Matrix Completion When Missing Is Not at Random and Its Applications in Causal Panel Data Models 111This research was supported by NSF Grants DMS-2015285 and DMS-2052955, and NIH Grant R01-HG01073.

Abstract

This paper develops an inferential framework for matrix completion when missing is not at random and without the requirement of strong signals. Our development is based on the observation that if the number of missing entries is small enough compared to the panel size, then they can be estimated well even when missing is not at random. Taking advantage of this fact, we divide the missing entries into smaller groups and estimate each group via nuclear norm regularization. In addition, we show that with appropriate debiasing, our proposed estimate is asymptotically normal even for fairly weak signals. Our work is motivated by recent research on the Tick Size Pilot Program, an experiment conducted by the Security and Exchange Commission (SEC) to evaluate the impact of widening the tick size on the market quality of stocks from 2016 to 2018. While previous studies were based on traditional regression or difference-in-difference methods by assuming that the treatment effect is invariant with respect to time and unit, our analyses suggest significant heterogeneity across units and intriguing dynamics over time during the pilot program.

Keywords: Matrix completion; Missing not at random (MNAR); Weak signal-to-noise ratio; Multiple treatments; Tick size pilot program

1 Introduction

The problem of noisy matrix completion in which we are interested in reconstructing a low-rank matrix from partial and noisy observations of its entries arises naturally in numerous applications. It has attracted a considerable amount of attention in recent years, and a lot of impressive results have been obtained from both statistical and computational perspectives. See, e.g., Candes and Plan, (2010); Mazumder et al., (2010); Koltchinskii et al., (2011); Negahban and Wainwright, (2012); Chen et al., 2019a ; Chen et al., 2020b ; Jin et al., (2021); Xia and Yuan, (2021); Bhattacharya and Chatterjee, (2022) among many others. A common and crucial premise underlying these developments is that observations of the entries are missing at random. Although this is a reasonable assumption for some applications, it could be problematic for many others. In the past several years, there has been growing interest to investigate how to deal with situations where missing is not at random and to what extent the techniques and insights that are initially developed assuming missing at random can be extended to these cases. See, e.g. Agarwal et al., (2020, 2021); Athey et al., (2021); Bai and Ng, (2021); Chernozhukov et al., (2021); Cahan et al., (2023); Xiong and Pelger, (2023) among others.

This fruitful line of research is largely inspired by the development of synthetic control methods in causal inference. See, e.g., Abadie and Gardeazabal, (2003); Abadie et al., (2010); Abadie, (2021). The close connection between noisy matrix completion and synthetic control methods for panel data was first made formal by Athey et al., (2021) who showed that powerful matrix completion techniques such as nuclear norm regularization can be very useful for many causal panel data models where missing is not at random. It also helps bring together two complementary perspectives of noisy matrix completion: one focuses on statistical inferences assuming a strong factor structure and the other aims at recovery guarantees with minimum signal strength requirement. The main objective of this work is to further bridge the gap between these two schools of ideas and develop a general and flexible inferential framework for matrix completion when missing is not at random and without the requirement of strong factors.

In particular, we shall follow Athey et al., (2021) and investigate how the technique of nuclear norm regularization can be used to infer individual treatment effects under a variety of missing mechanisms. One of the key observations to our development is the fact that if the number of missing entries is sufficiently small when compared to the panel size, then they can be estimated well even when missing is not at random. For more general missing patterns with an arbitrary proportion of missingness, we can judicially divide the missing entries into smaller groups and leverage this fact by applying the nuclear norm regularization to a submatrix with a small number of missing entries. This is where our approach differs from that of Athey et al., (2021) who suggest applying the nuclear norm regularized estimation to the full matrix. We shall show that subgrouping is essential in producing more accurate estimates and more efficient inferences about individual treatment effects. It is worth noting that it is computationally more efficient to estimate all missing entries together, as suggested by Athey et al., (2021). But estimating too many missing entries simultaneously can be statistically suboptimal. In a way, our results suggest how to trade-off between the computational cost and statistical efficiency.

Our proposal of subgrouping is similar in spirit to the approach taken by Agarwal et al., (2021) who suggested estimating the missing entries one at a time. For estimating a single missing entry, they propose a matching scheme that constructs multiple “synthetic” neighbors and averages the observed outcomes associated with each synthetic neighbor. Separating the observations into different sets of neighbors, however, could lead to a loss in efficiency. For example, when estimating the mean of an matrix with one missing entry, the estimation error of the approach from Agarwal et al., (2021) for the missing entry converges at the rate of , which is far slower than the rate of attained by our method.

Furthermore, we show that, with appropriate debiasing, our proposed estimate is asymptotically normal even with fairly weak signals. More specifically, the asymptotic normality holds if where is the smallest nonzero singular value of the mean of an matrix and is the variance of the observed entries. Our development builds upon and complements a series of recent works that show that statistical inference for matrix completion is possible with a low signal-to-noise ratio when the data are missing uniformly at random. See, e.g., Chen et al., 2019a ; Chen et al., 2020b ; Xia and Yuan, (2021). Our results also draw an immediate comparison with the recent works by Bai and Ng, (2021); Cahan et al., (2023) who developed an inferential theory for the asymptotic principle component (APC) based approaches when the signal is much stronger, e.g., . It is worth pointing out that the nuclear norm regularization and APC-based approach each has its own merits and requires different treatment. For example, APC-based methods usually assume that the factors are random and impose moment conditions to ensure that the factor structure is strong and identifiable, whereas our development assumes that the factors are deterministic but incoherent and allows for weaker signals.

Our work is motivated by a number of recent studies on the Tick Size Pilot Program, an experiment conducted by the Security and Exchange Commission (SEC) to evaluate the impact of widening the tick size on the market quality of small and illiquid stocks from 2016 to 2018. See, e.g., Albuquerque et al., (2020); Chung et al., (2020); Werner et al., (2022). The pilot consisted of three treatment groups with a control group: 1) The first treatment group was quoted in $0.05 increments but still traded in $0.01 increments (only Q rule), 2) The second treatment group was quoted and traded in $0.05 increments (Q+T rule), 3) The third treatment group was quoted and traded in $0.05 increments, and also subject to the trade-at rule (Q+T+TA rule). The trade-at rule, in general, prevents price matching by exchanges that are not displaying the best price. The control group was quoted and traded in $0.01 increments. Previous studies (see, e.g., Chung et al.,, 2020) on the effects of the quote rule (Q), trade rule (T), and trade rule (TA) on the liquidity measure are based on traditional regression or difference-in-difference methods and assume that the treatment effect is invariant with respect to time and unit. As we shall demonstrate, this assumption is problematic for the Tick Size Pilot Program data and there is significant heterogeneity in the treatment effect across both time and units. Indeed, more insights can be obtained using a potential outcome model with interactive fixed effects to capture such heterogeneity. To do so, we extend our methodology from estimating a single matrix to the simultaneous completion of multiple matrices, accounting for the multiple potential situations.

The remainder of this paper is organized as follows. Section 2 introduces the method of using the nuclear norm penalized estimation when missing is not at random and provides the convergence rates of the estimator. Section 3 discusses how to reduce bias and provides inferential theory using the debiased estimator. Section 4 shows how our proposed methodology can be applied to infer the treatment effect in the Tick Size Pilot Program and presents the empirical findings of our analysis. Section 5 examines the finite sample performance of our estimators using simulation studies. Finally, we conclude with a few remarks in Section 6. All proofs are relegated to the Appendix due to the space limit.

In what follows, we use , , and to denote the matrix Frobenius norm, spectral norm, and nuclear norm, respectively. In addition, denotes the entrywise norm, and the largest norm of all rows of the matrix, i.e., . For any vector , denotes its norm. For any set , is the number of elements in . We use to denote the Hadamard product or the entry-by-entry product between matrices of conformable dimensions. means for some constant and means for some constant . means that both and are bounded. indicates for some sufficiently small constant and indicates for some sufficiently small constant . In addition, .

2 Noisy Matrix Completion

Consider a panel data setting where is a matrix of rank (). We use as the cross-section index and as the time index. Following the convention of the matrix completion literature, we shall assume that the singular vectors of are incoherent in that there is a such that , where and denote the left and right singular vectors of , respectively. The incoherence condition requires the singular vectors to be de-localized, in the sense that entries are not dominated by a small number of rows or columns.

Instead of , we observe a subset of the entries of where is a noise matrix whose entries are independent and identically distributed zero-mean, sub-Gaussian random variable, i.e., , , and some constant . Let indicate the observed entries: if and only if is observed. The goal of noisy matrix completion is to estimate from . A popular approach to do so is the nuclear norm penalization:

where is a tuning parameter. The properties of are by now well understood in the case of missing completely at random, especially when the entries of are independently sampled from a Bernoulli distribution. See, e.g., Koltchinskii et al., (2011); Chen et al., 2020b . Instead, we are interested here in the situation where is not random.

