Optimal Liquidation with Conditions on Minimum Price111This work was supported by TUBITAK (The Scientific and Technological Research Council of Turkey) through project number 118F163.

Abstract

The classical optimal trading problem is the closure of an initial position in a financial asset over a fixed time interval; the trader tries to maximize an expected utility under the constraint that the position be fully closed by terminal time. Given that the asset price is stochastic, the liquidation constraint may be too restrictive; the trader may want to relax the full liquidation constraint or slow down/stop trading depending on price behavior. We consider two additional parameters that serve these purposes within the Almgren-Chriss liquidation framework: a binary valued process that prescribes when trading takes place and a measurable set that prescribes when full liquidation is required. We give four examples for and which are all based on a lower bound specified for the price process. The terminal cost of the stochastic optimal control problem is over ; this represents the liquidation constraint. The permanent price impact defines the negative part of the terminal cost over the complement of The parameter enters the stochastic optimal control problem as a multiplier of the running cost. Except for quadratic liquidation costs the problem turns out to be non-convex. A terminal cost that can take negative values implies 1) the backward stochastic differential equation (BSDE) associated with the value function of the control problem can explode to backward in time and 2) the existence results on minimal supersolutions of BSDE with singular terminal values and monotone drivers are not directly applicable. To tackle these we introduce an assumption that balances the market volume process and the permanent price impact in the model over the trading horizon. In the quadratic case, assuming only that the noise driving the asset price is a martingale, we show that the minimal supersolution of the BSDE gives both the value function and the optimal control of the stochastic optimal control problem. A key point in our arguments is that the negative part of the terminal value of the BSDE (arising from permanent price impact) is bounded. For the non-quadratic case, we assume a Brownian motion driven stochastic volatility model and focus on choices of and that are either Markovian or can be broken into Markovian pieces. These assumptions allow us to represent the value functions as solutions of PDE or PDE systems. The PDE arguments are based on the smoothness of the value functions and do not require convexity.

We quantify the financial performance of the resulting liquidation algorithms by the percentage difference between the initial stock price and the average price at which the position is (partially) closed in the time interval We note that this difference can be divided into three pieces: one corresponding to permanent price impact (), one corresponding to random fluctuations in the price () and one corresponding to transaction/bid-ask spread costs (). turns out to be a linear function of the portion of the portfolio that is closed; therefore, its distribution is fully determined by the distribution of that portion. We provide a numerical study of the distribution of the closed portion and the conditional distributions of and given the closed portion under the assumption that the price process is Brownian for and a corresponding to a lowerbound on terminal price.

Keywords: liquidation, non-convex optimal control, backward stochastic differential equations, Hamilton Jacobi Bellman equation.

MSC 2020: 35K57, 49K45, 49L25, 60H30, 60H99, 93E20.

1 Introduction

There is a range of order types available to an investor to close a position on an asset; the book [14] presents the following: implementation shortfall (IS), target close and volume weighted average price. Given a trading horizon , all of these order types are constrained to close an initial position at a terminal time . Mathematically this is expressed as the constraint , where denotes the position of the investor at time (we assume , i.e., an initial long position, for a more brief presentation; everything below applies to a short position ). Given that the price process is stochastic, this constraint can be too restrictive. For example, in IS orders the goal is to close an initial position near the initial price ; it may happen that the price drops substantially during the trading interval and the investor holding the position may no longer wish to be strict about closing the position. The present work studies algorithms that offer this type of flexibility in execution. We focus on IS type orders targeting the initial price because this is the most basic and most commonly studied order in the current literature but similar ideas can be considered for other types of orders and pursued in future research. The work [16] already presents an optimal liquidation algorithm in which the full liquidation constraint is relaxed; the algorithms presented in the current work extend those in [16] in two directions: 1) the model in the present work involves a permanent market impact component and 2) we allow the model to impose constraints on when trading takes place (for example, the model can be set up so that trading is allowed only when the current price is above a given threshold). The resulting stochastic optimal control problem leads to a backward stochastic differential equation of the form

with a singular terminal condition (i.e., can take the value ). When compared to BSDE with singular terminal values arising from optimal liquidation problems studied in [16] and other works on optimal liquidation, this BSDE has three new features: its generator/driver is not monotone in (see below for the precise definition), vol is allowed to be , and its terminal value can take negative values. For several versions of the problem with a Markovian formulation we also treat the partial differential equation (PDE) versions of this equation. As we discuss in detail below, the new features have nontrivial implications for the analysis of the BSDE and the PDE.

The IS order is commonly formulated as a stochastic optimal control problem optimizing the expected utility of the cash position that the order generates [14, Chapter 4]. Section 2 presents the stochastic optimal control formulation of the modified IS orders that the present work focuses on. A great deal of the literature on optimal liquidation, including the model presented in section 2, is based on a model proposed by Almgren and Chriss in [3]. This model assumes that the price consists of three pieces: a random fluctuations term , a transaction cost term and a permanent market impact term. The permanent price impact is a term added to where is the time derivative of at time ; together with the random fluctuation term they make up the midprice process . The transaction cost term corresponds to trading commissions and the bid-ask spread; this is modeled using a so-called execution cost function . The common choice for is a power function , (we reserve the letter for the Hölder conjugate of , which arises in the solution of the problem). In most liquidation models the permanent price impact is assumed to be linear in (see [12] for more comments on this assumption). This and the constraint of the standard IS order lead to an interesting situation for this type of order: the permanent price impact ends up having no role in the stochastic optimal control formulation of the standard IS order (see (5) and (7)). These assumptions have another important mathematical implication for the standard IS order: the position variable can be factored out of the value function and out of the backward stochastic differential and partial differential equations that the value function satisfies (see Proposition 3.3)- we will refer to this property of the value function as homogeneity. When we relax the constraint the permanent price impact enters directly into the stochastic optimal control problem as a part of the terminal cost. In the modifications of the IS order we treat in the present work we would like to keep the homogeneity property of the value function as this greatly influences the analysis of the problem. This turns out to be possible if the permanent price price impact function is chosen compatible with the execution cost function as follows:

remains linear in ; for () decays (increases) with the size of the remaining position.

As we have already noted, the permanent price impact has no role in the continuous time stochastic optimal control formulation of the standard IS order in the Almgren-Chriss framework. We see a reflection of this fact in the optimal liquidation literature that is based on this framework, as follows: some works introduce a permanent price impact parameter in the model (see e.g., [10, 24] and [14, Chapter 3]), but it ends up having no role in the stochastic optimal control problem, while others drop the permanent price impact parameter altogether from the model assumptions, see, e.g., [4, 16]. The seminal work [3] includes a permanent price impact parameter in a discrete time framework, which ends up having a role in the optimal controls but this role disappears as the discrete time step size converges to . A key feature of the problem and the analysis presented in the current work is how the permanent price impact enters and changes the analysis when the full liquidation constraint is relaxed. We discuss this in detail below.

The output of the standard IS order is the cash position generated by the trading algorithm. When full liquidation is no longer required, i.e., when we don’t have the constraint , the output of the trading process at time will be where is the cash generated by the trading process and is the position remaining in the asset being traded. There are several choices available to formulate an expected utility maximization problem based on this output. One option is to use a general utility function whose input is the pair ; a simpler option is to first assign a monetary value to the position , use a utility function whose only input is a monetary value and apply it to . In the present work we use the latter approach. For the present work focuses on ; this is the market value of the position at terminal time ignoring trading costs. The technical advantage of this choice is that it preserves the homogeneity of the value function; a term can also be added that preserves homogeneity. For the utility function we focus on the identity function, i.e., we consider the problem of maximizing expected terminal position; an additional risk term can be included in the final stochastic optimal control problem with minor modifications to the analysis. We further comment on these points in the conclusion (Section 7).

