Empirical Review of Smart Contract and DeFi Security:

Vulnerability Detection and Automated Repair

Abstract

Decentralized Finance (DeFi) is emerging as a peer-to-peer financial ecosystem, enabling participants to trade products on a permissionless blockchain. Built on blockchain and smart contracts, the DeFi ecosystem has experienced explosive growth in recent years. Unfortunately, smart contracts hold a massive amount of value, making them an attractive target for attacks. So far, attacks against smart contracts and DeFi protocols have resulted in billions of dollars in financial losses, severely threatening the security of the entire DeFi ecosystem. Researchers have proposed various security tools for smart contracts and DeFi protocols as countermeasures. However, a comprehensive investigation of these efforts is still lacking, leaving a crucial gap in our understanding of how to enhance the security posture of the smart contract and DeFi landscape.

To fill the gap, this paper reviews the progress made in the field of smart contract and DeFi security from the perspective of both vulnerability detection and automated repair. First, we analyze the DeFi smart contract security issues and challenges. Specifically, we lucubrate various DeFi attack incidents and summarize the attacks into six categories. Then, we present an empirical study of 42 state-of-the-art techniques that can detect smart contract and DeFi vulnerabilities. In particular, we evaluate the effectiveness of traditional smart contract bug detection tools in analyzing complex DeFi protocols. Additionally, we investigate 8 existing automated repair tools for smart contracts and DeFi protocols, providing insight into their advantages and disadvantages. To make this work useful for as wide of an audience as possible, we also identify several open issues and challenges in the DeFi ecosystem that should be addressed in the future. As a side contribution, we release an annotated dataset that consists of DeFi protocols ( DeFi smart contracts) and concerns six types of DeFi attacks, hoping to facilitate the DeFi community.

Index Terms:

Smart Contract; Decentralized Finance (DeFi); Blockchain; Vulnerability Detection; Automated RepairI Introduction

Blockchain and its killer applications, e.g., Bitcoin [1] and smart contract [2], are taking the world by storm, giving rise to a variety of interesting and compelling decentralized applications [3, 4, 5]. A blockchain is essentially a replicated and distributed ledger that is shared among all bookkeeping nodes in a peer-to-peer network following a consensus protocol [6, 7]. Each block in the blockchain consists of a number of transactions. Every time a new transaction occurs, a record of that transaction is added to the ledger of every bookkeeping node [8]. The duplicate ledgers stored in the worldwide participating nodes ensure that transactions are immutable once recorded, endowing the blockchain with tamper-proof and decentralized nature [9].

Smart contracts are programs running on a blockchain system. They encode predefined terms into executable contract code. Once a smart contract is deployed on the blockchain, its defined rules will be strictly followed during execution. Smart contracts make the automatic execution of contract terms possible, facilitating complex decentralized applications [10, 11]. So far, tens of millions of contracts have been deployed on Ethereum, one of the most prominent blockchain platforms, enabling a variety of applications, such as wallet [12], gambling game [13], supply chain [14], healthcare [15], and cross-industry finance [16].

Recently, we have witnessed a dramatic rise in the popularity of decentralized finance (DeFi) applications [17, 18, 19, 20]. The total value locked (TVL) in DeFi has increased to as high as $248.84 billion due to the rapid growth of these applications. DeFi has shown its potential to expand the use of blockchain from simple value transfer to complex financial services [21]. Popular DeFi protocols now enable a variety of decentralized services, including lending and borrowing [22], portfolio management [23, 24], asset exchanges [25], and derivatives [26], all without the need for trusted parties.

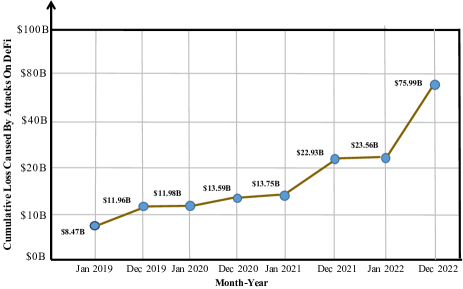

Motivation I: Understanding DeFi Attacks. While DeFi has been constantly improving, it is still in its infancy and the new DeFi ecosystem is crude, leaving a large room for security attacks [27, 28]. For example, in February 2020, the well-known DeFi protocol bZx suffered from two consecutive attacks [29]. Attackers made use of the logic flaws in bZx to achieve arbitrage (i.e., stealing over $8 million ETH at that time) at a low cost. This case is not isolated, and attacks on DeFi protocols happen every few months [30]. In April 2020, cybercriminals hacked into the DeFi protocol UniswapV1 and exploited the reentrancy vulnerability to steal 1,278 ETH [31]. In October 2021, the DeFi protocol Cream.Finance suffered from an external attack, yielding losses of more than $130 million [32]. Recently, DeFi cross-chain project Poly Network [33] and NFT game Ronin [34] were attacked by hackers, losing $611 million and $622 million respectively, which are the two most severe attacks in DeFi at the time of writing. According to the statistics from the REKT Database [35], DeFi protocols have lost a total of $77.1 billion due to scams, hacks, and exploits, out of which only $6.5 billion has been returned. Fig. 1 shows the cumulative financial losses caused by attacks on DeFi over the past three years. Obviously, frequent attacks have caused huge losses to the DeFi ecosystem and severely hindered its development.

Notwithstanding recent efforts have been directed towards investigating DeFi attacks [21, 36, 37], a broad and well-structured overview of this important research topic is still missing. In particular, current studies mostly revolve around financial applications and services of DeFi [38, 39], while lacking an in-depth review on DeFi attacks. Motivated by this, we strive to provide a comprehensive understanding of various DeFi attacks, hoping to facilitate the DeFi community.

Motivation II: Investigating State-of-the-Art Smart Contract and DeFi Security Tools. Like traditional computer programs, smart contracts contain vulnerabilities. Distinct from the traditional programs, exposed bugs in the on-chain smart contracts cannot be patched due to the immutability of the blockchain [40]. Since DeFi protocols typically consist of multiple smart contracts, they inevitably carry the risk of external attacks. Therefore, it is important to identify potential vulnerabilities in smart contracts. A number of works [41, 42, 43] have been developed to automatically detect flaws in smart contracts. They mainly focus on static analysis [44, 45, 46] and fuzzing techniques [47, 48, 49] to discover vulnerabilities. For example, Slither [50] converts smart contracts into an intermediate representation and performs taint analysis to detect vulnerabilities. ContractFuzzer [51] applies fuzzing techniques to smart contracts and reveals vulnerabilities by monitoring runtime behavior during fuzzing. However, most of these approaches are tailored for traditional smart contracts that usually comprise a single contract. Their ability to perform vulnerability analysis on complex DeFi protocols has yet to be investigated.

Several recent efforts [52, 53, 54] are devoted to detecting DeFi attacks by analyzing the transactions in DeFi protocols, from which they extract transaction patterns to expose potential attacks. For example, ProMutator [30] detects the price manipulation attack by reconstructing probable DeFi use patterns from historical transactions. DeFiRanger [55] identifies DeFi price oracle attacks according to recovered high-level DeFi semantics. Unfortunately, although the interest in DeFi attack detection is increasing, there is no systematic overview to probe the state-of-the-art DeFi attack detection approaches and gauge their effectiveness.

Another line of work focuses on identifying and patching vulnerabilities in smart contracts and DeFi protocols. For example, sGuard [56] compiles a smart contract into the bytecode, source map, and abstract syntax tree (AST). The bytecode is used to find bugs, while the source map and AST help fix the contract at the source code level. [57] develop an automated repair approach for DeFi protocols that can fix violations of functional specifications expressed as a property while providing solid correctness guarantees. To our knowledge, the review of existing automated repair tools for smart contracts and DeFi protocols is yet to be explored.

Our Work. In this paper, we aim to provide a comprehensive understanding of various DeFi attacks and an empirical review of state-of-the-art smart contract and DeFi security tools. On the one hand, we study 57 reported DeFi attack incidents, from which we summarize six common categories of DeFi attacks. In particular, we present concrete examples to illustrate the attack flow of each type of DeFi attack. Notably, we construct and release an annotated dataset consisting of DeFi protocols (a total of smart contracts). We ensure the traceability of each project by providing its address or URL. For each DeFi protocol, we annotate the type of attack or vulnerability it suffered. On the other hand, we investigate 50 security analysis tools that can either detect or repair vulnerabilities in smart contracts and DeFi protocols. Specifically, we first review the principles of bug detection tools for traditional smart contracts, and then conduct extensive experiments to evaluate their performance when applied to complex DeFi protocols. Then, we illustrate the design of existing DeFi attack hunting techniques and DeFi smart contract automated repair approaches, as well as their workflow. Finally, we analyze the limitations of existing security tools when dealing with DeFi protocols, and provide overall novel insights. Our study also identifies several open issues and challenges in the DeFi ecosystem that need to be addressed by future work.

Contributions. The key contributions of this paper are:

-

•

This work, to the best of our knowledge, is the first to present a comprehensive review of various DeFi attacks and a systematic evaluation of the state-of-the-art smart contract and DeFi security tools, empirically revealing both the capabilities and limitations of existing approaches.

