BIRP: Bitcoin Information Retrieval Prediction Model Based on Multimodal Pattern Matching

Abstract.

Financial time series have historically been assumed to be a martingale process under the Random Walk hypothesis. Instead of making investment decisions using the raw prices alone, various multimodal pattern matching algorithms have been developed to help detect subtly hidden repeatable patterns within the financial market. Many of the chart-based pattern matching tools only retrieve similar past chart (PC) patterns given the current chart (CC) pattern, and leaves the entire interpretive and predictive analysis, thus ultimately the final investment decision, to the investors. In this paper, we propose an approach of ranking similar PC movements given the CC information and show that exploiting this as additional features improves the directional prediction capacity of our model. We apply our ranking and directional prediction modeling methodologies on Bitcoin due to its highly volatile prices that make it challenging to predict its future movements.

1. Introduction

Since the introduction of Bitcoin (BTC) in 2008 [11], the cryptocurrency (crypto) market has grown significantly. As a result, it attracted many investors and researchers attempting to forecast the movement of these crypto assets in search of profits.

Technical analysis is a discipline that analyzes the statistical transformation of the undelying financial price and volume time series. In this paper, we apply Balance of Power (BOP), Even Better Sinewave (EBSW), Chaikin Money Flow (CMF), Differencing (DIFF), and Inter Ratios (INTRA), which is technical analysis on the historical Bitcoin prices and volume to help rank past chart (PC) movements given the current chart (CC) movements. In this work, we attempt to compare predictive capabilities of various ranking methodologies between PC patterns given CC patterns. Our contribution is mainly two folds:

-

•

We propose four different ranking methodologies for chart pattern matching and rank similar PC segments based on proposed metrics.

-

•

We propose a BTC directional forecasting model for trading BTCUSDT perpetual and show that using voting information from pattern matched chart segments in the past improve the performance of our forecasting model.

2. Related work

There are numerous researches on how to detect chart patterns such as [7] and [12]. However, it is challenging to find literature that uses detected chart patterns for further modeling or using such information to devise a trading strategy. There are previous approaches that use similar patterns for modeling but they do not apply these techniques specifically in the domain of finance, much less crypto or BTC[12; 5]. Moreover, there are chart pattern detecting applications available for the traders such as those provided by TrendSpider 111http://trendspider.com/ and BTC pattern calculator 222https://miningcalc.kr/chart/btc, but they simply detect the patterns and do not take it a step further. Our research is also closely related to CBITS [9] as we incorporate our Information Retrieval (IR) based feature engineering (FE) technique into the CBITS framework. Furthermore, we use one of the crypto language models (LM) introduced in CBITS, crypto DeBERTa, a transformer based LM that improves upon BERT [4] by exploiting disentangled attention and enhanced mask decoder [8] for our multimodal embedding based ranking method.

3. Problem Definition

In this section, we define the problem for the proposed methods of our model. We approach BTC price directional forecasting task as a three class classification problem. The labels are defined as follows:

-

•

BTC price rises by at least 0.75% within the next 4 hours i.e. .

-

•

BTC price drops by at least 0.75% within the next 4 hours i.e. .

-

•

BTC price change within the next 4 hours is less than 0.75% i.e and .

The label translates to long position, the label translates to short position and translates to holding (taking no action). If both and occur for the next 4 hours, then we gave the labeling priority to (i.e. when both taking long or short results in at least 0.75% profit then we simply label that timestep as long).

3.1. Dataset Description

We collected 4 hourly BTC/USDT data from Binance 333www.binance.com/en, one of the largest crypto exchanges, and we ended up with 11,812 data points ranging from 2017-08-23 16:00:00 to 2023-01-15 20:00:00. After labeling the data, we end up with a label distribution of approximately 48.11% for , 29.40% for , and 22.49% for . Out of the 11,812 data points, we use the first 80% of the data as candidates (9,449 data points) for pattern matching and the rest for experimentation. 2,363 data points ranging from 2021-12-18 04:00 to 2023-01-15 20:00:00 were split into train/validation/test dataset in 8:1:1 ratio, and each of these 2,363 data points were compared with the candidates to find its similar counterparts in the past. For each of the 2,363 data points, we collected the top 30 similar chart patterns for each of the four different similarity calculation strategies.

3.2. Modeling

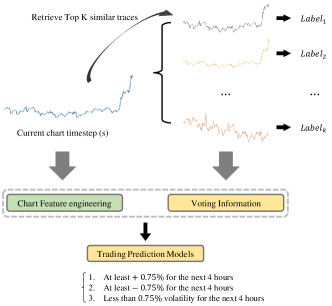

We employ XGBoost[2] as our directional forecasting model as it is fast to train and is robust for tabular data based classification tasks. To highlight some important hyper-parameters, we used 200 for the number of boosting rounds with a learning rate of 0.3. The maximum tree depth for base learners was set to 6, and the tree method was set to ”gpu_hist”. We also considered the class weights of the train dataset when training XGBoost. Essentially we compare the performance of when we use similar past chart information or not. We will denote these two cases as a system with IR-based FE and a system without IR-based FE. The overall approach is illustrated in Figure 1. We compare the performances of each method by calculating accuracy and weighted F1 score.

