These authors contributed equally to this work.

These authors contributed equally to this work.

These authors contributed equally to this work.

[1,2]\fnmGiuseppe \surPisano \equalcontThese authors contributed equally to this work.

These authors contributed equally to this work.

These authors contributed equally to this work.

1]\orgdivAlma-AI, \orgnameUniversity of Bologna, \orgaddress\streetVia Galliera 3, \cityBologna, \postcode40121, \countryItaly

2]\orgdivDepartment of Legal Studies, \orgnameUniversity of Bologna, \orgaddress\streetVia Zamboni 27-29, \cityBologna, \postcode40126 , \countryItaly

3]\orgdivDepartment of Electrical, Electronic, and Information Engineering “Guglielmo Marconi”, \orgnameUniversity of Bologna, \orgaddress\streetViale Risorgimento 2, \cityBologna, \postcode40136, \countryItaly

4]\orgdivDepartment of Information Engineering, \orgnameUniversity of Brescia, \orgaddress\streetVia Branze 38, \cityBrescia, \postcode25123, \countryItaly

5]\orgdivDepartment of Automation and Systems Engineering, \orgnameFederal University of Santa Catarina, \orgaddress\streetTrindade, \cityFlorianopolis, \postcode88040-900, \countryBrazil

Legal Summarisation through LLMs: The PRODIGIT Project

Abstract

We present some initial results of a large-scale Italian project called PRODIGIT which aims to support tax judges and lawyers through digital technology, focusing on AI. We have focused on generation of summaries of judicial decisions and on the extraction of related information, such as the identification of legal issues and decision-making criteria, and the specification of keywords. To this end, we have deployed and evaluated different tools and approaches to extractive and abstractive summarisation. We have applied LLMs, and particularly on GPT4, which has enabled us to obtain results that proved satisfactory, according to an evaluation by expert tax judges and lawyers. On this basis, a prototype application is being built which will be made publicly available.

keywords:

Large language models, automated summarisation, keyword extraction, sentence classification, tax law cases1 Introduction

The law is typically a natural-language-based domain, and natural-language texts are pervasive in the law. First, natural language is the medium that legislation (including administrative regulations of all kinds) uses to express legal prescriptions, which humans (both experts and laypeople) are assumed to understand and comply with. Legislative and regulatory bodies have produced complex and evolving networks of natural language texts, which have complex structures and interconnections and use diverse terminologies to express technical and non-technical content. Second, natural language is used in judicial proceedings and opinions. In a proceeding, the parties to a legal case rely on natural language to express their arguments, motions, and claims, as do witnesses in their testimonies. In their opinions, judges use natural language to report the facts of the case, summarise the arguments made by the parties, and express the reasons behind interpretations, rulings, and decisions. Natural language is normally used by private parties to express contracts and other agreements as well as the accompanying documents. Finally, natural language is the usual medium for a host of legally relevant documents, at any level of complexity, that are relevant for the creation, interpretation, and application of the law, such as doctrinal scholarship, legal theories, and case commentaries.

Natural language in a legal text may use complex syntactical structures and rich terminologies, whose dense meaning results from the combination of common sense, technical knowledge, and past legal interpretations. The complexity and density of legal language have so far been a key obstacle to the deployment of AI technologies. This has been the case, on the one hand, for the deployment of symbolic AI approaches, which have struggled to capture, through the chosen formalisms, the variety, ambiguity, and meaning density of legal language. The more such formalisms have tried to reproduce the richness of natural language, the more work-intensive the knowledge-representation exercise has been and the more debatable its outcomes. On the other hand, the complexity of legal language has also limited the application of machine-learning NLP-based approaches. Most commonly, a supervised approach has been adopted where the links between input texts and the targets being predicted have to be specified by manually tagging large training sets of legal documents. The preparation of such training sets is very labour-intensive, and the information to be extracted is limited to the connections emerging from the tags in the training set.

This scenario may now be changed by the advent of large language models, also called “foundational models”[1]. The largest and best performing family of such models so far is the GPT family, developed by Open AI, the latest releases of which are GPT3.5 and GPT4 (both embedded in ChatGPT) [2]. Other large language models have recently been produced, an example being Google’s Bard. As is known, these models are very large neural networks, operating on hundreds of billions of parameters (links in the network). They have been constructed by training such networks on enormous sets of natural language documents. Based on that, a network learns to predict the texts (sequences of words) that are likely to meaningfully complement the input contexts (the prompts) that are provided by users (for an introduction to LLMs, see [3]).

The results achievable through large language models have been surprisingly good. The “stochastic parrots” – as these systems have been called given their ability to express well-formed and seemingly meaningful language without having a real understanding of what is being said [4] – can draft complex texts that in many cases have sufficiently good quality for different uses relevant to the law (translation, summarisation, document analysis, draft generation, completion). It is true that in some cases such systems “hallucinate”, i.e., they provide content (e.g., legal citations or reasoning) that does not match reality, or give answers that violate basic logic. However, even if they only mimic the text generation of cognisant humans, their performance is considerable and in many cases surprisingly good, or at any rate satisfactory for many practical applications.

In the following, we shall discuss how LLMs have been used in the PRODIGIT project, an initiative developed in Italy by the Presidential Council of Tax Justice (Consiglio di Presidenza della Giustizia Tributaria, CPGT), in cooperation with the Ministry of the Economy and Finance (Ministero dell’Economia e delle Finanze, MEF), and funded by the National Operative Project for Governance and Institutional Capacity Programme 2014-2020. The general aim of the project is to provide support to tax judges and lawyers through digital technologies, in particular through AI techniques. In the project, LLMs have been used for two main purposes: (1) to prepare summaries and headnotes of judicial decisions and extract related information; and (2) to provide semantic tools for searching and analysing the case law.

In the following, we shall first describe the context of the project (Section 2) and the dataset used (Section 3) and will then address the summary-generation function (Sections 4 to 7). Following this analysis, we present the evaluation procedure based on surveys carried out with legal experts (Section 8). Finally, we consider related work on the use of LLMs in the legal domain (Section 9) and provide some considerations for future work (Section 10).

2 Tax Law Adjudication

Italian tax law adjudication involves three levels: (1) tax courts of first instance, (2) tax courts of second Instance, and (3) the Supreme Court of Cassation.

The process begins with the tax courts of first instance, where taxpayers can file complaints against the decisions made by central and local Italian tax authorities. These courts have jurisdiction over cases related to most tax matters, including income tax, value-added tax (VAT), corporate tax, and local taxes. Both parties (taxpayers and tax authorities) present their arguments and evidence during the first instance proceedings, after which the court issues a legally binding judgement. If dissatisfied, either the taxpayer or the tax authority or tax office can appeal to a tax court of second instance, which have jurisdiction over an entire region. These have the power to confirm, modify, or overturn the first-instance decision. Further appeals can be made to the Supreme Court of Cassation, the highest judicial authority, on matters of law (the Court of Cassation cannot re-examine the facts of the case). Tax law judges are a mixed group, including both professional and non-professional judges. The latter are usually lawyers or accountants who serve part-time in a judicial capacity and are paid based on the number of cases they decide. The quality of their decisions is often said to vary significantly, and to be on average lower than in other parts of the judiciary.

Italy, like other countries, faces a very large number of tax-related cases. This is determined by many factors, among which the large taxpayer base, the relatively low level of tax compliance, and the uncertainties in tax law, as determined by the complexity of the tax regime and the frequent changes in tax law provisions. The 2022 report provided by the Department of Finance111MEF Dipartimento delle Finanze, Relazione sul Contenzioso della Giustizia Tributaria, giugno 2023 https://www.finanze.gov.it/export/sites/finanze/.galleries/Documenti/Contenzioso/Relazione-monitoraggio-contenzioso-2022.pdf shows that the number of complaints received by tax courts of first instance in 2022 was about 145,972, while appeals brought to courts of second instance were 41,051. The Court of Cassation receives about 10,531 appeals against second-instance decisions.

Italy has made some efforts to modernise its tax adjudication system by embracing digital solutions. One significant development is the introduction of electronic filing and communication systems, referred to as a “telematic tax process” (Processo Tributario Telematico), which has allowed for the almost complete digitisation of all stages of the judicial process. Through this system, taxpayers can submit appeals, supporting documents, and relevant information, and judges can read, write, and deliver their measures electronically, eliminating the need for physical paperwork, time-consuming procedures, and administrative burdens. In particular, with regard to the decision-making phase, the platform for preparing a judicial decision in digital form (referred to as a “digital judicial decision” – Provvedimento Giurisdizionale Digitale, or PGD) has been fully operational in all tax courts since 1 December 2021 and allows the judge to draft, sign, and file decisions fully electronically. At present, the PGD enables the electronic drafting of collegiate (panel) judgements, as well as orders and judgements issued by a sole judge.