-

•

In light of 57 reported DeFi attack incidents, we summarize six categories of DeFi attacks or vulnerabilities. Further, we also construct a benchmark dataset, which contains a total of DeFi smart contracts. To facilitate the community, we have released this dataset for public use at https://github.com/Messi-Q/DeFi-Protocol.

-

•

We empirically study 42 bug detection tools and 8 automated repair techniques for smart contracts and DeFi protocols, with the analysis of their performance. We also discuss several open issues and challenges in the DeFi ecosystem that need to be tackled by future research.

Paper Organizations. The remainder of the paper is organized as follows. In Section II, we give a brief introduction to the background of blockchain, smart contract, and decentralized finance (DeFi). Thereafter, we summarize six common types of DeFi attacks and present concrete examples in Section III. In Section IV, we investigate state-of-the-art bug detection and repair techniques for smart contracts and DeFi protocols. Section V describes the dataset construction, and presents the evaluation results of available automated vulnerability detection tools on DeFi protocols. In Section VI, we discuss several open issues and challenges. Finally, we conclude the paper in Section VII.

II Background

Before diving into the key components, please allow us to introduce the required background on blockchain, smart contract, and decentralized finance.

II-A Blockchain In A Nutshell

Blockchain, a distributed ledger maintained in a decentralized manner, was first popularized as the technology behind Bitcoin [58]. The ledger is shared among all participating nodes in the blockchain network. A public blockchain network has an open and transparent infrastructure, which is not owned or controlled by any centralized organization [59]. Put differently, blockchain can guarantee the fidelity and security of the recorded data without the need for a trusted intermediary.

More specifically, the distributed ledger contains a sequence of blocks, each of which records a set of transactions. Every block links to its previous block, forming a chain. When a user wants to add a new transaction to the ledger, the transaction data is verified by the so-called miners (bookkeeping nodes) and put into a new block [60]. Once the new block is confirmed by miners that follow a consensus protocol, it is added to the chain [61]. Each miner stores a duplicate transaction ledger, which endows the blockchain with decentralized and immutable nature, that is, nobody can alter and delete the data recorded in the ledger.

Evolution of Blockchain. The first implementation of a blockchain system was Bitcoin, i.e., decentralized digital currency verified using cryptography [62]. The second wave of decentralized blockchain applications started with the advent of Ethereum [63], which introduced smart contracts and enabled multiple types of dapps. In recent years, a new subfield of blockchain, decentralized finance [64], which specializes in advancing financial technologies and services on top of a permissionless blockchain (typically Ethereum), has attracted considerable attention worldwide. For a thorough background on blockchain, readers can refer to SoKs, such as [65, 66, 67].

II-B Ethereum and Smart Contract

Ethereum is one of the most prevalent blockchain platforms, which is the first to introduce the functionality of smart contracts [68]. Ethereum smart contracts are developed in high-level programming languages such as Solidity [69] and Vyper [70]. Smart contracts are essentially a set of digital agreements with encoded rules that can be enforced without the involvement of a trusted third party. They are compiled to bytecode and executed within a virtual machine called the Ethereum Virtual Machine (EVM). Once deployed, smart contracts are uploaded to the blockchain and broadcast to all ledger nodes for backup.

A smart contract can implement arbitrary rules for manipulating digital assets [2]. The rules defined in a smart contract are strictly and automatically followed during execution, effectuating the ‘code is law’ logic [9]. While Ethereum is becoming one of the most influential blockchains, it has been exposed to a large number of smart contract security vulnerabilities [71]. Since DeFi protocols are usually composed of multiple smart contracts, it inevitably becomes an attractive attack target, which has caused numerous financial losses [72].

II-C DeFi: Decentralized Finance

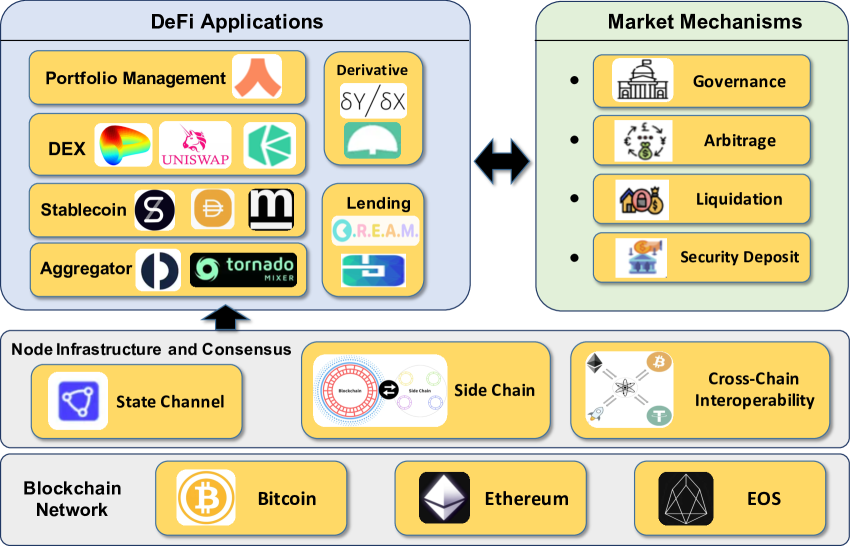

Decentralized finance, a peer-to-peer financial system powered by the blockchain, is flourishing [73]. With the widespread adoption of smart contracts, the concept of decentralized finance truly came to fruition, even to the point of hosting an economy exceeding $200 billion [38, 74]. DeFi builds upon the permissionless foundation provided by blockchains. Anyone is free to propose a novel financial contract, and anyone can interact with, transfer assets to, and withdraw assets from it, as long as the participants abide by the immutable contract rules. A DeFi protocol typically consists of multiple interactive smart contracts that run on top of the blockchain’s state machine. Currently, a variety of financial services are migrating to the DeFi ecosystem, including lending and borrowing, decentralized exchanges, portfolio management, derivatives, and many others [75, 76, 21, 77]. To provide an intuition of what DeFi is and what DeFi can do, we present a high-level overview of DeFi in Fig. 2. Explicitly, we summarize the applications of DeFi into six categories.

II-C1 Lending and Borrowing

Lending and borrowing of assets in a DeFi application are realized through protocols for funds loaning, which are referred to as the DeFi lending protocols [78]. Decentralized lending services constitute the largest class of DeFi applications, with a cumulative TVL of over $40 billion [79]. They offer loans to individuals or businesses using smart contracts as negotiators or intermediaries, as smart contracts automate the lending and borrowing process [80].

In DeFi applications, loans are generally of two forms. One is the over-collateralized loan, where the borrower is required to post collateral, i.e., provide something of value as security to cover the debt [81]. In this way, collateralization ensures that the lender can recover the loaned value and provides the borrower with an incentive to repay the loan. Another interesting form is the non-collateralized loan, i.e., flash loan [36]. Flash loans allow users to borrow any available amount of assets from a liquidity pool without upfront collateral, as long as the loan is repaid at the end of the transaction. Flash loans leverage the atomicity of the blockchain transaction (i.e., a transaction reverts to its previous state if the loan is not repaid within the current transaction) to facilitate several use cases, e.g., decentralized exchange arbitrage [82] and collateral swaps [73].

In general, a transaction reverts due to three possible reasons: 1) the transaction sender does not specify sufficient transaction fees, 2) the transaction does not satisfy a condition set forth by the interacting smart contract, or 3) the transaction conflicts (e.g., double spending) with another transaction [83]. Flash loans, therefore, entail two interesting properties. First, the lender is guaranteed that the borrower will repay the loan. If the repayment is not performed, the loan will not be given. Second, the borrower can technically request any amount of capital, up to the number of funds available in a flash loan pool. While providing convenience, flash loans allow adversaries to launch malicious attacks with a large number of assets that they do not actually own. Undesirable trades using the flash loan have resulted in numerous notorious attacks on DeFi applications, such as [84, 85, 86].

II-C2 Decentralized Exchange

Decentralized exchange (DEX) is essentially a kind of DeFi protocol that enables the on-chain exchange of digital assets [87]. Users can trade different tokens in a decentralized manner by interacting with smart contracts. Decentralized exchanges have accumulated over $25 billion locked funds. For example, one of the largest DEXs is Uniswap [88], whose users have locked up around $8 billion in token value. Compared to traditional centralized exchanges, DEXs have advantages in privacy protection and asset management. There are two modes in DEXs, i.e., list of booking (LOB) and automated market maker (AMM). DEXs in LOB mode maintain an off-chain order book to record users’ bids and asks, namely, the order matching is performed off-chain. DEXs in AMM mode achieve a fully decentralized exchange. AMM allows liquidity providers, the traders who are willing to provide liquidity to the market, to deposit assets into a liquidity pool. The market maker can deposit two or more tokens into a liquidity pool with a self-defined weight. The trade rate between cryptocurrencies in the pool is automatically calculated based on the pricing mechanism [89]. AMM has become the most popular mode in DEXs due to its flexible liquidity [90, 91].

