Generative AI for End-to-End Limit Order Book Modelling

Abstract.

Developing a generative model of realistic order flow in financial markets is a challenging open problem, with numerous applications for market participants. Addressing this, we propose the first end-to-end autoregressive generative model that generates tokenized limit order book (LOB) messages. These messages are interpreted by a Jax-LOB simulator, which updates the LOB state. To handle long sequences efficiently, the model employs simplified structured state-space layers to process sequences of order book states and tokenized messages. Using LOBSTER data of NASDAQ equity LOBs, we develop a custom tokenizer for message data, converting groups of successive digits to tokens, similar to tokenization in large language models. Out-of-sample results show promising performance in approximating the data distribution, as evidenced by low model perplexity. Furthermore, the mid-price returns calculated from the generated order flow exhibit a significant correlation with the data, indicating impressive conditional forecast performance. Due to the granularity of generated data, and the accuracy of the model, it offers new application areas for future work beyond forecasting, e.g. acting as a world model in high-frequency financial reinforcement learning applications. Overall, our results invite the use and extension of the model in the direction of autoregressive large financial models for the generation of high-frequency financial data and we commit to open-sourcing our code to facilitate future research.

1. Introduction

Ever since OpenAI opened access to ChatGPT, generative large language models (LLMs) have skyrocketed in popularity. Part of their appeal is due to their impressive few-shot learning and in-context learning abilities (Brown et al., 2020). Besides LLMs, generative diffusion models have had a similar rise in popularity for image generation (Croitoru et al., 2023). Financial applications similarly benefit from generative models for various applications, from data augmentation (Naritomi and Adachi, 2020; Liu et al., 2022), over anomaly detection (Henry-Labordere, 2019; Geiger et al., 2020), to forecasting (Zhou et al., 2018). Most current financial machine learning approaches employ training paradigms based on generative adversarial networks (GANs) (Goodfellow et al., 2014; Eckerli and Osterrieder, 2021), which usually generate series of price returns directly. Just a few years ago, Takahashi et al. (2019) stated that “Building auto-regressive models of financial time-series meets insurmountable difficulties.” Only very recently has there been work on bottom-up generators of limit order book (LOB) market micro-structure data (Hultin et al., 2023a). Our paper proposes to take the next step towards more powerful autoregressive financial micro-structure generative models, which do not suffer from problems commonly encountered with GANs, such as mode collapse (Bau et al., 2019; Zhang et al., 2018). Autoregressive models enable generating sequences of variable length and allow for improved interpretability, as the model learns conditional distributions of the next sequence token by design. The trained model, in conjunction with a replay simulator (Frey et al., 2023), which processes generated messages, is used to generate a realistic order flow. Such a conditional simulation model constitutes an interactive world model, which, in principle, can be used in downstream tasks, such as trading, order execution, or market making, potentially using a reinforcement learning algorithm (Coletta et al., 2023). We leave these applications to future work.

We propose the use of a deep state space model composed of simplified structured state space layers for sequence modeling (S5) (Smith et al., 2022), which are computationally efficient and excel at learning long-range dependencies. Recognizing the similarity between sequences of order book messages and natural language, our model learns the conditional data distribution of tokenized message sequences in a cross-entropy minimization task, accurately predicting the next token in the sequence. A token in a natural language task corresponds to a part of a word or a sequence of successive digits, whereas here it is the latter. The autoregressive setup has numerous virtues, compared to GANs, such as model scalability – as evidenced by LLMs – but also wins in model interpretability, as the model defines a distribution over all message sequences of arbitrary length. Challenges include modeling extremely long sequences (¿10,000 tokens), as we need to represent sequences of sequences, since each message is itself a sequence of tokens; and long-range data referentiality.

To our knowledge, this is the first paper to propose an autoregressive end-to-end generative model for micro-structure messages. Furthermore, we develop a tokenizer, converting LOB messages to a finite vocabulary of tokens. Model performance is quantified by calculating perplexity scores and by evaluating conditional distributions of generated data in an inference loop (see section 6) with a custom error correction mechanism (see section 5.2). We utilize the Jax framework (Bradbury et al., 2018) for hardware acceleration of both the model and simulator, accelerating training and model inference.

2. Related Literature

The generation of synthetic financial data and LOBs is an active topic of research, with a variety of approaches employed, including deep learning methods (Assefa et al., 2020; Sezer et al., 2020). Traditional methods focus on computational statistical methods to generate probabilities of LOB events but are often limited, as they make strong assumptions (Cont et al., 2010) and are not accurate enough to be used in many practical applications. Another approach is agent-based modeling (ABM). In ABMs, simulations are used to understand how the interaction of autonomous agents leads to aggregate statistics and emergent behavior in a system (Korczak and Hemes, 2017; Byrd et al., 2020). Recently, generative neural networks have been used as black-box models of the dynamics of LOBs (Coletta et al., 2021, 2022; Hultin et al., 2023a). Recent work has focused on the use of LSTMs (Rumelhart and McClelland, 1987; Hultin et al., 2023a) and generative adversarial networks (GANs) (Goodfellow et al., 2014), such as Coletta et al. (2021, 2022). Many variations of GANs have been developed, including autoregressive implicit quantile networks (Ostrovski et al., 2018), ExGAN (Bhatia et al., 2021), TimeGAN (Yoon et al., 2019) and CGAN (Mirza and Osindero, 2014), making GANs more easily applicable to financial data.

Examples of GAN’s applications to probabilistic forecasting of financial time series include Tail-GAN (Cont et al., 2022) and FinGAN (Vuletić et al., 2023). Both use custom economics-driven loss functions, making them better suited for financial applications. Vuletić et al. (2023) adapt FOR-GAN (Koochali et al., 2019), a combination of CGANs and RNNs used in probabilistic forecasting. Cont et al. (2022) simulate multivariate prices with the goal of producing accurate tail risk statistics for a set of benchmark strategies. To do this, they combine GANs with Principal Component Analysis (PCA), allowing the architecture to scale effectively to a large number of assets. Their loss function is a bi-level optimization equivalent to a max-min game, where the discriminator’s goal is to predict Value-at-Risk and Expected Shortfall.

An attempt at generating LOB messages directly on a granular level is Hultin et al. (2023b). They model the LOB as a continuous-time Markov chain with volumes across price levels defining the state, extending the model of Cont et al. (2010). For each state transition, every feature (event type, order size, and price) is modeled separately, using a dedicated RNN per feature. The joint probability is then obtained from the product of the individual conditional probabilities. Instead of tokenizing messages, large numerical values – such as order sizes or timestamps – are binned, leading to a loss of precision. In contrast, our approach models the full level-3 representation, referencing individual orders, rather than the level-2 aggregation.

3. Background

3.1. Limit Order Books (LOBs)

The LOB contains a set of all unmatched limit orders submitted to an exchange and a mechanism by which incoming orders are matched (Gould et al., 2013). In a price-time priority book, limit orders are ordered, first by their price, and second by their arrival time. For buy orders (bids), the orders with the highest price are prioritized, and for sell orders (asks) the lowest prices are. When an incoming order “crosses the spread”, i.e. accepts a lower (higher) price than the best bid (ask), the incoming order is matched with the existing orders according to price-time priority. Upon matching two orders, a trade occurs, and the ownership of the underlying security is transferred. The evolution of the state of the LOB can be wholly reconstructed given an initial book state and the total set of arriving order messages in a time interval. LOB messages types are described in Section 4.

3.2. State-Space Models

Recently, transformers (Vaswani et al., 2017) have been the most successful and widely used approach to long-range sequence modeling (Rombach et al., 2022; Jumper et al., 2021; Chowdhery et al., 2022), despite their quadratic complexity in sequence length . The S4 architecture (Gu et al., 2021) (and subsequent variants S4D (Gu et al., 2022) and S5 (Smith et al., 2022)) achieve state-of-the-art performance in the Long Range Arena task (Tay et al., 2020), which is designed to measure long-range reasoning abilities, while maintaining linear complexity in at inference time. The S4 architecture employs the state-space model (SSM), commonly used in control theory. The SSM is defined as:

| (1) | ||||

The state vector denotes the current state of the system and the input vector, which is the set of variables affecting . Combined with deep learning and the HiPPO framework (Gu et al., 2020), matrices , , and can be learned through standard gradient descent to achieve high performance. While the SSM equations are defined in continuous-time, they can be easily discretized using either the bilinear method (Tustin, 1947), or zero-order hold (ZOH), using a fixed time step. S4’s features allow it to be extremely computationally efficient: it is easily parallelizable during training by “unrolling” it as a convolution using fast Fourier transform (FFT), and has complexity per step at inference time (where is the hidden dimension). The S5 model further improves on its predecessor by employing a parallel scan operation to compute the hidden state each step and using matrix multiplication instead of applying a convolutional kernel. This is facilitated by S5’s use of one multi-input, multi-output SSM instead of the many single-input, single-output SSMs in S4, and the approximate diagonalization of the HiPPO matrix. This allows the model to maintain linear complexity over sequence length while also being able to model time sequences with varying sampling time steps (Smith et al., 2022).

3.3. Autoregressive Models

An autoregressive generative model, for example an LLM, defines a (conditional) probability distribution over entire sequences of tokens. Model quality can thereby be measured by evaluating the probability the model assigns to the test data. One such statistic that is often applied in NLP is perplexity (PPL) (Chen et al., 1998). PPL measures the expected per-token surprisal by the data. It is the exponential of the per-token cross-entropy loss:

| (2) | ||||

where denotes the conditional probability of token under the model. Perplexity for individual sequences is calculated as the exponential of the mean loss over autoregressive one-step-ahead predictions of all tokens of that sequence. This is because log probabilities of sequences are conditionally separable:

4. Data

We use the LOBSTER data of LOBs of NASDAQ cash equities (Huang and Polak, 2011). In particular, we train and evaluate our model separately on data from Alphabet (GOOG) and Intel (INTC). For each stock, we use 102 days of training data (1 July 2022 to 11 November 2022), and 12 days of validation (28 November to 13 December 2022) and test data (14 December to 30 December 2022). These two stocks represent examples of small-tick (GOOG) and large-tick LOBs, which exhibit different dynamics (Eisler et al., 2012). Large-tick stocks, those where the tick size of $0.01 is large relative to the stock price, tend to have less sparse LOBs and a more constant spread over time. We only use data during regular NASDAQ trading times, on working days between 09:30 and 16:00 US East Coast time. We utilize level-3 messages pertaining to the best price levels recorded at any given moment in time. In contrast to level-2 data, where only aggregate open volumes are recorded per price level, level-3 messages allow for a full-fidelity reconstruction of LOB dynamics within certain constraints. For each new message, the data set also contains a snapshot of prices and volumes at the best price levels, for both buy orders (bids) and sell orders (asks). We use levels of LOB data, which is a common threshold for full LOB investigations (Cont et al., 2021).

