remarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersAn efficient sieving based secant methodQian Li, Defeng Sun, and Yancheng Yuan \externaldocumentex_supplement

An efficient sieving based secant method for sparse optimization problems with least-squares constraints††thanks: Submitted to the editors DATE. \fundingThe work of the second author was supported by grants from the Research Grants Council of the Hong Kong Special Administrative Region, China (GRF Project No. 15304721 and RGC Senior Research Fellow Scheme No. SRFS2223-5S02). The work of the third author was supported by the Hong Kong Polytechnic University under grant P0038284.

Abstract

In this paper, we propose an efficient sieving based secant method to address the computational challenges of solving sparse optimization problems with least-squares constraints. A level-set method has been introduced in [X. Li, D.F. Sun, and K.-C. Toh, SIAM J. Optim., 28 (2018), pp. 1842–1866] that solves these problems by using the bisection method to find a root of a univariate nonsmooth equation for some , where is the value function computed by a solution of the corresponding regularized least-squares optimization problem. When the objective function in the constrained problem is a polyhedral gauge function, we prove that (i) for any positive integer , is piecewise in an open interval containing the solution to the equation ; (ii) the Clarke Jacobian of is always positive. These results allow us to establish the essential ingredients of the fast convergence rates of the secant method. Moreover, an adaptive sieving technique is incorporated into the secant method to effectively reduce the dimension of the level-set subproblems for computing the value of . The high efficiency of the proposed algorithm is demonstrated by extensive numerical results.

keywords:

level-set method, secant method, semismooth analysis, adaptive sieving90C06, 90C25, 90C90

1 Introduction

In this paper, we consider the following least-squares constrained optimization problem

| (CP()) |

where and are given data, is a given parameter satisfying , and is a proper closed convex function with that possess the property of promoting sparsity. Without loss of generality, we assume that Eq. CP() admits active solutions here.

Let be a given positive parameter. Compared to the following regularized problem of the form

| () |

the constrained optimization problem Eq. CP() is usually preferred in practical modeling since we can regard as the noise level, which can be estimated in many applications. However, the optimization problem Eq. CP() is perceived to be more challenging to solve in general due to the complicated geometry of the feasible set [1]. Some algorithms such as the alternating direction method of multipliers (ADMM) [14, 12] are applicable to solve Eq. CP(). Nevertheless, to obtain an acceptable solution remains challenging for these algorithms. In particular, when applying the ADMM for solving Eq. CP(), it is computationally expensive to form the matrix or to solve the linear systems involved in the subproblems. Recently, the dimension reduction techniques, such as the adaptive sieving [39, 38], have achieved some success in solving large-scale sparse optimization problems numerically by exploiting the solution sparsity. But it is still unclear how to apply dimension reduction techniques to Eq. CP() due to the potential feasibility issue for reduced problems.

A popular approach for solving Eq. CP() and the more general convex constrained optimization problems is the level-set method [34, 35, 1], which has been widely used in many interesting applications [34, 35, 1, 18]. The idea of exchanging the role of the objective function and the constraints, which is the key for the level-set method, has a long history and can date back to Queen Dido’s problem (see [27, Page 548]). Readers can refer to [1, Section 1.3] and the references therein for a discussion of the history of the level-set method. In particular, the level-set method developed in [34, 35] solves the optimization problem Eq. CP() by finding a root of the following univariate nonlinear equation

| () |

where is the value function of the following level-set problem

| (1) |

Therefore, by executing a root-finding procedure for Eq. (e.g., the bisection method), one can obtain a solution to Eq. CP() by solving a sequence of problems in the form of Eq. 1 parameterized by . In implementations, one needs an efficient procedure to compute the metric projection of given vectors onto the constraint set . However, such an efficient computation procedure may not be available. One example can be found in [18], where is the fused Lasso regularizer [32]. Moreover, it is still not clear to us how to deal with the feasibility issue when a dimension reduction technique is applied to Eq. 1.

Recently, Li et al. [18] proposed a level-set method for solving Eq. CP() via solving a sequence of Eq. . The dual of Eq. can be written as

| () |

where is the Fenchel conjugate function of . Let be the solution set to Eq. . Let be the gauge function of the subdifferential of at the origin. In this paper, we assume

| (2) |

and that for any , there exists satisfying the following Karush-Kuhn-Tucker (KKT) system

| (KKT) |

where is the subdifferential of . Consequently, the solution set is nonempty, and is invariant for all since the solution to Eq. is unique. Based on this fact, Li et al. [18] proposed to solve Eq. CP() by finding the root of the following equation:

| () |

where is any solution to Eq. . We assume that Eq. has at least one solution . We then know that any is a solution to Eq. CP() [18, 11]. There are several advantages to this approach. Firstly, it requires computing the proximal mapping of , which is normally easier than computing the projection over the constraint set of Eq. 1. Secondly, efficient algorithms are available to solve the regularized least-squares problem Eq. for a wide of class of functions [17, 18, 19, 41, 2, 14]. More importantly, this approach is well-suited for applying dimension reduction techniques to solve Eq. as can be seen in subsequent sections.

In this paper, we propose an efficient sieving based secant method for solving Eq. CP() by finding the root of Eq. . We call our algorithm SMOP as it is a root finding based Secant Method for solving the Optimization Problem Eq. CP(). We focus on the case where is a gauge function (see [28, Section 15]), i.e., is a nonnegative positively homogeneous convex function with . We start by studying the properties of the value function and the convergence rates of the secant method for solving Eq. . To address the computational challenges for solving Eq. and computing the function value of , we incorporate an adaptive sieving (AS) technique [39, 38] into the secant method to effectively reduce the dimension of Eq. . The AS technique can exploit the sparsity of the solution of Eq. so that one can obtain a solution to Eq. by solving a sequence of reduced problems with much smaller dimensions. Extensive numerical results will be presented in this paper to demonstrate the superior performance of the proposed algorithm in solving Eq. CP().

The main contributions of this paper can be summarized in the following:

- 1.

-

2.

Under the assumption that is a polyhedral gauge function, we show that the secant method converges at least 3-step Q-quadratically for solving Eq. , and if is a singleton, the secant method converges superlinearly with Q-order at least . Furthermore, for a general strongly semismooth function , if is a singleton, the secant method converges superlinearly with R-order of at least .

-

3.

We propose an efficient sieving based secant method to address the computational challenges for solving Eq. CP(). The algorithm incorporates a fast convergent secant method for root-finding of Eq. , along with an AS technique for effectively reducing the dimension of subproblems in the form of Eq. . The efficiency of the proposed algorithm for solving Eq. CP() will be demonstrated by extensive numerical results.

The rest of the paper is organized as follows: We will introduce some necessary preliminary results in Section 2. We discuss the properties of the value function in Sections 3 and 4. A secant method for solving Eq. CP() will be introduced and analyzed in Section 5. We will introduce the AS technique in Section 6 followed by presenting extensive numerical results in Section 7. We conclude the paper in Section 8.

Notation. Let be any given integer. Denote the nonnegative orthant and the positive orthant of as and , respectively. We denote . We denote the subvector generated by indexed by as and submatrix generated by the columns (rows) of indexed by () as (). For any and any integer , the norm of is defined as . We denote . Let be an open set. We say that a function is for some integer if is -times continuously differentiable on . Let be a proper closed convex function. The proximal mapping of is defined by

Let be the Fenchel conjugate function of , i.e., . The polar of is defined by . Let be a nonempty closed convex set. The indicator function of is defined as

The gauge function of is defined as .

2 Preliminaries

Let and be two finite dimensional real vector spaces each equipped with a scalar product and its induced norm . Denote the set of all linear operators from to by . We first review some preliminary results related to the generalized Jacobians and the semismoothness. Let be an open set and be a locally Lipschitz continuous function on . According to Rademacher’s theorem, is differentiable (in the sense of Frchet) almost everywhere on . Denote by the set of all points on where is differentiable. Denote as the Jacobian of at . Define the B-subdifferential of at as

| (3) |

The Clarke generalized Jacobian of at is then defined as follows [8]:

| (4) |

Note that both and are compact valued and upper-semicontinuous multi-valued functions. For finitely valued convex functions, the Clarke generalized Jacobian coincides with the subdifferential in the sense of convex analysis [8, Proposition 2.2.7]. Now, we introduce the concept of G-semismoothness (with respect to a multifunction).

Definition 2.1.