New technologies, including machine learning and LLMs, are starting to be used to address certain aspects of tax administration. For instance, data analytics and AI tools are currently employed by the Italian Tax Administration to analyse large bodies of financial and transactional data and detect potential discrepancies or irregularities.222Bloomberg Tax, Italy Turns to AI to Find Taxes in Cash-First, Evasive Culture, available at https://news.bloombergtax.com/daily-tax-report-international/italy-turns-to-ai-to-find-taxes-in-cash-first-evasive-culture Hopefully, this will allow for a more efficient and targeted approach to tax audits and investigations. Tax adjudication is lagging behind in the use of AI technologies by comparison with tax administration. The PRODIGIT project aims to make AI technologies available in tax adjudication as well, so as to provide judges and professionals with better, more targeted information and help them efficiently address the complexities of tax law.

3 The PRODIGIT Dataset

The PRODIGIT project aims to provide tools that can be applied to the whole of Italian case law in the tax domain. However, for the purpose of experimentation and prototyping, a restricted domain was selected, namely, decisions concerning the registration and recordation tax (imposta di registro). This tax concerns the registration and recordation of deeds and other legally relevant documents and applies in particular to various kinds of contracts (such as those involving the transfer of real estate). It has the dual purpose of providing tax revenue and of paying the state for the service it provides to private individuals, namely, keeping track of particular deeds and financial transactions to give them legal certainty. It is governed by Presidential Decree No 31/1986 (Testo Unico dell’imposta di registro).

We only considered those decisions that have been produced in a native digital format through the online platform provided to tax judges. In the future, the data set will be expanded to also include the vast amount of past decisions that are currently only available as scanned images of paper documents.

We started with a collection of approximately 1,500 decisions addressing certain selected topics within the domain of the registration tax. Of such decisions, 750 were delivered by tax courts of first instance and 712 by tax courts of second instance. These decisions span between 2021 and 2023, with most decisions issued in 2022. They have been delivered by the tax courts of different Italian regions and provinces.

The decisions have a standard structure consisting of the following parts:

-

1.

Introduction, reporting (i) the number of the decision, (ii) the composition of the judicial panel, (iii) the parties and their attorneys (if present), the latter of which had previously been anonymised;

-

2.

Development of the Proceeding, reporting (a) the facts related to the tax administrative process and, when delivered at the second instance (on appeal), the procedural facts related to the first-instance (trial court) proceedings (e.g., the parties’ requests, claims, and arguments, as well as first-instance decisions by the tax court); (b) the requests by the parties, often presented with the related claims and arguments, possibly formulated as appeals against the first-instance decision;

-

3.

Grounds of the Decision, stating the reasons in fact and in law supporting the court’s decision;

-

4.

Final Ruling, stating whether the complaint or appeal has been accepted or denied, and allocating the costs of the proceedings.

A dataset of 17,000 decisions from various areas of tax law is currently being normalised – i.e., anonymised, segmented into relevant partitions, and corrected to fix typos and garbled text – and will be used in future developments of the project.

4 Summarisation of Tax Law Decisions

The first task addressed in the PRODIGIT project concerns the summarisation of judicial decisions. In this section, we introduce the concept of summarisation and present the running example that will be used in the following section

4.1 Summarisation in the Legal Domain

Summarisation is the process of condensing a large set of input information into a shorter document, the summary, which still contains the most significant information, or at any rate the information that is relevant to the task at hand. In general, summarisation is subject to the need to jointly satisfy conflicting requirements as best as possible: providing a summary that is as short as possible but still includes as much of the relevant information as possible.

Summarisation is very important in the legal domain, where the amount of available legal materials overwhelms the human capacity to process them. By providing summaries of decisions, judges and lawyers are given a chance to determine more quickly whether a precedent is relevant to the issue at hand, and decide whether it is worth their while engaging with the text in its entirety. Moreover, summarisation may highlight the key points of a lengthy decision, enabling lawyers to focus on them. Legal documents are particularly challenging for summarisation compared to other types of texts. These challenges relate to multiple aspects, such as the length of the documents, the hierarchical and interconnected structure of their parts, theit complex technical vocabulary, and the ambiguity of natural legal language, as well as the importance of citations to legal sources.

In Italian legal culture, we can distinguish two kinds of summary accounts (or statements) of judicial decisions.

The first account consists of so-called “maxims” (massime in Italian). A maxim (massima) specifies the most significant principles stated in leading judicial decisions. There exists an office in the Italian Supreme Court (the Ufficio Massimario) that is tasked with preparing maxims from the case law of that court. The highly qualified judges working in this office identify what decisions deserve a maxim, since they introduce principles that are particularly important, establishing new law or solving a previously unsettled issue. These principles are given compact linguistic formulations (the maxims) which are published in an online collection. In the tax domain, the function of preparing maxims has until recently been carried out by regional bodies and will be entrusted to a national body in the future. Maxims are important in the Italian legal system since they are often taken as authoritative statements of the law, and are used in arguments to support interpretive and other claims. There is indeed a debate among Italian lawyers on the extent to which maxims effectively contribute to a knowledge of the law and to legal certainty, capturing with precision the underlying rationale or ratio decidendi of important cases. In any event, this is an important and persisting aspect of Italian legal culture.

The second account consists, more modestly, in providing summaries, i.e., abstracts of legal cases, to be used to “triage” retrieved cases and identify the points in them that are most relevant. In other words, a summary enables lawyers decide whether they should engage with the whole case (or a section of it) and points them to its most significant aspects. It is this second kind of account (the summary) that we aim to provide with PRODIGIT. We do not undertake to replace the production of maxims, a task that, as noted, requires advanced legal skills, with the maxims themselves playing a distinctive role and institutional arrangement in the Italian legal system. However, we believe that automated summarisation, particularly in the form of the automated extraction of “decision-making criteria” (see Section 7 may provide useful support to the office tasked with preparing the maxims, the Ufficio Massimario).

We experimented with both extractive and abstractive summarisation, considering that both approaches are potentially useful in the legal domain, and indeed they present complementary advantages and disadvantages.

Extractive summarization selects the most meaningful sentences in the input text and combines them to form the summary. No change is made to the textual content of the extracted sentences. The extractive approach has the advantage of ensuring that all content in the summary is obtained from the input document, without any spurious addition. Moreover, it enables the reader to move from the selected sentences to their position in the original document, so as to obtain a context for such sentences, when needed. On the other hand, the extractive approach may fail to capture all relevant content or may do so only at the cost of reproducing large parts of the original texts, thus defeating the very purpose of summarization.

Abstractive summarization generates a new text which aims to provide a synoptic statement of the content of the input documents, without reproducing their wording. The abstractive approach – when it does its job well – has the advantage of providing a short text that, in an appropriate linguistic form, still captures the salient content of a much larger document. But it may not work well, so it carries the risk of misleading readers by “hallucinating”, generating content that is not found in the original text.

Both extractive and abstractive summarization can find their use in the legal domain. The extractive approach is most appropriate in those cases in which the input documents are well-structured, being divided into relatively short sentences, each of which delivers a separate message. This is usually the case with decisions by the highest courts, which generally address separately the different issues submitted by the parties (the claims against lower-level decisions being contested), presenting in an orderly manner the reasons for deciding the case in one way or the other. These high courts see it as part of their mission to state binding or at least persuasive principles that should guide lower courts, and they often expressly state these principles in separate, well-recognisable sentences. Unfortunately, this was not the case with the decisions we considered, namely, first-instance and appeal decisions in the tax domain, which often include long sentences addressing different issues, often introducing new elements that concern issues discussed in previous sentences.

The abstractive approach may be more appropriate when the legal reasoning is developed in long, sprawling sentences, having mixed content, or when a long decision needs to be summarised into a short and clear account, regardless of the way in which this content is expressed in the original document. In our experiments, we used both extractive and abstractive approaches and submitted their outcome to the evaluation of legal experts (see Section 8).

4.2 Running Example

As a running example, we use Decision No. 7683 issued on 14 September 2022 by the Court of Second Instance of Sicily.

The case concerns the application of the first-time home buyer tax relief on the purchase of a house by a person who already owns another property. The buyers argued that they were entitled to the relief since that property was unsuitable for housing.

The tax office had nevertheless refused to grant the relief, so the buyer attacked this decision in front of the tax court of first instance, winning the case, i.e., finding that the buyer was entitled to the relief.

The tax administration appealed the decision, and the court of second instance upheld the first-instance decision on the ground that the property already owned by the buyer was unsuitable for housing according to an expert home-inspection report. This was argued based on the case law of the Supreme Court, according to which the law on the registration tax has to be interpreted in such a way that the tax relief is to be denied only to those who own a house concretely suitable to be used as a dwelling.

In the following, we shall use this case both for extractive and abstractive summarisation, which we will illustrate by presenting some portions of (the English translations of) the outputs of our experiments. The entire text of the case and some summaries being produced are available in the Appendix A, in an English translation. The original outcomes of our experiments, in Italian, as well as further outputs, are available in this online repository.

The implementation was conducted within the IBM Cloud Pak for Data environment333https://www.ibm.com/products/cloud-pak-for-security - Accessed on August 1st, 2023. This platform offers comprehensive packages essential for AI-based solutions. To access OpenAI models, we utilized the Microsoft Azure API444https://azure.microsoft.com/ - Accessed on August 1, 2023.

