A novel approach for quantum financial simulation and quantum state preparation

Abstract

Quantum state preparation is a vital process in quantum computing and quantum information processing. The ability to accurately and reliably prepare specific quantum states is essential for a variety of applications. One of the promising applications of quantum computers is quantum simulation. This requires preparing a quantum state that represents the system we’re trying to simulate. This research introduces a novel simulation algorithm, the multi-Split-Steps Quantum Walk (multi-SSQW), designed to learn and load complicated probability distributions using parameterized quantum circuits (PQC) with a variational solver on classical simulators. The multi-SSQW algorithm is a modified version of the split-steps quantum walk, enhanced to incorporate a multi-agent decision-making process, rendering it suitable for modeling financial markets. The study provides theoretical descriptions and empirical investigations of the multi-SSQW algorithm to demonstrate its promising capabilities in probability distribution simulation and financial market modeling. Harnessing the advantages of quantum computation, the multi-SSQW models complex financial distributions and scenarios with high accuracy, providing valuable insights and mechanisms for financial analysis and decision-making. The multi-SSQW’s key benefits include its modeling flexibility, stable convergence, and instantaneous computation. These advantages underscore its rapid modeling and prediction potential in dynamic financial markets.

Keywords quantum walk, quantum state preparation, quantum simulation, quantum finance

1 Introduction

The advent of digital computing in the 1950s significantly empowered scientists to tackle complex problems quantitatively. As computing technology progressed, it has propelled the development of modern quantitative finance, reshaping the landscape of financial analysis and decision-making. Quantum mechanics introduces several foundational principles, including superposition, entanglement, and interference which are primary characteristics of quantum mechanics. As modern science and technology advance, quantum computing emerges as a groundbreaking solution to some intractable problems for classical computing. In recent years, the convergence of computer science and quantum physics has shown promising implications in solving computationally intractable or complex problems for classical computers. Leveraging the uncertain nature of quantum mechanics, quantum algorithms have emerged as potential tools to efficiently model complicated probability distributions, challenging conventional simulation methods used by classical computers. Utilizing matter’s inherently quantum mechanical properties to perform complex computations, offers an entirely novel perspective on computational methods and processes. This makes it possible for a quantum computer to perform certain operations, such as factorization[1] and simulation[2, 3], much more quickly than a classical computer.

Uncertainty is an inherent nature of financial markets, manifesting in the unpredictability of market participants’ cognitive processes, their decision-making routines, and the general macroeconomic conditions and structural dynamics of the financial market, which directly influence asset valuation. This concept is strikingly similar to quantum theory. Quantum computing is particularly promising for the financial sector, which stands to benefit significantly from this innovation. This is primarily due to many financial scenarios that could be resolved using quantum algorithms. Our ambitions focus on developing quantum states to encapsulate the inherent uncertainties that pervade financial markets, which can be processed using quantum computers. Additionally, we aim to devise quantum algorithms to simulate the dynamic nature of financial systems.

In traditional finance, the random walk theory is a prevalent model. This theory, first postulated by the French mathematician Louis Bachelier[4], posits that the trajectory of stock prices is essentially random. In other words, the future price of a stock is independent of its past prices, making it impossible to predict a stock’s future trajectory based on historical data alone. This idea forms the basis of the Efficient Market Hypothesis[5], asserting that all available information is already incorporated into the stock’s current price, and changes to that price will only be triggered by unforeseen events. Stock prices are the product of an ongoing interplay of buying and selling transactions from all participants in the stock market. This dynamic process reflects the collective sentiment, beliefs, and actions of all these market participants. Therefore, the random walk theory of stock prices doesn’t mean prices are entirely chaotic, but rather that they evolve based on the aggregate of numerous decisions made by market participants, often in response to new information.

The potential applications of quantum computing in the financial sector[6, 7] are incredibly vast. More recent work has focused on the quantum algorithm for amplitude estimation[8] and Monte Carlo with the pricing of financial derivatives[9, 10, 11, 12, 13, 14, 15, 16]. Given that uncertainty is a fundamental characteristic shared by both finance and quantum mechanics, it is promising to employ quantum principles for the simulation of financial markets.

Indeed, utilizing the principles of quantum mechanics in financial markets offers an intriguing and novel perspective. By conceptualizing states of financial uncertainty as quantum states, we assign each potential financial outcome to a unique state within a quantum system.

| (1) |

We can then simulate the development of financial markets by applying a model resembling quantum evolution to this system.

| (2) |

We apply the quantum walk algorithm, the extension concept of random walk, to simulate the impact of investor sentiment on the price formation process. This method could provide a level of complexity in modeling financial systems that exceeds the capabilities of traditional models because of the inherently probabilistic nature and superposition capabilities of quantum systems. By tapping into the intricate and nuanced world of quantum mechanics, we can explore economic phenomena from a new vantage point, potentially uncovering insights previously unattainable with classical models.

Quantum walks, the quantum mechanical counterparts to classical random walks, offer an innovative financial simulation approach. Whereas classical random walks allow a system to move randomly from one point to another, quantum walks incorporate the principles of superposition and entanglement, enabling a quantum system to exist in multiple states simultaneously and to explore many paths at once.

In a financial context, a quantum walk could simulate multiple behaviors in parallel, potentially capturing the complexity and randomness of financial markets more accurately than a classical random walk. Therefore, applying the quantum walk algorithm to financial simulations could provide a more detailed and comprehensive understanding of potential outcomes and market behavior. This extension of random walks to the quantum realm could open new financial modeling and risk management.

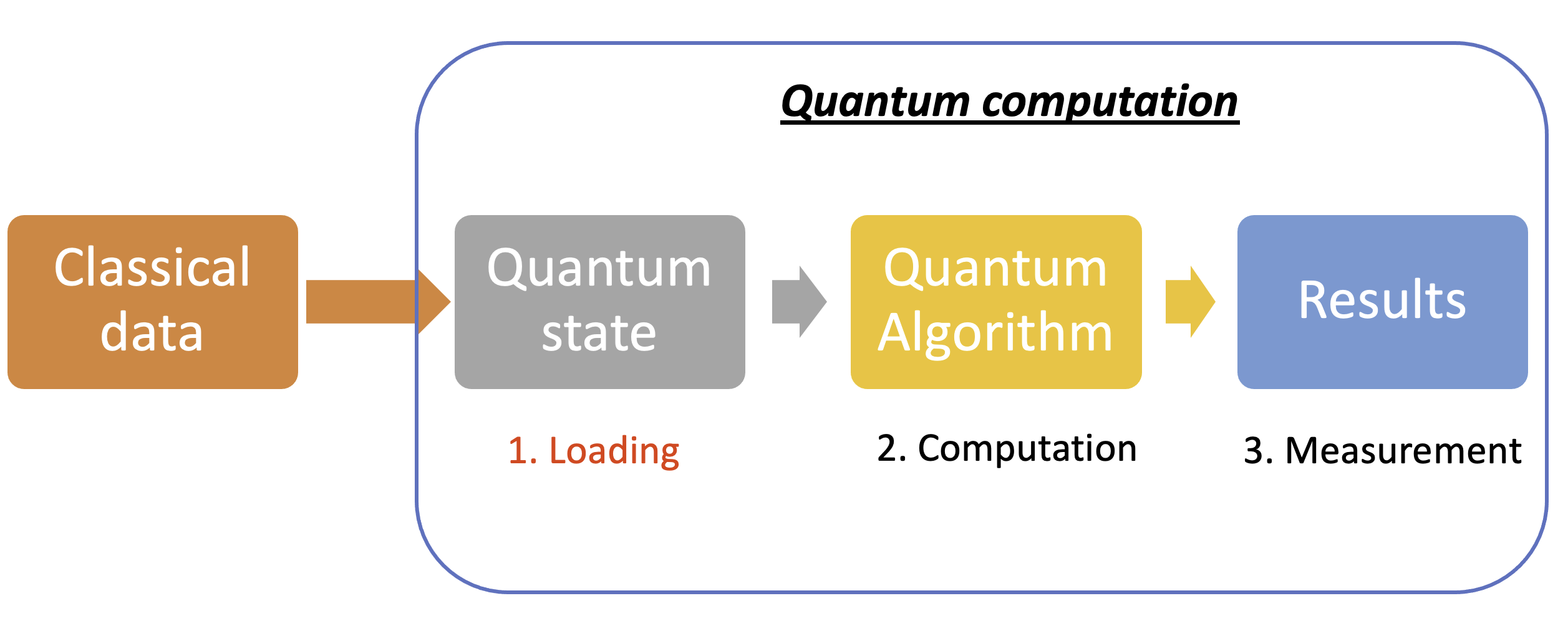

Using the quantum walk algorithm in the financial simulations allows us to set up the quantum state in a superposition of states, each corresponding to a potential financial outcome. This method generates designated amplitudes for these states in a way that closely resembles a targeted probability distribution and could also provide a novel method for quantum state preparation. Quantum state preparation is a crucial step in quantum computing and quantum simulations. The ability to prepare quantum states allows for parallel information processing, enabling quantum computers to solve specific quantum algorithms[8, 17, 18, 19, 20, 21] significantly faster than classical computers. The achievement of quantum advantage is considered an essential goal in quantum computing. The three steps of realizing quantum advantage: quantum state preparation, quantum algorithm computation, and result measurements, are shown in Fig.1.

The ability to prepare quantum states in quantum circuits has many conceivable applications. Efficient methods for simulating probability distributions in quantum circuits are critical as an ineffective and inefficient quantum state preparation algorithm could diminish the potential impact of quantum computing[22]. The randomness of quantum systems has been demonstrated [23] with the distribution of states close to the Haar-random. Haar-random[24, 25] is significant in quantum computations, as they can be used to generate arbitrary quantum states and perform quantum gates that enable applications of these quantum devices in a much broader context. These preparation methods of a generic quantum state have been designed[10, 26, 27, 28, 29, 30, 31]. Grover has proposed a scheme [26] to generate the probability distributions. It shows how to generate a superposition of quantum states by taking an ancilla register that performs a controlled rotation of angle :

| (3) |

Using ancilla qubits makes it possible to reduce the circuit depth, resulting in complexity mitigation at a scale less than exponential[30].

