OE_^ OmOE_^ OmOE_^ Omm!OE_^ mmmmOE_^

Machine Learning-powered Combinatorial Clock Auction

Abstract

We study the design of iterative combinatorial auctions (ICAs). The main challenge in this domain is that the bundle space grows exponentially in the number of items. To address this, several papers have recently proposed machine learning (ML)-based preference elicitation algorithms that aim to elicit only the most important information from bidders. However, from a practical point of view, the main shortcoming of this prior work is that those designs elicit bidders’ preferences via value queries (i.e., “What is your value for the bundle ?”). In most real-world ICA domains, value queries are considered impractical, since they impose an unrealistically high cognitive burden on bidders, which is why they are not used in practice. In this paper, we address this shortcoming by designing an ML-powered combinatorial clock auction that elicits information from the bidders only via demand queries (i.e., “At prices , what is your most preferred bundle of items?”). We make two key technical contributions: First, we present a novel method for training an ML model on demand queries. Second, based on those trained ML models, we introduce an efficient method for determining the demand query with the highest clearing potential, for which we also provide a theoretical foundation. We experimentally evaluate our ML-based demand query mechanism in several spectrum auction domains and compare it against the most established real-world ICA: the combinatorial clock auction (CCA). Our mechanism significantly outperforms the CCA in terms of efficiency in all domains, it achieves higher efficiency in a significantly reduced number of rounds, and, using linear prices, it exhibits vastly higher clearing potential. Thus, with this paper we bridge the gap between research and practice and propose the first practical ML-powered ICA.

1 Introduction

Combinatorial auctions (CAs) are used to allocate multiple items among several bidders who may view those items as complements or substitutes. In a CA, bidders are allowed to submit bids over bundles of items. CAs have enjoyed widespread adoption in practice, with their applications ranging from allocating spectrum licences (Cramton 2013) to TV ad slots (Goetzendorff et al. 2015) and airport landing/take-off slots (Rassenti, Smith, and Bulfin 1982).

One of the key challenges in CAs is that the bundle space grows exponentially in the number of items, making it infeasible for bidders to report their full value function in all but the smallest domains. Moreover, Nisan and Segal (2006) showed that for general value functions, CAs require an exponential number of bids in order to achieve full efficiency in the worst case. Thus, practical CA designs cannot provide efficiency guarantees in real world settings with more than a modest number of items. Instead, the focus has shifted towards iterative combinatorial auctions (ICAs), where bidders interact with the auctioneer over a series of rounds, providing a limited amount of information, and the aim of the auctioneer is to find a highly efficient allocation.

The most established mechanism following this interaction paradigm is the combinatorial clock auction (CCA) (Ausubel, Cramton, and Milgrom 2006). The CCA has been used extensively for spectrum allocation, generating over Billion in revenue between and alone (Ausubel and Baranov 2017). Speed of convergence is a critical consideration for any ICA since each round can entail costly computations and business modelling for the bidders (Kwasnica et al. 2005; Milgrom and Segal 2017; Bichler, Hao, and Adomavicius 2017). Large spectrum auctions following the CCA format can take more than bidding rounds. In order to decrease the number of rounds, many CAs in practice use aggressive price update rules (e.g., increasing prices by up to % each round), which can harm efficiency (Ausubel and Baranov 2017). Thus, it remains a challenging problem to design a practical ICA that elicits information via demand queries, is efficient, and converges in a small number of rounds. Specifically, given the value of resources allocated in such real-world ICAs, increasing their efficiency by even one percentage point already translates into monetary gains of hundreds of millions of dollars.

1.1 ML-Powered Preference Elicitation

To address this challenge, researchers have proposed various ways of using machine learning (ML) to improve the efficiency of CAs. The seminal works by Blum et al. (2004) and Lahaie and Parkes (2004) were the first to frame preference elicitation in CAs as a learning problem. In the same strand of research, Brero, Lubin, and Seuken (2018, 2021), Weissteiner and Seuken (2020) and Weissteiner et al. (2022b) proposed ML-powered ICAs. At the heart of those approaches lies an ML-powered preference elicitation algorithm that uses an ML model to approximate each bidder’s value function and to generate the next value query, which in turn refines that bidder’s model. Weissteiner et al. (2022a) designed a special network architecture for this framework while Weissteiner et al. (2023) incorporated a notion of uncertainty (Heiss et al. 2022) into the framework, further increasing its efficiency. Despite their great efficiency gains compared to traditional CA designs, those approaches suffer from one common limitation. They fundamentally rely on value queries of the form “What is your value for bundle ”, which are cognitively more complex, and thus typically impractical for real-world ICAs that instead prioritize employing demand queries.

Conceptually, most related to the present paper is the work by Brero and Lahaie (2018) and Brero, Lahaie, and Seuken (2019), who proposed integrating ML in a price-based ICA to generate the next price vector in order to achieve faster convergence. Similar to our design, in these works the auctioneer maintains a model of each agent’s value function, which are updated as the agents bid in the auction and reveal more information about their values. Then, those models are used in each round to compute new prices and drive the bidding process. Unlike our approach, the design of this prior work focuses only on clearing potential, as the authors do not report efficiency results. Additionally, their design suffers from some significant limitations: (i) it does not exploit any notion of similarity between bundles that contain overlapping items, (ii) it only incorporates a small part of the information revealed by the agents’ bidding. Specifically, they only make use of the fact that for the bundle an agent bids on, her value for it must be larger than its price, and (iii) their approach is computationally intractable already in medium-sized auction domains, as their price update rule requires a large number of posterior samples for expectation maximization and then solving a linear program whose number of constraints for each bidder is proportional to times the number of bids by that agent. These limitations are significant, as they can lead to large efficiency decreases in complex combinatorial domains. Furthermore, their design cannot be easily modified to alleviate these limitations.

1.2 Our Contributions

In this paper, we address the main shortcomings of prior work by designing an ML-powered combinatorial clock auction. Our auction elicits information from bidders via demand queries instead of value queries, while simultaneously being computationally feasible for large domains and incorporating the complete information the demand query observations provide into the training of our ML models. Concretely, we use Monotone-Value Neural Networks (MVNNs) (Weissteiner et al. 2022a) as ML models, which are tailored to model monotone and non-linear combinatorial value functions in CAs.

The main two technical challenges are (i) training those MVNNs only on demand query observations and (ii) efficiently determining the next demand query that is most likely to clear the market based on the trained MVNNs. In detail, we make the following contributions:

-

1.

We first propose an adjusted MVNN architecture, which we call multiset MVNNs (mMVNNs). mMVNNs can be used more generally in multiset domains (i.e., if multiple indistinguishable copies of the same good exist) (Section 3.1) and we prove the universality property of mMVNNs in such multiset domains (Theorem 1).

-

2.

We present a novel method for training mMVNNs on demand query observations (Section 3.2).

-

3.

We introduce an efficient method for determining the price vector that is most likely to clear the market based on the trained ML models (Section 4). For this, we derive a simple and intuitive price update rule that results from performing GD on an objective function which is minimized exactly at clearing prices (Theorem 3).

- 4.

-

5.

We experimentally show that compared to the CCA, our ML-powered clock auction can achieve substantially higher efficiency on the order of 9% points. Furthermore, using linear prices, our ML-powered clock auction exhibits significantly higher clearing potential compared to the CCA (Section 6).

GitHub

Our source code is publicly available on GitHub via: https://github.com/marketdesignresearch/ML-CCA.

1.3 Further Related Work

In the field of automated mechanism design, Dütting et al. (2015, 2019), Golowich, Narasimhan, and Parkes (2018) and Narasimhan, Agarwal, and Parkes (2016) used ML to learn new mechanisms from data, while Cole and Roughgarden (2014); Morgenstern and Roughgarden (2015) and Balcan, Sandholm, and Vitercik (2023) bounded the sample complexity of learning approximately optimal mechanisms. In contrast to this prior work, our design incorporates an ML algorithm into the mechanism itself, i.e., the ML algorithm is part of the mechanism. Lahaie and Lubin (2019) suggest an adaptive price update rule that increases price expressivity as the rounds progress in order to improve efficiency and speed of convergence. Unlike that work, we aim to improve preference elicitation while still using linear prices. Preference elicitation is a key market design challenge outside of CAs too. Soumalias et al. (2023) introduce an ML-powered mechanism for course allocation that improves preference elicitation by asking students comparison queries.

1.4 Practical Considerations and Incentives

Our ML-powered clock phase can be viewed as an alternative to the clock phase of the CCA. In a real-world application, many other considerations (beyond the price update rule) are also important. For example, the careful design of activity rules is vital to induce truthful bidding in the clock phase of the CCA (Ausubel and Baranov 2017). The payment rule used in the supplementary round is also important, and it has been argued that the use of the VCG-nearest payment rule, while not strategy-proof, induces good incentives in practice (Cramton 2013). Similar to the clock phase of the CCA, our ML-powered clock phase is not strategyproof. If our design were to be fielded in a real-world environment, we envision that one would combine it with carefully designed activity and payment rules in order to induce good incentives. Thus, we consider the incentive problem orthogonal to the price update problem and in the rest of the paper, we follow prior work (Brero, Lahaie, and Seuken 2019; Parkes and Ungar 2000) and assume that bidders follow myopic best-response (truthful) bidding throughout all auction mechanisms tested.

2 Preliminaries

2.1 Formal Model for ICAs

We consider multiset CA domains with a set of bidders and a set of distinct items with corresponding capacities, i.e., number of available copies, . We denote by a bundle of items represented as a positive integer vector, where iff item is contained -times in . The bidders’ true preferences over bundles are represented by their (private) value functions , i.e., represents bidder ’s true value for bundle . We collect the value functions in the vector . By we denote an allocation of bundles to bidders, where is the bundle bidder obtains. We denote the set of feasible allocations by . We assume that bidders have quasilinear utility functions of the form where can be highly non-linear and denotes the bidder’s payment. This implies that the (true) social welfare of an allocation is equal to the sum of all bidders’ values . We let denote a social-welfare maximizing, i.e., efficient, allocation. The efficiency of any allocation is determined as .