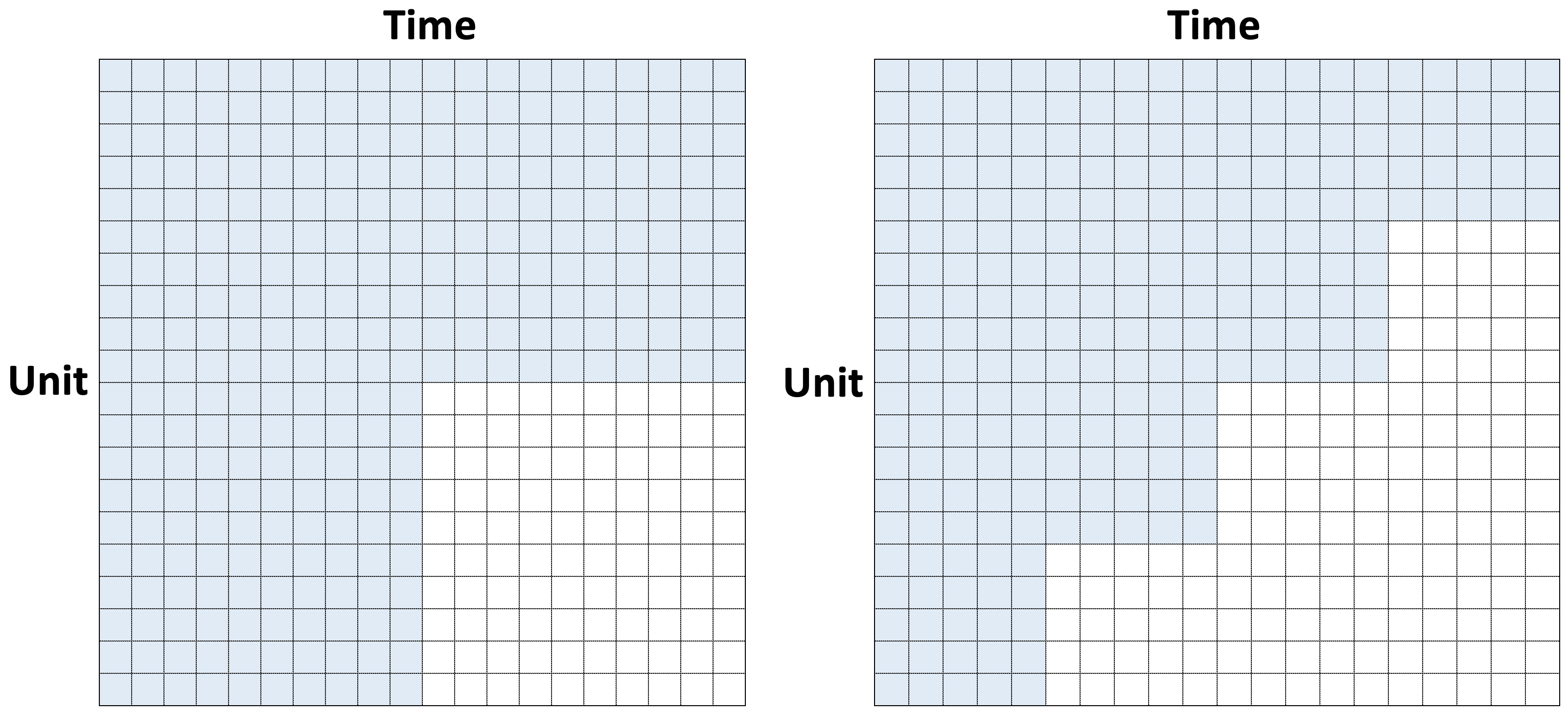

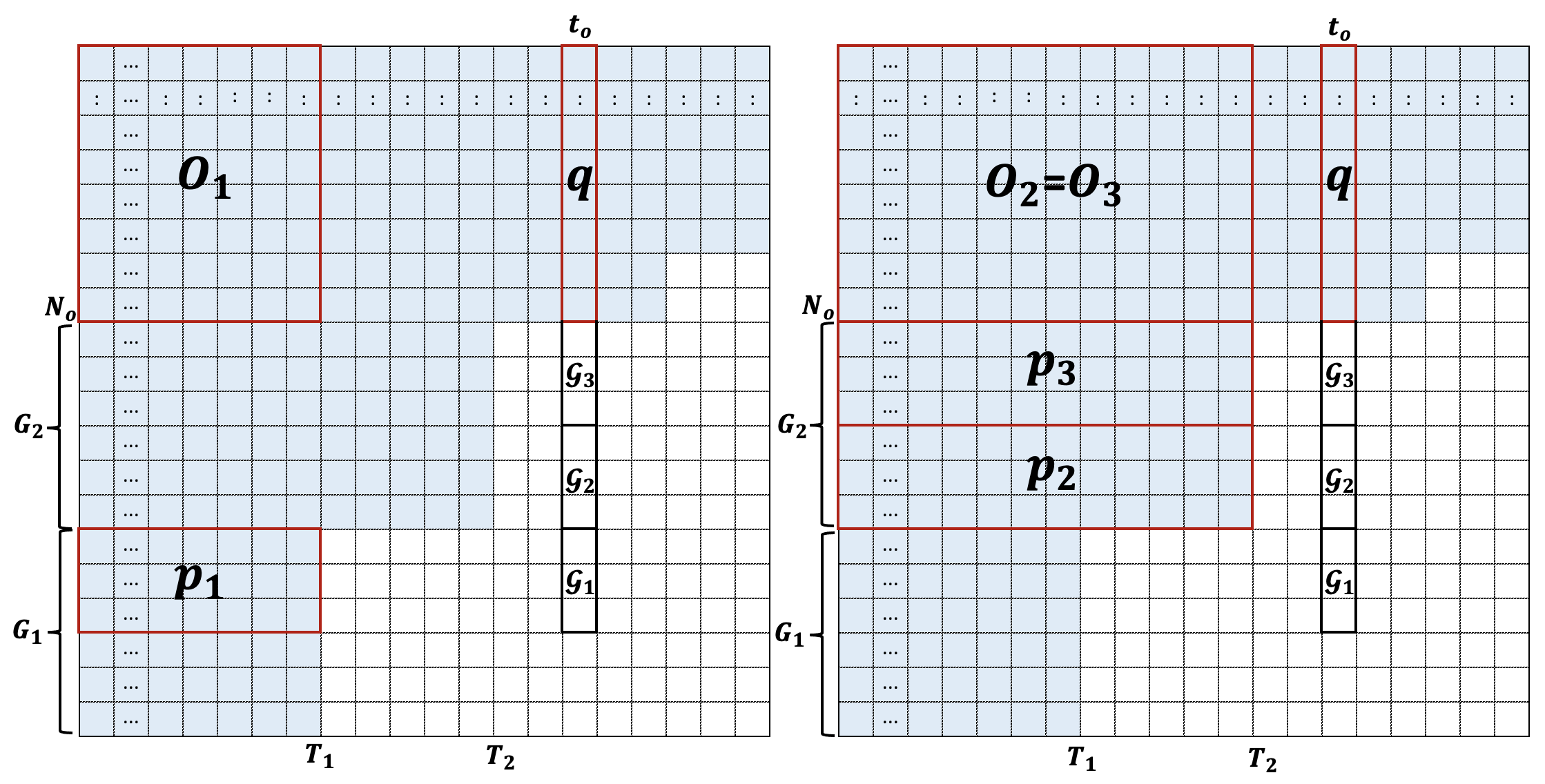

Situations when missing is not at random arise naturally in many causal panel models. Consider, for example, the evaluation of a program that takes effect after time for the last units. If is the potential outcome under the control, then we do not have observations of its entries for and , e.g., , yielding a block missing pattern as shown in the left panel of Figure 1. A more general setting that often arises in causal panel data is the staggered adoption where units may differ in the time they are first exposed to the treatment, yielding a missing pattern as shown in the right panel of Figure 1. See Athey et al., (2021); Agarwal et al., (2021) for other similar missing patterns that are common in the context of recommendation systems and A / B testing.

Note that if the entries are observed uniformly at random, then

for sufficiently large and . The right-hand side is minimized by , which justifies as a plausible estimate of . This intuition, however, no longer applies when is not random and has more structured patterns. Our proposal to overcome this problem is dividing the missing entries into smaller groups and estimating each group via nuclear norm regularization. The main inspiration behind our method is the observation that is a good estimate of when there are only a few missing entries, even if they are missing not at random.

It is instructive to start with a single treated period, e.g., . In this case, the number of missing entries is . Denote by and the largest and smallest nonzero singular value of , respectively, and its condition number. The following theorem provides bounds for the estimation error of .

Theorem 2.1.

Assume that

-

(i)

;

-

(ii)

;

-

(iii)

.

Then, with probability at least , we have

for some absolute constant .

Some immediate remarks are in order. Consider the situation where , and . Ignoring the logarithmic term, the signal-to-noise ratio requirement given by Assumption (i) reduces to which is significantly weaker than those in the existing literature. More specifically, if there is a single missing entry, e.g., , Agarwal et al., (2021) suggest to partition the submatrix into smaller matrices. In particular, their Theorem 2 states that the best estimation error for their estimate is given by

by setting . In contrast, under the assumptions of Agarwal et al., (2021), are bounded and hence the convergence rate of our estimator is

Theorem 2.1 serves as our building block for dealing with more general and common missing patterns, which we shall now discuss in detail.

Single Treated Period.

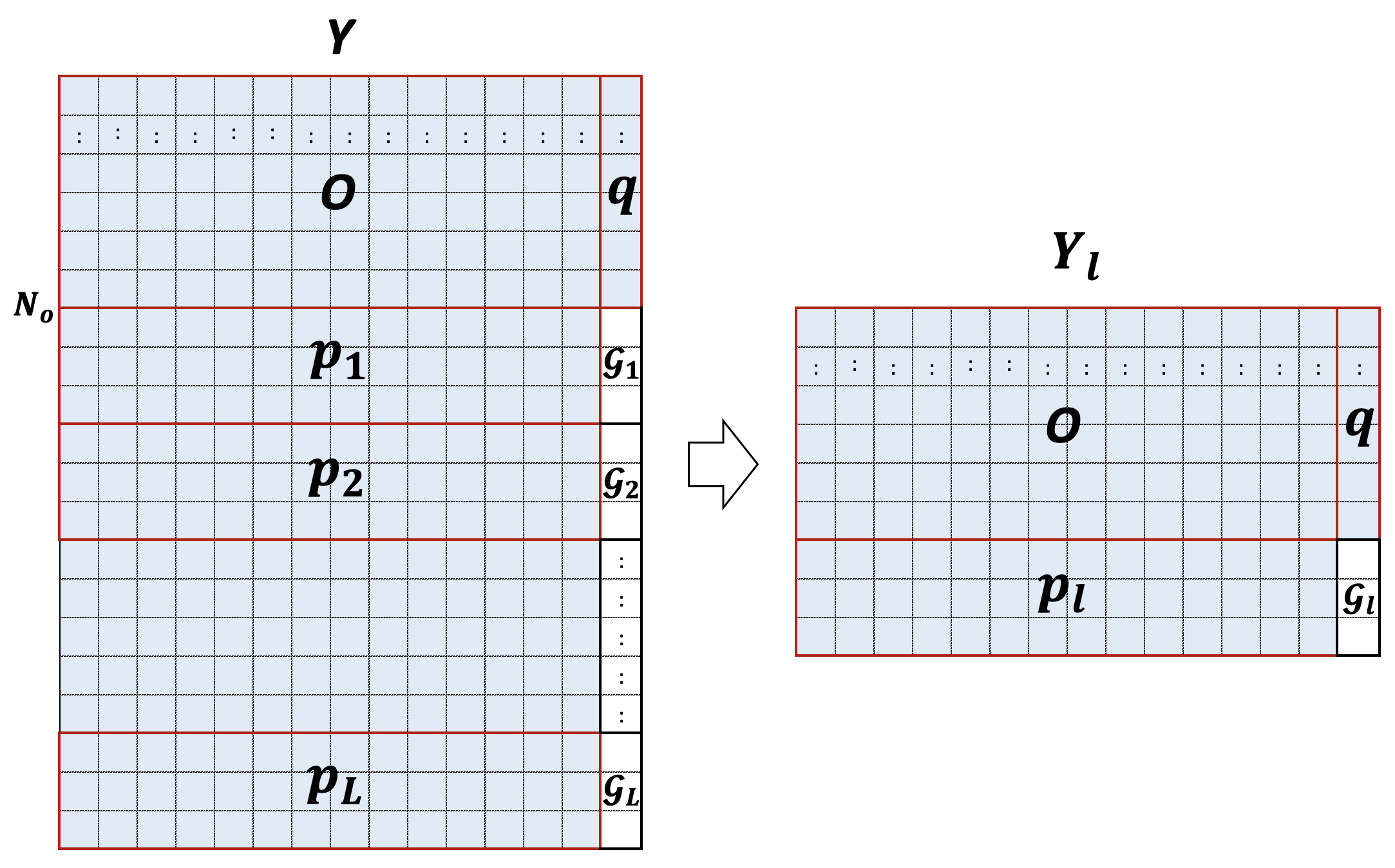

Note that Assumption (iii) of Theorem 2.1 restricts the number of missing entries not to be large compared to and . In particular, if and , then it requires that . To deal with a larger number of missing entries, we shall leverage this result by splitting the missing entries into small groups and estimating them separately, as illustrated in Figure 2.

Specifically, we split the missing entries into small groups, denoted by , and construct the submatrices as illustrated in Figure 2. For each , we estimate , the corresponding submatrix of , using the nuclear norm penalization:

| (2.1) |

where and is the corresponding submatrix of . We shall then assemble these estimated submatrices into an estimate of . Note that each missing entry appears in one and only one of the submatrices and can therefore be estimated accordingly. The entries from in Figure 2, e.g., the principle submatrix of , on the other hand, are estimated for all groups. We can estimate these entries by averaging all of these estimates. Let the smallest nonzero singular value of be , where is the submatrix of corresponding to . Denote by and the -th row of and -th row of , respectively. We can then derive the following bounds from Theorem 2.1.

Corollary 2.2.

Assume that

-

(i)

;

-

(ii)

;

-

(iii)

, ;

-

(iv)

There are constants such that

where and are the largest and smallest singular value of , respectively.

Then, with probability at least , we have

for some absolute constant .

The main difference from Theorem 2.1 lies in Assumptions (iii) and (iv) of Corollary 2.2. Assumption (iii) specifies how large a block can be. In principle, we can always take , that is, recovering one entry at a time so that this condition is trivially satisfied with sufficiently large and . However, there could be enormous computational advantages in creating groups as large as possible because the number of s that need to be computed decreases with increasing group size.

Assumption (iv) can be viewed as an incoherence condition to ensure that the singular vectors of are not dominated by either the treated or untreated units. It is easy to see that when there are few missing entries, e.g., , the condition is satisfied by virtue of the incoherence of s. In general, if is exchangeable or if the treated units are uniformly selected, then this condition is satisfied with high probability, at least for sufficiently large , since by means of matrix concentration inequalities (see, e.g., Tropp et al.,, 2015).

Single Treated Unit.

A similar estimating strategy can also be used to deal with a single treated unit. Without loss of generality, let . Then the fully observed submatrix is . As in the case of a single treated period, we split the missing entries into smaller groups, denoted by , by periods, and estimate them separately as before. Similar to Theorem 2.2, we have the following bounds for the resulting estimate.

Corollary 2.3.

Assume that

-

(i)

;

-

(ii)

;

-

(iii)

, ;

-

(iv)

There are constants such that

Then, with probability at least , we have

for some absolute constant .

General Block Missing Pattern.

We can also apply the grouping and estimating procedure to general block missing structures such as that depicted in the left panel of Figure 1, e.g., , by estimating missing entries one period at a time (or one unit at a time). Denote by the groups of missing units (or periods). The following result again follows from Theorem 2.1:

Corollary 2.4.

Assume that

-

(i)

;

-

(ii)

;

-

(iii)

, ;

-

(iv)

There are constants such that

Then, with probability at least , we have

for some absolute constant .

It is worth noting that both Corollary 2.2 and Corollary 2.3 can be viewed as special cases of Corollary 2.4. It is also of interest to compare the rates of convergence with those of Athey et al., (2021). Athey et al., (2021) considered a direct application of the nuclear norm penalized estimation to the full matrix. Their Theorem 2 states that

ignoring the logarithmic factors and , , and . In other words, the estimate could be inconsistent when . On the other hand, the convergence rate of our estimator is given by

up to a logarithmic factor when we assume . Hence, our estimator is consistent as long as diverges. Furthermore, the simulation results in Section 5 also show that applying the nuclear norm penalized estimation to the submatrix indeed performs much better than applying it to the full matrix as long as and are not too small.

Staggered Adoption.

