An Offline Learning Approach to Propagator Models

Abstract

We consider an offline learning problem for an agent who first estimates an unknown price impact kernel from a static dataset, and then designs strategies to liquidate a risky asset while creating transient price impact. We propose a novel approach for a nonparametric estimation of the propagator from a dataset containing correlated price trajectories, trading signals and metaorders. We quantify the accuracy of the estimated propagator using a metric which depends explicitly on the dataset. We show that a trader who tries to minimise her execution costs by using a greedy strategy purely based on the estimated propagator will encounter suboptimality due to so-called spurious correlation between the trading strategy and the estimator and due to intrinsic uncertainty resulting from a biased cost functional. By adopting an offline reinforcement learning approach, we introduce a pessimistic loss functional taking the uncertainty of the estimated propagator into account, with an optimiser which eliminates the spurious correlation, and derive an asymptotically optimal bound on the execution costs even without precise information on the true propagator. Numerical experiments are included to demonstrate the effectiveness of the proposed propagator estimator and the pessimistic trading strategy.

- Mathematics Subject Classification (2010):

-

62L05, 60H30, 91G80, 68Q32, 93C73, 93E35, 62G08

- JEL Classification:

-

C02, C61, G11

- Keywords:

-

optimal portfolio liquidation, price impact, propagator models, predictive signals, Volterra stochastic control, offline reinforcement learning, nonparametric estimation, pessimistic principle, regret analysis

1 Introduction

Price impact refers to the empirical fact that execution of a large order affects the risky asset’s price in an adverse and persistent manner and is leading to less favourable prices for the trader. Accurate estimation of transactions’ price impact is instrumental for designing profitable trading strategies. Propagator models serve as a central tool in describing these phenomena mathematically (see Bouchaud et al. [9], Gatheral [20]). These models express price moves in terms of the influence of past trades, and give a reliable reduced form view on the limit order book reaction for trades execution. The model’s tractability provides a convenient formulation for stochastic control problems arising from optimal portfolio liquidation [4, 22, 2, 3].

For an agent who wishes to liquidate a large order, a common practice for avoiding undesirable execution costs due to price impact, is to split the so called metaorder into smaller child orders described by over a time interval of length . Propagator models assume that there exists a matrix , known as the propagator or the price impact kernel, such that the asset’s execution price is given by

| (1.1) |

where the process represents the fundamental (or unaffected) asset price. Here is often referred to as a trading signal and is a mean-zero noise process (see e.g., Bouchaud et al. [10, Chapter 13]). The propagator typically decays for and hence the sum on the right-hand side of (1.1) is often referred to transient price impact. A well-known example à la Almgren and Chriss, discusses the case where all entries of are similar, then this sum represents permanent price impact. If , where and is the identity matrix, then the sum represents temporary price impact (see [6, 7]).

In the aforementioned setting, the trader can only observe the visible price process , her own trades and the trading signal . In order to quantify the price impact and to design a profitable trading strategy, the trader needs a precise estimation of the matrix . Some estimators for the convolution case (i.e., where were proposed in [9, 18, 38, 40] and in Chapter 13.2 of [10]. These regression based estimation methods are already a common practice in the industry, however they ignore numerous mathematical issues, such as the illposedness of the least-squares estimation problem, dependencies between price trajectories and spurious correlations between the estimator and greedy strategies. Hence the convergence of these price impact estimators remains unproved and rigorous results on the convergence rate are considered as long-standing open problem.

In [34] a novel approach for nonparametric estimation of the price impact kernel was proposed for the continuous time version of (1.1). Sharp bounds on the convergence rate which are characterised by the singularity of the propagator were derived therein. The estimation phase in [34] was designed for an online reinforcement learning framework where the agent interacts with the environment while trading. However, there are a few crucial drawbacks for the estimation methods developed in [34]: the trader’s strategy had to be similar and deterministic in all interactions with the market, and moreover the price trajectories in each episode were assumed to be independent. These assumptions do not apply in crowded markets for example, where all agents are following similar trading signals (see [33]). Lastly, but most importantly, online learning for portfolio liquidation is very expensive. In order to get one sample path of in (1.1) the trader needs to execute an order according to a highly suboptimal strategy, which leads to undesirable liquidation costs. For this reason most propagator calibrations are done offline, while fine tuning of the estimator should take place using online algorithms.

In order to resolve the above issues, the goals of this work are as follows:

-

(i)

to provide an offline estimator for the propagator in (1.1) based on a static dataset of historical trades and prices and to derive optimal convergence rate for this estimator.

-

(ii)

to propose a stochastic control framework that will eliminate the correlation between the offline estimator and a greedy trading strategy based on , and to derive a tight bound on its performance gap.

We will first provide details on objective (i). We choose to work in a discrete time setting, which is compatible with financial datasets and is inline with common practice in the financial industry. Our approach for the propagator estimation is offline since most of the existing data available to researchers is historical. Further, as mentioned before, online learning in order execution is expensive due to suboptimal interaction with the market using greedy trading strategies. Hence, deriving estimates for the price impact based on existing datasets could save substantial trading costs. In the following, we assume that there exists a dataset with price and signal trajectories, including the corresponding agents’ metaorders following the dynamics in (1.1),

| (1.2) |

see Definition 2.4 for details. In Theorems 2.10 and 2.14, we improve the convergence rate results of Theorem 2.10 of [34]. Our contribution to propagator estimations is as follows:

-

(i)

We relax the assumption on independence between the price trajectories, by assuming that the noise process is conditionally sub-Gaussian (see Assumption 2.8).

-

(ii)

We allow for any price adaptive strategies in the dataset , in contrast to choosing only one deterministic strategy that will repeat itself (i.e., for all ) as in Theorem 2.10 of [34] .

-

(iii)

We allow for estimation of non-convolution propagators and we show that in the convolution case the convergence rate is substantially faster (see Remark 2.15).

-

(iv)

We present a conceptually new norm,

(1.3) which not only quantifies the estimation error in terms of the quality of the dataset, but will also have a crucial role in the pessimistic offline learning approach which we present in the following. Here denotes the estimated propagator, and is a matrix that measures the covariance between the ’s in (see (2.18)).

Next we discuss objective (ii) of this work, to propose a stochastic control framework that will eliminate the correlation between a greedy strategy and the estimated price impact kernel. Precise estimation of the propagator is crucial in portfolio liquidation and portfolio selection problems in order minimise the trading costs. The following cost functional measures the expected costs of a trade of size executed within the time interval (see [12, 21, 22, 27] among others):

| (1.4) |

where satisfies a fuel constraint i.e., . The first term in the expectation on the right-hand side of (1.4) represents the price impact costs and the second term represents the fundamental price of the trade.

The two step procedure starting with offline estimation of the propagator and then using the estimator in order to obtain a greedy strategy (i.e., to optimize over a set of admissible controls) introduces some statistical issues and challenges which fit into the framework of offline reinforcement learning (offline RL). As mentioned before typical training schemes of online RL algorithms rely on interaction with the environment, where in the case of trading this interaction is expensive and in other areas such autonomous driving, or healthcare it is dangerous. Recently, the area of offline RL has emerged as a promising candidate to overcome this barrier. Offline RL algorithms learn a policy from a static dataset which is collected before the agent executes any greedy policy. However, these algorithms may suffer from several pathological issues which classified as follows:

-

(i)

Intrinsic uncertainty: the dataset possibly fails to cover the trajectory induced by the optimal policy, which however carries the essential information.

-

(ii)

Spurious correlation: the dataset possibly happens to cover greedy trajectories unrelated to the optimal policy, which by chance induces low execution costs. This leads to an estimation error of the true parameters, and to an underperforming greedy policy correlated with the estimated parameters.

These issues were outlined and partially quantified for Markov decision processes with unknown distribution of transition probabilities and rewards in [13, 25, 26, 28, 39]. We demonstrate how these issues emerge in offline propagator estimation. In the spirit of Section 3.1 of [25], we decompose the suboptimality of any strategy into the following ingredients: the spurious correlation, intrinsic uncertainty and optimization error. We denote by the true propagator, the optimal strategy and the associated cost functional in (1.4), respectively. We use the notation for the estimator of the true kernel , a convex cost functional using , and a greedy strategy minimising this functional. Note that we do not insist that and necessarily agree, that is we allow for some or all ’s.

We further define the suboptimality of an arbitrary algorithm that aims to estimate and also produces a strategy as follows:

We decompose the suboptimality of such algorithm into the following components along the same lines as Lemma 3.1 of [25],

| SubOpt | (1.5) |

Note that term (i) in (1.5) is the most challenging to control, as , and hence simultaneously depend on the dataset . This leads to a spurious correlation between them. In Example A.1 of Appendix A, we show that such spurious correlation can lead to a greedy strategy , which is substantially suboptimal in a specific tractable case. More involved examples are given in Section 3. We refer to Section 3.2 of [25] for an additional negative example for multi-armed bandit problems.

In particular, due to the correlation between and , term (i) can have a large expectation, with respect to the probability measure induced by the dataset, even under the assumption that is an unbiased estimator of . In contrast, term (ii) is less challenging to control, as is the minimiser of , hence it does not depend on and in particular on . In Section 4.3 of [25], it was shown that the intrinsic uncertainty is impossible to eliminate for linear Markov decision processes. Finally we notice that the optimization error in term (iii) is nonpositive as long as is greedy (i.e., optimal) with respect to .

