A novel two-sample test within the space of symmetric positive definite matrix distributions and its application in finance

PhD student at the Faculty of Mathematics

University of Belgrade

Belgrade, 11000, Serbia

zikicamaster@gmail.com

&

Faculty of Mathematics

University of Belgrade

Belgrade, 11000, Serbia

bojana.milosevic@matf.bg.ac.rs

Abstract

This paper introduces a novel two-sample test for a broad class of orthogonally equivalent positive definite symmetric matrix distributions. Our test is the first of its kind and we derive its asymptotic distribution. To estimate the test power, we use a warp-speed bootstrap method and consider the most common matrix distributions. We provide several real data examples, including the data for main cryptocurrencies and stock data of major US companies. The real data examples demonstrate the applicability of our test in the context closely related to algorithmic trading. The popularity of matrix distributions in many applications and the need for such a test in the literature are reconciled by our findings.

Keywords Hankel transform Wishart distribution inverse Wishart distribution stability of cryptomarkets

MSC 2020: Primary: 62H15; Secondary: 62P05, 62E20

1 Introduction

Modern computational methods have given rise to the popularity of matrix distributions in contemporary statistics and statistical learning. The distributions and their properties have recently been studied in the context of cluster analysis [13, 42], classification [41], and regression [10].

Positive semi-definite matrices have many applications, including medical imaging [33] and finance [9]. Positive definite matrix variate distributions have recently been studied in [35, 43], but the works regarding goodness-of-fit testing in this context are sparse. The work of Hadjicosta and Richards [18] is the only known goodness-of-fit (GOF) test utilising integral transform methods in this context to date. The work of Alfelt, et al. [2] considers the Bartlett decomposition to construct a goodness-of-fit test for the centralized Wishart process. In addition, there has been recent interest regarding covariance matrix testing in high dimensions [11, 15, 25].

This is in stark contrast to the current developments in the univariate case. Hankel transform GOF tests have been developed for the exponential distribution [4, 5] and gamma distribution [17], while closely related Laplace transforms have been used for the development of GOF tests for exponential [8, 21, 32], gamma [22], inverse Gaussian [20] and Rayleigh distribution [31]. Baringhaus and Kolbe developed in the univariate case a two-sample goodness-of-fit test using empirical Hankel transforms [3].

We now turn our attention to the fundamental concepts that will be used in the subsequent section of this paper. Before we define the Hankel transform of a matrix random variable we introduce the following notation. We denote the matrix transpose of as , and indicates that is a positive definite matrix. In addition, we denote with the expression . We would, without explicit mention, assume that the arguments of Bessel functions are symmetric matrices, i.e. such that . denotes the space of positive definite matrices. denotes the real part of the complex number.

Definition 1.

[18]Let be a symmetric random matrix with probability density function . For the Hankel transform of order is defined as the function

where is a symmetric matrix, denotes the multivariate Gamma function and denotes the Bessel function of the first kind of order .

For more information regarding Bessel functions of matrix argument and closely related concepts of zonal and Laguerre polynomials, we point out to [16, 23, 26, 34].

The Hankel transform has many attractive properties. It is a continuous function of , its norm is bounded from above by 1, there exists an inversion formula [17], it is continuous with respect to and uniquely determines the distribution of the random variable , i.e. the following theorem proved in [18] holds.

Theorem 1.

[18]Let and be positive definite random matrices with Hankel transforms and respectively. If , then .

However, the Hankel transform is not orthogonally invariant, thus being dependent on the choice of basis. An orthogonally invariant Hankel transform is defined as follows

Definition 2.

[18]Let be a random matrix with probability density function . For we define the orthogonally invariant Hankel transform of order as the function

where , denotes the multivariate Gamma function and denotes the Bessel function of the first kind of order with two matrix arguments.

We use the following notation throughout the paper:

and

We call two matrix distributions X and Y orthogonally equivalent in distribution if there exists an orthogonal matrix such that .