5 NLP Summarisation Tools

Natural Language Processing is a flourishing field with methods ranging from classical statistical approaches to very large ML-based models capturing subtle semantic features.

In our research, we tested both special-purpose NLP tools for extractive summarization and the recent large language models, which we deployed for both extractive and abstractive summarization.

5.1 Special-Purpose NLP Tools

Extractive summarization techniques have been around for several decades and are widely used, including in the legal domain. As noted above, the goal of these methods is to extract the most significant sentences from a text with multiple paragraphs, under the assumption that such selected sentences can sum up the meaning of the entire text, or at least convey its most significant legal content.

As a first option, we tackled extractive summarization using the following established techniques.

Latent Semantic Analysis (LSA)

LSA uses singular value decomposition to identify the underlying relationships between words in a document. It assigns a weight to each sentence based on its semantic similarity to the entire document. Sentences with greater weights are considered more important and are included in the summary. The goal is to create summaries with wide coverage of the document’s main content while avoiding redundancy [5].

Lex-Rank

Lex-Rank uses a graph-based approach to identify the most important sentences in a document. It creates a graph where each sentence is a node, and the edges between the nodes represent the similarity (cosine) between sentences. The most important sentences are those that have the highest centrality scores, which are calculated using PageRank [6]. Lex-Rank is quite insensitive to the noise in the data that may result from an imperfect topical clustering of documents [7].

TextRank

This is a general-purpose graph-based ranking algorithm for NLP. Essentially, it runs PageRank on a graph designed for summarization. It builds a graph using some set of text units as vertices. Edges are based on the measure of semantic or lexical similarity between the text unit vertices. Unlike PageRank, the edges are typically non-directed and can be weighted to reflect degrees of similarity.

Luhn

Luhn uses a statistical approach to identify the most important sentences in a document. The approach assigns a score to each sentence based on the frequency of important words in the sentence. One advantage of Luhn is that it is a simple and interpretable algorithm that can be easily implemented.

Natural Language Toolkit (NLTK)

NLTK is a platform for building Python programs to work with human language data. Its summarizer applies a variation of the TextRank algorithm. It creates a graph where each sentence is a node, and the edges between the nodes represent the similarity between sentences. It assigns a score to each sentence based on its centrality in the graph. The NLTK summarizer is easy to use and can generate high-quality summaries. However, the NLTK summarizer may struggle to handle documents with complex language or a large number of irrelevant sentences.

5.2 Large Language Models

Besides exploring task-specific techniques, we also explored the applicability of more general-purpose tools like Large Language Models (LLMs), among which IT5 and GPT.

LLMs use transformer architectures based on a combination of large neural networks with attention mechanisms to track relationships between the words in a text. Transformers are pre-trained on large amounts of text in a self-supervised fashion, i.e., they are automatically trained from the input text without human intervention. In this way, they learn the statistical connections between words. In their sequences, a piece of information is used to develop the basic ability of these models, namely, to effectively predict the next words given an initial text. Though LLMs can be seen as language-to-language machines, all internal processing is numeric. Hence LLM input stages provide embedding functions, i.e., mappings from text chunks to high-dimensional numeric vectors that reflect the semantic features of such text chunks. In more advanced LLMs, the core statistical engine may be wrapped in further layers, which provide the system with additional capacities, such as following instructions, producing output in a prescribed format, and preventing the delivery of inappropriate output.

Though, in principle, pre-trained LLMs can be fine-tuned to specific text corpora, so far we have not engaged in any further training. This is due to the fact that good results could be obtained without fine-tuning the general GTP4 model, and also by the fact that we did not have a large set of tax decisions summarised by humans. Some summaries have been created in the past, but their number is limited and their styles and quality vary greatly. Moreover, the improvement obtained by fine-tuning large language models so far appears to be limited and probably will be even more limited in the future, when the capabilities of state-of-the-art tools improve. However, we plan to engage in some fine-tuning experiments in future developments of this project. We will assess whether this direction is worth taking on the basis of outcomes of these experiments.

In the following, we give further details on the LLM we employed.

IT5

The IT5 model family offers a sequence-to-sequence transformer model for the Italian language. Based on the Transformer-XL architecture, this model has been pre-trained on a vast dataset of over 5 million web pages, enabling it to capture long-term dependencies in the text. The model provides more coherent and consistent text compared to earlier transformer-based models. Additionally, it has the capability to generate text from a given prompt, making it well-suited for tasks such as summarization, question-answering, and dialogue generation [8]. One can use IT5 for such tasks by accessing the model available at Huggingface platform555https://huggingface.co/efederici/sentence-it5-base, which is straightforward to use with the Python programming language. Of the available models for IT5, we used both large and small ones.

GPT

GPT, short for Generative Pre-trained Transformer, is an auto-regressive language model that employs deep learning techniques to produce text that resembles human language. This model is based on a large-scale transformer architecture and has been trained using a vast dataset of webpages. GPT uses a deep neural network to generate text that is highly similar to human writing. The model is trained in a self-supervised learning task, which involves predicting the next word in a sequence of words, given all the previous words. As a result, GPT can produce coherent, fluent, and practically indistinguishable text from human-written text. It can be leveraged for a wide range of natural language processing tasks, such as answering questions, summarising text, and translating languages. Those interested in using GPT can easily access the API offered by OpenAI. We used GPT both in version 3.5 [9] and version 4 [2], the latter being the latest and, according to its developers, far more capable than its predecessor in tasks like sentiment analysis and text classification. GPT-4 can also process a more significant number of input and output tokens, thus accessing more sophisticated tasks.

6 Extractive Summarisation

We applied all the special-purpose NLP tools described in Subsection 5.1 and the generative models from Subsection 5.2 to the task of extractive summarization.

6.1 Extractive Summarisation through Special-Purpose NLP Tools

All special-purpose NLP tools were applied to judicial decisions in order to obtain summaries to be evaluated by legal experts. Unfortunately, the results were far from satisfactory (see Section 8). In general, we obtained lengthy summaries, in which the relevant legal information was, on the one hand, scattered across the different paragraphs of the summary and, on the other hand, incomplete.

In the following, we provide an English translation of a sentence selected by all the examined techniques:

Example 1.

Even after this legislative innovation and, therefore, in relation to the current text, the prevailing jurisprudence of the Supreme Court (see lastly Cass. Civ. No. 20981/2021) has adhered to the interpretative option according to which the mere ownership of a real estate asset is not an obstacle to the recognition of the concession, which is instead due to the taxpayer who does not own a property that can be used as a dwelling (in this sense also Cass., Sec. 5, Order No. 19989 of 27/07/2018, according to which “on the subject of tax concessions for the first home, pursuant to art. 1, note II bis, of the tariff attached to the d.p.r. no. 131 of 1986, in the text (applicable “ratione temporis”) amended by art. 3, paragraph 131, of Law no. 549 of 1995, the concept of “suitability” of the pre-owned house – an obstacle to the enjoyment of the benefit (and expressly provided for in the previous legislation) – must be considered intrinsic to the notion of “dwelling house” itself, to be understood as accommodation that is concretely suitable, both from an objective-material and legal point of view, to meet the housing needs of the interested party”; as well as Cass., Sec. 5, Judgment No. 2565 of 02/02/2018, which ruled that “on the subject of first home concessions … “the suitability” of the pre-owned dwelling must be assessed both from an objective point of view – actual uninhabitability – and from a subjective point of view – building inadequate in size or qualitative characteristics –, in the sense that the benefit also applies in the case of the availability of accommodation that is not concretely suitable, in terms of size and overall characteristics, to meet the housing needs of the interested party. “ and in the same sense also Cass., Sec. 6-5, Order No. 5051 of 24/02/2021, Cass., Sec. 6-5, Order No. 18091 of 05/07/2019, and Cass., Sec. 6-5, Order No. 18092 of 05/07/2019).

6.2 Extractive Summarisation through LLMs

Although generative models are not intended to be used for extractive tasks, we attempted to use them for this purpose, too. To this end, we designed a prompt meant to push generative models toward literal extraction, and we tested it with both GPT-3 and GPT-4. In a preliminary phase, IT5 was also tried, but the results were unsatisfactory, since the model appeared to be unable to follow the instructions for creating the summaries.

Instructions in our prompt were divided into three sections:

-

•

In the first section, the concept of an “extractive summary” goal was declared and defined.

-

•

In the second section, we described a method for obtaining a summary, i.e., breaking up the document into sentences, assigning a score to each sentence according to its semantic relevance, and identifying the most relevant sentences.

-

•

A final section indicated the format in which the output had to be produced, i.e., as a list of sentences and associated scores.

We fed out the prompt to GPT 3.5 and 4. Here below we can see the prompt we used and its translation into English.

The extractive summary obtained through this prompt was shorter than the outcome provided by the specific NLP tools. Following is the output produced feeding GPT-4 with the grounds of the decision in Subsection 4.2.

Example 2.

