C++ design patterns for low-latency applications including high-frequency trading

Abstract

This work aims to bridge the existing knowledge gap in the optimisation of latency-critical code, specifically focusing on high-frequency trading (HFT) systems. The research culminates in three main contributions: the creation of a Low-Latency Programming Repository, the optimisation of a market-neutral statistical arbitrage pairs trading strategy, and the implementation of the Disruptor pattern in C++. The repository serves as a practical guide and is enriched with rigorous statistical benchmarking, while the trading strategy optimisation led to substantial improvements in speed and profitability. The Disruptor pattern showcased significant performance enhancement over traditional queuing methods. Evaluation metrics include speed, cache utilisation, and statistical significance, among others. Techniques like Cache Warming and Constexpr showed the most significant gains in latency reduction. Future directions involve expanding the repository, testing the optimised trading algorithm in a live trading environment, and integrating the Disruptor pattern with the trading algorithm for comprehensive system benchmarking. The work is oriented towards academics and industry practitioners seeking to improve performance in latency-sensitive applications. The repository, trading strategy, and the Disruptor library can be found at https://github.com/0burak/imperial_hft.

1 Introduction

1.1 Aims

The overarching aim of this work is to enable individuals to optimise latency-critical code to improve speed. Specifically, the research focuses on programming strategies and data structures relevant to high-frequency trading. Given that the financial industry—particularly buy-side firms focusing on public markets—is secretive, there are not many resources available to guide novice programmers in the field of low-latency programming with a focus on trading. The strategy employed in this research to achieve this goal was to create a bespoke Low-Latency Programming Repository containing various techniques. This was accomplished through extensive research and statistical benchmarking. Using this repository, a systematic trading backtest strategy was optimised. Finally, to provide a holistic view of optimisation techniques for HFT, the Disruptor pattern was implemented in C++ to demonstrate how such data structure can be used in an Order Management Systems (OMS).

1.2 Research context

The existing body of literature on optimising various aspects of High-Frequency Trading (HFT) systems primarily originates from industry practitioners who are bound by confidentiality and competitive advantage considerations. Consequently, much of the cutting-edge research in the domain, particularly in areas such as latency improvements, code efficiency, and cache optimisation, remains a closely guarded secret. This underscores the challenge and also the need for academic and open-source initiatives aimed at understanding and improving the inner workings of HFT systems.

Several works have explored the broader domain of HFT from economic and financial perspectives, attempting to bridge the gap between financial research and computational research. Aldridge focussed on the overarching landscape, system strategies, and economic impact, while publications by Cartea et al. delve into the mathematical models that form the backbone of algorithmic trading systems [1, 14]. However, these works and other literature seldom provide detailed technical insight into aspects like code optimisation or latency reduction. Public talks and conference papers sometimes shed light on HFT systems and their design [34]. Yet, these platforms usually provide a macroscopic view, without direct benchmarking or applying the strategies to relevant systematic trading strategies. When it comes to language-specific research, literature on C++ is comparatively more abundant. However, this literature typically focuses on the design rationale behind C++ and its Standard Template Library, without translating these principles into the specific context of ultra-low-latency HFT systems [22, 50, 46, 51]. In the online domain, blogs and posts sometimes engage with this topic, albeit at a surface level. They often provide averaged latency data, without much analysis into the intricate behaviors affecting cache-access or instruction-execution latencies [42, 68, 44, 69, 11].

In light of these gaps, the present research aims to make a significant contribution by focusing on the computational and technical aspects of latency optimisation in HFT. This work will not only investigate but also implement and rigorously test various programming strategies within an HFT context, offering insights for both academics and industry practitioners.

1.3 Summary

Section 2 explores existing literature and software relevant to the field. Section 2.1 delves into High-Frequency Trading, elucidating its key elements and components such as Data Feed, OMS, Algorithmic Trading Strategies, Risk Management, and Execution Infrastructure. This section also highlights the role of hardware, like FPGAs, in achieving low-latency targets. Section 2.2 evaluates the suitability of the C++ language for HFT, contrasting it with other languages like Java and Rust, and elaborating on specific C++ features beneficial for low-latency applications. Section 2.3 lists and briefly describes various programming strategies and design patterns aimed at optimising C++ code for lower latencies in HFT systems, including Cache Warming, Compile-time Dispatch, and SIMD, among others. Section 2.4 introduces the LMAX Disruptor, a high-performance, low-latency messaging framework designed to minimize contention and latency in concurrent systems. It offers advantages such as efficient memory allocation and optimised sequencing mechanisms for enhanced scalability. Section 2.5 discusses the significance of benchmarking in High-Frequency Trading, specifically addressing the features and limitations of the Google Benchmark library for code performance optimisation in such environments. Section 2.6 outlines the critical role of networking in HFT, detailing technologies and strategies—like fiber-optic communications, colocation, and specialized hardware—geared toward minimizing latency. This section also touches upon the regulatory landscape that shapes these choices. Section 3 contains the Low-Latency Programming Repository. The section is broken down into five sections: compile-time features, optimisation techniques, data handling, concurrency, and system programming. Each section elaborates on their respective programming techniques. Section 4 outlines a market-neutral trading strategy, statistical arbitrage pairs trading, that leverages the mean-reverting nature of price spreads between cointegrated assets. This section focuses on its quantitative foundations, execution methodology, and risk management aspects. It also delves into the critical concept of cointegration, presents the algorithm through a case study involving Goldman Sachs and Morgan Stanley, and discusses CPU-level optimisations for reducing latency. Section 5 details the development and testing of a C++ implementation of the LMAX Disruptor, a high-performance, lock-free inter-thread communication library. This library significantly outperforms traditional queuing methods in both latency and speed by leveraging a ring buffer, sequence numbers, and a specialized waiting strategy. Section 6 evaluates the performance of the Low-Latency Programming Repository, the trading algorithm, and the Disruptor pattern through multiple metrics. These include user feedback, speed improvements, and statistical significance. The section highlights areas for improvement and discusses the impact of latency reduction on trading profitability and risk. Section 7 concludes this work and highlights potential future directions.

1.4 Contributions

This work offers both academic and practical contributions to the fields of low-latency programming and high-frequency trading (HFT). The research furnishes comprehensive insights into low-latency programming techniques, as well as the strategies prevalent in the high-frequency trading industry.

-

•

Low-Latency Programming Repository: This repository serves as more than just a theoretical compendium; it is a practical guide enriched by rigorous statistical benchmarking. It offers a curated collection of programming techniques, design patterns, and best practices, all of which are tailored to mitigate latency in HFT systems.

-

•

Optimisation of Market-Neutral Trading Strategy: The research led to the successful optimisation of a market-neutral statistical arbitrage pairs trading strategy. This was accomplished through the integration of latency-reduction techniques and CPU-level optimisations. As a result, the trading strategy has shown notable improvements in both execution speed and profitability.

-

•

Creation of the Disruptor Pattern Library in C++: This implementation yielded a significant performance enhancement over traditional queuing methods, thus underscoring the real-world applicability and benefits of the Disruptor pattern in latency reduction. It particularly highlights the possible implementation of such a data structure in an HFT system’s Order Management System (OMS).

In summary, this work provides contributions in both the research and software library domains, benefiting a broad spectrum of readers ranging from academics to industry practitioners.

2 Background

2.1 HFT

High-frequency trading (HFT) is an automated trading strategy that utilises technology and algorithms to execute numerous trades at high speeds. Defining HFT precisely can be challenging as it encompasses various aspects of both computer science and finance. The SEC Concept Release on Equity Market Structure outlines five key elements that define this discipline, including high-speed computing, co-location practices, short timeframes for position establishment and liquidation, the submission of multiple promptly followed by cancelled orders, and the objective of concluding the trading day with minimal unhedged positions and near-neutral exposure overnight [18]. HFT systems are mainly built from five main components, including the data feed, order management system (OMS), trading strategies, risk management, and execution infrastructure such as networking. The primary areas of focus in this work will be the trading strategy and OMS.

The data feed is responsible for receiving and processing real-time market data from various sources, enabling the algorithms to make buy, sell, or wait decisions. The order management system (OMS) component handles the submission, routing, and monitoring of trade orders, ensuring efficient execution and management of trading activities. Trading strategies form a critical component of HFT systems, as they employ automated algorithms to identify market opportunities, make trading decisions, and execute trades at high speeds. HFT systems encompass four main sections: arbitrage, directional event-based trading, automated market making, and liquidity detection [1]. Within these sections, a variety of trading algorithms are utilised. Statistical arbitrage involves identifying pricing discrepancies between related financial instruments and taking advantage of those discrepancies by simultaneously buying and selling the instruments to profit from the price convergence. Momentum trading strategies focus on exploiting short-term price trends and market momentum, aiming to identify and capitalize on price movements in the direction of the prevailing trend. Pairs trading involves identifying pairs of securities with a historically established correlation and taking simultaneous long and short positions in the two securities, aiming to profit from the convergence or divergence of their prices. Liquidity detection algorithms are designed to identify and trade in illiquid or thinly traded instruments, leveraging advanced data analysis techniques to identify opportunities in less liquid markets or specific trading conditions. News-based Trading algorithms are designed to process and react to news events, such as economic releases or corporate announcements, aiming to exploit market reactions by quickly executing trades based on predefined criteria [34]. Risk management plays a crucial role in HFT systems by implementing measures to assess and mitigate potential risks associated with high-speed trading, ensuring the preservation of capital and minimizing losses. Execution Infrastructure, including networking components, provides the necessary technological framework for low-latency communication and trade execution in HFT systems. Additionally HFT firms make strong use of Field Programmable Gate Arrays (FPGAs) to achieve low-latency targets. FPGAs are a type of programmable circuit which are designed to be configured after manufacturing. FPGAs can execute specific trading algorithms up to 1000 times faster than conventional computers [37]. Donadio elucidates that the four key characteristics of FPGAs are programmability, capacity, parallelism, and determinism [26]. First, FPGAs are easily programmable and reprogrammable, capable of handling complex trading algorithms due to their configurable logic blocks (CLBs) and flexible switches. Second, they offer immense capacity with millions of CLBs, although this capacity has physical limitations related to signal propagation times on the silicon die. Third, unlike CPUs that have a fixed architecture and operating system overhead, FPGAs operate on a parallel architecture, allowing multiple code paths to run simultaneously without resource contention, thereby enhancing resilience and speed in trading operations. Lastly, FPGAs offer a high level of determinism, providing repeatable and predictable performance, which is particularly helpful during bursts of market activity. These attributes collectively make FPGAs a powerful tool for HFT, offering advantages in speed, capacity, and reliability. By eliminating software layers and reducing overhead, traders can directly implement algorithms in FPGA hardware, accelerating critical computations and significantly speeding up trading algorithms in HFT. However, this work will primarily focus on software and programming methods for achieving low-latency, excluding discussions on FPGAs and similar hardware solutions.

According to a 2017 estimate by Aldridge and Krawciw, HFT accounted for 10-40% of trading volume in equities and 10-15% in foreign exchange and commodities in 2016 [2]. Given the substantial trading volumes and profound impact on financial markets, there is an abundance of information available regarding the economic effects of HFT [48, 14]. However, the literature on the computational and technical aspects of HFT is limited due to the secretive nature of the industry and potential conflicts of interest. Fortunately, there are some insights available from industry experts regarding the requirements for building HFT software, for example ([22, 50, 46, 21, 49, 42, 68]). Carl Cook has covered several C++ optimisation strategies, including Variadic templates, Loop unrolling, Constexpr, and more [46]. This work aims to build upon existing resources and offer the reader a comprehensive compilation of tested data on the performance enhancements achieved through the implementation of these programming strategies within the applied context of HFT.