The following theorem provides the uniqueness of the orthogonal Hankel transform in the class of random matrices which are orthogonally equivalent in distribution.

Theorem 2.

Let and be random symmetric positive-definite matrices and and their orthogonally invariant Hankel transforms respectively. Then if and only if and are orthogonally equivalent in distribution.

Proof.

From [34, p. 260], we have that for every positive definite matrix and every symmetric matrix the following equality holds:

| (1) |

The last equality emerges from the fact that matrices and have the same eigenvalues if is an orthogonal matrix and is a function of eigenvalues.

Assume now that . We obtain

Note that the Haar measure is orthogonally invariant, therefore if we denote with , we obtain

Therefore, directly from the definition of the orthogonal Hankel transform and using the fact that the Jacobian of the orthogonal transform is always equal to 1 (orthogonal transform is linear, the derivative of the linear map is equal to itself and the determinant of the orthogonal matrix equals 1), we get

Let’s assume the equality of orthogonal Hankel transforms. The equality

holds because of the definition of Hankel transform and (1).

From the equality given above, and the definition of the orthogonally invariant Hankel transform, we have that

Now we use the fact that depends only on the eigenvalues of its arguments to obtain

but since and for some orthogonally equivalent to are symmetric matrices which have the same eigenvalues, and that the Jacobian of the orthogonal transform is equal to 1, we have:

We obtain the similar result for , i.e. that , and the equality of distributions and follows from Theorem 1. Now, since and , where , we get that is orthogonally equivalent to . ∎

Our focus will be on the orthogonally invariant Hankel transform. The rationale for this decision is based on the readily available theoretical framework presented in [18] and algorithmic solutions outlined in [28]. Additionally, one may wish to orthogonally transform the data, such as by performing PCA or removing the dependence on the scale parameter. Orthogonal transforms are a popular method in finance as well [39, 44].

The primary goal of this paper is to extend the work presented in [18] by developing an integral two-sample test of equality of two positive definite matrix-valued distributions using the properties of orthogonal Hankel transforms. In Section 2, the test statistic are presented. Its asymptotic properties are studied in Section 3. Section 4 is dedicated to the power study, while Section 5 contains real data examples that demonstrate an application of the proposed methodology.

2 Test statistic

Let and be two independent random samples identically distributed as and , where and are symmetric positive definite random matrices respectively. Based on these samples, we present the novel test statistic for testing the null hypothesis

assuming and are symmetric positive definite random matrices. From the results in Section 1, the null hypothesis can be reformulated as:

Since the notion of orthogonal equivalence in distribution is defined in terms of the equality of corresponding orthogonal Hankel transforms, a natural way to construct a test is based on the difference of appropriate empirical counterparts, i.e. empirical orthogonal Hankel transforms of order given by

| (2) |

and

| (3) |

For all properties of this that we will use in the sequel we refer to [18]. It leads us to the following statistic

| (4) |

where and are empirical orthogonal Hankel transform of and Y respectively, defined in (2), and (3), and is a standard Wishart measure.

For all properties of this transform that we will use in the sequel we refer to [18].

Using the result from [18] we have

| (5) | ||||

| (6) |

Following the calculations in [18], we obtain:

and similarly

Finally, we obtain that (4) has the following form:

where is of the form

The evaluation of the test statistic is computationally intensive due to the complexity of evaluating the functions involved, which increases with the dimensionality of the problem.

3 Asymptotic properties of the novel test

In this section, we investigate the asymptotic behaviour of the test statistic.

It is noted in [18] that the space of Borel measurable functions such that forms a separable Hilbert space, when equipped with the inner product

The norm in this space is defined as . Assume is a symmetric positive definite matrix. Let us define the stochastic process

Note that although the process depends on , we drop the index for the sake of brevity. The same applies to the test statistic .

The following inequality ([18]), valid for every positive definite symmetric matrix and every positive definite symmetric matrix , will be of importance in bounding the norm of :

| (7) |

By applying (7) and using the triangle inequality, we obtain that

Now it follows that

| (8) |

Therefore, the random field is a random element of . The test statistic can be represented as . Denote with . We now formulate the main result of this section.

