Duopoly insurers’ incentives for data quality under a mandatory cyber data sharing regime

Abstract

We study the impact of data sharing policies on cyber insurance markets. These policies have been proposed to address the scarcity of data about cyber threats, which is essential to manage cyber risks. We propose a Cournot duopoly competition model in which two insurers choose the number of policies they offer (i.e., their production level) and also the resources they invest to ensure the quality of data regarding the cost of claims (i.e., the data quality of their production cost). We find that enacting mandatory data sharing sometimes creates situations in which at most one of the two insurers invests in data quality, whereas both insurers would invest when information sharing is not mandatory. This raises concerns about the merits of making data sharing mandatory.

keywords:

Cyber risk , Data sharing , Data quality , Cyber insurance , Cournot model1 Introduction

With an ever-increasing societal dependence upon information technology and digital services, cyber risk has received much attention lately. Such risk is not limited to any particular sector, but can be found everywhere; from manufacturing [Wells et al., 2014, Ani et al., 2017] over healthcare [Kruse et al., 2017, Coventry and Branley, 2018] and the power grid [Ericsson, 2010, Sridhar et al., 2011] to financial services [Kopp et al., 2017, Dupont, 2019, Varga et al., 2021].

Not only is cyber risk increasingly found everywhere, but the interconnectedness and interdependency of this modern world also poses challenges of its own. As pointed out by Böhme and Kataria [2006], there are at least two important forms of interdependent cyber risk: First, firms are connected to each other. While allowing huge efficiency gains when exchanging information across complex supply-chains, this also means that diligent security efforts at any one firm always risk being undermined by sloppy security somewhere else. The proverbial chain is never stronger than its weakest link. Second, many firms use the same systems, so a vulnerability found in a popular operating system, web browser, or encryption protocol may immediately put millions if not billions of machines at risk.

These difficulties are particularly relevant for insurers and reinsurers who underwrite cyber risks as part of cyber insurance offerings, and it has been repeatedly observed that interdependent cyber risk poses an important challenge to the development of a more mature and well-functioning cyber insurance market [Anderson and Moore, 2006, OECD, 2017, pp. 93–98]. This is not the place to review the extensive literature on cyber insurance—a comprehensive but slightly dated literature review is offered by Böhme and Schwartz [2010] and a more recent review is given by Marotta et al. [2017], Barreto et al. [2021]. Some notable complications with cyber insurance—in addition to the interdependence of cyber risks noted above—include unclear coverage, immature market offerings, various information asymmetries, and lack of cyber security experience and expertise on the part of insurers. In our context, however, the most important complication is lack of good actuarial data [see e.g. Biener et al., 2015, Franke, 2017, EIOPA European Insurance and Occupational Pensions Authority, 2019, OECD, 2017, pp. 94–95].

To some extent, this lack of data reflects more general problems with cyber risk data, not limited to cyber insurance. A recent attempt to systematize quantitative studies of the consequences of cyber incidents by Woods and Böhme [2021] found several contradictory and sometimes spurious results, and cautions against employing too simple statistical relationships. Similarly, a review of estimates of cyber risk likelihood found contradicting trends and emphasizes the need for rigorous and transparent methods to avoid jumping to erroneous conclusions [Woods and Walter, 2022]. In the insurance context, the difficulty of properly quantifying cyber risk forces expert-based or best-guess rather than actuarial pricing. Clearly, this may lead to undesirable outcomes, such as underpricing, where insurers unknowingly accept too much cyber risk, overpricing, where insureds pay too much for their risk transfer, or blanket exclusions of certain kinds of customers, who thus cannot reap the benefits of insurance [see, e.g., Gordon et al., 2003b, Mott et al., 2023]. Against this background, it has been proposed that increased sharing of data between insurers might be beneficial.

A recent example is an analysis by the OECD [2020] on how to enhance the availability of data for cyber insurance underwriting. The report walks through existing practices such as cyber incident data being published by CERTs or regulators, information exchange (such as the CRO forum), commercial catastrophe models made available by firms such as AIR Worldwide and RMS, and reinsurer collections of aggregate data, but ultimately concludes that “[n]one of these data sources on their own provide sufficient information for underwriting coverage as incident data is seen to be incomplete, historical experience covers too few claims and models are relatively new and untested” [OECD, 2020, p. 9]. Instead, three recommendations for government action are made; (i) to remove legal obstacles to incident and claims data sharing, (ii) to encourage industry associations to establish mechanisms for incident and claims data sharing, and (iii) to encourage international collaboration.

Another recent example is a strategy note on cyber underwriting published by the European Insurance and Occupational Pensions Authority [EIOPA European Insurance and Occupational Pensions Authority, 2020]. Here, lack of data is identified as a primary obstacle to the understanding of cyber risk, and accordingly, to appropriate coverage being offered on the market. It is also noted that the mandatory incident reporting regimes established by recent legislation such as the GDPR and the NIS directive will create relevant data. Against this background it is argued that access to a cyber incident database “could be seen as a public good and underpin the further development of the European cyber insurance industry and act as an enabler of the digital economy” [EIOPA European Insurance and Occupational Pensions Authority, 2020, p. 3]. The strategy delineated consists of EIOPA (i) promoting a harmonized cyber incident reporting taxonomy with “an aim to promote the development of a centralised (anonymised) database” [EIOPA European Insurance and Occupational Pensions Authority, 2020, p. 4], (ii) engaging with the industry to understand their perspective, and (iii) encouraging data sharing initiatives.

The industry association Insurance Europe [2020], in a direct response to the EIOPA strategy, broadly welcomes the strategy’s recognition that lack of data is a serious impediment to the growth of the European cyber insurance market. However, Insurance Europe also notes that there are trade-offs involved. Specifically, it is cautioned that while a common cyber incident database should ideally be more detailed than the GDPR and NIS data it should at the same time not impose unnecessary burdens of additional reporting or IT system adaptation, and such a database should not distort competition.111Despite the enthusiasm of Insurance Europe about using GDPR and NIS incident reports to improve cyber insurance offerings, not everyone offering cyber insurance is even aware of this possibility, as shown by a study in Norway where the interviewed “insurers seem oblivious to this aspect of NIS” [Bahşi et al., 2019]. Specifically, “if an insurer shares data it must gain access to an equal quantity and quality of data in return” [Insurance Europe, 2020, p. 2].