2.2 C++

Low-latency applications such as the ones utilised in HFT tend to prioritise compile-time overhead over runtime overhead, making compiled languages like C++, Java, and Rust more suitable. However, Python is not very well suited for such applications due to its interpreted nature, as it introduces runtime overhead. C++ is one of the most popular choices for building software-based HFT systems. This is attributed to the language’s fundamental design principles, Ghosh highlights that C++ is preferred for low-latency applications due to its compiled nature, close proximity to hardware, and control over resources, which allow for optimised performance and efficient resource management [33]. Its rich feature set, including static typing, multiple programming paradigms, and extensive libraries, make it a versatile and highly portable language [59, 60]. However, Rust has emerged as an upcoming alternative to C++ in recent years. Rust offers advantages such as memory safety, concurrency support, developer productivity, performance, and a growing ecosystem, making it an appealing choice for HFT systems development [51]. C++ gained popularity in performance-driven industries due to its “zero-overhead” principle. This principle is a broad term but it can be witnessed through many ways. For example C++ does not have a garbage collector. This means that programmers must manually allocate and deallocate memory which leads to a more efficient and deterministic memory usage and avoids unnecessary overhead. However, it’s worth noting that Java has been successfully used in latency-critical applications, such as the development of the Disruptor by the LMAX Group, as discussed in greater detail in Section 2.4. Java mitigates the impact of garbage collection in the Disruptor pattern by preallocating and reusing objects within the ring buffer, minimizing frequent memory allocation and subsequent garbage collection pauses. Under specific circumstances, Java can exhibit superior performance compared to C++, particularly when the virtual machine and garbage collector are carefully optimised to align with the application’s garbage collection interrupt frequency. Such fine-tuning can lead to Java outperforming C++ in certain scenarios, as observed by Chandler Carruth [21]. Furthermore, Aldrige highlights the example of the Nasdaq OMX system, which is developed in Java with the garbage collector disabled [1]. In contrast to Java, Rust does not employ a garbage collector. Instead, Rust utilises its unique ownership system and “ownership and borrowing” concept to manage memory. The ownership system ensures that each piece of memory has a single owner at any given time, and Rust automatically frees the memory when the owner goes out of scope. This approach provides a middle ground between the memory management models of C++ and Java.

Additionally, C++ offers various techniques to shift processing tasks from runtime to compile-time. For instance, templates enable developers to move the runtime overhead associated with dynamic polymorphism to compile-time in exchange for flexibility. The “Curiously Recurring Template Pattern” is a notable example in this regard. Another technique utilised in C++ is the use of inline functions, which allows the compiler to directly insert the function’s code at the call site. This reduces the overhead of a standard function call. Finally, the “constexpr” keyword can be used to evaluate computations at compile time instead of runtime, resulting in quicker and more efficient code execution. These techniques contribute to C++’s versatility and enable optimisation at the compile-time level, enhancing performance. As C++ is one of the most suitable languages for HFT, it will be the focus of this work. However, it is important to consider that factors such as the compiler (and its version), machine architecture, 3rd party libraries, build and link flags can also affect latency. Therefore, it is crucial to examine the machine instructions produced by C++. To accomplish this, Compiler Explorer will be utilised. Compiler Explorer, designed by Matt Godbolt, is an online platform that enables users to explore and analyze the output generated by various compilers for different programming languages. It provides an interface for writing code and viewing the corresponding compiled assembly or intermediate representations of the code. Rasovsky discussed the challenges of benchmarking time-sensitive operations in a high-frequency trading environment. Rasovsky initially found that the commonly used clock_gettime system call appeared to be 85 times slower than using Intel’s Time Stamp Counter (TSC) on a benchmarking website, but upon running tests on her actual server, the gap narrowed to only twice as slow [23]. The talk emphasizes the importance of context-sensitive benchmarking and reveals how different environments and underlying system configurations can dramatically impact performance metrics.

2.3 Design patterns

Design patterns and programming strategies will be used interchangeably throughout this work. As mentioned earlier there are many ways to optimise C++ code to achieve lower latencies. The strategies that will be examined in this work are as follows.

-

•

Cache Warming: To minimize memory access time and boost program responsiveness, data is preloaded into the CPU cache before it’s needed [50].

-

•

Compile-time Dispatch: Through techniques like template specialization or function overloading, optimised code paths are chosen at compile time based on type or value, avoiding runtime dispatch and early optimisation decisions.

-

•

Constexpr: Computations marked as constexpr are evaluated at compile time, enabling constant folding and efficient code execution by eliminating runtime calculations [46].

-

•

Loop Unrolling: Loop statements are expanded during compilation to reduce loop control overhead and improve performance, especially for small loops with a known iteration count.

-

•

Short-circuiting: Logical expressions cease evaluation when the final result is determined, reducing unnecessary computations and potentially improving performance.

-

•

Signed vs Unsigned Comparisons: Ensuring consistent signedness in comparisons avoids conversion-related performance issues and maintains efficient code execution.

-

•

Avoid Mixing Float and Doubles: Consistent use of float or double types in calculations prevents implicit type conversions, potential loss of precision, and slower execution.

-

•

Branch Prediction/Reduction: Accurate prediction of conditional branch outcomes allows speculative code execution, reducing branch misprediction penalties and improving performance.

-

•

Slowpath Removal: Optimisation technique aiming to minimize execution of rarely executed code paths, enhancing overall performance.

-

•

SIMD: Single Instruction, Multiple Data (SIMD) allows a single instruction to operate on multiple data points simultaneously, significantly accelerating vector and matrix computations.

-

•

Prefetching: Explicitly loading data into cache before it is needed can help in reducing data fetch delays, particularly in memory-bound applications.

-

•

Lock-free Programming: Utilises atomic operations to achieve concurrency without the use of locks, thereby eliminating the overhead and potential deadlocks associated with lock-based synchronization.

-

•

Inlining: Incorporates the body of a function at each point the function is called, reducing function call overhead and enabling further optimisation by the compiler.

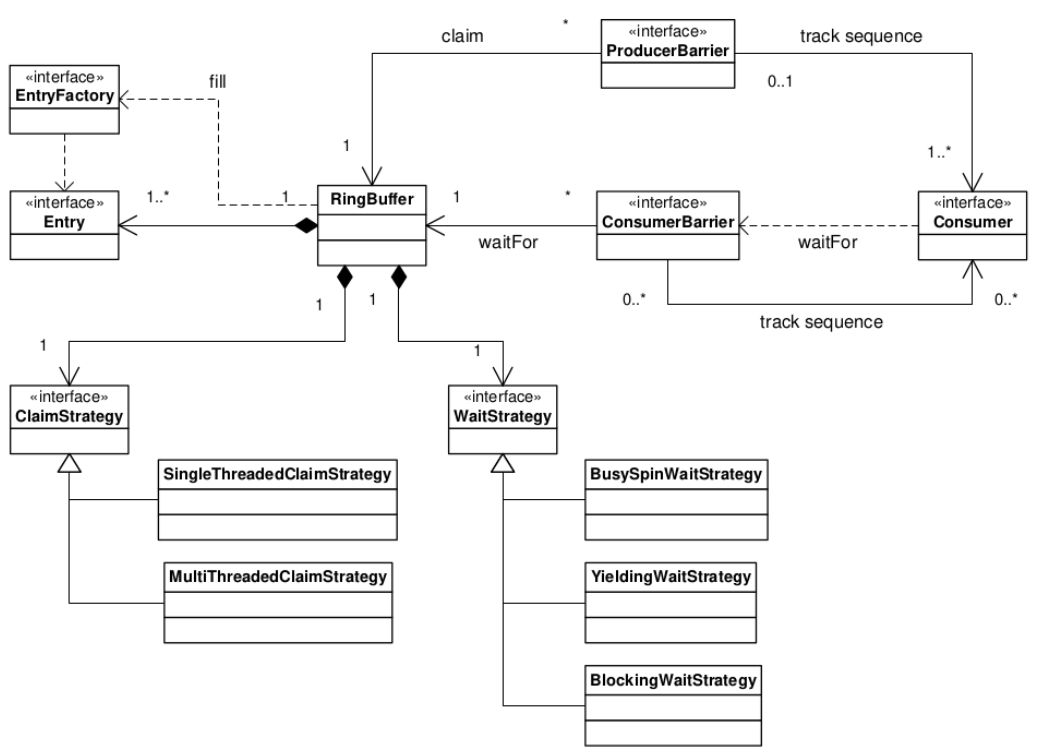

2.4 LMAX Disruptor

The LMAX Disruptor was created by LMAX Exchange to address the specific requirements of their high-performance, low-latency trading system. The LMAX Disruptor offers a highly optimised and efficient messaging framework that enables concurrent communication between producers and consumers with minimal contention and latency [63]. Traditional multithreaded applications often suffer from contention issues when multiple threads try to access shared resources concurrently. Locking mechanisms, such as mutexes or semaphores, are commonly used to synchronize access to shared data structures, but they can introduce significant overhead and contention, leading to poor scalability and increased latency. This is because locks require arbitration when contended, and this arbitration is achieved by a context switch. However, context switches are costly as the cache associated with the previous thread or process may be invalidated, causing cache misses. The cache might also need to be flushed, resulting in additional latency. Finally, when a new thread or process starts, it takes time to populate the cache with relevant data, affecting performance initially [63].

Another way to tackle contention is the use of Compare And Swap (CAS) operations. CAS is an atomic instruction used in concurrent programming to implement synchronization and ensure data integrity in multi-threaded environments. It is a fundamental building block for lock-free and wait-free algorithms. Firstly, each thread involved in the CAS operation reads the current value of the shared variable from memory. Next, the thread compares this current value with its expected value, which it has in mind. If the current value matches the expected value, indicating that no other thread has modified the shared variable since the read operation, the thread proceeds to atomically swap the current value with a new desired value. Following the swap, the CAS operation returns a status indicating whether the swap was successful or not. If successful, it signifies that the thread has successfully updated the shared variable; otherwise, it means that another thread had modified the shared variable in the meantime, requiring the thread to retry the CAS operation. CAS is definitely better than the use of locks, but they’re still not cost-free. Firstly, orchestrating a complex system using CAS operations can be harder than the use of locks. Secondly, to ensure atomicity, the processor locks its instruction pipeline, and a memory barrier is used to ensure that changes made by a thread become visible to other threads [63]. Queues can be implemented using linked lists or arrays, but unbounded queues can lead to memory exhaustion if producers outpace consumers. To prevent this, queues are often bounded or actively tracked in size. However, bounded queues introduce write contention on head, tail, and size variables, leading to high contention and potential cache coherence issues. Managing concurrent access to queues becomes complex, especially when dealing with multiple producers and consumers.

