Target PCA: Transfer Learning Large Dimensional Panel Data††thanks: We thank Jose Blanchet, Kay Giesecke, Serena Ng, Neil Shephard and seminar and conference participants at Stanford, University of Rochester, Oxford, the NBER-NSF Time-Series Conference, California Econometrics Conference, SoFiE Conference, and NASMES for helpful comments.

First draft: December 14, 2022)

This paper develops a novel method to estimate a latent factor model for a large target panel with missing observations by optimally using the information from auxiliary panel data sets. We refer to our estimator as target-PCA. Transfer learning from auxiliary panel data allows us to deal with a large fraction of missing observations and weak signals in the target panel. We show that our estimator is more efficient and can consistently estimate weak factors, which are not identifiable with conventional methods. We provide the asymptotic inferential theory for target-PCA under very general assumptions on the approximate factor model and missing patterns. In an empirical study of imputing data in a mixed-frequency macroeconomic panel, we demonstrate that target-PCA significantly outperforms all benchmark methods.

Keywords: Factor Analysis, Principal Components, Transfer Learning, Multiple Data Sets, Large-Dimensional Panel Data, Large and , Missing Data, Weak Factors, Causal Inference

JEL classification: C14, C38, C55, G12

1 Introduction

Panel data with a large number of units and time periods are widely available in macroeconomics, finance, and many other areas of social sciences. In many cases, these panels can be well described by an approximate factor structure, that is, a small number of common factors explain a large portion of the co-movements. A common approach is to estimate latent factors with statistical methods from the panel of interest, which we refer to as target data. In the era of big data, there often exist auxiliary panels, that contain relevant information and share some common factors with the target panel. Combining the information in multiple panels can increase the efficiency of the estimated factor model for the target. Even more importantly, using auxiliary panels can identify the factors that only affect a small subset of units or are not detectable due to the missing observations in the target. The idea of using auxiliary panel data to estimate a model that is applied to a target data set is conceptually similar to transfer learning, which has been successfully used for machine learning tasks.

There is a broad class of practical problems which our setup is relevant. A particularly important case is mixed-frequency data, which is empirically studied in this paper. For example, some macroeconomic time series are only available at a quarterly or lower frequency, for example, GDP, while other time series are available at a higher frequency, for example, stock returns. As long as some factors in stock returns are also correlated with the macroeconomic movements, they can be used to obtain higher frequency factors and imputed values for the lower frequency target panel. Another important case is casual inference on panel data with non-random treatment, where missing data in the target panel correspond to the unobserved counterfactual outcomes. The auxiliary data could be panels for another set of units or the same set of units but with different outcome variables, which are correlated with the target time series. By leveraging auxiliary data, the latent factor model can be more precisely estimated, thus improving the precision of missing data imputation in the target panel.

These examples illustrate the benefits, but also fundamental challenges, of using auxiliary data. First, the cross-sectional dimensionality and the signal-to-noise ratio of the panels can be very different. Second, the target panel might include information not contained in the auxiliary data. Therefore, naive methods, such as simply concatenating target and auxiliary data to one large panel or using them separately, can be sub-optimal or infeasible.

We propose to estimate a latent factor model for the target data by optimally combining information from auxiliary panels with the target panel. We refer to this method as target-PCA (T-PCA). This method is broadly applicable but easy to implement: It applies principal component analysis (PCA) to a weighted average of the second-moment matrices of the target and auxiliary panels. Our method can be interpreted as applying PCA to an auxiliary panel with a reward for factors that are useful for the target panel. We show the consistency and provide the inferential theory for target-PCA under general assumptions on the latent factor model and missing observations. The asymptotic distribution is essential for two reasons: First, it provides guidance on selecting efficient weights in target-PCA; second, it provides confidence intervals for missing data imputation from the estimated latent factor model.

We show two important effects of the relative weights between target and auxiliary data in target-PCA. The first effect is the consistency effect for factor identification. This matters when neither the target nor the auxiliary data alone are sufficient to estimate all the factors that we care about. Factors cannot be consistently estimated from the target panel when their signal is too weak or when the partially observed data is insufficient, for example, when certain times are unobserved for the full panel. Suppose that these weak factors are strong in the auxiliary data, but the auxiliary data might not contain the other factors for the target. In this case, target-PCA can consistently estimate all factors, if we select the target weight for the auxiliary data at the right rate to account for the different dimensions of the panels.

The second effect is the efficiency effect in the estimation of latent factors and loadings. This effect arises when target and auxiliary data are observed with different noise levels. If the weighting in target-PCA properly accounts for the noise ratio between target and auxiliary data, then we can improve the efficiency of the estimated latent factor model. Hence, after selecting the target weight in the right order to ensure consistency, we can improve the efficiency by selecting the optimal scale of the weights.

These two important effects show that the optimal selection of weights in target-PCA is a challenging problem that can depend on the relative factor strength, observation pattern, noise level, and dimensionality between target and auxiliary data. To address this problem, we develop the inferential theory for the estimated factors, loadings, and imputed values for a general weighting scheme in target-PCA. The inferential theory is then used as guidance for selecting the weights in target-PCA. The naive cases of concatenating the target and auxiliary data, or using only one of the panels, are special cases of our general method. We show that these special cases are generally less efficient and even lack identification in the worst case.

Our work contributes to four distinct areas. First, we contribute to the literature on large dimensional factor models by proposing a new setup where the latent factors can be jointly estimated from multiple panel data. Second, we provide a new solution to the problem of weak factors, which cannot be consistently estimated with conventional PCA estimators and require additional signals. We show how to leverage the information in supplementary panels to overcome the weak signal problem. Third, our paper complements the recent work on imputing missing data in large panels. We show that leveraging auxiliary data allows us to impute missing observations with higher precision and makes it possible to impute values that could otherwise not be imputed using only the target panel. Last but not least, we contribute to causal inference and can estimate heterogeneous and time-dependent treatment effects for general interventions.

Our asymptotic results are developed under the framework of an approximate latent factor structure for both target and auxiliary data, both with large cross-section and time-series dimensions. Our new setup of using multiple panels generalizes the existing factor modeling literature, which only uses one panel so far. When the data is fully observed, Bai and Ng (2002) show that the factor model can be estimated with PCA applied to the covariance matrix of the data. Bai (2003) and Fan, Liao, and Mincheva (2013) derive the consistency and asymptotic normality of the estimated factors, loadings and common components. Extensions of latent factor models with fully observed data include among others adding observable factors in Bai (2009), sparse and interpretable latent factors in Pelger and Xiong (2021a), conditional loadings in Fan, Liao, and Wang (2016), Pelger and Xiong (2021b), Chen, Roussanov, and Wang (2021) and Chen (2022), time-varying, locally estimated loadings in Su and Wang (2017) and high-frequency estimation in Pelger (2019). The idea of increasing the efficiency by weighting panels differently is related to the GLS type weighting for PCA estimators suggested among others in Breitung and Tenhofen (2011) and Choi (2012). Boivin and Ng (2006) study empirically the benefits for PCA estimators when down-weighting or dropping uninformative information.

Our work complements the recent work on estimating the latent factor model from one large panel with missing observations and developing entry-wise inferential theory. Our results extend the framework of Xiong and Pelger (2023) to the new setup of multiple panels. Other closely related work includes the recent papers by Jin, Miao, and Su (2021), Bai and Ng (2021), and Cahan, Bai, and Ng (2023). These papers differ in the algorithms to impute the missing observations, the generality of the missing patterns, and the proportion of required observed entries relative to the missing entries. Bai and Ng (2021), and Cahan, Bai, and Ng (2023) leverage a block structure in missing data. Jin, Miao, and Su (2021) focuses on the case of missing-at-random and analyzes the EM estimator considered in Stock and Watson (1998). We show that by leveraging auxiliary data, we not only increase the precision for imputing missing values, but can also accommodate more general missing patterns. The problem of missing data imputation has been actively studied in the matrix completion literature since Candès and Recht (2009). The data imputation algorithms are largely based on rank-regularized methods with worst-case guarantees. Until recently, the entry-wise inferential theory is provided by the celebrated work of Chen, Fan, Ma, and Yan (2019) under the assumption of i.i.d. sampling. In contrast, we build on the large dimensional factor modeling literature, allowing us to make progress on the inferential theory under general observation patterns.

Our proposal of using auxiliary data brings the idea of transfer learning to the estimation of latent factors. The concept of transfer learning is to apply a model estimated on auxiliary data to target data. Transfer learning has been successfully used for machine learning tasks as surveyed by Pan and Yang (2009). Related to our work, Huang, Jiang, Li, Tong, and Zhou (2022) propose to forecast one target time series by scaling each of the auxiliary predictors by its predictive power on the target. In contrast, our target-PCA allows for a large cross-sectional dimension of the target with missing observations.

Our work provides a complementary and novel solution for weak factor estimation. Onatski (2012) has shown that conventional PCA estimators cannot consistently estimate factors that are too weak. Onatski (2010), Ahn and Horenstein (2013), Bai and Ng (2023), Onatski (2022) and others have studied the properties of weak factors and test the number of factors, with a focus on one panel. Lettau and Pelger (2020) have demonstrated that including additional information from other moments of the data can overcome the problem for certain types of weak factors. Similarly, our novel use of additional information from the auxiliary data can upweight the weak signals, allowing for the identification and efficient estimation of weak factors.

Our work is also complementary to the literature on mixed-frequency data imputation. A specific application of our general framework is to impute low-frequency observations in a target panel using auxiliary panels of higher frequency. One approach to dealing with data sampled at different frequencies has emerged in work by Ghysels, Santa-Clara, and Valkanov (2004), and Andreou, Ghysels, and Kourtellos (2010) using Mi(xed) Da(ta) S(ampling) (MIDAS) regressions, and its many extensions have been surveyed among others in Ghysels, Kvedaras, and Zemlys-Balevičius (2020). The MIDAS regression relates the low-frequency time series that we wish to predict to observables at high and low frequencies. Our framework shares some similarities as it relates latent factors of higher frequency to a large panel of lower-frequency observations. Another alternative is to use state space models to deal with mixed frequency data - usually estimated using the Kalman filter (see Bai, Ghysels, and Wright (2013) for a comparison with MIDAS). State space models are parameter-driven and impose different assumptions on the data generating process.111Stock and Watson (2016) discusses the issues with state space estimation of factor models with missing data. Another complementary idea is based on interpolation arguments as for example in Chow and Lin (1971). The recent work of Ng and Scanlan (2023) emphasizes the importance of residual correlation in the imputation of mixed frequency data. They propose a dynamic matrix completion approach by combining the state space setup and Chow and Lin (1971) type bridge regressions with latent factor models estimated from a large partially observed panel.

