Brief Paper

Stochastic Optimal Investment Strategy for Net-Zero Energy Houses

Abstract

In this research, we investigate Net-Zero Energy Houses (ZEH), which harness regionally produced electricity from photovoltaic (PV) panels and fuel cells, integrating them into a local power system in pursuit of achieving carbon neutrality. This paper examines the impact of electricity sharing among users who are working towards attaining ZEH status through the integration of PV panels and battery storage devices. We propose two potential scenarios: the first assumes that all users individually invest in storage devices, hence minimizing their costs on a local level without energy sharing; the second envisions cost minimization through the collective use of a shared storage device, managed by a central manager. These two scenarios are formulated as a stochastic convex optimization and a cooperative game, respectively. To tackle the stochastic challenges posed by multiple random variables, we apply the Monte Carlo sample average approximation (SAA) to the problems. To demonstrate the practical applicability of these models, we implement the proposed scenarios in the Jono neighborhood in Kitakyushu, Japan.

1 Introduction

Addressing the urgent and formidable challenge of global warming by reducing emissions has become a paramount concern, largely due to the detrimental effects of climate change on both the environment and human society. In 2019, one-third of Japan’s electricity was generated from coal, and fossil fuels accounted for of Japan’s power supply Country2020 ; Japan2021 . As the Japanese government aims for carbon neutrality by 2050 CarbonNeu , renewable energy sources like solar and wind power are gaining importance as alternative fuel sources. Although renewable energy constituted less than of Japan’s total energy consumption in 2019, the decreasing costs of solar and wind power, along with the ongoing economic recovery from COVID-19, are expected to increase the share of renewable energy in Japan’s energy mix in the coming years Country2020 .

As the world strives for carbon neutrality and the integration of renewable energy sources, the concept of Net-Zero Energy Houses (ZEH) is getting increasing attention as a technology to reduce emissions at home. A ZEH is a house that has an annual net energy consumption of around zero by maximizing energy savings while maintaining a comfortable living environment. Achieving an annual net energy consumption of around zero is made possible through improved heat insulation, high-efficiency equipment, and photovoltaic (PV) power generation efficiency2015definition . To attain ZEH status, devices such as PV panels, fuel cells, and battery storage devices must be integrated into a regional power system wu2021residential . However, it is vital to quantitatively assess the effects of introducing these devices to ensure the safe penetration of ZEH into the power grid.

In general, PV panels do not generate stable power output. The incorporation of battery storage can help mitigate these power fluctuations by effectively charging and discharging as needed. The integration of PV systems and battery storage into power grids has been a research focus for many years, and numerous studies have been conducted, including notable reviews such as hoppmann2014economic ; azuatalam2019energy ; khezri2022optimal . In hoppmann2014economic , the economic aspect of battery storage is reviewed and a techno-economic model for calculating the profitability of investing in battery storage is proposed for residential PV systems in Germany. In azuatalam2019energy , a systematic review of energy management strategies for PV-battery systems under various scenarios is conducted. In khezri2022optimal , a comprehensive review of key parameters to be considered for optimal planning of PV panels and battery storage systems is provided. In particular, various optimization-based analyses have been conducted on the design and management of PV panels and battery storage systems under different scenarios, including those by pham2009optimal ; zhu2014optimal ; ratnam2015optimization ; khalilpour2016planning ; bordin2017linear ; yan2018optimized . Ref. pham2009optimal considers the optimal operation of a PV-battery energy system using anticipation and reactive management. Ref. zhu2014optimal proposes an optimal design and management strategy for an energy system with PV and battery storage to reduce energy costs. Ref. khalilpour2016planning introduced a multi-period mixed-integer linear program to solve the investment problem of PV-battery systems. Ref. bordin2017linear considers battery degradation costs in the energy management of off-grid systems. Ref. yan2018optimized focused on the energy management of a commercial EV charging station with integrated PV generation and battery storage.

In recent years, sharing economy models via battery storage have become crucial for managing energy and reducing electricity costs in regional power systems wang2013active ; kalathil2017sharing ; parra2017interdisciplinary ; chakraborty2018sharing ; wang2019incentive ; henni2021sharing . An energy management strategy for demand response using shared battery storage is proposed in wang2013active . Ref. kalathil2017sharing formulates a cooperative game for the optimal battery storage investment of a group of users sharing their electricity storage, considering fluctuations in power prices, while chakraborty2018sharing uses cooperative game theory to evaluate scenarios where users invest in battery storage individually or jointly. Ref. wang2019incentive presents an incentive design to encourage users to share power obtained from PV generation in local power systems. In henni2021sharing , a sharing economy model allowing residential communities to share excess PV generation, stored electricity, and storage capacity is proposed. However, these studies do not specifically address the optimal investment strategy to attain ZEH status. Numerous critical studies on Net-Zero Energy Buildings (ZEB) have been presented in vieira2017energy ; harkouss2019optimal ; ahmed2022assessment and references therein. While these studies provide invaluable insights, they do not consider the optimal strategies for investment in energy sharing among users, which requires further investigation.

