Faster Stochastic Variance Reduction Methods for Compositional MiniMax Optimization

Abstract

This paper delves into the realm of stochastic optimization for compositional minimax optimization—a pivotal challenge across various machine learning domains, including deep AUC and reinforcement learning policy evaluation. Despite its significance, the problem of compositional minimax optimization is still under-explored. Adding to the complexity, current methods of compositional minimax optimization are plagued by sub-optimal complexities or heavy reliance on sizable batch sizes. To respond to these constraints, this paper introduces a novel method, called Nested STOchastic Recursive Momentum (NSTORM), which can achieve the optimal sample complexity of to obtain the -accuracy solution. We also demonstrate that NSTORM can achieve the same sample complexity under the Polyak-Łojasiewicz (PL)-condition—an insightful extension of its capabilities. Yet, NSTORM encounters an issue with its requirement for low learning rates, potentially constraining its real-world applicability in machine learning. To overcome this hurdle, we present ADAptive NSTORM (ADA-NSTORM) with adaptive learning rates. We demonstrate that ADA-NSTORM can achieve the same sample complexity but the experimental results show its more effectiveness. All the proposed complexities indicate that our proposed methods can match lower bounds to existing minimax optimizations, without requiring a large batch size in each iteration. Extensive experiments support the efficiency of our proposed methods.

1 Introduction

In recent years, minimax optimization theory has been considered more attractive due to the broad range of machine learning applications, including generative adversarial networks Goodfellow et al. (2014); Arjovsky, Chintala, and Bottou (2017); Gulrajani et al. (2017), adversarial training of deep neural networks Madry et al. (2018); Wang et al. (2021); Qu et al. (2023), robust optimization Chen et al. (2017); Mohri, Sivek, and Suresh (2019); Qu et al. (2022), and policy evaluation on reinforcement learning Sutton and Barto (2018); Hu et al. (2019); Zhang et al. (2021). At the same time, many machine learning problems can be formulated as compositional optimizations, for example, model agnostic meta-learning Finn, Abbeel, and Levine (2017); Gao, Li, and Huang (2022) and risk-averse portfolio optimization Zhang and Lan (2020); Shapiro, Dentcheva, and Ruszczynski (2021). Due to the important growth of these two problems in machine learning fields, the compositional minimax problem should be also clearly discussed, which can be formulated as follows:

| (1) |

where , , , and are convex and compact sets. Suppose that is a strongly concave objective function with respect to for all .

Numerous research studies have been dedicated to investigating the convergence analysis of minimax optimization problems Nemirovski et al. (2009); Palaniappan and Bach (2016); Lin, Jin, and Jordan (2020); Yang, Kiyavash, and He (2020); Chen et al. (2020); Rafique et al. (2022) across diverse scenarios. Various methodologies have been devised to address these challenges. Approaches such as Stochastic Gradient Descent Ascent (SGDA) have been proposed Lin, Jin, and Jordan (2020), accompanied by innovations like variance-reduced SGDA Luo et al. (2020); Xu et al. (2020) that aim to expedite convergence rates. Moreover, the application of Riemannian manifold-based optimization has been explored Huang, Gao, and Huang (2020) across different minimax scenarios, showcasing the breadth of methodologies available. However, all of these methods are only designed for the non-compositional problem. It indicates that the stochastic gradient can be assumed as an unbiased estimation of the full gradient of both the two sub-problems. Because it is too difficult to get an unbiased estimation in compositional optimization, these methods cannot be directly used to optimize the compositional minimax problem.

Recent efforts have yielded just two studies on the nonconvex compositional minimax optimization problem (1), named Stochastic Compositional Gradient Descent Ascent (SCGDA) Gao et al. (2021) and Primal-Dual Stochastic Compositional Adaptive (PDSCA) Yuan et al. (2022). However, they only can obtain the sample complexity for achieving the -accuracy solution, which limits the applicability in many machine learning scenarios. Consequently, there is a pressing need to devise a more streamlined approach capable of tackling this challenge. In addition, some compositional minimization optimizations have been proposed, such as SCGD Wang, Fang, and Liu (2017), STORM Cutkosky and Orabona (2019), and RECOVER Qi et al. (2021). They may not be directly utilized for the minimax problem (1), because the minimization of objective depends on the maximization of objective for any . Furthermore, the combined errors from Jacobian and gradient estimators worsen challenges in both sub-problems. We aim to develop an approach effectively tackling the compositional minimax problem (1), optimizing sample complexities efficiently, without requiring a large batch size.

In this paper, to address the aforementioned challenges, we first develop a novel Nested STOchastic Recursive Momentum (NSTORM) method for the problem (1). The NSTORM method leverages the variance reduction technique Cutkosky and Orabona (2019) to estimate the inner/outer functions and their gradients. The theoretical result shows that our proposed NSTORM method can achieve the optimal sample complexity of . To the best of our knowledge, NSTORM is the first method to match the best sample complexity in existing minimax optimization studies Huang, Wu, and Hu (2023); Luo et al. (2020) without requiring a large batch size. We also demonstrate that NSTORM can achieve the same sample complexity under the Polyak-Łojasiewicz (PL)-condition, which indicates an insightful extension of NSTORM. In particular, the central idea of our proposed NSTORM method and analysis has two aspects: 1) the variance reduction is applied to both function and gradient values, which is different from Gao et al. (2021); Yuan et al. (2022) and 2) the estimator of the inner gradient is updated with a projection to ensure that the error can be bounded regardless of the minimization sub-problem. Furthermore, because NSTORM requires a small learning rate to obtain the optimal sample complexity, it may be difficult to set in real-world scenarios. To address this issue, we take advantage of adaptive learning rates in NSTORM and design an adaptive version, called ADAptive NSTORM (ADA-NSTORM). We also demonstrate that ADA-NSTORM can also obtain the same sample complexity as NSTORM, i.e., and performs better in practice without tuning the learning rate manually.

2 Related Work

Compositional minimization problem: The compositional minimization optimization problem is common in many machine learning scenarios, e.g., meta-learning Finn, Abbeel, and Levine (2017) and risk-averse portfolio optimization Zhang and Lan (2020), which can be defined as follows:

| (2) |

A typical challenge to optimizing the compositional minimization problem is that we cannot obtain an unbiased estimation of the full gradient by SGD, i.e., . To address this issue, some methods have been developed in the past few years. For example, Wang, Fang, and Liu (2017) uses stochastic gradient for the inner function value when computing the stochastic gradient. However, the convergence rate only can achieve for the nonconvex objective, which has an obvious convergence gap to the regular SGD method. To improve the convergence speed, some advanced variance reduction techniques have been leveraged into Stochastic Compositional Gradient Descent (SCGD) Wang, Fang, and Liu (2017). For example, SAGA Zhang and Xiao (2019a), SPIDER Fang et al. (2018), and STORM Cutkosky and Orabona (2019) were leveraged into SCGD and achieved a better convergence result, i.e., . Recently, some studies Yuan, Lian, and Liu (2019); Zhang and Xiao (2021); Jiang et al. (2022); Tarzanagh et al. (2022) bridged the gap between stochastic bilevel or multi-level optimization problems and stochastic compositional problems, and developed efficient methods. However, all of these methods only investigated the convergence result for minimization problems, ignoring the maximization sub-problem.

Minimax optimization problem: The minimax optimization problem is an important type of model and leads to many machine learning applications, e.g., adversarial training and policy optimization. Typically, the minimax optimization problem can be defined as follows:

| (3) |

Note that both and in (3) are trained from the same dataset. Currently, the prevailing approach for solving minimax optimization problems involves alternating between optimizing the minimization and maximization sub-problems. Stochastic Gradient Descent Ascent (SGDA) methods Lin, Jin, and Jordan (2020); Yan et al. (2020); Yuan and Hu (2020) have been proposed as initial solutions to address this problem. Subsequently, accelerated gradient descent ascent methods Luo et al. (2020); Xu et al. (2020) emerged, leveraging variance reduction techniques to tackle stochastic minimax problems based on the variance reduction techniques. Additionally, research efforts have been made to explore non-smooth nonconvex-strongly-concave minimax optimization Huang, Gao, and Huang (2020); Chen et al. (2020). Moreover, Huang, Gao, and Huang (2020) proposed the Riemannian stochastic gradient descent ascent method and some variants for the Riemannian minimax optimization problem. (Qiu et al., 2020) reformulated nonlinear temporal-difference learning as a minimax optimization problem and proposed the single-timescale SGDA method. However, all of these methods fail to address the compositional structure inherent in the compositional minimax optimization problem presented in (1).

3 The Proposed Method

3.1 Design Challenge

Compared to the conventional minimax optimization problem, the main challenge in compositional minimax optimization is that we cannot obtain the unbiased gradient of the objective function . Although we can access the unbiased estimation of each function and its gradient, i.e., , and , it is still difficult to obtain an unbiased estimation of the gradient . This is due to the fact that the expectation over cannot be moved into the gradient , i.e., . Similarly, we cannot get the unbiased estimation of the function value such that .

Motivated by the aforementioned challenge, one potential approach to improve the evaluation of both function values and Jacobians is to utilize variance-reduced estimators. These estimators can effectively reduce estimation errors. However, applying variance-reduced estimators directly to minimax optimization in compositional minimization Zhang and Lan (2020); Qi et al. (2021) is not straightforward. This is because if the estimators for Jacobians are not bounded, the estimation error may increase for the maximization sub-problem. In order to address this issue, Gao et al. (2021) and Yang, Zhang, and Fang (2022) have developed SCGDA and PDSCA methods to approach the compositional minimax optimization, respectively. However, they only obtain the sample complexity as to achieve -accuracy solution, which is much slower than existing compositional minimization or minimax optimization methods. To obtain the optimal sample complexity without requiring large batch sizes, our proposed method modifies the STORM (Cutkosky and Orabona, 2019; Jiang et al., 2022) estimator and incorporates gradient projection techniques. This modification ensures that the Jacobians can be bounded for the minimization sub-problem and the gradients are projected onto a convex set for the maximization problem, thereby reducing gradient estimation errors.

3.2 Nested STOchastic Recursive Momentum (NSTORM)

In this subsection, we will present our proposed method, named the Nested STOchastic Recursive Momentum (NSTORM), to solve the compositional minimax problem in (1). We aim to find an -accuracy to achieve low sample complexity without using large batch sizes.

Our proposed NSTORM method is illustrated in Algorithm 1. Inspired by STROM (Cutkosky and Orabona, 2019), the NSTORM method leverages similar variance-reduced estimators for both the two sub-problems in (1). Note that our goal is to find an -stationary point with low sample complexity. As we mentioned before because we cannot obtain the unbiased estimation of , we use estimators and to estimate the inner function and its gradient , respectively. In each iteration , the two estimators and can be computed by:

| (4) |

| (5) |

where . Note that the projection operation aims to bound the error of the stochastic gradient estimator, which also facilitates the outer level estimator. More specifically, we need to reduce the variance of the estimator (because true gradients are in the projected domain, projection does not degrade the analysis); on the other side, we must avoid the variance of the estimator accumulating after the outer level, i.e., maximization sub-problem.

For the outer level function, if we use the same strategy to compute the gradient as SCGDA Gao et al. (2021), i.e., , we have to use large batches and the variance produced by cannot be bounded. Therefore, we also estimate the outer function by the NSTORM method, which results in a tighter bound for . As such, we estimate the gradient by , which can be computed by:

| (6) |

Based on the chain rule, the estimated compositional gradient is equal to , i.e., . To avoid using large batches, we estimate the outer function by based on the NSTORM estimator, which can be computed by:

| (7) |

where . After obtaining the estimators and , we can use the following strategy to update the parameters and in the compositional minimax problem:

| (8) |

where is the step size, and is the learning rate. Note that in the first iteration, we evaluate all estimators by directly computing inner level function and gradients, i.e., line 4 in Algorithm 1. The reason we choose two level estimators is to avoid using large batches, and only need to draw two samples, i.e., and , to calculate estimators for updating and , respectively. The common idea to achieve the optimal solution of minimax Lin, Jin, and Jordan (2020) is that the step size of should be smaller than . In addition, the compositional minimization sub-problem will generate larger errors, which incurs more challenges for NSTORM. Particularly, in (8), if we simply set the same step sizes of and , our proposed NSTORM method may fail to converge, which is confirmed in the subsequent proof. Therefore, we set to ensure that the step size of is less than .