An ICA mechanism defines how the bidders interact with the auctioneer and how the allocation and payments are determined. In this paper, we consider ICAs that iteratively ask bidders linear demand queries. In such a query, the auctioneer presents a vector of item prices and each bidder responds with her utility-maximizing bundle, i.e.,

| (1) |

where denotes the Euclidean scalar product in .

Even though our approach could conceptually incorporate any kind of (non-linear) price function , our concrete implementation will only use linear prices (i.e., prices over items). Linear prices are most established in practice since they are intuitive and simple for the bidders to understand (e.g., (Ausubel, Cramton, and Milgrom 2006)).

For bidder , we denote a set of such elicited utility-maximizing bundles and price pairs as . Let be the tuple of elicited demand query data from all bidders. The ICA’s (inferred) optimal feasible allocation and payments are computed based on the elicited reports only. Concretely, is defined as

| (2) |

As payment rule one could use any reasonable choice (e.g., VCG payments, see Appendix A). As the auctioneer can only ask a limited number of demand queries (e.g., ), an ICA needs a practically feasible and smart preference elicitation algorithm.

2.2 The Combinatorial Clock Auction (CCA)

We consider the CCA (Ausubel, Cramton, and Milgrom 2006) as the main benchmark auction. The CCA consists of two phases. The initial clock phase proceeds in rounds. In each round, the auctioneer presents anonymous item prices , and each bidder is asked to respond to a demand query, declaring her utility-maximizing bundle at . The clock phase of the CCA is parametrized by the reserve prices employed in its first round, and the way prices are updated. An item is over-demanded at prices , if, for those prices, its total demand based on the bidders’ responses to the demand query exceeds its capacity, i.e., . The most common price update rule is to increase the price of all over-demanded items by a fixed percentage, which we set to for our experiments, as in many real-world applications (e.g., (Industry Canada 2013)).

The second phase of the CCA is the supplementary round. In this phase, each bidder can submit a finite number of additional bids for bundles of items, which are called push bids. Then, the final allocation is determined based on the combined set of all inferred bids of the clock phase, plus all submitted push bids of the supplementary round. This design aims to combine good price discovery in the clock phase with good expressiveness in the supplementary round. In simulations, the supplementary round is parametrized by the assumed bidder behaviour in this phase, i.e., which bundle-value pairs they choose to report. As in (Brero, Lubin, and Seuken 2021), we consider the following heuristics when simulating bidder behaviour:

-

•

Clock Bids: Corresponds to having no supplementary round. Thus, the final allocation is determined based only on the inferred bids of the clock phase (Equation 2).

-

•

Raised Clock Bids: The bidders also provide their true value for all bundles they bid on during the clock phase.

-

•

Profit Max: Bidders provide their true value for all bundles that they bid on in the clock phase, and additionally submit their true value for the bundles earning them the highest utility at the prices of the final clock phase.

3 Training on Demand Query Observations

In this section, we first propose a new version of MVNNs that are applicable to multiset domains and extend the universality proof of classical MVNNs. Finally, we present our demand-query training algorithm.

3.1 Multiset MVNNs

MVNNs (Weissteiner et al. 2022a) are a recently introduced class of NNs specifically designed to represent monotone combinatorial valuations. In the following, we present an adapted version of the MVNNs, which we call multiset MVNNs (mMVNNs). For mMVNNs, we add a linear normalization layer D after the input layer. We add this normalization since the input (i.e., a bundle) is a positive integer vector instead of a binary vector as in the classic case of indivisible items with capacities for all . This normalization ensures that and thus we can use the weight initialization scheme from (Weissteiner et al. 2023). For details, please see Appendix B.

Definition 1 (Multiset MVNN).

An mMVNN for bidder is defined as

| (3) |

-

•

is the number of layers ( hidden layers),

-

•

are the MVNN-specific activation functions with cutoff , called bounded ReLU (bReLU):

(4) -

•

with and with are the non-negative weights and non-positive biases of dimensions and , whose parameters are stored in .

-

•

is the linear normalization layer that ensures and is not trainable.

In Theorem 1, we extend the proof from Weissteiner et al. (2022a) and show that mMVNNs are also universal in the set of monotone value functions defined on a multiset domain . For this, we first define the following properties:

-

(M)

Monotonicity (“more items weakly increase value”):

For : if , i.e. , it holds that , -

(N)

Normalization (”no value for empty bundle”):

,

These properties are common assumptions and are satisfied in many market domains. We can now present the following universality result:

Theorem 1 (Multiset Universality).

Any value function that satisfies (M) and (N) can be represented exactly as an mMVNN from Definition 1, i.e., for it holds that

| (5) |

Proof.

Please, see Section B.2 for the proof. ∎

Furthermore, we can formulate maximization over mMVNNs, i.e., , as a mixed integer linear program (MILP) analogously to Weissteiner et al. (2022a), which will be key for our ML-powered clock phase.

3.2 Training Algorithm

In Algorithm 1, we describe how we train, for each bidder , a distinct mMVNN on demand query data .

Our design choices regarding this training algorithm are motivated by the information that responses to demand queries provide. According to myopic best response bidding, at each round , bidder reports a utility-maximizing bundle at current prices . Formally, for all :

| (6) |

Notice that for any epoch and round , the loss for that round calculated in Algorithms 1, 1 and 1 is always non-negative, and can only be zero if the mMVNN (instead of ) satisfies Equation 6. Thus, the loss for an epoch is zero iff the mMVNN satisfies Equation 6 for all rounds, and in that case the model has captured the full information provided by the demand query responses of that bidder. Finally, note that Algorithm 1 can be applied to any MILP-formalizable ML model whose parameters can be efficiently updated via GD, such as MVNNs or ReLU-NNs.

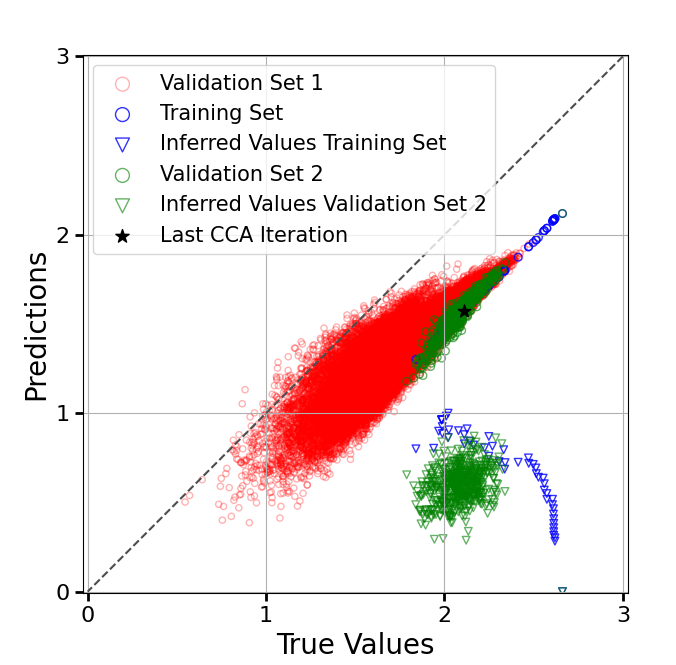

In Figure 1, we present a prediction vs. true plot of an mMVNN, which we trained via Algorithm 1. We present the training set of demand query data points in blue circles, where the prices are generated according to the same rule as in CCA. Additionally, we mark the bundle from this last CCA iteration (i.e., the one resulting from ) with a black star. Moreover, we present two different validation sets on which we evaluate mMVNN configurations in our hyperparameter optimization (HPO): Validation set 1 (red circles), which are uniformly at random sampled bundles , and validation set 2 (green circles), where we first sample price vectors where the price of each item is drawn uniformly at random from the range of to times the average maximum value of an agent of that type for a single item, and then determine utility-maximizing bundles (w.r.t. ) at those prices (cp. Equation 1). While validation set 1 measures generalization performance in a classic sense over the whole bundle space, validation set 2 focuses on utility-maximizing bundles. We additionally demonstrate the inferred values of the bundles of the training set and validation set 2 using triangles of the same colour, i.e., . These triangles highlight the only cardinal information that our mMVNNs have access to during training and are a lower bound of the true value. In Figure 1, we see that our mMVNN is able to learn at the training points (blue circles) the true value functions almost perfectly up to a constant shift , i.e., . This is true even though the corresponding inferred values (blue triangles) are very far off from the true values . Moreover, the mMVNN generalizes well (up to the constant shift ) on validation sets 1 and 2. Overall, this shows that Algorithm 1 indeed leads to mMVNNs which are a good approximation of . Note that learning the true value function up to a constant shift suffices for our proposed demand query generation procedure presented in Section 4.

4 ML-powered Demand Query Generation

In this section, we show how we generate ML-powered demand queries and provide the theoretical foundation for our approach by extending a well-known connection between clearing prices, efficiency and a clearing objective function. First, we define indirect utility, revenue and clearing prices.

Definition 2 (Indirect Utility and Revenue).

For linear prices , a bidder’s indirect utility and the seller’s indirect revenue are defined as

| (7) | |||

| (8) |

i.e., at prices , Equations 7 and 8 are the maximum utility a bidder can achieve for all and the maximum revenue the seller can achieve among all feasible allocations.

Definition 3 (Clearing Prices).

Prices are clearing prices if there exists an allocation such that

-

1.

for each bidder , the bundle maximizes her utility, i.e., , and

-

2.

the allocation maximizes the sellers revenue, i.e., .111For linear prices, this maximum is achieved by selling every item, i.e., (see Section C.2).