1.1 A motivating case study

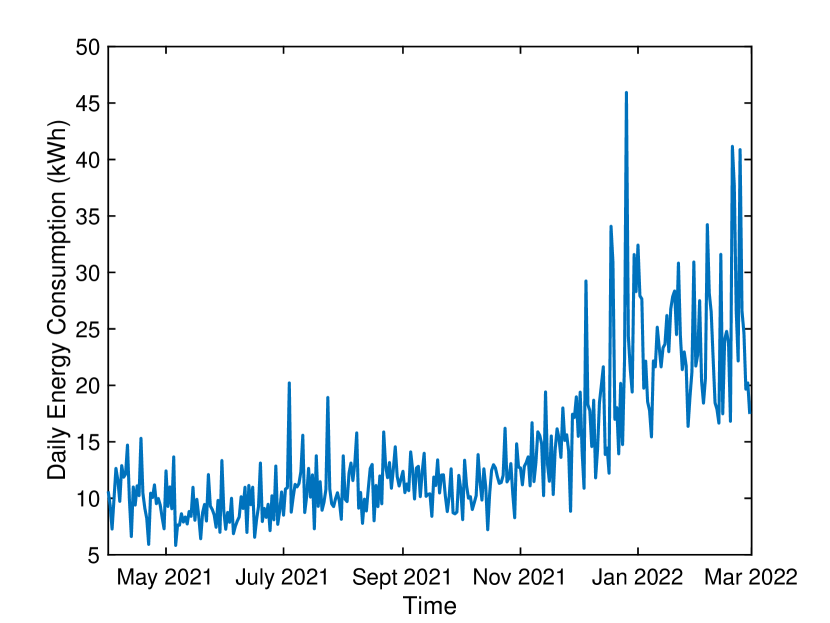

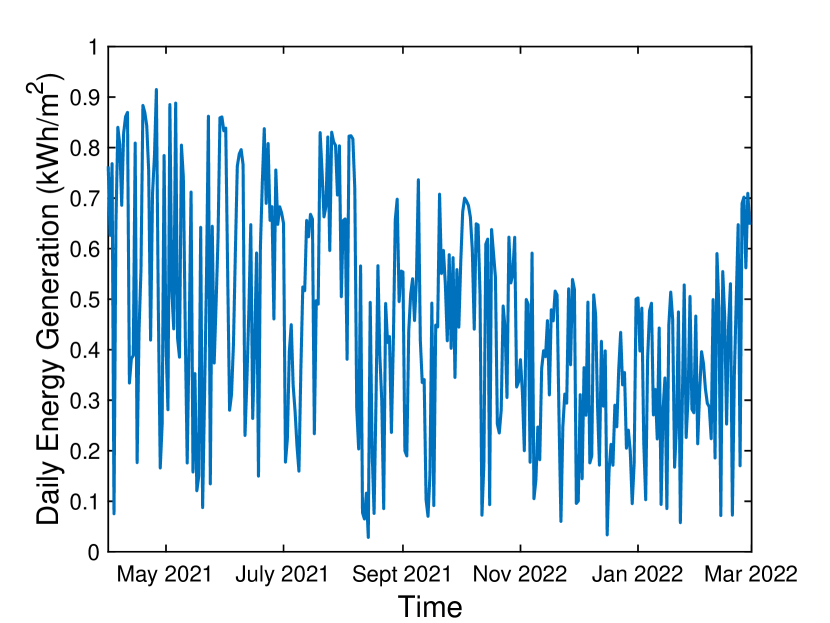

Jono, a neighborhood in Kitakyushu, Japan, serves as an ideal case study for our research. This community consists of households, which together form a distinct regional power system connected to the main power grid. These households have installed rooftop PV panels. Fig. 1(a) and 1(b), display the daily power consumption and generation for one specific household. The figures highlight the time-varying nature of power generation from PV panels, making it challenging to maintain a power balance within the system. However, using batteries to store excess energy during peak solar generation times and drawing upon this stored energy when solar panels produce less can potentially mitigate this power imbalance and attain ZEH status within the regional power system.

This example also suggests that power generation from photovoltaic systems can be modeled using random variables based on existing data. We will investigate the optimal investment problem of PV panels and battery storage devices from an economic standpoint.

1.2 Contributions

In this paper, we propose an optimal investment strategy for PV panels and battery storage devices within a regional power system aiming to attain ZEH status for users, with a focus on electricity sharing. We consider two scenarios involving users and a manager in the regional power system. We examine two scenarios within the regional power system, involving users and a manager. The first scenario focuses on individual investment in battery storage, while the second scenario revolves around joint investment in a shared storage solution. These scenarios are formulated as stochastic convex optimization and cooperative game problems respectively, with cost functions demonstrated to be convex. As the proposed investment problems are of stochastic nature and thus many random variables are present (PV power generation, daily consumption, etc.), we employ the Monte Carlo sample average approximation approach, which allows us to generate solvable deterministic convex problems. It is important to note that in the application to the Jono neighborhood, the sampling data generated is derived from real historical data on PV generation and power consumption.

Compared to the aforementioned literature on PV-battery power systems, our research specifically centers around the optimization-based investment of PV and battery storage, coupled with power sharing for attaining Net-Zero Energy Houses. Notably, our approach is distinct as it utilizes real data collected from an entire neighborhood, comprising multiple users. In contrast to the formulations of power sharing presented in kalathil2017sharing and chakraborty2018sharing , our approach incorporates the investment considerations for PV panels. Moreover, by introducing a manager into the framework, we formulate a game with convex functions that are globally solvable, preferable to nonconvex functions employed in kalathil2017sharing .

The remainder of the paper is organized as follows. In Section 2, we formulate the two scenarios for optimal investment in PV panels and battery storage. In Section 3, we apply the Monte Carlo sample average approximation (SAA) approach to solve the stochastic problems. In Section 4, we discuss a case study in Jono using the two scenarios. Finally, we conclude the paper in Section 5.

2 Optimal Investment Problems

Notation: and represent the expected value and variance of random variables. denotes the max-norm of a vector, i.e., , where .

Let us consider a regional power grid consisting of households and one manager. We assume that users in this regional power system generate electricity using rooftop PV panels and fuel cells, and may also exchange electricity with the manager. The manager is connected to the main power grid, and exchanges power with both individual users and the power grid. The goal of ZEH is to balance each user’s energy consumption with the energy generated by PV power generation, fuel cells, and other sources, ultimately reducing the net energy consumption to zero. Assuming that reducing the net energy consumption of the entire region to zero is practically achievable using ZEH, we propose the following two formulations regarding investment plans for PV panels and battery storage devices:

-

1.