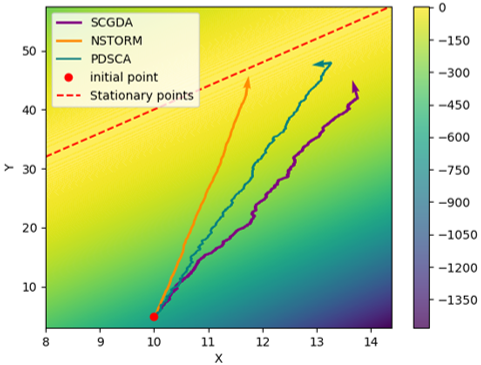

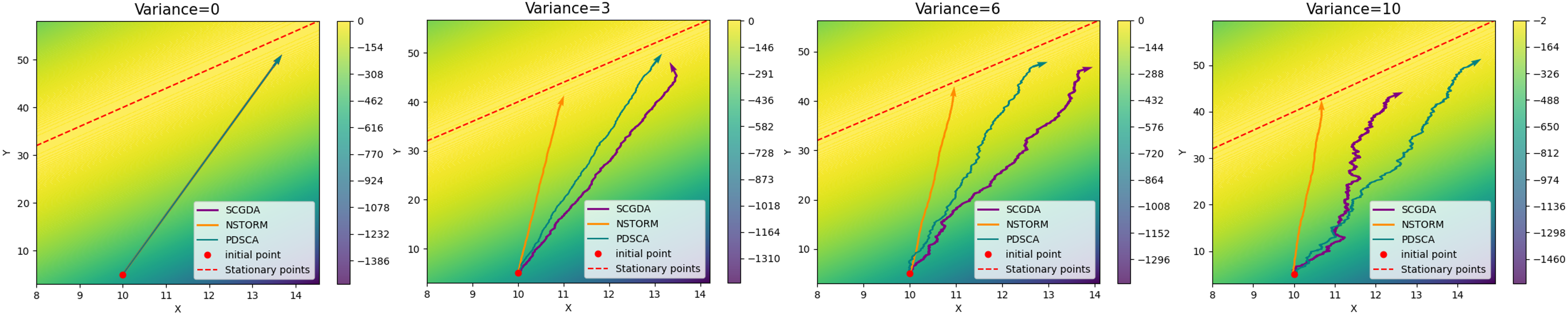

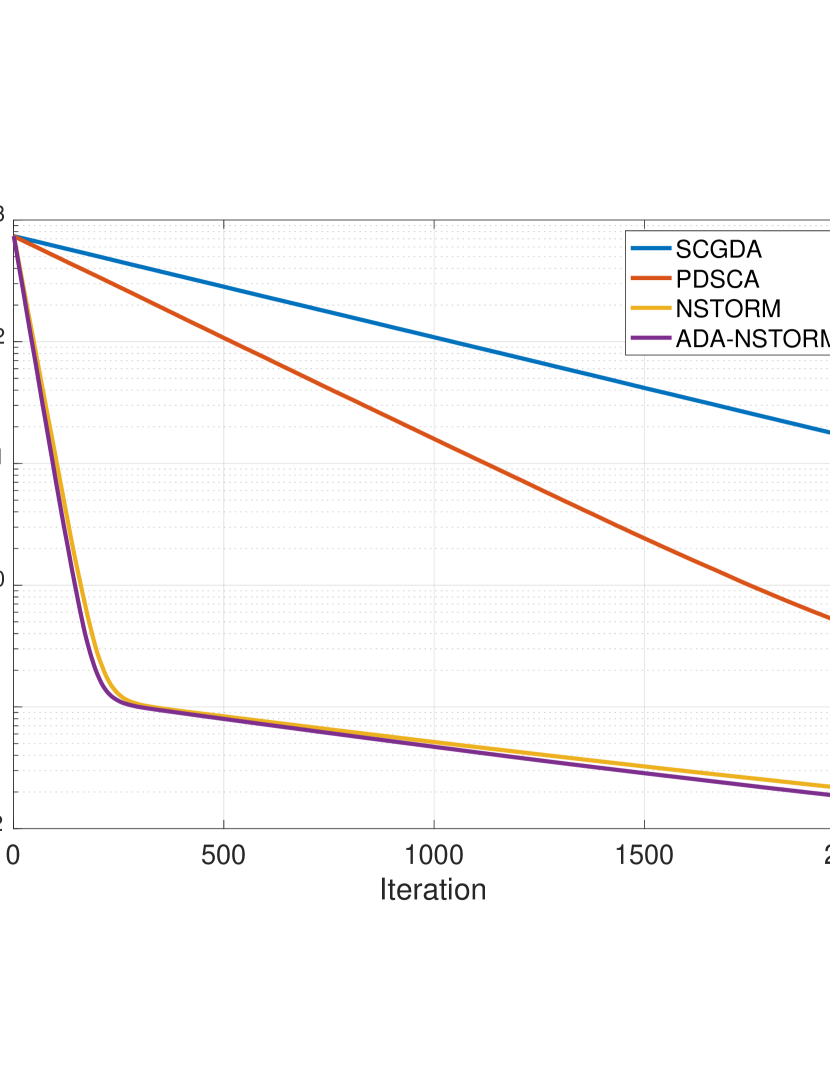

To clearly explain the advantages of NSTORM, a toy example is illustrated in Figure 1. Consider the following concrete example of a nonconvex-strongly-concave function.: , where . In Figure 1, we simulate these stochastic oracles by adding noise when obtaining function gradients and function values. This function obtains the biased estimation in the minimization sub-problem affording the problem in (1). It can be observed that NSTORM performs more robustness on noisy and biased estimation, which brings up an opportunity to obtain the optimal solution with shorter and smoother paths compared to other benchmarks.

3.3 Convergence Analysis of NSTORM

In what follows, we will prove the convergence rate of our proposed NSTROM method in Algorithm 1. We first state some commonly-used assumptions for compositional and minimax optimizations Gao et al. (2021); Wang, Fang, and Liu (2017); Xian et al. (2021); Yuan, Lian, and Liu (2019); Zhang and Lan (2020) to facilitate our convergence analysis. In order to simplify the notations and make the paper coherence, we denote for in the following assumptions, where and .

Assumption 1.

(Smoothness) There exists a constant , such that

where . In addition, we assume that there exists a constant , such that

where .

Assumption 2.

(Bounded Gradient) There exist two constants and , where the two gradients can be bounded by and .

Assumption 3.

(Bounded Variance) There exist three constants , , and , where the three kinds of variance can be bounded by:

Assumption 4.

(Strongly Concave) There exists a constant , such that

where and .

Similar to existing minimax studies Lin, Jin, and Jordan (2020); Xian et al. (2021), we also use -point of , i.e., as the convergence criterion in our focused compositional minimax problem, where and . We demonstrate that is differentiable and -smooth, where , and is -Lipschitz, which has some differences compared to the minimax optimization Lin, Jin, and Jordan (2020). We defer detailed proof in the supplementary.

Now, we can obtain the following convergence result of our proposed NSTORM method in Algorithm 1 to solve the compositional minimax problem in (1):

Theorem 1.

Remark 1. As discussed in the previous section, our proposed NSTORM method in Algorithm 1 results in tighter bounds for all variances, i.e., , , and , which makes NSTROM method converge faster comparing with existing studies. Therefore, it is very important to show the upper bounds of these variances. We will show the detailed analysis in the supplementary.

Remark 2. Without loss of generality, let , we have . Therefore, our proposed NSTORM method has a convergence rate of . Let , we have . Because we only need two samples, i.e., , to estimate the stochastic to compute the gradient in each iteration, and need iterations. Therefore, our NSTORM method requires sample complexity of for finding an -accuracy point of the compositional minimax problem in (1). Because the SCGDA method Gao et al. (2021) only achieves with requiring a large batch size as , it is observed that our proposed NSTROM method improves the convergence rate significantly.

Remark 3. It is worth noting that if we moderate the assumption of with respect to to follow the PL-condition instead of strongly-concave in Assumption 4, NSTORM can also obtain the sample complexity, i.e., . To the best of our knowledge, this is the first study to design the method for compositional minimax optimization, which highlights the extensibility and applicability of NSTORM. The detailed description will be shown in the supplementary.

4 ADAptive-NSTORM (ADA-NSTORM)

4.1 Learning Procedure of ADA-NSTORM

According to the analysis of variance in the NSTORM method, due to the large variance of the two-level estimator, we must select a smaller learning step to update parameters and . As a result, this degrades the applicability of NSTORM. Adaptive learning rates Huang, Gao, and Huang (2020); Huang, Wu, and Hu (2023) have been developed to accelerate many optimization methods including (stochastic) gradient-based methods based on momentum technology. Therefore, we leverage adaptive learning rates in NSTORM and propose ADAptive NSTORM (ADA-NSTORM) method, which is illustrated in Algorithm 2.

In each iteration , we first use the NSTORM method to update all estimators related to the inner/outer functions and their gradients. At Line 13 in Algorithm 2, we generate the adaptive matrices and for the two variables and , respectively. In particular, the general adaptive matrix is updated for the variable , and the global adaptive matrix is for . It is worth noting that we can generate the two matrices and by a class of adaptive learning rates generators such as Adam Kingma and Ba (2014), AdaBelief, Zhuang et al. (2020), AMSGrad Reddi, Kale, and Kumar (2018), AdaBound Luo, Xiong, and Liu (2019). Due to the space limitation, we only discuss Adam Kingma and Ba (2014) in the main paper, and other Ada-type generators will be deferred in the supplementary. In particular, the Adam generator can be computed by:

| (9) |

| (10) |

where , and . Due to the biased full gradient in the compositional minimax problem, we leverage the gradient estimator and to update adaptive matrices instead of simply using the gradient, i.e., and (Huang, Gao, and Huang, 2020; Huang, Wu, and Hu, 2023). After obtaining adaptive learning matrices and , we use adaptive stochastic gradient descent to update the parameters and as follows:

where and are step sizes for updating and , respectively. At Line 15 in Algorithm 2, we use the momentum iteration to further update the primal variable and the dual variable as follows:

| (11) |

4.2 Convergence analysis of ADA-STORM

We will introduce one additional assumption to facilitate the convergence analysis of ADA-NSTORM.

Assumption 5.

In Algorithm 2, the adaptive matrices , for updating the variables satisfies and , where is an appropriate positive number. We consider the adaptive matrics , for updating the variables satisfies , where denotes a -dimensional identity matrix.

Remark 4. Assumption 5 ensures that the adaptive matrices , are positive definite, which is widely used in Huang, Gao, and Huang (2020); Huang, Wu, and Hu (2023); Huang (2023). This Assumption also guarantees that the global adaptive matrices , are positive definite and bounded, resulting in mild conditions. To support the mildness of this assumption, we will empirically show that the learning performance does not have obvious changes by varying the bound of and . In particular, we also show the requirement of some popular Adam-type generators in the supplementary and provide the corresponding advice on compositional minimax optimization.

Theorem 2.

Remark 5. Without loss of generality, let and . The proof of Theorem 2 is deferred in supplementary. From Theorem 2, given , where , , , we can see that , , . Then, we can get the convergence rate . Therefore, to achieve -accuracy solution, the total sample complexity is . It is worth noting that the term is bounded to the existing adaptive learning rates in Adam algorithm Kingma and Ba (2014) and so on. Yuan et al. (2022) develops a PDSCA method with adaptive learning rates to approach the compositional minimax optimization problem and achieves complexity. However, Yuan et al. (2022) sets , which is difficult to know in practice.

5 Experiments

In this section, we present the results of our experiments that assess the performance of two proposed methods: NSTORM and ADA-NSTORM in the deep AUC problem Yuan et al. (2020, 2022). To establish a benchmark, we compare our proposed methods against existing compositional minimax methods, namely SCGDA (Gao et al., 2021) and PDSCA Yuan et al. (2022). To optimize the AUC loss, the outer function corresponds to an AUC loss and the inner function represents a gradient descent step for minimizing a cross-entropy loss, as Yuan et al. (2022). The deep AUC problem can be formulated as follows:

| (12) |

The function is to optimize the AUC score. The inner function aims to optimize the average cross-entropy loss . is a hyper-parameter.