The relevance of data quality is underscored by recent empirical research on NIS incident reports. Based on all the mandatory NIS incident reports received by the responsible government agency in Sweden in 2020, Franke et al. [2021] find the economic aspects of reports to be incomplete and sometimes difficult to interpret. Thus, it is concluded that “just making NIS reporting, as-is, available to insurers would not by itself solve the problem of lack of data for cyber insurance. Making the most of the reporting requires additional quality assurance mechanisms.”

It is this unfolding policy issue that motivates the research question of this article: What would happen to data quality under a mandatory cyber data sharing regime for insurers? To answer it, a game-theoretic model is constructed where cyber insurers interact on a Cournot oligopoly market, but are uncertain about their (and their competitors’) production costs, i.e., the true costs of the cyber incidents underwritten. When forced to share what information they do have, they cannot refuse, but they can choose whether to invest in improving the data quality of their own information, or just provide it as-is. The model can be seen as an attempt to formalize Insurance Europe’s remark about sharing equal quantities and qualities of data—how would such sharing unfold? It should be stressed that both the OECD and EIOPA stop short of recommending mandatory cyber data sharing laws. Nevertheless, the question is implicitly on the table, and our investigation aims to bring one more perspective to this important issue.

The rest of the paper is structured as follows. In the next section, some related work is discussed, and the contribution is positioned with respect to this literature. In Section 3 the formal model is introduced, and the main results are shown in Section 4. We find mandatory data sharing changes the feasible Nash Equilibria (NE) and creates situations in which at most one of the two insurers invests in data quality, whereas both insurers would invest when information is not shared. The results are followed by a discussion of implications and conclusions in Section 6.

2 Related work

The general topic of cyber security information sharing is extensively addressed in the literature. A good starting point is the literature survey provided by Skopik et al. [2016], who offer a comprehensive and broad overview of legal, technical and organizational aspects. Koepke [2017] provides a more focused literature review on incentives and barriers, complemented by a survey of 25 respondents. Of particular interest in our context are the collaborative barriers related to “a lack of reciprocity from other stakeholders or the problem of free-riders. This barrier category also includes the risk of sharing with rivals/competitors who may use the shared information to enhance their competitive position” [Koepke, 2017, p. 4].

Turning to formal game-theory, two classic treatments are offered by Gal-Or and Ghose [2005], Gordon et al. [2003a], who show information sharing may yield benefits to firms, but also can result in free-riding. Later works typically find similar results, and address the question of what the incentives needed for cooperation look like. For example, Naghizadeh and Liu [2016] study the effects of repeated interactions, focusing on the effectiveness of monitoring regimes to detect and punish non-cooperative behavior. Similarly, in a series of papers Tosh et al. study a game where players face the binary choice of either participating in a sharing regime or not to, including its evolutionary stability [see e.g. Tosh et al., 2015, 2017].

Whereas the previous treatments consider symmetric players—the potential victims of cyber attacks—asymmetric games have also been studied. Laube and Böhme [2016] devise a principal–agent model of mandatory security breach reporting to authorities (such as those mandated under the GDPR and the NIS directive). Assuming imperfect audits which cannot determine for certain whether the failure to report an incident is deliberate concealment or mere lack of knowledge, Laube and Böhme find that it may be difficult to enact the sanctions level needed for the breach notification law to be socially beneficial.

Whereas the works mentioned above treat for-profit parties interested in sharing and receiving information there are also non-profit actors who can participate in such arrangements. For instance, Dykstra et al. [2022] analyze information sharing of unclassified cyber threat information by a government institution. Such non-profit institutions may share unclassified information in order to improve social welfare, rather than maximize their own profits.

For a fuller literature review of game theory models of cyber security information sharing, see Laube and Böhme [2017], who not only summarize the literature, but also systematize it using an illuminating unified formal model. However, in our context, it is important to note that their review does not include any articles investigating information sharing among insurers. Thus, whereas information sharing between the firms at risk is a standard component in game theoretic models of cyber risk—models which often include insurance—information sharing between the insurers underwriting the firms at risk has not yet been formally investigated using game theory, despite the policy attention described in Section 1.

Our model is inspired in the seminal work by Gal-Or [1986], which addresses information transmission in oligopolies. In her model, firms can share information about their production cost, which is unknown and different for each firm. Gal-Or [1986] finds that under Cournot competition, firms chose to share information, because they benefit when competing firms make an accurate estimation of their production cost. In our model the insurers have the same cost (e.g., they compete in the same market); hence, by sharing information a firm may reduce the uncertainty of the competitor (which is what we expect in an insurance market).

As mentioned above, we have not found any work formally investigating cyber security information sharing among insurers. Instead, the work that is most closely related to ours is a qualitative study by Nurse et al. [2020], who explore data use by cyber-underwriters in general, and the feasibility and utility of a ‘pre-competitive dataset’ shared within the industry in particular. Such a dataset is in fact precisely what is “encouraged” by the OECD [2020] and EIOPA European Insurance and Occupational Pensions Authority [2020]. However, the idea was met with considerable skepticism by the 12 cyber insurance professionals who participated in the focus groups conducted by Nurse et al. [2020]. They were all concerned about the implications for competitiveness, asking why incumbents would jeopardize their advantage by sharing information with market entrants. Indeed, the very structure of such a dataset was deemed sensitive, as even proposal forms are considered proprietary, even though there are published studies based on such forms, see Woods et al. [2017]. “People are insanely protective,” remarked one participant [Nurse et al., 2020, p. 6].

3 Market model

We use a Cournot model to study situations in which two insurers compete in a market, given that the claims (risk level) is uncertain. Before giving the formal statement of the model, it is appropriate to discuss some of the modeling choices. First, the Cournot model is an oligopoly model. Thus, on the one hand, competition is not perfect—insurers make profits, which they would not if competition drove marginal prices down to equal marginal costs [Varian, 1992, pp. 180–181]. To understand why competition is not perfect, recall that economies of scale and rigorous regulation raise barriers to entry, making it harder for new insurance companies to challenge the incumbents. On the other hand, insurers are not monopolists who can raise prices arbitrarily—there is competition even among oligopolists. For cyber insurance, this is confirmed by several studies: Nurse et al. [2020, p. 3] speak of “an extremely competitive cyber insurance market” and Woods and Moore [2019, p. 27] fear that “Competitive pressures drive a race to the bottom in risk assessment standards”. Furthermore, the Cournot model is not an uncommon choice for modeling general (non-cyber) insurance markets [see, e.g., Gale et al., 2002, Wang et al., 2003, Cheng and Powers, 2008, Gao et al., 2016].