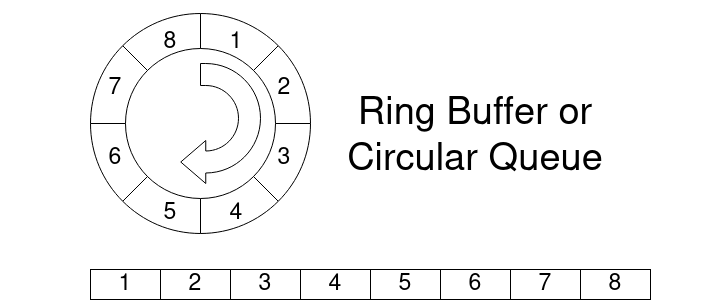

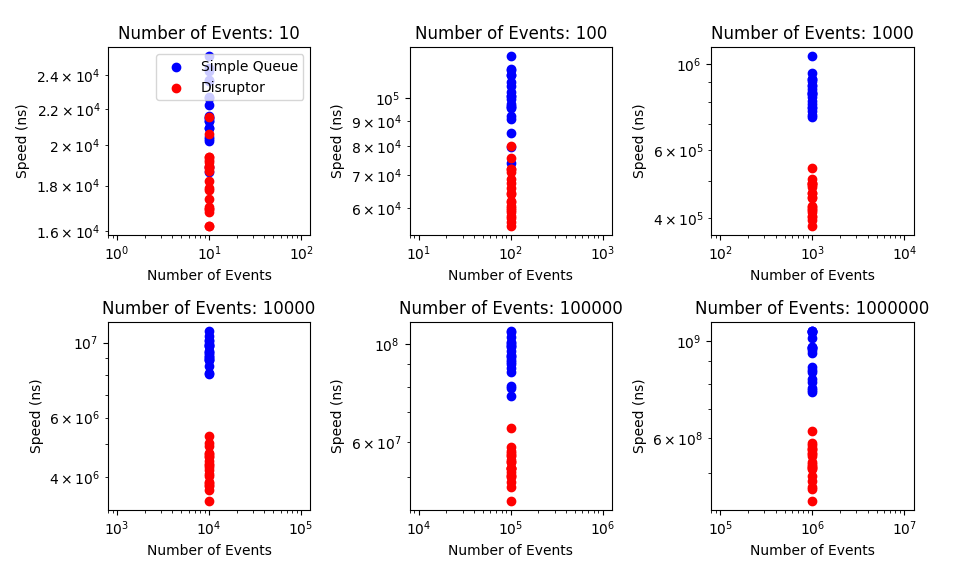

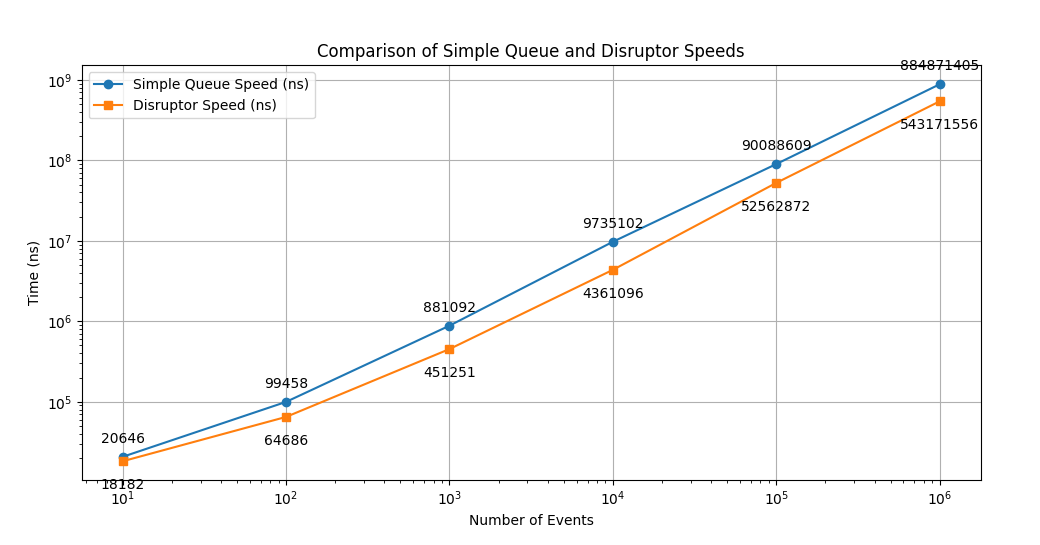

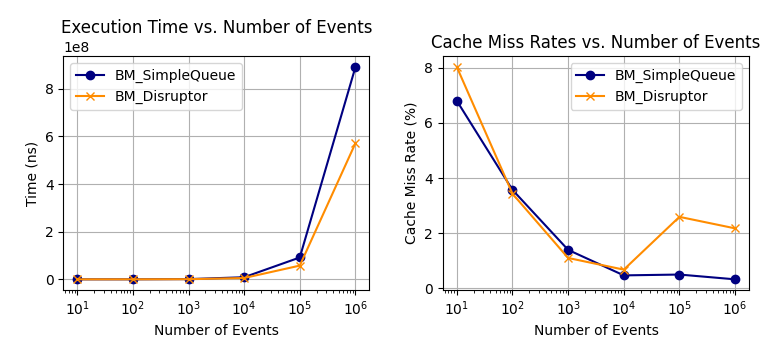

The LMAX Disruptor aims to resolve the mentioned issues and optimise memory allocation efficiency while operating effectively on modern hardware. It achieves this through a pre-allocated bounded data structure called a ring buffer. Producers add data to the ring buffer, and one or more consumers process it. According to LMAX’s benchmark results, they state that the Disruptor achieves significantly lower mean latency, by three orders of magnitude, compared to an equivalent queue-based approach in a three-stage pipeline [63]. Additionally, the Disruptor demonstrates approximately 8 times higher throughput handling capacity [63]. The ring buffer can store either an array of pointers to entries or an array of structures representing the entries. Typically, each entry in the ring buffer does not directly contain the data being passed but serves as a container or holder for the data. As the LMAX Disruptor was built on Java, the garbage collector was an issue. As mentioned earlier, the ring buffer is pre-allocated, meaning the entries in the buffer do not get cleaned up by the garbage collector, and they exist for the lifetime of the Disruptor. In most use cases of the Disruptor, there is typically only one producer, such as a file reader or network listener, resulting in no contention on sequence/entry allocation. However, in scenarios with multiple producers, they race to claim the next available entry in the ring buffer, which can be managed using a CAS operation on the sequence number. Once a producer copies the relevant data to the claimed entry, it can make it public to consumers by committing the sequence. Consumers wait for a sequence to become available before reading the entry, and various strategies can be employed for waiting, including condition variables within a lock or looping with or without thread yield. The Disruptor avoids CAS contention present in lock-free multi-producer-multi-consumer queues, making it a scalable solution.

Sequencing is a fundamental concept in the Disruptor for managing concurrency. Producers and consumers interact with the ring buffer based on sequencing. Producers claim the next available slot in the sequence, which can be a simple counter or an atomic counter with CAS operations. Once a slot is claimed, the producer can write to it and update a cursor representing the latest entry available to consumers. Consumers wait for a specific sequence by using memory barriers to read the cursor, ensuring visibility of changes. Consumers maintain their own sequence to track their progress and coordinate work on entries. In cases with a single producer, locks or CAS operations are not needed, and concurrency coordination relies solely on memory barriers. The Disruptor offers an advantage over queues when consumers wait for an advancing cursor in the ring buffer. If a consumer notices that the cursor has advanced multiple steps since it last checked, it can process entries up to that sequence without involving concurrency mechanisms. This allows the consumer to quickly catch up with producers during bursts, balancing the system. This batching approach improves throughput, reduces latency, and provides consistent latency regardless of load until the memory system becomes saturated.

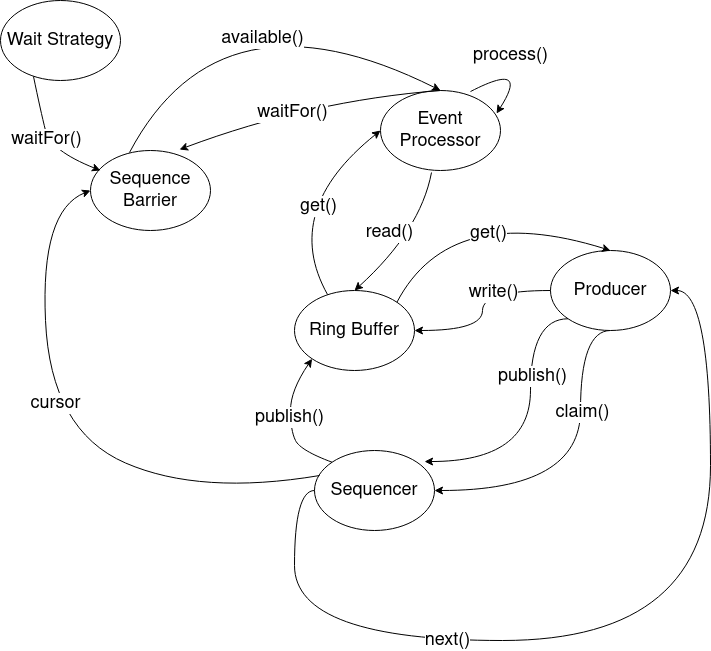

The Disruptor framework can be seen in Figure 1. It simplifies the programming model by allowing producers to claim entries, write changes into them, and commit them for consumption via a ProducerBarrier. Consumers only need to implement a BatchHandler to receive callbacks when new entries are available. This event-based programming model shares similarities with the Actor Model.

By separating concerns that are typically intertwined in queue implementations, the Disruptor enables a more flexible design. The central component is the RingBuffer, which facilitates data exchange without contention. Producers and consumers interact with the RingBuffer independently, with concurrency concerns handled by the ProducerBarrier for slot claiming and dependency tracking, and the ConsumerBarrier for notifying consumers of new entries. Consumers can be organized into a dependency graph, representing multiple stages in a processing pipeline.

2.5 Benchmarking

In the realm of HFT, where decisions are made in microseconds, optimising the code performance becomes an absolute necessity. Given the spped at which trades are conducted, even minor improvements can have significant impacts on the overall performance and profitability. The challenge, therefore, lies in effectively identifying, analysing, and implementing these enhancements, a task that necessitates the deployment of robust profiling and benchmarking tools. In this work two main tools were used, Google Benchmark for speed and perf (Linux) for cache analysis.

Google Benchmark

Google Benchmark is an open-source library designed for benchmarking the performance of code snippets in C++ applications. However, it is critical to evaluate the appropriateness of Google Benchmark for HFT environments. One of the standout features of Google Benchmark is its use of statistically rigorous methodology. The library performs multiple iterations of specific code snippets or functions, thereby generating accurate performance metrics. Such precision in performance measurement is critical in the context of HFT, where the software stack’s efficiency can directly influence the trading strategy’s efficacy. Furthermore, Google Benchmark offers an impressive versatility with its support for multiple benchmarking modes, including CPU-bound and real-time modes. This can, in turn, guide the code optimisation strategies to meet the specific requirements of applications. However, it is important to note that while Google Benchmark excels in providing detailed performance metrics, it might not cover some specifics unique to HFT scenarios, such as network latency, co-location effects, and hardware timestamping, among others. It primarily focuses on CPU-bound tasks, which may not always reflect the entire performance landscape in HFT [43]. Therefore, while Google Benchmark serves as a powerful tool in optimising code and improving computational efficiency, it should be supplemented with other performance analysis tools that can monitor and optimise these HFT-specific factors.

perf (Linux)

The perf tool, also known as Performance Counters for Linux (PCL), is a sophisticated performance monitoring utility that is integrated into the Linux kernel. It provides a rich set of commands and options for profiling and tracing software performance and system events at multiple layers, from hardware-level instruction cycles to application-level function calls. For this work perf was utilised for cache analysis, in particular cache misses.