Rather than the deep AUC problem, we also evaluate our proposed methods on the risk-averse portfolio optimization problem Shapiro, Dentcheva, and Ruszczynski (2021); Zhang et al. (2021) and the policy evaluation in reinforcement learning Yuan, Lian, and Liu (2019); Zhang and Xiao (2019b). All experimental setups and results will be shown in the supplementary.

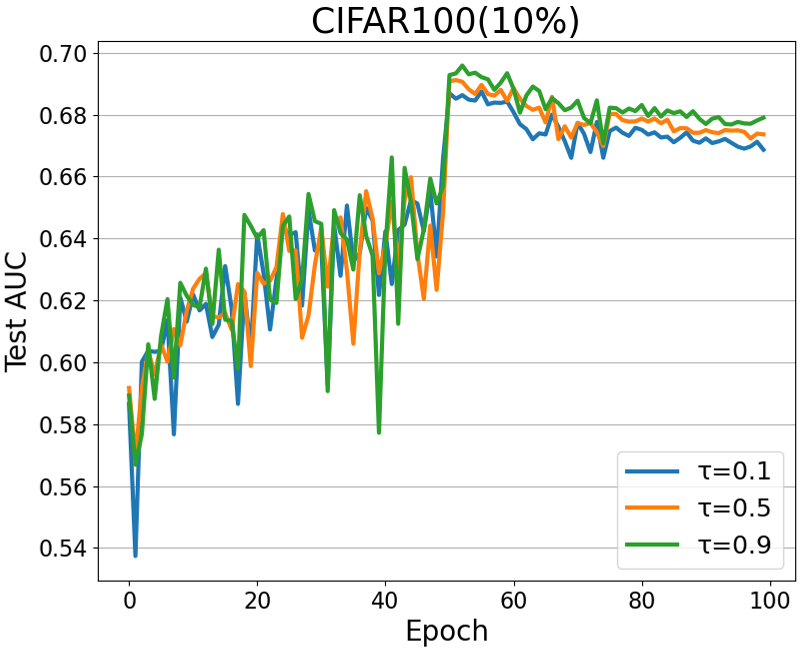

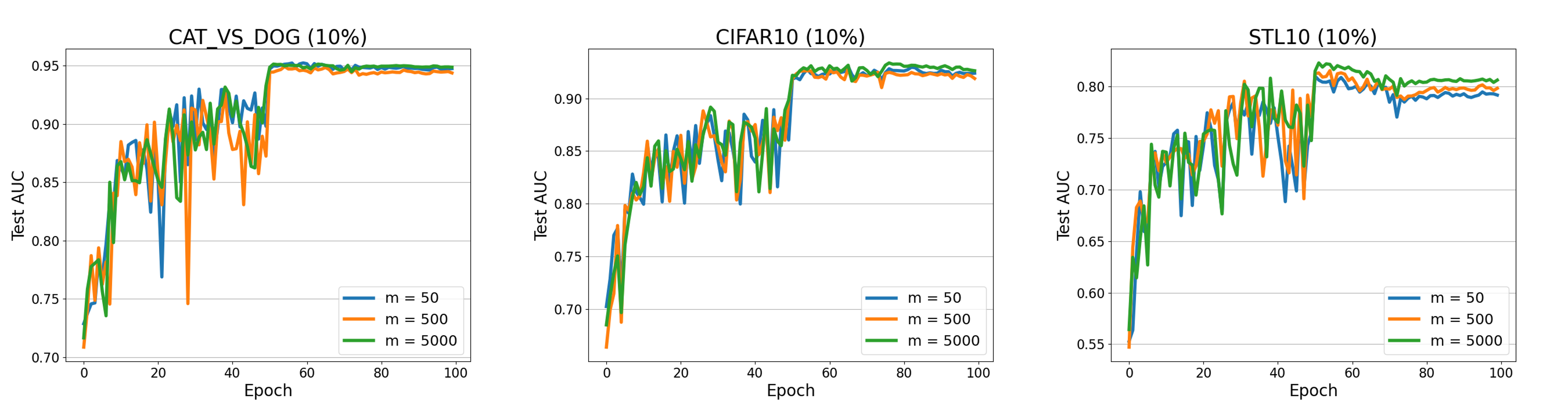

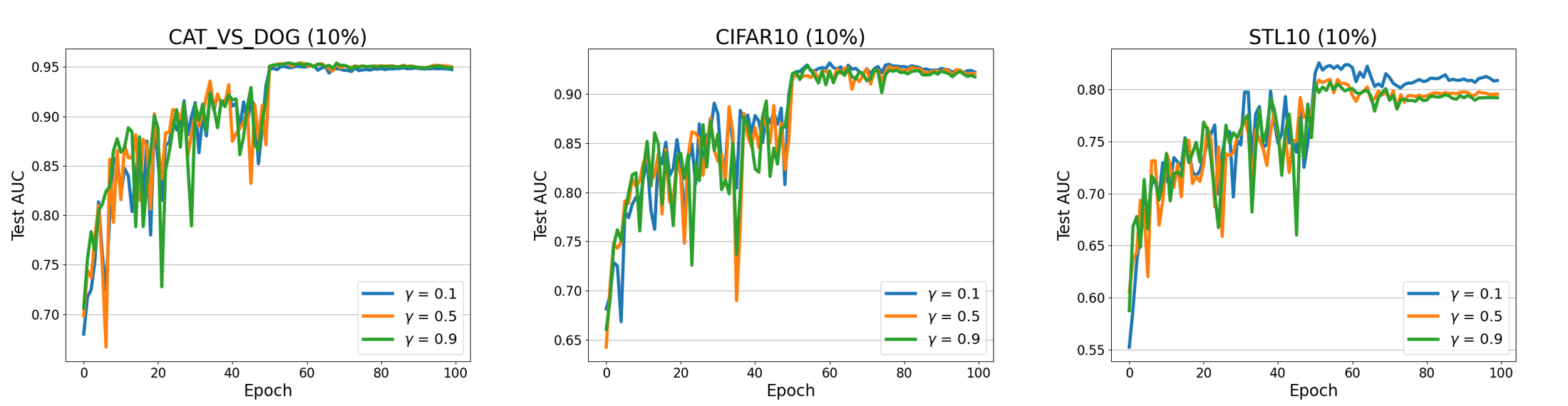

Learning Model and Datasets. We employ four distinct image classification datasets in our study: CAT_vs_DOG, CIFAR10, CIFAR100 Krizhevsky, Hinton et al. (2009), and STL10 Coates, Ng, and Lee (2011). To create imbalanced binary variants prioritizing AUC optimization, we followed Yuan et al. (2020) methodology. Similarly, as in Yuan et al. (2022), ResNet20 He et al. (2016) was used. Weight decay was consistently set to 1e-4. Each method was trained with batch size 128, spanning 100 epochs. We varied parameter (50, 500, 5000) and set (1, 0.9, 0.5). Learning rate reduced by 10 at 50% and 75% training. Also, is set to 0.9. For robustness, each experiment was conducted thrice with distinct seeds, computing mean and standard deviations. Notably, the ablation study focused on the CIFAR100 dataset, 10% imbalanced ratio, as detailed in the main paper.

