19]. Therefore, side-payments or uplifts are provided to these generators to make them whole, which may modify their incentives. Alternative mechanisms have been proposed, including removing the negative uplifts, such that no generator incurs a loss, and raising the commodity price above marginal cost to reduce uplifts [20, 21]. One principled version of that is the \sayconvex hull pricing scheme, which minimizes the uplifts by langragifying the energy balance constraint and maximizing over its dual price [22, 23]. Possibly only [24] and [25] discuss pricing in robust UC. However, they do not use ARO and [25] does not offer extended theoretical results. For a detailed review of the pricing methods, see [26].

Current pricing approaches used by Independent System Operators (ISOs) (marginal pricing) and proposed in the literature (convex hull pricing) have two major disadvantages: a) they are deterministic in nature, that is they do not adapt to the load and capacity uncertainty, and b) require uplift payments to the generators that are typically determined by ad hoc procedures and create inefficiencies that motivate self-scheduling. In contrast, we extend pay-as-bid and uniform pricing mechanisms to propose the first adaptive pricing method in electricity markets that adapts to the load and capacity uncertainty, eliminates post-market uplifts and deters self-scheduling, addressing both disadvantages.

I-A Contributions

In this work, we propose the first pricing method for ARO in energy markets with load and capacity uncertainty by offering contracts contingent to the uncertainty in the data of the day-ahead problem. We summarize the main contributions:

-

•

We introduce adaptive pay-as-bid and marginal pricing contracts for UC problems featuring load and capacity uncertainty. We specify fully the day-ahead payments and provide an upper-bound on the next-day or intra-day payments based on the day-ahead commitments. The payments are functions of the load and capacity uncertainty.

-

•

We show that the adaptive day-ahead pay-as-bid scheme is equivalent to the adaptive uniform pricing scheme. Also, if the worst-case uncertainty is realized in the next day, the forecasted intra-day payments are optimal and the generators are indifferent between the market schedule and their optimal schedule, eliminating self-scheduling.

-

•

We display the adaptive pricing in detail on the adaptive robust version of the Scarf example, see [18], and on realistic UC problems featuring ramp constraints. We compare it to deterministic marginal and convex hull pricing and find that adaptive pricing eliminates the corrections that are necessary in deterministic day-ahead problems.

The paper is organized as follows: in Section II, we introduce the ARO formulations for UC. In Section III, we present the adaptive pricing and its theoretical properties on UC with load and capacity uncertainty. In Section IV and in Section V we provide adaptive pricing on examples with load and capacity uncertainty. In Section VI, we demonstrate our method on a realistic example with ramp constraints and compare it to convex hull pricing. Finally, Section VII summarizes our conclusions.

The notation that we use is as follows: we use bold faced characters such as to represent vectors and capital letters such as to represent matrices. Also, denotes the transpose of the column vector and is the th unit vector. We define . The norm of a vector refers to the norm , the norm refers to and refers to .

II Adaptive Robust UC

In this section, we introduce the ARO formulation for an energy market robust to load and capacity uncertainty. The formulation is based on the popular Scarf example, see [18], but considers uncertainty in the load and capacity parameters. Reserves, transmission and ramp constraints can be added using linear constraints with small changes.

Consider the following example which tries to minimize the total cost of meeting a fixed level of demand.

|

|

We have generators, each with a turn-on cost of and a unit production cost of . The expected maximum production levels of generator are . We also have demand nodes, with expected demand or load at each node . The binary variable , if generator is turned on, otherwise . Note, the variable represents the dispatch of generator .

We can expand on this model by considering uncertainty in the load and in the capacity . In ARO, we describe the uncertainty in the parameters with an uncertainty set that contains all scenarios against which we want to be robust. Essentially, the constraints in our problem should be satisfied for all possible realizations of and in their uncertainty sets [27, 28, 29]. We consider uncertainty sets where the norm of the residuals from the expected load is at most and where the norm of residuals from the expected capacity is at most .

with corresponding to the budget, ellipsoidal and box uncertainty sets. The values of and control the conservativeness of our formulation [30].