Note that even with the tools developed in this paper, the estimation of price impact can be quite sensitive to various conditions in the market, which are sometimes difficult to quantify precisely. As pointed out before such deviations in the estimations of the true propagator will lead to undesirable costs due to spurious correlation (see Example A.1). For example in [29, 30] permanent and temporary price impact on the Russell 3000 annual additions and deletions events were computed. It was found that after 2008, the temporary market impact often presented a negative sign, presumably amenable to the 2010s bull market which signed a positive trend in the equity stock market [37, 16, 36]. While a regression model can be applied in order to fully test the effect of market trends on price impact, both the reference market index SP500 and individual stock returns present significant autocorrelations across different lags [24], hence this type of analysis is quite involved.

In order to minimise the ingredients of the suboptimality in (1.5) we adopt a pessimistic offline RL framework, which penalises trading strategies visiting states or using actions, which were not explored in the static dataset. We define the uncertainty quantifier which is a key concept in this theory. In the following we denote by the probability measure governing the dataset (see Section (2.3) for the precise definition). We refer to as the class of admissible controls with respect to the cost functional in (1.4), where a precise definition is given in (2.1).

Definition 1.1 (-uncertainty quantifier).

We say that is a -uncertainty quantifier with respect to if the following event

satisfies for .

Assuming that we have -uncertainty quantifier we now propose a candidate for so that the spurious correlation in (1.5) is nonpositive,

| (1.6) |

We also require that is convex so that the cost functional (1.6) is convex. Indeed by Definition 1.1 and (1.6), the spurious correlation is now bounded by

| (1.7) |

with probability for .

Using as in (1.6) concludes that suboptimality in (1.5) only corresponds to term (ii) which characterizes the intrinsic uncertainty. Our definitions and main results in Sections 2.3 and 2.4 propose such a -uncertainty quantifier which is sufficiently efficient and helps us to establish a tight upper bound for the suboptimality in (1.5). It is important to notice that deriving as in (1.1) is highly nontrivial since the true propagator is not an observable. In order to derive an uncertainty quantifier we use the bounds, which were developed in the estimation part of the paper, on the distance between the estimator and in (1.3), under the norm . Specifically, in (2.34) we choose and in Corollary 2.19 we show that the -uncertainty quantifier is given by,

| (1.8) |

for some constant . The optimiser of is referred to as a pessimistic optimal strategy and it is denoted by . In Example A.2 we demonstrate the effect of on the pessimistic optimal strategy in a simple and tractable setup. More realistic examples are given in Section 3. This is the first application of pessimistic offline RL in the area of quantitative finance and also in continuous state stochastic control. In the reinforcement learning literature, mathematical results that quantify these issues of offline RL are scarce, and they focus on Markov decision processes (MDPs). In the following we summarise our contribution in this direction:

-

(i)

In Theorem 2.18(i) we prove that the spurious correlation of is nonpositive and that the suboptimality of , which is essentially due to the intrinsic uncertainty, is bounded by

for any admissible strategy including which is unknown.

-

(ii)

In Theorem 2.23(i), we prove that , where corresponds to the the number of samples in the static dataset (1.2), under the assumption of a well-explored dataset (see Assumption 2.21 and Remark 2.22) . Together with (1.5) and (1.7) this leads to the asymptotic behaviour of the performance gap,

(1.9) where the constants of this rate are given explicitly. Special treatment and slightly refined results are given for convolution kernels in Theorems 2.18(ii) and 2.23(ii). In Remark 2.22, we show that for a convolution type propagator the assumption of a well-explored dataset should hold with asymptotically high probability for large , in contrast to a Volterra type propagator.

-

(iii)

Note that the expected convergence rate for a generic least-square estimator to the true kernel is of order , hence the statement of Theorem 2.23 is sharp up to a logarithmic factor. In fact the logarithmic correction in (1.9) is a result of the estimation scheme of , as described in (2.16), which is subject to quality of coverage of the dataset (see (2.19)). For a sufficiently regular dataset the regularization is not needed and the logarithmic term in Theorem 2.10 will vanish. This will give us asymptotically sharp bounds in Theorem 2.23(i), that is .

We compare the contribution of this work to [25], where partial results on pessimistic offline RL with respect to spurious correlation and intrinsic uncertainty were derived for MDPs. The bound on suboptimality in Theorem 2.18 coincides with the corresponding bound established in Theorem 4.2 of [25] that deals with a much simpler case of a class of MDPs where the rewards and distribution of the transition probabilities are Markovian. Note that stochastic control problems that involve propagators not only take place in a continuous state space but are also non-Markovian (see e.g., [2]). The convergence rate of in Theorem 2.23 coincides with the convergence rate established in Corollary 4.5 of [25] for linear MDP under similar assumptions.

Structure of the paper:

In Section 2 we setup the trading model and describe our main results on propagator estimation in Theorems 2.10 and 2.14, and on the performance gap for pessimistic learning in Theorems 2.18 and 2.23. Section 3 is dedicated to numerical illustrations of the propagator estimation and of pessimistic learning strategies. In Section 4, we develop the mathematical foundations for our results on convergence of the propagator estimators. Sections 5–7 are dedicated to the proofs of the main results. In Appendix A we provide some simple and tractable examples for the framework of pessimistic RL in portfolio liquidation. In Appendix B we provide further numerical experiments for estimation of Volterra kernels.

2 Problem formulation and main results

In this section we present our results on the optimal liquidation model which was briefly described in (1.4), the price impact estimation with offline data and finally on the pessimistic control problem which corresponds to (1.6).

2.1 The optimal liquidation model

We fix along with an equidistant partition of the interval , . Let be a filtered probability space and let be the null -field. Let and be -adapted stochastic processes satisfying

where we further assume that

We consider a trader with a target position of shares in a risky asset. The number of shares the trader holds at time is prescribed as

where denotes her trading speed, choosen from a set of admissible strategies

| (2.1) |

We will further impose the fuel constraint , hence can be regarded as the target inventory to be achieved by the terminal time. We fix an matrix , which is called the propagator, such that

| (2.2) |

We assume that the trader’s trading activity causes transient price impact on the risky asset’s execution price in the sense that her orders are filled at prices

| (2.3) |

where is an -measurable, square integrable random variable, which describes the initial price. Note that in this setup the process represents the fundamental (or unaffected) asset price, where is often referred to as a trading signal see e.g., Section 2 of [32].

Following a similar argument as in Section 2 of [27] we consider the following performance functional, which measures the costs of the trader’s strategy in the presence of transient price impact and a signal,

| (2.4) |

where satisfies a fuel constraint. We therefore wish to solve the following cost minimization problem,

| (2.5) |

In order to derive the optimiser to (2.5), we introduce some additional definitions and notation.

Notation

For as in (2.2), we denote by the smallest eigenvalue of the positive definite matrix and define

| (2.6) |

so that satisfies

| (2.7) |

Here is the identity matrix, where we often omit the subscript when there is no ambiguity. We define the following -vectors: and . Lastly we denote for any . For as in (2.6), let

| (2.8) |

We further define the matrices

and with

| (2.9) |

The following theorem derives an explicit solution to the constrained optimal liquidation problem in (2.5).

Theorem 2.1.

There exists a unique admissible strategy solving (2.5) which is given by

where

| (2.10) | ||||

and, for ,

with

Remark 2.2.

In the case where the signal the execution problem reduces to the deterministic optimization problem which was presented in Proposition 1 of Alfonsi et al. [5]. The solution to the problem in this special case is a straightforward generalization of equation (5) therein and it is given by

which is well-defined since is symmetric positive definite hence is invertible.

Remark 2.3.

The proof of Theorem 2.1 generalises the methods that were recently developed in [2, 3] in order to tackle such non-Markovian problems as (2.5) in two directions. First, we provide a framework for solving problems with constraints by introducing a stochastic Lagrange multiplier. Moreover we manage to solve the non-regularized problem, that is, without the linear temporary price impact term in the right-hand side of (2.3) (compare with equation (2.4) in [2]). This allows us to study the propagator model in its original form as introduced in Section 3.1 of [9].

2.2 Main results on price impact estimation with offline data

In this section, we provide an offline estimator for the propagator in (2.3) based on a static dataset of historical trades and prices and derive optimal convergence rates for this estimator. In order to tackle the estimation problem, we assume that the agent has access to an offline dataset, which consists of price trajectories and metaorders across several episodes. The precise properties of the dataset are given below.

Definition 2.4 (Offline dataset).

Let be the number of episodes in the dataset and consider

where , and are price trajectories, trading strategies and trading signals available in the -th episode, respectively.

We call an offline dataset for (2.3) if are realisations of random variables defined on a probability space satisfying the following properties: for each , is measurable with respect to the -algebra where

and there exist -measurable random variables such that,

| (2.11) |

where is the true (unknown) propagator and for all .

Remark 2.5.

Definition 2.4 accommodates dependent trading strategies that may not optimize the control objective (2.4). This setting is relevant for various practical scenarios such as crowded markets where agents with different objective functionals follow similar signals (see [15, 31, 33]). Moreover, these strategies may be generated adaptively in the data collecting process, meaning that the trader has incorporated historical observations and currently observed signals in order to design the trading strategy for the -th episode.