Next, we provide an important connection between clearing prices, efficiency and a clearing objective . Theorem 2 extends Bikhchandani and Ostroy (2002, Theorem 3.1).

Theorem 2.

Consider the notation from Definitions 2 and 3 and the objective function . Then it holds that, if a linear clearing price vector exists, every price vector

| (9a) | |||||

| such that | (9b) | ||||

is a clearing price vector and the corresponding allocation is efficient.222More precisely, constraint (9b) should be reformulated as where , since in theory, does not always have to be unique.

Proof.

We provide the proof in Section C.1. ∎

Theorem 2 does not claim the existence of linear clearing prices (LCPs) . For general value functions , LCPs may not exist (Bikhchandani and Ostroy 2002). However, in the case that LCPs do exist, Theorem 2 shows that all minimizers of (9) are LCPs and their corresponding allocation is efficient. This is at the core of our ML-powered demand query generation approach, which we discuss next.

The key idea to generate ML-powered demand queries is as follows: As an approximation for the true value function , we use for each bidder a distinct mMVNN that has been trained on the bidder’s elicited demand query data (see Section 3). Motivated by Theorem 2, we then try to find the demand query minimizing subject to the feasibility constraint (9b). This way, we find demand queries which, given the already observed demand responses , have high clearing potential. Note that unlike the CCA, this process does not result in monotone prices.

Remark 1 (Constraint (9b)).

An important economic insight is that minimizing is optimal, when LCPs exist (also without constraint (9b) as shown in Lemma 2 in Section C.1). If however LCPs do not exist, it is favourable to minimize under the constraint of having no predicted over-demand for any items (see Section D.9 for an empirical comparison of minimizing with and without constraint (9b)). This is because in case the market does not clear, our ML-CCA (see Section 5), just like the CCA, will have to combine the clock bids of the agents to produce a feasible allocation with the highest inferred social welfare according to Equation 2. See Section D.6 for details.

Note that (9) is a hard, bi-level optimization problem. We minimize (9) via gradient descent (GD), since Theorem 3 gives us the gradient and convexity of .

Theorem 3.

Let be a tuple of trained mMVNNs and let denote each bidder’s predicted utility maximizing bundle w.r.t. . Then it holds that is convex, Lipschitz-continuous and a.e. differentiable. Moreover,

| (10) |

is always a sub-gradient and a.e. a classical gradient.

Proof.

In Section C.2 we provide the full proof. Concretely, Lemmas 3 and 4 prove the Lipschitz-continuity and the convexity. In the following, we provide a sketch of how the (sub-)gradients are derived. First, since is finite, it is intuitive that is a piece-wise constant function and thus (as intuitively argued by Pogančić et al. (2020) and proven by us in Lemma 6). Then we can compute the gradient a.e. as if was a constant:

For a mathematically rigorous derivation of sub-gradients and a.e. differentiability see Lemmas 5 and 6. ∎

With Theorem 3, we obtain the following update rule of classical GD . Interestingly, this equation has an intuitive economic interpretation. If the th item is over/under-demanded based on the predicted utility-maximizing bundles , then its new price is increased/decreased by the learning rate times its over/under-demand. However, to enforce constraint (9b) in GD, we asymmetrically increase the prices times more in case of over-demand than we decrease them in case of under-demand. This leads to our final update rule (see Item 1 in Section D.6 for more details):

| (11a) | |||

| (11b) |

To turn this soft constraint into a hard constraint, we increase this asymmetry via iteratively until we achieve feasibility and in the end we select the GD step with the lowest value within those steps that were feasible. Based on the final update rule from (11), we propose NextPrice (Algorithm 3 in Section D.6), an algorithm that generates demand queries with high clearing potential, which additionally induce utility-maximizing bundles that are predicted to be feasible (see Section D.6 for all details).

| GSVM | LSVM | SRVM | MRVM | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Mechanism | Eclock | Eraise | Eprofit | Clear | Eclock | Eraise | Eprofit | Clear | Eclock | Eraised | Eprofit | Clear | Eclock | Eraise | Eprofit | Clear |

| ML-CCA | 98.23 | 98.93 | 100.00 | 56 | 91.64 | 96.39 | 99.95 | 26 | 99.59 | 99.93 | 100.00 | 13 | 93.04 | 93.31 | 93.68 | 0 |

| CCA | 90.40 | 93.59 | 100.00 | 3 | 82.56 | 91.60 | 99.76 | 0 | 99.63 | 99.81 | 100.00 | 8 | 92.44 | 92.62 | 93.18 | 0 |

5 ML-powered Combinatorial Clock Auction

In this section, we describe our ML-powered combinatorial clock auction (ML-CCA), which is based on our proposed new training algorithm from Section 3 as well as our new demand query generation procedure from Section 4.

We present ML-CCA in Algorithm 2. In Lines 2 to 2, we draw the first price vectors using some initial demand query method and receive the bidders’ demand responses to those price vectors. Concretely, in Section 6, we report results using the same price update rule as the CCA for . In each of the next up to ML-powered rounds, we first train, for each bidder, an mMVNN on her demand responses using Algorithm 1 (Algorithm 2). Next, in Algorithm 2, we call NextPrice to generate the next demand query based on the agents’ trained mMVNNs (see Section 4). If, based on the agents’ responses to the demand query (Algorithm 2), our algorithm has found market-clearing prices, then the corresponding allocation is efficient and is returned, along with payments according to the deployed payment rule (Algorithm 2). If, by the end of the ML-powered rounds, the market has not cleared, we optionally allow bidders to submit push bids, analogously to the supplementary round of the CCA (Algorithm 2) and calculate the optimal allocation and the payments (Algorithms 2 and 2). Note that ML-CCA can be combined with various possible payment rules , such as VCG or VCG-nearest.

6 Experiments

In this section, we experimentally evaluate the performance of our proposed ML-CCA from Algorithm 2.

Experiment Setup.

To generate synthetic CA instances, we use the GSVM, LSVM, SRVM, and MRVM domains from the spectrum auction test suite (SATS) (Weiss, Lubin, and Seuken 2017) (see Section D.1 for details). We compare our ML-CCA with the original CCA. For both mechanisms, we allow a maximum of clock rounds per instance, i.e., we set . For CCA, we set the price increment to % as in (Industry Canada 2013) and optimized the initial reserve prices to maximize its efficiency. For ML-CCA, we create price vectors to generate the initial demand query data using the same price update rule as the CCA, with the price increment adjusted to accommodate for the reduced number of rounds following this price update rule. In GSVM, LSVM and SRVM we set for ML-CCA, while in MRVM we set . After each clock round, we report efficiency according to the clock bids up to that round, as well as efficiency if those clock bids were raised (see Section 2.2). Finally, we report the efficiency if the last clock round was supplemented with bids using the profit max heuristic. Note that this is a very unrealistic and cognitively expensive bidding heuristic in practice, as it requires the agents to both discover their top most profitable bundles as well as report their exact values for them, and thus only adds theoretical value to gauge the difficulty of each domain.

Hyperparameter Optimization (HPO).

We optimized the hyperparameters (HPs) of the mMVNNs for each bidder type of each domain. Specifically, for each bidder type we trained an mMVNN on the demand responses of a bidder of that type on CCA clock rounds and selected the HPs that resulted in the highest on validation set as described in Section 3.1. For more details please see Section D.3.

Results.

