Deep Policy Gradient Methods in Commodity Markets

Jonas Rotschi Hanetho

![[Uncaptioned image]](/html/2308.01910/assets/DUO_UiO_segl.png)

Thesis submitted for the

degree of

Master in

Informatics: Programming and System Architecture

60 credits

Institute for Informatics

Faculty of mathematics and natural sciences

UNIVERSITY OF OSLO

Spring 2024

Deep Policy Gradient Methods in Commodity Markets

Jonas Rotschi Hanetho

© 2024 Jonas Rotschi Hanetho

Deep Policy Gradient Methods in Commodity Markets

http://www.duo.uio.no/

Printed:

Reprosentralen, University of Oslo

Acknowledgements

This thesis would not have been possible without my supervisors, Dirk Hesse and Martin Giese. My sincere thanks are extended to Dirk for his excellent guidance and mentoring throughout this project and to Martin for his helpful suggestions and advice. Finally, I would like to thank the Equinor data science team for insightful discussions and for providing me with the tools needed to complete this project.

Abstract

The energy transition has increased the reliance on intermittent energy sources, destabilizing energy markets and causing unprecedented volatility, culminating in the global energy crisis of 2021. In addition to harming producers and consumers, volatile energy markets may jeopardize vital decarbonization efforts. Traders play an important role in stabilizing markets by providing liquidity and reducing volatility. Forecasting future returns is an integral part of any financial trading operation, and several mathematical and statistical models have been proposed for this purpose. However, developing such models is non-trivial due to financial markets’ low signal-to-noise ratios and nonstationary dynamics.

This thesis investigates the effectiveness of deep reinforcement learning methods in commodities trading. It presents related work and relevant research in algorithmic trading, deep learning, and reinforcement learning. The thesis formalizes the commodities trading problem as a continuing discrete-time stochastic dynamical system. This system employs a novel time-discretization scheme that is reactive and adaptive to market volatility, providing better statistical properties for the sub-sampled financial time series. Two policy gradient algorithms, an actor-based and an actor-critic-based, are proposed for optimizing a transaction-cost- and risk-sensitive trading agent. The agent maps historical price observations to market positions through parametric function approximators utilizing deep neural network architectures, specifically CNNs and LSTMs.

On average, the deep reinforcement learning models produce an percent higher Sharpe ratio than the buy-and-hold baseline when backtested on front-month natural gas futures from 2017 to 2022. The backtests demonstrate that the risk tolerance of the deep reinforcement learning agents can be adjusted using a risk-sensitivity term. The actor-based policy gradient algorithm performs significantly better than the actor-critic-based algorithm, and the CNN-based models perform slightly better than those based on the LSTM. The backtest results indicate the viability of deep reinforcement learning-based algorithmic trading in volatile commodity markets.

1 Introduction

1.1 Motivation

The transition to sustainable energy sources is one of the most critical challenges facing the world today. By 2050, the European Union aims to become carbon neutral [eur]. However, rising volatility in energy markets, culminating in the 2021 global energy crisis, complicates this objective. Supply and demand forces determine price dynamics, where an ever-increasing share of supply stems from intermittent renewable energy sources such as wind and solar power. Increasing reliance on intermittent energy sources leads to unpredictable energy supply, contributing to volatile energy markets [SRH20]. Already volatile markets are further destabilized by evolutionary traits such as fear and greed, causing human commodity traders to overreact [Lo04]. Volatile markets are problematic for producers and consumers, and failure to mitigate these concerns may jeopardize decarbonization targets.

Algorithmic trading agents can stabilize commodity markets by systematically providing liquidity and aiding price discovery [Isi21, Nar13]. Developing these methods is non-trivial as financial markets are non-stationary with complicated dynamics [Tal97]. Machine learning (ML) has emerged as the preferred method in algorithmic trading due to its ability to learn to solve complicated tasks by leveraging data [Isi21]. The majority of research on ML-based algorithmic trading has focused on forecast-based supervised learning (SL) methods, which tend to ignore non-trivial factors such as transaction costs, risk, and the additional logic associated with mapping forecasts to market positions [Fis18]. Reinforcement learning (RL) presents a suitable alternative to account for these factors. In reinforcement learning, autonomous agents learn to perform tasks in a time-series environment through trial and error without human supervision. Around the turn of the millennium, Moody and his collaborators [MW97, MWLS98, MS01] made several significant contributions to this field, empirically demonstrating the advantages of reinforcement learning over supervised learning for algorithmic trading.

In the last decade, the deep learning (DL) revolution has made exceptional progress in areas such as image classification [HZRS15] and natural language processing [VSP+17], characterized by complex structures and high signal-to-noise ratios. The strong representation ability of deep learning methods has even translated to forecasting low signal-to-noise financial data [XNS15, HGMS18, MRC18]. In complex, high-dimensional environments, deep reinforcement learning (deep RL), i.e., integrating deep learning techniques into reinforcement learning, has yielded impressive results. Noteworthy contributions include achieving superhuman play in Atari games [MKS+13] and chess [SHS+17], and training a robot arm to solve the Rubik’s cube [AAC+19]. A significant breakthrough was achieved in 2016 when the deep reinforcement learning-based computer program AlphaGo[SHM+16] beat top Go player Lee Sedol. In addition to learning by reinforcement learning through self-play, AlphaGo uses supervised learning techniques to learn from a database of historical games. In 2017, an improved version called AlphaGo Zero[SSS+17], which begins with random play and relies solely on reinforcement learning, comprehensively defeated AlphaGo. Deep RL has thus far been primarily studied in the context of game-playing and robotics, and its potential application to financial trading remains largely unexplored. Combining the two seems promising, given the respective successes of reinforcement learning and deep learning in algorithmic trading and forecasting.

1.2 Problem description

This thesis investigates the effectiveness of deep reinforcement learning methods in commodities trading. It examines previous research in algorithmic trading, state-of-the-art reinforcement learning, and deep learning algorithms. The most promising methods are implemented, along with novel improvements, to create a transaction-cost- and risk-sensitive parameterized agent directly outputting market positions. The agent is optimized using reinforcement learning algorithms, while deep learning methods extract predictive patterns from raw market observations. These methods are evaluated out-of-sample by backtesting on energy futures.

Machine learning relies on generalizability. A common criticism against algorithmic trading approaches is their alleged inability to generalize to “extreme” market conditions [Nar13]. This thesis investigates the performance of algorithmic trading agents out-of-sample under unprecedented market conditions caused by the energy crisis during 2021-2022. It will address the following research questions

-

1.

Can the risk of algorithmic trading agents operating in volatile markets be controlled?

-

2.

What reinforcement learning algorithms are suitable for optimizing an algorithmic training agent in an online, continuous time setting?

-

3.

What deep learning architectures are suitable for modeling noisy, non-stationary financial data?

1.3 Thesis Organization

The thesis consists of three parts: the background (part I), the methodology (part II), and the experiments (part III). The list below provides a brief outline of the chapters in this thesis:

-

•

Chapter 2: Overview of relevant concepts in algorithmic trading.

-

•

Chapter 3: Overview of relevant machine learning and deep learning concepts.

-

•

Chapter 4: Overview of relevant concepts in reinforcement learning.

-

•

Chapter 5: Formalization of the problem setting.

-

•

Chapter 6: Description of reinforcement learning algorithms.

-

•

Chapter 7: Description of the neural network function approximators.

-

•

Chapter 8: Detailed results from experiments.

-

•

Chapter 9: Suggested future work.

-

•

Chapter 10: Summary of contributions, results, and main conclusions.

Part I Background

2 Algorithmic trading

A phenomenon commonly described as an arms race has resulted from fierce competition in financial markets. In this phenomenon, market participants compete to remain on the right side of information asymmetry, which further reduces the signal-to-noise ratio and the frequency at which information arrives and is absorbed by the market [Isi21]. An increase in volatility and the emergence of a highly sophisticated breed of traders called high-frequency traders have further complicated already complex market dynamics. In these developed, modern financial markets, the dynamics are so complex and change at such a high frequency that humans will have difficulty competing. Indeed, there is reason to believe that machines already outperform humans in the world of financial trading. The algorithmic hedge fund Renaissance Technologies, founded by famed mathematician Jim Simons, is considered the most successful hedge fund ever. From 1988 to 2018, Renaissance Technologies’ Medallion fund generated 66 percent annualized returns before fees relying exclusively on algorithmic strategies [Zuc19]. In 2020, it was estimated that algorithmic trading accounts for around 60-73 percent of U.S. and European equity trading, up from just 15 percent in 2003 [Int20]. Thus, it is clear that algorithms already play a significant role in financial markets. Due to the rapid progress of computing power111Moore’s law states that the number of transistors in an integrated circuit doubles roughly every two years. relative to human evolution, this importance will likely only grow.

This chapter provides an overview of this thesis’s subject matter, algorithmic trading on commodity markets, examines related work, and justifies the algorithmic trading methods described in part II. Section 2.1 presents a brief overview of commodity markets and energy futures contracts. Sections 2.2, 2.3, and 2.4 introduce some basic concepts related to trading financial markets that are necessary to define and justify a trading agent’s goal of maximizing risk-adjusted returns. This goal has two sub-goals: forecasting returns and mapping forecasts to market positions, which are discussed separately in sections 2.5 and 2.6. Additionally, these sections provide an overview of how the concepts introduced in the following chapters 3 and 4 can be applied to algorithmic trading and provide an overview of related research. The sections 2.7 and 2.8 describe how to represent a continuous financial market as discrete inputs to an algorithmic trading system. To conclude, section 2.9 introduces backtesting, a form of cross-validation used to evaluate algorithmic trading agents.

2.1 Commodity markets

Energy products trade alongside other raw materials and primary products on commodity markets. The commodity market is an exchange that matches buyers and sellers of the products offered at the market. Traditionally trading was done in an open-outcry manner, though now an electronic limit order book is used to maintain a continuous market. Limit orders specify the direction, quantity, and acceptable price of a security. Limit orders are compared to existing orders in the limit order book when they arrive on the market. A trade occurs at the price set by the first order in the event of an overlap. The exchange makes money by charging a fee for every trade, usually a small percentage of the total amount traded.

