On Prediction Feature Assignment in the Heckman Selection Model

Abstract

Under missing-not-at-random (MNAR) sample selection bias, the performance of a prediction model is often degraded. This paper focuses on one classic instance of MNAR sample selection bias where a subset of samples have non-randomly missing outcomes. The Heckman selection model and its variants have commonly been used to handle this type of sample selection bias. The Heckman model uses two separate equations to model the prediction and selection of samples, where the selection features include all prediction features. When using the Heckman model, the prediction features must be properly chosen from the set of selection features. However, choosing the proper prediction features is a challenging task for the Heckman model. This is especially the case when the number of selection features is large. Existing approaches that use the Heckman model often provide a manually chosen set of prediction features. In this paper, we propose Heckman-FA as a novel data-driven framework for obtaining prediction features for the Heckman model. Heckman-FA first trains an assignment function that determines whether or not a selection feature is assigned as a prediction feature. Using the parameters of the trained function, the framework extracts a suitable set of prediction features based on the goodness-of-fit of the prediction model given the chosen prediction features and the correlation between noise terms of the prediction and selection equations. Experimental results on real-world datasets show that Heckman-FA produces a robust regression model under MNAR sample selection bias.

Index Terms:

sample selection bias, missing-not-at-random, Heckman selection model, robust linear regressionI Introduction

Regression is sensitive to dataset shift [16], where the training and testing sets come from different distributions. Dataset shift can arise due to sample selection bias, where a sample is non-uniformly chosen from a population for training a model. This type of bias can cause a subset of training samples to be partially observed, where any of the covariates or outcome of a sample is missing, or completely unobserved. Consequently, the performance of the model after training on this biased set will be degraded when the model is deployed. Most approaches such as [3], [13], and [19] handle the missing-at-random (MAR) setting, where the selection of training samples is assumed to be independent from the outcome given the observed variables in the training set. However, these approaches cannot properly account for the missing-not-at-random (MNAR) setting, where the selection of training samples is assumed to not be independent from the outcome given the observed variables in the training set.

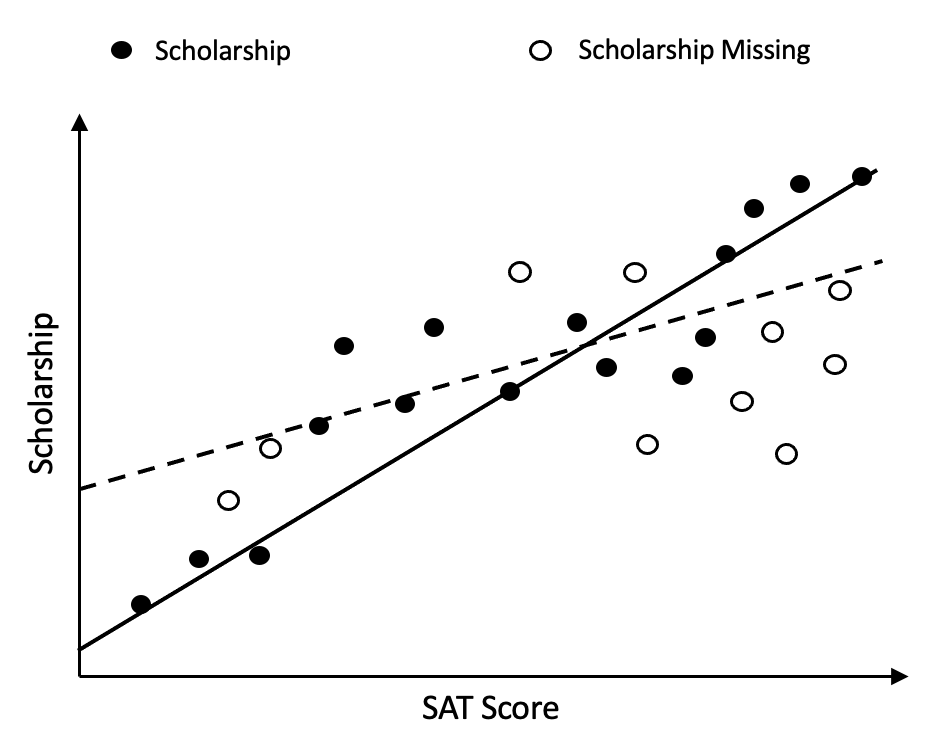

In this work, we focus on the problem of MNAR sample selection bias on the outcome. We provide an example of this bias scenario in Figure 1 by considering the relationship between SAT score (feature) and the amount of scholarship offered by a certain university (outcome), where some students have missing values of scholarship. There could be some hidden mechanism behind the missing outcomes. For instance, amounts of scholarship offered to students who have not declared their majors are not collected. When the undeclared students are omitted from the training, a biased model is produced and could be very different from the ground truth model that would have been trained had scholarship amounts of all students been collected. However, their feature information are available during training. In order for the trained model to be close to the ground truth model, we leverage the observed feature information of those records with missing outcomes in the training process.

The Heckman selection model [7] is a Nobel-Prize winning approach that addresses MNAR sample selection bias on the outcome. The method involves two equations: the prediction equation and the selection equation. The prediction equation describes the relationship between the covariates and the outcome of interest. The selection equation specifies the probability that a sample is selected in the training data. Estimation of the selection equation requires an exclusion restriction, where the selection equation includes one or more variables that are not included in the outcome equation. To handle MNAR sample selection bias on the outcome, the Heckman model considers the respective noise terms of the prediction and selection equations, which follow a bivariate normal distribution.