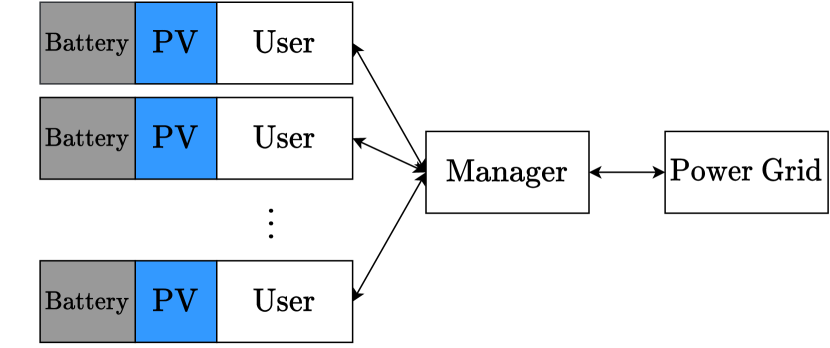

In the first scenario, we assume that all users invest in individual storage devices and minimize their costs locally without sharing energy.

-

2.

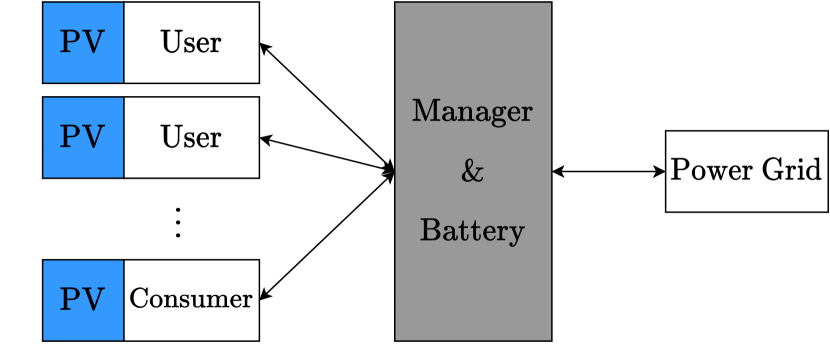

In the second scenario, all users aim to minimize their own costs while sharing a common joint storage device, the capacity of which is distributed to users by the manager.

The relationships among users, the manager, and the main power grid for the two scenarios are illustrated in Figures 2(a) and 2(b), respectively.

2.1 Individual storage investment

In this subsection, we examine the scenario in which individual users independently achieve a balance between electricity supply and demand. We propose a stochastic optimization problem for the investment strategy of PV panels and battery storage devices.

In this scenario, we assume that user will invest in PV panels, battery storage, and a household fuel cell to determine an optimal energy management strategy for days into the future. Let be the power consumption of user on the -th day, and be the power generation per unit area of the PV panels. Both and are random variables with known distribution functions. Then, user decides to invest a total area of for the photovoltaic panels and a total of for battery storage.

First, let us consider the case where the power consumption cannot be compensated by the power generation from the PV power generation. In this situation, the user will compensate for the shortage using the remaining capacity of the battery storage, and if the remaining storage is insufficient, they will resort to a household fuel cell. In this case, the purchase cost of gas used for power generation becomes a penalty for not being able to supplement power. Therefore, the cost of power generation by household fuel cells when PV power generation is insufficient is given by

| (1) |

where represents the power generation cost per unit of electricity from household fuel cells with ¥ representing JPY, and the power in the battery storage at the beginning of day is given by , with .

Next, let us consider the case where the power from the PV power generation exceeds the power consumption . At this time, if the residual power exceeds the allowable amount of charge of the battery storage, the surplus power must flow to the main power grid. However, reverse power flow is an action that puts a burden on the power grid. Therefore, we try to suppress it by imposing a penalty according to the reverse flow rate. The cost for the excess of PV power generation is given by

| (2) |

where represents the price for reverse power flow per unit power.

Lastly, the cost of investing PV panels and battery storage should be considered. Let denote the capital cost per unit area of the PV panels amortized over its lifespan, and the capital cost per unit capacity of the battery storage, amortized over its lifespan. Then, the cost for the one-time capital investment is given by

| (3) |

Summing up the above terms (1)–(3), we obtain the cost function for user to achieve the power balance between demand and supply. The investment strategy is formulated as an optimization problem,

| (4) |

where the arguments of , on the right-hand side are omitted for ease of notation.

2.2 Joint storage investment with storage distribution

The investment strategy in the last subsection can be readily extended to the global investment in PV panels and battery storage devices following similar arguments. Specifically, the optimization problem for global investment is given by

| (5) |

where

| (6) |

| (7) |

| (8) |

, and denotes the joint storage to invest. However, the storage distribution for users is unclear from the solution to the above optimization. Therefore, a scheme containing the dispatch of the storage devices should be introduced.

In this subsection, we explore another scenario where all users in the region share joint battery storage through a manager and achieve a power balance between demand and supply. In this scenario, user invests in PV panels and a household fuel cell, while the manager invests in joint battery storage and trades power with the user. The definitions of , , and remain the same as in the previous subsection. User decides on the area of PV panels to invest while the manager determines the capacity for the battery storage investment. Furthermore, the manager is responsible for making adjustments to achieve the power balance. The overall cost consists of two parts: one from the users and the other from the manager.

First, let us consider the cost borne by the users. The users aim to minimize their cost by designing the area of PV panels based on the capacity provided by the manager. In this scenario, when the power generated by user ’s PV panels exceeds their power consumption , user can earn a profit by selling surplus power to the manager. This profit is considered a negative cost, given by

| (9) |

where represents the selling price of electricity to the manager. Note that can also be a negative value, analogous to the penalty imposed for reverse power flow into the main power grid in the individual scenario.

When the power consumption exceeds the power generation from PV power generation, users can either purchase power from the manager or supplement it with power generated by household fuel cells. Here, the following assumptions are made for their selection of power source.