The basis of energy trade is energy futures, a derivative contract with energy products as the underlying asset [CGLL19]. Futures contracts are standardized forward contracts listed on stock exchanges. They are interchangeable, which improves liquidity. Futures contracts obligate a buyer and seller to transact a given quantity of the underlying asset at a future date and price. The quantity, quality, delivery location, and delivery date are all specified in the contract. Futures contracts are usually identified by their expiration month. The “front-month” is the nearest expiration date and usually represents the most liquid market. Natural gas futures expire three business days before the first calendar day of the delivery month. To avoid physical delivery of the underlying commodity, the contract holder must sell their holding to the market before expiry. Therefore, the futures and underlying commodity prices converge as the delivery date approaches. A futures contract achieves the same outcome as buying a commodity on the spot market on margin and storing it for a future date. The relative price of these alternatives is connected as it presents an arbitrage opportunity. The difference in price between a futures contract and the spot price of the underlying commodity will therefore depend on the financing cost, storage cost, and convenience yield of holding the physical commodity over the futures contract. Physical traders use futures as a hedge while transporting commodities from producer to consumer. If a trader wishes to extend the expiry of his futures contract, he can “roll” the contract by closing the contract about to expire and entering into a contract with the same terms but a later expiry date [CGLL19]. The “roll yield” is the difference in price for these two contracts and might be positive or negative. The exchange clearinghouse uses a margin system with daily settlements between parties to mitigate counterparty risk [CGLL19].

2.2 Financial trading

Financial trading is the act of buying and selling financial assets. Owning a financial asset is called being long that asset, which will realize a profit if the asset price increases and suffer a loss if the asset price decreases. Short-selling refers to borrowing, selling, and then, at a later time, repurchasing a financial asset and returning it to the lender with the hopes of profiting from a price drop during the loan term. Short-selling allows traders to profit from falling prices.

2.3 Modern portfolio theory

Harry Markowitz laid the groundwork for what is known as Modern Portfolio Theory (MPT)[Mar68]. MPT assumes that investors are risk-averse and advocates maximizing risk-adjusted returns. The Sharpe ratio [Sha98] is the most widely-used measurement of risk-adjusted return developed by economist William F. Sharpe. The Sharpe ratio compares excess return with the standard deviation of investment returns and is defined as

| (2.1) |

where is the expected return over samples, is the risk-free rate, and is the standard deviation of the portfolio’s excess return. Due to negligible low interest rates, the risk-free rate is commonly set to . The philosophy of MPT is that the investor should be compensated through higher returns for taking on higher risk. The St. Petersburg paradox222For an explanation of the paradox, see the article [Pet22]. illustrates why maximizing expected reward in a risk-neutral manner might not be what an individual wants. Although market participants have wildly different objectives, this thesis will adopt the MPT philosophy of assuming investors want to maximize risk-adjusted returns. Hence, the goal of the trading agent described in this thesis will be to maximize the risk-adjusted returns represented by the Sharpe ratio. Maximizing future risk-adjusted returns can be broken down into two sub-goals; forecasting future returns and mapping the forecast to market positions. However, doing so in highly efficient and competitive financial markets is non-trivial.

2.4 Efficient market hypothesis

Actively trading a market suggests that the trader is dissatisfied with market returns and believes there is potential for extracting excess returns, or alpha. Most academic approaches to finance are based on the Efficient Market Hypothesis (EMH)[Fam70], which states that all available information is fully reflected in the prices of financial assets at any time. According to the EMH, a financial market is a stochastic martingale process. As a consequence, searching for alpha is a futile effort as the expected future return of a non-dividend paying asset is the present value, regardless of past information, i.e.,

| (2.2) |

Practitioners and certain parts of academia heavily dispute the EMH. Behavioral economists reject the idea of rational markets and believe that human evolutionary traits such as fear and greed distort market participants’ decisions, creating irrational markets. The Adaptive Market Hypothesis (AMH)[Lo04] reconciles the efficient market hypothesis with behavioral economics by applying evolution principles (competition, adaptation, and natural selection) to financial interactions. According to the AHM, what behavioral economists label irrational behavior is consistent with an evolutionary model of individuals adapting to a changing environment. Individuals within the market are continually learning the market dynamics, and as they do, they adapt their trading strategies, which in turn changes the dynamics of the market. This loop creates complicated price dynamics. Traders who adapt quickly to changing dynamics can exploit potential inefficiencies. Based on the AHM philosophy, this thesis hypothesizes that there are inefficiencies in financial markets that can be exploited, with the recognition that such opportunities are limited and challenging to discover.

2.5 Forecasting

Unless a person is gambling, betting on the price movements of volatile financial assets only makes sense if the trader has a reasonable idea of where the price is moving. Since traders face non-trivial transaction costs, the expected value of a randomly selected trade is negative. Hence, as described by the gambler’s ruin, a person gambling on financial markets will eventually go bankrupt due to the law of large numbers. Forecasting price movements, i.e., making predictions based on past and present data, is a central component of any financial trading operation and an active field in academia and industry. Traditional approaches include fundamental analysis, technical analysis, or a combination of the two [GD34]. These can be further simplified into qualitative and quantitative approaches (or a combination). A qualitative approach, i.e., fundamental analysis, entails evaluating the subjective aspects of a security [GD34], which falls outside the scope of this thesis. Quantitative (i.e., technical) traders use past data to make predictions [GD34]. The focus of this thesis is limited to fully quantitative approaches.

Developing quantitative forecasts for the price series of financial assets is non-trivial as financial markets are non-stationary with a low signal-to-noise ratio [Tal97]. Furthermore, modern financial markets are highly competitive and effective. As a result, easily detectable signals are almost certainly arbitraged out. Researchers and practitioners use several mathematical and statistical models to identify predictive signals leading to excess returns. Classical models include the autoregressive integrated moving average (ARIMA) and the generalized autoregressive conditional heteroskedasticity (GARCH). The ARIMA is a linear model and a generalization of the autoregressive moving average (ARMA) that can be applied to time series with nonstationary mean (but not variance) [SSS00]. The assumption of constant variance (i.e., volatility) is not valid for financial markets where volatility is stochastic [Tal97]. The GARCH is a non-linear model developed to handle stochastic variance by modeling the error variance as an ARMA model [SSS00]. Although the ARIMA and GARCH have practical applications, their performance in modeling financial time series is generally unsatisfactory [XNS15, MRC18].

Over the past 20 years, the availability and affordability of computing power, storage, and data have lowered the barrier of entry to more advanced algorithmic methods. As a result, researchers and practitioners have turned their attention to more complex machine learning methods because of their ability to identify signals and capture relationships in large datasets. Initially, there was a flawed belief that the low signal-to-noise ratio leaves viable only simple forecasts such as those based on low-dimensional ordinary least squares [Isi21]. With the recent deep learning revolution, deep neural networks have demonstrated strong representation abilities when modeling time series data [SVL14]. The Makridakis competition evaluates time series forecasting methods. In its fifth installment held in 2020, all 50 top-performing models were based on deep learning architectures [MSA22]. A considerable amount of recent empirical research suggests that deep learning models significantly outperform traditional models like the ARIMA and GARCH when forecasting financial time series [XNS15, MRC18, SNN18, SGO20]. These results are somewhat puzzling. The risk of overfitting is generally higher for noisy data like financial data. Moreover, the loss function for DNNs is non-convex, which makes finding a global minimum impossible. Despite the elevated overfitting risk and the massive overparameterization of DNNs, they still demonstrate stellar generalization. Thus, based on recent research, the thesis will apply deep learning techniques to model financial time series.

A review of deep learning methods in financial time series forecasting [SGO20] found that LSTMs were the preferred choice in sequence modeling, possibly due to their ability to remember both long- and short-term dependencies. Convolutional neural networks are another common choice. CNNs are best known for their ability to process 2D grids such as images; however, they have shown a solid ability to model 1D grid time series data. Using historical prices, Hiransha et al. [HGMS18] tested FFNs, vanilla RNNs, LSTMs, and CNNs on forecasting next-day stock market returns on the National Stock Exchange (NSE) of India and the New York Stock Exchange (NYSE). In the experiment, CNNs outperformed other models, including the LSTM. These deep learning models can extract generalizable patterns from the price series alone [SGO20].

2.6 Mapping forecasts to market positions

Most research on ML in financial markets focuses on forecast-based supervised learning approaches [Fis18]. These methods tend to ignore how to convert forecasts into market positions or use some heuristics like the Kelly criterion to determine optimal position sizing [Isi21]. The forecasts are usually optimized by minimizing a loss function like the Mean Squared Error (MSE). An accurate forecast (in the form of a lower MSE) may lead to a more profitable trader, but this is not always true. Not only does the discovered signal need adequate predictive power, but it must consistently produce reliable directional calls. Moreover, the mapping from forecast to market position needs to consider transaction costs and risk, which is challenging in a supervised learning framework [MW97]. Neglecting transaction costs can lead to aggressive trading and overestimation of returns. Neglecting risk can lead to trading strategies that are not viable in the real world. Maximizing risk-adjusted returns is only feasible when accounting for transaction costs and risk. These shortcomings are addressed using reinforcement learning [MW97, MWLS98]. Using RL, deep neural networks can be trained to output market positions directly. Moreover, the DNN can be jointly optimized for risk- and transaction-cost-sensitive returns, thus directly optimizing for the true goal: maximizing risk-adjusted returns.

Moody and Wu [MW97] and Moody et al. [MWLS98] empirically demonstrated the advantages of reinforcement learning relative to supervised learning. In particular, they demonstrated the difficulty of accounting for transaction costs using a supervised learning framework. A significant contribution is their model-free policy-based RL algorithm for trading financial instruments recurrent reinforcement learning (RRL). The name refers to the recursive mechanism that stores the past action as an internal state of the environment, allowing the agent to consider transaction costs. The agent outputs market positions and is limited to a discrete action space , corresponding to maximally short, no position, and maximally long. At time , the previous action is fed into the policy network along with the external state of the environment in order to make the trade decision, i.e.,

where is a linear function, and the external state is constructed using the past returns. The return is realized at the end of the period and includes the returns resulting from the position held through this period minus transaction costs incurred at time due to a difference in the new position from the old . Thus, the agent learns the relationship between actions and the external state of the environment and the internal state.

Moody and Saffel [MS01] compared their actor-based RRL algorithm to the value-based Q-learning algorithm when applied to financial trading. The algorithms are tested on two real financial time series; the U.S. dollar/British pound foreign exchange pair and the S&P 500 stock index. While both perform better than a buy-and-hold baseline, the RRL algorithm outperforms Q-learning on all tests. The authors argue that actor-based algorithms are better suited to immediate reward environments and may be better able to deal with noisy data and quickly adapt to non-stationary environments. They point out that critic-based RL suffers from the curse of dimensionality and that when extended to function approximation, it sometimes fails to converge even in simple MDPs.