3.2.1. Without IR-based FE

When we do not use IR-based FE we simply use chart based features only as inputs to XGBoost for training. Most of the chart features that were used are features focused on calculating volatility or simply ratios of the open, high, low, close and volume features. Although XGBoost does not require feature scaling/normalization, in order to make the training more stable we purposely chose features with similar value ranges.

-

•

BOP: The balance of power (BOP) is an oscillator that measures the strength of the buy and sell pressures. When BOP is positive it suggests that the market is bullish and vice-versa. BOP that is close to zero indicates a balance between the two powers and it may signify a trend reversal.

-

•

EBSW: The even better sinewave (EBSW) is a variation of the Hilbert sine wave, and it is an indicator that can inform the model about the bullish and bearish cycle of prices.

-

•

CMF: The chaikin money flow (CMF) is an indicator used to monitor both the accumulation and distribution of an asset over a specified period. The default period of 20 is used for CMF.

-

•

DIFF: This is identical to the differencing features presented in [9]. It is the ratio of raw chart features across different periods. The first differencing of close prices would be calculated as

and in general the Kth differencing of the close prices is simply

Similarly we carry out this differencing procedure for all open, high, low, close and volume and used K = 1,2,…,12 for differencing.

-

•

INTRA: This feature is a ratio of different features in the current timestep. Specifically we used , , , , , .

after pre-processing the chart features we end up with a total of 68 features for training.

3.2.2. With IR-based FE

We use the same chart features presented in section 3.2.1 in addition to the vote information from past similar ranked chart features. Given a timestep , we retrieve at most top 30 timesteps that is the most similar to the timestep under one of the four ranking methods. Then we separately calculate the performance of the model’s directional forecast when we use voting information from the top most similar past patterns. Given top similar , we count the number of cases when the labels were or . For example, if and out of those top similar instances if 6 of them were , 3 were , and 1 was , then the voting vector can be formed as . Before we use this as additional input features to the XGBoost model we softmax normalize these scores. For example, the count for will be normalized as follows:

Similar transformation is applied to the count for and . After repeating this procedure for all , we calculate the average accuracy and weighted F1 scores for final comparison with the model that does not use IR-based FE.

4. Ranking Methods

In this section we describe our ranking approaches in detail. For all the ranking methods we ranked the top 30 most similar past timesteps given the query timestep.

4.1. Euclidean Distance

Our data is represented as follows: for timestep .

where denotes a feature and is the total number of features (in our case 68 as explained in section 3.2.1). Given some timestep the euclidean distance (L2 norm) is calculated via the following formula:

we retrieve top 30 such that has the smallest euclidean distance to .

4.2. TS2Vec

The timeseries to vector (TS2Vec) embedding method was first proposed in [13] and it has proved to effectively extract time series representations that are task agnostic. There are two major components to the TS2Vec architecture:

-

•

The TS2Vec encoder consists of the input projection layer, the timestamp masking layer and the dilated convolutions layer in this order. The timestamp masking layer randomly binary masks the latent vector and this idea was motivated by [3] and [6] to create augmented context views. The encoder is then optimized via the temporal contrast loss and instance-wise contrastive loss.

-

•

The input time series is randomly cropped into two different time series with overlapping timesteps for positive pair creation in an unsupervised setting.

Due to its design the TS2Vec requires a time series of length and we set , or 24 hours worth of time frame since we are dealing with 4 hourly chart data. We first train the TS2Vec encoder for 100 epochs, batch size 16, learning rate 0.001, hidden dimension size 64 and output dimension size 128 on NVIDIA A100-80GB GPU. The TS2Vec encoder is trained only on the candidate pool and not on the train/validation/test dataset. Afterwards, we calculate the TS2Vec embeddings for the train/validation/test dataset and all the embeddings for the candidate pool, and calculate the cosine distance between the embeddings. We obtain the top 30 embeddings based on the closeness of the cosine distances. Given that the query is and the candidate is :

| No FE | Top 5 | Top 10 | Top 15 | Top 20 | Top 25 | Top 30 | Average | |

| Ranking Strategy 1. Random Sampling | ||||||||

| Accuracy(%) | 51.899 | 54.084(+2.185) | 53.873(+1.974) | 53.608(+1.709) | 53.485(+1.586) | 53.840(+1.941) | 53.658(+1.759) | 53.758(+1.859) |