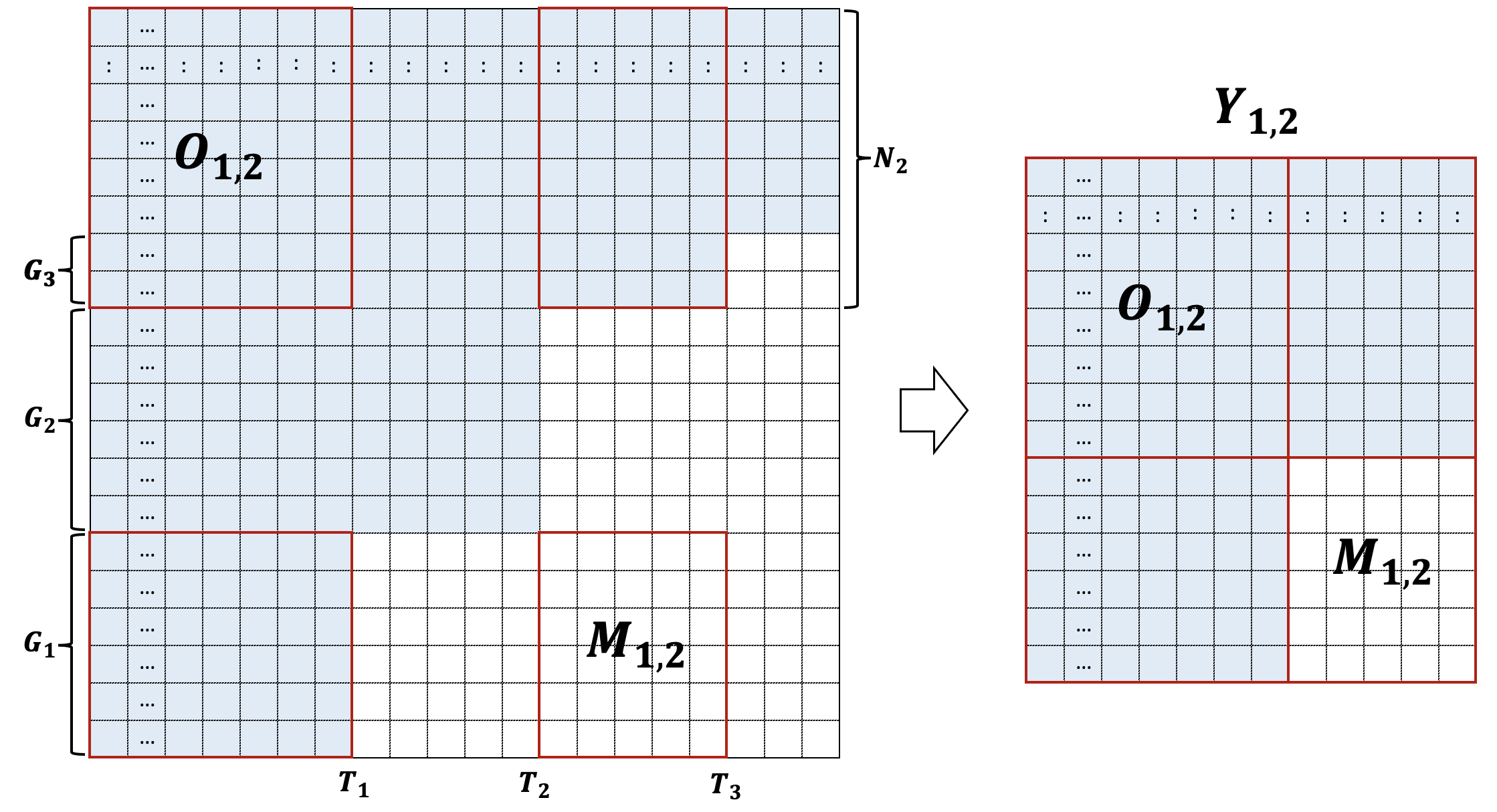

More generally, we can take advantage of our estimation strategy for staggered adoption where there are number of adoption time points, says , and number of corresponding groups of treated units, says . That is, for each , the units in adopt the treatment in the time period . We can utilize the strategy for block missing patterns to estimate the missing entries. More specifically, denote by the submatrix with missing entries corresponding to units in and time periods in , with the convention that , where . To estimate these missing entries, we can assemble a submatrix, denoted by , with units untreated prior to and time periods in , as well as units in and time periods in . As shown in Figure 3, is now the missing block of , and can be estimated as described in the previous case.

Denote by the groups for missing units in such as , the number of units that are untreated prior to , and the smallest singular value of the submatrix . The performance of the resulting estimate is given by Corollary 2.5.

Corollary 2.5.

Assume that

-

(i)

;

-

(ii)

;

-

(iii)

, ;

-

(iv)

There are constants such that

Then, with probability at least , we have

for some absolute constant .

It is worth comparing the rates of convergence with those of Bai and Ng, (2021) which apply their TW algorithm to the full matrix. For all missing entries, the convergence rates of the estimators in Bai and Ng, (2021) are . On the other hand, if we assume , the convergence rate of our estimator is up to a logarithmic factor. Since and for all and , our convergence rate is faster than that of Bai and Ng, (2021) except for the estimation of missing entries in part for which both estimates have similar rates of convergence. This shows the advantage of exploiting submatrices for the imputation of missing entries.

3 Debiasing and Statistical Inferences

We now turn our attention to inferences. While the nuclear norm regularized estimator enjoys good rates of convergence, it is not directly suitable for statistical inferences due to the bias induced by the penalty. To overcome this challenge, we propose an additional projection step after applying the nuclear norm penalization in recovering missing entries from group :

| (3.1) |

where is the best rank- approximation of . We now discuss how this enables us to develop an inferential theory for estimating the missing entries. To fix ideas, we shall focus on inferences about the average of a group of entries at a given time period, e.g., , where .

Block Missing Patterns.

We shall begin with general block missing patterns, e.g., if or . Note that both the single treated period and single treated unit examples from the previous section can be viewed as special cases with and , respectively.

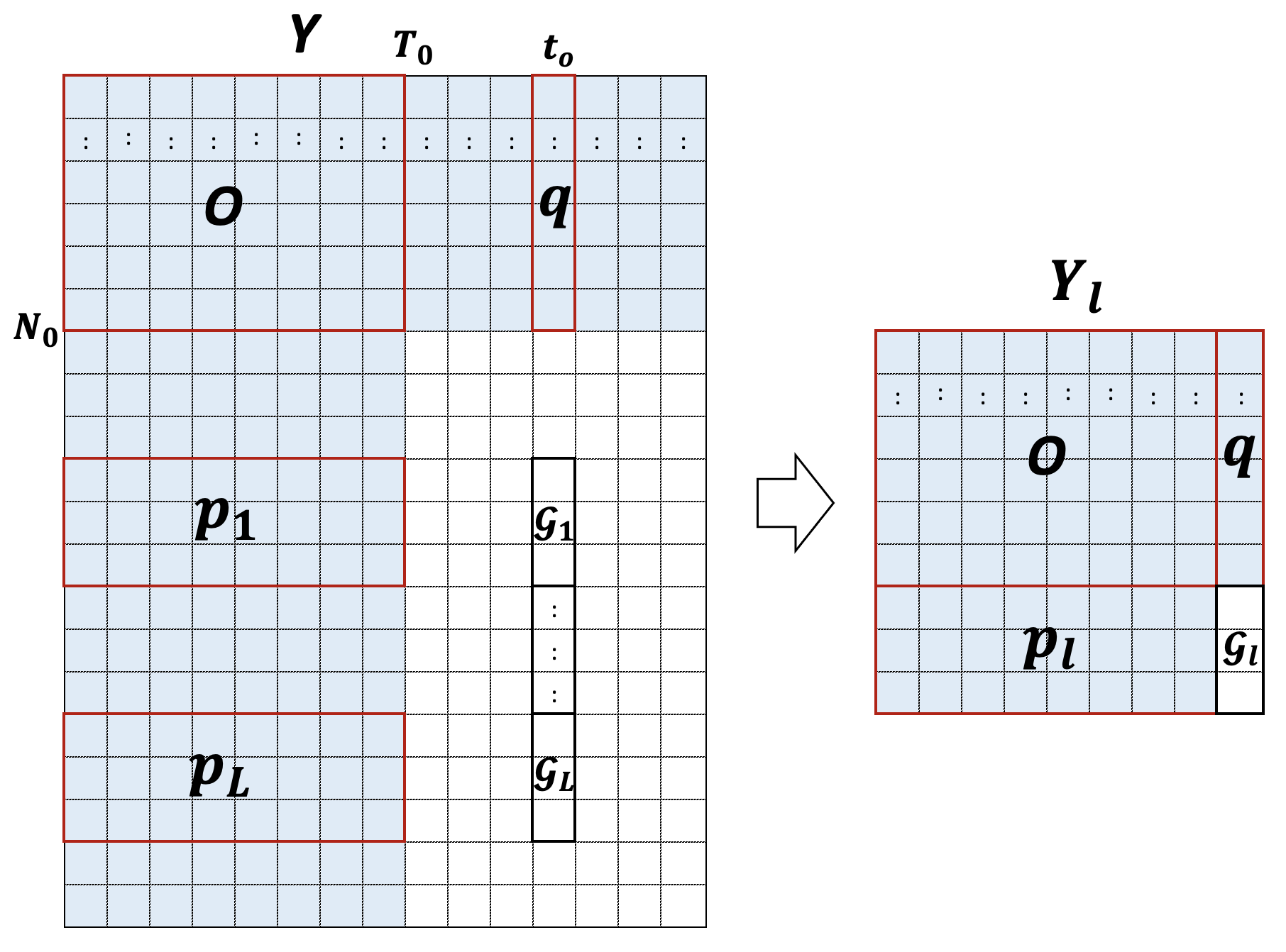

Suppose that we are interested in the inference of the average of a group of entries at the time , , where and . Similar to before, we split the interesting group, , into smaller subgroups, denoted by with the convention that , and construct the corresponding submatrices as illustrated in Figure 4, and construct if .

Recall that is the smallest nonzero singular value of the matrix . The following theorem establishes the asymptotic normality of the group average estimator, .

Theorem 3.1.

Assume that

-

(i)

;

-

(ii)

;

-

(iii)

, ;

-

(iv)

There are constants such that

-

(v)

and for some constant where .

Then, we have

where

Staggered Adaption.

More generally, consider the case of staggered adoption when there are number of adoption time points, , and number of corresponding groups of treated units, . As in the previous situation, suppose that we are interested in inference for the group average at time . Denote by the number of units that are untreated until , and by the number of time periods where is untreated, respectively.

We proceed by first splitting into smaller groups, denoted by with the convention that . In doing so, we want to make sure that all units in each subgroup have the same adoption time point, e.g., , as illustrated in Figure 5. Denote by and by the smallest singular value of the submatrix .

Theorem 3.2.

Assume that for any and ,

-

(i)

;

-

(ii)

;

-

(iii)

;

-

(iv)

there are constants such that

-

(v)

and for some constant .

Then, we have

where

with the convention that .

Variance Estimation.

In practice, to use the results above for inferences, we also need to estimate the variance. To this end, let be the SVD of . Denote by and . They can be viewed as estimates of rescaled left and right singular vectors. However, as such, they are significantly biased and the bias can be reduced by considering instead

We can then use and in place of the left and right singular vector in defining , leading to the following variance estimate

where , , and . The following corollary shows that asymptotic normality established in Theorem 3.2 continues to hold if we use this variance estimate.

Corollary 3.3.

4 Application to Tick Size Pilot Program

Our work was motivated by the analysis of the Tick Size Pilot Program, which we shall now discuss in detail to demonstrate how the proposed methodology can be applied in causal panel data models.

4.1 Data and Methods

Background.

In October 2016, the SEC launched the Tick Size Pilot Program to evaluate the impact of an increase in tick sizes on the market quality of stocks. As noted before, the pilot consisted of a control group and three treatment groups:

-

Control.

stocks in the control group was quoted and traded in $0.01 increments;

-

Q rule.

stocks in the Q rule group was quoted in $0.05 increments but still traded in $0.01 increments;

-

Q+T rule.

stocks in this rule group was quoted and traded in $0.05 increments;

-

Q+T+TA rule.

stocks in this group are also subject to the additional trade-at rule, a regulation which makes exchanges display the NBBO (National Best Bid and Offer) when they execute a trade at the NBBO.

This pilot program has attracted considerable attention, and there are a growing number of studies on the impact of these changes on market quality, often represented by a liquidity measure such as the effective spread since its conclusion in 2018. See, e.g., Albuquerque et al., (2020); Chung et al., (2020); Griffith and Roseman, (2019); Rindi and Werner, (2019); Werner et al., (2022).

Data.