Theorem 3.

Let and be two sequences of independent orthogonally equivalent matrix random variables having the same orthogonal Hankel transform . Assume that when . Then

where is a centered Gaussian process on with a covariance kernel

Proof.

The proof will follow one outlined in [1].

Let and denote the following random processes: and respectively.

Note that under we can write

It is worth mentioning that if constants and satisfy , the process has the covariance structure . Since and , it follows that converges in distribution to the Gaussian process with the covariance kernel . The result of the theorem follows from the continuous mapping theorem.

Noting that for every , , direct computation yields

∎

It is important to emphasize that the null distribution of our test statistics depends on the underlying distributions of and , therefore the application of certain approximation techniques is necessary to perform testing in practice. This issue will be addressed in the next section.

4 Power study

For practical use in dimensions and , the parameter could be fixed to , as is common practice in problems of this nature [4].

In this section, we present the results of the power study. The empirical powers are obtained using a warp-speed bootstrap algorithm (see, e.g., [14]) with replications. The method owes its name to the significant computational savings it offers in comparison to the traditional bootstrap approach. We provide the pseudocode for the warp-speed bootstrap algorithm below. The computation is done using MATLAB [24].

The level of significance is set to , and large values of the test statistic are considered to be significant. The algorithm developed in [28] was implemented to evaluate the Bessel functions of two matrix arguments. In all cases, we assume denotes the dimension of the respective matrices. When estimating sample covariance matrices, samples of dimension have been considered. The following distributions were considered:

-

1.

Wishart distribution with the shape parameter and the scale matrix , denoted by , with a density

-

2.

Inverse Wishart distribution with the shape parameter and the scale matrix , denoted by , with a density

-

3.

Sample covariance matrix distributions obtained from the uniform vectors , where , denoted by , with a density

-

4.

Sample covariance matrix distributions obtained from the random vectors having the multivariate distribution with degrees of freedom, denoted by , with a density

Whenever a matrix in Table 1 or 2 is symmetric, we leave the lower part of the table empty. It is significant that the test is able to differentiate between the different distributions with the same expectation ( versus and versus ) with a fair degree of accuracy. The power of the test generally decreases with an increase in the number of dimensions. Nevertheless, the test appears to be well-calibrated, and the bootstrap approximation does not suffer from size distortions.

Denote with the following covariance matrix: and denote with the following covariance matrix:

5 39 12 100 33 41 45 87 92 67 87 5 10 100 82 7 8 44 60 24 33 5 100 36 7 14 62 74 37 49 5 100 100 100 100 99 100 100 4 96 89 97 99 91 95 5 8 57 73 33 48 5 49 61 28 41 5 6 10 16 5 7 11 5 6 5

5 49 19 100 38 46 57 93 97 79 89 44 5 12 100 90 6 9 55 70 29 43 9 11 5 100 34 6 17 71 81 45 59 100 100 100 5 100 100 100 100 100 100 100 45 91 48 100 4 97 96 99 100 96 98 46 10 11 100 96 5 11 70 82 44 62 50 8 19 100 94 7 5 59 71 37 50 92 48 66 100 99 63 53 6 7 10 6 97 66 80 100 100 79 68 6 5 19 11 75 22 42 100 95 35 31 12 21 5 7 87 36 58 100 98 51 42 8 13 6 5

5 61 24 100 43 55 68 97 99 90 94 50 5 16 100 95 5 10 66 81 37 53 10 11 5 100 37 5 19 80 90 55 68 100 100 100 5 100 100 100 100 100 100 100 55 96 62 100 4 99 99 100 100 99 100 53 11 20 100 98 5 14 80 90 54 70 56 8 26 100 98 7 5 70 82 46 60 96 56 75 100 100 68 58 5 7 11 6 99 73 87 100 100 85 77 7 5 22 12 83 23 47 100 99 37 22 13 23 5 8 93 39 64 100 100 55 50 8 14 6 5