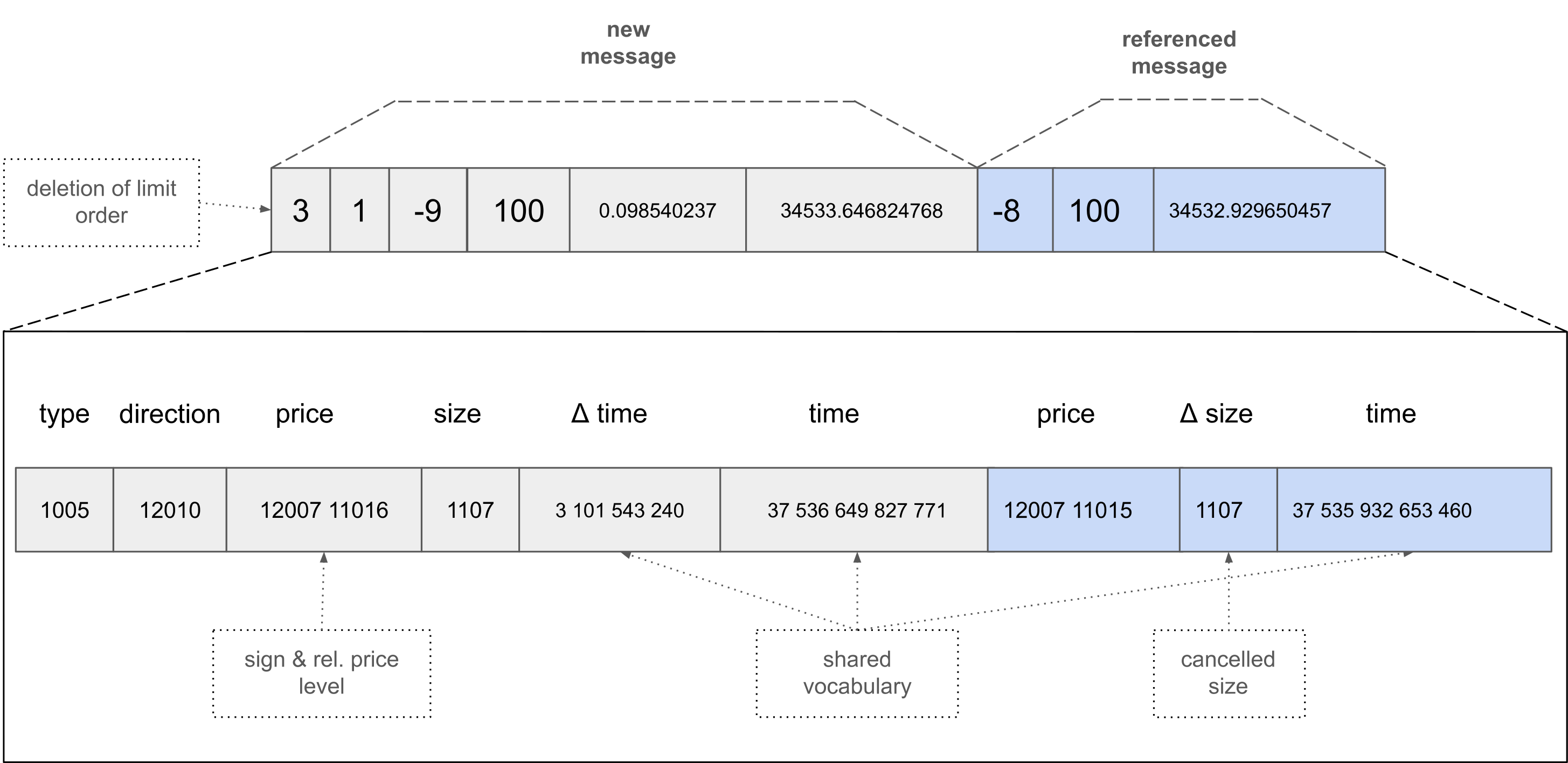

LOBSTER data contains 7 message types: new limit orders, partial order cancellations, full order deletions, visible order executions, hidden order executions, auction trades, and trading halts. However, we only use the first 4 types, ignoring hidden orders, which do not affect the visible dynamics of the LOB, and trading halts. Auction trades only occur outside regular daily trading times, and are therefore not contained in our data. Each message has 6 constituting elements: a timestamp in nanoseconds after midnight, the event type (1-4), the order ID, the order size, the price, and the trading direction (buy or sell). An example order is shown in Figure 1.

4.1. Pre-processing

The data is pre-processed to make it better suited for a deep learning task, such as generative modeling. However, our choice of data representation is general enough for other machine learning tasks. Our proposed model architecture uses both order flow information, in the form of messages, and sequences of level-2 order book states. While some models use LOB data in a price-volume representation, e.g. DeepLOB (Zhang et al., 2019), transforming the data into a more stationary representation can considerably improve performance (Kolm et al., 2021). We propose and use a sparse representation of liquidity in the book as separate volume features around the mid-price, coupled with one feature representing mid-price changes from the previous observation. This results in a dimensional vector at each point in time, which is sparse when the LOB’s price levels are sparsely populated. This representation fixes a dollar-range volume image, which also preserves price levels in the price range without any volume. Empty levels can carry important information, such as the size of the bid-ask spread, or the shape of book volume at deeper levels, which are usually squashed in other data representations. Furthermore, our representation is especially useful for a generative model, since the model can place orders at a new price level without changing the absolute price a specific book feature refers to. Since we do not generate order book states directly, but message sequences, there is no need to tokenize the book data. Instead, these can be input directly into the model as continuous features.

Before messages are encoded as token sequences, we convert them to a more stationary data representation and a finite token vocabulary. After filtering the data to the relevant order types, prices are converted from dollar values to ticks (cents) from the previous mid-price. In case the mid-price lies between valid ticks, it is rounded down to the next tick. Modified prices can thus be represented as integers and become more stationary over time. We then truncate modified prices below -999 and above 999 ticks around the mid-price to enable encoding the data with a finite and fixed vocabulary. Similarly, extremely rare individual large orders are truncated to an order size of 9999. In practice, these thresholds affect less than 0.1% of the data.

Besides new limit orders, all other message types are referential, as they subtract liquidity from an existing open order in the book. This might be obvious for partial order cancellations or full deletions, but it is modeled analogously for order executions. Execution messages must therefore refer to the order ID of the highest priority bid or ask order in the book. A challenge arises in encoding this referentiality in the message data, since numeric order IDs are a poor choice, due to their arbitrary nature and non-stationarity. As an alternative, we append information about the referenced original message as additional features to all messages. These fields are the original modified price, size, and timestamp, which we use to identify the referenced limit order.111In the rare case of exactly identical orders, recorded at the same nanosecond, we choose the last order in the list. Since arrival times are monotonically increasing, and thus a difficult distribution to generate from, we also add inter-arrival times between messages as additional features. Finally, we reorder the message features so that longer fields, corresponding to higher-entropy token distributions, occur later in the message and can thus condition on previous fields in our target task of left-to-right “causal” prediction. The order of features is: event type, direction, price, size, inter-arrival time , arrival time; followed by the reference fields: price, size, and time of the original message. In the case of a new limit order, the reference fields receive an NA value.

4.2. Encoding

Analogously to a generative language model, we propose a token-based encoding scheme for LOB messages. This allows the model to be trained using cross-entropy loss on flattened token sequences so that it learns the conditional distribution over a target token. Figure 1 illustrates the encoding mechanism of a pre-processed order deletion message. Here, each field of the pre-processed message corresponds to a sequence of tokens in the encoded message. The message vocabulary contains 12011 distinct tokens, which are represented as integer values. Event type, direction, and size fields are each encoded with a single token, while prices are split into two, the first corresponding to the sign (above or below the mid-price) and the second to the tick distance from the mid-price. A difference to language encoders is that we use non-overlapping token ranges for some fields. For example, even though event type and price level might have the same raw numerical value, they are encoded using different tokens to make effective use of our a priori knowledge of their semantic difference. Due to their similarity, arrival times and inter-arrival times () share the same vocabulary and are tokenized in groups of 3 digits. A timestamp with nanosecond precision (15 digits) thus corresponds to a 5-token sequence and the 9 fields of the pre-processed message are converted to 22 tokens. While we conduct all data pre-processing for our entire data set before model training and inference, message encoding and decoding are done dynamically when loading the data. Dynamically decoding messages is required for generated messages to be submitted to the simulator during model inference. This is done computationally efficiently by relying on just-in-time (JIT) compilation on hardware accelerators (such as GPUs) using the Jax framework (Bradbury et al., 2018).

5. Model

5.1. Model Architecture

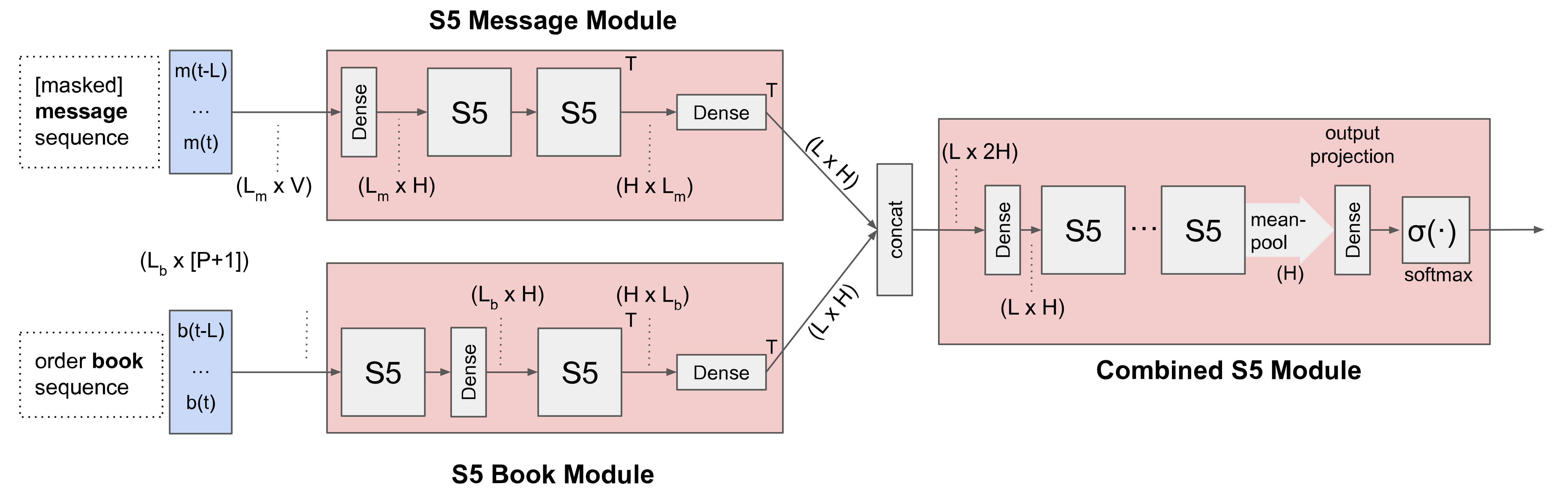

The model architecture uses a deep network of simplified structured state-space layers (S5) (Smith et al., 2022) (see section 3.2). Model inputs are flattened sequences of tokenized LOB messages and of volume images of the level-2 LOB states , where is the token vocabulary and the space of transformed book snapshots containing P volumes and the previous mid-price change . This way, message at sequence location acts upon order book state and transitions it to . So, for each book state, the model receives the corresponding successor message.

Similarly to masked language modeling (Kenton and Toutanova, 2019), during training, we mask a random token in the last message, using a token, and replace all tokens to the right of this with tokens, so the model does not condition on those fields. Time tokens of new messages are not predicted but instead calculated from generated inter-arrival times . Therefore, these are not selected to be masked during training. Time tokens do however remain part of input sequences and time tokens of referenced messages are prediction targets as these are essential in identifying original messages. These are easier targets, as they are already part of the message sequence when the referenced limit order had been submitted, which is often contained in the input sequence.

We define the model , parametrised by , as mapping a message sequence and a book sequence to a vector of logits where is the size of the token vocabulary. By requiring that the model defines a distribution over , which learns the distribution of the masked token, conditional on the input sequences. To achieve this, the model parameters are trained by minimizing cross-entropy loss

| (3) | ||||

over tuples of training data using gradient descent with the Adam (Kingma and Ba, 2014) optimizer. The scalar denotes the target token from the data. In practice, tokens are one-hot encoded, so that the model learns an input embedding.

The model architecture is shown in Figure 2. The network has two separate input branches, one receiving the masked message sequences, and the other the book state sequences. Both are processed separately for a few layers, combining S5 with dense layers, before projecting both sequences to a common sequence length . The concatenated sequences are then further processed by a stacked block of S5 layers, before projecting the output to output neurons. The message branch starts with a linear embedding layer, projecting each one-hot token vector to the model’s hidden dimension , followed by S5 layers. The book branch, on the other hand, first passes each -dimensional observation through an S5 layer before also projecting it to the embedding dimension .

We trained the model on input sequences of messages and LOB states, corresponding to encoded sequence lengths of 11,000 tokens for the messages (22 tokens per message), and 500 observations for the book states as these are not tokenized. To vary the exact input sequences and token location, in every training epoch, a random number of observations – between 0 and – are skipped from the start of each day.

