An entropy penalized approach for stochastic control problems. Complete version.

Abstract

In this paper, we propose an alternative technique to dynamic programming for solving stochastic control problems. We consider a weak formulation that is written as an optimization (minimization) problem on the space of probabilities. We then propose a regularized version of this problem obtained by splitting the minimization variables and penalizing the entropy between the two probabilities to be optimized. We show that the regularized problem provides a good approximation of the original problem when the weight of the entropy regularization term is large enough. Moreover, the regularized problem has the advantage of giving rise to optimization problems that are easy to solve in each of the two optimization variables when the other is fixed. We take advantage of this property to propose an alternating optimization algorithm whose convergence to the infimum of the regularized problem is shown. The relevance of this approach is illustrated by solving a high-dimensional stochastic control problem aimed at controlling consumption in electrical systems.

Key words and phrases: Stochastic control; optimization; Donsker-Varadhan representation; exponential twist; relative entropy.

2020 AMS-classification: 49M99; 49J99; 60H10; 60J60; 65C05.

1 Introduction

Stochastic control problems appear in many fields of application such as robotics [34], economics and finance [37]. Their numerical solution is most often based on the dynamic programming principle allowing the representation of the value function via nonlinear Hamilton-Jacobi-Bellman PDEs or Backward Stochastic Differential Equations (BSDEs). This permits to estimate recursively the value (Bellman) functions backwardly from the terminal instant to the initial instant. However, when the state space is large, estimating the Bellman functions becomes challenging due to the curse of dimensionality. In the last twenty years, mainly motivated by applications in finance, important progress has been made in this field, especially around the numerical resolution of BSDEs or PDEs. We can mention in particular variance reduction techniques [4, 19, 20], neural network based approaches [21, 18], time reversal techniques [23] or Lagrangian decomposition techniques [11, 31].

The idea of this paper is to propose a radically different approach based on a weak reformulation of the stochastic control problem as an optimization problem on the space of probabilities. Interest in optimization problems on the space of probabilities has increased strongly during the recent years with the Monge-Kantorovitch optimal transport problem, which, for two fixed Borel probabilities on , and consists in determining a joint law whose marginals are precisely and , minimizing an expected given cost. Benamou and Brenier in [3] propose a dynamical formulation of this problem: it consists in an optimal control problem where the aim is to minimize the integrated kinetic energy of a deterministic dynamical system over a given time horizon, in order to go from the initial law to as terminal law. Mikami and Thieullen in [35] replace the deterministic dynamical system with a diffusion introducing the so called stochastic mass transportation problem. This consists in controlling the drift of the diffusion to minimize over a given finite horizon a mean integrated cost depending on the drift and the state of the process, while imposing the initial and final distribution of the diffusion. Those authors formulate their problem as an optimization on a space of probabilities, for which they make use of convex duality techniques. Tan and Touzi generalize these techniques in [33], controlling the volatility as well. Those authors also propose a numerical scheme in order to approximate the dual formulation of their stochastic mass transport problem.

In the same spirit as in [35], in this paper, we formulate a stochastic optimal control problem as a minimization on the space of probability measures. We propose an entropic regularization of this optimization problem which suitably approximates the original control problem. Under mild convexity conditions, we prove the convergence of an alternating optimization algorithm to the infimum of the regularized problem and the performance of this algorithm is shown to be competitive in simulation with existing regression-based Monte Carlo approaches relying on dynamic programming. The proof of the convergence of our algorithm relies on geometric arguments rather than classical convex optimization techniques.

More precisely, on some filtered probability space , we are interested in a problem of the type

| (1.1) |

where is a progressively measurable processes taking values in some fixed convex compact domain . will be a controlled diffusion process taking values in of the form

| (1.2) |

The above problem corresponds to the strong formulation of a stochastic control problem in the sense of Problem (II.4.1.SS) in [38], and can be generally associated with a weak formulation in the sense of Problem (II.4.2.WS) in [38], resulting in an optimization problem on a space of probability measures of the form

| (1.3) |

with a set of probability measures defined in Definition 3.2, such that under the canonical process is decomposed as

| (1.4) |

where is a progressively measurable process with respect to the canonical filtration of taking values in and is some standard Brownian motion. We refer to [25, 37] for a detailed account of stochastic optimal control in strong form and to [38, 15] for more details on the weak formulation of stochastic optimal control. The link between those two formulations is discussed in Appendix 7.4.

Our essential hypothesis is here that the running cost is convex in the control variable . Besides the question of the existence of a probability for which in (1.3), the problem of approximation is crucial. One major difficulty is the lack of convexity of the functional in (1.3) with respect to , even though the literature includes some techniques to transform the original problem into a minimization of a convex functional, see e.g. [3]. For that reason, we cannot rely on classical convex analysis techniques, see e.g. [14], in order to perform related algorithms, see e.g. [7]. As announced above, our method consists in replacing Problem (1.3) with the regularized version

| (1.5) |

where is a subset of elements defined in Definition 3.7, is the relative entropy, see Definition 2.1, and the regularization parameter is intended to vanish to zero in order to impose . In Theorem 3.9 one shows that previous infimum is indeed a minimum (attained on some admissible couple of probability measures ). Given one solution of Problem (1.5), Proposition 3.10 shows that is an approximate solution of Problem (1.3) in the sense that and the infimum can be indeed approached by when and more precisely .

The interest of the regularized Problem (1.5) with respect to the original Problem (1.3) is that the minimization of the functional with respect to one variable or (the other variable being fixed) can be provided explicitly, see Section 5.1 (for the minimization with respect to ) and Section 5.2 (for the minimization with respect to ). Indeed, on the one hand, the resolution with respect to is a well-known problem in the area of large deviations, see [13]. It gives rise to a variational representation formulas relating log-Laplace transform of the costs and relative entropy which is linked to a specific case of stochastic optimal control for which it is possible to linearize the HJB equation by an exponential transform, see [16, 17]. This type of problem is known as path integral control and has been extensively studied with many applications, see [36, 34, 10]. On the other hand, the minimization with respect to can be reduced to pointwise minimization. Indeed can be expressed as a function such that for all , is independently obtained as the minimum of a strictly convex function. Concerning the convergence of the algorithm we insist again on the fact that is not jointly convex with respect to , so, in Section 4 we rely on geometric arguments developed in [12] to prove that the iterated values of the algorithm converge to the minimum value . In Section 6, we show the relevance of this algorithm compared with classical Monte Carlo based regression techniques by considering an application dedicated to the control of thermostatic loads in power systems.