5 68 25 100 59 68 80 99 100 94 98 64 5 19 100 99 7 12 76 89 41 60 15 14 5 100 58 8 28 89 95 62 78 100 100 100 5 100 100 100 100 100 100 100 66 99 68 100 5 100 100 100 100 100 100 64 10 17 100 100 5 14 87 95 61 77 73 10 36 100 100 8 5 78 90 54 69 99 69 85 100 100 84 75 5 7 14 7 100 86 95 100 100 94 88 7 5 29 16 93 33 61 100 100 51 45 17 30 5 8 98 55 76 100 100 73 66 8 17 8 5

5 79 26 100 77 78 89 100 100 98 100 5 19 100 100 9 15 84 95 48 71 6 100 78 16 49 95 99 74 89 5 100 100 100 100 100 100 100 4 100 100 100 100 100 100 5 15 94 99 69 86 5 87 95 64 80 5 8 19 37 5 9 20 5 9 5

5 25 6 100 16 51 19 57 71 52 69 5 20 100 39 5 42 22 35 17 29 5 100 10 33 11 51 67 47 61 5 100 100 100 100 100 100 100 6 80 8 63 80 63 78 5 80 23 36 19 29 6 66 80 63 78 4 6 5 8 5 5 6 5 6 5

4 36 7 100 14 65 17 70 85 66 80 25 4 21 100 41 3 45 29 43 23 38 4 27 5 100 8 43 8 64 78 60 75 100 100 100 5 100 100 100 100 100 100 100 23 54 16 100 6 89 7 78 90 77 88 56 7 44 100 84 5 88 33 48 26 43 30 57 17 100 10 90 6 79 92 79 89 62 21 56 100 71 20 74 5 7 5 10 80 36 73 100 88 38 88 6 5 5 6 57 17 53 100 67 18 71 5 5 5 7 74 31 70 100 87 31 87 8 6 7 5

5 52 10 100 12 75 14 83 93 81 91 26 4 21 100 46 3 48 36 55 31 48 2 37 5 100 4 50 6 78 89 73 88 100 100 100 5 100 100 100 100 100 100 100 36 72 23 100 5 96 4 90 97 90 96 66 9 53 100 93 5 95 44 62 36 56 45 73 25 100 13 97 6 92 97 90 96 70 22 60 100 83 20 83 5 8 5 6 86 41 82 100 95 40 95 6 5 8 4 65 17 61 100 81 15 81 6 12 5 8 84 33 78 100 94 32 96 5 7 7 5

4 55 8 100 21 84 29 90 97 87 97 44 5 33 100 70 4 70 43 62 35 54 3 41 5 100 10 61 11 85 95 82 93 100 100 100 5 100 100 100 100 100 100 100 37 77 22 100 5 99 5 96 99 95 99 79 7 63 100 99 5 99 47 67 40 60 47 80 24 100 11 99 6 96 99 96 99 86 33 80 100 94 32 94 5 8 5 5 96 55 93 100 99 60 99 7 5 11 6 83 26 76 100 94 25 94 6 12 5 9 95 48 91 100 99 51 99 6 7 7 6

5 63 6 100 39 92 50 96 99 95 99 6 48 100 86 5 88 47 73 39 64 4 100 19 76 21 93 98 90 98 5 100 100 100 100 100 100 100 5 100 9 99 100 99 100 5 100 54 78 43 68 6 99 100 99 100 5 9 6 15 5 5 6 5 9 6

5 Real data examples

Matrix-valued distributions have been used recently to model stock market data [18, 19]. However, despite the popularity of cryptocurrencies in the scientific community, such methods have not yet been implemented for the cryptocurrency market. The extreme volatility of cryptocurrency markets [30] makes it essential for traders to be aware of any significant changes in the statistical properties of assets. The properties of logarithmic returns can be of interest in analysing the cryptocurrency market [6, 7, 37]. The correlation structure of major cryptocurrency prices was investigated in [38].