II-C3 Portfolio Management

As more and more DeFi protocols motivate clients to provide liquidity, a new type of project, known as portfolio management, debuts to help users (i.e., liquidity providers) invest their assets [92, 93]. They automatically find the DeFi protocols that provide the highest annual percentage yield (APY). However, liquidity allocation is an arduous task for liquidity providers who seek to maximize their profits due to the complex and expansive space of yield-generating options. Therefore, the management of on-chain assets that serve as decentralized investment funds can be automated through DeFi protocols. An investment strategy that entails transacting with other DeFi protocols is encoded in the smart contracts, and the invested assets are deposited into the contract [94].

II-C4 Derivative

DeFi derivatives are built upon the smart contracts that derive value from the performance of an underlying entity, such as currencies, bonds, and interest rates [95]. Tokenized derivatives can be created without trusted third parties and are able to prevent the influence of malicious attacks. While approximately 99% of the derivative trading volume is created on centralized exchanges, a number of DeFi protocols have emerged that provide similar functionality, with a particular focus on futures, perpetual swaps, and options [96]. Popular examples of DeFi derivatives include CompliFi [97], dYdX [98], and BarnBridge [99], etc.

II-C5 Stablecoin

Stablecoins are a class of cryptocurrencies designed to ensure price stability [100, 101]. Typically, stablecoins are stabilized by either being directly/indirectly backed or intervened through various stabilization mechanisms. The popular stablecoins, such as USDC or USDT, are custodial and fall outside the scope of DeFi, as they primarily rely on a trusted third party. In decentralized settings, the challenge for the protocol designer is to construct a stablecoin that achieves price stability in an economically secure and stable manner and where all necessary parties can continue to participate profitably [102]. Price stability is achieved through on-chain collateral that provides a foundation of secured loans from which the stablecoin derives its economic value. Non-custodial stablecoins aim to be independent of the societal institutions that custodial designs rely on. Popular stablecoins in DeFi include Tether [103], DAI [104], Diem [105], etc.

II-C6 Aggregator

DeFi aggregator is essentially a platform that consolidates trades from various decentralized platforms into one place, increasing the efficiency of cryptocurrency trading [106]. Typically, a DeFi aggregator leverages multiple DEXs and implements various buying and selling strategies to help users maximize profits, while mitigating gas fees and DEXs trading commissions [64]. Not only do aggregators pull the best prices, but some DeFi aggregators even offer a unique, user-friendly way to analyze and combine other users’ trading strategies via a convenient drag-and-drop mechanism [107]. In particular, with the advent of DeFi aggregators, new entrants to the industry can benefit from DeFi without understanding the complex technologies such as trading, decentralized services, and blockchain. Overall, an aggregator helps users make better trading decisions. Popular DeFi aggregators include 1inch [108], Matcha [109], and Plasma.Finance [110].

III Overview of DeFi Attack

DeFi has taken an incredible wave of popularity and enabled growing penetration in various industries. Nevertheless, due to the trillion dollars wealth it holds, DeFi attracts numerous external attacks, which severely threaten the security of the entire DeFi ecosystem [111, 112]. While multifarious DeFi attacks have attracted considerable attention, there is still a lack of a well-structured overview for providing an in-depth review and analysis of DeFi attacks. Motivated by this, we present a comprehensive review of various DeFi attacks, hoping to inspire the readers. Specifically, we examine the well-known DeFi attack incidents over the past three years, which are listed in Table I. We summarize these attacks into six categories, i.e., flash loan attack (pump and arbitrage, price manipulation, reentrancy), deflation token attack, sandwich attack, and rug pull attack. It is worth noting that many existing works have investigated a variety of vulnerabilities in traditional smart contracts, such as timestamp dependency and unhandled exception [66, 113, 114]. Instead, in this work, we mainly take an insight into attacks and vulnerabilities targeting DeFi protocols. Next, we will go through the details of the DeFi attacks one by one.

III-A Flash Loan Attack

As an emerging service in the DeFi ecosystem, the flash loan allows users to apply for a non-collateral loan. While providing convenience, it enables adversaries to launch malicious attacks with a large number of assets that they do not have [27]. After scrutinizing existing DeFi attacks, we found that around of DeFi attack incidents involve flash loans [36]. Flash loan attack has become the most prominent form among various DeFi attacks. In particular, we summarize three major types of flash loan attacks, namely, pump and arbitrage [28], price manipulation [55], and reentrancy [32]. For each type of flash loan attack, we present the intuition to identify the essence of the attack. We then deliver a concrete example to clarify the attack.

III-A1 Pump and Arbitrage

Generally speaking, arbitrage is the practice of making a profit by trading on different exchanges that provide different prices for the same asset. Since the DeFi market reacts more slowly to events on the blockchain network than the real-world market, attackers can take advantage of market inefficiencies to buy and sell an asset at different prices, gaining financial benefits. With the flash loan, attackers can achieve arbitrage without any pre-owned asset. Particularly, once the price difference is found, attackers can instantly borrow a considerable amount of assets with a flash loan service and further achieve arbitrage.

Intuition. The nucleus of the pump and arbitrage attack is that the attacker leverages the different prices of the same asset on different exchanges. For example, the attacker pumps the ETH/WBTC exchange rate on a constant product AMM (e.g., Uniswap) with the leveraged funds of ETH in a margin trade. Afterwards, the attacker purchases ETH at a cheaper price on the distorted price market with the borrowed WBTC from a lending platform.

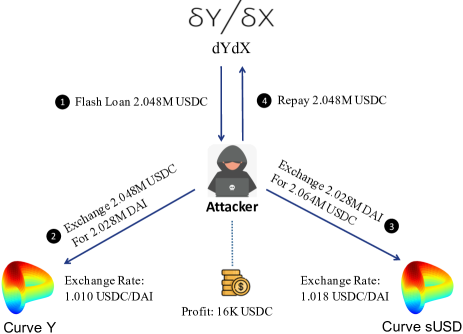

Example. We present, as an example, the specific details of the pump and arbitrage attack on the DeFi protocol dYdX111dYdX: https://dydx.exchange, which is shown in Fig. 3. Specifically, the attacker first borrows a flash loan of 2.048 million USDC from the exchange dYdX in step ❶. Then, the attacker exchanges all holding USDC for 2.028 million DAI in another exchange Curve Y with an exchange rate of 1.010 USDC/DAI in step ❷. Thereafter, he/she exchanges all DAI for 2.064 million USDC in the third exchange Curve sUSD with an exchange rate of 1.018 USDC/DAI in step ❸. Finally, the attacker repays the original borrowed 2.048 million USDC in step ❹. With the two exchanges, the attacker finally gains an arbitrage of 16 thousand USDC (i.e., 16 thousand = 2.064 million - 2.048 million).

III-A2 Price Manipulation

Price manipulation is one of the most common flash loan attacks. In such attacks, the adversary distorts the reported price and propagates the distortion using a vulnerable customized function, causing the victim to receive inaccurate price information. As a result, the victim is tricked into overvaluing or undervaluing the target asset. Typically, the process of a price manipulation attack consists of the following four steps, all of which are executed within the same transaction to avoid being interrupted by other operations [30].

-

•

Prepare Target Asset. First, an attacker prepares a target asset, whose price the attacker intends to inflate. Furthermore, the attacker borrows a large number of funds with a flash loan for the next phase.

-

•

Inflate Asset Price. Then, the attacker manipulates the price of the target asset by significantly reducing its reserves in the corresponding AMM liquidity pools. This is typically done by swapping a large amount of the target asset for another token. The attacker reports the manipulated price of the target asset to the victim.

-

•

Profit From Victim. Since the victim may overvalue the target asset, the attacker makes a profit by exchanging the target asset for another asset through the victim’s services (e.g., collateralized borrowing).

-

•

Recover Asset Price. Finally, the attacker performs the reverse actions to restore the unbalanced AMM liquidity pools to their original state. As a result, the attacker avoids the losses caused by the second-step price slippage and repays all his original assets, paying only for the swap fees.

Intuition. The core of the price manipulation attack is that the attacker lowers the token exchange rate by using a flash loan. In the second step, the adversary benefits from the decreased exchange rate. As an example, the attacker can gain a profit from the decreased ETH/sUSD exchange rate by borrowing ETH against sUSD as collateral.

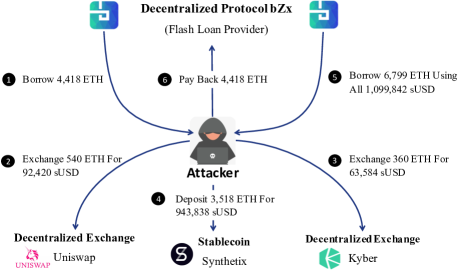

Example. To further elaborate on the price manipulation attack, we present a real-world attack example on the DeFi protocol bZx222bZx: https://bzx.network , as shown in Fig. 4. In this case, the attacker exploits the dependency of bZx on other DeFi protocols (i.e., Uniswap and Kyber) to manipulate the asset exchange rates, making profits within a single atomic transaction. In particular, the attacker takes a sequence of six transactions, consisting of borrowing, exchanging, and repaying assets (e.g., ETH and sUSD). Note that these transactions are packed into the same transaction in the exact order.