In ARO, the second-stage decisions are functions of both uncertain parameters and the problem that minimizes the worst-case commitment and dispatch cost is

|

|

The optimization variable , called a decision rule, is in fact a vector function [29]. In this paper, to make the problem tractable, we restrict to linear functions or linear decision rules (LDR). Such a decision rule may not be optimal, because of the restriction to a certain class, but LDR have shown very good performance in practice and are optimal in many settings [31, 29, 32]. Alternatively, we can use decomposition schemes to learn the decision rule implicitly [10, 33].

Using LDR, the second-stage decisions are linear functions of the uncertain parameters . So, we have an -dimensional vector , an matrix , an matrix and or, for each , . The dispatch contains a non-adaptive part and an adaptive part that depends on and . We will use these terms for the rest of the paper. If we set and , the problem becomes an RO problem. Using LDR, the previous formulation is equivalent to

|

|

(1) |

where constraints involving hold for all and .

Let the objective function of Problem (1) be . The solution and satisfies the constraints for any realization of and of . For example, the second constraint ensures that the total production will be more than the total demand for all scenarios in the uncertainty sets. In addition, to make pricing more intuitive, we have included the third constraint, which ensures that the total non-adaptive dispatch is equal to the expected load. The previous formulation is equivalent to:

|

|

or, by using the robust counterpart with and , where is the dual norm of , and is the -th row of and is the -th row of ,

|

|

We are going to work with the following version of the previous formulation, because we want to use the dual problem as well. Following the example of [18], we also set the binary variables to their optimal values .

|

|

(2) |

where the right column contains the dual variables for the corresponding constraints. The Lagrangian of the previous problem is

|

|

By taking the minimum of the Lagrangian over the primal variables and then maximizing over the dual variables, we obtain the dual problem [34]. Note that if , otherwise it is . The same holds for the other similar terms in the Lagrangian. So, at optimality, for all ,

|

|

(3) |

|

|

(4) |

|

|

(5) |

|

|

(6) |

The corresponding dual problem is

|

|

(7) |

III Adaptive Pricing

In this section, we introduce adaptive pricing and provide its theoretical properties.

We suggest that the day-ahead payments include only the commitment and non-adaptive dispatch costs. So, the day-ahead payments reflect the cost of meeting the expected load while planning for the worst-case scenario. The adaptive part of the dispatch serves as an upper bound on the intra-day payments, which take place the following day based on the economic dispatch problems. This upper bound is also equal to the optimal intra-day payments, when the worst-case uncertainty is realized.

| Uncertainty Set | Pay-as-bid | Uniform | ||

|---|---|---|---|---|

| Budget | ||||

| Ellipsoidal | ||||

| Box |

Pay-as-bid pricing

The day-ahead payments to generator are based on their bids and the non-adaptive part of the dispatch. Specifically, each generator is paid

|

|

Marginal pricing

The price for the non-adaptive dispatch is and each generator is paid some uplift in a discriminatory way. So, each generator is paid

|

|

In contrast to deterministic pricing, we also price the uncertainty by introducing payments based on sizes and of the uncertainty sets. Note that if we set in the uncertainty set , we do not consider the capacity uncertainty. Table I summarizes the payments when there is only load uncertainty or . Similarly, if we set , we do not consider uncertainty in the load.

III-A Pay-As-Bid and Uniform Pricing Equivalence

One important theoretical property of our approach is that the day-ahead pay-as-bid and marginal pricing payments are the same. This result is presented more formally in the following theorem.

Theorem 1.

The pay-as-bid payment and the uniform price payment to each generator

|

|

are equal.

III-B Total Worst-Case Cost Equivalence

In the previous section, we considered only the day-ahead payments. In this section, we show that when the worst-case uncertainty is realized, the pay-as-bid and marginal pricing payments are the same. Let and be the worst case realization of the residual load and the residual capacity respectively for the objective function of Problem (1).

