11affiliationtext: Department of Epidemiology, Harvard T.H. Chan School of Public Health, Boston, MA. 22affiliationtext: CAUSALab, Harvard T.H. Chan School of Public Health, Boston, MA. 33affiliationtext: Department of Biostatistics, Harvard T.H. Chan School of Public Health, Boston, MA. 44affiliationtext: Department of Biostatistics, Brown University School of Public Health, Providence, RI.

Assessing model performance for counterfactual predictions

Counterfactual prediction methods are required when a model will be deployed in a setting where treatment policies differ from the setting where the model was developed, or when the prediction question is explicitly counterfactual. However, estimating and evaluating counterfactual prediction models is challenging because one does not observe the full set of potential outcomes for all individuals. Here, we discuss how to tailor a model to a counterfactual estimand, how to assess the model’s performance, and how to perform model and tuning parameter selection. We also provide identifiability results for measures of performance for a potentially misspecified counterfactual prediction model based on training and test data from the same (factual) source population. Last, we illustrate the methods using simulation and apply them to the task of developing a statin-naïve risk prediction model for cardiovascular disease.

Keywords: causal inference, prediction model, treatment drop-in, transportability, model performance, machine learning

1 Introduction

Many common tasks in prediction modeling can be viewed as a form of counterfactual prediction. First, prediction models are often deployed in settings that differ from those in which they are trained and one of the ways settings may differ is in terms of treatment patterns after baseline [1]. For example, a model fit in a setting where 5% are treated over the follow up period may not produce valid predictions in a setting where 50% are treated and vice versa. Even when models are deployed in the same setting, treatment policies may change over time, affecting who is likely to be treated and leading to problems of “domain adaption” or “dataset shift” [2, 3]. These differences between training and deployment settings can cause the performance of models to degrade, particularly when, as is often the case, model predictors are themselves correlated with, or direct determinants of, treatment [4, 5, 6].

When faced with a change in treatment policy, ideally, one would re-train the model using data reflecting the current patterns of treatment in the target population where the model will be applied. Collecting the necessary data to re-train the model, however, may be inordinately expensive or time consuming. Absent sufficient resources or as a stop gap, one might consider using existing training data to tailor the model to target the expected outcome that would be observed were treatment to be administered as in the deployment setting [7]. Alternatively, one might want to estimate how poorly the existing model is likely to perform in the deployment setting, to determine whether additional data collection efforts are worthwhile. In either case, the research questions pertain to counterfactual predictions.

Second, there are instances in which the prediction question itself is inherently counterfactual. For instance, clinicians may use a model to counsel patients about their risk of disease if they were to remain untreated or to compare risks under alternative treatment strategies [8, 9]. In some circumstances, such as when data from a randomized trial are used to model conditional average treatment effects, this can be done without additional formalism [10, 11, 12, 13, 14]. In contrast, when training data are obtained from an observational study where treatment initiation over follow up is not strictly controlled by the investigators, the predictions most relevant to decision-making are counterfactual [15, 9].

In both instances, when treatment policies change across settings or when the prediction question is inherently counterfactual, we need methods for tailoring models to answer counterfactual prediction questions, when data on the full set of potential outcomes is not available. We also need performance measures that evaluate model performance in these new environments without assuming the prediction model is correctly specified. Here, we examine the conditions under which tailoring a model for counterfactual prediction is possible using training data alone. Under similar conditions, we also show that the counterfactual performance of the model may be estimated independently from the method used to fit the model and may be evaluated even if the model is misspecified. Performance measures can therefore be used to differentiate between better and worse-performing models or to quantify how badly a model is likely to perform in a new setting.

2 Set up and notation

Let be the outcome of interest, a vector of baseline covariates, and an indicator of treatment over the follow up period. We assume that data are obtained from a simple random sample from a target population in which treatment is initiated according to pattern . Covariates in include a set sufficient to control confounding of the treatment-outcome relationship () as well as additional predictors of the outcome (). Our goal is to build a prediction model for using only covariates which are a subset of , chosen based on their availability and predictive potential rather than on whether they can help control confounding (note that can include components of both and ). An example causal directed acyclic graph for this process is shown in Figure 1.

The data are randomly split into a training set of observations and a test set of observations, with . Let and be indicators of whether an observation is in the training set or test set respectively. As is customary, we use the training set to build a prediction model for the expected outcome conditional on covariates and, then use the test set to evaluate model performance. Our results, however, apply equally to existing prediction models or (directly measured) biomarkers, in which case splitting is not necessary. Let be a parametric model, indexed by parameter , and be the “fitted” model using parameter estimates . We allow for the possibility that model is misspecified. For a particular estimand such as , a model is correctly specified if there exists , where is the parameter space of , such that and the model is misspecified if no such exists. We use generically to denote densities.

To define counterfactual estimands of interest, let be the potential outcome under an intervention which sets treatment to . To keep our notation simple, here we focus on the case that treatment is time-fixed – it is initiated after baseline and sustained throughout or its effect is independent of duration. In Section B of the Appendix, we extend our setup to handle time-varying treatments. We also assume interventions on are deterministic, but extend to random and dynamic interventions in Section A.4 of the Appendix. These may be more relevant for some real world prediction tasks, for instance, when evaluating the performance of models in settings where treatment differences are stochastic. Finally, we also assume that there is no loss to follow up, but note that our results can be extended by recognizing censoring can be accommodated using the methods we proposed for time-varying treatment [16] for a hypothetical intervention to prevent loss-to-followup.

3 Estimands for assessing model performance

Our goal is to train a model for counterfactual prediction and determine the model’s performance. We posit a parametric prediction model for the expected potential outcome under intervention conditional on covariates , which we wish to estimate from the training dataset. The model may be misspecified, such as if, for instance, it is a model trained on another target such as the expected (factual) outcome in the source population .

To evaluate prediction model performance, a number of measures have been proposed in the prediction literature [17, 18, 19]. These measures generally compare fitted predictions and the observed outcomes via a distance function and associated sample statistic. For counterfactual predictions, however, model evaluation is more challenging because the potential outcome is not directly observed. Yet, as we will show, under certain conditions the expected value of the performance measure may still be identified from the observed data in the test set. An example performance measure of interest is

where the squared error loss quantifies the discrepancy between the potential outcome under treatment level and the model prediction in terms of the squared difference. In the main text, we focus on the mean squared error as the performance measure of interest . In the Appendix, we extend our results to the case where the measure is any member of a generic class of counterfactual loss functions (Section A.2) as well as more complex risk-based measures such as area under the receiver operating characteristics curve (AUC, Section E), which depends on paired observations, and the calibration curve (Section D), which is a functional. Importantly, all the measures considered are identifiable without assuming that the model is correctly specified.

4 Identifiability conditions

We will assume the following identifiability assumptions which have been described in more detail elsewhere [16, 20, 21].

-

A1.

Consistency. If , then

-

A2.

Conditional exchangeability.

-

A3.

Positivity. For all with positive density, i.e. ,

Consistency implies that observed outcomes among those with reflect potential outcomes under corresponding level of treatment. It would be violated if, for instance, there were multiple “hidden” versions of the treatment under consideration [22]. The exchangeability condition stipulates that treatment is conditionally independent of the potential outcome given covariates . Finally, the positivity condition implies that there is a positive probability of observed treatment level in all strata of .

5 Tailoring a model for counterfactual predictions

As we show in Appendix Section A.1, under the conditions above is identified by

| (1) |

or, equivalently, using an inverse probability weighted expression

| (2) |

The two expressions for suggest possible approaches for tailoring the model for counterfactual predictions using only the training data.