2 Notations and definitions

In this section we introduce the basic notions and notations used throughout this document. In what follows, will be a fixed time horizon.

-

•

All vectors are column vectors. Given , will denote its Euclidean norm.

-

•

Given a matrix , will denote its Frobenius norm.

-

•

Given , , and will denote respectively the partial derivative of with respect to (w.r.t.) , its gradient and its Hessian matrix w.r.t. .

-

•

Given any bounded function , being Banach spaces, we denote by its supremum.

-

•

will denote the closure of a bounded and convex open subset of (in particular is a convex compact subset of ). will denote its diameter.

-

•

For any topological spaces and will denote the Borel -field of () will denote the linear space of functions from to that are continuous (resp. Borel). will denote the Borel probability measures on . Given will denote the expectation with respect to (w.r.t.)

-

•

Except if differently specified, will denote the space of continuous functions from to For any we denote by the coordinate mapping on We introduce the -field . On the measurable space we introduce the canonical process .

We endow with the right-continuous filtration The filtered space will be called the canonical space (for the sake of brevity, we denote by ). -

•

Given a continuous (locally) square integrable martingale , will denote its quadratic variation.

-

•

Equality between stochastic processes are in the sense of indistinguishability.

Definition 2.1.

(Relative entropy). Let be a topological space. Let The relative entropy between the measures and is defined by

| (2.1) |

with the convention .

Remark 2.2.

The relative entropy is non negative and jointly convex, that is for all , for all , . Moreover, is lower semicontinous with respect to the weak convergence on Polish spaces. We refer to [13] Lemma 1.4.3 for a proof of these properties.

Definition 2.3.

(Minimizing sequence, solution and -solution). Let be a generic set. Let be a function. Let (which can be finite or not). A minimizing sequence for is a sequence of elements of such that . We will say that is a solution to the optimization Problem

| (2.2) |

if In this case, . For , we will say that is an -solution to the optimization Problem (2.2) if . We also say that is -optimal for the (optimization) Problem (2.2).

We remark that a -solution is a solution of the optimization Problem (2.2).

3 From the stochastic optimal control problem to a regularized optimization problem

In this section we consider a stochastic control problem that we reformulate in terms of an optimization problem on a space of probabilities. Later we propose a regularized version of that problem whose solutions are -optimal for the original problem.

3.1 The stochastic optimal control problem

We specify the assumptions and the formulation of the stochastic optimal control Problem (1.3) stated in the introduction. Let us first consider a drift and a diffusion matrix following the assumptions below.

Hypothesis 3.1.

(SDE Diffusion coefficients).

-

(i)

There exists a constant such that for all

-

(ii)

There exists such that for all

is referred in the rest of the paper as elliptic.

-

(iii)

For all ,

Let us define the admissible set of probabilities for Problem (1.3).

Definition 3.2.

Let be the set of probability measures on such that for all , under the canonical process decomposes as

| (3.1) |

with , is a local martingale such that , is a progressively measurable process with values in . If in addition there exists such that -a.e, we will denote .

Remark 3.3.

If in the sense of Definition 3.2, then the following equivalent properties hold.

-

1.

One has

(3.2) with , .

-

2.

is solution of the martingale problem (in the sense of Stroock and Varadhan in [32]) associated with the initial condition and the operator defined for all , by

(3.3) with .

-

3.

is a solution (in law) of

(3.4) for some suitable Brownian motion .

We will often make use of the following proposition.

Proposition 3.4.

Proof.

This result follows from Theorem 10.1.3 in [32]. ∎

Let then , referred to as the running cost and the terminal cost respectively, and assume that the following holds.

Hypothesis 3.5.

(Cost functions).

-

1.

The functions are positive. There exists , such that for all

-

2.

is continuous in , is convex for all and is continuous.

We conclude this section by a moment estimate, see e.g. Corollary 12 in Section 5.2 in [25], which will be often used in the rest of the paper.

Lemma 3.6.

Let be a filtered probability space. Let be an -progressively measurable process. Let be an Itô process on which decomposes as

where is a martingale such that . Let . Under Hypothesis 3.1 there exists a constant which depends only on , (and ), such that for all ,

3.2 The regularized optimization problem

As mentioned earlier, finding a numerical approximation of the solution of a stochastic optimal control problem often relies on solving the associated Hamilton-Jacobi-Bellman (HJB) equation. This is typically done via finite difference schemes when and by Monte Carlo methods for estimating Forward BSDE (i.e. a BSDE whose underlying is a Markov diffusion) when We aim at finding another way to compute an optimal strategy that does not require the approximation of the solution of the HJB equation. To this aim we regularize Problem (1.3) by doubling the decision variables and adding a relative entropy term in the objective function. We get the regularized Problem (1.5) where is the subset of elements defined below.

Definition 3.7.

Let be the set of probability measures such that

-

(i)

,

-

(ii)

In the perspective of solving the regularized optimization Problem (1.5) we will introduce in Sections 5.1 and 5.2 two subproblems. The regularization is justified by the fact that each of these subproblems and can be treated by classical techniques of the literature and will build the two steps of our alternating minimization algorithm. The one in Section 5.2 is a minimization on , the probability being fixed and it is related to a variational representation formula whose solution is expressed as a so called exponential twist, see e.g. [13]. In particular we will make use of the following result.

Proposition 3.8.

Let be a Borel function and . Assume that is bounded below. Then

| (3.5) |

Moreover there exists a unique minimizer given by

Proof.

Applying Proposition 3.8 to our framework for we get that under Hypothesis 3.5 the subproblem admits a unique solution given by

| (3.6) |

and that the optimal value is

| (3.7) |

This subproblem is further analyzed in Section 5.2. In particular Proposition 5.3 allows to identify as the law of a semimartingale with Markovian drift. On the other hand, the subproblem in Section 5.1 is a minimization on , the probability remaining unchanged. The solution arises via a pointwise real minimization providing the function associated with the optimal probability by Proposition 5.2.

The next theorem proves that the regularized Problem (1.5) has as Markovian solution.

Theorem 3.9.

In fact by a slight abuse of notation denotes a function on and at the same time. The proof of this result relies on technical lemmas. For the convenience of the reader it is postponed to Appendix 7.3. The following proposition justifies the use of the regularized Problem (1.5) to approximatively solve the initial stochastic optimal control Problem (1.3).

Proposition 3.10.