5.2. Inference: Combining Model and Simulator

We learned that training and validation loss drastically improves when using book data in addition to message sequences. To reconstruct the state of the LOB solely from order flow, extremely long message sequences need to be combined non-linearly, which is why both have been found to contain orthogonal information in prediction tasks (Zhang et al., 2021). While it is easy to combine both data sources during training, we require a mechanism to generate new book states during multi-step autoregressive inference.

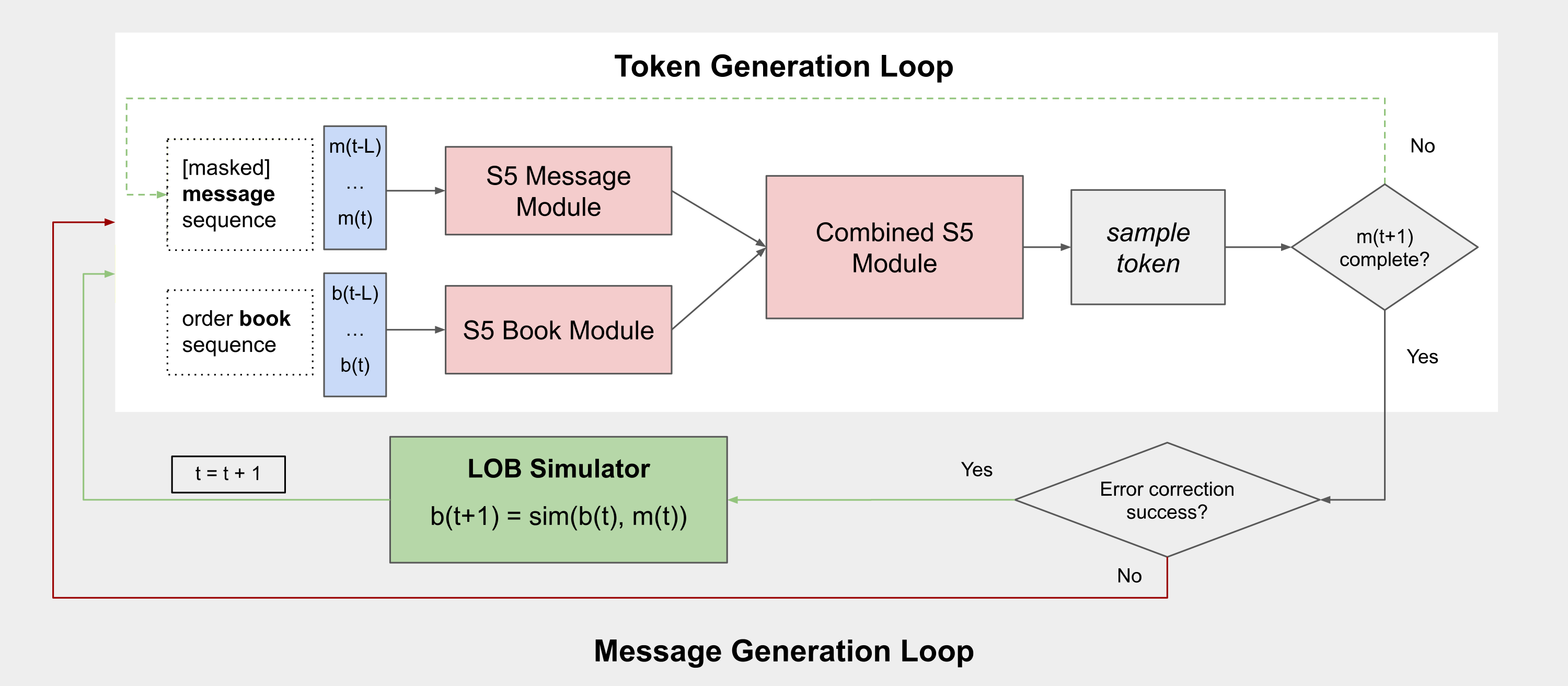

Our solution is a LOB simulator, which takes the most recent LOB state and applies the generated message according to LOB matching rules. To ensure proper processing by the simulator, the generated message is initially decoded and subsequently passed through an error correction mechanism. The simulator is therefore an essential component of the inference pipeline. We utilize the novel LOB simulator, introduced in Frey et al. (2023), implemented in Jax (Bradbury et al., 2018), and end-to-end just-in-time (JIT) compiled for GPU.

The inference pipeline is illustrated in Figure 3. It starts with the model receiving a tokenized message sequence, where the first token of the last message is set to , and the remainder to . Tokens are then sampled autoregressively left-to-right using the softmax over output logits. Once all tokens constituting have been sampled, the message’s arrival time is calculated by adding to the previous message’s time stamp. The new arrival time is then tokenized and inserted into the message sequence. During sampling, we restrict the distribution to syntactically valid tokens for the currently masked field but otherwise sample proportionately to the predicted token scores without truncation or beam-search.

After initializing the simulator with a LOB state, the message sequence is then replayed to advance the state to the current time step. This is necessary as the book states are represented as a level-2 image, which means that we only have the aggregate volume of each individual order at a price level. This initial volume is represented by the simulator as a single order. By replaying the message sequence, we can thereby recreate a partial level-3 representation, which is required to replay referential orders.

The role of the error correction procedure is to correct the occasionally hallucinated message reference components, which do not exist in the data and the simulator. As new limit orders do not require a reference component, this is only done for cancellations, deletions, and order executions. Past limit orders in the sequence, which are still in the LOB, are first searched for an order direction, price, size, and time matching the generated reference. If this matching should fail, the search is repeated excluding the time field as this field exhibits the highest error rates. Should there still be no satisfactory match, which would happen if a message references order flow before the start of the input sequence, cancellations are applied to the initial volume, if the simulator has any left at the correct price level. As executions of multiple order blocks at the same time are modeled as separate events, correct order executions are easier to guarantee. There is only a single referenced candidate order on each side of the book, namely the limit order at the best price with the earliest arrival time.

6. Results

The primary objective of a generative model is to produce data that closely approximates the target distribution. We propose to evaluate model performance in three distinct ways.

-

(1)

We compare various unconditional marginal distributions produced by the model with the corresponding data distributions.

-

(2)

Next, to evaluate the model’s capacity to match conditional distributions, correlations between generated mid-price returns and realized returns are calculated. Results indicate that the model’s significant forecasting horizon is competitive with deep learning models, trained explicitly to forecast mid-prices (Zhang et al., 2019).

-

(3)

Finally, as a succinct measure of model performance across the entire distribution, we calculate perplexity scores, which are common in the evaluation of large language models (LLMs) (Chen et al., 1998).

For evaluation purposes, we sample 1000 random test sequences, each comprising 600 messages and corresponding LOB states, which temporally follow the training and validation period. From each sequence, we extract the first observations between time steps and as the model input. The model generates the succeeding 100 messages from time steps to . We then compare the generated data against the actual 100 realized messages from the data.

The mid-price at time is the mean of the best bid and the best ask price , at the most recent time when there are orders on both sides of the book:

| (4) | ||||

The mid-price returns messages into the future between time and is then defined as