Theorem 2.

If the worst-case uncertainty is realized, then the total pay-as-bid payment to generator

and the uniform price payment to generator

are equal and satisfy , the optimal solution value of Problem (1).

Proof.

By complementary slackness between Problems (2) and (7), for all , we have

|

|

Also, using equations (5) and (6) and the constraints , , and of Problem (2), for all ,

|

|

So, for all , using the same complementary slackness conditions as Theorem 1,

|

|

Next, we show that

|

|

Using equation (3) and the constraints and of Problem (2) and of Problem (7),

|

|

and

|

|

Then, is the worst-case load uncertainty, because and is in the uncertainty set or by the constraints of Problem (7). Similarly, is the worst-case capacity uncertainty, because . Note, and may not be unique.

So, for all and . ∎

III-C Absence of Self-Scheduling

In this section, we show that when the worst-case uncertainty is realized, the generators are indifferent between the market schedule and their optimal dispatch, so they do not have an incentive to self-schedule. The ISO solves the \saycentralized Problem (2) and sets prices for the non-adaptive dispatch, and for the adaptive dispatch, and for the commitment. Also, each generator has commitment costs and dispatch costs . The cost of the adaptive dispatch is a linear function of and , as defined earlier and specified by the ISO. So, generator has revenue , while it has a cost . Each generator decides if they will self-schedule by maximizing the difference between the revenue and the costs. They solve the following \saydecentralized problem which maximizes their individual profit:

|

|

(8) |

The constraints are the robust counterparts of the capacity and non-negativity constraints for each , which means that the dispatch of the decentralized problem will be non-negative and less than the maximum capacity of generator for all and .

Let be the objective of the decentralized problem (8) for commitment and dispatch . Also, let be an optimal solution to the centralized problem (2) and be a solution to the decentralized problem (8) for generator . Generator has no incentive to self-schedule only if

Theorem 3.

Proof.

Let be the prices determined by the dual variables of the Problem (7). Using the results of Theorem 2, , because .

Consider ,

|

|

|

|

The first inequality is valid because , by the constraints of Problem (8) and and by Problem (7). The third inequality is valid because , , and by the constraints of Problem (7). Also, the second inequality is valid, because

|

|

|

|

|

|

|

|

by the dual norm properties and the constraints of Problem (7). Specifically, if are two -dimensional vectors, then and for all [34].

So, , i.e., no generator can obtain a solution giving a greater profit than the centralized solution. ∎

Also, are market-clearing or for all and , so the generators do not have incentive to self-schedule.

IV Example with load uncertainty

In this section, we demonstrate adaptive pricing in detail on the Scarf example with load uncertainty. The day-ahead payments and prices in the ARO problem are larger than those in the deterministic problem, because the commitments and dispatch are more conservative. However, the ARO approach reduces the need for ad hoc corrections, so the total cost may be significantly lower once the uncertainty is realized.

The Scarf example, after fixing the binary variables to their optimal values, is based on the following formulation

|

|

There are only two types of generators, whose costs and capacities are asymmetrical. Their characteristics are summarized in Table II.

| Type | |||

|---|---|---|---|

| 1 | 53 | 3 | 16 |

| 2 | 30 | 2 | 7 |

Suppose we have two generators of Type 1 and 6 generators of type 2. We also have five consumers with expected load , so the total expected load is .

The results for the deterministic problem are summarized in Table III.

-

•

Objective: $ 260,

-

•

Dual price of the load: 2 $ / unit.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| Commitment | 0 | 0 | 1 | 1 | 1 | 1 | 1 | 1 |

| Dispatch | 0 | 0 | 5 | 7 | 7 | 7 | 7 | 7 |

Table IV summarizes the pay-as-bid payments, which are for each .