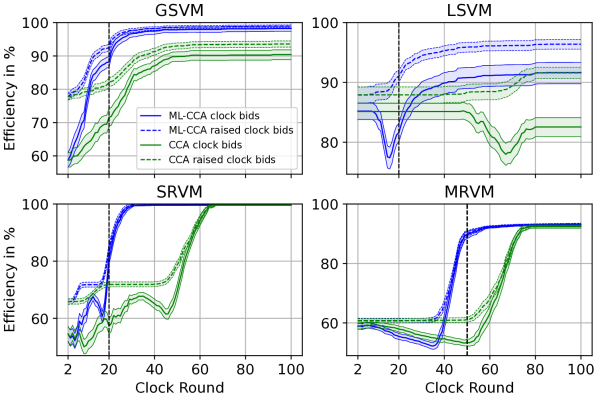

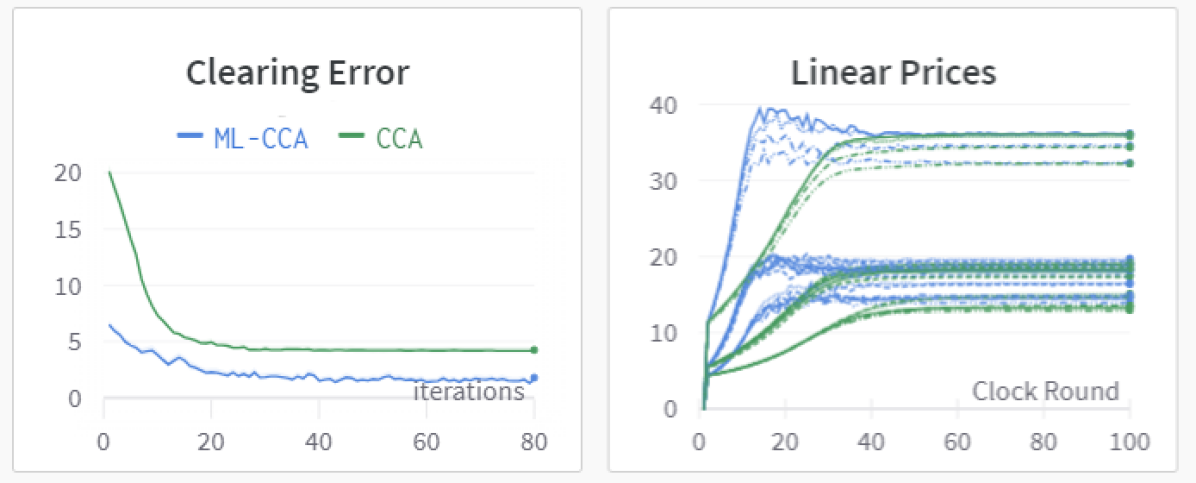

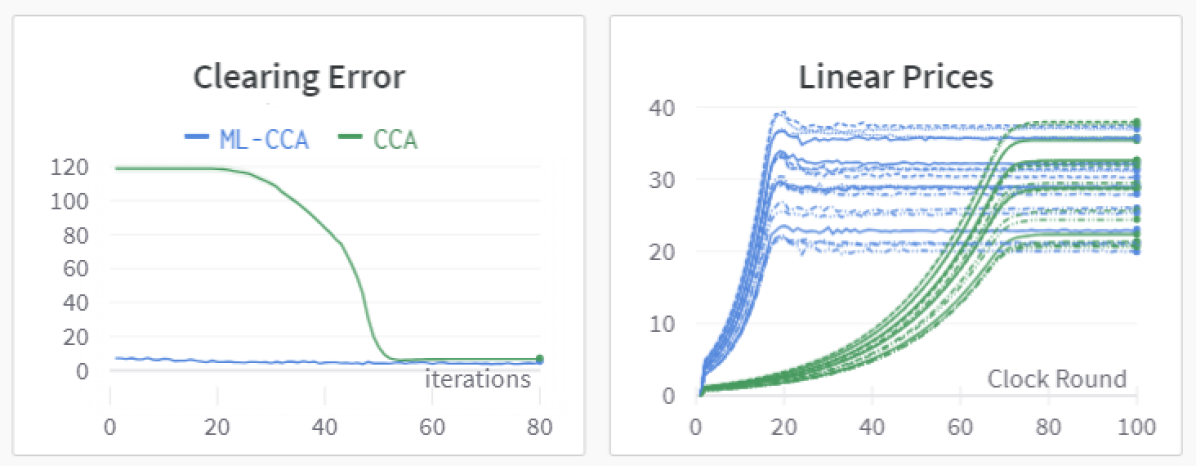

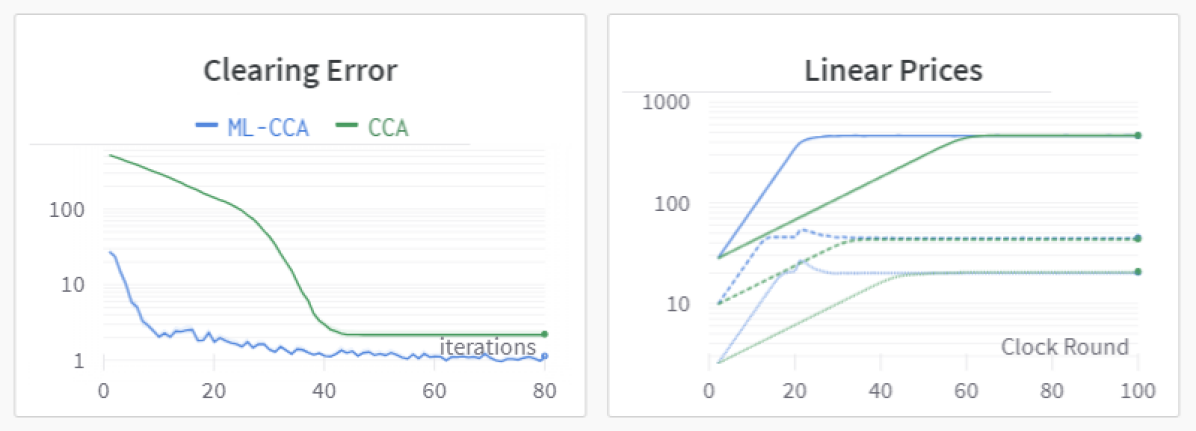

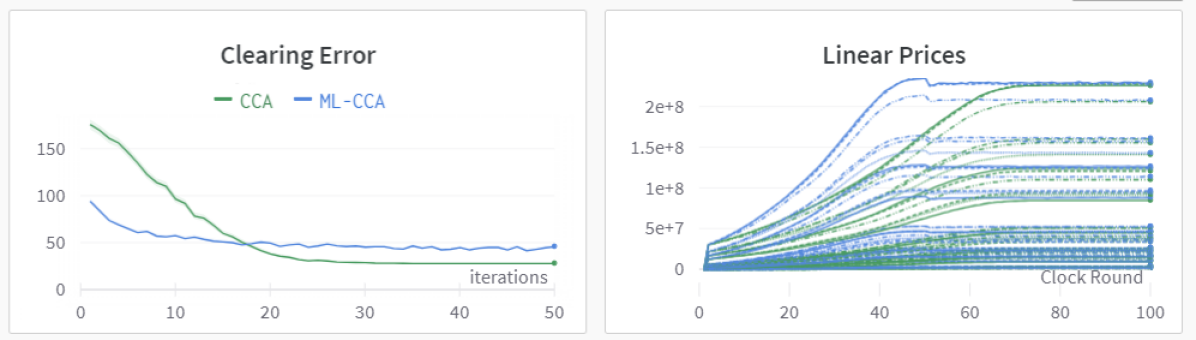

All efficiency results are presented in Table 1, while in Figure 2 we present the efficiency after each clock round, as well as the efficiency if those clock bids were enhanced with the clock bids raised heuristic (for % CIs and -values see Section D.7). In GSVM, ML-CCA’s clock phase exhibits over % points higher efficiency compared to the CCA, while if we add the clock bids raised heuristic to both mechanisms, ML-CCA still exhibits over % points higher efficiency. At the same time, ML-CCA is able to find clearing prices in % of the instances, as opposed to only % for the CCA. The results for LSVM are qualitatively very similar; ML-CCA’s clock phase increases efficiency compared to the CCA by over % points, while clearing the market in % of the cases as opposed to %. If we add the clock bids raised heuristic to both mechanisms, ML-CCA still increases efficiency by over % points. The SRVM domain, as suggested by the existence of only unique goods, is quite easy to solve. Thus, both mechanisms can achieve almost % efficiency after their clock phase. For the clock bids raised heuristic our method reduces the efficiency loss by a factor of more than two (from % to %), and additionally, one can see from Figure 2 that our method reaches over % in less than rounds. In MRVM, ML-CCA again achieves statistically significantly better results for all 3 bidding heuristics. Notably, the CCA needs both the clock bids raised heuristic and profit max bids to reach the same efficiency as our ML-CCA clock phase, i.e., it needs up to additional value queries per bidder (see Section D.7). In MRVM, LCPs never exist, thus neither ML-CCA nor the CCA can ever clear the market. To put our efficiency improvements in perspective, in the GSVM, LSVM and MRVM domains, ML-CCA’s clock phase achieves higher efficiency than the CCA enhanced with the clock bids raised heuristic, i.e., the CCA, even if it uses up to an additional value queries per bidder, cannot match the efficiency of our ML-powered clock phase. In Figure 2, we see that our ML-CCA can (almost) reach the efficiency numbers of Table 1 in a significantly reduced number of clock rounds compared to the CCA, while if we attempt to “speed up” the CCA, then its efficiency can substantially drop, see Section D.8. In particular, in GSVM and LSVM, using clock rounds, our ML-CCA can achieve higher efficiency than the CCA can in clock rounds.

7 Conclusion

We have proposed a novel method for training MVNNs to approximate the bidders’ value functions based on demand query observations. Additionally, we have framed the task of determining the price vector with the highest clearing potential as minimization of an objective function that we prove is convex, Lipschitz-continuous, a.e. differentiable, and whose gradient for linear prices has an intuitive economic interpretation: change the price of every good proportionally to its predicted under/over-demand at the current prices. The resulting mechanism (ML-CCA) from combining these two components exhibits significantly higher clearing potential than the CCA and can increase efficiency by up to % points while at the same time converging in a much smaller number of rounds. Thus, we have designed the first practical ML-powered auction that employs the same interaction paradigm as the CCA, i.e., demand queries instead of cognitively too complex value queries, yet is able to significantly outperform the CCA in terms of both efficiency and clearing potential in realistic domains.

Acknowledgments

This paper is part of a project that has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (Grant agreement No. 805542).

References

- Ausubel and Baranov (2017) Ausubel, L. M.; and Baranov, O. 2017. A practical guide to the combinatorial clock auction. Economic Journal, 127(605): F334–F350.

- Ausubel and Baranov (2019) Ausubel, L. M.; and Baranov, O. 2019. Iterative Vickrey Pricing in Dynamic Auctions.

- Ausubel and Baranov (2020) Ausubel, L. M.; and Baranov, O. 2020. Revealed Preference and Activity Rules in Dynamic Auctions. International Economic Review, 61(2): 471–502.

- Ausubel and Baranov (2014) Ausubel, L. M.; and Baranov, O. V. 2014. Market Design and the Evolution of the Combinatorial Clock Auction. The American Economic Review, 104(5): 446–451.

- Ausubel, Cramton, and Milgrom (2006) Ausubel, L. M.; Cramton, P.; and Milgrom, P. 2006. The clock-proxy auction: A practical combinatorial auction design. In Cramton, P.; Shoham, Y.; and Steinberg, R., eds., Combinatorial Auctions, 115–138. MIT Press.

- Balcan, Sandholm, and Vitercik (2023) Balcan, M.-F.; Sandholm, T.; and Vitercik, E. 2023. Generalization Guarantees for Multi-item Profit Maximization: Pricing, Auctions, and Randomized Mechanisms. arXiv:1705.00243.

- Bertsekas (1971) Bertsekas, D. P. 1971. Control of uncertain systems with a set-membership description of the uncertainty. Ph.D. thesis, Massachusetts Institute of Technology.

- Bertsekas (1999) Bertsekas, D. P. 1999. Nonlinear Programming. Athena scientific optimization and computation series. Athena Scientific. ISBN 9781886529007.