| (5) |

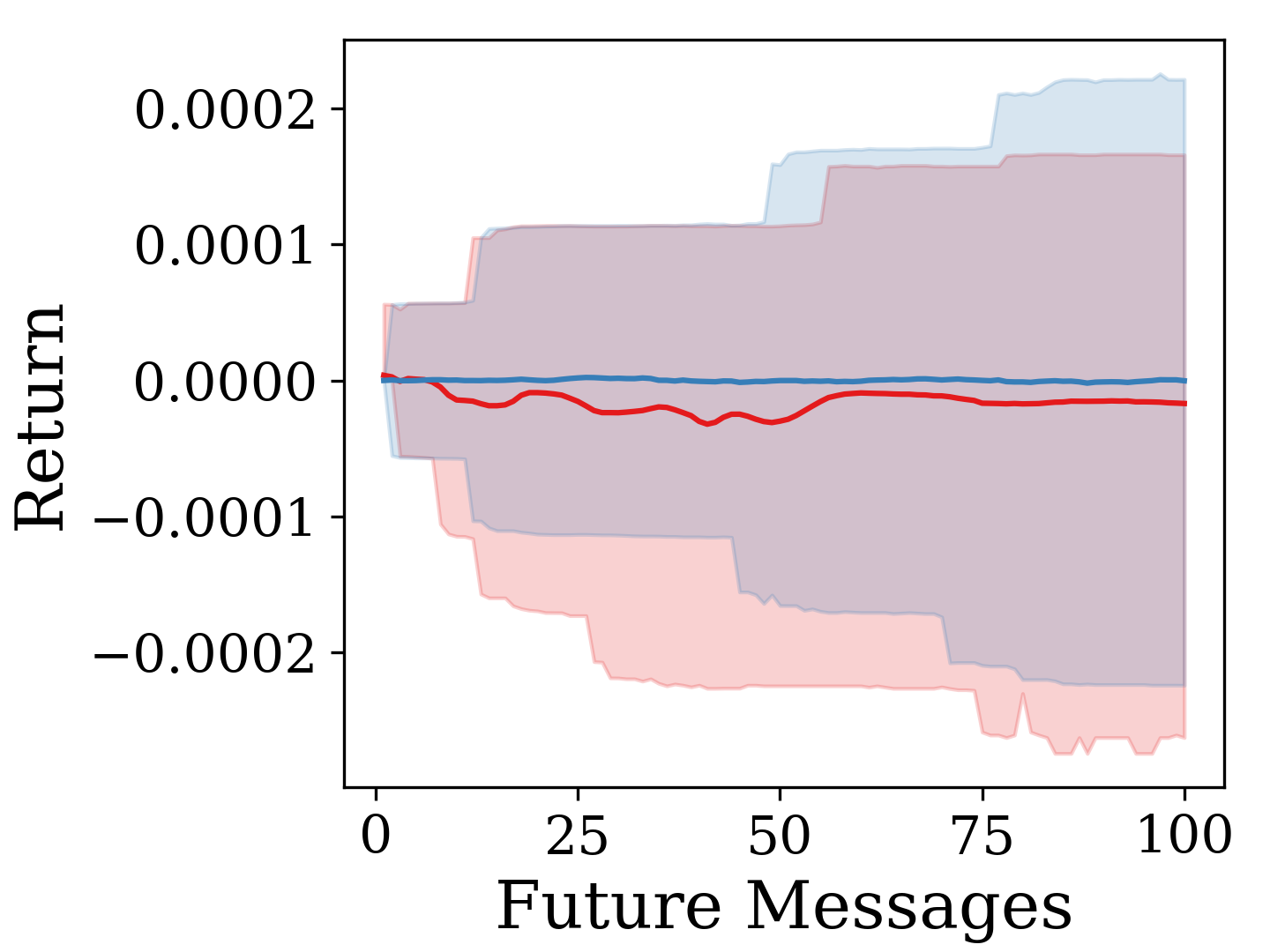

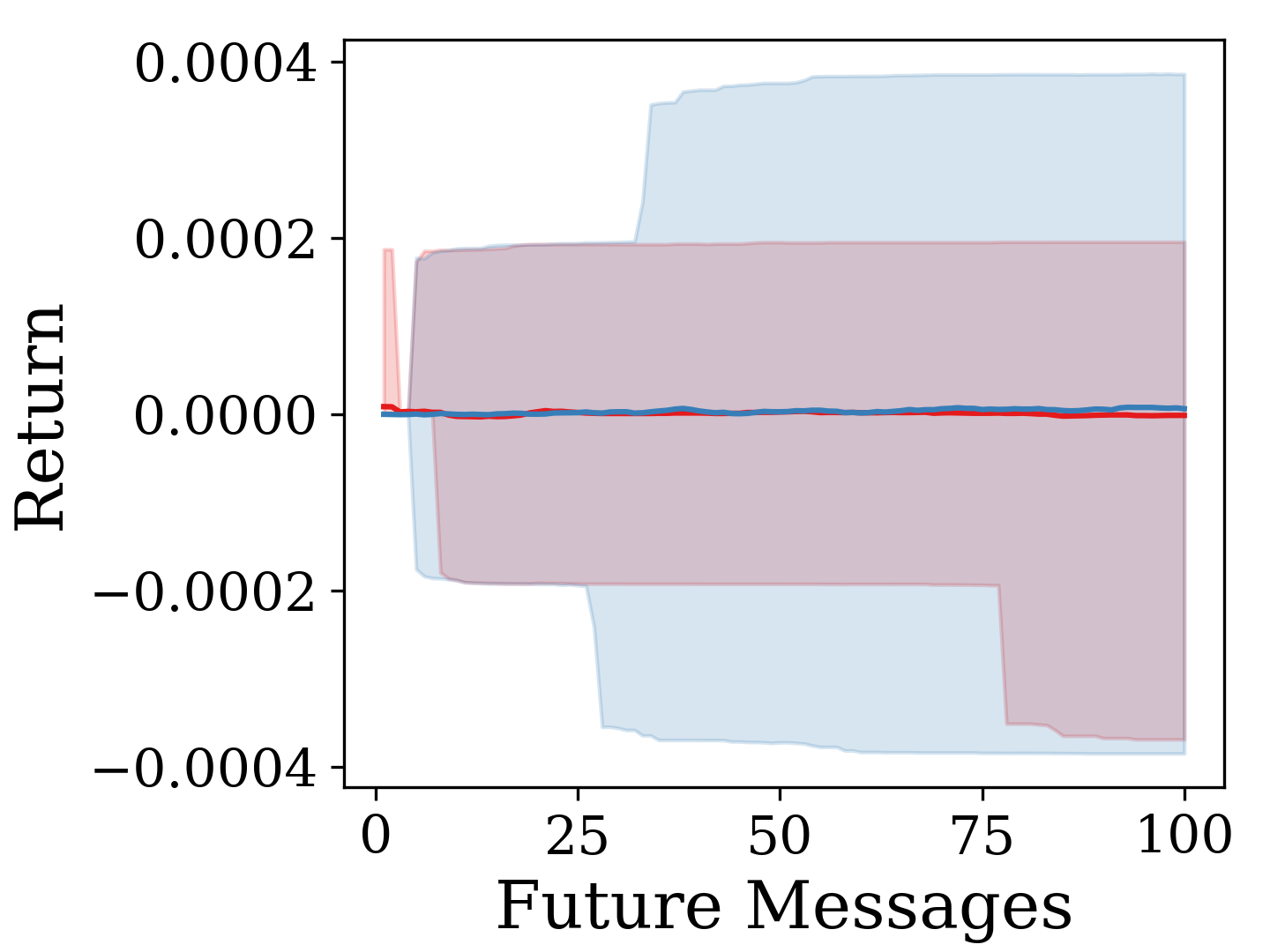

Figure 4 compares the generated and realized return distributions for 100 future messages. This shows that the model reproduces mid-price return distributions without this being an explicit part of the training loss. The mean returns do not exhibit any obvious drift or trend, and the shaded intervals, covering 95% of the distribution, overlap approximately.

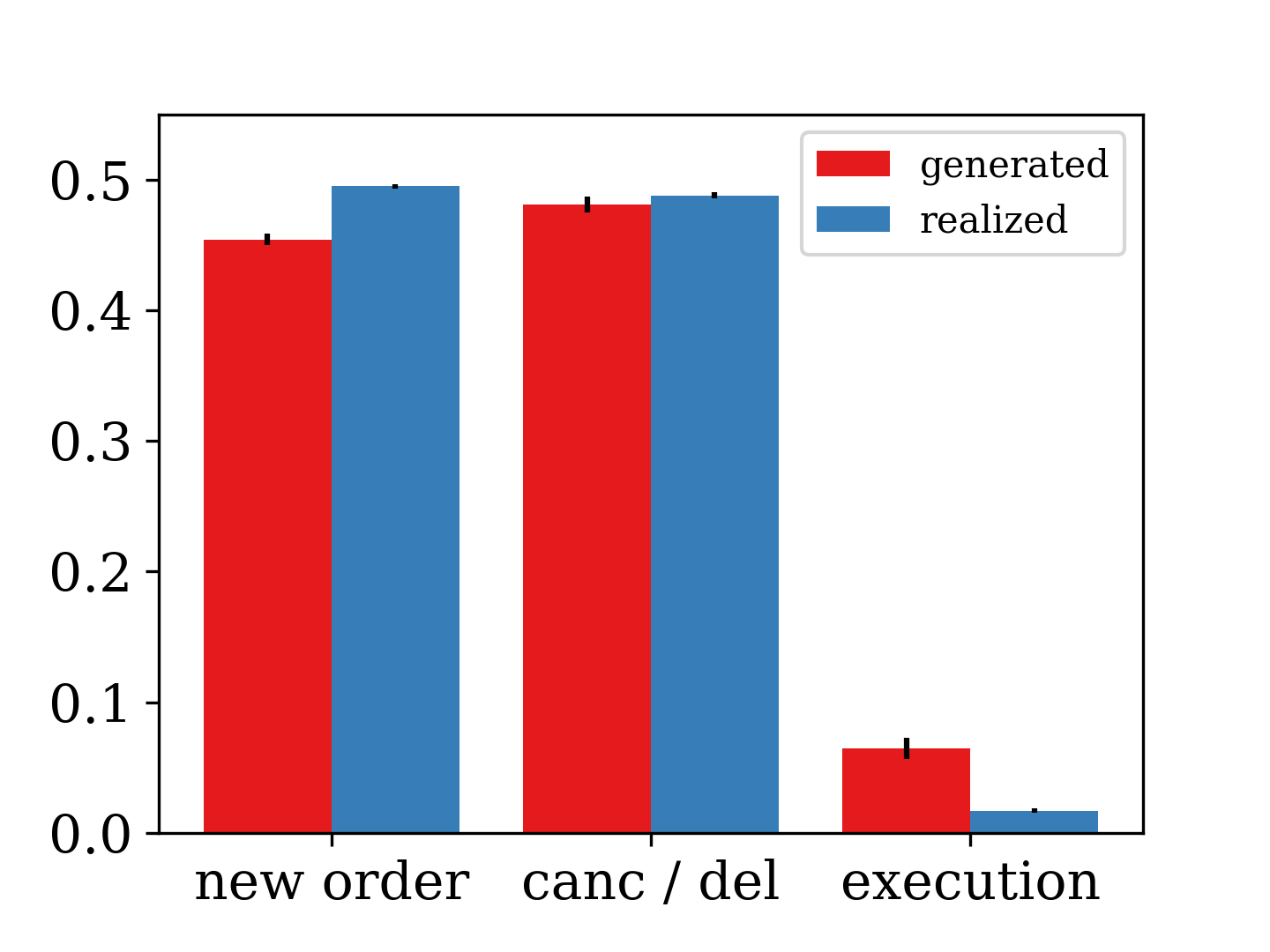

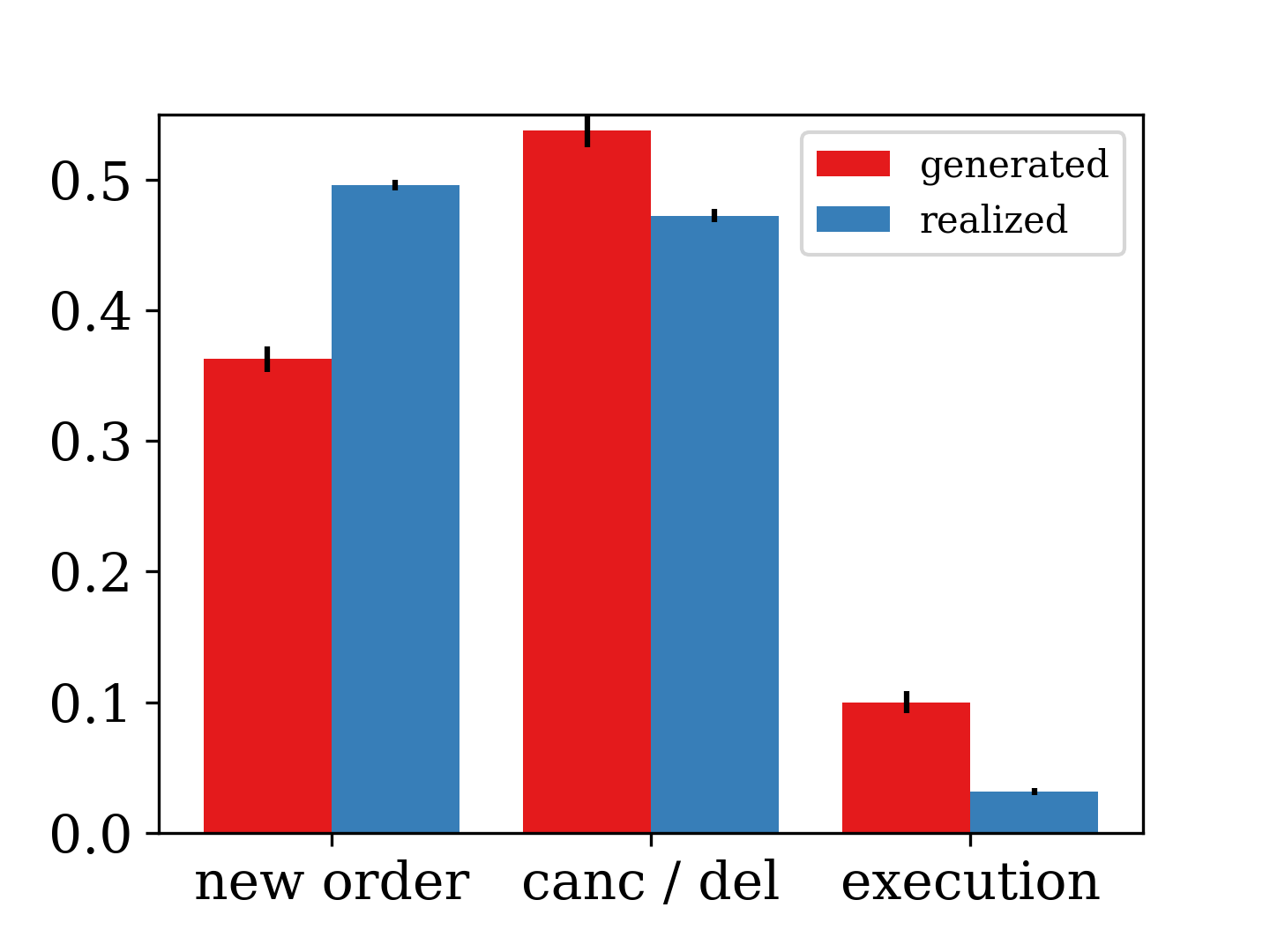

Another desirable distribution to match is the relative frequency of message types (see Figure 5). Partial cancellations and full deletions are aggregated as the simulator only tracks individual orders if they are contained in the input sequence. As the removal of liquidity from limit orders submitted before the start of the sequence affects the aggregate initialization volume, a partial cancellation cannot be differentiated from a full deletion. While both models approximately match event frequencies, execution events are over-represented in the generated data. Similar effects can be observed for rare events in LLMs, and are potentially due to the mode-covering property of cross-entropy loss (Bishop and Nasrabadi, 2006; Li and Farnia, 2023).