The fundamental preliminary question concerns the evaluation of the suitability or otherwise of the property pre-purchased by the appellant, with respect to the housing needs of himself and his family. It appears from the same that the property in question consists of a small room and a bathroom (depicted in the attached photographic documentation), having a total cadastral area of 25.00 sqm and a usable living area of 17.90 sqm (as shown in the attached plan). The technician also ascertained that the property shows traces of rising damp, mold and fungi, concluding that it is not suitable for meeting the most basic housing needs for a family unit composed of a father and two school-aged children. Based on the aforementioned assessment, supported by plans and photographs, it must therefore be considered established that the property purchased by the respondent_1 on 19/3/2003, must be considered unsuitable for meeting the housing needs of the aforementioned and his family, so that the first judge correctly considered such purchase not preclusive with respect to the tax benefits claimed. Therefore, the appeal filed must be rejected and the contested judgment must be confirmed

Note that in many cases, unlike the extractive tools, GPT constructed the extractive summaries by selecting and combining phrases or sentence fragments (see, for example, the summary produced by GPT-3 using the same decision in the appendix). In this way, shorter and more informative summaries could be obtained.

7 Abstractive Summarisation

We relied on IT5 and on both versions of GPT to produce abstractive summaries of two kinds: (1) “flowing-text” summaries and (2) “issues-based” summaries.

7.1 Flowing-Text Summaries

Flowing-text abstractive summaries have no prescribed structure. We tested IT5, GPT3, and GPT4 to generate such summaries of each of the two sections of our decisions: “development of the proceedings” (svolgimento del processo) and “reasons of the decision” (motivi della decisione). For this purpose, a very simple prompt, which we used for all of the three models, was enough:

Here below is the summary generated for the decision in Section XXX (development of the proceedings) using GPT4 (the GPT models provide a much better outcome than IT5, with regard to both readability and completeness; see Appendix).

Example 3.

The text concerns the issue of the suitability of a property pre-purchased by the applicant to meet the housing needs of his family. The sworn appraisal filed by the respondent highlights that the property, small in size and with traces of humidity, mould, and fungi, is not suitable for accommodating a family unit consisting of a father and two school-aged children. Therefore, the judge deemed it appropriate not to consider such a purchase as preclu- sive for the tax benefits claimed. The prevailing case law maintains that mere ownership of a property is not enough to deny the relief, which is instead granted to those who do not own a suitable dwelling. The appeal submitted is rejected and the contested judgment is confirmed, with the costs of this phase charged to the office.

7.2 Issue-Based Summaries

We exploited the capacities of GPT for providing issue-based summaries. The idea is to distinguish the issues addressed by the judges and to provide a separate summary analysis for each of them. This approach was motivated by the hypothesis that this style of summarization may facilitate lawyers in identifying and examining the aspects of the case that are relevant to them. This hypothesis was confirmed by the expert evaluations, which were most favourable for this kind of summary (see Section 8).

GPT-3.5 and GPT-4 were instructed on what to look for and list as output by a suitably designed prompt. We also tested IT5, but this experiment was unsuccessful, since IT5 appeared to be unable to follow the instructions for creating issue-based summaries.

The set of instructions we used for GPT is devoted to the description of the intended output in two directions: a formal requirement and a conceptual requirement.

According to the formal requirement, the output consists of a sequence of questions/answer pairs where questions are denoted as QD1, …, QDn, and the answers are denoted as PD1, …, PDn. The prompt also makes it possible to switch between a more human-readable list and a json structure.

According to the conceptual requirement, the answers consist in the specification of principles, where a principle is defined as the application or interpretation of an explicit norm, regulation, or previous decision.

After introducing principles, the prompt continues by stating that a question is something that is answered by means of a principle.

To make the model focus on essential but independent issues, we added a few prescriptions, namely, two principles must be very different from each other; the number of principles in a text is usually 1 or 2 with more principles appearing only in lengthy texts.

We also specified that a principles are to be reported explicitly, and that questions are to be stated in general terms, i.e., without reference to the specific case at hand.

The adopted prompt is shown below, in the original Italian version and in an English translation (the variant requesting the output in a JSON structure is omitted):

In the following, you can find one of the principles extracted using GPT4:

Example 4.

QD2: What is the current interpretation of the legislation on tax concessions on a first home in relation to the suitability of a pre-owned dwelling?

PD2: The suitability of the pre-owned dwelling must be assessed both from an objective point of view (actual uninhabitability) and from a subjective one (inadequate building in terms of size or qualitative characteristics), meaning that the benefit also applies in the case of the availability of a dwelling that is not concretely suitable, in terms of size and overall characteristics, to meet the housing needs of the interested party (Cass., sect. 5, order n. 19989 of 27/07/2018, Cass., sect. 5, judgment n. 2565 of 02/02/2018).

We also experimented with expanding the prompt to include instructions for identifying the original text addressing the summarised issue, and for extracting keywords.

Line 14 of the original prompt was substituted with

While Line 25 was expanded into

A keyword (KW) refers to relevant legal concepts and subjects contained in the text. The keyword-related portion of the prompt follows the extraction of legal principles, as they should provide contextual information to narrow down the generation to the most relevant keyword with substantive legal meaning.

The prompt also includes instructions for connecting the extracted principles to the relevant part of the original decisions, from which they were extracted (BT). Such a reference allows us to easily verify the correspondence between the extracted principles and the original text. The model is requested to extract three fragments at most, without the introduction of any variation relative to the original text.

Following are the text and keywords associated with the principles in the example above:

Example 5.

BT1: [on the subject of tax concessions for the first home, pursuant to art. 1, note ii bis, of the tariff attached to the d.p.r. n. 131 of 1986, in the text (applicable “ratione temporis”) amended by art. 3, paragraph 131, of the law n. 549 of 1995] BT2: [the concept of “suitability” of the pre-owned home - an obstacle to the enjoyment of the benefit (and expressly provided for in the previous legislation) - must be considered intrinsic to the very notion of “house of residence”, to be understood as a dwelling concretely suitable, both from an objective-material and legal point of view, to meet the housing needs of the interested party] BT3: [the concessions under examination respond to the reasonable rationale of favoring the purchase of a dwelling in the place of residence or work for the benefit of those who do not have possession of another house of residence objectively suitable to meet their needs]

KW: [tax concessions, first home, housing suitability, housing needs, uninhabitability, inadequacy, property ownership, legislation, jurisprudence]

8 Evaluation

The standard automated tools for accessing the quality of summaries, such as ROUGE, do not apply satisfactorily to abstractive summarisation. Thus we submitted questionnaires to tax law experts, asking them to evaluate the process. The questionnaires were previously submitted to the ethical committee of the PRODIGIT project, which reviewed them, proposed refinements and clarifications on the questions and the methodology, and finally approved the revised questionnaires. Based on the indications of the ethical committee, the evaluation only concerned the comparison between different automated systems, to the exclusion of summaries written by humans. This limitation responds to the following considerations: on the one hand, having human-prepared summaries for all tax law decisions is not a viable option, this due to the size of that case base; on the other hand, on the proposed approach, automated summarisation can be combined with human intervention at the validation and revision stage.

We performed two different evaluations: The first one was devoted to choosing a subset of models that were performing better, this in order to reduce the number of models to be considered. The second one was focused on the resulting small set of models, aiming at collecting from domain experts how these models perform in the context of tax law.

The questionnaires encompassed various evaluation criteria, including:

-

•

Satisfaction: Degree of satisfaction with the overall quality of the summary.

-

•

Correctness: Accuracy in capturing the source documents’ key points, legal nuances, and essential information.

-

•

Form: Coherence, readability, and adherence to legal writing conventions.

-

•

Completeness: Coverage of important details and comprehensive representation of the source content.

The domain experts reviewed the summaries, rated them under each criterion, and provided corresponding scores in the range. They also had the option of expressing their comments. They were encouraged to provide their insights, suggestions, and concerns regarding the quality of the summaries. The evaluations were blind, in the sense that the reviewers were not told by what models the summaries were generated.

By incorporating the feedback and ratings from domain experts through the questionnaires, we obtained a holistic evaluation of the generated summaries. This evaluation process enabled us to gauge the strengths and weaknesses of each model, identify areas for improvement, and make informed decisions about the quality and effectiveness of the generated summaries in accordance with the domain-specific requirements.

In the next sections, we report and describe the evaluation for the summaries.