- Bichler, Hao, and Adomavicius (2017) Bichler, M.; Hao, Z.; and Adomavicius, G. 2017. Coalition-based pricing in ascending combinatorial auctions, 493–528. Cambridge University Press. ISBN 9781107135345.

- Bikhchandani and Ostroy (2002) Bikhchandani, S.; and Ostroy, J. M. 2002. The package assignment model. Journal of Economic theory, 107(2): 377–406.

- Blum et al. (2004) Blum, A.; Jackson, J.; Sandholm, T.; and Zinkevich, M. 2004. Preference elicitation and query learning. Journal of Machine Learning Research, 5: 649–667.

- Brero and Lahaie (2018) Brero, G.; and Lahaie, S. 2018. A Bayesian clearing mechanism for combinatorial auctions. In Proceedings of the 32nd AAAI Conference on Artificial Intelligence.

- Brero, Lahaie, and Seuken (2019) Brero, G.; Lahaie, S.; and Seuken, S. 2019. Fast Iterative Combinatorial Auctions via Bayesian Learning. In Proceedings of the 33rd AAAI Conference of Artificial Intelligence.

- Brero, Lubin, and Seuken (2018) Brero, G.; Lubin, B.; and Seuken, S. 2018. Combinatorial Auctions via Machine Learning-based Preference Elicitation. In Proceedings of the 27th International Joint Conference on Artificial Intelligence.

- Brero, Lubin, and Seuken (2021) Brero, G.; Lubin, B.; and Seuken, S. 2021. Machine Learning-powered Iterative Combinatorial Auctions. arXiv preprint arXiv:1911.08042.

- Cole and Roughgarden (2014) Cole, R.; and Roughgarden, T. 2014. The Sample Complexity of Revenue Maximization. In Proceedings of the Forty-Sixth Annual ACM Symposium on Theory of Computing, STOC ’14, 243–252. New York, NY, USA: Association for Computing Machinery. ISBN 9781450327107.

- Cramton (2013) Cramton, P. 2013. Spectrum auction design. Review of Industrial Organization, 42(2): 161–190.

- Danskin (1967) Danskin, J. M. 1967. The theory of Max-Min and its application to weapons allocation problems [by] John M. Danskin. Springer-Verlag Berlin, New York.

- Dütting et al. (2019) Dütting, P.; Feng, Z.; Narasimhan, H.; Parkes, D. C.; and Ravindranath, S. S. 2019. Optimal auctions through deep learning. In Proceedings of the 36th International Conference on Machine Learning.

- Dütting et al. (2015) Dütting, P.; Fischer, F.; Jirapinyo, P.; Lai, J. K.; Lubin, B.; and Parkes, D. C. 2015. Payment rules through discriminant-based classifiers. ACM Transactions on Economics and Computation, 3(1): 5.

- Goeree and Holt (2010) Goeree, J. K.; and Holt, C. A. 2010. Hierarchical package bidding: A paper & pencil combinatorial auction. Games and Economic Behavior, 70(1): 146–169.

- Goetzendorff et al. (2015) Goetzendorff, A.; Bichler, M.; Shabalin, P.; and Day, R. W. 2015. Compact Bid Languages and Core Pricing in Large Multi-item Auctions. Management Science, 61(7): 1684–1703.

- Golowich, Narasimhan, and Parkes (2018) Golowich, N.; Narasimhan, H.; and Parkes, D. C. 2018. Deep Learning for Multi-Facility Location Mechanism Design. In Proceedings of the Twenty-seventh International Joint Conference on Artificial Intelligence and the Twenty-third European Conference on Artificial Intelligence, 261–267.

- Heiss et al. (2022) Heiss, J. M.; Weissteiner, J.; Wutte, H. S.; Seuken, S.; and Teichmann, J. 2022. NOMU: Neural Optimization-based Model Uncertainty. In Proceedings of the 39th International Conference on Machine Learning, volume 162 of Proceedings of Machine Learning Research, 8708–8758. PMLR.

- Industry Canada (2013) Industry Canada. 2013. ”Responses to Clarification Questions on the Licensing Framework for Mobile Broadband Services (MBS) — 700 MHz Band”.

- Kwasnica et al. (2005) Kwasnica, A. M.; Ledyard, J. O.; Porter, D.; and DeMartini, C. 2005. A New and Improved Design for Multiobject Iterative Auctions. Management Science, 51(3): 419–434.

- Lahaie and Lubin (2019) Lahaie, S.; and Lubin, B. 2019. Adaptive-Price Combinatorial Auctions. In Proceedings of the 2019 ACM Conference on Economics and Computation, EC ’19, 749–750. New York, NY, USA: Association for Computing Machinery. ISBN 9781450367929.

- Lahaie and Parkes (2004) Lahaie, S. M.; and Parkes, D. C. 2004. Applying learning algorithms to preference elicitation. In Proceedings of the 5th ACM Conference on Electronic Commerce.

- Milgrom and Segal (2017) Milgrom, P.; and Segal, I. 2017. Designing the US incentive auction. Handbook of spectrum auction design, 803–812.

- Morgenstern and Roughgarden (2015) Morgenstern, J.; and Roughgarden, T. 2015. The Pseudo-Dimension of near-Optimal Auctions. In Proceedings of the 28th International Conference on Neural Information Processing Systems - Volume 1, NIPS’15, 136–144. Cambridge, MA, USA: MIT Press.

- Narasimhan, Agarwal, and Parkes (2016) Narasimhan, H.; Agarwal, S. B.; and Parkes, D. C. 2016. Automated mechanism design without money via machine learning. In Proceedings of the 25th International Joint Conference on Artificial Intelligence.

- Nisan and Segal (2006) Nisan, N.; and Segal, I. 2006. The communication requirements of efficient allocations and supporting prices. Journal of Economic Theory, 129(1): 192–224.

- Parkes and Ungar (2000) Parkes, D. C.; and Ungar, L. H. 2000. Iterative combinatorial auctions: Theory and practice. In Proceedings of the seventeenth national Conference on artificial intelligence, 74–81.

- Pogančić et al. (2020) Pogančić, M. V.; Paulus, A.; Musil, V.; Martius, G.; and Rolinek, M. 2020. Differentiation of blackbox combinatorial solvers. In International Conference on Learning Representations.

- Rassenti, Smith, and Bulfin (1982) Rassenti, S. J.; Smith, V. L.; and Bulfin, R. L. 1982. A combinatorial auction mechanism for airport time slot allocation. The Bell Journal of Economics, 402–417.

- Rockafellar (1970) Rockafellar, R. T. 1970. Convex Analysis. Princeton: Princeton University Press. ISBN 9781400873173.

- Scheffel, Ziegler, and Bichler (2012) Scheffel, T.; Ziegler, G.; and Bichler, M. 2012. On the impact of package selection in combinatorial auctions: an experimental study in the context of spectrum auction design. Experimental Economics, 15(4): 667–692.

- Soumalias et al. (2023) Soumalias, E.; Zamanlooy, B.; Weissteiner, J.; and Seuken, S. 2023. Machine Learning-powered Course Allocation. arXiv preprint arXiv:2210.00954.

- Weiss, Lubin, and Seuken (2017) Weiss, M.; Lubin, B.; and Seuken, S. 2017. Sats: A universal spectrum auction test suite. In Proceedings of the 16th Conference on Autonomous Agents and MultiAgent Systems, 51–59.

- Weissteiner et al. (2022a) Weissteiner, J.; Heiss, J.; Siems, J.; and Seuken, S. 2022a. Monotone-Value Neural Networks: Exploiting Preference Monotonicity in Combinatorial Assignment. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI-22, 541–548. International Joint Conferences on Artificial Intelligence Organization. Main Track.

- Weissteiner et al. (2023) Weissteiner, J.; Heiss, J.; Siems, J.; and Seuken, S. 2023. Bayesian Optimization-based Combinatorial Assignment. Proceedings of the AAAI Conference on Artificial Intelligence, 37.

- Weissteiner and Seuken (2020) Weissteiner, J.; and Seuken, S. 2020. Deep Learning—Powered Iterative Combinatorial Auctions. Proceedings of the AAAI Conference on Artificial Intelligence, 34(02): 2284–2293.

- Weissteiner et al. (2022b) Weissteiner, J.; Wendler, C.; Seuken, S.; Lubin, B.; and Püschel, M. 2022b. Fourier Analysis-based Iterative Combinatorial Auctions. In Proceedings of the Thirty-First International Joint Conference on Artificial Intelligence, IJCAI-22, 549–556. International Joint Conferences on Artificial Intelligence Organization. Main Track.

Appendix

Appendix A Payment and Activity Rules

In this section, we reprint the VCG and VCG-nearest payment rules, as well as give an overview of activity rules for the CCA, and argue why the most prominent choices are also applicable to our ML-CCA.

A.1 VCG Payments from Demand Query Data

Definition A.1.

(VCG Payments from Demand Query Data) Let denote an elicited set of demand query data from each bidder and let . We then calculate the VCG payments as follows:

| (12) | ||||

| (13) |

where is the allocation that maximizes the inferred social welfare (SW) when excluding bidder , i.e.,

| (14) |

and denote the corresponding price vectors that lead to , and is a inferred-social-welfare-maximizing allocation (see Equation 2) with corresponding prices .

Thus, when using VCG, bidder ’s utility is:

Remark A.1.

Note that Definition A.1 defines VCG payments for a set of elicited demand query data using the bidders’ inferred values from this data set. Specifically, those would be the VCG payments after the CCA’s clock phase for example (i.e., if there was no supplementary round). However, one can analogously define VCG-payments for any given set of reported bundle-value pairs (see Weissteiner et al. (2023, Definition B.1.)). For example, in the case of additional value bids, such as supplementary round push bids, one would use Weissteiner et al. (2023, Definition B.1.) and set , where is the bidder’s supplementary round bid for that bundle (or zero, if she did not bid on it in the supplementary round), i.e., bidder ’s bid for any bundle is the maximum of her largest inferred value for that bundle based on the clock round bids and the supplementary round bids.