We suppose Hypothesis 3.1 and item of Hypothesis 3.5. Let and let be the first component of an -solution of Problem (1.5) in the sense of Definition 2.3 with We set where corresponds to the appearing in decomposition (3.1). Then the following holds.

-

1.

There is a constant depending only on of Hypothesis 3.5 and the diameter of such that where denotes the variance of under .

-

2.

We have

where we recall that was defined in (1.3).

Remark 3.11.

- 1.

-

2.

By definition of infimum, for , the existence of an -solution is always guaranteed without any convex assumption on the running cost w.r.t. the control variable.

- 3.

-

Proof (of Proposition 3.10). We first prove item Let be an -solution of Problem (1.5). By Hypothesis 3.5, for all , one has

Combining this inequality with Lemma 3.6 implies the existence of a constant depending only on and the diameter of such that . We go on with the proof of item First a direct application of Lemma 7.17 with yields

Let then be the solution of given by (3.6). Then by (3.7) which implies

(3.8) Observe that . Besides, as Problem (1.3) rewrites , it holds that . Then

(3.9) Using (3.8) and (3.9) finally yields

(3.10) This concludes the proof of item ∎

From now on, will be implicit in the cost function to alleviate notations.

4 Alternating minimization algorithm

In this section we present an alternating algorithm for solving the regularized Problem (1.5). Let . We will define a sequence verifying by the alternating minimization procedure

| (4.1) |

4.1 Convergence result

The convergence of alternating minimization algorithms has been extensively studied in particular in Euclidean spaces. In general the proof of convergence results requires joint convexity and smoothness properties of the objective function, see [2]. The major difficulty in our case is that the convexity only holds w.r.t (in fact the set is not even convex). To prove the convergence we need to rely on other techniques which exploit the properties of the entropic regularization. Let us first assume that the initial probability measure is Markovian in the following sense.

Hypothesis 4.1.

For a fixed Borel function we set

| (4.2) |

Let satisfying Hypothesis 4.1. We set . We build a sequence of elements of according to the following procedure. Let .

-

•

Let

(4.3) By Proposition 5.3 there exists a measurable function such that under the canonical process decomposes as

(4.4) where is a martingale such that .

- •

Lemma 4.2 below states that the sequence defined above verifies the alternating minimization procedure (4.1).

Lemma 4.2.

The main result of this section is given below.

Theorem 4.3.

The proof of the theorem uses the so-called three and four-points properties introduced in [12]. The whole convergence proof makes use of the specific features of the sub-problems , whose study is the object of Section 5.1, and which is the object of Section 5.2.

Lemma 4.4.

(Three points property). For all ,

| (4.7) |

Proof.

We can suppose that , otherwise and the inequality holds trivially. Let

where (and ) have been defined in (4.5).

Remark 4.5.

Whenever , previous proof shows that (4.7) is indeed an equality.

Lemma 4.6.

(Four points property). For all

| (4.8) |

Proof.

Let If or , the inequality is trivial. We then assume until the end of the proof that and .

By construction (see (4.4)), there exists a measurable function such that under the canonical process has decomposition

where is a martingale under and .

We now characterize the probability measure . By Lemma 7.4 in the Appendix with and the fact that , there exists a progressively measurable process with respect to the canonical filtration such that under the canonical process has the decomposition

| (4.9) |

where is a martingale such that , and

| (4.10) |

We set

| (4.11) |

so that (4.10) can be rewritten

| (4.12) |

We now prove the four-points property (4.8). Let then be the function introduced in (4.5) replacing with . Let be given by (4.2). Since is convex in the variable, for all one has

| (4.13) | ||||

where denotes a subgradient of in . We focus on the last two terms in the previous inequality. Applying the algebraic equality with

where we have omitted the dependencies in of all the quantities at hand for conciseness, we have

On the other hand

Combining what precedes yields

From the inequality (4.13) we then get

| (4.14) | ||||

By definition (4.5) is the minimum of for all , where the application is the one defined in (4.2). We recall that is (strictly) convex in with subgradient . Consequently, for the generic probability we get that the term on third line of inequality (4.14) is non-negative by the first order optimality condition for subdifferentiable functions at . Next by the classical inequality for all , term on the second line of (4.14) gives

From inequality (4.14) we get

and integrating the previous inequality with respect to yields

| (4.15) |

By (4.9) and (4.11), under , the canonical process decomposes as

| (4.16) |

where is a martingale verifying . We recall the decomposition (3.1). As by assumption, Lemma 7.4 item applied to with states the existence of a predictable process such that

| (4.17) |

where is a local martingale (with respect to the canonical filtration). Identifying the bounded variation component between (4.17) and decomposition (4.16) under , yields and (7.16) in Lemma 7.4 item implies that

| (4.18) |

Then recalling the definition of in (1.5), by (4.18)

| (4.19) |

From (4.19) and (4.12) it holds

and by (4.15)

In particular, , hence . Then by Lemma 7.4 item applied to with and , we have

| (4.20) |

and by (4.20)

| (4.21) |

Finally applying (4.21) in the previous inequality we get

This concludes the proof. ∎

Remark 4.7.

The three points property holds even if the set is not compact, but our proof of the four points property crucially relies on the uniqueness in law of which is in particular guaranteed when is compact. Otherwise it is unclear how to adapt the proof.

We conclude the section by stating a lemma which is a reformulation in our setting of Proposition 3.9 in [5]. This allows us to estimate the drift in the algorithm via a conditional derivative.

Lemma 4.8.

Assume Hypothesis 3.1. For almost all , it holds that

| (4.22) |

4.2 Entropy penalized Monte Carlo algorithm

The previous alternating minimization procedure suggests a Monte Carlo algorithm to approximate a solution to Problem (1.3). In the following, is a regular subdivision of the time interval with step the number of particles and the number of descent steps of the algorithm. will denote the set of valued polynomials defined on of degree . Recall that for all , is the probability measure given by Proposition 3.4.

The estimation of the drift in Step 2 of the algorithm below is performed via regression. It is inspired by (4.22) in Lemma 4.8, which is a reformulation in our setting of Proposition 3.9 in [5].

The term in the argmin is a weighted Monte Carlo approximation of the expectation of under the exponential twist probability of .

An interest of the entropy penalized Monte Carlo algorithm is that in Lemma 4.8, (4.22) can be independently estimated by regression techniques at each time step , , while in dynamic programming approaches, conditional expectations are recursively computed in time, implying an error accumulation from time to . Moreover one can expect that the trajectories simulated under localize around the optimally controlled trajectories when the number of iterations of the algorithm increases to . Hence the computation effort to estimate the optimal control focuses on this specific region of the state space, whereas standard regression based Monte Carlo approaches are blindly exploring the state space with forward Monte Carlo simulations of the process.

