Choosing a Proxy Metric from Past Experiments

Abstract

In many randomized experiments, the treatment effect of the long-term metric (i.e. the primary outcome of interest) is often difficult or infeasible to measure. Such long-term metrics are often slow to react to changes and sufficiently noisy they are challenging to faithfully estimate in short-horizon experiments. A common alternative is to measure several short-term proxy metrics in the hope they closely track the long-term metric – so they can be used to effectively guide decision-making in the near-term. We introduce a new statistical framework to both define and construct an optimal proxy metric for use in a homogeneous population of randomized experiments. Our procedure first reduces the construction of an optimal proxy metric in a given experiment to a portfolio optimization problem which depends on the true latent treatment effects and noise level of experiment under consideration. We then denoise the observed treatment effects of the long-term metric and a set of proxies in a historical corpus of randomized experiments to extract estimates of the latent treatment effects for use in the optimization problem. One key insight derived from our approach is that the optimal proxy metric for a given experiment is not apriori fixed; rather it should depend on the sample size (or effective noise level) of the randomized experiment for which it is deployed. To instantiate and evaluate our framework, we employ our methodology in a large corpus of randomized experiments from an industrial recommendation system and construct proxy metrics that perform favorably relative to several baselines.

1 Introduction

Randomized controlled trials (RCTs) are the gold standard approach for measuring the causal effect of an intervention (Hernán and Robins, 2010); however, designing and analyzing high-quality RCTs requires various considerations to ensure scientifically robust results. For example, an experimenter must clearly define the intervention, control, and choose a primary outcome for the study. In this work, we will assume that the intervention and control are clearly defined, and consider the problem of choosing a good primary outcome. A common approach is to choose the primary outcome to be a key metric which drives downstream decision-making. Such metrics are critical components in the decision-making pipelines of many large-scale technology companies (Chen and Fu, 2017; Rachitsky, ) as well as used to guide policy decisions in economics and medicine (Athey et al., 2019; Elliott et al., 2015). Unfortunately, direct measurement of such a metric can be impractical or infeasible. In many cases, they are long-term outcomes observed with a significant temporal delay, making them slow to move (i.e. insensitive) in the short term, and inherently noisy. Moreover, they may be prohibitively expensive to query.

On the other hand, proxy metrics (or surrogates) that are easier to measure or faster to react are often available to use in lieu of the long-term outcome. For example in clinical settings, CD4 white-blood cell counts in blood serve as a surrogate for mortality due to AIDS (Elliott et al., 2015), while in online experimentation platforms diversity of consumed content serves a proxy for long-term visitation frequencies (Wang et al., 2022). A significant literature exists on designing and analyzing proxy metrics and experiments that use them as a primary outcome. One important question addressed by this literature is choosing (or combining) proxy metrics to be a good surrogate for measuring the effect of the intervention on the long-term outcome (Prentice, 1989; Hohnhold et al., 2015; Parast et al., 2017; Athey et al., 2019; Wang et al., 2022, 2023). To do so, one needs a principled reason for why the measured treatment effect on the proxy outcome is related to the treatment effect on the long-term outcome. Frequently, this is done by making causal assumptions about the relationship between the treatment, proxy outcome, and long-term outcome (see, e.g., VanderWeele, 2013; Athey et al., 2019; Kallus and Mao, 2022). However, motivated by the unique way that trials are run in technology product applications, we take a different approach based on statistical regularity assumptions in a population of experiments, similar to meta-analytic approaches such as that taken by Elliott et al. (2015).

RCTs performed in technology products are typically referred to as A/B tests. They are used for a wide variety of applications in the technology industry, however one of the most common applications is for assessing the effect of a candidate launch of a new product feature or change on the user’s experience. If the results of the A/B test suggest that the candidate launch has a positive effect on the user experience, then it will be deployed to all users. Depending on the scale of the product and engineering team, many candidate launches requiring many A/B tests may be required on a regular basis. The results of these A/B tests on long-term outcomes and proxy metrics are logged, serving as a history of past candidate launches that we may use to guide the choice of future proxy metrics to use for decision making.

This perspective has been studied in the technology research literature previously, for example in Richardson et al. (2023) and Wang et al. (2022), to develop useful heuristics for choosing a proxy metric for use in future A/B tests. In this work, we define a precise statistical framework for choosing a proxy metric based on this historical A/B test data, and develop a method for optimizing a composite proxy, an affine combination of base proxy metrics, that can be used as a primary outcome for future A/B tests.

The central contributions of our paper are the following:

-

•

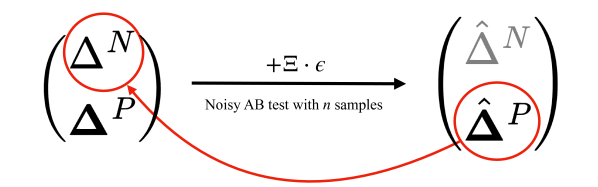

We define a new notion of optimality for a proxy metric we term proxy quality, for use in a homogeneous population of randomized experiments. Our definition differs from the existing literature in that it phrases optimality as ensuring the observed proxy metric closely tracks the unobserved population treatment effect on the long-term outcome (see Figure 1). Conveniently, our definition also packages two important considerations for a proxy metric – short-term sensitivity of the proxy metric and directional alignment with the long-term outcome – into a single objective (see Equation 2).