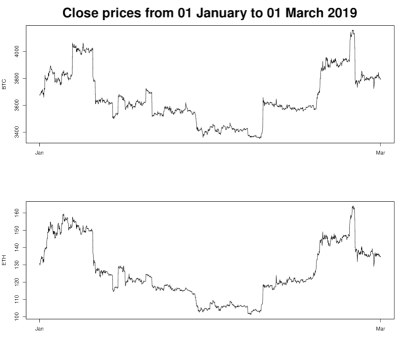

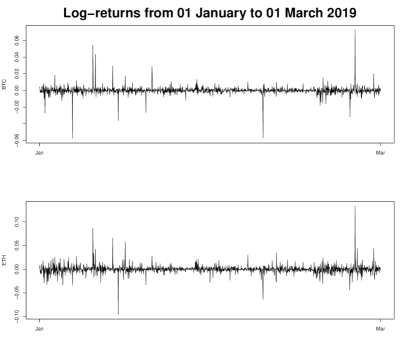

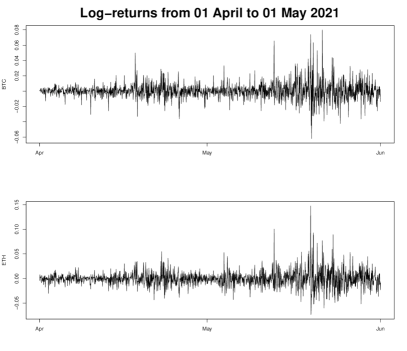

We have looked at hourly data of two of the biggest cryptocurrencies, Bitcoin (BTC) and Ethereum (ETH). The data was downloaded from Gemini (http://www.gemini.com). We have selected two periods. The first period consists of days between 01 January 2019 and 01 March 2019. In this period, the market dynamic experienced no significant changes (see Fig. 1 and 2). The second one consists of days between 01 April 2021 and 01 June 2021. In this period, the market experienced a positive bubble followed by a negative bubble [40]. The first period consists of points, while the second period consists of points. Daily observations consist of 24 points, each corresponding to one hour.

We partition the hourly close prices into daily periods consisting of 24 observations. We calculate hourly logarithmic returns and calculate the unnormalized covariance matrix for each day.

We have computed 59 covariance matrices for the first period and split it to 31 corresponding to January and 28 corresponding to February. The p-value of the statistic equals 0.9756, which points out that the statistic detected no significant change in the covariance structure of the asset hourly logarithmic returns in the period January - March 2019.

In the case of the second period, we obtained 61 matrices which we have split into 31 corresponding to April and 30 corresponding to May. We estimated the p-value using bootstrap and replications. We obtained that the p-value of the statistic equals 0.0003, which points out that the covariance structure of the asset hourly logarithmic returns has significantly changed from April to May 2021.

Furthermore, we have analyzed the behaviour of the covariance structure of the hourly logarithmic returns 15 days before and 15 days after the well-documented drops in Bitcoin price that coincide with prominent historical events [12]. Every period has points, and the results are presented in Table 3. In most cases the test is unable to detect the change in the covariance structure. Furthermore, we conducted an analysis of 1-minute BTC [45] and ETH [29] data. We selected two-day periods and computed the minute logarithmic returns. We computed covariance matrices for every hour, resulting in a total of covariance matrices, with 24 for the first day and 24 for the second day. The results presented in Table 4 indicate that our test has detected statistically significant difference in the distribution of covariance matrices both on the day and a day after the occurrence of the event, while it hasn’t detected statistically significant difference a day prior to the occurrence of the event. This could be of significant practical importance in implementing stop losses [27].