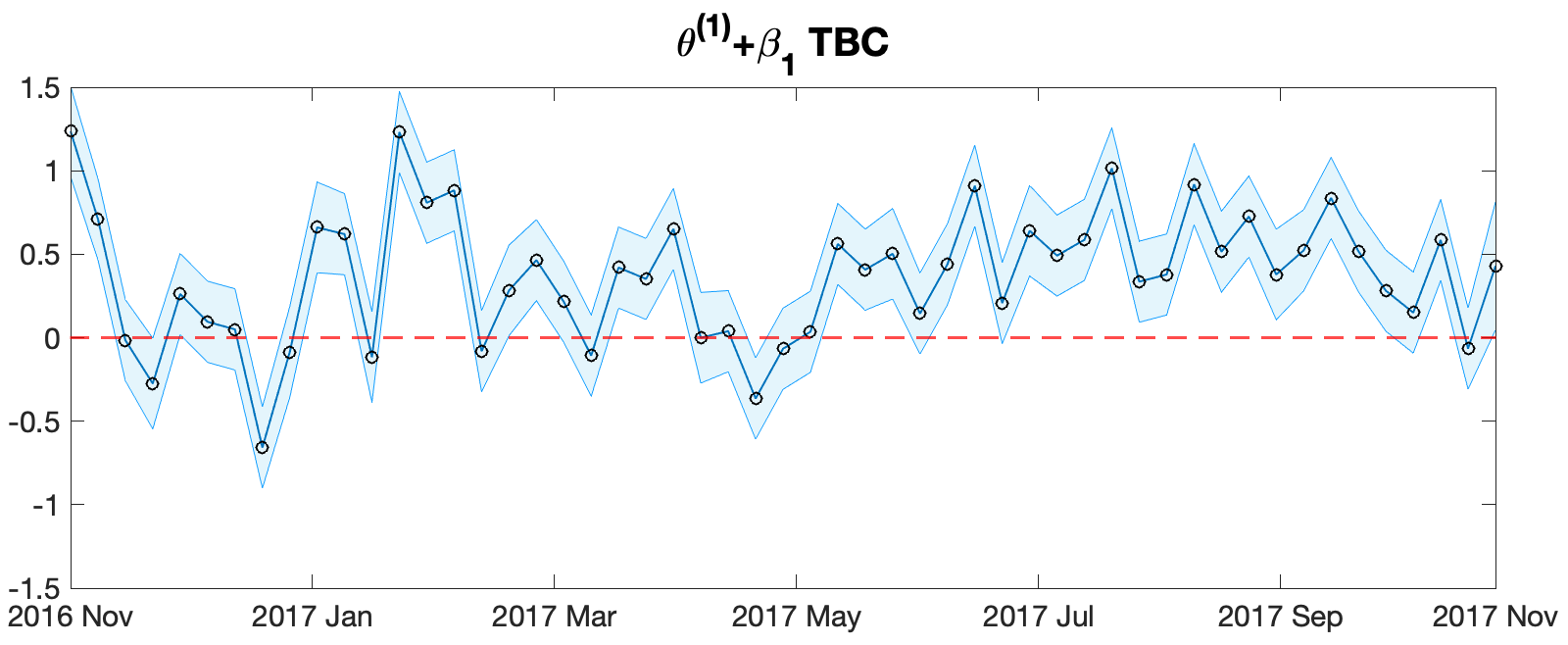

Data for control variables were obtained from the Center for Research in Security Prices (CRSP) and the daily share-weighted dollar effective spread data from the Millisecond Intraday Indicators by Wharton Research Data Services (WRDS). A key control variable introduced by Chung et al., (2020) is TBC which measures the extent to which the new tick size ($0.05) is a binding constraint on the quoted spreads in the pilot periods and is estimated by the percentage of quoted spreads during the day that are equal to or less than 5 cents, which is the new minimum quoted tick size under the Q rule. Specifically, we calculate the percentage of NBBO updates with quoted spread less than or equal to 5 cents for each day. Using the TBC variable, we can check the effect of an increase in the minimum quoted spread (from 1 cent to 5 cents) on the effective spread.

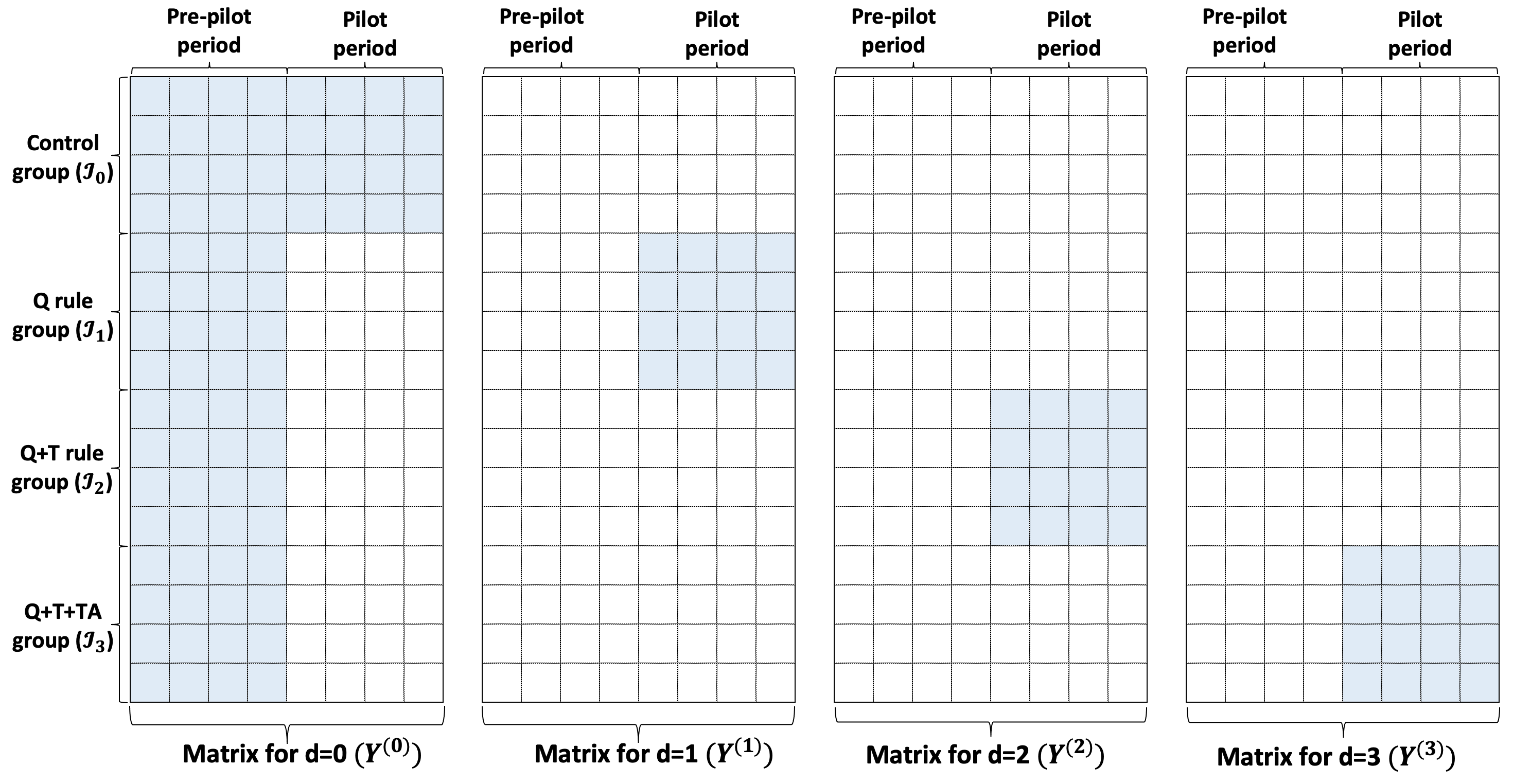

A data-cleaning process similar to Chung et al., (2020) yields a total of stocks with in the control group, in the Q group, in the Q+T group, and in the Q+T+TA group. Following Chung et al., (2020), data from Oct 1, 2015 to Sep 30, 2016 were used as the pre-pilot periods and Nov 1, 2016 to Oct 31, 2017 as the pilot periods, i.e., and for daily data. See Chung et al., (2020) for further discussion of data collection. As is common in previous studies, we consider the daily effective spread in cents as a measure of liquidity. Denote by the potential outcome for stock at time under treatment with the convention that corresponds to the control, the Q rule, the Q + T rule, and the Q + T + TA rule, respectively. The four matrices have block missing patterns, as shown in Figure 6.

Model.

Previous studies of the effects of the quote (Q) rule, the trade (T) rule, and the trade-at (TA) rule on the liquidity measure are usually based on traditional regression or difference-in-difference methods by assuming that the treatment effect is constant across all units and time periods. For instance, Chung et al., (2020) postulated if unit receives treatment at time where the potential outcomes

and

| (4.1) |

Here, , , s and s are unknown parameters, and is a set of control variables that includes typical stock characteristics like stock prices and trading volumes, and TBC, a variable measuring the extent to which the new tick size ($0.05) is a binding constraint on the quoted spreads in the pilot period. See Section E in the Appendix for further details. It is worth noting that, in addition to the treatment effects (, and ), their differences are also of interest, as they represent the treatment effects of quote rule, trade rule, and trade-at rule, respectively.

However, (4.1) fails to account for the significant heterogeneity in the treatment effects across units and time periods. To this end, we shall consider a more flexible model:

| (4.2) |

where is a -dimensional vector of (latent) unit specific characteristics and is the corresponding coefficients of at time in the potential situation . As we shall see later in this section, (4.2) allows us to get more insights into the treatment effects of the pilot program.

One of the key assumptions of Model (4.2) is that the subspace spanned by the left singular vector of for all is included in the subspace spanned by the left singular vector of . Agarwal et al., (2020) propose a subspace inclusion test to check the validity of this assumption. We carried out this test on the pilot data, which confirms this is a reasonable assumption.

We note that similar low-rank models have also been considered by Agarwal et al., (2020) and Chernozhukov et al., (2021) earlier. However, it is unclear how their methodology can be adapted for the analysis of the Tick Size Program. For example, Chernozhukov et al., (2021) impose conditions on the missing pattern that are clearly violated by the pilot data; Agarwal et al., (2020) only study the average treatment effect and so cannot be used to assess the heterogeneity or dynamics of the treatment effects across units and time periods, respectively.

Estimation.

We now discuss how we can apply the methodology in the previous sections to analyze the tick size program, and in particular to estimate and make inferences about (4.2). More specifically, we are interested in estimating the group-averaged treatment effects: for an interesting group of treated units ,

and their differences:

for . Especially, when is a certain unit, it reduces to the individual treatment effect and if is the group of all treated units, it becomes the cross-sectional averaged treatment effect. To this end, we shall derive estimates for under Model (4.2).

First, note that, for this particular application, one of the covariates (TBC) is only present for the pilot periods. Therefore, we cannot hope to estimate the regression coefficient using the pre-pilot data alone, as suggested by Bai and Ng, (2021). Nonetheless, under (4.2), s follow an interactive fixed effect model:

for some low rank components and therefore the regression coefficient can be estimated at the rate of . See Bai, (2009) for details. This is much faster than that of the estimates of . For brevity, we shall, therefore, treat the regression coefficient as known in what follows, without loss of generality.

For , we can apply the method proposed in the previous sections to the potential outcome panel . As illustrated in Figure 6, it has a block missing pattern with if and only if or . As such, we can derive estimates for .

When , we can only observe if unit receives treatment and , so our method cannot be applied directly. Instead, we shall combine all observations from prepilot periods and these observations to form a panel whose entry is if receives treatment and , is if , and is missing otherwise. Let be a matrix whose entry is if , and otherwise. can be viewed as the noisy observation of with a block missing pattern: if and only if unit receives treatment or . Under (4.2), where if and otherwise. Therefore, we can again apply our method to to obtain estimates for .

We shall then proceed to estimate the treatment effects by

Inferences.

We can also use the results from the last section to derive the asymptotic distribution for and . More specifically, let be a matrix that combines all observed outcomes: the first columns of consist of the potential outcomes under the control for the whole periods , the next columns the potential outcomes under the Q rule for the pilot periods , followed by those under the Q+T rule again for the pilot periods , and finally those under the Q+T+TA rule . Note that is also a rank- matrix. Let be its singular value decomposition. Denote by and the -th row vector of and -th row vector of , respectively. In addition, denote by the group of units treated by treatment with the convention that is the control group. Then, under suitable conditions, we have

and where

Similar to before, the variance can be replaced by its estimate. Due to the space limit, we shall defer the formal statements and proofs, as well as derivations of the variance estimator to the Appendix.

4.2 Empirical Findings

Fixed Effects vs Interactive Effects.