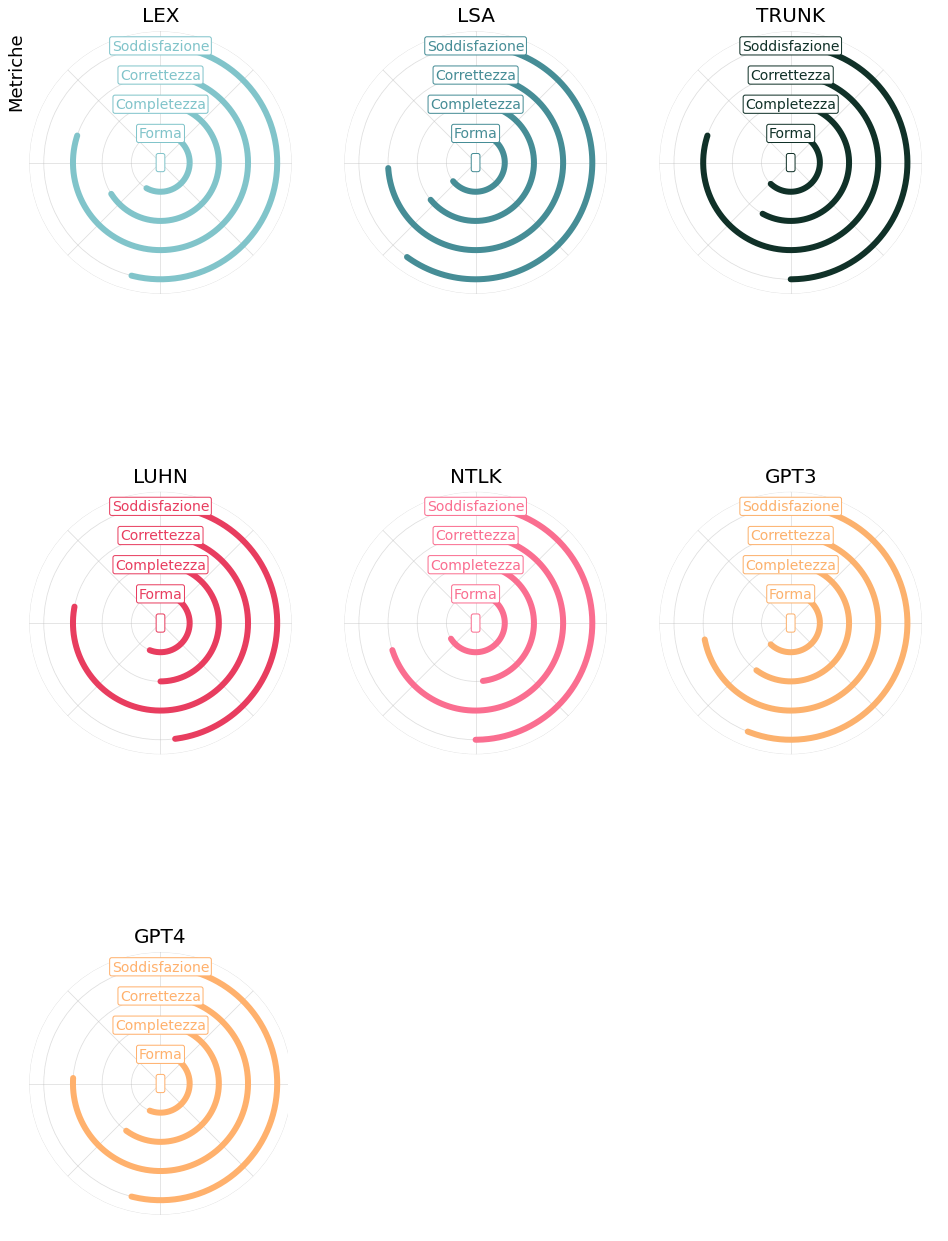

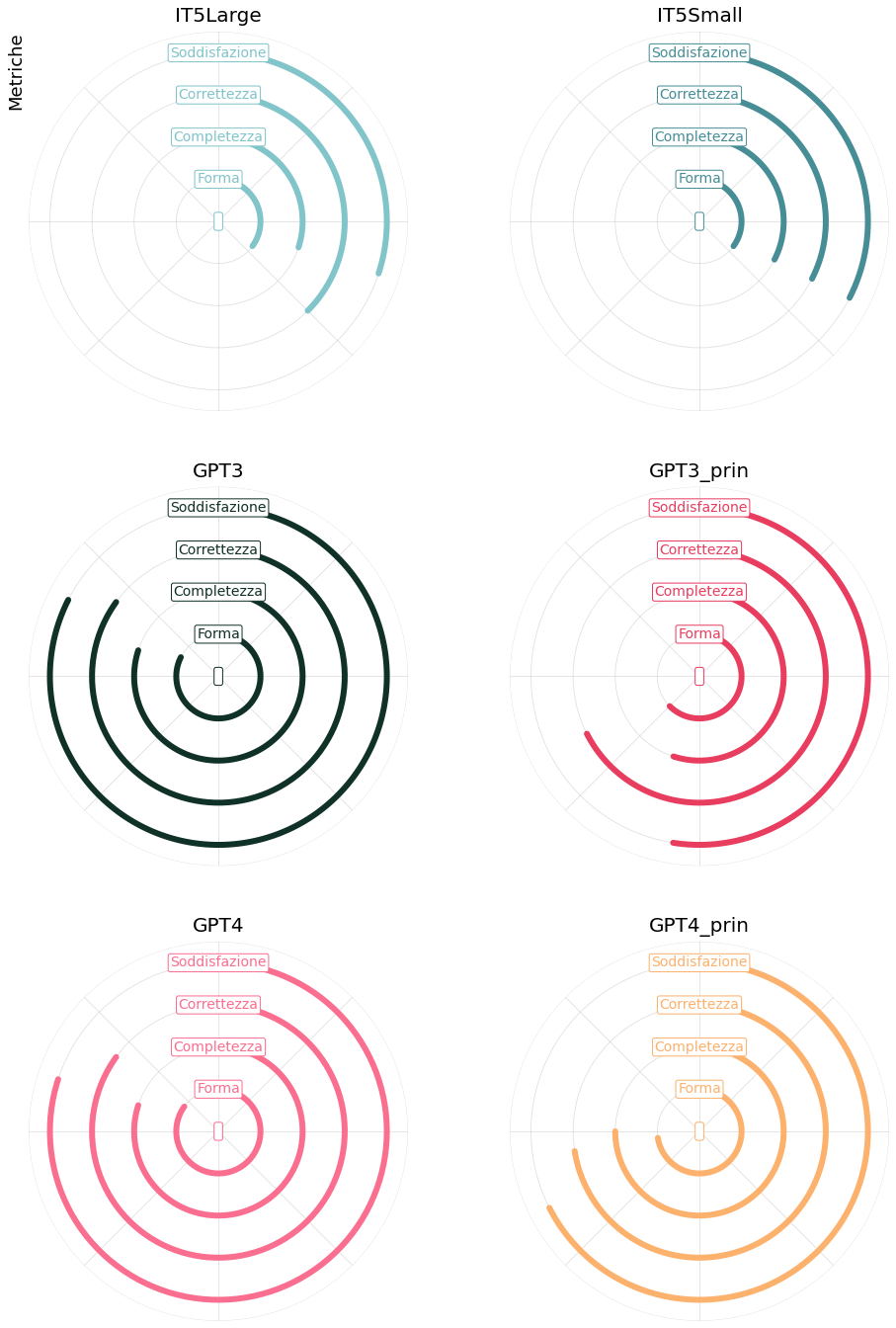

We report the average scores for each metric considered in Figures 1, 2, and 3. Each graph corresponds to a model, and for each model, we can notice the average value for each metric.

8.1 First Evaluation

As observed, the first evaluation had the purpose of selecting the most promising approaches, which would then be subject to the second evaluation. It was carried out by a limited number (12) of experts in tax law.

Extractive Summaries

Figure 1 and Table 1 show that the special-purpose NLP tools perform similarly. This is because the extractive nature of the task does not allow for outputs that differ too much in form. The correctness of all the models is quite high, as is to be expected, since they consisted of phrases literally extracted from the original text. Completeness is weak, as the information from other sentences was completely omitted. As a consequence the the experts’ satisfaction was on average low. Similar –through slightly better – outcomes can be seen for the extractive summaries produced with generative tools (GPT3 and GPT4).These models as well appear to have omitted much relevant information, especially when dealing with long decisions. On the basis of this evaluation, we decided to discard all extractive approaches and limit the second evaluation to the abstractive methods. However, as shown in Section 7.2 we incorporated an extractive aspect in the issue-based summary so as to enable the user to link the abstracted principles to their textual basis.

| LEX | LSA | TRUNK | LUHN | NTLK | GPT4 | GPT3 | |

|---|---|---|---|---|---|---|---|

| Form | 2.85 (1.23) | 3.00 (1.11) | 3.09 (1.00) | 2.73 (0.96) | 3.30 (0.90) | 3.10 (0.54) | 2.80 (0.75) |

| Completeness | 3.15 (1.51) | 2.85 (1.29) | 2.82 (1.27) | 2.45 (0.99) | 2.40 (1.43) | 3.00 (0.89) | 3.00 (1.10) |

| Correctness | 3.69 (1.26) | 3.54 (1.39) | 3.91 (1.00) | 3.73 (1.14) | 3.50 (1.20) | 3.60 (1.11) | 3.80 (1.17) |

| Satisfaction | 2.69 (1.32) | 2.77 (1.19) | 2.45 (1.08) | 2.36 (0.88) | 2.50 (1.36) | 2.80 (0.87) | 2.70 (0.64) |