Specifically, the attacker first borrows 4,418 ETH from bZx (step ❶ in Fig. 4), then the attacker uses the 4,418 borrowed ETH to exchange for sUSD using other DeFi protocols, i.e., Uniswap, Synthetix, and Kyber, respectively (steps ❷–❹ in Fig. 4). Since bZx relies on Uniswap and Kyber for price oracles, which are susceptible to large amounts of transactions, the attacker can thus heavily skew the exchange rate of ETH/sUSD in bZx in his/her favor. After that, the attacker triggers step ❺, namely, borrowing 6,799 ETH using all holding 1,099,842 sUSD. Finally, the attacker pays back 4,418 ETH in step ❻, which is borrowed at the very beginning. The outcome of steps ❶–❻ is that the attacker gains a net profit of 2,381 ETH (i.e., 2,381 = 6,799 - 4,418), with only a small amount of ETH to pay a gas fee.

III-A3 Reentrancy

In traditional smart contracts, reentrancy is a well-known vulnerability that caused the notorious DAO attack [115]. When a function of a victim contract transfers money to a malicious attack contract , due to the default settings of smart contracts, the fallback function of is automatically triggered. The attack contract can set a malicious operation in its fallback function, i.e., calling again to perform an illegal second-time transfer. As the current execution of is waiting for the first-time transfer to finish, the balance of may not be reduced yet, making wrongly believe that still has enough balance and transfer to again. Therefore, the attack contract can exploit the reentrancy vulnerability to successfully steal additional money from the victim contract. Similarly, DeFi protocols have also suffered from such a reentrancy attack [116]. However, unlike a traditional reentrancy attack on a single smart contract, the flash loan reentrancy attack on DeFi protocols usually involves multiple smart contracts.

Intuition. In essence, a reentrancy attack is caused by some untrusted external calls that interrupt some atomic transactions (e.g., transferring and accounting), resulting in inconsistent variable states. The core of the flash loan reentrancy attack is that the attacker exploits the inconsistent state of different loan pools before and after a contract’s lending (i.e., transferring) to achieve multiple unregistered loans.

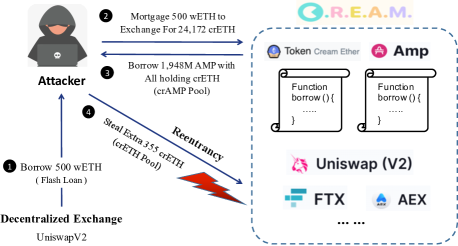

Example. To further illustrate the flash loan reentrancy attack, we present a typical example of the DeFi protocol Cream.Finance333Cream.Finance: https://cream.finance in Fig. 5. Specifically, attacker borrows 500 wETH from UniSwapV2 with a flash loan in step ❶. Then, collateralizes the borrowed 500 wETH to Cream.Finance in exchange for 24,172 crETH in step ❷. Note that Cream.Finance consists of multiple loan pools, each of which is essentially a smart contract. Thereafter, invokes the function borrow in the crAMP pool and exchanges for 1,948 million AMP with all holding crETH in step ❸. However, the transfer of an AMP automatically triggers the fallback function in the attacker’s contract. Since the borrowing status of in the crAMP pool has not been updated, attacker calls the function borrow in another pool crETH in step ❹, thus gaining an extra crETH from the pool.

III-B Deflation Token Attack

Deflation is a term used in crypto finance to describe a drop in the value of an asset due to certain factors such as over-minting [117]. Token deflation refers to the phenomenon that the total supply of tokens decreases each time a token transfer happens. With the rise of decentralized finance, various deflation tokens are emerging. Some types of deflation tokens in DeFi are implemented in the form of deducting a certain percentage of tokens for destruction and redistribution each time a user performs a transaction transfer [21]. This may result in the actual number of tokens received by the recipient being less than the amount paid by the sender. The principle of the deflation token attack is that the attacker exploits such characteristics to reduce the number of a target token by performing multiple in and out transfers, in order to profit from the difference in the amount of the deflation token.

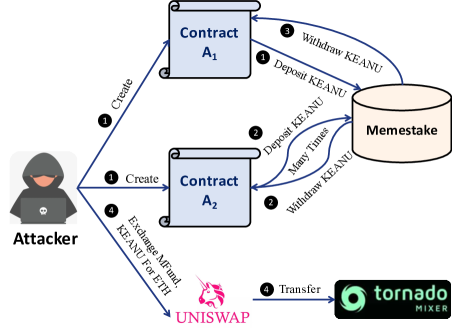

Example. Fig. 6 presents a real-world example to illustrate the deflation token attack on the Memestake contract of the DeFi protocol Sanshu Inu444Sanshu Inu: https://sanshuinufinance.com. The overall attack process can be summarized into the following four steps.

-

•

First, the attacker creates two contracts and initializes them accordingly. Specifically, contract is an investment contract that deposits 2,049 billion KEANU tokens into the Memestake pool, and is the attack contract that is used to manipulate the reward calculation of Memestake.

-

•

Then, the attacker calls to deposit/withdraw a large number of KEANU tokens to/from Memestake many times, forcing Memestake to trade KEANU in large quantities. Since KEANU is a deflation token, each transaction costs of the transaction amount, resulting in the real number of tokens that users deposit to Memestake being smaller than the registered number in user.amount maintained by Memestake. However, when performs the withdrawal operation, Memestake still transfers the recorded amount of tokens to , which leads to the continuous reduction of the token holdings of KEANU in the Memestake pool.

-

•

Next, the attacker uses to modify the value of accMfundPerShare in the Memestake. This value depends on the number of KEANU tokens in the pool that the attacker manipulated in Step ❷. That is, the real number of KEANU tokens in the Memestake has been reduced to a small one. Thus, when withdraws the KEANU tokens deposited in Step ❶, it can receive a reward of MFund tokens far in excess of the normal value.

-

•

Finally, the attacker swaps the extracted MFund and KEANU tokens to ETH, and transfers them away through Tornado, making a net profit of 56 ETH.

III-C Sandwich Attack

A sandwich attack is a typical predatory trading strategy in which a trader wraps a victim transaction with two malicious transactions, one before the victim transaction and one after the victim transaction [54, 89, 118, 79]. In such attacks, the malicious attacker first scans the mempool for pending transactions and finds that a user (i.e., the victim) is trying to trade an asset X for another asset Y. Then, the attacker buys asset Y at a low price. This transaction may be earlier than the victim’s transaction. Once this transaction is completed before the victim’s transaction, the price of asset Y will increase accordingly555 The exchange rate of each transaction is determined by preset algorithms and market liquidity reserves [119]. A buy order will increase the price of an asset, while a sell order decreases the price of the asset. . When the victim’s transaction is carried out, he/she will receive a smaller quantity of asset Y than he/she was supposed to receive due to the increase in the price of asset Y. Finally, the attacker sandwiches the victim’s transaction by selling off asset Y at a higher price than he/she bought it, thereby profiting from the manipulated price. This attack sequence allows the attacker to pocket a profit by front-running and back-running a trader, creating an artificial price rise.

It is worth mentioning that, in the blockchain, the miners sort the transactions in the memory pool according to the gas price, and then select the transactions in the order of the gas price from high to low when creating a block [120, 121]. Therefore, an attacker can achieve the sandwich attack as long as the gas price of the front-running transaction is set slightly higher than that of the victim transaction, and the gas price of the back-running transaction is lower than that of the victim transaction.

Intuition. The core of the sandwich attack is that the attacker hunts for a victim transaction. Then, he/she quickly buys the asset at a low price and ensures that this transaction is scheduled just before the victim transaction (i.e., front-running). Finally, the attacker sells the asset shortly after the victim’s transaction (i.e., back-running) to make a profit.

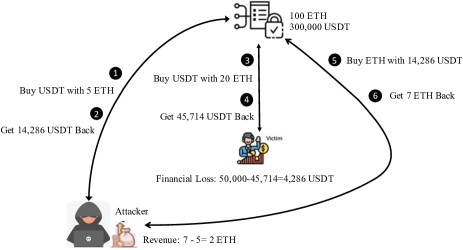

Example. As shown in Fig. 7, the attacker front-runs the victim transaction with a buy order of USDT and back-runs the victim transaction with a sell order. Specifically, the victim transaction aims to buy USDT with 20 ETH. If there are no attackers, the trader will get back 500,000 USDT. However, the attacker front-runs to exchange 14,286 USDT for 5 ETH in steps ❶–❷ and sandwiches the victim transaction. Since the reserves in the liquidity pool change after each transaction. The original state of ETH/USDT is 1/3,000. After the attacker’s first transaction, the state of ETH/USDT becomes 1/2,721. Therefore, in steps ❸–❹, the victim can only exchange 45,714 USDT for 20 ETH, resulting in a loss of 4,286 USDT. After the victim’s transaction, the state of ETH/USDT in the liquidity pool changes to 1/1,920. Finally, the attacker uses all holding 14,286 USDT to exchange for 7 ETH in steps ❺–❻, gaining a profit of 2 ETH.

III-D Rug Pull Attack

Rug pull refers to the draining of investments from DEX liquidity pools or the sudden dereliction of a project, sweeping away investors’ funds without any warning signs [122, 123]. The rug pull attack occurs mostly in decentralized exchanges (DEXs) and is a typical scam in DeFi. Scammers invest a lot of money in liquidity pools and publish attractive advertisements on social media to attract investors. Once investors deposit tokens into these liquidity pools, the scammers will “sweep the carpet”, namely, withdraw all the tokens from the pools.