Although the presence of an exclusion restriction avoids multicollinearity for the prediction model [14], the process to identify a valid exclusion restriction is often difficult in practice. This is first due to the lack of clear theoretical knowledge on which selection features should be included in the prediction model [6]. Moreover, using the Heckman selection model with an invalid exclusion restriction can lead to non-robust regression on the biased training set [23]. Choosing from features that affect the selection, one way to address these challenges is to search through all combinations of selection features to find a suitable set of prediction features for the Heckman selection model. However, this search process becomes computationally expensive as we deal with a large number of selection features in real-world data.

| Notation | Description |

|---|---|

| size of | |

| () | training samples with observed (missing) outcome |

| , , | features, outcome, selection for th training sample |

| () | selection (prediction) features of a sample |

| () | number of selection (prediction) features |

| correlation coefficient between the noise terms | |

| assignment function | |

| categorical sample matrix | |

| probability of (not) assigning th selection feature | |

| number of training epochs | |

| number of Gumbel-Softmax samples (extraction) |

I-A Problem Formulation

We provide a list of important symbols used throughout the paper in Table I. In our work, we generally use unbolded letters to denote scalars, bold lower-case letters to denote vectors, and bold upper-case letters to denote matrices. For accented letters, we use a hat to denote estimations, tilde to denote approximations, and underline to denote augmented vectors or matrices. As exceptions to these conventions, we use to denote the th column of any matrix and to denote the probability matrix.

We let be the feature space and be the continuous target attribute. We also denote as the training set of samples that are originally sampled from the population to be modeled yet biased under MNAR sample selection bias. We define each sample as

| (1) |

where the binary variable indicates whether or not is observed. We define as the set containing the first training samples where each sample is fully observed and as the set that contains the remaining training samples with unobserved outcome.

Definition I.1 (MNAR Sample Selection)

Missing-not-at-random (MNAR) sample selection occurs for a sample if is not independent of given , i.e. .

MNAR means that both the probability of data missingness and the value of missing observations are affected by unobserved variables. For the Heckman model, the selection mechanism models the missingness of in terms of a set of selection features. Thus the following assumptions are additionally made in this work:

-

(i)

For all , consists of every prediction feature and additional features that do not affect the outcome. The selection features can be specified by domain users or simply learned via goodness-of-fit as all feature information are available in the training data.

-

(ii)

Given selection features of the th training sample, is approximated by computing .

Problem Statement. To perform regression, a linear model with prediction features and parameters is fitted by learning to minimize a loss function over . Given that is biased due to MNAR sample selection, we seek to choose prediction features from a set of selection features using an assignment function . Based the extracted assignment of prediction features, a model is fitted after running the Heckman model, where denotes the extracted prediction features augmented with the inverse Mills ratio (IMR) and denotes the Heckman coefficients.

I-B Contributions

In this work, we present the Heckman selection model with Feature Assignment (Heckman-FA) as a framework that finds a suitable assignment of prediction features for the Heckman model to robustly handle MNAR sample selection bias on the outcome. The core contributions of our work are summarized as follows. First, Heckman-FA trains an assignment function that determines whether a selection feature is assigned as a prediction feature or not. The assignment function is defined in terms of samples from the Gumbel-Softmax distribution [9]. Second, using the parameters of the trained assignment function, Heckman-FA extracts the set of prediction features for the Heckman model based on goodness-of-fit and the correlation between the noise terms of the prediction and selection equations. Third, we apply our method to real-world datasets and compare the performance of Heckman-FA against other regression baselines. We empirically show that Heckman-FA produces robust prediction models against MNAR sample selection bias and outperforms these regression baselines.

II Related Work

II-A Incorporating the Heckman Selection Model

The Heckman selection model has been widely utilized to handle MNAR sample selection bias in different applications. For example, [2] evaluated the utility of the Heckman selection model in criminology by testing the method on sentencing data. In epidemiology, [1] proposed a Heckman-type selection model to account for HIV survey nonparticipation and HIV status. Variants of the Heckman selection model have also been proposed (see a comprehensive survey [21]). In the area of fair machine learning, [4] applied the Heckman model to correct MNAR sample selection bias while achieving fairness for linear regression models. Very recently, [10] extended the Heckman model to model multiple domain-specific sample selection mechanisms and proposed to jointly learn the prediction model and the domain selection model to achieve generalization on the true population. For approaches that incorporate the Heckman selection model and its variants, the prediction features are manually chosen beforehand. Our work makes a data-driven choice for the prediction features based on a trained feature assignment function.

Empirical analysis has often been used to examine the effect of exclusion restrictions on the performance of the Heckman selection model. [14] conducted Monte Carlo experiments with and without exclusion restrictions and found that the Heckman model is susceptible to collinearity issues in the absence of exclusion restrictions. Recently, [23] conducted a simulation showing that naive ordinary least squares (OLS) on the biased training set outperforms the Heckman model based approaches that do not have a valid exclusion restriction.