Let be an open set, be a locally Lipschitz continuous function, and be a nonempty and compact valued, upper-semicontinuous set-valued mapping. is said to be G-semismooth at with respect to the multifunction , if for any with ,

| (5) |

Let be a constant. is said to be -order (strongly, if ) G-semismooth at with respect to if for any with ,

| (6) |

is said to be G-semismooth (respectively, -order G-semismooth, strongly G-semismooth) on with respect to the multifunction if it is G-semismooth (respectively, -order G-semismooth, strongly G-semismooth) everywhere in with respect to the multifunction . All the above definitions of G-semimsoothness will be replaced by semismoothness if happens to be directionally differentiable at the concerned point .

Let be a real valued functional. Denote for that

| (7) |

The following lemma is useful for analyzing the convergence of the secant method. Part (i) of this lemma is from [23, Lemma 2.2], and Part (ii) can be proved by following a similar procedure as in the proof of [23, Lemma 2.3].

Lemma 2.2.

Assume that is semismooth at . Denote the lateral derivatives of at by

| (8) |

Then the lateral derivatives and exist and

It holds that

| (9) | |||

| (10) |

moreover, if is -order semismooth at for some , then

| (11) | |||

| (12) |

3 Properties of the value function

In this section, we first discuss some useful properties of the function . Since is assumed to be a nonnegative convex function with , we know that .

Proposition 3.1.

Assume that . It holds that {romannum}

for all , and ;

the value function is nondecreasing on and for any , implies , where for any , is an optimal solution to Eq. .

Proof 3.2.

(i) Since , for all , it holds that

which implies that . Since and is closed, we know

which implies that . Therefore, for all , and .

(ii) Let be arbitrarily chosen. Let and . Then, we have

| (13) | |||||

| (14) |

which implies that

| (15) |

Since , we know that . It follows from (13) that

which implies that if . This completes the proof of the proposition.

Due to Proposition 3.1, we can apply the bisection method to solve Eq. and for any we can obtain a solution satisfying in iterations, where is a solution to Eq. . In this paper, we will design a more efficient secant method for solving Eq. . To achieve this goal, we first study the (strong) semismoothness property of .

In this paper, we focus on the case where is a gauge function. In most of the applications, is a norm function, which is automatically a gauge function. We will leave the study of the (strong) semismoothness of for a general as future work. Because of its repeated occurrence in this section, we present the following assumption:

Assumption A: Assume that is a gauge function.

Under Assumption A, and the optimization problem Eq. is equivalent to

| (16) |

where

| (17) |

Then by performing a variable substitution, we have the following useful observation about the solution mapping to Eq. 16.

Proposition 3.3.

The following proposition is useful in understanding the semismoothness of and even if is non-polyhedral. The definition of a tame set and a globally subanalytic set can be found in [3, Definition 2] and [3, Example 2(a)], respectively. Part (ii) of the proposition is generalized from [18, Proposition 1 (iv)] ( is assumed to be a polyhedral gauge function in [18]) and we provide a more explicit proof that does not rely on the piecewise linearity of the solution mapping in Eq. 18.

Proposition 3.4.

Assume that . Under Assumption A, it holds that {romannum}

the functions and are locally Lipschitz continuous on ;

the function is strictly increasing on ;

if the set is tame, then is semismooth on ;

if is globally subanalytic, then is -order semismooth on for some .

Proof 3.5.

For convenience, we denote for any .

(i) Since is Lipschitz continuous with modulus , both and are locally Lipschitz continuous on . Therefore, is locally Lipschitz continuous on .

(ii) It follows from Proposition 3.1 that is nondecreasing. We will now prove that is strictly increasing on . We prove it by contradiction. Assume that there exist such that . Let and be arbitrarily chosen. From Proposition 3.1 (ii), we know that

which implies that and . Therefore, we get

| (19) |

Since is a gauge function, we know that [10, Proposition 2.1 (iv)]. Since is also a gauge function [28, Theorem 15.1], for any , the constraint in Eq. 16 is equivalent to

| (20) |

Thus, it holds that

The optimality condition to Eq. 16 (replacing the constraint with Eq. 20) implies that and . Therefore, we have

which is a contradiction.

(iii) Since is locally Lipschitz continuous on , it follows from [3] that is semismooth on if is a tame set. Since is strongly semismooth, we know that is semismooth on . Therefore, is semismooth on [9, Proposition 7.4.4, Proposition 7.4.8].

(iv) The -order semismoothness of can be proved similarly as for (iii).

The above proposition can be used to prove the semismoothness of for a wide class of functions . For example, the next corollary shows the semismoothness of when is the nuclear norm function defined on , using the fact that is linear matrix inequality representable [26].

Corollary 3.6.

Denote the adjoint of the linear operator as . Let be the nuclear norm function defined on . Then is a tame set and is semismooth.

Next, we will show that can be strongly semismooth for a class of important instances of .

Proposition 3.7.

Define and

For any , denote as the Canonical projection of onto . Under Assumption A, it holds that {romannum}

if is strongly semismooth and is nondegenerate at some satisfying , then and are strongly semismooth at ;

if is further assumed to be polyhedral, the function is piecewise affine and is strongly semismooth on .

Proof 3.8.

(i) It follows from the Moreau identity [28, Theorem 31.5] that for any ,

The rest of the proof can be obtained from the fact that is linear and the Implicit Function Theorem for semismooth functions [29, 20].

(ii) When is a polyhedral gauge function, we know that the set defined in Eq. 17 is a convex polyhedral set [28, Theorem 19.3] and the projector is piecewise affine [9, Proposition 4.1.4]. Therefore, is a piecewise affine function on . Then both and are strongly semismooth on [9, Proposition 7.4.7, Proposition 7.4.4, Proposition 7.4.8].

Remark 3.9.

We make some remarks on the assumptions in Part (i) of Proposition 3.7. On one hand, the strong semismoothness of the projector has been proved for some important non-polyhedral closed convex sets . In particular, is strongly semismooth if is the positive semidefinite cone [31], the second-order cone [6], or the norm ball [41, Lemma 2.1]. On the other hand, the assumption of the nondegeneracy of at the concerned point is closely related to the important concept of strong regularity of the KKT system of Eq. . One can refer to the Monograph [4] and the references therein for a general discussion, and to [30, 5] for the semidefinite programming problems.

4 The HS-Jacobian of for polyhedral gauge functions

In this section, we assume by default that is a polyhedral gauge function. Then the set is polyhedral [28, Theorem 19.2], which can be assumed without loss of generality, to take the form of

| (21) |

for some and .

Inspired by the generalized Jacobian for the projector over a polyhedral set derived by Han and Sun [15], which we call the HS-Jacobian, we will derive the HS-Jacobian of the function . As an important implication, we will prove that the Clarke Jacobian of at any is positive. Note that the open interval contains the solution to Eq. .

Let be arbitrarily chosen. Let be the unique solution to Eq. with the parameter . Here, we denote to simplify our notation and hide the dependency on . Then there exists such that satisfies the following KKT system:

| (22) |

Therefore, is the unique solution to the following optimization problem

| (23) |

and there exists such that satisfies the following KKT system for Eq. 23:

| (24) |

As a result, there exists such that satisfies the following augmented KKT system

| (25) |

Let be the set of Lagrange multipliers associated with defined as

Since , we obtain the following system by eliminating the variable in Eq. 25:

| (26) |

where . Denote

| (27) |

Then, the set is equivalent to

| (28) |

Denote the active set of as

| (29) |

For any , we define

| (30) |

Since the polyhedral set does not contain a line, this implies that has at least one extreme point [28, Corollary 18.5.3]. Note that and , which implies that and is nonempty.

Define the HS-Jacobian of as

| (31) |

where is the subvector of indexed by . For notational convenience, for any and , denote

| (32) |

Define

| (33) |

where . The following lemma is proved by following the same line as in [15, Lemma 2.1].

Lemma 4.1.

Let be arbitrarily chosen. It holds that

| (34) |

Moreover, there exists a positive scalar such that and for all , {romannum}

;

.

Proof 4.2.

Choose a sufficiently small such that and let be arbitrarily chosen. Denote and for notational simplicity.

Let be arbitarily chosen. From Eq. 26, there exists with such that satisfies

| (35) |

where is the complement of , which implies

Since is of full column rank, we have

Consequently, we have

where .

(i) It follows from Proposition 3.4 that is locally Lipshitz continuous, which implies that . Next, we prove that . If not, then there exists a sequence converges to , such that for all , there is an index set . Denote the solution to Eq. with the parameter as . Since there exist only finitely many choices for the index sets in , if necessary by taking a subsequence we assume that the index sets are identical for all . Denote the common index set as . Then, the matrix has full column rank and there exists (and ) such that but . Since , then there is no such that . However, since , it satisfies

| (36) |

As is locally Lipschitz continuous and is of full column rank, the sequence is bounded. Let be an accumulation point of , then and . This is a contradiction. Therefore, . From the definition of in Eq. 31, we also have .