-

1.

The maximum amount of daily purchasable power from the manager for user is set as , where .

-

2.

When compensating for power shortages, users will buy electricity from the manager first, and then use household fuel cells if it is still insufficient.

Therefore, for user , the costs of purchasing power from the manager is given by

| (10) |

and the cost of getting power from the household fuel cell is given by

| (11) |

respectively, where represents the selling price per unit of electricity by the manager, and represents the power generation cost per unit of electricity from the household fuel cells.

Furthermore, the cost of PV panels for user is expressed by the following,

| (12) |

where represents the price per unit area of PV panels.

Summarizing, the investment strategy for user is formulated as an optimization problem

| (13) |

where the arguments of , on the right-hand side are omitted for ease of notation. Next, let us consider the cost borne by the manager. As the manager is responsible for power exchange with all users, the total amount of power bought from users is given by

| (14) |

and power sold to users is given by

| (15) |

respectively. Thus, the cost of exchanging power with users is given by

| (16) |

When the total amount of power sold to users is greater than the total amount of power purchased from users, the manager will extract power from the joint battery storage from the beginning of day to compensate for the shortage. If the shortage is still not filled, the manager will purchase power from the main power grid with the price per unit of electricity. Then, the cost in this case is given by

| (17) |

where denotes the power at the beginning of day , with .

On the other hand, when is less or equal to , the manager will charge the surplus power to the battery storage. However, if the surplus power exceeds the charging capacity, the residual power will flow to the main power grid. Then, a penalty for reverse power flow is imposed as in (2.1),

| (18) |

Moreover, the investment cost for the battery storage bought by the manager is

| (19) |

To sum up, the investment strategy for the manager is formulated into an optimization problem

| (20) |

where the arguments of , are omitted here for ease of notation. The manager will determine the capacity to invest for given , .

The investment strategy is a cooperative game between users and the manager with cost functions defined in (13) and (20), respectively. The game is called cooperative in the sense that all users will agree to share joint battery storage chakraborty2018sharing . It will be shown in the next section that the aforementioned cost functions are convex, and Monte Carlo sample average approximation can be applied to solve these problems.

3 Stochastic optimal investment strategy

The two scenarios introduced in the previous section are formulated into stochastic problems in the following form,

| (21) |

where is a nonempty closed subset of , is a random variable whose probability distribution is supported on a set , and is a function of the two vector variables. We assume that the expectation function is well-defined and finite-valued for all . The formulated problems involve evaluating the expected value of functions of multiple random variables. Thus, it is difficult to solve the stochastic problem analytically. In this section, we apply the Monte Carlo sample average approximation (SAA) approach to obtain an approximated solution to problems (2.1) and (13), (20).

3.1 Monte Carlo sample average approximation

Let us consider a sample of realization of the random vector , which can be viewed as data generated by Monte Carlo sampling techniques. For any we can estimate the expected value by SAA:

| (22) |

Assume problem (21) is feasible and is the optimal solution to problem (21). For , We say that is a -optimal solution of the problem of minimization of over if

Denote , as the sets of optimal solutions to problem (21) and (22), respectively. Then, , are defined as the sets of -optimal solutions, -optimal solutions to (21) and (22), respectively.

Denote as the diameter of and assume it is finite, where denotes the max-norm of . Assume further that the expectation function is -Lipschitz continuous on , that is, for all . Given a significance level for the null hypothesis, the relation between the sample size and the probability of the solutions to problem (22) being close enough to those of problem (21) is given by the following theorem.

Theorem 1 (ruszczynski2003stochastic ).

For all small enough, , and , and for the sampling size satisfying

| (23) |

where is the dimension of ,

| (24) |

where is the domain excluding the -optimal solution to problem (21). Then, it follows that

| (25) |

3.2 Convexity of cost functions

We show that cost functions in (2.1) and (13), (20) are all convex with respect to their decision variables, under reasonable conditions.

Lemma 1.

The cost function in (2.1) is convex with respect to , .

Proof.

The pointwise maximum and the nonnegative weight sum (as well as the expectation) of functions preserves convexity [boyd2004convex, , p. 79]. Thus, the in (2.1) is convex with respect to both and . ∎

Lemma 2.

The cost function in (13) is convex with respect to , if .

Proof.

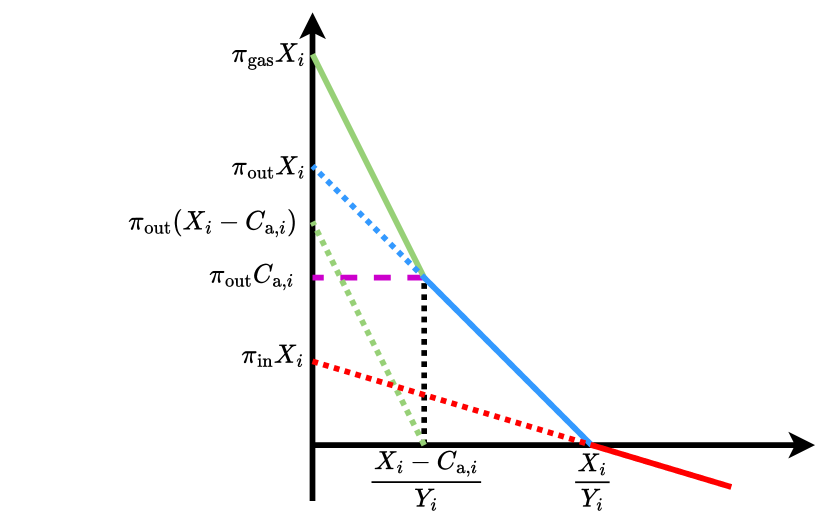

Since is linear, we only need to consider the second term on the right-hand side of (13). Define as

Then, . We can observe that is a piecewise linear function which can be rewritten as

which is shown in Fig. 3.