A typical type of rug pull attack involves manipulating the token price with the attacker’s reserves, such as provoking the token value to drop precipitously to zero. The rug pull attacks in DeFi have caused more than $2.8 billion in losses in 2021, making it the biggest scam in the DeFi ecosystem (accounting for of all scam revenue in 2021) [124].

Example. In July 2021, the digital collectible platform Bondly Finance was compromised [125]. According to the disclosure of the project, the attacker gained access to the password account of the CEO of Bondly Finance through a carefully planned strategy. The password account contains the mnemonic recovery phrase of his hardware wallet, which allows the attacker to access the BONDLY smart contract after copying the password. The attacker exploited this vulnerability to mint 373 million BONDLY on Ethereum, resulting in a significant drop in the token price and a loss of $5.9 million.

| # | DeFi Protocols | Category | Attack Type | Loss2 | Date | Ref. |

|---|---|---|---|---|---|---|

| 1 | bZx-V1 | Lending and Borrowing | Flash Loan Attack | $9.4 Million | 2020.02.17 | [126] |

| 2 | MakerDAO | Other | $9 Million | 2020.03.12 | [127] | |

| 3 | UniSwap | Decentralized Exchange | $0.3 Million | 2020.04.18 | [128] | |

| 4 | bZx-V2 | Lending and Borrowing | $8.1 Million | 2020.09.15 | [129] | |

| 5 | Eminence Finance | Gaming | $15 Million | 2020.09.29 | [130] | |

| 6 | Harvest Finance | Derivative | $33.8 Million | 2020.10.26 | [131] | |

| 7 | Akropolis | Aggregator | $2 Million | 2020.11.12 | [132] | |

| 8 | Pickle Finance | Yield Aggregator | $20 Million | 2020.11.22 | [133] | |

| 9 | Warp Finance | Lending and Borrowing | $7.7 Million | 2020.12.17 | [134] | |

| 10 | Alpha Homora | Derivative | $37.5 Million | 2021.02.13 | [135] | |

| 11 | Spartan | Decentralized Exchange | $40 Million | 2021.05.02 | [136] | |

| 12 | Value DeFi | Derivative | $28 Million | 2021.05.07 | [137, 138, 139] | |

| 13 | Venus | Lending and Borrowing | $300 Million | 2021.05.19 | [140] | |

| 14 | PancakeBunny | Aggregator | $47.1 Million | 2021.05.20 | [141, 142] | |

| 15 | Burgerswap | Decentralized Exchange | $7.2 Million | 2021.05.28 | [143] | |

| 16 | JulSwap | Decentralized Exchange | $0.7 Million | 2021.05.28 | [144] | |

| 17 | Belt Finance | Decentralized Exchange | $50 Million | 2021.05.30 | [145] | |

| 18 | SushiSwap | Decentralized Exchange | $0.11 Million | 2021.07.21 | [146] | |

| 19 | THORChain | Cross-Chain Bridge | $5.8 Million | 2021.07.22 | [147] | |

| 20 | Vee Finance | Lending and Borrowing | $13.5 Million | 2021.09.21 | [148] | |

| 21 | Indexed Finance | Aggregator | $16 Million | 2021.10.14 | [149] | |

| 22 | Cream Finance | Lending and Borrowing | $130 Million | 2021.10.27 | [150] | |

| 23 | Nerve | Portfolio Management | $8 Million | 2021.11.15 | [151] | |

| 24 | Beanstalk | Stablecoin | $182 Million | 2022.04.17 | [152] | |

| 25 | Saddle Finance | Decentralized Exchange | $10 Million | 2022.04.30 | [153] | |

| 26 | Balancer | Portfolio Management | Deflation Token Attack | $0.5 Million | 2020.06.28 | [154] |

| 27 | Sanshu Inu | Gaming | $5 Million | 2020.12.28 | [155] | |

| 28 | Ankr | Other | $5 Million | 2022.12.02 | [156] | |

| 29 | Lendf.Me | Lending and Borrowing | Reentrancy Attack | $25 Million | 2020.04.18 | [157] |

| 30 | Origin | Other | $7 Million | 2020.11.17 | [158] | |

| 31 | Grim Finance | Derivative | $30 Million | 2021.12.19 | [159] | |

| 32 | Rari Capital | Lending and Borrowing | $90 Million | 2022.04.30 | [160, 161] | |

| 33 | FEI protocol | Stablecoin | $80 Million | 2022.04.30 | [162] | |

| 34 | Mango | Decentralized Exchange | Sandwich Attack | $100 Million | 2022.10.12 | [163] |

| 35 | BONDLY | Stablecoin | Rug Pull Attack | $22 Million | 2021.07.15 | [164] |

| 36 | Bancor | Decentralized Exchange | Smart Contract Logic Bug | $23.5 Million | 2020.06.16 | [165] |

| 37 | DODO Pool | Decentralized Exchange | $3.8 Million | 2021.03.09 | [166] | |

| 38 | Uranium Finance | Decentralized Exchange | $50 Million | 2021.04.28 | [167] | |

| 39 | ChainSwap | Cross-Chain Bridge | $4.8 Million | 2021.07.11 | [168, 169] | |

| 40 | Popsicle | Derivative | $25 Million | 2021.08.04 | [170] | |

| 41 | Poly Network | Cross-Chain Bridge | $611 Million | 2021.08.10 | [171] | |

| 42 | Compound Finance | Lending and Borrowing | $160 Million | 2021.10.03 | [172] | |

| 43 | PAID Network | Decentralized Exchange | Compromised Private Key | $160 Million | 2021.03.05 | [173] |

| 44 | Ronin | Gaming | $622 Million | 2022.03.23 | [34] | |

| 45 | Oypn | Insurance | Other | $0.37 Million | 2020.08.04 | [174] |

| 46 | Chainlink | Stablecoin | $0.34 Million | 2020.08.30 | [175] | |

| 47 | Cover | Insurance | $5 Million | 2020.12.28 | [176] | |

| 48 | yCredit Finance | Decentralized Exchange | $326 Million | 2021.01.02 | [177] | |

| 49 | Yearn Finance | Aggregator | $11 Million | 2021.02.04 | [178] | |

| 50 | Furucombo | Aggregator | $15 Million | 2021.02.27 | [179] | |

| 51 | EasyFi | Lending and Borrowing | $80 Million | 2021.04.20 | [180] | |

| 52 | VaultSX | Other | $13.5 Million | 2021.05.16 | [181] | |

| 53 | AnySwap | Decentralized Exchange | $7.9 Million | 2021.07.10 | [182] | |

| 54 | SafeDollar | Stablecoin | $0.25 Million | 2021.07.28 | [183] | |

| 55 | BadgerDAO | Other | $120 Million | 2021.12.02 | [184] | |

| 56 | Wormhole | Message Passing | $7.7 Million | 2022.02.02 | [185] | |

| 57 | Nomad | Cross-chain Bridge | $190 Million | 2022.08.02 | [186] |

Due to the complexity and diversity of the DeFi ecosystem, we are unable to describe each type of DeFi attack and vulnerability in detail. We have listed the well-known DeFi protocols that have suffered from a DeFi attack over the past three years in Table I. Additionally, we refer the readers to [187] for more hacks, frauds, and scams in DeFi.

IV Review of Smart Contract and DeFi Security Tools

To safeguard the security of participant funds and privacy in smart contracts and DeFi protocols, recent advancements put forward corresponding solutions by incorporating vulnerability detection and automated repair techniques.

-

•

Vulnerability Detection. A plethora of work has been designed to automatically identify vulnerabilities in smart contracts. Existing surveys have provided a relatively comprehensive overview of current bug-finding tools for smart contracts. However, a fine-grained classification and empirical comparison of existing methods is still lacking. Moreover, many of these approaches are tailored for traditional smart contracts, which are typically single contracts. It is necessary and critical to verify whether these methods can effectively handle complex DeFi protocols. Towards these, we not only perform an empirical analysis of existing smart contract bug detection tools but also evaluate their effectiveness in detecting vulnerabilities in DeFi protocols.

Furthermore, several recent efforts have explored detecting attacks against DeFi protocols by analyzing the DeFi transactions and restoring the high-level DeFi semantics. Given the lack of review of attack detection tools on DeFi protocols, we illustrate the design of existing DeFi attack hunting techniques, as well as their workflow.

-

•

Automated Repair. While existing tools are able to identify vulnerabilities and highlight the affected code lines in smart contracts, they exhibit certain limitations in automatically providing patches. In this context, smart contract automated repair is emerged as a countermeasure. Unfortunately, due to the immutability of the underlying blockchain, the smart contract cannot be updated once deployed. Therefore, traditional program repair techniques cannot be applied to smart contracts. This makes it challenging to fix vulnerabilities in smart contracts. Recently, several efforts have been proposed to automatically patch vulnerabilities in smart contracts and DeFi protocols, leading to a new branch of smart contract security. However, a systematic review of existing automated repair methods for smart contracts is still missing. Towards this, we conduct a comprehensive review of current automated repair approaches, expecting to provide overall insights and facilitate future work.

In what follows, we will introduce the existing bug detection and automated repair techniques for smart contracts and DeFi protocols, respectively.