(ii) Let be arbitarily chosen. It follows from Eq. 34 that

where . Since and , in a same vein, we have

As a result, for all ,

We complete the proof of the lemma.

Next, we prove the nondegeneracy of for any , which is important for analyzing the convergence rates of the secant method for solving Eq. .

Theorem 4.3.

Let be a polyhedral gauge function. For any , it holds that {romannum}

for any integer , the function is piecewise in an open interval containing ;

all are positive.

Proof 4.4.

Choose a sufficiently small such that and for any . Let and be arbitrarily chosen. Denote

Then, we have .

Now, we prove Part (i) of the theorem. From the fact

and Lemma 4.1, we know that

Define by

| (37) |

From Proposition 3.4, we know that is strictly increasing on . Therefore, it holds that

| (38) |

which implies that . Since is arbitrarily chosen, we obtain that

| (39) |

Thus, for any integer , is on .

Denote . We know that and is finite. Moreover,

| (40) |

which implies that for any , is piecewise on .

5 A secant method for Eq. CP()

In this section, we will design a fast convergent secant method for solving Eq. and prove its convergence rates.

5.1 A fast convergent secant method for semismooth equations

Let be a locally Lipschitz continuous function which is semismooth at a solution to the following equation

| (43) |

In this section, we analyze the convergence of the secant method described in Algorithm 1 with two generic starting points and .

| (44) |

The convergence results of Algorithm 1 are given in the following proposition. The proof can be obtained by following the procedure in the proof of [23, Theorem 3.2].

Proposition 5.1.

Suppose that is semismooth at a solution to Eq. 43. Let and be the lateral derivatives of at as defined in Eq. 8. If and are both positive (or negative), then there are two neighborhoods and of , , such that for , Algorithm 1 is well defined and produces a sequence of iterates such that . The sequence converges to 3-step Q-superlinearly, i.e., . Moreover, it holds that {romannum}

for ;

if , then converges to Q-linearly with Q-factor ;

if is -order semismooth at for some , then for sufficiently large ; the sequence converges to 3-step quadratically if is strongly semismooth at .

Here, we only consider the case for since the function we are interested in is nondecreasing. For the case , one can refer to [23, Theorem 3.3].

When is small and is strongly semimsooth, we know from Proposition 5.1 that the secant method converges with a fast linear rate and 3-step Q-quadratic rate. We provide a numerical example slightly modified from [23, Equation (3.15)] to illustrate the convergence rates obtained in Proposition 5.1. We test Algorithm 1 with and for finding the zero of

| (45) |

where is chosen from . The numerical results are shown in Table 1, which coincide with our theoretical results.

| Case | Iter | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

|---|---|---|---|---|---|---|---|---|---|

| I | -5.1e-5 | -4.3e-6 | 2.2e-10 | -2.2e-11 | -1.8e-12 | 4.1e-23 | -4.1e-24 | -3.4e-25 | |

| II | -5.1e-5 | -1.7e-5 | 8.4e-10 | -4.2e-10 | -1.1e-10 | 4.5e-20 | -2.2e-20 | -5.6e-21 | |

| III | -5.1e-5 | -2.6e-5 | 1.3e-9 | -1.5e-9 | -5.1e-10 | 7.4e-19 | -8.2e-19 | -2.8e-19 |

Note that [23, Lemma 4.1] implies that the sequence generated by Algorithm 1 converges suplinearly with Q-order at least . Next, we will prove that the sequence generated by Algorithm 1 converges superlinearly to a solution to Eq. 43 with R-order at least when is strongly semismooth at and is a singleton and nondegenerate. This coincides with the convergence rate of the secant method for solving smooth equations [33].

Proposition 5.2.

Let be a solution to Eq. 43. Let be the sequence generated by Algorithm 1 for solving (43). Denote (for ) and (for ). Assume that is a singleton and nondegenerate. It holds that {romannum}

if is semismooth at , the sequence converges to Q-superlinearly;

if is strongly semismooth at , then either one of the following two properties is satisfied: (1) converges to superlinearly with Q-order at least ; (2) converges to superlinearly with R-order at least and there exist a constant and a subsequence satisfying .

Proof 5.3.

Let and be the neighborhoods of specified in Proposition 5.1. Assume that . Then Algorithm 1 is well defined and it generates a sequence which converges to . Denote for some . Let and be the lateral derivatives of at as defined in Eq. 8. Then,

Let be a sufficiently large integer. For all , we have

| (46) |

(i) Assume that is semismooth at . We estimate

by considering the following two cases.

(i-a) or . From Lemma 2.2, we obtain that

(i-b) or . We will consider the first case. The second case can be treated similarly. By Lemma 2.2, it holds that

Therefore,

Thus, we prove that the sequence converges to Q-superlinearly.

(ii) Now, assume that is strongly semismooth at . We build the recursion for for sufficiently large integers by considering the following two cases.

(ii-a) or . From Lemma 2.2, we obtain

(ii-b) or . We will consider the first case. The second case can be treated similarly. By Lemma 2.2, it holds that

and

Therefore, for sufficiently large integers , we have,

| (47) |

and

| (48) |

Then, there exists a constant and a positive integer such that

Therefore, it follows from [21, Theorem 9.2.9] that converges to with R-order at least .

If there exists a constant such that for sufficiently large , it follows from [22, Corollary 3.1] that converges to Q-superlinearly with Q-order at least . We complete the proof.

Proposition 5.4.

Let be a polyhedral gauge function. Let be the solution to (). If is a singleton, the sequence generated by Algorithm 1 for solving () converges to Q-superlinearly with Q-order at least .

Proof 5.5.

The assumption is a singleton implies that is strictly differentiable at [8, Proposition 2.2.4]. It follows from Theorem 4.3 that and is piecewise for any positive integer in a neighborhood of .

Choose a sufficiently small such that and for any . Denote . Let be arbitrarily chosen. Define by

By choosing a smaller if necessary, we assume that is a minimal local representation for at . Therefore, it follows from [25, Theorem 2] that

Since , we have

Therefore, is on for any integer . It follows from [33, Example 6.1] that converges to Q-superlinearly with Q-order at least .

We give the following example to show that a function satisfying the assumptions in (ii) of Proposition 5.2 is not necessarily piecewise smooth:

| (49) |

where is a given constant.

Proposition 5.6.

The function defined in Eq. 49 is strongly semismooth at but not piecewise smooth in the neighborhood of .

Proof 5.7.

By the construction of , we know that it is not piecewise smooth in the neighborhood of since there are infinitely many non-differentiable points. Next, we show that is strongly semismooth at .

Firstly, it is not difficult to verify that is Lipschitz continuous with modulus . Secondly, we know that , and for any integer , it holds that

which implies that

Therefore, is directionally differentiable at . Note that both and are singleton when .

Next, we show that is strongly G-semismooth at . On the one hand, for any , we have

On the other hand, for any integer and , we know

which implies that

Therefore,

The proof of the proposition is completed.

We end this subsection by illustrating the numerical performance of Algorithm 1 for finding the root of given in Eq. 49 with . Note that is the unique solution. In Algorithm 1, we choose and . The numerical results are shown in Table 2.

| Iter | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 |

|---|---|---|---|---|---|---|---|---|

| 1.7e-1 | 3.6e-2 | 4.0e-3 | 1.0e-4 | 2.7e-7 | 2.0e-11 | 4.0e-18 | 6.1e-29 | |

| 1.9e-1 | 3.7e-2 | 4.0e-3 | 1.0e-4 | 2.7e-7 | 2.0e-11 | 4.0e-18 | 6.1e-29 |

We can observe that the generated sequence converges to the solution superlinearly with R-order at least .

5.2 A globally convergent secant method for Eq. CP()

In this section, we propose a globally convergent secant method for solving Eq. CP() via finding the root of Eq. . The algorithm is described in Algorithm 2.

| (50) |

Theorem 5.8.

Let be a gauge function. Denote as the solution to Eq. . Then Algorithm 2 is well defined and the sequences and converge to and a solution to Eq. CP(), respectively. Denote for all . Suppose that both and of at as defined in Eq. 8 are positive, the following properties hold for all sufficiently large integer : {romannum}

If is semismooth at , then ;

if is -order semismooth at for some , then ;

if is a singleton and is semismooth at , then converges to zero Q-superlinearly; if is further assumed to be polyhedral and is a singleton, then converges to zero superlinearly with Q-order .