| Datasets | CAT_vs_DOG | CIFAR10 | ||||||

|---|---|---|---|---|---|---|---|---|

| imratio | SCGDA | PDSCA | NSTORM | ADA-NSTORM | SCGDA | PDSCA | NSTORM | ADA-NSTORM |

| 1% | 0.750 | 0.792 | 0.786 | 0.786 | 0.679 | 0.699 | 0.689 | 0.703 |

| 0.004 | 0.009 | 0.001 | 0.011 | 0.011 | 0.008 | 0.003 | 0.008 | |

| 5% | 0.826 | 0.890 | 0.895 | 0.901 | 0.782 | 0.878 | 0.882 | 0.894 |

| 0.006 | 0.006 | 0.006 | 0.004 | 0.006 | 0.003 | 0.002 | 0.005 | |

| 10% | 0.857 | 0.932 | 0.932 | 0.933 | 0.818 | 0.926 | 0.926 | 0.931 |

| 0.009 | 0.002 | 0.005 | 0.002 | 0.004 | 0.001 | 0.001 | 0.001 | |

| 30% | 0.897 | 0.969 | 0.970 | 0.972 | 0.882 | 0.953 | 0.953 | 0.955 |

| 0.008 | 0.002 | 0.001 | 0.001 | 0.005 | 0.001 | 0.002 | 0.001 | |

| Datasets | CIFAR100 | STL10 | ||||||

| imratio | SCGDA | PDSCA | NSTORM | ADA-NSTORM | SCGDA | PDSCA | NSTORM | ADA-NSTORM |

| 1% | 0.588 | 0.583 | 0.583 | 0.593 | 0.670 | 0.682 | 0.659 | 0.657 |

| 0.007 | 0.004 | 0.007 | 0.002 | 0.006 | 0.016 | 0.013 | 0.003 | |

| 5% | 0.641 | 0.651 | 0.648 | 0.655 | 0.734 | 0.775 | 0.779 | 0.781 |

| 0.007 | 0.006 | 0.003 | 0.007 | 0.007 | 0.003 | 0.005 | 0.007 | |

| 10% | 0.673 | 0.708 | 0.709 | 0.715 | 0.779 | 0.824 | 0.827 | 0.833 |

| 0.005 | 0.006 | 0.002 | 0.006 | 0.014 | 0.011 | 0.007 | 0.004 | |

| 30% | 0.713 | 0.787 | 0.786 | 0.787 | 0.843 | 0.901 | 0.893 | 0.895 |

| 0.002 | 0.007 | 0.001 | 0.001 | 0.010 | 0.002 | 0.005 | 0.007 | |

5.1 Performance Evaluation

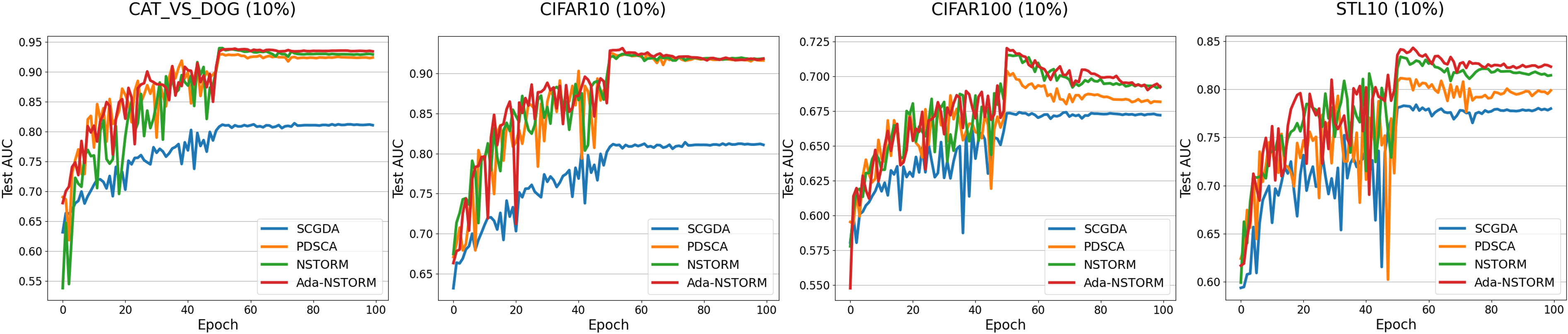

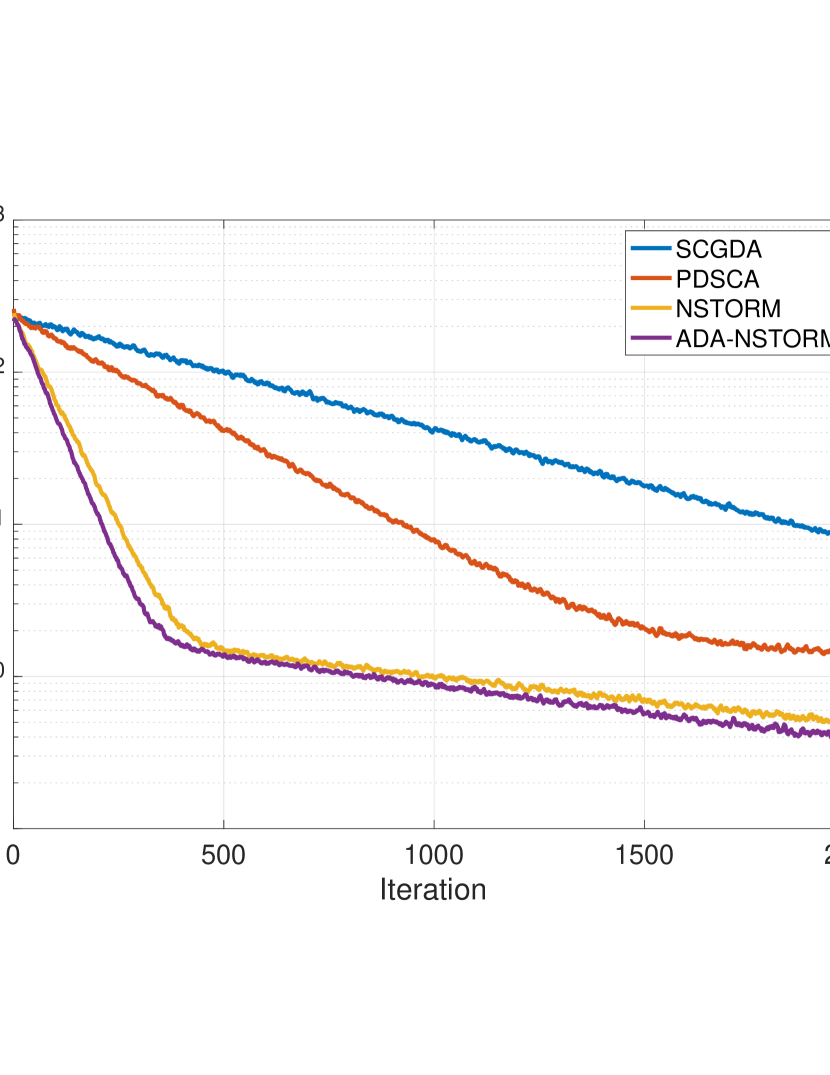

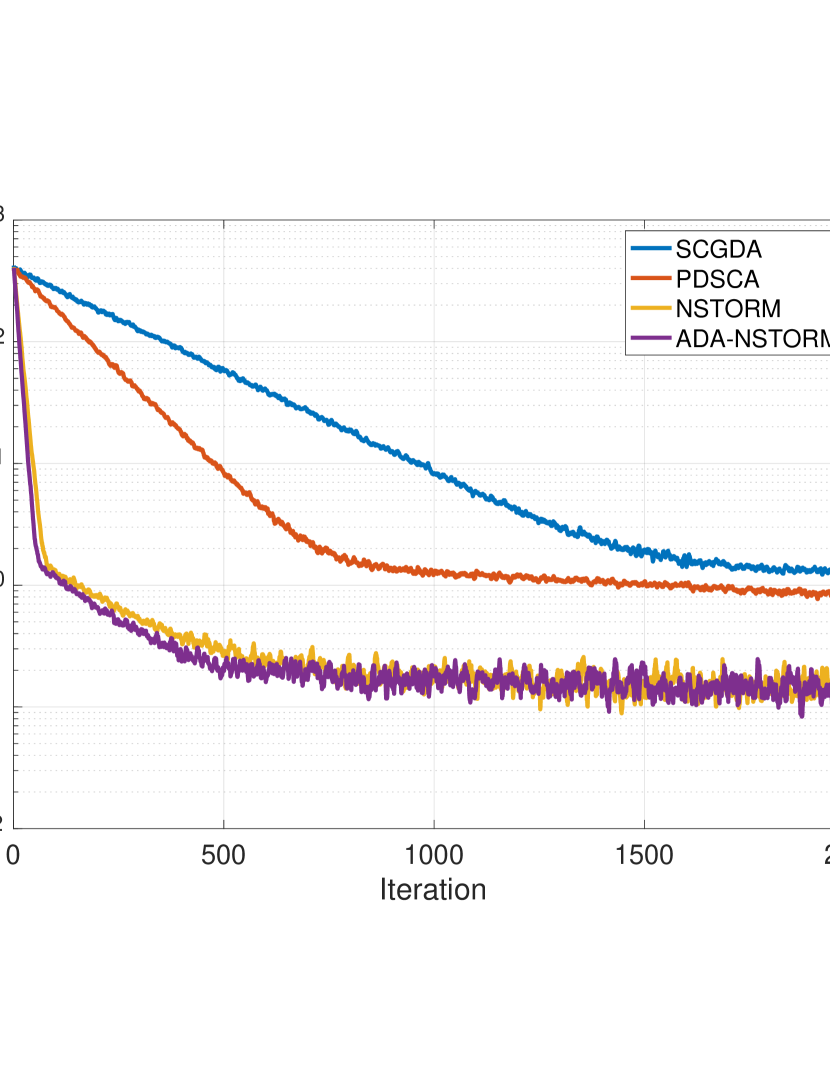

The training progression of deep AUC is illustrated in Figure 2. It shows the notable swiftness of convergence exhibited by our two proposed methods. Furthermore, across all four datasets, our methods consistently yield the most favorable test AUC outcomes. It is evident from the results depicted in Figure 2 that even NSTORM, which lacks an adaptive generator, surpasses the performance of SCGDA and PDSCA methods, thus reinforcing the validity of our theoretical analysis. Intriguingly, despite ADA-NSTORM sharing a theoretical foundation with NSTORM, it outperforms the testing AUC performance in the majority of scenarios.

The testing AUC outcomes are summarized in Table 1, with the optimal AUC values among 100 epochs. Combining these findings with Figure 2, a recurring pattern emerges: best testing AUC performance is typically attained around the 50th epoch, followed by overfitting. Both Table 1 and Figure 2 show that our proposed methods consistently outperform benchmarks. ADA-NSTORM achieves an impressive AUC of 0.833 on STL10 with a 10% imbalanced ratio. Notable exceptions are the CAT_vs_DOG and CIFAR100 datasets with a 1% imbalanced ratio, possibly due to their proximity to the training set’s distribution.

5.2 Ablation Study

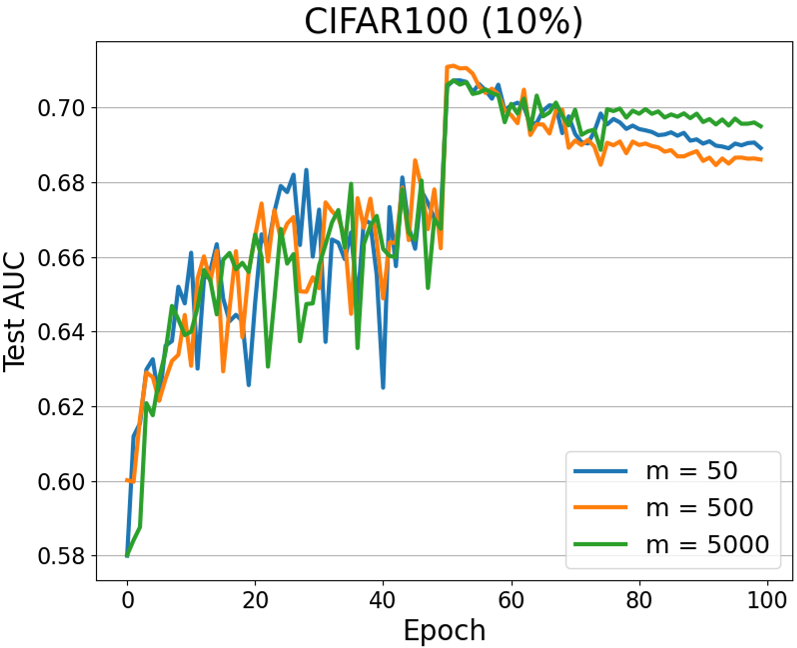

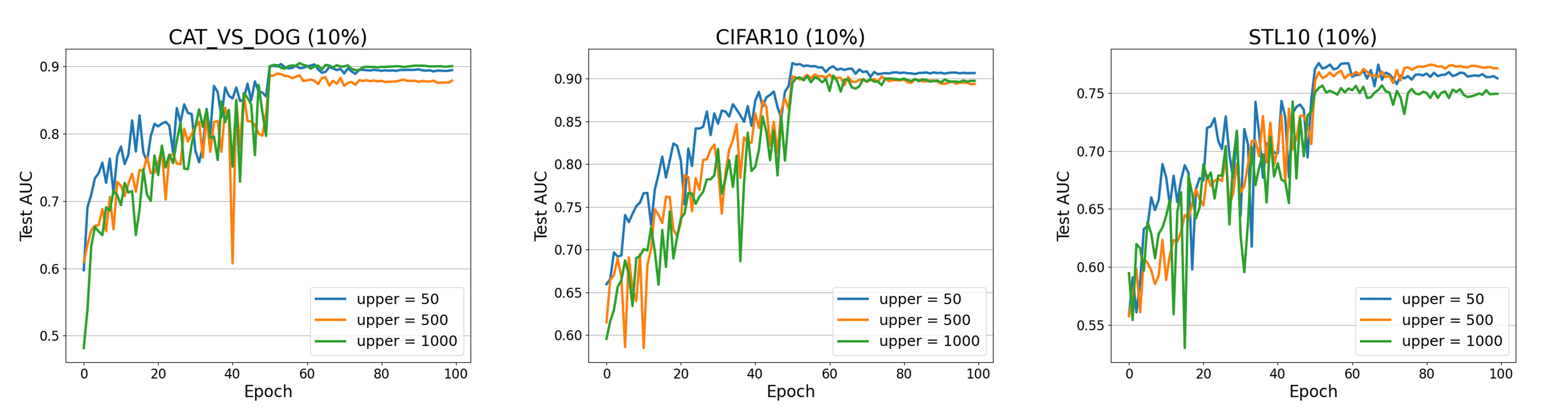

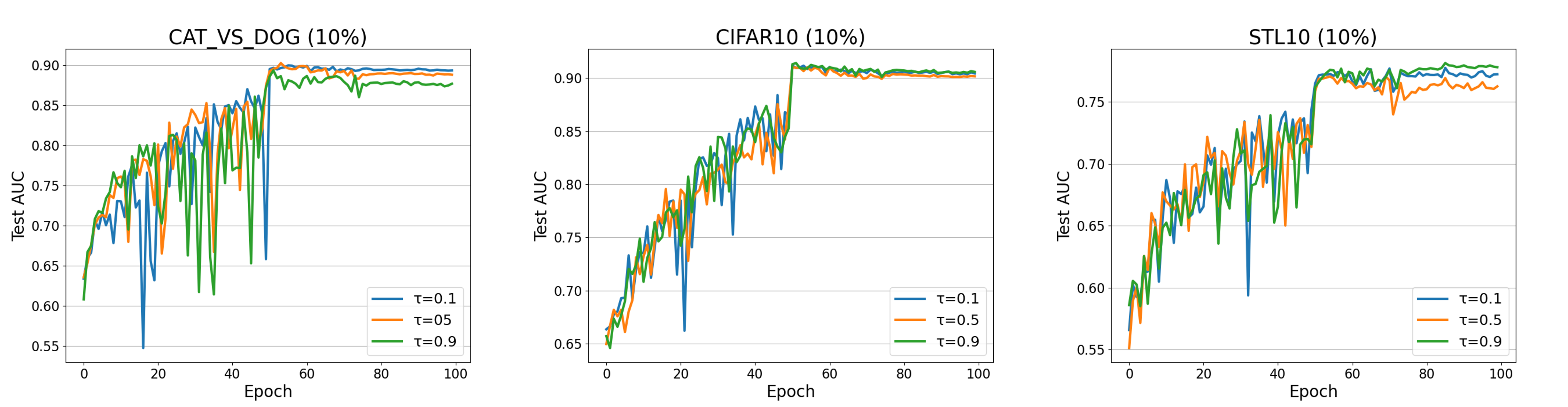

We conducted experiments to fine-tune parameters and for NSTORM, as demonstrated in Figure 6 and Figure 6. In Theorem 1, we consider as the lower bound, controlling the learning rate . Interestingly, adjusting yields minimal alterations. On the other hand, determines the relative step sizes of and . Figure 6 reveals that an optimal value of approximately 0.5 yields a testing AUC of 0.827.