Moreover, Rocchetto has proposed a method[27] based on variational autoencoders to encode the probability distribution of quantum states and benchmark the performance of deep networks on states. Quantum Generative Adversarial Networks (qGAN) have been demonstrated to load distributions[10]. The qGAN combines a quantum generator and a classical discriminator to learn the probability distribution of classical training data. The quantum generator, a parametrized quantum channel, is trained to convert an input state of n-qubits, represented by , into an output state of n-qubits. A method using variational solvers to fix the rotation parameters of the gate has been proposed to generate symmetrical and asymmetrical probability distributions[28]. The authors demonstrated trajectories of the individual quantum states to understand the effect of an ancilla register to control rotation.

In this study, we introduce a novel methodology based on eq.(2) that incorporates multi-SSQW, and expanded the concept of Single-Split-Step Quantum Walk (SSQW), into the simulation of the financial system and quantum state preparation. The multi-SSQW leverages an ancilla qubit as a coin space to control the position space, representing the targeted quantum state. The structure of the paper unfolds as follows:

Firstly, we rethink the theoretical underpinnings of quantum walks and shed light on their role in simulating financial pricing and preparing quantum states. Nextly, we engineer the methodology of multi-SSQW and apply the approach on a range of test cases, on financial pricing process simulating and quantum state preparation, including normal, log-normal, and binomial distributions, with a quantum simulator accessible via the IBM Q Experience. We then demonstrate using the multi-SSQW method to facilitate quantum benefit in financial derivative pricing.

2 Multi-split-steps quantum walk (multi-SSQW)

2.1 Mathematical Model

The multi-SSQW represents an expansion of conventional quantum walks, extending its capabilities and potential applications. Quantum walks (QW)[32, 33, 34, 35, 36, 37, 38, 39, 40], which are the quantum equivalent of classical random walks, are used as a foundation for generating models of controlled quantum simulation. Quantum walks enable the walker to simulate several quantum mechanical phenomena by tuning a QW’s parameters and evolution coin operators. The formalism for quantum walks is broadly classified into the discrete-time quantum walk (DTQW) and the continuous-time quantum walk (CTQW). Both approaches have unique features that cause them suitable for performing quantum computing tasks. Here we will focus only on the one-dimensional DTQW. A classical walk can be described using just a position Hilbert space, while a DTQW, or quantum walk, requires an additional coin Hilbert space to express its dynamics fully. This coin space represents the internal state of the walker and is necessary to capture the controlled dynamics of the walker. Hilbert space of quantum walk is defined as follows.

| (4) |

where is the coin Hilbert space and is the position Hilbert space. The coin Hilbert space for one-dimensional DTQW has the basis states and the position Hilbert space is defined by the basis states where . The probability amplitude of the quantum state at position can be represented by

| (5) |

where describe the state of DTQW with two internal degrees of freedom . In a Discrete-Time Quantum Walk (DTQW), the system’s evolution is governed by two unitary operators: the coin operator and the shift operator. The shift operator moves the walker in a superposition of position states, while the coin operator acts on the coin Hilbert space and determines the amplitudes of the position space. The coin Hilbert space represents the internal state of the walker and plays a crucial role in determining the overall dynamics of the system. A universal operator is defined as

| (6) |

where are the three independent parameters and the most general unitary coin operator. Therefore, accurately estimating the coin parameters is essential for effectively using quantum walks as a quantum simulation tool and for further research on modeling realistic dynamics. Finding patterns in complex data can be challenging, but an algorithm that automates the learning process can solve this problem.

The shift operator is an essential part of the DTQW. A unitary operator moves the quantum walker in a superposition of position states. The shift operation is defined as,

| (7) |

In other words, the shift operator shifts the position of the particle one step to the right if the internal state is or one step to the left . The initial state of the system is a superposition of the position states, with the internal state of the particle determined by the coin operator and defined as

| (8) |

At each time step, the shift operator is applied to the position state after the coin operator is applied to the internal state of the particle. Together, these two operators form the evolution operator of the DTQW, which describes the overall dynamics of the system. This process is repeated several times, and the system’s final state is a superposition of position states, with the amplitudes determined by the coin operator.

| (9) |

where is an identity in space.

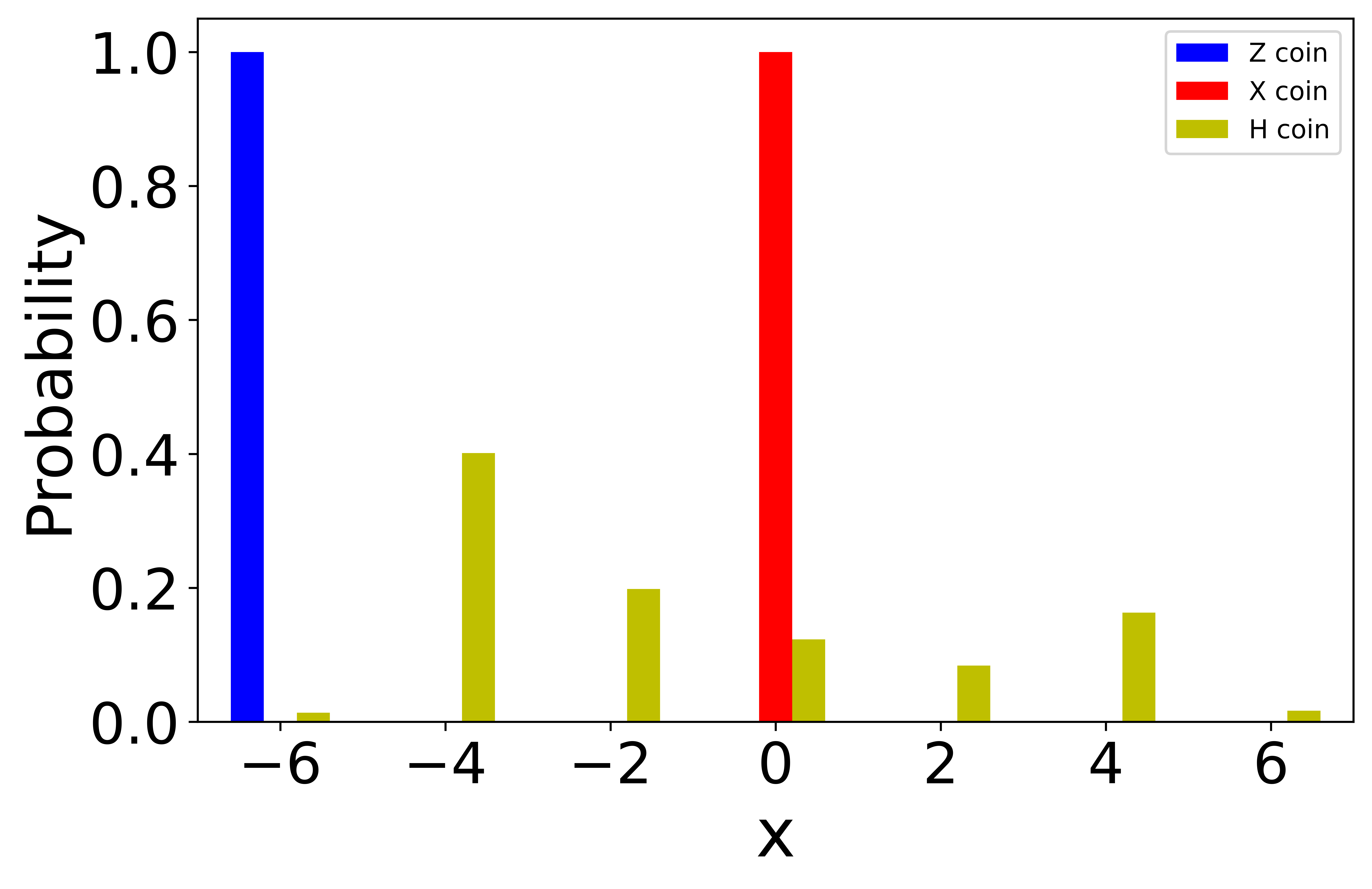

The probability distributions in position space of a discrete-time quantum walk (DTQW)[35, 36, 38], shown in Fig.(2), do not resemble the probability distributions in everyday life. In the marketplace, prices are typically determined by the interaction of buyers and sellers. The price of a good or service in the market is established through the agreement between investors. Sentiment-induced buying and selling is an important determinant of stock price variation. The shaping of short-term financial market prices predominantly hinges on the sentiment of investor[41, 42], broadly classified into optimism and pessimism. Investors who are optimistic play a proactive role in investing, which creates an upward push for the stock price. On the contrary, pessimistic investors, who decide to sell and withdraw from the market, generate a downward pull on the stock price. Inspired by the free market economy, we introduce the split-step quantum walk(SSQW)[43, 44] that can be regarded as a financial simulation.

SSQW is a specific type of quantum walk that divides the evolution of the quantum system into two steps, one to the right and one to the left. The evolution operator is divided by a composition of two half-steps,

| (10) |

where is a universal coin operator as Eq.(6) and shift operators are defined as,

| (11) | ||||

where represents the walker goes to right() or stop in place() and represents the walker goes to left() or stop in place().

The coin operators, and , serve as indicators of investor sentiment, representing optimism and pessimism respectively. embodies the amplitude of the investor’s optimism, influencing the likelihood of a price increase. Conversely, reflects the amplitude of the investor’s pessimism, regulating the probability of a price decrease.

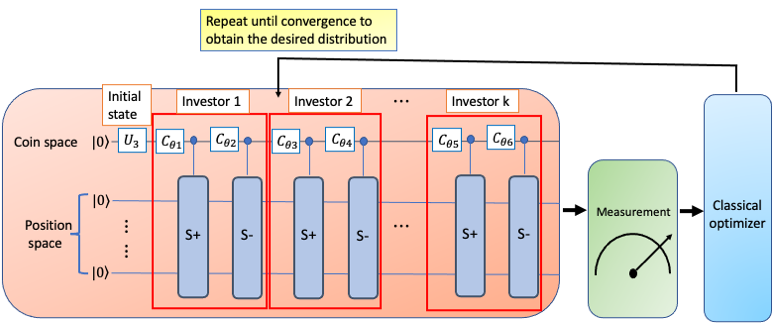

The financial market is marked by the participation of a diverse range of investors, each with their unique attitudes and investment strategies. In order to capture this diversity, we build upon existing concepts and introduce the multi-SSQW that corresponds to a multitude of investors. This approach allows us to design a quantum model that simulates various investor sentiments. Such a quantum model aids in simulating trader sentiment within the financial market, enabling us to predict the distribution of short-term financial prices. The scheme for simulating the distribution of short-term financial prices is introduced with a practical approach to find patterns in complex data and map them to a multi-SSQW dynamic system and the architecture has shown below in Fig.(4). In the multi-split-step quantum walk (multi-SSQW) scheme, the initial coin state, represented by the U3 gate, incorporates three parameters corresponding to the current financial state or the indicator of the general attitude or mood of the whole market sentiment. Moreover, each operator, simulated by two U3 gates, indicates the attitude or sentiment of investors toward a particular security. These parameters are leveraged to encapsulate the diverse sentiments of investors in our model.

