MARLIM: Multi-Agent Reinforcement Learning

for Inventory Management

Abstract

Maintaining a balance between the supply and demand of products by optimizing replenishment decisions is one of the most important challenges in the supply chain industry. This paper presents a novel reinforcement learning framework called MARLIM, to address the inventory management problem for a single-echelon multi-products supply chain with stochastic demands and lead-times. Within this context, controllers are developed through single or multiple agents in a cooperative setting. Numerical experiments on real data demonstrate the benefits of reinforcement learning methods over traditional baselines.

1 Introduction

Inventory control [49] is one of the major problems in the supply chain industry. The main goal is to ensure the right balance between the supply and demand of products by optimizing replenishment decisions. More precisely, a controller observes the past demands and local information of the inventory and has to decide about the next ordering values. Accurate inventory management is key to running a successful product business with benefits ranging from better inventory accuracy and insights to cost savings and avoidance of shortage and stock overflows.

The main issue of the supply chain is the environment uncertainty [64]. In an ideal world with deterministic demand and lead-times, an inventory controller would be able to place a perfect order equal to the demand size at the right time. However, in practice, both the demands and lead-times are stochastic with potentially high volatility, making the inventory management problem hard to solve. In most cases, the inventory controller may exceedingly or insufficiently order. The former case leads to paying unnecessary ordering and holding costs while the latter results in shortage costs which may jeopardize the company’s performance.

Classical methods for solving the inventory management problem rely on basic heuristics [63, 55] due to the complexity of the mathematical modeling of the inventory system. While these approaches are easy to implement, they are not able to capture the randomness of the demand and lead-times. Another way of solving the inventory management problem is dynamic programming [5]. Despite being efficient, this technique requires exact knowledge of the mathematical model of the inventory system, which becomes intractable for big companies with very large inventories. Inventory management models can quickly become too complex and time-consuming, leading to unworkable models [22]. To escape this curse of dimensionality, one may apply approximate dynamic programming [23, 17] which performs well in specific settings at the cost of strong assumptions and simplifications.

Since the environment uncertainty is the major problem of inventory control [12], reinforcement learning (RL) methods appear as a natural solution since they can model complex situations and generalize well in a data-driven manner. The reinforcement learning task [53] consists, for an autonomous agent (e.g., a robot), in learning the actions to be taken, from trials, in order to optimize a quantitative signal over time. Such paradigm has reached tremendous success in games [35, 48, 56], but the early applications of reinforcement learning to real-world tasks, e.g., robotics [29] or autonomous driving [37, 45] remain a challenge and an active field of research. Furthermore, most of the literature on inventory management systems is meant to be applied for companies which are specialized in the retail industry where (i) the items of the inventory are meant to be sold and (ii) item shortages may be addressed through back orders. However, many companies are interested in inventory management for factories and warehouses where the objective is to ensure the performance of a production line and avoid the drastic consequences of item shortages.

The main goal of this paper is to develop a novel reinforcement learning framework, called MARLIM, to address the inventory management problem for a single-echelon multi-products supply chain on a production line with stochastic demands and lead-times.

Related work. The stochastic inventory control problem is one of the most studied problems in inventory theory. It was initiated by the seminal works of [20] and [49] which presented the basic heuristics to solve the inventory management problem. The so-called (s,S) policy [63], which results from the economies of scale in procurement, is a widely used policy nowadays in practice. However such heuristic cannot capture the randomness of the demand and lead-times, making it difficult to apply to realistic use cases. Later on, several authors developed the theory of inventory management and one may refer to the books of [64, 40] and [32] for an in-depth coverage of the topic. The different state-of-the-art models for inventory management systems may be found in the recent survey of [12].

In the past few years, many comprehensive studies related to the integration of reinforcement learning techniques to the inventory management problem were presented, starting with the work of [21] which considered production and distribution functions of global supply chain with multiple stages assuming a single item. Later on, different variations were derived with a particular focus on a supply chain with two echelons [28, 31], multiple echelons [27, 30, 11, 52] or multiple retailers [25, 16]. In all these studies, reinforcement learning methods have been implemented to specify near-optimal ordering policies in the entire supply chain with different goals such as maximizing the profit (when considering retailers) or minimizing costs composed of either ordering and holding costs or holding and backorder costs but not all of them at the same time. Furthermore, all the mentioned studies are dealing with a simplified assumption of independent products with no interactions among them.

In order to handle multiple items and accurately model the inter-dependency between them, the proposed framework of this paper is based on the multi-agent reinforcement learning paradigm [36] where each item may be seen as a single agent. Such framework seems promising to improve the training efficiency as suggested by the recent survey of [61] and the two recent studies of multi-agent reinforcement learning applied to inventory management problems [2, 51]. In [2], the authors derive a reinforcement strategy for a grocery retailer with multiple items and fixed delivery times where the focus is on the items availability rather than their associated costs. Similarly the study of [51] deals with a multiple echelons supply chain with predefined lead times whose aim is to maximise product sales and minimise wastage of perishable products. Conversely, the developed method of this paper is focused on the reduction of operating costs on a production line with stochastic demands and lead-times for real-world applications.

The framework of MARLIM is also related to the joint replenishment problem, i.e., when one considers the interdependency among different groups of products in a same order provided by a single supplier [26, 57, 44]. The objective is to optimize a global replenishment cost composed of inventory ordering and holding costs [42, 58] but does not take into account the losses induced by item shortages. In contrast to these previous studies, the aim of the proposed method whose is not only to reduce the global replenishment cost but also to avoid stock-outs of items.

Contributions.

The main contributions of this paper may be summarized as follows.

• A novel reinforcement learning framework, called MARLIM, is developed to address the inventory management problem for a single-echelon multi-products supply chain on a production line with stochastic demands and lead-times.

• A methodology to train agents in different scenarios for fixed or shared capacity constraints with specific handling of storage overflows is provided.

• Various numerical experiments on real-world data demonstrate the benefits of the developed method over classical baselines.

Outline. Section 2 presents the mathematical background of reinforcement learning and Section 3 deals with the inventory management model. The methodology and details of the developed supply chain environment are described in Section 4. Numerical experiments are performed in Section 5 to highlight the relevance of the developed model on real-world data and Section 6 concludes the article with further discussion.

2 Preliminaries on Reinforcement Learning

Markovian setting. Markov Decision Processes (MDP) [41] are a formalization of sequential decision making, where actions influence not just immediate rewards, but also subsequent situations. Consider the classical framework of a MDP defined as a tuple comprised of a state space an action space a Markovian transition kernel where denotes the set of probability density functions over a reward function a discount factor and an initial-state distribution . The reinforcement learning problem consists of finding the best strategy or policy in order to maximize the performance. The criterion here is defined in terms of future rewards that can be expected and depend on the agent’s behavior. The solution of a MDP is an optimal policy that maximizes the value function in all the states over some policy set of interest : . Such optimal policy is guaranteed to exist thanks to the theorem of [6]. In practice, can be found through dynamic programming and Bellman equations [7, 9, 24] with different schemes, e.g., policy iteration [8, 10] or value iteration [39, 50]. Another way is to consider policy-gradient methods [60, 4] which use a parameterized policy with and update the policy parameter on each step in the direction of an estimate of the gradient of the performance with respect to the policy parameter.

Parametric policies. Given a parameter space , consider a class of smoothly parameterized stochastic policies that are twice differentiable w.r.t. , i.e., for which the gradient and the Hessian are defined everywhere and finite. When the action space is finite, a popular choice is to use Gibbs policies, a.k.a. softmax policies, for all and ,

| (1) |

where is an appropriate feature-extraction function, often computed using a neural network. When the action space is continuous , a popular choice is to use Gaussian policies so the policy can be defined as the normal probability density over a real-valued scalar action, with some parametric mean and standard deviation that depend on the state, for all and ,

| (2) |

Multi-Agent Reinforcement Learning (MARL). Originated from the seminal works of [47] and [34], Markov Games are the standard generalization of Markov Decision Processes as they capture the interaction of multiple agents. A Markov game is defined as a tuple where denotes the set of agents, is the state space observed by all agents, is the action space of agent . denotes the joint action space, is the transition kernel, is the immediate reward function of agent and is the discount factor. At time step , each agent selects an action based on the system state . The system then transitions to state according to and rewards each agent with . The goal of agent is to optimize its own long-term reward by finding the policy such that . Therefore, the marginal value function of agent becomes a function of the joint policy defined by Thus, the solution concept of a Markov game deviates from that of a MDP since the optimal performance of each agent is controlled not only by its own policy, but also the choices of all other players of the game. The most common solution concept for Markov games is Nash equilibrium [3, 18].

As a standard learning goal for MARL, Nash equilibrium always exists for finite-space infinite-horizon discounted Markov games [18], but may not be unique in general. Most of the multi-agent reinforcement learning algorithms are contrived to converge to such an equilibrium point, if it exists.

3 Inventory Management Model

Denote by the discrete product space where refers to the item in the inventory and is the total number of items. At each time step, the inventory controller decides about the order to take based on the current inventory level and the previous demands. This order arrives in the inventory after a stochastic lead-time. After receiving the replenishment quantity of different products, the demands are satisfied and the environment incurs inventory costs. The aim of this Section is to describe the complete inventory management model from the inventory features and inventory costs to the inventory dynamics of the system.

3.1 Inventory features

The different inventory features are the basis of the inventory management model as they model the state space and the dynamics of the underlying Markov game. The inventory level is the on-hand inventory at time , i.e., the quantity of products sitting on the shelf in the inventory. At each time step, the inventory controller receives a stochastic demand signal and can order a quantity of items. These quantities arrive in the inventory after some lead-time . The inventory replenishment quantity is the associated quantity of products which is on its way to the inventory, i.e., it is the quantity that will be added to the inventory level when the inventory check is done at the next time step.

| Symbol | Feature |

|---|---|

| maximum capacity of subspace | |

| inventory level of product at time | |

| order of product at time | |

| replenishment of product at time | |

| temporary level of product at time | |

| overflow weight of product at time | |

| stock overflow of subspace at time | |

| demand of product at time | |

| lead-time of product at time | |

| backlog of product at time | |

| Ordering cost of product | |

| Holding cost of product | |

| Shortage cost of product |

When receiving the replenishment quantity, the inventory levels are temporarily updated through and some storage overflow may happen. When this overflow event happens, denoted by , the replenishment quantities are scaled using weights to ensure that the total inventory level does not exceed the maximum storage capacity . Finally, the demands are satisfied and the controller updates the inventory levels . When demand exceeds the available inventory level for an item, it yields a shortage cost computed through a backlog level . When optimizing the decisions relative to the inventory, the controller must take into account the different inventory costs.