Second, production costs are uncertain—insurers do not know beforehand how much it will cost to produce their product, i.e. how large the indemnities owed will be. This reflects the uncertainty about cyber risk and lack of actuarial pricing described in Section 1: insurers underwriting cyber risks are uncertain about those risks.

Third, these uncertain production costs are assumed to be the same for all the market competitors. This reflects the interdependency of cyber risk described in Section 1: for an insurer. More precisely, cyber risk can only be managed up to a point by practices such as insuring customers in different geographical locations or from different industries. While such practices are effective against incident causes such as an outage at a payment service provider servicing a market of just one or a few countries, they are ineffective against other risks, such as the Heartbleed [see, e.g., Zhang et al., 2014] or Log4J [see, e.g., Srinivasa et al., 2022] vulnerabilities, or prolonged outages at major cloud service providers [Lloyd’s, 2018]. It is these risks—the ones that are difficult to manage—that is our concern here. With respect to these risks, thus, insurers can be seen as essentially picking and insuring insureds from the very same set of eligible firms (with some firms being excluded by all insurers using similar rules-of-thumb). Thus, while the outcomes of claims in a particular year will certainly differ, it is not unreasonable to model these outcomes with random variables representing production costs being the same for all market actors. Indeed, such an assumption—in one form or another—is implicit in the entire discussion about data sharing.

Fourth, the uncertainties are modeled using normal random variables. The immediate rationale for this assumption is that it allows analytic calculations of conditional random variables. Therefore, it is almost always used in the extant literature on uncertainties on oligopoly markets [most prominently Gal-Or, 1986, and the secondary literature citing her]. However, this should be seen as a convenient mathematical approximation, not an empirical claim. Indeed, the literature on the statistics of cyber risk instead typically suggests more heavy-tailed distributions [see, e.g., the review by Woods and Böhme, 2021], and our model does not question that. This approximation is further discussed in Section 5.

Turning to the formal model, in the Cournot competition two firms select their production levels,222It may seem unrealistic that production levels have to be chosen this way. After all, an insurance policy differs from physical goods and is not subject to the same production constraints. However, this is too simplistic—an insurer cannot scale production arbitrarily fast. Even if the constraints are not identical to those of physical production, important constraints are indeed imposed by, e.g., the ability to hire underwriters and claims managers, by access to capital (whether from investors or from bank loans), by the capacity of the brokers who act as middlemen on the cyber insurance market [see, e.g., Franke, 2017, Woods and Moore, 2019], and by regulation. which determine the market price of their goods. Let be the set of firms and the real quantity their production, for . In this case represents the number of policies offered. We define the inverse demand function, i.e., the unitary price of a product as

| (2) |

where . The value represents the premium, i.e., the payment that the insurer receives.

We assume that each insurer has a linear production cost , where is the marginal cost (the claims of each policy). For simplicity we assume that the insurers offer identical products (), allowing the price to be written as a function of the total production . We also assume that the insurers have the same marginal production costs (), an unknown value with distribution , where is the uncertainty about the production cost.333While variance is often denoted , for simplicity, we adhere to the notation of Gal-Or [1986] and denote it as . Note that the assumption that has mean zero does not affect the results, but considerably simplifies the exposition.444 Consider the marginal cost , where and represent fixed and variable components. With an inverse demand function of the form the profit can be rewritten as (3) The last step results by making . We can set the parameter large enough to guarantee that .

The use of a single random cost variable merits some additional discussion. Importantly, this means that insurers do not benefit from the law of large numbers, as they would if instead there was rather a sum of single random cost variables—one per insured. To understand why this is reasonable, recall the discussion above about the fact that cyber risk can only be managed up to a point by practices such as insuring customers in different geographical locations or from different industries. Some risks remain, namely, the ones stemming from irreducible interdependence, as discussed in Section 1. These risks—e.g., the risks that all of the insureds are hit by something like Heartbleed or Log4J—are precisely the ones that have prompted the policy interest in cyber insurance information sharing, i.e., the risks that are our concern here. These risks are well modeled by the use of a single random cost variable, and this is what the model is designed to reflect. Of course, this is not to deny that the law of large numbers works well for other risks, including (some) other cyber risks, and that this is a cornerstone of insurance. But the model developed here aims to reflect precisely the interdependent cyber risks that cannot be tamed by the law of large numbers.

In our model each insurer conducts a risk assessment and finds a noisy signal about the claims (i.e., the production cost), denoted , where the noise is independent from the cost . Here represents the uncertainty inherent in the signal. We assume that is a private signal that depends on investments to improve the risk assessment process and its output. We do not explicitly model the mechanisms by which can be improved. However, it is clear that many possibilities exist, ranging from better security audits before underwriting clients, to continuous SIEM-like monitoring of clients’ systems, to improving DFIR (Digital Forensics and Incident Response) processes once incidents occur. It is equally clear that such possibilities entail costs. Note that as opposed to Gal-Or, we do not assume that firms deliberately garble any information. We do, however, assume that data quality is a real issue, and that it may be low in the absence of deliberate and costly efforts to improve it. Recall the results from the study of Swedish NIS reports: “Making the most of the reporting requires additional quality assurance mechanisms” [Franke et al., 2021]. Concretely, an investment leads to an uncertainty

| (4) |

where represents the uncertainty without any investments (e.g., when the assessment is made using publicly available data555 Public reports, like the studies conducted by NetDiligence or the Ponemon Institute, may offer some information about the cyber risks of different industries. In addition, information sharing may take place among business partners, e.g., between insurance firms and their reinsurance providers and/or third parties that offer technical support. ) and represents the efficacy reducing noise. Again, we assume that these parameters are equal for both insurers. From Eq. 4 the investment needed to have an uncertainty is

| (5) |

which is a concave with respect to the uncertainty level . Eq. 5 implies that it’s prohibitively expensive to have no uncertainty (). Now, the profit of firm , denoted , is equal to its income minus both production and risk assessment costs

| (6) |

3.1 Game formulation

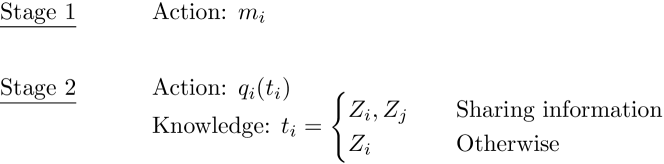

In our Cournot model the insurers make two decisions at different stages (see Fig. 1):

-

1.