We have extended the concept of a Split-Step Quantum Walk (SSQW) to a multi-Split-Step Quantum Walk (multi-SSQW), employing multiple quantum walkers to represent investors with diverse investment strategies in the market. In modeling the intrinsic uncertainty in financial markets, we showcase the efficacy of our purpose-built multi-SSQW quantum algorithm and circuitry through its application in replicating the price distribution in real-world stock markets.

2.2 Solution Architecture

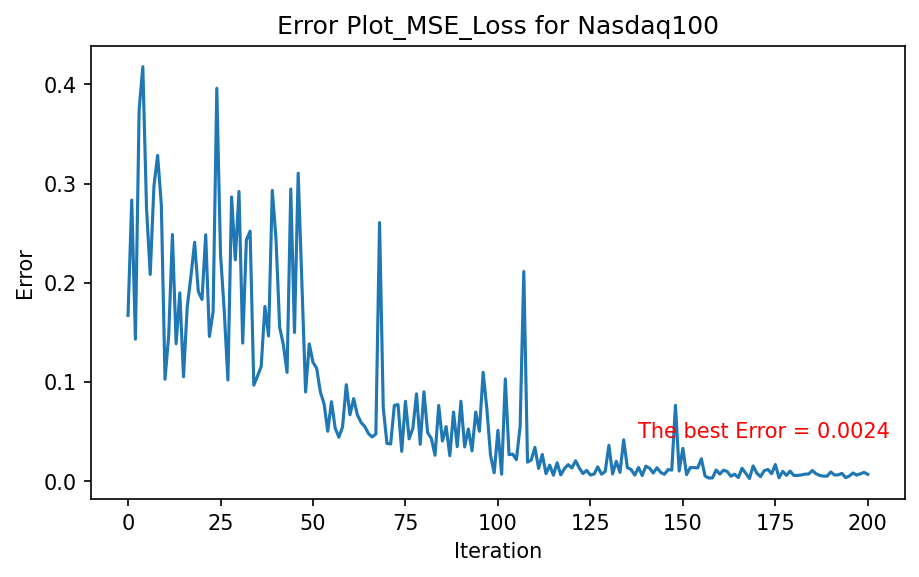

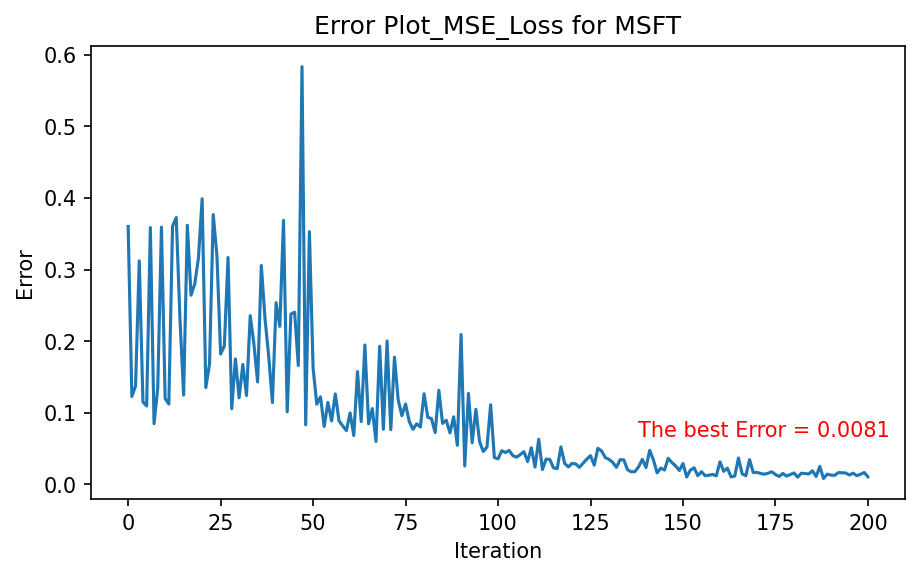

The multi-SSQW framework leverages a dual-domain computational approach, involving a Parameterized Quantum Circuit (PQC) and a classical optimizer. The PQC is composed of n+1 qubits, one designated for coin space and the remainder for position space. This setup is employed to represent and emulate the distribution of short-term financial prices. To fine-tune these parameters in alignment with empirical data, the framework employs a classical optimizer. The optimizer implements the Constrained Optimization By Linear Approximation (COBYLA) algorithm to refine the trained results toward the target distribution. The COBYLA optimizer uses the mean-square error (MSE) and KL divergence as loss functions for an enhanced approach to the targeted distribution. This methodology allows for financial simulation and preparing the probability data into a quantum state, effectively bridging the gap between classical finance models and quantum simulation.

The coin space of a multi-SSQW that performs a controlled motion of a walker on the position space is similar to the ancilla qubit taking a controlled rotation in Eq.(3). The goal is to optimize the coin parameters of a multi-SSQW to achieve the targeted distribution of the position space, and then we only compute the position space. We will accomplish this by using parameterized quantum circuits (PQC). The steps for this process are as follows:

-

•

Begin with a classical targeted data set sampled from a distribution of short-term financial prices.

-

•

Implementation of multi-SSQW uses an ancilla qubit representing the coin space and N qubits representing distributions in the position space.

-

•

Imply operators or walkers on the quantum circuit and repeat steps.

-

•

Measure the state amplitudes of the position space and compute the trained distribution.

-

•

Update the coin parameters using the classical optimizer with the mean square error(MSE) and KL-divergence to quantify the difference between the trained probability distribution from the targeted probability distribution.

-

•

Iterate times until converge to the targeted distribution

3 Results

3.1 Performances with daily return distributions of stocks

We conducted an extensive simulation to gauge the effectiveness of the multi-SSQW framework with daily return distributions of various stocks. Our results indicate that this approach successfully leverages the advantages of quantum computation within the financial arena.