3.2 Inventory costs

The inventory costs may be classified into three categories [55]: ordering, holding and shortage.

(i) Ordering costs: in the case of an ordering setting, these costs include the functioning costs, reception and tests costs, the salaries of the personnel, information systems costs and customs costs. In the case of a production setting, these costs include the raw material costs, labor costs, fixed and variable overheads, e.g., rent of a factory or the energy consumption allocated for production.

(ii) Holding costs: these are associated with storing inventory that remains unused and may be divided into two categories: financial and functional costs. The former represent the financial interest of the money invested in procuring the stocked products. The latter include the rent and maintenance of the required space, insurance costs, equipment costs, inter-warehouses transportation and obsolescence costs.

(iii) Shortage costs: when demand exceeds the available inventory for an item. The related costs fall in one of the two following categories: lost sales costs and backlogging costs. When considering lost sales, the unsatisfied demands are completely lost whereas with backlogging costs, there is a penalty shortage cost. Note that in the case where the stock is internal, the inventory shortage will induce the stop of production of therefore all the consequent costs.

For any item , denote by and the unit ordering, holding and shortage costs respectively. The different features of the inventory management system are summarized in the Table above.

Remark 1

(Costs and priority) The different unit costs are the keystone to accurately model different behaviors among the items. Intuitively, items with high shortage cost correspond to critical items that should not run out-of-stock. On the contrary, items with high ordering cost should be ordered sparingly. In general, an optimal controller should consider some reward function which leverages these three factors to find the right balance between the different costs.

3.3 Inventory Dynamics

The different relations between the inventory features are the mainstay to model a Markov game. First of all, there is a capacity constraint on the storage space and several structures are to be considered. On the one hand, a natural assumption is to consider that each item has a maximum capacity . In practice, thanks to expert’s knowledge, an estimate of the mean demand of each item may be available so that the capacity of each product can be upper bounded. On the other hand, for economical reasons, the total storage space may be shared among all items. This model allows more flexibility as products can compete for storage space but it assumes that all items belong to a same category. A unified and more realistic setting is the following: the different products may be classified into different types and they only compete for storage space inside their category (see Remark 2). In other words, the product space can be decomposed into different clusters of products, i.e.,

Each product subspace has a maximum storage capacity . For the sake of clarity, all items are assumed to have the same volume (see Remark 3). At each time step , the available storage space of each product subspace should be non-negative, i.e., for all

| (3) |

The replenishment quantity depends on the previous orders and their associated lead-times. Indeed, the received quantity of product at time corresponds to all the previous orders made at time step such that the receiving time obtained by adding the associated lead-time matches the current time step , i.e., for ,

When receiving these replenishment quantities at time , the inventory levels are temporarily updated as and it may happen that the storage space of subspace overflows which translates into the following event

In virtue of Eq.(3), on it holds . This means that when the stock overflow happens in then the received replenishment quantities of products in exceed the available storage space of . In that case, the replenishment quantities are weighted to completely fill the available storage space, i.e., some overflow weights are chosen such that . In order to promote the replenishment of critical products (see Remark 4), the overflow weights are set to be proportional to the shortage cost of items. For all and ,

| (4) |

Since the quantities of products are non-negative integers, only the integer part of the weighted replenishment quantities are added to the current inventory levels . When the demands exceed the available on-hand inventory levels, a backlog is computed to monitor the unmet demands and measure the associated shortage costs.

For each item , the inventory level and backlog are updated as

where and denote the positive and negative parts respectively. The inventory dynamics is summarized in Figure LABEL:fig:inventory_dynamics above.

Remark 2

(Product clusters) In practice, the different items of a warehouse are naturally classified into several groups according to their storage conditions: size, weight and specific climatic conditions, e.g., temperature, pressure, humidity levels, ventilation and light.

Remark 3

(Storage capacity) In the case where the total storage space is shared among all items (), the capacity constraint is fulfilled as soon as where is the maximum capacity of the warehouse. To model different volumes of items, one can simply consider a vector of unit volumes where is the unit volume of product and ensures that for all . Similarly, when dealing with types of products, the capacity constraint of each subspace becomes for all .

Remark 4

(Storage overflow) Different options are available to address the storage overflow of a product subspace . If all items in have equal priority levels, one could think of a uniform split of the available storage space of the form . However, in practice, some items are more important than others and may even be critical for production. This is why, when the storage space overflows, the replenishment quantities should be weighted to favor the replenishment of products non only with low inventory levels but also the ones associated to large shortage costs (see Eq.(4))

4 MARL for Inventory Management

Recall that the goal of any MARL algorithm is to find a policy maximizing the expected discounted reward The goal of this Section is to derive the necessary formalism, namely the Markov games and associated rewards, in order to apply such MARL methods.

Markov games. The inventory management problem can be modeled as different Markov games. Consider a fixed product subspace with . At time step , the state of agent is comprised of: the inventory level , the replenishment quantity , the lead time and backlogs , i.e., . The action of each agent concerns the ordering quantity . The joint state space and action space are respectively given by and . The transition kernel is implicitly defined by all the inventory dynamics equations of Section 3.3.

Costs and rewards. According to Section 3.2, at each time step and for a given product subspace , each agent incurs some inventory costs given by the combination of ordering, holding and shortage costs. In other words, the overall inventory cost may be described as

where with are weighting coefficients that translate some expert’s knowledge about the desired strategy. This expression translates the trade-off between the different inventory costs. Hopefully, a trained agent will learn to order low quantities of products that are costly to stock and supply, while maintaining sufficient inventory levels to avoid stock-outs for critical products associated to large shortage costs. This is validated in the numerical experiments of Section 5.

The inventory costs of each agent are associated to the single reward defined as: . Observe that inside a product subspace , the agents are working in a cooperative setting in order to optimize the average reward corresponding to . This average reward model allows more heterogeneity among agents and facilitates the development of decentralized MARL algorithms [62, 15]. More subtly, the reward function is sometimes not sharable with others, as the preference may be private to each agent. Note that this setting finds broad applications in engineering systems as sensor networks [43], smart grid [14], intelligent transportation systems [1], and robotics [13].

5 Numerical Experiments

This Section is dedicated to numerical experiments on real data. Various scenarios regarding the capacity constraints of the warehouses are considered: (i) when the items in a product cluster have their own capacity constraints then it is enough to train a single RL agent and apply the resulting behavior to all the items in that cluster; (ii) when the items compete for storage space then one may apply some MARL algorithm to deal with the interdependency of items.

Stochastic Model. The demands and lead-times are assumed to be stochastic with stationary distributions. The lead-times follow geometric distributions and the demands follow a mixed law of Poisson process with zero plateaus. More precisely, for each item , the lead-time is given by with parameter and the demand distribution is given by

In other words, the demand process of item is with and .

Real data. The data comes from a company with warehouses in different countries. The data is used to find the model parameters of the stochastic distributions using some maximum likelihood estimators [19, 59, 38]. For a fixed item with historical data of demands and lead-times , the MLE estimators and are given by the empirical averages

For the case study, the total number of products is equal to with time steps equal to months. The history is ranging from to on different warehouses leading to a maximum number of historical data points equal to . The horizon is set to months and the methods are tested over replications (independent random seeds). The different parameter values of each item are summarized in Tables 8-12 in Appendix B.

Agents battle. In order to evaluate the performance of the developed approach, different baselines are implemented along with the reinforcement learning methods.

• MinMax agents: a standard min-max strategy from operation research. For these agents, each item has a safety stock , where is the c.d.f. of , represents the target service level and are the mean and variance of the demands and lead-times. The value of the service level is set to the classical value and the means and variances are computed using the MLE estimators. As soon as the inventory level goes below the safety stock, the controller orders the maximum capacity of the corresponding item. Note that such approach is easy to implement but may fail to anticipate spikes in the demand signal.

• Oracle agents: such agents implement the following heuristic: given the knowledge of the mean and variance of the demand signal, it is natural to order, at each timestep, according to a random law with mean and variance . More precisely, the oracle agents have access to the estimated mean and standard deviation of their associated products and order at each time according to a normal law which is clamped to fit the bounds of the action space.

• MARL agents: the reinforcement learning agents are trained using Proximal Policy Optimization (PPO) algorithms [46] which are stable and effective policy gradient methods. When working with capacity constraints per item, both discrete (Eq. (1)) and continuous (Eq.(2)) policies are considered, denoted by PPO-D and PPO-C respectively. When the items compete for storage space, IPPO [54] which is an independent version of PPO for multi-agent frameworks is implemented. The different parameter configurations are given in Appendix A.

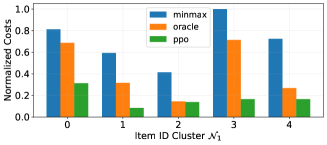

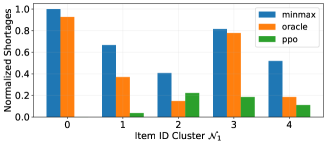

Results. In the idea that similar items among a cluster share some intrinsic features, the question of generalization for a single agent is raised. For that matter, first consider a scenario with a cluster of items with their own capacity constraints and a single RL agent trained on an average item, i.e., a ”virtual” item whose features are given by taking the mean of the features of all the items in that cluster is trained. Then the learned behavior on the items of the cluster is tested and the different cumulative costs are reported. Table 1 below presents the average cumulative costs in $ obtained over replications of the different methods for the items over an horizon of months.