We can observe from Fig. 3 that when holds, the epigraph of is convex and thus is convex with respect to . Next, since the non-negative weight sum of functions preserves convexity [boyd2004convex, , p. 79], we have that the expectation is convex and the sum of it over days is also convex with respect to . ∎

Lemma 3.

The cost function in (20) is convex with respect to if .

Proof.

Let us focus on the term in (20), since is linear with respect to . is convex with respect to , as the pointwise maximum and expectation preserve convexity. Meanwhile, if , we can obtain that is a monotonically non-decreasing function in each argument, i.e., , and , respectively. Meanwhile, , are convex with respect to . Following from the composition rule [boyd2004convex, , p. 86], is convex with respect to . Therefore, we have that in (20) is convex. ∎

Remark 1.

The condition is a reasonable constraint to impose. The first inequality ensures that the user will first purchase electricity from the manager at the price , and only turn to the fuel cell for power if there is still a shortage, at a higher price . The second inequality prevents users from making a profit by engaging in electricity trading, where they buy electricity from the manager at a lower price and sell it back at a higher price. Overall, these constraints promote efficient electricity consumption and discourage wasteful behavior. The condition is also reasonable for the manager as it will not lose money during the process of transmitting power from the grid to users.

Remark 2.

Since the cost functions in (13) and (20) are convex, there exists a Nash equilibrium for the non-cooperative game facchinei2010generalized , that is, at the equilibrium, the users and the manager cannot decrease their cost function any further by changing their investments unilaterally.

3.3 Application of the SAA approach

In this subsection, we discuss the application of the Monte Carlo SAA approach on the formulated stochastic optimization problems to obtain approximated deterministic optimization problems. To evaluate sample sizes from Theorem 1, we need to compute the diameters , Lipschitz constants , and variances of the corresponding cost functions. The following lemmas provide an estimation of the sample sizes for (2.1), (13) and (20), respectively.

Lemma 4.

Proof.

Since , , we have that the diameter of the domain is . Denote as any point in the domain. Recall that is a piecewise linear function, and the Lipschitz constant of a piecewise linear function is bounded by the largest Lipschitz constant among all pieces. Therefore, we have

where

Next, recall the property of variance that for any constant , and . We can obtain from (24) that

This completes the proof. ∎

Lemma 5.

Proof.

Lemma 6.

The proof is analogous to the above lemmas and is thus omitted here.

4 A case study

We implement the optimal investment strategy for PV and battery storage in the Jono neighborhood mentioned in Section 1.1. In this neighborhood, there are households and an operation period of days is considered. The daily power generation and power consumption for the users are represented as random variables, generated based on their historical data (see, e.g., Figure 1). The price for PV is set to and the price for battery storage is set to . These prices are amortized over a ten-year lifespan. We set the electricity price at , and the penalty for reverse power flow at . The monetary unit ¥ indicates JPY. The charge rate of the battery is set to , ensuring it has the capacity to charge or discharge every day.