-

•

We show this new notion of proxy quality can be used to construct optimal proxy metrics for new A/B tests via an efficient two-step procedure. The first step reduces the construction of an optimal weighted combination of base proxies, that maximize our definition of proxy quality, to a classic portfolio optimization problem. This optimization problem is a function of the latent variability of the unobservable population treatment effects and the noise level of the new experiment under consideration (see Section 2.1.2). We then use a hierarchical model to denoise the observed treatment effects on the proxy and long-term outcome in a historical corpus of A/B tests to extract the variation in the unobserved population treatment effects (see Section 2.2). The variance estimates of the population TEs are then used as plug-ins to the aforementioned optimization.

-

•

We highlight the adaptivity of our proxy metric procedure to the inherent noise level of each experiment for which it will be used. In our framework the optimal proxy metric for a given experiment is not apriori fixed. Rather it should depend on the sample size (or effective noise level) of the randomized experiment for which it is deployed in order to profitably trade-off bias from disagreement with the long-term outcome and intrinsic variance (see Section 2.1.1 and Figure 3).

-

•

Finally, we instantiate and evaluate our framework on a set of 307 real A/B tests from an industrial recommendation engine showing how the proxy metrics we construct can improve decision-making in a large-scale system (see Section 3).

1.1 Statistical Framework

Consider a corpus of randomized experiments (or A/B tests) where the -th experiment is of sample size . In each experiment, there is a specific intervention that has some population treatment effect (TE) that we denote .111This may be an average TE (ATE) or relative ATE, however, we will not emphasize the differences between these two as they are immaterial for this work. In the experiment, we measure an estimated TE on the subset of the population included in our experiment. Note that the entire population may be included in the experiment, but remains a random quantity, given , because of the random assignment of treatments in the experiment.

To differentiate between the TE on the long-term outcome and the proxy metrics, we will attach a superscript as in or for the long-term outcome (we use since these are sometimes referred to as north star metrics), and a superscript as in and for the proxy metrics. Note that there may be multiple base proxy metrics, so . Throughout, we assume that is large enough, and that the experimental design is sufficiently regular such that conditional on , is well-approximated by a Normal distribution centered around the population TE222Note that in our framework, the notion of proxy quality in Section 2.1.1 and Section 2.1.2 only relies on low-order moments and doesn’t explicitly require Gaussianity but the estimation procedure in Section 2.2 makes explicit use of this structure. (due to the central limit theorem); and that the joint (within-experiment) covariance of , denoted as , has a good estimator, denoted as . Our discussion is agnostic to the precise estimator of the TEs and their covariances. We only require black-box access to their values. For the historical corpus of randomized experiments, we assume that these triplicates of measurements are available.

Our goal in this paper is to revisit the proxy metric problem: the selection of short-term proxy metrics (or a weighted combination thereof) that track the long-term outcome in a new st experiment where measurements of the long-term outcome are unavailable, but measurements of short-term proxy metrics are. In order to develop a statistical framework to construct proxies in a new experiment, we leverage a meta-analytic approach to model the relationship between different experiments. To this end, we assume the population TEs for each experiment are drawn i.i.d. from a common joint distribution ,

| (1) |

supported over . We acknowledge this assumption is strong and not suitable for all applications. However, in our motivating application of interest – studying a corpus of AB tests from a large technology company – historical intuition and various tests do not provide significant evidence this assumption is violated. The approach of placing a distributional prior on the population ATE in similar settings of A/B testing at large-scale technology companies (Deng and Shi, 2016; Deng, ) as well as other meta-analytic studies of RCTs (Elliott et al., 2015; Elliott, 2023) has also been advocated for as a useful assumption in prior work.

2 Methods

With the above setting in place we first define the measure of quality of a proxy metric which relates the estimated TE on the short-term proxies to the population TE on the long-term outcome for a new experiment. Subsequently, we show how the relevant latent parameters contained in the definition of proxy quality can be efficiently estimated via a hierarchical model.

2.1 Optimal Proxy Metrics

In order to judge the quality of a proxy metric we first define a new notion of utility for a proxy metric. Our key insight is that in a new experiment333In the following since we assume all the experiments are i.i.d. we suppress index notation on this arbitary experiment drawn from . where , the observed TEs of the short-term proxies should closely track the latent TE of the long-term outcome (see Figure 1).444Note in a new experiment the estimated treatment effect on the long-term outcome may be unavailable. This is because decisions that are intended to move will be made on the basis of . Thus, we would like these quantities to be well-correlated.