In subsection 2.1 we discuss two ways the stochastic optimal control problem modeling the IS order can be modified to delay/stop liquidation depending on price behavior 1) by relaxing the full liquidation constraint if the price is too low (which was first proposed in [16]) 2) stopping/pausing trade if the price is too low (proposed in the present work). These two modifications are parameterized in the stochastic optimal control problem by a measurable set and a process taking values in . The set prescribes when full liquidation is required and enters the stochastic optimal control problem as a part of the terminal cost; the process prescribes when trading takes place and enters the stochastic optimal control problem by multiplying the volume process (see (13)). We give four examples for and in subsection 2.1 which are all based on a lower bound specified for the price process: puts no constraints on trading, the position is constrained to be fully closed if the closing price is above a given threshold; allows trading until the price goes below a given threshold, the position is constrained to be fully closed if the price remains above the given threshold across the whole trading interval; allows trading only when the price is above a given threshold, the position is constrained to be fully closed if the closing price is above the given threshold; is the same as previous except that for trading to restart the price process first has to upcross a higher threshold. The resulting stochastic optimal control problem for the modified IS order is given in (13). This problem has the same structure as the one studied in [16] except for the following differences: 1) inclusion of the permanent market impact in the model implies that the terminal cost can take negative values 2) the presence of the term in the running cost (for and the problem in fact reduces to the one studied in [16]). The solution method in [16] is the derivation and the analysis of a BSDE associated with the value function of the control problem. This is also one of the solutions approaches we will pursue in the present work. We next discuss how the above new features of the problem impact the associated BSDE and its analysis.

The set (specifying conditions for full liquidation) defines the singular component of the terminal condition of the BSDE; allowing a nontrivial permanent price impact term introduces an additional negative term in the terminal condition of the BSDE. The driver of a BSDE is said to be monotone if there exists such that for any and almost surely. The monotonicity of the driver is a key property in establishing the existence of solutions to BSDE. The work [16] focuses on non-negative terminal costs; a non-negative terminal cost corresponds to a nonnegative terminal condition for the associated BSDE. This and the dynamics and cost structure of the control problem lead in [16] to a BSDE with the monotone driver (for , ). In the case of the stochastic optimal control problem (13), the terminal condition is allowed to take negative values and this forces us to work with the non-monotone convex driver Finally, as already noted, the process (specifying when trading is allowed) enters the BSDE by multiplying the driver of the BSDE. The resulting BSDE is given in (25) and (23).

Note that although the terminal condition (23) can take negative values, the negative component is bounded above by a constant. For this reason we focus on terminal conditions with bounded negative parts. The challenges/new points that arise in the analysis of (25), (23) as a result of these new features are as follows: the currently available literature doesn’t contain existence results on the minimal supersolution of a BSDE such as (25) with a singular terminal condition (23) and with a driver involving the function Secondly, a terminal condition that can take negative values and the superlinearity of the driver imply that the solution of the BSDE can explode to backwards in time.

We handle both of these issues in Section 3 by deriving an apriori lower bound process on any supersolution of the BSDE with a terminal condition whose negative part is bounded by a constant ; is obtained by solving (25) with the terminal condition (for which (25) reduces to an ordinary differential equation). The interval over which is defined depends on model parameters. We introduce an assumption on the permanent price impact parameter and market volume that guarantees the existence and boundedness of the lower bound process over the interval (Assumption 1). The lower bound process is increasing in ; therefore, the value provides a lower bound on supersolutions on the whole interval We then deal with the non-monotonicity of the driver by replacing the portion of over with its linear approximation over the same interval, which results in a monotone driver. Hence existence and uniqueness of the solution for BSDE for integrable terminal condition is obtained in Proposition 3.1. The only way the term impacts the analysis of the BSDE is by entering Assumption 2 that guarantees that the supersolution can attain the singular value at terminal time ; in particular Assumption 2 requires for for some Under these conditions, Proposition 3.2 provides a minimal supersolution for the BSDE with singular terminal condition.

The verification argument presented in subsection 3.1 connects the minimal supersolution of the BSDE (25), (22) to the value function and optimal control of the stochastic optimal control problem (13) (Proposition 3.3). This argument is based on the convexity of the cost in ; under Assumption 2, this turns out to be the case only for the quadratic case (Lemma 2), therefore this verification argument assumes

Assumption 2 is a stringent condition and , , proposed in subsection 2.1 (see (15), (16) and (17)) which depend on price behavior don’t satisfy it. In subsections 3.2 and 3.3, we break up the stochastic optimal control problem and the BSDE corresponding to these choices of into pieces where each piece involving a singular terminal condition satisfies Assumption 2 (Proposition 3.5 and Lemma 4).

The main advantage of the BSDE arguments in Section 3 is that we can work with a general filtration, without any further assumption except the standard ones (completeness and right-continuity) and the left-continuity at time . The drawback is the restriction to the quadratic case

We call the problem Markovian if the price process is Markovian and the cost structure of the problem is a function of the price process. In Section 4 we explore the case and a PDE representation of the value function and the optimal control when the problem is Markovian or can be broken into Markovian pieces. A popular choice for price dynamics in finance applications is the stochastic volatility model. To the best of our knowledge it is rarely treated in the context of optimal liquidation; in Section 4 we assume the price dynamics to follow this model. For a direct PDE representation (i.e., identifying the value function as a supersolution of a related PDE), the process and the measurable set must also be functions of the price process. Of the four possible choices for and given in (14)-(17), only is given as a function of the price process. In subsection 4.1 we present the PDE representation of this case. For , , the decompositions/reductions given in subsections 3.2 and 3.3 yield Markovian subproblems. The resulting PDE problems are treated in subsections 4.2-4.4. The PDE representation of involves two coupled PDE (one for active trading and one when trading is paused). To compute a solution we introduce an additional parameter , which is the number of switches allowed between trading and no trading. We solve this problem recursively, letting gives the solution to the coupled PDE. To the best of our knowledge, there exists no readily available results in the current literature for the existence and smoothness of solutions of PDE that arise in the analysis presented in Section 4. We obtain solutions to these PDE as follows: we use the BSDE results of Section 3 to first obtain viscosity supersolutions. We then use regularization bootstrapping, parameter smoothing and the regularity of the underlying price process to obtain the smoothness of these supersolutions. Once smoothness is proved classical verification arguments from stochastic optimal control can be constructed to relate the solutions to the stochastic optimal control problems. These arguments do not require as opposed to the verification arguments given in Section 3 which are directly based on the BSDE representation.

The output of the standard IS order is the cash position at time generated by the trading algorithm; under the assumption that the price process is a Brownian motion, turns out to be normally distributed whose mean and variance have simple formulas in terms of the model parameters. When we relax the IS order so that full liquidation is no longer required at terminal time, the output of the IS order consists of the pair of real random variables where is, as before, the total cash generated by the trading process and is the remaining position at terminal time in the asset being traded. For the relaxed/modified IS orders, is not normally distributed even when the price process is taken to be Brownian and the joint distribution of doesn’t have an explicit form. Define

| (1) |

is the percentage deviation from the target price of the average price at which the position is (partially) closed in the time interval In Section 5 we study the joint distribution of . We note that can be divided into three pieces: one corresponding to permanent price impact (), one corresponding to transaction/bid-ask spread costs () and one corresponding to random fluctuations in the price (). turns out to be a linear function of ; therefore, its distribution is fully determined by that of . We provide a numerical study of the distribution of and the conditional distributions of and given under the assumption that for the case . The same section also provides numerical examples of the sample path behavior of the optimal controls of this modified IS order. Section 7 comments further on the models presented in this work and on possible future research.