Deng et al. [DBK+16] combine Moody’s direct reinforcement learning framework with a recurrent neural network to introduce feature learning through deep learning. Another addition is the use of continuous action space. To constrain actions to the interval , the RNN output is mapped to a function. Jiang et al. [JXL17] presents a deterministic policy gradient algorithm that trades a portfolio of multiple financial instruments. The policy network is modeled using CNNs and LSTMs, taking each period’s closing, lowest, and highest prices as input. The DNNs are trained on randomly sampled mini-batches of experience. These methods account for transaction costs but not risk. Zhang et al. [ZZW+20] present a deep RL framework for a risk-averse agent trading a portfolio of instruments using both CNNs and LSTMs. Jin and El-Saawy [JES16] suggest that adding a risk-term to the reward function that penalizes the agent for volatility produces a higher Sharpe ratio than optimizing for the Sharpe ratio directly. Zhang et al. [ZZW+20] apply a similar risk-term penalty to the reward function.

2.7 Feature engineering

Any forecast needs some predictor data, or features, to make predictions. While ML forecasting is a science, feature engineering is an art and arguably the most crucial part of the ML process. Feature engineering and selection for financial forecasting are only limited by imagination. Features range from traditional technical indicators (e.g., Moving Average Convergence Divergence, Relative Strength Index) [ZZR20] to more modern deep learning-based techniques like analyzing social-media sentiment of companies using Natural Language Processing [ZS10] or using CNNs on satellite images along with weather data to predict cotton yields [TOdSMJZ20]. Research in feature engineering and selection is exciting and potentially fruitful but beyond this thesis’s scope. The most reliable predictor of future prices of a financial instrument tends to be its past price, at least in the short term [Isi21]. Therefore, in this thesis, higher-order features are not manually extracted. Instead, only the price series are analyzed.

2.8 Sub-sampling schemes

Separating high- and low-frequency trading can be helpful, as they present unique challenges. High-frequency trading (HFT) focuses on reducing software and hardware latency, which may include building a $300 million fiber-optic cable to reduce transmission time by four milliseconds between exchanges to gain a competitive advantage [LB14] 333Turns out they forgot that light travels about slower in glass than in air, and they lost their competitive advantage to simple line-of-sight microwave networks [LB14].. This type of trading has little resemblance to the low-frequency trading examined in this thesis, described in minutes or hours rather than milliseconds.

Technical traders believe that the prices of financial instruments reflect all relevant information [Tal97]. From this perspective, the market’s complete order history represents the financial market’s state. This state representation would scale poorly, with computational and memory requirements growing linearly with time. Consequently, sub-sampling schemes for periodic feature extraction are almost universally employed. While sampling information at fixed intervals is straightforward, there may be more effective methods. As exchange activity varies throughout the day, sampling at fixed intervals may lead to oversampling during low-activity periods and undersampling during high-activity periods. In addition, time-sampled series often exhibit poor statistical properties, such as non-normal returns, autocorrelation, and heteroskedasticity [DP18].

The normality of returns assumption underpins several mathematical finance models, e.g., Modern Portfolio Theory [Mar68], and the Sharpe-ratio [Sha98]. There is, however, too much peaking and fatter tails in the actual observed distribution for it to be relative to samples from Gaussian populations [Man97] 444Assuming that the S&P 500 index returns were normally distributed, the probability of daily returns being below five percent between 1962 and 2004 ( observations) would be approximately . However, it happened times [Has07].. Mandelbrot showed in 1963 [Man97] that a Lévy alpha-stable distribution with infinite variance can approximate returns over fixed periods. In 1967, Mandelbrot and Taylor [MT67] argued that returns over a fixed number of transactions may be close to Independent and Identically Distributed (IID)Gaussian. Several empirical studies have since confirmed this [Cla73, AG00]. Clark [Cla73] discovered that sampling by volume instead of transactions exhibits better statistical properties, i.e., closer to IID Gaussian distribution. Sampling by volume instead of ticks has intuitive appeal. While tick bars count one transaction of contracts as one bar, transactions of one contract count as bars. Sampling according to transaction volume might lead to significant sampling frequency variations for volatile securities. When the price is high, the volume will be lower, and therefore the number of observations will be lower, and vice versa, even though the same value might be transacted. Therefore, sampling by the monetary value transacted, also called dollar bars, may exhibit even better statistical properties [DP18]. Furthermore, for equities, sampling by monetary value exchanged makes an algorithm more robust against corporate actions like stock splits, reverse splits, stock offerings, and buybacks. To maintain a suitable sampling frequency, the sampling threshold may need to be adjusted if the total market size changes significantly.

Although periodic feature extraction reduces the number of observations that must be processed, it scales linearly in computation and memory requirements per observation. A history cut-off is often employed to represent the state by only the most recent observations to tackle this problem. Representing the state of a partially observable MDP by the most recent observations is a common technique used in many reinforcement learning applications. Mnih et al. [MKS+13] used stacked observations as input to the DQN agent that achieved superhuman performance on Atari games to capture the trajectory of moving objects on the screen. The state of financial markets is also usually approximated by stacking past observations [JXL17, ZZR20, ZZW+20].

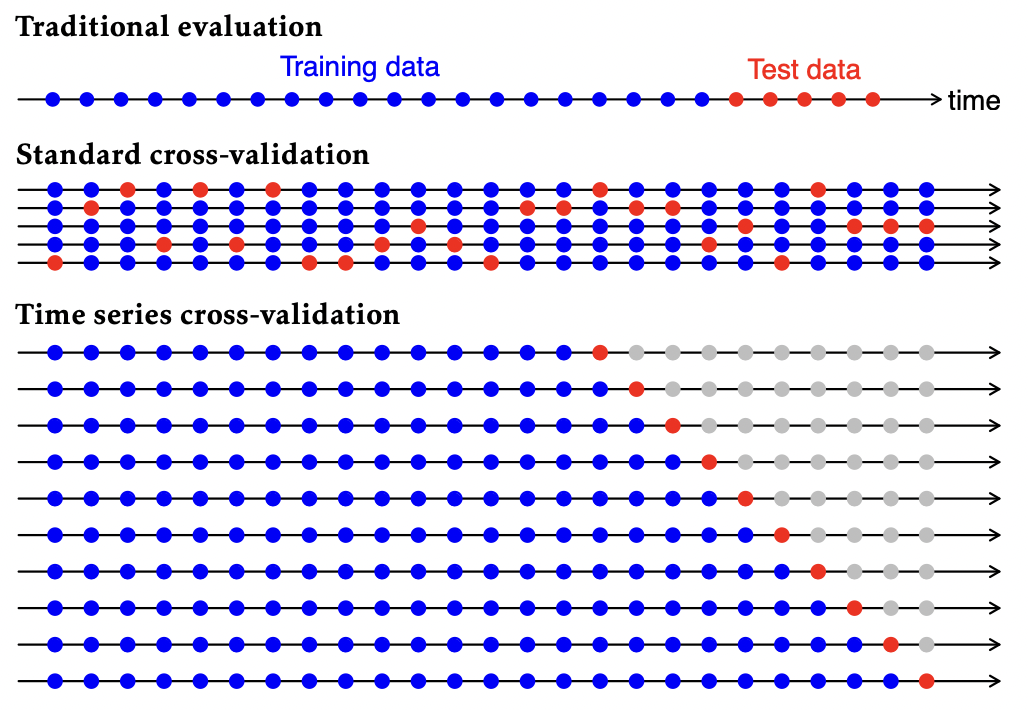

2.9 Backtesting

Assessing a machine learning model involves estimating its generalization error on new data. The most widely used method for estimating generalization error is Cross-Validation (CV), which assumes that observations are IID and drawn from a shared underlying data-generating distribution. However, the price of a financial instrument is a nonstationary time series with an apparent temporal correlation. Conventional cross-validation ignores this temporal component and is thus unsuitable for assessing a time series forecasting model. Instead, backtesting, a form of cross-validation for time series, is used. Backtesting is a historical simulation of how the model would have performed should it have been run over a past period. The purpose of backtesting is the same as for cross-validation; to determine the generalization error of an ML algorithm.

To better understand backtesting, it is helpful to consider an algorithmic trading agent’s objective and how it operates to achieve it. The algorithmic trading process involves the agent receiving information and, based on that information, executing trades at discrete time steps. These trades are intended to achieve a specific objective set by the stakeholder, which, in the philosophy of modern portfolio theory, is maximizing risk-adjusted returns. Thus, assessing an algorithmic trading agent under the philosophy of modern portfolio theory entails estimating the risk-adjusted returns resulting from the agent’s actions. However, when testing an algorithmic trading agent, it cannot access data ahead of the forecasting period, as that would constitute information leakage to the agent. For this reason, conventional cross-validation fails in algorithmic trading.

The most precise way to assess the performance of an algorithmic trading agent is to deploy it to the market, let it trade with the intended amount of capital, and observe its performance. However, this task would require considerable time since low-frequency trading algorithms are typically assessed over long periods, often several years555There are a couple of reasons for this; first, there are, on average, 252 trading days per year. Low-frequency trading algorithms typically make fewer than ten trades per day. In order to obtain sufficient test samples, the agent must trade for several years. Second, testing the algorithmic trading agent under various market conditions is crucial. A successful model in particular market conditions may be biased towards those conditions and fail to generalize to other market conditions. . Additionally, any small error would likely result in devastating losses, making algorithmic trading projects economically unfeasible.

Backtesting is an alternative to this expensive and time-consuming process where performance on historical simulations functions as a proxy for generalization error. Backtesting involves a series of tests that progress sequentially through time, where every test set consists of a single observation. At test , the model trains on the training set consisting of observations prior to the observation in the test set (). The forecast is, therefore, not based on future observations, and there is no leakage from the test set to the training set. Then the backtest progresses to the subsequent observation , where the training set increases666The test set can also be a fixed-size FIFO queue. to include observations . The backtest progresses until there are no test sets left. The backtesting process is formalized in algorithm 1.

Train the model on the first observations (of total observations).

Measure performance using registered trades and the corresponding prices at time .

When conducting historical simulations, knowing what information was available during the studied period is critical. Agents should not have access to data beyond the point at which they are located in the backtest, in order to avoid lookahead bias. Lookahead bias is a research bug of inadvertently using future data, whereas real-time production trading is free of such “feature”. Data used in forecasting must be stored point-in-time (PIT), which indicates when the information was made available. An incorrectly labeled dataset can lead to lookahead bias.