| F1 score | 0.580 | 0.598(+0.018) | 0.595(+0.015) | 0.593(+0.013) | 0.592(+0.012) | 0.595(+0.015) | 0.593(+0.013) | 0.595(+0.015) |

| Ranking Strategy 2. Euclidean Distance | ||||||||

| Accuracy(%) | 51.899 | 51.477(-0.422) | 55.274(+3.375) | 56.118(+4.219) | 52.321(+0.422) | 56.540(+4.641) | 56.118(+4.219) | 54.641(+2.742) |

| F1 score | 0.580 | 0.579(-0.001) | 0.611(+0.031) | 0.614(+0.034) | 0.583(+0.003) | 0.622(+0.042) | 0.616(+0.036) | 0.604(+0.024) |

| Ranking Strategy 3. TS2Vec Embedding | ||||||||

| Accuracy(%) | 51.899 | 56.540(+4.641) | 58.650(+6.751) | 50.211(-1.688) | 53.586(+1.687) | 51.899(+0.000) | 52.743(+0.844) | 53.938(+2.039) |

| F1 score | 0.580 | 0.616(+0.036) | 0.635(+0.055) | 0.563(-0.017) | 0.593(+0.013) | 0.578(-0.002) | 0.582(+0.002) | 0.595(+0.015) |

| Ranking Strategy 4. Multimodal Embedding | ||||||||

| Accuracy(%) | 51.899 | 57.806(+5.907) | 51.899(+0.000) | 55.274(+3.375) | 56.540(+4.641) | 57.384(+5.485) | 55.696(+3.797) | 55.767(+3.868) |

| F1 score | 0.580 | 0.628(+0.048) | 0.578(-0.002) | 0.610(+0.030) | 0.615(+0.035) | 0.624(+0.044) | 0.609(+0.029) | 0.610(+0.030) |

4.3. Multimodal

The multimodal method of ranking involves the use of both chart and news data to generate the embeddings for the time series. It also uses the same length and calculates the TS2Vec embedding of that time series first, then additionally computes the average news embedding between times and by using Crypto DeBERTa[9]. If the current timestep is then we use information from timesteps to calculate the TS2Vec embedding and gather all the news that were released in (not the entire 24 hours but just the past 4 hours) to calculate the average news embedding in this timeframe. We simply extract the [CLS] embedding of DeBERTa’s output for each news and average these [CLS] token representations. Then the average news embedding and the TS2Vec embedding are summed to create a multimodal embedding and similar to 4.2, we use the cosine distances of these embeddings to get the top 30 most similar past timesteps. Before summing the average news embedding and the TS2Vec embedding, we shrink the news embedding dimension from by applying uniform manifold approximation and projection[10]. For the news data we use Coinness Korea444https://coinness.com/, which is also followed in [9]. Multimodal embeddings should allow us to capture both the news sentiments and chart dynamics when searching for past patterns.

4.4. Random Sampling

Given some query timestep , the random sampling samples from all such that randomly. We use random sampling to observe the differences in performance boost when using random sampling versus some other ranking method, thus verifying that our ranking methods do indeed catch patterns from the past that in turn help model BTC price movement. For each query, we randomly sample top 30 past patterns 100 times and calculate the performance of random sampling 100 times with these 100 sampling cases to get a better idea of how random sampling performs.

5. Experimental Results

5.1. Performance Comparison

We can make interesting observations from the results in Table 1.

-

•

On average all of our IR-based FE improves over the baseline of no FE, with the multimodal strategy performing the best. Using the top 5 most similar multimodal embeddings has the best F1 score of 0.628 and we will be using this model for backtesting in section 5.2. The TS2Vec and multimodal strategies may have improved performance had we used a longer , but we leave this investigation for future research.

-

•

For our multimodal strategy, we separately calculated the accuracy of the model for the cases when it predicts or and when the ground truth action is also or . Considering this case is important because when the model chooses it does nothing so it does not incur any profit or loss. If the model chooses or but the ground truth is then even if the model’s decision is wrong, it would not result in a huge profit or loss since the volatility for that time frame would be small. Significant gains or losses happen when the model predicts or and when the ground truth action is also or . In this case the multimodal strategy outperforms the no IR-based FE baseline by more than 5% on average, while using the top 5 MultiModal IR-based FE outperforms no FE by close to 10%.

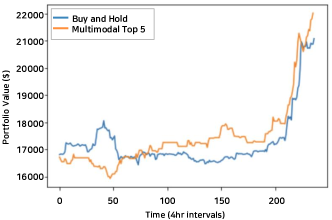

5.2. Backtest on Test set

The following assumptions were made for back testing: (1) We assume no take profit and a stop loss of 0.75%. (2) We use commission rate of 0.04%, equivalent to the maker fee when trading BTC/USDT perpetual in Binance. As a result in figure 2 shows, our model outperforms buy and hold for the duration of the test set. It is notable that the model predicts (short) effectively when the BTC prices are falling (e.g. around index 50), gaining edge over buy and hold. Also the model predicts (hold) very well (e.g. around index 100) for periods when there is less volatility and also predicts (long) around index 200 when the prices actually began to soar.