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 30 | 30 | 30 | 30 | 30 | 30 | |

| 0 | 0 | 10 | 14 | 14 | 14 | 14 | 14 | |

| Payments | 0 | 0 | 40 | 44 | 44 | 44 | 44 | 44 |

The uniform price payments are for each , where is the dual variable of the constraint. They are are summarized in Table V. In general, is not the same as .

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| 0 | 0 | 10 | 14 | 14 | 14 | 14 | 14 | |

| Uplifts | 0 | 0 | 30 | 30 | 30 | 30 | 30 | 30 |

| Payments | 0 | 0 | 40 | 44 | 44 | 44 | 44 | 44 |

In the adaptive problem we also need to select the budget of uncertainty. Suppose we use a budget uncertainty set with , which means that we are protected from an increase of the expected demand from 40 to 60 or a decrease from 40 to 20. In this case, . The results for the ARO problem are summarized in Table VI.

-

•

Objective: $ 378,

-

•

Dual price of the load: 3 $ / unit.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| Commitment | 1 | 1 | 1 | 0 | 0 | 1 | 1 | 1 |

| 8 | 14.5 | 7 | 0 | 0 | 3.5 | 3.5 | 3.5 |

The LDR for each generator is . The matrix is

|

|

For each , is the same for all consumers , because the load bundles consumers together. This can change if we add different coefficients for each in the uncertainty set.

Table VII summarizes the day-ahead payments in an adaptive pay-as-bid scheme, where each generator is paid and the total payments are $ 328.5.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| 53 | 53 | 30 | 0 | 0 | 30 | 30 | 30 | |

| 24 | 43.5 | 14 | 0 | 0 | 7 | 7 | 7 | |

| Payments | 77 | 96.5 | 44 | 0 | 0 | 37 | 37 | 37 |

Table VIII summarizes the day-ahead payments in the adaptive marginal pricing scheme. They payments are the same as the pay-as-bid scheme. Note that the uplifts all less than the deterministic case for each generator of Type 2.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| 24 | 43.5 | 21 | 0 | 0 | 10.5 | 10.5 | 10.5 | |

| Uplifts | 53 | 53 | 23 | 0 | 0 | 26.5 | 26.5 | 26.5 |

| Payments | 77 | 96.5 | 44 | 0 | 0 | 37 | 37 | 37 |

Both the deterministic problem and the commitments and non-adaptive dispatch in the ARO problem try to meet a load of 40. However, the deterministic cost is $ 280, while the non-adaptive ARO cost is $ 328.5. This is because the ARO commitment is also feasible for an increase in the load up to 20, which is the worst-case scenario in our uncertainty set. The deterministic problem cannot meet such an increase, because Type 2 generators are used at capacity, except the first one, which can provide only two more units of power. To meet the demand of , we would need to turn on more generators the following day, which would be very costly and would require large payments.

IV-A Intra-day dispatch and payments

In this section, we consider the intra-day economic dispatch problem and the pricing implications of uncertain scenarios.

Suppose that the following day the uncertainty is realized, so the realized load is . We have made some commitments in the day-ahead market, so we can solve the following linear optimization problem (LP) to find the optimal dispatch, based on the new data.

|

|

where and are the solution for generator based on the ARO problem. So, we want to meet only the additional realized load , while we have already committed to produce to meet the expected load.

The intra-day electricity price is 2 for loads smaller than 10 and 3 for loads larger than 10, which is equal to the ARO price. Using ARO, we can provide the intra-day electricity price for all realizations of the uncertain parameters. As a result, the pricing is more transparent and predictable and the market participants can plan their bids.