One approach, based on equation 1, is to subset to participants with corresponding treatment level in the training data and fit a model for the observed conditional , i.e. . Then when the desired predictors are a subset of , the covariates sufficient to ensure exchangeability, predictions are marginalized (standardized) over the covariates in that are not in . When the dimension of is small, this can be done nonparametrically; however, when is higher-dimensional, an additional modeling step will be required either (1) modeling the estimated as a function of , i.e. or (2) modeling the conditional density of given , i.e. . The resulting predictions will be consistent for provided all models are correctly specified. An alternative suggested in [7], would be to simulate samples from the model and fit a second stage model using only the subset of the predictors of interest. This is similar to the first standardization method above and has the advantage that the second stage model may be developed using an outcome with same support as the original .

A second approach, based on 2, is to fit a weighted model , using for instance weighted maximum likelihood, with weights equal to the probability of receiving treatment level conditional on covariates necessary to ensure exchangeability, i.e., sample analogs of . This is the basis for previously proposed methods for counterfactual prediction based on inverse probability of treatment weighting [23, 1]. Note that, as before, it is possible to specify a subset of predictors used in the prediction model as compared to the full set of covariates required for exchangeability which are only necessary for defining the weights , however a second marginalization or simulation step is not required. This means tailoring the model for counterfactual predictions using the weighting approach can be accomplished more easily using off-the-shelf software.

6 Assessing model performance

Using the same identifiability conditions, in Appendix Section A.2, we show the model performance measure is identifiable using data from the test set through the expression

| (3) |

or, equivalently, using an inverse probability weighted expression,

| (4) |

regardless of whether the model has been tailored to target or is correctly specified in general.

As before, the two expression suggest two different approaches for the estimation of model performance using the test data alone.

First, using the sample analog of expression (3), an estimator of the target MSE is

| (5) |

where is an estimator for the conditional loss and from the perspective of estimating may be considered a nuisance function. To keep notation simple, we suppress the dependency of on . When the dimension of is small it may be possible to use sample analogs of . In almost all practical cases though some form of modeling will be required; in these cases, is a consistent estimator for as long as the model for is correctly specified.

Next, using the sample analog of expression (4), an alternative weight-based estimator of the target MSE is

| (6) |

where is another nuisance function estimating the probability of receiving treatment level conditional on , i.e. . Again, when the dimension of is small it may be possible to use the sample analog of , but in most cases, it will have to be modeled. In these cases, is a consistent estimator of as long as the model for is correctly specified.

The conditional loss estimator (5) relies on correctly specifying the model for the conditional loss and the weighting estimator (6) relies on correctly specifying the model for the probability of treatment. In some settings, one estimator may be preferred over the other: when more is known about the mechanism for “assigning” treatment or when the outcome is very rare, the weighting estimator may be preferred [24, 25]; when the process that gives rise to the outcomes is well understood the conditional loss estimator may be preferred. In practice, however, both models may be difficult to specify correctly. Using data-adaptive and more flexible machine learning estimators for estimation of these nuisance models offers the possibility of capturing more complex data generation processes. These data-adaptive estimators generally have slower rates of convergence than the rates of parametric models and therefore will not yield asymptotically valid confidence intervals [26]. To address this challenge, we can use a doubly-robust estimator which combines models for the conditional loss and the probability of treatment , such as

| (7) |

As we show in Appendix section C, under mild regularity conditions [27], this estimator will be consistent if one of and is correctly specified. It also permits the use of machine learning or data-adaptive estimators that converge at rate slower than , thus allowing for more flexible estimation of the nuisance functions. This is due to the fact that the empirical process terms governing the convergence of involve a product of the estimation errors for and which converge under the weaker condition that only the combined rate of convergence for both nuisance functions is at least [26].

7 Model and tuning parameter selection

Up to this point, we have assumed that is a pre-specified parametric model and ignored any form of model selection (e.g. variable or other specification search) or data-adaptive tuning parameter selection, which may be the case when using an existing (validated) model. In many cases, however, analysts have to select between multiple models or perform a data-adaptive search through a parameter space for tuning parameter selection when developing a prediction model [19]. To avoid overfitting, analysts typically use methods such as cross-validation or the bootstrap to perform selection. These techniques rely on optimizing some measure of model performance, such as the MSE.

When performing model or tuning parameter selection for counterfactual prediction, the results from the previous sections suggest that the model performance measure should be targeted to the counterfactual performance if the intervention of interest were universally applied. For example, when using cross-validation for model selection the analyst splits the data into mutually exclusive “folds” and fits the candidate models using of the folds and estimates the performance of each in the held out fold. This process is repeated times where each fold is left out once. The final performance estimate is the average of the estimates and the model with best overall performance is selected (or, alternatively, the tuning parameter with the best performance). When performing counterfactual prediction, at each stage in the procedure the analyst should use modified performance measures such as those in section 6 above. Failure to do so, can lead to sub-optimal selection with respect to the counterfactual prediction of interest.

8 Simulation experiments

We performed two Monte Carlo simulation experiments to illustrate (i) the benefits of tailoring models to the correct counterfactual estimand of interest, (ii) the potential for bias when using naïve estimators of model performance such as the MSE, (iii) the importance of correct specification of the nuisance models when estimating counterfactual performance, and (iv) the properties of the doubly-robust estimator under misspecification of the nuisance models. We adapt data generation processes previously used for transporting models between settings under covariate shift [28, 29].

8.1 Experiment 1

We simulated treatment initiation at baseline based on the logistic model , where predictors are drawn from Uniform . Under this model, about 50% initiate treatment but those with higher values of are less likely to start treatment than those with lower values of . We then simulated the outcome using the linear model , where . We set the total sample size to 1000 and the data were randomly split in a 1:1 ratio into a training and a test set. In this simulation, . The full process may be written:

Our goal was to estimate a model in the same population where, contrary to fact, treatment was universally withheld, i.e. we targeted . Note that, for simplicity, in this case predictor variables are the same set necessary to control confounding . Under this data generating mechanism, the MSE under no treatment is larger than the MSE under the natural course and identifiability conditions 1-3 are satisfied. We considered two specifications of prediction models :

-

1.

a correctly specified linear regression model that included the main effects of and , i.e. .

-

2.

a misspecified linear regression model that only included the main effect of , i.e. .

For each specification, we also considered two estimation strategies: one using ordinary least squares regression (OLS) and ignoring treatment initiation and the other using weighted least squares regression (WLS) where the weights were equal to the inverse of the probability of being untreated. As discussed above the latter specifically targets the counterfactual estimand under no treatment. Finally, we considered two approaches for estimating the performance of the models in the test set: a naïve estimate of the MSE using observed outcome values, i.e.

and the inverse-probability weighted estimator from section 6. For the latter, we fit a correctly specified logistic regression model for , i.e. , in the test set to estimate the weights. Lastly, we also calculated the “true” MSE under intervention to withold treatment by generating test data under same process as above but setting the treatment to for everyone and then averaging across simulations.

| Model | Naïve | IPW | Truth |

| Correct | |||

| OLS | 2.9 | 3.6 | 3.6 |

| WLS | 5.5 | 1.0 | 1.0 |

| Misspecified | |||

| OLS | 16.8 | 17.5 | 17.5 |

| WLS | 19.5 | 15.0 | 15.0 |

-

•

Correct and misspecified refers to the specification of the prediction model . OLS = model estimation using ordinary least squares regression (unweighted); WLS = model estimation using weighted least squares regression with weights equal to the inverse probability of being untreated. Results were averaged over 10,000 simulations. The true counterfactual MSE was obtained using numerical methods.