5 Solving the subproblems

In this short section we aim at describing the two subproblems and appearing in the alternating minimization algorithm proposed in Section 4.

5.1 Pointwise minimization subproblem

Let us first describe the minimization where the probability is fixed and is such that, under , the canonical process is a fixed Itô process. In this section we assume that Hypotheses 3.1 and 3.5 are fulfilled. We introduce the following assumption for a given probability on the canonical space.

Hypothesis 5.1.

There is a Borel function for which the canonical process decomposes as

| (5.1) |

where .

For the proposition below we recall that if is a bounded measurable function then denotes the associated probability measure given by Proposition 3.4.

Proposition 5.2.

Proof.

As is continuous and strongly convex on the convex compact set , it admits a unique minimum on denoted The measurability of the application follows e.g. from Theorem 18.19 in [1].

Let then . We want to show that

| (5.3) |

Recall that, by Definition 3.2, there exists a progressively measurable process taking values in such that under the canonical process has decomposition

| (5.4) |

where is a martingale and . If then inequality (5.3) is trivially fulfilled. We consider now such that .

Then and by Lemma 7.4 item there exists a process of the form such that, under , decomposes as

| (5.5) |

and

Identifying the bounded variation and the martingale components in decompositions (5.1) and (5.5) under we get -a.e. and . Hence

Previous inequality yields

| (5.6) | ||||

Proposition 5.1 in [9] and the tower property of the conditional expectation gives the existence of such that -a.e. Fubini’s theorem and Jensen’s inequality for the conditional expectation applied to (5.6) then yields

| (5.7) | ||||

By the definition (5.2) of , it holds that

| (5.8) |

In particular

By item of Lemma 7.4 with and we have that . Hence

This concludes the proof of inequality (5.3). ∎

5.2 Exponential twist subproblem

In this section we focus on the minimization , being the reference probability. We recall that is the solution of given by Proposition 3.8.

Proposition 5.3.

Assume that, under , the canonical process decomposes as

where is a martingale such that and . Then there exists such that under the canonical process decomposes as

where is a martingale such that . Moreover, is a Markov process under and for all .

6 Application to the control of thermostatic loads in power systems

We consider in this section the problem of controlling a large, heterogeneous population of air-conditioners in order that their overall consumption tracks a given target profile on a given time horizon . This problem was introduced in [23]. Air-conditioners are aggregated in clusters indexed by depending on their characteristics. We denote by the number of air-conditioners in the cluster . Individually, the temperature in the room with air-conditioner in cluster is assumed to evolve according to the following dynamics

| (6.1) |

where : is the outdoor temperature; is a positive thermal constant; is the heat exchange constant; is the maximal power consumption of an air-conditioner in cluster . are independent Brownian motion that represent random temperature fluctuations inside the rooms, such as a window or a door opening. For each cluster, a local controller decides at each time step to turn or some conditioners in the cluster by setting or in order to satisfy a prescribed proportion of active air-conditioners. We are interested in the global planner problem which consists in computing the prescribed proportion of air conditioners ON in each cluster in order to track the given target consumption profile . For each the average temperature in the cluster follows the aggregated dynamics

| (6.2) |

with

We consider the stochastic control Problem (1.3) on the time horizon with and . The running cost is defined for any such that

| (6.3) |

where , the first term in the above cost function penalizes the deviation of the the overall consumption with respect to the target consumption , quantifies the penalization for irregular controls in cluster while penalizes the exits of the mean temperatures in the cluster from a comfort band . Finally the terminal cost is given by where is a target temperature for cluster . Clearly the cost functions and satisfy Hypothesis 3.5. To estimate an optimal policy for this problem we use Algorithm 1 with a time step for . The parameters of the problem are the same as in [23]. We perform independent runs of the algorithm, providing estimations of an optimal control on the whole period . For each estimation , we simulate iid trajectories of the process controlled by and compute the associated costs . The average cost is finally estimated by .

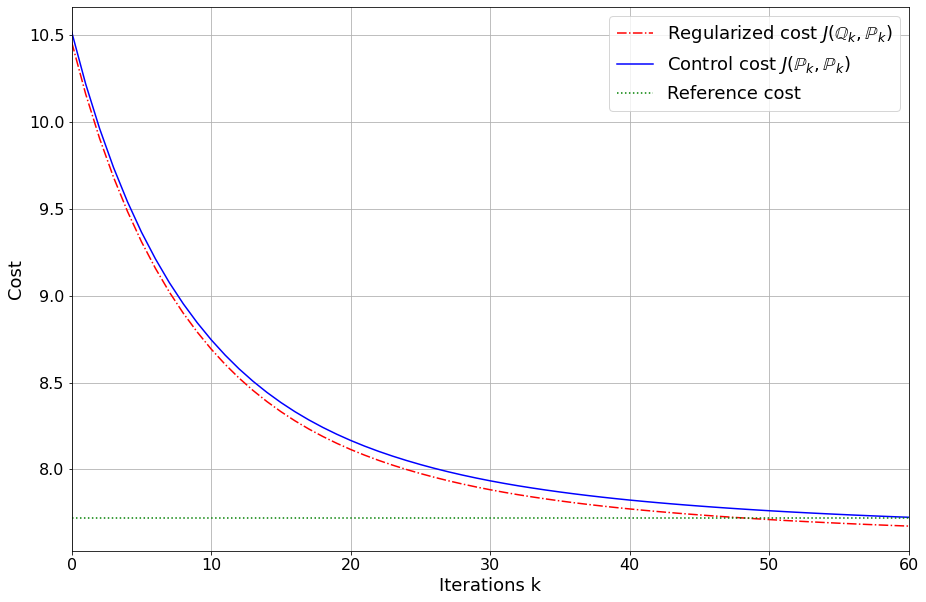

To evaluate the performances of our approach, we compare it with the classical regression-based Monte Carlo technique relying on a BSDE representation of the problem implemented in [23]. We underline that we only aim to obtain lower costs compared to the BSDE technique in [23], there are no benchmark costs. The results are reported in Table 1 for dimensions . For both methods, particles are used to estimate an optimal policy for each dimension . For the entropy penalized Monte Carlo algorithm, we use a regularization parameter and iterations for dimensions and and iterations for dimensions ; concerning the approximation in Step 1 of the Algorithm 1 we limit ourselves to the set of polynomials of degree as the problem is very localized in space. On Table 1 we can observe very good performances that seem to be weakly sensitive to the dimensions of the problem. On Figure 1, we have reported the cost and as a function of the iteration number obtained on one run of the algorithm with and . Theses costs are compared to a reference cost obtained with a run of our algorithm with particles. As expected is decreasing and converging to a limiting value. It is interesting to notice that is also decreasing and very close to . Hence, it seems that the parameter does not need to be so small to obtain a good approximation of the original control Problem (1.3).

| Method | Entropy | BSDE | Entropy | BSDE | Entropy | BSDE | Entropy | BSDE |

|---|---|---|---|---|---|---|---|---|

7 Appendices

7.1 Decomposition of a semimartingale in its own filtration

We give here a proposition discussing the decomposition of a semimartingale in its own filtration. Even though it is a natural result, we have decided to carefully write its proof, as it raises several measurability issues. Recall that given a process defined on a probability space , denotes the natural filtration of .