In simulation and empirical studies, we show the superior performance of our target-PCA method relative to benchmarks under a variety of settings. Our comprehensive simulations compare target-PCA to the natural benchmarks of applying PCA to separate panels or simple concatenated panels. Target-PCA substantially outperforms the alternatives in- and out-of-sample under different observation patterns. Our empirical analysis shows the good performance of target-PCA for imputing missing values in popular macroeconomic panels. We demonstrate the potential of target-PCA for nowcasting macroeconomic panels by imputing unbalanced low-frequency panels with higher-frequency auxiliary data.

The rest of the paper is organized as follows. Section 2 introduces the model and target-PCA. Section 3 illustrates the two important effects of weighting auxiliary data. Section 4 formalizes the assumptions on the observation pattern and approximate factor model. Section 5 provides the consistency and asymptotic results for our estimator, which can be used as guidance to select the weight in target-PCA. Section 6 discusses the extensions of our method, whose good performance compared to other methods is demonstrated by the extensive simulations in Section 7. Section 8 shows the practical relevance of target-PCA through empirical examples of imputing missing entries in macroeconomic data. Section 9 concludes the paper.

2 Model Setup

2.1 Model

We partially observe a target panel data set with time periods and cross-sectional units, where both and are large. has an approximate latent factor structure with common factors,

Here, denotes the data for the -th cross section at time , is a vector of latent factors, is its corresponding latent factor loadings, is the common component of and is the idiosyncratic component of . This factor model can also be written in a matrix notation as

Our goal is to estimate the latent factor structure in . We are particularly interested in the important case, where some entries in can be missing. In many practical applications, the panel might not be informative enough to estimate the latent factor model. First, the factors in can be weak, that is, affect only a small subset of cross-sectional units. In this case, it is possible that the factors cannot be separated from the noise, and conventional principal component analysis (PCA) fails to estimate them. Second, the observed data might be insufficient to estimate the full factor model, either because certain times are never observed in the panel, for example with low-frequency data, or because the missingness depends on the factor structure.

Our solution is to use additional information from auxiliary panel data . Suppose we observe auxiliary data that contain relevant information and can be helpful for the estimation of latent factors in . For the exposition, we focus on the case where there is only one auxiliary panel data and study how to optimally use the information in to estimate the factors in . Our results can easily be extended to the case of multiple auxiliary panels, as discussed in Section 6.3.

Suppose has an approximate latent factor structure with time periods and cross-section units, where is large. Both panels and are observed for the same time periods. has factors

where is a vector of latent factors, is its corresponding latent factor loadings and is the idiosyncratic error of .

The auxiliary panel data can be useful when it has some factors in common with . Without loss of generality, we can use the rotation of the factor models such that the concatenated factors in and in are orthogonal. We denote by the union of the factors in and . The total number of non-redundant latent factors in equals the rank of the concatenated panel matrix . Given our normalization, is a diagonal matrix. It is notationally convenient to write both the target panel data and auxiliary panel in terms of , that is the union of all the non-redundant factors. Hence, the target follows

where is the total number of non-redundant latent factors in , and is a vector of loadings on . Note that we explicitly allow the loadings to be zero for some factors. More specifically, for factors that are unique to and do not appear in , the corresponding loadings in are zero. Similarly, we express the auxiliary panel data as

where is a vector of factor loadings for in .

In an approximate factor model, a large part of the variation is explained by the factors, while the noise is only weakly dependent. We allow for the empirically relevant case, where not all factors in are strong, but only affect a subset of the panel. Let be unit ’s loading for the -th factor of . We refer to the -th factor as a strong factor in , if it affects a large number of units in . Formally, factor is strong factor if it satisfies for . On the other hand, if grows at a rate smaller than , then we refer to the -th factor as a weak factor in . The weak factor only affects a small fraction of units, with the fraction converging to zero as grows. Without loss of generality, we assume that all factors are strong factors in . As our objective is to estimate the factor model for , we are not interested in estimating the weak factors in . However, it is straightforward to extend our results to the case of weak factors in .

For the cross-sectional dimension of and , we focus on the setting where . This includes two cases: and are of the same order (i.e., ) and is much larger than (i.e., ). When , we consider the finite case in Section 6.2. The setting of is analogous and can be studied by similar arguments.

2.2 Observation Patterns

We allow the target data to have missing observations. Let be the observation pattern of , where if is observed and zero otherwise. For simplicity, we assume the auxiliary data is fully observed, but our methods and results can be easily generalized to the case where is only partially observed as well.

We allow for very general observation patterns in . Whether an entry is observed or not can depend on whether other entries are observed, and on the factor model itself. The formal assumptions on the observation patterns are introduced in Section 4. To provide some intuition, Figure 1 shows three important examples of the observation patterns that we are interested in. In the first example, entries are missing completely at random, that is, whether an entry is observed or not does not depend on whether other entries are observed or not.

The second example is the observation pattern for control panels with staggered treatment adoption. Once a unit adopts the treatment, it stays treated afterwards, which can be modeled as missing values. This pattern is widely assumed in the literature on causal inference in panel data.

The third and attentive example shows the observation pattern of low-frequency time-series variables in , where variables in other data sets (including ) and applications are at a higher frequency. For example, assume that is a macroeconomic panel data set, where the time series are only available at a quarterly frequency, but a downstream application requires these time series as inputs at a monthly frequency. The monthly observations in between the quarters are modeled as missing observations. Importantly, in this example, there is no information in for the months where the quarterly variables are not reported, invalidating the existing latent factor estimation methods from partially observed only (Bai and Ng, 2021; Cahan, Bai, and Ng, 2023; Xiong and Pelger, 2023). In contrast, our proposed method can identify the latent factor values in these months by using auxiliary data of higher frequency.

|

|

|

| (a) Randomly missing | (b) Staggered treatment adoption | (c) Low-frequency observation |

These figures show examples of observation patterns. The entries with dark color denote observed entries, while the entries with light color denote missing entries. Each row represents the observation pattern for a time period and each column represents the observation pattern for a unit.

2.3 Main Objective and Key Challenges

The main objective of this paper is to estimate a complete factor model, that is, all the relevant factors for the target , their loadings on the target, and the implied common component for the target, and to provide a complete inferential theory for all components of the factor model. There are three key challenges for this objective, specifically in the presence of missing observations, that invalidate the standard approaches for latent factor estimation. In particular, applying conventional PCA to either , , or a simple concatenated panel of and will either be infeasible, inconsistent, or inefficient.

First, the information in may not be sufficient to estimate the factors at all time periods with conventional PCA methods. If some factors in are weak in , then the identification assumptions underlying PCA are violated, and a conventional PCA estimate cannot separate those factors from the noise. This problem can arise even for fully observed data. If the panel has missing data, then this can pose additional challenges. For only partially observed data in , it is possible that even the strong factors in cannot be estimated for all time periods. The leading example is when is only observed at a lower frequency, for example, annual data. In that case, we cannot infer the factor realizations for a higher frequency, for example, monthly, even for strong factors. As another complication, missingness can “weaken” the factor signal in the observed data, as the missing pattern can depend on the factor model and affect the effective sample size. In all these three cases, we can only learn the strong factors in from the target for the time periods with sufficiently many observations. Hence, in these situations, we need to take advantage of the additional information in .

Second, the auxiliary panel may not contain all the factors in , and hence applying PCA only to can fail to consistently estimate the factors for . In applications, there is no reason to assume a priori that the strong factors in a supplementary data set, that is not specifically targeted for , include all the factors . Hence, we cannot ignore the information in , and need a way to combine the two panels.

Third, the dimensions of the panels and can be very different. It is natural to assume that in many applications, the auxiliary panel is much larger in the hope that it contains some useful information for . If is much larger than , then applying PCA to the concatenated panel of and can only identify the factors in , but not the factors that are unique to and not included in . This is because the target panel can receive a weight that is too low in a naively concatenated panel.

Therefore, the presence of these three challenges requires new methods to estimate all the factors in . Our target-PCA proposed in Section 2.4 below provides a solution to simultaneously address these three challenges. Target-PCA extracts the factors from that are the most useful for explaining , and efficiently combines them with the information in .

In the following, we focus on the practically relevant and challenging case where the auxiliary data does not contain all the factors in , which is formalized in Assumption G1.

Assumption G1 ( ).

There exist some strong factors in the target that are not strong or not contained in the auxiliary panel , that is,

where denotes the loadings in that correspond to the strong factors in , and denotes the number of strong factors in .

Section 6.1 discusses the simpler case, where the strong factors in include all factors for , and hence the auxiliary panel is sufficient to learn the factors in . This special case is a subset of our more comprehensive analysis.

2.4 Estimator

We propose a novel estimator, target-PCA, to estimate the latent factors in by combining the information in and . Then we use the estimated factor model to impute missing observations in .

To illustrate the intuition of our target-PCA estimator, we start with the case where is fully observed. Recall, that in the conventional setup where we have only one fully-observed panel, we can estimate the latent factors that explain most variation in the data by minimizing the objective function of PCA. Our target-PCA estimator combines the PCA objective function for the auxiliary panel and the PCA objective function for the target with a positive target weight as

| (1) |

This combination aims to extract the latent factors of , by optimally weighting the information in and through the parameter . The target parameter can be interpreted as a reward for factors that help to explain the target panel . In this sense, is similar to a regularization parameter and controls the reward given to factors that reduce the error in explaining . As we will show next, can also be interpreted as a relative weight for the information in and in a concatenated panel.