Proof 5.9.

When is a gauge function, we know from Proposition 3.4 that is strictly increasing on , which implies that the sequences and generated in Algorithm 2 are well defined. For any , if we run the algorithm for three more iterations, then it holds that either (a) will reduce at least half; or (b) . Therefore, the sequence will converge to . Suppose that is semismooth at and both and are positive. We know from Proposition 5.1 that there exists a positive integer such that for all , and

| (51) |

Therefore, it follows from Lemma 2.2 that

Thus, for all ,

The rest of the proof of this theorem follows from Proposition 5.1 and Proposition 5.4.

To better illustrate the efficiency of Algorithm 2, we will compare its performance to the HS-Jacobian based semismooth Newton method for solving Eq. on the least-squares constrained Lasso problem, where the HS-Jacobian is available. The following proposition shows that for the least-squares constrained Lasso problem, is positive for any .

Proposition 5.10.

Proof 5.11.

Recall that is nonempty. Let be arbitrarily chosen. We know that is of full column rank. Denote . Since , it holds that

Therefore, it follows from Lemma 4.1 and the facts and that

which implies that

Since is arbitrarily chosen, we know that for all .

When , the set has the representation of

In other words, and . Therefore, for any and .

The numerical results in Section 7 will show that the secant method and the semismooth Newton method are comparable for solving the least-squares constrained Lasso problem, which also demonstrates the high efficiency of the secant method even for the case that the HS-Jacobian can be computed.

6 An adaptive sieving based secant method for Eq. CP()

A main computational challenge (especially for high dimensional problems) for solving Eq. comes from computing the function value of , which requires solving the optimization problem Eq. . To address this challenge, we will incorporate a dimension reduction technique called adaptive sieving to Algorithm 2.

6.1 An adaptive sieving technique for sparse optimization problems

We briefly introduce the AS technique developed in [39] for solving sparse optimization problems of the following form:

| (52) |

where is a continuously differentiable convex function, and is a closed proper convex function. We assume that the convex composite optimization problem Eq. 52 has at least one solution. Certainly, the optimization problem Eq. is a special case of Eq. 52. We define the proximal residual function as

| (53) |

The norm of is a standard measurement for the quality of an obtained solution, and is a solution to Eq. 52 if and only if .

Let be an index set. We consider the following constrained optimization problem with the index set :

| (54) |

where is the complement of . A key fact is that, a solution to Eq. 54 is also a solution to Eq. 52 if there exists a solution to Eq. 52 such that . The AS technique is motivated by this fact. Specifically, starting with a reasonable guessing , the AS technique is an adaptive strategy to refine the current index set based on a solution to Eq. 54 with . We present the details of the AS technique for solving Eq. 52 in Algorithm 3.

| (55) |

| (56) |

| (57) |

It is worthwhile mentioning that, in Algorithm 3, the error vectors , in (55) and (57) are not given but imply that the corresponding minimization problems can be solved inexactly. We can just take (for ) if we solve the reduced subproblems exactly. The following proposition shows that we can obtain an inexact solution by solving a reduced problem with a much smaller dimension.

Proposition 6.1 ([39, Proposition 1]).

For any given nonnegative integer , the updating rule of in Algorithm 3 can be interpreted in the procedure as follows. Let be a linear map from to defined as

and , be functions from to defined as , for all . Then can be computed as

and , where is an approximate solution to the problem

| (58) |

which satisfies

| (59) |

and is the parameter given in Algorithm 3.

The finite termination property of Algorithm 3 for solving Eq. 52 is shown in the following proposition.

6.2 An adaptive sieving based secant method for Eq. CP()

When applying the level-set method to solve Eq. CP(), one needs to solve a sequence of regularized problems in the form of Eq. with generated by the root-finding algorithm for solving Eq. . This naturally motivates us to incorporate Algorithm 3 into Algorithm 2 for solving the regularized least-squares problems in the form of Eq. since we can effectively construct an initial index set for the AS technique based on the solution of the previous problem on the solution path. For the first problem on the solution path, we will choose to be relatively large such that its solution is highly sparse. In such a way, we choose in Algorithm 3 for the first problem. We present the details in Algorithm 4.

We make some remarks before concluding this section. Firstly, we can naturally apply Algorithm 4 to efficiently generate a solution path for Eq. CP() with a sequence of noise-level controlling parameters . Secondly, we know that, if we apply the AS technique to the level-set method based on Eq. , we may easily encounter the infeasibility issue if in Eq. 1.

7 Numerical experiments

In this section, we will present numerical results to demonstrate the high efficiency of our proposed SMOP. We will focus on solving Eq. CP() with two objective functions: (1) the penalty: , ; (2) the sorted penalty: , with given parameters and , where , which serve as illustrative examples to highlight the efficiency of our algorithm. It is worthwhile mentioning that the sorted penalty is not separable.

| Problem idx | Name | m | n | Sparsity(A) | norm(b) |

|---|---|---|---|---|---|

| 1 | E2006.train | 16087 | 150360 | 0.0083 | 452.8605 |

| 2 | log1p.E2006.train | 16087 | 4272227 | 0.0014 | 452.8605 |

| 3 | E2006.test | 3308 | 150358 | 0.0092 | 221.8758 |

| 4 | log1p.E2006.test | 3308 | 4272226 | 0.0016 | 221.8758 |

| 5 | pyrim5 | 74 | 201376 | 0.5405 | 5.7768 |

| 6 | triazines4 | 186 | 635376 | 0.6569 | 9.1455 |

| 7 | bodyfat7 | 252 | 116280 | 1.0000 | 16.7594 |

| 8 | housing7 | 506 | 77520 | 1.0000 | 547.3813 |

In our numerical experiments, we measure the accuracy of the obtained solution for Eq. CP() by the following relative residual:

where . We test all algorithms on datasets from UCI Machine Learning Repository as in [17, 18], which are originally obtained from the LIBSVM datasets [7]. Table 3 presents the statistics of the tested UCI instances. All our computational results are obtained using MATLAB R2023a on a Windows workstation with the following specifications: 12-core Intel(R) Core(TM) i7-12700 (2.10GHz) processor, and 64 GB of RAM. In all the tables presented in this section, represents the number of elements in the solution obtained by SMOP (with a stopping tolerance of ) for solving Eq. CP() that have an absolute value greater than . Besides, We denote BMOP (NMOP) as the root finding based bisection method (hybrid of the bisection method and the semismooth Newton method) for solving the optimization problem Eq. CP().

7.1 The penalized problems with least-squares constraints

In this subsection, we focus on the problem Eq. CP() with . We will compare the efficiency of SMOP to the state-of-the-art SSNAL-LSM algorithm [18], SPGL1 solver [34, 36] and ADMM. Moreover, we perform experiments to demonstrate that our secant method is considerably more efficient than the bisection method for root finding while performing on par with the semi-smooth Newton method, where the HS-Jacobian is computable.

| Test | idx | 1 | 2 | 3 | 4 | 5 | 6 | 7 | 8 \bigstrut |

|---|---|---|---|---|---|---|---|---|---|

| I | c | 0.1 | 0.1 | 0.08 | 0.08 | 0.05 | 0.1 | 0.001 | 0.1 \bigstrut[t] |

| nnz(x) | 339 | 110 | 246 | 405 | 79 | 655 | 107 | 148 | |

| 2.6-7 | 2.8-4 | 4.2-7 | 2.1-4 | 5.7-3 | 2.8-3 | 1.1-6 | 1.3-3 \bigstrut[b] | ||

| II | c | 0.09 | 0.09 | 0.06 | 0.06 | 0.015 | 0.03 | 0.0001 | 0.04 \bigstrut[t] |

| nnz(x) | 1387 | 1475 | 884 | 1196 | 92 | 497 | 231 | 377 | |

| 1.1-7 | 6.2-5 | 1.7-7 | 9.6-5 | 3.0-4 | 5.6-5 | 3.8-8 | 3.0-5 \bigstrut[b] |

In practice, we have multiple choices for solving the sub-problems in SMOP. In our experiments, we utilized the squared smoothing Newton method [24, 13] and SSNAL to solve the sub-problems in SMOP. The maximum number of iterations for SPGL1, SSNAL, and ADMM is set to 100,000, while for SMOP and SSNAL-LSM, the maximum number of iterations of the outermost loop is set to 200. Additionally, we have set the maximum running time to 1 hour. To select , we use the values of in Table 4 for each instance listed in Table 3, and let . At last, we point out that the adaptive sieving technique is not employed in the SSNAL-LSM.