Abstractive Summaries

In Figure 2 and Table 2, we report the average scores for abstractive summaries. In this case, IT5 models, which are the baseline, were evaluated as quite poor, while GPT3 and GPT4 performed very well in all the dimensions. On the basis of this evaluation, we decided for the second stage to keep GPT4 summaries, both in the flowing text and issue-based versions. We also kept IT5 as a baseline. We chose to omit GPT3, given its similarity to its successor, namely, GPT4.

| IT5Small | IT5Large | GPT3 | GPT4 | GPT3 item | GPT4 item | |

|---|---|---|---|---|---|---|

| Form | 1.75 (0.97) | 1.75 (1.30) | 4.12 (0.60) | 4.25 (0.66) | 3.12 (1.36) | 3.62 (1.32) |

| Completeness | 1.62 (1.32) | 1.50 (1.00) | 4.00 (0.71) | 4.00 (0.71) | 2.75 (1.20) | 3.75 (1.39) |

| Correctness | 1.62 (0.99) | 1.88 (1.54) | 4.25 (0.66) | 4.25 (0.66) | 3.38 (1.32) | 3.62 (1.41) |

| Satisfaction | 1.62 (1.32) | 1.50 (1.00) | 4.12 (0.33) | 4.00 (0.71) | 2.62 (1.11) | 3.38 (1.32) |

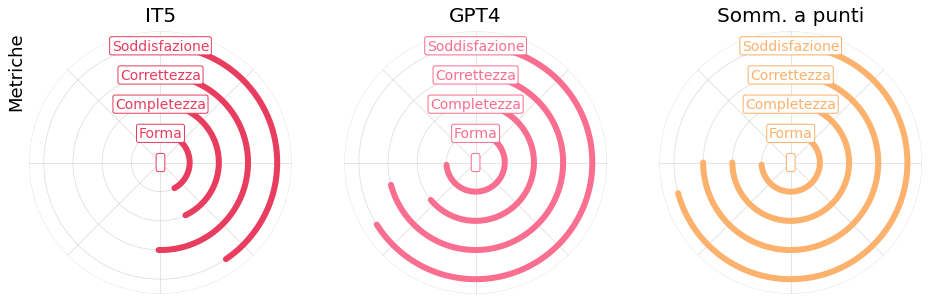

8.2 Second Evaluation: Abstractive Summaries

The second evaluation was focused on IT5Small, flowing-text GPT4, and issue-based GPT4. This evaluation involved around 80 experts, drawn from a pool of judges, lawyers, and others. Each evaluator assessed, for 5 decisions, the summaries produced by the 3 models.

We received on average 50 answers for each model. Figure 3 reports the average values and Table 3 reports average values and standard deviation.

| IT5 | GPT4 | GPT4 items | |

|---|---|---|---|

| Form | 2.11 (1.10) | 3.69 (1.06) | 3.69 (1.14) |

| Completeness | 2.15 (1.06) | 3.20 (1.25) | 3.75 (1.02) |

| Correctness | 2.51 (1.17) | 3.54 (1.15) | 3.75 (1.05) |

| Satisfaction | 2.03 (1.04) | 3.30 (1.32) | 3.54 (1.12) |

From Figure 3 it appears that GPT4 scored better than IT5. It also appears that the issue-based summary outperformed the flowing-text summary under both completeness, correctness, and general satisfaction. It can also be seen from Table 3 that there is relatively high dispersion in the assessments (according to the indicated standard deviation). We plan to study this aspect to understand whether it relates to the nature of cases, to the language used in the judicial opinions, or to idiosyncrasies of the evaluators.

9 Related Work

Since the focus, and the most significant results, of our work concern applying LLMs to the summarization task, the related work most relevant to our project concerns, on the one hand, the use of LLMs in the legal domain and, on the other, automated summarisation.

9.1 Large Language Models in the Law

Large language models (LLMs), such as BERT, GPT, or XLM-RoBERTa, have already demonstrated considerable potential in various legal tasks.

Notable areas for the deployment of LLMs have been judgement prediction and statutory reasoning. The study by [10] introduces legal prompt engineering (LPE) to enhance LLM performance in tasks involving predicting legal judgements. This method has proven effective across three multilingual datasets, highlighting the model’s potential in handling the complexity of legal language and reasoning across multiple sources of information. Another study by [11] investigates GPT-3’s capacity for statutory reasoning, revealing that dynamic few-shot prompting enables the model to achieve high accuracy and confidence in this task.

Advancements in prompting techniques have played a crucial role in the success of LLMs in legal reasoning tasks. The paper by [12] introduces Chain-of-Thought (CoT) prompts, which guide LLMs in generating coherent and relevant sentences that follow a logical structure, mimicking a lawyer’s analytical approach. The study demonstrates that CoT prompts outperform baseline prompts in the COLIEE entailment task based on Japanese Civil Code articles.

LLMs have also been employed to understand fiduciary obligations, as explored in [13]. This study employs natural language prompts derived from US court opinions, illustrating that LLMs can capture the spirit of a directive, thus facilitating more effective communication between AI agents and humans using legal standards.

The potential of LLMs in legal education has been examined in studies such as [14] and [15]. In [14], the authors task ChatGPT with writing law school exams without human assistance, revealing potential concerns and insights about LLM capabilities in legal assessment. On the other hand, the paper by [15] addresses the ethical use of AI language models like ChatGPT in law school assessments, proposing ways to teach students appropriate and ethical AI usage.

The role of LLMs in supporting law professors and providing legal advice has also been investigated. The study in [16] suggests that LLMs can assist law professors in administrative tasks and streamline scholarly activities.

Furthermore, LLMs have been explored as quasi-expert legal advice lawyers in [17], showcasing the possibility of using AI models to support individuals seeking affordable and prompt legal advice. The potential impact of LLMs on the legal profession has been a subject of debate, as discussed in [18]. This paper evaluates the extent to which ChatGPT can serve as a replacement for litigation lawyers by examining its drafting and research capabilities.

Finally, the study by [19] proposes a legal informatics approach to align AI with human goals and societal values. By embedding legal knowledge and reasoning in AI, the paper contributes to the research agenda of integrating AI and law more effectively. In conclusion, LLMs have shown promising results in various legal tasks, with the advancement of prompting techniques playing a crucial role in their success. However, challenges remain in ensuring the ethical use of LLMs and addressing their potential impact on the legal profession.

9.2 Legal Text Summarization

Summarisation of has been a forefront task in legal informatics for some years. In 2004 a seminal contribution [20] provided the extractive summarisation of a legal dataset of 188 judgements from the House of Lords Judgement (HOLJ) website from 2001–2003. However, only recently have researchers started to produce promising results, thanks to state-of-the-art NLP, machine learning techniques, and, lately, LLMs.

Existing research on legal summarization mostly applies extractive methods. A wide range of approaches to this effect exist, from classical algorithms [5, 7, 6] to domain-specific methods. Among the latter, there are works based on nature-inspired methods, i.e., algorithms emulating natural processes [21], using optimization approaches that adapt to challenging circumstances [22]; graph-based methods, where sentences are selected based on the construction and search over similarity graphs [7, 23, 24]; and citation-based methods relying upon the set of citing sentences within documents to build summaries [25]. Finally, there are also machine-learning-based models in which classifiers predict which sentences to include in the summary [26].

Kanapala et al. [22] focused on a domain-specific automatic summarization system based on a nature-inspired method. The authors framed legal document summarization as a binary optimization problem, utilizing statistical features such as sentence length, position, similarity, term frequency-inverse sentence frequency, and keywords. The authors used the gravitational search algorithm (GSA) as the optimization technique for generating summaries. GSA adjusted the weights assigned to sentence features, capturing the importance and relevance of sentences within legal documents. To evaluate their method, the authors compared it with other approaches, including genetic algorithms, particle swarm optimization, TextRank, latent semantic analysis (LSA), MEAD, SumBasic, and MS-Word summarizer. They utilized the FIRE-2014 dataset, which consisted of 1,000 Supreme Court judgements from 1950 to 1989. The proposed algorithm outperformed the other methods based on ROUGE evaluation metrics.

Merchant and Pande [27] presented an automated text summarization system designed to help lawyers and citizens conduct comprehensive research for their legal cases. The researchers used LSA, a natural language processing technique, to capture concepts within individual documents. Two approaches were used – a single-document untrained approach and a multi-document trained approach – depending on the type of case (criminal or civil). The data used in the study was collected from the Indian official government websites and included Supreme Court, High Court, and District Court cases. The evaluation of the model resulted in an average ROGUE-1 score of 0.58. The system received the approval of professional lawyers.

Licari et al. [28] introduce a method for automatically extracting legal holdings from Italian cases using Italian-LEGAL-BERT and present a benchmark dataset called ITA-CaseHold for Italian legal summarization. They introduced HM-BERT, an extractive summarization tool based on Italian-LEGAL-BERT. HM-BERT selects relevant sentences using a similarity function based on unigram and bigram overlap. The model achieved prominent results in terms of ROUGE scores, and the extracted holdings were validated by experts. The paper acknowledges limitations such as potential redundancy in sentence selection and the challenge of explaining HM-BERT’s decisions.