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 0 | 48,554,986 | 10,183,088 | 4,863,202 | 4,616,016 |

| 1 | 52,993,931 | 16,917,389 | 6,865,991 | 6,385,378 |

| 2 | 70,467,282 | 21,426,806 | 8,727,215 | 8,087,258 |

| 3 | 72,220,832 | 12,722,887 | 9,854,047 | 5,280,345 |

| 4 | 79,235,272 | 16,976,630 | 8,801,628 | 4,808,191 |

| ID | 0 | 1 | 2 | 3 | 4 |

|---|---|---|---|---|---|

| MinMax | 39 | 41 | 42 | 51 | 49 |

| Oracle | 10 | 11 | 13 | 8 | 10 |

| PPO-D | 0 | 0 | 0 | 0 | 0 |

| PPO-C | 0 | 0 | 0 | 0 | 0 |

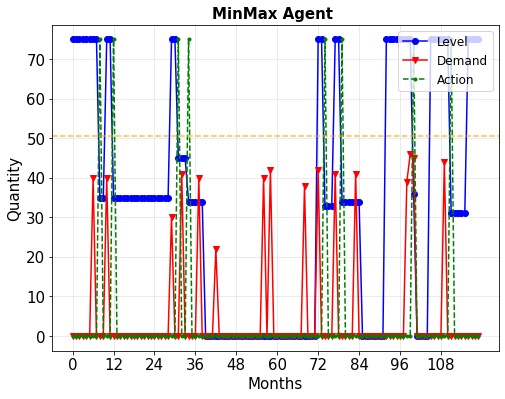

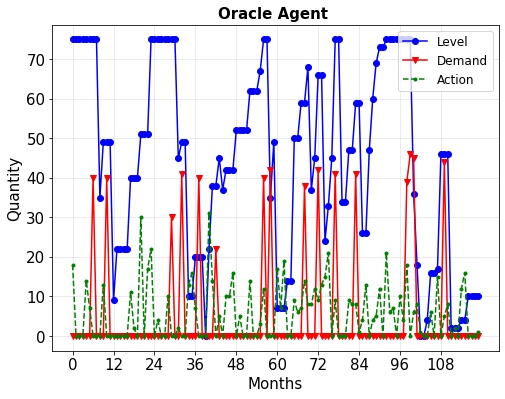

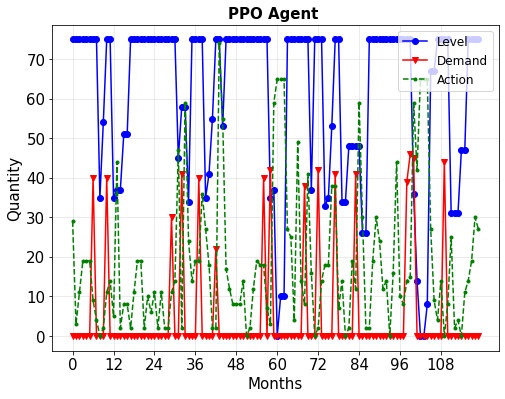

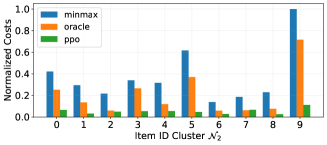

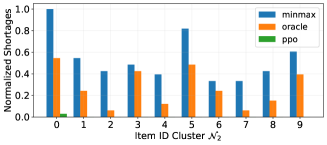

Regarding the average cumulative costs, the clear winners are the RL-based methods. Indeed, the PPO methods are statistically better than the two other baselines with a cost reduction factor ranging from (for item ID=1) to (for item ID=4) compared to the standard -strategy. Interestingly, among the PPO methods, the one with continuous actions presents the best performance. Another important result concerns the number of items shortages as shown by Table 2 above. Once again, the RL-based methods outperform the two standard baselines. Furthermore, the PPO agents learned an optimal strategy in terms of stock-outs since the number of item shortages is always equal to zero. Such careful behavior is confirmed by Figure 2 where the evolution of the inventory levels is plotted, over an horizon of months, for a particular item according to the different strategies. Note that compared to the MinMax and Oracle agents, the inventory levels of the PPO agent are always above the demand signal which ensure the avoidance of stock-outs. Interestingly, the RL agents have the nice following interpretation: whenever there is either a demand spike or a demand plateau for a long time, there is an incentive to order. Additional numerical results concerning all different items are available in Appendices C and D for the average cumulative costs and the average item shortages respectively.

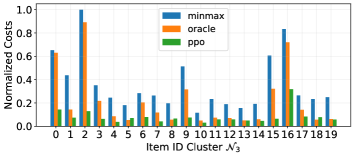

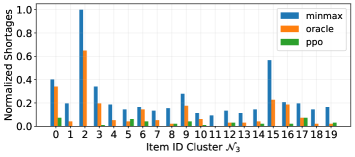

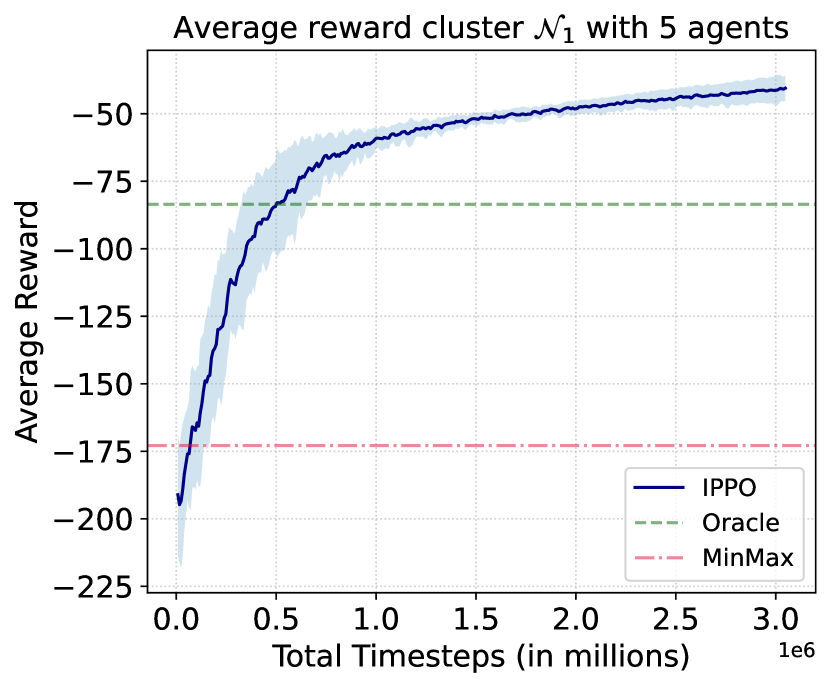

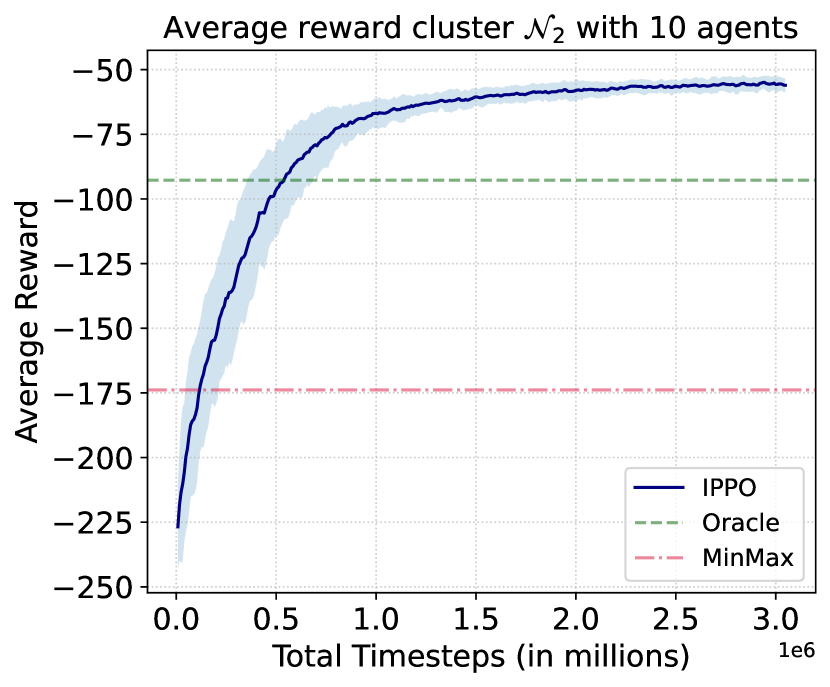

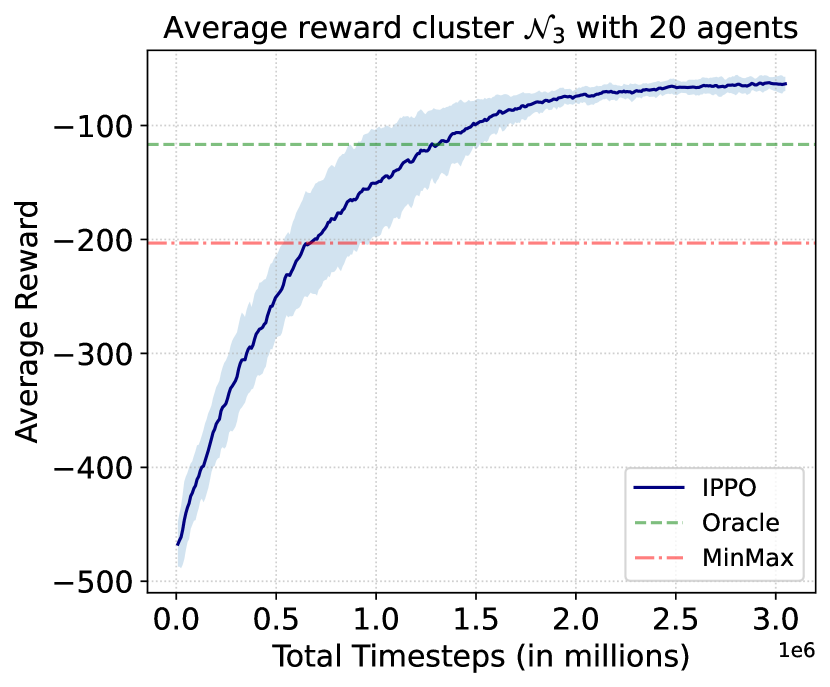

Another scenario involving storage capacity constraint is considered with three different clusters and composed of and items respectively. The last cluster represents a more complex task as it involves many agents. As before, the different methods based on the average cumulative cost over a cluster and the average item shortages over a cluster are compared, both over an horizon of months. For each cluster, one may take a look at the different training curves of the MARL agents. Such training is repeated on replications and the results are displayed in Figure 3 which gathers the evolution of the normalized average reward along the training episodes. The means and standard deviations of the average reward of the MARL agents are plotted in blue. For ease of comparison, two horizontal lines corresponding to the normalized average reward of the MinMax and Oracle agents are added. Thus, it allows to check the performance gain obtained with the RL-based methods compared to standard baselines. Observe that for clusters and , the MARL agents quickly outperform the baselines in approximately timesteps but need more than 1M timesteps on cluster to surpass the Oracle agents. Concerning the test performance of the learned behaviors, the different Tables below show the average cumulative cost and average stock-outs over the different items, obtained over replications and an horizon of months.