Proposition 7.1.

Let be a filtered probability space. Let be a progressively measurable process such that . Then there exists a measurable function such that the following properties hold.

-

(i)

The map is progressively measurable with respect to

(7.1) so that is a version of the conditional expectation.

-

(ii)

Let be a continuous -semimartingale. with decomposition

where is an -martingale. Then has the decomposition

where is an -martingale with .

Proof.

We follow closely the proof of Theorem 7.17 in [28]. As has a -measurable (adapted) version (see e.g. [22]), it follows from Chapter IV Theorem T46 in [29], see also Theorem 0.1 in [30], that has a a progressively measurable modification w.r.t that we denote precisely , which proves . Let then Let Then

where we used Fubini’s theorem for conditional expectation as well as the tower property. The process is an -martingale. Furthermore, since they are both equal to . So is also proved. ∎

7.2 Relative entropy related results

The theorem below is a Girsanov’s type theorem based on finite relative entropy assumptions. It is an adaptation of Theorem 2.1 in [27] on a general probability space instead of the canonical space.

Theorem 7.2.

Let be a filtered probability space. Let (resp. ) be a progressively measurable process with values in (resp. in the set of square non-negative defined symmetric matrices ). Let be a continuous process which decomposes as

| (7.2) |

where is a continuous -local martingale such that . Let be a probability measure on . Assume that .

Then there exists an -valued progressively measurable process such that

| (7.3) |

and such that, under , the process is still a continuous semimartingale with decomposition

| (7.4) |

where is a continuous -local martingale and . Furthermore,

| (7.5) |

Proof.

The existence of the process is given by Theorem 2.1 in [27], noticing that the proof of this result relies on a variational formulation of the relative entropy, which does not depend on the probability space, see Proposition 3.1 in [27]. For the proof of (7.5) we closely follows the proof of Theorem 2.3 in [27].

-

1.

Assume first that . Let (with the convention that the is if is empty). Setting and the Doléans exponential , we define . By Novikov’s criterion, is a martingale, therefore is a probability measure on equivalent to since is strictly positive and . It follows that

By definition of the process is a genuine martingale under . Hence

Letting increasingly as , a direct application of the monotone convergence theorem then yields

(7.6) -

2.

We consider now the general case. Since we know that and set . Then and by convexity of the relative entropy, see Remark 2.2, . By item , and the first part of the statement, using (7.6) with instead of , there exists a progressively measurable process such that

(7.7) Using the crucial estimate (33) in [27], whose proof once again can be carried out on any probability space, one has

which implies that

Letting in (7.7) yields the desired result.

∎

For the following lemma we keep the notations and assumptions of Theorem 7.2. Let in particular be a process fulfilling (7.2) with . Then by Theorem 7.2 there is a progressively measurable process such that (7.4) holds. For that we have the following estimates.

Lemma 7.3.

We suppose the existence of such that

-

1.

If , there exists a constant which depends only on and such that

-

2.

Suppose moreover . Then it holds that

and can be chosen such that

(7.8)

Proof.

- 1.

-

2.

Just before the statement of the present lemma we have mentioned the decomposition (7.4) holds, where the martingale verifies .

As , again Theorem 7.2, interchanging and , yields the existence of a progressively measurable process such that under the process decomposes as

where is a martingale and

Identifying the bounded variation and the martingale components of under , we get that and -a.e. In particular,

(7.13) Then, as in the proof of item , Hölder’s inequality, (7.9) with replaced by , and (7.13) yield

where, for the last inequality we have used (7.12) . This finally also implies the result (7.8).

∎

The results of Theorem 7.2 can be specified if one considers probability measures on the canonical space . In the following, are progressively measurable functions w.r.t. their corresponding Borel -fields. Let us reformulate Theorem 7.2 in our setting.

Lemma 7.4.

Let such that, under the canonical process can be decomposed as

| (7.14) |

where is a martingale with , where verifies item of Hypothesis 3.1. Let .

-

1.

Assume that Then we have the following.

-

(a)

There exists a progressively measurable process , with respect with natural filtration of (in particular of the form ) such that, under , decomposes as

(7.15) where is a martingale with and

(7.16) - (b)

-

(a)

-

2.

Assume that under the canonical process writes

(7.17) where is a martingale with and that uniqueness in law holds for (7.14).

If

then and

(7.18)

7.3 Proof of Theorem 3.9

To simplify the formalism of the proof we will assume that , as well as . Recall that in what follows, the filtration is the canonical filtration on the canonical space , see the notations in Section 2. Following Section 3.2 in [33] we will make use of an enlarged probability space as well as an analogous form of the set on this enlarged space, denoted . This is stated in the definitions below.

Definition 7.6.

Let and we denote its canonical process and the associated canonical filtration. We also denotes the natural filtration generated by the first component of the canonical process.

Definition 7.7.

Let be the subset of such that if the following holds.

-

(i)

-

(ii)

Under , decomposes as

(7.19) such that is an -local martingale, with .

-

(iii)

The processes is absolutely continuous w.r.t. the Lebesgue measure -a.s. and

(7.20) -

(iv)

-a.e.

Remark 7.8.

-

1.

The property in Definition 7.7 implies in particular that . Hence any property which is verified almost surely w.r.t. in the above definition also holds -a.s.

-

2.

Clearly we have

where we recall that previous is defined for all and all .

For we introduce the functional defined by

| (7.21) |

The proof of Theorem 3.9 requires several lemmas. We first need to establish a correspondence between the functional defined on and the functional defined on .