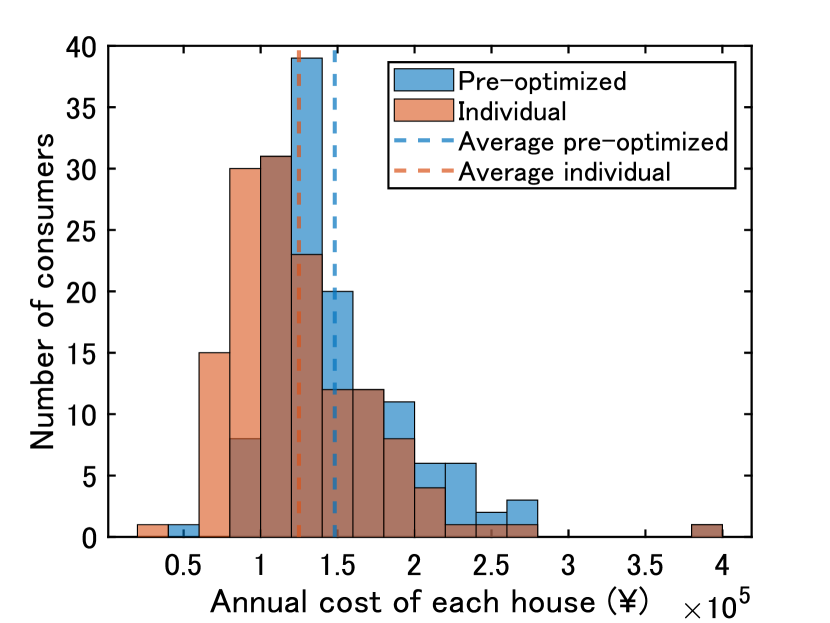

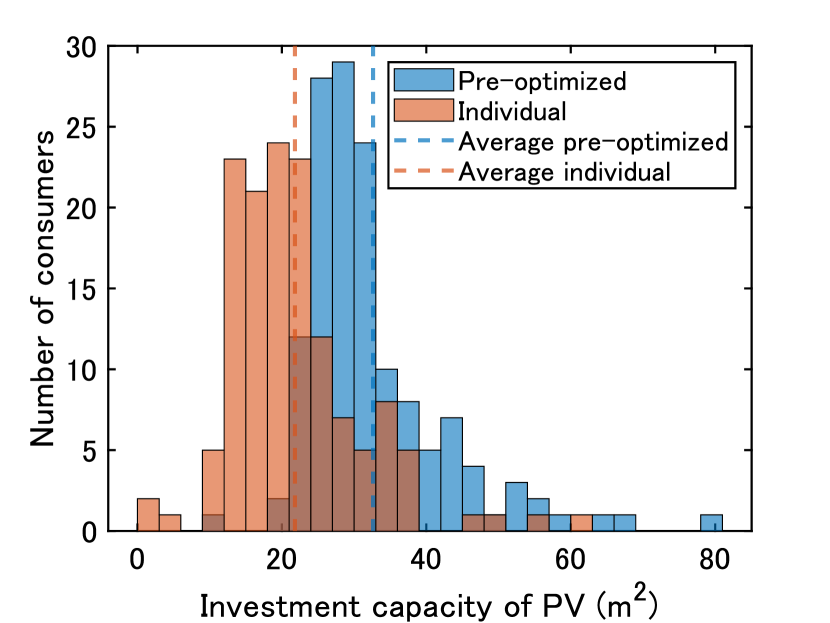

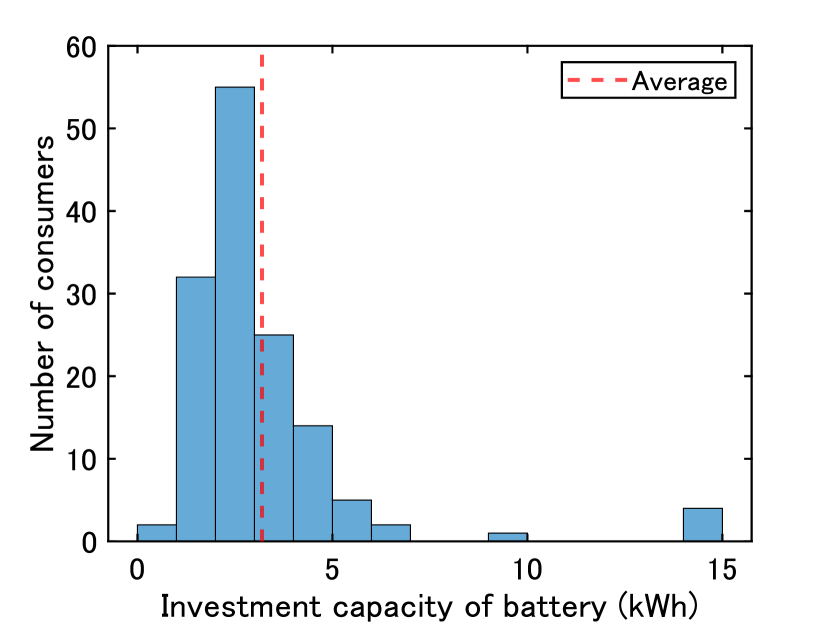

In the first scenario, users invest in PV panels and battery storage individually and we consider the problem represented by (2.1). The stochastic problem is solved by applying the Monte Carlo approach introduced in Section 3.1. Figure 4 depicts a comparison before and after the optimal planning and the optimal individual investment plans. It should be noted that no battery storage was utilized in the area before the implementation of the optimal planning. The results show that introducing battery storage allows users in the Jono neighborhood to invest less in PV panels while significantly reducing the annual cost.

Next, we consider the joint investment strategy in storage. First, let us examine the global optimization (5)–(2.2), assuming the same household data and equipment/electricity prices as in the individual case. It is important to note that this global optimization does not specify how the joint battery storage is distributed among individuals. Therefore, in the second scenario, we adopt a game setting. The manager determines the allocation of battery capacity, calculated through the manager’s optimization problem (20), for all users. Each user then utilizes their respective allocation to decide on the invested area of PV panels. We set the electricity price at , and the penalty for reverse power flow at . The selling price by the manager is , and the gas price is . We consider two cases in this game model, namely , representing the buy-in price from users, and indicating a penalty to users for excessive power generation. The investment strategy is the Nash equilibrium, which can be obtained by iteratively solving the optimization on the user’s side (13) and the manager’s side (20).

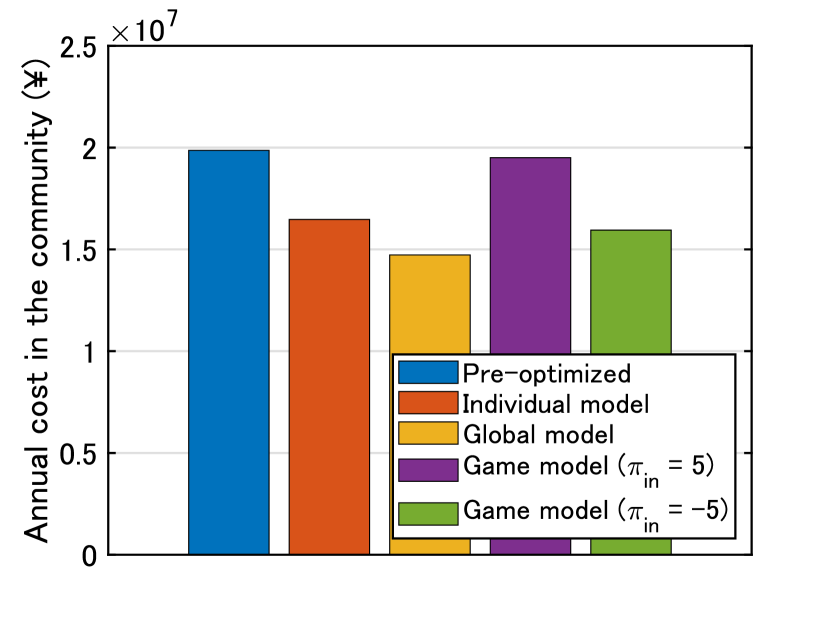

The comparison of simulation results among different models in the community is shown in Figure 5. The individual model corresponds to the first scenario (2.1), while the game models correspond to the second scenario (13), (20). On the other hand, the global model represents the ideal case (5), where the entire neighborhood is treated as a single user. Figure 5(a) shows the comparison of the total annual costs in the community with the past data. Both the individual and joint scenarios result in lower total costs compared to the non-optimized scenario. It is expected that the total costs in both scenarios are higher than the lower bound obtained from the global model. This gap arises due to the lack of sharing for the first scenario and the conflicting interests among individual users for the second scenario.