We can write (1) in matrix notation as

| (2) |

For exposition, we introduce the notation as the combination of and with target weight , i.e.,

With the identifying assumption , we can concentrate out in the objective function (2), and obtain from the following objective function222An alternative approach to obtain the optimal , and in the objective function (1) is based on the identifying assumption . Under this identifying assumption, we concentrate out both and in the objective function (2), and solve for from the objective function (3) Appendix D provides more details about how to adapt this alternative approach to allow for missing observations.

| (4) |

Hence, when is fully observed, we can estimate by applying PCA to . Note that is an estimator of the second moment of the weighted concatenated panel . We denote the second population moment of as , which equals the cross-sectional covariance matrix of in the case of demeaned data. Hence, target-PCA is equivalent to PCA on the weighted data .

When has missing observations, we can also apply PCA to an estimator of , but we need to account for the missing observations in in the estimation of . Conceptually, we can use the time periods when both cross-sectional units and are observed to estimate , where is the -th entry in . Formally, we introduce a new observation matrix , where if is observed and otherwise. For any two cross-sectional units and , let be the set of time periods where both and are observed. We use the time periods in to estimate

With the identifying assumption , the estimated loadings from PCA, denoted as , are times the eigenvectors of the largest eigenvalues of , that is,

where is the diagonal matrix of the largest eigenvalues of . In this step, we simultaneously estimate the factor loadings in and .

In a second step, we regress the observed on to estimate the factors, that is,

This step only uses the units that are observed at time , and runs a weighted regression of the observed units’ outcomes on the estimated loadings. The weight for units in is , while the weight for units in is .

Next we estimate the common component of with the plug-in estimator , and use the estimated common components to impute the missing entries in . Note that our proposed estimator for the latent factor model in the partially observed is the same type of estimator as in Xiong and Pelger (2023). The key distinction is that our estimator is applied to the weighted concatenated panel , while the estimator in Xiong and Pelger (2023) is applied to only.333It is possible to use other methods to estimate the factor model when the missing pattern has specific structures. For example, we can use Jin, Miao, and Su (2021) when observations are missing-at-random or use Bai and Ng (2021) and Cahan, Bai, and Ng (2023) for block-missing. The asymptotic results for alternative methods would require a case-by-case analysis, but we expect the general insights for the choice of the target weight to stay the same.

As shown in the original objective function (1), the key of target-PCA is the target weight . There are three special cases of target-PCA with different values of : First, when , target-PCA degenerates to applying PCA to . Second, when , target-PCA degenerates to applying PCA to . Third, when , target-PCA is equivalent to applying PCA to the concatenated panel . The key problem is to select the target weight appropriately. Intuitively, the target weight should not be too small in order to ensure that the selected factors are relevant for , and cannot be too large in order to take advantage of the supplementary information in .

The asymptotic distribution results for target-PCA require novel derivations and are not simply an application of Xiong and Pelger (2023) applied to . A key challenge is that the target weight can go to infinity with the sample size, which would lead to exploding moments in some of the components of and hence violate the assumptions in existing frameworks. Therefore, we need to carefully consider the separate components of , while allowing for joint asymptotics of growing with the sample size.

The main insight of target-PCA is that properly weighting the covariance matrices of multiple panels allows for the consistent and efficient estimation of latent factors. As will be shown in the next sections, the optimality of combining auxiliary data boils down to two aspects: (a) the detection of weak signals in the target panel; and (b) the efficient estimation of the factor structure. Our target-PCA estimator simultaneously achieves them in one step through the target weight . In fact, these two aspects correspond to two important effects of the target weight , which will be thoroughly discussed in Section 3.

3 Two Fundamental Effects of Target Weight

In this section, we illustrate and highlight the two important effects of the target weight in target-PCA: the consistency effect in factor identification and the efficiency effect in the estimation of factors and loadings. It is crucial to account for these two effects when choosing in target-PCA. In this section, we use simple models to explain these fundamental effects, and then provide the results for the general case in Section 5.

3.1 Effect 1: Consistency Effect of Target Weight

The first important effect is the consistent estimation of the factors. This effect is relevant when some factors in the observed are weak and cannot be identified by applying PCA to . For this case, if the weak factors in are strong factors in , then it is possible to identify these factors with target-PCA. Specifically, if we choose for some positive constant , then target-PCA can consistently estimate these weak factors. The intuition is as follows.

Target-PCA essentially estimates the factors from a matrix that combines and , where replaces the missing entries in with . Suppose that the auxiliary panel is fully observed and the number of common observations between any two units of the target is proportional to (the main setting studied in this paper). Then the top eigenvalues in and are at the order of and , respectively. If we select for some positive constant , then the top eigenvalues in and are at the same order, and equivalently, the factor strengths of the strong factors in and in are the same in the combined matrix of target-PCA. As the weak factors in are strong factors in , target-PCA can identify both the strong and weak factors in , leading to the consistency effect.

Next, we flesh out the intuition with a toy example. This two-factor example has the following key elements: (a) The dimension of the panel is much larger than , i.e., . (b) In panel , factor 1 is strong, but factor 2 is weak. Hence, we can only identify factor 1 from panel . (c) In panel , factor 2 is strong, but factor 1 has zero exposure to the units. Hence, we can only identify factor 2 from panel . Specifically, the loadings in follow

and loadings in follow

For simplicity, both the factors and idiosyncratic errors are drawn independently as and for all and . Furthermore, the factors and loadings have bounded fourth moments, and errors have bounded eighth moments. We assume that we can observe all the entries in . As we show in Section 5, the insights from this simplified setting carry over to our general model with missing observations.444Note that the observation pattern affects the asymptotic variance, but not the convergence rate of the estimated factor model or the top eigenvalues of , as shown in Xiong and Pelger (2023). Therefore, the intuition for this toy example carries over to other observation patterns.

In this example, separate PCA on either or is not able to consistently estimate both factors. However, target-PCA can identify both factors with an appropriately chosen . Without error terms and missing observations, target-PCA estimates factors from

where and denote the vector of the first and second factors, respectively. As , converges to

where and are the second-moment matrices of the loadings of and .555We use subscript in to account for the case where there are missing observations in and the second-moment loading matrices of is time-varying. 666If , we can estimate the second moment matrix . Selecting for a positive constant can still ensure that converges to a full rank matrix, which allows for the consistent estimation of both factors.

The key idea for selecting is to obtain full rank for the limit of the second-moment matrix . Choosing with some positive constant ensures that both eigenvalues in the limit of are of the same order, and therefore, both factors can be identified from . If is not chosen at this rate, for example, , then only the second factor can be identified as a strong factor in the concatenated panel. We formalize the above discussion in the following proposition, which is a special case of the general Theorem 1, and provide further details in Section 5.

Proposition 1.

Under the data generating process and observation pattern described in this section, let and assume that . Target-PCA with for some positive scaling constant can consistently estimate the latent factors. As , there exists some rotation matrix such that

If , then can be inconsistent.

3.2 Effect 2: Efficiency Effect of Target Weight

After we have selected in the right order to ensure consistency, we can improve the efficiency by selecting the optimal scale of . We call this the efficiency effect of . The essence of this effect is to use the target weight to balance the idiosyncratic noise levels between and , thus achieving the smallest asymptotic variance in the estimation of factors, loadings, and common components.

In this section, we illustrate the efficiency effect of through a simple one-factor model, where factor identification is not a concern and where we can focus on the efficiency effect. The key element is that the idiosyncratic noise levels in and are different.

More specifically, we assume that and contain the same latent factor. Factors, loadings and idiosyncratic errors are drawn independently from , and . Furthermore, the factors and loadings have bounded fourth moments, and errors have bounded eighth moments. Suppose all entries in are missing at random with observation probability and the number of units in and are at the same order, i.e., for some bounded away from . As shown in our general model, the main conclusions do not depend on these specific assumptions.

In this setting, Proposition 2 provides the asymptotic distribution of the common components of . The result is a special case of the general Theorem 2 in Section 5. We optimize by minimizing the asymptotic variance.

Proposition 2.

Under the data generating process and observation pattern described in this section, let and suppose . As , the asymptotic distribution of the estimated common component of for any and is

where

The optimized that minimizes is for any and .

The optimized minimizes , which is the asymptotic variance of the common components as a function of . In this case, the optimized is the ratio of the variances of idiosyncratic errors and . We up-weight the target panel if ; otherwise, we down-weight the target panel . Interestingly and counter-intuitively, when observations are missing at random, the optimized is the same for all and , and does not depend on any of the following parameters, even though is a function of these parameters: the observation probability , the value of factors and loadings , variance of factors and loadings and , and number of cross-section units and . The intuition in this setting is the same as that for choosing the optimal weighting matrix for a weighted least squares (WLS) estimator. Specifically, suppose the heteroscedasticity of residuals does not depend on values of covariates as in this setting; then the optimal weighting matrix in WLS is proportional to the inverse variance of residuals and does not directly depend on the covariates and model parameters.