Period I start date Period II start date Date of event () Period II end date Event description 9 October 2017 24 October 2017 8 November 2017 23 November 2017 Developers cancel splitting of Bitcoin. 0.31 0.05 28 November 2017 13 December 2017 28 December 2017 12 January 2018 South Korea announces strong measures to regulate trading of cryptocurrencies. 0.32 0.27 14 December 2017 28 December 2017 13 January 2018 28 January 2018 Announcement that 80% of Bitcoin has been mined. 0.21 0.22 31 December 2017 15 January 2018 30 January 2018 14 February 2018 Facebook bans advertisements promoting, cryptocurrencies. 0.17 0.82 5 February 2018 20 February 2018 7 March 2018 22 March 2018 The US Securities and Exchange Commission says it is necessary for crypto trading platforms to register. 0.03 0.01 12 February 2018 28 February 2018 14 March 2018 29 March 2018 Google bans advertisements promoting cryptocurrencies. 0.50 0.34

Date of event () Event description 8 November 2017 Developers cancel splitting of Bitcoin. 0.0523 0.0832 0.2049 28 December 2017 South Korea announces strong measures to regulate the trading of cryptocurrencies. 0.5889 0.0027 0.0080 13 January 2018 Announcement that 80% of Bitcoin has been mined. 0.0300 0.0035 0.0493 30 January 2018 Facebook bans advertisements promoting cryptocurrencies. 0.8224 0.0352 0.7774 7 March 2018 The US Securities and Exchange Commission says it is necessary for crypto trading platforms to register. 0.0029 0.0225 0.6398 14 March 2018 Google bans advertisements promoting cryptocurrencies. 0.403 0.3019 0.0453

The second data set consists of the stock data of the three biggest S&P 500 companies at the moment. We calculate the daily log-returns for the closing prices of Apple Inc. (AAPL), Microsoft (MSFT), and Amazon (AMZN) from January 1, 2021, to January 1, 2023, covering 503 trading days. The data are sourced from Yahoo Finance (https://finance.yahoo.com). We partition the data into blocks of 7 trading days and compute a covariance matrix for each block. We then test if there is a significant change in the covariance structure between the first 31 blocks (January 1, 2021, to November 19, 2021) and the remaining 30 blocks (November 20, 2021, to January 1, 2023), obtaining a p-value of 0.001. The outcome suggests that there is a significant change in the covariance structure of the three largest companies in the S&P 500 [36].

Conclusion

In this paper, we propose the first test statistic for testing the equality of matrix distributions in the space of symmetric positive definite matrices. Our test provides important insights into the uncertainty of covariance estimates and is able to differentiate between different distributions with the same expectation. While the power study in higher dimensions is left for further research due to computational demands, our real data examples demonstrate the test’s ability to detect changes in the time series of logarithmic returns, which could prove to be significant in change-point problems.

Declaration of interest

The authors have no interest to declare.

Acknowledgements

The authors would like to express their deepest gratitude to Professor Donald Richards for his comments, which have significantly improved the paper.

The work of B. Milošević is supported by the Ministry of Science, Technological Development and Innovations of the Republic of Serbia (the contract 451-03-47/2023-01/ 200104), and by the COST action CA21163 - Text, functional and other high-dimensional data in econometrics: New models, methods, applications (HiTEc).

References

- [1] MV Alba-Fernández, Apostolos Batsidis, María-Dolores Jiménez-Gamero, and Pedro Jodrá. A class of tests for the two-sample problem for count data. Journal of Computational and Applied Mathematics, 318:220–229, 2017.

- [2] Gustav Alfelt, Taras Bodnar, and Joanna Tyrcha. Goodness-of-fit tests for centralized Wishart processes. Communications in Statistics-Theory and Methods, 49(20):5060–5090, 2020.

- [3] L Baringhaus and D Kolbe. Two-sample tests based on empirical Hankel transforms. Statistical Papers, 56:597–617, 2015.

- [4] Ludwig Baringhaus and Fatemeh Taherizadeh. Empirical Hankel transforms and its applications to goodness-of-fit tests. Journal of Multivariate Analysis, 101(6):1445–1457, 2010.