Table 1 shows the results of the experiment based on 10,000 simulations. In general, correctly specified models yielded smaller average MSE than misspecified models. Comparing the performance of OLS and WLS estimation, when using , the naïve estimator of the MSE, OLS seemed to produce better predictions than WLS when correctly specified (average MSE of 2.9 vs. 5.5) as well as when misspecified (average MSE of 16.8 vs. 19.5). In contrast, when using , the inverse-probability weighted estimate of the MSE, WLS performed better than OLS both when the model was correctly specified (average MSE of 1.0 vs. 3.6) and when misspecified (average MSE of 15.0 vs. 17.5). For reference, in the last column we show the true counterfactual MSE that would be obtained if one had access to the potential outcomes (obtained via numerical methods). We found that the average of the inverse probability weighted estimator across the simulations was equivalent to this quantity for all specifications and for both OLS and WLS estimation. This suggests that only the modified estimators of model performance in section 6 are able to accurately estimate the counterfactual performance of the model. Indeed, under this data generation process, if one were to use the naïve estimator one might erroneously conclude that the OLS model is the better choice.

8.2 Experiment 2

In the previous experiment, we assumed the nuisance models for the MSE were correctly specified. We now consider estimation of model performance in the more likely case that nuisance models are misspecified. Using the results from Section E in the Appendix, we also estimate the area under the receiver operating characteristics curve (AUC). We simulated treatment initiation over follow up based on the logistic model , where is now a vector of predictors drawn from a 3-dimensional multivariate normal with mean vector and covariance matrix . This resulted in expected treatment initiation over follow up of 55%. We also simulated a binary outcome from a Bernoulli distribution with mean , implying an average probability of the outcome of 66% among the untreated and 32% among treated. Again, we set the total sample size to 1000 and randomly split the data in a 1:1 ratio into a training and a test set.

Our prediction model was a main effects logistic regression model fit in the training data, i.e. . This model was misspecified with respect to the true data generating process. We assessed the counterfactual performance of the model in an untreated population using the AUC and the MSE, which for a binary outcome is equivalent to the Brier score [30]. In general, positing a parametric model for may be difficult as the outcome is a squared difference. For binary outcomes, however, expanding the square shows that to estimate it is enough to estimate , which is the approach we used. To determine the effect of the specification of nuisance models and on performance estimates, we compared four estimators of AUC and MSE (, , , and ) using different combinations of correctly specified and misspecified models for and :

-

1.

Correct - main effects logistic regression model with linear and quadratic terms.

-

2.

Misspecified - main effects logistic regression model with linear terms only terms.

-

3.

Correct - main effects logistic regression model with linear and quadratic terms.

-

4.

Misspecified - main effects logistic regression model with linear terms only terms.

Finally, we also considered using more flexible estimation techniques for nuisance terms and . Specifically, we fit generalized additive models for both using the mgcv package in entering all covariates as splines using the default options in the gam function.

| MSE | AUC | |||||||

| Estimator | Mean | Percent | Mean | Percent | ||||

| Naïve | 0.207 | 0.176 | -0.140 | -2.1 | 0.742 | 0.491 | -1.335 | -5.4 |

| Correct | ||||||||

| CL | 0.212 | 0.333 | 0.015 | 0.2 | 0.783 | 0.767 | -0.045 | -0.2 |

| IPW | 0.212 | 0.517 | 0.011 | 0.2 | 0.782 | 1.258 | -0.062 | -0.3 |

| DR | 0.211 | 0.454 | 0.000 | 0.0 | 0.783 | 1.192 | -0.028 | -0.1 |

| misspecified | ||||||||

| CL | 0.212 | 0.333 | 0.015 | 0.2 | 0.783 | 0.767 | -0.045 | -0.2 |

| IPW | 0.221 | 0.358 | 0.316 | 4.7 | 0.762 | 0.876 | -0.699 | -2.8 |

| DR | 0.212 | 0.349 | 0.016 | 0.2 | 0.782 | 0.841 | -0.066 | -0.3 |

| misspecified | ||||||||

| CL | 0.217 | 0.356 | 0.194 | 2.9 | 0.777 | 0.803 | -0.224 | -0.9 |

| IPW | 0.212 | 0.517 | 0.011 | 0.2 | 0.782 | 1.258 | -0.062 | -0.3 |

| DR | 0.211 | 0.625 | 0.001 | 0.0 | 0.783 | 1.317 | -0.024 | -0.1 |

| Both misspecified | ||||||||

| CL gam | 0.213 | 0.348 | 0.052 | 0.8 | 0.782 | 0.800 | -0.063 | -0.3 |

| IPW gam | 0.214 | 0.422 | 0.075 | 1.1 | 0.778 | 1.032 | -0.181 | -0.7 |

| DR gam | 0.211 | 0.403 | 0.010 | 0.1 | 0.784 | 0.966 | -0.021 | -0.1 |

| Truth | 0.211 | 0.784 | ||||||

-

•

Average of estimates, estimated bias, estimated standard deviation (SD), and estimated relative bias for the naïve empirical, weighting (IPW), conditional loss (CL), and doubly robust (DR) estimators. is the number of observations in the test set. Here, is a model for and denotes a model for . Relative bias is calculated as . Correct and Misspecified refer to the nuisance models, or or both. In the final rows, gam indicates that a generalized additive model was used to estimate nuisance models. Results were averaged over 10,000 simulations.

Table 2 shows the results from experiment 2. As in the previous experiment, the naïve empirical estimators of the AUC and MSE were biased relative to the true counterfactual values with a relative bias of 2.1% and respectively. When all models were correctly specified, the weighting, conditional loss, and doubly robust estimators were all unbiased (absolute relative bias between 0.2% to 0.3%). When was misspecified, the weighting estimator was biased (relative bias of 4.7% and -2.8%) but the conditional loss and doubly robust estimator were unbiased (absolute relative bias of 0.2% to 0.3%). Under misspecification of , the conditional loss estimator was biased (relative bias of 2.9% and -0.9%), but the weighting estimator and the doubly robust estimator were unbiased (absolute relative bias of 0.0% to 0.3%). When both models and were misspecified all estimators, including the doubly robust estimator, were biased. Finally, when a more flexible generalized additive model was used to estimate both and , the doubly robust estimator was unbiased (absolute relative bias of 0.1%). Across all scenarios, the weighting estimator generally had the largest standard errors and the conditional loss estimator had the smallest standard errors.

9 Application to prediction of statin-naïve risk

We apply the proposed methods to evaluate the performance of two counterfactual prediction models targeting the statin-naïve risk of cardiovascular disease: that is the risk in the same population if, contrary to fact, statins had been withheld. We compare one model that was explicitly tailored for the counterfactual estimand of interest and a second that was not.

9.1 Study design and data

The Multi-Ethnic Study on Atherosclerosis (MESA) study is a population-based sample of 6,814 men and women aged 45 to 84 drawn from six communities (Baltimore; Chicago; Forsyth County, North Carolina; Los Angeles; New York; and St. Paul, Minnesota) in the United States between 2000 and 2002. The design, sampling procedures, and collection methods of the study have been described previously [31]. Study teams conducted five examination visits between 2000 and 2011 in 18 to 24 month intervals focused on the prevalence, correlates, and progression of subclinical cardiovascular disease. These examinations included assessments of lipid-lowering medication use (primarily statins), as well as assessments of cardiovascular risk factors such as systolic blood pressure, serum cholesterol, cigarette smoking, height, weight, and diabetes.

In a previous analysis, we used data from the MESA study to emulate a trial comparing continuous statin use versus no statins and benchmarked our results against those from published randomized trials. To construct a model of the statin-naïve risk, we then emulated a single arm trial in which no one started statins over a 10-year follow up period. To determine trial eligibility, we followed the AHA guidelines [32] on statin use which stipulate that patients aged 40 to 75 with serum LDL cholesterol levels between 70 mg/dL and 190 mg/dL and no history of cardiovascular disease should initiate statins if their (statin-naïve) risk exceeds 7.5%. Therefore, we considered MESA participants who completed the baseline examination, had no previous history of statin use, no history of cardiovascular disease, and who met the criteria described in the guidelines (excluding the risk threshold) as eligible to participate in the trial. The primary endpoint was time to atherosclerotic cardiovascular disease (ASCVD), defined as nonfatal myocardial infarction, coronary heart disease death, or ischemic stroke.