Convention.

For any we denote by the inner product in and by the Euclidean norm. For any matrix we denote by its Frobenius norm, i.e.,

| (2.12) |

where represents the trace of . We further define the Frobenius inner product,

| (2.13) |

We define the following class of admissible propagators. The true propagator is assumed to be in the following set with some known constant :

| (2.14) |

Remark 2.6.

Note that the conditions in agree with the assumptions on the propagator which were made in (2.2). Indeed the constant coincides with in (2.6) and it can be regarded as a lower bound on the temporary price impact. The lower diagonal structure of ensures non-anticipative structure (see (2.11)). The fact that the entries of are nonnegative ensures that a sell (buy) transaction, which causes a negative (positive) change in the inventory, will push the price downwards (upwards) in (2.11).

Remark 2.7.

We present a couple of typical examples for price impact Volterra kernels, whose projection on a finite grid belongs to . More examples for convolution kernels are discussed in Remark 2.13. The following non-convolution kernel was introduced in order to model price impact in bond trading (see Section 3.1 of [11]):

where is a usual nonnegative definite decay kernel and is a bounded function satisfying , due to the terminal condition on the bond price. In another example which was proposed in [19] for modelling order books with time-varying liquidity, the propagator is given by , where are bounded strictly positive functions.

In the following assumption we classify the noise in (2.11) as conditionally sub-Gaussian.

Assumption 2.8.

Based on the dataset , the unknown price impact coefficients can be estimated via a least-squares method. Note that for any , the observed data and satisfy

| (2.15) |

This motivates us to estimate by minimising the following quadratic loss over all admissible price impact coefficients:

| (2.16) |

where is a given regularisation parameter and is given in (2.14).

Remark 2.9.

The regularisation parameter ensures that the loss function (2.16) is strongly convex in . This along with the fact that is nonempty, closed and convex implies that is uniquely defined. The necessity of such regularisation can be clearly seen later in (2.19), as it ensures the invertibility of the matrix on the right-hand side of the equality. The need for this regularisation is often ignored in the propagator estimation literature (see e.g., Section 13 of [10]).

The estimator can be computed by projecting the unconstrained least-squares estimator onto the set . Indeed, if one sets

| (2.17) | ||||

then

| (2.18) |

where we recall that denotes the identity matrix. The unconstrained problem (2.17) can be solved explicitly as

| (2.19) |

while the optimisation problem (2.18) can be efficiently solved by standard convex optimisation packages (see e.g., [17]).

The following theorem provides a confidence region of the estimated coefficient in terms of the observed data.

Theorem 2.10.

Remark 2.11.

Theorem 2.5 quantifies the accuracy of the estimator with an explicit dependence on the given dataset and the magnitude of . The result is applicable to a general discrete-time Volterra propagator and non-Markovian and correlated observations (as stated in Remark 2.5). It is worth noting that this error estimate substantially improves the result presented in [34, Theorem 2.10], as the latter assumes the propagator to be a (continuous-time) convolution kernel and requires the observed trading speeds to be fixed (i.e., for all ) and deterministic vectors.

Examples where the Volterra price impact kernel is in fact a convolution kernel arise from empirical studies and are quite popular in the literature (see e.g., [9, 20, 35]). In the sequel, we incorporate this structural property of the price impact coefficient to enhance our estimation procedure. We therefore assume that for the true price impact kernel there exists such that

| (2.21) |

and is in the following class of admissible convolution kernels:

| (2.22) |

Remark 2.12.

Note that (2.22) assumes that the price impact is determined by a convex and decreasing kernel evaluated at equally distributed time grids. Specifically this means that there exists a function , called a resilience function, such that (with ) for all , then it is easy to see that the first constraint in (2.22) holds if is convex and decreasing.

Remark 2.13.

We present some typical examples for price impact convolution kernels, whose projection on a finite grid belongs to . In [9, 20] among others, the following kernel was introduced: , for some constants . The example of for were proposed by Gatheral in [20]. The case where , for some constant , was proposed by Obizhaeva and Wang [35].

The convolution structure in (2.21) simplifies the estimation of the matrix to the estimation of . Let be a given dataset. By (2.21) and (2.11), we have for any ,

| (2.23) |

which can be equivalently written as , with

| (2.24) |

The data series of in (2.23) motivates us to consider the following constrained least-squares estimator:

| (2.25) |

where is a given regularisation parameter, and is given in (2.22). Similar to in (2.16), can be computed by projecting the unconstrained least-squares estimator onto the parameter set :

| (2.26) |

where

| (2.27) |

with and defined in (2.24). Given , the associated propagator is then defined according to (2.21):

| (2.28) |

The following theorem is analogue to Theorem 2.10 and provides a confidence region of the estimator .

Theorem 2.14.

Remark 2.15.

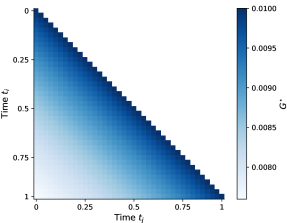

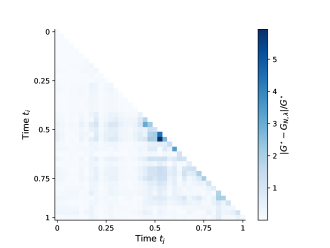

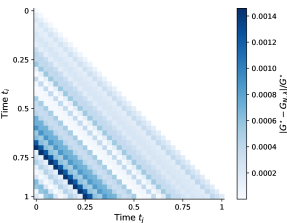

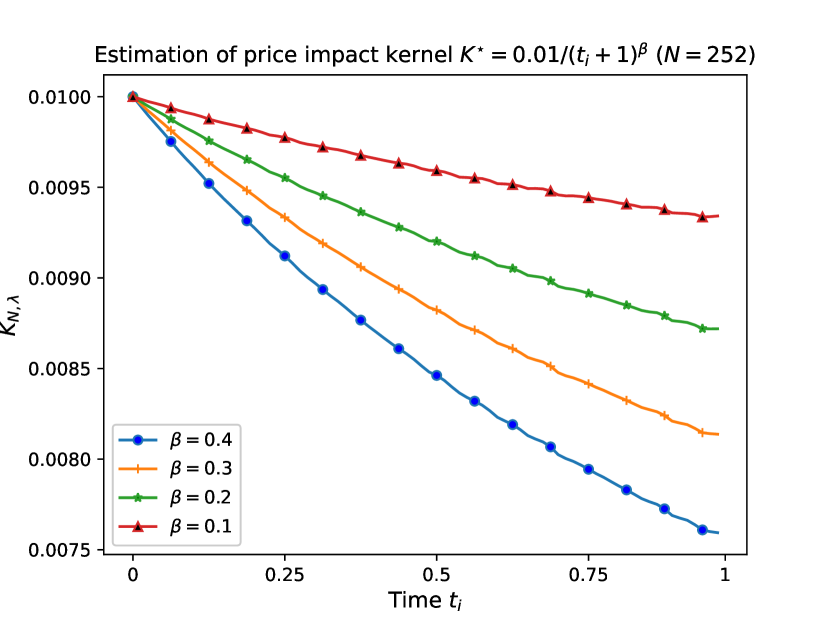

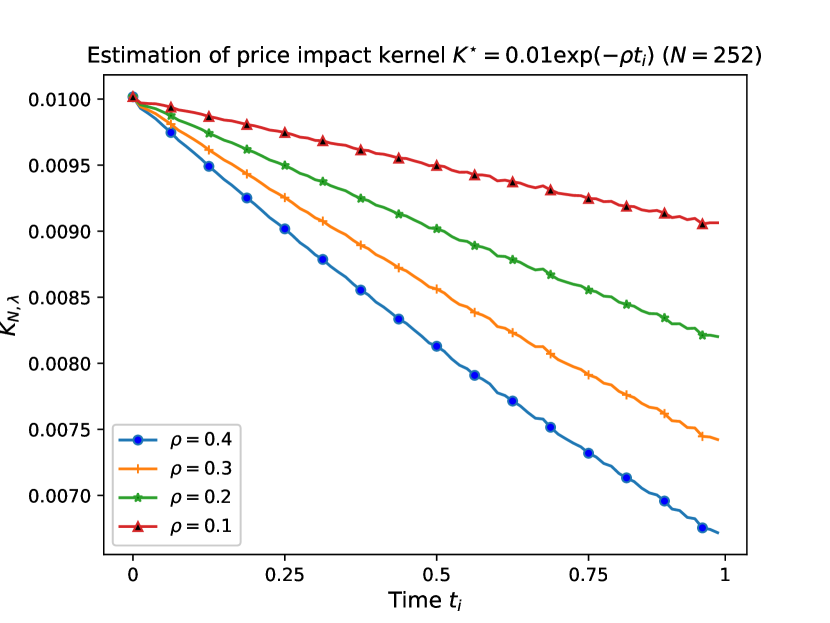

By imposing the structural property (2.21), we achieve in Theorem 2.14 a better dependence in the number of trading periods compared to Theorem 2.10. Specifically compare the power of in the first term on the right-hand side of (2.20) to the corresponding term in (2.29). We present in Remark 2.22 some additional important advantages for using a convolution kernel in the context of the regret analysis of the pessimistic control problem. See Figure 1 for a numerical comparison of the estimators (2.17) and (2.25).