IV-A Vulnerability Detection

In this subsection, we investigate 42 well-known approaches that are able to detect smart contract vulnerabilities and DeFi attacks, which are listed in Table II. More specifically, we first demonstrate the principles of the smart contract vulnerability detection tools, organized by the specific analysis techniques on which they are mainly based on. Furthermore, we summarize the vulnerability types supported by the smart contract vulnerability detection tools and list them in Table III. Finally, we elaborate on the design of existing DeFi attack hunting approaches as well as their workflow, hoping to push forward the boundaries of this research direction.

| # | Tool | Type | Analysis Level | Public Available | Reference |

| 1 | Securify | Formal Verification | Bytecode | https://github.com/eth-sri/securify2 | [188, 189] |

| 2 | VeriSmart | Source Code | https://github.com/kupl/VeriSmart-public | [190] | |

| 3 | VeriSol | Source Code | https://github.com/microsoft/verisol | [191] | |

| 4 | Zeus | Source Code | Not Available | [192] | |

| 5 | DefectChecker | Symbolic Execution | Bytecode | https://github.com/Jiachi-Chen/DefectChecker | [193] |

| 6 | HoneyBadger | Bytecode | https://github.com/christoftorres/HoneyBadger | [194] | |

| 7 | Maian | Bytecode | https://github.com/MAIAN-tool/MAIAN | [195] | |

| 8 | Manticore | Bytecode | https://github.com/trailofbits/manticore | [196] | |

| 9 | Mythril | Bytecode | https://github.com/ConsenSys/mythril | [197] | |

| 10 | Oyente | Bytecode | https://github.com/melonproject/oyente | [198] | |

| 11 | Osiris | Bytecode | https://github.com/christoftorres/Osiris | [199] | |

| 12 | Sereum | Bytecode | https://github.com/uni-due-syssec/eth-reentrancy-attack-patterns | [200] | |

| 13 | TeEther | Bytecode | https://github.com/nescio007/teether | [201] | |

| 14 | VerX | Source Code | https://github.com/eth-sri/verx-benchmarks | [202] | |

| 15 | Ethir | Intermediate Representation | Bytecode | https://github.com/costa-group/ethIR | [203] |

| 16 | Smartcheck | Source Code | https://github.com/smartdec/smartcheck | [204] | |

| 17 | Slither | Source Code | https://github.com/crytic/slither | [50] | |

| 18 | Vandal | Bytecode | https://github.com/usyd-blockchain/vandal | [205] | |

| 19 | ContractFuzzer | Fuzzing Test | Bytecode | https://github.com/gongbell/ContractFuzzer | [51] |

| 20 | ContraMaster | Source Code | https://github.com/ntu-SRSLab/vultron | [206, 207] | |

| 21 | Regurad | Source Code | Not Available | [208] | |

| 22 | ILF | Source Code | https://github.com/eth-sri/ilf | [209] | |

| 23 | Harvey | Source Code | Not Available | [210, 47] | |

| 24 | ConFuzzius | Bytecode | https://github.com/christoftorres/ConFuzzius | [211] | |

| 25 | sFuzz | Bytecode | https://github.com/duytai/sFuzz | [212] | |

| 26 | xFuzz | Source Code | https://github.com/ToolmanInside/xfuzz_tool | [213] | |

| 27 | Smartian | Bytecode | https://github.com/SoftSec-KAIST/Smartian | [214] | |

| 28 | RLF | Source Code | https://github.com/Demonhero0/rlf | [215] | |

| 29 | IR-Fuzz | Source Code | https://github.com/Messi-Q/IR-Fuzz | [216] | |

| 30 | ItyFuzz | Source Code | https://github.com/fuzzland/ityfuzz | [217] | |

| 31 | SaferSC | Deep Learning | Bytecode | https://github.com/wesleyjtann/Safe-SmartContracts | [218] |

| 32 | ReChecker | Source Code | https://github.com/Messi-Q/ReChecker | [219] | |

| 33 | ContractWard | Bytecode | Not Available | [220] | |

| 34 | S-gram | Source Code | https://github.com/njaliu/sgram-artifact | [221] | |

| 35 | TMP | Source Code | https://github.com/Messi-Q/GNNSCVulDetector | [222, 9] | |

| 36 | DeeSCVHunter | Source Code | Not Available | [223] | |

| 37 | CodeNet | Source Code | Not Available | [224] | |

| 38 | DL-MDF | Source Code | Not Available | [225] | |

| 39 | BlockEye | DeFi Attack Hunting | DeFi protocol | Not Available | [53] |

| 40 | DeFiRanger | DeFi protocol | Not Available | [55] | |

| 41 | Flashot | DeFi protocol | Not Available | [52] | |

| 42 | ProMutator | DeFi protocol | https://github.com/csienslab/ProMutator | [30] |

| Tool | Vulnerability Type | |||||||||||||||

| AC | AF | BD | DS | DD | FE | GS | LE | RE | IO | SC | SA | TO | TX | UC | UE | |

| CodeNet [224] | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ |

| ConFuzzius [211] | ✗ | ✓ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ |

| ContractFuzzer [51] | ✓ | ✗ | ✓ | ✗ | ✓ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ |

| ContraMaster [206, 207] | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ |

| ContractWard [220] | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ |

| DeeSCVHunter [223] | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| DefectChecker [193] | ✗ | ✗ | ✓ | ✓ | ✗ | ✓ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ |

| DL-MDF [225] | ✗ | ✗ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| Ethir [203] | ✓ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ |

| Harvey [210, 47] | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ |

| HoneyBadger [194] | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| ILF [209] | ✓ | ✗ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ |

| IR-Fuzz [216] | ✓ | ✗ | ✓ | ✗ | ✓ | ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ |

| ItyFuzz [217] | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ |

| Maian [195] | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ |

| Manticore [196] | ✓ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ |

| Mythril [197] | ✓ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ |

| Oyente [198] | ✓ | ✓ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ |

| Osiris [199] | ✗ | ✓ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| ReChecker [219] | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| Regurad [208] | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| RLF [215] | ✗ | ✗ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ |

| SaferSC [218] | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ |

| Securify [188, 189] | ✓ | ✗ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | ✓ |

| Sereum [200] | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| S-gram [221] | ✗ | ✓ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| sFuzz [212] | ✓ | ✗ | ✓ | ✗ | ✓ | ✓ | ✓ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ |

| Smartcheck [204] | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ |

| Smartian [214] | ✗ | ✓ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ |

| Slither [50] | ✓ | ✗ | ✓ | ✓ | ✓ | ✓ | ✗ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ |

| TeEther [201] | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ |

| TMP [222, 9] | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| Vandal [205] | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ |

| VeriSmart [190] | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| VeriSol [191] | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| VerX [202] | ✓ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✗ |

| xFuzz [213] | ✗ | ✗ | ✓ | ✗ | ✓ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✓ | ✗ | ✗ |

| Zeus [192] | ✗ | ✗ | ✓ | ✗ | ✗ | ✗ | ✗ | ✗ | ✓ | ✓ | ✗ | ✗ | ✓ | ✓ | ✓ | ✓ |

IV-A1 Static Analysis

Static analysis refers to the technique of analyzing programs without actually executing them. It examines code in the absence of real input data and is capable of detecting potential security violations, runtime errors, and logical inconsistencies. Static analysis techniques have been widely applied to smart contract vulnerability detection, which can be broadly divided into two categories, i.e., formal verification [228] and symbolic execution [229]. In particular, when performing static analysis on smart contracts, researchers often utilize intermediate representation-based analysis methods [230], which can store and preserve the rich semantics of the Source Code.

Formal Verification

Formal verification eliminates the ambiguity and incompatibility in a smart contract by transforming its concepts, judgments, and logic into a formal model [231]. It cooperates with rigorous proofs to verify the correctness and security of functions in smart contracts. Common formal verification methods include model checking [232] and deductive verification [233]. Specifically, model checking enumerates all possible states of a smart contract through state-space searching and then checks whether the contract has corresponding security properties. Deductive verification uses logical formulas to describe a verification system and then proves whether the system has certain security properties through predefined rules. In general, formal verification techniques mainly propose a formal model and define the formal semantics of contracts to verify the security properties in smart contracts. We review existing formal verification methods for smart contract bug detection and give their brief principles as follows.

-

•

Securify [188] extracts the semantic information from the bytecode of smart contracts and then takes advantage of a set of compliance and violation security patterns that capture sufficient conditions to prove the presence or absence of vulnerabilities.

-

•

VeriSmart [190] is an accurate verifier for ensuring arithmetic safety of smart contracts. Particularly, it takes advantage of a domain-specific algorithm to automatically discover and exploit transaction invariants, which are essential for precisely analyzing smart contracts.

-

•

VeriSol [191] is a highly automated formal verifier that checks the semantic compliance of smart contracts against a state machine model with an access control policy.

-

•

Zeus [192] employs abstract interpretation and symbolic model checking to ascertain verification conditions, and verifies the correctness of smart contracts during the formal verification process.