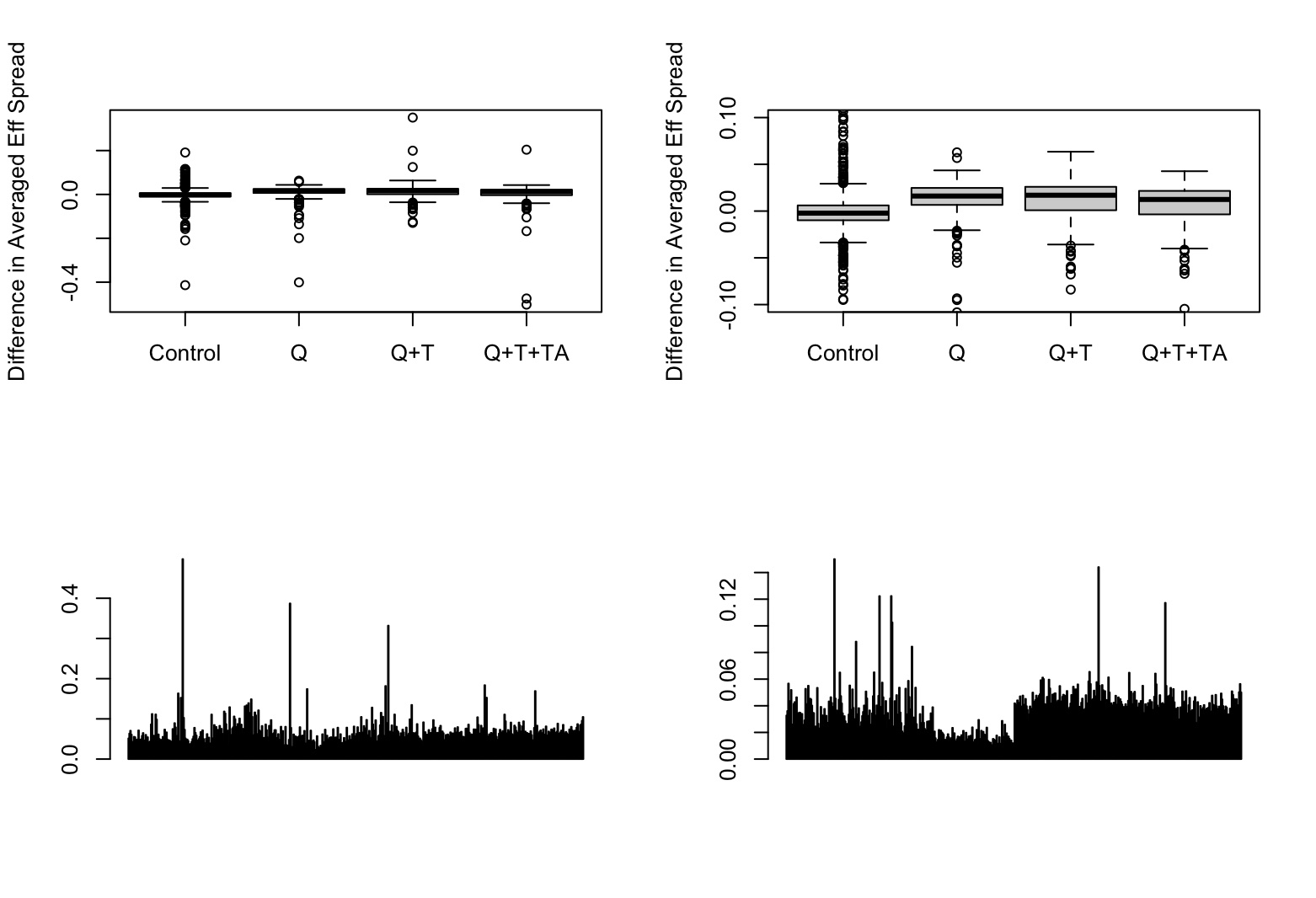

We begin with some exploratory analyses to illustrate the impact of the pilot program. The top left panel of Figure 7 gives the boxplots of difference in the effective spread, averaged over time, after and before the pilot. There are a few units with differences that are much larger in magnitude than usual. For better visualization, the top right panel zooms in with a difference between -10 cents and 10 cents. Taken together, it is clear that the three treatment groups have a significant impact on the effective spread.

The treatment effect of the pilot, however, differs between units. The bottom panels of Figure 7 show barplots of the time series of the effective spread of two typical stocks. The impact of the treatment is much clearer for the stock depicted in the bottom right panel.

The difference in treatment effect among the units suggests that the interactive effect model is more suitable than the fixed effect model used in the previous studies. Note that the fixed effect model (4.1) can be viewed as a special case of the interactive effect model (4.2) with , . We conducted a Hausman-type model specification test to further show that the fixed effect model is inadequate in capturing the heterogeneity of the treatment effect. More specifically, denote our estimator of by and the two-way fixed effect estimator of in Model (4.1) by . We considered the following test statistic for model specification:

where is the group of all treated stocks, , and is the estimator of the asymptotic variance of . Moreover, to test whether is time and unit invariant or not, we also considered the test statistic such that

where .

We derived the large sample distributions of the test statistics under the null and corresponding critical values using the Gaussian bootstrap method (see, e.g., Belloni et al.,, 2018). And the null hypothesis that Model (4.1) is well specified and the null hypotheses that are time and unit invariant are all rejected at 1% significance level, again indicating that Model (4.1) is misspecified and are time and unit variant.

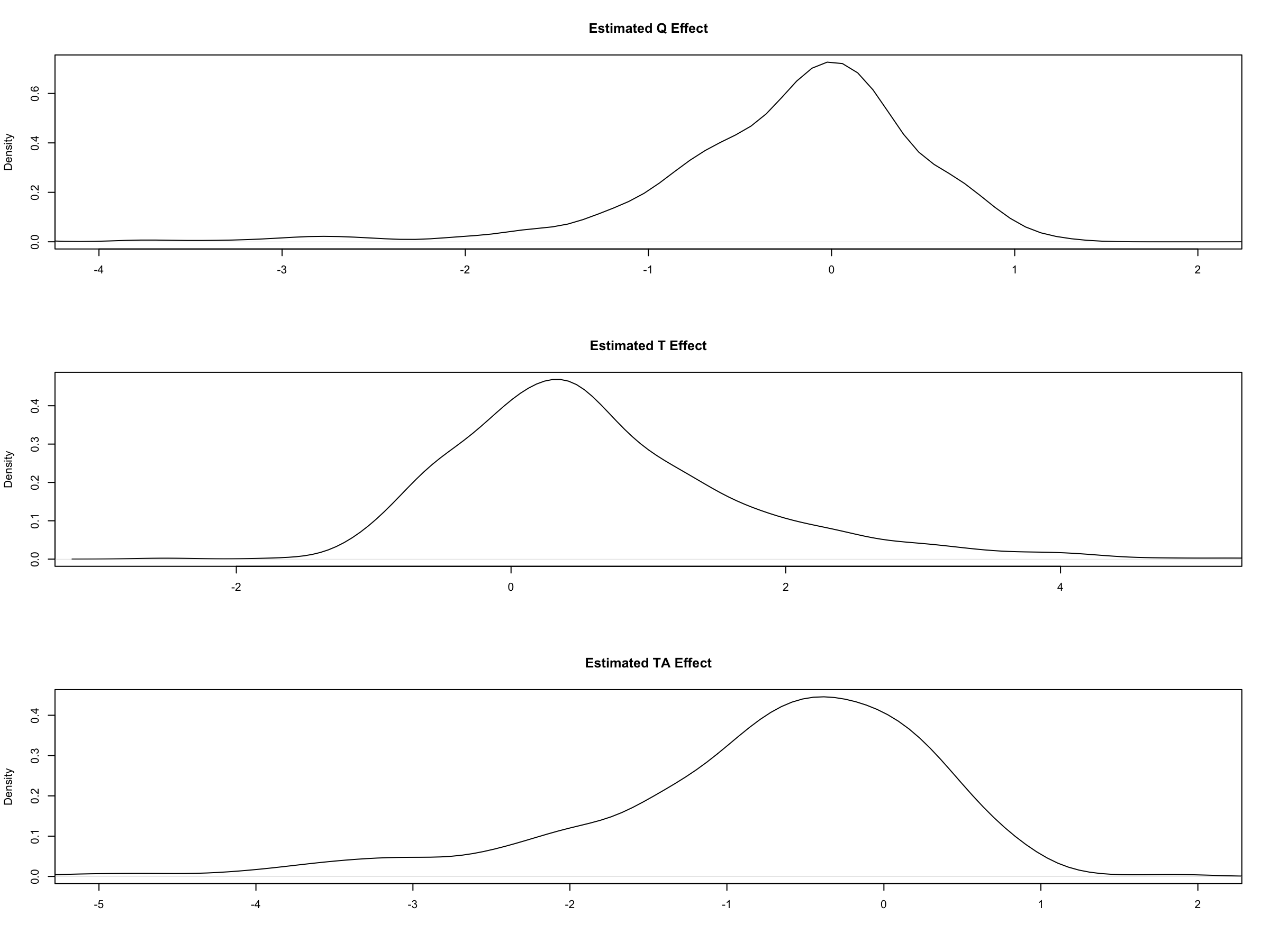

To further illustrate the heterogeneity of the treatment effect, we compute the estimated unit-specific treatment effect averaged over time: and Figure 8 gives the kernel density estimates of these unit-specific treatment effects for the Q rule, T rule and TA rule respectively. It is evident from these density plots that there is considerable amount of variation and skewness among the estimated treatment effects across units.

Note that a key assumption behind the interactive effect model is that the unit specific characteristic remains the same across all treatment groups as well as the control group so that they can be learned from the pre-pilot periods and utilized for the estimation of during the pilot period. This amounts to the assumption that the left singular space of is included in that of . To check the validity of the assumption, we carry out the subspace inclusion test for introduced in Agarwal et al., (2020), and the test statistics are , and with corresponding critical values at 95% level , and . Additionally, we also confirm that the ranks of and are the same for all using the typical rank estimation method (e.g., Ahn and Horenstein,, 2013), which implies the validity of this assumption.

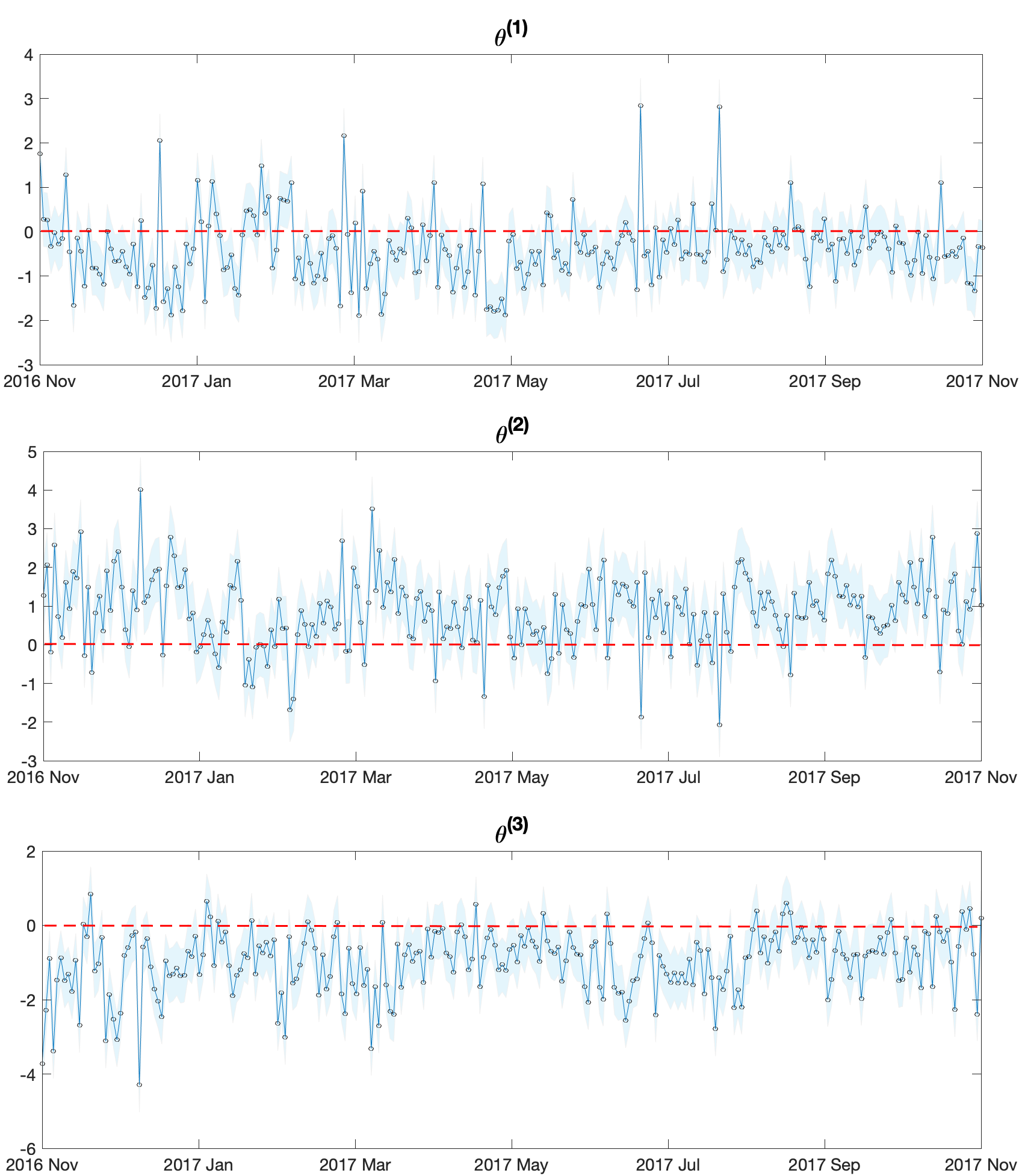

Dynamics of Treatment Effects.

Next, we examine the dynamics of the treatment effects of the Q rule, the T rule, and the TA rule.