For the Heckman selection model, the correlation between the two noise terms carries information about the sample selection process. Because the noise terms are unobserved, the true value of the correlation is unknown. [6] used a range of values for the correlation to derive uncertainty intervals for the parameters of the prediction model. In our work, we also consider a range of values for the correlation. However, rather than defining the range of correlation values for a fixed set of prediction features, we specify the range of correlation values as we dynamically assign prediction features for the Heckman selection model.

The idea of variable assignment based on reparametrized random samples has also been explored in previous work. For instance, [15] proposed to train an assignment function that maps each latent variable to some causal factor as part of learning a causal representation. Similar to our work, the assignment function is trained by sampling an assignment from the Gumbel-Softmax distribution. In our work, however, we do not map variables to causal factors. Instead, we map each variable to a value that indicates whether or not the variable is assigned as a feature for the predictive model.

II-B Learning under Biased Training Data

Machine learning on missing training data has been well-studied. There are a number of techniques that handle MAR sample selection bias in the training set. Importance weighting [20] is commonly used to handle the MAR setting to reweigh the training samples. However, it can result in inaccurate estimates due to the influence of data instances with large importance weights on the reweighted loss. To address this drawback, recent MAR approaches have been constructed based on distributionally robust optimization of the reweighted loss. [3] proposed a robust bias-aware regression approach, which considers a worst-case shift between the training and testing sets to adversarially minimize the reweighted loss. [19] introduced Rockafellar-Uryasev (RU) regression to produce a model that is robust against bounded MAR sample selection bias, where the level of distribution shift between the training and testing sets is restricted. Based on the assumption for MNAR sample selection bias, methods that account for MAR bias would not properly model the MNAR data mechanism. Thus we expect methods that handle MAR bias to not be robust against MNAR sample selection bias. On the other hand, our approach uses the Heckman selection model to model the MNAR data mechanism, where the selection of samples is expressed as a linear equation. Moreover, unlike the above MAR approaches, we consider observed features of training samples with missing outcomes when modeling the missing data mechanism.

In particular, there are recent approaches that address the problem of MNAR labels in training data. In recommender learning, [22] proposed the joint learning of an imputation model and a prediction model to estimate the performance of rating prediction given MNAR ratings. [12] adopted two propensity scoring methods into its loss function to handle bias of MNAR feedback, where user feedback for unclicked data can be negative or positive-yet-unobserved. While the approaches in [12] and [22] also use separate propensity estimation models to predict the observation of a label, they consider matrix factorization as the prediction model, which is not for linear regression on tabular data.

In semi-supervised learning, [8] employed class-aware propensity score and imputation strategies on the biased training set toward developing a semi-supervised learning model that is doubly robust against MNAR data. We emphasize that our problem setting is different than semi-supervised learning. In semi-supervised learning, unlabeled samples are separated into clusters based on similarities. However, in our problem setting, we do not perform clustering on the samples with missing labels.

III Heckman Selection Model Revisited

Formally, the Heckman selection model [7] models the selection and prediction equations as follows. For any , the selection equation of the th sample is

| (2) |

where is the set of regression coefficients for selection, denotes the features for sample selection, and is the noise term for the selection equation. The selection value of the th sample is defined as:

| (3) |

The model learns the selection based on Eq. (3) and the prediction of the th sample based on linear regression, with

| (4) |

Assuming , we define where . Moreover, the noise terms and are correlated with a correlation coefficient of . If differs from zero, there is an indication that the missing observations are MNAR.

To correct the bias in , the conditional expectation of the predicted outcome

| (5) |

is computed over all samples in . Because and are correlated,

| (6) |

where is the inverse Mills ratio (IMR). We denote as the standard normal density function and as the standard normal cumulative distribution function. Thus Eq. (5) is rewritten as

| (7) |

where , , and .

We provide pseudocode of executing the Heckman model in Algorithm 1. The Heckman model follows two steps:

Step 1. Since there is no prior knowledge of the true value of for each sample in , is estimated as by first computing using probit regression over . As indicated in line 2 of Algorithm 1, we estimate after maximizing

| (8) |

over , where is the likelihood. As shown in line 4, is then used to compute for each in .

Step 2. Using , the prediction model is

| (9) |

The estimated set of coefficients is computed by minimizing over . As a result, is computed using the closed-form solution

| (10) |

as indicated in line 7.

Exclusion Restriction. The Heckman selection model assumes that the selection features consist of every prediction feature and additional features that do not affect the outcome. The selection and prediction features are generally not identical as it can introduce multicollinearity to the prediction model. Specifically, if the selection and prediction features are the same, the IMR would be expressed as

| (11) |

This would mean that Eq. (7) is properly identified through the nonlinearity of . However, is roughly linear over a wide range of values for [18]. Hence, Step 2 of the Heckman model would yield unrobust estimates for due to the multicollinearity between and .

IV Methodology

When choosing prediction features from a set of selection features, we encounter the following challenges. First, there are possible choices to make for the set of prediction features. For any dataset that has a large number of selection features, searching for a suitable set of prediction features becomes computationally expensive. Second, the Heckman selection model does not perform well for exclusion restrictions that are not valid. In other words, some choices for the set of prediction features are not helpful when using the Heckman model to handle MNAR sample selection bias on the outcome.