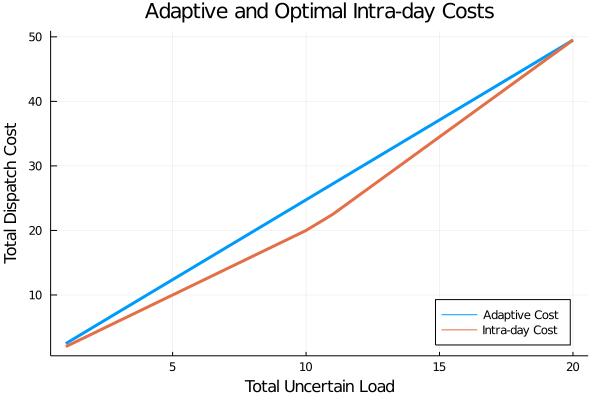

In Figure 1, we plot the cost of the LP and compare it to the adaptive part of the ARO cost . We gradually increase the total realized load from zero to , which is the worst-case scenario. The adaptive dispatch is an upper bound to the optimized intra-day dispatch. However, we have optimized for the worst-case uncertainty, so the adaptive problem and the LP will have the same cost, if the worst-case load is realized.

V Example with load and capacity uncertainty

We use the example of Section IV with uncertain load and consider the uncertainty in the capacity of each generator. Again, we set , which means that we are protected from a load increase from 40 to 60. Also, we choose , which means that we are protected from a decrease of the expected capacity from to for each generator . The results for the ARO problem are summarized in Table IX.

-

•

Objective: $ 402.25,

-

•

Dual price of the load: 3 $ / unit.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| Commitments | 1 | 1 | 1 | 1 | 1 | 1 | 1 | 0 |

| 8.0 | 8.0 | 3.5 | 3.5 | 3.5 | 6.75 | 6.75 | 0 |

The LDR is . The matrix is

|

|

The matrix is

|

|

Note that the sum of each column of is one and of is zero, because of the robust constraint . The norms are non-negative, so and .

Table X summarizes the day-ahead payments in a pay-as-bid scheme, where the total payments are $ 352.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| 53 | 53 | 30 | 30 | 30 | 30 | 30 | 0 | |

| 24 | 24 | 7 | 7 | 13.5 | 13.5 | 7 | 0 | |

| Payments | 77 | 77 | 37 | 37 | 43.5 | 43.5 | 37.0 | 0 |

Table XI summarizes the day-ahead payments in the adaptive marginal pricing scheme. The payments are the same as the pay-as-bid scheme. The uplifts for Type 2 generators are still smaller than the deterministic uplifts, while they are close to the adaptive uplifts with load uncertainty.

| Type | 1 | 1 | 2 | 2 | 2 | 2 | 2 | 2 |

|---|---|---|---|---|---|---|---|---|

| 24 | 24 | 10.5 | 10.5 | 20.25 | 20.25 | 10.5 | 0 | |

| Uplifts | 53 | 53 | 26.5 | 26.5 | 23.25 | 23.25 | 26.5 | 0 |

| Payments | 77 | 77 | 37 | 37 | 43.5 | 43.5 | 37.0 | 0 |

In this case, we also protect against drops in the available capacity, so we are more conservative. As a result, the prices and payments increase from $ 328.5 to $ 352. We turn on all generators, as the commitments in the deterministic problem and in the ARO problem with load capacity are not robust to a decrease of 0.5 in the capacity of the generators.

VI Multiperiod Pricing

In this section, we present our method on a realistic multiperiod formulation with ramp constraints and compare it to deterministic marginal and convex hull pricing. Again, the ARO commitments and dispatch are more conservative, so there is an increase in the payments and the prices compared to the deterministic case. However, there are no uplifts related to optimality gaps that are present in convex hull pricing.