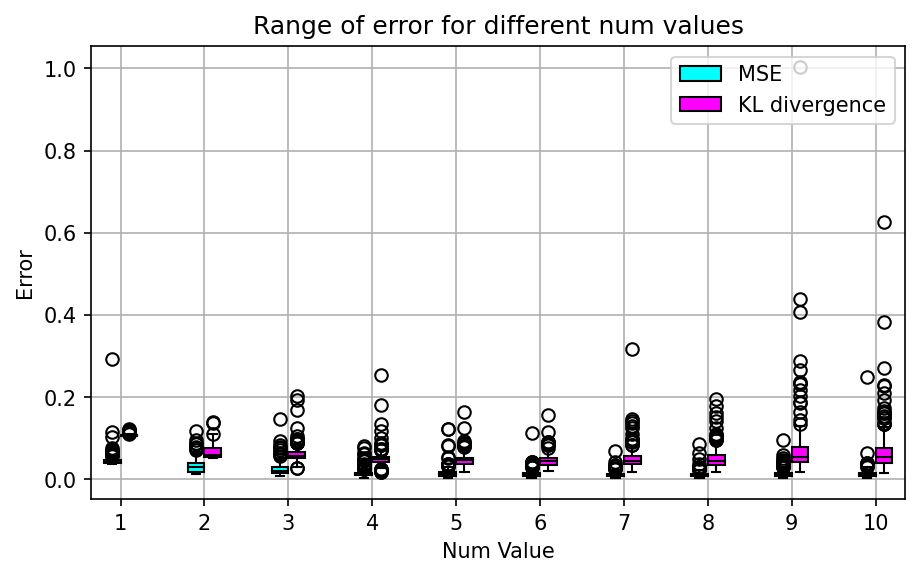

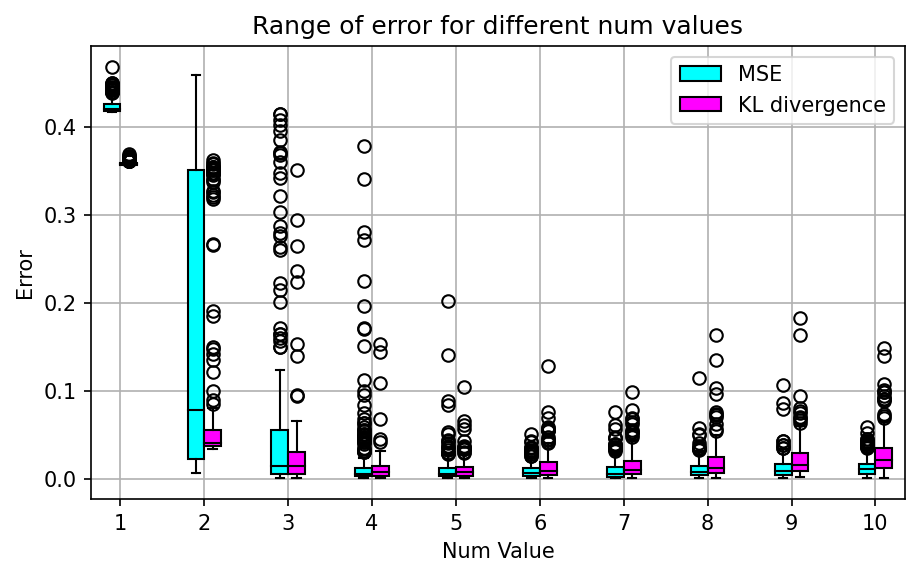

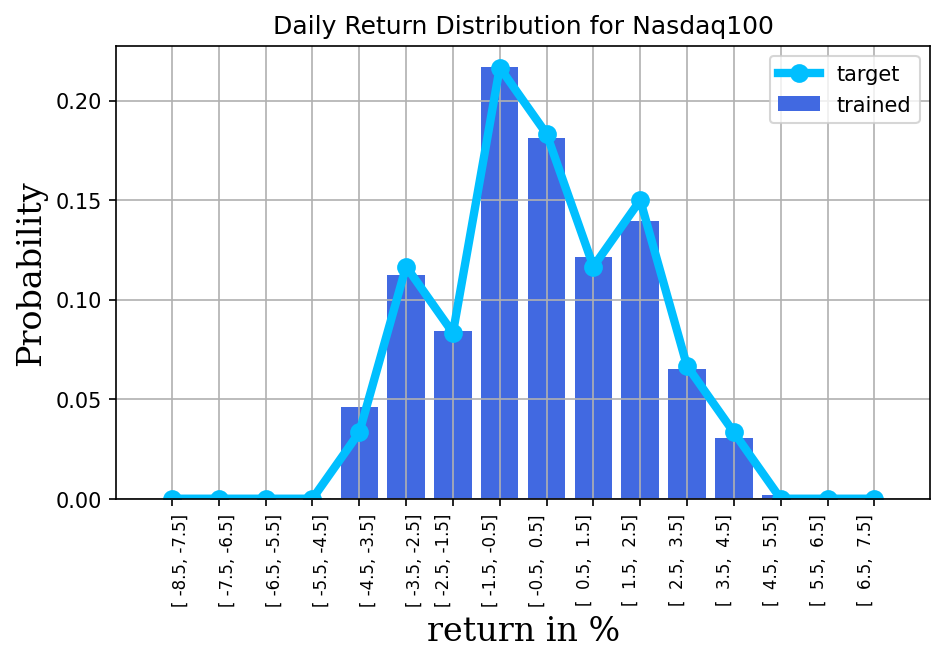

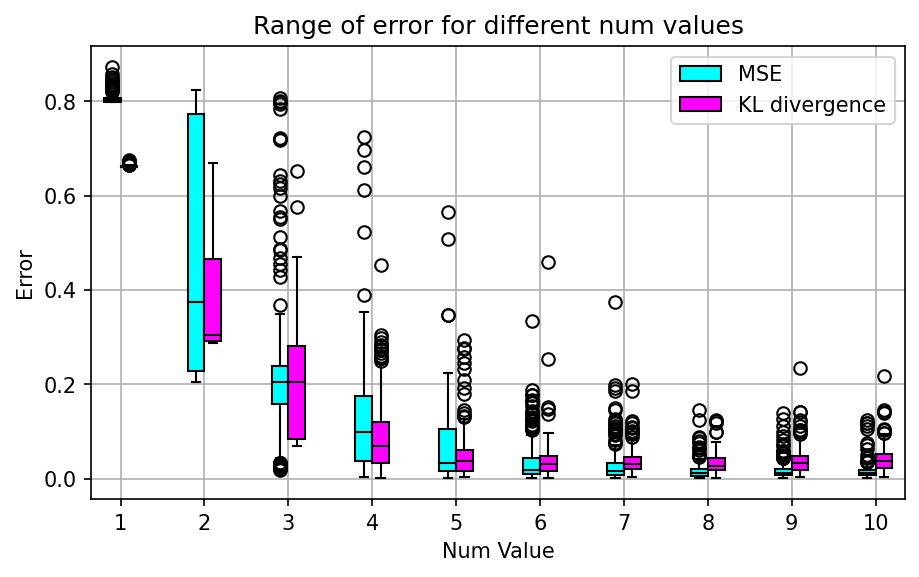

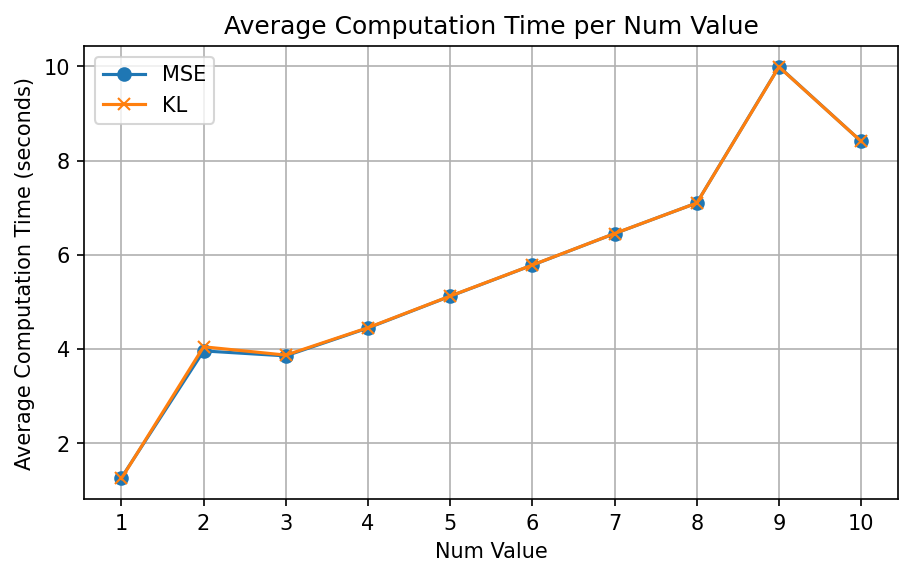

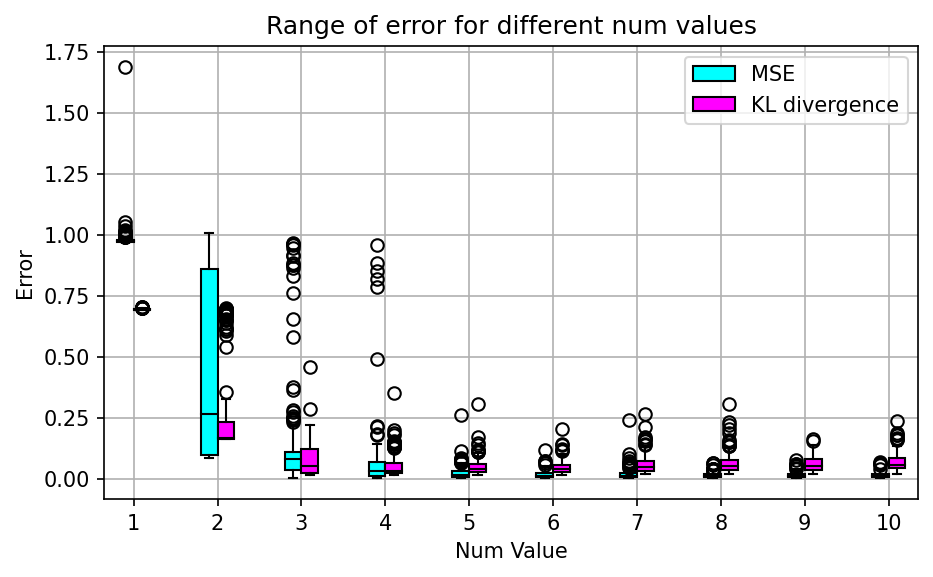

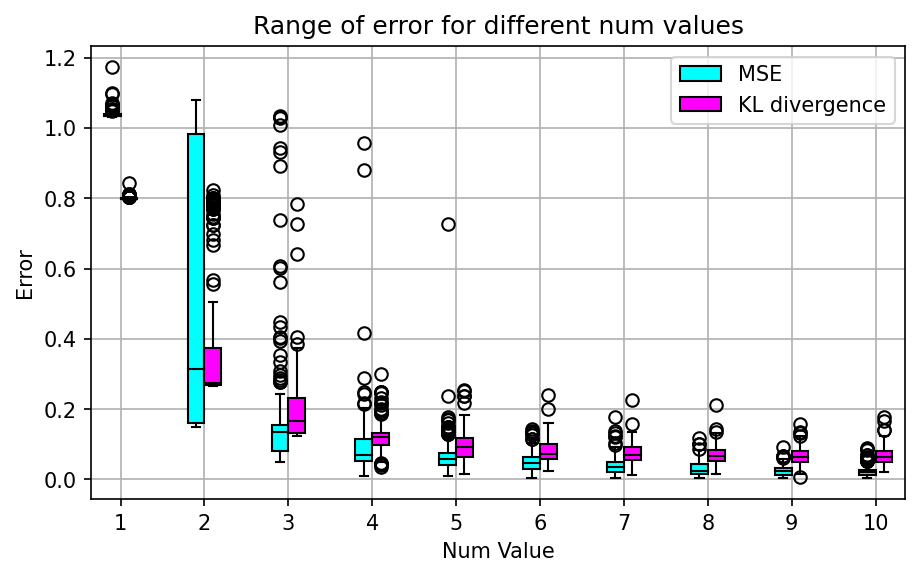

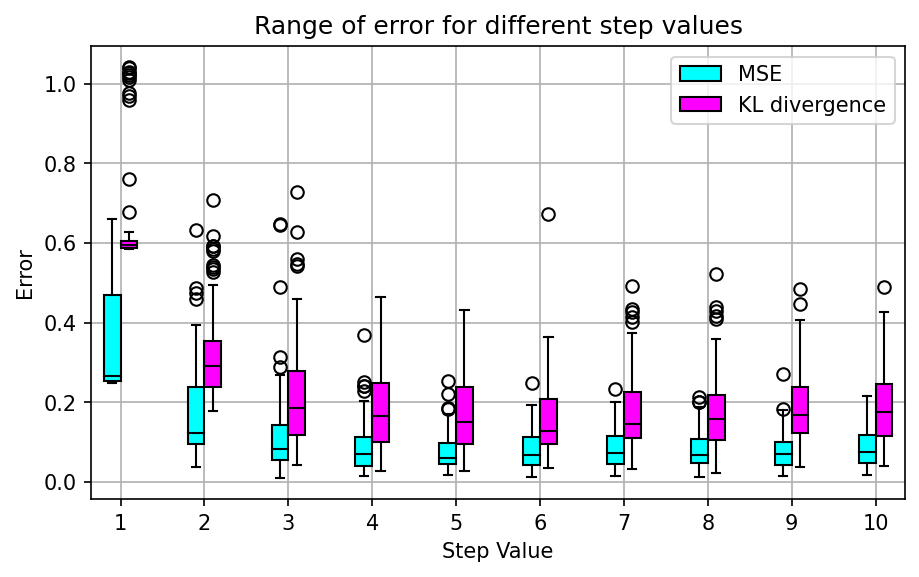

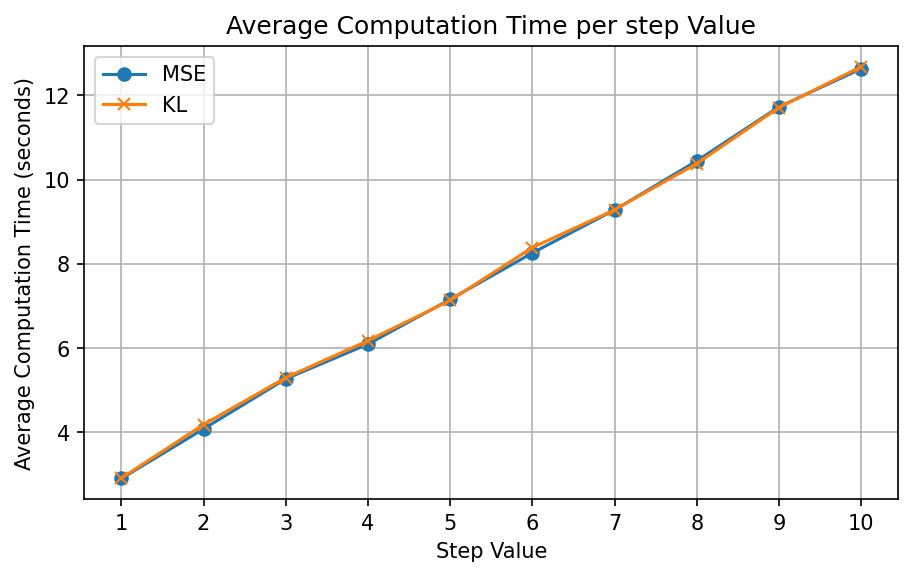

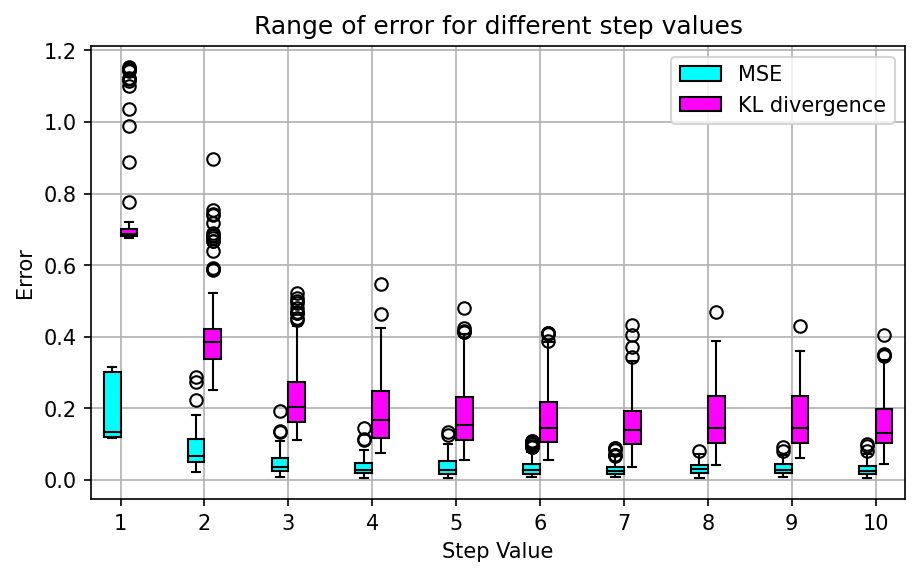

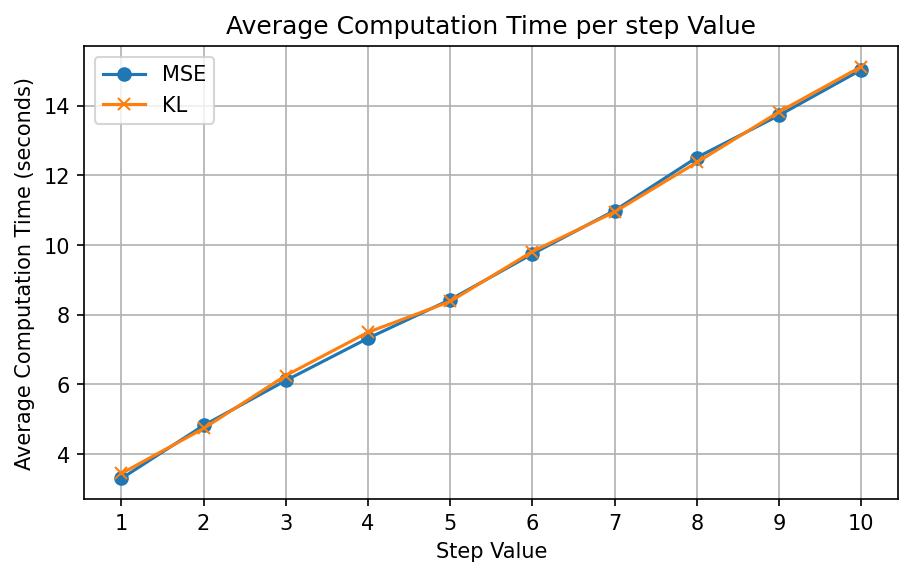

A daily return distribution offers a statistical portrayal of a financial asset’s daily returns, such as shares or commodities. It’s the day-to-day value change in percentage terms for the asset. This distribution illustrates the frequency of different return values, enabling investors to evaluate the associated risks and potential returns of an investment. Typically presented as a histogram, the x-axis represents the return percentage, while the y-axis indicates probability frequency. To create a daily return distribution, we initially collect real stock data from Yahoo Finance every day over a specified duration(2022-01 2022-03). We then categorize these daily returns into 16 distinct groups based on their respective percentages. This data is then transformed into a frequency distribution bar chart to provide a more visual and intuitive understanding of the returns distribution. Afterward, we employ the multi-SSQW approach to simulate these outcomes, yielding a more realistic probability distribution of the market. Our study involves simulating the daily return distribution over a quarter of various stocks or indices. Initially, we performed simulations 100 times, experimenting with num(the number of walkers) within a range from 1 to 10 and . This