Backtesting is a flawed procedure as it suffers from lookahead bias by design. Having experienced the hold-out test sample provides insight into what made markets rise and fall, a luxury not available before the fact. Thus, only live trading can be considered genuinely out-of-sample. Another form of lookahead bias is repeated and excessive backtest optimization leading to information leakage from the test to the training set. A machine learning model will enthusiastically grab any lookahead but fail to generalize to live trading. Furthermore, the backtests performed in this thesis rely on assumptions of zero market impact, zero slippage, fractional trading, and sufficient liquidity to execute any trade instantaneously at the quoted price. These assumptions do not reflect actual market conditions and will lead to unrealistic high performance in the backtest.

Backtesting should emulate the scientific method, where a hypothesis is developed, and empirical research is conducted to find evidence of inconsistencies with the hypothesis. It should be distinct from a research tool for discovering predictive signals. It should only be conducted after research has been done. A backtest is not an experiment but a simulation to see if the model behaves as expected [DP18]. Random historical patterns might exhibit excellent performance in a backtest. However, it should be viewed cautiously if no ex-ante logical foundation exists to explain the performance [AHM19].

3 Deep learning

An intelligent agent requires some means of modeling the dynamics of the system in which it operates. Modeling financial markets is complicated due to low signal-to-noise ratios and non-stationary dynamics. The dynamics are highly nonlinear; thus, several traditional statistical modeling approaches cannot capture the system’s complexity. Moreover, reinforcement learning requires parameterized function approximators, rendering nonparametric learners, e.g., support vector machines and random forests, unsuitable. Additionally, parametric learners are generally preferred when the predictor data is well-defined[GBC16], such as when forecasting security prices using historical data. In terms of nonlinear parametric learners, artificial neural networks comprise the most widely used class. Research suggests that deep neural networks, such as LSTMs and CNNs, effectively model financial data [XNS15, HGMS18, MRC18]. Therefore, the algorithmic trading agent proposed in this thesis will utilize deep neural networks to model commodity markets.

This chapter introduces the fundamental concepts of deep learning relevant to this thesis, starting with some foundational concepts related to machine learning 3.1 and supervised learning 3.2. Next, section 3.3 covers artificial neural networks, central network topologies, and how they are initialized and optimized to achieve satisfactory results. The concepts presented in this chapter are presented in the context of supervised learning but will be extended to the reinforcement learning context in the next chapter (4).

3.1 Machine learning

Machine Learning (ML)studies how computers can automatically learn from experience without being explicitly programmed. A general and comprehensive introduction to machine learning can be found in “Elements of Statistical Learning” by Trevor Hastie, Robert Tibshirani, and Jerome Friedman [HTFF09]. Tom Mitchell defined the general learning problem as “A computer program is said to learn from experience E with respect to some class of tasks T and performance measure P, if its performance on T, as measured by P, improves with experience E.” [MM97]. In essence, ML algorithms extract generalizable predictive patterns from data from some, usually unknown, probability distribution to build a model about the space. It is an optimization problem where performance improves through leveraging data. Generalizability relates to a model’s predictive performance on independent test data and is a crucial aspect of ML. Models should be capable of transferring learned patterns to new, previously unobserved samples while maintaining comparable performance. ML is closely related to statistics in transforming raw data into knowledge. However, while statistical models are designed for inference, ML models are designed for prediction. There are three primary ML paradigms; supervised learning, unsupervised learning, and reinforcement learning.

3.1.1 No-free-lunch theorem

The no-free-lunch theorem states that there exists no single universally superior ML learning algorithm that applies to all possible datasets. Fortunately, this does not mean ML research is futile. Instead, domain-specific knowledge is required to design successful ML models. The no-free-lunch theorem results only hold when averaged over all possible data-generating distributions. If the types of data-generating distributions are restricted to classes with certain similarities, some ML algorithms perform better on average than others. Instead of trying to develop a universally superior machine learning algorithm, the focus of ML research should be on what ML algorithms perform well on specific data-generating distributions.

3.1.2 The curse of dimensionality

The Hughes phenomenon states that, for a fixed number of training examples, as the number of features increases, the average predictive power for a classifier will increase before it starts deteriorating. Bellman termed this phenomenon the curse of dimensionality, which frequently manifests itself in machine learning [SB18]. One manifestation of the curse is that the sampling density is proportional to , where is the dimension of the input space and is the sample size. If represents a dense sample for , then is the required sample size for the same sampling density with inputs. Therefore, in high dimensions, the training samples sparsely populate the input space [HTFF09]. In Euclidean spaces, a non-negative term is added to the distance between points with each new dimension. Thus, generalizing from training samples becomes more complex, as it is challenging to say something about a space without relevant training examples.

3.2 Supervised learning

Supervised Learning (SL)is the machine learning paradigm where a labeled training set of observations is used to learn a functional dependence that can predict from a previously unobserved . Supervised learning includes regression tasks with numerical targets and classification tasks with categorical targets. A supervised learning algorithm adjusts the input/output relationship of in response to the prediction error to the target . The hypothesis is that if the training set is representative of the population, the model will generalize to previously unseen examples.

3.2.1 Function approximation

Function approximation, or function estimation, is an instance of supervised learning that concerns selecting a function among a well-defined class that underlies the predictive relationship between the input vector and output variable . In most cases, , where , and . Function approximation relies on the assumption that there exists a function that describes the approximate relationship between . This relationship can be defined as

| (3.1) |

where is some irreducible error that is independent of where and . All departures from a deterministic relationship between are captured via the error . The objective of function approximation is to approximate the function with a model . In reality, this means finding the optimal model parameters . Ordinary least squares can estimate linear models’ parameters .

Bias-variance tradeoff

Bias and variance are two sources of error in model estimates. Bias measures the in-sample expected deviation between the model estimate and the target and is defined as

| (3.2) |

and is a decreasing function of complexity. Variance measures the variability in model estimates and is defined as

| (3.3) |

and is an increasing function of complexity. The out-of-sample mean square error for model estimates is defined as

| (3.4) |

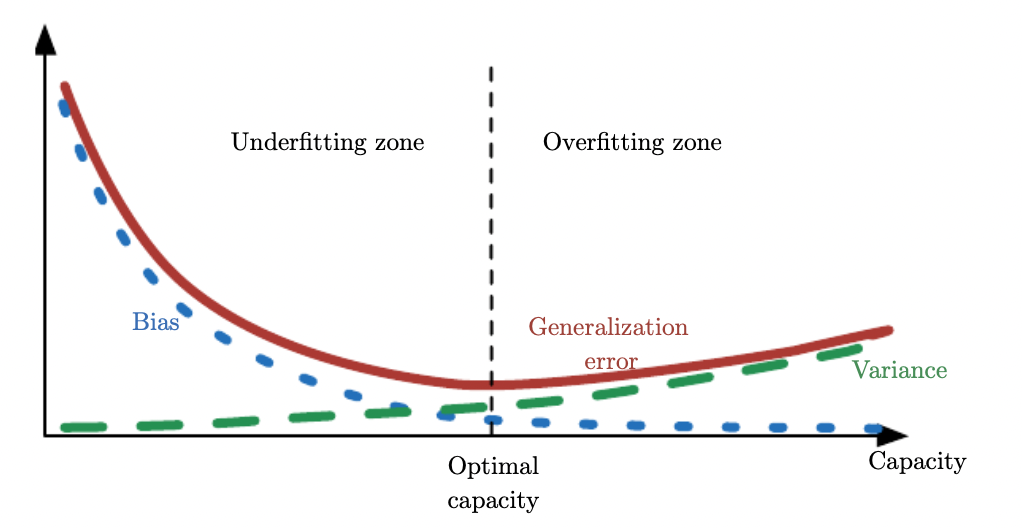

where the last term is the irreducible noise error due to a target component not predictable by . The bias can be made arbitrarily small using a more complex model; however, this will increase the model variance, or generalization error, when switching from in-sample to out-of-sample. This is known as the bias-variance tradeoff.

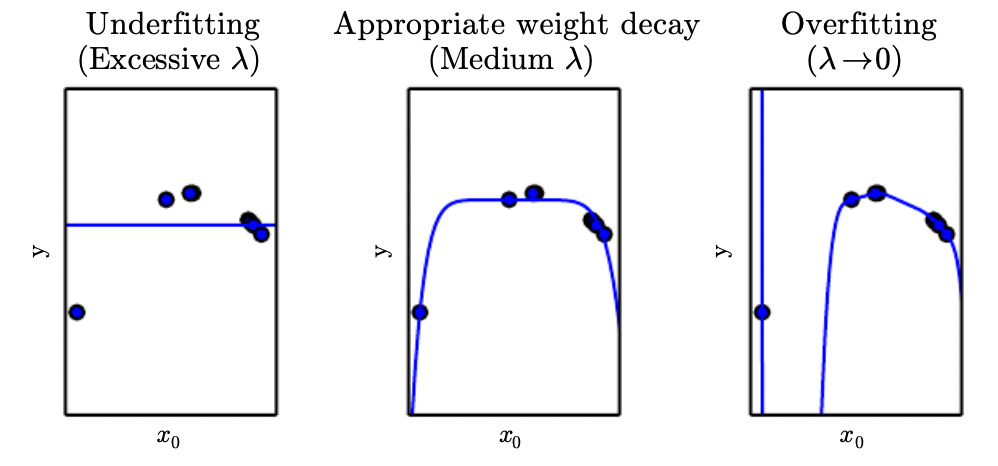

Overfitting

A good ML model minimizes the model error, i.e., the training error (bias) and the generalization error (variance). This is achieved at some optimal complexity level, dependent on the data and the model. Increasing model complexity, or capacity, can minimize training error. However, such a model is unlikely to generalize well. Therefore, the difference between training error and generalization error will be high. This is known as overfitting and happens when the complexity of the ML model exceeds that of the underlying problem. Conversely, underfitting is when the training error is high because the model’s complexity is lower than that of the underlying problem.

To minimize model error, the complexity of the ML model, or its inductive bias, must align with that of the underlying problem. The principle of parsimony, known as Occam’s razor, states that among competing hypotheses explaining observations equally well, one should pick the simplest one. This heuristic is typically applied to ML model selection by selecting the simplest model from models with comparable performance.

Recent empirical evidence has raised questions about the mathematical foundations of machine learning. Complex models such as deep neural networks have been shown to decrease both training error and generalization error with growing complexity [ZBH+21]. Furthermore, the generalization error keeps decreasing past the interpolation limit. These surprising results contradict the bias-variance tradeoff that implies that a machine learning model should balance over- and underfitting. Belkin et al. [BHMM19] reconciled these conflicting ideas by introducing a “double descent” curve to the bias-variance tradeoff curve. This increases performance when increasing the model capacity beyond the interpolation point.