| Cluster | |||

|---|---|---|---|

| MinMax | 49,219,195 | 55,148,027 | 63,319,299 |

| Oracle | 29,596,024 | 31,047,144 | 38,002,027 |

| IPPO-C | 12,048,666 | 7,905,165 | 14,239,567 |

| Cluster | |||

|---|---|---|---|

| MinMax | 18 | 18 | 23 |

| Oracle | 13 | 9 | 11 |

| IPPO-C | 3 | 0 | 2 |

Once again, the MARL-based agents present the best performance, both in terms of cost savings (see Table 4) and avoidance of shortages (see Table 4). Observe that for cluster , the MARL agents allows an overall cost reduction of compared to the standard strategy, for cluster and about for cluster . For each cluster, the details about the average costs and shortages of all items are available in Appendix E.

6 Conclusion & Discussion

Maintaining the right balance between the supply and demand of products by optimizing replenishment decisions is one of the most important challenges for inventory management systems. In this paper, a rigorous methodological and practical reinforcement learning framework to address the inventory management problem for a single-echelon multi-products supply chain on a production line with stochastic demands and lead-times has been developed. The method has been illustrated with extensive numerical experiments on real data for both single and multi-agents algorithms.

This problem is very close to real-world use cases. Not only does it handle stochastic demands and lead-times but is designed for deployment as an actual business solution on production lines. Future work will focus on the statistical properties of the developed framework by further exploring links with mean-field approximation theory and the effects of exogenous variables in reinforcement learning.

Acknowledgements

The authors report financial support was provided by TotalEnergies SE. The authors have patent issued to TotalEnergies SE.

References

- Adler and Blue, [2002] Adler, J. L. and Blue, V. J. (2002). A cooperative multi-agent transportation management and route guidance system. Transportation Research Part C: Emerging Technologies, 10(5-6):433–454.

- Barat et al., [2019] Barat, S., Khadilkar, H., Meisheri, H., Kulkarni, V., Baniwal, V., Kumar, P., and Gajrani, M. (2019). Actor based simulation for closed loop control of supply chain using reinforcement learning. In Proceedings of the 18th international conference on autonomous agents and multiagent systems, pages 1802–1804.

- Başar and Olsder, [1998] Başar, T. and Olsder, G. J. (1998). Dynamic noncooperative game theory. SIAM.

- Baxter and Bartlett, [2001] Baxter, J. and Bartlett, P. L. (2001). Infinite-horizon policy-gradient estimation. Journal of Artificial Intelligence Research, 15:319–350.

- Bellman, [1966] Bellman, R. (1966). Dynamic programming. Science, 153(3731):34–37.

- Bellman and Dreyfus, [1959] Bellman, R. and Dreyfus, S. (1959). Functional approximations and dynamic programming. Mathematical Tables and Other Aids to Computation, pages 247–251.

- Bellman and Kalaba, [1957] Bellman, R. and Kalaba, R. (1957). Dynamic programming and statistical communication theory. Proceedings of the National Academy of Sciences of the United States of America, 43(8):749.

- Bertsekas, [2011] Bertsekas, D. P. (2011). Approximate policy iteration: A survey and some new methods. Journal of Control Theory and Applications, 9(3):310–335.

- Bertsekas and Tsitsiklis, [1996] Bertsekas, D. P. and Tsitsiklis, J. N. (1996). Neuro-dynamic programming, volume 5. Athena Scientific Belmont, MA.

- Buşoniu et al., [2012] Buşoniu, L., Lazaric, A., Ghavamzadeh, M., Munos, R., Babuška, R., and De Schutter, B. (2012). Least-squares methods for policy iteration. Reinforcement learning, pages 75–109.

- Chaharsooghi et al., [2008] Chaharsooghi, S. K., Heydari, J., and Zegordi, S. H. (2008). A reinforcement learning model for supply chain ordering management: An application to the beer game. Decision Support Systems, 45(4):949–959.

- Chaudhary et al., [2018] Chaudhary, V., Kulshrestha, R., and Routroy, S. (2018). State-of-the-art literature review on inventory models for perishable products. Journal of Advances in Management Research.

- Corke et al., [2005] Corke, P., Peterson, R., and Rus, D. (2005). Networked robots: Flying robot navigation using a sensor net. In Robotics research. The eleventh international symposium, pages 234–243. Springer.

- Dall’Anese et al., [2013] Dall’Anese, E., Zhu, H., and Giannakis, G. B. (2013). Distributed optimal power flow for smart microgrids. IEEE Transactions on Smart Grid, 4(3):1464–1475.

- Doan et al., [2019] Doan, T., Maguluri, S., and Romberg, J. (2019). Finite-time analysis of distributed td (0) with linear function approximation on multi-agent reinforcement learning. In International Conference on Machine Learning, pages 1626–1635. PMLR.

- Dogan and Güner, [2015] Dogan, I. and Güner, A. R. (2015). A reinforcement learning approach to competitive ordering and pricing problem. Expert Systems, 32(1):39–48.

- Fang et al., [2013] Fang, J., Zhao, L., Fransoo, J. C., and Van Woensel, T. (2013). Sourcing strategies in supply risk management: An approximate dynamic programming approach. Computers & Operations Research, 40(5):1371–1382.

- Filar and Vrieze, [2012] Filar, J. and Vrieze, K. (2012). Competitive Markov decision processes. Springer Science & Business Media.

- Fisher, [1922] Fisher, R. A. (1922). On the mathematical foundations of theoretical statistics. Philosophical Transactions of the Royal Society of London. Series A, Containing Papers of a Mathematical or Physical Character, 222(594-604):309–368.

- Fukuda, [1964] Fukuda, Y. (1964). Optimal policies for the inventory problem with negotiable leadtime. Management Science, 10(4):690–708.

- Giannoccaro and Pontrandolfo, [2002] Giannoccaro, I. and Pontrandolfo, P. (2002). Inventory management in supply chains: a reinforcement learning approach. International Journal of Production Economics, 78(2):153–161.

- Gijsbrechts et al., [2021] Gijsbrechts, J., Boute, R. N., Van Mieghem, J. A., and Zhang, D. (2021). Can deep reinforcement learning improve inventory management? performance on dual sourcing, lost sales and multi-echelon problems. Manufacturing & Service Operations Management.

- Halman et al., [2009] Halman, N., Klabjan, D., Mostagir, M., Orlin, J., and Simchi-Levi, D. (2009). A fully polynomial-time approximation scheme for single-item stochastic inventory control with discrete demand. Mathematics of Operations Research, 34(3):674–685.

- Howard, [1960] Howard, R. A. (1960). Dynamic programming and markov processes.

- Jiang and Sheng, [2009] Jiang, C. and Sheng, Z. (2009). Case-based reinforcement learning for dynamic inventory control in a multi-agent supply-chain system. Expert Systems with Applications, 36(3):6520–6526.

- Khouja and Goyal, [2008] Khouja, M. and Goyal, S. (2008). A review of the joint replenishment problem literature: 1989–2005. European Journal of Operational Research, 186(1):1–16.

- Kim et al., [2005] Kim, C., Jun, J., Baek, J., Smith, R., and Kim, Y.-D. (2005). Adaptive inventory control models for supply chain management. The International Journal of Advanced Manufacturing Technology, 26(9):1184–1192.

- Kim et al., [2008] Kim, C. O., Kwon, I.-H., and Baek, J.-G. (2008). Asynchronous action-reward learning for nonstationary serial supply chain inventory control. Applied Intelligence, 28(1):1–16.

- Kober et al., [2013] Kober, J., Bagnell, J. A., and Peters, J. (2013). Reinforcement learning in robotics: A survey. The International Journal of Robotics Research, 32(11):1238–1274.

- Kwak et al., [2009] Kwak, C., Choi, J. S., Kim, C. O., and Kwon, I.-H. (2009). Situation reactive approach to vendor managed inventory problem. Expert Systems with Applications, 36(5):9039–9045.

- Kwon et al., [2008] Kwon, I.-H., Kim, C. O., Jun, J., and Lee, J. H. (2008). Case-based myopic reinforcement learning for satisfying target service level in supply chain. Expert Systems with applications, 35(1-2):389–397.

- Levi et al., [2014] Levi, D. S., Chen, X., and Bramel, J. (2014). The logic of logistics: theory, algorithms, and applications for logistics management. Springer.

- Liang et al., [2018] Liang, E., Liaw, R., Nishihara, R., Moritz, P., Fox, R., Goldberg, K., Gonzalez, J., Jordan, M., and Stoica, I. (2018). Rllib: Abstractions for distributed reinforcement learning. In International Conference on Machine Learning, pages 3053–3062. PMLR.

- Littman, [1994] Littman, M. L. (1994). Markov games as a framework for multi-agent reinforcement learning. In Machine learning proceedings 1994, pages 157–163. Elsevier.