- [5] Ludwig Baringhaus and Fatemeh Taherizadeh. A KS type test for exponentiality based on empirical Hankel transforms. Communications in Statistics-Theory and Methods, 42(20):3781–3792, 2013.

- [6] Markus Bibinger, Nikolaus Hautsch, Peter Malec, and Markus Reiss. Estimating the spot covariation of asset prices—statistical theory and empirical evidence. Journal of Business & Economic Statistics, 37(3):419–435, 2019.

- [7] Jeffrey Chu, Saralees Nadarajah, and Stephen Chan. Statistical analysis of the exchange rate of bitcoin. PloS one, 10(7):e0133678, 2015.

- [8] Marija Cuparić, Bojana Milošević, and Marko Obradović. New consistent exponentiality tests based on V-empirical Laplace transforms with comparison of efficiencies. Revista de la Real Academia de Ciencias Exactas, Físicas y Naturales. Serie A. Matemáticas, 116(1):42, 2022.

- [9] Petros Dellaportas and Mohsen Pourahmadi. Cholesky-GARCH models with applications to finance. Statistics and Computing, 22:849–855, 2012.

- [10] Shanshan Ding and R Dennis Cook. Matrix variate regressions and envelope models. Journal of the Royal Statistical Society Series B: Statistical Methodology, 80(2):387–408, 2018.

- [11] Nina Dörnemann. Likelihood ratio tests under model misspecification in high dimensions. Journal of Multivariate Analysis, 193:105122, 2023.

- [12] Wolfgang Fruehwirt, Leonhard Hochfilzer, Leonard Weydemann, and Stephen Roberts. Cumulation, crash, coherency: A cryptocurrency bubble wavelet analysis. Finance Research Letters, 40:101668, 2021.

- [13] Michael PB Gallaugher and Paul D McNicholas. Finite mixtures of skewed matrix variate distributions. Pattern Recognition, 80:83–93, 2018.

- [14] Raffaella Giacomini, Dimitris N Politis, and Halbert White. A warp-speed method for conducting Monte Carlo experiments involving bootstrap estimators. Econometric theory, 29(3):567–589, 2013.

- [15] Lingzhe Guo and Reza Modarres. Testing the equality of matrix distributions. Statistical Methods & Applications, 29:289–307, 2020.

- [16] Elena Hadjicosta. Integral transform methods in goodness-of-fit testing. PhD thesis, The Pennsylvania State University, 2019.

- [17] Elena Hadjicosta and Donald Richards. Integral transform methods in goodness-of-fit testing, I: the gamma distributions. Metrika, 83(7):733–777, 2020a.

- [18] Elena Hadjicosta and Donald Richards. Integral transform methods in goodness-of-fit testing, II: the Wishart distributions. Annals of the Institute of Statistical Mathematics, 72(6):1317–1370, 2020b.

- [19] Leonard Haff, Peter Kim, Ja-Yong Koo, and Donald Richards. Minimax estimation for mixtures of Wishart distributions. The Annals of Statistics, 2011.

- [20] Norbert Henze and Bernhard Klar. Goodness-of-fit tests for the inverse Gaussian distribution based on the empirical Laplace transform. Annals of the Institute of Statistical Mathematics, 54:425–444, 2002.

- [21] Norbert Henze and Simos G Meintanis. Tests of fit for exponentiality based on the empirical Laplace transform. Statistics, 36(2):147–161, 2002.

- [22] Norbert Henze, Simos G Meintanis, and Bruno Ebner. Goodness-of-fit tests for the gamma distribution based on the empirical Laplace transform. Communications in Statistics-Theory and Methods, 41(9):1543–1556, 2012.

- [23] Carl S Herz. Bessel functions of matrix argument. Annals of Mathematics, pages 474–523, 1955.

- [24] The MathWorks Inc. MATLAB version: 9.14.0.2206163 (R2023a), 2023. URL https://www.mathworks.com.