Follow up began at the second examination cycle to enable a “wash out” period for statin use and to ensure adequate pre-treatment covariates to control confounding (some were taken from the first cycle and others from the second). In the original analysis, we constructed a sequence of nested trials starting at each exam, however here for simplicity we limited our attention to the first trial. We used the questionnaire in examinations three through five to determine statin initiation over the follow up period. Because the exact timing of statin initiation was not known with precision, we estimated it by drawing a random month between the current and previous examinations (sensitivity analyses conducted in original study).

Of the 6,814 MESA participants who completed the baseline examination, 4,149 met the eligibility criteria for our trial emulation. There were 288 ASCVD events and 190 non-ASCVD deaths. For simplicity, here we dropped those lost to follow up and who first have competing events although in practice both can be accommodated in our framework for evaluating the performance of a counterfactual prediction model. For model training and evaluation, we further randomly split the dataset into training and test sets of equal size.

9.2 Model estimation and performance

We compared two prediction models: one that was explicitly tailored to the statin-naïve risk and a second that was not. Both models used the same regression specification with main effects of baseline predictors commonly used in cardiovascular risk prediction: age, sex, smoking status, diabetes history, systolic blood pressure, anti-hypertensive medication use and total and HDL serum cholesterol levels.

We tailored the first model for the statin-naïve risk using inverse probability of censoring weights. In the emulated single arm trial, statin initiation can be viewed as “non-adherence” which can be adjusted for by inverse probability weighting, therefore we censored participants when they initiated statins. To calculate the stablized weights, we estimated two logistic regression models: one for the probability of remaining untreated given past covariate history (denominator model) and one for probability of remaining untreated given the selected baseline predictors (numerator model). The list of covariates in the weight models are given in section F.1 of the Appendix. To create a prediction model for the statin-naïve risk, we used the estimated weights to fit a weighted logistic regression model conditional on the baseline predictors of interest.

For comparison, we fit a second traditional (factual) prediction model by regressing the observed ASCVD event indicator on the same set of baseline predictors, but ignoring treatment initiation over the follow up period. This approach targets the “natural course” risk (i.e., the risk under the statin initiation policies that prevailed at the time of the study) rather than the statin-naïve risk. We fit the model using standard logistic regression based on maximum likelihood.

To assess the performance of the models, we estimated the naïve and counterfactual MSE in the test set. For the latter we used the conditional loss, inverse probability weighting, and doubly robust estimators of the MSE. Models for the initiation of treatment and for the conditional loss were implemented as main effects logistic regression models. As in the simulation example, to estimate the conditional loss it is sufficient to model the probability of the outcome alone. To quantify uncertainty, we used the non-parametric bootstrap with 1000 bootstrap replicates.

| MSE | AUC | |||

| Estimator | Logit | Weighted Logit | Logit | Weighted Logit |

| Naïve | 0.069 | 0.072 | 0.710 | 0.708 |

| (0.003) | (0.003) | (0.013) | (0.014) | |

| CL | 0.086 | 0.085 | 0.719 | 0.727 |

| (0.005) | (0.004) | (0.015) | (0.015) | |

| IPW | 0.109 | 0.099 | 0.753 | 0.778 |

| (0.013) | (0.009) | (0.025) | (0.029) | |

| DR | 0.090 | 0.087 | 0.740 | 0.751 |

| (0.006) | (0.005) | (0.023) | (0.023) | |

-

•

The columns refer to the posited prediction model: Logit is an (unweighted) logistic regression model and weighted logit is a logistic regression model with inverse probability weights for remaining statin-free. The rows are the model performance estimates of the MSE and AUC. Naïve is the empirical estimator using factual outcomes (), CL is the conditional loss estimator (), IPW is the inverse probability weighting estimator (), DR is the doubly-robust estimator (). Standard error estimates are shown in parentheses obtained via 1000 bootstrap replicates.

9.3 Results

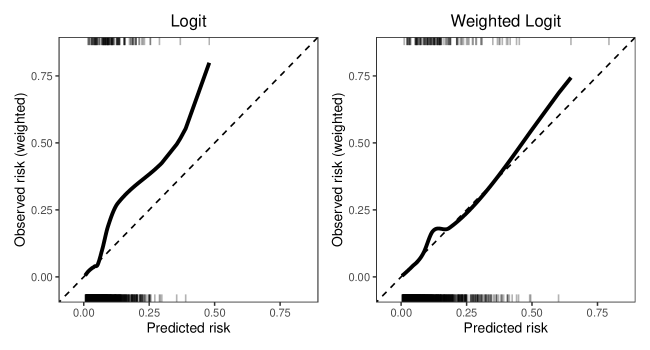

Table 3 shows estimates of the AUC and MSE and the associated standard errors in a hypothetical statin-naïve population for both prediction models using the naïve empirical, conditional loss, weighting, and doubly robust estimators. Across both measures, the conditional loss, weighting, and doubly robust estimators yielded estimates that were greater (30-50% for MSE, 3-10% for AUC) than those of the naïve empirical estimator, suggesting performance of both models in statin-naïve population is worse than in the source population. Of the three estimators of the statin-naïve performance, the weighting estimator had greater standard errors than the doubly robust estimator (by 10-100%) as well as the conditional loss estimator (by 60-160%). Consistent with the first simulation experiment, the inverse probability weighted logistic model, which was tailored to target the statin-naïve risk, performed worse in the source population, but had lower MSE and higher AUC values in the counterfactual statin-naïve population. There were sizeable differences (2-3 standard errors) in estimates of the MSE and AUC in the counterfactual statin-naïve population across the proposed CL, IPW, and DR estimators. All three should give equivalent results in expectation if models for the nuisance functions and are correctly specified. Their divergence suggests at least one (but possibly both) of the nuisance functions may be misspecified. Finally, drawing on the results in section D in the appendix, we estimate the counterfactual calibration of both prediction models in a statin-naïve population using a weighted loess estimator where the weights are based on inverse probability of remaining statin free. Figure 2 shows the results. As expected, the weighted prediction model, which was tailored to target the statin-naïve risk, was better calibrated than the unweighted model, which generally underestimated the counterfactual risk.

10 Discussion

Many practical prediction problems call for the development and evaluation of counterfactual prediction models, for example, when the treatment distribution changes between the time training data are obtained and when the model will be deployed, or when predictions are meant to inform decisions about treatment initiation. In this paper, we considered the setting when the counterfactual prediction model has to be developed using observational training data. We described how to estimate counterfactual prediction models and the conditions necessary to identify these models. Separately, we also discussed how to adjust common measures of model performance to estimate the performance of counterfactual prediction model. Importantly, results for performance measures were valid even when the prediction model is misspecified. A key insight was that performance measures that have not been tailored for counterfactual prediction will be biased. We also showed that performance can be assessed even if the prediction model itself is misspecified. We proposed estimators for these performance measures based on modeling the conditional loss, the probability of treatment, and a doubly robust estimator that can be used with data-adaptive estimators of either nuisance function.