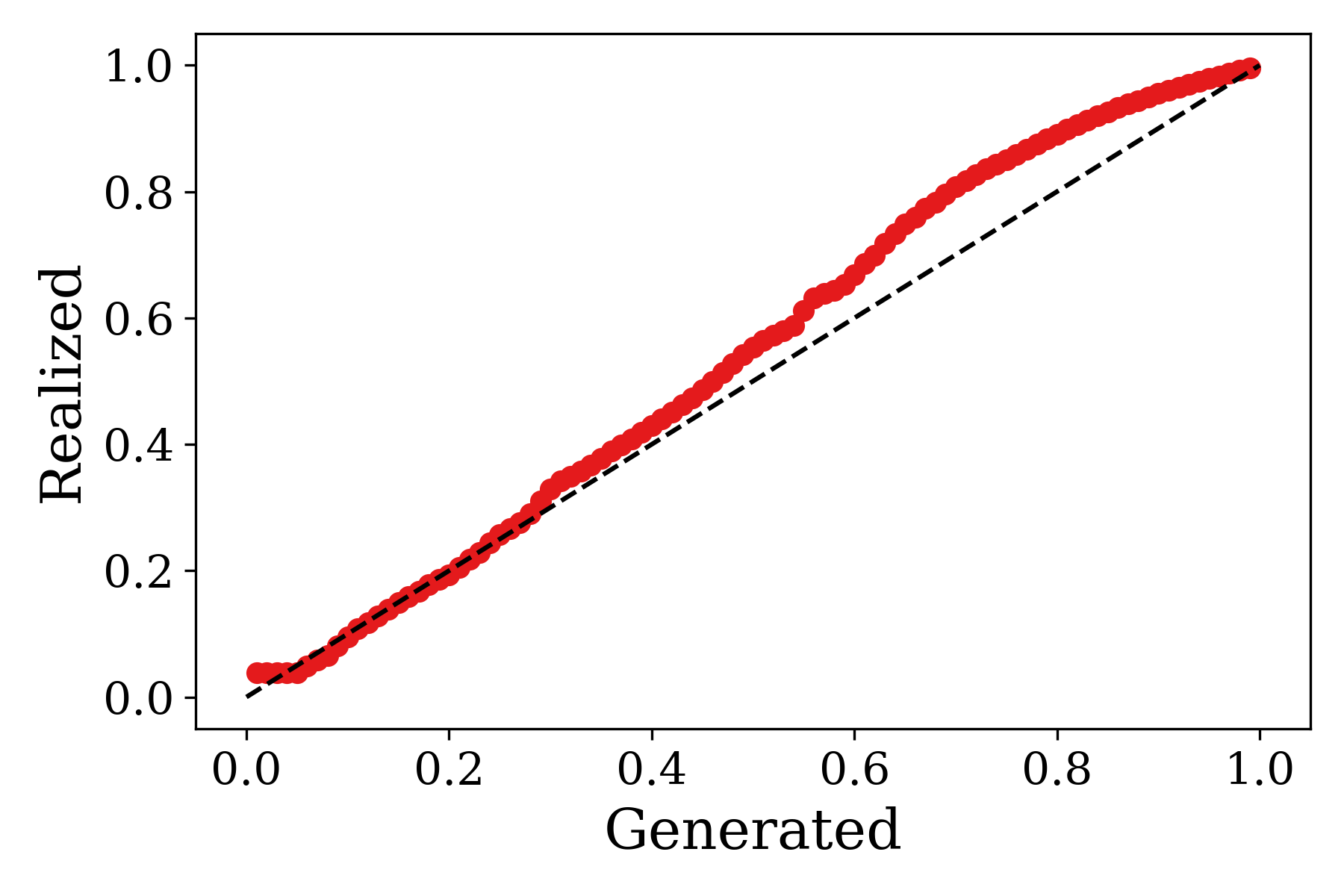

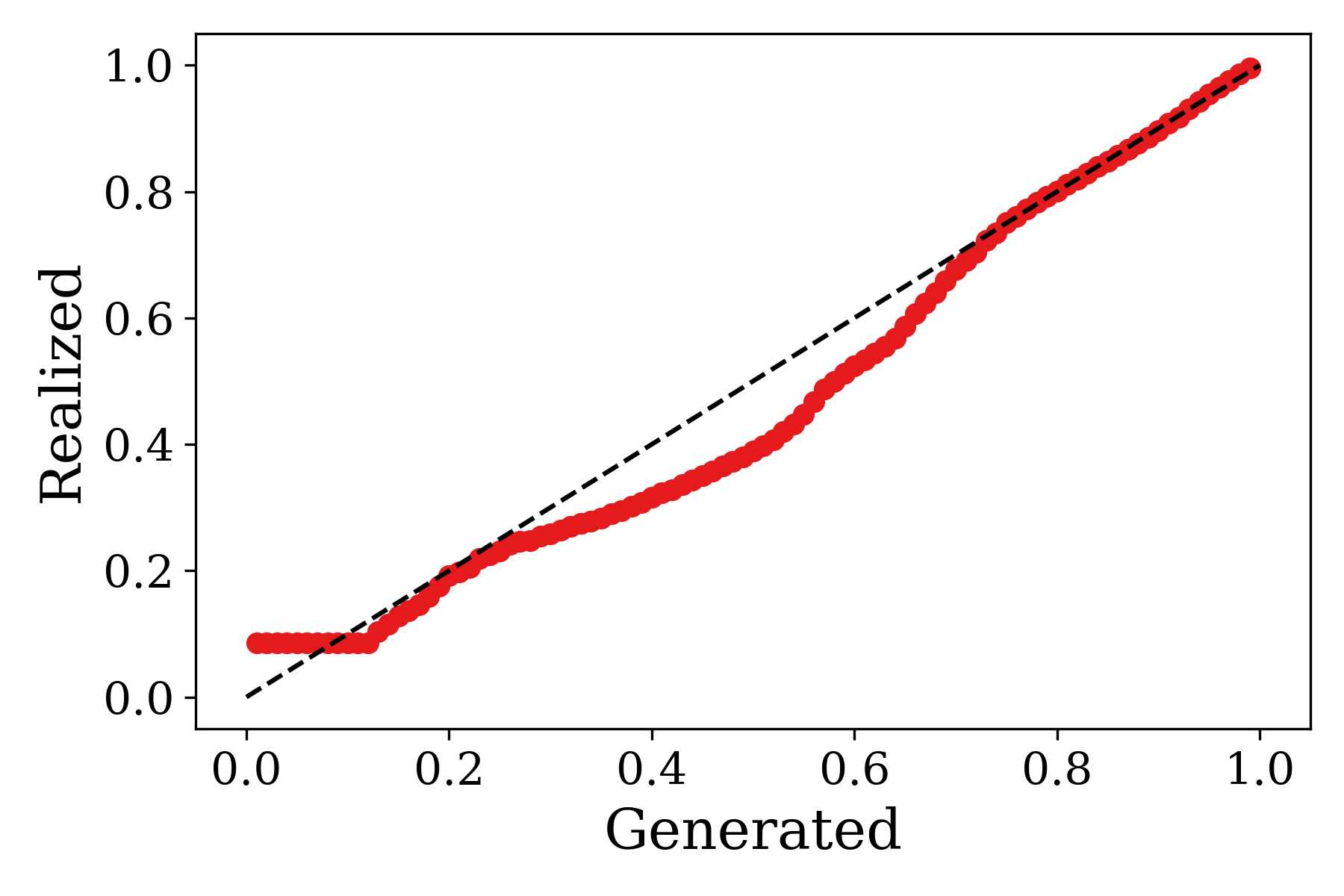

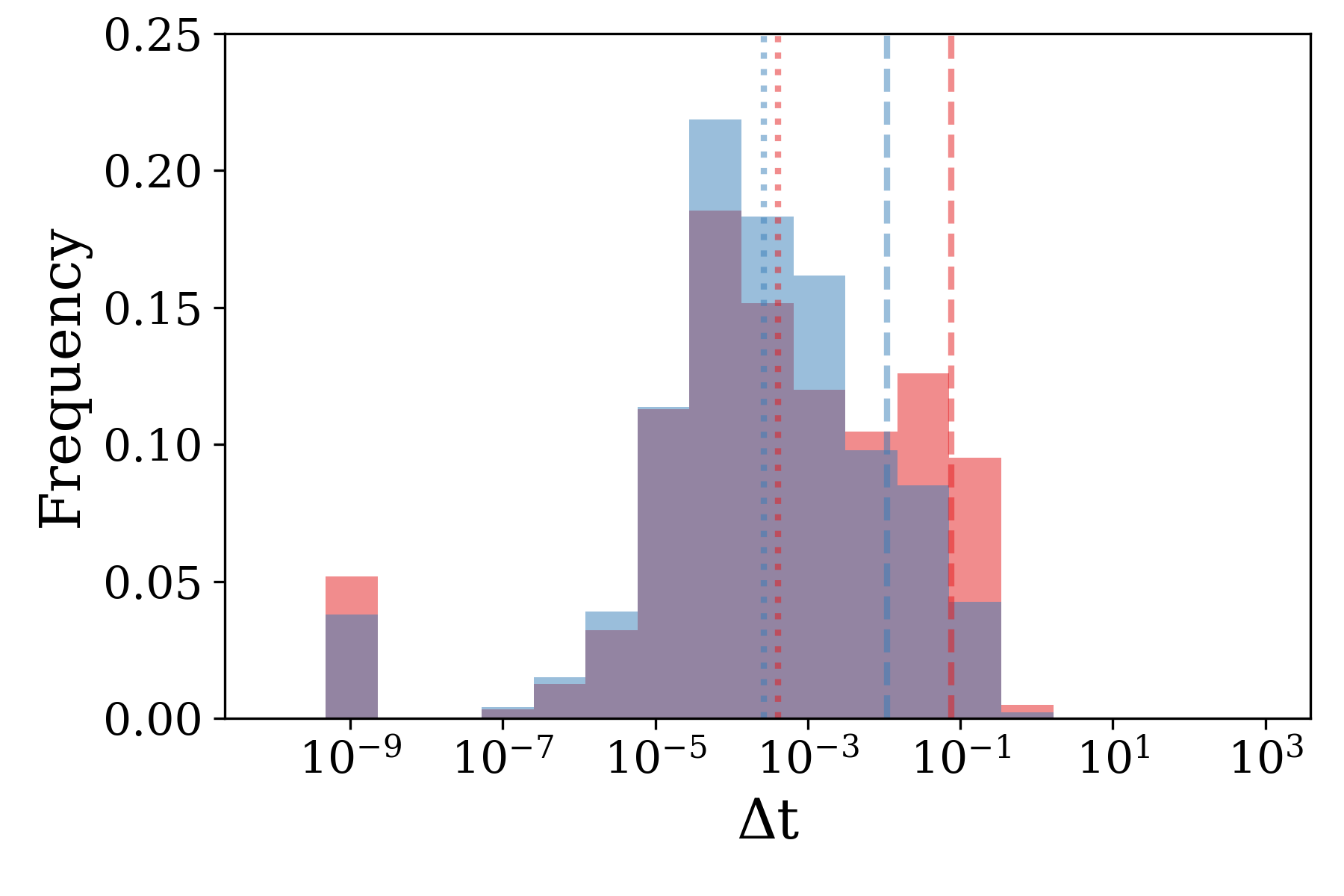

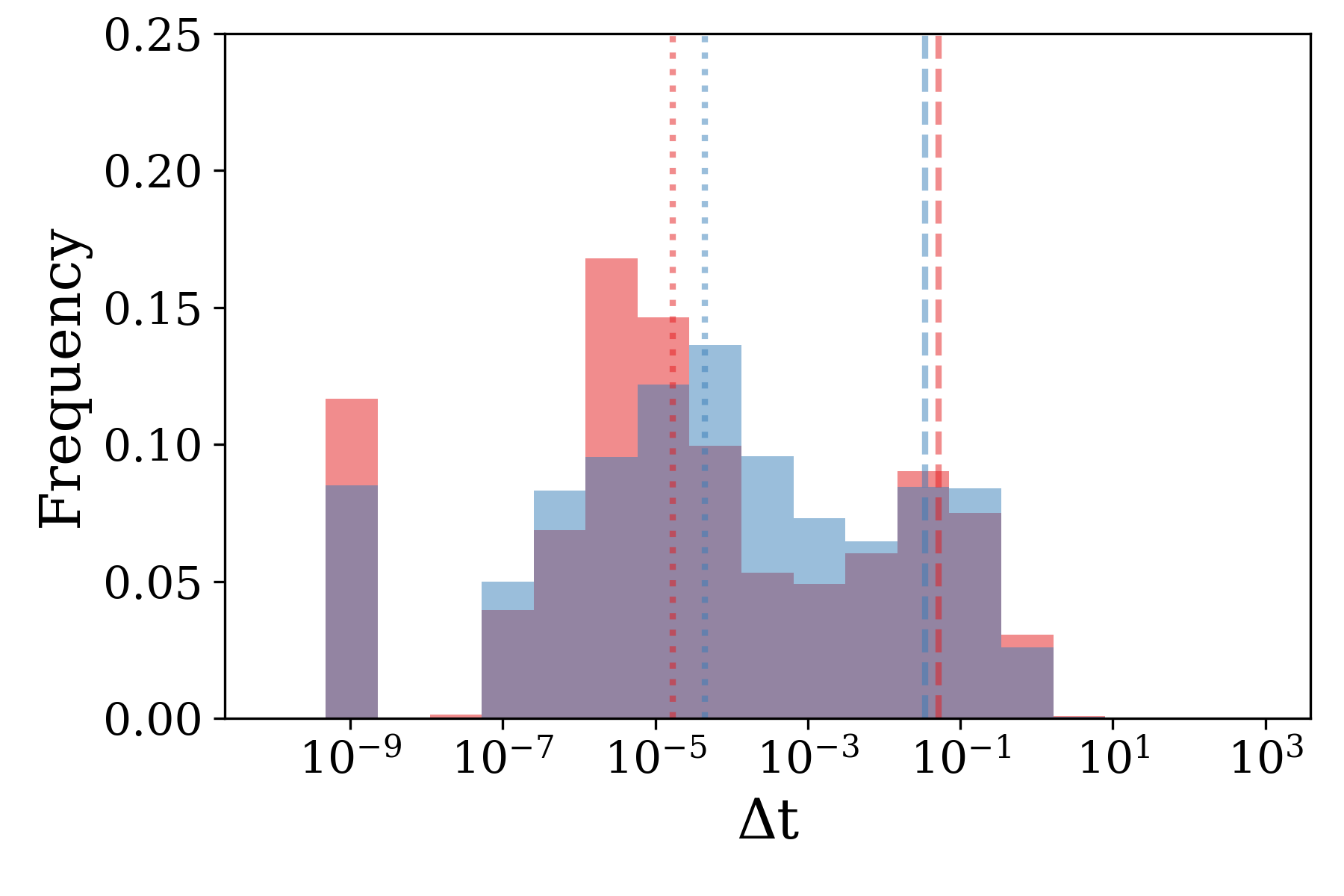

As described in section 4.2, for every message the model generates 4 inter-arrival time tokens , which are decoded and added to the previous message’s time stamp. Figure 6 compares the generated and realized message inter-arrival time distributions. The top two panels show probability plots (P-P plots), tracing the points across the support of , where is the empirical cumulative distribution function (ECDF) of the generative distribution of and the realized ECDF. An equivalent interpretation is that is shown on the y-axis for , where deviations from the diagonal indicate distributional