Let . By Definitions 3.7 and 3.2, under the canonical process decomposes as

where is an -martingale such that and is a progressively measurable process with respect to the canonical filtration with values in . We rely on this decomposition in the following lemma for the association of the functional to .

Lemma 7.9.

Let introduced above. Let (resp. ) be the law of under (resp. ). Then , is absolutely continuous with respect to with where is the projection on the first component of the space , and .

Proof.

Letting (resp. ) be the law of induced by (resp. ) on we get

Furthermore, recalling that is the first coordinate projection on , one has and this yields

It follows that ∎

We establish a partial converse of the connection between and in Lemma 7.10 below, whose proof crucially relies on the convexity of the functions and Jensen’s inequality.

Lemma 7.10.

Let . Assume that . There exists such that and .

Proof.

The proof of this result consists in two steps. In the first step we provide a lower bound of the cost in term of an expectation under the marginal law of the first component of the vector . In the second step, we introduce a probability such that where is the law of a diffusion process mimicking the marginals of at each fixed time . We keep in mind the characterization of given by (7.19) and (7.20). In particular, under decomposes as

-

1.

Consequently, since see item of Definition 7.7, by Theorem 7.2, on the space equipped with the probabilities and with , there exists a progressively measurable process w.r.t. on such that under the process writes as

(7.22) where is (again under ) an -local martingale with and

(7.23) Moreover, under the process has some integrability properties. Indeed, by Lemma 3.6 we have that for all , In particular, by linear growth of it holds that

(7.24) for all . Then we can apply Lemma 7.3 item which implies that for any

(7.25) Let us now decompose the semimartingale under in its own filtration. To this aim, we denote by the process . In particular, as is -essentially bounded, we get from (7.25) that . Then by Proposition 7.1 item , there exist progressively measurable functions with respect to , such that

(7.26) Consequently, under , by (7.22), the process is also an -semimartingale with decomposition

(7.27) where is an -martingale and By Fubini’s theorem and Jensen’s inequality for the conditional expectation

(7.28) where is the first marginal of , i.e. the law of the first component of the vector under . Moreover, the entropy inequality (7.23) rewrites

(7.29) and again Fubini’s theorem and Jensen’s inequality for the conditional expectation gives

(7.30) -

2.

Next by Fubini’s theorem and Jensen’s inequality for the conditional expectation and taking into account (7.26), it holds that

(7.31) First, observe that as , (7.24) is also true replacing by . Hence from (7.31) and (7.24) with we deduce that , and by Corollary 3.7 in [9] there exist a measurable function and a probability measure on such that the following holds.

-

•

For all , -a.e.

-

•

Under the canonical process can be expressed as where is a -local martingale with .

-

•

Finally Proposition 5.1 in [9] provides a measurable function such that

(7.32) We modify on the Borel set so that for all . Then once again by Fubini’s theorem and Jensen’s inequality for the conditional expectation, we get that

(7.33) and also

(7.34) As is bounded and , chosen here for simplicity equal to zero, has also linear growth, Theorem 10.1.3 in [32] proves existence and uniqueness of a solution to the martingale problem with initial condition , and the operator defined in (3.3) so, by Remark 3.3

where is a local martingale vanishing at zero such that By Lemma 7.4 item 2., the right-hand side of (7.34) is equal to . Combining alltogether the expressions (7.28), (7.30), (7.33) and (7.34) we get . This concludes the proof.

-

•

∎

We emphasize that, even though the condition in Lemma 7.10 is very restrictive, we will see at the end of this section that it will be enough to prove Theorem 3.9. The connection between and is thus established. To prove the theorem we also need tightness results on our enlarged space. This is stated in the following lemma and proposition.

Lemma 7.11.

Let be a sequence of elements of . Then is tight.

Proof.

In this proof, denotes a generic non-negative constant. By definition, under , the canonical process has decomposition

where takes values in , is a martingale and . Let . For we have

| (BDG inequality) | ||||

| (Hypothesis 3.1) | ||||

| (Hölder inequality) | ||||

so is a tight sequence by Kolmogorov criteria, see e.g. Problem 4.11 of [24].

∎

We will need in the following a simple technical observation.

Lemma 7.12.

Let be a sequence of Borel probability measures on a Polish space that weakly converges towards a probability measure Let be a continuous function. Assume that there exists such that

| (7.35) |

Then

Proof.

By Skorokhod’s representation theorem, there exists a probability space , a sequence of random variable on and a random variable such that and -a.s. Condition (7.35) implies that the sequence is uniformly integrable. Furthermore, by continuity of , -a.s. Thus

or equivalently

∎

Remark 7.13.

Let be a sequence of couples of probability measures on a measurable space, where both the sequences and are tight. Then there is a couple of probability measures and a subsequence such that (resp. ) converges weakly to (resp. ). Such a couple will be called limit point of the sequence .

Proposition 7.14.

Let be a sequence of elements of such that and . Let be the corresponding sequence of probability measures on given by Lemma 7.9. Then the following properties hold.

-

1.

The sequences and are tight and under any corresponding limit point of , the process has absolutely continuous paths.

-

2.

Any limit point of belongs to .

Proof.

-

1.

Let . By Definitions 3.7 and 3.2 there is a progressively measurable process with values in such that

(7.36) for some local martingale . As is bounded, we have

(7.37) We set . As (7.37) holds, Lemma 2 in [40] yields tightness of the laws and under any limit point , the second component of the canonical process on , has absolutely continuous path w.r.t. the Lebesgue measure. Moreover by Lemma 7.11 the sequence is tight. It follows from what precedes that each marginal of under is tight, hence tightness of the laws of previous vector on the product space , and under any limit point the paths of are absolutely continuous. Finally Lemma 7.9 states that , where denotes the projection on the first component of the space . This implies that , and tightness of the sequence then follows from the tightness of .

-

2.

Let be any limit point of the sequence , see Remark 7.13. One can assume that both sequences and converges weakly towards and respectively. We are going to prove that . By item item of Definition 7.7 of holds. Let us verify item of the same definition. Indeed by Lemma 7.9 we have . We recall that is lower semicontinous with respect to the weak convergence on Polish spaces, see Remark 2.2, being the Polish space. Consequently

Let us now check item . Let . Let belonging to the space of smooth functions with compact support on . By (3.1), under we have where is an absolutely continuous process. By Itô’s formula applied to (3.1) under , the process

is a martingale under . We want to prove that is a martingale under .