3.3 Artificial neural networks

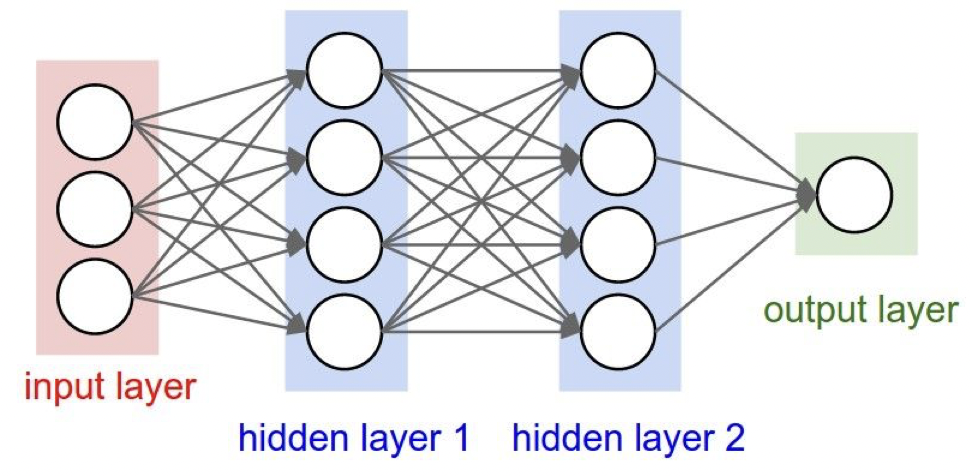

An Artificial Neural Network (ANN)is a parametric learner fitting nonlinear models. The network defines a mapping where is the input dimension, is the output dimension, and are the network weights. A neural network has a graph-like topology. It is a collection of nodes organized in layers like a directed and weighted graph. The nodes of an ANN are typically separated into layers; the input layer, one or more hidden layers, and the output layer. Their dimensions depend on the function being approximated. A multi-layer neural network is called a Deep Neural Network (DNN).

3.3.1 Feedforward neural networks

A Feedforward Network (FFN), or fully-connected network, defines the foundational class of neural networks where the connections are a directed acyclic graph that only allows signals to travel forward in the network. A feedforward network is a mapping that is a composition of multivariate functions , where is the number of layers in the neural network. It is defined as

| (3.5) |

The functions , represent the network’s hidden layers and are composed of multivariate functions. The function at layer is defined as

| (3.6) |

where is the activation function and is the bias at layer . The activation function is used to add nonlinearity to the network. The network’s final output layer function can be tailored to suit the problem the network is solving, e.g., linear for Gaussian output distribution or Softmax distribution for categorical output distribution.

3.3.2 Parameter initialization

Neural network learning algorithms are iterative and require some starting point from which to begin. The initial parameters of the networks can affect the speed and level of convergence or even whether the model converges at all. Little is known about weight initialization, a research area that is still in its infancy. Further complicating the issue: initial parameters favorable for optimization might be unfavorable for generalization [GBC16]. Developing heuristics for parameter initialization is, therefore, non-trivial. Randomness and asymmetry between the network units are desirable properties for the initial weights [GBC16]. Weights are usually drawn randomly from a Gaussian or uniform distribution in a neighborhood around zero, while the bias is usually set to some heuristically chosen constant. Larger initial weights will prevent signal loss during forward- and backpropagation. However, too large values can result in exploding values, a problem particularly prevalent in recurrent neural networks. The initial scale of the weights is usually set to something like where is the number of inputs to the network layer.

Kaiming initialization [HZRS15] is a parameter initialization method that takes the type of activation function (e.g., Leaky-ReLU) used to add nonlinearity to the neural network into account. The key idea is that the initialization method should not exponentially reduce or magnify the magnitude of input signals. Therefore, each layer is initialized at separate scales depending on their size. Let be the size of the inputs into the layer . Kaiming He et al. recommend initializing weights such that

Which corresponds to an initialization scheme of

Biases are initialized at .

3.3.3 Gradient-based learning

Neural nets are optimized by adjusting their weights with the help of objective functions. Let define the differentiable objective function for a neural network, where are the network weights. The choice of the objective function and whether it should be minimized or maximized depends on the problem being solved. For regression tasks, the objective is usually to minimize some loss function like mean-squared error (MSE)

| (3.7) |

Due to neural nets’ nonlinearity, most loss functions are non-convex, meaning it is impossible to find an analytical solution to . Instead, iterative, gradient-based optimization algorithms are used. There are no convergence guarantees, but it often finds a satisfactorily low value of the loss function relatively quickly. Gradient descent-based algorithms adjust the weights in the direction that minimizes the MSE loss function. The update rule for parameter weights in gradient descent is defined as

| (3.8) |

where is the learning rate and the gradient is the partial derivatives of the objective function with respect to each weight. The learning rate defines the rate at which the weights move in the direction suggested by the gradient of the objective function. Gradient-based optimization algorithms, also called first-order optimization algorithms, are the most common optimization algorithms for neural networks [GBC16].

Stochastic gradient descent

Optimization algorithms that process the entire training set simultaneously are known as batch learning algorithms. Using the average of the entire training set allows for calculating a more accurate gradient estimate. The speed at which batch learning converges to a local minima will be faster than online learning. However, batch learning is not suitable for all problems, e.g., problems with massive datasets due to the high computational costs of calculating the full gradient or problems with dynamic probability distributions.

Instead, Stochastic Gradient Descent (SGD)is often used when optimizing neural networks. SGD replaces the gradient in conventional gradient descent with a stochastic approximation. Furthermore, the stochastic approximation is only calculated on a subset of the data. This reduces the computational costs of high-dimensional optimization problems. However, the loss is not guaranteed to decrease when using a stochastic gradient estimate. SGD is often used for problems with continuous streams of new observations rather than a fixed-size training set. The update rule for SGD is similar to the one for GD but replaces the true gradient with a stochastic estimate

| (3.9) |

where is the stochastic estimate of the gradient computed from observation . The total loss is defined as where is the total number of observations. The learning rate at time is . Due to the noise introduced by the SGD gradient estimate, gradually decreasing the learning rate over time is crucial to ensure convergence. Stochastic approximation theory guarantees convergence to a local optima if satisfies the conditions and . It is common to adjust the learning rate using the following update rule , where , and the learning rate is kept constant after iterations, i.e., , [GBC16].

Due to hardware parallelization, simultaneously computing the gradient of observations will usually be faster than computing each gradient separately [GBC16]. Neural networks are, therefore, often trained on mini-batches, i.e., sets of more than one but less than all observations. Mini-batch learning is an intermediate approach to fully online learning and batch learning where weights are updated simultaneously after accumulating gradient information over a subset of the total observations. In addition to providing better estimates of the gradient, mini-batches are more computationally efficient than online learning while still allowing training weights to be adjusted periodically during training. Therefore, minibatch learning can be used to learn systems with dynamic probability distributions. Samples of the mini-batches should be independent and drawn randomly. Drawing ordered batches will result in biased estimates, especially for data with high temporal correlation.

Due to noisy gradient estimates, stochastic gradient descent and mini-batches of small size will exhibit higher variance than conventional gradient descent during training. The higher variance can be helpful to escape local minima and find new, better local minima. However, high variance can also lead to problems such as overshooting and oscillation that can cause the model to fail to converge. Several extensions have been made to stochastic gradient descent to circumvent these problems.

Adaptive gradient algorithm

The Adaptive Gradient (AdaGrad) is an extension to stochastic gradient descent introduced in 2011 [DHS11]. It outlines a strategy for adjusting the learning rate to converge quicker and improving the capability of the optimization algorithm. A per-parameter learning rate allows AdaGrad to improve performance on problems with sparse gradients. Learning rates are assigned lower for parameters with frequently occurring features and higher for parameters with less frequently occurring features. The AdaGrad update rule is given as

| (3.10) |

where , and , is the outer product of all previous subgradients. is a smoothing term to avoid division by zero. As training proceeds, the squared gradients in the denominator of the learning rate will continue to grow, resulting in a strictly decreasing learning rate. As a result, the learning rate will eventually become so small that the model cannot acquire new information.

Root mean square propagation

Root Mean Square Propagation (RMSProp) is an unpublished extension to SGD developed by Geoffrey Hinton. RMSProp was developed to resolve the problem of AdaGrad’s diminishing learning rate. Like AdaGrad, it maintains a per-parameter learning rate. To normalize the gradient, it keeps a moving average of squared gradients. This normalization decreases the learning rate for more significant gradients to avoid the exploding gradient problem and increases it for smaller gradients to avoid the vanishing gradient problem. The RMSProp update rule is given as

| (3.11) |

where where is the exponentially decaying average of squared gradients and is a second learning rate conventionally set to .

Adam

The Adam optimization algorithm is an extension of stochastic gradient descent that has recently seen wide adoption in deep learning. It was introduced in 2015 [KB14] and derives its name from adaptive moment estimation. It utilizes the Adaptive Gradient (AdaGrad) Algorithm and Root Mean Square Propagation (RMSProp). Adam only requires first-order gradients and little memory but is computationally efficient and works well with high-dimensional parameter spaces. As with AdaGrad and RMSProp, Adam utilizes independent per-parameter learning rates separately adapted during training. Adam stores a moving average of gradients with learning rate . Like RMSProp, Adam also stores a moving average of squared gradients with learning rate . The Adam update rule is given as

| (3.12) |

where and . The authors recommend learning rates , , as well as . Adam has been shown to outperform other optimizers in a wide range of non-convex optimization problems. Researchers at Google [ARS+20] recommend the Adam optimization algorithm for SGD optimization in reinforcement learning.

3.3.4 Backpropagation

Gradient-based optimization requires a method for computing a function’s gradient. For neural nets, the gradient of the loss function with respect to the weights of the network is usually computed using the backpropagation algorithm (backprop) introduced in 1986 [RHW85]. Backprop calculates the gradient of the loss function with respect to each weight in the network. This is done by iterating backward through the network layers and repeatedly applying the chain rule. The chain rule of calculus is used when calculating derivatives of functions that are compositions of other functions with known derivatives. Let be functions defined as and . By the chain rule

| (3.13) |

Generalizing further, let , and define mappings and . If and , then the chain rule is

| (3.14) |

which can be written in vector notation as

| (3.15) |

where is the Jacobian matrix of . Backpropagation is often performed on tensors and not vectors. However, backpropagation with tensors is performed similarly by multiplying Jacobians by gradients. Backpropagation with tensors can be performed by flattening a tensor into a vector, performing backprop on the vector, and then reshaping the vector back into a tensor. Let and be tensors and and . The chain rule for tensors is

| (3.16) |

By recursively applying the chain rule, a scalar’s gradient can be expressed for any node in the network that produced it. This is done recursively, starting from the output layer and going back through the layers of the network to avoid storing subexpressions of the gradient or recomputing them several times.