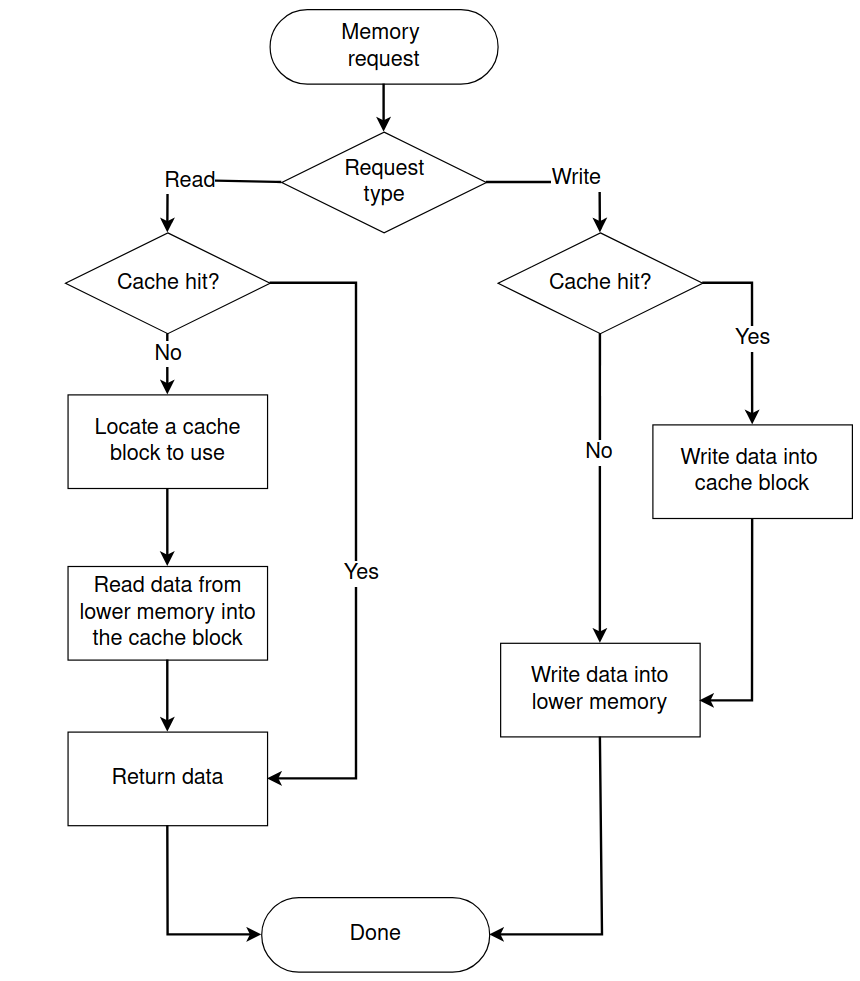

2.6 Cache analysis

In computer science, a cache is a hardware or software component that stores a subset of data, typically transient in nature, so that future requests for that data can be served more rapidly [56]. The data most recently or frequently accessed is usually stored in the cache, as subsequent reads or writes to the same data can often be completed more quickly. By storing data closer to the processor or the end-user, the cache reduces latency and improves I/O efficiency, thus accelerating data access and enhancing overall system performance. Caches are implemented in various levels of a computing architecture, including but not limited to, CPU caches (L1, L2, L3), disk caches, and even distributed network caches [57]. The terms “cache hit” and “cache miss” refer to the efficacy of data retrieval from the cache. A cache hit occurs when a data request can be fulfilled by the cache, negating the need to access the slower, underlying data store, whether that be main memory, disk storage, or a remote server [41]. This results in a faster response time and less resource utilisation for the specific data operation. Conversely, a cache miss signifies that the requested data is not present in the cache, necessitating a fetch from the slower data store to both fulfill the current request and update the cache for potential future accesses [41]. Cache misses are generally more expensive in terms of time and computational resources, and they can occur for various reasons, including the first-time access of data (cold start), eviction of data due to cache size limitations, or an ineffective cache management strategy [70]. Figure 2 outlines this concept. The ratio of cache hits to total access attempts is often used as an important metric for evaluating the effectiveness of a cache system, and is a metric which is used in this work for evaluation of both the trading strategy and the Disruptor pattern.

2.7 Networking

Low-latency networks are the linchpin of high-frequency trading. Although networking is not a key aspect of this work it is still important to inform the reader with the basic understanding of the surrounding pieces of a complex HFT system. The propagation delays in transmitting information can have immediate financial implications. As such, most HFT firms opt for fiber-optic communication to enable data transmission at speeds close to the speed of light [1]. However, firms are continuously researching ways to shave off additional microseconds. One such method is through the use of microwave and millimeter-wave communications. Such technologies bypass the physical limitations of fiber-optic cables and can transmit data even faster over shorter distances [44]. Colocation remains a crucial strategy for HFT firms, providing them the benefit of proximity to a stock exchange’s data center, thus further minimizing latency [69, 11]. The advantages gained through colocation have led to its commercialization, with exchanges now charging significant fees for premium colocation services [4]. Beyond networking protocols and physical infrastructure, HFT firms invest in specialized hardware. Field-Programmable Gate Arrays (FPGAs) and Application-Specific Integrated Circuits (ASICs) are common choices, as they can execute trading algorithms more efficiently than general-purpose processors [58, 36]. Another critical aspect is the network topology used within the trading infrastructure. The design of these networks focuses on maximizing speed and minimizing the number of hops between network nodes. This often involves direct connections between key components in the trading infrastructure, thereby avoiding potential points of latency and failure [1, 19]. While speed is of the essence, the robustness and security of the network cannot be compromised. Redundancy measures are usually put in place, including dual network paths, failover systems, and backup data centers to maintain a 100% uptime [40, 1]. The rising threats of cyber-attacks also necessitate that HFT firms employ robust security protocols to protect their systems [24]. Continuous monitoring and real-time analytics are also crucial for maintaining optimal performance. HFT firms utilise network monitoring solutions that can detect and alert in real-time if the latency exceeds predetermined thresholds [47, 61]. Additionally time is a critical factor in high-frequency trading, and the use of precise time-synchronization protocols like Precision Time Protocol (PTP) is becoming increasingly important. Accurate timestamping of events allows for fairer market conditions and is often a regulatory requirement [12]. Advancements in networking technology have attracted the attention of regulators concerned about market fairness. Regulations like the U.S. SEC’s Regulation NMS (National Market System) aim to foster both innovation and competition while maintaining a level playing field for investors [10, 64]. In summary, the networking technology in HFT is an intricate web of hardware, software, and topological design optimised for speed and reliability. It is a dynamic field with continuous innovation, driven by the relentless pursuit of a competitive advantage and also shaped by regulatory considerations.

3 Low-Latency Programming Repository

This section contains the Low-Latency Programming Repository, whichc can be accessed from https://github.com/0burak/imperial_hft. The programming techniques are aggregated into five main categories: compile-time features, optimisation techniques, data handling, concurrency, and system programming.

3.1 Compile-Time Features

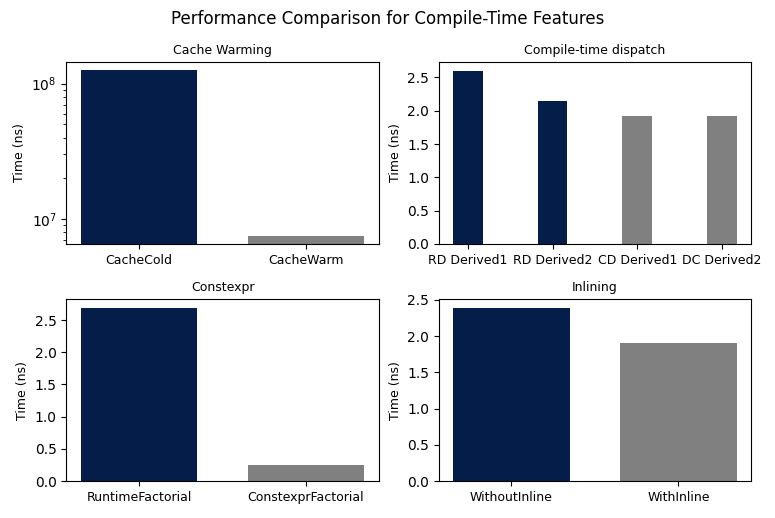

Cache Warming

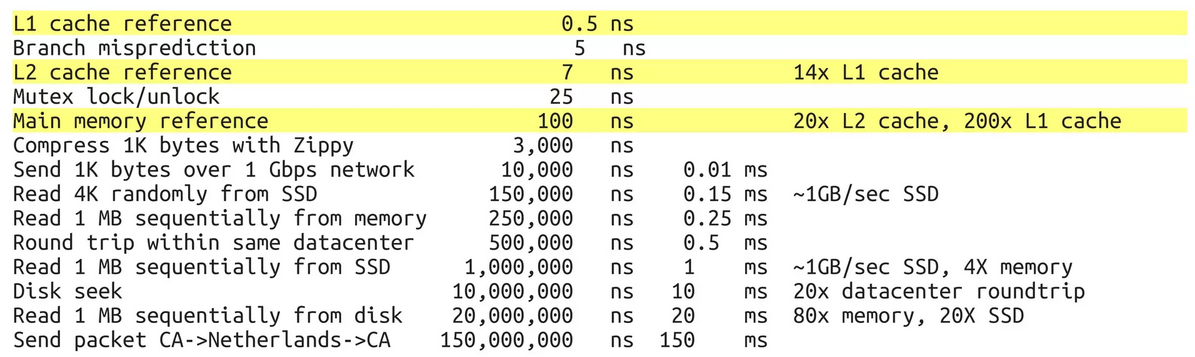

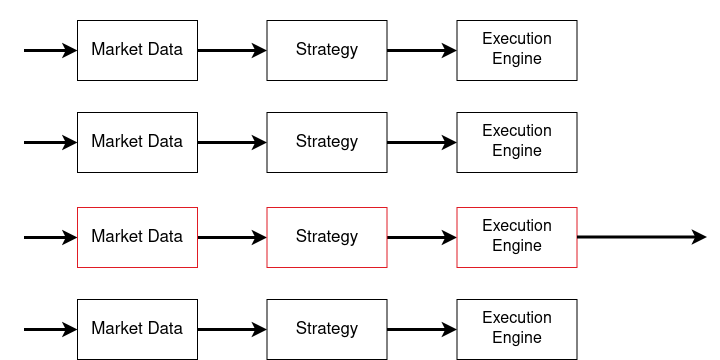

Cache warming, in computing, refers to the process of pre-loading data into a cache memory from its original storage disk, with the intent to accelerate data retrieval times. The logic behind this practice is that accessing data directly from the cache, which is considerably faster than the hard disk or even solid-state drives, significantly reduces latency and improves overall system performance. By pre-loading or “warming up” the cache, the system is prepared to serve the required data promptly when it is needed, bypassing the need to retrieve it from the slower primary storage. Figure 3 highlights the speed difference for accessing data in different levels of the cache. This technique is particularly useful when the data access pattern is predictable, allowing specific data to be pre-loaded efficiently into the cache.