We focused on measures of performance under a particular treatment policy. However, prediction models may instead target the estimation of conditional treatment effects, that is, comparisons between treatment regimes such as . In some cases, effects may be easier to communicate to end users or may be desirable to evaluate benefits versus harms of treatment initiation [12]. However, absolute means and risks are common outputs of existing prediction models. Several authors have proposed model performance measures for conditional average treatment effects which are identified under similar assumptions to our own [33, 34, 35, 36, 37]. From an estimation standpoint, methods for targeting the conditional average treatment effect and their performance have to balance the estimation of the conditional risk function for the outcome under different treatment levels with the estimation of the treatment effect function, with optimality depending on the relative smoothness of these functions [38].

Throughout, we did not assume that the covariates needed to satisfy the exchangeability assumption were the same covariates used in the prediction model. This is an important aspect of our work because in practice predictors are often chosen based on their availability in a clinical setting rather than what would be optimal from a causal (or even predictive) perspective [19, 39]. Moreover, our methods reflect the fact that confounding is a problem that needs to be adjusted for in the setting where the model is developed, whereas predictions often need to be optimized for the setting where the model will be applied (although as discussed below allowing the covariate distribution to differ between settings can introduce further subtleties).

One limitation of our approach is that it require that a set of covariates sufficient to ensure exchanageability can be identified at the time of training the model. Violations of this exchangeability condition can be examined in sensitivity analyses [40, 41], for example, to explore how violations of this assumption might affect estimates of model performance. Further work may also examine identification of counterfactual prediction models and their performance under alternative identifiability conditions.

In this work, we assumed that the distribution of predictors is the same in the training and deployment setting. In many cases, however, the covariate distributions are also likely to differ between settings [42, 43]. Like differences in treatment initiation, differences in covariate distributions may cause the performance of the prediction model to degrade, particularly when the model is misspecified. Methods for transporting prediction models from source to target populations which relate to our own have previously been proposed [43, 44, 45, 28, 46, 29] as have methods for transporting conditional average effects from trials to target populations with different covariate distributions [47, 48, 49, 50]. In future work, our results could be extended to allow for both differences in the distribution of treatment and the covariates between training and deployment settings.

References

- [1] Nan Geloven et al. “Prediction Meets Causal Inference: The Role of Treatment in Clinical Prediction Models” In Eur J Epidemiol 35.7, 2020, pp. 619–630 DOI: 10.1007/s10654-020-00636-1

- [2] Samuel G. Finlayson et al. “The Clinician and Dataset Shift in Artificial Intelligence” In N Engl J Med 385.3 Massachusetts Medical Society, 2021, pp. 283–286 DOI: 10.1056/NEJMc2104626

- [3] Adarsh Subbaswamy and Suchi Saria “From Development to Deployment: Dataset Shift, Causality, and Shift-Stable Models in Health AI” In Biostatistics 21.2, 2020, pp. 345–352 DOI: 10.1093/biostatistics/kxz041

- [4] Romin Pajouheshnia et al. “Accounting for Treatment Use When Validating a Prognostic Model: A Simulation Study” In BMC Med Res Methodol 17.1, 2017, pp. 103 DOI: 10.1186/s12874-017-0375-8

- [5] Rolf H. H. Groenwold et al. “Explicit Inclusion of Treatment in Prognostic Modeling Was Recommended in Observational and Randomized Settings” In J Clin Epidemiol 78, 2016, pp. 90–100 DOI: 10.1016/j.jclinepi.2016.03.017

- [6] Amanda Coston, Alan Mishler, Edward H. Kennedy and Alexandra Chouldechova “Counterfactual Risk Assessments, Evaluation, and Fairness”, 2020 DOI: 10.48550/arXiv.1909.00066

- [7] Barbra A. Dickerman et al. “Predicting Counterfactual Risks under Hypothetical Treatment Strategies: An Application to HIV” In Eur J Epidemiol 37.4, 2022, pp. 367–376 DOI: 10.1007/s10654-022-00855-8

- [8] Lijing Lin et al. “A Scoping Review of Causal Methods Enabling Predictions under Hypothetical Interventions” In Diagn Progn Res 5.1, 2021, pp. 3 DOI: 10.1186/s41512-021-00092-9

- [9] Peter Schulam and Suchi Saria “Reliable Decision Support Using Counterfactual Models” In Advances in Neural Information Processing Systems 30 Curran Associates, Inc., 2017 URL: https://proceedings.neurips.cc/paper/2017/hash/299a23a2291e2126b91d54f3601ec162-Abstract.html

- [10] Jeroen Hoogland et al. “A Tutorial on Individualized Treatment Effect Prediction from Randomized Trials with a Binary Endpoint” In Statistics in Medicine 40.26, 2021, pp. 5961–5981 DOI: 10.1002/sim.9154

- [11] David M. Kent, Ewout Steyerberg and David Klaveren “Personalized Evidence Based Medicine: Predictive Approaches to Heterogeneous Treatment Effects” In BMJ 363 British Medical Journal Publishing Group, 2018, pp. k4245 DOI: 10.1136/bmj.k4245

- [12] David M. Kent et al. “The Predictive Approaches to Treatment Effect Heterogeneity (PATH) Statement” In Ann Intern Med 172.1 American College of Physicians, 2020, pp. 35–45 DOI: 10.7326/M18-3667

- [13] Paul P. Glasziou and Les M. Irwig “An Evidence Based Approach to Individualising Treatment” In BMJ 311.7016 British Medical Journal Publishing Group, 1995, pp. 1356–1359 DOI: 10.1136/bmj.311.7016.1356

- [14] Issa J Dahabreh, Rodney Hayward and David M Kent “Using Group Data to Treat Individuals: Understanding Heterogeneous Treatment Effects in the Age of Precision Medicine and Patient-Centred Evidence” In International Journal of Epidemiology 45.6, 2016, pp. 2184–2193 DOI: 10.1093/ije/dyw125

- [15] Barbra A. Dickerman and Miguel A. Hernán “Counterfactual Prediction Is Not Only for Causal Inference” In Eur J Epidemiol 35.7, 2020, pp. 615–617 DOI: 10.1007/s10654-020-00659-8

- [16] Miguel A Hernán and James M Robins “Causal Inference: What If” Boca Raton: Chapman & Hall/CRC, 2020

- [17] Frank E. Harrell, Kerry L. Lee and Daniel B. Mark “Multivariable Prognostic Models: Issues in Developing Models, Evaluating Assumptions and Adequacy, and Measuring and Reducing Errors” In Statistics in Medicine 15.4, 1996, pp. 361–387 DOI: 10.1002/(SICI)1097-0258(19960229)15:4¡361::AID-SIM168¿3.0.CO;2-4

- [18] Douglas G. Altman and Patrick Royston “What Do We Mean by Validating a Prognostic Model?” In Statistics in Medicine 19.4, 2000, pp. 453–473 DOI: 10.1002/(SICI)1097-0258(20000229)19:4¡453::AID-SIM350¿3.0.CO;2-5

- [19] Ewout W. Steyerberg “Clinical Prediction Models: A Practical Approach to Development, Validation, and Updating”, Statistics for Biology and Health Cham: Springer International Publishing, 2019 DOI: 10.1007/978-3-030-16399-0

- [20] James Robins “A New Approach to Causal Inference in Mortality Studies with a Sustained Exposure Period—Application to Control of the Healthy Worker Survivor Effect” In Mathematical Modelling 7.9, 1986, pp. 1393–1512 DOI: 10.1016/0270-0255(86)90088-6

- [21] James Robins “A Graphical Approach to the Identification and Estimation of Causal Parameters in Mortality Studies with Sustained Exposure Periods” In Journal of Chronic Diseases 40, 1987, pp. 139S–161S DOI: 10.1016/S0021-9681(87)80018-8

- [22] Donald B. Rubin “Randomization Analysis of Experimental Data: The Fisher Randomization Test Comment” In Journal of the American Statistical Association 75.371 [American Statistical Association, Taylor & Francis, Ltd.], 1980, pp. 591–593 DOI: 10.2307/2287653