2 Definitions

The following model is based on the Almgren Chriss framework for liquidation with price impact (see, e.g., [14, Chapter 3]). Everything is assumed to be defined on a probability space equipped with a filtration , which satisfies the usual assumptions: completeness and right-continuity. The market volume at time is denoted by , which is a positive process adapted to the filtration The initial position is denoted by The position of the investor at time is , in particular The process is assumed to be absolutely continuous in the time variable, let denote its derivative at time ; and are adapted to

We will be working with two positive real numbers and that are Hölder conjugates of each other ; we use in the problem formulation, appears in the associated backward stochastic and partial differential equations.

We suppose that the permanent price impact function is

| (2) |

where is a real constant. For (), decreases (increases) with position size and for it is independent of position size. For , reduces to which is the standard choice for permanent price impact (see [12] or [14, Chapter 3]). The midprice process is

| (3) |

where is a martingale adapted to .

The actual trading price at time is where models transaction costs and the bid-ask spread ( depends on , and ). The process is often specified via the so-called execution cost function : . The actual trading price at time , expressed in terms of is

The cash position that generates is

| (4) |

( corresponds to selling, hence an increase in , and corresponds to buying, a decrease in ). Note that ; this and integrating the first term by parts give:

Then

where

Let us first review the classical IS order, in which the position is required to be closed fully at terminal time, i.e., we impose the constraint on the problem. The terminal cash position under this constraint is

| (5) |

To identify the optimal liquidation strategy one maximizes the expected utility , over the admissible strategies , where is the utility function of the trader. The standard choice for the utility function in optimal liquidation literature is

| (6) |

where is the risk aversion parameter of the investor [14]. In the current work we will be focusing on the case , for which the problem becomes555Using when goes to zero.

| (7) |

with

see Definition 2.1 below. The term is a martingale666In general it is only a local martingale. However we will show that for the optimal strategy, is bounded. Hence there is no harm in assuming that this process is indeed a martingale. ; taking the expectation of in (5), (7) reduces to

This is the standard version of the stochastic optimal control formulation of the IS order in the Almgren Chriss framework for This problem and its generalization where is a well studied problem in the current literature, as in [13, 24, 25]. In the next subsection we propose several modifications to this problem relaxing the constraint and introducing constraints on when trading takes place.

2.1 Modifications

When full liquidation is no longer required, i.e., when we don’t have the constraint , the output of the trading process at time will be where is the cash generated by the trading process and is the position remaining in the asset being traded. As discussed in the introduction, to formulate a utility maximization problem similar to (7), we assign a monetary value to the position and add it to . In the present work we mainly focus on the following simple choice for : the market value of the position at terminal time ignoring trading costs, i.e., . With this choice, the monetary value of the position is

| (8) |

Recall that our goal is to modify the IS order to not liquidate depending on price behavior in two ways 1) by relaxing the full liquidation constraint if the price is too low 2) stopping/pausing trade if the price is too low. The following formulation allows both of these possibilities. Let be an adapted process taking values in Let be a measurable set. The trading set is defined by

Definition 2.1.

Define as the set of processes that satisfy:

-

•

is absolutely continuous in and is progressively measurable ;

-

•

;

-

•

if (liquidation constraint) ;

-

•

for -almost every , (if , ) ;

-

•

the cost

belongs to for some .

For ease of notation set

| (9) |

i.e., when and we simply write instead of

We modify (7) to

The formula (8) implies that this control problem is equivalent to:

As noted in the introduction we work with the execution cost function

where is an adapted and positive valued process. This choice of reduces the problem to

| (10) |

Let us next note that can always be assumed to be by appropriately modifying the volume process, i.e., if we set

| (11) |

(10) can be written as

in what follows we always assume and that Vol is modified to if the original process is not identically . A commonly used convention in the prior literature is

| (12) |

In addition to this we will also set and for With these conventions (10) can be written as

| (13) |

where we use the convention (9). Note that the process controls when trading takes place (by effectively switching the volume process on and off) and the event controls when full liquidation is required.

In the next section we obtain a representation of the value function and the optimal control of the problem (13) via the minimal supersolution of an associated BSDE. Before that let us give several examples for the process and the event The midprice process consists of two components: and The first component, , is the random component of the change in the midprice; a large and unpredictable drop in price that the investor may fear can only arise from this component. Given this observation, a reasonable approach in choosing and is by putting a lower bound on this component. For this, define:

Then some possible choices for and are:

| (14) | ||||

| trading is allowed at all times, full liquidation is forced only when the terminal price is above . | ||||

| (15) | ||||

| trading stops once hits the lower bound ; full liquidation takes place if remains above throughout | ||||

| (16) | ||||

trading pauses when the price is below , full liquidation takes place if the price process remains above in the time interval and trading stops if goes below in the same interval; is a small fixed constant.

Let us comment on the parameter in this formulation: essentially we would like to continue with the liquidation when the price is not too below our target price and close the position fully if the terminal price is also near our target price. However, allowing trading (re)start arbitrarily close to and forcing a full liquidation implies high transaction costs (in fact, transaction costs under the current model). This is the reason for the parameter: full liquidation is forced only if the price remains above in the time interval

In the last formulation trading pauses once hits ; if is a continuous diffusion process, once it hits , it will hit infinitely often and the trading process will switch on and off infinitely often as crosses . One can get a discrete sequence of on and off trading intervals by putting a buffer of size above between trading and no trading; once trading pauses, it is turned back on once goes above The corresponding and are expressed through the following sequence of hitting times:

Adding a buffer of size between no-trading and trading in (16) amounts to the following definitions:

| (17) |

3 BSDE Analysis

In our arguments the concepts of monotonicity (of the driver of a BSDE) and the minimal supersolution of a BSDE play a key role, let us begin by giving a precise definition of these terms.

Definition 3.1.

The function is said to be monotone if there exists such that a.s. and for any and ,

Let be an -measurable real valued random variable. A pair is said to be a supersolution of the BSDE

if

-

1.

is adapted to ;

-

2.

is a martingale777In this paper, we always consider a right-continuous with left limits modification of the martingale ;

-

3.

for ;

-

4.

the inequality

(18) holds a.s..

It is said to be minimal if a.s. for any , for any other supersolution

The work [16] studies the following stochastic optimal control problem:

| (19) |

where: is a non-negative random variable that is allowed to take the value , is the absolutely continuous part of , is the jumping part of , a running cost associated with , and an appropriate modification of On the set , the constraint is necessary to ensure a finite cost. Compared to (13) this problem has an additional term in its dynamics and two additional terms ( and ) in its cost structure. To focus on the novelties associated with the terminal cost we will assume these terms to be . The work [16] identifies the value function of (19) as where is the minimal supersolution of the BSDE

| (20) |

The generator of this BSDE is monotone and establishing the existence of the minimal supersolution makes use of this property of the generator. The reason that [16] is able to use this monotone generator is the assumption . In the present work we allow to take negative values therefore it is no longer possible to work with a generator involving the function . The BSDE corresponding to the stochastic optimal control problem (13) turns out to be

| (21) |

with terminal condition

| (22) |

| (23) |

(a rigorous link between this BSDE and (13) will be established in subsection 3.1 via a verification argument).

Define

| (24) |

vol is the restricted volume process available to the trader (up to some constant). Then we can write (21) also as

| (25) |

Compared to (20) the novel features of (25), (22) are the following: its terminal condition is allowed to take negative values, its driver is convex in and not monotone and its generator can take the value (because of the presence of the term). We introduce several assumptions to deal with these new features when obtaining the existence of a minimal supersolution to this BSDE. First, note that the terminal condition of (23) is bounded below by ; for this reason for our purposes it suffices to focus on terminal conditions whose negative parts are bounded above by a constant, i.e., all of the terminal conditions we consider satisfy

The generator of (25) is defined in terms of the function and its terminal value can take negative values: a consequence of these facts is that any solution to (25) and (22) can explode to backward in time (see Lemma 1 below). To deal with this, we introduce the following assumption that ensures that an explosion doesn’t happen in :

Assumption 1.

is non-negative and one of the next two conditions holds:

-

•

is deterministic and satisfies

(26) -

•

is bounded by a constant such that

(27)

We will assume throughout that either (26) or (27) holds. Note that when satisfies one of these, also does because This assumption balances the negative part of the terminal condition (determined by the permanent price impact parameter ) with the trading volume available to the trader.