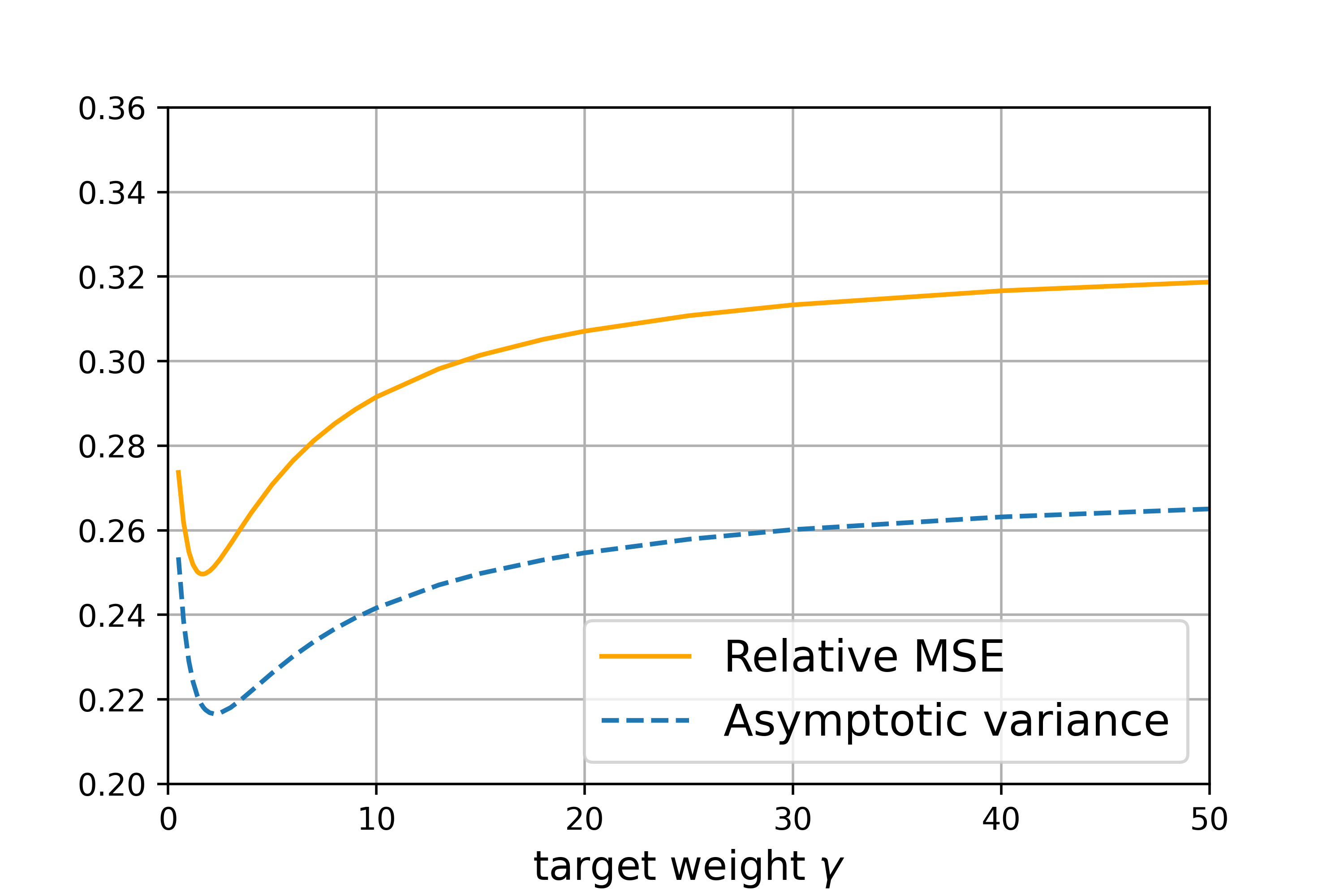

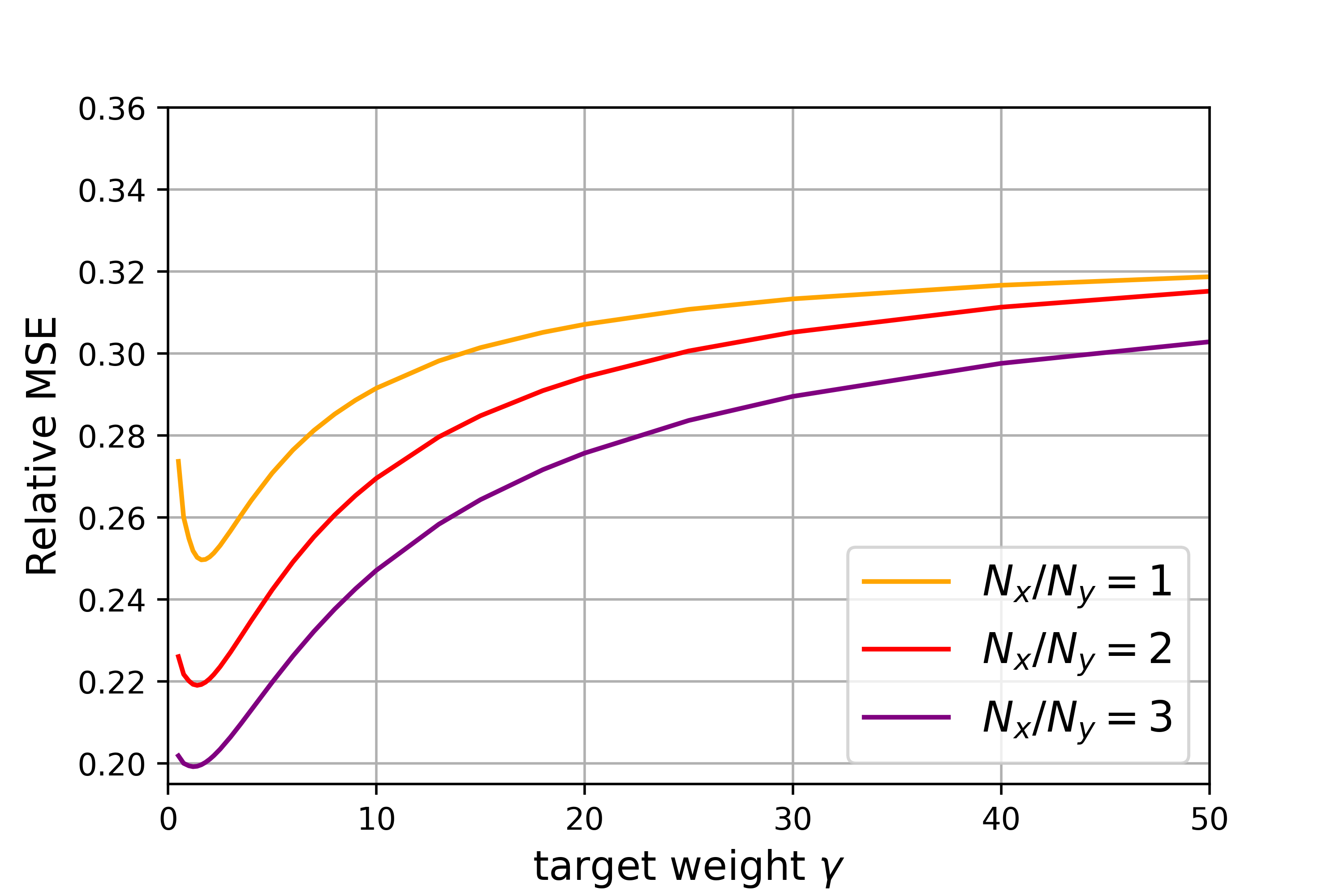

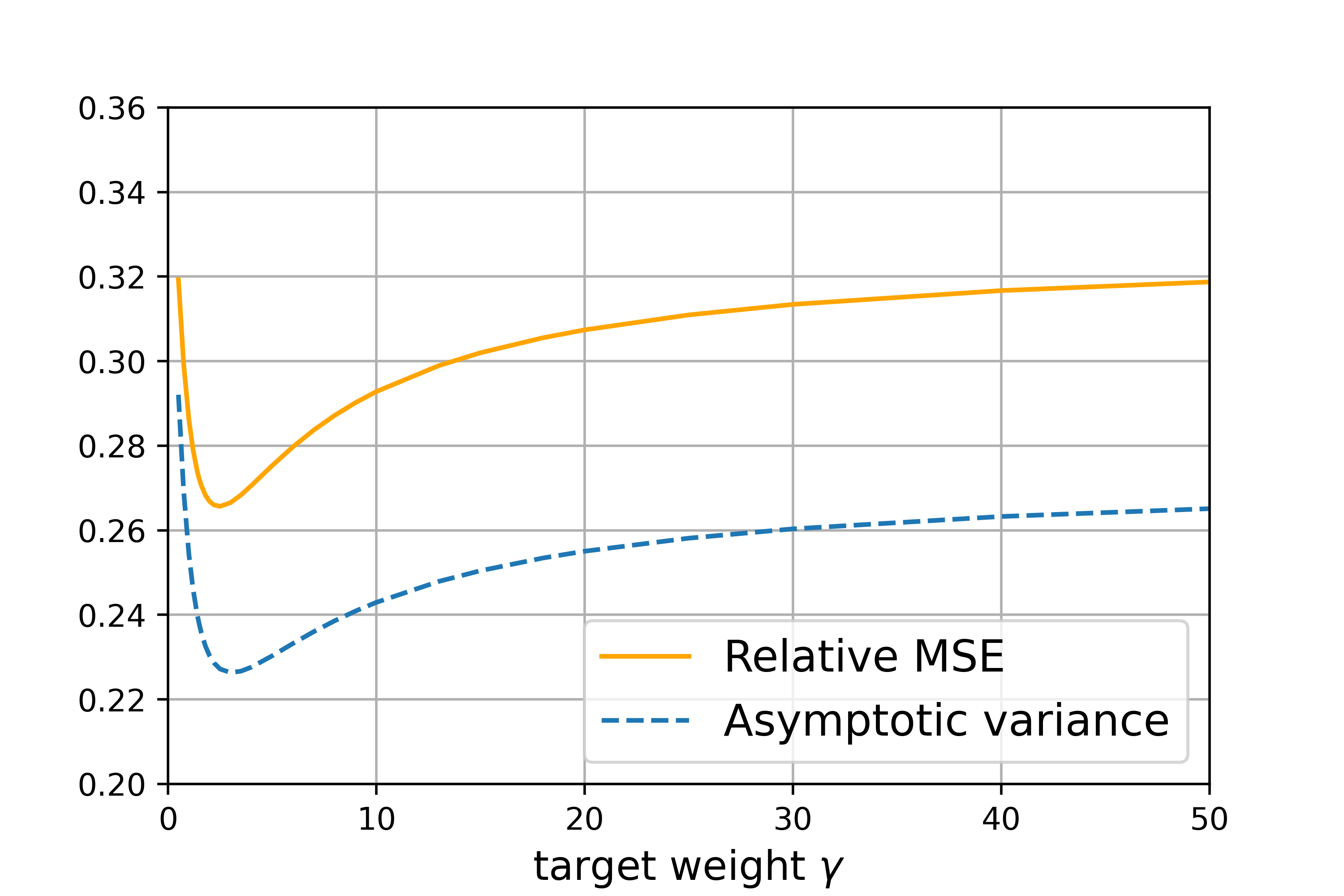

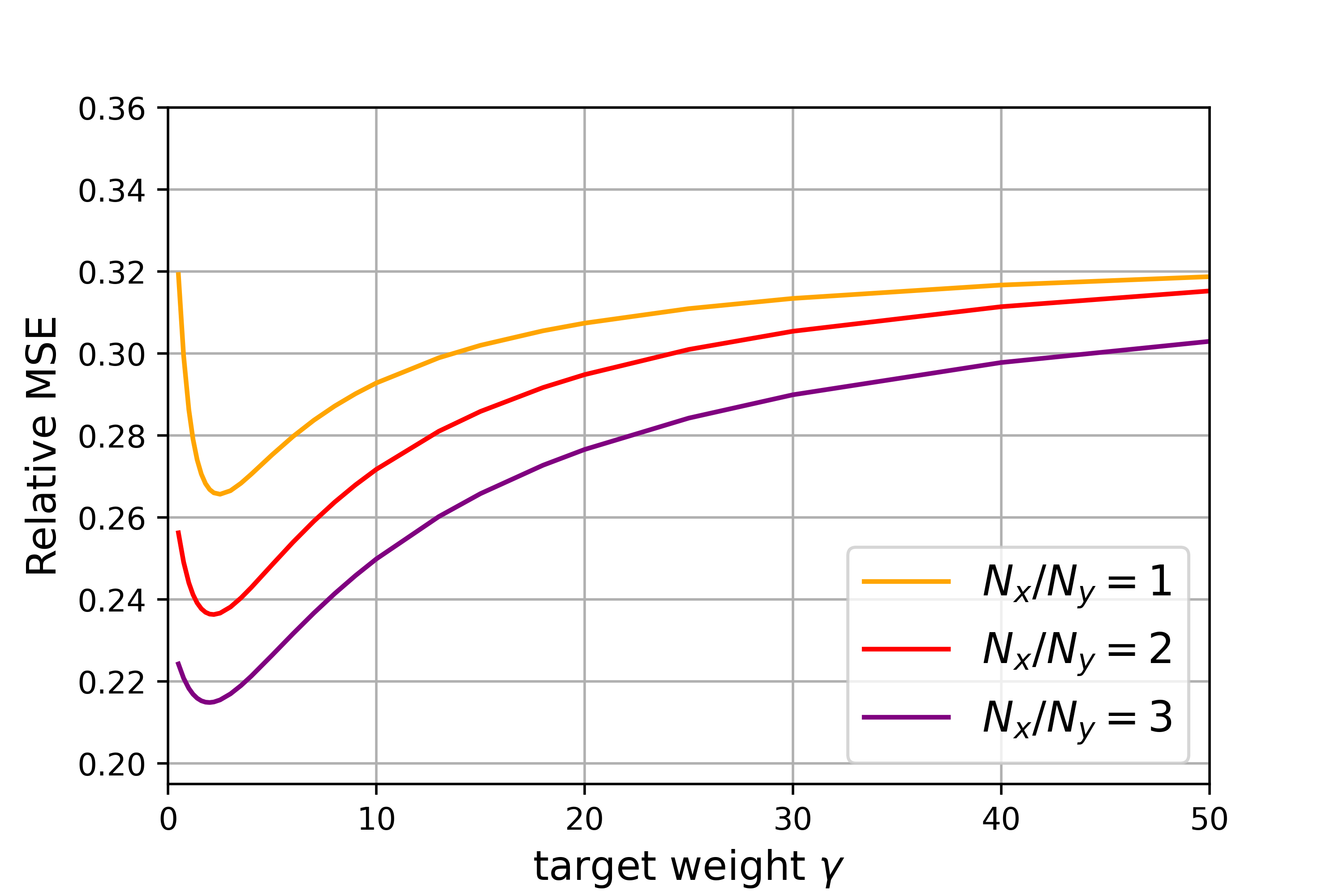

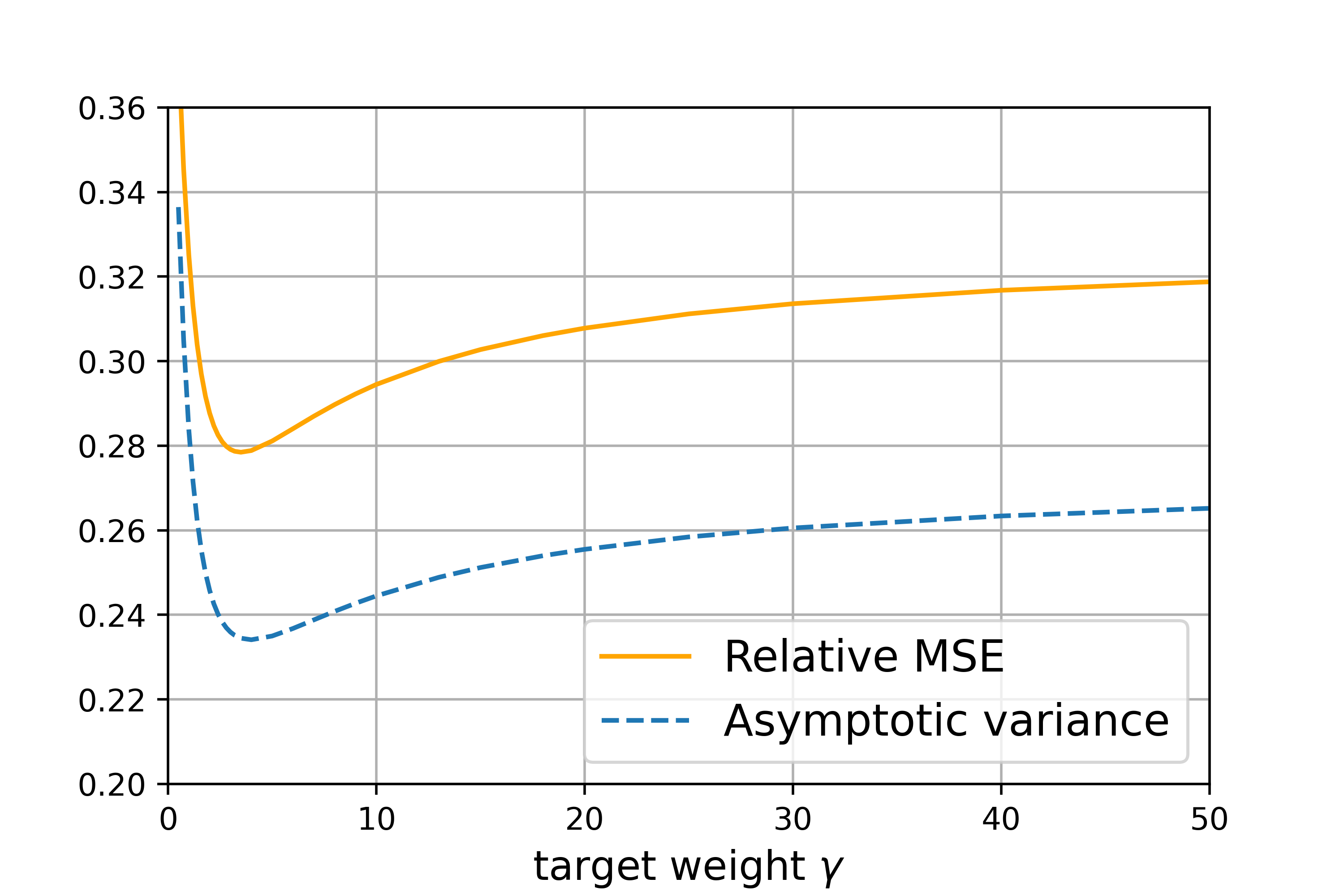

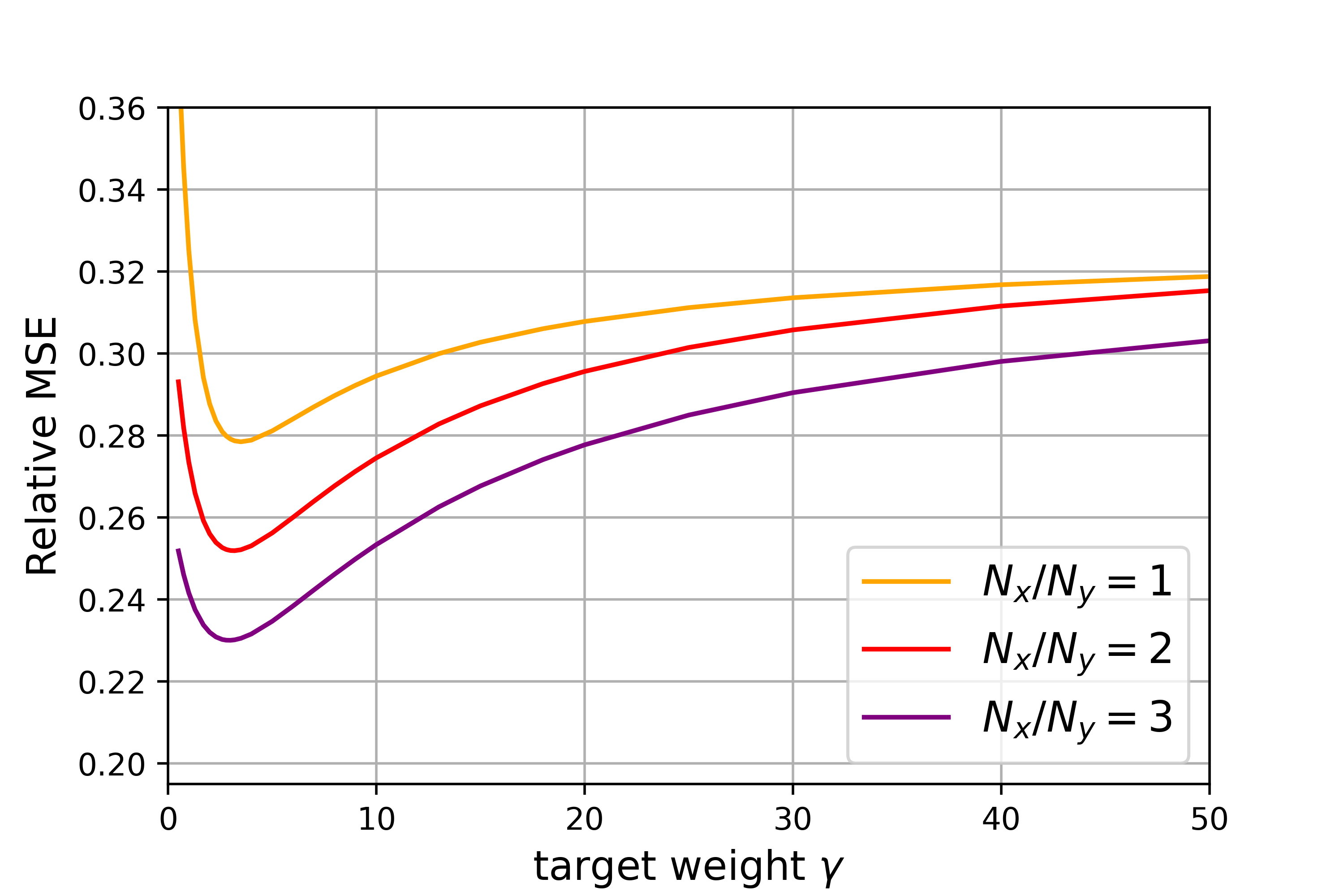

These figures show the relative MSE of the estimated common components of all entries in . The data generating process and the observation pattern follow the example described in Section 3.2. Specifically, the factors, loadings, and errors are generated from normal distributions with mean zero and and , , and observation probability . For the subplots in the first row, we set . We run 200 simulations for each setup.