- [23] Matthew Sperrin et al. “Using Marginal Structural Models to Adjust for Treatment Drop-in When Developing Clinical Prediction Models” In Statistics in Medicine 37.28, 2018, pp. 4142–4154 DOI: 10.1002/sim.7913

- [24] James M. Robins, Steven D. Mark and Whitney K. Newey “Estimating Exposure Effects by Modelling the Expectation of Exposure Conditional on Confounders” In Biometrics 48.2 [Wiley, International Biometric Society], 1992, pp. 479–495 DOI: 10.2307/2532304

- [25] Leonard E. Braitman and Paul R. Rosenbaum “Rare Outcomes, Common Treatments: Analytic Strategies Using Propensity Scores” In Ann Intern Med 137.8 American College of Physicians, 2002, pp. 693–695 DOI: 10.7326/0003-4819-137-8-200210150-00015

- [26] Victor Chernozhukov et al. “Double/Debiased Machine Learning for Treatment and Structural Parameters” In Econom J 21.1 Oxford Academic, 2018, pp. C1–C68 DOI: 10.1111/ectj.12097

- [27] James Robins, Lingling Li, Eric Tchetgen and Aad Vaart “Higher Order Influence Functions and Minimax Estimation of Nonlinear Functionals” In Probability and Statistics: Essays in Honor of David A. Freedman 2 Institute of Mathematical Statistics, 2008, pp. 335–422 DOI: 10.1214/193940307000000527

- [28] Jon A Steingrimsson, Constantine Gatsonis, Bing Li and Issa J Dahabreh “Transporting a Prediction Model for Use in a New Target Population” In American Journal of Epidemiology 192.2, 2023, pp. 296–304 DOI: 10.1093/aje/kwac128

- [29] Samantha Morrison et al. “Robust Estimation of Loss-Based Measures of Model Performance under Covariate Shift”, 2022 arXiv: http://arxiv.org/abs/2210.01980

- [30] Glenn W. Brier “VERIFICATION OF FORECASTS EXPRESSED IN TERMS OF PROBABILITY” In Mon. Wea. Rev. 78.1 American Meteorological Society, 1950, pp. 1–3 DOI: 10.1175/1520-0493(1950)078¡0001:VOFEIT¿2.0.CO;2

- [31] Diane E. Bild et al. “Multi-Ethnic Study of Atherosclerosis: Objectives and Design” In American Journal of Epidemiology 156.9, 2002, pp. 871–881 DOI: 10.1093/aje/kwf113

- [32] Grundy Scott M. et al. “2018 AHA/ACC/AACVPR/AAPA/ABC/ACPM/ADA/AGS /APhA/ASPC/NLA/PCNA Guideline on the Management of Blood Cholesterol: A Report of the American College of Cardiology/American Heart Association Task Force on Clinical Practice Guidelines” In Circulation 139.25 American Heart Association, 2019, pp. e1082–e1143 DOI: 10.1161/CIR.0000000000000625

- [33] Alejandro Schuler, Michael Baiocchi, Robert Tibshirani and Nigam Shah “A Comparison of Methods for Model Selection When Estimating Individual Treatment Effects”, 2018 arXiv: http://arxiv.org/abs/1804.05146

- [34] Craig A Rolling and Yuhong Yang “Model Selection for Estimating Treatment Effects” In Journal of the Royal Statistical Society: Series B (Statistical Methodology) 76.4 Wiley Online Library, 2014, pp. 749–769

- [35] Yizhe Xu and Steve Yadlowsky “Calibration Error for Heterogeneous Treatment Effects”, 2022 arXiv: http://arxiv.org/abs/2203.13364

- [36] Mark J Laan and James M Robins “Unified Methods for Censored Longitudinal Data and Causality” Springer, 2003

- [37] Ahmed Alaa and Mihaela Van Der Schaar “Validating Causal Inference Models via Influence Functions” In Proceedings of the 36th International Conference on Machine Learning PMLR, 2019, pp. 191–201 URL: https://proceedings.mlr.press/v97/alaa19a.html

- [38] Edward H. Kennedy “Towards Optimal Doubly Robust Estimation of Heterogeneous Causal Effects”, 2022 arXiv: http://arxiv.org/abs/2004.14497

- [39] Amanda Coston, Edward H. Kennedy and Alexandra Chouldechova “Counterfactual Predictions under Runtime Confounding”, 2021 arXiv: http://arxiv.org/abs/2006.16916

- [40] James M. Robins, Andrea Rotnitzky and Daniel O. Scharfstein “Sensitivity Analysis for Selection Bias and Unmeasured Confounding in Missing Data and Causal Inference Models” In Statistical Models in Epidemiology, the Environment, and Clinical Trials, The IMA Volumes in Mathematics and Its Applications New York, NY: Springer, 2000, pp. 1–94 DOI: 10.1007/978-1-4612-1284-3˙1

- [41] Jon A. Steingrimsson, Sarah E. Robertson and Issa J. Dahabreh “Sensitivity Analysis for Studies Transporting Prediction Models”, 2023 arXiv: http://arxiv.org/abs/2306.08084

- [42] Steffen Bickel, Michael Brückner and Tobias Scheffer “Discriminative Learning Under Covariate Shift” In J. Mach. Learn. Res. 10, 2009, pp. 2137–2155

- [43] Masashi Sugiyama, Matthias Krauledat and Klaus-Robert Müller “Covariate Shift Adaptation by Importance Weighted Cross Validation” In Journal of Machine Learning Research 8.35, 2007, pp. 985–1005 URL: http://jmlr.org/papers/v8/sugiyama07a.html

- [44] Steffen Bickel, Michael Brückner and Tobias Scheffer “Discriminative Learning for Differing Training and Test Distributions” In Proceedings of the 24th International Conference on Machine Learning, ICML ’07 New York, NY, USA: Association for Computing Machinery, 2007, pp. 81–88 DOI: 10.1145/1273496.1273507

- [45] Masashi Sugiyama and Motoaki Kawanabe “Machine Learning in Non-Stationary Environments: Introduction to Covariate Shift Adaptation” MIT press, 2012

- [46] Bing Li, Constantine Gatsonis, Issa J. Dahabreh and Jon A. Steingrimsson “Estimating the Area under the ROC Curve When Transporting a Prediction Model to a Target Population” In Biometrics, 2022, pp. biom.13796 DOI: 10.1111/biom.13796

- [47] Megha L Mehrotra et al. “Transporting Subgroup Analyses of Randomized Controlled Trials for Planning Implementation of New Interventions” In American Journal of Epidemiology 190.8, 2021, pp. 1671–1680 DOI: 10.1093/aje/kwab045

- [48] Marissa J. Seamans et al. “Generalizability of Subgroup Effects” In Epidemiology 32.3, 2021, pp. 389–392 DOI: 10.1097/EDE.0000000000001329

- [49] Sarah E. Robertson et al. “Estimating Subgroup Effects in Generalizability and Transportability Analyses”, 2021 arXiv: http://arxiv.org/abs/2109.14075

- [50] Sarah E. Robertson, Jon A. Steingrimsson and Issa J. Dahabreh “Regression-Based Estimation of Heterogeneous Treatment Effects When Extending Inferences from a Randomized Trial to a Target Population” In European Journal of Epidemiology 38.2, 2023, pp. 123–133 DOI: 10.1007/s10654-022-00901-5

Appendix A Time-fixed treatment initiation

A.1 Tailoring models for counterfactual predictions

Our goal is to build a model that targets the expected potential outcome under a hypothetical intervention, e.g. the parametric model

However, we do not observe for all individuals. Nonetheless, as the following theorem shows, targets like are identifiable from the observed data under certain assumptions.