Symbolic Execution. Symbolic execution methods analyze software programs using symbolic values as inputs rather than specific values during execution [234]. Once a program branch is reached, the analyzer collects the corresponding path constraints following a constraint solver to obtain specific values that can trigger each branch. Notably, symbolic execution is capable of exploring multiple paths simultaneously. However, it also faces unavoidable problems such as path explosion. In most cases, the symbolic executor first constructs a control flow graph (CFG) from the Bytecode. It then designs appropriate constraints based on the characteristics of the vulnerabilities. Finally, the executor uses the constraint solver to analyze the control flow graph and generate the bug report. We present well-known symbolic execution-based vulnerability detection methods for smart contracts as follows.

-

•

DefectChecker [193] is a symbolic execution-based bug checker that analyzes the smart Bytecode to generate the CFG, stack event, and three code features (i.e., Money Call, Loop Block, and Payable Function), and combines them to detect vulnerabilities.

-

•

HoneyBadger [194] is built on a taxonomy of honeypot techniques. It adopts symbolic execution and well-defined heuristics to pinpoint various types of honeypots in smart contracts.

-

•

Maian [195] keeps track of contracts that can self-destruct or drain Ether from arbitrary addresses, or those that accept Ether but have no payout functionality. It performs inter-procedural symbolic analysis and uses a concrete validator to expose vulnerabilities.

-

•

Manticore [196] is a dynamic symbolic execution framework for analyzing bytecode of smart contracts, providing an effective way to maximize code coverage and find execution paths that lead to vulnerabilities and reachable self-destruct operations.

- •

-

•

Oyente [198] is one of the pioneer smart contract analysis tools. It uses symbolic execution to identify smart contract vulnerabilities based on the control flow graph. Oyente is also used as a basis for several other tools, such as HoneyBadger, Maian, and Osiris.

-

•

Osiris [199] extends Oyente and supports to detect the integer overflow vulnerability of smart contracts.

-

•

Sereum [200] employs dynamic taint tracking to monitor the data flow during the contract execution, avoiding inconsistent states and effectively preventing reentrancy attacks.

-

•

teEther [201] searches for vulnerable execution traces in a contract’s control flow graph and automatically creates an exploit for a contract given only its bytecode.

-

•

VerX [202] is a automated verifier prove functional specifications of smart contracts. It incorporates the delayed predicate abstraction approach, which combines symbolic execution during transaction execution with abstraction at transaction boundaries, facilitating the automatic verification of the security properties of smart contracts.

Intermediate Representation. As the logic of smart Source Code becomes more complex, it becomes increasingly difficult to deal with the source code directly [236]. A family of works, instead, can deal with pure bytecode [237, 238]. However, they still suffer from low accuracy due to the inherent difficulty of interpreting bytecode and restoring comprehensive data and control flow dependencies in the missing source code. To facilitate the analysis of smart contracts, researchers probe to convert the source code or bytecode of a smart contract into an abstract code structure that is conducive for further processing, referred to as an intermediate representation (IR), and then analyze the IR to discover security problems. An intermediate representation of the smart contract is an arbitrary representation of a program between the source code and the bytecode [230, 50, 239, 240, 241]. Since the intermediate representation abandons the complex logic in the source code while preserving rich data and control flow semantics, it can be favorable to further processing and analysis. We conclude intermediate representation-based analysis techniques for smart contracts as follows.

-

•

Ethir [203] converts the control flow graph of smart contracts into the rule-based intermediate representation (RBP), and then infers the security properties of smart contracts based on the RBP.

-

•

SmartCheck [204] is an extensible static analysis tool for smart contracts, which converts the source code of a smart contract into an XML-based intermediate representation. It uses the lexical and syntactic analysis of the Solidity source code, looking for vulnerability patterns and bad coding practices.

-

•

Slither [50] converts the smart Source Code into an intermediate representation of SlithIR. SlithIR uses a static single allocation (SSA) form and a reduced instruction set to simplify the contract analysis process while preserving the semantic information of the source code.

-

•

Vandal [205] is composed of an analysis pipeline and a decompiler. The decompiler performs an abstract interpretation to convert the bytecode into an intermediate representation in the form of logical relations, and then uses novel logic-driven methods to detect vulnerabilities in smart contracts.

IV-A2 Fuzzing Test

Fuzzing has proven to be a successful technique for discovering software bugs over the past decades [242]. A wide variety of fuzzing methods have emerged, such as whitebox, blackbox, and greybox [243, 244, 245]. The main idea of fuzzing techniques is to feed a mass of test inputs (i.e., test cases) into the program under test and expose vulnerabilities by monitoring the reported abnormal results or exceptions [51]. When applied to smart contracts, a fuzzing engine first attempts to generate initial seeds and form executable transactions. With the assistance of the feedback of test results, it will dynamically adjust the generated test cases to explore as much contract state space as possible. This process is repeated until a stopping criterion is satisfied. Finally, the fuzzer will analyze the results generated during fuzzing and report to users. We review current smart contract fuzzing methods and summarize their principles as follows.

-

•

ContractFuzzer [51] is one of the earliest fuzzing frameworks for smart contracts, which identifies vulnerabilities by monitoring runtime behavior during a fuzzing campaign.

-

•

ContraMaster [206] is an oracle-supported dynamic exploit generation framework for detecting vulnerabilities in smart contracts. It combines the analysis of data-flows, control-flows, and contract state information to guide seed mutation.

-

•

ReGuard [208] is a fuzzing-based analyzer to automatically detect reentrancy vulnerabilities in Ethereum smart contracts. It dynamically identifies reentrancy bugs by iteratively generating random but diverse transactions.

-

•

ILF [209] proposes a new approach for learning an effective yet fast fuzzer from symbolic execution by phrasing the learning task in the framework of imitation learning.

-

•

Harvey [210] extends standard greybox fuzzing for predicting new test inputs that are more likely to cover new paths or reveal vulnerabilities in smart contracts.

-

•

ConFuzzius [211] is a hybrid fuzzer for smart contracts that uses evolutionary fuzzing to exercise shallow parts of a smart contract. Specifically, it employs constraint solving to generate test cases, enforcing the fuzzer to reach complex and deep branches.

-

•

sFuzz [212] presents an efficient and lightweight multi-objective adaptive strategy to dig out potential vulnerabilities hidden in the hard-to-cover branches.

-

•

xFuzz [213] is a machine learning-guided smart contract fuzzing framework that uses machine learning predictions to guide fuzzers for vulnerability detection.

-

•

Smartian [214] employs a novel feedback mechanism, i.e., data-flow-based feedback, to guide the greybox fuzzer to systematically generate critical transaction sequences.

-

•

RLF [215] introduces a reinforcement learning-guided fuzzing framework for smart contracts, which drives the fuzzer to generate vulnerable transaction sequences.

-

•

IR-Fuzz [216] extends sFuzz, which engages in a sequence generation strategy that contains invocation ordering and prolongation to trigger deeper states in a smart contract.

-

•

ItyFuzz [217] is a snapshot-based fuzzer for testing smart contracts, which incorporates new waypoint mechanisms optimized to prioritize the exploration of interesting snapshot states, allowing for efficient program exploitation. In particular, ItyFuzz is able to analyze complex DeFi protocols and identify the price manipulation vulnerability.

IV-A3 Deep Learning-based Methods

In recent years, there has been a growing practice of detecting program security vulnerabilities using deep learning technologies [246, 247]. The advancement of deep learning has promoted the emergence of various vulnerability detection methods [248, 249]. Existing deep learning-based methods usually convert smart contracts into intermediate representations and then construct a deep neural network as the detection model. As deep learning technology has demonstrated its superiority in handling sophisticated data, it can also be applied to deal with the complex business logic of DeFi protocols. We provide existing deep learning-based smart contract vulnerability detection methods as follows, hoping to inspire others.

-

•

SaferSC [218] is the first deep learning-based vulnerability detection model for smart contracts, which analyzes the operation code (i.e., opcode) of smart contracts and trains a long short-term memory network (LSTM) as the detection model.

-

•

ReChecker [219] constructs the bidirectional long short-term memory network based on an attention mechanism to precisely detect the reentrancy vulnerability.

-

•

ContractWard [220] extracts bigram features from the smart contract opcode and adopts a variety of machine learning algorithms to detect bugs in smart contracts.

-

•

S-gram [221] introduces a novel semantic-aware security auditing technique for analyzing smart contracts. The key insight behind S-gram is a combination of -gram language modeling and lightweight static contract analysis.

-

•

TMP [222] proposes to cast the source code of a smart contract into a contract graph and builds a temporal-message-propagation graph model to identify vulnerabilities.

-

•

DeeSCVHunter [223] uses a modularized and systematic deep learning-based framework to detect vulnerabilities in smart contracts. It employs the proposed vulnerability candidate slice (VCS) to guide the model to capture the critical part of the vulnerability.

-

•

CodeNet [224] is a code-targeted convolutional neural network (CNN) architecture that detects vulnerable smart contracts while preserving their semantics and context.

-

•

DL-MDF [225] identifies smart contract vulnerabilities based on deep learning and multimodal decision fusion. Specifically, it extracts the features of the source code, operation code, and control flow of a smart contract through multiple models respectively, and then adopts a multimodal decision fusion strategy to output the detection results.