2.1.1 Proxy Quality of a Single Short-Term Metric in a New Experiment

For simplicity, we first consider the case when the vector-valued sequence of proxies reduces to a single scalar proxy. In order to capture the intuition that the short-term estimated proxy TE, should track the population long-term outcome TE, we define the proxy quality as the correlation between the aforementioned quantities. The correlation is a simple and natural measure which captures the predictive relationship between the proxy metric and long-term outcome. Under stronger conditions in Section 2.2, we also argue that optimizing for this measure of proxy quality minimizes the probability of a (signed) decision error or surrogate paradox.

In our setting we consider the case where the estimated TEs are unbiased estimators of their underlying latent population quantities – so we can parameterize , where is an independent random zero-mean, unit-variance random variable. Hence we can define and simplify the proxy quality as:

| (2) |

In our setting, the definition of proxy quality decomposes the predictive relationship between the estimated proxy TE and population long-term outcome TE into latent predictive correlation – a property of the distribution – and an effective inverse signal-to-noise ratio – which is also a function of the noise level of the experiment. We now make several comments on the aforementioned quantities.

-

•

The latent predictive correlation tracks the alignment between the population proxy metric TE and the population long-term outcome TE. In particular, this correlation is reflective of the intrinsic predictive quality of a fixed proxy metric. This quantity is not easily accessible since we do not directly observe data sampled from . We return to the issue of estimating such quantities in Section 2.2.

-

•

The quantity computes the ratio of the within-experiment noise in the estimated proxy metric TE—due to fluctuations across experimental units and treatment assignments—to the latent variation of the population proxy metric TE across experiments. For the former quantity we expect to depend on the size of the randomized experiment in consideration (i.e. , where is the sample size of the experiment), since it is a variance over independent treatment units. Meanwhile captures how easily the population proxy metric TE moves in the experiment population . In a (large enough) given experiment, is easily estimated by using the sample covariance estimator. Meanwhile, is difficult to measure directly, just like . We later show how to use a hierarchical model to estimate these parameters (see Section 2.2). Finally, it is worth noting this ratio term in the denominator is also closely related to a formal definition of metric sensitivity which appears in the A/B testing literature (Deng, ; Richardson et al., 2023).

Together the numerator and denominator in Equation 2 trade off two (often competing) desiderata into a single objective: the numerator favors alignment with the population TE on the long-term outcome while the denominator downweights this by the signal-to-noise ratio of the proxy metric.555This tradeoff between directional alignment of the proxy metric/long-term outcome and sensitivity of the proxy metric is further discussed in (Richardson et al., 2023). One unique property of this proxy quality measure is that, given a set of base proxies, the “optimal” single proxy is not an intrinsic property of the proxy metric or distribution of treatment effects captured by . Rather, it also depends on the experimental design. Specifically, it is a function of the experiment sample size , which will control the size of . This behavior represents a form of bias-variance trade-off. For large sample sizes, as , Equation 2 will favor less biased metrics whose population-level TEs are aligned with the long-term outcome (i.e. the numerator is large). Meanwhile, for small sample sizes where is large, Equation 2 will favor less noisy metrics with a high signal-to-noise ratio so the denominator is small.

2.1.2 Composite Proxy Quality in a New Experiment

The previous discussion on assessing the quality of a single proxy metric captures many of the important features behind our approach. However, in practice, we are often not restricted to picking a single proxy metric to approximate the long-term outcome. Rather, we are free to construct a composite proxy metric which is a convex combination of the TEs of a set of base proxy metrics to best predict the effect on the long-term outcome.

In our framework, the natural extension to the vector-valued setting takes a convex combination of the proxies for a normalized weight vector , instead of restricting ourselves a single proxy. However, beyond just defining the quality of a weighted proxy metric, we can also optimize for the quality of this weighted sum of base proxy metrics:

| (3) |

Again, the estimated TEs are unbiased estimators of their underlying latent population quantities, so we can parameterize , where is an independent random zero-mean, identity-covariance random vector. So the objective expands to:

| (4) |

Essentially all considerations noted in the previous section translate to the vector-valued setting mutatis mutandis. In particular, the numerator in Equation 4 captures the alignment between the true latent weighted proxy and the population long-term outcome, while the denominator downweights the numerator by the effective noise in each particular experiment. As before we expect with the sample size, , of the experiment. Hence, the optimal weights for a given experiment will adapt to the noise level (or equivalently sample size) of the experiment run.

The formulation in Equation 4 raises the question of how to efficiently compute . Indeed, at first glance the optimization problem as phrased in Equation 4 is non-convex. Fortunately, the objective in Equation 4 (up to a constant pre-factor) maps exactly onto the Sharpe ratio (or reward-to-volatility ratio) maximization problem often encountered in portfolio optimization (Sharpe, 1966, 1998). As is well-known in the optimization literature, the program in Equation 4 can be converted to an equivalent (convex) quadratic programming problem which can be efficiently solved (Cornuejols and Tütüncü, 2006, Section 8.2). We briefly detail this equivalence explicitly in Appendix B.

The portfolio perspective also lends an additional interpretation to the objective in Equation 4. If we analogize each specific proxy metric as an asset to invest in, then is the returns vectors of our assets, and is their effective covariance–so captures the risk of our portfolio of proxies. Just as in portfolio optimization, where two highly-correlated assets should not be over-invested in, if two proxy metrics are both strongly aligned with the long-term outcome, but are themselves very correlated, the objective in Equation 4 will not assign high weights to both of them.