- [25] Dandan Jiang, Tiefeng Jiang, and Fan Yang. Likelihood ratio tests for covariance matrices of high-dimensional normal distributions. Journal of Statistical Planning and Inference, 142(8):2241–2256, 2012.

- [26] Lin Jiu and Christoph Koutschan. Calculation and properties of zonal polynomials. Mathematics in Computer Science, 14(3):623–640, 2020.

- [27] Kathryn M Kaminski and Andrew W Lo. When do stop-loss rules stop losses? Journal of Financial Markets, 18:234–254, 2014.

- [28] Plamen Koev and Alan Edelman. The efficient evaluation of the hypergeometric function of a matrix argument. Mathematics of Computation, 75(254):833–846, 2006.

- [29] Prasoon Kottarathil. Ethereum Historical Dataset. https://www.kaggle.com/datasets/prasoonkottarathil/ethereum-historical-dataset?select=ETH_1min.csv, 2020. Version 2. Accessed: 2023-04-09.

- [30] Jinan Liu and Apostolos Serletis. Volatility in the cryptocurrency market. Open Economies Review, 30:779–811, 2019.

- [31] Simos Meintanis and George Iliopoulos. Tests of fit for the Rayleigh distribution based on the empirical Laplace transform. Annals of the Institute of Statistical Mathematics, 55:137–151, 2003.

- [32] Bojana Milošević and Marko Obradović. New class of exponentiality tests based on U-empirical Laplace transform. Statistical Papers, 57(4):977–990, 2016.

- [33] Maher Moakher and Philipp G Batchelor. Symmetric positive-definite matrices: From geometry to applications and visualization. Visualization and processing of tensor fields, pages 285–298, 2006.

- [34] Robb J Muirhead. Aspects of multivariate statistical theory. John Wiley & Sons, 1982.

- [35] Frédéric Ouimet. A symmetric matrix-variate normal local approximation for the Wishart distribution and some applications. Journal of Multivariate Analysis, 189:104923, 2022.

- [36] Tamás Péli. Assessing the Financial Performance of the Companies that Shape the S&P 500 Index. Acta Polytechnica Hungarica, 20(3), 2023.

- [37] Fulvia Pennoni, Francesco Bartolucci, Gianfranco Forte, and Ferdinando Ametrano. Exploring the dependencies among main cryptocurrency log-returns: A hidden Markov model. Economic Notes, 51(1):e12193, 2022.

- [38] Anoop S Kumar and Taufeeq Ajaz. Co-movement in crypto-currency markets: evidences from wavelet analysis. Financial Innovation, 5(1):1–17, 2019.

- [39] Agam Shah, Yagnesh Chauhan, and Bhaskar Chaudhury. Principal component analysis based construction and evaluation of cryptocurrency index. Expert Systems with Applications, 163:113796, 2021.

- [40] Min Shu, Ruiqiang Song, and Wei Zhu. The 2021 bitcoin bubbles and crashes—detection and classification. Stats, 4(4):950–970, 2021.

- [41] Geoffrey Z Thompson, Ranjan Maitra, William Q Meeker, and Ashraf F Bastawros. Classification with the matrix-variate-t distribution. Journal of Computational and Graphical Statistics, 29(3):668–674, 2020.

- [42] Salvatore D Tomarchio, Antonio Punzo, and Luca Bagnato. Two new matrix-variate distributions with application in model-based clustering. Computational Statistics & Data Analysis, 152:107050, 2020.

- [43] Caroline Uhler, Alex Lenkoski, and Donald Richards. Exact formulas for the normalizing constants of Wishart distributions for graphical models. The Annals of Statistics, 46(1):90–118, 2018.

- [44] Libin Yang. An application of principal component analysis to stock portfolio management. PhD thesis, University of Canterbury, 2015.

- [45] Mark Zielinski. Bitcoin Historical Data. https://www.kaggle.com/datasets/mczielinski/bitcoin-historical-data, 2021. Version 7. Accessed: 2023-04-09.