In the first stage insurers make investments and commit to an information sharing policy. This is equivalent to selecting the uncertainty level , which in turn determines the investment . We assume that the sharing policy is defined before the game starts.

-

2.

In the second stage the marginal production cost is realized and each firm gets an estimate . Then the information transmission takes place and each firm uses the information available, represented as , to select the production quantity . The information available is when insurers share their cost estimations, otherwise it is .

Thus, the strategy of each firm has the form , which satisfies the subgame perfect equilibria if it is a Nash Equilibrium (NE) in each stage of the game. We start by analyzing the second stage game to determine the production (see Fig. 1). With this result we build the game in the first stage and then formulate the problem of selecting the optimal uncertainty (noise level) of the data . Some of the results in this section resemble the findings of Gal-Or [1986], because the Cournot model there is similar (at a high level) to ours; however, the precise solution for our model is different. We find the precise profit function for each scenario in the next section.

3.2 Second stage (low level) game

In this stage and are given and each firm chooses a production that maximizes their expected profits given the available information (Fig. 1). We define the game in the second stage as

| (7) |

where is the set of players, is the strategy space, and is the payoff function of the ith firm, which in this case corresponds to the expected profit in a Cournot competition (see Eq. 6) given the signal . The following result shows the form of as a function of the optimal production .

Lemma 1.

Proof.

The expected profit in a Cournot competition (see Eq. 6) is

| (10) |

The expectation is made with respect to the unknown parameters, such as the cost (and the signal when the firms do not share information). Thus,

| (11) |

where is an estimation of the production cost and is the estimated production of the adversary, given the available observation . The optimal production must satisfy the following first order condition (FOC)

| (12) |

In this case the optimal production is unique, since the expected profit is concave with respect to :

| (13) |

Now, from Eq. 12 the optimal production satisfies

| (14) |

Replacing Eq. 14 in Eq. 11 we obtain

| (15) | ||||

| (16) |

∎

3.3 First stage (upper level) game

We define the game in the first stage (see Fig. 1) as

| (17) |

where insurers can select an uncertainty level and the utility is the expected profit, given that firms choose in the second stage (see Lemma 1). In this stage hasn’t been realized; hence, the optimal production can be seen as a random variable. The following result shows the form of .

Lemma 2.

Proof.

Remark 1.

We cannot guarantee that has a Nash Equilibrium (NE). Also, rather than finding the precise NE of , we focus on finding the conditions in which investing in risk assessment is feasible or not. Thus, we classify the possible NE in the following categories

-

1.

Both insurers invest (but different amounts): , with and .

-

2.

Both insurers invest the same amount: , with .

-

3.

Only one insurer invests in risk assessment: , with .

-

4.

Neither insurer invests: .

3.4 Cost Estimation

Since both the cost and the noise are normally distributed, the sample is also normally distributed: . This property makes it easier to find the closed form expressions of variables of interest. For instance, the estimation of the cost conditional to the sample is

| (20) |

with . Moreover, we can find the expected cost given two observations, and , using the multivariate normal distribution

| (21) |

where . Fig. 2 shows the Bivariate distribution of and with parameters and .

The samples and are correlated through the cost ; hence, . For this reason the insurer can estimate the sample of it’s adversary as

| (22) |

Note that sharing information creates a conflict, because although insurers may benefit, they may also help the competing insurer.

Fig. 3 shows an example of the cost distribution given some observations. In this case each additional observation reduces the uncertainty of the cost (variance). Note that the insurers use to make decisions in the second stage, rather than the rv depicted in Fig. 3.

4 Analysis of the market’s equilibria

In this section we find the optimal production and the utility function in the upper level game for each scenario (sharing and non-sharing information). Then we find the possible equilibria of the game and illustrate them with examples.

4.1 Market with information sharing

In this case the firms share their private information . Thus, they have the same signal , and therefore, make the same cost estimation , where (see Eq. 21). Moreover, since firms have the same characteristics and possess the same information, there is no uncertainty about the production of the adversary, because . In addition, they produce the same quantity . Thus, from Eq. 14 we get

| (23) |

Now, recall that the cost , , and are independent normal random variables. Thus, in the first stage, when neither , nor have been realized, we can see as a random variable (see Eq. 21)

| (24) |

where , , and , with . Thus, the cost estimation is normally distributed with

| (25) |

Now, from Eq. 23 the optimal production can be seen as a random variable . Therefore, the profit of the game (see Eq. 18) is

| (26) | ||||

| (27) |

The following result shows that only one firm may invest in risk assessment.

Proposition 1.

A duopoly in which insurers share information can have two types of Nash equilibria (but only one of this scenarios can occur in a game):

-

1.

Neither firm invests () if or if

(28) -

2.

Only one insurer invests (e.g., and ) if

(29) where .

The reader can find the proof of this and the following results in the appendix.

Fig. 4 illustrates the possible equilibria for different values of and (see Proposition 1). Fig. 5 shows examples with the two possible NE, namely and . In this case, free-riding can occur because at most one insurer invests in data quality (when is large, i.e., when the data quality is low without any investment) . In these examples we use the following parameters: , , , and . Moreover, for the NE examples we use (Fig. 5(a)) and (Fig. 5(b)).

4.2 Market without information sharing

In this case the information available is . From Gal-Or [1986], Radner [1962] the decision rules must be affine in the vector of observations (in this case ), therefore,

| (30) |

for some constants and . From Eq. 30 we can find the expected demand of the adversary given the information

| (31) |

We can use Eq. 22 to rewrite Eq. 31 as

| (32) |

Replacing Eq. 20 and Eq. 31 in Eq. 14 we obtain

| (33) |

Eq. 30 and Eq. 33 are equivalent, therefore the coefficients and must satisfy

| (34) |

which have the following solution

| (35) |

Now, in the first stage the optimal production can be seen as a random variable. Since is normal, the production is also normal (see Eq. 30)

| (36) |

Then, the profit of is

| (37) | ||||

| (38) |

The following result states that the market can have three types of equilibria. Unlike the previous case, not sharing information creates the conditions to have both insurers investing in data quality.

Proposition 2.