deviations. The lower panels depict corresponding histograms of on a log-x-axis, as most observations are close to 0 with a long tail. Overall the model does a good job of matching the time features.

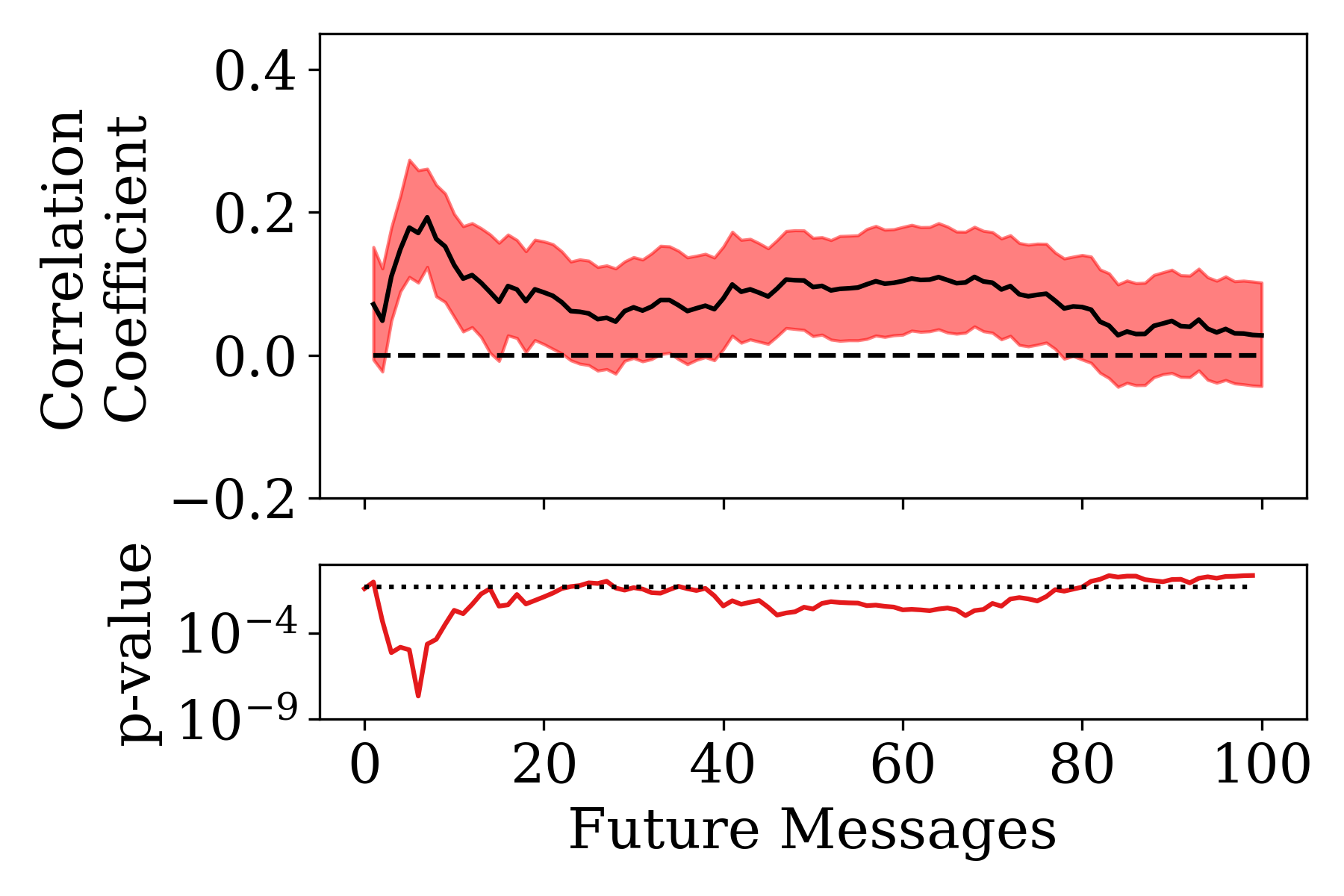

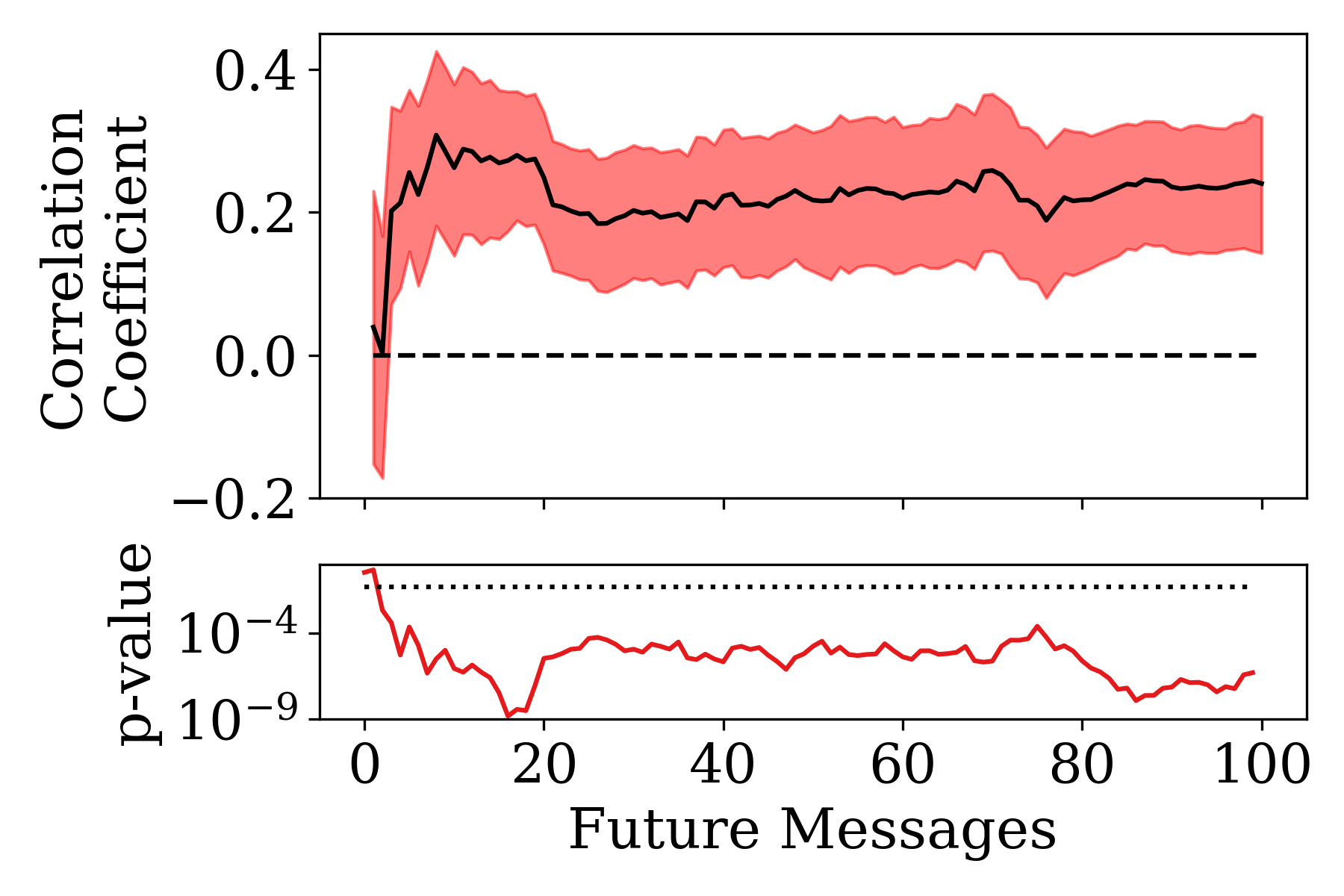

Sampling from conditional distributions enables the model to make forecasts. To evaluate the performance of the model prediction, we calculate the Pearson correlation coefficient between the generated returns and the realized returns for messages into the future. Figure 8 shows a sustained positive correlation for both GOOG () and INTC (). For INTC, the stock with less liquidity, correlations remain statistically significant at least 100 messages into the future.