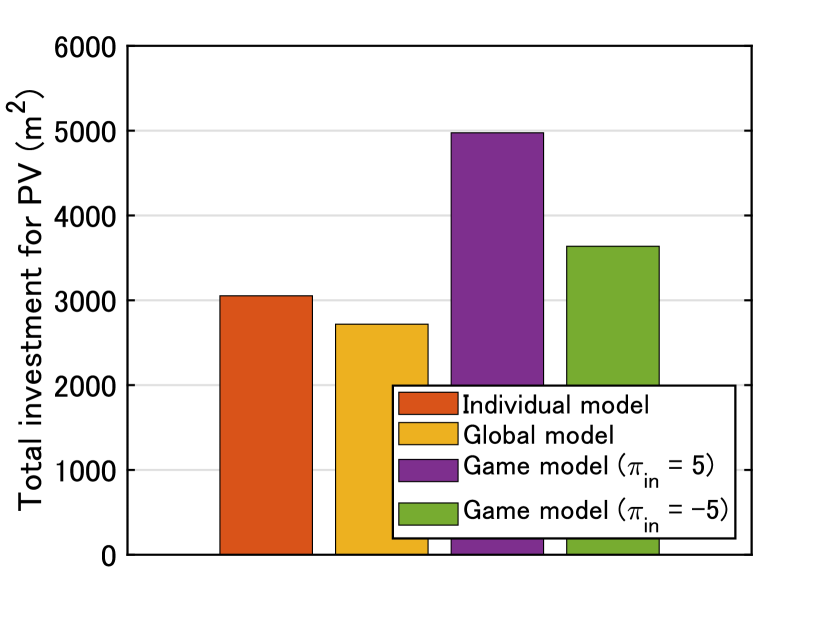

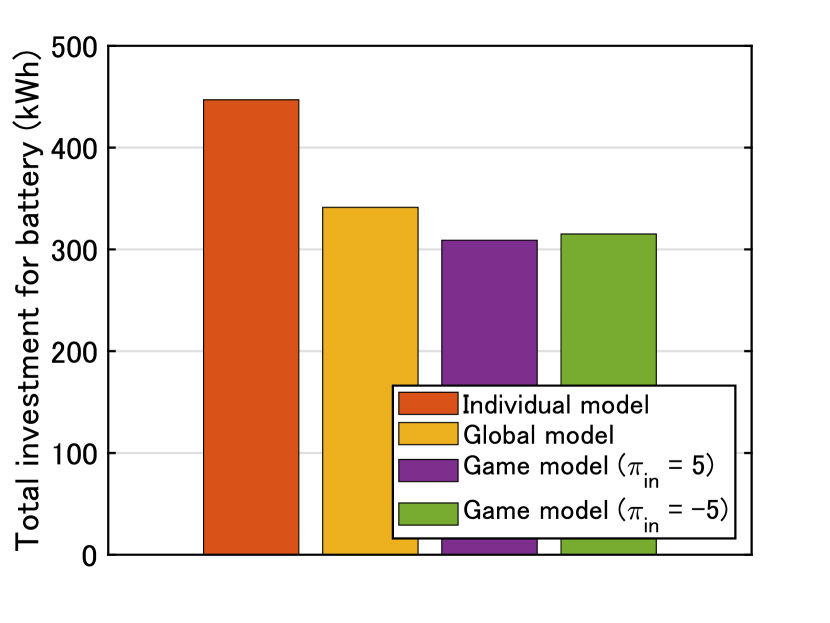

It is worth noting that the total cost from the individual model is lower than that of the joint investment game model when . This situation arises as users can profit by selling their excess electricity to the manager, thereby leading to an amplified investment in PV panels to maximize this financial advantage. However, this over-investment ultimately escalates the manager’s expenses, resulting in elevated overall costs. To solve the above issue, let the excessive power generation be penalized similarly to the individual model. Note that the penalty is less than , which still provides users an incentive to participate in the joint investment. The simulation result in Figure 5(a) shows a decrease in total cost. Intriguingly, this discovery compels us to reassess the intuitive understanding of the sharing economy. It underscores the necessity for an appropriate sharing strategy to prevent users from over-exploiting communal resources, which, without careful management, could lead to inflated overall costs in the long run. It thus highlights the challenges of implementing the joint model, as it requires a significant effort to reconcile the competing interests of users. Furthermore, Figure 5(b) illustrates the total investment amount for PV panels in the community, indicating a clear incentive to invest in PV panels when energy recycling from users is taken into account. Figure 5(c) depicts the total investment amount for battery storage in the community, which suggests that sharing energy can help restrain redundant battery investments.

All the stochastic problems are approximated as deterministic problems through the Monte Carlo approach. Let and the significance level . The estimation of the sample sizes yields for Lemma 4, for Lemma 5 and for Lemma 6, respectively. We remark that conservative estimations of the variances are carried out in Lemma 4–6 and thus only conservative estimates of the required sample sizes are provided. In practice, much smaller sample sizes are sufficient to guarantee accurate results. However, finding a tight sample size is not our goal in this paper.

5 Conclusion

In this paper, we have explored the investment strategy for PV panels and battery storage to attain the Net-Zero Energy House status within a regional power system comprising a manager and multiple users.

We have demonstrated through a case study in Kitakyushu that incorporating battery storage into the power system effectively reduces power imbalances and enhances energy utilization efficiency, which is crucial for attaining ZEH objectives. Furthermore, our analysis of the two proposed scenarios has revealed their potential to significantly decrease annual electricity costs.

Additionally, we have highlighted the importance of implementing a proper sharing policy to incentivize individual users to share electricity while preventing the excessive exploitation of communal resources. Our future work will concentrate on formulating games that meet these requirements and foster the desired outcomes.

Acknowledgment

This work is supported by the Ministry of the Environment, Government of Japan.