A duopoly in which insurers do not share information can have the following equilibria

-

1.

is the only NE if

-

2.

is the only feasible NE if

(39) where .

-

3.

and are feasible NE if

(40) where .

Fig. 6 shows the feasible equilibria (when insurers do not share information) for different values of and . Investments in data quality occur only when is large, that is, when the data quality is low without any investment. Fig. 7 shows two examples of the possible equilibria in the market without sharing information. In particular, Fig. 7(b) shows that, unlike in the market that with information sharing enforced, one or both firms can invest in data quality in the equilibria. In these examples (same as the example in Fig. 5). Fig. 7(a) has and Fig. 7(b) .

5 Relaxing the normal approximation

In this section we argue that the previous results are also valid—to some extent—when we consider extreme events in the costs, i.e., cost distributions with heavier right tails than the normal distribution, as is often the case with cyber risks. Let us consider a cost distribution with pdf

| (41) |

where , , is a normal pdf, a Generalized Pareto Distribution (GPD). In this case, claims that exceed the threshold are modeled with the GPD. Now, an estimation of the cost given some information is

| (42) |

Let us decompose the estimation into two terms, one corresponding to the most frequent events and one to the tail

| (43) | ||||

| (44) |

Here and represent the lower and upper estimates of the cost. We assume that the first term is close to the cost estimation assuming a normal distribution. Intuitively, estimations assuming a normal distribution ignore the contribution of the tail.

The optimal amount of policies issued by each insurer—see Eq. 9—then becomes666 We can use Lemmas 1 and 2 because they are independent of the distributions of and .

| (45) |

Note that the optimal production is lower when we consider the costs from the tail. Now, let us express the optimal production as

| (46) |

where is the optimal production assuming a normal distribution. Substituting Eq. 46 into Eq. 45 we obtain

| (47) |

The previous expression can be rewritten as

| (48) | ||||

| (49) |

The last step results from using Lemma 1 to get the optimal production when we estimate the cost assuming a normal distribution (i.e., using the cost estimate ). From Eq. 46 and Eq. 48 conclude that

| (50) |

Through Eq. 50 we express the impact of the tail in the optimal decision (in the second stage of the game). Now we can analyze how the tail affects the game in the first stage. Concretely, the utility function becomes (see Lemma 2)

| (51) |

Note that depends on both and . Thus, we argue that if the tail of the cost has finite mean and variance, then we can approximate Eq. 51 with

| (52) |

where represents the utility in the first stage that we obtain using the normal approximation. If the tail of the cost has finite mean and variance,777Heavy tail distributions like the Lognormal distribution, sometimes used to model the size of cyber incidents [Woods and Böhme, 2021], satisfy and . then we can find some bounds s.t.

| (53) | |||

| (54) |

It follows from Lemma 10 that the NE obtained assuming a normal distribution is close to the NE that we would obtain considering the tail of the distribution [see the discussion of -equilibria in Myerson, 1978, Fudenberg and Levine, 1986]. How close depends on the size of the tail.

6 Discussion and Conclusions

Fig. 8 compares the equilibria resulting with each information policy. When insurers share information, they tolerate data with poorer quality (i.e., large ) before starting to invest. Also, forcing information sharing may reduce the investment in data quality of the risk assessments, because the NE changes from or to a NE where neither insurer invests (see region A). Likewise, mandatory information sharing can restrict the NE to a situation of free-riding, because is not feasible (see region B).

These results illustrate important concerns about mandatory information sharing about cyber incidents in insurance. With no way to enforce data quality, a mandatory information sharing regime may be (i) counterproductive if leading to no investment in data quality—an NE—or (ii) unfair if leading to free-riding—an NE. This result is a bit reminiscent of Laube and Böhme [2016], who show that mandatory security breach reporting to authorities may have adverse effects unless it can be determined whether the failure to report an incident is deliberate concealment or mere lack of knowledge.

Needless to say, the model employed is simplified, and does not capture the full complexity of reality. A first aspect of this is that it is exceedingly difficult to determine the parameters needed to facilitate exact calculations according to the model. Nevertheless, the model does show what we believe are important qualitative properties of mandatory information sharing situations: potentially undesirable transitions to counterproductive or unfair NEs if mandatory information sharing is enacted. A second aspect of this relates to the normal approximation discussed in Section 5. A third aspect is that the model treats duopoly rather than the more general oligopoly situation. Now, there is good reason to believe that our results should generalize to the oligopoly situation—Raith [1996, see 3.a, p. 263] has shown that for Cournot markets, the results from Gal-Or [1986] and similar duopoly studies are valid for oligopolies as well. A detailed investigation of the oligopoly case, however, is beyond the scope of this paper. Nonetheless, we would expect that insurers would have lower incentives to invest in data quality for two reasons: 1) the profit of firms will be lower with each additional competitor; and 2) imposing data sharing in an oligopoly will give each firm access to more data.

In addition to the simplifications of the model, the NE concept also has some limitations. Concretely, the existence of a particular NE only says that if the players are there, none of them has anything to gain from unilaterally deviating. However, if they are not there, the NE concept does not provide any mechanism for how the NE could be reached. This means that it is not possible to say which outcome will actually occur when there are multiple NEs. Despite this, our analysis is important because it reveals strategic tensions between the players. For example, in practice, situations that create opportunities for free-riding may result in no investments, because each firm will try to free-ride.

Future research directions include analyzing whether sharing information policies benefit insurers and consumers (despite of creating free-riding scenarios) and designing incentives that could improve the data quality. Also, it would be interesting to contemplate other cost and risk aversion functions on the part of the insurers, as well as extending the treatment in Section 5 of alternative cost distributions.

Appendix A Additional results and proofs

The following results show some properties of the decision of each firm. We use these results to analyze the equilibria of the market with different data sharing policies.

Lemma 3.

Let be a feasible decision in the game when the adversary selects . The following is satisfied

-

1.

is not feasible

-

2.

is feasible if

-

3.

is feasible if and ,

where and represent the first and second derivative of with respect to .

Proof of Lemma 3.

We formulate the decision of each firm with the following optimization problem

| (55) |

whose Laplacian is

| (56) |

The noise level is a local maxima if the following necessary conditions are satisfied

| (57) |

and

| (58) |

with . Moreover, the second order sufficient condition is

| (59) |

Now let us analyze the strategies that the insurer may choose:

-

1.

is a valid solution if , and

(60) however, this is not possible because

(61) -

2.

is a valid solution if , and

(62) which means that

(63) -

3.

is a valid solution if , and

(64) with the second order condition

(65)

∎

The next result shows that, except a special case, and cannot be NE simultaneously. Thus, we assume that only one of these NE can occur.