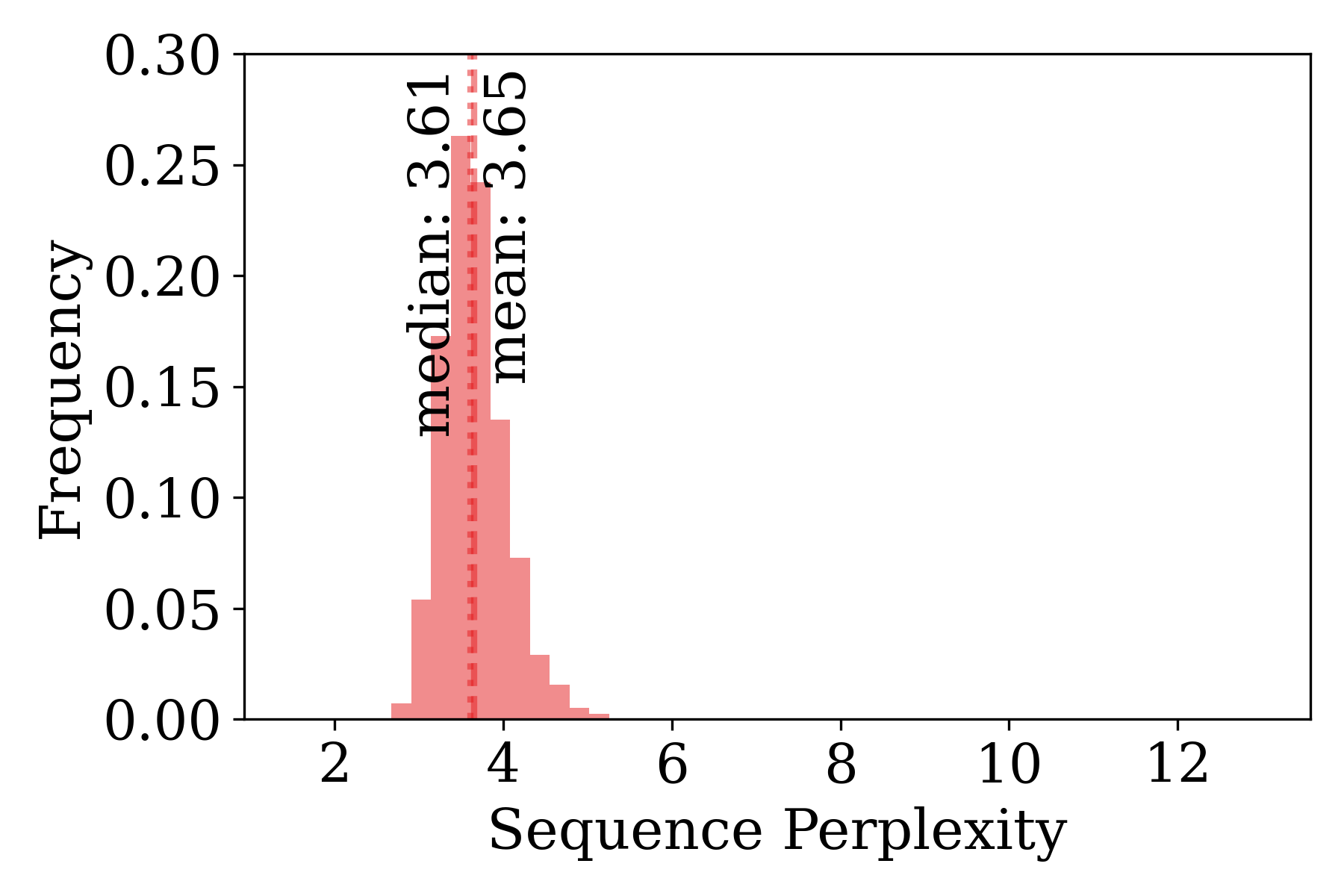

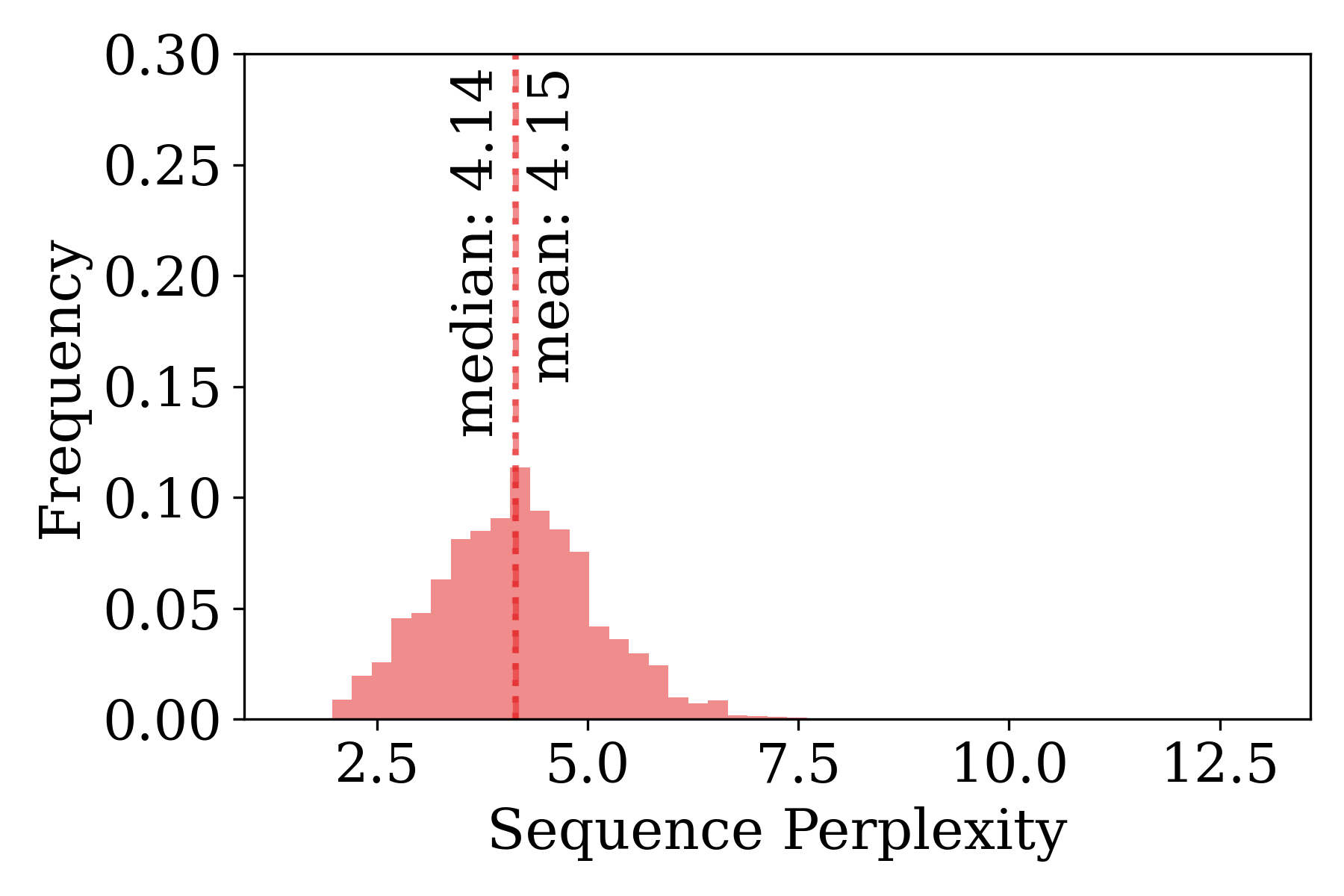

Figure 7 plots histograms of 100-message test sequence perplexity scores for both stocks. The model trained on GOOG data gets an overall lower perplexity than INTC with fewer extreme values of low probability sequences. This could be owed to more GOOG data being available during training as the stock has a higher trading volume and more messages in the same time period. Calculating overall per-token perplexity results in a score of (std.err. 0.0047) for GOOG and (std.err. 0.0043) for INTC. Table 1 calculates the perplexity for each of the token positions generated in a message. We observe that later digits of inter-arrival times become harder to predict as these are higher entropy distributions. In contrast, reference time tokens are easier to predict as these usually refer to earlier time tokens in the sequence. Generally, for this reason, reference tokens have lower perplexity than their counterpart fields in the new message. Comparing GOOG with INTC we observe, that the GOOG model has higher perplexity in generating an order’s price level, while INTC has higher uncertainty of order sizes. The difference in price level predictability agrees with the fact that INTC, as a small-tick stock, exhibits a denser order book on average (Eisler et al., 2012), while GOOG order sizes have lower entropy than INTC.

Stock Type Direction Price Size t Priceref Sizeref Timeref GOOG 2.15 1.71 1.04 5.55 3.18 1.00 6.21 405.49 770.01 1.04 1.45 1.07 1.01 1.63 2.41 2.09 1.93 INTC 1.92 1.55 1.02 2.41 13.51 1.01 5.45 122.93 524.66 1.03 1.21 1.22 1.02 1.96 3.76 6.58 7.94

7. Conclusions

We develop an end-to-end autoregressive generative model for electronic exchange message flow, trained on tokenized message sequences and LOB states, using a custom tokenizer. By embedding the model in an inference loop with a market replay simulator, we are able to generate full-fidelity granular trajectories of entire LOBs. A challenge of predictive machine learning models in finance, particularly in high-frequency market micro-structure, is market impact, i.e. the fact that market actions affect dynamics. Modeling realistic market impact is thus an important open problem, for which generative models of this kind provide a promising solution.

For tasks in natural language processing, autoregressive LLMs have proven superior to GAN-based models in cases where sufficient training data is available. Arguably, market micro-structure provides a similar domain with 2500 different stocks trading on the NASDAQ exchange alone, each with up to millions of daily messages. Our results show that such models are reasonable, can provide good performance, and could potentially be scaled up to something like autoregressive large financial environment models, which could be used for reinforcement learning. Similar approaches using GANs have not yet been very successful due to agents learning to exploit model errors (Coletta et al., 2023).

One challenge to generative micro-structure models is posed by message-arrival times. To our knowledge, we propose the first generative micro-structure data model, which treats times the same as other data features and learns a generative distribution, compared to e.g. binning time intervals as done in (Hultin et al., 2023a).

Despite the fact that the model is trained on tokenized micro-structure messages, we are able to match data distributions, such as the distribution of mid-price returns. This radical bottom-up approach, in combination with large neural networks, has been driving recent successes in LLMs and could similarly usher in the next generation of generative financial models.

Given these promising results, our work provides many interesting directions for future research. Current model limitations include errors when generating referential orders and computationally intensive message error correction. These issues could be abated by increasing the model and data set size. Besides larger models, future work could similarly investigate training on longer sequences. Different architectural choices, either improvements to the S5 layer (Zhang et al., 2022), or efficient transformer-based networks (Child et al., 2019) could be explored as alternatives.

Acknowledgements.

We thank Jan-Peter Calliess and Chris Lu for interesting discussions at different stages of this project.References

- (1)

- Assefa et al. (2020) Samuel A Assefa, Danial Dervovic, Mahmoud Mahfouz, Robert E Tillman, Prashant Reddy, and Manuela Veloso. 2020. Generating synthetic data in finance: opportunities, challenges and pitfalls. In Proceedings of the First ACM International Conference on AI in Finance. 1–8.

- Bau et al. (2019) David Bau, Jun-Yan Zhu, Jonas Wulff, William Peebles, Hendrik Strobelt, Bolei Zhou, and Antonio Torralba. 2019. Seeing what a gan cannot generate. In Proceedings of the IEEE/CVF International Conference on Computer Vision. 4502–4511.

- Bhatia et al. (2021) Siddharth Bhatia, Arjit Jain, and Bryan Hooi. 2021. Exgan: Adversarial generation of extreme samples. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 35. 6750–6758.

- Bishop and Nasrabadi (2006) Christopher M Bishop and Nasser M Nasrabadi. 2006. Pattern recognition and machine learning. Vol. 4. Springer.

- Bradbury et al. (2018) James Bradbury, Roy Frostig, Peter Hawkins, Matthew James Johnson, Chris Leary, Dougal Maclaurin, George Necula, Adam Paszke, Jake VanderPlas, Skye Wanderman-Milne, and Qiao Zhang. 2018. JAX: composable transformations of Python+NumPy programs. http://github.com/google/jax

- Brown et al. (2020) Tom Brown, Benjamin Mann, Nick Ryder, Melanie Subbiah, Jared D Kaplan, Prafulla Dhariwal, Arvind Neelakantan, Pranav Shyam, Girish Sastry, Amanda Askell, et al. 2020. Language models are few-shot learners. Advances in neural information processing systems 33 (2020), 1877–1901.

- Byrd et al. (2020) David Byrd, Maria Hybinette, and Tucker Hybinette Balch. 2020. ABIDES: Towards high-fidelity multi-agent market simulation. In Proceedings of the 2020 ACM SIGSIM Conference on Principles of Advanced Discrete Simulation. 11–22.

- Chen et al. (1998) Stanley F Chen, Douglas Beeferman, and Roni Rosenfeld. 1998. Evaluation metrics for language models. (1998).

- Child et al. (2019) Rewon Child, Scott Gray, Alec Radford, and Ilya Sutskever. 2019. Generating long sequences with sparse transformers. arXiv preprint:1904.10509 (2019).

- Chowdhery et al. (2022) Aakanksha Chowdhery, Sharan Narang, Jacob Devlin, Maarten Bosma, Gaurav Mishra, Adam Roberts, Paul Barham, Hyung Won Chung, Charles Sutton, Sebastian Gehrmann, et al. 2022. Palm: Scaling language modeling with pathways. arXiv preprint arXiv:2204.02311 (2022).