2.3 Pessimistic control design with offline data

In the following two subsections, we propose a stochastic control framework that will eliminate the spurious correlation, which was defined in (1.5), between the offline estimator and a greedy trading strategy based on , and derive a tight bound on the associated performance gap.

An important consideration in designing trading strategies arise from the fact that pre-collected data may not provide a uniform exploration of the parameter space, and hence certain entries of the unknown propagator may have been estimated with limited accuracy. Consequently, if a trading strategy is solely based on the estimated propagator in (2.16), its performance in real deployment may be suboptimal. To overcome this challenge, in this section we introduce an additional loss term that takes into account the statistical uncertainty of the estimated propagator. This is often referred to as the principle of pessimism in the face of uncertainty in the offline reinforcement learning literature (see e.g., [25, 13]).

We recall that the offline dataset from Definition 2.4 is built out of trajectories of prices, trading speeds and signals which are defined on the probability space . In Section 2.1 we have specified the filtered probability space in which the optimal liquidation problem (2.5) takes place. We define the following product space

We further define to be the probability measure on the product space conditioned on a realisation of and as the corresponding conditional expectation.

Next we introduce the pessimistic stochastic control problem in the spirit of (1.6) that corresponds to the optimal liquidation problem (2.5). For the remainder of this section we assume that and the dataset in (2.4) are fixed and that for any , is defined as in (2.18).

Let . We define a subclass of the admissible strategies in (2.1) and admissible kernels in (2.14) as follows:

| (2.30) |

Remark 2.16.

We choose to be large enough so that contains strategies satisfying the fuel constraint of (2.40). The constant is chosen so that . Since provides a radius for the parameter space, using Theorem 2.1 and our assumption that the signal is known to the trader, we can also choose such that the optimal strategy (2.1) with , is in the set .

Now, for an arbitrary admissible control strategy , we define the following penalization functional

| (2.31) |

where bounds the estimation error from Theorem 2.10 and it is given by,

| (2.32) |

Here we have used the fact that for any two matrices we have in the Frobenius norm

| (2.33) |

The regularized cost functional for the pessimistic Volterra liquidation problem is given by,

| (2.34) |

The cost functional (2.34) replaces the unknown propagator in (2.4) with the estimated propagator and includes an additional cost term to discourage the agent from taking actions that are not supported by the offline data. We identify the expectation of as a -uncertainty quantifier (see (1.8)). This statement will be made precise in Section 2.4. The penalty strength is determined by the inverse covariance matrix , where a larger implies higher uncertainty in the estimated model and a stronger penalty . As we will show in Section 2.4, this pessimistic loss yields a trading strategy that can compete with any other admissible strategy, with regret depending explicitly on the offline dataset.

In the case where the price impact kernel is given by a convolution kernel as in (2.21), the impact of a trading speed on the price includes the following matrix (see (2.23)):

| (2.35) |

Similarly to in (2.30), we define the following subclass of convolution kernels, recalling that is a vector,

| (2.36) |

We then introduce the following regularization

| (2.37) |

where was defined in (2.27) and is the estimation error from Theorem 2.14,

| (2.38) |

Recall that the estimated convolution kernel was defined in (2.25). The regularized objective functional in the convolution case is given by,

| (2.39) |

where we used the relation (2.28) between the estimated convolution kernel and the associated propagator . Note that since the estimated propagator is of convolution form, the cost in (2.37) measures the impact of the statistical uncertainty of on a trading speed through the corresponding matrix (compare to in (2.31) and (2.34)).

We define the following pessimistic optimization problems for :

| (2.40) |

2.4 Main results on performance of pessimistic strategies

The following theorem provides an upper bound on the performance gap between the pessimistic solution to (2.40) and any arbitrary admissible strategy including the optimal strategy from Theorem 2.1 using the true propagator , in terms of the mean of . We also derive the asymptotic behaviour of this bound with respect to large values of the sample size in Theorem 2.23. Throughout this section we assume that the dataset is fixed according to Definition 2.4.

We recall that the performance functional is related to the original control problem (2.4), and the performance functional is related to the pessimistic control problem (2.40) conditioned on . Further, which is determined by was defined in (2.16) and (2.28). The class of admissible Volterra kernels was defined in (2.14), and the subclass of convolution kernels with kernels in , was defined in (2.22).

Theorem 2.18.

Let be the minimizer of , . Then under Assumption 2.8, for all and we have with -probability at least ,

-

(i)

if is a Volterra kernel,

-

(ii)

if is a convolution kernel with ,

One of the by-products of the proof of Theorem 2.18 is the fact that is a -uncertainty quantifier in the sense of Definition 1.1.

Corollary 2.19.

Under Assumption 2.8, for all and we have with -probability at least ,

-

(i)

if is a Volterra kernel,

-

(ii)

if is a convolution kernel with ,

Hence, is a -uncertainty quantifier.

In order to derive a convergence rate for the error bound on the regret, which was established in Theorem 2.18, we make the following assumptions. Recall that are the strategies recorded in the dataset (see Definition 2.4) and that for any , is the matrix defined in (2.24).

We give the definition of the Loewner order, i.e., the partial order defined by the convex cone of positive semi-definite matrices.

Definition 2.20.

For any two symmetric matrices we say that if for any , we have .

Assumption 2.21.

For any there exists a (known) constant such that the following bound holds with probability ,

-

(i)

if is a Volterra kernel

-

(ii)

if is a convolution kernel with ,

where and are symmetric positive-definite matrices, not depending on .

Remark 2.22.

There is an important advantage in verifying Assumption 2.21(ii) for convolution kernels compared to Assumption 2.21(i) for Volterra kernels. Note that in case (ii), is a product of two triangular matrices (see (2.24)) which is positive definite if the first entry . This means that is positive definite if , which is an event with probability , if the transaction size is assumed to be continuous. In reality the transaction size is quantized, and this event will have probability asymptotically close to for large . This means that normalising this sum of matrices, with respect to a symmetric positive-definite matrix is a very natural assumption, which is expected to hold for almost any dataset of metaorders. On the other hand, in case (i) the the product yields a matrix of rank , hence in order for the assumption to hold the number of samples has to be much larger than the number of grid points .

Notation:

We denote by (resp. ) the minimal eigenvalue of (resp. ), and by (resp. ) the maximal eigenvalue of (resp. ).

In the following we show that our pessimistic strategy is close to any competing strategy, where corresponds to the sample size of the dataset specified in Definition 2.4.

Theorem 2.23.

Remark 2.24.

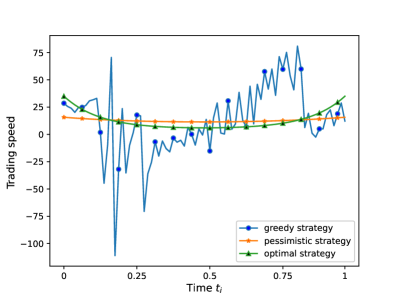

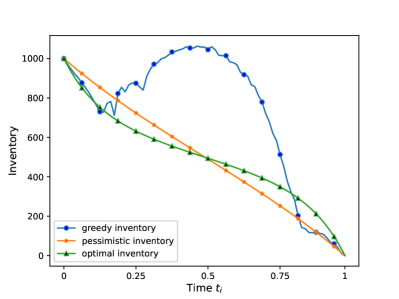

Theorem 2.23 derives upper bounds of order for the performance difference between the optimal pessimistic strategies and any arbitrary strategy of a competitor having access to a similar dataset. Note that also includes the optimal strategy using the unknown from Theorem 2.1. This framework introduces a novel approach for nonparametric estimation of financial models, which is particularly effective in the case where the quality of the common dataset is poor or it contains a relatively low number of samples, the statistical estimators can be biased and resulting greedy strategies may create unfavorable costs. See Figure 3 for numerical illustrations.

Remark 2.25.

Our results using the pessimistic learning approach can be compared to the well-known robust finance approach, in which strong assumptions are made on the parametric model, and the unknown parameters are assumed to be within a certain radius from the true parameters. Our nonparametric framework suggests that the radius of feasible models is in fact measured by matrix norms induced by and on the left-hand side of (2.20) and (2.29), respectively. In contrast to the robust finance approach theses norms are determined directly from the dataset and are not chosen as a hyperparameter (see (2.18) and (2.27)).

Remark 2.26.

We briefly compare the results of Theorems 2.23 and 2.18 to existing results in the offline reinforcement learning literature. These results typically focus on the much simpler setup of Markov decision processes (MDPs) with unknown transition probabilities and rewards. Note that stochastic control problems related to propagators as in (2.4) and (2.34) not only take place in a continuous state space but are also non-Markovian (see e.g., [2]). In [25] some results on pessimistic offline RL with respect to minimization of the spurious correlation and intrinsic uncertainty were derived for MDPs. The bound on suboptimality in Theorem 2.18 coincides with the corresponding bound for MDPs established in Theorem 4.2 of [25]. The convergence rate of order in Theorem 2.23 is compatible with the convergence rate of order established in Corollary 4.5 of [25] for linear MDP, under similar assumptions as in Assumption 2.21. The logarithmic correction in Theorem 2.23 is a result of the estimation scheme for (see (2.16)), which is subject to the regularisation of the dataset in (2.19). This estimation procedure is completely independent from the results of [25] and for a sufficiently regular dataset the regularization is not needed and the logarithmic term in Theorem 2.10 will vanish.