We introduce Heckman-FA, a framework for using the Heckman selection model via a learned feature assignment. Heckman-FA first learns the weights of an assignment function that draws samples from the Gumbel-Softmax distribution [9]. This function outputs an assignment of prediction features given a matrix of probabilities of including a selection feature in the prediction model. The framework then uses this assignment of prediction features to run the Heckman model and compute the mean absolute error (MAE) of predictions on when using the Heckman selection model. To optimize , we minimize the MAE with respect to . This results in an estimated probability matrix . To extract the prediction features, Heckman-FA looks through different prediction feature matrices by sampling from the Gumbel-Softmax distribution using . When determining the extracted prediction feature matrix, we first consider whether or not the estimated correlation between the noise terms is within a range that is user-defined based on prior domain knowledge. We further consider goodness-of-fit to ensure that the prediction model is of quality. Using the selection and extracted prediction features, we run the Heckman model to fit a robust prediction model under MNAR sample selection bias on the outcome.

IV-A Assignment Function

We formally introduce an assignment function , which is defined as

| (12) |

In general, an assignment function determines which of the selection features are also features in the prediction equation.

Assignment Computation. In Algorithm 2, we provide the pseudocode for computing a matrix of assigned prediction features from the selection feature matrix . We assume that both and have columns. However, we define the features assigned for prediction as the columns in that are not equal to the zero vector .

To obtain based on selection features, we compute the assignment for the th selection feature by drawing samples from a categorical distribution. Let be a categorical sample matrix such that each element is either 0 or 1. The Gumbel-Max trick is used to efficiently draw categorical samples. Following the steps of [9], a sample , the th column of , is drawn from a categorical distribution with class probabilities and , where () is the probability that the th selection feature is (not) assigned to the prediction model. Formally, is expressed as

| (13) |

where and . Thus, in terms of , we express the assignment for the th selection feature as

| (14) |

and compute

| (15) |

for each selection feature as indicated in lines 5 and 6 of Algorithm 2, using to denote elementwise multiplication.

Input: Training set , number of selection features , probability matrix

Output: prediction feature matrix

Backpropagation. To train the assignment function , we learn and for each selection feature. However, is expressed in terms of argmax, which is non-differentiable. Thus we cannot derive in order to learn . On the other hand, we can use the Gumbel-Softmax distribution [9] to approximate the categorical sample . By the Straight-Through Gumbel Estimator, we compute as a continuous, differentiable approximation of argmax, where

| (16) |

with as the softmax temperature. Notice that as , Eq. (16) will approximate the argmax function in Eq. (13), and the Gumbel-Softmax sample vector will approach a one-hot vector. Hence , where

| (17) |

Therefore, although we use Eq. (14) to obtain assignments, we use instead of when performing backpropagation to update .

Based on Eq. (17), is well-defined, so we are able to learn the assignment function and estimate parameters . Formally, we compute a probability matrix such that

| (18) |

where for the th selection feature. To ensure that the Heckman model is a quality prediction model, we consider the predictive performance of the Heckman model on to learn the assignment function. In this work, we choose to minimize the MAE over in order to obtain . For , using on Eq. (17), we see that

| (19) |

where . Thus is well-defined. Moreover, is not a zero matrix, meaning that is updated during backpropagation.

Discussion. Although other metrics such as mean squared error (MSE) and root mean squared error (RMSE) are typically used to evaluate the performance of linear regression, we cannot minimize these metrics in order to obtain . We show that if our objective is to minimize the MSE or RMSE, then does not change at all during backpropagation. As an example, consider , which denotes the MSE loss function. For , we see that

| (20) |

where

| (21) |

where is the error of predicting the outcome of using the Heckman selection model. Given that has length , consider two cases on the th selection feature. First, for any th selection feature not assigned for prediction, , where is the th column of . Thus after running the Heckman selection model and hence . Second, for any th selection feature assigned for prediction, for all . Thus

| (22) |

where is the error vector. Now is considered part of the input space that is used to compute and in turn . Because the values in are estimated by minimizing , then is orthogonal to the columns of the input space used to compute , which includes . Thus , and for all selection features assigned for prediction. Based on these two cases, for all selection features. Hence is a zero matrix.

IV-B Extraction of Suitable Assignment

After we train the assignment function , we utilize the estimated parameters to extract a suitable set of features for the prediction model. We propose a sampling-based strategy to extract using . We base this strategy on the estimated correlation between the noise terms and and the adjusted value, denoted as . Specifically, a suitable assignment of prediction features is extracted based on a user-defined range of values for the correlation. The range of values is provided based on prior domain knowledge on a given dataset. Moreover, we observe that multiple prediction feature assignments can correspond to a correlation that is within the user-defined range. To further decide on which prediction feature matrix to extract, we also consider goodness-of-fit to ensure that the prediction model is of quality.

In general, carries information about the nature of the sample selection process. However, because and are unobserved for all , the true value of is unknown for a dataset. We must instead consider the estimated correlation . To compute , we note that a consistent estimator of can be derived based on the Heckman selection model. First, define as the error of predicting the outcome of the th sample using the Heckman selection model. The true conditional variance of is

| (23) |

Consider the average conditional variance over all samples in , where

| (24) |

with plim denoting convergence in probability. Now the average conditional variance over all samples in is estimated using the mean squared error

| (25) |

of predicting the outcome using the Heckman model. Thus, using Eq. (24) and (25), can be estimated by computing

| (26) |

where is an estimate of . Therefore, using Eq. (26), we obtain .