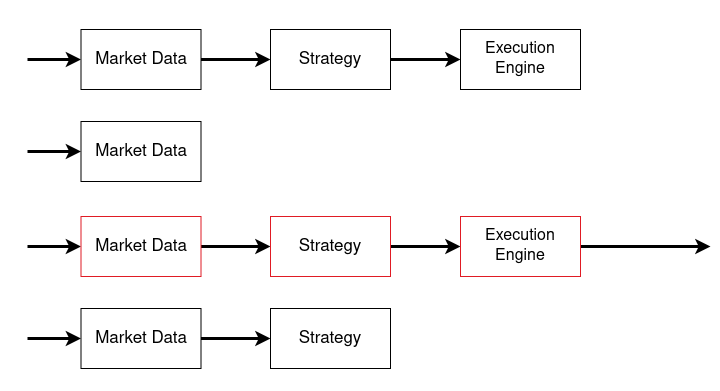

In HFT, the execution path that reacts to a trade signal is known as the hot path [1]. Although the hot path isn’t triggered frequently, when it is, it’s vital for it to run swiftly due to the extremely tight time frames HFT operates on. To achieve this speed, cache warming is utilised. Cache warming pre-loads the necessary data and instructions for the hot path into the cache [67, 50]. This means when a trade signal is detected, the system can immediately access the required data from the fast cache memory, rather than slower storage mediums, significantly reducing latency and potentially increasing the success rate of the trade. This approach leverages the waiting periods in HFT to prepare, or warm, the cache for instantaneous action once a trading signal occurs. As observed in Figure 4, the execution engine code is not executed every time therefore when it needs to be executed the cache is not warm. However in Figure 5, the execution engine code is executed every single time but only released the order when a trade must be placed. This keeps the cache “warm”.

Two scenarios are tested: BM_CacheCold and BM_CacheWarm. In BM_CacheCold, data is accessed in a random order, creating a situation where the cache is “cold”—data has to be fetched from the main memory, which incurs significant latency. In BM_CacheWarm, the cache is “warmed up” by accessing data in a sequential order. In this scenario, the data is already present in the cache (due to the spatial locality principle), resulting in faster access times. The benchmark::DoNotOptimise function is used to prevent the compiler from optimizing the code during the warming-up and testing process.

From the benchmark results, it can be seen that the warm cache scenario (BM_CacheWarm) performed significantly better than the cold cache scenario (BM_CacheCold). The cold cache test took approximately 267,685,006 nanoseconds, while the warm cache test took about 25,635,035 nanoseconds. This indicates that cache warming resulted in an immense speed improvement of about . This dramatic improvement is due to the fact that, with cache warming, the data required for computations is readily available in the cache, eliminating the need to fetch it from the main memory. Therefore, these results underscore the value and efficiency of cache warming in scenarios where data access patterns are predictable and regular.

To further examine the results, perf was used to analyse cache utilisation behaviour. The results can be seen in Table 1. The Cache Cold scenario entailed accessing elements from a large array in a random order, thereby demonstrating poor spatial and temporal locality. This resulted in a high number of cache misses, with approximately of all cache references leading to a miss. On the other hand, the BM_CacheWarm scenario involved a pre-pass that accessed data in a sequential manner before the timed loop. This access pattern leveraged spatial locality, effectively reducing the total number of cache references. Interestingly, the cache miss rate remained relatively stable in both scenarios— in BM_CacheCold versus in BM_CacheWarm. However, the total number of cache references was lower in the BM_CacheWarm case, thereby illustrating more efficient cache utilisation.

The difference in execution time between the two scenarios further emphasizes the impact of cache behavior. The BM_CacheWarm scenario exhibited significantly lower execution time due to its more efficient use of cache, despite the large data set that likely exceeded any cache level’s capacity. The instruction count also increased substantially in the BM_CacheWarm case, which can be attributed to the higher number of iterations executed in the same loop owing to the time saved by reduced cache misses. This experiment underscores the critical role that cache access patterns play in affecting program performance, even when the cache miss rate exhibits only minor variations.

| Metrics | BM_CacheCold | BM_CacheWarm |

|---|---|---|

| Speed (ns) | 267,685,006 | 25,635,035 |

| Instructions | 4,931,929,489 | 12,013,354,366 |

| Cache References | 146,264,562 | 61,306,992 |

| Cache Misses (% of all cache refs) | 73.964 | 71.559 |

Compile-time dispatch

Runtime dispatch and compile-time dispatch are two techniques in object-oriented programming that determine which specific function gets executed [35]. Runtime dispatch, also known as dynamic dispatch, resolves function calls at runtime. This method is primarily associated with inheritance and virtual functions [13]. In such cases, the function that gets executed relies on the object’s type at runtime. Conversely, compile-time dispatch determines the function call during the compilation phase and is frequently used in conjunction with templates and function overloading. Since the dispatch decision occurs during compilation, it typically results in swifter execution, eliminating the runtime overhead.

In the benchmark results, a distinct performance difference emerges between runtime and compile-time dispatch. For the runtime dispatch test, BM_RuntimeDispatch, times were and for Derived1 and Derived2 respectively. In contrast, the compile-time dispatch test, BM_CompileTimeDispatch, recorded a more efficient time of for both Derived1 and Derived2. These data points underscore the efficiency of compile-time dispatch, which shaves off approximately and in execution time respectively. The noted efficiency in compile-time dispatch is due to decisions about function calls being made during the compilation phase. By bypassing the decision-making overhead present in runtime dispatch, programs can execute more swiftly, thus boosting performance.

Constexpr

Constexpr is a keyword in C++ facilitating the evaluation of expressions during compilation rather than runtime [59]. Its advantage lies in enhancing performance by computing values at compile time, thus obviating the necessity for runtime computations. This is particularly helpful for constant expressions with values determinable at compile time. In the present study, an experiment delved into the performance contrast between two computation methodologies: computation at compile-time using C++’s constexpr keyword and conventional runtime computation. Google Benchmark tool gauged the time necessary to ascertain the factorial of 10 through two analogous functions: one utilising constexpr and another adhering to standard runtime computations.

Both the constexpr function, termed factorial, and its parallel, runtime_factorial, are functionally congruent, employing recursion for factorial computations. Their distinctive feature is the incorporation of the constexpr keyword in the former, informing the compiler of its potential for compile-time computations. Performance evaluation hinged on two benchmark functions, BM_ConstexprFactorial and BM_RuntimeFactorial. These functions invoke the factorial and runtime_factorial functions within a repetitive framework. The benchmark::DoNotOptimise function was integrated within both benchmarks to deter the compiler from early optimisation of the factorial calculation, ensuring accurate performance metrics. Data showcased a notable performance gap between the factorial functions. The constexpr function recorded a computational span of approximately nanoseconds per iteration, while its runtime counterpart necessitated a heftier nanoseconds per iteration. These results suggest the constexpr function’s speed exceeded its runtime counterpart by about in computing the factorial of 10. However, it’s imperative to understand that this marked performance variance doesn’t imply constexpr consistently amplifies runtime speed. The primary objective of the constexpr keyword is to shift computations from runtime to compile-time, not necessarily to boost runtime velocity.

It’s also pivotal to acknowledge that compilers aren’t inhibited from optimising either constexpr or non-constexpr code. Consequently, in various instances, discernible runtime performance disparities might remain elusive. The pronounced performance elevation observed in the constexpr function in this study can be ascribed predominantly to the distinct way the compiler addressed constexpr and optimisation nuances.

Inlining

In computer programming, inlining refers to a compiler optimisation method in which a function call is replaced by the actual content of the function [59]. This procedure aims to reduce the overhead typically linked with function calls, such as parameter transmission, stack frame handling, and the function call-return process. The directive __attribute__((always_inline)) is a particular instruction for the GNU Compiler Collection (GCC), guiding the compiler to persistently inline the designated function, irrespective of the optimisation level chosen for the compilation.

The benchmark test in the given code contrasts two analogous functions: add and add_inline. The latter bears the __attribute__((always_inline)) directive. Results indicate that the function utilising the inlining directive (BM_WithInline) exhibited faster performance, averaging nanoseconds per operation. In contrast, the function without inlining (BM_WithoutInline) registered nanoseconds per operation. This denotes a speed enhancement of approximately . The performance enhancement can be attributed to the always_inline function, which sidesteps the overhead linked to function calls, thereby curtailing latency. These findings underscore the potential performance advantages of inlining, particularly for compact functions that are invoked frequently. However, it’s imperative to approach this method with discretion, as over-reliance on inlining may inflate the binary size, possibly undermining instruction cache efficacy.

3.2 Optimisation Techniques

Loop unrolling

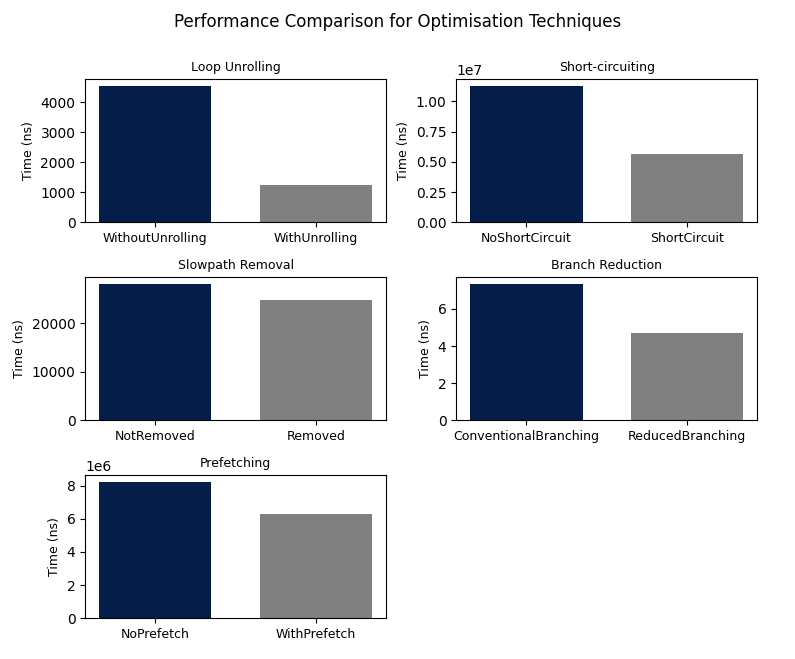

Loop unrolling is a technique used in computer programming to optimise the execution of loops by reducing or eliminating the overhead associated with loop control [29]. It’s a form of trade-off between processing speed and program size. The technique involves duplicating the contents of the loop so that there are fewer iterations, which decreases the number of conditional jumps the CPU has to make. Each iteration of the loop performs more work, allowing the program to execute faster. In the given test, two functions were benchmarked: one with a regular loop (BM_LoopWithoutUnrolling) and one with loop unrolling (BM_LoopWithUnrolling).

The time taken for the unrolled loop was significantly less than the standard loop. The standard loop took around 4539 ns to execute, while the unrolled loop took only 1260 ns, illustrating that the loop unrolling resulted in an improvement by . However, there are some challenges and considerations. Loop unrolling can increase the binary size, potentially causing more instruction cache misses. The performance benefits can also experience diminishing returns if a loop is excessively unrolled. Furthermore, loops that are heavily dependent on memory access speeds might not benefit significantly from unrolling. Therefore, while loop unrolling can be advantageous, its efficacy depends on specific loop characteristics, hardware considerations, and surrounding code, necessitating careful analysis and profiling.