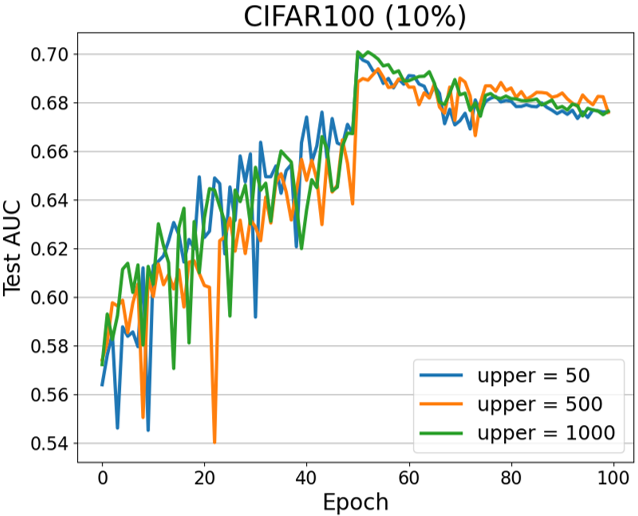

To assess the influence of and in Assumption 5, we investigate the testing AUC under varying upper bounds for and , as illustrated in Figure 6. Notably, changing from an upper bound of 50 to 1000 yields a minimal change in the testing AUC, validating the mildness of Assumption 5. In addition, the parameter is related to the adaptive generator within ADA-NSTORM. Figure 6 shows the impact of on ADA-NSTORM’s performance within the deep AUC problem. Intriguingly, varying from 0.1 to 0.9 leads to a mere change of 0.127. These ablation studies effectively reinforce the robustness of our proposed methods.

6 Conclusion

In this paper, we first proposed a novel method named NSTORM for optimizing the compositional minimax problem. By leveraging variance-reduced techniques of both function and gradient values, we demonstrate that the proposed NSTORM method can achieve the sample complexity of for finding an -stationary point without using large batch sizes. NSTORM under the PL-condition is also demonstrated to achieve the same sample complexity, which indicates its extendability. To the best of our knowledge, all theoretical results match the best sample complexity in existing minimax optimization. Because NSTORM requires a small learning rate to achieve the optimal complexity, this limits its applicability in real-world machine learning scenarios. To take advantage of adaptive learning rates, we develop an adaptive version of NSTORM named ADA-STORM, which can achieve the same complexity with the learning rate changing adaptively. Extensive experimental results support the effectiveness of our proposed methods.

References

- Arjovsky, Chintala, and Bottou [2017] Arjovsky, M.; Chintala, S.; and Bottou, L. 2017. Wasserstein generative adversarial networks. In International conference on machine learning, 214–223. PMLR.

- Chen et al. [2020] Chen, C.; Luo, L.; Zhang, W.; and Yu, Y. 2020. Efficient projection-free algorithms for saddle point problems. Advances in Neural Information Processing Systems, 33: 10799–10808.

- Chen et al. [2017] Chen, R. S.; Lucier, B.; Singer, Y.; and Syrgkanis, V. 2017. Robust optimization for non-convex objectives. Advances in Neural Information Processing Systems, 30.

- Coates, Ng, and Lee [2011] Coates, A.; Ng, A.; and Lee, H. 2011. An analysis of single-layer networks in unsupervised feature learning. In Proceedings of the fourteenth international conference on artificial intelligence and statistics, 215–223. JMLR Workshop and Conference Proceedings.

- Cutkosky and Orabona [2019] Cutkosky, A.; and Orabona, F. 2019. Momentum-based variance reduction in non-convex sgd. Advances in neural information processing systems, 32.

- Fang et al. [2018] Fang, C.; Li, C. J.; Lin, Z.; and Zhang, T. 2018. Spider: Near-optimal non-convex optimization via stochastic path-integrated differential estimator. Advances in Neural Information Processing Systems, 31.

- Finn, Abbeel, and Levine [2017] Finn, C.; Abbeel, P.; and Levine, S. 2017. Model-agnostic meta-learning for fast adaptation of deep networks. In International conference on machine learning, 1126–1135. PMLR.

- Gao, Li, and Huang [2022] Gao, H.; Li, J.; and Huang, H. 2022. On the convergence of local stochastic compositional gradient descent with momentum. In International Conference on Machine Learning, 7017–7035. PMLR.

- Gao et al. [2021] Gao, H.; Wang, X.; Luo, L.; and Shi, X. 2021. On the Convergence of Stochastic Compositional Gradient Descent Ascent Method. In Thirtieth International Joint Conference on Artificial Intelligence (IJCAI).

- Goodfellow et al. [2014] Goodfellow, I. J.; Pouget-Abadie, J.; Mirza, M.; Xu, B.; Warde-Farley, D.; Ozair, S.; Courville, A. C.; and Bengio, Y. 2014. Generative Adversarial Nets. In NIPS.

- Gulrajani et al. [2017] Gulrajani, I.; Ahmed, F.; Arjovsky, M.; Dumoulin, V.; and Courville, A. C. 2017. Improved training of wasserstein gans. Advances in neural information processing systems, 30.

- He et al. [2016] He, K.; Zhang, X.; Ren, S.; and Sun, J. 2016. Deep residual learning for image recognition. In Proceedings of the IEEE conference on computer vision and pattern recognition, 770–778.

- Hu et al. [2019] Hu, W.; Li, C. J.; Lian, X.; Liu, J.; and Yuan, H. 2019. Efficient smooth non-convex stochastic compositional optimization via stochastic recursive gradient descent. Advances in Neural Information Processing Systems, 32.

- Huang [2023] Huang, F. 2023. Enhanced Adaptive Gradient Algorithms for Nonconvex-PL Minimax Optimization. arXiv preprint arXiv:2303.03984.

- Huang, Gao, and Huang [2020] Huang, F.; Gao, S.; and Huang, H. 2020. Gradient descent ascent for min-max problems on riemannian manifolds. arXiv preprint arXiv:2010.06097.

- Huang, Wu, and Hu [2023] Huang, F.; Wu, X.; and Hu, Z. 2023. Adagda: Faster adaptive gradient descent ascent methods for minimax optimization. In International Conference on Artificial Intelligence and Statistics, 2365–2389. PMLR.

- Jiang et al. [2022] Jiang, W.; Wang, B.; Wang, Y.; Zhang, L.; and Yang, T. 2022. Optimal algorithms for stochastic multi-level compositional optimization. arXiv preprint arXiv:2202.07530.

- Kingma and Ba [2014] Kingma, D. P.; and Ba, J. 2014. Adam: A method for stochastic optimization. arXiv preprint arXiv:1412.6980.

- Krizhevsky, Hinton et al. [2009] Krizhevsky, A.; Hinton, G.; et al. 2009. Learning multiple layers of features from tiny images.

- Lin, Jin, and Jordan [2020] Lin, T.; Jin, C.; and Jordan, M. 2020. On gradient descent ascent for nonconvex-concave minimax problems. In International Conference on Machine Learning, 6083–6093. PMLR.

- Luo, Xiong, and Liu [2019] Luo, L.; Xiong, Y.; and Liu, Y. 2019. Adaptive Gradient Methods with Dynamic Bound of Learning Rate. In International Conference on Learning Representations.

- Luo et al. [2020] Luo, L.; Ye, H.; Huang, Z.; and Zhang, T. 2020. Stochastic recursive gradient descent ascent for stochastic nonconvex-strongly-concave minimax problems. Advances in Neural Information Processing Systems, 33: 20566–20577.

- Madry et al. [2018] Madry, A.; Makelov, A.; Schmidt, L.; Tsipras, D.; and Vladu, A. 2018. Towards Deep Learning Models Resistant to Adversarial Attacks. In International Conference on Learning Representations.

- Mohri, Sivek, and Suresh [2019] Mohri, M.; Sivek, G.; and Suresh, A. T. 2019. Agnostic federated learning. In International Conference on Machine Learning, 4615–4625. PMLR.

- Nemirovski et al. [2009] Nemirovski, A.; Juditsky, A.; Lan, G.; and Shapiro, A. 2009. Robust stochastic approximation approach to stochastic programming. SIAM Journal on optimization, 19(4): 1574–1609.

- Palaniappan and Bach [2016] Palaniappan, B.; and Bach, F. 2016. Stochastic variance reduction methods for saddle-point problems. Advances in Neural Information Processing Systems, 29.

- Qi et al. [2021] Qi, Q.; Guo, Z.; Xu, Y.; Jin, R.; and Yang, T. 2021. An online method for a class of distributionally robust optimization with non-convex objectives. Advances in Neural Information Processing Systems, 34: 10067–10080.

- Qiu et al. [2020] Qiu, S.; Yang, Z.; Wei, X.; Ye, J.; and Wang, Z. 2020. Single-timescale stochastic nonconvex-concave optimization for smooth nonlinear TD learning. arXiv preprint arXiv:2008.10103.

- Qu et al. [2022] Qu, Z.; Li, X.; Duan, R.; Liu, Y.; Tang, B.; and Lu, Z. 2022. Generalized Federated Learning via Sharpness Aware Minimization. arXiv preprint arXiv:2206.02618.

- Qu et al. [2023] Qu, Z.; Li, X.; Han, X.; Duan, R.; Shen, C.; and Chen, L. 2023. How To Prevent the Poor Performance Clients for Personalized Federated Learning? In Proceedings of the IEEE/CVF Conference on Computer Vision and Pattern Recognition, 12167–12176.

- Rafique et al. [2022] Rafique, H.; Liu, M.; Lin, Q.; and Yang, T. 2022. Weakly-convex–concave min–max optimization: provable algorithms and applications in machine learning. Optimization Methods and Software, 37(3): 1087–1121.

- Reddi, Kale, and Kumar [2018] Reddi, S. J.; Kale, S.; and Kumar, S. 2018. On the Convergence of Adam and Beyond. In International Conference on Learning Representations.

- Shapiro, Dentcheva, and Ruszczynski [2021] Shapiro, A.; Dentcheva, D.; and Ruszczynski, A. 2021. Lectures on stochastic programming: modeling and theory. SIAM.

- Sutton and Barto [2018] Sutton, R. S.; and Barto, A. G. 2018. Reinforcement learning: An introduction. MIT press.

- Tarzanagh et al. [2022] Tarzanagh, D. A.; Li, M.; Thrampoulidis, C.; and Oymak, S. 2022. FedNest: Federated Bilevel, Minimax, and Compositional Optimization. In International Conference on Machine Learning, 21146–21179. PMLR.

- Wang et al. [2021] Wang, J.; Zhang, T.; Liu, S.; Chen, P.-Y.; Xu, J.; Fardad, M.; and Li, B. 2021. Adversarial attack generation empowered by min-max optimization. Advances in Neural Information Processing Systems, 34: 16020–16033.

- Wang, Fang, and Liu [2017] Wang, M.; Fang, E. X.; and Liu, H. 2017. Stochastic compositional gradient descent: algorithms for minimizing compositions of expected-value functions. Mathematical Programming, 161(1): 419–449.

- Xian et al. [2021] Xian, W.; Huang, F.; Zhang, Y.; and Huang, H. 2021. A faster decentralized algorithm for nonconvex minimax problems. Advances in Neural Information Processing Systems, 34: 25865–25877.

- Xu et al. [2020] Xu, T.; Wang, Z.; Liang, Y.; and Poor, H. V. 2020. Enhanced first and zeroth order variance reduced algorithms for min-max optimization.

- Yan et al. [2020] Yan, Y.; Xu, Y.; Lin, Q.; Liu, W.; and Yang, T. 2020. Optimal epoch stochastic gradient descent ascent methods for min-max optimization. Advances in Neural Information Processing Systems, 33: 5789–5800.

- Yang, Kiyavash, and He [2020] Yang, J.; Kiyavash, N.; and He, N. 2020. Global convergence and variance reduction for a class of nonconvex-nonconcave minimax problems. Advances in Neural Information Processing Systems, 33: 1153–1165.

- Yang, Zhang, and Fang [2022] Yang, S.; Zhang, Z.; and Fang, E. X. 2022. Stochastic Compositional Optimization with Compositional Constraints. arXiv preprint arXiv:2209.04086.

- Yuan and Hu [2020] Yuan, H.; and Hu, W. 2020. Stochastic recursive momentum method for non-convex compositional optimization. arXiv preprint arXiv:2006.01688.

- Yuan, Lian, and Liu [2019] Yuan, H.; Lian, X.; and Liu, J. 2019. Stochastic recursive variance reduction for efficient smooth non-convex compositional optimization. arXiv preprint arXiv:1912.13515.

- Yuan et al. [2022] Yuan, Z.; Guo, Z.; Chawla, N.; and Yang, T. 2022. Compositional Training for End-to-End Deep AUC Maximization. In International Conference on Learning Representations.