3.3.5 Activation function

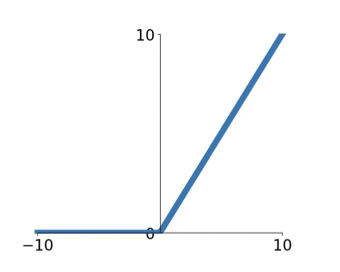

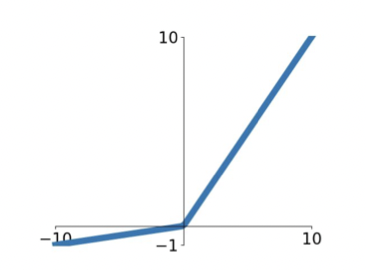

The activation function adds nonlinearity to a neural net. If the activation function in the hidden layer is linear, then the network is equivalent to a network without hidden layers since linear functions of linear functions are themselves linear. The activation function must be differentiable to compute the gradient. Choosing an appropriate activation function depends on the specific problem. Sigmoid functions , like the logistic function, are commonly used, as well as other functions such as the hyperbolic tangent function . The derivative of the logistic function is close to except in a small neighborhood around . At each backward step, the is multiplied by the derivative of the activation function. The gradient will therefore approach and thus produce extremely slow learning. This is known as the vanishing gradient problem. For this reason, the Rectified Linear Unit (ReLU)is the default recommendation for activation function in modern deep neural nets [GBC16]. ReLU is a ramp function defined as . The derivative of the ReLU function is defined as

| (3.17) |

The derivative is undefined for , but it has subdifferential , and it conventionally takes the value in practical implementations. Since ReLU is a piecewise linear function, it optimizes well with gradient-based methods.

ReLU suffers from what is known as the dying ReLU problem, where a large gradient could cause a node’s weights to update such that the node will never output anything but . Such nodes will not discriminate against any input and are effectively “dead”. This problem can be caused by unfortunate weight initialization or a too-high learning rate. Generalizations of the ReLU function, like the Leaky ReLU (LReLU) activation function, has been proposed to combat the dying ReLU problem [GBC16]. Leaky ReLU allows a small “leak” for negative values proportional to some slope coefficient , e.g., , determined before training. This allows small gradients to travel through inactive nodes. Leaky ReLU will slowly converge even on randomly initialized weights but can also reduce performance in some applications [GBC16].

3.3.6 Regularization

Minimization of generalization error is a central objective in machine learning. The representation capacity of large neural networks, expressed by the universal approximation theorem (3.3.8), comes at the cost of increased overfitting risk. Consequently, a critical question in ML is how to design and train neural networks to achieve the lowest generalization error. Regularization addresses this question. Regularization is a set of techniques designed to reduce generalization error, possibly at the expense of training error.

Regularization of estimators trades increased bias for reduced variance. If effective, it reduces model variance more than it increases bias. Weight decay is used to regularize ML loss functions by adding the squared norm of the parameter weights as a regularization term to the loss function

| (3.18) |

where is a constant weight decay parameter. Increasing punishes larger weights harsher. Weight decay creates a tradeoff for the optimization algorithm between minimizing the loss function and the regularization term .

Dropout [SHK+14] is another regularization strategy that reduces the risk of overfitting by randomly eliminating non-output nodes and their connections during training, preventing units from co-adapting too much. Dropout can be considered an ensemble method, where an ensemble of “thinned” sub-networks trains the same underlying base network. It is computationally inexpensive and only requires setting one parameter , which is the rate at which nodes are eliminated.

Early stopping is a common and effective implicit regularization technique that addresses how many epochs a model should be trained to achieve the lowest generalization error. The training data is split into training and validation subsets. The model is iteratively trained on the training set, and at predefined intervals in the training cycle, the model is tested on the validation set. The error on the validation set is used as a proxy for the generalization error. If the performance on the validation set improves, a copy of the model parameters is stored. If performance worsens, the learning terminates, and the model parameters are reset to the previous point with the lowest validation set error. Testing too frequently on the validation set risks premature termination. Temporary dips in performance are prevalent for nonlinear models, especially when trained with reinforcement learning algorithms when the agent explores the state and action space. Additionally, frequent testing is computationally expensive. On the other hand, infrequent testing increases the risk of not registering the model parameters near their performance peak. Early stopping is relatively simple but comes at the cost of sacrificing parts of the training set to the validation set.

3.3.7 Batch normalization

Deep neural networks are sensitive to initial random weights and hyperparameters. When updating the network, all weights are updated using a loss estimate under the false assumption that weights in the prior layers are fixed. In practice, all layers are updated simultaneously. Therefore, the optimization step is constantly chasing a moving target. The distribution of inputs during training is forever changing. This is known as internal covariate shift, making the network sensitive to initial weights and slowing down training by requiring lower learning rates.

Batch normalization (batch norm) is a method of adaptive reparametrization used to train deep networks. It was introduced in 2015 [IS15] to help stabilize and speed up training deep neural networks by reducing internal covariate shift. Batch norm normalizes the output distribution to be more uniform across dimensions by standardizing the activations of each input variable for each mini-batch. Standardization rescales the data to standard Gaussian, i.e., zero-mean unit variance. The following transformation is applied to a mini-batch of activations to standardize it

| (3.19) |

where the is a small number such as added to the denominator for numerical stability. Normalizing the mean and standard deviation can, however, reduce the expressiveness of the network [GBC16]. Applying a second transformation step to the mini-batch of normalized activations restores the expressive power of the network

| (3.20) |

where and are learned parameters that adjust the mean and standard deviation, respectively. This new parameterization is easier to learn with gradient-based methods. Batch normalization is usually inserted after fully connected or convolutional layers. It is conventionally inserted into the layer before activation functions but may also be inserted after. Batchnorm speeds up learning and reduces the strong dependence on initial parameters. Additionally, it can have a regularizing effect and sometimes eliminate the need for dropout.

3.3.8 Universal approximation theorem

In 1989, Cybenko [Cyb89] proved that a feedforward network of arbitrary width with a sigmoidal activation function and a single hidden layer can approximate any continuous function. The theorem asserts that given any 777Continuous function on the -dimensional unit cube., and sigmoidal activation function , there is a finite sum of the form

| (3.21) |

where and , for which

| (3.22) |

for all . Hornik [Hor91] later generalized to include all squashing activation functions in what is known as the universal approximation theorem. The theorem establishes that there are no theoretical constraints on the expressivity of neural networks. However, it does not guarantee that the training algorithm will be able to learn that function, only that it can be learned for an extensive enough network.

3.3.9 Deep neural networks

Although a single-layer network, in theory, can represent any continuous function, it might require the network to be infeasibly large. It may be easier or even required to approximate more complex functions using networks of deep topology [SB18]. The class of ML algorithms that use neural nets with multiple hidden layers is known as Deep Learning (DL). Interestingly, the universal approximation theorem also applies to networks of bounded width and arbitrary depth. Lu et al. [LPW+17] showed that for any Lebesgue-integrable function and any , there exists a fully-connected ReLU network with width , such that the function represented by this network satisfies

| (3.23) |

i.e., any continuous multivariate function can be approximated by a deep ReLU network with width .

Poggio et al.[PMR+17] showed that a deep network could have exponentially better approximation properties than a wide shallow network of the same total size. Conversely, a network of deep topology can attain the same expressivity as a larger shallow network. They also show that a deep composition of low-dimensional functions has a theoretical guarantee, which shallow networks do not have, that they can resist the curse of dimensionality for a large class of functions.

Several unique network architectures have been developed for tasks like computer vision, sequential data, and machine translation. As a result, they can significantly outperform larger and more deeply layered feedforward networks. The architecture of neural networks carries an inductive bias, i.e., an a priori algorithmic preference. A neural network’s inductive bias must match that of the problem it is solving to generalize well out-of-sample.