If , can take the value with positive probability and the terminal condition is said to be singular (terminal condition is said to be singular also when doesn’t belong to for some ). We need a further assumption to deal with this possible singularity. To ensure that there exists a solution which is finite on , the generator should not be equal to zero close to time . The corresponding assumption in [16] is [16, (A.6)], which is: . In the present work, to guarantee the existence of a minimal supersolution, we make the following assumption on :

Assumption 2.

There exists some and some such that

| (28) |

Evoke that is the Hölder conjugate of .

Assumption 2 can be interpreted as the availability of liquidity (through Vol and ) at terminal time. In particular it means that on .

We begin our analysis by deriving a lower bound process which we will use to guarantee that the minimal supersolution to (20) doesn’t explode to in . Under Assumption 1 the lower bound process is defined as follows:

| (29) |

if (26) holds; and

| (30) |

if (27) holds.

Lemma 1.

Proof.

The standard way to obtain the minimal supersolution of a BSDE with a singular terminal condition is approximation from below, i.e., we truncate the terminal condition to , solve the resulting BSDE and let . Therefore, the treatment of singular terminal values requires the solution of the same BSDE with bounded/integrable terminal values. The next proposition addresses such terminal values:

Proposition 3.1.

In the Brownian setting, is replaced by and

Proof.

Recall that the generator is not monotone. However, if the negative part of the solution is bounded by some constant , that is, if is bounded from below by , then we can replace the generator by a monotone continuous generator defined as follows:

| (33) |

This generator is indeed monotone since

for any Since ,

Furthermore, by Assumption 1, vol belongs to almost surely. These imply that the uniqueness result for BSDE driven by a monotone generator ([19, Proposition 5.24] or [15, Lemma 5]) apply in our current setting; therefore, if it exists and if its negative part is bounded, the solution of (25) is unique.

We know from Lemma 1 that the process is bounded from below by . Consider the generator and the BSDE

| (34) |

Since is monotone with respect to and since , BSDE (34) has a unique solution (see again [19, Proposition 5.24] or [15, Theorems 1 and 2]). Note that for , the solution is . Since , the comparison principle ([15, Proposition 4] or [19, Proposition 5.33]) states that a.s. for any . In other words is a solution of the BSDE (25), and this achieves the proof of the proposition. ∎

Remark 1 (On the negative part of ).

Itô-Tanaka formula (applied to and ) implies that is a subsolution of the BSDE

| (35) |

The generator is not monotone. However, it is increasing and positive. From Lemma 1, is a bounded supersolution of this BSDE. Following [8], we deduce the existence of a minimal bounded supersolution which is also bounded and non-negative (see [8, Theorems 3.3 and 4.1]). Using again , we deduce that in fact is the unique solution of the BSDE (35). Therefore, assumptions in the previous proposition can be replaced by the existence of a supersolution to the BSDE (35). In other words, these assumptions are sufficient to obtain a supersolution, but not necessary. As a by-product of these calculations, we obtain a better bound: . almost surely for any

Remark 2 (On the positive part of ).

Consider the BSDE

where is the solution of (35). is bounded by and imply that the driver is monotone:

and the existence and uniqueness of the solution holds, if belongs to some space . Define and :

Hence, solves the BSDE (25) and holds almost surely for

Another estimate can be obtained using the Itô-Tanaka formula since

If solves the BSDE with monotone generator

the comparison principle implies that a.s. for any , .

Our main result on the BSDE (25) when its terminal condition is singular is the following:

Proposition 3.2.

Suppose and Assumptions 1 and 2 hold. Assume that the filtration is left-continuous at time . Then there exists a minimal888among all supersolutions with bounded negative part supersolution to the BSDE (25) with terminal condition such that has a left-limit at time and the negative part of this minimal supersolution is bounded.

Several points: there is no condition on , the only condition on is , in particular, the terminal condition (23) arising from the stochastic optimal control problem satisfies the conditions of this proposition. Condition (28) implies that vol should remain away from zero close to .

Proof.

The proof proceeds parallel to that of [16, Proposition 3]. Let us consider for any

The solution of

has the same upper bound for the negative part for any . Using the comparison principle for monotone BSDE, arguing as in [16] gives

From Remark 2, with

From [16, Lemma 1], we have

for any , almost surely. Therefore, from (28), , , is finite and bounded in uniformly with respect to . In particular, for any , there exists a constant such that for any ,

Stability result for BSDE ([19, Theorem 5.10]) shows that converges to :

Thus solves (25): for any

Moreover . And since the filtration is left-continuous at time , we obtain that a.s.

Finally, minimality can be obtained as in the proof of [16, Proposition 4]. If is another supersolution, we add to both solutions and the quantity and the same arguments on and lead to a.s. .

The only remaining problem is the existence of a limit at time . Compared to [21, Theorem 2.1], the novelty is the negative part of or of , which approximates . To deal with the negative part, we can apply the arguments of the proof of [21, Theorem 2.1] using the function

( can be defined in terms of the hypergeometric functions):

where and are two non-negative supermartingales such that converges a.s. to zero. To obtain this result, we crucially use that the negative part of is bounded uniformly with respect to and also that the martingale is uniformly bounded in the sense that there exists a constant such that for any

To obtain this last inequality, the Itô-Tanaka formula for is applied (see Remark 1 and Equation (35)). Since the negative part of is bounded, a apriori estimate for BSDE ([19, Proposition 5.7] or [15, Proposition 2]) leads to this uniform estimate on . The other arguments can be copied from the proof of [21, Theorem 2.1] with straightforward modifications. This achieves the proof. ∎

Our next task is to relate the solution/minimal supersolution of the BSDE (25) to the solution of the stochastic optimal control problem (13).

3.1 Solution of the quadratic stochastic optimal control problem

The goal of this subsection is to relate the minimal supersolution of the BSDE (25) with terminal condition (22) to the solution of the stochastic optimal control problem (13). This will be achieved through a verification argument based on the convexity of the cost structure of (13). The convex structure holds only for , for this reason in this subsection we assume We deal with the case in the next section in a Markovian framework.

For ease of reference let us restate our stochastic optimal control problem (13):

| (36) |

we remind the reader that in the second formulation we are using the convention (12); the definitions of , and vol are given Definition (2.1), (9) and (24).

Remark 3.

Our goal is to prove the following result:

Proposition 3.3.

Suppose Suppose Assumptions 1 and 2 hold, suppose and let be the minimal supersolution of (25), (22). Then

| (37) |

(equivalently, ) is the optimal state process for the stochastic optimal control problem (36). Moreover the value function of (36) at time , namely

is given by ( is defined by Definition 2.1, but the process starts at time from the deterministic position ).

The proof directly follows from the next two lemmas and is given at the end of this subsection. Let’s call the expression inside the in (36): for

We start with the following observation:

Lemma 2.

If

| (38) |

almost surely, then the functional is strictly convex. The Gâteaux derivative of at point in direction , is given by

Proof.

Taking and and , we have

We use the Cauchy-Schwarz inequality for the inequality. Now for any and and

Letting to zero gives the desired formula. ∎

The last intermediate result we need is a version of Proposition 3.3 where is bounded.

Lemma 3.

Proof.

Note that for bounded , the BSDE (25) with terminal condition has a unique solution and it equals the minimal supersolution: , . Since is bounded, from Proposition 3.1, is bounded and for any

Thus

is also bounded and from Assumption 1

is bounded. Thus is in .