allows us to analyze the error statistically, observe the convergence behavior, and document the computation time for each scenario. Subsequently, we introduce random parameters to execute optimization simulations. These simulations enable us to generate the resultant data and the status of error convergence, thereby validating the efficacy and reliability of our approach. This structured and systematic procedure aids in providing a comprehensive understanding of the daily return distribution for different financial assets.

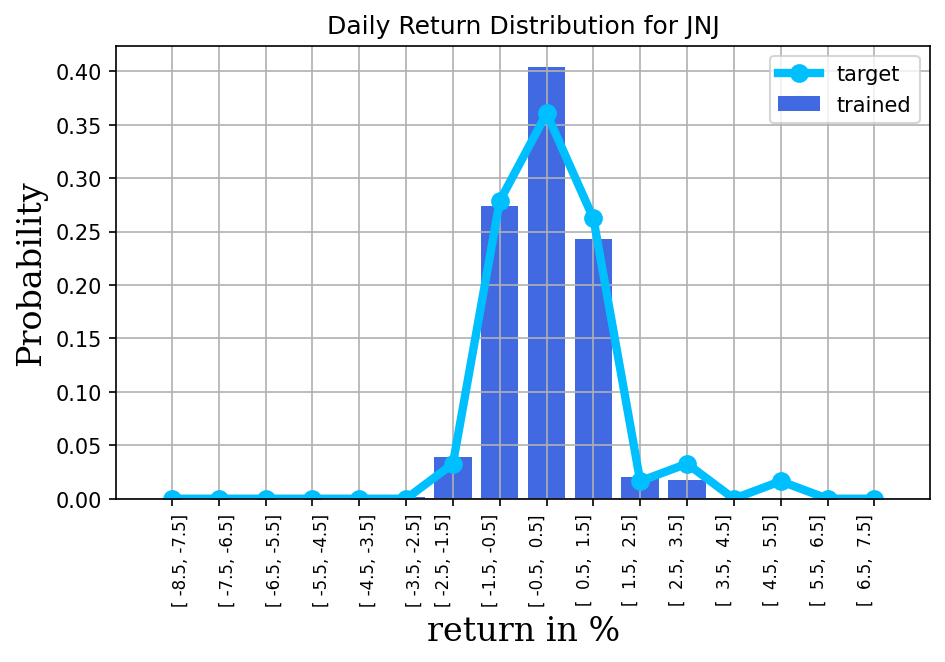

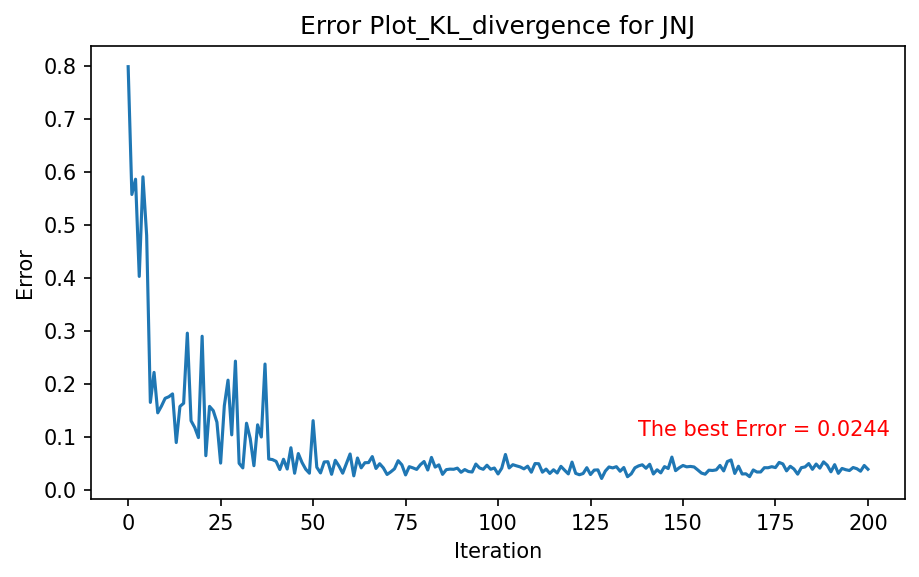

In Fig 5, We conducted an evaluation of the multi-SSQW method’s efficacy with respect to Johnson & Johnson (JNJ). Our investigation involved the utilization of multi-SSQW to generate a simulation of the distribution of daily returns for JNJ over a quarter. The results indicate a strong correspondence when the number of walkers is set to 4, with the simulated and actual distributions closely aligning.

From a financial perspective, JNJ is a multinational corporation based in the United States that manufactures pharmaceutical and consumer packaged goods and often viewed as a defensive sector because the demand for healthcare products and services remains relatively steady, regardless of economic cycles. This characteristic makes JNJ an attractive option for conservative investors seeking stable returns. In our simulation, the findings display a strong alignment when the number of walkers is set to 4. This pattern suggests the prevalence of less sentiment-driven investors, which can be interpreted from a financial perspective as a tendency towards stability and predictability in the stock’s performance.