- Mnih et al., [2015] Mnih, V., Kavukcuoglu, K., Silver, D., Rusu, A. A., Veness, J., Bellemare, M. G., Graves, A., Riedmiller, M., Fidjeland, A. K., Ostrovski, G., et al. (2015). Human-level control through deep reinforcement learning. nature, 518(7540):529–533.

- Nguyen et al., [2020] Nguyen, T. T., Nguyen, N. D., and Nahavandi, S. (2020). Deep reinforcement learning for multiagent systems: A review of challenges, solutions, and applications. IEEE transactions on cybernetics, 50(9):3826–3839.

- Okuda et al., [2014] Okuda, R., Kajiwara, Y., and Terashima, K. (2014). A survey of technical trend of adas and autonomous driving. In Technical Papers of 2014 International Symposium on VLSI Design, Automation and Test, pages 1–4. IEEE.

- Owen, [2001] Owen, A. B. (2001). Empirical likelihood. Chapman and Hall/CRC.

- Pineau et al., [2003] Pineau, J., Gordon, G., Thrun, S., et al. (2003). Point-based value iteration: An anytime algorithm for pomdps. In IJCAI, volume 3, pages 1025–1032. Citeseer.

- Porteus, [2002] Porteus, E. L. (2002). Foundations of stochastic inventory theory. Stanford University Press.

- Puterman, [1994] Puterman, M. L. (1994). Markov decision processes: discrete stochastic dynamic programming. John Wiley & Sons.

- Qu et al., [2015] Qu, H., Wang, L., and Liu, R. (2015). A contrastive study of the stochastic location-inventory problem with joint replenishment and independent replenishment. Expert Systems with Applications, 42(4):2061–2072.

- Rabbat and Nowak, [2004] Rabbat, M. and Nowak, R. (2004). Distributed optimization in sensor networks. In Proceedings of the 3rd international symposium on Information processing in sensor networks, pages 20–27.

- Salameh et al., [2014] Salameh, M. K., Yassine, A. A., Maddah, B., and Ghaddar, L. (2014). Joint replenishment model with substitution. Applied Mathematical Modelling, 38(14):3662–3671.

- Sallab et al., [2017] Sallab, A. E., Abdou, M., Perot, E., and Yogamani, S. (2017). Deep reinforcement learning framework for autonomous driving. Electronic Imaging, 2017(19):70–76.

- Schulman et al., [2017] Schulman, J., Wolski, F., Dhariwal, P., Radford, A., and Klimov, O. (2017). Proximal policy optimization algorithms. arXiv preprint arXiv:1707.06347.

- Shapley, [1953] Shapley, L. S. (1953). Stochastic games. Proceedings of the national academy of sciences, 39(10):1095–1100.

- Silver et al., [2018] Silver, D., Hubert, T., Schrittwieser, J., Antonoglou, I., Lai, M., Guez, A., Lanctot, M., Sifre, L., Kumaran, D., Graepel, T., et al. (2018). A general reinforcement learning algorithm that masters chess, shogi, and go through self-play. Science, 362(6419):1140–1144.

- Silver and Peterson, [1985] Silver, E. A. and Peterson, R. (1985). Decision systems for inventory management and production planning, volume 18. Wiley.

- Sondik, [1971] Sondik, E. J. (1971). The optimal control of partially observable markov processes. Technical report, Stanford Univ Calif Stanford Electronics Labs.

- Sultana et al., [2020] Sultana, N. N., Meisheri, H., Baniwal, V., Nath, S., Ravindran, B., and Khadilkar, H. (2020). Reinforcement learning for multi-product multi-node inventory management in supply chains. arXiv preprint arXiv:2006.04037.

- Sun and Zhao, [2012] Sun, R. and Zhao, G. (2012). Analyses about efficiency of reinforcement learning to supply chain ordering management. In IEEE 10th International Conference on Industrial Informatics, pages 124–127. IEEE.

- Sutton and Barto, [2018] Sutton, R. S. and Barto, A. G. (2018). Reinforcement learning: An introduction. MIT press.

- Tan, [1993] Tan, M. (1993). Multi-agent reinforcement learning: Independent vs. cooperative agents. In Proceedings of the tenth international conference on machine learning, pages 330–337.

- Toomey, [2000] Toomey, J. W. (2000). Inventory management: principles, concepts and techniques, volume 12. Springer Science & Business Media.

- Vinyals et al., [2019] Vinyals, O., Babuschkin, I., Czarnecki, W. M., Mathieu, M., Dudzik, A., Chung, J., Choi, D. H., Powell, R., Ewalds, T., Georgiev, P., et al. (2019). Grandmaster level in starcraft ii using multi-agent reinforcement learning. Nature, 575(7782):350–354.

- Wang et al., [2012] Wang, L., He, J., and Zeng, Y.-R. (2012). A differential evolution algorithm for joint replenishment problem using direct grouping and its application. Expert Systems, 29(5):429–441.

- Wang et al., [2015] Wang, L., Shi, Y., and Liu, S. (2015). An improved fruit fly optimization algorithm and its application to joint replenishment problems. Expert systems with Applications, 42(9):4310–4323.

- White, [1982] White, H. (1982). Maximum likelihood estimation of misspecified models. Econometrica: Journal of the econometric society, pages 1–25.

- Williams, [1992] Williams, R. J. (1992). Simple statistical gradient-following algorithms for connectionist reinforcement learning. Machine learning, 8(3):229–256.

- Zhang et al., [2021] Zhang, K., Yang, Z., and Başar, T. (2021). Multi-agent reinforcement learning: A selective overview of theories and algorithms. Handbook of Reinforcement Learning and Control, pages 321–384.

- Zhang et al., [2018] Zhang, K., Yang, Z., Liu, H., Zhang, T., and Basar, T. (2018). Fully decentralized multi-agent reinforcement learning with networked agents. In International Conference on Machine Learning, pages 5872–5881. PMLR.

- Zheng and Federgruen, [1991] Zheng, Y.-S. and Federgruen, A. (1991). Finding optimal (s, s) policies is about as simple as evaluating a single policy. Operations research, 39(4):654–665.

- Zipkin, [2000] Zipkin, P. H. (2000). Foundations of inventory management.

Appendix

Appendix A collects the technical details related to the implementation of Proximal Policy Optimization algorithms, namely the different loss functions and the associated hyper-parameters used for the training phase. Appendix B gathers the different item parameters of the real data. Appendices C and D present additional results concerning the cumulative costs and item shortages for single agents. Similarly, Appendix E is dedicated to the detailed numerical results of MARL based methods.

Appendix A Proximal Policy Optimization algorithms

A.1 PPO methodology and model

PPO is a model-free on-policy RL algorithm that works well for both discrete and continuous action space environments. PPO utilizes an actor-critic framework, where there are two networks, an actor (policy network) and critic network (value function). Such algorithms are part of the family of policy gradient algorithms which use a parameterized action-selection policy with and update the policy parameter on each step in the direction of an estimate of the gradient of the performance with respect to the policy parameter:

where is the learning rate, is a gradient estimate, is an estimator of the advantage function at timestep and the expectation indicates the empirical average over a finite batch of samples, in an algorithm that alternates between sampling and optimization.

The implementation of the Proximal Policy Optimization algorithms follows the one of the open-source library RLlib [33]. Whereas standard policy gradient methods perform one gradient update per data sample, PPO enables multiple epochs of minibatch updates. According to [46], compared to TRPO methods, PPO algorithms are much simpler to implement, more general, and have better sample complexity (empirically). PPO’s clipped objective supports multiple SGD passes over the same batch of experiences and RLlib’s PPO can scale out using multiple workers for experience collection, and also with multiple GPUs for SGD.

Denote by the probability ratio between old and new policies so that TRPO methods aim at optimizing the following surrogate objective: . In comparison, PPO methods rely on the following clipped objective function:

The motivation for this objective is as follows. The second term inside the min modifies the surrogate objective by clipping the probability ratio, which removes the incentive for moving outside of the interval . By taking the minimum of the clipped and unclipped objective, the final objective is a lower bound (i.e., a pessimistic bound) on the unclipped objective. With this scheme, PPO methods only ignore the change in probability ratio when it would make the objective improve, and include it when it makes the objective worse. This very idea of clipping can also be applied to the critic whose aim is to approximate the value function using some neural network, leading to the following critic loss

Furthermore, in addition to clipped surrogate objective, consider some KL divergence and entropy terms. For the KL term, this follows from the fact that a certain surrogate objective (which computes the max KL over states instead of the mean) forms a lower bound (i.e., a pessimistic bound) on the performance of the current policy. Finally, the total objective can be augmented by adding an entropy bonus to ensure sufficient exploration, as suggested in past work [35]. Overall, the goal is to maximize the following objective function

where is the policy loss, is the critic loss, is the Kullback-Liebler divergence and is the entropy bonus. The constants and are the value-function loss coefficient, the KL coefficient and the entropy coefficient.