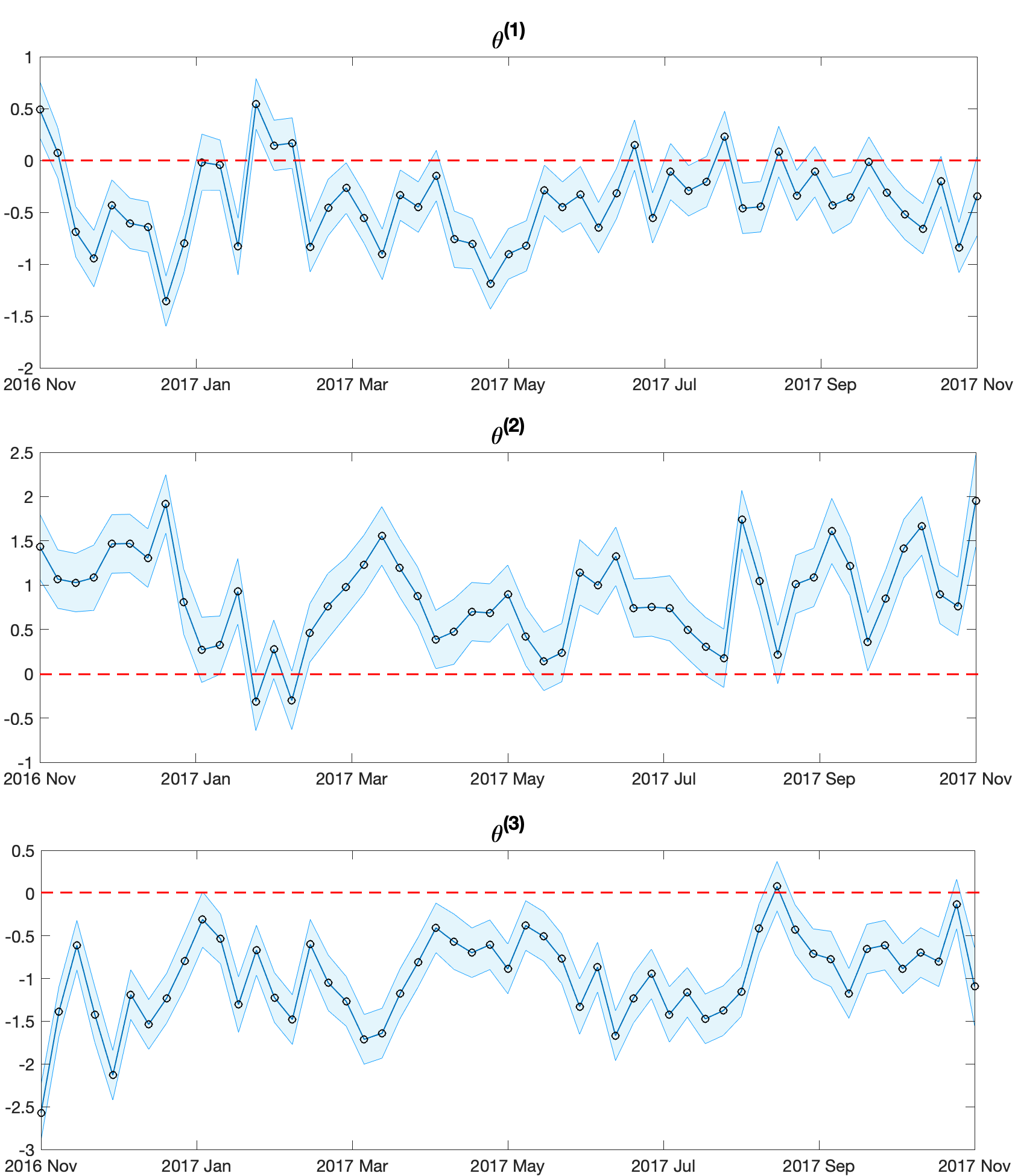

To better visualize the dynamics, we plot in Figure 9 the estimated daily treatment effects along with their 95% confidence interval, adjusted with Bonferoni correction. To gain further insights, we also plot in Figure 10 the weekly average of the estimated daily treatment effects, again with their 95% confidence interval adjusted with Bonferoni correction. Note that to do so, we need to consider the estimator of the form

where is a week of interest. We can generalize the inferential theory from the previous section straightforwardly with the new variance:

where

and can be interpreted as the treatment effects of the T rule and the TA rule. As expected by theory in the literature, we have the positive treatment effects of T rule most of the time. The T rule has a negative effect on price improvements, as liquidity providers are less likely to offer them when the minimum possible price improvement is larger. For example, if the T rule makes the minimum possible price improvement to be 5 cents, liquidity providers who would have been willing to provide less than 5 cents of price improvements are unlikely to offer any price improvement at all. Since the effective spread is “quoted spread - price improvement”, we can expect that treatment effects of the T rule is positive. Here, we use the following definitions: , , and , where is the national best ask price at time , is the national best bid price at time , and is the transaction price.

Interestingly, one can observe that the periods associated with large effects of the T rule usually correspond to large trading volumes. In particular, there were large trading volumes in November, early and mid-December in 2016, March, mid and late June, early August, early September, and late October in 2017, and, by and large, these periods coincide with periods with larger impact of the T rule. In general, the correlation coefficients between the estimated effect of the T rule and the trading volume is . This suggests that the effect of the T rule becomes stronger when transactions are more active. This agrees with the well-known fact that price improvement is more likely to occur when stocks are actively traded, and therefore the effect of the T rule through price improvement will become amplified and strong when trades are active.

Moreover, we find that the treatment effects of the TA rule are negative most of the time. The TA rule increases visible liquidity by exposing hidden liquidity because, under the TA rule, a venue should display the best bid or ask to execute incoming market orders at the NBBO. It implies a decrease in the quoted spread and a smaller room for price improvements. Chung et al., (2020) expect that the effect on the quoted spread is likely to be greater than the effect on price improvements, and so the TA rule decreases the effective spread. Our result corroborates with their conjecture. Further discussion about the empirical findings is given in Section E in the Appendix.

5 Simulated Experiments

To further demonstrate the practical merits and finite sample performance of our methodology, we conducted several sets of simulation experiments.

5.1 Basic Setting

The first set of simulations was designed to compare the performance of the proposed estimator with that of other existing estimators in a staggered adoption setting. Here, the size of “no adoption” group (G0) was set to 200. There are three adoption groups (G1, G2, G3), and the size of each adoption group was set to 100. The number of time points was 500 with G1 adopting the intervention at the 201st time period, G2 at the 301st time period, and G3 at the 401st time period. The potential outcome under the control follows a low-rank model where the noise was sampled independently from the standard normal distribution. The unit specific characteristics s were sampled independently from for G0, for G1, for G2, and for G3. In addition, the corresponding coefficient s were sampled independently from .

To fix ideas, we consider estimating the missing potential outcome of a randomly chosen unit in G2 during the last time period () using different estimators including ours (CY) along with those from Bai and Ng, (2021) (BN), Agarwal et al., (2021) (ADSS) and Athey et al., (2021) (ABDIK). For ADSS, following the recommendation in Agarwal et al., (2021), we set the number of sub-subgroup to be . Table 1 reports the RMSE, summarized from 1,000 simulation runs. The performance of CY, BN, and ADSS are superior to that of ABDIK with CY slightly better than BN and ADSS.

| CY | BN | ADSS | ABDIK | |

| RMSE | 0.1157 | 0.1176 | 0.1193 | 0.3507 |

In addition, we recorded the coverage probabilities of the (asymptotic) confidence intervals associated with each method, with the exception of ABDIK for which such inferential tools have not been developed in the literature. From Table 2, we can see that the coverage probabilities of ADSS are not close to the nominal level, indicating that the asymptotic distributional properties may not provide good approximations in this setting. On the other hand, our method and BN are more accurate, with ours more closely following the target probabilities.

| Target probability | |||

|---|---|---|---|

| Estimator | 90% | 95% | 99% |

| CY | 90.50% | 95.90% | 99.30% |

| BN | 94.20% | 97.50% | 99.50% |

| ADSS | 68.90% | 76.10% | 84.80% |

5.2 Interactive Effect Model

Our next set of simulations mimics the setting of the pilot program studied in the previous section. More specifically, we considered Model (4.2) with two treatment groups, and , and a control group, . Each treatment group receives a different treatment in the pilot periods.

We set and generated the unit specific characteristics from , , , , and . In addition, two control variables were included: is generated from while is generated from if and 0 otherwise. We set the regression coefficient and estimated it using the interactive fixed effect estimation with data of whole periods. The numbers of , , and were set to 250 and the numbers of pre-pilot periods and pilot periods were both set to 250.

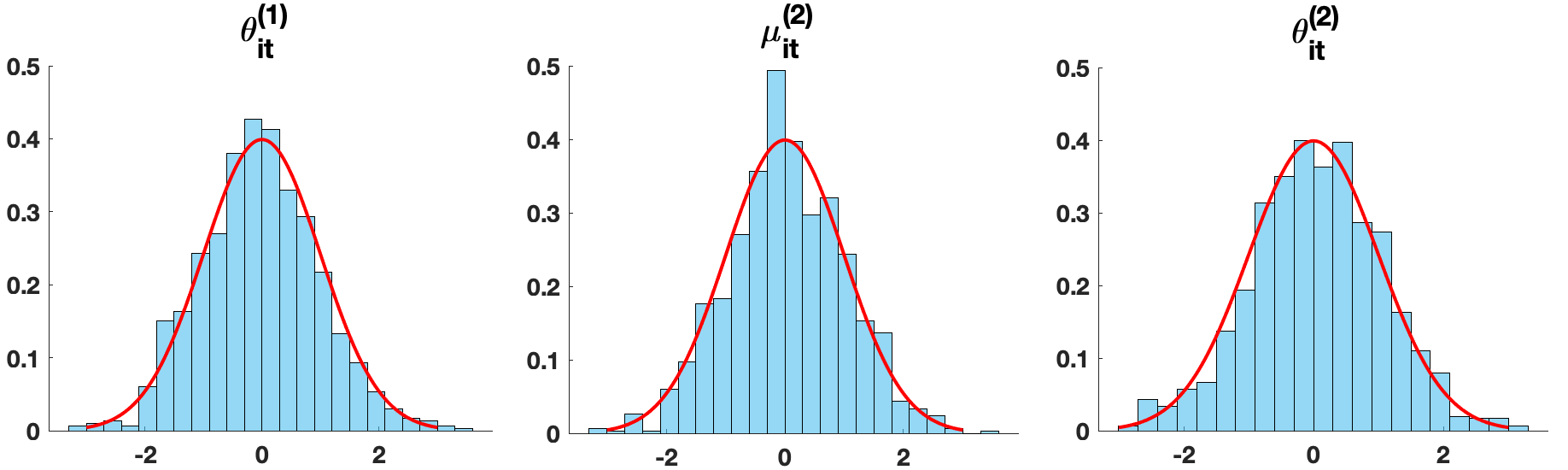

As before, we estimated and for of a randomly chosen unit in at the last period (). Table 3 reports the coverage probabilities of our methods for , , and , summarized from 1,000 simulation runs. It is evident that our coverage probabilities are quite close to the corresponding target probabilities. This is complemented by Figure 11 that shows the histograms of the standardized estimates (t-statistics) along with the standard normal distribution, which again confirms the asymptotic normality of our estimates.

| Target probability | |||

|---|---|---|---|

| Parameter | 90% | 95% | 99% |

| () | 90.20% | 95.60% | 98.70% |

| 90.70% | 95.80% | 99.00% | |

| 89.20% | 94.20% | 98.50% | |

5.3 Simulated Tabacco Sales Experiments

Our final experiment is similar to that from Agarwal et al., (2021) and Athey et al., (2021) and is based on the tobacco sales data of Abadie et al., (2010). In 1988, California introduced the first anti-tobacco legislation in the United States (Proposition 99) and to study the effect of this legislation on tobacco sales, Abadie et al., (2010) used the per capita cigarette sales data which was collected across 39 U.S. states from 1970 to 2000. We considered the time horizon of years and restricted our focus to the untreated states (excluding California) in their dataset. This data was encoded into a matrix, , where the entry represents the potential outcome of per capita cigarette sales (in packs) for state in year under control, i.e., without any intervention in place.

To generate MNAR data, we artificially introduced interventions to a subset of states where the probability that a state adopts an intervention (e.g., tobacco control program) depends on their change in cigarette sales pre-1986 and post-1986. More specifically, we considered the following adoption protocol: First, we clustered states into four categories — severe, moderate, mild, and good — based on their percentage change in average cigarette sales during 1986-2000 compared to that during 1970-1985. The severe states are the states where average cigarette sales are hardly reduced (, MO,WV,SC,AL,AR,TN), and the moderate states are the states whose percentage change is between and (KY,DE,GA,IN,OH,MS). The mild states are the states where the percentage change is between and (NE,LA,IA,SD,WI,PA). The rest are good states ().

We then designated the timing and probability of intervention for mild, moderate, severe, and good states differently. Half of the severe states adopt an intervention in 1986 and the other half in 1991. Half of the moderate states adopt the intervention at 1991 and the other half in 1996. Half of the mild states adopt the intervention in 1996, and the other half do not adopt the intervention. In addition, the good states do not adopt the intervention at all. This setup reflects the scenario in which a state whose average sales may not be reduced sufficiently without the intervention is more likely to adopt the intervention early.

Table 4 shows the average RMSE of missing components caused by the intervention in 10 experiments. Here, the missing components mean the potential “control (no adoption)” outcomes in the intervention period. The only randomization lies in the resampling of the observation patterns. We can check that ABDIK performs relatively poorly. In addition, the performance of our estimator is slightly better than that of BN and ADSS.

| CY | BN | ADSS | ABDIK | |

| average RMSE | 18.362 (0.431) | 19.692 (0.400) | 19.619 (0.432) | 25.522 (0.414) |

6 Concluding Remarks

This article develops an inference framework for the matrix completion when missing is not at random and without the need for strong signals. One of the key observations to our development is that if the number of missing entries is small enough compared to the size of the panel, they can be well estimated even if missing is not at random. We judicially divide the missing entries into smaller groups and use this observation to provide accurate estimates and efficient inferences. Moreover, we showed that our proposed estimate, even with fairly weak signals, is asymptotically normal with suitable debiasing. As an application, we studied the treatment effects in the tick size pilot program, an experiment conducted by the SEC to assess the impact of tick size extension on the market quality of small and illiquid stocks from 2016 to 2018. While previous studies on this program were based on traditional regression or difference-in-difference methods by assuming that the treatment effect is invariant with respect to time and unit, we observed significant heterogeneity in treatment effects and gained further insights about treatment effects in the pilot program using our estimation method. Lastly, we conducted simulation experiments to further demonstrate the practical merits of our methodology.