We consider a set of prediction features to be suitable for the Heckman selection model if is within the range , where the values of and are user-specified. We work with this user-specified range because the true value of is unknown. We expect that the values of and are appropriately chosen to indicate that the Heckman model properly handles MNAR sample selection bias. On one hand, the range should not contain 0 since indicates MAR sample selection bias. On the other hand, and should not be too negative or too positive since strong correlation renders the Heckman model unstable [17].

Because there may be multiple values of that are in , we also obtain by computing

| (27) |

where is the coefficient of determination and is the number of prediction features. Having the largest number of prediction features such that is in does not imply that the linear model is the best fitted. Thus is helpful since it also factors in the number of prediction features when measuring the goodness-of-fit for a linear model.

Input: Training set , number of selection features , estimated parameters , lower correlation threshold , upper correlation threshold , number of Gumbel-Softmax samples

Output: Prediction feature matrix

As our strategy to extract for the Heckman selection model, we propose to collect Gumbel-Softmax samples based on . Out of the samples, we choose the prediction feature matrix such that the prediction model has the highest value of given that is in . The pseudocode for this process is listed in Algorithm 3. In lines 2-12, we iteratively look for . In line 3, we sample by executing Algorithm 2 based on . In line 4, we execute the Heckman model based on and get and . In line 5, we compute using Eq. (26). In line 6, we calculate by dividing by . In line 7, we compute . Throughout each iteration, we check whether or not is in and is larger than the current largest value. If this condition is satisfied, then we update , as indicated in line 9. In line 13, is returned.

Input: Training set , number of selection features , initial fixed value , number of training epochs , learning rate , lower correlation threshold , upper correlation threshold , number of Gumbel-Softmax samples

Output: Augmented prediction feature matrix , estimated Heckman coefficients

| Dataset | Selection Features |

|---|---|

| CRIME | householdsize, racepctblack, racePctWhite, |

| racePctAsian, racePctHisp, agePct12t21, agePct12t29, | |

| agePct16t24, agePct65up, numbUrban, pctUrban, | |

| medIncome, pctWWage, pctWFarmSelf, pctWInvInc, | |

| pctWSocSec, pctWPubAsst, pctWRetire, medFamInc, | |

| perCapInc, whitePerCap, HispPerCap, blackPerCap, | |

| indianPerCap, AsianPerCap, OtherPerCap | |

| COMPAS | sex, age, juv_fel_count, juv_misd_count, |

| priors_count, two_year_recid, age_cat_25 - 45, | |

| age_cat_Greater than 45, race_Caucasian, | |

| c_charge_degree_M |

| Extracted prediction features | Naive | RU[19] | Heckman-FA | |||||

| Train MSE | Test MSE | Train MSE | Test MSE | Train MSE | Test MSE | |||

| CRIME | ||||||||

| 1, 2, 3, 4, 5, 7, 8, | ||||||||

| 11, 15, 16, 21, 22, 23, 24 | 0.0423 | 0.4780 | 0.0159 | 0.0218 | 0.0109 | 0.0212 | 0.0159 | 0.0203 |

| COMPAS | ||||||||

| 1, 2, 5, 7, 8, 9, 10 | 0.2364 | 0.3453 | 0.0757 | 0.2560 | 0.0730 | 0.2589 | 0.0757 | 0.2506 |

IV-C Heckman Selection Model with Feature Assignment

Algorithm 4 gives the pseudocode of Heckman-FA. In lines 1-3, we initialize . In this work, we use a fixed value to initialize and for the th selection feature. This means that each selection feature has an equal probability of being assigned as a prediction feature when we start training . For , we give users some flexibility to choose which value to use. However, we suggest for users to not use values that are extremely close to 0 or 1 for . This ensures that is trained on a variety of sets of prediction features based on random Gumbel-Softmax samples. In lines 5-9, is trained over epochs. In line 5, we obtain the prediction feature matrix by executing Algorithm 2. In line 6, we execute the steps of the Heckman model to get and . In line 7, we use and to compute . In line 8, we update by computing using Eq. (19). In line 11, using , we extract the assigned prediction feature matrix by calling Algorithm 3. In line 12, we run the Heckman model using the extracted prediction features and obtain and . After having as the concatenation of and in line 13, Heckman-FA returns and .

Heckman-FA*. We also present Heckman-FA* as alternative option to Heckman-FA, where users extract by simply ranking the selection features based on the largest value of instead of using Algorithm 3. In other words, we rank the likeliest selection features to be assigned as prediction features based on the objective in Eq. (18) that computes . We then examine the first selection features in the ranking for all . Letting the first selection features in the ranking be prediction features, we run the Heckman selection model on the training set and obtain . We then compute , , and using the same steps indicated in lines 5-7 in Algorithm 3. Finally, out of all , we choose the set of top selection features in the ranking as prediction features such that and is at a maximum given . As a result, the columns of corresponding to these features do not equal .

Computational Complexity. To derive the computational complexity of Algorithm 4 (Heckman-FA), we first have to consider the complexity of Algorithm 2. The assignment computation takes time. During the training of in lines 4-10, the assignment computation is repeated for epochs. Thus the complexity of lines 4-10 is . Moreover, the complexity of Algorithm 3 is as the assignment computation is repeated for Gumbel-Softmax samples. Therefore, Heckman-FA has a computational complexity of .