6. Conclusion and Future Work

In this research, we investigated how chart pattern matching can be incorporated into a BTC directional prediction model training framework. Among our proposed pattern matching methods, the multimodal embedding based method is the most effective. Overall, chart pattern matching based feature engineering seems promising and it can be further explored or coupled with other modeling techniques to more accurately forecast the volatile price movement of BTC.

7. Presentor Bio

Minsuk Kim received his B.S. degree in mathematics from Stanford University, Stanford, CA, USA, in 2021. He is currently working as an AI Scientist and an Engineer at MindsLab in Korea. His research interests include financial machine learning and natural language processing.

8. Company Portrait

We are primarily focuses on creating machine learning based trading bots and indicators for trading crypto assets.

References

- [1]

- Chen and Guestrin [2016] Tianqi Chen and Carlos Guestrin. 2016. XGBoost: A Scalable Tree Boosting System. In Proceedings of the 22nd ACM SIGKDD International Conference on Knowledge Discovery and Data Mining (San Francisco, California, USA) (KDD ’16). ACM, New York, NY, USA, 785–794. https://doi.org/10.1145/2939672.2939785

- Chen et al. [2020] Ting Chen, Simon Kornblith, Mohammad Norouzi, and Geoffrey Hinton. 2020. A simple framework for contrastive learning of visual representations. In International conference on machine learning. PMLR, 1597–1607.

- Devlin et al. [2019] Jacob Devlin, Ming-Wei Chang, Kenton Lee, and Kristina Toutanova. 2019. BERT: Pre-training of Deep Bidirectional Transformers for Language Understanding. In Proceedings of the 2019 Conference of the North American Chapter of the Association for Computational Linguistics: Human Language Technologies, Volume 1 (Long and Short Papers). Association for Computational Linguistics, Minneapolis, Minnesota, 4171–4186. https://doi.org/10.18653/v1/N19-1423

- Dong and Taslimitehrani [2016] Guozhu Dong and Vahid Taslimitehrani. 2016. Pattern-aided regression modeling and prediction model analysis. In 2016 IEEE 32nd International Conference on Data Engineering (ICDE). 1508–1509. https://doi.org/10.1109/ICDE.2016.7498398

- Gao et al. [2021] Tianyu Gao, Xingcheng Yao, and Danqi Chen. 2021. SimCSE: Simple Contrastive Learning of Sentence Embeddings. In Proceedings of the 2021 Conference on Empirical Methods in Natural Language Processing. Association for Computational Linguistics, Online and Punta Cana, Dominican Republic, 6894–6910. https://doi.org/10.18653/v1/2021.emnlp-main.552

- Gong and Si [2013] Xueyuan Gong and Yain-Whar Si. 2013. Comparison of subsequence pattern matching methods for financial time series. In 2013 Ninth International Conference on Computational Intelligence and Security. IEEE, 154–158.

- He et al. [2021] Pengcheng He, Xiaodong Liu, Jianfeng Gao, and Weizhu Chen. 2021. DEBERTA: DECODING-ENHANCED BERT WITH DISENTANGLED ATTENTION. In International Conference on Learning Representations. 1–21. https://openreview.net/forum?id=XPZIaotutsD

- Kim et al. [2023] Gyeongmin Kim, Minsuk Kim, Byungchul Kim, and Heuiseok Lim. 2023. CBITS: Crypto BERT Incorporated Trading System. IEEE Access 11 (2023), 6912–6921. https://doi.org/10.1109/ACCESS.2023.3236032

- McInnes et al. [2018] Leland McInnes, John Healy, and James Melville. 2018. Umap: Uniform manifold approximation and projection for dimension reduction. arXiv preprint arXiv:1802.03426 (2018).

- Nakamoto [2008] Satoshi Nakamoto. 2008. Bitcoin: A peer-to-peer electronic cash system. Decentralized Business Review (2008), 21260.

- Velay and Daniel [2018] Marc Velay and Fabrice Daniel. 2018. Stock chart pattern recognition with deep learning. arXiv preprint arXiv:1808.00418 (2018).

- Yue et al. [2022] Zhihan Yue, Yujing Wang, Juanyong Duan, Tianmeng Yang, Congrui Huang, Yunhai Tong, and Bixiong Xu. 2022. Ts2vec: Towards universal representation of time series. In Proceedings of the AAAI Conference on Artificial Intelligence, Vol. 36. 8980–8987.