Lemma 4.

The tuples and , with , can be NE simultaneously only if they return the same profit, i.e., . Otherwise, only one of them can be a NE.

Proof of Lemma 4.

Assume that is a NE, this means that

| (66) |

If the inequality is strict, i.e., , then cannot be a NE. We can make the same argument when is a NE. ∎

Now we introduce some results that specify conditions that restrict the possible NE.

Corollary 1.

If for all , then and , with , are the only possible NE.

Proof of Corollary 1.

Lemma 5.

If is decreasing with respect to , then the best response of the insurer , denoted , is decreasing with respect to . In such cases, if is a feasible NE, then no other NE exists.

Proof.

Suppose that is the best response to the strategy . This means that is a local maxima, i.e., and (see Lemma 3). Then the following applies for two strategies and

| (67) |

Let us assume without loss of generality that . If is decreasing wrt , then

| (68) |

Now, replacing Eq. 68 in Eq. 67 we obtain

| (69) |

Since we know that is decreasing wrt . Hence,

| (70) |

In other words, the best response function is decreasing wrt . ∎

A.1 Market with information sharing

Now we are ready to prove Proposition 1.

Proof of Proposition 1.

In this proof we first find the form of the possible NE and then find the conditions to guarantee that they are feasible. From Eq. 26 the first and second derivatives of the profit are:

| (71) |

and

| (72) |

Let us show that a NE in which both firms invest () does not exist. Note that , with , is a feasible equilibria if it satisfies for each firm. This FOC can be rewritten as (see Eq. 71)

| (73) |

Since the right hand side is identical for each firm we obtain

| (74) |

The above expression implies that (this is the only possible solution). Replacing in Eq. 73 results in

| (75) |

Now, the second derivative evaluated on is

| (76) |

Replacing Eq. 75 in the previous expression leads to

| (77) | ||||

| (78) |

Thus, a pair that satisfies the FOC corresponds to a local minimum; hence, it is not a valid NE. This implies that in the NE at least one of the firms doesn’t invest at all. Following this observation we set and investigate possible values of in the NE. A pair is a feasible NE if it satisfies the FOC

| (79) |

The above expression leads to

| (80) |

which is a quadratic equation of the form

| (81) |

with , , and . The solution of Eq. 81 has the well known form

| (82) |

where

| (83) |

Now, let us investigate the conditions in which Eq. 82 has no valid solution. In other words, cases in which for all . If this happens then the game can have a single NE, namely (see Lemma 3). Eq. 82 has an imaginary value if , that is, if

| (84) |

This inequality holds in the following two cases:

-

1.

If and

(85) -

2.

If .

In summary, is the only NE if or if and .

Now, a real solution exists only if , that is, if

| (86) |

Moreover, observe that (since ). Therefore, if then we have two positive solutions. This occurs if

| (87) |

The above holds when

| (88) |

Note that the conditions in Eq. 88 hold when Eq. 86 is true. For this reason, if Eq. 81 has real solutions, then they are positive.

Now, let us find the conditions to have a feasible NE of the form , where . Alternatively, we are looking for situations in which is not a feasible solution, i.e., when . This is the case when Eq. 81 has only one solution in the interval . In other words, if the largest root is greater than :

| (89) |

From the above inequality we obtain

| (90) |

which leads to

| (91) |

We expand Eq. 91 to obtain

| (92) |

The above in turn leads to

| (93) |

where . Observe that when Eq. 86 has real roots. Therefore, Eq. 93 holds if

| (94) |

Thus, from Eqs. 86 and 94 is a feasible solution when

| (95) |

∎

A.2 Market without information sharing

Let us define , , , and the functions

| (96) |

and

| (97) |

to write the marginal profit as

| (98) |

Before proving Proposition 2 we need the following results:

Lemma 6.

The equation

| (99) |

has no positive solution (i.e., ) when . However, if , then there is only one positive solution .

Proof.

Lemma 7.

A game where insurers do not share information can have a NE of the form if .

Proof.

From the second derivative of the profit and the FOC we get

| (104) |

where . Observe that we only need to identify the sign of .

Now, replacing , i.e., , and we get

| (105) |

If then and is a local maximum.

Replacing , i.e., and , we get

| (106) |

If then and is a local maxima.

In summary, is a feasible NE if . ∎

Lemma 8.

A game where insurers do not share information can have a NE of the form if .

Proof.

From the second derivative of the profit and the FOC we get

| (107) |

where . Expanding the right hand side

| (108) |

We can reorganize as

| (109) |

Replacing we obtain

| (110) |

Then, if we can guarantee that , which means that a NE o the form is feasible. ∎

Lemma 9.

Consider a game without sharing information. If is a feasible solution, then is also a feasible solution, but the converse is not necessarily true.

Proof.

Let be a feasible solution, which means that

| (111) |

| (112) |

Without loss of generality we assume that . Note that the marginal profit is decreasing wrt , that is,

| (113) |

The inequality follows since .

Since the function is continuous wrt and , then there exist a such that . ∎

Now we are ready to prove Proposition 2.

Proof of Proposition 2.

First, let us consider a scenario in which a pair with is a NE, which satisfies the FOC for both firms (see Lemma 3). We can reorganize Eq. 98 for each player to obtain

| (116) |

The above expression leads to

| (117) |

which has two solutions, namely and . Thus, the NE can have the following form:

| (118) |

for some .

An equilibria of the form has multiple restrictions. Concretely, it is a local maxima only if (see Lemma 7). In addition, it restricts the range of to ; hence, such solutions are feasible only if (i.e., ).

Lemma 9 shows that if is a feasible NE, then is also feasible (however, the converse is not necessarily true). Note that a NE of the form is a local maxima if (see Lemma 8). We focus on equilibria of the form because it has less restrictions.

Now let us analyze the conditions for the following equilibria: , , and , for .

Let us show that for all , which according to Corollary 1, is enough to guarantee that is the only NE. Note that

| (119) |

with . Since and , then

| (120) | ||||

| (121) |

Then if . Note that if , then an equilibria of the form is possible.