Let be in with -integrability, and define , and . If

integration by parts gives:

Hence and are martingales (since is bounded). Moreover

this and 3 imply

Hence is also a martingale.

Now integration by parts implies:

This and Lemma 2 give

which is a martingale. With the convexity of we obtain

Therefore, is the optimal control (unique from the strict convexity of ). Itô’s formula applied to gives

Since is a martingale,

In other words is the value function of the control problem. ∎

We now give

Proof of Proposition 3.3.

For , one can use arguments parallel to those in the proof of the previous lemma to show that is a martingale on . Since is bounded (by ) we have

This and Assumption 1 imply that is also bounded. Since is also bounded, the martingale is bounded from below. Therefore, the limit at time of exists in and

tends to zero a.s. on the set , since .

Now we apply Itô’s formula to : for any

with . Taking the conditional expectation we get

By the the monotone convergence theorem

And by Fatou’s lemma ( is bounded)

Recall the definition of and that the limit of at time exists in . Moreover , when . Therefore, if , then

(with the convention ). If , then

In both cases we obtain

Thus dominates the value function of the constrained control problem.

Now if is in , it is in (no terminal constraint on ). Therefore, the value function dominates the value function of the unconstrained control problem with terminal penalty , for any . Denote by the solution of the BSDE (25) with bounded terminal value . From Lemma (3), is the value function of the unconstrained control problem. We deduce that for any

Since converges to , we obtain that is the value function of the constrained control problem and that is the optimal state process.

3.2 Reduction to random time interval for

In general, for any . therefore, for , Assumption 2 in general doesn’t hold regardless of what Vol is. For a natural way to deal with this is to consider the problem on the random interval : for we have , for Therefore, the stochastic optimal control problem (13) can also be expressed as

| (39) |

The corresponding BSDE is again (25) but with terminal condition

| (40) |

and we have a BSDE with random terminal time . Note that now the dynamics of is considered only on the random interval and on this random interval.

The next proposition (formulated in terms of a general stopping time ) states that the BSDE (25) has a minimal supersolution for terminal conditions of the form

| (41) |

where is a stopping time and , are bounded from below by and is also bounded from above; (40) is a special case of (41).

Proposition 3.4.

Assumption 1 holds. Let be as in (41). If for some

| (42) |

then the BSDE (25) with terminal condition (41) has a unique solution such that

-

•

-a.s., on the set , and ,

-

•

-a.s., for all ,

-

•

and for some constant depending on , and

If, instead of the integrability condition (42) on , the following modified version of condition (28) holds

| (43) |

then there exists a minimal supersolution for the BSDE (25) with terminal condition (41).

Proof.

The first part of the claim comes from [15, Proposition 6] on BSDEs with random terminal time. Note that our terminal time is bounded. As in the proof of Proposition 3.1, since the negative part of the data is bounded, we can modify the generator in order to have a monotone generator (see Equation (33)).

In the singular case, we proceed by truncation. For sufficiently large:

Again we construct a sequence of solutions , such that is non-decreasing. It only remains to control , uniformly in .

We define as the solution with terminal condition . Note that is bounded. Now for any we have

Hence solves the BSDE with terminal condition and generator

Once again, the map is not monotone on . But since the negative part of the data is bounded, we can modify on , such that becomes monotone (see Equation (33)). And again by the comparison principle, is non-negative.

To control , we again follow the arguments of [16, Lemma 1]. Young’s inequality implies that for any and

Recall that is the Hölder conjugate of . Thus with

Since if , explicit solution for linear BSDE and comparison principle imply that for

This uniform bound on , thus on , allows us to define the solution of the BSDE with terminal time and a singular terminal condition. ∎

For we have and for the existence of a minimal supersolution Vol must satisfy (43). The next proposition connects the value function of (39) to the minimal supersolution whose existence was derived above.

Proposition 3.5.

3.3 Reduction to time interval for and

As already noted, for and , Assumption 2 doesn’t hold in general since both and can be zero for arbitrarily close to . However, in both of these cases the problem can be reduced to the time interval where this assumption is no longer needed.

Both and consist of two phases: before and after time , the reason for this was explained in the paragraph following (16). In both cases the trading process for and proceeds exactly as in after time : if the algorithm is in trading mode at time , the position is fully closed only when the price remains above throughout the interval ; trading stops (and doesn’t restart) if the price hits . This implies that the stochastic optimal control problem (36) can be written as

| (44) |

where is the value function of the stochastic optimal control problem corresponding to on the time interval with initial position For , we know by Proposition 3.5 that where is the minimal supersolution of the BSDE (25) on the time interval with terminal condition

Existence of follows from Proposition 3.4. Then for , (44) can be written as

with terminal cost factor

| (45) |

is -measurable and belongs to . Now consider the solution of the BSDE (25) on the time interval with the -measurable terminal condition of (45). Define

Lemma 4.

Suppose . For any ,

(equivalently, ) is the optimal control for the stochastic optimal control problem corresponding to or . Moreover, the value function of the same control problem at time equals

Proof.

From our previous arguments, we know that if is the derivative of , with starting point , then for any other strategy we have

| (46) |

Now let us define for

and . From Proposition 3.5, is the value function of the related control problem starting at time from :

| (47) |

for any process with derivative starting at time from . Multiplying this equality by , we obtain

If for

we have

and therefore

From (46) and (47), we deduce the optimality of the defined process . ∎

4 PDE Analysis

In this section, we will assume the price process to be Markovian and the cost structure to be a function of the price process; under these assumptions, our goal is to relate the value function of the stochastic optimal control problem (13) to a PDE version of the BSDE for the four choices of and given in (14)-(17).

As noted in the introduction, we assume the price process to be driven by a stochastic volatility model:

where is the stochastic volatility process:

| (48) |

is a Brownian motion in (, , have unit variance, but they are correlated with coefficient ). We assume that the Feller condition, , ensuring a positive process holds. Let denote the second-order differential operator corresponding to these dynamics:

| (49) |

The variables belong to .

To get a PDE representation we take and Vol processes to be functions of . With a slight abuse of notation, we assume the market volume process to be where is a non negative valued function; similarly the transaction cost process is where is a strictly positive valued function. In this section we still use (11) and (24), we denote by Vol the quantity , and will use the assumption (27) on vol:

| (50) |

where and is the constant in the permanent impact given by (2).

4.1 PDE representation for

In this subsection we assume , i.e., Let us consider terminal values of the form

| (51) |

where

| (52) |

is a measurable function. By (23), the choice corresponds to the function

Under the Markovian assumptions of the present section, and for the BSDE (25) and the terminal condition (51) correspond to the following PDE: for any and

| (53) |

with the terminal constraint

| (54) |

Our goal, under the Markovian assumptions of the present section, is to prove that the value function of the stochastic optimal control problem (13) with and can be expressed as a multiple of the unique solution of this PDE with terminal condition To express the value function as a solution to the above PDE, we first extend the stochastic optimal control problem (13) to allow it to start from any time point . Accordingly, we define

Under our assumptions on Vol and , Proposition 3.2 implies that the following BSDE has a unique minimal supersolution:

set

| (55) |

As we already noted, our goal in this subsection is to prove that is the minimal supersolution (or the unique solution if is finite) of the PDE (53) for any of the form (52) (and in particular for ). Our first step in this direction is the following:

Lemma 5.

If is continuous and with polynomial growth on and if is also continuous on , then is a continuous function of and is the unique viscosity solution of the PDE (53) with polynomial growth on .

Proof.

See [19, Theorem 5.37] or [5, Theorems 3.4 and 3.5] (see also [22]). If is bounded, the solution and thus are also bounded. Hence our generator is Lipschitz continuous.