| idx | time (s) | outermost iter \bigstrut | |

| A1 A2 A3 A4 | A1 A2 A3 A4 | A1 A2 A3 A4 \bigstrut | |

| Test I with stoptol = \bigstrut[t] | |||

| 1 | 1.39+0 2.18+2 3.51+2 4.22+2 | 2.3-5 4.9-5 1.0-4 1.0-4 | 24 29 7342 2049 \bigstrut[t] |

| 2 | 2.29+0 5.12+2 1.45+3 6.84+2 | 3.1-6 7.8-5 9.0-5 8.7-5 | 12 16 3445 1470 |

| 3 | 4.021 5.83+1 3.21+2 8.87+1 | 9.4-6 2.6-5 1.0-4 1.0-4 | 24 30 21094 4918 |

| 4 | 1.59+0 2.06+2 7.19+2 9.90+1 | 1.2-5 7.3-5 9.5-5 1.3-5 | 13 15 3174 854 |

| 5 | 2.731 1.20+1 9.81+0 5.63+0 | 6.9-6 5.4-6 7.4-5 2.2-5 | 6 14 498 273 |

| 6 | 2.32+0 1.74+2 3.35+2 1.01+2 | 5.8-6 4.4-5 9.1-5 7.5-5 | 9 17 1987 571 |

| 7 | 4.351 9.12+0 8.98+0 8.59+0 | 2.8-5 5.9-5 9.8-5 9.9-5 | 15 18 539 583 |

| 8 | 2.991 9.07+0 1.29+1 7.94+0 | 2.6-5 8.6-5 1.0-4 9.0-5 | 10 14 515 424 |

| Test I with stoptol = \bigstrut[t] | |||

| 1 | 1.45+0 3.22+2 1.51+3 7.06+2 | 2.5-7 6.1-8 9.9-7 1.0-6 | 25 36 28172 3539 \bigstrut[t] |

| 2 | 2.52+0 6.68+2 1.75+3 3.42+3 | 9.9-8 3.5-8 9.2-7 9.9-7 | 13 24 4155 8725 |

| 3 | 4.121 7.40+1 2.11+3 1.81+2 | 1.1-8 2.3-7 6.2-6 1.0-6 | 25 35 100000 10100 |

| 4 | 1.72+0 3.40+2 1.04+3 4.03+2 | 1.3-9 5.7-7 7.2-7 7.9-7 | 14 26 4584 3820 |

| 5 | 2.931 1.61+1 4.58+1 3.95+2 | 1.0-7 6.0-8 9.1-7 9.8-7 | 7 19 2468 20155 |

| 6 | 2.47+0 2.13+2 8.24+2 2.31+3 | 3.0-7 4.0-7 8.2-7 3.4-7 | 10 23 5578 13672 |

| 7 | 4.681 1.18+1 9.11+0 1.85+1 | 1.9-9 9.6-7 2.7-7 9.9-7 | 17 22 544 1250 |

| 8 | 3.281 1.45+1 3.84+1 4.40+1 | 2.4-7 8.4-8 4.0-7 8.7-7 | 11 24 1539 2427 |

| Test II with stoptol = \bigstrut[t] | |||

| 1 | 7.26+0 4.51+2 1.38+3 6.12+2 | 3.0-6 4.6-5 1.0-4 1.0-4 | 26 30 27775 3014 \bigstrut[t] |

| 2 | 6.79+0 1.54+3 1.32+3 4.01+2 | 1.8-5 3.6-5 9.7-5 6.8-5 | 14 21 3000 733 |

| 3 | 3.51+0 1.84+2 1.50+3 1.34+2 | 1.3-5 2.3-5 8.7-2 1.0-4 | 25 29 100000 7333 |

| 4 | 2.91+0 6.91+2 6.23+2 4.94+1 | 7.5-6 3.6-6 9.6-5 5.8-5 | 14 22 2694 385 |

| 5 | 6.231 1.53+1 8.65+0 2.01+1 | 2.8-5 7.9-6 6.6-5 9.5-5 | 9 13 395 1000 |

| 6 | 9.02+0 3.46+2 3.60+3 3.82+2 | 6.8-6 3.7-5 7.6-2 9.9-5 | 12 17 24924 2232 |

| 7 | 1.50+0 1.59+1 3.06+2 3.39+1 | 1.6-5 8.7-6 9.9-5 9.8-5 | 12 18 19820 2340 |

| 8 | 2.37+0 1.90+1 1.69+2 1.19+1 | 1.4-6 8.9-5 9.1-5 9.8-5 | 13 18 5914 644 |

| Test II with stoptol = \bigstrut[t] | |||

| 1 | 7.23+0 5.96+2 3.60+3 8.82+2 | 3.79 2.9-7 3.6-2 1.0-6 | 27 35 62384 4453 \bigstrut[t] |

| 2 | 7.37+0 1.85+3 2.04+3 1.46+3 | 1.47 3.9-7 9.7-7 1.0-7 | 15 27 4688 3464 |

| 3 | 3.59+0 2.36+2 1.49+3 1.99+2 | 8.1-10 8.3-7 8.7-2 1.0-6 | 26 36 100000 11051 |

| 4 | 3.02+0 8.44+2 1.37+3 2.18+2 | 3.19 4.3-7 9.9-7 6.0-7 | 15 28 5912 1980 |

| 5 | 6.371 2.49+1 4.14+2 1.48+2 | 2.47 3.0-8 8.7-7 9.7-7 | 10 22 22091 7592 |

| 6 | 9.37+0 4.25+2 3.60+3 3.60+3 | 5.4-11 6.7-7 7.5-2 1.2-7 | 14 22 25158 21556 |

| 7 | 1.59+0 2.09+1 3.37+2 8.54+1 | 3.27 1.9-8 8.8-7 9.7-7 | 13 23 21523 5817 |

| 8 | 2.39+0 2.68+1 1.65+3 3.34+1 | 4.57 6.9-7 8.8-7 9.8-7 | 14 26 59147 1834 |

We compare SMOP to SPGL1, SSNAL-LSM and ADMM to solve Eq. CP() with the tolerances of and , respectively. The test results are presented in Table 5. These results indicate that SMOP successfully solves all the tested instances and outperforms SSNAL-LSM, SPGL1 and ADMM. It can be seen from Table 5 that SMOP can achieve a speed-up of up to 1,000 times compared to SPGL1 for the problems that can be solved by SPGL1 (a significant number of instances cannot be solved by SPGL1 to the required accuracy). Regarding ADMM, SMOP remains significantly superior in terms of efficiency for all cases, with a speed-up of over 1300 times. Furthermore, compared to SSNAL-LSM, SMOP also shows vast superiority, with efficiency improvements up to more than 260 times. Note that SPGL1 has two modes: the primal mode (denoted by SPGL1) and the hybrid mode (denoted by SPGL1_H). We do not print the results of SPGL1_H since SPGL1 outperforms SPGL1_H in most of the cases in our tests.

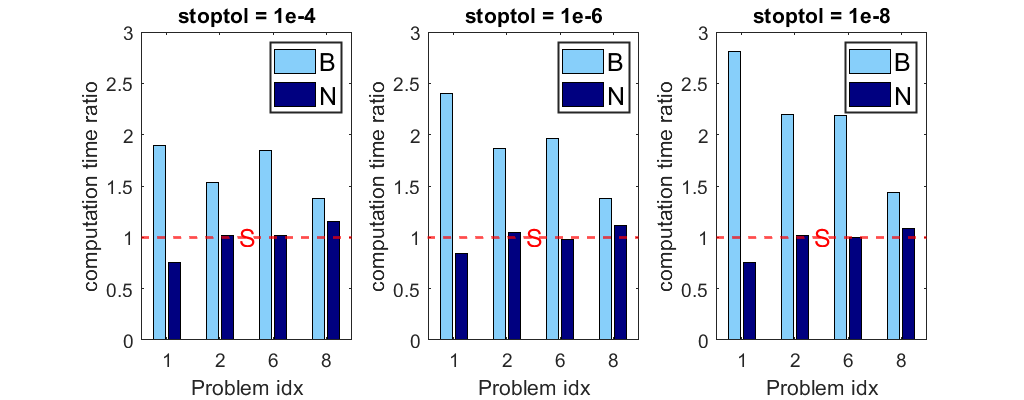

Subsequently, we perform numerical experiments to compare the performance of the secant method to the bisection method and the HS-Jacobian based semismooth Newton method for finding the root of Eq. to further illustrate the efficiency of SMOP. Fig. 1 presents the ratio of computation time between BMOP and NMOP to the computation time of SMOP on solving Eq. CP() for some instances. The numerical results show that SMOP easily beats BMOP, with a large margin when a higher precision solution is required. The results also reveal that SMOP performs comparably to NMOP for solving the penalized least-squares constrained problem, in which the HS-Jacobian are computable. This is another strong evidence to illustrate the efficiency of SMOP.