- Yuan et al. [2020] Yuan, Z.; Yan, Y.; Sonka, M.; and Yang, T. 2020. Robust deep auc maximization: A new surrogate loss and empirical studies on medical image classification. arXiv preprint arXiv:2012.03173, 8.

- Zhang and Xiao [2019a] Zhang, J.; and Xiao, L. 2019a. A composite randomized incremental gradient method. In International Conference on Machine Learning, 7454–7462. PMLR.

- Zhang and Xiao [2019b] Zhang, J.; and Xiao, L. 2019b. A stochastic composite gradient method with incremental variance reduction. Advances in Neural Information Processing Systems, 32.

- Zhang and Xiao [2021] Zhang, J.; and Xiao, L. 2021. Multilevel composite stochastic optimization via nested variance reduction. SIAM Journal on Optimization, 31(2): 1131–1157.

- Zhang et al. [2021] Zhang, X.; Liu, Z.; Liu, J.; Zhu, Z.; and Lu, S. 2021. Taming Communication and Sample Complexities in Decentralized Policy Evaluation for Cooperative Multi-Agent Reinforcement Learning. Advances in Neural Information Processing Systems, 34: 18825–18838.

- Zhang and Lan [2020] Zhang, Z.; and Lan, G. 2020. Optimal algorithms for convex nested stochastic composite optimization. arXiv preprint arXiv:2011.10076.

- Zhuang et al. [2020] Zhuang, J.; Tang, T.; Ding, Y.; Tatikonda, S. C.; Dvornek, N.; Papademetris, X.; and Duncan, J. 2020. Adabelief optimizer: Adapting stepsizes by the belief in observed gradients. Advances in neural information processing systems, 33: 18795–18806.

Appendix A Additional Toy Examples

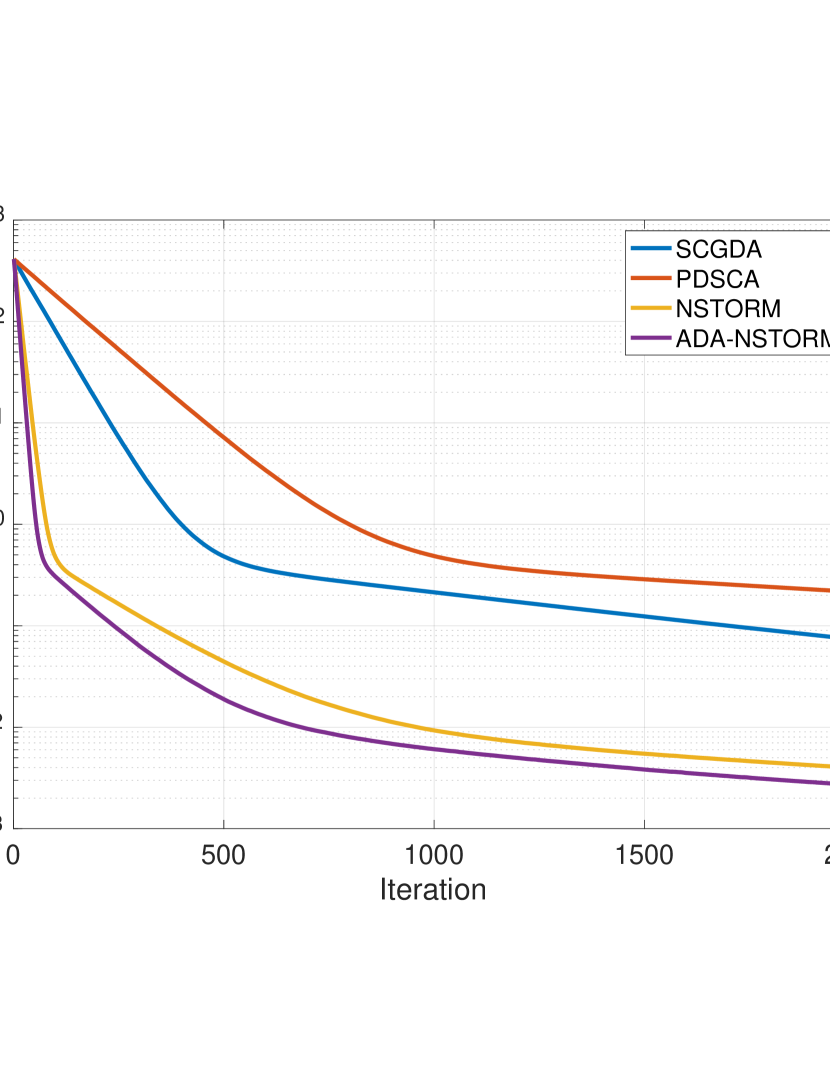

In Figure 7, the trajectories of the four benchmarks are shown beneath the variances of different levels. This visualization is based on the setting of the same number of iterations, identical and step sizes, as well as a common value. and we can find that the four benchmarks follow the same trajectory to reach the stationary point when the variance is equal to 0. As the variance increases, our method reaches the stationary point with a smoother and shorter path, which indicates that our method has better robustness to very noisy datasets.

Appendix B Useful Lemmas

The following two lemmas aim to show the Lipschitz and smooth properties of the compositional minimization optimization, and they can facilitate the proof of all theorems.

Proof.

According to the definition of , we have , then we can get

| (13) | ||||

where the first inequality holds by -strong concavity and the second inequality holds by -Smoothness. ∎

Proof.

| (14) | ||||

where the last two inequality holds by Lemma 1 and the last inequality holds by . ∎

Appendix C Proof of Theorem 1

We first provide some useful lemmas and then we show the sample complexity of the proposed NSTORM method in Theorem 1.

Proof.

It is worth noting that the estimated error of gradient in is determined by , and . Therefore, as long as these three terms have smaller errors, the estimated error of gradient is smaller. The following lemmas aim to show how to control these errors.

Proof.

| (17) | ||||

This completes the proof. ∎

Proof.

| (18) | ||||

where the last two inequality is derived from . ∎

We have the flexibility to control the term from the right side by selecting sufficiently small values for , due to the definition of . Similarly, by choosing a small enough step size , i.e., , we can control the term . It’s worth noting that in Gao et al. [2021], they adopt a strategy of using a large batch size to control the variance caused by the function value estimator and the gradient estimator of the inner function. However, this approach incurs significant computational costs.

Proof.

| (19) | ||||

where the last inequality holds by Assumption 3. ∎

Proof.

| (20) | ||||

where the first inequality holds by the smoothness and the last inequality holds by Lemma 4. ∎

The gap between the gradient estimator of the outer function and its true value is greater than the gap for the inner function estimator. This is due to two reasons. First, during iterations, updates to introduce errors when is subsequently updated. Second, multi-layer estimators for combined functions propagate more errors through the layers. However, the accumulation of error is bounded.

Proof.

| (21) | ||||

Next, we bound the term :

| (22) | ||||

Then, according to Lemma 4, we can conclude that:

| (23) | ||||

This completes the proof. ∎

According to the proof of Lemma 8, we can find that the variance is produced by more terms, such as . But based on Lemma 4, the error of growth is also very limited. So, taking the same strategy, i.e., small and , we can control the variance.

Lemma 9.

Proof.

Proof.

Similar to Xian et al. [2021], define for some constant . Due to the strongly concave of in , we have:

| (27) | ||||

Besides, as function is smooth in , we have:

| (28) |

Due to the definition of , we have . combine (27) and (28) we have:

| (29) | ||||

By Cauchy-Schwartz inequality we have:

| (30) |

Adding (30) and (29), and setting , we obtain:

| (31) |

As we have:

| (32) |

Summing (31) and (32), and rearranging terms, we obtain:

| (33) |

According to Young’s inequality:

| (34) | ||||

where the second inequality holds by (33) and . ∎

Based on the above lemmas, we can approach the proof of Theorem 1. Define the potential function, for any :

| (35) |

where . We denote that , , , and . Then based on the above lemmas, we have:

| (36) | ||||

By setting , , , and we have:

| (37) | ||||

where the first inequality holds by .

Let , we have:

| (38) |

and we also have:

| (39) |

Let , we have:

| (40) |

By setting and , we can get:

| (41) | ||||

where the last inequality holds by .

Setting , then by summing up and rearranging, we have:

| (42) |

From the initialization condition, it is easy to get:

| (43) |

where is is the variance produced by the first iteration. Since is decreasing, we have:

| (44) |

Similar to the proof of Theorem 1 in STORM Cutkosky and Orabona [2019], denoting that , we have:

| (45) |

which indicates that:

| (46) |

using Cauchy-Schwarz inequality, we have:

| (47) |

therefore we have:

| (48) |

Therefore, we get the result in Theorem 1.

Appendix D NSTORM under -PL condition

In this section, we consider moderating the function with respect to to follow the PL condition, which highlights the extensibility and applicability of our proposed NSTORM method. In particular, we rely on Assumption 6 in place of Assumption 4.

Assumption 6.

(-PL condition) There exists a constant , such that , where and .

Note that Assumption 6 moderates Assumption 4, which does not require the function to be strongly concave with respect to . In fact, Assumption 6 holds even if is not concave in at all. If Assumption 6 holds, then we also get that quadratic growth condition and error bound condition hold, and we give the definitions of quadratic growth condition and error bound condition below in the subsequent Lemma 11.

Lemma 11.

(karimi2016linear) Function is -smooth and satisfies PL condition with constant , then it also satisfies error bound (EB) condition with , i.e.,

where . It also satisfies quadratic growth (QG) condition with ,i.e.,

where is the minimum value of the function, and is the distance of the point to the optimal solution set.

So in summary, Assumption 6 is a weaker condition than Assumption 4, and its validity implies the quadratic growth and error bound conditions hold, even without concavity of in .

Before giving specific details of the proof, we would like to use another form of gradient for a better convergence analysis. We replace line 13 in Algorithm 1:

| (49) |

Note that we add an extra parameter when updating , but it turns out that in this case Theorem 3 still holds as long as . Therefore, as long as the theorem holds for this update rule with the additional parameter, NSTORM also satisfies the conditions of Theorem 3. For simplicity, we refer to the replaced algorithm still as Algorithm 1 in the following part.

Theorem 3.

Then we start from the counterpart of Lemma 9.

Proof.

Due to the smoothness of , we have:

| (50) | ||||

Then, we bound the term :

| (51) | ||||

where the last inequality is due to the -PL condition. Similar to Huang [2023], we have:

| (52) | ||||

rearranging the terms:

| (53) | ||||

Next, due to , We can observe that the function exhibits smoothness with respect to . As a result, we can deduce that:

| (54) |

then we have:

| (55) | ||||

where the second inequality holds by Cauchy-Schwartz inequality. Then according to the smoothness of , we can get:

| (56) |

Combining (55) and (56), we obtain:

| (57) | ||||

where the last inequality holds by quadratic growth (QG) condition with .

Then we have:

| (58) | ||||

Substituting (58) in (53), we get:

| (59) | ||||

where the last inequality holds by , and and the following inequalities:

| (60) | ||||

∎

We provide the following definitions and Lemma 13 to prove the counterpart of Lemma 2. Given a -strong function , we define a Bregman distancecensor1981iterative censor1992proximal associated with as follows:

| (61) |

Where is a closed convex set. Assume is a convex and possibly non-smooth function, we define a generalized projection problem as [ghadimi2016mini]:

| (62) |

Where and . . Following ghadimi2016mini, we define a generalized gradient as follows:

| (63) |

Lemma 13.

(Lemma 1 in ghadimi2016mini) Let be given in Eq.(62). Then we have, for any and :

where depends on strongly convex function .

Based on Lemma 13, let , we have:

| (64) |

Lemma 14.

Proof.

According to Lemma 2, i.e., function is -smooth, we have:

| (66) | ||||

Given the mirror function is -strongly convex, we define Bergman distance as in ghadimi2016mini:

| (67) |

By applying Lemma 13 to Algorithm 1 ,i.e., the problem , we obtain:

| (68) |

thus we have:

| (69) |

Next, we bound the term :

| (70) | ||||

where the last inequality holds by Assumption 1. Now back to the proof, similar to Huang [2023], we get:

| (71) | ||||

where the last two inequality holds by . Then, based on Lemma 3, we can obtain the following:

| (72) | ||||

This completes the proof. ∎

Note that replacing the Assumption does not affect the bounded variance of the estimators. With this in mind, we now present the convergence analysis. Defining the Lyapunov function, for any :

| (73) | ||||

where . And we denote that , , , , , according to above lemmas, we have:

| (74) | ||||

Let , , and , we have , and , then following (37), we can get .