Now, using we can obtain the following

| (122) |

Let be such that the upper bound in Eq. 127 is equal to zero, that is,

| (123) |

From Lemma 6 we know that the previous expression has a positive solution if , where . Concretely, the solution to Eq. 123 is

| (124) |

if

| (125) |

In summary,

| (126) |

for , and according to Lemma 3, is a feasible NE. Moreover, since is decreasing wrt , then is the only NE (see Lemma 5).

Next, using we obtain

| (127) |

Let such that the upper bound in Eq. 127 is equal to zero

| (128) |

We can rewrite the above as

| (129) |

where . From Lemma 6 we know that the previous expression has a positive solution if , that is, if

| (130) |

If the above is satisfied, then the solution is

| (131) |

Note that Eq. 127 is decreasing wrt ; hence,

| (132) |

for , in which case is a feasible NE. ∎

Lastly, the next result defines conditions to have an Nash Equilibrium:

Lemma 10.

Consider the games and . If is an approximation of s.t.

| (133) | |||

| (134) |

for and any for , then a NE of is an -NE (or near NE) of .

Acknowledgments

This research was supported by Länsförsäkringar (O. Reinert & T. Wiesinger), the Swedish Foundation for Strategic Research, grant no. SM19-0009 (U. Franke), and Digital Futures (U. Franke & C. Barreto). We would like to thank the anonymous reviewers for their insightful feedback, which helped us to improve the manuscript.

References

- Anderson and Moore [2006] Anderson, R., Moore, T., 2006. The economics of information security. Science 314, 610–613. URL: http://dx.doi.org/10.1126/science.1130992.

- Ani et al. [2017] Ani, U.P.D., He, H.M., Tiwari, A., 2017. Review of cybersecurity issues in industrial critical infrastructure: manufacturing in perspective. Journal of Cyber Security Technology 1, 32–74. doi:10.1080/23742917.2016.1252211.

- Bahşi et al. [2019] Bahşi, H., Franke, U., Langfeldt Friberg, E., 2019. The Cyber-Insurance Market in Norway. Information and Computer Security 28, 54–670. doi:10.1108/ICS-01-2019-0012.

- Barreto et al. [2021] Barreto, C., Schwartz, G., Cardenas, A.A., 2021. Cyber-insurance, in: Safety, Security and Privacy for Cyber-Physical Systems. Springer, pp. 347–375.

- Biener et al. [2015] Biener, C., Eling, M., Wirfs, J.H., 2015. Insurability of cyber risk: An empirical analysis. The Geneva Papers on Risk and Insurance-Issues and Practice 40, 131–158. doi:10.1057/gpp.2014.19.

- Böhme and Kataria [2006] Böhme, R., Kataria, G., 2006. Models and measures for correlation in cyber-insurance., in: Workshop on Economics of Information Security – WEIS.

- Böhme and Schwartz [2010] Böhme, R., Schwartz, G., 2010. Modeling Cyber-Insurance: Towards a Unifying Framework., in: Workshop on Economics of Information Security – WEIS.

- Cheng and Powers [2008] Cheng, J., Powers, M.R., 2008. Can independent underwriters benefit insurers in high-risk lines? a cournot market-game analysis. Assurances (Insurance and Risk Management) 76, 5–44.

- Coventry and Branley [2018] Coventry, L., Branley, D., 2018. Cybersecurity in healthcare: a narrative review of trends, threats and ways forward. Maturitas 113, 48–52. doi:10.1016/j.maturitas.2018.04.008.

- Dupont [2019] Dupont, B., 2019. The cyber-resilience of financial institutions: significance and applicability. Journal of Cybersecurity 5, 1–17. doi:10.1093/cybsec/tyz013.

- Dykstra et al. [2022] Dykstra, J., Gordon, L.A., Loeb, M.P., Zhou, L., 2022. The economics of sharing unclassified cyber threat intelligence by government agencies and departments. Journal of Information Security 13, 85–100.

- EIOPA European Insurance and Occupational Pensions Authority [2019] EIOPA European Insurance and Occupational Pensions Authority, 2019. Cyber risk for insurers – Challenges and opportunities. doi:10.2854/305969.

- EIOPA European Insurance and Occupational Pensions Authority [2020] EIOPA European Insurance and Occupational Pensions Authority, 2020. EIOPA strategy on cyber underwriting. doi:10.2854/793935.

- Ericsson [2010] Ericsson, G.N., 2010. Cyber security and power system communication—essential parts of a smart grid infrastructure. IEEE Transactions on Power Delivery 25, 1501–1507. doi:10.1109/TPWRD.2010.2046654.

- Franke [2017] Franke, U., 2017. The cyber insurance market in Sweden. Computers & Security 68, 130–144. doi:10.1016/j.cose.2017.04.010.

- Franke et al. [2021] Franke, U., Turell, J., Johansson, I., 2021. The cost of incidents in essential services—data from Swedish NIS reporting, in: 16th International Conference on Critical Information Infrastructures Security (CRITIS 2021), Springer. pp. 116–129. doi:10.1007/978-3-030-93200-8_7.

- Fudenberg and Levine [1986] Fudenberg, D., Levine, D., 1986. Limit games and limit equilibria. Journal of Economic Theory 38, 261–279. doi:10.1016/0022-0531(86)90118-3.

- Gal-Or [1986] Gal-Or, E., 1986. Information transmission—Cournot and Bertrand equilibria. The Review of Economic Studies 53, 85–92. doi:10.2307/2297593.

- Gal-Or and Ghose [2005] Gal-Or, E., Ghose, A., 2005. The economic incentives for sharing security information. Information Systems Research 16, 186–208.

- Gale et al. [2002] Gale, D., Hellwig, M., et al., 2002. Competitive Insurance Markets with Asymmetric Information: A Cournot-Arrow-Debreu Approach. Technical Report. Sonderforschungsbereich 504, Universität Mannheim.

- Gao et al. [2016] Gao, Y., Nozick, L., Kruse, J., Davidson, R., 2016. Modeling competition in a market for natural catastrophe insurance. Journal of Insurance Issues , 38–68URL: https://www.jstor.org/stable/43741101.

- Gordon et al. [2003a] Gordon, L.A., Loeb, M.P., Lucyshyn, W., 2003a. Sharing information on computer systems security: An economic analysis. Journal of Accounting and Public Policy 22, 461–485. doi:10.1016/j.jaccpubpol.2003.09.001.