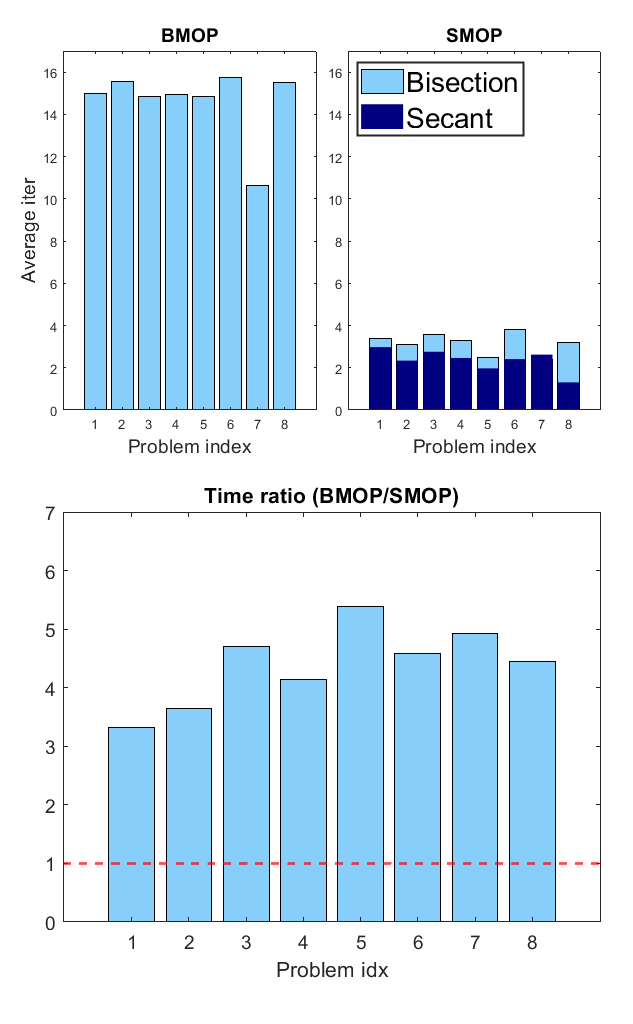

Next we perform tests on BMOP and SMOP to generate a solution path for Eq. CP() involving multiple choices of tuning parameters . In this test, we solve Eq. CP() with , where and is the same constant as in Table 4. In this test, we apply the warm-start strategy to both algorithms. The average iteration numbers of BMOP and SMOP and the ratio of the computation time of BMOP to the time of SMOP are shown in Fig. 2 with tolerances . From this figure, it is evident that utilizing the secant method for root-finding significantly reduces the number of iterations by around 4 times. The reduction in iterations results in a substantial decrease in computation time for SMOP, which is typically less than one-third of the time required by BMOP.

7.2 The sorted penalized problems with least-squares constraints

In this subsection, we will present the numerical results of SMOP in solving the sorted penalized problems with least-squares constraints Eq. CP(). For comparison purposes, we also conducted tests on Newt-ALM-LSM (similar to SSNAL-LSM, but with the sub-problems solved by Newt-ALM [19]) and ADMM for Eq. CP().

| idx | c nnz(x) | time (s) | outermost iter \bigstrut | |

| A1 A2 A4 | A1 A2 A4 | A1 A2 A4 \bigstrut | ||

| Test I \bigstrut | ||||

| 2 | 0.15 3 2.4-2 | 3.84+0 1.34+2 3.60+3 | 1.1-7 5.3-7 2.8-1 | 8 21 8637 \bigstrut[t] |

| 4 | 0.1 3 4.8-3 | 4.79+0 1.35+2 3.60+3 | 6.0-7 8.9-7 2.9-4 | 10 17 28891 |

| 5 | 0.1 113 1.9-2 | 6.291 4.98+1 4.23+2 | 1.0-7 4.5-7 1.5-7 | 7 22 17974 |

| 6 | 0.15 413 1.0-2 | 3.10+0 2.43+2 3.60+3 | 2.7-7 1.6-7 1.9-4 | 9 21 19071 |

| 7 | 0.002 22 1.9-5 | 3.561 1.67+1 2.44+1 | 3.6-9 6.0-7 9.9-7 | 14 22 1616 |

| 8 | 0.15 95 6.9-3 | 6.061 2.55+1 1.57+2 | 1.3-7 7.7-7 9.0-7 | 10 23 8329 |

| Test II \bigstrut | ||||

| 1 | 0.1 339 2.6-7 | 2.53+1 1.40+2 5.13+2 | 2.9-7 5.6-7 1.0-6 | 25 34 2490 \bigstrut[t] |