3 Numerical Illustration

In this section, we examine the performance of the propagator estimators in Section 2.2 and the pessimistic strategies presented in Section 2.4. Using a synthetic dataset, we illustrate the following characteristics of our methods:

-

•

Directly estimating a Volterra propagator using (2.16) may result in large estimation errors unless the dataset contains sufficiently noisy trading strategies. By imposing a convolution structure and shape constraints of the estimated model, (2.25) significantly improves the estimation accuracy, even with a smaller sample size.

-

•

Minimising the execution costs in (2.4) after substituting the estimated propagator instead of the true one, yields a greedy strategy that is very sensitive to the accuracy of the estimated model and also creates unfavorable transaction costs. The pessimistic strategy takes the model uncertainty into account and achieves more stable performance and drastically reduces the execution costs.

We start by describing the construction of the synthetic dataset for our experiments. For fixed -trading days, we split each trading day into minute bins. Hence, for a trading day of hours we have . We assume that the unaffected price process has the following dynamics:

where is the initial price, is the expected return following an Ornstein-Uhlenbeck dynamics (cf. [27, Section 2.3]),

| (3.1) |

and the values of , and are given in Table 1. The signal in (2.11) at time is then given by

We consider a market with 3 types of traders, trading simultaneously over one year (i.e. trading days). For simplicity, we construct a dataset with buy strategies, by sampling the target inventory of each type of trade uniformly from . Including sell strategies in our dataset will not change our estimation. We assume that the traders do not have precise information on the true price impact parameters and adopt the following commonly used strategies:

-

•

TWAP trades, aiming at stocks and buying at a constant rate throughout each day:

- •

- •

| Parameter | Value |

|---|---|

| Price volatility | 0.0088 |

| Signal volatility | 0.06 |

| Signal mean reversion | 0.1 |

| Trading Cost | |

| Resilience |

Given the above three trading strategies, for each , we generate the observed price trajectories according to the following dynamics (see (2.11)):

| (3.2) |

where is a realisation of

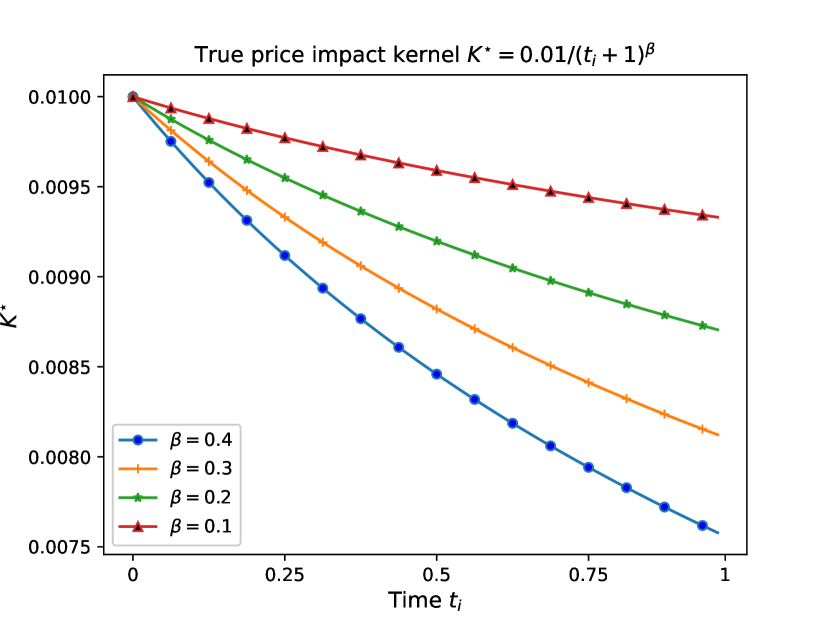

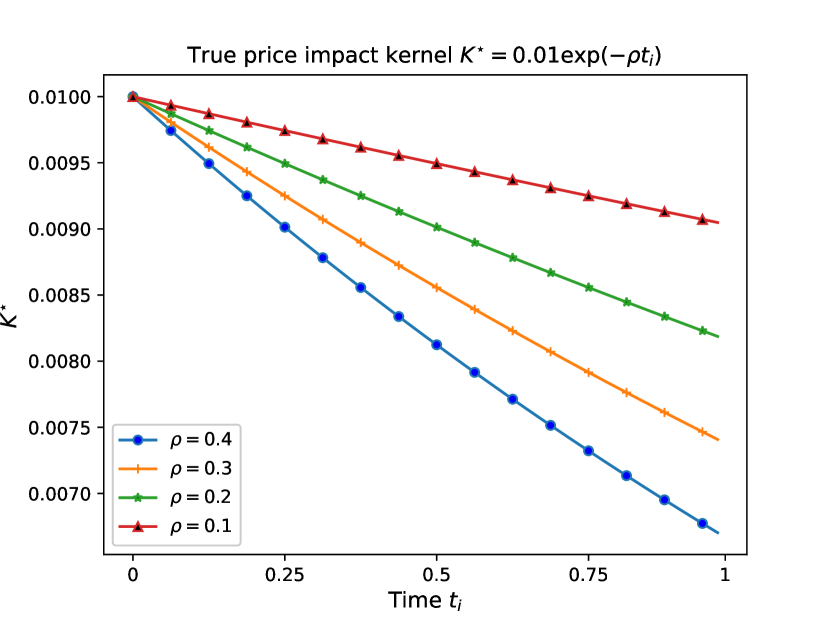

Here, we construct the market by giving equal weight to each of the type of trade, but similar results can be obtained by varying different weights to every strategy. We consider the true parameter in (3.2) to be a convolution-type propagator from one of the following two classes:

| (3.3) |

and

| (3.4) |

where is given in Table 1.

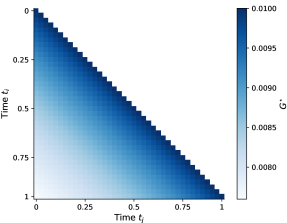

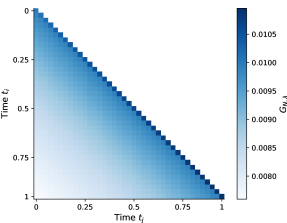

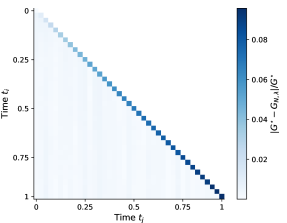

Given the above synthetic dataset , we examine the accuracy of the estimators (2.16) and (2.25), where the former performs a fully nonparametric estimation of the Volterra propagator, and the latter imposes a convolution structure of the estimated model. These estimators are implemented as in (2.18) and (2.26) with , where the projection step is carried out using the Python optimisation package CVXPY [17]. Our numerical results show that in the present setting, the Volterra estimator (2.18) yields large estimation errors, as the observed trading speeds in the dataset are not random enough to fully explore the parameter space (see Remark 2.22). This is demonstrated in Figure 1, where we consider a propagator associated with the power-law kernel (3.3) with and , and present the accuracy of the two estimators. Figure 1 (right) shows that the Volterra estimator (2.18) yields large component-wise relative errors, and hence it is difficult to recover the power-law kernel from the estimated model. We refer the reader to Figure 4 in Appendix B, which shows that if the historical trading speeds in the dataset are sufficiently noisy, then the estimator (2.18) recovers the true propagator accurately.

In contrast, Figure 1 (bottom) clearly shows that by imposing a convolution structure of the estimated model, the estimator (2.26) achieves a much higher accuracy using the same dataset. The estimator also recovers the true convolution kernel accurately, even with a smaller sample size. This can be seen from Figure 2, where we plot in (3.3) and in (3.4) for the above listed values of (see Figures 2(a) and 2(c)) and compare them to the estimated kernels obtained by (2.26) (see Figures 2(b) and 2(d)). One can clearly observe that, for both considered kernels, the proposed estimator captures the behavior of the true propagators accurately. To quantify the accuracy of our estimators and to demonstrate the importance of the projection step, we define the following relative errors for different sample sizes :

where refers to the power-law kernel (3.3) with , refers to the exponential kernel (3.4) with , is the estimated kernel using the plain least-squares estimator (2.27), and is obtained by (2.26) with the additional projection step. Table 2 summarises the estimation accuracy for sample sizes , which shows that both estimators achieve relative errors of order . Moreover, one can see that by imposing monotonicity and convexity on the estimated model, the estimator (2.26) improves the accuracy of the plain least-squares estimator at least by a factor of 2.

| Power-law kernel | Exponential kernel | |||

|---|---|---|---|---|

| Sample size | ||||

| 63 | ||||

| 126 | ||||

| 252 | ||||

Given the above estimated models, we proceed to investigate the performance of the pessimistic trading strategy. Our numerical results show that the performance of a naive greedy strategy using the estimated model is very sensitive to the quality of the estimated model. In contrast, the pessimistic trading strategy exhibits a stable performance regardless of the accuracy of the estimated models, and achieves an execution cost close to the optimal one.