2.2 Estimation of Latent Parameters via a Hierarchical Model

As the last piece of our framework, we finally turn to the question of obtaining estimates of the unobservable latent quantities arising in Equation 4. While is easily estimated from the within-experiment sample covariance , the quantities , are tied to the latent, unobservable population TEs of the proxy metrics and long-term outcome.

In order to gain a handle on these quantities, we take a meta-analytic approach which combines two key pieces. First, as in our previous discussion, we require the setting described in Equation 1 – that is we assume the true population TEs are drawn i.i.d. from a common joint distribution. While only this assumption was needed for our previous discussion, we now introduce additional parametric structure in the form of an explicit generative model to allow for tractable estimation of the parameters and . Second, we assume access to a pool of homogeneous RCTs for which unbiased estimates of the TE on the short-term proxy metrics and long-term outcome are available (i.e. for ). With these two pieces we can construct a hierarchical (or linear mixed) model to estimate the latent parameters:

| (5) | ||||

| (6) |

which due to the joint Gaussianity we can marginalize as:

| (7) |

We use the notation to capture the latent covariance of the joint distribution which we parameterize by a multivariate normal (i.e. MVN). So in our case, and for . Moreover, for the purposes of inference we simply use the plug-in estimate which is routinely done in similar hierarchical modeling approaches (Gelman et al., 1995). While using multivariate normality in Equation 5 is an assumption (albeit we believe reasonable in our case), it is not essential to the content of our results. Our proxy quality definition relies only on inferring low-order moments of for which this parametric structure is convenient. The second approximation that the noisy TEs are multivariate normal around their true latent values (Equation 6) is well-justified by the central limit theorem in our case, since the experiments we consider all have at least treatment units. Since inference in this model is not closed-form, we implement the aforementioned generative model in the open-source probabilistic programming language NumPyro (Phan et al., 2019) to extract the latent parameters. Additional details on the inference procedure are deferred to Appendix C.

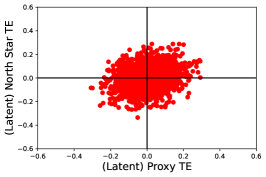

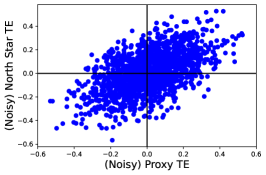

Figure 2 provides an example where the inference procedure is used to extract the latent population variation in a synthetically generated dataset. Although this example is synthetic (and exaggerated), empirically in our corpus we observe many base proxy metrics with correlations to the long-term outcome of in their experimental noise matrix . Thus, the example shows a case where the raw correlation may provide an over-optimistic estimate of the underlying alignment between a proxy metric and long-term outcome. The denoising model we fit helps mitigate the impact of correlated within-experiment noise in our setting. We schematically detail the end-to-end algorithm which composes the denoising model fit and portfolio optimization to construct a proxy for a new A/B test in Algorithm 1.

Lastly, with the generative model in Equations 5, LABEL: and 6 in place we can provide an alternative interpretation of our definition of composite proxy quality. Under the condition that 666This condition may not be true in all applications but is approximately satisfied in our dataset with all metrics having the ratio of their global mean to global standard deviation being bounded by but often being even less., the probability of a signed alignment (or equivalently the complement of a surrogate paradox Elliott et al. (2015)) can be simplified too,

| (8) |

for . This computation relies on the joint Gaussianity of the model and centering condition to explicitly compute the alignment probability. Given is our definition of the vector-valued proxy quality and the inverse-sine function is monotone increasing, optimizing the proxy quality over can be interpreted as minimizing the probability of a signed decision error in this setting.

3 Results

In this section, we turn to evaluating the performance of our composite proxy procedure against several baselines. As raw proxy metrics to consider in our evaluations we use a small set of 3 hand-selected proxy metrics which capture different properties domain experts believe are relevant to long-term user satisfaction in our setting. We first highlight a unique feature of our proxy procedure – its adaptivity to the sample size of the experiment for which it will be applied. We then perform a comparison of our new proxy procedure against the raw proxy metrics and a baseline procedure (Richardson et al., 2023) appearing in the literature.