Consider the following example by Chen et al. [35], which includes two generators and a 3-hour horizon with expected load 95, 100, and 130 MW. G1 has a maximum of 100 MW, and energy offer /MWh. G2 has a 20 MW minimum, 35 MW maximum, energy offer /MWh, start-up cost , no-load cost , ramp rate 5 MW/hour, start-up rate 22.5 MW/hour, shut-down rate 35 MW/hour, minimum up/down times of one hour, and is initially offline. The UC formulation is provided below.

|

|

with and representing the status, start-up and shut-down variables respectively. The results for the deterministic problem are summarized in Table XII. We turn on G2 at and both generators are on for all time periods. The objective is $ 7340 and the electricity price is $ / MW.

| Generator | 1 | 2 |

|---|---|---|

| Dispatch | [75, 75, 100] | [20, 25, 30] |

The convex hull payments are summarized in Table XIII. The convex hull prices are $ / MW, so G1 is paid 2500, while G2 is paid 4445 and an uplift of 365 [23].

| Generator | 1 | 2 |

|---|---|---|

| [750, 750, 27600] | [200, 250, 8250] | |

| Uplifts | -26600 | -4255 |

| Payments | 2500 | 4445 |

The objective of the convex hull method is 365 less than the optimal objective, because of the duality gap. So, there is an additional uplift of 365 that is paid to G2.

The deterministic pay-as-bid payments are summarized in Table XIV. They are are the same as the convex hull payments but do not feature a duality gap. In addition, these payments are equivalent to a marginal pricing scheme by [18].

| Generator | 1 | 2 |

|---|---|---|

| Commitment Cost | [0, 0, 0] | [1030, 30, 30] |

| Dispatch Cost | [750, 750, 1000] | [1000, 1250, 1500] |

| Total Cost | [750, 750, 1000] | [2030, 1280, 1530] |

| Payments | 2500 | 4840 |

In the ARO problem we use budget uncertainty sets with and at each time period. The objective increases to $ 7860 and the electricity price is $ / MW. Again, we turn on G2 at and both generators are on for all time periods.

| Generator | 1 | 2 |

|---|---|---|

| Dispatch | [72.5, 72.5, 97.5] | [22.5, 27.5, 32.5] |

The LDR is . The non-adaptive dispatch results are summarized in Table XV. The matrix at each time period is

|

|

with the rows corresponding to the G1 and G2 and the columns corresponding to three consumers that share the load. Also, contains only zeros.

The day-ahead payments to the generators are $ 7640. They pay-as-bid payments are summarized in Table XVI and each generator is paid , where the coefficients correspond to the commitment and dispatch costs.

| Generator | 1 | 2 |

|---|---|---|

| Commitment Cost | [0, 0, 0] | [1030, 30, 30] |

| Dispatch Cost | [725, 725, 975] | [1125, 1375, 1625] |

| Total Cost | [725, 725, 975] | [2155, 1405, 1655] |

| Payments | 2425 | 5215 |

The adaptive marginal price payments are summarized in Table XVII.

| Generator | 1 | 2 |

|---|---|---|

| [725, 725, 12675] | [225, 275, 4225] | |

| Uplifts | -11700 | 490 |

| Payments | 2425 | 5215 |

The non-adaptive dispatch in the ARO problem and the dispatch in the deterministic problem try to meet the same level of demand, namely [95, 100, 130]. However, the cost is higher in the ARO problem, because we protect against uncertainty in the load and in the capacity. For example, the commitments and dispatch are still feasible for a drop of [0, 7.5, 0.5] in the capacity of each generator and an increase of [10, 10, 2] in the load. So, the payments to the generators and the price of electricity are higher compared to the deterministic case. In addition, the adaptive payment mechanisms we use do not feature a duality gap.

VII Conclusion

In this work, we introduce the first pay-as-bid and marginal pricing methods for energy markets with non-convexities under uncertainty. We consider ARO formulations that protect against uncertainty in the load and capacity parameters and we provide the corresponding adaptive pricing schemes. We apply our method to realistic examples with increasing degrees of complexity and show, both theoretically and empirically, that it eliminates uplifts and corrections that are necessary in deterministic approaches.

References

- [1] P. Pinson, “What may future electricity markets look like?,” Journal of Modern Power Systems and Clean Energy, 2023.