We also consider the complexity of Heckman-FA*. Similar to Heckman-FA, we first see that is trained in time when running Heckman-FA*. However, the complexity of extraction is different for Heckman-FA* than for Heckman-FA. Because the Heckman selection model is called for sets of selection features, the extraction process has a complexity of . Thus the complexity of Heckman-FA* is .

V Experiments

V-A Setup

We evaluate the performance of our framework on CRIME [5] and COMPAS [11] datasets. The CRIME dataset contains socio-economic, law enforcement, and crime information for communities in the United States. For each community, we predict the total number of violent crimes committed (per 100,000 population). The COMPAS dataset consists of records collected from defendants in Florida between 2013 and 2014. Given attributes such as race, age, and priors count, we predict the defendant’s decile score.

For each dataset, we split the dataset to include 70% of samples in . We then construct based on . For the CRIME dataset, we create sample selection bias in by selecting communities such that the proportion of people under poverty is less than 0.05. As a result, 976 out of 1,395 communities in are in . For the COMPAS dataset, we select defendants in who have a violent decile score of less than 10. As a result, there are 2,585 samples in . We provide the set of selection features used for each dataset in Table II, where for the CRIME dataset and for the COMPAS dataset.

Baselines and Hyperparameters. We compare our approach to the following baselines: (1) naive linear regression (Naive) on and (2) Rockafellar-Uryasev (RU) regression [19], which involves fitting two neural networks with the RU loss to train a robust model under bounded MAR sample selection bias. In our experiments, we examine the RU regression baseline where the distribution shift between training and testing sets are restricted given . Unlike Heckman-FA, the baselines do not have access to features that model the selection of training samples. As a result, we should expect the baselines to not be as effective as Heckman-FA in handling regression under MNAR sample selection bias.

As we compute using Heckman-FA, we work with the following hyperparameters. When initializing , we set . We then train for epochs with the softmax temperature for both datasets. We set the learning rate equal to 0.75 for the CRIME dataset and 0.05 for the COMPAS dataset. For the extraction of prediction features, we draw Gumbel-Softmax samples. In all experiments, the range is set to be for the CRIME dataset and [0.1, 0.3] for the COMPAS dataset. All models are implemented using Pytorch and executed on the Dell XPS 8950 9020 with a Nvidia GeForce RTX 3080 Ti.

| Comparison | Test MSE Difference | P-value |

|---|---|---|

| CRIME | ||

| Heckman-FA - Naive | -0.0008 0.0004 | 0.0001 |

| Heckman-FA - RU | -0.0007 0.0007 | 0.0053 |

| COMPAS | ||

| Heckman-FA - Naive | -0.0060 0.0008 | 7.546e-10 |

| Heckman-FA - RU | -0.0093 0.0012 | 1.039e-9 |

V-B Results on Heckman-FA

In Table III, we report the training and testing MSE to compare Heckman-FA to the other baselines when using the extracted prediction features. When evaluating the methods using the extracted prediction features, we observe that the training MSE is equal for Heckman-FA and Naive. However, we see that the testing MSE is lower for the Heckman-FA than Naive. For instance, the testing MSE for Heckman-FA on the CRIME and COMPAS datasets is 0.0203 and 0.2506, respectively, which is lower than the testing MSE for Naive. For both datasets, we see that Heckman-FA produces a model that outperforms Naive given the extracted prediction features. When comparing Heckman-FA and RU, the training MSE of RU is 0.0050 and 0.0027 lower than Heckman-FA on the CRIME and COMPAS datasets, respectively. This is expected as RU fits a non-linear model for regression. On the other hand, we see that the testing MSE for Heckman-FA is 0.0009 and 0.0083 lower than RU for the CRIME and COMPAS datasets, respectively.

We also run a paired -test on 10 different assignments of prediction features to analyze the significance of the comparison between Heckman-FA and the other baselines. Table IV shows results of the test. We see that the p-value is very small after running the hypothesis test on both datasets. For instance, on the CRIME dataset, the p-value is 0.0001 and 0.0053 when comparing Heckman-FA with Naive and RU, respectively. Given that Heckman-FA significantly outperforms Naive and RU, the results in Tables III and IV show that Heckman-FA outputs a robust regression model under MNAR sample selection bias.