References

- [1] ‘Country analysis executive summary: Japan’. (U.S. Energy Information Administration, 2020.

- [2] ‘Japan 2021 energy policy review’. (IEA, Paris, 2021.

- [3] JapanGov. ‘Carbon neutrality’. (, 2022. https://www.japan.go.jp/global_issues/carbon_neutrality/index.html

- [4] ‘Definition of ZEH and future measures proposed by the ZEH roadmap examination committee’. (Energy Efficiency and Conservation Division Agency for Natural Resources and Energy Ministry of Economy, Trade and Industry, 2015.

- [5] Wu, W., Skye, H.M.: ‘Residential net-zero energy buildings: Review and perspective’, Renewable and Sustainable Energy Reviews, 2021, 142, pp. 110859

- [6] Hoppmann, J., Volland, J., Schmidt, T.S., Hoffmann, V.H.: ‘The economic viability of battery storage for residential solar photovoltaic systems–a review and a simulation model’, Renewable and Sustainable Energy Reviews, 2014, 39, pp. 1101–1118

- [7] Azuatalam, D., Paridari, K., Ma, Y., Förstl, M., Chapman, A.C., Verbič, G.: ‘Energy management of small-scale PV-battery systems: A systematic review considering practical implementation, computational requirements, quality of input data and battery degradation’, Renewable and Sustainable Energy Reviews, 2019, 112, pp. 555–570

- [8] Khezri, R., Mahmoudi, A., Aki, H.: ‘Optimal planning of solar photovoltaic and battery storage systems for grid-connected residential sector: Review, challenges and new perspectives’, Renewable and Sustainable Energy Reviews, 2022, 153, pp. 111763

- [9] Pham, T.H., Wurtz, F., Bacha, S. ‘Optimal operation of a PV based multi-source system and energy management for household application’. In: 2009 IEEE International Conference on Industrial Technology. (IEEE, 2009. pp. 1–5

- [10] Zhu, D., Wang, Y., Chang, N., Pedram, M. ‘Optimal design and management of a smart residential PV and energy storage system’. In: 2014 Design, Automation & Test in Europe Conference & Exhibition (DATE). (IEEE, 2014. pp. 1–6

- [11] Ratnam, E.L., Weller, S.R., Kellett, C.M.: ‘An optimization-based approach to scheduling residential battery storage with solar PV: Assessing customer benefit’, Renewable Energy, 2015, 75, pp. 123–134

- [12] Khalilpour, R., Vassallo, A.: ‘Planning and operation scheduling of PV-battery systems: A novel methodology’, Renewable and Sustainable Energy Reviews, 2016, 53, pp. 194–208

- [13] Bordin, C., Anuta, H.O., Crossland, A., Gutierrez, I.L., Dent, C.J., Vigo, D.: ‘A linear programming approach for battery degradation analysis and optimization in offgrid power systems with solar energy integration’, Renewable Energy, 2017, 101, pp. 417–430

- [14] Yan, Q., Zhang, B., Kezunovic, M.: ‘Optimized operational cost reduction for an EV charging station integrated with battery energy storage and PV generation’, IEEE Transactions on Smart Grid, 2018, 10, (2), pp. 2096–2106

- [15] Wang, Z., Gu, C., Li, F., Bale, P., Sun, H.: ‘Active demand response using shared energy storage for household energy management’, IEEE Transactions on Smart Grid, 2013, 4, (4), pp. 1888–1897

- [16] Kalathil, D., Wu, C., Poolla, K., Varaiya, P.: ‘The sharing economy for the electricity storage’, IEEE Transactions on Smart Grid, 2017, 10, (1), pp. 556–567

- [17] Parra, D., Swierczynski, M., Stroe, D.I., Norman, S.A., Abdon, A., Worlitschek, J., et al.: ‘An interdisciplinary review of energy storage for communities: Challenges and perspectives’, Renewable and Sustainable Energy Reviews, 2017, 79, pp. 730–749

- [18] Chakraborty, P., Baeyens, E., Poolla, K., Khargonekar, P.P., Varaiya, P.: ‘Sharing storage in a smart grid: A coalitional game approach’, IEEE Transactions on Smart Grid, 2018, 10, (4), pp. 4379–4390

- [19] Wang, J., Zhong, H., Qin, J., Tang, W., Rajagopal, R., Xia, Q., et al.: ‘Incentive mechanism for sharing distributed energy resources’, Journal of Modern Power Systems and Clean Energy, 2019, 7, (4), pp. 837–850

- [20] Henni, S., Staudt, P., Weinhardt, C.: ‘A sharing economy for residential communities with PV-coupled battery storage: Benefits, pricing and participant matching’, Applied Energy, 2021, 301, pp. 117351

- [21] Vieira, F.M., Moura, P.S., de Almeida, A.T.: ‘Energy storage system for self-consumption of photovoltaic energy in residential zero energy buildings’, Renewable energy, 2017, 103, pp. 308–320

- [22] Harkouss, F., Fardoun, F., Biwole, P.H.: ‘Optimal design of renewable energy solution sets for net zero energy buildings’, Energy, 2019, 179, pp. 1155–1175

- [23] Ahmed, A., Ge, T., Peng, J., Yan, W.C., Tee, B.T., You, S.: ‘Assessment of the renewable energy generation towards net-zero energy buildings: A review’, Energy and Buildings, 2022, 256, pp. 111755

- [24] Ruszczynski, A., Shapiro, A.. ‘Stochastic programming (handbooks in operations research and management science)’. (Elsevier, 2003

- [25] Boyd, S., Vandenberghe, L.: ‘Convex optimization’. (Cambridge University Press, 2004)

- [26] Facchinei, F., Kanzow, C.: ‘Generalized Nash equilibrium problems’, Annals of Operations Research, 2010, 175, (1), pp. 177–211