IV-A4 DeFi Attack Hunting

Generally speaking, detecting DeFi attacks requires the ability to recover and understand the logical semantics of DeFi protocols, which is typically missing in the aforementioned solutions that find bugs only in traditional smart contracts. Current DeFi attack hunting methods [55, 30, 53] consider simulating the attack process to detect potential DeFi attack behaviors. Technically, they monitor the contract transactions during the attack simulation and reveal DeFi attacks using the patterns with the recovered high-level semantics of DeFi protocols. In what follows, we will elaborate on the specific design and workflow of existing DeFi attack hunting tools.

BlockEye

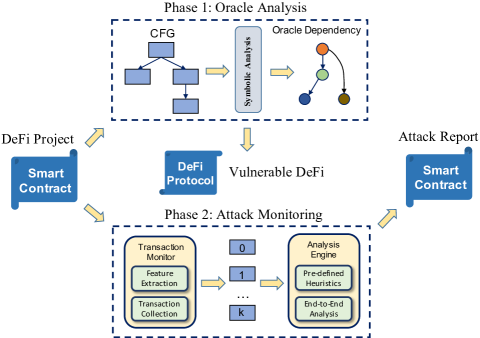

BlockEye [53] is a real-time attack detection system for DeFi protocols. It models interdependencies between DeFi protocols and flags potential DeFi attacks with an end-to-end analysis in real-time. The key insights behind BlockEye are symbolic oracle analysis and pattern-based runtime transaction validation. To illustrate the overall insights of BlockEye, we further describe its workflow in Fig. 8, where BlockEye works in two phases. In the first phase, BlockEye performs symbolic analysis on smart contracts of a given DeFi protocol. Specifically, the goal of this phase is to model the inter-DeFi oracle dependency, i.e., how the oracle data provided by one DeFi protocol affects the services of another. Once oracle-dependent state updates are found, BlockEye identifies the DeFi protocols as potentially vulnerable. In the second phase, BlockEye installs a runtime monitor for vulnerable DeFi protocols to detect external attacks. Specifically, BlockEye employs a transaction monitor to collect related transactions based on extracted characteristics. Then, the end-to-end analysis of transactions is performed according to predefined heuristics, e.g., a large profit is made in a short period. Potential attacks are flagged by BlockEye if an abnormal sequence of transactions is detected. Finally, BlockEye generates an analysis report for attack verification.

DeFiRanger

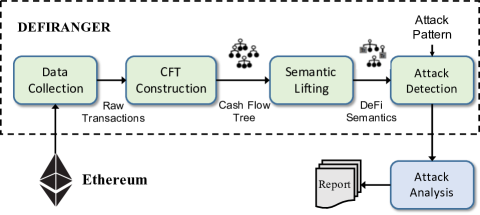

DeFiRanger [55] is designed to detect price manipulation attacks on DeFi protocols. Specifically, DeFiRanger restores the high-level semantics of DeFi protocols by constructing the cash flow tree (CFT) from transactions and lifting the low-level semantics to high-level ones. After that, DeFiRanger detects price manipulation attacks using the patterns expressed with recovered DeFi semantics. The workflow of DeFiRanger is depicted in Fig. 9. DeFiRanger initially collects raw Ethereum transactions, and then constructs the cash flow tree that is used to convert raw transactions to token transfers. Then, DeFiRanger uses a lifting algorithm to recover the DeFi semantics from the CFT. Finally, DeFiRanger detects price manipulation attacks by matching recovered semantics with attack patterns or rules.

ProMutator

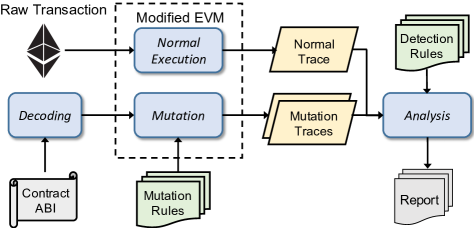

ProMutator [30] is a scalable security analysis framework that can detect price oracle vulnerabilities in DeFi protocols. ProMutator simulates price oracle attacks on a DeFi protocol locally and observes how a price oracle handles abnormal price data feeds. Fig. 10 shows the high-level workflow of ProMutator, which processes each transaction through three phases: decoding, mutation, and analysis. ProMutator detects the price oracle bug by using built-in mutation and detection rules, which can be extended to cover other types of vulnerabilities using custom mutation and detection rules. ProMutator outputs whether a target DeFi protocol is vulnerable based on the detection rules and the analysis of mutated traces.

Flashot

Flashot [52] is a framework that is able to reveal the microscopic process of the flash loan attack in a clear and precise way. Specifically, Flashot is designed to illustrate the precise asset flows intertwined with smart contracts in a standardized diagram. In addition, Flashot performs an in-depth analysis of a typical flash loan attack (e.g., pump and arbitrage), with a more accurate model and solution regarding the optimization problem, as well as some economic explanations for the attacker’s malicious behavior.

IV-B Automated Repair

In this subsection, we review 8 existing automated repair tools for smart contracts and DeFi protocols, which are listed in Table IV. In particular, we summarize the principles of each automated repair tool, and then present their advantages and disadvantages.

SCRepair

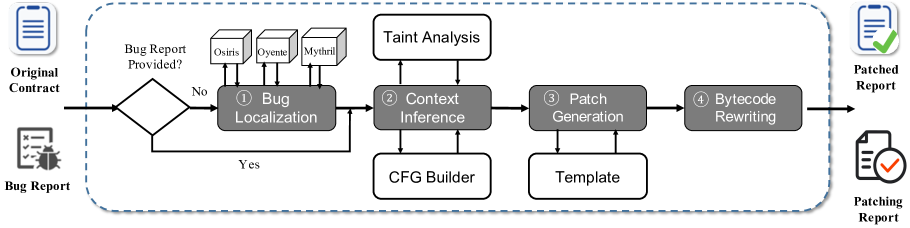

[250] propose an automated smart contract repair tool SCRepair using a genetic programming search method. SCRepair performs parallel genetic repair by partitioning the large search space of candidate patches into smaller mutually exclusive search spaces that can be processed individually. Considering the gas consumption of patches, SCRepair integrates a gas-awareness technique that compares candidate patches in terms of gas cost, thus screening out the patches that are useful and lower gas cost. Notably, SCRepair suffers from the inherent problems: 1) the generated patches are incomplete, which can sometimes lead to ineffectiveness, 2) the selected patches may break the functionality of the original contract, and 3) it is unable to repair the off-chain contracts.

[b] Tool Analysis Level Vulnerability Number Public Available Reference SCRepair Source Code 4 https://github.com/xiaoly8/SCRepair [250] SMARTSHIELD Bytecode 3 Not Available [251] sGuard Source Code 4 https://github.com/duytai/sGuard [252] EVMPatch Bytecode 2 https://github.com/uni-due-syssec/evmpatch-developer-study [253] Aroc Source Code 4 Not Available [254] HCC Source Code 2 Not Available [255] Elysium Bytecode 7 https://github.com/christoftorres/Elysium [256] DeFinery1 Source Code 4 https://sites.google.com/view/ase2022-definery [257]

-

1

DeFinery is built on SCRepair. DeFinery enables property-based automated repair of smart contracts while providing formal correctness guarantees.

SMARTSHIELD

[251] develop a bytecode rectification system SMARTSHIELD to automatically fix three types of bugs in smart contracts. The overall workflow of SMARTSHIELD consists of three steps: 1) extracting the abstract syntax tree (AST) and the unfixed bytecode of a smart contract to capture its bytecode-level semantic information; 2) generating the patches to repair the insecure control flows and data operations based on the semantic information; 3) outputting the patched bytecode and a bug repair report.

sGuard

[252] propose an automatic fixing approach that can transform smart contracts to be free of 4 kinds of vulnerabilities. Given a smart contract, sGuard works in two phases: 1) collects a finite set of symbolic execution traces of the smart contract and then performs static analysis on the collected traces to identify potential vulnerabilities, and 2) applies specific fixing patterns for each type of bug at the source code level. Unfortunately, sGuard performs source code rewriting without further analysis of the interactions between different functions and the global dependencies of memory variables. The lack of such analysis in smart contract patching typically results in the destruction of the functionality of the original contract.

EVMPatch

[253] present an automated repair framework, called EVMPatch, to patch faulty smart contracts. EVMPatch works in two main steps. In the first step, based on designed patch rules, EVMPatch uses a bytecode rewriting engine to fix a basic block that has a vulnerability and appends the fixed block to the end of the contract. In the second step, after fixing a contract, EVMPatch replays some of the historical transactions of the original contract on a local Ethereum client to verify that the fixed contract is correct by observing whether attack transactions are blocked and whether other transactions are normal. However, EVMPatch only works when the vulnerability is located within a single bytecode basic block, while having difficulties in handling vulnerabilities across separated basic blocks.

Aroc

[254] propose a smart contract repairer named Aroc that can automatically fix vulnerable on-chain contracts without updating the contract code. Aroc consists of three main components: 1) an information extraction module, which captures the variable dependencies, path constraints, and contract metadata to synthesize patches given vulnerable contract source code and bug types; 2) a patch generation module, which produces patches according to the repair templates; 3) an enhanced EVM, which binds the generated patches to fix the vulnerable contract and block the malicious transactions. However, Aroc only works on its own enhanced EVM, and the binding features cannot yet be accepted by the official Ethereum.

HCC