Theorem 1

Under conditions A1-A3 in section 4, is identified by the observed data functionals

| (A1) |

and

| (A2) |

in which case we can build a model for by targeting either estimand in the training dataset.

Proof. For the first representation we have

where the first line follows from the random sampling of the training set, the second from the law of iterated expectations, the third from the exchangeability condition A1, and the fourth from the consistency condition A2. Recall that is a subset of . For the second representation, we show that it is equivalent to the first

where the second line follows from the definition of conditional expectation, and the last reverses the law of iterated expectations.

A.2 Identification of general loss functions

Many common model performance measures, such as the mean squared error, Brier score, and absolute error are special cases of a generic loss function . To assess the performance of counterfactual predictions, we would like to estimate

where is not observed for all individuals. The following theorem states that, under the conditions of section 4, is identified using the observed data alone.

Theorem 2

Proof. For the first representation we have

where the first line follows from the definition of , the second from random sampling of the test set, the third from the law of iterated expectations, the fourth from the exchangeability condition A1, and the fifth from the consistency condition A2. Recall that is a subset of . For the second representation, we show that it is equivalent to the first

where the second line follows from the definition of conditional expectation, and the last reverses the law of iterated expectations.

A.3 Plug-in estimation

Using sample analogs for the identified expressions A3 and A4, we obtain two plug-in estimators for the expected loss for a generalized loss function

and

where is an estimator for and is an estimator for . Using the terminology in Morrison et al., we call the first plug-in estimator the conditional loss estimator and the second the inverse probability weighted estimator .

A.4 Random and dynamic regimes

Above we consider static interventions which set treatment to a particular value . We might also consider interventions which probabilistically set based on a known density, possibly conditional on pre-treatment covariates, e.g. . For instance, instead of a counterfactual prediction if everyone or no one had been treated, we may be interested in the prediction if 20% or 50% were treated. We term such an intervention a random intervention to contrast it with static interventions considered previously. Random interventions are closer to the counterfactual interventions of interest under dataset shift which may be approximated as probabilistic changes in the natural course of treatment due to changes in guidelines or prescribing patterns or the wider-availability. For general counterfactual loss function , the expected loss under a random intervention is identified by the functionals

| (A5) |

and

| (A6) |

in the test set under the time-fixed setup described in section 2. The primary difference between these expressions and the ones in section A.1. is that the expectation is taken with respect to the intervention density.

Appendix B Time-varying treatment initiation

B.1 Set up

Here we extend the set up of section 2 in the case that treatment initiation is time-varying over the follow up period. We now observe i.i.d. longitudinal samples from a source population. For each observation, let

where is a vector of covariates, is an indicator of treatment, and is an event indicator all measured at time , where . Overbars denote the full history of a variable, such that . Again we assume the goal is to build a prediction model for end of follow up outcome conditional on baseline covariates which are now a subset of baseline covariates , i.e. . An example DAG for a two time point process is shown in Figure A1.

We would like to assess the performance of the model in a counterfactual version of the source population in which a new treatment policy is implemented. As previously, is the potential outcome under an intervention which sets treatment to . For a sequence of time-varying treatments , we further define a treatment regime as a collection of functions for determining treatment assignment at each time , possibly based on past treatment and covariate history. For a hypothetical treatment regime , we would like to determine the performance of fitted model under the new regime by estimating the expected loss

for generalized loss function .

B.2 Identifiability conditions

We now consider modified identifiability conditions under time-varying treatment initiation. For all from 0 to , we require

-

B1.

Exchangeability:

-

B2.

Consistency: and if

-

B3.

Positivity:

B.3 Identification of general loss functions

The following theorem extends Theorem 2 to the case of a time-varying treatment.

Theorem 3

Under conditions B1-B3 above, the expected counterfactual loss under time-varying regime is identified by the functionals

| (A7) | ||||

and

| (A8) |

in the test set for general loss function , where the first expression is a sequence of iterated expectations and the second is an inverse-probability weighted expectation.

Proof. For the first representation we have

where the first line follows from the definition of , the second from random sampling of the test set, the third from the law of iterated expectations, and the fourth from the exchangeability condition B1. Arguing recursively from to , we can repeatedly invoke iterated expectations and exchanageability to insert and , such that

where the last line follows by consistency condition B2. For the second representation, note that for the inner most expectations we can proceed as previously

where the second line follows from the definition of conditional expectation, the third removes the constant fraction outside expectation, and the last reverses the law of iterated expectations and where

Arguing recursively from to , we get

which is the inverse-probability weighted representation with weights equal to

B.4 Plug-in estimation

Using sample analogs for the identified expressions A7 and A8, we obtain two plug-in estimators for the expected counterfactual loss under a generalized loss function

and

where and is recursively defined for =

is an estimator for and is an estimator for . Note that as the number of time points (i.e. ) increases, the proportion in the test set who actually follow the regime of interest, i.e. those for whom may be prohibitively small, in which case plug-in estimation may not be feasible. In this case, additional modeling assumptions will be necessary to borrow information from other regimes.

Appendix C Doubly robust estimators

C.1 Efficient influence function

We have shown previously that, under the identifiability conditions of section 4, the expected counterfactual loss of a generalized loss function is identified by the observed data functional

In the following theorem, we identify the efficient influence function for under a nonparametric model for the observed data in the test set.

Theorem 4

The influence function for under a nonparametric model for the observable data is

As the influence function under a nonparametric model is always unique, it is also the efficient influence function.

Proof. To show that is the efficient influence function, we will use the well-known fact that the influence function is a solution to

where is the score of the obeservable data under the true law and is a parametric submodel indexed by and the pathwise derivative of the submodel is evaluated at corresponding to the true law . Let . Beginning with the left hand side

where the first line is the definition, the second line applies the chain rule, the third applies definition of the score, and the last uses linearity of expectations. Returning to original supposition, it follows that the influence function is

C.2 One-step estimator

Given the efficient influence function above and random sampling in the test set, the one-step estimator for is given by

C.3 Asymptotic properties

In previous sections, the asymptotic properties of and follow from standard parametric theory111after separating estimation of from the evaluation of performance by random partition of test set.. However, the asymptotic properties of are complicated by the estimation of two nuisance functions, and , and the fact that, we do not immediately assume a parametric model for either. To simplify the derivation of the large sample properties of we begin by defining

for arbitrary functions , and . Here we suppress the dependence on being in the test set for ease of exposition, but note that the rest procedes the same if we were to limit our focus to the test set. Note, the doubly robust estimator can be written as . We define the probability limits of and as and , respectively. By definition, when and are correctly specified, the limits are and .

To derive the asymptotic properties of , we make the following assumptions:

-

D1.

and its limit fall in a Donsker class.

-

D2.

.

-

D3.

(Finite second moment). .

-

D4.

(Model double robustness). At least one of the models or is correctly specified. That is, at least one of or holds, but not necessarily both.

Assumption D1 is a well-known restriction on the complexity of the functionals and . As long as , and are Donsker and all are uniformly bounded then Assumption D1 holds by the Donsker preservation theorem. Many commonly used models such as generalized linear models fall within the Donsker class. This requirement can be further relaxed through sample-splitting, in which case more flexible machine learning algorithms such as random forests, gradient boosting, or neural networks may be used to estimate and .

Using Assumptions D1 through D4, below we prove:

-

1.

(Consistency) .

-

2.

(Asymptotic distribution) has the asymptotic representation

where

and thus if and converge at combined rate of at least then

C.3.1 Consistency

Using the probability limits and defined previously, the double robust estimator converges in probability to

Here we show that the right-hand side is equal to under assumptions D1- D4 when either:

-

1.

is correctly specified

-

2.

is correctly specified

First consider the case where is correctly specified, that is , but we do not assume that the limit is equal to . Recall, as shown previously

Next consider the case when is correctly specified, that is

and this time we do not make the assumptions that the limit is equal to . Recall, as shown previously .