A.2 VCG-Nearest Payments

To define the VCG-nearest payments, we must first introduce the core:

Definition A.2.

(The Core) An outcome (i.e., a tuple of a feasible allocation and payments ) is in the core if it satisfies the following two properties:

-

1.

The outcome is individual rational, i.e, for all

-

2.

The core constraints

(15) where is bidder ’s value for bundle and is the set of feasible allocations.

In words, a payment vector (together with a feasible allocation ) is in the core if no coalition of bidders is willing to pay more for the items than the mechanism is charging the winners. Note that by replacing the true values with the bidders’ (possibly untruthful) bids in Definition A.2 one can equivalently define the revealed core.

Now, we can define

Definition A.3.

(Minimum Revenue Core) Among all payment vectors in the (revealed) core, the (revealed) minimum revenue core is the set of payment vectors with smallest -norm, i.e., which minimize the sum of the payments of all bidders.

We can now define VCG-nearest payments:

Definition A.4.

(VCG-Nearest Payments) Given an allocation for bidder reports , the VCG-nearest payments are defined as the vector of payments in the (revealed) minimum revenue core that minimizes the -norm to the VCG payment vector .

A.3 On the Importance of Activity Rules to Align Incentives

In the CCA, activity rules serve multiple purposes. First, they can help speed up the auction process. Second, they reduce ”bid-sniping” opportunities, i.e., bidders concealing their true intentions until the very last rounds of the auction.333The notion of “bid-sniping” first originated in eBay auctions with predetermined ending times, where the high-value bidder can sometimes reduce her payments by submitting her bid at the very last moment. Third, they can limit surprise bids in the supplementary round of the CCA and significantly reduce a bidder’s ability to drive up her opponents payments by overbidding on bundles that she can no longer win (Ausubel and Baranov 2017). There are two types of activity rules that are implemented in a CCA:

-

1.

Clock phase activity rules, that limit the bundles that an agent can bid on during the clock phase, based on her bids in previous clock rounds.

-

2.

Supplementary round activity rules, that restrict the amount that an agent can bid on for various sets of items during the supplementary round.

Most of the activity rules that were traditionally used for the clock phase of the CCA were based on either revealed-preference considerations or some points-based system, where the main idea is to assign points to each item prior to the auction, and only allow bidders to submit monotonically non-increasing in points bids, i.e., as the rounds progress and the prices increase, the bidders cannot submit bids for larger sets of items. Both of these approaches, as well as hybrid combinations thereof, were shown to actually further interfere with truthful bidding in some cases (Ausubel and Baranov 2014, 2020).

However, Ausubel and Baranov (2019) showed that basing the clock phase activity rule not on the above but instead entirely upon the generalized axiom of revealed preference (GARP) can dynamically approximate VCG payoffs and thus improve the bidding incentives of the CCA. GARP imposes revealed-preference constraints (see Definition A.5) to the bidder’s demand responses, i.e., the GARP activity rule requires the bidder to exhibit rational behaviour in her demand choices. Importantly, the GARP activity rule does not require a monotonic price trajectory. Thus, it can also be applied in our ML-powered clock phase, allowing the clock phase of our ML-CCA to enjoy the same improvement in bidding incentives.

For the supplementary round, the CCA’s most prominent activity rules are again based on a combination of the same points-based system and revealed-preference ideas. For this, we need to define the following constraint:

Definition A.5.

(Revealed-preference constraint) The revealed-preference constraint for bundle with respect to clock round is

| (16) |

where is bidder ’s bid for bundle in the supplementary round, is the bundle demanded by the agent at clock round , is the final bid for bundle and is the linear price vector of clock round .

Intuitively, the revealed-preference constraint states that a bidder is not allowed to claim a high value for bundle relative to bundle , given that she claimed to prefer bundle at clock round (see Inequality (6)). The difference between the three most prominent supplementary round activity rules is with respect to which clock rounds the revealed-preference constraint should be satisfied. Specifically:

-

1.

Final Cap: A bid for bundle should satisfy the revealed-preference constraint (Definition A.5) with respect to the final clock round’s price and bundle .

-

2.

Relative Cap: A bid for bundle should satisfy the revealed-preference constraint (Definition A.5) with respect to the last clock round for which the bidder was eligible for that bundle , based on the points-based system.

-

3.

Intermediate Cap: A bid for bundle should satisfy the revealed-preference constraint (Definition A.5) with respect to all eligibility-reducing rounds, starting from the last clock round for which the bidder was eligible for based on the point system.

Ausubel and Baranov (2017) showed that combining the Final Cap and Relative Cap activity rules leads to the largest amount of reduction in bid-sniping opportunities for the UK 4G auction, as measured by the theoretical bid amount that each bidder would need to increase her bid by in the supplementary round in order to protect her final clock round bundle. Finally, note that the Final- and Intermediate Cap activity rules can also be applied to our ML-CCA.444With the modification for the Relative Cap rule that the revealed-preference constraint should hold for the rounds that follow the same price update rule as the CCA, and then the ML-powered clock rounds should be treated as corresponding to the same amount of points, since the prices in these rounds on aggregate stay very close to the prices of the last round, as shown in Figures 5, 6, 7 and 8.

To conclude, we observe that for both its clock phase and the supplementary round, our ML-CCA (with the same method as the CCA), is compatible with the most prominent activity rules for the corresponding phases of the CCA, while it is also obviously compatible with the most prominent payment rule, VCG-nearest prices (Definition A.4). This, combined with the fact that the ML-CCA has the same interaction paradigm for the bidders as the CCA, is a very strong indication that our ML-CCA can reduce the opportunities for the bidders to misreport to a similar extent as the classical CCA.

Appendix B Multiset MVNNs

B.1 Advantages of mMVNNs over MVNNs

In Weissteiner and Seuken (2020) and Weissteiner et al. (2022b, a, 2023) items with a capacity , were treated as distinct items, without exploiting the prior knowledge that these items are indistinguishable to the bidders. Sufficiently large classical MVNNs that were trained on large enough training sets would at some point learn that these items are indistinguishable, but this prior information was not incorporated at an architectural level. For multiset MVNNs this hard prior knowledge is hard-coded directly into the architecture (see Definition 1). This additional prior knowledge is particularly beneficial for small training data sets in terms of generalization.

Also the MILPs solve times should be able to benefit from the reduced number of variables of mMVNNs compared to MVNNs. (For classical MVNNs one had to introduce one binary variable for each indistinguishable copy of an item, i.e., classical MVNNs got binary variables at input, while mMVNNs get only integer variables as input.)

B.2 Universality of mMVNNs

Note that Weissteiner et al. (2022a) have proven universality of MVNNs only for the case of binary input vectors corresponding to classical sets (i.e., ). Here, we prove in Section B.2 universality of mMVNNs for arbitrary capacities corresponding to multiset domains such as our .

First, we recall the following definition:

Definition B.1.

The set of all monotonic555Within this paper, by “monotonic”, we always refer to weakly monotonically increasing (M), i.e., monotonically non-decreasing. In multiset-notation this reads as: . and normalized functions from to is defined as

| (17) |

The following lemma says that every mMVNN is monotonic (M) and and normalized (N) in the sense of Definition B.1.

Lemma 1.

Let be an mMVNN from Definition 1. Then it holds that for all and .

Proof.

The proof of this lemma is perfectly analogous to the proof of (Weissteiner et al. 2022a, Lemma 1). ∎

Now we are ready to present a constructive proof for Theorem 1.

Proof of Theorem 1

Proof.

This proof follows a similar strategy as the proof of (Weissteiner et al. 2022a, Theorem 1).

-

1.

This direction follows immediately from Lemma 1.

-

2.

Let . For the reverse direction, we give a constructive proof, i.e., we construct an mMVNN with such that for all .

Let denote the values corresponding to of all possible bundles sorted by value in increasing order, i.e, let with

(18) let with

(19) and for with

(20) In the following, for , we use the notation iff . Thus, we write iff , i.e., iff is not the case.666Note, that in the multidimensional case , the two symbols and have a different meaning, i.e., . Further note that , and exactly correspond to , and respectively in multiset notation. Furthermore, we denote by the Euclidean scalar product on . Then, for all :

(21) (22) where the second equality follows since

(23) (24) (25) which implies that

(26) and

(27) To match the structure of the mMVNN architecture defined in Definition 1, we can write and plug in instead of in Equation 22.777The diagonal matrix is invertible with , since all capacities are strictly larger than 0.

Equation 22 can be rewritten as the following mMVNN

(28) in the matrix-notation of Definition 1 with weight matrices and bias-vectors be given as:

(29) (30) (31) (32) (33) (34) (35) (36) where is an alternative notation to describe Equation 31. Thus, is an mMVNN from Definition 1 with 6 layers in total (i.e., 1 input layer, 1 linear normalization layer D, 3 non-linear hidden layers and 1 output layer) and respective dimensions .

∎

Remark B.1 (Normalization Layer).

Note that our proof of Theorem 1 would also work without the linear normalization layer D. The normalization layer has the advantage that we can use similar hyperparameters as for classical MVNNs. E.g., we can use the same values of the parameters in the initialization scheme as provided in Weissteiner et al. (2023, Section 3.2 and Appendix E).

Remark B.2 (Number of Hidden Layers).

Note that for binary input vectors (corresponding to classical sets, i.e., ), 2 non-linear hidden layers were sufficient (Weissteiner et al. 2022a, Proof of Theorem 1), while for integer-valued input vectors (corresponding to multisets with capacities ), we used 3 non-linear hidden layers for our proof of Theorem 1. It is an interesting open question if 2 non-linear hidden layers would already be sufficient also for our multiset setting with capacities .888Our proof of Theorem 1 works with 1 input layer, 1 linear normalization layer D (which is optional, see Remark B.1), 3 non-linear hidden layers and 1 output layer (i.e., 5 or 6 layers in total). Whereas the (Weissteiner et al. 2022a, Proof of Theorem 1) only required 1 input layer, 2 non-linear hidden layers and 1 output layer (i.e., 4 layers in total).