A.2 Implementation Details

When working with storage constraints per item, it is enough to only train a few agents. The items of the different warehouses are split in groups according to the median of lead-time in order to train only average RL agent. Such agents are then tested on all the items in the corresponding group. In order to compare the effect of working with discrete or continuous actions spaces, two RL agents are trained using Discrete actions (PPO-D1 and PPO-D2), and 2 RL agents using Continuous actions (PPO-C1 and PPO-C2). When working with items competing for storage space, MARL algorithms are used, suchg as IPPO and other variations with shared critic. Tables 5 and 6 gather all the details about the different hyper parameters used for the traning of (MA)RL agents. In all the experiments, the following parameters are fixed:

| Parameter | Value |

|---|---|

| HORIZON | 200 |

| GAMMA | 0.99 |

| LEARNING RATE | 1e-4 |

| VF SHARE LAYERS | False |

| ROLLOUT FRAGMENTLENGTH | 200 |

| BATCHMODE | complete |

| TRAIN BATCH SIZE | 8000 |

| SGD MINIBACTH SIZE | 250 |

| NUM SGD ITER | 20 |

| NORMALIZE ACTIONS | True |

| FCNET ACTIVATION | relu |

| USE CRITIC | True |

| GAE LAMBDA | 1 |

| KL COEFF | 2e-1 |

| KL TARGET | 1e-2 |

| ENTROPY COEFF | 0.01 |

| CLIP PARAM | 0.3 |

The following parameters are specific to the different RL agents:

| Parameter | PPO-D1 | PPO-D2 | PPO-C1 | PPO-D2 |

|---|---|---|---|---|

| FCNET HIDDEN | [512, 512] | [512, 512] | [512, 512] | [512, 512] |

| GRAD CLIP | 40 | 40 | 40 | 40 |

| LEARNING RATE | 1e-4 | 1e-4 | 1e-4 | 2e-4 |

| VF SHARE LAYERS | False | False | False | False |

| USE GAE | True | True | True | True |

| VF CLIP PARAM | 1e3 | 1e4 | 1e3 | 5e2 |

| VF LOSS COEFF | 1 | 1e-2 | 1e-2 | 1e-2 |

| Parameter | IPPO- | IPPO- | IPPO- |

|---|---|---|---|

| FCNET HIDDEN | [512, 256] | [512,256] | [512,256] |

| GRAD CLIP | 40 | 20 | 20 |

| LEARNING RATE | 5e-5 | 2e-5 | 2e-5 |

| VF SHARE LAYERS | True | True | True |

| USE GAE | False | False | False |

| VF CLIP PARAM | 5e2 | 5e2 | 5e2 |

| VF LOSS COEFF | 1e-3 | 1e-4 | 1e-4 |

Appendix B Item Hyperparameters

The data is used to find the model parameters of the stochastic distributions using some MLE estimators. For a fixed item with historical data of demands and lead-times , the MLE estimators and are given by the empirical averages

The different Tables below summarize the parameter values for each item.

| ID | ||||||

|---|---|---|---|---|---|---|

| 0 | 0.33 | 6.23 | 0.12 | 1,010 | 57 | 11,097 |

| 1 | 0.12 | 17.33 | 0.17 | 1,092 | 125 | 11,800 |

| 2 | 0.21 | 11.0 | 0.17 | 1,363 | 159 | 14,887 |

| 3 | 0.24 | 9.04 | 0.11 | 1,125 | 131 | 12,881 |

| 4 | 0.17 | 12.0 | 0.11 | 1,007 | 119 | 14,758 |

| 5 | 0.31 | 6.87 | 0.11 | 1,174 | 65 | 15,954 |

| 6 | 0.17 | 12.5 | 0.12 | 1,280 | 104 | 18,109 |

| 7 | 0.12 | 17.25 | 0.12 | 1,220 | 71 | 14,450 |

| 8 | 0.18 | 11.82 | 0.19 | 2,250 | 269 | 23,984 |

| 9 | 0.29 | 8.46 | 0.13 | 1,356 | 129 | 13,998 |

| ID | ||||||

|---|---|---|---|---|---|---|

| 10 | 0.29 | 8.08 | 0.15 | 1,597 | 170 | 21,512 |

| 11 | 0.11 | 22.0 | 0.14 | 1,069 | 100 | 14,184 |

| 12 | 0.4 | 8.25 | 0.2 | 1,020 | 112 | 15,244 |

| 13 | 0.17 | 16.25 | 0.15 | 1,342 | 149 | 14,059 |

| 14 | 0.15 | 20.59 | 0.12 | 1,080 | 112 | 11,352 |

| 15 | 0.08 | 24.0 | 0.41 | 3,380 | 298 | 37,941 |

| 16 | 0.24 | 9.83 | 0.1 | 1,857 | 194 | 23,874 |

| 17 | 0.12 | 26.67 | 0.14 | 1,042 | 107 | 11,000 |

| 18 | 0.12 | 20.0 | 0.1 | 1,360 | 174 | 17,718 |

| 19 | 0.4 | 7.07 | 0.12 | 1,690 | 215 | 20,403 |

| ID | ||||||

|---|---|---|---|---|---|---|

| 20 | 0.08 | 40.0 | 0.15 | 1,110 | 95 | 12,873 |

| 21 | 0.38 | 9.5 | 0.12 | 1,270 | 181 | 13,578 |

| 22 | 0.08 | 32.67 | 0.1 | 1,276 | 184 | 16,441 |

| 23 | 0.17 | 23.58 | 0.2 | 1,170 | 60 | 15,026 |

| 24 | 0.14 | 20.4 | 0.11 | 2,084 | 270 | 25,725 |

| 25 | 0.08 | 40.0 | 0.12 | 1,371 | 177 | 14,804 |

| 26 | 0.11 | 32.5 | 0.09 | 1,092 | 152 | 12,305 |

| 27 | 0.08 | 32.0 | 0.11 | 2,104 | 135 | 24,015 |

| 28 | 0.11 | 36.5 | 0.15 | 1,252 | 139 | 14,186 |

| 29 | 0.39 | 7.81 | 0.1 | 1,792 | 93 | 25,279 |

| ID | ||||||

|---|---|---|---|---|---|---|

| 30 | 0.28 | 15.25 | 0.1 | 1,085 | 77 | 14,038 |

| 31 | 0.08 | 40.0 | 0.08 | 1,445 | 164 | 14,742 |

| 32 | 0.19 | 18.3 | 0.11 | 2,284 | 304 | 23,957 |

| 33 | 0.26 | 19.73 | 0.16 | 1,142 | 138 | 13,926 |

| 34 | 0.17 | 26.0 | 0.15 | 1,342 | 196 | 16,559 |

| 35 | 0.33 | 10.39 | 0.07 | 1,851 | 267 | 19,626 |

| 36 | 0.14 | 26.0 | 0.15 | 1,765 | 225 | 25,052 |

| 37 | 0.1 | 35.67 | 0.11 | 2,070 | 130 | 20,910 |

| 38 | 0.12 | 30.17 | 0.09 | 1,380 | 204 | 20,550 |

| 39 | 0.33 | 6.58 | 0.06 | 4,470 | 456 | 51,326 |

| ID | ||||||

|---|---|---|---|---|---|---|

| 40 | 0.29 | 18.14 | 0.17 | 1,689 | 158 | 22,534 |

| 41 | 0.08 | 50.0 | 0.1 | 1,329 | 141 | 17,654 |

| 42 | 0.22 | 20.77 | 0.13 | 2,312 | 257 | 29,177 |

| 43 | 0.44 | 14.33 | 0.1 | 1,308 | 100 | 15,170 |

| 44 | 0.08 | 70.0 | 0.1 | 1,308 | 179 | 13,718 |

| 45 | 0.17 | 34.0 | 0.18 | 3,590 | 328 | 38,035 |

| 46 | 0.08 | 108.0 | 0.12 | 1,011 | 87 | 10,134 |

| 47 | 0.19 | 111.0 | 0.12 | 1,049 | 100 | 15,621 |

| 48 | 0.18 | 97.88 | 0.11 | 1,851 | 171 | 20,451 |

| 49 | 0.08 | 217.0 | 0.11 | 1,851 | 114 | 25,362 |

Appendix C Average Cumulative Costs

C.1 Numerical Results

The different Tables below present the full results of cumulative costs for the numerical experiments with storage space constraints per item. The items are split in groups according to the median of lead-time in order to train only average RL agent. Such agents are then tested on all the items in the corresponding group.

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 0 | 48,554,986 | 10,183,088 | 4,863,202 | 4,616,016 |

| 1 | 52,993,931 | 16,917,389 | 6,865,991 | 6,385,378 |

| 2 | 70,467,282 | 21,426,806 | 8,727,215 | 8,087,258 |

| 3 | 72,220,832 | 12,722,887 | 9,854,047 | 5,280,345 |

| 4 | 79,235,272 | 16,976,630 | 8,801,628 | 4,808,191 |

| 5 | 79,945,152 | 17,793,765 | 9,068,217 | 4,270,027 |

| 6 | 94,856,066 | 23,070,095 | 6,725,252 | 6,330,215 |

| 7 | 94,888,885 | 23,194,601 | 9,540,166 | 4,599,449 |

| 8 | 96,678,620 | 30,082,381 | 15,010,899 | 13,646,991 |

| 9 | 98,917,563 | 15,738,319 | 7,593,699 | 7,229,608 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 10 | 110,582,575 | 24,999,881 | 9,564,232 | 9,038,083 |

| 11 | 112,399,072 | 42,910,634 | 7,574,747 | 6,628,323 |

| 12 | 115,603,447 | 46,823,147 | 6,853,628 | 6,103,570 |

| 13 | 124,832,231 | 39,888,919 | 8,243,508 | 7,665,907 |

| 14 | 152,157,505 | 47,941,527 | 6,445,518 | 6,418,000 |

| 15 | 156,482,922 | 64,905,614 | 26,221,197 | 18,708,044 |

| 16 | 162,805,503 | 32,745,666 | 15,653,937 | 8,462,765 |

| 17 | 165,864,536 | 74,037,166 | 10,165,442 | 9,631,728 |

| 18 | 167,274,515 | 46,875,740 | 12,546,177 | 7,122,270 |

| 19 | 174,895,434 | 56,821,488 | 10,050,155 | 9,706,447 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 20 | 182,267,502 | 130,132,350 | 33,743,915 | 36,077,127 |

| 21 | 188,855,483 | 66,602,602 | 8,227,594 | 7,704,383 |

| 22 | 209,851,096 | 101,916,137 | 18,964,499 | 19,156,603 |

| 23 | 240,876,429 | 119,152,696 | 10,058,032 | 9,181,690 |

| 24 | 253,729,788 | 94,653,074 | 18,857,686 | 14,191,791 |

| 25 | 259,717,238 | 154,572,208 | 39,887,428 | 41,316,087 |

| 26 | 275,654,944 | 136,723,841 | 21,806,460 | 28,917,117 |

| 27 | 294,354,320 | 13,3290,131 | 25,792,146 | 22,497,325 |

| 28 | 297,756,076 | 195,971,759 | 34,602,990 | 39,975,903 |

| 29 | 317,748,541 | 78,399,969 | 13,360,829 | 6,625,366 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 30 | 340,850,617 | 118,356,448 | 8,428,058 | 5,674,420 |