C.3.2 Asymptotic distribution

For a random variable we define notation

and thus the asymptotic representation of can be written

where we add and subtract the term and add another zero term in . For the first term, Assumption D1 implies

Let

now we have

Let’s try to calculate the upper bound of . First, note

We rewrite term as:

Combining the above gives

Using the Cauchy-Schwartz inequality we get.

If both models and are correctly specified and converge at a combined rate faster than , then and

By the central limit theorem,

completing the proof.

Appendix D Risk calibration curve

When the outcome is binary, another common metric of model performance is risk calibration. Calibration is a measure of the relibability of the risk estimates produced by the fitted model . For instance, among a sample of patients who receive a risk prediction of 17% does the outcome really occur for roughly 17% of them over the follow up period? This can be nonparametrically evalutated across a range of risks by estimating the so-called “calibration” curve, i.e. the observed risk as a function of the predicted risk. For counterfactual predictions the relevant calibration curve is the counterfactual risk that would be observed under intervetion as a function of the predicted risk, or

| (A9) |

D.1 Identification

Here we show that the counterfactual calibration curve is identified using the observed data under the assumptions of section 4.

Theorem 5

Under conditions A1-A3, the risk calibration curve is identified by the observed data functionals

| (A10) |

and

| (A11) |

in the test set.

Proof. For the first representation we have

where the first line follows from the definition of , the second from random sampling of the test set, the third from the law of iterated expectations, the fourth from the exchangeability condition A1, and the fifth from the consistency condition A2. Recall that is a subset of . For the second representation, we show that it is equivalent to the first

where the second line follows from the definition of conditional expectation, and the last reverses the law of iterated expectations.

D.2 Estimation

Unlike previous sections, estimation of the full risk calibration curve using sample analogs of the identified expressions A10 and A11 is generally infeasible because they are conditional on a continuous risk score. Instead analysts typically perform either kernel or binned estimation of the calibration curve functional. In the case of the counterfactual risk calibration curve under a hypothetical intervention, the expression above suggests modifying these approaches either through the use of inverse probability weights or an outcome model.

Appendix E Area under ROC curve

Another common metric for the performance of a risk prediction model is the area under the receiver operating characteristic (ROC) curve, often referred to as simply the area under the curve (AUC). The AUC can be interpreted as the probability that a randomly sampled observation with the outcome has a higher predicted value than a randomly sampled observation without the outcome. In that sense, it is a measure of the discriminative ability of the model, i.e. the ability to distinguish between cases and noncases. For counterfactual predictions the relevant AUC is the counterfactual AUC that would be observed under intervetion , or

| (A12) |

E.1 Identification

Here, we show that the counterfactual AUC is identified by the observed data under a modified set of identification conditions, namely:

-

E1.

Exchangeability.

-

E2.

Consistency. if

-

E3.

Positivity. (i) for all that have positive density in , (ii) , where is a random observation that has the outcome and is random observation without the outcome.

Theorem 6

Under conditions E1-E3, the counterfactual AUC is identified by the observed data functionals in the test set

| (A13) |

and

| (A14) |

where the subscripts and denote a random pair of observations from the test set where

and

for a pair of covariate vectors and .

Proof. For the first representation we have

where the first line follows from the definition of , the second from the definition of conditional probability, the third from the law of iterated expectations, the fourth from the definition of conditional expectation, the fifth from the exchangeability condition E1, the sixth from independence of potential outcomes, the seventh from the consistency condition E2, the eighth from random sampling of the test set, and the ninth applies the definition of . Recall that is a subset of . For the second representation, we will show that it is equivalent to the first. Starting from line five above

where the second line follows from consistency , the third from the definition of conditional probability, the fourth from iterated expectations, the fifth removes the constant fraction outside expectation, the sixth reverses the law of iterated expectations and the last applies random sampling of the test set and the definition of .

E.2 Plug-in estimation

Using sample analogs for the identified expressions A13 and A14, we obtain two plug-in estimators for the counterfactual AUC

and

where and is an estimator for and where and is an estimator for . Here, we call the first plug-in estimator the outcome model estimator and the second the inverse probability weighted estimator .

Appendix F Additional application details

The Multi-Ethnic Study on Atherosclerosis (MESA) study is a population-based sample of 6,814 men and women aged 45 to 84 drawn from six communities (Baltimore; Chicago; Forsyth County, North Carolina; Los Angeles; New York; and St. Paul, Minnesota) in the United States between 2000 and 2002. The sampling procedure, design, and methods of the study have been described previously [31]. Study teams conducted five examination visits between 2000 and 2011 in 18 to 24 month intervals focused on the prevalence, correlates, and progression of subclinical cardiovascular disease. These examinations included assessments of lipid-lowering (primarily statins) and other medication use as well as cardiovascular risk factors such as systolic blood pressure, serum cholesterol, cigarette smoking, height, weight, and diabetes.

Our goal was to emulate a single-arm trial corresponding to the AHA guidelines on initiation of statin therapy for primary prevention of cardiovascular disease in the MESA cohort and use the emulated trial to develop a prediction model for the treatment-naive risk. The AHA guidelines stipulate that patients aged 40 to 75 with serum LDL cholesterol levels between 70 mg/dL and 190 mg/dL and no history of cardiovascular disease should initiate statins if their risk exceeds 7.5%. Therefore, we considered MESA participants who completed the baseline examination, had no recent history of statin use, no history of cardiovascular disease, and who met the criteria described in the guidelines (excluding the risk threshold) as eligible to participate in the trial. The primary endpoint was time to atherosclerotic cardiovascular disease (ASCVD), defined as nonfatal myocardial infarction, coronary heart disease death, or ischemic stroke.

Follow up began at the second examination cycle to enable a “wash out” period for statin use and to ensure adequate pre-treatment covariates to control confouding. We constructed a sequence of nested trials starting at each examination cycle from exam 2 through exam 5 and pooled the results from all 4 trials into a single analysis and used a robust variance estimator to account for correlation among duplicated participants. In each nested trial, we used the corresponding questionnaire to determine eligibility as well as statin initiators versus non-initiators. Because the exact timing of statin initiation was not known with precision, in each trial, we estimated the start of follow up for initiators and non-initators by drawing a random month between their current and previous examinations. We explored alternative definitions of the start of follow up in sensitivity analyses in the appendix. To mimic the targeted single-arm trial we limited to non-initiators for development of the prediction models.

F.1 Propensity score models

In the emulated single arm trial, statin initiation can be viewed as “non-adherence” which can be adjusted for by inverse probability weighting, therefore we censored participants when they initiated statins. To calculate the weights, we estimated two logistic regression models: one for the probability of remaining untreated given past covariate history (denominator model) and one for probability of remaining untreated given the selected baseline predictors (numerator model). In the denominator model we included the following covariates:

-

•

Demographic factors - Age, gender, marital status, education, race/ethnicity, employment, health insurance status, depression, perceived discrimination, emotional support, anger and anxiety scales, and neighborhood score.

-

•

Risk factors - Systolic and diastolic blood pressure, serum cholesterol levels (LDL, HDL, Triglycerides), hypertension, diabetes, waist circumference, smoking, alcohol consumption, exercise, family history of CVD, calcium score, hypertrophy on ECG, CRP, IL-6, number of pregnancies, oral contraceptive use, age of menopause.

-

•

Medication use - Anti-hypertensive use, insulin use, daily aspirin use, anti-depressant use, vasodilator use, anti-arryhtmic use.

Time-varying demographic factors and risk factors were lagged such that values from the previous examination cycle were used.