In particular, recall that given the present dataset, the Volterra estimator (2.16) yields a poor estimated propagator as illustrated in Figure 1. As a result, a naive deployment of a greedy strategy as in Theorem 2.1, using the estimator , can lead to substantially suboptimal costs as discussed after (1.5). To illustrate this phenomenon clearly, we continue with the aforementioned example (for the power-law kernel (3.3) with and ) and present in Figure 3 the trading speeds and inventories for the relevant strategies, where we neutralize the effects of exogenous trading signals on these strategies. Specifically, we plot the optimal strategy with precise information on the propagator (3.3), the greedy strategy from Theorem 2.1 using the estimator in (2.16), and the pessimistic strategy minimizing the cost functional (2.34), using the same (with and ). We observe in Figure 3 that the greedy strategy exhibits an uninterpretable behaviour as a result of oscillation in the estimator, and that these oscillations are regularized by the pessimistic strategy. We further report that the optimal costs using the true propagator with zero signal, defined in Theorem 2.1 attains the value . Executing a greedy strategy as in Theorem 2.1 but with the estimated propagator yields excessive costs , while for the pessimistic strategy with , the execution costs are significantly closer to optimality, (see Table 3).

On the other hand, when the convolution estimator (2.26) is employed to estimate the propagator, both the greedy strategy and the pessimistic strategy yield a close-to-optimal expectation cost. This is due to the fact that the estimator (2.26) recovers the true kernel accurately, and hence stability properties of the associated optimal liquidation problem imply that introducing a regularization in the cost functional as in (2.25), will not provide a significant improvement. However, it is important to note that in practice, the true propagator and the accuracy of an estimated model are unknown to the agent, and hence compared with the pessimistic strategy, it is more challenging to assess the performance of a greedy strategy before its real deployment (see the discussion after (1.5)).

| Type of strategy | liquidation costs |

|---|---|

| Optimal strategy () | |

| Greedy strategy () | |

| Pessimistic strategy () |

4 Martingale tail inequality for least-squares estimation

This section first establishes a martingale tail inequality for noise in a general finite dimensional Hilbert space. Based on this tail inequality, we derive high probability bounds for least-squares estimators resulting from correlated observations. The results of this section are of independent interest and extend the results from [1] from observation taking values in to observations taking values in a general finite dimensional Hilbert space, which will be needed in order to prove Theorems 2.10 and 2.14.

We introduce some definitions and notation which are relevant to our setting.

Notation:

For all real finite dimensional Hilbert spaces and , we denote by the identity map on , and by be the space of linear maps equipped with the Hilbert-Schmidt norm , where is an orthonormal basis of of dimension . The norm is induced by an inner product such that for all . Both and do not depend on the choice of the basis of . We write for simplicity.

For each , we denote by the adjoint of , and say is symmetric if . We denote by the space of symmetric linear maps satisfying for all , and by the space of symmetric linear maps satisfying for all and . For any , we define the seminorm by for all . We write for simplicity.

The following definition introduces conditional sub-Gaussian random variables.

Definition 4.1.

Let be a probability space, let be a finite dimensional real Hilbert space, and let be a mean zero random variable. Let be sub-sigma field and a constant. We say is -conditionally sub-Gaussian with respect to if

| (4.1) |

We first extend the martingale tail inequality with scalar noise, which was introduced in [1, Theorem 1], to noise in a general finite dimensional Hilbert space.

Our setting:

For the remainder of this section we fix and to be real finite dimensional Hilbert spaces and let be a probability space with a filtration . We define as a -valued process predictable with respect to , and the noise process as a -valued process adapted to such that

and is -conditionally sub-Gaussian with respect to (cf. Definition 4.1).

We further define the following stochastic processes. Let and be such that for all ,

| (4.2) |

and

| (4.3) |

Now we are ready to introduce our martingale tail inequality for noise in a general finite dimensional Hilbert space.

Theorem 4.2.

In order to prove Theorem 4.2 we introduce the following auxiliary results.

Lemma 4.3.

Proof.

For any we define,

| (4.4) |

with . From (4.2) and (4.3) we get,

with

Since is measurable, and is -conditional sub-Gaussian with respect to we get from (4.1),

Thus by the measurability of with respect to , we get for all ,

hence is a super-martingale with respect to . Using the fact that , we deduce for all .

Now let be a stopping time with respect to the filtration . Then is a nonnegative super-martingale. By the optional stopping theorem, for any . By Doob’s martingale convergence theorem, exists and is finite a.s., hence along with Fatou’s lemma it follows that . ∎

Proof.

As is a finite dimensional space and is symmetric and positive definite, it follows that is invertible, and . A singular value decomposition of implies that there exists and an orthonormal basis of such that

| (4.5) |

Let , and be standard normal random variables that are mutually independent and are independent of . Define

| (4.6) |

Let be fixed, and further define

| (4.7) |

Then, since for all , we get from (4.4) and (4.6),

| (4.8) | ||||

where the last identity used and the fact that for all and ,

Since and are measurable with respect to , are standard Gaussian random variables independent of , by writing we get from (4.8) and (4.5) that

| (4.9) | ||||

where the last identity used .

Now we are ready to prove Theorem 4.2.

Proof of Theorem 4.2.

Let be fixed. For each , define the event

Define the stopping time such that for all . Then by the identity and by Proposition 4.4,

This proves the desired estimate. ∎

Based on Theorem 4.2, we establish the following high probability bounds of a projected least-squares estimator based on correlated observations. Recall that the Hilbert spaces , and , the filtration and the predictable process were defined before (4.2) and that was introduced in (4.2) and that -conditional sub-Gaussian random variables were defined in Definition 4.1.

Theorem 4.5.

Let be an -valued process adapted with respect to . Assume that there exists a nonempty closed convex subset , and such that

| (4.10) |

where , and is -conditional sub-Gaussian with respect to . Define

| (4.11) |

Then for any and , with probability at least we have for all ,

Proof.

Note that for any and the map which is given by

is strongly convex. Hence is well-defined and it satisfies the following first-order condition:

Substituting in the above inqeuality and using gives,

Now let and . Then

which along with the invertibility of and the Cauchy-Schwarz inequality implies that

This together with the identitity for all yields

The desired estimate then follows from Theorem 4.2 with and . ∎

5 Proof of Theorems 2.10 and 2.14

Proof of Theorem 2.10.

Let be the filtration given in Definition 2.4, and for each , let be such that for all , and let be the adjoint of . Then by (2.15), for all , and the least-squares estimator (2.16) is equivalent to

| (5.1) |

Recall that is a finite-dimensional Hilbert space with the inner product for all . Then by Theorem 4.5 (with and ), for all and , with probability at least ,

| (5.2) | ||||

where denotes the Fredholm determinant, , is the identity map on , and the norm is defined by

| (5.3) |

In the sequel, we fix and , and simplify the estimate (5.2). Observe that for all , , and for all and ,

which implies that is given by for all . Thus satisfies for all . Then by (5.3),

Let . Then for all , , and . As is symmetric and positive definite, for all ,

| (5.4) | ||||

and similarly,

| (5.5) | ||||

It remains to compute the Fredholm determinant . For each , let be the matrix such that the -th entry is and all remaining entries are zero. Then is an orthonormal basis of , and the Fredholm determinant of can be computed using its matrix representation with respect to the basis . Indeed, by [23, Theorem 3.2 p. 117],

where is the Kronecker’s delta (i.e., if and and otherwise). A direct computation shows that for all , , , and, hence, . Thus

which implies that

This along with (5.2) and (5.4) shows that

| (5.6) | ||||

This proves the desired estimate. ∎

6 Proof of Theorems 2.18 and 2.23 and Corollary 2.19

Proof of Theorem 2.18.

(i) Let and . By Theorem 2.10, (2.20) holds with probability . Using the invertibility of (recall (2.18)), and Cauchy-Schwarz inequality we get for all ,

| (6.1) | ||||

From (2.20), (2.30), (2.32) and (6.1), we obtain with probability at least ,

| (6.2) | ||||

where we used (2.31) in the last equality.

From (2.4), (2.34), (6.2) and Cauchy-Schwarz inequality, we get (with probability at least )

| (6.3) | ||||

Further, we deduce from (6.3) and the optimality of with respect to that with probability ,

| (6.4) | ||||

where we used the Cauchy-Schwarz inequality and (6.2) to derive the last estimate. This completes the proof of (i).

Proof of Corollary 2.19.

(i) Repeating similar steps as in (6.3) we have with -probability at least , for any ,

| (6.6) | ||||

which completes the proof.

(ii) the proof follows similar lines as the proof of (i), hence it is omitted. ∎

Proof of Theorem 2.23.

(i) Let and . Then there exists an event with , on which both Theorem 2.18(i) and Assumption 2.21(i) hold. We work on the event in the subsequent analysis. From Theorem 2.18(i) it follows that we need to bound . We note that by using (2.31) and Jensen’s inequality, we can estimate as follows,

| (6.7) | ||||

By (2.18) and Assumption 2.21(i), on the event ,

| (6.8) |

where we used by the hypothesis of the theorem. Inequality (6.8) is to be interpreted as follows,

Note that exists since is a symmetric positive-definite matrix.

By using the Rayleigh quotient bounds on the symmetric positive-definite matrix we have,

| (6.9) |

where is the minimal eigenvalue of , hence it is the maximal eigenvalue of .