Let be a bounded continuous function. Then

(7.38) On the one hand, the function

is bounded and continuous. Hence

(7.39) On the other hand, there exists a constant which only depends on such that for all ,

Combining the previous inequality with Lemma 3.6 we get that for some ,

(7.40) Hence it holds

and by Lemma 7.12 with , taking into account Hypothesis 3.1 , we get

(7.41) Combining (7.39) and (7.41) and letting in (7.38) yields

Hence the process is an -martingale for all .

By standard usual stochastic calculus arguments, this implies that under the process writes

where is a -local martingale with

hence item . Finally, it remains to prove . Let , large enough. As is convex and closed, one has for all . Moreover, as is closed, the set is closed under the uniform convergence. By Portmanteau Theorem, see Theorem 2.1 in [6], . Hence -a.s., . As is continuous, -a.s., for all and , . being closed, letting yields

and we conclude that -a.e.

∎

To apply Proposition 7.14 we will need the lemma below.

Lemma 7.15.

There exists a minimizing sequence for such that the following holds.

-

(i)

and .

-

(ii)

for all .

Proof.

Let be a minimizing sequence for . Let

| (7.42) |

Then from Proposition 3.8 applied to , we get that thus is also a minimizing sequence for It follows from Hypothesis 3.5 that

| (7.43) |

Hypothesis 3.5 and Lemma 3.6 imply the existence of independent of such that

| (7.44) |

By Jensen’s inequality, we get for all

Consequently

hence

| (7.45) |

and

This establishes item .

We are finally ready to prove Theorem 3.9.

-

Proof (of Theorem 3.9). Let be a minimizing sequence as provided by Lemma 7.15. Let be the corresponding sequence of probability measures induced by on given by Lemma 7.9. By Proposition 7.14 the sequences and are tight. Let then be a limit point of ), see Remark 7.13. By Proposition 7.14 , . By Hypothesis 3.5 and Lemma 7.15 (ii) for any given we have

(7.46) Since converges weakly to , by Lemma 7.12, for all we have

By (7.46), Fubini’s and dominated convergence theorems

We recall now that the relative entropy is lower semicontinuous with respect to the two variables for the topology of weak convergence on Polish spaces, see Remark 2.2. Hence, keeping in mind (7.21)

(7.47) Since is a minimizing sequence,

(7.48) where for the third equality we have used Lemma 7.9. We set , where corresponds to the one in item in Definition 7.7 and we define the probability measure such that

(7.49) By Proposition 3.8 with we obtain . As , the nominator of the Radon-Nykodim density of (7.49) is smaller or equal to and the denominator is strictly positive number so that . Hence by Lemma 7.10 there exists such that and . Finally combining what precedes with (7.48) yields and this implies that is a solution to Problem (1.5). ∎

7.4 Strong and weak controls

We give here some details on the equivalence between a strong formulation of our stochastic optimal control (1.1) and our optimization problem (1.3). We assume in this section that the coefficients of the diffusion and are Lipschitz continuous which ensures in particular well-posedness for the SDEs for each strong control. Given some filtered probability space endowed with a Brownian motion , let be the set of -progressively measurable processes on taking values in . By Theorem 3.1 in [37], there exists a unique process on such that

An application of Proposition 7.1 yields the existence of an -progressively measurable function such that -a.e. and, under it has decomposition

where . Setting it is then clear that . Hence

Assume now that the previous inequality is strict. Then there exists a probability measure such that . Then again, by Corollary 3.7 in [9] there exist a measurable function and a probability measure on such that the following holds.

-

•

For all , .

-

•

Under the canonical process decomposes as

where is an -local martingale such that .

-

•

.

We modify on the Borel set so that for all . On the one hand, Fubini’s theorem and Jensen’s inequality for conditional expectation yields

On the other hand, Theorem 1.1 in [39] ensures the existence of a unique (strong) solution (on the space to the SDE . In particular the process , and we have

hence a contradiction and we conclude that .

7.5 Miscellaneous

We gather in this section two useful technical results. In the following, all the random variables are defined on a filtered probability space .

Lemma 7.17.

Let be a squared-integrable, non negative random variable. Then for all ,

Proof.

For all , it holds by Taylor’s formula with integral remainder that

Let . A direct application of this formula with , yields

Taking the expectation in the previous inequality we get

and as for all we have

Notice that is a constant, hence . We then have

where the first inequality follows from Jensen’s inequality. ∎

Lemma 7.18.

Let be an -adapted process of the form

where for some and where is a martingale. For Lebesgue almost all

Proof.

In this proof we extend the process by continuity after and by zero for . Let . Notice first that

and that for all , for almost all , by Lebesgue differentiation theorem,

| (7.50) |

To conclude by a uniform integrability argument w.r.t. we need to prove that

Previous expectation, by Hölder inequality, is bounded above by

where interchanging the integral inside the expectation is justified by Fubini’s theorem. The family is uniformly integrable with respect to and we conclude using the Lebesgue’s dominated convergence theorem. ∎

Remark 7.19.

If is a.e. -measurable then the statement of Lemma 7.18 still holds replacing the -field with . This is an obvious property of the tower property of the conditional expectation.

Acknowledgments

The research of the first named author is supported by a doctoral fellowship PRPhD 2021 of the Région Île-de-France. The research of the second and third named authors was partially supported by the ANR-22-CE40-0015-01 project (SDAIM).

References

- [1] C. D. Aliprantis and K. C. Border. Infinite dimensional analysis. A hitchhiker’s guide. Berlin: Springer, 3rd ed. edition, 2006.

- [2] A. Auslender. Optimisation. Méthodes numériques. Mai̧trise de mathematiques et applications fondamentales. Paris etc.: Masson. 178 p. F 115.00 (1976)., 1976.

- [3] J.-D. Benamou and Y. Brenier. A computational fluid mechanics solution to the Monge-Kantorovich mass transfer problem. Numer. Math., 84(3):375–393, 2000.

- [4] C. Bender and T. Moseler. Importance sampling for backward SDEs. Stochastic Anal. Appl., 28(2):226–253, 2010.

- [5] J. Bierkens and H. J. Kappen. Explicit solution of relative entropy weighted control. Syst. Control Lett., 72:36–43, 2014.

- [6] P. Billingsley. Convergence of probability measures. John Wiley & Sons, 1968.

- [7] J. F. Bonnans, J. Ch. Gilbert, C. Lemaréchal, and C. A. Sagastizábal. Numerical optimization. Theoretical and practical aspects. Transl. from the French. Universitext. Berlin: Springer, 2nd revised. edition, 2006.