3.1 Proxy Quality and Sample Size Dependence

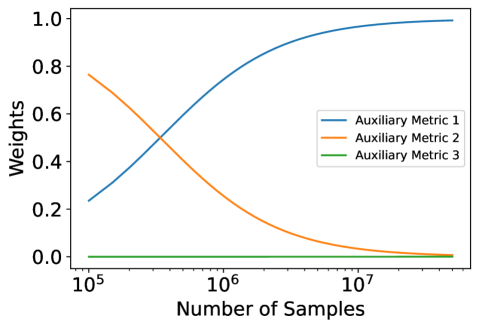

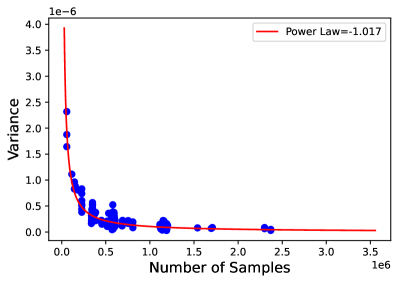

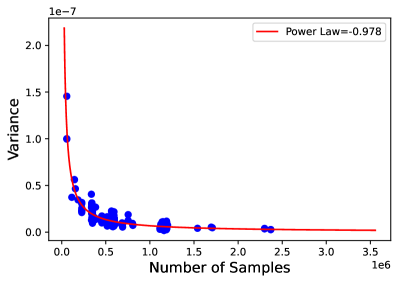

One unique feature of our procedure is its adaptivity to the noise level (or effectively sample size of the experiment); recall in Equation 4 the optimal weights will depend on the latent parameters which are inferred from the pool of homogeneous RCTs on which they are fit, but also the experiment noise estimate which depends on the new A/B test it is to be used for. While in practice one could recompute a proxy metric depending on the aposteriori results of each A/B test (so is known), it is also desirable to be able to fit a proxy for each A/B test apriori, without knowledge of its results. To do so, we found that in our application, could be estimated with reasonable accuracy purely on the basis of historical data of other A/B tests in our population of experiments by postulating a scaling of the form . Here the reference matrix can be thought of as the within experiment variance of an A/B test in the population with one sample. The ansatz , combines two observations. The first is that the variance of a TE estimate decays as in the number of treatment units , which is immediate from the independence of treatment units. However, the second is that the constant prefactor in the variance is approximately the same across different A/B tests in our corpus. The reference matrix can then be estimated as a weighted average of from the corpus. Additional details and verification of these hypotheses are provided in Appendix A. The upshot of this approach is that the computation of the optimal weights in Equation 4 for a new A/B test can then be done using only the sample size () of this new experiment (i.e. before the new experiment is “run”).

To understand the dependence of our new composite proxies weighting on the experiment sample size, we fit the latent parameters (from the hierarchical model in Equations 5, LABEL: and 6) and on the entire corpus for the results in Figure 3. We then use the scaling to estimate the optimal weights of our new composite proxy from Equation 4 for different sample sizes for a hypothetic new A/B test. Figure 3 shows how as the sample size increases the new composite proxy smoothly increases its weighting on raw metrics which are noisier but more strongly correlated with the long term outcome. Moreover, while the Auxiliary Metric 3 is an intuitively reasonable metric, its value as determined by the measure of proxy quality is dominated by a mixture of the other two components.

3.2 Held-out Evaluation of Proxy Procedures

The primary difficulty of this evaluation is that in TE estimation there is the lack of ground-truth “labels” of the treatment effect (i.e. in our framework the population latent TEs such as are never observed). However, in our setting we do have access to a large corpus of 307 A/B tests as noted earlier. Hence, we use held-out/cross-validated evaluations of certain criterion which depend on the noisy metrics aggregated over an evaluation set, to gauge the performance of proxy metrics fit on a training set.

We consider several relevant criteria for performance which have been used in the literature. Two important measures which appear in (Richardson et al., 2023) are the proxy score and sensitivity. To define the criteria, recall that a TE metric is often used to make a downstream decision by thresholding its t-statistic, as , , and . Given a corpus of A/B tests we can then compute the decisions induced by a short-term proxy metric, the decisions induced by the long-term outcome and check the number of A/B tests for which they align. After normalization, the number of detections (both metrics decisions are positive or negative) minus the number of mistakes (one metric decision is positive while the other is negative) defines the proxy score. Similarly, for a short-term proxy metric we can compute its sensitivity – which is the number of times it triggers a statistically significant decision by being positive or negative. Loosely speaking, these two criterion function like the notions of precision and recall in information retrieval. Ideally, a short-term metric would maximize both quantities by being sensitive and triggering often (so as to not miss any A/B tests where the TE for the long-term outcome is significant) but not over triggering and leading to many false positives (or negatives). Additional details on these metrics are provided in the Appendix D777It is worth noting these measures are still imperfect in the sense that comparisons are made against the decisions induced by the noisy estimate of the long-term outcome TE not the latent population long-term outcome TE. This is further complicated by the fact that we empirically find that experimental noise in the A/B tests is correlated between short-term proxies and the long-term outcome (i.e. the phenomena detailed in Figure 1). In fact, this phenomena provides partial motivation for our definition of denoised proxy quality.. As another measure of performance, we also compute and report our definition of our composite proxy quality for a given composite proxy’s learned weights.