- [2] J. M. Morales, A. J. Conejo, H. Madsen, P. Pinson, and M. Zugno, Integrating renewables in electricity markets: operational problems, vol. 205. Springer Science & Business Media, 2013.

- [3] S. Oren, “When is a pay-as bid preferable to uniform price in electricity markets,” in IEEE PES Power Systems Conference and Exposition, pp. 1618–1620, IEEE, 2004.

- [4] M. Hannan, M. Mollik, A. Q. Al-Shetwi, S. Rahman, M. Mansor, R. Begum, K. Muttaqi, and Z. Dong, “Vehicle to grid connected technologies and charging strategies: Operation, control, issues and recommendations,” Journal of Cleaner Production, p. 130587, 2022.

- [5] K. M. Tan, V. K. Ramachandaramurthy, and J. Y. Yong, “Integration of electric vehicles in smart grid: A review on vehicle to grid technologies and optimization techniques,” Renewable and Sustainable Energy Reviews, vol. 53, pp. 720–732, 2016.

- [6] M. Khorasany, A. Paudel, R. Razzaghi, and P. Siano, “A new method for peer matching and negotiation of prosumers in peer-to-peer energy markets,” IEEE Transactions on Smart Grid, vol. 12, no. 3, pp. 2472–2483, 2020.

- [7] T. Morstyn, N. Farrell, S. J. Darby, and M. D. McCulloch, “Using peer-to-peer energy-trading platforms to incentivize prosumers to form federated power plants,” Nature energy, vol. 3, no. 2, pp. 94–101, 2018.

- [8] Z. Zhang, H. Tang, J. Ren, Q. Huang, and W.-J. Lee, “Strategic prosumers-based peer-to-peer energy market design for community microgrids,” IEEE Transactions on Industry Applications, vol. 57, no. 3, pp. 2048–2057, 2021.

- [9] L. Silva-Rodriguez, A. Sanjab, E. Fumagalli, A. Virag, and M. Gibescu, “Short term wholesale electricity market designs: A review of identified challenges and promising solutions,” Renewable and Sustainable Energy Reviews, vol. 160, p. 112228, 2022.

- [10] D. Bertsimas, E. Litvinov, X. A. Sun, J. Zhao, and T. Zheng, “Adaptive robust optimization for the security constrained unit commitment problem,” IEEE Transactions on Power Systems, vol. 28, no. 1, pp. 52–63, 2012.

- [11] A. Lorca, X. A. Sun, E. Litvinov, and T. Zheng, “Multistage adaptive robust optimization for the unit commitment problem,” Operations Research, vol. 64, no. 1, pp. 32–51, 2016.

- [12] P. Xiong, P. Jirutitijaroen, and C. Singh, “A distributionally robust optimization model for unit commitment considering uncertain wind power generation,” IEEE Transactions on Power Systems, vol. 32, no. 1, pp. 39–49, 2016.

- [13] Q. P. Zheng, J. Wang, and A. L. Liu, “Stochastic optimization for unit commitment—a review,” IEEE Transactions on Power Systems, vol. 30, no. 4, pp. 1913–1924, 2014.

- [14] R. Jiang, J. Wang, and Y. Guan, “Robust unit commitment with wind power and pumped storage hydro,” IEEE Transactions on Power Systems, vol. 27, no. 2, pp. 800–810, 2011.

- [15] S. S. Reddy, V. Sandeep, and C.-M. Jung, “Review of stochastic optimization methods for smart grid,” Frontiers in Energy, vol. 11, pp. 197–209, 2017.

- [16] G. Dutta and K. Mitra, “A literature review on dynamic pricing of electricity,” Journal of the Operational Research Society, vol. 68, no. 10, pp. 1131–1145, 2017.

- [17] N. Mazzi, J. Kazempour, and P. Pinson, “Price-taker offering strategy in electricity pay-as-bid markets,” IEEE Transactions on Power Systems, vol. 33, no. 2, pp. 2175–2183, 2017.