Short-circuiting

Short-circuiting is a logical operation in programming where the evaluation of boolean expressions stops as soon as the final result is determined [59]. For example, in a logical OR operation (), if is true, there’s no need to evaluate because the overall expression is already determined to be true, regardless of ’s value. This concept can significantly improve performance by avoiding unnecessary computations.

The given code involves benchmarking tests comparing the performance of short-circuiting and non-short-circuiting operations. Two functions, BM_NoShortCircuit and BM_ShortCircuit, represent these two operations. The function BM_NoShortCircuit does not use short-circuiting, while BM_ShortCircuit does. The benchmark results show that BM_ShortCircuit (which uses short-circuiting) consistently performs faster than BM_NoShortCircuit (which does not use short-circuiting). For instance, at the 8 iterations level, BM_ShortCircuit operates roughly two times faster than BM_NoShortCircuit. Even at higher iteration levels, such as 8192, BM_ShortCircuit demonstrates superior performance, completing in roughly half the time as BM_NoShortCircuit. These results highlight the computational efficiency gained through short-circuiting, especially when dealing with expensive computations.

Based on the benchmark results provided, the short-circuiting operation (BM_ShortCircuit) offers significant performance improvements compared to the non-short-circuiting operation (BM_NoShortCircuit). The results can be seen in Table 2.

| Iterations | NoShortCircuit (ns) | ShortCircuit (ns) | Improvement (%) |

|---|---|---|---|

| 8 | 11,264,440 | 5,638,579 | 49.96 |

| 64 | 89,993,360 | 45,423,755 | 49.53 |

| 512 | 720,858,287 | 363,692,844 | 49.56 |

| 4,096 | 5,823,645,596 | 2,900,137,804 | 49.78 |

| 8,192 | 12,400,000,000 | 5,844,914,620 | 52.83 |

Therefore, across all these iterations, short-circuiting consistently results in approximately a 50% improvement in speed.

Slowpath removal

Separating slowpath code from the hotpath can significantly enhance latency in code execution [22]. In computing, a hotpath refers to the segment of code that is frequently executed, forming the critical path in terms of performance. Conversely, slowpath code pertains to less frequently accessed, heavier operations, like error handling, logging, or non-critical routines. The principle suggests to modularize and isolate such slowpath code from the hotpath. This ensures that the processor’s instruction cache, which is limited in capacity, remains primarily dedicated to serving the hotpath, thereby reducing unnecessary cache pollution and context switches. The first code snippet represents a less optimised design where error handling is directly included in the decision structure. The second code snippet proposes a better design where a function, HandleError, which is marked as non-inline, encapsulates the slowpath operations. This approach keeps the slowpath code away from the hotpath, reducing instruction cache load and improving overall performance.

The benchmark to test this programming strategy implemented two benchmark scenarios: SlowpathNotRemoved and SlowpathRemoved. In both scenarios, the hotpath is hit of the time, and the slowpath of the time. In the SlowpathNotRemoved scenario, slowpath operations (i.e., sendToClient, removeFromMap, logMessage) are executed directly. Conversely, in the SlowpathRemoved scenario, these operations are encapsulated inside the HandleError function, which is explicitly marked as non-inline to ensure it does not bloat the hotpath code.

Based on the benchmark results, the optimised scenario (SlowpathRemoved) exhibits a significant performance improvement over the less optimised one (SlowpathNotRemoved). Specifically, the execution time reduces from nanoseconds to nanoseconds, indicating approximately a performance improvement. This boost in speed arises primarily due to the efficient use of the processor’s instruction cache. In the optimised scenario, slowpath code is modularized into the non-inline function HandleError, thus reducing the footprint on the instruction cache, especially during frequent hotpath execution. Consequently, cache hits are maximized, resulting in less time spent on fetching instructions from memory. This demonstrates the effectiveness of separating slowpath code from the hotpath as a design strategy in improving latency.

Branch reduction

Branch prediction has become a cornerstone of contemporary Central Processing Units (CPUs), where it functions to anticipate the path that will be followed in a branching operation. When this prediction is accurate, it allows for the prefetching of instructions from memory, leading to seamless and efficient execution. However, a mispredicted branch results in a penalty, causing the CPU to stall until the correct instructions are fetched, thus hampering execution speed. This context underscores the potential value of implementing compile-time branch prediction hints, such as __builtin_expect in GCC. These hints have the potential to guide the compiler in generating more optimal code structures. Furthermore, another essential approach to minimising latency includes isolating error handling from the frequently executed parts of the code (hotpath), hence reducing the number of branches, and consequently, the opportunities for misprediction. This is branch reduction [22].

In a conventional programming approach, the handling of errors and the execution of the main function (often referred to as the “hotpath”) are often intertwined in a series of if-else statements. For instance, as demonstrated in the first code snippet, each potential error is checked in sequence; only when no errors are detected does the program proceed to execute the main function. This structure is quite common, yet it presents opportunities for branch misprediction, as the direction of execution could change at each conditional check.

In contrast, the alternative approach, illustrated in the second code snippet, adopts a distinct strategy that fundamentally separates error handling from the main function execution. Here, an integer variable (in this case, errorFlags) is utilised to represent the presence of different errors. If an error is detected, it is handled by a dedicated function HandleError(errorFlags), which uses the value of errorFlags to decide the specific error handling routine. If no errors are detected, the program proceeds directly to the main function, bypassing all the conditional checks present in the conventional approach. This method reduces the chances of branch misprediction and could potentially lead to improved program execution speed. This hypothesis forms the basis for the empirical analysis conducted to evaluate the impact of this approach on program execution latency.

The benchmark for branch reduction consisted of two distinct code structures, one implementing the conventional branching scheme and the other utilising a reduced branching technique. In the conventional scheme, error handling was interlaced with the critical execution path, whereas, in the latter, a bitwise operation was employed to check for errors, thereby separating it from the hotpath.

The results of the benchmark revealed performance improvements with the adoption of the reduced branching technique. The conventional branching approach resulted in an average execution time of 7.35 nanoseconds per iteration. In contrast, the reduced branching technique yielded an average time of 4.68 nanoseconds per iteration, marking an approximate speed increase of 36%. Thus, the findings corroborate the thesis that by minimising unnecessary branches and avoiding potential branch mispredictions, substantial reductions in program latency can be achieved.

Prefetching

Prefetching is a technique used by computer processors to boost execution performance by fetching data and instructions from the main memory to the cache before it is actually needed for execution [22, 59]. It anticipates the data needed ahead of time, and therefore, when the processor needs this data, it is readily available from the cache, rather than having to fetch it from the slower main memory. Prefetching reduces latency as it minimises the time spent waiting for data fetch operations, allowing a more efficient use of the processor’s execution capabilities. The technique is beneficial in scenarios where data access patterns are predictable, such as traversing arrays, processing matrices, or accessing data structures in a sequential manner. In these scenarios, prefetching can significantly lower the latency, resulting in faster code.

The benchmark to test this programming strategy included two functions: NoPrefetch and WithPrefetch, both of which sum up the elements of a very large vector. However, the WithPrefetch function also includes the __builtin_prefetch command to prefetch data. Analyzing the benchmark results, it’s evident that prefetching has improved the execution speed of the WithPrefetch function by approximately 23.5% (8235924 ns for NoPrefetch vs. 6301400 ns for WithPrefetch). This improvement is due to the prefetching technique used in the WithPrefetch function, which preemptively loads the data into the cache before it is needed. This reduces the latency associated with fetching data from the main memory. The processor, in the WithPrefetch function, experiences fewer cache misses and thus spends less time waiting for data from the main memory, which results in an overall speedup of the operation. It should be noted that the actual improvement may depend on several factors such as the processor’s architecture, the size of the data set, and the predictability of the data access pattern.

3.3 Data Handling

Signed vs unsigned comparisons

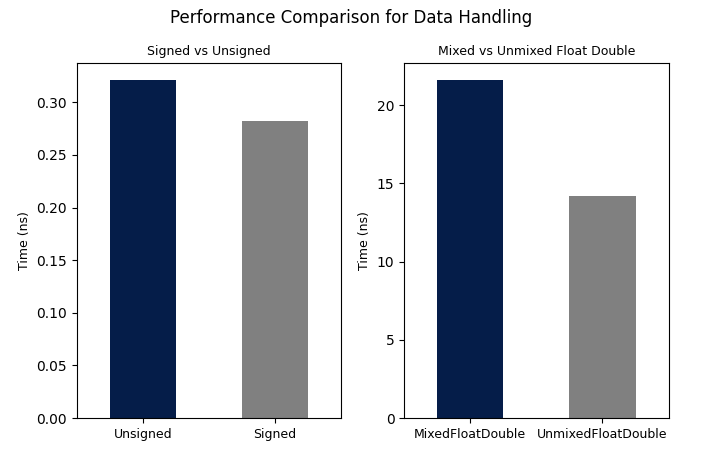

In computer programming, the terms ‘signed’ and ‘unsigned’ refer to whether or not a binary number is capable of representing negative values [59]. ‘Signed’ means that a binary number can represent both positive and negative numbers, whereas ‘unsigned’ means that a binary number can only represent positive numbers. This distinction plays a role in various aspects of programming, including arithmetic operations, comparisons, and loop control as we have in this example.

The benchmark test was conducted to investigate the speed difference between using a signed integer versus an unsigned integer in a specific scenario – a loop operation where a value of is incremented by 1 for 10 iterations. Two functions, f_signed and f_unsigned, were created, one using a signed integer for the loop variable and the other using an unsigned integer. These functions were then benchmarked using Google’s Benchmark library, with the rand() function used to generate a random input value for each function. The objective of the test was to compare the execution speed of these two versions of the function, and thereby ascertain whether using a signed or unsigned integer had any impact on performance.

According to the benchmark results, the function using the signed integer (BM_Signed) had an average execution time of 0.282 nanoseconds. The function using the unsigned integer (BM_Unsigned), on the other hand, had an average execution time of 0.321 nanoseconds. This indicates that, based on these specific benchmark results, using a signed integer instead of an unsigned integer led to a roughly 12.15% speed improvement.

The reason for this difference lies in the assembly code. The additional instructions in the assembly code generated for the f_unsigned function compared to the f_signed function are due to how the compiler is handling the potential for overflow with the unsigned integer. In the f_unsigned function, when is close to the maximum value that an integer can hold, adding 10 to it can result in an overflow. An overflow with an unsigned integer is defined in C++ and causes the integer to wrap around and become a small value. Thus, the loop for (unsigned k = i; k < i + 10; ++k) may not behave as expected and could become an infinite loop. The cmp, sbb, and bitwise AND operations are part of the compiler’s attempt to handle this scenario correctly. The lea instruction is used to compute the effective address once and use it in the loop. The cmp and sbb instructions are used to check whether has overflowed. The result of sbb is 0 if there was no overflow and -1 if there was. The and operation with 10 is used to get 0 if there was an overflow (an infinite loop is avoided) and 10 otherwise.