APPENDIX

Appendix A Estimation of submatrix where missing occurs only at one column

We shall first present the statistical properties of our estimators when missing occurs only at one column, since the estimation in this case serves as the main tool for dealing with more general and common missing patterns. More specifically, we consider the estimation of an arbitrary submatrix of that is constructed using the indices and . Without loss of generality, assume that and . The model we consider is the following:

and where is the SVD of . Denote by and we treat it as a given one. Importantly, missing occurs only in the column : if and , otherwise. Denote the number of missing entries by . In addition, we put the subscript ‘’ in all parameters regarding the submatrix to distinguish them from the parameters of the full matrix .

A.1 Definitions of estimators

Our proof follows a general strategy recently developed by Chen et al., 2020a ; Chen et al., 2019b ; Chen et al., 2020b : we first establish the statistical properties of a certain non-convex estimator and then show that it is close to the nuclear norm penalized estimator. There are two main reasons why this approach is more suitable for our purpose than the usual the restricted strong convexity (RSC) condition based techniques. See, e.g., Negahban and Wainwright, (2012); Klopp, (2014); Athey et al., (2021); Hamdi and Bayati, (2022). First, this approach is more amenable for deriving estimation error in max norm. Moreover, RSC based approach has difficulty in handling situations where the observation probabilities of some entries are deterministically zero. We shall show that even though the strategy was developed for missing at random, it can be used to deal with deterministic missing patterns and in particular when some entries are missing with probability one.

Recall that the nuclear norm penalized estimator is

and the corresponding debiased estimator is

Here, , and where . The estimators for and are defined as and where is the SVD of . In addition, their corresponding debiased estimators are defined as

These quantities will also be useful in defining the variance estimation later on.

We now introduce the non-convex estimators. We start with defining the following two loss functions, one for the typical non-convex estimator and the other for the leave-one-out estimator:

| (A.1) | |||

| if , | (A.2) |

where and are and matrices, respectively. Here, for each , where . Also, where . Note that the estimator constructed from the loss function is independent of . Similarly, for each , we define where , and where . In this case, the estimator is constructed from , which is independent of . Then, based on (A.1), we define the following gradient descent iterates:

| (A.3) |

where , , , and . Here, is the step size. Similarly, for (A.2), we define

| (A.4) |

where , . Note that the gradient descent iterates in (A.3) and (A.4) are not computable because the initial value is unknown. However, it does not cause any problems in the paper since we do not need to actually compute , , , and and only use their existence and theoretical properties for the proof. In addition, we define the corresponding debiased iterates:

Moreover, we define corresponding rotation matrices:

and is the set of orthogonal matrix.

Finally, we define the non-convex estimators using the gradient descent iterates. Let

Then, the non-convex estimators are defined as:

and the corresponding debiased estimators are defined as:

with the corresponding rotation matrices , , , and . Lastly, we define the rotation matrix for as where .

A.2 Key propositions for inferential theory

This subsection provides several key propositions for developing the inferential theory of our debiased estimator . First, we derive a suitable decomposition for the asymptotic normality of the debiased estimator (Propositions A.1 and A.2). By using the proximity between and (Proposition A.3) with this decomposition, we derive a decomposition of , which is used to show the asymptotic normality of (Proposition A.4). We begin by introducing several assumptions.

Assumption A.1 (Noise).

is i.i.d. zero mean sub-Gaussian random variable such that , , , , for some constant .

Assumption A.2 (Incoherence).

There is such that , . Here, and denote the left and right singular vector of , respectively.

Assumption A.3 (Signal to noise ratio).

where is the smallest nonzero singular value of .

Assumption A.4 (Size of and parameters).

(i) and (ii) .

Denote by the diagonal matrix consisting of and by the diagonal matrix consisting of .

Proposition A.1.

Proposition A.2.

Proposition A.3.

A.3 Proofs of Propositions A.1-A.4

Proof of Proposition A.1.

We first derive a decomposition of . From the definition of the gradient with the decomposition

where , we have

In addition, a simple calculation shows that . Then, by combining these two equations, we have

Multiplying both sides by , we have

Moreover, because the left hand side can be also represented as

where , we have

by multiplying . Then, using the identity where , we have the following decomposition:

Furthermore, by defining where

we have the following decomposition for :

where .

Part 1.

Part 2.

Note that

Because

and we have

In addition, by the matrix Berstein inequality, we have

with probability at least . So, we have with probability at least ,

Part 3.

Note that

by the incoherence condition. By Lemma A.5 and the fact that , we have

Next, we bound . Let and . Then, . Following the proof of Lemma 6 in Chen et al., 2019b , we can reach

where . First, we bound . Note that

By the Bernstein inequality, we have

In addition, we have by Lemmas A.5 and D.4 that . Hence, we have

Moreover, since

by Lemma D.7, we have

By Lemma A.5, we know

Lastly, the term is bounded like

due to Lemmas A.5 and A.9, and the relation (A.4). Therefore, we have

Part 4.

Part 5.

Part 6.

Lastly, we check the proximity between the non-convex debiased estimator and the convex debiased estimator to bound . The proof is basically the same as Section C.2 of Chen et al., 2019b . Denote the SVD of by . First, we show that is close to . By Lemma 20 of Chen et al., 2020b , there is an invertible matrix such that and . Denote the SVD of by . Then, we have by Lemma 20 of Chen et al., 2020b that

Here, we use the fact and Lemma A.8. Let . Then, we have by Lemma 13 of Chen et al., 2019b with the above result

A similar bound holds for . Note that

Hence, we have

Next, we show that is also close to . Because is a balanced factorization of , and is that of , we have by the theory for the perturbation bounds on the balanced factorization (Appendix B.7 of Ma et al., (2020), Appendix B.2.1 of Chen et al., 2020a ),

| (A.5) |

Then, by repeating the same argument as above, we can conclude from (A.3) that

| (A.6) |

Hence, we have

∎

Part 2.

In this case, we have

because So, we have with probability at least that

Part 4.

Note that

Let . Then, because

we have

Other parts are the same as that of the proof of Proposition A.1. ∎

Proof of Proposition A.3.

Note that

Replacing by results in

where . Then, by Lemma A.9, we can bound

Denote the SVD of by . By the simple modification of Claim 2 in Chen et al., 2020b for our missing pattern, we can have

where is a residual matrix such that

with probability at least . Here, is the tangent space of . Then, we have

Note that for all and

where is the -th largest singular value of . Then, because and are orthogonal to each other, we know is the top- SVD of , for all , and . In addition, denote the top- SVD of by . Note that

since by Lemma A.9. Hence, we have

Then, because , we can apply Lemma 14 of Chen et al., 2019b to obtain

| (A.7) |

Moreover, we can also obtain from (A.6) that

| (A.8) |

where

Proof of Proposition A.4.

Thanks to Propositions A.1, A.2, and A.3, we have the following decomposition:

First, because of Proposition A.1 and the inequality , we have

Similarly, due to Proposition A.2, we have

In addition, by Lemma A.5 with the assertion in Part 6 of the proof for Proposition A.1 that

we obtain

Lastly, we have

by Proposition A.3. This completes the proof. ∎

A.4 Technical lemmas: Statistical properties of the debiased estimators

This section presents the statistical properties of the debiased estimators. Although this section studies the convergence rates of the nonconvex debiased estimators , since the nonconvex debiased estimators are very close to the convex debiased estimators , as noted in Part 6 of the proof of Proposition A.1, these results are frequently used when we prove the propositions in Section A.2. Remind that

Lemma A.5.

Additionally, the following lemma is exploited in Part 1 of the proof of Proposition A.1 to bound some residual term.

Lemma A.6.

The proofs of the lemmas above are as follows.

Proof of Lemma A.5.

Basically, the proof is similar to that in Section I.2 of Chen et al., 2019b . Note that

In addition, we have

Define

Then, using Lemma 13 of Chen et al., 2019b with Lemma A.8,

| (A.17) |

In addition, by Lemma 13 of Chen et al., 2019b , we have

Hence, we have (A.9) from the above bounds. Similarly, we can derive

which is (A.11). For (A.10), note that

Then, by using Lemma 36 of Ma et al., (2020), we have

and it gives (A.10). In addition, by the similar logic with Lemma A.8, we can derive (A.12) also. For (A.13), notice that

Then, by the above bounds, we can derive (A.13). Using the similar methods of deriving (A.10) and (A.12), we can derive (A.14) and (A.15) also. Lastly, we show (A.16). Set , and . Then, assumptions of Lemma D.23 are satisfied as noted in Section I of Chen et al., 2019b . So, we can apply Lemma D.23 to obtain

∎

Proof of Lemma A.6.

Define

where . Then,

Note that and are independent across conditioning on . Hence, we have by the matrix Bernstein inequality with Claim A.7 that

Claim A.7.

With probability at least , we have for all and ,

The proof for the part

is similar, and therefore omitted for brevity. ∎

Proof of Claim A.7.

By Lemma 12 of Chen et al., 2019b with Lemma A.5, we have

In addition, because

we have from Lemma A.5 that

∎

A.5 Technical lemmas: Statistical properties of the nuclear norm penalized estimators and the corresponding non-convex estimator

Lastly, we present the statistical properties of the non-convex estimator . Since this estimator is very close to the nuclear norm penalized estimator as we will see in Lemma A.9, we can derive the convergence rates of the nuclear norm penalized estimator from this result. Besides, the statistical properties of the debiased estimators in the previous section are largely based on the result of the non-convex estimators in this section.

Basically, the result in this section is the modification of Chen et al., 2020b for the case where missing is not at random and occurs only at one column. To save space, we omit the proofs of some lemmas if the proof is a simple modification of that in Chen et al., 2020b . We are willing to provide the full proofs upon request.

First, the following lemma shows the statistical properties of the nonconvex estimator which are used for the proofs in the previous sections. Remind that

Lemma A.8.

Proof.

Because the initial estimators, and , are set to , (A.18) - (A.25) are satisfied when . Then, by the mathematical induction, Lemmas D.16 - D.20 with Lemmas D.8, D.14 show that the iterates and satisfy (A.18) - (A.25) with probability at least . In addition, (A.26) - (A.29) are derived from Lemmas D.21 and D.22. ∎

The technical lemmas used in this proof are relegated to Section D. The following lemma shows the proximity between the non-convex estimator and the nuclear norm penalized estimator.

Lemma A.9.

Proof.

Appendix B Proofs of theorems and corollaries in the main text

Using the tools from the previous section, we shall now prove the theorems and corollaries in the main text.

B.1 Proofs for Section 2

Proof of Theorem 2.1.

Note that

Here, are the nonconvex estimator introduced in Section A.1 and where is the SVD of . Note that Assumptions A.1 - A.4 are satisfied since the number of missing entries is in this case. Then, we have from Lemmas A.8 and A.9 that

where for some constant , since we have by Lemma A.8

First, we prove Corollary 2.2. By Assumption (iii), we know . Then, we have by Assumptions (iii) and (iv)

| (B.1) | ||||

Similarly, we can have . Then, using Lemma B.3, we can have , , and , where and are the incoherence parameter and condition number of the submatrix , and is the smallest nonzero singular value of . Using these relations, we can check that submatrix satisfies Assumptions A.1 - A.4 under the assumptions of Corollary 2.2. Then, we can derive the bound of by the same way as in the proof of Theorem 2.1 from Lemmas A.8 and A.9. In addition, we replace and in the bound of with and using the above relations from Lemma B.3, and replace with since . Lastly, the bound of trivially follows from that of since any entry of is included in at least one of .

Symmetrically, we can prove Corollary 2.3 using the same way. So, we omit the proof.

Proof of Corollary 2.4

It is a simple extension of Corollary 2.2 and the proof is same as that of Corollary 2.2. The only difference is that the dimension of the submatrix becomes where and . Here, we have from Assumption (iv) that

| (B.2) |

and . Then, by (B.1) and (B.1), we can exploit Lemma B.3. In the bounds of , we replace and with and using the results of Lemma B.3, and replace and with and since and . In addition, the bound of trivially follows from that of .

Proof of Corollary 2.5

In the case of the estimation of missing entries in the matrix , the dimension of each submatrix is where and . By the similar way to (B.1) and (B.1), we can show

Hence, we can exploit Lemma B.3 to replace , , with , , and replace and with and in our conditions and then, we can check that for each , Assumptions A.1 - A.4 are satisfied. Then, we derive the bounds of by the same way as in the proof of Theorem 2.1 using Lemmas A.8 and A.9. The bound of trivially follows from that of .

B.2 Proofs for Section 3

Proof of Theorem 3.1

First of all, by using the fact from Lemma B.3 that , , and the relations that and w.h.p., we can check that Assumptions A.1 - A.4 are satisfied for each submatrix. Denote by the group where the unit is included in. That is, . Then, by Proposition A.4, we have the following decomposition:

Here, where is the SVD of . is the transpose of the row of corresponding to the unit and is the transpose of the row of corresponding to the time period . Because for each , there is an invertible matrix such that , we have

Similarly, we can show that

Note that

Hence, we have

Then, for any , we have by Cauchy-Schwarz and Markov inequalities that

since

for some constant . Then, we have by Lindeberg theorem that

In the same way, we can derive

where . Then, because and are independent, by using the similar assertion in the proof of Theorem 3 of Bai, (2003), we have

since .