| 2 | 0.095 629 1.0-4 | 5.39+1 4.82+2 2.87+3 | 1.7-7 2.9-7 9.4-7 | 17 27 6770 |

| 3 | 0.08 246 4.2-7 | 4.98+0 6.54+1 1.60+2 | 2.0-8 7.1-7 1.0-6 | 25 36 8491 |

| 4 | 0.07 758 1.4-4 | 2.26+1 4.26+2 5.86+2 | 4.0-8 9.0-7 9.8-7 | 16 27 4550 |

| 5 | 0.02 95 5.7-4 | 2.05+0 9.87+1 3.58+2 | 3.2-8 5.6-7 7.6-7 | 11 20 15582 |

| 6 | 0.05 997 5.5-4 | 2.32+1 1.04+3 3.60+3 | 8.4-7 2.1-7 3.5-6 | 10 23 19159 |

| 7 | 0.001 107 1.1-6 | 1.02+0 2.85+1 1.30+1 | 5.9-8 6.9-9 9.5-7 | 17 22 826 |

| 8 | 0.08 206 4.3-4 | 3.38+0 1.03+2 5.58+1 | 5.7-9 7.4-7 3.8-7 | 13 25 2842 |

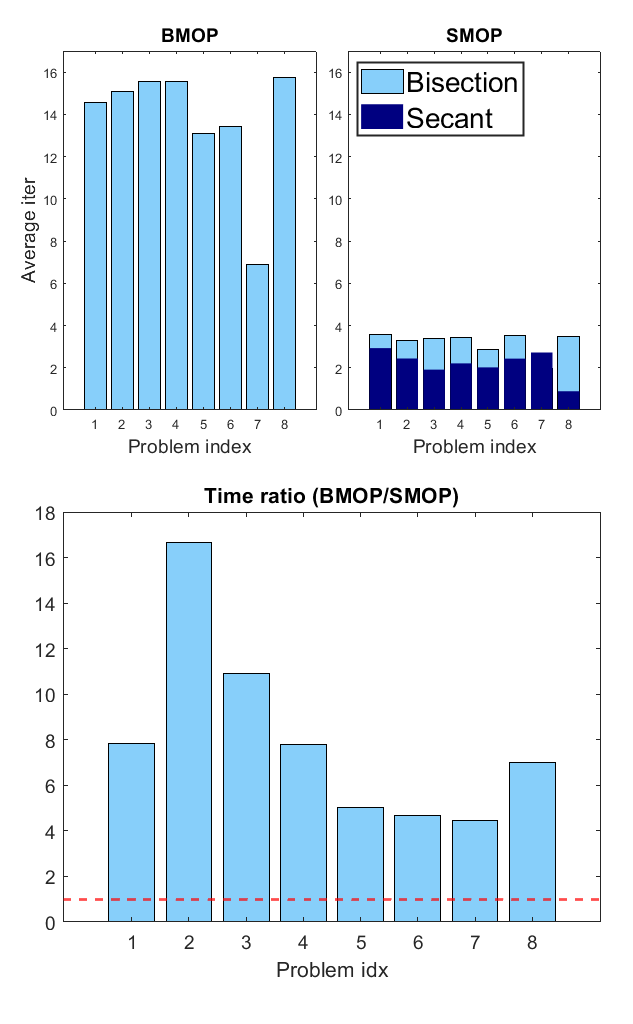

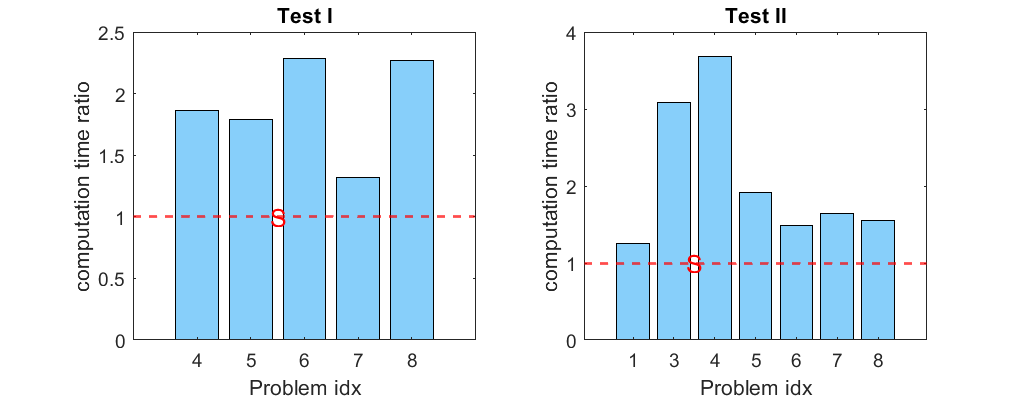

In our numerical experiments, we choose the parameters in the sorted penalty function . The maximum iteration number is set to 200 for SMOP and Newt-ALM-LSM, and 100,000 for ADMM. The sub-problems in SMOP are resolved using Newt-ALM in this test. In all experiments within this subsection, a stopping tolerance of was used. Additionally, tests were conducted with a stopping tolerance of , but the results are similar to those obtained with a tolerance of . Therefore, we will not present the results with the stopping tolerance to save space. We set , where the values of are specified in Table 6. The numerical results are presented in Table 6. From the table, it is evident that SMOP outperforms Newt-ALM-LSM and ADMM for all the cases. More specifically, SMOP can be up to around 80 times faster than Newt-ALM-LSM and up to more than 600 times faster than ADMM for the problems that can be solved by ADMM. Additionally, Figure 3 presents the computation time ratio between BMOP and SMOP for both Test I and Test II. This also demonstrates the significance of the secant method in root-finding for achieving higher efficiency.

7.3 A group lasso penalized problems with least-squares constraints

| idx | c | nnz(x) | \bigstrut | |

| Test I | 4 | 0.1 | 6 | 4.4-3 \bigstrut[t] |

| 5 | 0.1 | 50 | 2.4-2 | |

| 6 | 0.15 | 138 | 1.3-2 | |

| 7 | 0.002 | 28 | 2.4-5 | |

| 8 | 0.15 | 66 | 8.4-3 | |

| Test II | 1 | 0.105 | 95 | 7.5-7 \bigstrut[t] |

| 3 | 0.08 | 403 | 4.3-7 | |

| 4 | 0.08 | 731 | 2.2-4 | |

| 5 | 0.02 | 120 | 9.1-4 | |

| 6 | 0.05 | 372 | 6.3-4 | |

| 7 | 0.001 | 186 | 1.3-6 | |

| 8 | 0.08 | 260 | 4.9-4 |

| idx | time (s) | outermost iter \bigstrut | |

| A1 A2 A3 A4 | A1 A2 A3 A4 | A1 A2 A3 A4 \bigstrut | |

| Test I \bigstrut | |||

| 4 | 3.75+0 1.16+2 8.49+2 3.60+3 | 1.37 3.1-7 6.37-7 7.2-5 | 11 21 3024 22125 \bigstrut[t] |

| 5 | 8.141 2.74+2 2.96+1 9.16+2 | 1.49 3.5-7 6.05-7 1.0-6 | 11 21 1319 38530 |

| 6 | 5.19+0 1.46+3 1.70+2 3.02+3 | 3.2-10 4.5-7 5.98-7 9.8-7 | 10 22 1086 15768 |

| 7 | 5.981 8.80+0 3.02+1 2.59+1 | 3.78 5.0-7 2.07-7 1.0-6 | 14 19 2102 1627 |

| 8 | 6.881 1.41+2 8.30+0 1.19+2 | 1.88 2.6-7 2.46-7 9.6-7 | 9 22 334 6211 |

| Test II \bigstrut | |||

| 1 | 3.29+0 4.33+1 3.18+3 1.12+3 | 2.7-7 2.7-7 9.8-7 1.0-6 | 24 29 55596 5826 \bigstrut[t] |

| 3 | 3.83+0 3.00+1 2.06+3 2.57+2 | 1.3-7 3.4-7 3.8-6 1.0-6 | 22 36 100000 13031 |

| 4 | 2.97+1 2.42+3 1.19+3 5.86+2 | 5.2-7 9.6-9 8.6-7 7.4-7 | 13 27 4241 3401 |

| 5 | 1.70+0 1.29+2 3.30+2 9.27+1 | 8.0-7 1.7-8 8.9-7 6.5-7 | 9 20 18001 3959 |

| 6 | 2.51+1 1.39+3 3.60+3 3.60+3 | 1.3-8 1.4-7 5.8-5 2.6-7 | 11 22 20646 19075 |

| 7 | 1.22+0 1.88+1 5.99+2 2.69+1 | 5.3-8 2.1-8 6.9-7 9.9-7 | 15 23 41578 1685 |

| 8 | 5.75+0 1.47+2 1.14+2 1.94+2 | 2.5-7 3.7-7 4.4-7 9.8-7 | 15 25 4373 9974 |

In this subsection, we will present the numerical experiments conducted to solve a group lasso penalized problems with least-squares constraints. The purpose of this demonstration is to illustrate the potential and high efficiency of our proposed secant method in solving the equation for the non-polyhedral function penalized problems with least squares constraints. We will compare our algorithm, SMOP, with other state-of-the-art algorithms to demonstrate its high efficiency and robustness.

We consider the following penalty function in this subsection:

| (60) |

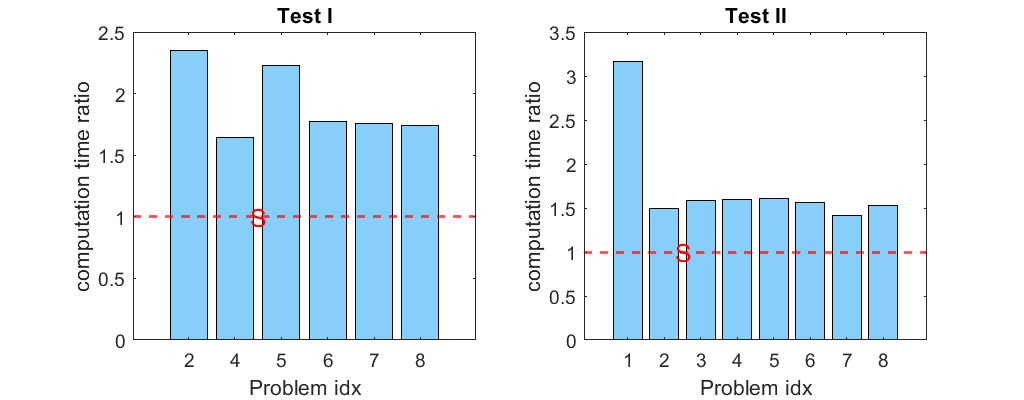

For the purpose of demonstration, we will keep using the UCI dataset that was utilized in the previous two subsections. However, it is necessary to ensure that the value of n is even. Next, we group the -th and -th elements together for all . The values of utilized to obtain are presented in Table 7. In SMOP, the sub-problems are solved using SSNAL [40]. The maximum iteration number for both SMOP and SSNAL-LSM is set to 200, while for SPGL1 and ADMM, their maximum iteration number is set to 100,000. As for the maximum running time, it remains set at 1 hour. Next, we will compare SMOP with the state-of-the-art algorithms SSNAL-LSM, SPGL1, and ADMM. The results of the tests are presented in Table 8. From the table, it is evident that SMOP outperforms SSNAL-LSM, SPGL1, and ADMM with speed-ups of up to 300, 900, and 1,100, respectively. In addition, Figure 4 illustrates the ratio of computation time between BMOP and SMOP. This figure clearly shows that using the secant method can greatly enhance overall efficiency, resulting in a speed improvement of approximately 1.5-4 times, even when dealing with the non-polyhedral penalty function Eq. 60.