We conclude from (6.11) that in order to derive an explicit bound on in terms of we need to further analyse the constant , which was defined in (2.32). To do so, we first bound the so called information gain,

Denote the eigenvalues of by . Using (2.18), Assumption 2.21(i) and the monotonicity of the determinant of positive definite matrices we obtain

| (6.12) | ||||

Plugging in our choice of , we get

| (6.13) | ||||

where we recall that is the maximal eigenvalue of . From (6.8) and (2.12) we get that,

| (6.14) |

where we recall that is the minimal eigenvalue of . From (2.32), (6.12), (6.13) and (6.14) and , it follows that,

| (6.15) | ||||

(ii) Using (2.27), Assumption 2.21(ii) with , it follows that . Together with the Cauchy-Schwarz inequality and (2.33), we deduce that with probability ,

| (6.16) | ||||

where we used (cf. (2.35)) and (6.9), which gives in the last inequality.

Following similar lines as in (6.7)–(6.11), using Theorem 2.18(ii), Assumption 2.21(ii) with and (6.16), we get with probability ,

| (6.17) |

From (2.27), Assumption 2.21(ii) with , it follows that . Together with (2.12) we get,

| (6.18) |

where we recall that is the minimal eigenvalue of .

By using (6.18) and repeating similar steps that were leading to (6.15), we get the following bound on the left-hand side of (2.38),

| (6.19) | ||||

We note that there is a difference in a factor of between (6.15) and (6.19), due to a difference between the powers of in the logarithm terms of (2.32) and (2.38), respectively. From (6.17) and (6.19), (ii) follows. ∎

7 Proof of Theorem 2.1

Proof of Theorem 2.1.

Note that the uniqueness of the optimizer of (2.5) follows immediately from the convexity of the cost functional, see e.g., Theorem 2.3 in [27].

Next we derive the solution to (2.5). Let be -measurable, square-integrable random variable. We write the Lagrangian of the performance functional in (2.4) as follows

| (7.1) |

The first order condition with respect to (7.1) is given by

| (7.2) | ||||

| (7.3) |

Let , then from (7.2) and the tower property we have

So if

| (7.4) |

holds then (7.2) is satisfied.

Recall that for . We rewrite explicitly for each entry in (7.4) (conditioned on ) to get,

| (7.5) |

Using (2.6) we obtain the following condition for the optimal strategy,

| (7.6) |

In the following we fix such that . Taking conditional expectation on both sides of (7.6), using the tower property we get for all ,

| (7.7) |

Define such that

By multiplying both sides of (7.7) by we get for all :

| (7.8) | ||||

where is the -th row of the matrix which was introduced in (2.8) and

| (7.9) |

Let , then from (7.8) we get,

| (7.10) |

We present the following technical lemma, which will be proved at the end of this section.

Lemma 7.1.

The matrix

is invertible for any .

From (7.10) and Lemma 7.1 we get,

| (7.11) |

We now plug-in (7.11) to (7.6) to get an equation for

| (7.12) |

We first consider the second and third terms on the left-hand side of (7.12). Using (7.9) we get,

| (7.13) | ||||

where is the following lower triangular matrix,

| (7.14) | ||||

which agrees with (2.9).

From (7.12) and (7.13) we get,

| (7.15) | ||||

We define and as follows,

| (7.16) | ||||

Writing (7.15) in matrix form gives

| (7.17) |

where we introduce the notation

so that,

From (7.14) it follows that is lower triangular matrix and

hence it is invertible. We therefore get from (7.17),

| (7.18) |

Let

and note that is measurable since and hence are lower triangular matrices. We can rewrite (7.18) as follows:

By using the tower property we get for any ,

Summing over and using , which follows from (7.3), we get

It follows that satisfies the following forward equation:

where

which admits the following solution:

∎

Proof of Lemma 7.1.

From (2.2) and (2.6) if follows that is symmetric nonnegative definite matrix. Therefore, is symmetric positive definite, hence it is invertible, or equivalently its determinant is nonzero. Now, is the same as except that the off-diagonal entries of the first row, , for are zero. In general, for , the entries , for and , of are zero and equal to otherwise. Therefore, the determinant of can be expressed as

where is the symmetric -matrix obtained by deleting the first row and first column of (or equivalently the first row and first column of ). Now, observe that

since and , which is a consequence of , for all . To see this, set the first component of equal to zero which implies for any , and thus is invertible. A similar argument holds for the matrices , . ∎

Appendix A Illustrative examples

In the following example, we demonstrate how spurious correlation (i) in (1.5) could lead to unfavourable costs.

Example A.1 (Spurious correlation for propagator estimation).

As described in Section 1, we consider the scenario of underestimating the price impact, and we capture the estimation error between the true propagator to the estimator as follows,

| (A.1) |

for some constant . The above inequality is understood as partial order defined by the convex cone of positive semi-definite matrices (see Definition 2.20). Note that in (A.1) we neglect the error of off-diagonal elements for convenience. Including these error terms would clearly make the spurious correlation larger.

From (1.5) it follows that the cost created by the spurious correlation of a greedy strategy is given by,

| SpurCor | (A.2) | |||

Note however that underestimating the propagator will lead to underestimation of price impact costs and will result in a faster execution strategy and hence create additional trading costs. This monotonicity relation is demonstrated in Figure 4 of [2], where it is shown that smaller propagators allow for faster execution rate. Next, we derive a lower bound for the spurious correlation contribution in (A.2), by considering a special case that will help to simplify the computations and keep this example tractable. We assume that the price impact is temporary, i.e., , and , for some constants . Note that in (A.2) we have . We further make the assumption that the unobserved asset price has the following dynamics,

where is a Brownian motion and are constants. Specifically is a trend that can be regarded as a deterministic signal. In this case one can solve the continuous time analog of the execution problem (2.4) (see [12, Exercise E.6.3, Chapter 6.9]) to get,

In [14, Table 2 , Section 4.3], the price impact coefficient was estimated from proprietary dataset of real transactions executed by a large investment bank, where it was found that . Since in a bullish market a daily stock return of is quite common we have . Therefore, if we wish to execute stocks within one day of hours of trading and the basic time unit is seconds, we have and it is clear that , except for a small interval . Outside this interval we have,

| (A.3) |

Hence from (A.3) and (A.2) it follows that

| SpurCor | (A.4) |

where we have neglected the aforementioned small interval in which with a smaller order contribution.

We learn from (A.4) that underestimating the price impact has an amplifying effect of order on the transaction costs when a greedy strategy is implemented.

In fact in this simple case we can compare the pessimistic strategy to the greedy strategy . Recall that,

so the (optimal) uncertainty quantifier in Definition 1.1 takes the form and the pessimistic cost functional in (1.6) is

The minimiser of is given by

Since we get so the pessimistic strategy outperforms the greedy strategy due to the optimality of with respect to . Note that in practice we do not know (or ). Therefore, we need to choose a which may be not be as sharp as in this example. In Section 3 we present further examples for spurious correlation costs in the presence of trading signals and more general propagators.

We recall that denotes the optimal strategy with respect to the pessimistic cost functional (1.6). In the following simple example, we show how our choice of in (1.8) as a -uncertainty quantifier (see (1.6)) helps to keep the pessimistic optimal strategy close to trajectories which are frequently observed in the dataset.

Example A.2 (Effect of -penalty function on order execution).

The role of the penalty in (1.8) is to discourage the strategies to visit out-of-distribution actions. We will illustrate this effect in the following simple example. Consider a dataset of buy metaorders, such that each order is executed over two even time bins, that is . The dataset contains the following strategies , for . It is well known that in buy execution problems without signals we should have

| (A.5) |

due to risk aversion terms and inventory constraints (see e.g., [12, Chapter 6.5, Figure 6.2]). For our example we choose for simplicity in and hence

It follows that we can write,

where from the fact that follows from . Our assumptions also imply . Hence, is invertible and we have,

Now let and consider

Since according to our assumption we expect , it follows that will penalize strategies where , which are not covered by the dataset (see (A.5)).

Appendix B Volterra kernel estimation for a noisy dataset

In this example, we construct the trading dataset as follows: the strategies for each and are i.i.d. samples from a normal distribution with mean 50 and standard deviation . We consider the propagator , with and , and apply (2.16) to estimate it using observed price trajectories. For the estimation procedure, we set , , . Numerical results are presented in Figure 4, which indicate that (2.16) recovers the true propagator reasonably well.

References

- Abbasi-Yadkori et al. [2011] Y. Abbasi-Yadkori, D. Pál, and C. Szepesvári. Improved algorithms for linear stochastic bandits. Advances in neural information processing systems, 24, 2011.

- Abi Jaber and Neuman [2022] E. Abi Jaber and E. Neuman. Optimal liquidation with signals: the general propagator case. arXiv:2211.00447, 2022.

- Abi Jaber et al. [2023] E. Abi Jaber, E. Neuman, and M. Voss. Equilibrium in functional stochastic games with mean-field interaction. arXiv:2306.05433, 2023.

- Alfonsi and Schied [2013] A. Alfonsi and A. Schied. Capacitary measures for completely monotone kernels via singular control. SIAM Journal on Control and Optimization, 51(2):1758–1780, 2013. doi: 10.1137/120862223. URL https://doi.org/10.1137/120862223.