In addition, note that the difference between and is just one element , and that between and is just . Hence, without difficulty, we can show that . Moreover, note that since

for some constant , we have

Hence, by Proposition A.4, we have with probability at least that

for an absolute constant . Then, by Assumptions (i), (ii), and (iii) with the relations that , , and w.h.p., we have . Therefore,

Proof of Theorem 3.2

By using the fact from Lemma B.3 that , , , and the relations that and w.h.p., we can check that Assumptions A.1 - A.4 are satisfied for each submatrix . Then, by Proposition A.4, we have the following decomposition:

with the convention that . Then, we can represent as

Because is independent across and , is a sum of independent random variables and so, we can use Lindeberg CLT. To check the Lindeberg condition, we first bound . Note that

Hence, we have

In addition, because when , we have

For each , we have

because

Then, we have

where . Therefore, we can reach

Then, for any , we have by Cauchy-Schwarz and Markov inequalities with Claim B.1,

Because , we have by the Assumption (ii). Hence, the Lindeberg condition is satisfied.

Claim B.1.

(i) and (ii) .

Therefore, by using the Lindeberg CLT with Claim B.1 (ii), we have . Next, we show that . Since for all , we have by Proposition A.4 with probability at least that

for an absolute constant . Then, by Assumptions (i), (ii), and (iii) with the relations that , , and , we have . Therefore,

Proof of Claim B.1.

(i) We have , because for some constant ,

(ii) A simple calculation shows that

where . Hence, we have . In addition, note that where

Then, we have

Hence, we have . ∎

Proof of Corollary 3.3

From the proof of Claim B.1 (ii), we know that where and . Note that

Hence, we have

where . In addition, as noted in the proof of Claim B.1 (ii), we have

First, we show that

where

Note that

Because

we know by Claims B.1 and B.2 that

Claim B.2.

Next, we want to bound the following term:

As noted in the proof of Proposition A.4, we have

In addition, because

and

we have

Here, is the left singular vector of and is the -th row of it. Hence, we obtain

and

Then, we have

by Assumptions (i), (ii), and (iii) with the relations that , , and . In the same token, we can also show that

where . Then, we have and it implies that . Then, by the Slutsky’s theorem with Theorem 3.2, we have the desired result.

Proof of Claim B.2.

Note that

where . As noted in the proof of Proposition A.4, we have

Hence, we get

Moreover, we have by concentration inequalities that

Since the first term dominates the second term using the relations that , , we have the desired result. ∎

B.3 Relations about eigenvalue and eigenvector between the full matrix and its submatrix

Lastly, we present one lemma which shows the relations about eigenvalue and eigenvector between the full matrix and its submatrix.

Lemma B.3.

(i) Let be a matrix of rank and be a submatrix of where and . The SVD of is , and the -th row of is and the -th row of is . In addition, , denote the incoherence parameter and the condition number of , and denote those of . If there are constants such that

we have and .

(ii) Let and be submatrices of where , , , and . If

there are constants such that for all ,

we have where is the smallest singular value of .

Proof of Lemma B.3.

(i) Without loss of generality, assume that and . Let the SVD of be . Then, we can say

for and . In addition, let where and where . Then, we have . Define

Let be a matrix whose columns are the eigenvectors of such that is a descending order diagonal matrix of the eigenvalues of . Define

Note that

In addition, we have

Hence, the column of are the eigenvector of corresponding to the eigenvalue . Hence, is the left singular vector of , that is, . Then, since

| (B.3) |

we have the following incoherence condition for the submatrix:

where for some constant . Similarly, we can have where for some constant . Hence, the incoherence parameter for the submatrix is for some constant .

Note that

Then, by using the relation (B.3), we have

where is a eigenvector matrix of . Then, we have

| (B.4) | ||||

So, the condition number of the submatrix can be bounded like .

(ii) By using the relation (B.4) with the fact that , we know

Similarly, we can show . Hence, we have that .

∎

Appendix C Formal inferential theory for the treatment effect estimation in Section 4

This section provides the formal inferential theory for the group averaged treatment effects, and in Section 4. The assumption on the noise is the same as that in Section 2, and the singular vectors of are incoherent in that there is a such that , .

Denote by , and the smallest nonzero singular value of it by . In addition, denote by the subgroups of for the estimation of . Then, we have the following asymptotic normality of the group averaged estimator.

Theorem C.1.

Assume that for any and ,

-

(i)

;

-

(ii)

;

-

(iii)

;

-

(iv)

There are constants such that

where is the number of columns of ;

-

(v)

for some constant where .

Then, we have

and where

For completeness, we provide the variance estimator. For each and , denote by the debiased estimators derived from which is the submatrix of constructed for the estimation of . In addition, denotes a row of which corresponds to the unit and denotes a row of which corresponds to the -th column of .

Corollary C.2 (Feasible CLT of Theorem C.1).

Suppose the assumptions in Theorem C.1 hold. In addition, we have for all , . Then,

and where

, , . In addition, .

Proof of Theorem C.1

(i) Case 1 : Following the proof of Theorem 3.1, we have the decomposition:

| (C.1) |

where is a residual term. First, we want to show the Lindeberg condition. Note that

Using the same way in the proof of Theorem 3.2, we have and . Then, by the same token as the proof of Theorem 3.2, we have

Similarly, we have

where . Then, for any , we have by Cauchy-Schwarz and Markov inequalities with Claim C.3,

where , , and . Because the last term is , the Lindeberg condition is satisfied.

Claim C.3.

(i) and (ii) .

Therefore, by Lindeberg CLT, we have . In addition, by the same token as in the proof of Theorem 3.1, we can show . Therefore,

(ii) Case 2 : The proof is the same as that of Case 1 if we change to . Since it is a simple extension of the proof of Case 1, we omit it.

Proof of Claim C.3.

(i) Since and is disjoint with , we have

A Simple calculations show that

Hence, we have .

(ii) Note that

since . In addition, we have

for some constant . Similarly, we have for some constant . Therefore, we reach . ∎

Proof of Corollary C.2

(i) Case 1 : From the proof of Claim C.3, we know

where and . Following the similar argument in the proof of Corollary 3.3 with the definitions in (C), we have

where , , and . Here, are the SVD of which is the submatrix of constructed for the estimation of . In addition, we have

where . Note that for all , by Claim C.3. Then, by the same way as the proof of Corollary 3.3, we have

Similarly, we can show that

where

Hence, we have and it implies that . Then, by the Slutsky’s theorem with Theorem C.1, we have the desired result.

(ii) Case 2 : The proof is the same as that of Case 1 if we change to . Since it is a simple extension of the proof of Case 1, we omit it.

Appendix D Modification of results from Chen et al., 2020b

Finally, we present technical tools used for proving Lemmas A.8 and A.9 in Section A.5. These results are modifications of similar results from Chen et al., 2020b when missing is random. Indeed the overall architecture of our proof is the same as those in Chen et al., 2020b , and for brevity, we shall omit proofs of lemmas that are straightforward adaptation of those in Chen et al., 2020b .

D.1 Proximity between the nonconvex estimator and the nuclear norm penalized estimator

We begin by introducing further notations. For any matrix , we denote by (resp. ) the -th row (resp. column) of . Let be a matrix with rank and be SVD of . Then the tangent space of , denoted by , is defined as

Let be the orthogonal projection onto , that is,

for any . When there is no risk of confusion, we will simply denote by instead of . Let be the orthogonal complement of and be the projection onto . Note that and . Lastly, we define , for all .

The following lemma plays a key role in showing the proximity between the nonconvex estimator and the nuclear norm penalized estimator . We will eventually set where and .

Condition D.1 (Regularization parameter).

The regularization parameter satisfies (i) and (ii) .

Condition D.2 (Injectivity).

Let be the tangent space of . There is a quantity such that for all .

Lemma D.3.

Proof.

This lemma is the simple modified version of Lemma 2 of Chen et al., 2020b . If we follow their proof by setting and considering our observation pattern with caution, we can get the result. To save space, we omit the proof. ∎

The following lemmas are used to show that our nonconvex estimator satisfies Conditions D.1 and D.2. Lemma D.4 shows Condition D.1 (i) is satisfied when for a sufficiently large constant . In addition, Lemma D.5 is used when we show Condition D.1 (ii) and Condition D.2 are satisfied in the case .

Lemma D.4.

With probability at least , we have

(i) , (ii) .

Proof.

(i) All elements of excluding the elements of are . Because the elements of are and , it is trivial.

(ii) Denote a matrix excluding the -th column of by . By Theorem 5.39 of Vershynin, (2010), we have

where is the matrix excluding the -th column of . In addition, it is trivial that

where and are the -th column of and , respectively. ∎

Lemma D.5.

Suppose that

Assume that for some large constant . Further, let denote the tangent space of . Then, with probability at least ,

hold uniformly for all satisfying

| (D.2) |

for some constant .

Lemma D.6.

Assume that and . Let denote the tangent space of . Then, with probability at least ,

holds uniformly for all such that

where is some sufficiently small constant.

Proof.

This Lemma is the simple modification of Lemma 7 of Chen et al., 2020b . If we follow their proof by considering our observation pattern cautiously, we can get the result. Importantly, we use Lemma D.12 which is the modified version of Corollary 4.3 of Candès and Recht, (2009) in the place where Chen et al., 2020b use Corollary 4.3 of Candès and Recht, (2009). To save space, we omit the proof. ∎

Lemma D.7.

Assume that

Let for some large constant . Then, with probability at least ,

holds uniformly for all satisfying (D.2).

Proof.

This Lemma is the simple modification of Lemma 8 of Chen et al., 2020b . To save space, we omit the proof. ∎

D.2 Quality of non-convex estimates

Before we proceed, we introduce some notations. Define an augmented loss function to be

Then, the gradient of is given by

The difference between gradients of and are

In addition, note that we have the following properties of :

The following Lemma is the one of the main parts where we require the condition . While it is the modified version of Lemma 12 in Chen et al., 2020b , the proof of it is quite different from theirs. Hence, we provide the full proof.

Lemma D.8.

Proof.

Fix . The definition of and the unitary invariance of Frobenius norm yield

By the gradient update rules (A.3) and (A.4), we obtain

Here, we use the facts that and for any matrix and any orthonormal matrix . Hereinafter, we control and separately. The way of bounding and are the same as the proof of Lemma 12 in Chen et al., 2020b while the way of bounding is quite different.

-

1.

The first term can be bounded using the same derivation as in the proof of Lemma 10 of Chen et al., 2020b :

with probability at least . Here, we use the assumptions

and .

-

2.

Regarding , the triangle inequality gives us, with probability at least ,

Following the bound of in the proof of Lemma 10 of Chen et al., 2020b , we obtain

Additionally, Lemma D.20 and the argument for bounding in the proof of Lemma 10 of Chen et al., 2020b together give us

The three inequalities together allow us to have

with probability at least , where the last inequality follows from the assumption .

-

3.

For bounding , observe that

We invoke the following three claims to control , , and , , whose proofs are provided after the proof of Lemma D.8.

Claim D.9.

Assume that

Then, for each , we have

Claim D.10.

Assume that

Then, for each , we have

Claim D.11.

Assume that

Then, for each , we have

with probability at least .

Then, the triangle inequality yields, with probability at least

Here, the last inequality follows from Lemma D.22 (i).

Combining the bounds on , , we reach, with probability at least ,

for some constant . The penultimate inequality uses the induction hypothesis (A.20), and the last inequality holds provided that is sufficiently large and . Therefore, with probability at least we have

∎

Proof of Claim D.9.

Assume that and define and . Using the unitary invariance of Frobenius norm, we have . First of all, if , . Hence, . If , has only one nonzero element . So, we have

where is the max norm, and the last inequality follows from Lemma D.22 (iv) provided that

Additionally, observe that Lemma D.22 (iv) gives

Finally, we have

Now, assume that and define . First, if , . If , we have

Then, since

we can obtain

∎

Proof of Claim D.10.

First, assume that . We follow the notation in the proof of Claim D.9. When , . If , we have

So, we have

Assume now that . Using the unitary invariance of Frobenius norm, we have . If , then . In addition, if , we obtain

Therefore, we have

∎

Proof of Claim D.11.

First, we bound . Assume that . Since Frobenius norm is unitary invariant, we have

By the way of construction of leave-one-out estimates, are independent of . Therefore, we have , and conditioning on , are independent across . Hence, conditioning on , we can exploit the matrix Bernstein inequality (Koltchinskii et al.,, 2011, Proposition 2). Note that

where denotes the sub-exponential norm; see Koltchinskii et al., (2011); Tropp et al., (2015). Further, we can see that

Then, the matrix Bernstein inequality reveals that, with probability at least ,

where the last relation uses the assumption . Applying Lemma D.22 (iv) with the assumption

we reach, with probability at least ,

Now, we consider the case of . Since Frobenius norm is unitary invariant and only the -th column of the matrix has nonzero elements,

Similarly, conditioning on , we can exploit the matrix Bernstein inequality (Koltchinskii et al.,, 2011, Proposition 2). Note that

Then, the matrix Bernstein inequality reveals that, with probability at least ,

where the last relation uses the assumption . Applying Lemma D.22 (iv) with the assumption

we reach, with probability at least ,

We turn to . Assume . Since Frobenius norm is unitary invariant, we have

Similarly, conditioning on , we can exploit the matrix Bernstein inequality. Note that and

Then, the matrix Bernstein inequality reveals that, with probability at least ,