Recently, in connection with the availability of transformer models, some attempts at abstractive summarisation have been developed. Schraagen et al. [29] applied two abstractive models to a Dutch legal domain dataset and evaluated their performance using ROUGE scores and evaluation by legal experts. The study presents a hybrid model based on reinforcement learning and a transformer-based BART model trained on a large dataset of Dutch court judgements. The results show promising transferability of the models across domains and languages, with ROUGE scores comparable to state-of-the-art studies on English news articles. However, human evaluation shows that handwritten summaries are still perceived as more relevant and readable. Furthermore, summarisers struggle to include all necessary elements in the summary, leading to the omission of important details. The authors suggest that the abstractive summarisation process can be improved by incorporating domain-specific constraints, such as focusing on citations of legal sources and structuring summaries into facts, arguments, and decisions.

Prabhakar et al. [30] presented a method using T5 to generate abstractive summaries of Indian legal judgements. The system uses a dataset of 350 judgements of the Honourable Supreme Court of India, compiled with the assistance of a lawyer. The generated summaries are evaluated using the ROUGE score, with a Rouge-L precision of .

Feijo et al. [31] addressed the problem of “hallucination” in abstractive text summarisation, focusing specifically on legal texts. They proposed a novel method, called LegalSumm, which aimed to improve the fidelity and accuracy of the generated summaries. To achieve this, the authors created multiple “views” of the source text and trained summarisation models to generate independent versions of the summaries. They also introduced an entailment module to evaluate the fidelity of candidate summaries to the source text. The authors demonstrated the effectiveness of their approach by showing significant improvements in ROUGE scores across all evaluation metrics. As well as contributing to the field of legal summarisation, the study provides a basis for further advances in the production of reliable and accurate summaries.

Koniaris et al. [32] addressed the challenge of automatic summarization of Greek legal documents. To overcome the lack of suitable datasets in the Greek language, the authors developed a metadata-rich dataset of selected judgements from the Supreme Civil and Criminal Court of Greece, along with their reference summaries and category tags. They adopted state-of-the-art methods for abstractive (BERT) and extractive (LexRank) summarization and conducted a comprehensive evaluation using both human and automatic metrics, such as ROUGE. The results showed that extractive methods had average performance, while abstractive methods generated moderately fluent and coherent text but received low scores in relevance and consistency metrics. They identified the need for better metrics to evaluate legal document summaries’ coherence, relevance, and consistency. The authors suggested future research directions involving better datasets and improved evaluation metrics, as well as exploring advanced techniques such as deep learning with various neural network architectures to enhance the quality of generated summaries.

Huang et al. [33] proposed a two-stage legal judgement summarization model to address the challenges posed by lengthy legal judgements and their technical terms. They leveraged raw legal judgements with varying granularities as input information and treated them as sequences of sentences. Key sentence sets were selected from the full texts to serve as the input corpus for the summary generation. Additionally, the authors incorporated an attention mechanism by extracting keywords related to technical terms and specific topics in the legal texts, which were integrated into the summary-generation model. Experimental evaluations on the CAIL2020 and LCRD datasets demonstrated that their model, based on recurrent neural networks and attention mechanisms, outperformed baseline models (Lead-3, TextRank, and others), achieving an overall improvement of 0.19–0.41 in ROUGE scores. The results indicated that their method effectively captured essential and relevant information from lengthy legal texts and generated improved legal judgement summaries.

10 Conclusion

We have presented some preliminary results obtained in the early development of the PRODIGIT project, a tax law initiative aimed at supporting judges, lawyers, and other legal practitioners. We have focused on the summarisation task, one of the main goals of PRODIGIT, which aims to support the summarisation of all Italian tax law decisions.

We first introduced tax law adjudication in the Italian legal system, discussed the significance of summarisation for judges and practitioners, and described the database we used for our experiments. We then introduced the tools and approaches we used in our experiments, which range from single special-purpose NLP tools, based on classical statistical approaches, to the most recent LLMs. We described our experiments with regard to all such tools, providing examples of the obtained outputs and discussing the limitations and potentialities of each approach. In particular, we provided an in-depth account of our use of generative LLMs, which yielded clearly superior results. In this regard, we listed the prompts used to obtain such results. The most interesting approach we developed is that of “issue-based summarisation”, i.e., outlining the legal issues examined by the judges and the corresponding legal criteria (principles). Issue-based summarisation was complemented by the extraction of issue-relative keywords and textual fragments. For this purpose an appropriate prompt had to be devised to direct generative tools toward providing legally meaningful information. We think that this is the most significant development our work provides in relation to the literature cited in Section 9.

We have submitted the results of our experiments to an extensive evaluation by legal experts, from which emerged a clear preference for the outcomes delivered by generative tools. In particular, the issue-based summarisation delivered by GPT4 appeared to be the preferred approach, considering its linguistic quality, completeness, and correctness, as well as general satisfaction. This comparative assessment is also a significant innovative contribution to the theory and practice of legal summarisation, which cannot avoid facing the challenge of LLMs.

We think that some interesting lessons emerge from our experience.

The first takeaway is that the most advanced LLMs can provide very good results in automated summarisation, clearly outperforming earlier NLP tools. Different kinds of summaries can be obtained by carefully designing the corresponding prompt. We have observed that high-quality outcomes can be obtained even without fine-tuning large LLMs. The extent to which fine-tuning can provide improvements in performance is an important issue for further research.

The second takeaway is that extensive human evaluation is needed to assess the outcomes of summarisation in the legal domain. As noted, we submitted the results of our experiment to expert evaluation, based on questionnaires reviewed by an ethical committee. This evaluation provided us with a clear comparative assessment of the summaries, on which the implementation of summarisation within PRODIGIT will be based. We do not think that, at the state of the art, any automated methods can be deployed to test the quality of summarisation, particularly in the abstractive case. In addition to the two-step formal evaluation described in Section 8, in multiple round we submitted our preliminary results to the judgement of expert tax lawyers involved in the project. This enabled us to refine our methods, and in particular to refine our prompts in order to approximate the desired outcomes before the formal evaluation.

A third takeaway is that summarisation provides different satisfactory outcomes with regard to different input texts. In fact, Italian tax law decisions very greatly in length, in the language used, and in the clarity of reasoning. In some cases, making sense of their content may be a challenge for human readers; thus it is not surprising that automated summarisers give different results. Thus, it is important to preserve convenient human supervision over the outcomes of automated summarization. Under the PRODIGIT project, an application is being developed to enable expert lawyers to review and possibly revise the automatically generated summaries. Their feedback will support further improvement of automated summarisation.

Based on the successful experiments described in this paper, summarisation of the PRODIGIT project will take steps toward putting out publicly available results.

The idea is to include the automatically generated summaries in a publicly accessible database of all Italian tax law decisions: we first provide the summaries of decisions in the registration-tax area will, and if the public’s response is positive, the exercise will be extended to all domains of tax law.

We are also experimenting with using summaries – in the issue-based versions – for the purpose of indexing and searching the case law. The extracted information – legal issues and keywords – are being used to construct a conceptual graph through which to access the case-law database.

References

- \bibcommenthead

- Bommasani et al. [2022] Bommasani, R., Hudson, D.A., Others: On the opportunities and risks of foundation models. Arxiv (2022)

- OpenAI [2023] OpenAI: GPT-4 Technical Report (2023)

- Wolfram [2023] Wolfram, S.: What Is ChatGPT, (2023)

- Bender et al. [2021] Bender, E.M., Gebru, T., McMillan-Major, A., Shmitchell, S.: On the dangers of stochastic parrots: Can language models be too big? In: FAccT ’21, March 3–10, 2021, Virtual Event, Canada, (2021)

- Gong and Liu [2001] Gong, Y., Liu, X.: Generic text summarization using relevance measure and latent semantic analysis. In: Proceedings of the 24th Annual International ACM SIGIR Conference on Research and Development in Information Retrieval. SIGIR ’01, pp. 19–25. Association for Computing Machinery, New York, NY, USA (2001). https://doi.org/10.1145/383952.383955

- Brin and Page [1998] Brin, S., Page, L.: The anatomy of a large-scale hypertextual web search engine. Computer Networks and ISDN Systems 30(1-7), 107–117 (1998) https://doi.org/10.1016/s0169-7552(98)00110-x

- Erkan and Radev [2004] Erkan, G., Radev, D.R.: LexRank: Graph-based lexical centrality as salience in text summarization. Journal of Artificial Intelligence Research 22, 457–479 (2004) https://doi.org/10.1613/jair.1523

- Sarti and Nissim [2022] Sarti, G., Nissim, M.: IT5: Large-scale Text-to-text Pretraining for Italian Language Understanding and Generation (2022)

- Brown et al. [2020] Brown, T.B., Mann, B., Ryder, N., Subbiah, M., Kaplan, J., Dhariwal, P., Neelakantan, A., Shyam, P., Sastry, G., Askell, A., Agarwal, S., Herbert-Voss, A., Krueger, G., Henighan, T., Child, R., Ramesh, A., Ziegler, D.M., Wu, J., Winter, C., Hesse, C., Chen, M., Sigler, E., Litwin, M., Gray, S., Chess, B., Clark, J., Berner, C., McCandlish, S., Radford, A., Sutskever, I., Amodei, D.: Language Models are Few-Shot Learners (2020)