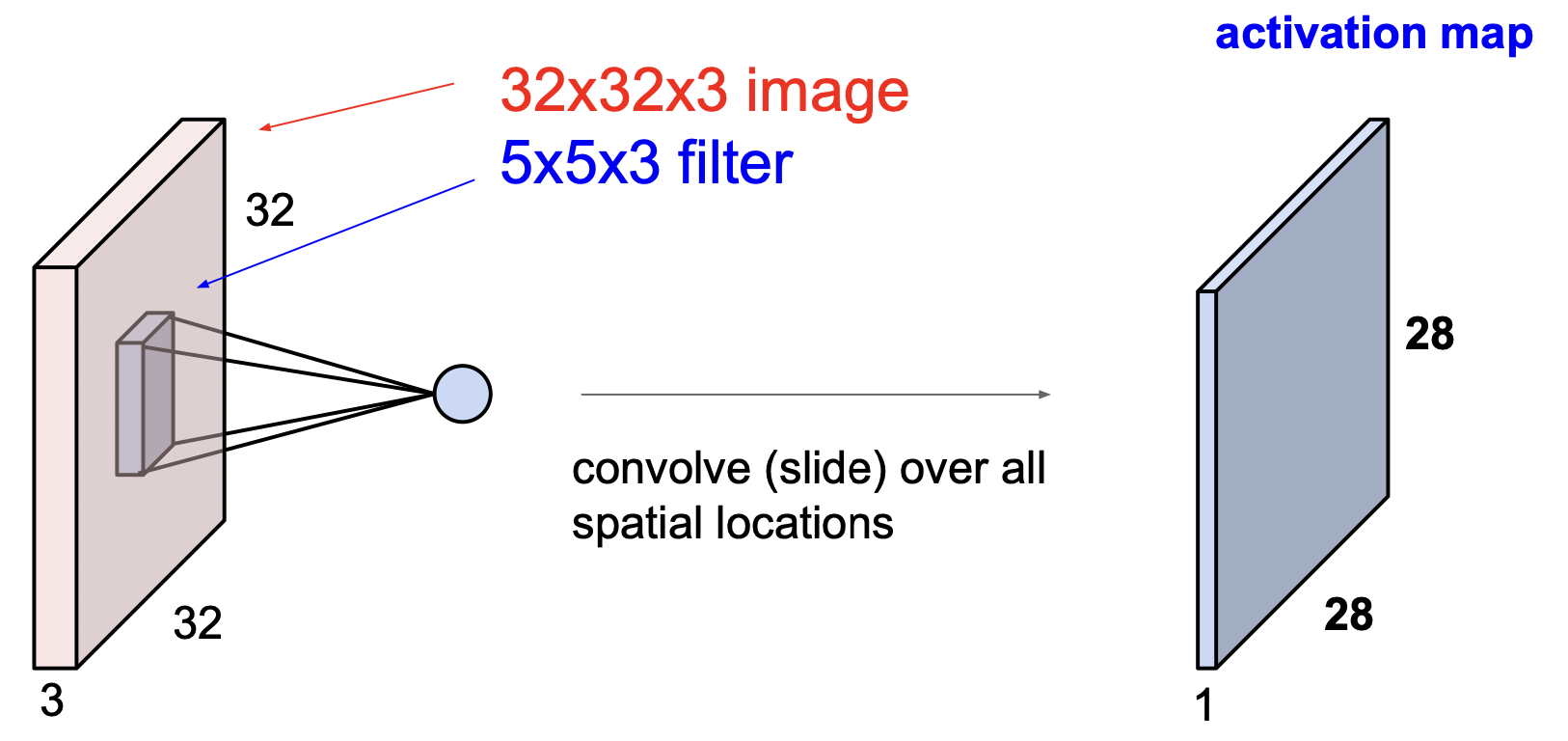

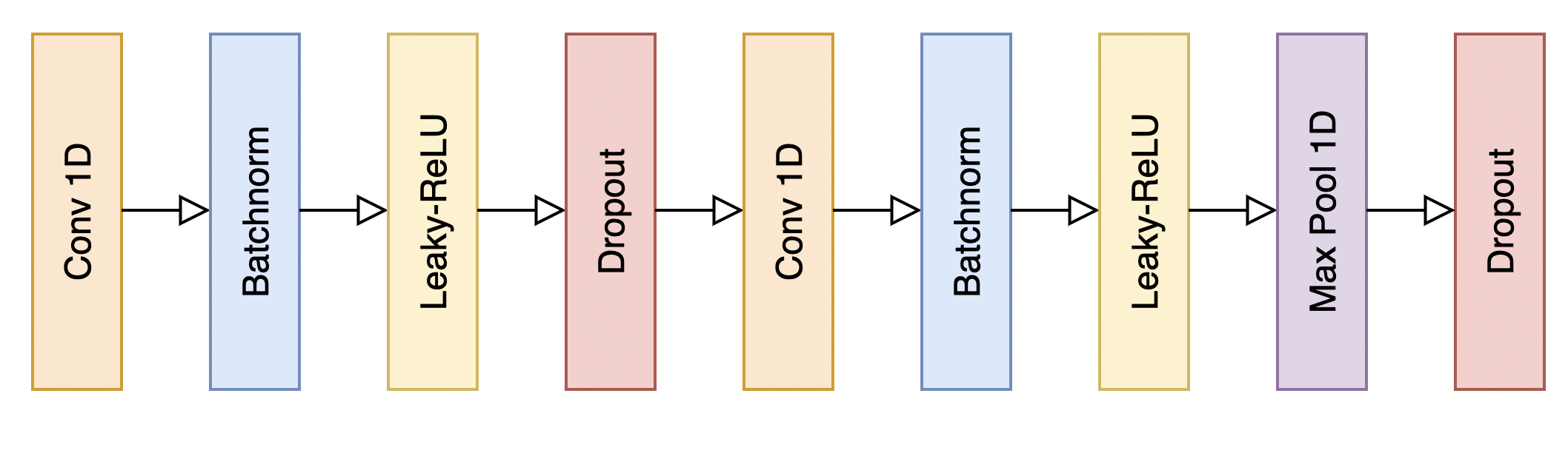

3.3.10 Convolutional neural networks

A Convolutional Neural Network (CNN)is a type of neural network specialized in processing data with a known, grid-like topology such as time-series data (1-dimensional) or images (2-dimensional) [GBC16]. Convolutional neural networks have profoundly impacted fields like computer vision [GBC16] and are used in several successful deep RL applications [MKS+13, HS15, LHP+15]. A CNN is a neural net that applies convolution instead of general matrix multiplication in at least one layer. A convolution is a form of integral transform defined as the integral of the product of two functions after one is reflected about the y-axis and shifted

| (3.24) |

where and is a weighting function.

The convolutional layer takes the input with its preserved spatial structure. The weights are given as filters that always extend the full depth of the input volume but are smaller than the full input size. Convolutional neural nets utilize weight sharing by applying the same filter across the whole input. The filter slides across the input and convolves the filter with the image. It computes the dot product at every spatial location, which makes up the activation map, i.e., the output. This can be done using different filters to produce multiple activation maps. The way the filter slides across the input can be modified. The stride specifies how many pixels the filter moves every step. It is common to zero pad the border if the stride is not compatible with the size of the filter and the input.

After the convolutional layer, a nonlinear activation function is applied to the activation map. Convolutional networks may also include pooling layers after the activation function that reduce the dimension of the data. Pooling can summarize the feature maps to the subsequent layers by discarding redundant or irrelevant information. Max pooling is a pooling operation that reports the maximum output within a patch of the feature map. Increasing the stride of the convolutional kernel also gives a downsampling effect similar to pooling.

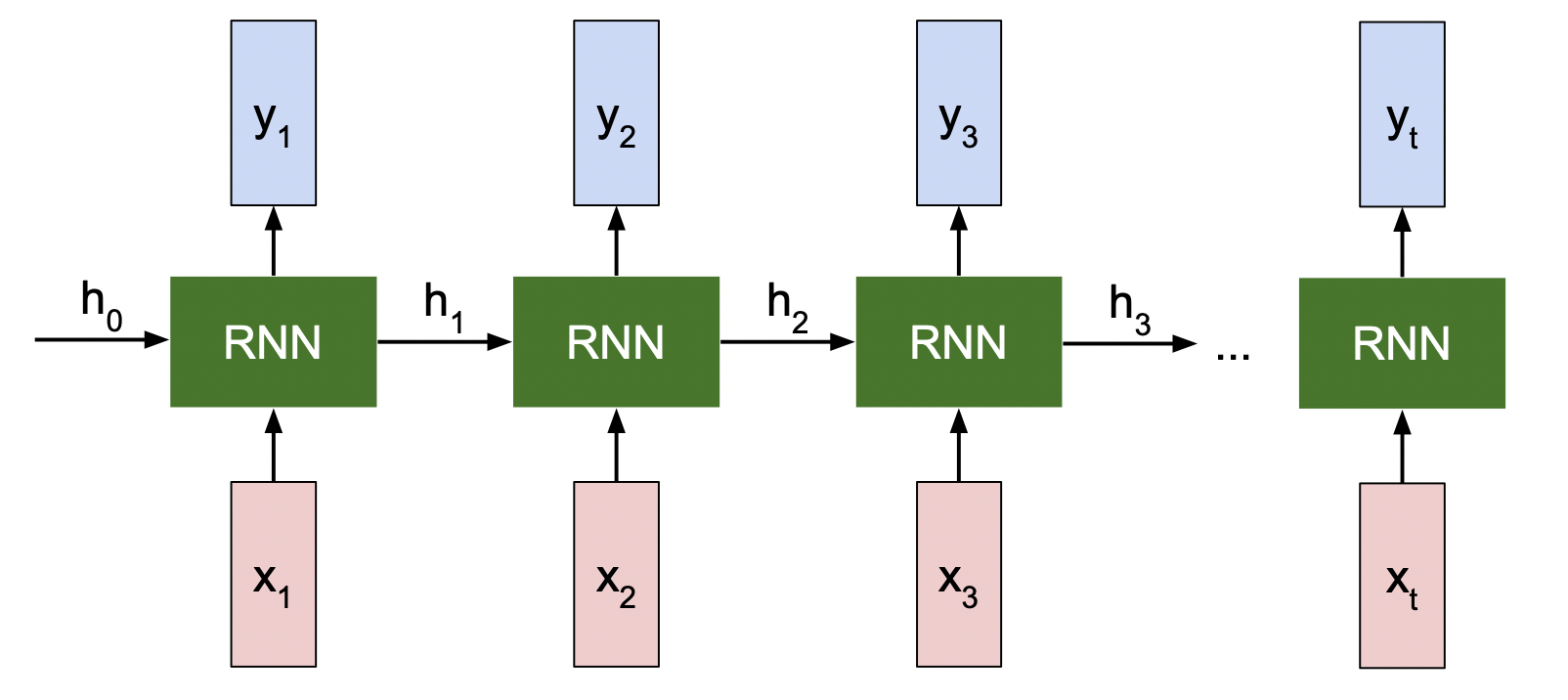

3.3.11 Recurrent neural networks

A Recurrent Neural Network (RNN)is a type of neural network that allows connections between nodes to create cycles so that outputs from one node affect inputs to another. The recurrent structure enables networks to exhibit temporal dynamic behavior. RNNs scale far better than feedforward networks for longer sequences and are well-suited to processing sequential data. However, they can be cumbersome to train as their recurrent structure precludes parallelization. Furthermore, conventional batch norm is incompatible with RNNs, as the recurrent part of the network is not considered when computing the normalization statistic.

RNNs generate a sequence of hidden states . The hidden states enable weight sharing that allows the model to generalize over examples of various lengths. Recurrent neural networks are functions of the previous hidden state and the input at time . The hidden units in a recurrent neural network are often defined as a dynamic system driven by an external signal

| (3.25) |

Hidden states are utilized by RNNs to summarize problem-relevant aspects of the past sequence of inputs up to when forecasting future states based on previous states. Since the hidden state is a fixed-length vector, it will be a lossly summary. The forward pass is sequential and cannot be parallelized. Backprop uses the states computed in the forward pass to calculate the gradient. The backprop algorithm used on unrolled RNNs is called backpropagation through time (BPTT). All nodes that contribute to an error should be adjusted. In addition, for an unrolled RNN, nodes far back in the calculations should also be adjusted. Truncated backpropagation through time that only backpropagates for a few backward steps can be used to save computational resources at the cost of introducing bias.