Next, Let , we have:

| (75) |

and

| (76) |

Let , we get:

| (77) |

Then, setting , , where , we have:

| (78) | ||||

Taking average over on both sides of (78), we have:

| (79) | ||||

Since is decreasing, we have:

| (80) | ||||

Setting , from the initialization, we can easily get:

| (81) |

We set:

| (82) | ||||

According to Jensen’s inequality, we have:

| (83) | ||||

According to -PL condition we have:

| (84) | ||||

then we have:

| (85) |

Besides,

| (86) | ||||

and we also have:

| (87) | ||||

Combine (85), (86) and (87), we have:

| (88) | ||||

Then we obtain:

| (89) |

This completes the proof and obtains the results in Theorem 3.

Let , we have . Therefore, NSTORM under -condition has the same convergence rate, i.e., . Similarly, let , we have . Moreover, in each iteration NSOTRM only requires two samples, and , to estimate the gradient and function values. Therefore, the sample complexity for NSOTRM to find an -stationary point for compositional minimax problems is .

Appendix E Proof of Theorem 2

Proof.

Since is -Lipschitz continuous gradient, we have:

| (90) | ||||

According to Assumption 5, we get , then according to Lemma 13, we have:

| (91) |

thus we have:

| (92) |

For the term , we have:

| (93) | ||||

where the second inequality holds by , , and the last inequality holds by Assumption 1.

Similarly, for the term , we have:

| (94) |

Combine the term and , we have:

| (95) | ||||

where the last inequality follows by .

Then according to Lemma 3, we have:

| (96) | ||||

This completes the proof. ∎

Proof.

Similar to the proof of Lemma 6 in Huang, Wu, and Hu [2023], according to -strongly concave of function in , we have:

| (97) | ||||

Due to the smooth of function in , we have:

| (98) |

Summing up (97)) and (98)), we have:

| (99) | ||||

By the optimal of lines 14-15 in Algorithm 2 and the definition of , we have:

| (100) |

then,

| (101) | ||||

Summing up (99) and (101), we have:

| (102) | ||||

Due to the definition of , then:

| (103) | ||||

By , we have:

| (104) | ||||

then,

| (105) |

Considering the term , we have:

| (106) | ||||

By plugging the inequalities (106) and (105) into (103), we have:

| (107) | ||||

where the second inequality holds by and , and the last inequality is due to , it implies that:

| (108) |

Next, we considering the term :

| (109) | ||||

where the first inequality holds by Cauchy-Schwarz inequality and Young’s inequality.

Combine the Eq.(108) and Eq.(109), since , , we have , and , we have:

| (110) | ||||

This completes the proof. ∎

Proof.

| (111) | ||||

where the first inequality holds by Assumption 1. ∎

Proof.

| (112) | ||||

This completes the proof. ∎

Proof.

Proof.

| (114) | ||||

Next, we bound the term :

| (115) | ||||

Then, according to Lemma 4, we can conclude that:

| (116) | ||||

This completes the proof. ∎

Similar to the proof of Lemma 5, Lemma 6, Lemma 7 and Lemma 8, we can conclude that the variance between the estimators and their true values can be controlled by simple strategy, i.e., proper step size of and the proper value of .

Now, we come into the proof of Theorem 2. Define the potential function, for any :

| (117) |

where . Denote that , , , and . Then according to the above lemmas, we have:

| (118) | ||||

By setting , , and , according to (37) we have:

| (119) |

Let and we can get:

| (120) |

and

| (121) |

Then setting , where , , we can get:

| (122) | ||||

Taking average over on both sides of above inequality, we have:

| (123) | ||||

Since is decreasing, we have:

| (124) | ||||

Denote that , then from the initialization, we can easily get:

| (125) | ||||

According to Jensen’s inequality, we have:

| (126) | ||||

Besides, , we have:

| (127) | ||||

Looking at the term , we have:

| (128) |

Then for the term , we have:

| (129) | ||||

Next, for the term , we have:

| (130) | ||||

Then,

| (131) | ||||

We can get . By using Cauchy-Schwarz inequality, we have:

| (132) |

Based on (126), we have:

| (133) |

Thus, we have:

| (134) | ||||

Therefore, we get the result in Theorem 2.

Appendix F ADA-NSTORM with the Different Adam-Type Generator

Adaptive learning rates have been widely used in stochastic optimization problems, with many successful methods proposed such as Adam Kingma and Ba [2014], AdaBelief Zhuang et al. [2020], AMSGrad Reddi, Kale, and Kumar [2018], and AdaBound Luo, Xiong, and Liu [2019]. However, their application in stochastic compositional problems remains less explored. To enable adaptive learning rates, we propose generating adaptive learning rate matrices in different ways. We give ADA-NSTORM with different Adam-type as Algorithm 3. is an arbitrary positive constant that is greater than 0. It is introduced to prevent the matrices or from containing zeros, which would cause issues with the scoring factor calculations.

In case 1, we consider using AMSGrad. AMSGrad enhances Adam optimization by retaining the maximum of all past learning rates , denote as . This maximal learning rate replaces when calculating the current learning rate . As a result, the learning rate decays more slowly over training compared to Adam, where continually decreases. By preserving larger historical learning rates in , AMSGrad stabilizes the learning rate at a higher value, avoiding premature convergence. On certain tasks, AMSGrad achieves superior performance to Adam.

In case 2, we consider using AdaBelief. In conventional non-convex optimization, parameter updates for typically rely solely on noisy gradient value or gradient estimator value. AdaBelief incorporates both the noisy gradients and estimator values when updating x. It increases the update size when the estimator and noisy gradient are in close agreement. But when there is a large gap between the estimator and noisy gradient, AdaBelief slows down the updates. Thus, AdaBelief adapts the update pace based on the alignment between these two information sources. Nonetheless, this method cannot be directly applied to our problem, i.e., we can only obtain the biased estimation of the full gradient. As such, combining with NSTORM, we consider the gap between the inner estimator and the gradient of , i.e., .

In Case 1 and Case 2 of Algorithm 3, we can see that making the same assumptions as in Theorem 2, specifically Assumptions 1-4 and 5, leaves the recursion inequalities for the estimation error of the inner and outer functions’ values and gradients unchanged. That is, Lemmas 15-20 still hold. Now under Assumptions 1-5 for Algorithm 3, by setting the same parameters as in Theorem 2, we can obtain:

| (138) |

where and represents the minimum value of . Therefore, the sample complexity for Algorithm 3 with Case 1 and Case 2 remains .

Note that this is the first work that introduces AdaBelief into the compositional minimax optimization problem without using a large batch size.

In Case 3, we consider using AdaBound which constrains learning rates within predefined minimum and maximum bounds. In 137, where , the projection restricts to the range . We can use an analysis similar to Theorem 2 to derive the sample complexity. Furthermore, Theorem 2 still applies to Case 3 of Algorithm 3 even without needing Assumption 5. We only require a minor modification - the projection threshold is set equal to from Assumption 5.Specifically, Under Assumption 1-4 for Algorithm 3, setting , , , , , , where , , , , , we can obtain

| (139) |

where and represents the minimum value of . Consequently, the sample complexity of Algorithm 3 using Case 3 remains .

Appendix G Additional Experiments

G.1 Experimental Setup of deep AUC

Dataset description. Table 2 reports the detailed statistics for the different datasets. Note that "Number of image" refers to the number of samples in the original training set. The "Imbalance Ratio" represents the ratio of the number of positive examples to the total number of examples.

| Dataset | Number of images | Imbalance Ratio | Number of labels |

|---|---|---|---|

| CAT_VS_DOG Krizhevsky, Hinton et al. [2009] | 20,000 | 1%,5%,10%,30% | 2 |

| CIFAR10 Krizhevsky, Hinton et al. [2009] | 50,000 | 1%,5%,10%,30% | 2 |

| CIFAR100 Krizhevsky, Hinton et al. [2009] | 50,000 | 1%,5%,10%,30% | 2 |

| STL10 Coates, Ng, and Lee [2011] | 5,000 | 1%,5%,10%,30% | 2 |

Training configurations. All benchmark datasets were evaluated using the NVIDIA GTX-3090. The same dataloaders from Yuan et al. [2020]111https://libauc.org/were used for all datasets. Specifically, for the benchmark datasets, a 19k/1k, 45k/5k, 45k/5k, and 4k/1k training/validation split was applied for CatvsDog, CIFAR10, CIFAR100, and STL10, respectively.

Loss function.We use to denote an example. where denotes the input and denotes its corresponding label.

| (140) |

Note that we define the vector , are the number of positive (negative) examples, , we rewrite , where the first part , the second part and the last part . It’s notable that the inner function is equal to , and involves the Hessian matrix , we use the same strategy as Yuan et al. [2022] that simply ignore the second-order term. The loss function is transformed from a special surrogate loss gao2015consistency , due to the solution of this surrogate loss is computationally expensive, where is a margin parameter, e.g., .

G.2 Additional Experimental Results of Deep AUC

As shown in Figure 8, we tested the effect of changing the hyperparameter from 50 to 5000 for NSOTRM on different datasets. We found that varying the value of had a slight effect on the results. Similarly, we tested the effect of changing the step size ratio of and , specifically the hyperparameter as shown in Figure 9, on different test sets. We found that the best results consistently occurred when the step size for was less than the step size for . In Figure 10, we can see that changing the upper bound from 50 to 5000 had little effect on the results across the three datasets. This provides stronger evidence for the moderation implied by Assumption 5. Additionally, in Figure 11, changing the value of from 0.1 to 0.9 leads to only small changes in the results. This demonstrates the robustness of our algorithm.

G.3 Additional Ablation Studies of Deep AUC

G.4 Risk-Averse Portfolio Optimization

We then consider the risk-averse portfolio optimization problem. In this problem, we have assets to invest during each iteration , and represents the payoff of assets in iteration . Our objective is to simultaneously maximize the return on the investment and minimize the associated risk. One commonly used formulation for this problem is the mean-deviation risk-averse optimization Shapiro, Dentcheva, and Ruszczynski [2021], where the risk is measured using the standard deviation. This mean-deviation model is widely employed in practical settings and serves as a common choice for conducting experiments in compositional optimization Zhang and Xiao [2021]. The problem can be formulated as follows:

| (141) |

where and decision variable denotes the investment quantity vector in assets and . In the experiment, we test different methods on real-world datasets from Keneth R. French Data Library222https://mba.tuck.dartmouth.edu/pages/faculty/ken.french/data_library.html.