| 31 | 346,677,835 | 165,513,863 | 38,211,495 | 50,257,711 |

| 32 | 372,022,376 | 140,849,611 | 20,580,162 | 13,426,053 |

| 33 | 379,189,787 | 176,014,600 | 17,857,314 | 12,033,561 |

| 34 | 379,417,845 | 187,467,258 | 20,350,345 | 18,721,088 |

| 35 | 429,201,653 | 125,815,263 | 15,920,620 | 10,148,258 |

| 36 | 450,249,676 | 197,138,780 | 20,805,554 | 21,535,008 |

| 37 | 467,942,296 | 221,381,388 | 40,233,046 | 51,880,344 |

| 38 | 517,401,650 | 217,431,556 | 25,188,489 | 35,934,573 |

| 39 | 529,054,715 | 113,253,016 | 35,899,378 | 19,663,470 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 40 | 548,632,612 | 274,992,151 | 19,614,638 | 14,265,377 |

| 41 | 614,478,713 | 351,832,711 | 91,357,970 | 158,742,424 |

| 42 | 802,247,508 | 318,672,823 | 28,692,777 | 22,605,438 |

| 43 | 826,810,789 | 277,103,747 | 13,143,955 | 18,262,774 |

| 44 | 897,278,509 | 593,855,529 | 278,916,815 | 434,302,595 |

| 45 | 1205,603,289 | 856,462,764 | 193,219,445 | 184,847,412 |

| 46 | 1463,640,790 | 1196,188,961 | 1013,385,300 | 1137,694,029 |

| 47 | 7013,730,126 | 5018,246,734 | 4692,465,941 | 5153,720,918 |

| 48 | 7033,366,188 | 4830,858,675 | 4348,154,722 | 4928,213,014 |

| 49 | 10354,442,106 | 9275,492,362 | 9137,883,131 | 9309,276,387 |

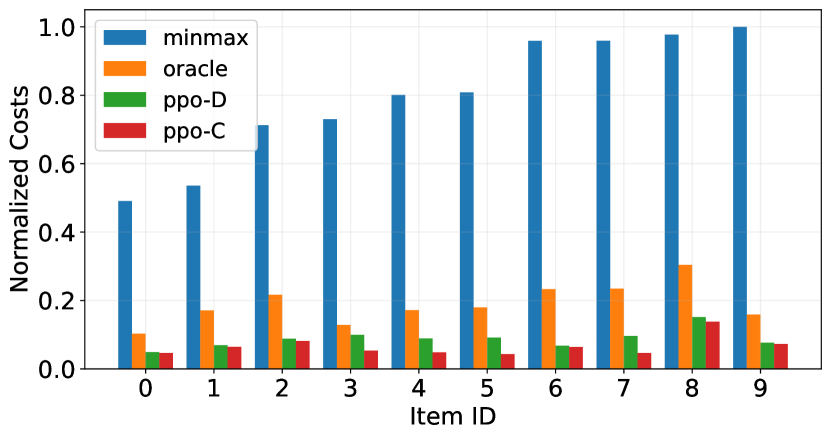

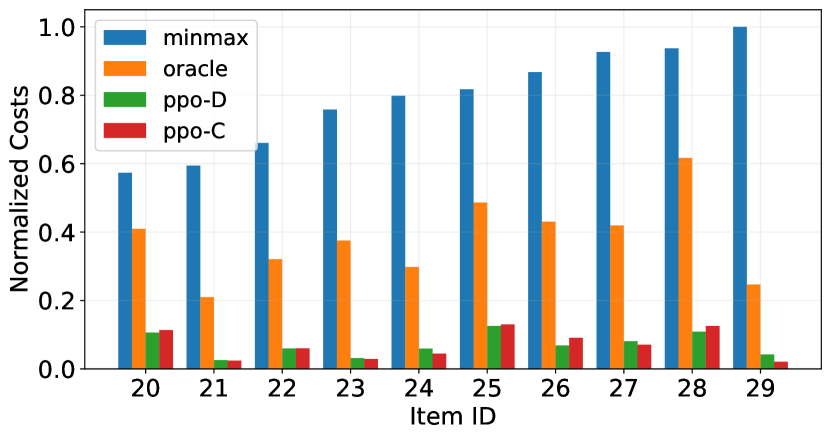

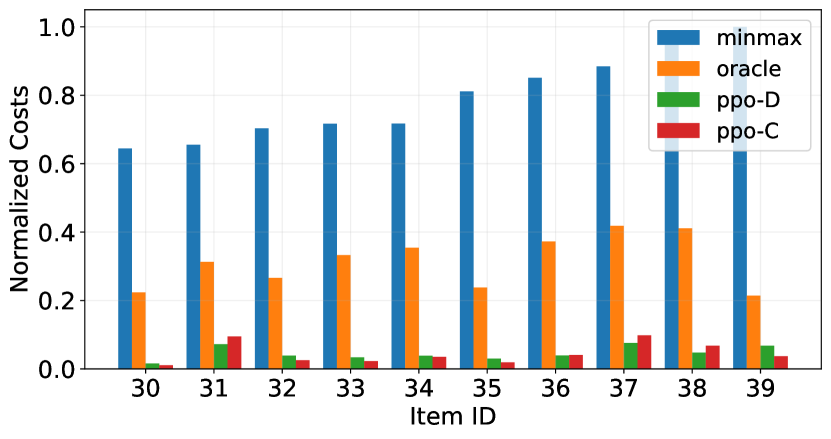

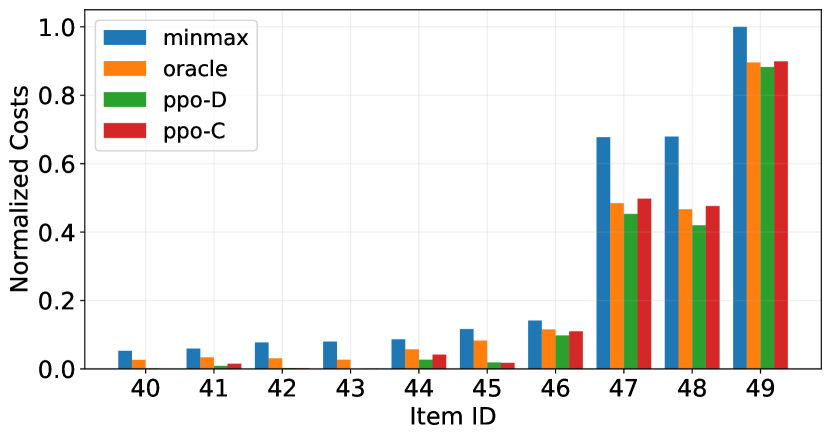

C.2 Barplots results

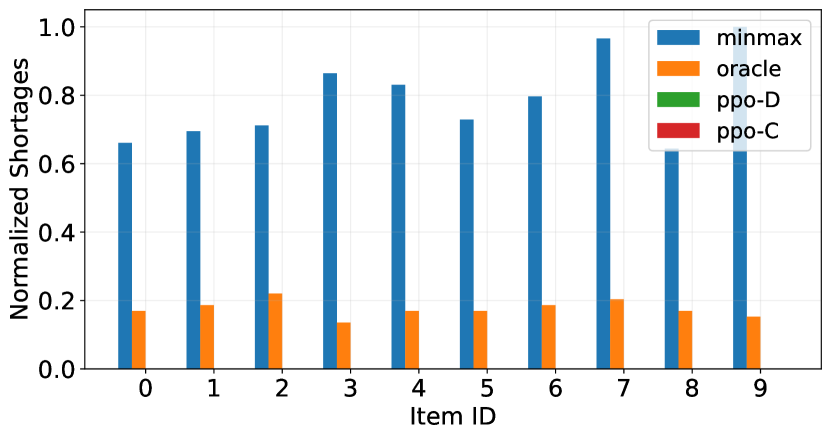

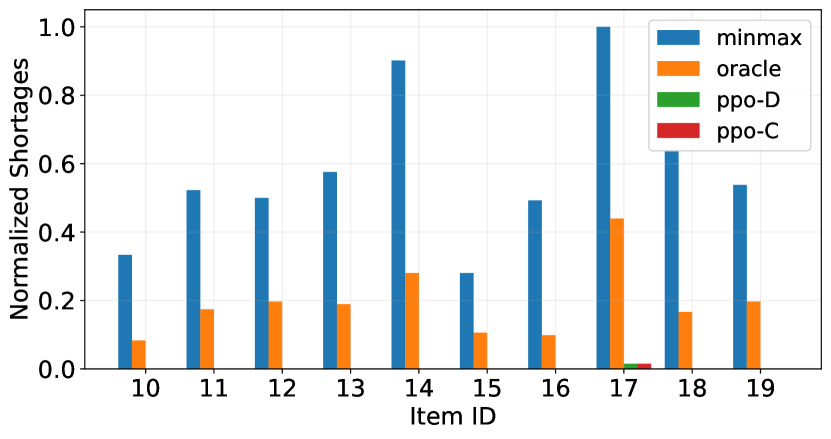

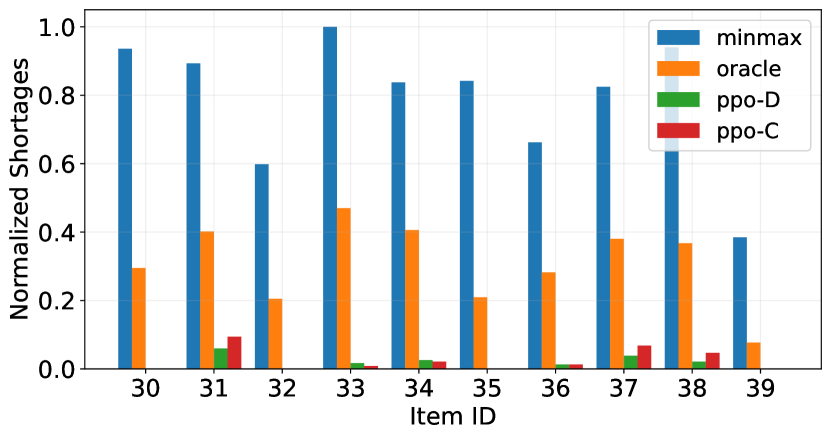

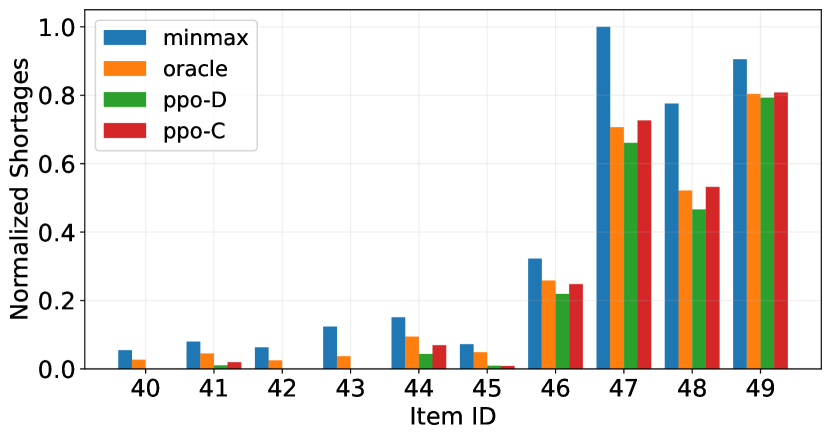

Similarly to Section C.1, the different barplots below present the full results of cumulative costs for the numerical experiments with storage space constraints per item. The items are split in groups according to the median of lead-time in order to train only average RL agent. Such agents are then tested on all the items in the corresponding group.

Appendix D Average Item Shortages

D.1 Numerical results

The different Tables below present the full results of item shortages for the numerical experiments with storage space constraints per item. The items are split in groups according to the median of lead-time in order to train only average RL agent. Such agents are then tested on all the items in the corresponding group.

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 0 | 39 | 10 | 0 | 0 |

| 1 | 41 | 11 | 0 | 0 |

| 2 | 42 | 13 | 0 | 0 |

| 3 | 51 | 8 | 0 | 0 |

| 4 | 49 | 10 | 0 | 0 |

| 5 | 43 | 10 | 0 | 0 |

| 6 | 47 | 11 | 0 | 0 |

| 7 | 57 | 12 | 0 | 0 |

| 8 | 38 | 10 | 0 | 0 |

| 9 | 59 | 9 | 0 | 0 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 10 | 44 | 11 | 0 | 0 |

| 11 | 69 | 23 | 0 | 0 |

| 12 | 66 | 26 | 0 | 0 |

| 13 | 76 | 25 | 0 | 0 |

| 14 | 119 | 37 | 0 | 0 |

| 15 | 37 | 14 | 0 | 0 |

| 16 | 65 | 13 | 0 | 0 |

| 17 | 132 | 58 | 2 | 2 |

| 18 | 84 | 22 | 0 | 0 |

| 19 | 71 | 26 | 0 | 0 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 20 | 125 | 84 | 16 | 17 |

| 21 | 119 | 41 | 0 | 0 |

| 22 | 108 | 52 | 3 | 5 |

| 23 | 132 | 69 | 1 | 1 |

| 24 | 95 | 29 | 0 | 0 |

| 25 | 155 | 88 | 16 | 16 |

| 26 | 200 | 89 | 7 | 14 |

| 27 | 109 | 46 | 2 | 4 |

| 28 | 182 | 114 | 15 | 18 |

| 29 | 109 | 26 | 0 | 0 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 30 | 219 | 69 | 0 | 0 |

| 31 | 209 | 94 | 14 | 22 |

| 32 | 140 | 48 | 0 | 0 |

| 33 | 234 | 110 | 4 | 2 |

| 34 | 196 | 95 | 6 | 5 |

| 35 | 197 | 49 | 0 | 0 |

| 36 | 155 | 66 | 3 | 3 |

| 37 | 193 | 89 | 9 | 16 |

| 38 | 220 | 86 | 5 | 11 |

| 39 | 90 | 18 | 0 | 0 |

| ID | MinMax | Oracle | PPO-D | PPO-C |

|---|---|---|---|---|

| 40 | 209 | 102 | 2 | 1 |