- Alfonsi et al. [2012] A. Alfonsi, A. Schied, and A. Slynko. Order book resilience, price manipulation, and the positive portfolio problem. SIAM Journal on Financial Mathematics, 3(1):511–533, 2012. ISSN 1945-497X. doi: 10.1137/110822098. URL http://dx.doi.org/10.1137/110822098.

- Almgren and Chriss [1999] R. Almgren and N. Chriss. Value under liquidation. Risk, 12:61–63, 1999.

- Almgren and Chriss [2000] R. Almgren and N. Chriss. Optimal execution of portfolio transactions. Journal of Risk, 3(2):5–39, 2000.

- Bonnans and Shapiro [2013] J. F. Bonnans and A. Shapiro. Perturbation analysis of optimization problems. Springer Series in Operations Research and Financial Engineering. Springer Science & Business Media, 1 edition, 2013.

- Bouchaud et al. [2004] J.-P. Bouchaud, Y. Gefen, M. Potters, and M. Wyart. Fluctuations and response in financial markets: the subtle nature of ‘random’ price changes. Quantitative finance, 4(2):176–190, 2004.

- Bouchaud et al. [2018] J.-P. Bouchaud, J. Bonart, J. Donier, and M. Gould. Trades, Quotes and Prices: Financial Markets Under the Microscope. Cambridge University Press, 2018. doi: 10.1017/9781316659335.

- Brigo et al. [2022] D. Brigo, F. Graceffa, and E. Neuman. Price impact on term structure. Quantitative Finance, 22(1):171–195, 01 2022. doi: 10.1080/14697688.2021.1983201. URL https://doi.org/10.1080/14697688.2021.1983201.

- Cartea et al. [2015] Á. Cartea, S. Jaimungal, and J. Penalva. Algorithmic and High-Frequency Trading (Mathematics, Finance and Risk). Cambridge University Press, 1 edition, Oct. 2015. ISBN 1107091144. URL http://www.amazon.com/exec/obidos/redirect?tag=citeulike07-20&path=ASIN/1107091144.

- Chang et al. [2021] J. Chang, M. Uehara, D. Sreenivas, R. Kidambi, and W. Sun. Mitigating covariate shift in imitation learning via offline data with partial coverage. Advances in Neural Information Processing Systems, 34:965–979, 2021.

- Collin-Dufresne et al. [2020] P. Collin-Dufresne, K. Daniel, and M. Saglam. Liquidity regimes and optimal dynamic asset allocation. Journal of Financial Economics, 136(2):379–406, 2020.

- Cont et al. [2023] R. Cont, E. Neuman, and A. Micheli. Fast and slow optimal trading with exogenous information. arXiv:2210.01901, 2023.

- Davies [2019] G. Davies. The great bull market reaches its 10th birthday. Available at https://www.ft.com/content/4f941406-5157-11e9-b401-8d9ef1626294., 2019.

- Diamond and Boyd [2016] S. Diamond and S. Boyd. CVXPY: A Python-embedded modeling language for convex optimization. Journal of Machine Learning Research, 17(83):1–5, 2016.

- Forde et al. [2022] M. Forde, L. Sánchez-Betancourt, and B. Smith. Optimal trade execution for Gaussian signals with power-law resilience. Quantitative Finance, 22(3):585–596, 03 2022. doi: 10.1080/14697688.2021.1950919. URL https://doi.org/10.1080/14697688.2021.1950919.

- Fruth et al. [2014] A. Fruth, T. Schöneborn, and M. Urusov. Optimal trade execution and price manipulation in order books with time-varying liquidity. Mathematical Finance, 24:651–695, 2014. URL http://ssrn.com/paper=1925808.

- Gatheral [2010] J. Gatheral. No-dynamic-arbitrage and market impact. Quantitative Finance, 10(7):749–759, 08 2010. doi: 10.1080/14697680903373692. URL https://doi.org/10.1080/14697680903373692.

- Gatheral et al. [2011] J. Gatheral, A. Schied, and A. Slynko. Exponential resilience and decay of market impact. In F. Abergel, B. Chakrabarti, A. Chakraborti, and M. Mitra, editors, Econophysics of Order-driven Markets, pages 225–236. Springer-Verlag, 2011.

- Gatheral et al. [2012] J. Gatheral, A. Schied, and A. Slynko. Transient linear price impact and Fredholm integral equations. Mathematical Finance, 22(3):445–474, 2012. doi: https://doi.org/10.1111/j.1467-9965.2011.00478.x. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/j.1467-9965.2011.00478.x.

- Gohberg et al. [1990] I. Gohberg, S. Goldberg, and M. A. Kaashoek. Classes of linear operators, volume 49. Birkhauser, 1990.

- Jegadeesh [1990] N. Jegadeesh. Evidence of predictable behavior of security returns. The Journal of Finance, 45(3):881–898, 1990. ISSN 00221082, 15406261. URL http://www.jstor.org/stable/2328797.

- Jin et al. [2021] Y. Jin, Z. Yang, and Z. Wang. Is pessimism provably efficient for offline RL? In International Conference on Machine Learning, pages 5084–5096. PMLR, 2021.

- Kidambi et al. [2020] R. Kidambi, A. Rajeswaran, P. Netrapalli, and T. Joachims. Morel: Model-based offline reinforcement learning. In H. Larochelle, M. Ranzato, R. Hadsell, M. Balcan, and H. Lin, editors, Advances in Neural Information Processing Systems, volume 33, pages 21810–21823. Curran Associates, Inc., 2020. URL https://proceedings.neurips.cc/paper_files/paper/2020/file/f7efa4f864ae9b88d43527f4b14f750f-Paper.pdf.

- Lehalle and Neuman [2019] C. A. Lehalle and E. Neuman. Incorporating signals into optimal trading. Finance and Stochastics, 23(2):275–311, 2019. doi: 10.1007/s00780-019-00382-7. URL https://doi.org/10.1007/s00780-019-00382-7.

- Li et al. [2021] J. Li, C. Tang, M. Tomizuka, and W. Zhan. Dealing with the unknown: Pessimistic offline reinforcement learning. arXiv:2111.05440, 2021.

- Madhavan [2003] A. Madhavan. The Russell reconstitution effect. Financial Analysts Journal, 59(4):51–64, 2003. doi: 10.2469/faj.v59.n4.2545. URL https://doi.org/10.2469/faj.v59.n4.2545.

- Micheli and Neuman [2022] A. Micheli and E. Neuman. Evidence of crowding on Russell 3000 reconstitution events. Market Microstructure and Liquidity, 2022. doi: 10.1142/S2382626620500094. URL https://doi.org/10.1142/S2382626620500094.

- Micheli et al. [2023] A. Micheli, J. Muhle-Karbe, and E. Neuman. Closed-loop Nash competition for liquidity. To appear in Mathematical Finance, 2023. doi: https://doi.org/10.1111/mafi.12409. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/mafi.12409.

- Neuman and Voss [2022] E. Neuman and M. Voss. Optimal signal-adaptive trading with temporary and transient price impact. SIAM Journal on Financial Mathematics, 13(2):551–575, 2022. doi: 10.1137/20M1375486. URL https://doi.org/10.1137/20M1375486.

- Neuman and Voss [2023] E. Neuman and M. Voss. Trading with the crowd. Mathematical Finance, 33(3):548–617, 2023. doi: https://doi.org/10.1111/mafi.12390. URL https://onlinelibrary.wiley.com/doi/abs/10.1111/mafi.12390.

- Neuman and Zhang [2023] E. Neuman and Y. Zhang. Statistical learning with sublinear regret of propagator models. arXiv preprint arXiv:2301.05157, 2023.

- Obizhaeva and Wang [2013] A. A. Obizhaeva and J. Wang. Optimal trading strategy and supply/demand dynamics. Journal of Financial Markets, 16(1):1 – 32, 2013. ISSN 1386-4181. doi: http://dx.doi.org/10.1016/j.finmar.2012.09.001. URL http://www.sciencedirect.com/science/article/pii/S1386418112000328.

- Randewich [2019] N. Randewich. Wall Street’s oldest-ever bull market turns 10 years old. Available at https://uk.reuters.com/article/usa-stocks-bull/rpt-wall-streets-oldest-ever-bull-market-turns-10-years-old-idUKL1N20V1RJ, 2019.

- Staff [2019] W. S. J. Staff. Inside a Decadelong Bull Run. Available at https://www.wsj.com/articles/inside-a-decade-long-bull-run-11552041001, 2019.

- Tóth et al. [2017] B. Tóth, Z. Eisler, and J. P. Bouchaud. The short-term price impact of trades is universal. Market Microstructure and Liquidity, 03(02):1850002, 2017. doi: 10.1142/S2382626618500028. URL https://doi.org/10.1142/S2382626618500028.

- Uehara and Sun [2021] M. Uehara and W. Sun. Pessimistic model-based offline reinforcement learning under partial coverage. arXiv:2107.06226, 2021.

- Vodret et al. [2022] M. Vodret, I. Mastromatteo, B. Tóth, and M. Benzaquen. Do fundamentals shape the price response? A critical assessment of linear impact models. Quantitative Finance, 22(12):2139–2150, 2022. doi: 10.1080/14697688.2022.2114376. URL https://doi.org/10.1080/14697688.2022.2114376.