In contrast, for the f_signed function, when is large, adding 10 to it causes an overflow. In the case of signed integers, such an overflow is technically undefined behavior in C++, but many compilers handle this by allowing the value to wrap around to a large negative number. The assembly code for f_signed reflects this: it moves the constant 10 into the eax register and returns this value, without any concern for handling overflow scenarios. Therefore, these extra instructions in the unsigned case are present to handle the overflow case correctly and safely, and this additional work is what causes the f_unsigned function to run slower than the f_signed function.

Mixing data types

Mixing floats and doubles can result in a minor runtime cost due to the need for type conversions [59]. When a computation involves both float and double types, implicit conversions are required. For instance, consider the operation , where float_var is a float. The double literal has a higher precision, which necessitates the temporary promotion of float_var to double for the computation. The result is then a double, which must be demoted back to float to match the original variable type, adding computational overhead.

The conversion process between float and double is far from trivial, especially when such operations occur within loops or are part of frequently called functions. While the computational cost of these conversions may appear negligible for isolated operations, they can become significant in high-performance computing scenarios where such conversions happen millions or billions of times. The speed loss is the trade-off for the increased precision when promoting from float to double. However, demoting the value back to float could also introduce a loss of accuracy, thereby posing potential precision-related issues.

The benchmark analysis was conducted to measure and compare the performance of two C++ functions, namely BM_MixedFloatDouble and BM_UnmixedFloatDouble. These functions differed in their approach to handling floating-point number computations. In BM_MixedFloatDouble, a floating-point operation involving both float and double types was performed. Within the function, two float variables and were declared, with being assigned a random value. was then multiplied by the double literal , and the resulting product was stored in . This multiplication required an implicit conversion from float to double and then back to float, thereby accommodating the higher precision of the double literal. In contrast, BM_UnmixedFloatDouble involved computations exclusively with float types. Similar to the first function, it declared and as float variables and assigned a random value. However, the multiplication used a float literal , thus eliminating the need for any conversions between float and double.

The results of the benchmarking were revealing. The BM_MixedFloatDouble function took approximately nanoseconds to execute, while the BM_UnmixedFloatDouble function required around nanoseconds. The calculations showed that the version using only float computations and no implicit conversions, BM_UnmixedFloatDouble, was approximately faster than the mixed version. This significant speed improvement supported the initial hypothesis, indicating that the overhead of converting between float and double can indeed introduce a non-negligible performance cost, particularly in time-sensitive or high-performance computing applications.

3.4 Concurrency

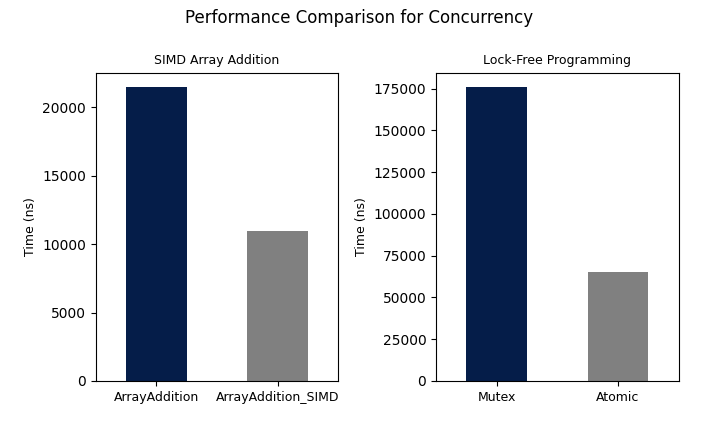

SIMD Instructions

SIMD, or Single Instruction Multiple Data, is a category of parallel computing architectures where a single instruction can act upon multiple data points simultaneously [30]. Modern CPUs offer built-in support for SIMD operations through specific instruction sets designed for parallel data processing [5]. For instance, the code in this example utilizes SSE2 (Streaming SIMD Extensions 2), a SIMD instruction set extension for the x86 architecture developed by Intel. SSE2 allows for the parallel processing of packed floating-point numbers stored in 128-bit registers, thereby substantially accelerating calculations on extensive data arrays.

The benchmark test focuses on comparing the performance of two functions: add_arrays and add_arrays_simd. The former function performs the addition of array elements in a sequential manner within a loop. The latter, on the other hand, employs SIMD instructions to execute the addition on four elements simultaneously. The benchmark results indicate a significant speed advantage for the SIMD-optimized function (BM_ArrayAddition_SIMD), which has an average execution time of nanoseconds per operation. In contrast, the non-optimized function (BM_ArrayAddition) takes approximately nanoseconds per operation. This translates to a reduction in operation time by roughly . The primary contributor to this speed-up is the SIMD architecture’s capability to process multiple data points concurrently, leading to increased data throughput and reduced latency, features especially beneficial for operations involving large data sets or arrays.

Lock-Free Programming

Lock-free programming is a concurrent programming paradigm that centers around the construction of multi-threaded algorithms which, unlike their traditional counterparts, do not employ the usage of mutual exclusion mechanisms, such as locks, to arbitrate access to shared resources [38]. The key concept that underpins this approach is the use of atomic operations which, in the context of multi-threaded programming, are operations that either fully complete or do not execute at all without the interference of other threads. The ability to guarantee such properties, while simultaneously maintaining data integrity across threads, eliminates the issues of deadlocks, livelocks, and other synchronization-related bottlenecks that are prevalent in lock-based designs, hence improving system-wide latency and throughput [31]. Lock-free programming achieves its objectives by employing low-level synchronization primitives, such as Compare-and-Swap (CAS) or Load-Link/Store-Conditional (LL/SC), which are typically provided by modern processor architectures [3]. These operations are the cornerstone of lock-free data structures and are used to resolve conflicting access to shared data. For instance, the CAS operation, given three operands - memory location, expected old value, and new value - atomically alters the memory location to the new value only if the current value at that location matches the expected old value. If the current value does not match, the operation is retried, usually in a loop until it succeeds. This operation is central to the implementation of many lock-free algorithms. While the latency and throughput improvements provided by lock-free programming can be quite significant, it’s important to underscore that lock-free programming is more complex than its lock-based counterparts and is thus more prone to bugs, particularly if misused [45]. Care must be taken to correctly design and test lock-free algorithms as the failure modes can be non-obvious and difficult to debug. In addition, not all problems lend themselves well to a lock-free solution, and so, it’s important to use these techniques judiciously and only when necessary.

The benchmarking code conducts an empirical evaluation comparing the performance of two distinct methods employed to increment a counter within the context of a multi-threaded environment: one facilitated through an atomic operation (increment_atomic) and another orchestrated through the deployment of a mutex (increment_locked). The primary technology utilised in executing the benchmark is Google Benchmark, a library renowned for its microbenchmarking capabilities. Each function designed for the benchmarking exercise is registered with Google Benchmark via the BENCHMARK macro, with each being subsequently executed with an argument quantified by ->Arg(10000). This argument effectively delineates the frequency of increment operations performed within each invocation of the corresponding function. The function increment_atomic leverages an atomic integer (atomic_counter) as the cornerstone of the counter implementation. The increment operation (++) executed on the atomic integer is certified to be atomic, a quality that guarantees the operation will either be executed in full or not at all, irrespective of the potential simultaneous calls from a multitude of threads. This level of thread-safety is accomplished without the need for additional synchronization mechanisms. On the contrary, the function increment_locked harnesses a rudimentary integer (locked_counter) in tandem with a mutex (counter_mutex) to enforce thread safety. Each increment operation is encapsulated within a std::lock_guard block, which locks the mutex at the commencement of the block and unlocks it at its conclusion (precisely when the lock_guard is destructed). This design ensures exclusive access, wherein only one thread is capable of incrementing the counter at any given moment. The most glaring discrepancy between these two methodologies lies in the necessity, or lack thereof, of locking. The process of locking can be computationally expensive, necessitating system calls and occasionally leading to the suspension of the calling thread if the lock is presently held by an alternate thread. In contrast, atomic operations are typically implemented using CPU instructions and do not demand context switches, thus conferring upon them a superior speed profile. As such, it is anticipated that the code will demonstrate a faster performance profile for the incrementation of the atomic counter as opposed to the locked counter, thereby illustrating how atomic operations can yield performance improvements in specific multi-threaded contexts.

The empirical results from the benchmarking exercise provide compelling insights into the temporal efficiencies of atomic versus mutex-based increment operations. The atomic incrementation (BM_Atomic/10000) registers an execution time of approximately , while the mutex-based incrementation (BM_Mutex/10000) records a significantly higher execution time of approximately . Given these observations, it becomes apparent that the atomic approach markedly outperforms the mutex-based method under the tested conditions. Specifically, the atomic operation resulted in a performance improvement of approximately when compared to the mutex-based method. This data reinforces the theoretical notion that lock-free programming, which includes atomic operations, can offer substantial performance benefits, especially in scenarios involving high contention. It’s important to underline that while these results are significant, the actual performance improvement may vary based on numerous factors, including hardware specifications, number of threads, and the workload’s contention level.

3.5 System Programming

Kernel Bypass

Kernel bypass is a technique that can significantly enhance the latency and throughput of a computer system, primarily by increasing speed. This is not a technique which was benchmarked in this work, however it is still a key topic which is covered to provide readers with a comprehensive arsenal of programming techniques. In a typical operating system architecture, network I/O (input/output) operations must pass through the operating system’s kernel. The kernel is the core component of an OS, managing tasks such as system calls, memory, and process scheduling. When a network packet is received, it’s processed by the network card, then passed to the kernel, which then copies it to user space for the application to process. This process involves multiple context switches between user space and kernel space, leading to relatively high latency due to overheads, such as the CPU cycles required for these switches, and memory copying overheads.

Kernel bypass mitigates these latency issues by facilitating direct communication between user applications and the network interface card (NIC). This is done by removing the kernel’s involvement in the data path for sending and receiving packets, thus ’bypassing’ the kernel. By leveraging this approach, the need for data copying and context switching is greatly reduced. Applications can write data directly to the network card’s buffers and read data straight from these buffers. In essence, the I/O operations are performed in user space instead of the kernel space, which saves significant amounts of time and thereby reduces latency. This is how kernel bypass can improve the speed of operations [52].

It’s important to note, however, that kernel bypass requires specialized network cards and drivers that provide such capabilities. The most widely used software that provides kernel bypass functionality includes Solarflare’s OpenOnload, Mellanox’s VMA, and Intel’s DPDK (Data Plane Development Kit). Barbosa discussed the use of kernel bypass with DPDK and states that DPDK can achieve a 7-fold decrease in latency when compared to a traditional Linux networking stack [7]. These tools allow applications to interact with the hardware directly, therefore reducing overheads and increasing speed. Additionally, they require careful tuning and management, as bypassing the kernel’s traditional security and isolation mechanisms can increase the risk of system instability or security vulnerabilities if not managed correctly. Despite these challenges, kernel bypass offers a compelling advantage in high-frequency trading, real-time analytics, high-performance computing, and other latency-sensitive applications [62].