If satisfies , then satisfies the condition imposed in Proposition 3.1. Thus and thus are bounded from below, and we can modify our generator such that it becomes monotone (see the proof of Proposition 3.1). Then existence and uniqueness follow from [19, Theorem 5.37] (this result is stated for in [19] but all arguments continue to work when ). ∎

Now suppose that is a continuous function from to . We use the proof of Proposition 3.2. For any , we consider the bounded function . By the previous lemma there exists a unique bounded viscosity solution and by comparison principle,

is well-defined with a bounded negative part. Suppose now that for some and some :

Then Condition (28) holds and we have on ,

| (56) |

On the rest of the interval , the bound of the solution is controlled by the previous estimate with . In other words we have a bound on which does not depend on . Hence is lower semi-continuous on and finite (even locally bounded) on . These considerations give us the following result:

Lemma 6.

Suppose is a continuous function from to ; then is the minimal viscosity solution of the PDE (53) on (among all viscosity solutions with bounded negative part).

Proof.

See [22, Theorem 1]. ∎

The concept of a viscosity solution allows even a discontinuous solution and doesn’t address the issue of smoothness/regularity of the solution; therefore the previous result doesn’t say anything about the regularity of . The properties of the operator (and smoothness assumptions on Vol and ) allow us to establish the smoothness of , with a regularization bootstrap argument for parabolic PDE. (see [26, Lemma 5] for a similar argument).

Lemma 7.

Proof.

Fix some and a compact subset of . First note that from (56), the bound of on does not depend on the terminal value, that is on , but only on and .

Moreover, the operator can be written as follows:

with

and

Our coefficients and are bounded on , and is uniformly elliptic on . Since vol is also continuously differentiable with respect to all of their arguments, then we can easily check that all conditions called a) (uniform ellipticity and boundedness condition), b) (growth condition on the derivatives, take ) and c) (regularity condition) of [17, Theorem VI.4.4] hold. From this theorem, if there exists a function continuous on and is of class for some (space of functions which are with -Hölder continuous second derivatives in the space variable and with -Hölder continuous in the times variable ), then the PDE

with the boundary condition , has a unique solution with the same regularity as . Now our viscosity solutions are continuous and bounded on . Let us consider a sequence of smooth mollifiers and define . There exists a classical smooth solution of the PDE (53) with boundary condition and pointwise converges to as goes to . As , the bound of on does not depend on and .

In the next step, we prove that belongs to (space of functions which -Hölder continuous in the space variable and -Hölder continuous in the times variable ) and that the norm of in this space does not depend on and . Note that Conditions (1.2) and (7.1) of [17, Chapter 3] are satisfied. Suppose that is a smooth solution of the PDE (53) on : for any

such that for any and any compact subset of , is bounded on . Thus solves on the PDE

where is a bounded function. We can apply [17, Theorem III.10.1]. Hence is in . The value of and the Hölder norm of depend on , and the bound on . In other words does not depend on the terminal value.

In the last step, we get the desired regularity. Now we know that belongs to and solves the PDE

Since vol is also in , then from [17, Theorem IV.10.1], is in for any and , and the norm depends only on the -norm of . Therefore, , and thus , belong to the same space999The Arzela-Ascoli theorem implies that (up to a subsequence) converges to some function . Here since pointwise convergence has been proved before., that is on any subset , and are in . ∎

The proof also shows that the regularity of any solution does not depend on the terminal value. In other words, far from and , the solutions are smooth and classical solutions.

Let us summarize the foregoing results:

Proposition 4.1.

Suppose that is continuously differentiable on , that is bounded from below by and that (27) holds. If one of the next conditions holds:

-

•

is continuous and with polynomial growth on ,

-

•

is continuous from to and for some and

then there exists a viscosity solution of the PDE (53) with terminal value . Moreover is of class and is the minimal viscosity solution (among all viscosity solutions with bounded negative part).

Remark 5.

The particular dynamics for is not important, as soon as the related operator regularizes the solution of the PDE.

Remark 6.

Here we use the existence of a solution for the BSDE to deduce the existence of a viscosity solution for the PDE and then we prove the regularity of the solution. The existence of a solution for the PDE could be directly proved (without probabilistic arguments) starting from [17, Theorem V.8.1]. The proof would involve arguments similar to those given above because of the lack of monotonicity (see Assumption b) in [17, Theorem V.8.1] or Condition (4.17) in [11, Chapter 7]). Hence the proof of existence of solutions using PDE arguments will be as involved as the BSDE based approach given above.

Let us next comment on the smoothness of on the boundary , called the hyperbolic part of the boundary. Recall that our operator is defined by (49) and that the dynamics of is given by (48). The Feller condition ensuring a positive process is . Under this condition, the Fichera function

is positive when goes to zero. Hence no boundary condition has to be supplied on (see for example [6]).

For the control problem, we have to consider the terminal condition

Note that we cannot directly apply Proposition 4.1, since is not continuous. Nonetheless

Lemma 8.

There exists a minimal viscosity solution , which is of class on .

Proof.

Indeed let us define

and

is continuous and non-decreasing with respect to and converges to . Therefore, the related continuous viscosity solutions converge to . Arguing as in the proof of Proposition 4.1, we obtain a uniform norm of in the space , for any compact subset of . Then we pass on the limit on to obtain the desired result. Minimality can be obtained as for Proposition 4.1. ∎

Next we connect the solutions of PDE obtained above to the value function of the control problem.

Extended control problem

The function corresponding to the permanent impact given by (2) is and the control problem (13) is

| (57) |

For , by Proposition 3.3, is the value function of the extended version of the stochastic optimal control problem. With a slight abuse of language, we will refer to simply as the value function of the extended stochastic optimal control problem with terminal cost

These give us the main result of this subsection:

Proposition 4.2.

Proof.

Since the proof is quite standard, let us provide an outline of the main arguments. First standard computations show that for any :

and that the infimum is attained at

If is continuous and bounded, by Proposition 4.1, is of class and bounded and continuous on . Now define This function has the same regularity as with respect to and is of class with respect to . Take and is its derivative. Then Itô’s formula leads to: for any

Note that . Thus

Hence we obtain

Letting tend to and taking the expectation, we have

Moreover if we take

we have an equality. The first part of the proposition is proved.

If , then is not continuous at time , but on . Hence for any :

We take the expectation and we use Fatou’s lemma:

A direct computation shows that is a martingale on . This martingale being bounded from below, it has a limit at time . Arguing as at the end of the proof of Proposition 3.3, we deduce that

Using the proof of Lemma 8, we obtain a sequence of smooth functions such that is the value function of (57) with as terminal condition. Hence

Passing through the limit on and then on achieves the proof of this proposition. ∎

An optimal state process given by (58) can be written:

And our proof shows that this control is admissible and

However, even for bounded , and except in the case , the lack of convexity prevents us proving equality. Therefore the Markovian setting and the fact that the solution of the HJB equation is smooth, are crucial to extend our result to any .

4.2 PDE representation for and

To get a PDE representation of the BSDE (25), (22) for , we consider the problem in the interval . As discussed in subsection 3.2, the corresponding BSDE is again (25) but with terminal condition (40). This reduced formulation of the problem is indeed Markovian. The PDE is the same as before (53) but solved over the domain and with boundary conditions

| (59) |

The value function of the extended version of the stochastic control problem is again defined through (55) and we have:

Proposition 4.3.

The proof proceeds parallel to the arguments given in the previous section. We therefore provide an outline. We begin by considering the case where the boundary condition is given by

| (60) |

where is a continuous and bounded function. If is bounded and if the compatibility constraint is verified, we can directly apply [19, Theorem 5.41] to obtain the existence of a unique viscosity bounded and continuous solution of the PDE (53) with the boundary condition (60). The regularity inside the domain can be obtained by the arguments of Lemma 7. If the compatibility condition does not hold, the solution still exists but is not continuous up to the boundary. Finally, the terminal condition can be handled via approximation from below (as was done in the previous section as well as in Section 3 in the treatment of the BSDE (25) and the singular terminal condition (22)).