- [18] R. P. O’Neill, P. M. Sotkiewicz, B. F. Hobbs, M. H. Rothkopf, and W. R. Stewart Jr, “Efficient market-clearing prices in markets with nonconvexities,” European Journal of Operational Research, vol. 164, no. 1, pp. 269–285, 2005.

- [19] R. P. O’Neill, A. Castillo, B. Eldridge, and R. B. Hytowitz, “Dual pricing algorithm in iso markets,” IEEE Transactions on Power Systems, vol. 32, no. 4, pp. 3308–3310, 2016.

- [20] M. Bjørndal and K. Jörnsten, “Equilibrium prices supported by dual price functions in markets with non-convexities,” European Journal of Operational Research, vol. 190, no. 3, pp. 768–789, 2008.

- [21] F. D. Galiana, A. L. Motto, and F. Bouffard, “Reconciling social welfare, agent profits, and consumer payments in electricity pools,” IEEE Transactions on Power Systems, vol. 18, no. 2, pp. 452–459, 2003.

- [22] B. Hua and R. Baldick, “A convex primal formulation for convex hull pricing,” IEEE Transactions on Power Systems, vol. 32, no. 5, pp. 3814–3823, 2016.

- [23] P. Andrianesis, D. Bertsimas, M. C. Caramanis, and W. W. Hogan, “Computation of convex hull prices in electricity markets with non-convexities using dantzig-wolfe decomposition,” IEEE Transactions on Power Systems, vol. 37, no. 4, pp. 2578–2589, 2021.

- [24] H. Ye, Y. Ge, M. Shahidehpour, and Z. Li, “Uncertainty marginal price, transmission reserve, and day-ahead market clearing with robust unit commitment,” IEEE Transactions on Power Systems, vol. 32, no. 3, pp. 1782–1795, 2016.

- [25] X. Fang, B.-M. Hodge, E. Du, C. Kang, and F. Li, “Introducing uncertainty components in locational marginal prices for pricing wind power and load uncertainties,” IEEE Transactions on Power Systems, vol. 34, no. 3, pp. 2013–2024, 2019.

- [26] G. Liberopoulos and P. Andrianesis, “Critical review of pricing schemes in markets with non-convex costs,” Operations Research, vol. 64, no. 1, pp. 17–31, 2016.

- [27] A. Ben-Tal, L. El Ghaoui, and A. Nemirovski, Robust optimization, vol. 28. Princeton University Press, 2009.

- [28] D. Bertsimas, D. B. Brown, and C. Caramanis, “Theory and applications of robust optimization,” SIAM review, vol. 53, no. 3, pp. 464–501, 2011.

- [29] D. Bertsimas and D. den Hertog, Robust and adaptive optimization. Dynamic Ideas, 2022.

- [30] Y. Guan and J. Wang, “Uncertainty sets for robust unit commitment,” IEEE Transactions on Power Systems, vol. 29, no. 3, pp. 1439–1440, 2013.

- [31] S. Dehghan, N. Amjady, and A. J. Conejo, “Adaptive robust transmission expansion planning using linear decision rules,” IEEE Transactions on Power Systems, vol. 32, no. 5, pp. 4024–4034, 2017.

- [32] R. A. Jabr, “Linear decision rules for control of reactive power by distributed photovoltaic generators,” IEEE Transactions on Power Systems, vol. 33, no. 2, pp. 2165–2174, 2017.

- [33] B. Zeng and L. Zhao, “Solving two-stage robust optimization problems using a column-and-constraint generation method,” Operations Research Letters, vol. 41, no. 5, pp. 457–461, 2013.

- [34] D. P. Bertsekas, “Nonlinear programming,” Journal of the Operational Research Society, vol. 48, no. 3, pp. 334–334, 1997.

- [35] Y. Chen, R. P. O’Neill, and P. Whitman, “A unified approach to solve convex hull pricing and average incremental cost pricing with large system study,” tech. rep., Working Paper, 2020.