- Trautmann et al. [2022] Trautmann, D., Petrova, A., Schilder, F.: Legal prompt engineering for multilingual legal judgement prediction. arXiv preprint arXiv:2212.02199 (2022)

- Blair-Stanek et al. [2023] Blair-Stanek, A., Holzenberger, N., Van Durme, B.: Can gpt-3 perform statutory reasoning? arXiv preprint arXiv:2302.06100 (2023)

- Yu et al. [2022] Yu, F., Quartey, L., Schilder, F.: Legal prompting: Teaching a language model to think like a lawyer. arXiv preprint arXiv:2212.01326 (2022)

- Nay [2023] Nay, J.J.: Large language models as fiduciaries: A case study toward robustly communicating with artificial intelligence through legal standards. arXiv preprint arXiv:2301.10095 (2023)

- Choi et al. [2023] Choi, J.H., Hickman, K.E., Monahan, A., Schwarcz, D.: Chatgpt goes to law school. Available at SSRN (2023)

- Hargreaves [2023] Hargreaves, S.: ‘words are flowing out like endless rain into a paper cup’: Chatgpt & law school assessments. The Chinese University of Hong Kong Faculty of Law Research Paper (2023-03) (2023)

- Oltz [2023] Oltz, T.P.: Chatgpt, professor of law. U. Ill. JL Tech. & Pol’y, 207 (2023)

- Macey-Dare [2023] Macey-Dare, R.: Chatgpt and generative ai systems as corporate ethics advisors. Available at SSRN (2023)

- Iu and Wong [2023] Iu, K.Y., Wong, V.M.-Y.: Chatgpt by openai: The end of litigation lawyers? Available at SSRN (2023)

- Nay [2022] Nay, J.J.: Law informs code: A legal informatics approach to aligning artificial intelligence with humans. Nw. J. Tech. & Intell. Prop. 20, 309 (2022)

- Grover et al. [2004] Grover, C., Hachey, B., Hughson, I.: The holj corpus. supporting summarisation of legal texts. In: Proceedings of the 5th International Workshop on Linguistically Interpreted Corpora, pp. 47–54 (2004)

- Yang [2014] Yang, X.-S.: Introduction to algorithms. In: Nature-Inspired Optimization Algorithms, pp. 1–21. Elsevier, ??? (2014)

- Kanapala et al. [2019] Kanapala, A., Jannu, S., Pamula, R.: Summarization of legal judgments using gravitational search algorithm. Neural Computing and Applications 31(12), 8631–8639 (2019) https://doi.org/10.1007/s00521-019-04177-x

- Kim et al. [2013] Kim, M.-Y., Xu, Y., Goebel, R.: Summarization of legal texts with high cohesion and automatic compression rate. In: New Frontiers in Artificial Intelligence, pp. 190–204. Springer, ??? (2013). https://doi.org/10.1007/978-3-642-39931-2_14

- Duan et al. [2019] Duan, X., Zhang, Y., Yuan, L., Zhou, X., Liu, X., Wang, T., Wang, R., Zhang, Q., Sun, C., Wu, F.: Legal summarization for multi-role debate dialogue via controversy focus mining and multi-task learning. In: Proceedings of the 28th ACM International Conference on Information and Knowledge Management. CIKM ’19, pp. 1361–1370. Association for Computing Machinery, New York, NY, USA (2019). https://doi.org/10.1145/3357384.3357940

- Galgani et al. [2015] Galgani, F., Compton, P., Hoffmann, A.: Summarization based on bi-directional citation analysis. Information Processing & Management 51(1), 1–24 (2015) https://doi.org/%****␣main.bbl␣Line␣400␣****10.1016/j.ipm.2014.08.001

- Zhong et al. [2019] Zhong, L., Zhong, Z., Zhao, Z., Wang, S., Ashley, K.D., Grabmair, M.: Automatic summarization of legal decisions using iterative masking of predictive sentences. In: Proceedings of the Seventeenth International Conference on Artificial Intelligence and Law. ICAIL ’19, pp. 163–172. Association for Computing Machinery, New York, NY, USA (2019). https://doi.org/10.1145/3322640.3326728

- Merchant and Pande [2018] Merchant, K., Pande, Y.: NLP based latent semantic analysis for legal text summarization. In: 2018 International Conference on Advances in Computing, Communications and Informatics (ICACCI), pp. 1803–1807 (2018). https://doi.org/10.1109/ICACCI.2018.8554831

- Licari et al. [2023] Licari, D., Bushipaka, P., Marino, G., Comandé, G., Cucinotta, T.: Legal holding extraction from italian case documents using italian-legal-bert text summarization. In: Nineteenth International Conference on Artificial Intelligence and Law (ICAIL 2023), p. 9. ACM, Braga, Portugal (2023)

- Schraagen et al. [2022] Schraagen, M., Bex, F., Van De Luijtgaarden, N., Prijs, D.: Abstractive summarization of Dutch court verdicts using sequence-to-sequence models. In: Proceedings of the Natural Legal Language Processing Workshop 2022, pp. 76–87. Association for Computational Linguistics, Abu Dhabi, United Arab Emirates (Hybrid) (2022). https://aclanthology.org/2022.nllp-1.7

- Prabhakar et al. [2022] Prabhakar, P., Gupta, D., Pati, P.B.: Abstractive summarization of indian legal judgments, pp. 256–261. IEEE, ??? (2022). https://doi.org/10.1109/OCIT56763.2022.00056 . https://ieeexplore.ieee.org/document/10053815/

- de Vargas Feijo and Moreira [2023] Vargas Feijo, D., Moreira, V.P.: Improving abstractive summarization of legal rulings through textual entailment. Artificial Intelligence and Law 31, 91–113 (2023) https://doi.org/10.1007/s10506-021-09305-4

- Koniaris et al. [2023] Koniaris, M., Galanis, D., Giannini, E., Tsanakas, P.: Evaluation of automatic legal text summarization techniques for greek case law. Information 14(4) (2023) https://doi.org/10.3390/info14040250

- Huang et al. [2023] Huang, Y., Sun, L., Han, C., Guo, J.: A high-precision two-stage legal judgment summarization. Mathematics 11(6) (2023) https://doi.org/10.3390/math11061320

Acknowledgments

This work was developed within the scope of the PRO.DI.GI.T project (Project for Innovation in Tax Justice, with the support of digital technologies and AI – Progetto per l’innovazione della Giustizia Tributaria, con il supporto della tecnologia digitale e dell’intelligenza artificiale) proposed and endorsed by the Presidency Council of Tax Justice (Consiglio di Presidenza della Giustizia Tributaria - CPGT) and the Ministry of Economy and Finance (Ministero dell’Economia e delle Finanze - MEF). We gratefully acknowledge SOGEI for its support and cooperation during the project.

Appendix A Appendix: Prodigit Summaries

In the following, we present the text related to our running example, namely, Decision No. 7683 of 14 September 2022 issued by the Court of Second Instance of Sicily (see Section 4.2).

A.1 Original Text

Development of the Proceedings

With separate judgments issued by the Provincial Tax Commission of Messina, the appeals filed by respondent_1 were accepted, respectively against the notice of tax assessment and imposition of sanctions with which the office had determined a higher registration tax of € 15,890.00, plus interest and penalties following the revocation of tax benefits for the purchase of the first home, relating to the award of the property located in place_1, address_1, in the land registry at folio 222, part. 87 sub 9; and against the notice of recovery of the substitute tax on the related mortgage transaction (at the ordinary rate of 2% instead of the reduced rate of 0.25%). The assessment originated from the finding that the taxpayer had actually previously purchased a separate residential property in the NCEU of place_1 at fol. 216, part. 115 sub 43, category A/4; so he would not have been in the condition of not being the exclusive owner or in communion with his spouse, of the property rights on another dwelling house. The first judge had annulled the contested acts, starting from the consideration that the “first home” benefit - governed by article 1 of the tariff - first part, note II bis, attached to the Presidential Decree no. 131/86 - allowed the appellant to benefit from the tax benefit (consisting in the application of the registration tax with the rate of 2% instead of 9%), since the appellant was indeed the owner of another real estate unit, purchased with a deed of sale registered in place_2 on 19.03.2003 at no. 277, but the same property was to be considered unsuitable for the housing needs of the appellant and his family, due to its consistency and intrinsic characteristics. Against these decisions, the second of which was consequential to the first, the office filed an appeal, complaining of their incorrectness both because the pre-acquired property was still classified as a residential category, and because its unsuitability could not be considered based on the simple assertions of the appellant, regarding the alleged size of 18 square meters, contradicted by the attached registry extract. Respondent_1 appeared in both judgments, contesting the appeal filed, for which he requested dismissal, producing extensive case law together with a sworn technical consultancy of the party. Therefore, at the hearing of 14/9/2022, duly scheduled, the two connected proceedings were joined and at the end, the commission decided as per the device.

Grounds for the Decision