We use the same set of raw proxy metrics as before in our evaluation. As a procedure to compare our methodology against, we use the baseline of optimizing the convex combination of these 3 metrics to optimize the aforementioned proxy score which is detailed in (Richardson et al., 2023). In each case we use stratified 4-fold cross-validation (CV) to compute the weights for each procedure on a training subset of the corpus and evaluate the metrics on the held-out set by computing the aforementioned evaluation scores. The baseline proxy method and base proxy metrics each learn a fixed set of weights888the base proxy metrics simply place all their weight on themselves. depending on the training fold, which is applied to each A/B test in the evaluation fold. For our procedure we use the ansatz mentioned in the previous setting to calculate as a simple weighted average from data only in the training fold of our CV split. The optimal proxy metric for each A/B test in the test fold can then be refit using only the sample size of that A/B test. This strategy has the additional benefit of enforcing strict separation of the data in train/test set folds in our CV split.

| Metric | Sensitivity | Proxy Score | Proxy Quality |

| New Composite Proxy | 0.181 | 0.666 | 0.302 |

| Baseline Composite Proxy | 0.182 | 0.611 | 0.279 |

| Auxiliary Metric 1 | 0.062 | 0.611 | 0.174 |

| Auxiliary Metric 2 | 0.368 | 0.222 | 0.258 |

| Auxiliary Metric 3 | 0.166 | 0.104 | 0.030 |

Results for our cross-validated evaluation are displayed in Table 1 across our corpus of 307 A/B tests. Note that both our new composite proxy and the baseline composite proxy improve significantly in the proxy score and proxy quality over the raw metrics without sacrificing unduly on sensitivity relative to Auxiliary Metric 2. Moreover, the new composite proxy achieves not only the highest proxy quality but also proxy score despite not explicitly optimizing for proxy score on the training set. We believe this may be a feature of our new composite proxy whose weights are adaptive to the size of each experiment in the A/B test (which vary in our corpus from approximately to in size).

4 Conclusion

We have presented a framework for both defining and constructing optimal composite proxy metrics, which are used to approximate the decisions induced by a difficult-to-measure long-term metric. One key insight from our framework is that the optimal proxy for a given experiment should depend on the noise level (or equivalently the size) of that experiment. In the future, more flexible modeling of the joint latent effect distribution – to accommodate more structured latent effects could be useful. Similarly, extending our framework to handle the construction of nonlinear composite proxy metrics is an interesting avenue for further exploration.

Appendix A Within-Experiment Covariance Scaling

As we note before, one interesting feature of our composite proxy quality procedure is its dependence on the noise level of of the randomized experiment it will be applied too. Recall in Equation 4 the optimal weights will depend not only on the latent parameters which are instrinsic properties of , but the experiment noise estimate which depends on the particular A/B test too which it is applied.

While in practice, one could recompute a composite proxy metric after an A/B test is run (so is known), in many applications it is also desirable to be able to fit weights for a composite proxy metric before each A/B test is run. In order to do this we found that we could build a simple predictive model for the experimental noise level in a given experiment on the basis of historical data of other A/B tests in our population of experiments. We did so by making an ansatz of the form , where can be thought of as the within experiment variance of an A/B test in the population with one sample. This ansatz follows from two facts. The first is that the variance of a TE estimate decays as in the number of treatment units , which is immediate from the independence of treatment units. However, the second – that the constant prefactor in the variance is approximately the same across different A/B tests – is an empirical observation due to underlying homogeneity in the population of A/B tests. This approximate homogeneity is evidenced in Figure 4.

On the basis of this ansatz for each A/B test,

we can construct an estimator for the reference constant matrix as,

| (9) |

for some convex combination of weights . While we can use an equal weighting scheme where , since the sample variance estimates themselves are noisy, we instead use a precision weighted combination of them to reduce variance by taking .

With this estimate in hand, for a new st A/B test with sample size we can approximates its within-experiment covariance as,

under the implicit homogeneity assumption we make.

Appendix B Sharpe Ratio and Portfolio Optimization

Under the mild condition (which is always satisified for us that at least one element of is positive), we can transform the Sharpe ratio optimization objective to an equivalent convex quadratic program:

| (10) |

where and . The solution to the original problem in Equation 4 can be recovered by normalizing as . The details of this standard transformation can be found in (Cornuejols and Tütüncü, 2006, Section 8.2), although the original reduction is a generalization of the Charnes-Cooper transformation (Charnes and Cooper, 1962) which dates back to at least (Schaible, 1974).

Appendix C Inference in Hierarchical Model

In order to extract estimates of the latent parameter we perform full Bayesian inference over the generative model in Equation 7 using Numpyro Phan et al. (2019) which uses the NUTS sampler to perform MCMC on the posterior. We found Bayesian inference to be more stable then estimating the MLE of the model. We augmented the generative model in Equation 7 with the weak priors:

where we use the operator to denote coordinatewise broadcasted multiplication. Here the vector-valued parameters meanscale, and devscale are set to match the overall scales of the raw mean and raw covariance of the corpous A/B tests. We found the overall inferences to be robust to the choice of scales in the Half-Cauchy prior on the pooled variance parameter and normal prior mean, which are both weakly-informative. (Gelman, 2006) and (Polson and Scott, 2012) both argue for the use of the Half-Cauchy prior for the top-level scale parameter in hierarchical linear models as opposed to the more traditional use of the Inverse-Wishart prior on both empirical and theoretical grounds. The choice of the LKJ prior with concentration parameter set to 1 is essentially a uniform prior over the space of correlation matrices (Gelman et al., 1995; Lewandowski et al., 2009).