4.3 PDE representation for and

In Section 3.3, we already explain how to reduce the problem on the interval . Let us consider the PDE

on the set , with terminal condition at time and on the lateral boundary . From the previous section, there exists a unique solution defined on .

Following the representation given by (45), we define

and solve

| (61) |

over with terminal boundary condition

Note that the terminal boundary condition is bounded and continuous. Nonetheless the free term is not continuous at .

Lemma 9.

There exists a function such that is bounded and continuous on and is a solution of class of the PDE (61) on .

Proof.

To circumvent the discontinuity of , let us introduce

This function is Lipschitz continuous with respect to , satisfies and converges increasingly and pointwise to when tends to zero.

From standard arguments (see [19, Theorem 5.37]), there exists a unique bounded and continuous viscosity solution of the PDE

with the same terminal condition as . Note that the bounds on do not depend on . Thus arguing as in Lemma 7, we can prove that is of class on with a norm independent of .

The comparison principle shows that is a decreasing sequence and thus we can define as the decreasing limit of as tends to zero. We obtain immediately that is bounded and upper semi-continuous and is a viscosity subsolution of PDE (61) (well-known result on stability for viscosity solutions [7]).

The only remaining point concerns the continuity of on the set . Let us define another approximating sequence defined as the solution of PDE (61) where is replaced by :

As , converges to , which is lower semi-continuous and is a viscosity supersolution of PDE (61). Moreover by comparison principle, . Comparing sub- and supersolution implies that (standard result for viscosity solution). Let us prove this statement in our case. For any we have

Here

Using the boundedness of and (uniformly with respect to ) and standard stability result for BSDEs, we obtain the existence of a constant independent of such that

Fix some . The uniform ellipticity of implies that there exists such that for any ,

Hence letting go to zero, we get for any

Thus and thus is continuous.

Finally, by a regularization argument, it is a classical solution of the PDE (61) on .

∎

4.4 PDE representation for and

Finally, let us derive a PDE representation for the control problem (57) with and . From Section 3.3, we know that the problem can be reduced to the time interval ; as opposed to what happens with and , the problem is not Markovian after this reduction. This is because, the choice and introduces an additional state variable, which is itself; keeps track of whether the system is in the trading state or in the waiting state (for is directly a function of and serves as the state of the system). Correspondingly, we expect a value function of the form where the additional variable (shown as a subscript) takes values in ( for the trading state and for no trading) and satisfies the coupled PDE system

| (62) |

where is defined by (49) solved in the region with boundary conditions

and

| (63) |

solved in the region with boundary conditions

Note that the first equation (corresponding to the waiting state) is linear since in this state no control is applied and the PDE is determined only by the underlying diffusion. We think that a solution to this system can be obtained from the minimal supersolution of the corresponding BSDE as we did in earlier sections. In the following subsection we provide an alternative solution based on the number of switches between trading and waiting states. The sequence of control problems where is bounded by can be solved recursively, letting gives a solution to the above system. An advantage of this approach is that it also gives a numerical algorithm to compute the value function. The difficulty in trying to numerically solve the above system directly is that and appear as boundary conditions in the equations that the other satisfies.

Finite trading approximation

Define

The number of trading intervals realized up to terminal time is equal to . Recall that for the set of all trading times before terminal time is

and . Define

Note that is one of the stopping times . The control problem with a limit on the number of active intervals is:

where

Lemma 10.

The sequence is non-increasing and tends to , the value function of the control problem (57) with , as tends to

Proof.

Note that is included in . Hence is a non-increasing sequence. Moreover taking and defining equal to on the random interval and equal to zero after , the strategy belongs to and

Taking the expectation, we have

Since , we have

under Assumption 1 on vol. Let us notice that

Thereby we obtain for any strategy and any :

From the monotone convergence theorem we deduce

Since this holds for any , we obtain the desired result. ∎

Now we consider the dynamical version of the control problem with trading intervals: for any :

the value function of the control problem starting at an arbitrary time . The additional variable indicates the starting value of the process ; means that the problem starts from a trading state and means that the problem starts from a waiting state. The definition of is the same as : there are at most trading intervals during the time interval .

Considering the problem until the first transition from one state to the other (from trading to no trading or vice versa) we can write the above optimal control problems recursively as follows:

| (64) |

where and

| (65) |

where is the first time after when the price goes below . In (64) the problem starts in a waiting interval; the controller waits until the first time after when goes above () or , whichever comes first. If it is , trading starts; if it is , the controller pays the terminal cost. Note that the recursion (64) involves no control since the liquidation process starts in the waiting state (i.e., no trading, ) and remains in that state until In (65) the agent already uses one trading possibility, after , there are at most trading intervals.

As before the homogeneous cost structure suggests

and we define to be the constant function : there is no trading (i.e., no control and ) and at terminal time the trader pays the terminal cost. The above recursions imply the following sequence of PDE to compute and for :

| (66) |

where is defined by (49) solved in the region with boundary conditions

| (67) |

And

| (68) |

solved in the region with boundary conditions

The PDE for and its boundary conditions on the set do not depend on . Hence on this set, we have (see Section 3.2 and the beginning of Section 4.3).

For we have: where is the value function in Section 4.2, Proposition 4.3. The arguments of Lemma 7 show that is of class on and continuous on . Once is available, the rest of the value functions can be computed recursively by solving (66) and (68) in the following order:

Note that solves the linear PDE (66) with smooth and bounded boundary conditions and . Therefore, is also of class on and continuous on . In particular . Hence the boundary condition for is continuous. Recursively all functions (resp. ) are well-defined and bounded on (resp. ), continuous on (resp. ) and of class on (resp. ).

Lemma 11 (Verification).

For , the representation , holds, and the optimal strategy is given by

where

Note that is the number of remaining trading intervals at time and indicates whether trading intervals have been used by time .

Proof.

The definition of vol implies when . Hence the optimal control is equal to zero when . For , there is no trading, , and

For , there are two cases. For () and : the control problem starts from the trading state and the result follows from Section 4.2: . Moreover for any , : indeed after , there could be some opportunity for trading. The second case is when the trader starts from a waiting state (): the trader has to wait until before trading and . Hence for any strategy,

Then due to the Markovian structure, for

is the optimal state process on the interval and

where the last equality comes from the boundary condition (67) of . The value function at time 0 is thus given by:

The PDE that satisfies and Itô’s formula give

Thus we get for any

which achieves the proof for the case .

The rest of the proof proceeds by induction on . Let us detail the case when . The trader starts by following the strategy . Itô’s formula gives:

If , we obtain that

from the definition of vol.

If , the problem stops and since the used strategy has the same dynamics as with the same terminal condition at time , from the case , we know that it is the best strategy on .

If , then the boundary condition connecting and over , the PDE satisfied by and Itô’s formula give

And since there is no trading between the times and , for any . The boundary conditions and for imply

Again the strategy is optimal and there are again two cases. If , the trading is finished and the agent has traded only one time. If , then the agent starts again to trade until . We use the step , starting at time from the value . The best strategy is to follow and the value function of the trader is given by:

Gathering all steps together leads to

Since we cover all possible scenarios and since the strategies are optimal on each (random) time intervals, taking the expectation, we conclude that

and that the optimal strategy is , which achieves the proof of this particular case.

The proof for the other scenarios uses very similar arguments. ∎

Remark 7.

Our sequence of solutions and satisfies for any and

The boundary condition imposed on in (61) is coherent with these previous properties. Moreover (resp. ) solves the PDE (66) on (resp. (68) on ). In other words they solve (61) on their own domain of definition.

A natural but non-trivial question is: do and provide some approximation of given by Lemma 9, when tends to zero and to ? This question is left for further research.