We illustrate the efficiency effect of this simple model in a simulation. Figure 2(c) shows the relative mean squared error (relative MSE) of the estimated common components and the theoretical asymptotic covariance averaged over all entries in as a function of . We consider different combinations of the noise ratio and the dimension ratio for this one-factor example.777Section 7 presents a comprehensive simulation analysis and provides further details for the simulation setup, including the formal definition of relative MSE.

There are three main takeaways from Figure 2(c). First, and most importantly, the target weight that minimizes the relative MSE equals the optimized that minimizes the asymptotic variance. Hence, we can use the inferential theory as a guidance for selecting the target weight . We will further elaborate on the optimal selection in Section 5. Second, we confirm that the optimized only varies with , but not in this missing at random example. Third, the effect of optimizing is larger if panel and are more different in terms of noise and dimension. In all cases, PCA on only (target PCA with ) or on only (target PCA with ) is not optimal. The difference in relative MSE between target PCA with the optimized and the corner case of PCA on increases with and (i.e., the information in is more useful). The difference in relative MSE between target PCA with the optimized and the corner case of PCA on only increases with and (i.e., the information in is less useful).

In summary, the consistency and efficiency effects combined provide the protocol for selecting . First, we select the rate of as to ensure consistency under general conditions. In the second step, we select the scaling positive constant to minimize the asymptotic variance of the common component to ensure an efficient estimation.

4 Assumptions

In this section, we lay out the assumptions on the observation patterns of and the approximate factor models on both and . First, we introduce the assumptions on the observation pattern.

Assumption G2 (Observation pattern).

-

1.

The observation matrix is independent of the factors and idiosyncratic errors .

-

2.

Let be the set of time periods when both units and of are observed. For any given observation matrix , there exists a positive constant such that for all . Let and . For any , and are positive constants bounded away from 0. Furthermore, the number of observed units in at any time period is proportional to , i.e., there exists a positive constant such that for all .

Assumption G2 allows for very general observation patterns. The observation matrix can depend on the cross-sectional information, for example, the factor loadings or time-invariant observed covariates of the units. For the purpose of identification, Assumption G2 rules out the dependence between and . Note that the time and cross-section dimensions are symmetric in the estimation of common components. Therefore, the symmetric case where depends on but is independent of is allowed by swapping the roles of and in the estimation of the factor model. We assume that is independent of , which is conceptually similar to the unconfoundedness assumption in Rosenbaum and Rubin (1983).

In Assumption G2, we assume that the number of time periods, for which any four units are simultaneously observed, grows at the order of . This assumption implies that every entry in the covariance matrix can be consistently estimated at the rate , and ensures that the asymptotic variances of the estimated factors, loadings and common components from Target-PCA are well-defined. In Appendix C, we generalize Assumption G2 to allow to grow sub-linearly in . This does not change the conceptual arguments, but leads to a more complex notation.

We assume that both, and , follow an approximate factor model similar to Bai (2003). We allow for non-trivial time-series dependency of factors, and non-trivial cross-sectional dependency of loadings in , in , and between and . In addition, the idiosyncratic errors can be weakly correlated in , , and between and , in both the time-series and cross-sectional dimensions. The asymptotic distributions are based on general martingale central limit theorems. However, we make a key relaxation for the factor model relative to Bai (2003). Some factors in are allowed to be weak and only affect a small subset of units in . However, those factors have to be strong in in order to identify them from with a properly chosen (as suggested in Section 3).

The assumptions for the general factor model are stated in Assumptions G3 and G4 in Appendix A. They are delegated to the Appendix as most elements are standard, but fairly technical. Our consistency result in Theorem 1 and asymptotic distribution result in Theorem 2 are derived under Assumptions G2, G3 and G4.

We use the simplified model in Example 1 to illustrate how our factor model generalizes the conventional approximate factor models. It allows us to highlight the relaxation of weak factors. Appendix B shows how our main results are simplified for this example and shows that this example is a special case of our general framework.

Example 1 (Simplified factor model).

There exists constant such that

-

1.

Factors: and for any

-

2.

Loadings: , where is positive semidefinite. and the loading of the -th factor , where is positive definite and the Bernoulli random variable is independent in with for some . Furthermore, , , , and is positive definite. For any and is positive definite.

-

3.

Idiosyncratic errors: , .

-

4.

Independence: and are independent.

The main difference to the conventional factor models is the loadings, while the factors and errors capture the stylized properties in a usual factor setup. The simplified model in this example assumes that all observations are i.i.d. Allowing for more complex dependencies as in our general model, does not change the arguments, but makes the notation more complex. The key element is the strength of the factors measured by their loadings. Specifically, we measure the strength of the factors by the fraction of units in that are affected by the corresponding factor. The error terms are non-systematic with bounded eigenvalues in the covariance matrix.

The assumptions on the loadings account for three cases of factor strength in . First, if is bounded away from as grows, then the -th factor is a strong factor in . Second, if decays to but is nonzero as grows, then the -th factor is a weak factor in . Third, if is for all , then does not contain the -th factor. Note that can be rank deficient, implying that the loadings of some factors can be zero for units in . However, our assumption on rules out the case of weak factors in as the estimation of weak factors in is not our objective. We assume that is positive definite to ensure that each factor in is strong in at least one of the two panels and . Specifically, weak factors in are strong in . Hence, all factors can be identified with target-PCA with a properly chosen .

The loading assumption also imposes assumptions on the missing pattern in to identify all factors when combining the partially observed and . More specifically, the second-moment matrix does not need to be full rank in Assumption S1.2, which relaxes the full-rank assumption of in Xiong and Pelger (2023). However, we assume that is positive definite, so that target-PCA can identify all factors from and partially observed .

We assume that the number of factors can be consistently estimated. Given a consistent estimator for the number of factors, we can treat as known. After selecting at the rate for some positive scaling constant , the estimation of the number of factors from the weighted concatenated panel is the same as in Xiong and Pelger (2023). Hence, given the various bounds and expansions derived in this paper, it seems possible to extend the estimator for the number of factors developed in Bai and Ng (2002) to our case of general missing values. A promising alternative is to use cross-validation arguments. However, this is non-trivial for complex missing patterns that can depend on the factor model itself. In summary, given our analysis and selecting at the right rate, we can transform the problem of estimating the number of factors into a familiar setup. Furthermore, in our empirical analysis, we show that our estimator can be robust to the number of factors once is selected appropriately.

5 Inferential Theory

In this section, we provide the asymptotic results of the estimated factor model from target-PCA under general assumptions on the approximate factor model and missing patterns. We present the consistency result in Section 5.1 and asymptotic normality results in Section 5.2.

5.1 Consistency

The loadings and factors can be consistently estimated only if is properly chosen. The consistency result is an important intermediate step to show the inferential theory in Section 5.2.

Theorem 1.

Let and suppose that . Under Assumptions G2 and G3, for :

-

1.

If for some positive constant , then and are positive definite. It holds that

(5) (6) where . This implies that the estimated loadings and common components of are consistent.

-

2.

Under Assumption G1, if and are not of the same order, then is not positive definite when . If is not positive definite, then does not converge at the rate and can be inconsistent for the factors that are strong in but not in .

Theorem 1 states the consistency effect of and generalizes Proposition 1 to general factor models. According to Theorem 1, choosing with some positive constant ensures that factors, loadings, and common components of can be consistently estimated up to a rotation matrix . The convergence rate is at the smaller of and . This rate is the same as the convergence rate in Bai and Ng (2002) that applies PCA to when all factors are strong in . This rate makes sense for target-PCA: When we up-weight by a rate of , the error from is always a leading term in target-PCA.

If is not selected at the right order, the estimates of the factors that are strong in , but not in , are inconsistent unless stronger assumptions are imposed. Specifically, if for some and , then the consistency requires , that is, a larger , analogous to Assumption A4 in Bai and Ng (2023). However, this assumption is not required if is chosen at the order of .

5.2 Asymptotic Normality

Based on the consistency results in Theorem 1, we develop the inferential theory for target-PCA in this section. Theorem 2 shows the asymptotic distribution of estimated factors, estimated loadings of , and estimated common components of with target weight for every positive scaling constant in target-PCA under general assumptions. We show the asymptotic distribution of because the factor model and common components of are of our primary interest. The asymptotic distribution of can be shown analogously.

Theorem 2.

Define . Suppose that and for some positive constant . If the eigenvalues of are distinct, then under Assumptions G2, G3 and G4, as we have for each and :

- 1.

-

2.

For and ,

- •

-

•

Case 2: Suppose some factors in are weak factors in . Let be the weak factors in , and let be the remaining strong factors in . For simplicity of notation, we assume that the loadings of the weak factors are asymptotically orthogonal to the loadings of the strong factors . The asymptotic distribution of the estimated weak factors corresponding to is

(9) where , , is the rate at which grows,

, is defined in Assumption G4.7, and are respectively the diagonal blocks of and corresponding to the weak factors.888The asymptotic distribution of the estimated strong factors is where is the diagonal block of corresponding to the strong factors .

-

3.

For and , the asymptotic distribution of the estimated common components of is

(10) where

, and function is defined in Assumption G4.8.