- Coletta et al. (2023) Andrea Coletta, Joseph Jerome, Rahul Savani, and Svitlana Vyetrenko. 2023. Conditional Generators for Limit Order Book Environments: Explainability, Challenges, and Robustness. arXiv preprint arXiv:2306.12806 (2023).

- Coletta et al. (2022) Andrea Coletta, Aymeric Moulin, Svitlana Vyetrenko, and Tucker Balch. 2022. Learning to simulate realistic limit order book markets from data as a World Agent. In Proceedings of the Third ACM International Conference on AI in Finance. 428–436.

- Coletta et al. (2021) Andrea Coletta, Matteo Prata, Michele Conti, Emanuele Mercanti, Novella Bartolini, Aymeric Moulin, Svitlana Vyetrenko, and Tucker Balch. 2021. Towards realistic market simulations: a generative adversarial networks approach. In Proceedings of the Second ACM International Conference on AI in Finance. 1–9.

- Cont et al. (2022) Rama Cont, Mihai Cucuringu, Renyuan Xu, and Chao Zhang. 2022. Tail-GAN: Learning to Simulate Tail Risk Scenarios. Available at SSRN 3812973 (2022).

- Cont et al. (2021) Rama Cont, Mihai Cucuringu, and Chao Zhang. 2021. Cross Impact of Order Flow Imbalances: Contemporaneous and Predictive. arXiv preprint arXiv:2112.13213 (2021).

- Cont et al. (2010) Rama Cont, Sasha Stoikov, and Rishi Talreja. 2010. A stochastic model for order book dynamics. Operations research 58, 3 (2010), 549–563.

- Croitoru et al. (2023) Florinel-Alin Croitoru, Vlad Hondru, Radu Tudor Ionescu, and Mubarak Shah. 2023. Diffusion models in vision: A survey. IEEE Transactions on Pattern Analysis and Machine Intelligence (2023).

- Eckerli and Osterrieder (2021) Florian Eckerli and Joerg Osterrieder. 2021. Generative Adversarial Networks in finance: an overview. arXiv preprint arXiv:2106.06364 (2021).

- Eisler et al. (2012) Zoltan Eisler, Jean-Philippe Bouchaud, and Julien Kockelkoren. 2012. The price impact of order book events: market orders, limit orders and cancellations. Quantitative Finance 12, 9 (2012), 1395–1419.

- Frey et al. (2023) Sascha Frey, Kang Li, Peer Nagy, Silvia Sapora, Chris Lu, Stefan Zohren, Jakob Foerster, and Anisoara Calinescu. forthcoming 2023. JAX-LOB: A GPU-Accelerated Limit Order Book Simulator to Unlock Large-Scale Reinforcement Learning for Trading. arXiv preprint (forthcoming 2023).

- Geiger et al. (2020) Alexander Geiger, Dongyu Liu, Sarah Alnegheimish, Alfredo Cuesta-Infante, and Kalyan Veeramachaneni. 2020. Tadgan: Time series anomaly detection using generative adversarial networks. In 2020 IEEE International Conference on Big Data (Big Data). IEEE, 33–43.

- Goodfellow et al. (2014) Ian Goodfellow, Jean Pouget-Abadie, Mehdi Mirza, Bing Xu, David Warde-Farley, Sherjil Ozair, Aaron Courville, and Yoshua Bengio. 2014. Generative adversarial nets. Advances in neural information processing systems 27 (2014).

- Gould et al. (2013) Martin D. Gould, Mason A. Porter, Stacy Williams, Mark McDonald, Daniel J. Fenn, and Sam D. Howison. 2013. Limit order books. Quantitative Finance 13, 11 (Nov. 2013), 1709–1742. https://doi.org/10.1080/14697688.2013.803148 Publisher: Routledge _eprint: https://doi.org/10.1080/14697688.2013.803148.

- Gu et al. (2020) Albert Gu, Tri Dao, Stefano Ermon, Atri Rudra, and Christopher Ré. 2020. Hippo: Recurrent memory with optimal polynomial projections. Advances in neural information processing systems 33 (2020), 1474–1487.

- Gu et al. (2022) Albert Gu, Karan Goel, Ankit Gupta, and Christopher Ré. 2022. On the parameterization and initialization of diagonal state space models. Advances in Neural Information Processing Systems 35 (2022), 35971–35983.

- Gu et al. (2021) Albert Gu, Karan Goel, and Christopher Ré. 2021. Efficiently Modeling Long Sequences with Structured State Spaces. In International Conference on Learning Representations.

- Henry-Labordere (2019) Pierre Henry-Labordere. 2019. Generative models for financial data. Available at SSRN 3408007 (2019).

- Huang and Polak (2011) Ruihong Huang and Tomas Polak. 2011. Lobster: Limit order book reconstruction system. Available at SSRN 1977207 (2011).

- Hultin et al. (2023a) Hanna Hultin, Henrik Hult, Alexandre Proutiere, Samuel Samama, and Ala Tarighati. 2023a. A generative model of a limit order book using recurrent neural networks. Quantitative Finance (2023), 1–28.

- Hultin et al. (2023b) Hanna Hultin, Henrik Hult, Alexandre Proutiere, Samuel Samama, and Ala Tarighati. 2023b. A generative model of a limit order book using recurrent neural networks. Quantitative Finance 23, 6 (2023), 931–958. https://doi.org/10.1080/14697688.2023.2205583 arXiv:https://doi.org/10.1080/14697688.2023.2205583

- Jumper et al. (2021) John Jumper, Richard Evans, Alexander Pritzel, Tim Green, Michael Figurnov, Olaf Ronneberger, Kathryn Tunyasuvunakool, Russ Bates, Augustin Žídek, Anna Potapenko, et al. 2021. Highly accurate protein structure prediction with AlphaFold. Nature 596, 7873 (2021), 583–589.

- Kenton and Toutanova (2019) Jacob Devlin Ming-Wei Chang Kenton and Lee Kristina Toutanova. 2019. BERT: Pre-training of Deep Bidirectional Transformers for Language Understanding. In Proceedings of NAACL-HLT. 4171–4186.

- Kingma and Ba (2014) Diederik P Kingma and Jimmy Ba. 2014. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980 (2014).

- Kolm et al. (2021) Petter N Kolm, Jeremy Turiel, and Nicholas Westray. 2021. Deep order flow imbalance: Extracting alpha at multiple horizons from the limit order book. Available at SSRN 3900141 (2021).

- Koochali et al. (2019) Alireza Koochali, Peter Schichtel, Andreas Dengel, and Sheraz Ahmed. 2019. Probabilistic Forecasting of Sensory Data With Generative Adversarial Networks – ForGAN. IEEE Access 7 (2019), 63868–63880. https://doi.org/10.1109/access.2019.2915544

- Korczak and Hemes (2017) Jerzy Korczak and Marcin Hemes. 2017. Deep learning for financial time series forecasting in a-trader system. In 2017 Federated Conference on Computer Science and Information Systems (FedCSIS). IEEE, 905–912.

- Li and Farnia (2023) Cheuk Ting Li and Farzan Farnia. 2023. Mode-Seeking Divergences: Theory and Applications to GANs. In International Conference on Artificial Intelligence and Statistics. PMLR, 8321–8350.

- Liu et al. (2022) Chunli Liu, Carmine Ventre, and Maria Polukarov. 2022. Synthetic Data Augmentation for Deep Reinforcement Learning in Financial Trading. In Proceedings of the Third ACM International Conference on AI in Finance. 343–351.

- Mirza and Osindero (2014) Mehdi Mirza and Simon Osindero. 2014. Conditional Generative Adversarial Nets. CoRR abs/1411.1784 (2014). arXiv:1411.1784 http://arxiv.org/abs/1411.1784

- Naritomi and Adachi (2020) Yusuke Naritomi and Takanori Adachi. 2020. Data augmentation of high frequency financial data using generative adversarial network. In 2020 IEEE/WIC/ACM International Joint Conference on Web Intelligence and Intelligent Agent Technology (WI-IAT). IEEE, 641–648.

- Ostrovski et al. (2018) Georg Ostrovski, Will Dabney, and Rémi Munos. 2018. Autoregressive quantile networks for generative modeling. In International Conference on Machine Learning. PMLR, 3936–3945.

- Rombach et al. (2022) Robin Rombach, Andreas Blattmann, Dominik Lorenz, Patrick Esser, and Björn Ommer. 2022. High-Resolution Image Synthesis With Latent Diffusion Models. In Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition (CVPR). 10684–10695.

- Rumelhart and McClelland (1987) David E Rumelhart and James L McClelland. 1987. Learning Internal Representations by Error Propagation. (1987).

- Sezer et al. (2020) Omer Berat Sezer, Mehmet Ugur Gudelek, and Ahmet Murat Ozbayoglu. 2020. Financial time series forecasting with deep learning : A systematic literature review: 2005–2019. Applied Soft Computing 90 (2020), 106181. https://doi.org/10.1016/j.asoc.2020.106181

- Smith et al. (2022) Jimmy TH Smith, Andrew Warrington, and Scott Linderman. 2022. Simplified State Space Layers for Sequence Modeling. In The Eleventh International Conference on Learning Representations.

- Takahashi et al. (2019) Shuntaro Takahashi, Yu Chen, and Kumiko Tanaka-Ishii. 2019. Modeling financial time-series with generative adversarial networks. Physica A: Statistical Mechanics and its Applications 527 (2019), 121261.

- Tay et al. (2020) Yi Tay, Mostafa Dehghani, Samira Abnar, Yikang Shen, Dara Bahri, Philip Pham, Jinfeng Rao, Liu Yang, Sebastian Ruder, and Donald Metzler. 2020. Long Range Arena: A Benchmark for Efficient Transformers. In International Conference on Learning Representations.

- Tustin (1947) Arnold Tustin. 1947. A method of analysing the behaviour of linear systems in terms of time series. Journal of the Institution of Electrical Engineers-Part IIA: Automatic Regulators and Servo Mechanisms 94, 1 (1947), 130–142.

- Vaswani et al. (2017) Ashish Vaswani, Noam Shazeer, Niki Parmar, Jakob Uszkoreit, Llion Jones, Aidan N Gomez, Łukasz Kaiser, and Illia Polosukhin. 2017. Attention is all you need. Advances in neural information processing systems 30 (2017).

- Vuletić et al. (2023) Milena Vuletić, Felix Prenzel, and Mihai Cucuringu. 2023. Fin-gan: Forecasting and classifying financial time series via generative adversarial networks. Available at SSRN 4328302 (2023).

- Yoon et al. (2019) Jinsung Yoon, Daniel Jarrett, and Mihaela van der Schaar. 2019. Time-series Generative Adversarial Networks. In Advances in Neural Information Processing Systems, H. Wallach, H. Larochelle, A. Beygelzimer, F. d'Alché-Buc, E. Fox, and R. Garnett (Eds.), Vol. 32. Curran Associates, Inc. https://proceedings.neurips.cc/paper_files/paper/2019/file/c9efe5f26cd17ba6216bbe2a7d26d490-Paper.pdf

- Zhang et al. (2022) Michael Zhang, Khaled Kamal Saab, Michael Poli, Tri Dao, Karan Goel, and Christopher Re. 2022. Effectively Modeling Time Series with Simple Discrete State Spaces. In The Eleventh International Conference on Learning Representations.

- Zhang et al. (2018) Zhaoyu Zhang, Mengyan Li, and Jun Yu. 2018. On the convergence and mode collapse of GAN. In SIGGRAPH Asia 2018 Technical Briefs. 1–4.

- Zhang et al. (2021) Zihao Zhang, Bryan Lim, and Stefan Zohren. 2021. Deep learning for market by order data. Applied Mathematical Finance 28, 1 (2021), 79–95.

- Zhang et al. (2019) Zihao Zhang, Stefan Zohren, and Stephen Roberts. 2019. Deeplob: Deep convolutional neural networks for limit order books. IEEE Transactions on Signal Processing 67, 11 (2019), 3001–3012.

- Zhou et al. (2018) Xingyu Zhou, Zhisong Pan, Guyu Hu, Siqi Tang, and Cheng Zhao. 2018. Stock market prediction on high-frequency data using generative adversarial nets. Mathematical Problems in Engineering (2018).