When the numbers of active intervals tends to

With Lemma 10 we saw that the value function of the control problem with a finite number of trading intervals converge to the value function of the same control problem with no bounds on the number of trading intervals. We now argue that 1) a similar result holds for the 2) the limit determines the value function of the control problem with unbounded number of trading intervals and 3) the limit is a solution of the coupled PDE system (62) and (63). Since the arguments follow the same lines as those above we only provide an outline.

The argument of the previous verification lemma gives

Together with Lemma 10, this shows that is a non-increasing sequence. Hence it converges pointwise to some function defined on for and for Moreover we have the relation:

Since is bounded from below and bounded from above by and is upper semi-continuous, (resp. ) is a viscosity subsolution of (66) (resp. (68)) with terminal condition (resp. ). Since the terminal conditions are bounded and continuous, the arguments of Lemma 7 imply that and are smooth solution of the PDE (66) and (68) on the set and .

Let us consider the lateral boundary conditions. For , is equal to , which is a smooth function. From [17], the PDE (66) with terminal condition at time and lateral condition has a unique smooth solution. A similar argument shows that is the unique smooth solution of (68) with terminal condition at time and lateral condition . These results give us the required regularity to proceed as in Lemma 11 and to prove that for

is an optimal control for the control problem (57) with and .

5 A partial analysis of the output of the algorithm and numerical examples

Recall of (1), which is the percentage deviation from the target price of the average price at which the position is (partially) closed in the time interval The actual output of the trading algorithm defined by the optimal control of (37) or (58), is the random pair , where is computed for . An important question is the distribution of this pair and the dependence of this distribution on model parameters. In this section we would like to give a partial analysis of this question including some numerical examples. Compared to the original IS order, the modified IS order considered in the present work has two additional parameters: the process that determines when trading takes place and the event that determines when full liquidation takes place. In the numerical examples we will limit ourselves to , . To further simplify the presentation and the calculations we take , , where is a standard Brownian motion, a constant and ; these are also the choices made for these parameters in the standard Almgren-Chriss framework [14, Chapter 3]. Under these assumptions we will compute by discretizing and numerically solving the corresponding PDE, which becomes:

| (69) |

where the domain of the equation and its boundary conditions depend on and .

To better understand how and change with the model parameters, we factor out as many parameters as possible from the calculations. If we let

| (70) |

the equation (69) reduces to

| (71) |

To see how depends on model parameters let us reduce the expression (1) as much as possible (remember that is the initial position size):

| By (4) (the expression for ) and the assumption : | ||||

| By the definition (3) of and the assumptions , : | ||||

Simplifying the last expression we get

| (72) |

From this expression we see that consists of three components: 1) one due to the permanent price impact 2) one due to random fluctuations in price and 3) one due to transaction costs. All components consist of a coefficient term and a term depending on or its derivative :

where

The permanent impact term is the portion of the initial position that is closed; depends linearly on this portion with coefficient . Secondly note that if , and are parameterized as multiples of then none of the coefficients appearing in depend on We will comment on the behavior of the other two terms below.

Before we move on let us note the following for comparison. The case and corresponds to the standard Almgren Chriss liquidation algorithm for which the optimal control is known to be

| (73) |

i.e., closing the position with uniform speed over the time interval Then and . These reduce to

for the standard IS algorithm. Similarly, for we have

| (74) |

which is normally distributed with mean by the iid normal increments of .

We continue our analysis with the choices and for and given in (14); these choices correspond to: no restriction on trading and closing the position fully is required only when the terminal price is above a given threshold . Parallel to the change of variable in (70) we assume is given as a multiple of ; with this convention and the assumption , becomes For , the PDE (71) is

| (75) |

for the domain and the boundary conditions for this PDE are: and

| (76) |

, where we again use the scaling (70).

Recall our convention that and are specified as multiples of ; it follows that PDE (75) and its boundary condition (76) are independent of The optimal control is computed from via the formula (58)

| (77) |

we note that is independent of We have already noted that the coefficients in (70) are independent of . We have observed above that the same is true also for , therefore all of , and are independent of as well. This gives us the following result:

Lemma 12.

Suppose all of , , and are parameterized as multiples of Then and do not depend on .

Note that the same analysis in fact holds for all of , , treated in the previous sections.

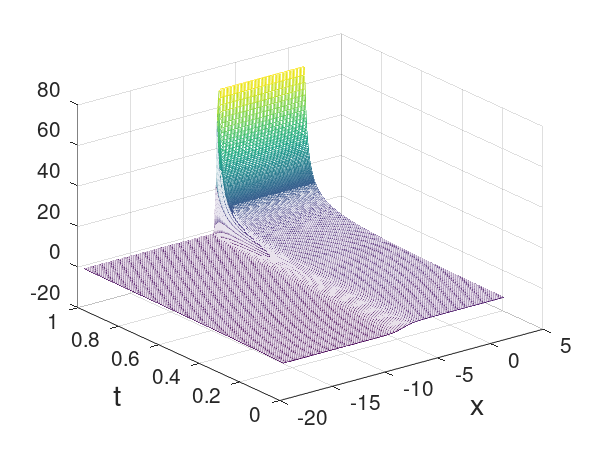

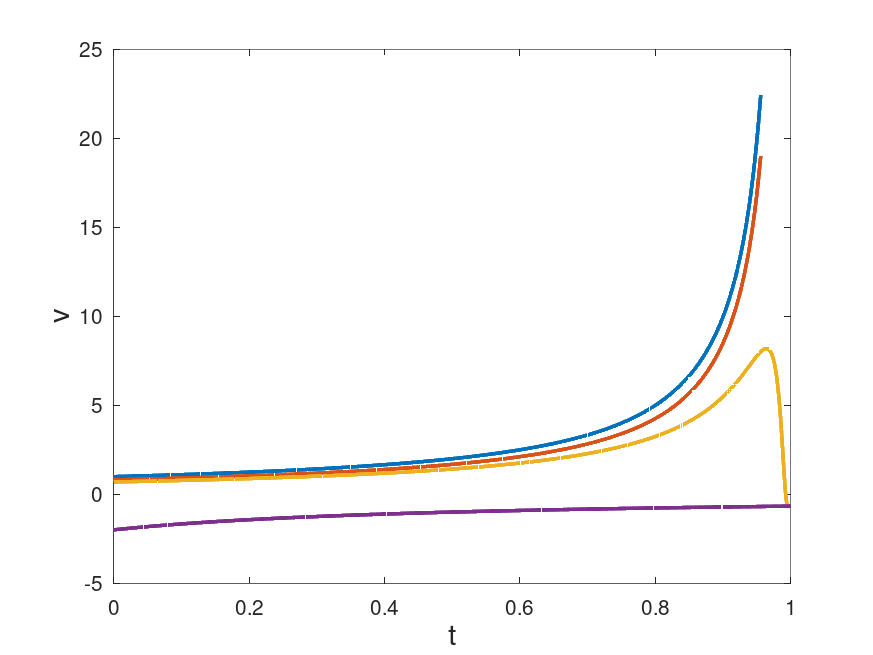

As already noted is computed via the solution of the PDE (75) which obviously doesn’t have an explicit solution. To see how behaves we will solve (75) numerically; for the parameter values we begin by considering those used in [14, Chapter 3]: , , , , . Recall that the permanent price impact parameter doesn’t appear in the control problem corresponding to the original IS order, so no value for is specified in [14, Chapter 3]. A value of accompanying these parameter values is given in [14, Chapter 8] in the context of block trade pricing. The assumption (1) in the present case reduces to

for the above parameter values we have , therefore the above parameter values do not satisfy Assumption 1. To continue with our numerical example, we take , and for these values we have which satisfies (1). In addition to these, we need to provide a value for the parameter, which we choose as . The graph of for the parameter values above are shown in Figures 1 and 2.