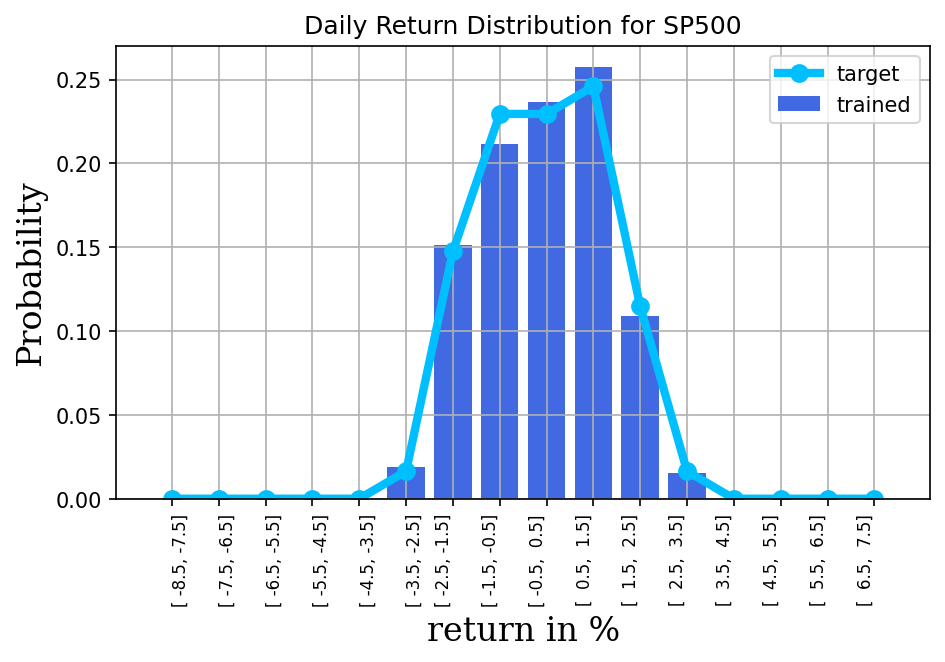

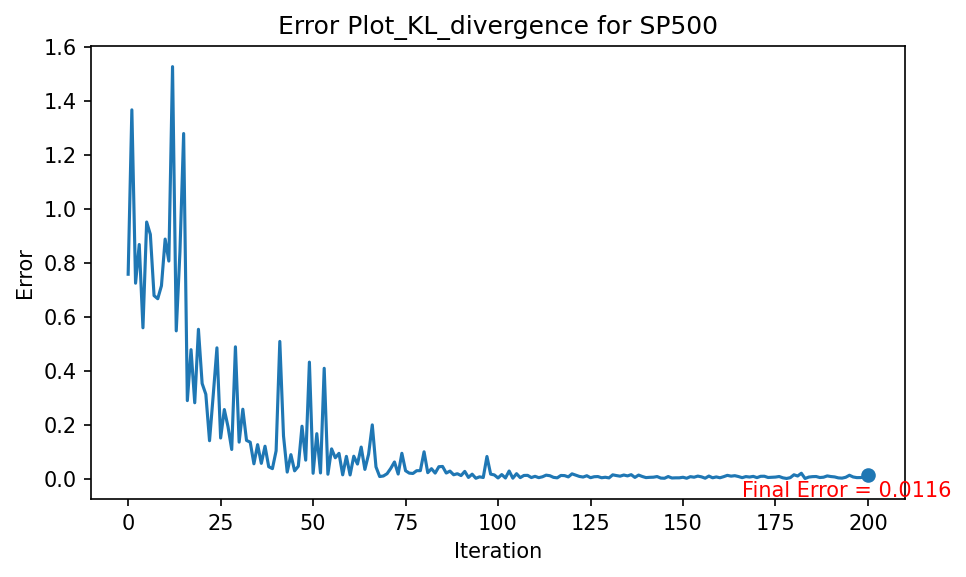

In Fig 6, we simulate the distribution of S&P500. The Standard & Poor’s 500(S&P500) is a stock market index that measures the stock performance of 500 large companies listed on stock exchanges in the United States. The index includes companies from all sectors of the economy. For large companies such as those in the S&P 500, stable operations, good corporate governance, clear future planning, and strong performance all attract long-term investors. Given the relatively homogeneous investor base, fewer numbers are required for the simulation results to converge to an optimal outcome.

The development of the technology sector is highly dependent on innovation, which often makes the prospects of tech companies full of uncertainty. A breakthrough technology or product can swiftly disrupt the market dynamics and are more prone to sentiment. This tends to draw in a significant number of noise investors who do not trade on the basis of information and make irrational investment decisions. Consequently, this causes the stock prices of some companies to experience dramatic swings. Tech stocks are usually significantly influenced by market sentiment. In Fig.7, the simulation shows the behavior could indicate a larger proportion of sentiment-driven investors.

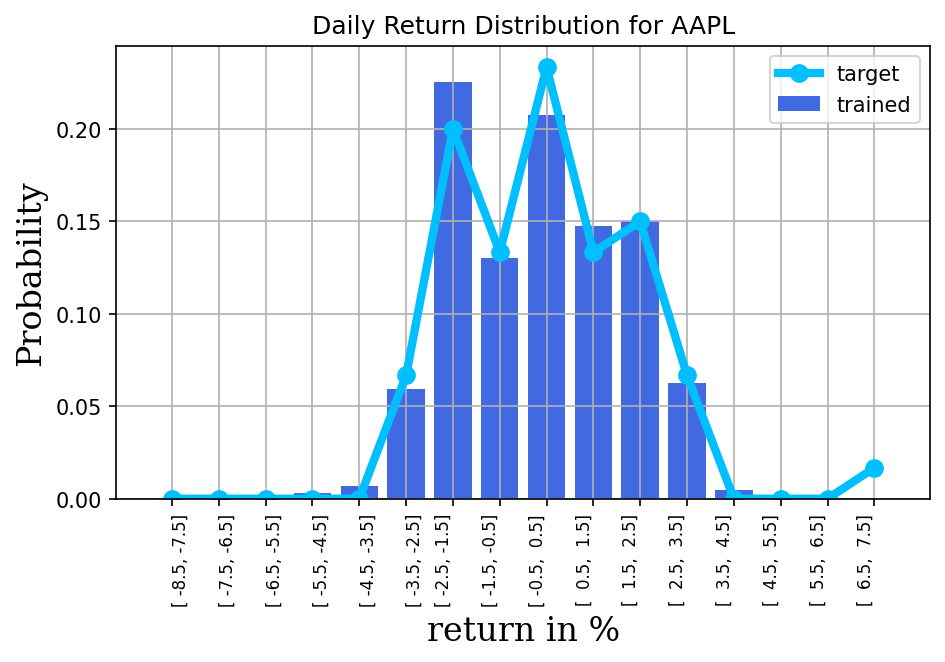

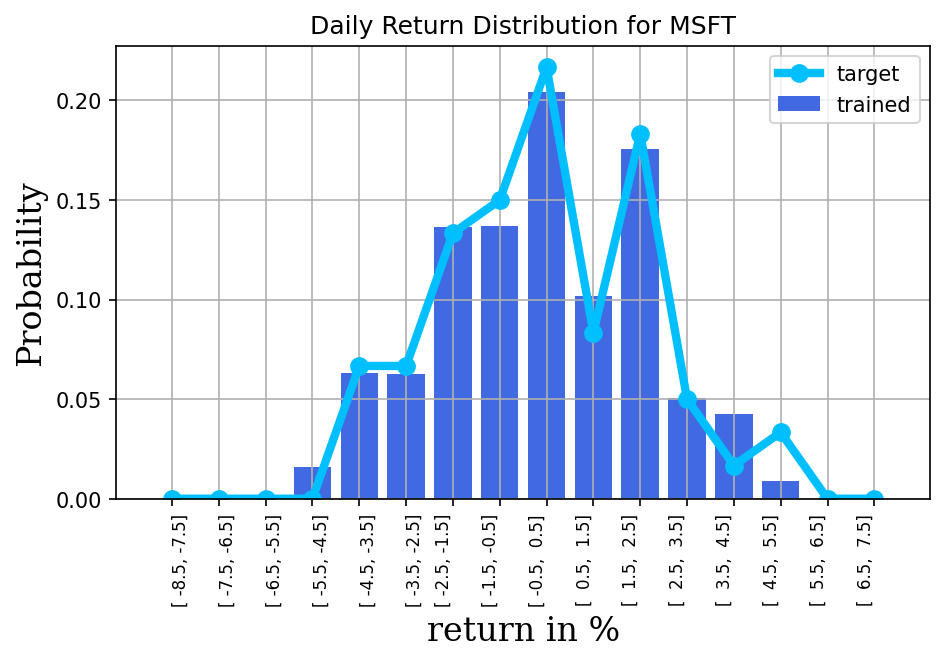

Apple and Microsoft stand among the world’s leading technology giants. They have a major influence on global technology trends and garners significant attention from investors globally. However, it is important to note that its distribution diverges from the typical normal distribution, escalating the complexity involved in its simulation. In Figure 8and 9, we demonstrate the robust simulation capabilities of the multi-SSQW methodology, specifically applied to complex entities such as Apple and Microsoft.