- [8] T. Bourdais, N. Oudjane, and F. Russo. A martingale problem approach to path-integral control. In preparation.

- [9] G. Brunick and S. Shreve. Mimicking an Itô process by a solution of a stochastic differential equation. The Annals of Applied Probability, 23(4):1584–1628, 2013.

- [10] N. Cammardella, A. Bušić, and S. Meyn. Simultaneous allocation and control of distributed energy resources via Kullback-Leibler-Quadratic optimal control. In 2020 American Control Conference (ACC), pages 514–520. IEEE, 2020.

- [11] P. Carpentier, J.-P. Chancelier, M. De Lara, and F. Pacaud. Mixed spatial and temporal decompositions for large-scale multistage stochastic optimization problems. J. Optim. Theory Appl., 186(3):985–1005, 2020.

- [12] I. Csiszár and G. Tusnády. Information geometry and alternating minimization procedures. Recent results in estimation theory and related topics, Suppl. Issues Stat. Decis. 1, 205-237, 1984.

- [13] P. Dupuis and R. S. Ellis. A weak convergence approach to the theory of large deviations. Wiley Ser. Probab. Stat. Chichester: John Wiley & Sons, 1997.

- [14] I. Ekeland and R. Témam. Convex analysis and variational problems., volume 28 of Classics Appl. Math. Philadelphia, PA: Society for Industrial and Applied Mathematics, unabridged, corrected republication of the 1976 English original edition, 1999.

- [15] N. El Karoui, D. Nguyen, and M. Jeanblanc-Picqué. Compactification methods in the control of degenerate diffusions: Existence of an optimal control. Stochastics, 20:169–219, 1987.

- [16] W. H. Fleming. Logarithmic transformations and stochastic control. Advances in filtering and optimal stochastic control, Proc. IFIP-WG 7/1 Work. Conf., Cocoyoc/Mex. 1982, Lect. Notes Contr. Inf. Sci. 42, 131-141 (1982)., 1982.

- [17] W. H. Fleming and S. K. Mitter. Optimal control and nonlinear filtering for nondegenerate diffusion processes. Stochastics, 8:63–77, 1982.

- [18] M. Germain, H. Pham, and X. Warin. Approximation error analysis of some deep backward schemes for nonlinear PDEs. SIAM J. Sci. Comput., 44(1):a28–a56, 2022.

- [19] E. Gobet and C. Labart. Solving BSDE with adaptive control variate. SIAM J. Numer. Anal., 48(1):257–277, 2010.

- [20] E. Gobet and P. Turkedjiev. Adaptive importance sampling in least-squares Monte Carlo algorithms for backward stochastic differential equations. Stochastic Processes Appl., 127(4):1171–1203, 2017.

- [21] C. Huré, H. Pham, and X. Warin. Deep backward schemes for high-dimensional nonlinear PDEs. Math. Comput., 89(324):1547–1579, 2020.

- [22] A. Irle. On the measurability of conditional expectations. Pacific Journal of Mathematics, 70(1):177–178, 1977.

- [23] L. Izydorczyk, N. Oudjane, and F. Russo. A fully backward representation of semilinear PDEs applied to the control of thermostatic loads in power systems. Monte Carlo Methods and Applications, 27(4):347–371, 2021.

- [24] I. Karatzas and S. E. Shreve. Brownian motion and stochastic calculus, volume 113 of Graduate Texts in Mathematics. Springer-Verlag, New York, second edition, 1991.

- [25] N. V. Krylov. Controlled diffusion processes, volume 14 of Stochastic Modelling and Applied Probability. Springer-Verlag, Berlin, 2009. Translated from the 1977 Russian original by A. B. Aries, Reprint of the 1980 edition.

- [26] D. Lacker. Hierarchies, entropy, and quantitative propagation of chaos for mean field diffusions. ArXiv preprint 2105.02983, 2021.

- [27] C. Léonard. Girsanov theory under a finite entropy condition. In Séminaire de Probabilités XLIV, pages 429–465. Springer, 2012.

- [28] R.S. Lipster and A.N Shiryaev. Statistics of Random Processes. I. General Theory. Application of Mathematics : Stochastic Modelling and Applied Probability. Springer-Verlag, second edition, 2001.

- [29] P. A. Meyer. Probability and potentials. Waltham, Mass.-Toronto-London: Blaisdell Publishing Company, a Division of Ginn and Company, xiii, 266 p. (1966)., 1966.

- [30] M. Ondreját and J. Seidler. On existence of progressively measurable modifications. Electronic Communications in Probability, 18:1–6, 2013.

- [31] A. Seguret, C. Alasseur, J. F. Bonnans, A. De Paola, N. Oudjane, and V. Trovato. Decomposition of high dimensional aggregative stochastic control problems. ArXiv preprint: 2008.09827, 2020.

- [32] D. W. Stroock and S. R. S. Varadhan. Multidimensional diffusion processes. Classics in Mathematics. Springer-Verlag, Berlin, 2006. Reprint of the 1997 edition.

- [33] X. Tan and N. Touzi. Optimal transportation under controlled stochastic dynamics. The Annals of Probability, 41(5):3201 – 3240, 2013.

- [34] E. Theodorou, J. Buchli, and S. Schaal. Reinforcement learning of motor skills in high dimensions: A path integral approach. In 2010 IEEE International Conference on Robotics and Automation, pages 2397–2403, 2010.

- [35] M. Thieullen and T. Mikami. Duality theorem for the stochastic optimal control problem. Stochastic Processes and their Applications, 116 n.12:1815–1835, 2006.

- [36] S. Thijssen and H.J. Kappen. Path integral control and state-dependent feedback. Physical Review E, 91(3):032104, 2015.

- [37] N. Touzi. Optimal stochastic control, stochastic target problems, and backward SDE, volume 29 of Fields Institute Monographs. Springer, New York; Fields Institute for Research in Mathematical Sciences, Toronto, ON, 2013. With Chapter 13 by Agnès Tourin.

- [38] J. Yong and X. Y. Zhou. Stochastic controls. Hamiltonian systems and HJB equations, volume 43 of Appl. Math. (N. Y.). New York, NY: Springer, 1999.

- [39] X. Zhang. Strong solutions of SDEs with singular drift and Sobolev diffusion coefficients. Stochastic Processes and their Applications, 115(11):1805–1818, 2005.

- [40] W. Zheng. Tightness results for laws of diffusion processes application to stochastic mechanics. Annales de l’I.H.P. Probabilités et statistiques, 21(2):103–124, 1985.