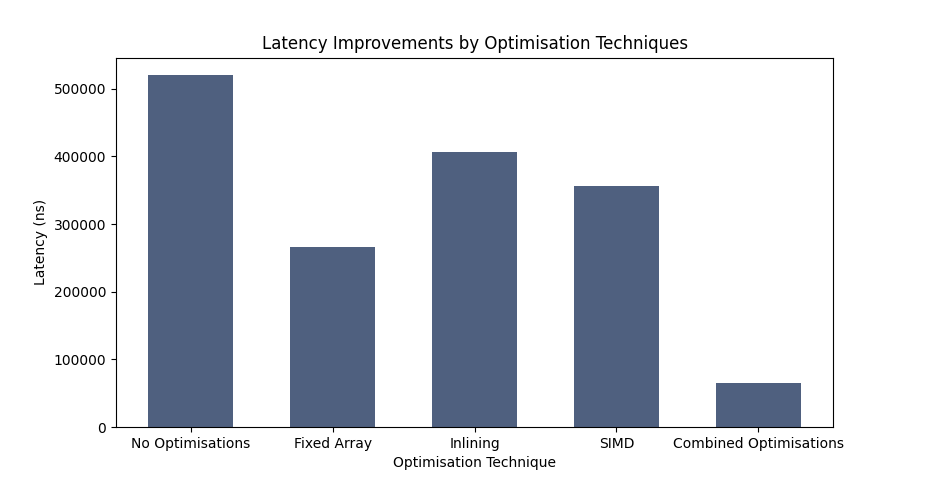

3.6 Results

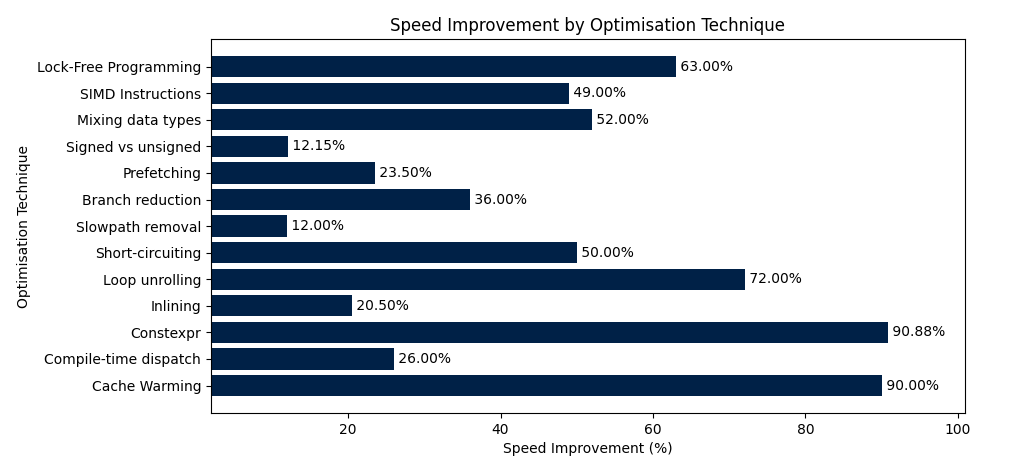

The benchmarked results of the Low-Latency Programming Repository can be seen in Figure 11. Cache warming and constexpr exhibited the most dramatic effects, boosting speed by approximately 90% each. Loop unrolling also made a considerable impact, achieving a 72% speed increase. Other techniques like Lock-Free Programming and Short-circuiting showed strong results, with speed improvements of 63% and 50% respectively. SIMD instructions were not far behind at 49%, while mixing data types yielded a 52% improvement. On the other hand, some techniques showed more moderate improvements: Compile-time dispatch at 26%, Inlining at 20.5%, Prefetching at 23.5%, and Branch reduction at 36%. The least impactful optimisations were slowpath removal and signed vs unsigned comparisons, which only achieved 12% and 12.15% improvements, respectively. Overall, these findings provide insights into the potential for enhancing computational efficiency using different optimisation techniques.

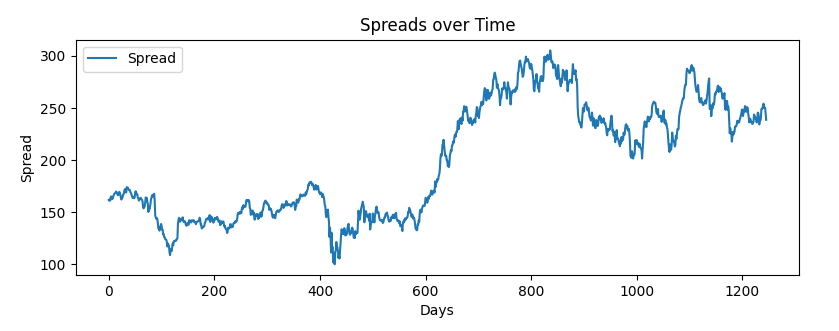

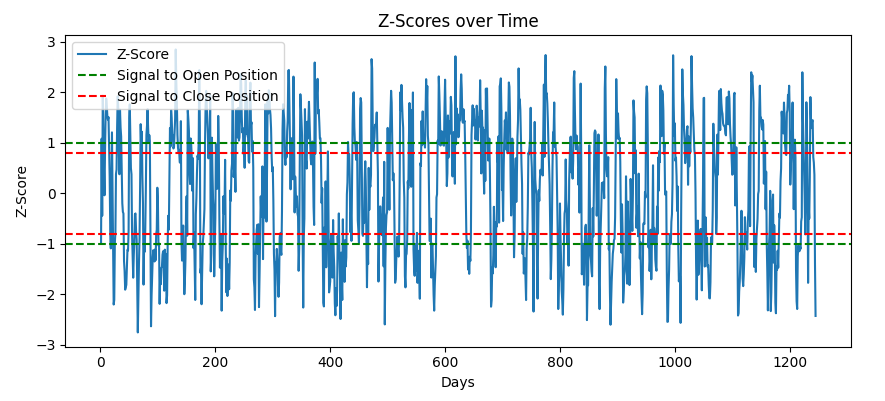

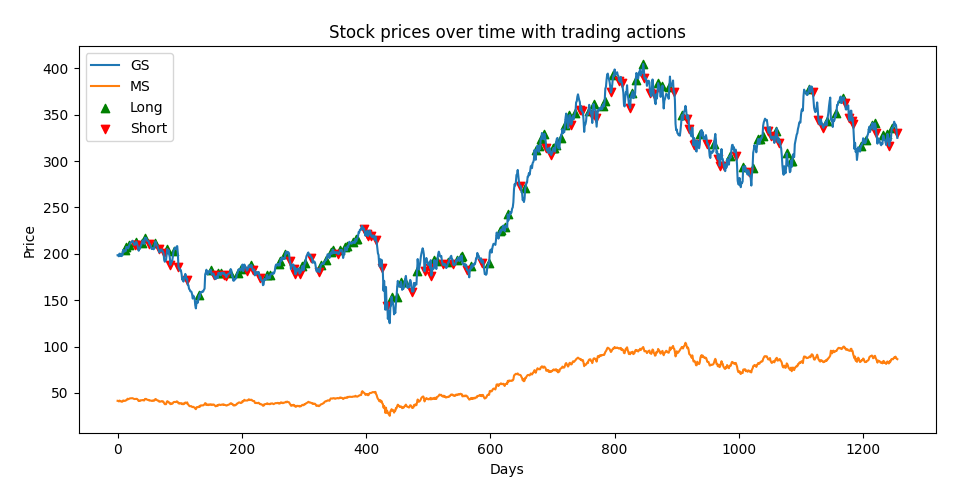

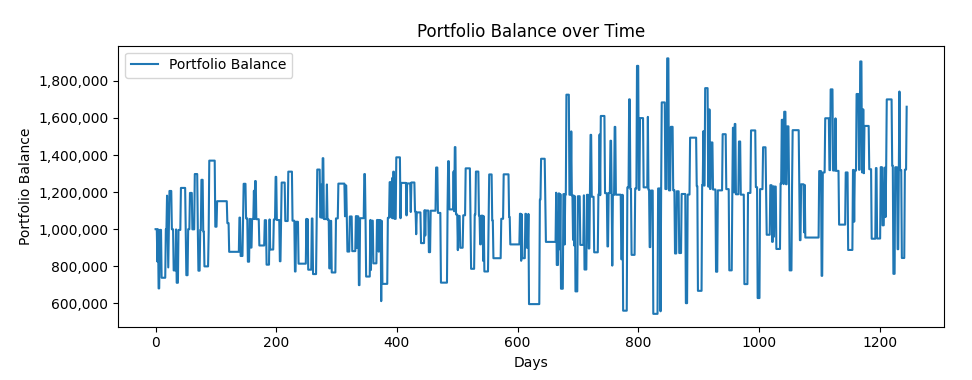

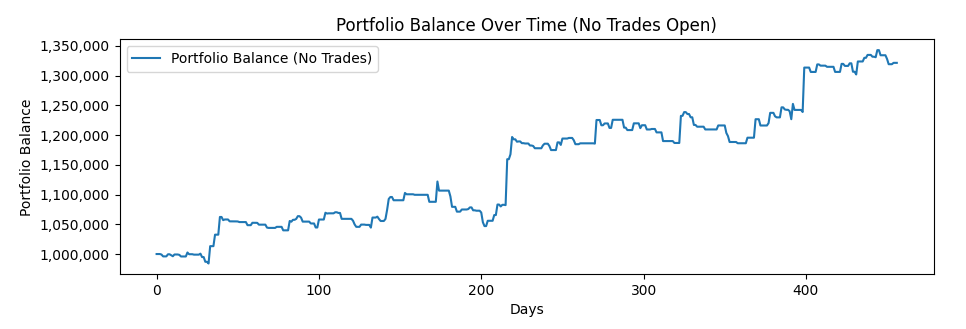

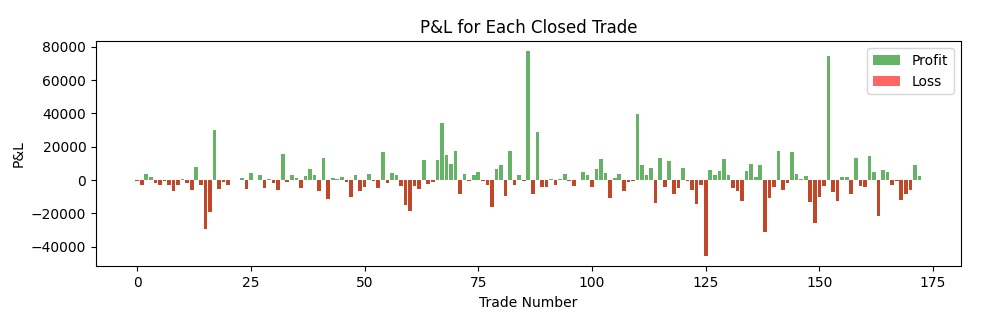

4 Pairs Trading

4.1 Introduction to strategy

The design patterns which were tested in isolation were combined in a statistical arbitrage pairs trading strategy to highlight a real life implementation of the discussed ideologies above. Pairs trading, also referred to as relative value arbitrage, constitutes a market-neutral quantitative trading strategy that leverages statistical and computational approaches to pinpoint asset pairs that display historical price correlations [32, 27, 15]. This strategy creates a unique opportunity for investors to capitalize on the dynamics of price behavior, particularly on the divergences and convergences that occur in the relationship between the pair of assets [27, 15]. The inception of pairs trading can be traced back to the late 1980s, attributed to the pioneering efforts of a quantitative group at Morgan Stanley led by Nunzio Tartaglia [32, 16]. The strategy was built on the observation that certain pairs of securities demonstrated a predictable relationship of price behavior over time, which laid the groundwork for this trading approach.