Remark B.3 (Number of Hidden Neurons).

The dimension of the mMVNN used in the proof of Theorem 1 is just an upper bound. This proof does not imply that such large networks are actually. From a theoretical perspective it is interesting that this upper bound is finite, while for NNs on continuous domains no finite upper bound for perfect approximation exits. In practice much smaller networks are usually sufficient. All the results reported in this paper were achieved by much smaller networks with at most 30 neurons per layer (see Table 2 in Section D.3).

Appendix C ML-powered Demand Query Generation:Theoretical Results

In this section, we prove Theorems 2 and 3.

C.1 Proof of Theorem 2

In this subsection, we first present and prove in Lemma 2 an unconstrained version of Theorem 2, which we later use to prove our main statement from Theorem 2.

Lemma 2 extends (Bikhchandani and Ostroy 2002, Theorem 3.1.). Concretely, we additionally show that if linear clearing prices exist, every minimizer of is a clearing price (while Bikhchandani and Ostroy (2002, Theorem 3.1.) only showed that every clearing price minimizes not specifying if there could be other minimizers of which are not clearing prices).

Lemma 2.

Consider the notation from Definitions 2 and 3 and the objective function . Then it holds that, if a linear clearing price exists, every price vector

| (37) |

is a clearing price and the corresponding allocation is efficient.

Proof of Lemma 2.

We first show in Item 1 that for clearing prices , the corresponding allocation is efficient. Next, in Item 2 we show that every linear clearing price minimizes , i.e., formally . Finally, in Item 3 we show that if linear clearing prices exist, any minimizer of is in fact a linear clearing price.

-

1.

Let be clearing prices and the corresponding supported allocation (see Definition 3). Furthermore, let be any other feasible allocation. Then it holds that:

(38) (39) (40) (41) (42) where the first inequality follows since are clearing prices and fulfill Items 1 and 2 in Definition 3 and because is another feasible allocation. This shows that a supported allocation is efficient.

-

2.

Let be clearing prices and the corresponding supported allocation (see Definition 3). Furthermore, let be any other linear prices. Then it holds that:

(43) (44) (45) (46) (47) (48) (49) where Equation 44 follows by definition of and Equation 45 follows since are clearing prices and the corresponding supported allocation, respectively Thus, we get that

(50) for all linear prices , which concludes the proof.

-

3.

Let be a minimizer of . Moreover, let denote a linear clearing price and let be the corresponding supported allocation (see Definition 3). Furthermore, let . We know from Item 2 that . Furthermore, we get that

(51a) (51b) (51c) (51d) (51e) where the last equation follows since is a clearing allocation supported by and thus . Next, we can subtract from both sides of Equation 51 to obtain

(52) Moreover, from the optimality of it follows that

(53) holds for every .

Using now Equations 52 and 53, it follows that for every

(54) (55) Taken all together, since and for all , we can conclude that by Definition 3 is a linear clearing price with corresponding supported allocation . This finalizes the proof of Lemma 2.

∎

Proof of Theorem 2.

Let be a solution to the constrained minimization problem defined by Equation 9. Moreover, let denote a linear clearing price vector and let be the corresponding supported allocation (see Definition 3).

In Item 2 in the proof of Lemma 2, we have seen that minimizes without any constraints. The clearing price vector obviously satisfies constraint (9b), thus is also a solution to the constrained optimization problem (9). Therefore, in the case that linear clearing prices exist the minimal objective value of the constrained optimization problem from (9) is equal to the minimal objective value of the unconstrained minimization problem (37). From this we can conclude that in the case that linear clearing prices exist, every solution of (9) is also a solution of the optimization problem (37). Finally, Lemma 2 tells us that every solution of the optimization problem (37) is a clearing price and is efficient. ∎

In Theorem 2 we proved that the constraint minimizer of has the same economical favourable properties as the unconstrained minimizer of if linear clearing prices exist. Thus, we do not lose anything in cases where linear clearing prices exist, while due to the constraint (9b) we have the advantage of receiving feasible allocations in the case that no linear clearing price exist.

C.2 Details: Proof of Theorem 3

Before we start with the proof, we will quickly provide a proof for Equation 8, since this equation (that we have not explicitly proven in the main paper) is essential in the proof of Theorem 3.

In the first lemma we prove that is Lipschitz-continuous. While neither , nor nor are continuous, (surprisingly) is continuous.

Lemma 3 (Continuity).

The map from to is Lipschitz-continuous with Lipschitz-constant .999Note that Lipschitz-continuity implies (uniform) continuity. The Lipschitz-constant , given in the proof, only depends on the capacities of and on the number of bidders . The proof also works for any other (possibly non-monotonic) value function instead of .

Proof.

Since is the sum of functions, we first quickly show that is Lipschitz-continuous in and afterwards we will show that also is Lipschitz-continuous in .

From Equation 8 it follows that is linear in and thus Lipschitz-continuous with Lipschitz-constant .

In the remainder of the proof we are going to show that is Lipschitz-continuous in . Let be two price vectors, then we have

| (62) | ||||

| (63) | ||||

| (64) | ||||

| (65) | ||||

| (66) | ||||

| (67) |

and thus

| (68) |

By exchanging the roles of and , we also obtain and thus,

| (69) |

Finally, Equations 68 and 69 together imply

| (70) |

Equation 70 by definition says that is Lipschitz-continuous in with Lipschitz-constant .

So, we finally obtain, that is Lipschitz-continuous in with Lipschitz-constant . ∎

Lemma 4 (Convexity).

The map from to is convex.101010The proof also works for any other (possibly non-monotonic) value function instead of .

Proof.

Since is the sum of functions, we first quickly show that is obviously convex in and afterwards we will show that also is convex in .

From Equation 8 it follows that is linear in and thus convex in .

In the remainder of the proof we are going to show that is convex in . For every and for every , the map is (affine-)linear111111In the following, we will call affine-linear functions “linear” too as commonly done in the literature. in and thus convex in . As the maximum over convex functions is always convex (Danskin 1967; Bertsekas 1971, 1999), is convex in .

So finally we get that is convex in , since it is the sum of convex functions. ∎

Lemma 5 (Sub-gradients).

Let denote the set of utility maximizing bundles w.r.t. for the -th bidder. Then the sub-gradients of the map from to are given by

| (71) |

where denotes the convex hull and denotes the Cartesian product. In particular, for each ,

| (72) |

is a subgradient of with respect to .121212The proof also works for any other (possibly non-monotonic) value function instead of .

Proof.

Since is the sum of functions, we first quickly compute the (sub-)gradient of with respect to and afterwards we will compute the sub-gradients of with respect to .

From Equation 8 it follows that is linear in and thus its sub-gradient is uniquely defined as its gradient , i.e., .

In the remainder of the proof we are going to compute the set of sub-gradients of with respect to with the help of Danskin’s theorem (originally proven by Danskin (1967) and later refined by Bertsekas (1971, 1999)). Let’s define . Then and . Next, we show that fulfills all the assumptions of Danskin’s theorem:

-

•

For every the map is convex and differentiable, since it is (affine-)linear.

-

•

For every the map is continuous, since is discrete and every function is continuous with respect to the discrete topology.

-

•

Furthermore, the set is compact (since it is finite).

Under these three assumptions Danskin’s theorem tells us that

| (73) |

Now we can simply compute for any constant , i.e.,

| (74a) | ||||

| (74b) | ||||

| (74c) | ||||

Plugging in Equation 74 into Equation 73 results in

| (75) |

Note that set of sub-gradients of a sum of real-valued131313Note that Rockafellar (1970, Theorem 23.8) is formulated for proper convex functions with overlapping effective domains that can potentially attain as value. In our case of real-valued function (which implies that they cannot attain ) all convex functions are proper and their effective domain is simply their domain. convex functions, is equal to the sum141414The (Minkowski) sum of two sets and is defined as the set of all possible sums of any element of the first set and any element of the second set . of the sets of sub-gradients of the individual functions (Rockafellar 1970, Theorem 23.8). Further note that the sum of convex hulls of sets is equal to the convex hull of their sum. We use these two insights and Equation 75 to finally compute the set of sub-gradients

| (76a) | |||

| (76b) | |||

| (76c) | |||

| (76d) | |||

| (76e) | |||

| (76f) | |||

| (76g) | |||

| (76h) | |||

which proves the main statement (71) of Lemma 5. This directly implies that for each ,

| (77) |

is an element of the convex hull in (76h) and thus a sub-gradient of with respect to . ∎

Next, Lemma 6 shows that the map from to is Lebesgue-almost everywhere differentiable with (proper) gradient151515Note that the gradient in Equations 78 and 80 actually denotes a classical gradient and not just a sub-gradient.

| (78) |

where denotes the utility maximizing bundle w.r.t. for the -th bidder, which is Lebesgue-almost everywhere unique.

Lemma 6 (A.e. Differentiable).

Let be a tuple of mMVNNs. Then there exists a dense161616The set being dense means that its topological closure covers the whole space, i.e., . subset such that is a Lebesgue null set171717The set being a (Lebesgue) null set means that its -dimensional Lebesgue measure (i.e., the -dimensional volume) . Within this work “a.e.” always corresponds to “Lebesgue almost everywhere”., and that

-

1.

A unique optimizer exists, i.e.,

(79) and

-

2.

the map is differentiable with gradient

(80) which is also the unique sub-gradient, i.e. .

-

3.