8 Conclusion

In this paper, we have designed an efficient sieving based secant method for solving Eq. CP(). When is a polyhedral gauge function, we have proven that for any , all are positive. Consequently, when is a polyhedral gauge function, the secant method can solve Eq. with at least a 3-step Q-quadratic convergence rate. We have demonstrated the high efficiency of our method for solving Eq. CP() by two representative instances, specifically, the and the sorted penalized constrained problems. It is worth mentioning that calculating or is not an easy task for the sorted penalized constrained problems, to the best of our knowledge. Moreover, our numerical results on the penalized constrained problems, in which the is computable as shown in Proposition 5.10, have verified that the efficiency of SMOP is not compromised compared to the performance of the HS-Jacobian based semismooth Newton method. This motivates us to use the secant method instead of the semismooth Newton method for solving Eq. regardless of the availability of the generalized Jacobians. For future research, we will investigate the properties of for non-polyhedral functions , particularly when the nondegenerate condition does not hold.

References

- [1] A. Y. Aravkin, J. V. Burke, D. Drusvyatskiy, M. P. Friedlander, and S. Roy, Level-set methods for convex optimization, Math. Program., 174 (2019), pp. 359–390.

- [2] A. Beck and M. Teboulle, A fast iterative shrinkage-thresholding algorithm for linear inverse problems, SIAM J. Imaging Sci., 2 (2009), pp. 183–202.

- [3] J. Bolte, A. Daniilidis, and A. Lewis, Tame functions are semismooth, Math. Program., 117 (2009), pp. 5–19.

- [4] J. F. Bonnans and A. Shapiro, Perturbation analysis of optimization problems, Springer Series in Operations Research, Springer-Verlag, New York, 2000.

- [5] Z. X. Chan and D. F. Sun, Constraint nondegeneracy, strong regularity, and nonsingularity in semidefinite programming, SIAM J. Optim., 19 (2008), pp. 370–396.

- [6] X. D. Chen, D. F. Sun, and J. Sun, Complementarity functions and numerical experiments on some smoothing Newton methods for second-order-cone complementarity problems, Comput. Optim. Appl., 25 (2003), pp. 39–56.

- [7] C. Chih-Chung, LIBSVM: A library for support vector machines, ACM Trans. Intell. Syst. Technol., 2 (2011), pp. 1–27.

- [8] F. H. Clarke, Optimization and Nonsmooth Analysis, Wiley, New York, 1983.

- [9] F. Facchinei and J.-S. Pang, Finite-dimensional variational inequalities and complementarity problems, Springer Series in Operations Research, Springer-Verlag, New York, 2003.

- [10] M. P. Friedlander, I. Macedo, and T. K. Pong, Gauge optimization and duality, SIAM J. Optim., 24 (2014), pp. 1999–2022.

- [11] M. P. Friedlander and P. Tseng, Exact regularization of convex programs, SIAM J. Optim., 18 (2007), pp. 1326–1350.

- [12] D. Gabay and B. Mercier, A dual algorithm for the solution of nonlinear variational problems via finite element approximation, Comput. Math. Appl., 2 (1976), pp. 17–40.

- [13] Y. Gao and D. F. Sun, Calibrating least squares covariance matrix problems with equality and inequality constraints, SIAM J. Matrix Anal. Appl, 31 (2009), pp. 1432–1457.

- [14] R. Glowinski and A. Marroco, Sur l’approximation, par éléments finis d’ordre un, et la résolution, par pénalisation-dualité d’une classe de problèmes de dirichlet non linéaires, Revue française d’automatique, informatique, recherche opérationnelle. Analyse numérique, 9 (1975), pp. 41–76.

- [15] J. Han and D. F. Sun, Newton and quasi-Newton methods for normal maps with polyhedral sets, J. Optim. Theory Appl., 94 (1997), pp. 659–676.

- [16] Q. Li, B. Jiang, and D. F. Sun, MARS: A second-order reduction algorithm for high-dimensional sparse precision matrices estimation, J. Mach. Learn. Res., 24 (134) (2023), pp. 1–44.

- [17] X. Li, D. F. Sun, and K.-C. Toh, A highly efficient semismooth Newton augmented Lagrangian method for solving Lasso problems, SIAM J. Optim., 28 (2018), pp. 433–458.

- [18] X. Li, D. F. Sun, and K.-C. Toh, On efficiently solving the subproblems of a level-set method for fused lasso problems, SIAM J. Optim., 28 (2018), pp. 1842–1866.

- [19] Z. Luo, D. F. Sun, K.-C. Toh, and N. Xiu, Solving the OSCAR and SLOPE models using a semismooth Newton-based augmented Lagrangian method, J. Mach. Learn. Res., 20 (106) (2019), pp. 1–25.

- [20] F. Meng, D. F. Sun, and G. Zhao, Semismoothness of solutions to generalized equations and the Moreau-Yosida regularization, Math. Program., 104 (2005), pp. 561–581.

- [21] J. M. Ortega and W. C. Rheinboldt, Iterative solution of nonlinear equations in several variables, Academic Press, New York-London, 1970.

- [22] F. A. Potra, On -order and -order of convergence, J. Optim. Theory Appl., 63 (1989), pp. 415–431.

- [23] F. A. Potra, L. Qi, and D. F. Sun, Secant methods for semismooth equations, Numer. Math., 80 (1998), pp. 305–324.

- [24] L. Qi, D. F. Sun, and G. Zhou, A new look at smoothing Newton methods for nonlinear complementarity problems and box constrained variational inequalities, Math. Program., 87 (2000), pp. 1–35.

- [25] L. Qi and P. Tseng, On almost smooth functions and piecewise smooth functions, Nonlinear Analysis: Theory, Methods & Applications, 67 (2007), pp. 773–794.

- [26] B. Recht, M. Fazel, and P. A. Parrilo, Guaranteed minimum-rank solutions of linear matrix equations via nuclear norm minimization, SIAM Rev., 52 (2010), pp. 471–501.

- [27] H. E. Richard and C. M. George, Computer Algebra Recipes: A Gourmet’s Guide to the Mathematical Models of Science, Springer, Berlin, 2001.

- [28] R. T. Rockafellar, Convex Analysis, Princeton University Press, 1970.

- [29] D. F. Sun, A further result on an implicit function theorem for locally Lipschitz functions, Oper. Res. Lett., 28 (2001), pp. 193–198.

- [30] D. F. Sun, The strong second-order sufficient condition and constraint nondegeneracy in nonlinear semidefinite programming and their implications, Math. Oper. Res., 31 (2006), pp. 761–776.

- [31] D. F. Sun and J. Sun, Semismooth matrix-valued functions, Math. Oper. Res., 27 (2002), pp. 150–169.

- [32] R. Tibshirani, M. Saunders, S. Rosset, J. Zhu, and K. Knight, Sparsity and smoothness via the fused lasso, J. R. Stat. Soc. Ser. B Stat. Methodol., 67 (2005), pp. 91–108.

- [33] J. F. Traub, Iterative methods for the solution of equations, Prentice-Hall, Inc., Englewood Cliffs, N.J., 1964.

- [34] E. van den Berg and M. P. Friedlander, Probing the Pareto frontier for basis pursuit solutions, SIAM J. Sci. Comput., 31 (2008), pp. 890–912.

- [35] E. van den Berg and M. P. Friedlander, Sparse optimization with least-squares constraints, SIAM J. Optim., 21 (2011), pp. 1201–1229.

- [36] E. van den Berg and M. P. Friedlander, SPGL1: A solver for large-scale sparse reconstruction, December 2019. https://friedlander.io/spgl1.

- [37] C. Wu, Y. Cui, D. Li, and D. F. Sun, Convex and nonconvex risk based statistical learning at scale, INFORMS J. Comput., (2023).

- [38] Y. Yuan, T.-H. Chang, D. F. Sun, and K.-C. Toh, A dimension reduction technique for large-scale structured sparse optimization problems with application to convex clustering, SIAM J. Optim., 32 (2022), pp. 2294–2318.

- [39] Y. Yuan, M. Lin, D. F. Sun, and K.-C. Toh, Adaptive sieving: A dimension reduction technique for sparse optimization problems, arXiv: 2306.17369, (2023).

- [40] Y. Zhang, N. Zhang, D. Sun, and K.-C. Toh, An efficient hessian based algorithm for solving large-scale sparse group lasso problems, Math. Program., 179 (2020), pp. 223–263.

- [41] Y. Zhang, N. Zhang, D. F. Sun, and K.-C. Toh, An efficient Hessian based algorithm for solving large-scale sparse group Lasso problems, Math. Program., 179 (2020), pp. 223–263.