Inference in this model was performed using the default configuration of the NUTS sampler in Numpyro (Phan et al., 2019). We also found it useful to initialize the parameters and to the scales of the raw mean and raw covariance of the corpus A/B tests. We diagnosed convergence and mixing of the NUTS sampler using standard diagnostics such as the r-hat statistic (Gelman et al., 1995). In all our experiments we found the sampler mixed efficiently and we achieved a perfect r-hat statistic for all parameters of 1.0. For each MCMC run we generated 10000 burn-in samples and 50000 MCMC samples for 4 parallel chains. We used the posterior means of the samples to extract estimates of for use in our proxy quality score.

Appendix D Proxy Score and Sensitivity

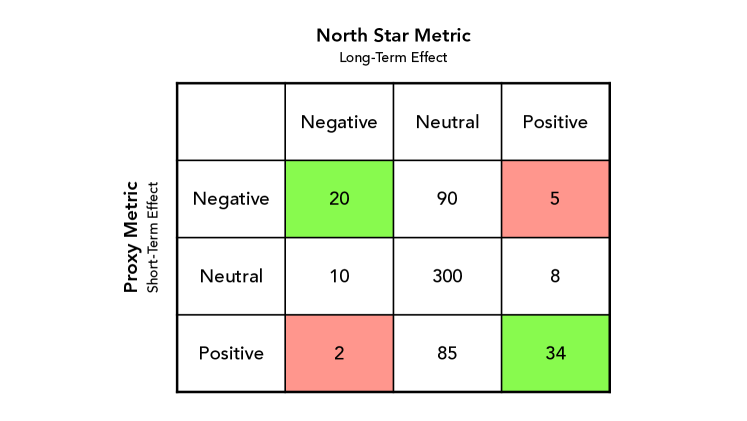

Here we explain several performance criterion we use for proxy metrics which are further detailed in the literature (Richardson et al., 2023). In order to define both quantities, recall that a TE metric is often used to make a downstream decision by thresholding its t-statistic, as , , and . The formal definitions of proxy score and sensitivity are most easily defined in the context of a contingency table visualized in Figure 5 which takes these decisions as inputs. The contingency table tabulates the decisions induced by a particular observed short term proxy metric and the observed long-term north star metric jointly over 554 A/B tests.

The green cells in Figure 5 represent cases where the proxy and north star are both statistically significant and move in the same direction (i.e. Detections). The red cells in Figure 5 again represent cases where the proxy and north star are both statistically significant, but where proxy and north star are misaligned (i.e. Mistakes). The remaining cells correspond to cases where at least one of the metrics is not statistically significant. The relative importance of these cells is more ambiguous.

In this setting, the sensitivity can be defined as:

| Metric Sensitivity |

Here the numerator can be obtained by summing over the first and last rows of the table. The proxy score can be defined as,

| Proxy Score |

The denominator here can be obtained by summing over the first column and last column. The sensitivity metric captures the ability of a metric to detect a statistically significant effect – which inherently takes into account its inherent moveability and susceptibility to experimental noise. Given that north star metrics are often noisy and slow to react in the short-term the goal of a proxy is to be sensitive.

The proxy score rewards metrics that are both sensitive and directionally aligned with the north star. Sensitive metrics need only populate the first and third rows of the contingency table. However, metrics in the first and third rows can only increase the proxy score if they are in the same direction as the long-term north star. A similar score, called Label Agreement, has been used by Dmitriev and Wu (2016).

References

- Athey et al. [2019] Susan Athey, Raj Chetty, Guido W Imbens, and Hyunseung Kang. The surrogate index: Combining short-term proxies to estimate long-term treatment effects more rapidly and precisely. Working Paper 26463, National Bureau of Economic Research, November 2019. URL http://www.nber.org/papers/w26463.

- Charnes and Cooper [1962] A. Charnes and W. W. Cooper. Programming with linear fractional functionals. Naval Research Logistics Quarterly, 9(3-4):181–186, 1962. doi: https://doi.org/10.1002/nav.3800090303. URL https://onlinelibrary.wiley.com/doi/abs/10.1002/nav.3800090303.

- Chen and Fu [2017] Albert C. Chen and Xin Fu. Data + intuition: A hybrid approach to developing product north star metrics. In Proceedings of the 26th International Conference on World Wide Web Companion, WWW ’17 Companion, page 617–625, Republic and Canton of Geneva, CHE, 2017. International World Wide Web Conferences Steering Committee. ISBN 9781450349147. doi: 10.1145/3041021.3054199. URL https://doi.org/10.1145/3041021.3054199.

- Cornuejols and Tütüncü [2006] Gerard Cornuejols and Reha Tütüncü. Optimization methods in finance, volume 5. Cambridge University Press, 2006.

- [5] Alex Deng. Metric Sensitivity Decomposition. Causal Inference and Its Applications in Online Industry. https://alexdeng.github.io/causal/sensitivity.html#metric-sensitivity-decomposition. [Online; accessed 21-December-2022].