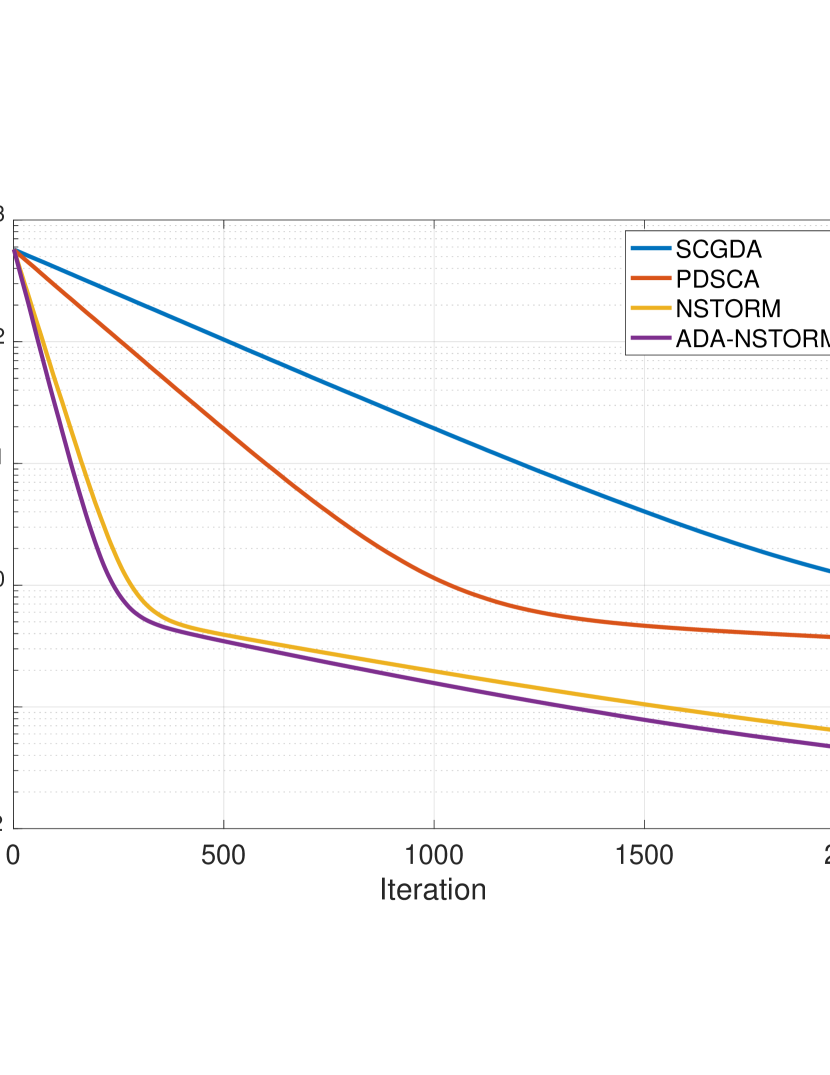

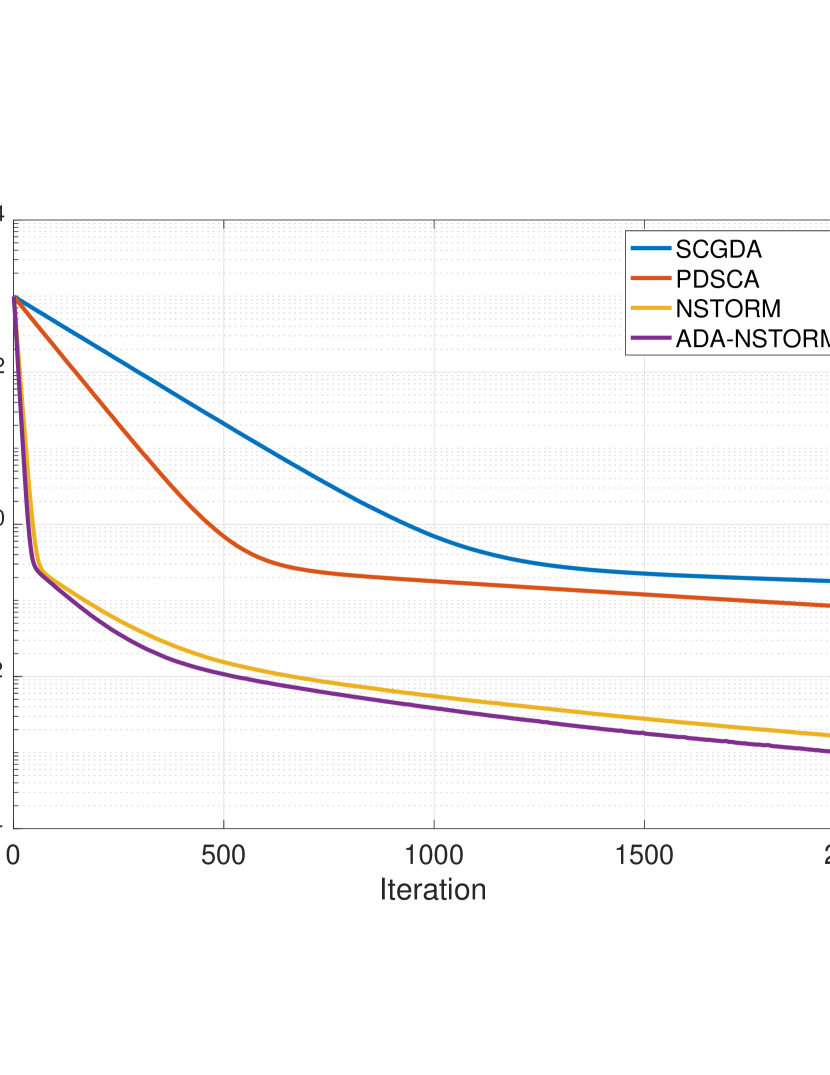

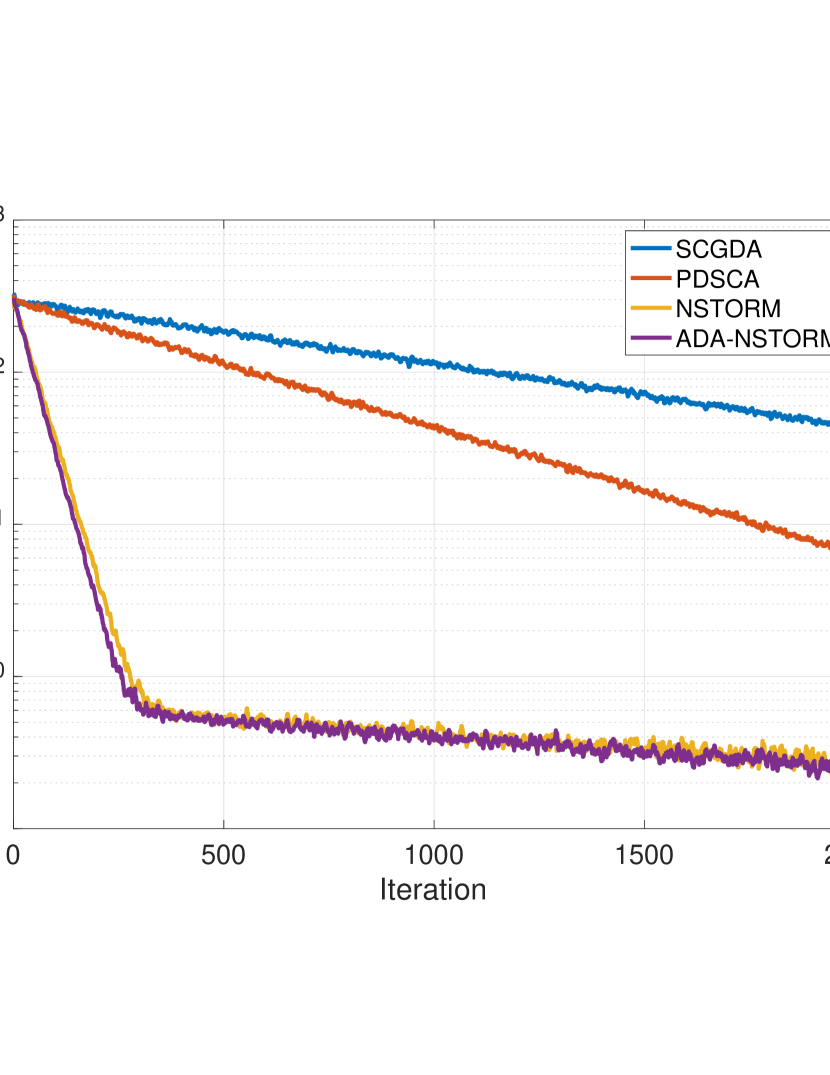

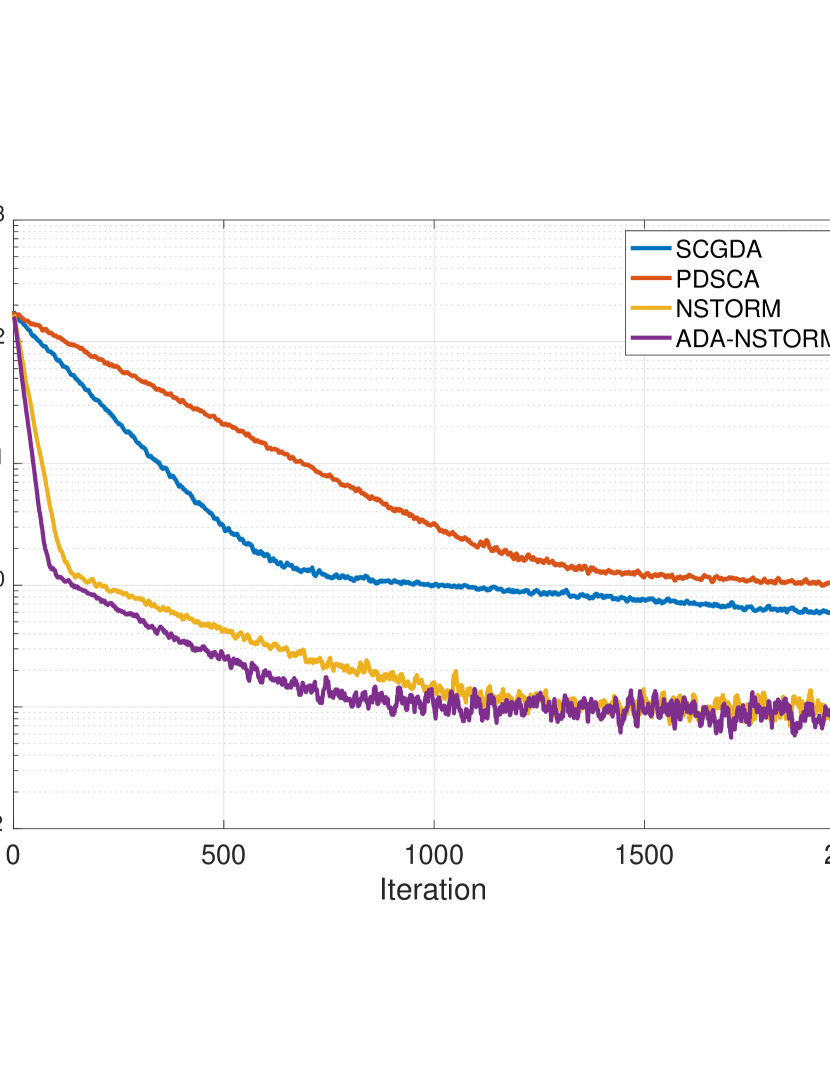

Figures 12-13 show the loss value and the norm of the gradient gaps against the number of samples drawn by each method, and all curves are averaged over 20 runs. We can see that our proposed two methods converge much faster than other methods in all datasets. More specifically, both the loss and the gradient of NSTORM and ADA-STORM decrease more quickly, demonstrating the low sample complexity of the proposed methods. In addition, although NSTORM and ADA-STORM obtain the sample complexity theoretically, the latter converges faster in practice due to the adaptive learning rate used in the training procedure.

G.5 Policy Evaluation in Reinforcement Learning

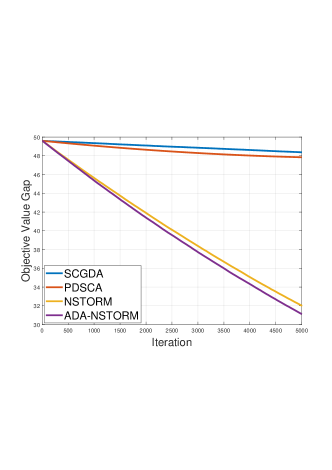

In this subsection, we aim to use NSTORM and ADA-NSTORM to optimize the policy evaluation of distributionally robust linear value function approximation in reinforcement learning Zhang and Xiao [2019b]. The value function in reinforcement learning is an important component to compute the reward. More specifically, given a Markov decision process (MDP) , where represents the state space, denotes the transition probability from state to state under a given policy , is the reward when state goes to state , and is the discount factor, then the value function at state is defined as . To estimate the value function, a typical choice is to parameterize it with a linear function: , where is fixed and is the model parameter which needs to be optimized. We are interested in the distributionally robust variant, i.e., the compositional loss function, Yuan, Lian, and Liu [2019], Zhang and Xiao [2019b], and hence the optimization is modified as follows:

| (142) |

where is the model parameter, , . Following Yuan, Lian, and Liu [2019], we generate an MDP that has 400 states and each state is associated with 10 actions. Regarding the transition probability, is drawn from uniformly. Additionally, to guarantee the ergodicity, we add to . Then, we use the four methods to optimize (142) on this dataset.

In Figure 14, it can be seen that the value function gap decreases with the training going on for all compositional minimax optimization methods. Among all methods, we can see that our proposed NSTORM and ADA-NSTORM methods outperform existing studies, i.e., SCGDA and PDSCA, which confirms the effectiveness of the proposed methods. More specifically, ADA-NSTORM incrementally decreases the gap of the function value, and it is more stable in changing learning rates.