The factors, loadings, and common components are asymptotically normally distributed. The asymptotic variance differs from the conventional PCA in Bai (2003) in three aspects. First, the asymptotic variances , and depend on (or equivalently when ). This will be important, as we will use it as the criteria to select the scale of . Second, in the case of missing data, we have additional correction terms to capture the additional uncertainty due to missingness. These correction terms follow the same structure and arguments as in Xiong and Pelger (2023). Without missing data, the correction matrices in the variance disappear. Third, as shown in Theorem 2.2, the strong and weak factors in have different convergence rates.999The estimated weak factors have faster convergence rates than the estimated strong factors . This is a consequence of growing at a smaller rate than , which implies that grows at a larger rate than . This result might seem to be counterintuitive at first glance, but makes sense after a careful analysis of the factor estimation errors. Note that the weak factors are essentially estimated from . Their estimation errors are dominated by the cross-sectional average of the errors of . In contrast, the strong factors are mainly estimated from and their estimation errors are dominated by those of , which then converge to zero at a slower rate as has fewer units than . The asymptotic distribution of the estimated common components is dominated by that of the strong factors in , as strong factors have a slower convergence rate than weak factors. Therefore, the two cases in Theorem 2.2 lead to the same case in Theorem 2.3. Importantly, this separation between strong and weak factors does not affect the asymptotic distribution of the estimated common components of . Hence, the asymptotic variance of the common components allows us to select an efficient target weight independent of the factor strength.

The distribution results of Theorem 2 simplify under Example 1, and we can provide explicit expressions for the asymptotic variances. Appendix B shows the analytical expression of the asymptotic variances under the simplified factor model, which allows us to gain intuition on how affects the efficiency of the estimation. The asymptotic variances depend on the following key quantities: the target weight , the noise ratio (NR) , the dimension ratio (DR) and the dependency structure in the missing pattern. We illustrate this dependency and the effect on the optimal choice of with a simulation example based on the model in Example 1 and different observation patterns.

We aim to select the optimized as the efficient target weight for the common components. The numerical examples in Table 1 illustrate how the optimized that minimizes depends on the observation pattern, noise ratio and dimension ratio, in a one-factor model. The fraction of observed data in varies between 60%, 75% and 90% with the four missing patterns: missing-at-random, block-missing, staggered-missing and mixed-frequency. The dimension ratio is either or 4, and the noise ratio varies between 0.25, 1 and 4.

NR=0.25

NR=1

NR=4

NR=0.25

NR=1

NR=4

60%

0.25

1.00

4.00

0.25

1.00

4.00

75%

0.25

1.00

4.00

0.25

1.00

4.00

90%

0.25

1.00

4.00

0.25

1.00

4.00

![[Uncaptioned image]](/html/2308.15627/assets/fig/thm/block.png) 60%

0.61

1.75

4.25

1.95

5.09

7.00

75%

0.42

1.53

4.35

1.06

3.62

6.12

90%

0.28

1.15

4.18

0.40

1.62

4.61

60%

0.55

1.96

4.66

1.69

5.52

7.84

75%

0.39

1.47

4.35

0.93

3.26

5.87

90%

0.28

1.13

4.13

0.40

1.58

4.51

60%

0.61

1.75

4.25

1.95

5.09

7.00

75%

0.42

1.53

4.35

1.06

3.62

6.12

90%

0.28

1.15

4.18

0.40

1.62

4.61

60%

0.55

1.96

4.66

1.69

5.52

7.84

75%

0.39

1.47

4.35

0.93

3.26

5.87

90%

0.28

1.13

4.13

0.40

1.58

4.51

![[Uncaptioned image]](/html/2308.15627/assets/fig/thm/mixed_fre_pattern.png) 60%

0.35

1.72

4.41

0.99

4.43

6.89

75%

0.35

1.41

4.26

0.79

3.00

5.64

90%

0.30

1.15

4.10

0.48

1.78

4.60

\floatfoot

This table reports the optimized for different missing patterns, dimension ratios and noise ratios (NR) . In this table, the optimized equals multiply by the efficient scaling obtained by minimizing in Corollary 1. The figures on the left show the observation patterns, with the shaded entries indicating the missing entries. We set and the fraction of observed entries to and . We generate a one-factor model where factors, loadings, and errors are drawn from normal distributions with . We let and for , for , and and for . The missing patterns in this table are generated as follows: (a) Missing uniformly at random: Entries are independently observed with probability . (b) Block-missing pattern: fraction of randomly selected units are missing from time . (c) Staggered treatment pattern: All units are in the control group for . Starting from time fraction of randomly selected units are in the treated group at time . (d) Mixed-frequency observation: Entries in the first half of the units are simultaneously observed at every time period and entries in the second half of the units are simultaneously observed at every time period. For , and ; for , and ; for , and .

60%

0.35

1.72

4.41

0.99

4.43

6.89

75%

0.35

1.41

4.26

0.79

3.00

5.64

90%

0.30

1.15

4.10

0.48

1.78

4.60

\floatfoot

This table reports the optimized for different missing patterns, dimension ratios and noise ratios (NR) . In this table, the optimized equals multiply by the efficient scaling obtained by minimizing in Corollary 1. The figures on the left show the observation patterns, with the shaded entries indicating the missing entries. We set and the fraction of observed entries to and . We generate a one-factor model where factors, loadings, and errors are drawn from normal distributions with . We let and for , for , and and for . The missing patterns in this table are generated as follows: (a) Missing uniformly at random: Entries are independently observed with probability . (b) Block-missing pattern: fraction of randomly selected units are missing from time . (c) Staggered treatment pattern: All units are in the control group for . Starting from time fraction of randomly selected units are in the treated group at time . (d) Mixed-frequency observation: Entries in the first half of the units are simultaneously observed at every time period and entries in the second half of the units are simultaneously observed at every time period. For , and ; for , and ; for , and .

This numerical example illustrates three points. First, the optimized can substantially deviate from the naive concatenating weight 1, even when the dimensions of and are the same. In particular, for complex missing patterns, the optimized target weight can deviate substantially from equally weighting the panels. Second, when observations are missing at random, the optimized only depends on the noise NR, but not on the dimension ratio or fraction of observed entries , confirming Proposition 2 in the illustration of the efficiency effect. However, for more complex observation patterns, the optimized can depend on , , and other quantities related to the observation pattern. Specifically, the optimized generally increases with and , implying that when the number of observations (or effective sample size) on is small compared to , the optimized increases to balance the relative contributions of the two panels. Third, the optimized grows with a larger dependency in the missing pattern. For the four observation patterns considered in Table 1, the dependency between the entries of is generally the highest for the block-missing pattern, followed by the staggered treatment pattern, then the mixed-frequency pattern, while missing-at-random has the lowest dependency. A higher dependency implies a smaller effective sample size in and hence a larger .

One application of our asymptotic distribution theory is to test causal effects. The fundamental problem in causal inference is that we observe an outcome either for the control or the treated data, but not for both at the same time. The unknown counterfactual of what the treated observations could have been without treatment can be naturally modeled as a data imputation problem. The same arguments as in Xiong and Pelger (2023) for how to use the results for causal inference apply to target-PCA. We can test in an analogous way for point-wise treatment effects that can be heterogeneous and time-dependent under general adoption patterns where the units can be affected by unobserved factors. Importantly, by optimally leveraging auxiliary data, we allow for more general adoption patterns and more precise estimates of the counterfactual outcomes.

5.3 Selection of Target Weight

As we have seen, selecting appropriately is crucial for the consistent and efficient estimation of the latent factor model on . We suggest a two-stage approach for choosing based on our inferential theory.

In the first stage, we select to consistently estimate the latent factor model. Based on Theorem 1, we can consistently estimate all the factors and loadings using target-PCA with . In the second stage, we estimate the asymptotic variance of the common component using the estimated factor model from the first stage and the inferential theory in Theorem 2 and Corollary 1. We then select the scaling constant to achieve efficiency by minimizing a linear combination of the estimated . If our goal is to estimate all common components as precisely as possible, then the objective function is to minimize . This is the objective that we use in our applications. If we want to impute the missing entries in as precisely as possible, then an appropriate objective function would be to minimize .

Generally, cross-validation could be an alternative approach for selecting . The idea of a cross-validation approach is to mask some observed entries in and select the value of that can most precisely estimate these masked out-of-sample entries. The challenge lies in how to mask the observed entries, and an appropriate implementation is more complicated than what it might appear to be. In particular, some naive masking schemes, such as random masking, may not be appropriate if the actual missing pattern is more complex. Intuitively, the masking should replicate the missing pattern, in order to ensure that the imputation errors of the masked entries can (unbiasedly) estimate the imputation errors of the missing entries in (if imputing missing entries in is our main goal). However, estimating the propensity of missingness is challenging and can be sensitive to the specification of a propensity model. In addition, the observation pattern can depend on the latent factor model itself, which further complicates the estimation. Our selection criterion based on the inferential theory avoids these issues.

6 Extensions

6.1 Auxiliary Data Sufficient to Estimate All Factors

So far, we have focused on the important setting where the auxiliary data is not sufficient to estimate all the factors for the target , which is assumed in Assumption G1. A simpler case is where already contains all the information to learn the factors in , that is, all the factors in are strong in . This is a special case of our more general analysis, where we can consistently estimate the factors by applying PCA to and we would only use target-PCA to achieve higher efficiency. Theorem 2 applies with minor modifications.

For this case, if , then choosing with any constant is equivalent to applying PCA on , which has the convergence rate of . Here, choosing is sub-optimal, since it up-weights and thus slows down the convergence rate of the estimated factors to . If with bounded away from 0, then it is beneficial to include the target panel in the estimation of factors to improve the efficiency. Specifically, we can select the optimized based on the asymptotic normality results similar to Theorem 2.

This setting is relevant when the target panel has a low-frequency observation pattern with no available information in for some time periods. If contains all the necessary information to estimate the latent factors in , then we can accurately impute the value of in the periods with no observations and, hence, obtain an imputed target panel with higher frequency observations.

We recommend the choice of target weight with a positive constant from the main setting for robustness. Even in the case where all relevant factors are strong in , selecting ensures consistent estimation. Importantly, this rate also guarantees consistency, when not all factors can be estimated from . In practice, we do not know if all factors for are strong factors in . In many applications, might not be selected in a targeted way, and hence it is likely that factors needed for can be missing or weak in . The selection procedure in Section 5.3 provides a robust solution.