| training epochs | ||||

|---|---|---|---|---|

| 100 | 500 | 1,000 | 2,000 | |

| CRIME | ||||

| 0.25 | 0.0205 | 0.0210 | 0.0209 | 0.0211 |

| 0.5 | 0.0211 | 0.0214 | 0.0211 | 0.0207 |

| 0.75 | 0.0217 | 0.0216 | 0.0212 | 0.0208 |

| COMPAS | ||||

| 0.25 | 0.2514 | 0.2506 | 0.2530 | 0.2507 |

| 0.5 | 0.2502 | 0.2505 | 0.2502 | 0.2502 |

| 0.75 | 0.2502 | 0.2502 | 0.2506 | 0.2502 |

| training epochs | ||||||

|---|---|---|---|---|---|---|

| Execution time | Testing MSE | |||||

| 100 | 500 | 1,000 | 100 | 500 | 1,000 | |

| CRIME | ||||||

| 100 | 5.32 | 17.67 | 29.33 | 0.0209 | 0.0206 | 0.0210 |

| 500 | 16.02 | 26.06 | 44.23 | 0.0213 | 0.0210 | 0.0209 |

| 1,000 | 37.84 | 56.87 | 75.28 | 0.0212 | 0.0206 | 0.0209 |

| COMPAS | ||||||

| 100 | 7.70 | 21.30 | 39.32 | 0.2503 | 0.2502 | 0.2505 |

| 500 | 22.16 | 37.39 | 54.05 | 0.2506 | 0.2506 | 0.2503 |

| 1,000 | 49.72 | 70.46 | 97.64 | 0.2502 | 0.2506 | 0.2502 |

| Extracted prediction features | Naive | RU[19] | Heckman-FA* | |||||

| Train MSE | Test MSE | Train MSE | Test MSE | Train MSE | Test MSE | |||

| CRIME | ||||||||

| 2, 3, 8, 12, 16, 18, 21, 24 | 0.0609 | 0.4375 | 0.0172 | 0.0236 | 0.0142 | 0.0232 | 0.0172 | 0.0216 |

| COMPAS | ||||||||

| 2, 5, 6, 8, 10 | 0.2000 | 0.3432 | 0.0762 | 0.2575 | 0.0751 | 0.2617 | 0.0762 | 0.2527 |

Sensitivity Analysis. We perform sensitivity analysis on Heckman-FA by testing the approach over different values for the number of epochs , fixed initial value , and number of Gumbel-Softmax samples drawn during assignment extraction. Table V gives the testing MSE of Heckman-FA across different values of and while fixing . For each combination of and listed in Table V, the testing MSE of Heckman-FA is almost equal to the testing MSE provided in Table III for both datasets. We have a similar observation for each combination of and as shown in the right three columns of Table VI, which give the testing MSE of Heckman-FA across different values of and while fixing . This shows that the performance of Heckman-FA is not sensitive to changes in how is initialized and the number of Gumbel-Softmax samples examined during extraction.

| Heckman-C | Heckman-FA* | |

|---|---|---|

| 6 | 0.0490 | 0.0290 |

| 7 | 0.0563 | 0.0290 |

| 8 | 0.0479 | 0.0216 |

| 9 | 0.0500 | 0.0215 |

| 10 | 0.0498 | 0.0216 |

| 11 | 0.0555 | 0.0216 |

| 12 | 0.0524 | 0.0216 |

We also look at , which is used to draw Gumbel-Softmax samples for assignment computation, to consider the condition . We compare using the learned to fixing all elements of as 0.5 when drawing Gumbel-Softmax samples during extraction. To fairly compare the two settings, we obtain after having . For each setting for , we compute the proportion of Gumbel-Softmax samples that correspond to out of 1,000 total samples. We repeat the experiment 40 times using the COMPAS dataset. We find that the average proportion of having is 0.0601 after using a fixed value of 0.5 for all elements of . However, when using the learned from Heckman-FA, the average proportion of having increases by 0.0211. This result indicates that compared to letting each element of be 0.5, Heckman-FA is more likely to extract assignments of prediction features such that when the Gumbel-Softmax samples are drawn using the learned .

Execution Time. We report the execution time after running Heckman-FA across different values of and the number of Gumbel-Softmax samples drawn during the assignment extraction in left three columns of Table VI. We observe that for both datasets, Heckman-FA runs fast for each combination of and . For instance, when and , Heckman-FA is completed after 5.32 and 7.70 seconds for the CRIME and COMPAS datasets, respectively. While the execution time increases as and increase, the testing MSE of Heckman-FA remains close to the testing MSE reported in Table III. This result shows that Heckman-FA is fast while maintaining quality performance on the testing set.

V-C Results on Heckman-FA*

In Table VII, we compare the performance of baselines to Heckman-FA*. When using the extracted prediction features, we see that while the training MSEs of Heckman-FA* and Naive are equal for both datasets, the testing MSE for Heckman-FA* is 0.0020 and 0.0048 lower than Naive on the CRIME and COMPAS datasets, respectively. This shows that by simply choosing prediction features after ranking selection features based on , Heckman-FA* is robust against MNAR sample selection bias. Moreover, in terms of the testing MSE, Heckman-FA* outperforms RU by 0.0016 and 0.0090 on the CRIME and COMPAS datasets, respectively.

Comparison with Correlation-Based Ranking. To further show the effectiveness of Heckman-FA*, which requires training , we also compare the ranking of selection features based on to the ranking of selection features based on their strength of correlation with the outcome. We use the name Heckman-C to describe the correlation-based ranking of selection features. Unlike the ranking based on , Heckman-C does not rely on training the assignment function beforehand. For Heckman-FA* and Heckman-C, we run each approach on the CRIME dataset using the top selection features across different values of . Table VIII provides the MSE of the models on the testing set. We consider the values of through . The underlined testing MSE corresponds to the size of the final set of prediction features. For Heckman-FA*, the final set of prediction features consists of prediction features. For Heckman-C, there is no testing MSE underlined as there is no set of top selection features extracted for the final set of prediction features. In other words, when ranking the selection features based on their correlation with the outcome using the CRIME dataset, there is no set of features from the ranking that ensures the robustness of Heckman-C under MNAR sample selection bias. In our experiment, we also find that the condition is satisfied for Heckman-FA* for the range through . However, for Heckman-C, no set of prediction features satisfies this condition for any value of . This indicates that when assigning prediction features for the Heckman model, ranking selection features based on after training is more effective than ranking based on the correlation of features with the outcome.