The unique optimizer is constant in a local neighborhood of , and thus .181818Note that one could even prove that the gradient is continuous on , while the gradient can have jumps at the null set . The proof also works for any other (possibly non-monotonic) value function instead of .

Proof.

We start this proof by defining and showing a.e. differentiability. Since is the sum of functions, we first quickly show that is obviously differentiable and afterwards we show that each is differentiable on a set . Afterwards we will define as their intersection.

From Equation 8 it follows that is linear in and thus differentiable.

Next, we show that is differentiable a.e. and define . We know already from the proof of Lemma 4 that is convex and Rockafellar (1970, Theorem 25.5 on p. 246) tells us that for any191919There are some very mild technical assumptions in Rockafellar (1970, Theorem 25.5 on p. 246) that do not matter in our case. Rockafellar (1970) assumes that the function is defined on . In our case we could easily extend the domain of our function from to . As Rockafellar (1970, Theorem 25.5 on p. 246) is formulated for proper convex functions that can also attain one could extend any convex function from a convex domain (such as ) to be defined to be outside of that convex domain. Note that if is dense in it is also dense in and that . real-valued convex function there exists a dense set on which the functions is differentiable with the complement of being a null set. Thus, for each , we obtain such a . If functions are differentiable at a point , then their sum is too. Thus, is differentiable on . Since each is dense in , is also dense in . Moreover, it holds that , i.e., the -dimensional Lebesgue measure of vanishes. Putting everything together, we get that is a.e. differentiable (concretely differentiable for all ).

Next, we prove the uniqueness of for every . We know that is differentiable at , and thus we know that the sub-gradient is unique, i.e., . We have already computed this set of sub-gradients in Equation 75 in the proof of Lemma 5. This set can only be a singleton, if is a singleton. Finally, immediately implies Item 1, i.e., the uniqueness of .

Using that is differentiable for every together with Item 1 and Lemma 5, we finally obtain Item 2 for every .

For Item 3 it is crucial that is finite. For every , we know from Item 1 that there is a unique maximizer with . Since is finite, we can define

| (81) |

which has to be strictly larger than 0 for every because of the uniqueness of the maximizer. Equation 81 implies that outperforms every other by at least a margin of . Since is continuous, cannot be “overtaken” by any other within a small neighbourhood of as we will calculate explicitly in the following using the Lipschiz constant of that we derived in the proof of Lemma 3: For any , we have

| (82a) | ||||

| (82b) | ||||

| (82c) | ||||

| (82d) | ||||

From this inequality we obtain, that within an open ball with radius around , the optimizers stay constant for every . Therefore, the differential is zero for all , which concludes the proof of Item 3. ∎

Putting everything together, we can finally prove Theorem 3.

Proof of Theorem 3.

Theorem 3 and most of the statements from Lemmas 3, 4, 5 and 6 can be proven under even less assumptions as we will discuss in the following Remarks C.1 and C.2 which generalize the theory to further settings.

Remark C.1 (General Value Functions).

Remark C.2 (Continuous Input Space ).

Theorem 3 and all of the statements from Lemmas 3, 4, 5 and 6 except Item 3 from Lemma 6 are also true if one replaces the finite set by any (possibly non-discrete) compact set (if one extends the definition of in the natural way from to ). When combining Remarks C.1 and C.2 one has to assume that the are continuous for our proof.202020Note that if is finite, every function is continuous by definition. Item 3 from Lemma 6 can be violated for compact if .212121Note that, while Item 3 from Lemma 6 was used for the intuitive sketch of the proof of Theorem 3 in the main paper, Item 3 from Lemma 6 is not necessary at all for the mathematical rigorous proof of Theorem 3 given in Section C.2.

Remark C.3 (Piece-wise Linear).

In our case of finite , one can intuitively see with similar arguments as in the proof of Lemma 4, that is piece-wise linear as a sum over a linear function and functions which are the maxima over finitely many linear functions.

Appendix D Experiment Details

In this section, we present all details of our experiments from Section 6.

D.1 SATS Domains

In this section, we provide a more detailed overview of the four SATS domains, which we use to experimentally evaluate ML-CCA:

-

•

Global Synergy Value Model (GSVM) (Goeree and Holt 2010) has 18 items with capacities for all , regional and national bidder. In GSVM the value of a package increases by a certain percentage with every additional item of interest. Thus, the value of a bundle only depends on the total number of items contained in a bundle which makes it one of the simplest models in SATS. In fact, bidders’ valuations exhibit at most two-way(i.e., pairwise) interactions between items.

-

•

Local Synergy Value Model (LSVM) (Scheffel, Ziegler, and Bichler 2012) has items with capacities for all , regional and national bidder. Complementarities arise from spatial proximity of items.

-

•

Single-Region Value Model (SRVM) (Weiss, Lubin, and Seuken 2017) has items with capacities and bidders (categorized as local, high frequency, regional, or national) and models UK 4G spectrum auctions.

-

•

Multi-Region Value Model (MRVM) (Weiss, Lubin, and Seuken 2017) has items with capacities for all and bidders (local, regional, or national) and models large Canadian 4G spectrum auctions.

In the efficiency experiments in this paper, we instantiated for each SATS domain the synthetic CA instances with the seeds . We used SATS version 0.8.1.

D.2 Compute Infrastructure

All experiments were conducted on a compute cluster running Debian GNU/Linux 10 with Intel Xeon E5-2650 v4 2.20GHz processors with 24 cores and 128GB RAM and Intel E5 v2 2.80GHz processors with 20 cores and 128GB RAM and Python 3.8.10.

D.3 Hyperparameter Optimization

In this section, we provide details on our exact HPO methodology and the ranges that we used.

We separately optimized the HPs of the mMVNNs for each bidder type of each domain, using a different set of SATS seeds than for all other experiments in the paper. Specifically, for each bidder type, we first trained an mMVNN using as initial data points the demand responses of an agent of that type during consecutive CCA clock rounds, and then measured the generalization performance of the resulting network on a validation set that was created by drawing price vectors where the price of each item was drawn uniformly at random from the range of zero to three times the average maximum value of an agent of that type for a single item (which was determined using separate seeds, see validation set 2 in Figure 1). The number of seeds used to evaluate each model was equal for all models and set to 10. Finally, for each bidder type we selected the set of HPs that performed the best on this validation set with respect to the coefficient of determination (). The full range of HPs tested for all agent types and all domains is shown in Table 2, while the winning configurations are shown in Table 3.

Additionally, we determined the set of HPs with the best generalization performance on validation set 2 using as evaluation metric a shift-invariant variation of , defined as:

| (83) |

where is the true value of the bidder for the -th bundle, is the neural network’s predicted value for that bundle, and and are their empirical means, respectively. The reason that we opted for this shift-invariant version of is that, as explained in Section 3.1, learning the true value functions of the agents up to a constant shift suffices for our query generation procedure as described in Section 4. Surprisingly, in all domains our mechanism performed slightly worse with those HPs, with the maximum efficiency delta between the two configurations being % in LSVM. However, in all domains results were qualitatively identical. The winning configurations for both metrics are shown in Tables 3 and 4. In all domains we chose the configurations from Table 3 for our efficiency experiments.

| Hyperparameter | HPO-Range |

|---|---|

| Non-linear Hidden Layers | [1,2,3] |

| Neurons per Hidden Layer | [8, 10, 20, 30] |

| Learning Rate | (1e-4, 1e-2) |

| Epochs222222For GSVM and LSVM, the number of epochs was fixed to 30 | [30, 50, 70, 100] |

| L2-Regularization | (1e-8, 1e-2) |

| Linear Skip Connections232323For the definition of (m)MVNNs with a linear skip connection, please see Weissteiner et al. (2023, Definition F.1) | [True, False] |

| Domain | Bidder Type | # Hidden Layers | # Hidden Units | Lin. Skip | Learning Rate | L2 Regularization | Epochs |

| GSVM | Regional | 2 | 20 | False | 0.005 | 0.00001 | 30 |

| National | 3 | 30 | True | 0.001 | 0.000001 | 30 | |

| LSVM | Regional | 1 | 30 | True | 0.01 | 0.000001 | 30 |

| National | 3 | 20 | False | 0.005 | 0.0001 | 30 | |

| SRVM | Local | 2 | 20 | True | 0.01 | 0.0001 | 30 |

| Regional | 1 | 20 | True | 0.01 | 0.0001 | 50 | |

| National | 1 | 30 | False | 0.005 | 0.00001 | 70 | |

| High Frequency | 2 | 20 | False | 0.01 | 0.00001 | 30 | |

| MRVM | Local | 3 | 20 | True | 0.005 | 0.000001 | 100 |

| Regional | 2 | 20 | True | 0.001 | 0.001 | 100 | |

| National | 3 | 20 | True | 0.001 | 0.0001 | 50 |

| Domain | Bidder Type | # Hidden Layers | # Hidden Units | Lin. Skip | Learning Rate | L2 Regularization | Epochs |

| GSVM | National | 3 | 10 | True | 0.001 | 0.001 | 30 |

| Regional | 2 | 10 | True | 0.01 | 0.001 | 30 | |

| LSVM | National | 1 | 10 | True | 0.005 | 0.01 | 30 |

| Regional | 3 | 20 | True | 0.005 | 0.0001 | 30 | |

| SRVM | Local | 2 | 30 | True | 0.01 | 0.0001 | 30 |

| Regional | 2 | 20 | True | 0.01 | 0.000001 | 50 | |

| National | 1 | 20 | True | 0.01 | 0.0001 | 50 | |

| High Frequency | 2 | 30 | True | 0.01 | 0.00001 | 70 | |

| MRVM | National | 1 | 20 | True | 0.001 | 0.000001 | 30 |

| Regional | 3 | 20 | True | 0.001 | 0.000001 | 50 | |

| Local | 2 | 20 | False | 0.001 | 0.000001 | 30 |

D.4 Details on mMVNN Training

Remark D.1 (Other ML-models).