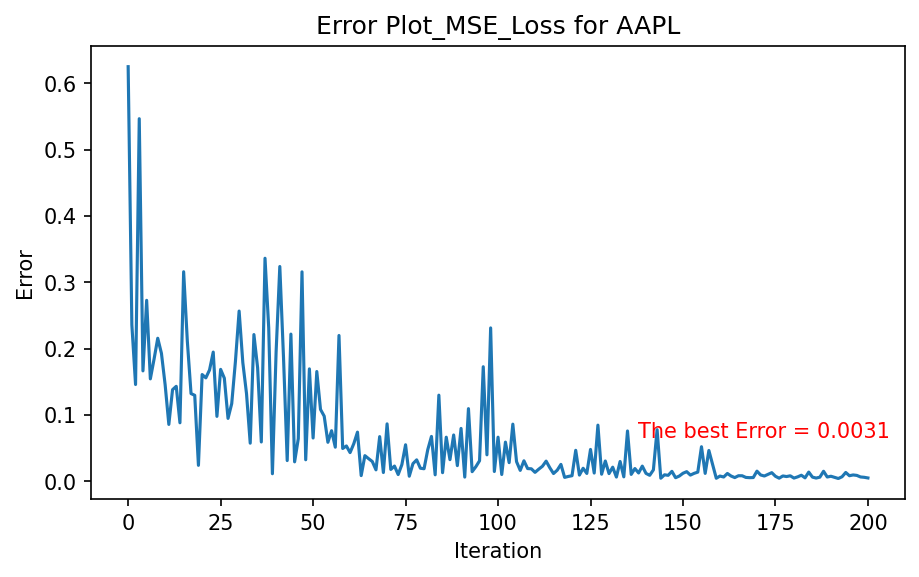

In this section, we demonstrate the ability of multi-SSQW to function as an effective financial simulator. It is capable of accurately modeling intricate financial systems and providing reliable simulations. One of the highlights of this approach is its inherent capability to exhibit convergence and provide instantaneous results, which makes it a powerful tool in financial analytics and modeling. Our experimental observations show that enhancing the count of walkers can significantly lower error rates. Increased participant diversity for a specific commodity can facilitate more precise valuations in finance. In machine learning, integrating more parameters can boost accuracy without imposing a substantial computational load. Crucially, the method demonstrates steady convergence, highlighting this approach’s efficacy.

3.2 Performances of the binomial distribution

The binomial distribution is a probability distribution that describes the number of successes in a fixed number of independent Bernoulli trials with the same probability of success. A common example of a binomial distribution is a coin toss, where the outcome can be either heads (success) or tails (failure), and each toss of the coin is an independent event.

Probability theory[45, 46], the mathematical study of randomness, is built upon the concept of probability distributions and the random variables they describe. Every distribution has a specific application and is characterized by certain parameters which help to define the shape and probabilities of the distribution.

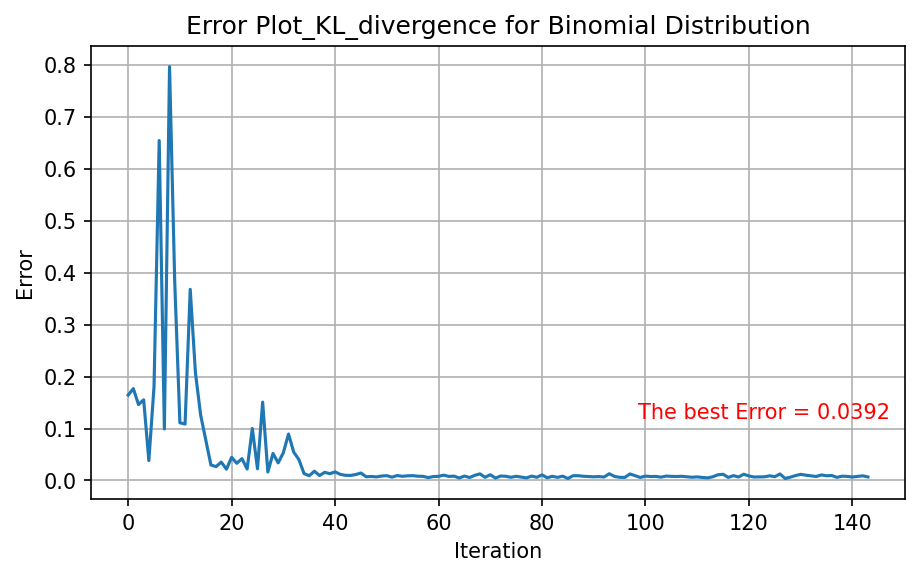

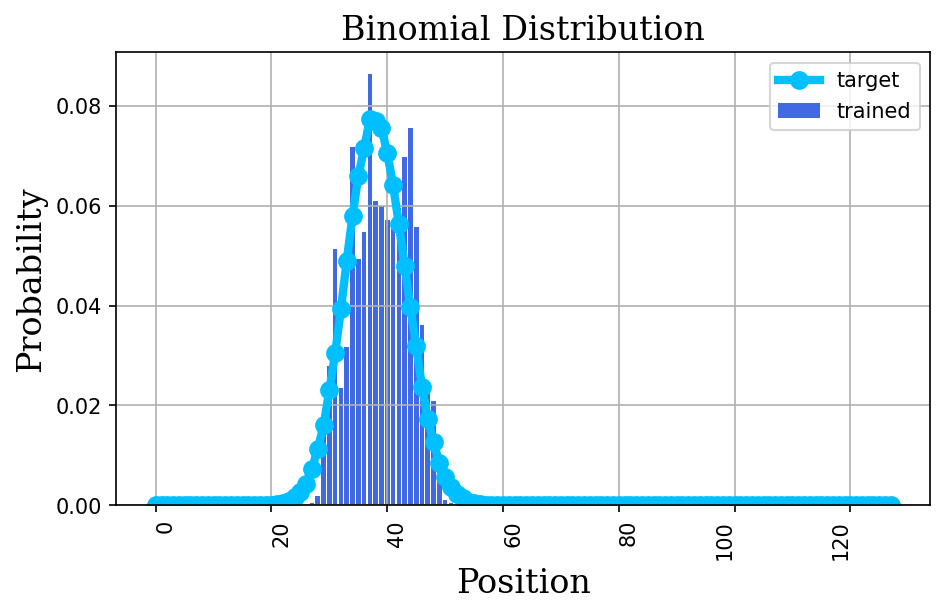

We demonstrate the utilization of multi-SSQW for the simulation of binomial distributions, shown in Figures 10, 11, and 12. These are accomplished by adjusting the coin operator coefficient and the walker count to mirror the success probability and fine-tuning the number of control steps to match the characteristics of the binomial distribution. We present three distinct binomial distributions, each with a success probability of 0.3, undergoing 31, 63, and 127 trials, respectively. The outcomes, derived via the multi-SSQW approach, validate our ability to use two quantum walks, incorporating six parameters each and a suitable number of steps, to depict the binomial distribution. The multi-SSQW approach enables us to procure a statistical approximation of the binomial distribution with control steps of 3, 5, and 10, respectively.

3.3 Application: European call option price

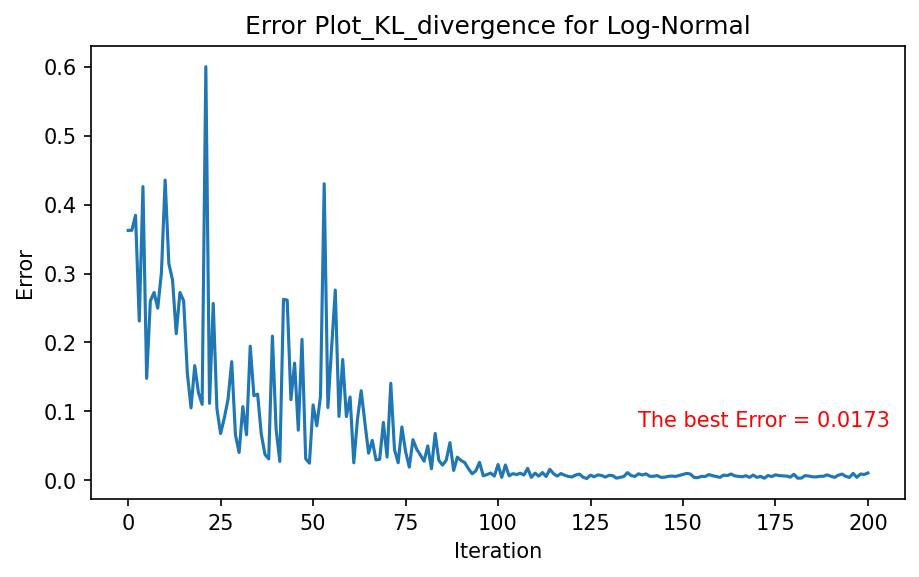

The log-normal distribution is a probability distribution of a random variable whose logarithm is normally distributed. One of the main properties of the log-normal distribution is that the values are skewed to the right, meaning that the tail of the distribution is on the right side, representing large values. It also has thicker tails than a normal distribution, meaning extreme events are more likely. This is why it helps model variables that fluctuate widely, such as stock prices. The log-normal distribution also can be used to price options by assuming that the underlying asset’s price follows a geometric Brownian motion, which means that the logarithm of the asset’s price follows a normal distribution. This assumption is the basis of the Black-Scholes model, which is a widely used method for pricing options. This is evidenced by its practical application in financial derivative pricing and the simulation of financial markets. In the following, we demonstrated that the multi-SSQW scheme enables the exploitation of the potential quantum advantage in finance, such as European call option pricing.

The Black-Scholes (BS) model[47] is widely used in the financial industry to value options and other financial derivatives. is used to determine the theoretical value of an option by using specific parameters such as the underlying asset’s price, strike price, time to expiration, risk-free interest rate, and volatility. The BS model calculates the option value by assuming that the underlying asset’s price follows a geometric Brownian motion, a continuous-time stochastic process. Considering this, the BS model can calculate the probability distribution of the underlying asset’s price at expiration.

We approximate the trained probability distribution, leveraging multi-SSQW with num=3 and step=4, and compare it with the targeted probability distribution for the parameters by plotting them together, as shown in Fig. 13. Now, the trained probability distribution can be used to evaluate the expectation value of the option’s payoff function. We can see that the analytically calculated expected payoff is 0.1739 when using the targeted distribution, and 0.1460 when using the trained distribution. Therefore, when the trained probability distribution is more accurate, resulting in a more favorable outcome after calculation.

Drawing from prior experience, we concurrently adjust the and parameters to model the log-normal distribution. We construct an approximation of the trained probability distribution, employing multi-SSQW with and . This approximation is juxtaposed against the targeted probability distribution for parameters ,, , and . The comparison is visualized in Fig. 13. The trained probability distribution is subsequently used to evaluate the expected value of the option’s payoff function. The analytical computation reveals an expected payoff of 0.1739 when using the targeted distribution and 0.1460 when employing the trained distribution. Hence, the more precise the trained probability distribution, the more favorable the outcome after calculation.

4 Discussions

In our research, we present preliminary theoretical exploration and practical applications that illustrate the effectiveness of our approach in conducting quantum financial simulations and quantum state preparation. Our strategy harnesses the unique strengths of quantum computation, and the multi-SSQW can accurately model intricate financial distributions and scenarios. This offers fresh insights and tools for financial analysis, decision-making, and quantum state preparation. The multi-SSQW algorithm offers several notable benefits:

Flexibility in Modeling: Multi-SSQW boasts exceptional adaptability in modeling complex systems, including those in the financial domain. By enabling adjustments to variables such as the number of walkers and steps and optimizing parameters in the coin space, it exhibits remarkable versatility. This adaptability allows it to accurately depict a wide range of complex systems, making it a potent and flexible tool for applications in financial simulations and beyond.