- Deng and Shi [2016] Alex Deng and Xiaolin Shi. Data-driven metric development for online controlled experiments: Seven lessons learned. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining, pages 77–86, 2016.

- Dmitriev and Wu [2016] Pavel Dmitriev and Xian Wu. Measuring metrics. In Proceedings of the 25th ACM international on conference on information and knowledge management, pages 429–437, 2016.

- Elliott [2023] Michael R. Elliott. Surrogate endpoints in clinical trials. Annual Review of Statistics and Its Application, 10(1):75–96, 2023. doi: 10.1146/annurev-statistics-032921-035359. URL https://doi.org/10.1146/annurev-statistics-032921-035359.

- Elliott et al. [2015] Michael R Elliott, Anna SC Conlon, Yun Li, Nico Kaciroti, and Jeremy MG Taylor. Surrogacy marker paradox measures in meta-analytic settings. Biostatistics, 16(2):400–412, 2015.

- Gelman [2006] Andrew Gelman. Prior distributions for variance parameters in hierarchical models (comment on article by Browne and Draper). Bayesian Analysis, 1(3):515 – 534, 2006. doi: 10.1214/06-BA117A. URL https://doi.org/10.1214/06-BA117A.

- Gelman et al. [1995] Andrew Gelman, John B Carlin, Hal S Stern, and Donald B Rubin. Bayesian data analysis. Chapman and Hall/CRC, 1995.

- Hernán and Robins [2010] Miguel A Hernán and James M Robins. Causal inference, 2010.

- Hohnhold et al. [2015] Henning Hohnhold, Deirdre O’Brien, and Diane Tang. Focus on the long-term: It’s better for users and business. In Proceedings 21st Conference on Knowledge Discovery and Data Mining, Sydney, Australia, 2015. URL http://dl.acm.org/citation.cfm?doid=2783258.2788583.

- Kallus and Mao [2022] Nathan Kallus and Xiaojie Mao. On the role of surrogates in the efficient estimation of treatment effects with limited outcome data, 2022.

- Lewandowski et al. [2009] Daniel Lewandowski, Dorota Kurowicka, and Harry Joe. Generating random correlation matrices based on vines and extended onion method. Journal of Multivariate Analysis, 100(9):1989–2001, 2009. ISSN 0047-259X. doi: https://doi.org/10.1016/j.jmva.2009.04.008. URL https://www.sciencedirect.com/science/article/pii/S0047259X09000876.

- Parast et al. [2017] Layla Parast, Tianxi Cai, and Lu Tian. Evaluating surrogate marker information using censored data. Statistics in medicine, 36(11):1767–1782, 2017.

- Phan et al. [2019] Du Phan, Neeraj Pradhan, and Martin Jankowiak. Composable effects for flexible and accelerated probabilistic programming in numpyro. arXiv preprint arXiv:1912.11554, 2019.

- Polson and Scott [2012] Nicholas G. Polson and James G. Scott. On the Half-Cauchy Prior for a Global Scale Parameter. Bayesian Analysis, 7(4):887 – 902, 2012. doi: 10.1214/12-BA730. URL https://doi.org/10.1214/12-BA730.

- Prentice [1989] Ross L. Prentice. Surrogate endpoints in clinical trials: definition and operational criteria. Statistics in medicine, 8(4):431–440, 1989.

- [20] Lenny Rachitsky. Choosing Your North Star Metric. https://future.com/north-star-metrics/.

- Richardson et al. [2023] Lee Richardson, Alessandro Zito, Dylan Greaves, and Jacopo Soriano. Pareto optimal proxy metrics. arXiv preprint arXiv:2307.01000, 2023.

- Schaible [1974] Siegfried Schaible. Parameter-free convex equivalent and dual programs of fractional programming problems. Zeitschrift für Operations Research, 18:187–196, 1974.

- Sharpe [1966] William F. Sharpe. Mutual fund performance. The Journal of Business, 39(1):119–138, 1966. ISSN 00219398, 15375374. URL http://www.jstor.org/stable/2351741.

- Sharpe [1998] William F Sharpe. The sharpe ratio. Streetwise–the Best of the Journal of Portfolio Management, 3:169–85, 1998.

- VanderWeele [2013] Tyler J. VanderWeele. Surrogate measures and consistent surrogates. Biometrics, 69(3):561–569, 2013. ISSN 0006341X, 15410420. URL http://www.jstor.org/stable/24538119.

- Wang et al. [2023] Xuan Wang, Layla Parast, Larry Han, Lu Tian, and Tianxi Cai. Robust approach to combining multiple markers to improve surrogacy. Biometrics, 79(2):788–798, 2023.

- Wang et al. [2022] Yuyan Wang, Mohit Sharma, Can Xu, Sriraj Badam, Qian Sun, Lee Richardson, Lisa Chung, Ed H Chi, and Minmin Chen. Surrogate for long-term user experience in recommender systems. In Proceedings of the 28th ACM SIGKDD Conference on Knowledge Discovery and Data Mining, pages 4100–4109, 2022.