6.2 Finite Cross-Sectional Dimension of Target Data

So far, we have focused on the case where . In some practical applications, may be finite (Huang, Jiang, Li, Tong, and Zhou, 2022). Our results can be extended to the case of finite with minor technical modifications.101010We need to modify the definition of in Assumption S2.3 to , when is finite. Specifically, we consider the choice of in two different settings depending on the nature of units in .

In the first setting, the units in are similar to the units in , and the idiosyncratic noise level in and are at the same scale, that is, . For this case, if all the factors in can be identified by applying PCA to , then selecting (i.e., PCA on ) is optimal. This is the degenerate case that asymptotically does not require for target-PCA.

In the second setting, units in are (weighted) averages of units, where is much larger than and can be of the same order as . An important example is when are the principal components from another panel. In this case, if , then we should choose , such that target-PCA can identify the factors in that are either weak or nonexistent in .111111This case is the same as choosing for the consistency effect, that is, our general rule for selecting the rate of still applies.

The following two propositions formalize the above discussion about choosing in each of the two different settings.

Proposition 3.

6.3 Multiple Panels

Target-PCA can be generalized to the setting with multiple auxiliary panels or/and multiple target panels , where and are the numbers of auxiliary and target panels.

In the case of multiple auxiliary panels , we can combine all auxiliary panels and the target panel into one panel with weights for the auxiliary panels

and apply our proposed estimator in Section 2.4 to . If , then the problem collapses to the setup in the main setting, and selecting the target weight as is the same as choosing the source weight as . Based on our previous discussion, we should choose for some positive constant , where is the number of units in . If there are multiple auxiliary panels, then the natural generalization is to choose for any and some positive constant . Such a choice of accounts for the case where different auxiliary panels may have different sets of factors that are useful for identifying the factors in (consistency effect), and may have different idiosyncratic noise levels (efficiency effect).

In the case of multiple target panels , we can use a sequential approach for estimating the factor model and imputing missing values in each target panel. Concretely, we first apply target-PCA to and , and impute the missing observations in . Second, we treat and the imputed panel as two auxiliary panels, and combine them with to estimate the factor model and impute missing values in . We repeat this procedure until the factor model is estimated and missing values are imputed for all the targets. Essentially, this sequential approach is conceptually the same as target-PCA with only one target panel, but with a more complicated notation.

6.4 Anchored Time Series

So far, all information for the factor model and the data imputation was based on the cross-sectional dependency in the contemporaneous outcomes in and . However, in the case of persistent time series, the prior realizations in can provide useful information for imputing missing entries. We propose an extension of target-PCA that takes advantage of prior realizations and the contemporaneous dependency structure. It can be interpreted as anchoring the imputed values around the prediction of a time-series model and correcting them with the innovations around the time-series model estimated from the contemporaneous auxiliary data.

We focus on the practically relevant case of low-frequency data in , which is combined with high-frequency supplementary data . In this case, the contemporaneous low-frequency outcomes in are not sufficient to impute the higher frequency missing values. As a concrete example, we refer to our empirical study, where we consider a panel of annually observed macroeconomic time series, while is a panel of monthly observed supplementary data. Many of these macroeconomic time series are highly persistent, and hence their differenced time series fluctuate around their mean value. Hence, the prior realizations of these time series can serve as anchor points.

A simple modification of target-PCA allows us to include prior values as anchor points, while the formal theoretical results continue to hold. Concretely, we replace missing entries in by their most recent observed values, and then apply target-PCA as before. For example, for yearly observed , we only observe entries in January, while observations from February to December are completely missing. In this case, we construct the anchored time series by filling in the missing entries from February to December with the observations in January of the corresponding year. This is a valid approach, if the common component based on prior factor realizations is an unbiased estimator of the common component in the next period. This is the case under the assumption that the factors have constant means, while errors have zero means. Under this assumption, the consistency result of Theorem 1 and the asymptotic distribution of Theorem 2 continue to hold. In particular, the optimal choice of follows the same arguments as for the conventional target-PCA.

Intuitively, the target weight implies a weighted average between the estimate of the common component of from the last period and the common component estimated on from the current period. Without the contemporaneous observations in or past values of , we cannot make any statements about the higher frequency observations in . The prior value of the common component of can be a noisy estimate of the next period’s value, and hence benefits from the cross-sectional contemporaneous information in to correct the variation and reduce the variance. The weight on the anchored panel could be interpreted as a prior for the past observation. If we put no weight on , we would simply use the prior common component to impute the missing values. In the other extreme case, where we put all weight on , we only use the factor model in for imputation, but ignore the prior values. The optimal choice of minimizes the variance of the weighted average of these two extreme estimators.

The extension to more complex time-series models is beyond the scope of this paper, but the general logic still applies. The weight would imply a weighted average of a time-series model forecast of the common component and the contemporaneous realization of the common component based on auxiliary data.

7 Simulation

In simulations, we show the superior performance of our target-PCA method relative to benchmarks under a variety of settings. For comparison, we include the three natural benchmark methods that apply PCA either to , a simple concatenated panel of and , or and separately and combine those factors. These are naive estimation methods for a target panel with auxiliary data. In more detail, we compare the following estimators:

-

1.

T-PCA: Target-PCA with optimized selected as with minimizing .

-

2.

: PCA estimator of Xiong and Pelger (2023) applied only to (special case of target-PCA with ).

-

3.

: PCA estimator of Xiong and Pelger (2023) applied to the concatenated panel (special case of target-PCA with ).

-

4.

SE-PCA: Separately estimate factors from and with the method of Xiong and Pelger (2023), combine the two sets of factors and estimate loadings of the combined factors to impute missing values on .121212Note that there is no simple way to determine the number of factors extracted from and respectively. When the factor number is for other methods, we simply combine factors from and factors from in SE-PCA. Note that SE-PCA uses factors in total to estimate the common components and impute missing entries in . Therefore, SE-PCA is more likely to identify all the factors, but at the cost of an efficiency loss compared to other methods.

We generate data from a two-factor model and , where and We consider three missing patterns for target :

-

1.

Missing-at-random: Entries of are missing uniformly at random.

-

2.

Low-frequency observation: Entries in are observed at a lower frequency and only every second time-series observation is available.

-

3.

Missingness depends on loadings: Entries of are missing conditional on a unit-specific characteristic This means that units that are more exposed to the second factor are more likely to be missing in . In this case, we assume , that is, factor 1 is not included in .

The detailed description of observation patterns and data-generating processes is in Table 2.

Table 2 compares the performance of the four methods in estimating the common components of the target . Specifically, it reports the relative mean squared error (relative MSE) of the estimated common components of the observed, missing, and all entries in , which is defined as

where denotes the set of either observed, missing, or all entries in . The MSE for the observed values can be interpreted as an in-sample evaluation, while the MSE for the imputed values serves as an out-of-sample evaluation as it evaluates the model on data that was not used in the estimation.

| Observation Pattern | T-PCA | SE-PCA | |||

|---|---|---|---|---|---|

|

obs | 0.184 | 0.408 | 0.224 | 0.530 |

| miss | 0.182 | 0.414 | 0.220 | 0.564 | |

| all | 0.183 | 0.411 | 0.222 | 0.547 | |

| |

obs | 0.291 | - | 0.846 | 1.059 |

| miss | 1.029 | - | 1.119 | 1.104 | |

| all | 0.656 | - | 0.979 | 1.080 | |

![[Uncaptioned image]](/html/2308.15627/assets/fig/simulation_3.png) |

obs | 0.219 | 0.238 | 0.262 | 0.280 |

| miss | 0.252 | 0.293 | 0.287 | 0.356 | |

| all | 0.244 | 0.280 | 0.281 | 0.338 |

This table reports the relative MSE of T-PCA (our benchmark method), (PCA on ), (PCA on concatenated panel) and SE-PCA (separate PCA). The figures on the left show patterns of missing observations with each row representing the observation pattern for a specific time period, and the shaded entries indicating the observed entries. Bold numbers indicate the best relative model performance. We generate a two-factor model and the observation patterns are generated as follows: (a) Missing uniformly at random: , and entries of are missing independently with observation probability (b) Low-frequency observation: , and entries in are only observed every second time period. (c) Missingness depends on loadings: and define a unit-specific characteristic Entries are missing independently with observation probability if , and if We assume and run 200 simulations for each setup.

As shown in Table 2, target-PCA performs well under different observation patterns and dominates the other benchmarks. Our estimator has the smallest relative MSEs as compared to the three benchmark methods, whereas the three benchmark methods are either infeasible or inefficient in different settings. These results hold for the observed and imputed observations for all types of missing patterns.

In the case of missing-at-random, target-PCA has the smallest relative MSEs as compared to the three benchmark methods. This is the setting where all benchmark methods can identify all the factors in , but target-PCA is more efficient by appropriately using the information in the auxiliary panel. The gain is particularly large relative to using only or estimating the factors separately from and . Both cases have a much smaller effective sample size than that of target-PCA, leading to more than double of the relative MSE.

In the setting of low-frequency observations, target-PCA continues to dominate the benchmark methods. This is a particularly interesting case, as the panel is not sufficient for estimating the full factor model, and hence is not feasible. As estimating latent factors on is not feasible in some periods, SE-PCA degenerates to PCA on , and therefore the performance of SE-PCA solely depends on the auxiliary panel . When has a low signal-to-noise ratio (i.e., is large), SE-PCA can perform poorly. simultaneously uses the information in both and , and therefore performs the best among the three benchmark methods. Target-PCA further improves upon by efficiently weighting the two panels and .

Target-PCA also has the smallest relative MSE when missingness depends on the loadings. This setting can be viewed as endogenously missing data: The second factor has a weak signal on the observed entries of , but is important to model the missing data in . This setting is similar to, but more complicated than, our toy example in Section 3.1. The auxiliary panel only contains the second factor, but not the first one; target contains both of the two factors, but the second factor is relatively weak on the observed entries of because the missing pattern depends on the factor loadings of . In this setting, performs worse than target-PCA because can hardly detect the second factor using the observed entries in . performs worse than target-PCA mainly because does not properly weight the two panels to account for their differences in the idiosyncratic noise levels. SE-PCA also performs worse than target-PCA because each separate estimation is noisier than our combined estimation.