| 41 | 305 | 172 | 40 | 75 |

| 42 | 240 | 95 | 3 | 3 |

| 43 | 472 | 141 | 1 | 5 |

| 44 | 575 | 360 | 167 | 264 |

| 45 | 276 | 186 | 35 | 33 |

| 46 | 1230 | 986 | 837 | 945 |

| 47 | 3814 | 2695 | 2520 | 2770 |

| 48 | 2959 | 1989 | 1778 | 2030 |

| 49 | 3453 | 3066 | 3025 | 3081 |

D.2 Barplots results

Similarly to Section D.1, the different barplots below present the full results of item shortages for the numerical experiments with storage space constraints per item. The items are split in groups according to the median of lead-time in order to train only average RL agent. Such agents are then tested on all the items in the corresponding group.

Appendix E Average Cumulative Costs and Item Shortages for Multi-Agent cases

E.1 Cluster

| ID | MinMax | Oracle | IPPO-C |

|---|---|---|---|

| -0 | 56,413,703 | 47,751,643 | 21,747,138 |

| -1 | 41,218,939 | 22,017,147 | 5,860,091 |

| -2 | 28,734,942 | 10,052,437 | 9,674,691 |

| -3 | 69,445,374 | 49,567,318 | 11,468,600 |

| -4 | 50,283,017 | 18,591,579 | 11,492,810 |

| Average | 49,219,195 | 29,596,024 | 12,048,666 |

| ID | MinMax | Oracle | IPPO-C |

|---|---|---|---|

| -0 | 27 | 25 | 0 |

| -1 | 18 | 10 | 1 |

| -2 | 11 | 4 | 6 |

| -3 | 22 | 21 | 5 |

| -4 | 14 | 5 | 3 |

| Average | 18 | 9 | 3 |

E.2 Cluster

| ID | MinMax | Oracle | IPPO-C |

|---|---|---|---|

| -0 | 61,746,686 | 37,154,240 | 9,576,664 |

| -1 | 43,195,470 | 19,817,180 | 4,755,388 |

| -2 | 31,719,337 | 8,849,048 | 7,232,925 |

| -3 | 49,873,610 | 38,995,232 | 7,999,544 |

| -4 | 46,383,922 | 17,470,651 | 8,097,309 |

| -5 | 90,361,502 | 54,257,529 | 6,974,378 |

| -6 | 20,349,092 | 8,573,083 | 4,180,512 |

| -7 | 27,434,488 | 9,091,921 | 9,855,567 |

| -8 | 33,681,010 | 11,145,783 | 3,862,856 |

| -9 | 146,735,155 | 105,116,776 | 16,516,513 |

| Average | 55,148,027 | 31,047,144 | 7,905,165 |

| ID | MinMax | Oracle | IPPO-C |

|---|---|---|---|

| -0 | 33 | 18 | 1 |

| -1 | 18 | 8 | 0 |

| -2 | 14 | 2 | 0 |

| -3 | 16 | 14 | 0 |

| -4 | 13 | 4 | 0 |

| -5 | 27 | 16 | 0 |

| -6 | 11 | 8 | 0 |

| -7 | 11 | 2 | 0 |

| -8 | 14 | 5 | 0 |

| -9 | 20 | 13 | 0 |

| Average | 18 | 9 | 0 |

E.3 Cluster

| ID | MinMax | Oracle | IPPO-C |

|---|---|---|---|

| -0 | 114,748,999 | 110,936,731 | 25,133,542 |

| -1 | 76,876,589 | 25,248,863 | 13,012,784 |

| -2 | 175,969,893 | 156,867,720 | 22,712,799 |

| -3 | 61,746,686 | 38,243,787 | 11,097,544 |

| -4 | 43,195,470 | 14,974,424 | 6,590,003 |

| -5 | 31,719,337 | 9,423,716 | 12,452,378 |

| -6 | 49,873,610 | 35,928,930 | 13,922,411 |

| -7 | 46,383,922 | 20,756,443 | 7,299,909 |

| -8 | 34,654,173 | 9,843,404 | 11,531,224 |

| -9 | 90,361,502 | 55,657,119 | 13,186,238 |

| -10 | 20,349,092 | 8,662,162 | 5,354,639 |

| -11 | 41,008,234 | 12,947,589 | 10,195,819 |

| -12 | 33,335,933 | 12,451,461 | 10,197,750 |

| -13 | 27,434,488 | 8,713,145 | 8,518,849 |

| -14 | 33,681,010 | 10,451,041 | 8,045,677 |

| -15 | 106,676,800 | 56,572,852 | 11,317,268 |

| -16 | 146,735,155 | 126,683,713 | 55,932,376 |

| -17 | 46,569,841 | 24,907,569 | 14,623,596 |

| -18 | 41,120,038 | 9,885,961 | 13,659,858 |

| -19 | 43,945,213 | 10,883,913 | 10,006,678 |

| Average | 63,319,299 | 38,002,027 | 14,239,567 |

| ID | MinMax | Oracle | IPPO-C |

|---|---|---|---|

| -0 | 39 | 33 | 7 |

| -1 | 19 | 4 | 0 |

| -2 | 97 | 63 | 0 |

| -3 | 33 | 19 | 1 |

| -4 | 18 | 5 | 0 |

| -5 | 14 | 4 | 6 |

| -6 | 16 | 14 | 4 |

| -7 | 13 | 5 | 0 |

| -8 | 15 | 2 | 2 |

| -9 | 27 | 17 | 4 |

| -10 | 11 | 6 | 1 |

| -11 | 9 | 0 | 0 |

| -12 | 13 | 3 | 3 |

| -13 | 11 | 3 | 0 |

| -14 | 14 | 4 | 2 |

| -15 | 55 | 22 | 0 |

| -16 | 20 | 18 | 2 |

| -17 | 19 | 7 | 7 |

| -18 | 14 | 2 | 0 |

| -19 | 16 | 2 | 3 |

| Average | 23 | 11 | 2 |