Stable Convergence: A key characteristic of the multi-SSQW is its stable convergence - a critical requirement for a resilient financial simulator. This feature ensures that the quantum walks consistently attain a stable state over time. Our results demonstrate that multi-SSQW can produce more accurate simulations. For instance, when approximating the binomial and log-normal distributions, we found that the error could be effectively minimized by increasing the number of walkers.

Instantaneous Computation: Multi-SSQW achieves instantaneity by efficiently navigating the complex quantum state space. The concurrent evolution of multiple walkers within this space allows for rapid exploration and convergence to the desired state or solution. Quantum superposition and entanglement, core aspects of quantum computation, further amplify this capacity by facilitating parallel processing and exponential computational speed-ups relative to classical methods.

An essential aspect of the multi-SSQW is the convergence and instantaneity. Convergence denotes the behavior of the error function, whereby as iterations continue, the error values stabilize and approach a minimum. This ensures steady progress towards an optimal state. Instantaneity pertains to the speed at which the error function reaches its minimum, signifying the swift learning and adjustment capability of the model, a highly valuable feature in the fast-paced and volatile financial sphere.

Further, by appropriately tuning the number of walkers, steps, and coin operator parameters, multi-SSQW can be optimized for swift convergence, thereby enhancing its instantaneity. It’s important to note, however, that achieving instantaneity necessitates a deep understanding of system dynamics and careful selection and tuning of parameters, a potentially challenging task.

In conclusion, the advantages of multi-SSQW, such as its capacity for rapid modeling and prediction, make it highly beneficial for financial simulations in the ever-evolving financial markets.

5 ACKNOWLEDGMENTS

We thank IBM Quantum Hub at NTU for providing computational resources and accesses for conducting the real quantum device experiments. We acknowledges support from National Science and technology council, Taiwan under Grants MOST111-2119-M-033-001, by the research project Applications of quantum computing in optimization and finances.

References

- [1] P.W. Shor, " Algorithms for quantum computation: discrete logarithms and factoring" Proceedings 35th Annual Symposium on Foundations of Computer Science, Santa Fe, NM, USA, 124-134 (1994).

- [2] R.P. Feynman, " Simulating physics with computers " International Journal of Theoretical Physics, 21 , 467-488 (1982).

- [3] A. Trabesinger, " Quantum simulation " Nature Phys, 8 , 263 (2012).

- [4] Louis Bachelier, Mark Davis, Alison Etheridge, "Louis Bachelier’s Theory of Speculation: The Origins of Modern Finance" Princeton: Princeton University Press, (2007)

- [5] Eugene F.Fama, " Quantum amplitude amplification and estimation “Efficient Capital Markets: A Review of Theory and Empirical Work.” The Journal of Finance, 252, 383–417 (1970).

- [6] Daniel J. Egger, Claudio Gambella, Jakub Marecek, et al., " Quantum Computing for Finance: State-of-the-Art and Future Prospects " IEEE Transactions on Quantum Engineering, 1 , 1-24 (2020).

- [7] Dylan Herman, Cody Googin, Xiaoyuan Liu, et al., " A Survey of Quantum Computing for Finance " arXiv, (2022).

- [8] Gilles Brassard and Peter Høyer and Michele Mosca and Alain Tapp, " Quantum amplitude amplification and estimation " American Mathematical Society, 305, 53-74 (2002).

- [9] Patrick Rebentrost, Brajesh Guptand Thomas R. Bromley, " Quantum computational finance: Monte Carlo pricing of financial derivatives" Phys. Rev. A, 98, 022321 (2018).

- [10] C. Zoufal, A. Lucchi and S. Woerner, " Quantum Generative Adversarial Networks for learning and loading random distributions" npj Quantum Inf, 5,103 (2019).

- [11] Hao Tang, Anurag Pal, Lu-Feng Qiao, et al., "Quantum Computation for Pricing the Collateralized Debt Obligations" arXiv:2008.04110 (2020)

- [12] Guanglei Xu, Andrew J. Daley, Peyman Givi and Rolando D. Somma, "Turbulent mixing simulation via a quantum algorithm" AIAA Journal, 56,5 687-699(2018)

- [13] Nikitas Stamatopoulos and Daniel J. Egger and Yue Sun and Christa Zoufal and Raban Iten and Ning Shen and Stefan Woerner, "Option Pricing using Quantum Computers" Quantum, 4 291(2020)

- [14] Nikitas Stamatopoulos, Guglielmo Mazzola, Stefan Woerner and William J. Zeng. "Towards Quantum Advantage in Financial Market Risk using Quantum Gradient Algorithms."Quantum, 6, 770 (2022).

- [15] Dong An, Noah Linden, JinPing Liu, Ashley Montanaro, Changpeng Shao, and Jiasu Wang "Quantum-accelerated multilevel Monte Carlo methods for stochastic differential equations in mathematical finance." Quantum,5, 481 (2021).

- [16] Shouvanik Chakrabarti, Rajiv Krishnakumar, Guglielmo Mazzola, Nikitas Stamatopoulos, Stefan Woerner, and William J. Zeng. "A Threshold for Quantum Advantage in Derivative Pricing." Quantum 5, 463 (2021).

- [17] A. W. Harrow,A. Hassidim and S. Lloyd, " Quantum algorithm for linear systems of equations " Phys. Rev. Lett, 103 , 150502 (2009).

- [18] S. Lloyd,M. Mohseni and P. Rebentrost, " Quantum principal component analysis " Nature Phys, 10 , 631-633 (2014).

- [19] V. Havlíček,A.D. Córcoles, K. Temme, et al., " Supervised learning with quantum-enhanced feature spaces " Nature, 567 , 209-212 (2019).

- [20] Chien-Hung Cho, Chih-Yu CHen, Kuo-Chin Chein, et al., " Quantum computation: Algorithms and Applications " Chinese Journal of Physics, 72 , 248-269 (2021).

- [21] A. Montanaro, " Quantum simulation " npj Quantum Information, 2 , 15023 (2021).

- [22] Yuval R. Sanders, Guang Hao Low, Artur Scherer,and Dominic W. Berry, " Black-Box Quantum State Preparation without Arithmetic" Phys. Rev. Lett, 122, 020502 (2019).

- [23] J. Choi, A.L. Shaw, I.S. Madjarov et al., " Preparing random states and benchmarking with many-body quantum chaos" Nature 613, 468-473 (2023).

- [24] M. A. Nielsen, and I. L. Chuang, " Quantum Computation and Quantum Information" Cambridge University Press (2010).

- [25] Hubert de Guise, Olivia Di Matteo, and Luis L. Sánchez-Soto, " Simple factorization of unitary transformations"Phys. Rev. A97, 022328 (2018).

- [26] L. Grover and T. Rudolph, " Creating superpositions that correspond to efficiently integrable probability distributions" arXiv:quant-ph/0208112v1 (2002).

- [27] A. Rocchetto, E.Grant, S. Strelchuk, et al., " Learning hard quantum distributions with variational autoencoders." npj Quantum Inf 4, 28 (2018).

- [28] Kalyan Dasgupta and Binoy Paine, " Loading Probability Distributions in a Quantum circuit" arXiv:2208.13372v1(2022).

- [29] Araujo, I.F., Park, D.K., Petruccione, F. et al., " A divide-and-conquer algorithm for quantum state preparation" Sci Rep 11, 6329 (2021).

- [30] Xiao-Ming Zhang, Tongyang Li and Xiao Yuan, "Quantum State Preparation with Optimal Circuit Depth: Implementations and Applications" Phys. Rev. Lett. 129, 230504(2022).

- [31] Pei Yuan and Shengyu Zhang, " Optimal (controlled) quantum state preparation and improved unitary synthesis by quantum circuits with any number of ancillary qubits" Quantum 7, 956 (2023).

- [32] R.P. Feynman, " Quantum mechanical computers" Found Phys, 16, 507-531(1986).

- [33] Y. Aharonov,L. Davidovich, and N. Zagury, " Quantum random walks" Phys. Rev. A, 48, 1687-1690(1993).

- [34] Andrew M. Childs," Universal Computation by Quantum Walk" Phys. Rev. Lett., 102, 180501(2009).

- [35] A. Mallick, C. Chandrashekar," Dirac Cellular Automaton from Split-step Quantum Walk" Sci Rep, 6, 25779(2016).

- [36] Parth Rajauria, Prateek Chawla and C. M. Chandrashekar," Estimation of one-dimensional discrete-time quantum walk parameters by using machine learning algorithms" arXiv:2007.04572 (2020).

- [37] Ellinor Wanzambi and Stina Andersson ," Quantum Computing: Implementing Hitting Time for Coined Quantum Walks on Regular Graphs" arXiv:2108.02723(2021).

- [38] Salvador Elías Venegas-Andraca, "Quantum walks: a comprehensive review" Quantum Information Processing, 11, 1015-1106 (2012)

- [39] Andrew M. Childs, Richard Cleve, Enrico Deotto, et al., "Exponential Algorithmic Speedup by a Quantum Walk" Association for Computing Machinery, 10, 59-68 (2003)

- [40] Andrew M. Childs and Jeffrey Goldstone, "Spatial search by quantum walk" Phys. Rev. A, 70,022314(2004)

- [41] A. R.Oxenfeldt, "A Decision-Making Structure for Price Decisions." Journal of Marketing, 37(1),48-51 (1973)

- [42] Bouteska Ahmed, "Understanding the impact of investor sentiment on the price formation process: A review of the conduct of American stock markets" The Journal of Economic Asymmetries, 22,e00172 (2020)

- [43] Y. Matsuzawa, "An index theorem for split-step quantum walks." Quantum Information Processing, 19, 227 (2020)

- [44] Akihiro Narimatsu, Hiromichi Ohno and Kazuyuki Wada, "Unitary equivalence classes of split-step quantum walks" arXiv:2104.13529 (2023)

- [45] Daniel W. Stroock, "Probability theory: an analytic view" Cambridge university press (2010)

- [46] Olav Kallenberg, "Foundations of modern probability" Springer-Verlag, New York (2002)

- [47] Fischer Black, Myron Scholes, "The Pricing of Options and Corporate Liabilities" Journal of Political Economy, 81 637–654(1973)