VI Conclusion

In this paper, we introduced Heckman-FA, a novel data-driven approach that obtains an assignment of prediction features for the Heckman selection model to robustly handle MNAR sample selection bias. Given a set of features that are used to fit the selection of samples, our approach first trains an assignment function by minimizing the MAE on the set of fully observed training samples. Heckman-FA finds a set of prediction features for the Heckman model by drawing a number of Gumbel-Softmax samples using the learned probability of assignment for each selection feature. This set is extracted based on the prediction model’s goodness-of-fit and the estimated correlation between noise terms. We observed that the Heckman-FA produces a robust regression model under MNAR sample selection bias on the outcome after training the model on real-world datasets. In the future, we plan to extend our approach to the problem of learning MNAR outcomes/labels in non-tabular data.

Reproducibility. The source code can be downloaded using the link https://tinyurl.com/25s786z6.

Acknowledgements

This work was supported in part by NSF 1946391 and 2137335.

References

- [1] Till Bärnighausen, Jacob Bor, Speciosa Wandira-Kazibwe, and David Canning. Correcting hiv prevalence estimates for survey nonparticipation using heckman-type selection models. Epidemiology, pages 27–35, 2011.

- [2] Shawn Bushway, Brian D Johnson, and Lee Ann Slocum. Is the magic still there? the use of the heckman two-step correction for selection bias in criminology. Journal of quantitative criminology, 23:151–178, 2007.

- [3] Xiangli Chen, Mathew Monfort, Anqi Liu, and Brian D Ziebart. Robust covariate shift regression. In AISTATS, pages 1270–1279. PMLR, 2016.

- [4] Wei Du, Xintao Wu, and Hanghang Tong. Fair regression under sample selection bias. In Big Data, pages 1435–1444. IEEE, 2022.

- [5] Dheeru Dua and Casey Graff. UCI machine learning repository. http://archive.ics.uci.edu/ml, 2017.

- [6] Minna Genbäck, Elena Stanghellini, and Xavier de Luna. Uncertainty intervals for regression parameters with non-ignorable missingness in the outcome. Statistical Papers, 56:829–847, 2015.

- [7] James J Heckman. Sample selection bias as a specification error. Econometrica: Journal of the econometric society, pages 153–161, 1979.

- [8] Xinting Hu, Yulei Niu, Chunyan Miao, Xian-Sheng Hua, and Hanwang Zhang. On non-random missing labels in semi-supervised learning. arXiv:2206.14923, 2022.

- [9] Eric Jang, Shixiang Gu, and Ben Poole. Categorical reparameterization with gumbel-softmax. arXiv:1611.01144, 2016.

- [10] Hyungu Kahng, Hyungrok Do, and Judy Zhong. Domain generalization via heckman-type selection models. In ICLR, 2023.

- [11] J. Larson, S. Mattu, L. Kirchner, and J. Angwin. Compas dataset. https://github.com/propublica/compas-analysis/, 2017.

- [12] Jae-woong Lee, Seongmin Park, and Jongwuk Lee. Dual unbiased recommender learning for implicit feedback. In SIGIR, pages 1647–1651, 2021.

- [13] Qi Lei, Wei Hu, and Jason Lee. Near-optimal linear regression under distribution shift. In ICML, pages 6164–6174, 2021.

- [14] Siu Fai Leung and Shihti Yu. On the choice between sample selection and two-part models. Journal of econometrics, 72(1-2):197–229, 1996.

- [15] Phillip Lippe, Sara Magliacane, Sindy Löwe, Yuki M Asano, Taco Cohen, and Stratis Gavves. Citris: Causal identifiability from temporal intervened sequences. In ICML, pages 13557–13603. PMLR, 2022.

- [16] Jose G. Moreno-Torres, Troy Raeder, Rocío Alaiz-Rodríguez, Nitesh V. Chawla, and Francisco Herrera. A unifying view on dataset shift in classification. Pattern recognition, 45(1):521–530, 2012.

- [17] Kazumitsu Nawata. A note on the estimation of models with sample-selection biases. Economics Letters, 42(1):15–24, 1993.

- [18] Patrick Puhani. The heckman correction for sample selection and its critique. Journal of economic surveys, 14(1):53–68, 2000.

- [19] Roshni Sahoo, Lihua Lei, and Stefan Wager. Learning from a biased sample. arXiv:2209.01754, 2022.

- [20] Hidetoshi Shimodaira. Improving predictive inference under covariate shift by weighting the log-likelihood function. Journal of statistical planning and inference, 90(2):227–244, 2000.

- [21] Francis Vella. Estimating models with sample selection bias: a survey. Journal of Human Resources, pages 127–169, 1998.

- [22] Xiaojie Wang, Rui Zhang, Yu Sun, and Jianzhong Qi. Doubly robust joint learning for recommendation on data missing not at random. In ICML, pages 6638–6647, 2019.

- [23] Sarah E Wolfolds and Jordan Siegel. Misaccounting for endogeneity: The peril of relying on the heckman two-step method without a valid instrument. Strategic Management Journal, 40(3):432–462, 2019.