Every time the gradient backpropagates through a vanilla RNN cell, it is multiplied by the transpose of the weights. A sequence of vanilla RNN cells will therefore multiply the gradient with the same factor multiple times. If then , and if then . If the largest singular value of the weight matrix is , the gradient will exponentially increase as it backpropagates through the RNN cells. Conversely, if the largest singular value is , the opposite happens, where the gradient will shrink exponentially. For the gradient of RNNs, this will result in either exploding or vanishing gradients. This is why vanilla RNNs trained with gradient-based methods do not perform well, especially when dealing with long-term dependencies. Bengio et al. [BSF94] present theoretical and experimental evidence supporting this conclusion. Exploding gradients lead to large updates that can have a detrimental effect on model performance. The standard solution is to clip the parameter gradients above a certain threshold. Gradient clipping can be done element-wise or by the norm over all parameter gradients. Clipping the gradient norm has an intuitive appeal over elementwise clipping. Since all gradients are normalized jointly with the same scaling factor, the gradient still points in the same direction, which is not necessarily the case for element-wise gradient clipping [GBC16]. Let be the norm of the gradient and be the norm threshold. If the norm crosses over the threshold , the gradient is clipped to

| (3.26) |

Gradient clipping solves the exploding gradient problem and can improve performance for reinforcement learning with nonlinear function approximation [ARS+20]. For vanishing gradients, however, the whole architecture of the recurrent network needs to be changed. This is currently a hot topic of research [GBC16].

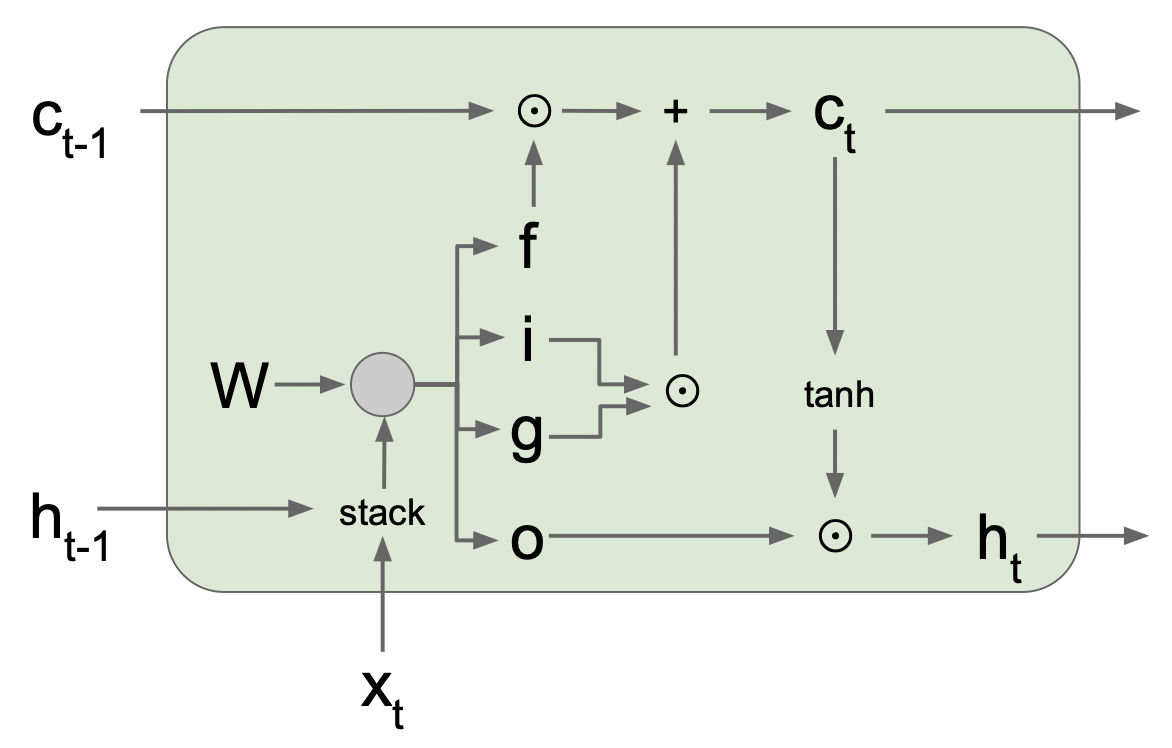

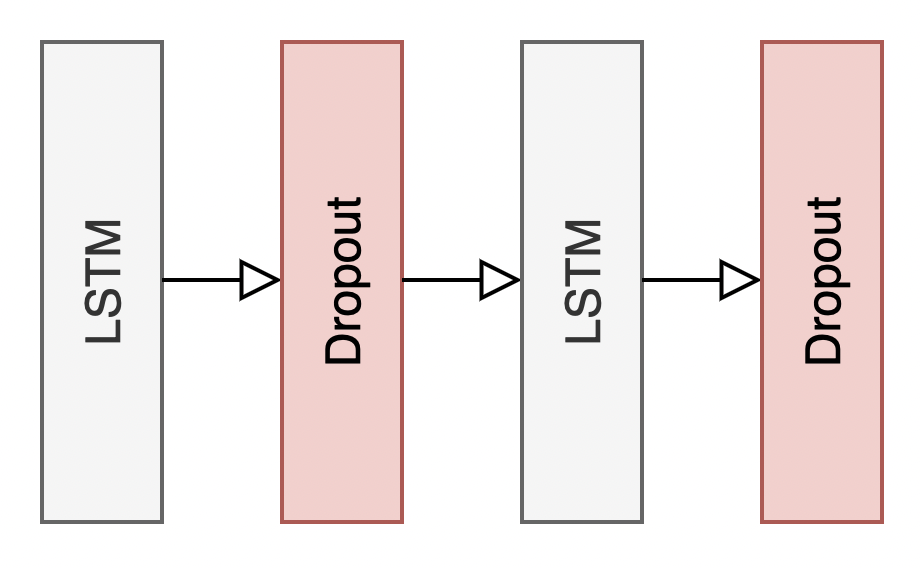

Long short-term memory

Long Short-Term Memory (LSTM)is a form of gated RNN designed to have better gradient flow properties to solve the problem of vanishing and exploding gradients. LSTMs were introduced in 1997 [HS97] and are traditionally used in natural language processing [GBC16]. Recently, LSMT networks have been successfully applied to financial time series forecasting [SNN18]. Although new architectures like transformers have impressive natural language processing and computer vision performance, LSTMs are still considered state-of-the-art for time series forecasting.

The LSTM is parameterized by the weight , which is optimized using gradient-based methods. While vanilla RNNs only have one hidden state, LSTMs maintain two hidden states at every time step. One is , similar to the hidden state of vanilla RNNs, and the second is , the cell state that gets kept inside the network. The cell state runs through the LSTM cell with only minor linear interactions. LSTMs are composed of a cell and four gates which regulate the flow of information to and from the cell state and hidden state

-

•

Input gate ; decides which values in the cell state to update

-

•

Forget gate ; decides what to erase from the cell state

-

•

Output gate ; decides how much to output to the hidden state

-

•

Gate gate ; how much to write to cell, decides how much to write to the cell state

The output from the gates is defined as

| (3.27) |

where is the sigmoid activation function. The cell state and hidden state are updated according to the following rules

| (3.28) |

| (3.29) |

When the gradient flows backward in the LSTM, it backpropagates from to , and there is only elementwise multiplication by the gate and no multiplication with the weights. Since the LSTMs backpropagate from the last hidden state through the cell states backward, it is only exposed to one nonlinear activation function. Otherwise, the gradient is relatively unimpeded. Therefore, LSTMs handle long-term dependencies without the problem of exploding or vanishing gradients.

4 Reinforcement learning

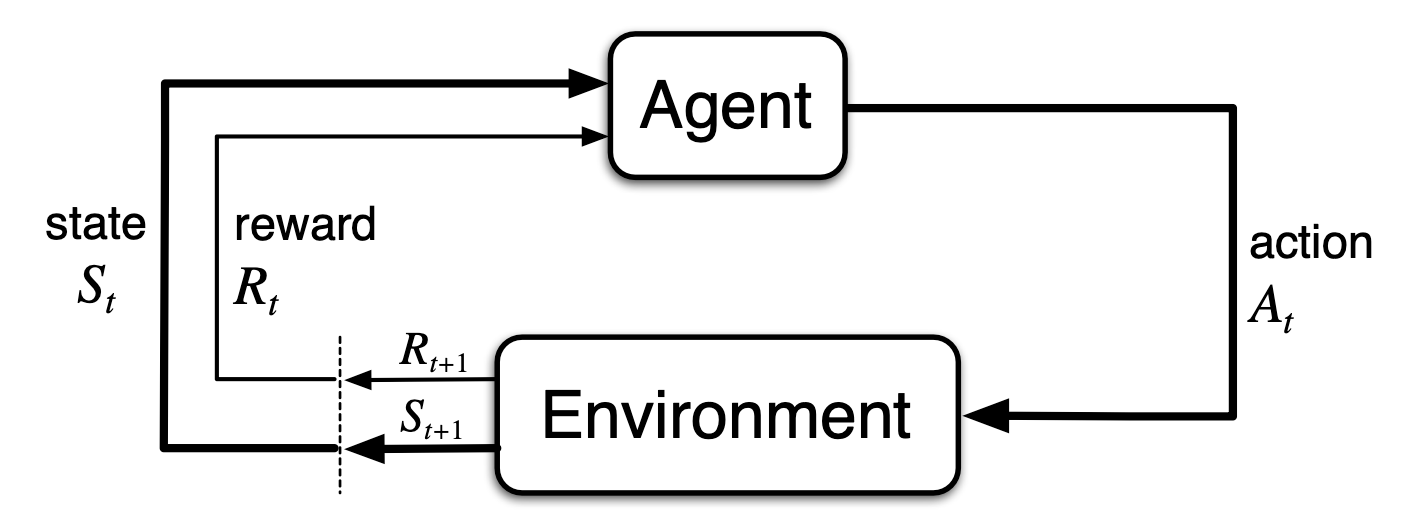

An algorithmic trading agent maps observations of some predictor data to market positions. This mapping is non-trivial, and as noted by Moody et al. [MWLS98], accounting for factors such as risk and transaction costs is difficult in a supervised learning setting. Fortunately, reinforcement learning provides a convenient framework for optimizing risk- and transaction-cost-sensitive algorithmic trading agents.

The purpose of this chapter is to introduce the fundamental concepts of reinforcement learning relevant to this thesis. A more general and comprehensive introduction to reinforcement learning can be found in “Reinforcement Learning: An Introduction” by Richard Sutton and Andrew Barto [SB18]. An overview of deep reinforcement learning may be found in “Deep Reinforcement Learning” by Aske Plaat [Pla22]. This chapter begins by introducing reinforcement learning 4.1 and the Markov decision process framework 4.2, and some foundational reinforcement learning concepts 4.3, 4.4. Section 4.5 discusses how the concepts introduced in the previous chapter (3) can be combined with reinforcement learning to generalize over high-dimensional state spaces. Finally, section 4.6 introduces policy gradient methods, which allow an agent to optimize a parameterized policy directly.

4.1 Introduction