- Gordon et al. [2003b] Gordon, L.A., Loeb, M.P., Sohail, T., 2003b. A framework for using insurance for cyber-risk management. Communications of the ACM 46, 81–85. doi:10.1145/636772.636774.

- Insurance Europe [2020] Insurance Europe, 2020. Key messages on EIOPA’s cyber underwriting strategy. URL: https://www.insuranceeurope.eu/key-messages-published-eiopa-cyber-strategy. Published June 15, 2020.

- Koepke [2017] Koepke, P., 2017. Cybersecurity information sharing incentives and barriers. Sloan School of Management at MIT University. https://cams.mit.edu/wp-content/uploads/2017-13.pdf.

- Kopp et al. [2017] Kopp, E., Kaffenberger, C., Wilson, C., 2017. Cyber risk, market failures, and financial stability. IMF Working Paper URL: https://www.imf.org/en/Publications/WP/Issues/2017/08/07/Cyber-Risk-Market-Failures-and-Financial-Stability-45104.

- Kruse et al. [2017] Kruse, C.S., Frederick, B., Jacobson, T., Monticone, D.K., 2017. Cybersecurity in healthcare: A systematic review of modern threats and trends. Technology and Health Care 25, 1–10. doi:10.3233/THC-161263.

- Laube and Böhme [2016] Laube, S., Böhme, R., 2016. The economics of mandatory security breach reporting to authorities. Journal of Cybersecurity 2, 29–41. doi:10.1093/cybsec/tyw002.

- Laube and Böhme [2017] Laube, S., Böhme, R., 2017. Strategic aspects of cyber risk information sharing. ACM Computing Surveys (CSUR) 50, 1–36. doi:10.1145/3124398.

- Lloyd’s [2018] Lloyd’s, 2018. Cloud Down: Impacts on the US economy. Technical Report. Lloyd’s of London. URL: https://www.lloyds.com/news-and-risk-insight/risk-reports/library/technology/cloud-down. accessed March 19, 2018.

- Marotta et al. [2017] Marotta, A., Martinelli, F., Nanni, S., Orlando, A., Yautsiukhin, A., 2017. Cyber-insurance survey. Computer Science Review 24, 35–61. doi:10.1016/j.cosrev.2017.01.001.

- Mott et al. [2023] Mott, G., Turner, S., Nurse, J.R., MacColl, J., Sullivan, J., Cartwright, A., Cartwright, E., 2023. Between a rock and a hard (ening) place: Cyber insurance in the ransomware era. Computers & Security , 103162doi:10.1016/j.cose.2023.103162.

- Myerson [1978] Myerson, R.B., 1978. Refinements of the Nash equilibrium concept. International Journal of Game Theory 7, 73–80. doi:10.1007/BF01753236.

- Naghizadeh and Liu [2016] Naghizadeh, P., Liu, M., 2016. Inter-temporal incentives in security information sharing agreements, in: 2016 Information Theory and Applications Workshop (ITA), IEEE. pp. 1–8. doi:10.1109/ITA.2016.7888179.

- Nurse et al. [2020] Nurse, J., Axon, L., Erola, A., Agrafiotis, I., Goldsmith, M., Creese, S., 2020. The data that drives cyber insurance: A study into the underwriting and claims processes, in: 2020 International Conference on Cyber Situational Awareness, Data Analytics and Assessment (CyberSA), pp. 1–8. doi:10.1109/CyberSA49311.2020.9139703.

- OECD [2017] OECD, 2017. Enhancing the Role of Insurance in Cyber Risk Management. doi:10.1787/9789264282148-en.

- OECD [2020] OECD, 2020. Enhancing the Availability of Data for Cyber Insurance Underwriting. URL: https://www.oecd.org/daf/fin/insurance/Enhancing-the-Availability-of-Data-for-Cyber-Insurance-Underwriting.pdf.

- Radner [1962] Radner, R., 1962. Team decision problems. The Annals of Mathematical Statistics 33, 857–881.

- Raith [1996] Raith, M., 1996. A general model of information sharing in oligopoly. Journal of economic theory 71, 260–288. doi:10.1006/jeth.1996.0117.

- Skopik et al. [2016] Skopik, F., Settanni, G., Fiedler, R., 2016. A problem shared is a problem halved: A survey on the dimensions of collective cyber defense through security information sharing. Computers & Security 60, 154–176. doi:10.1016/j.cose.2016.04.003.

- Sridhar et al. [2011] Sridhar, S., Hahn, A., Govindarasu, M., 2011. Cyber–physical system security for the electric power grid. Proceedings of the IEEE 100, 210–224. doi:10.1109/JPROC.2011.2165269.

- Srinivasa et al. [2022] Srinivasa, S., Pedersen, J.M., Vasilomanolakis, E., 2022. Deceptive directories and “vulnerable” logs: a honeypot study of the ldap and log4j attack landscape, in: 2022 IEEE European Symposium on Security and Privacy Workshops (EuroS&PW), IEEE. pp. 442–447. doi:10.1109/EuroSPW55150.2022.00052.

- Tosh et al. [2015] Tosh, D., Sengupta, S., Kamhoua, C., Kwiat, K., Martin, A., 2015. An evolutionary game-theoretic framework for cyber-threat information sharing, in: 2015 IEEE International Conference on Communications (ICC), IEEE. pp. 7341–7346. doi:10.1109/ICC.2015.7249499.

- Tosh et al. [2017] Tosh, D.K., Shetty, S., Sengupta, S., Kesan, J.P., Kamhoua, C.A., 2017. Risk management using cyber-threat information sharing and cyber-insurance, in: International conference on game theory for networks, Springer. pp. 154–164. doi:10.1007/978-3-319-67540-4_14.

- Varga et al. [2021] Varga, S., Brynielsson, J., Franke, U., 2021. Cyber-threat perception and risk management in the Swedish financial sector. Computers & Security 105. doi:10.1016/j.cose.2021.102239.

- Varian [1992] Varian, H.R., 1992. Microeconomic analysis. volume 3. Norton New York.

- Wang et al. [2003] Wang, J.L., Tzeng, L.Y., Wang, E.L., 2003. The nightmare of the leader: the impact of deregulation on an oligopoly insurance market. Journal of Insurance Issues , 15–28.

- Wells et al. [2014] Wells, L.J., Camelio, J.A., Williams, C.B., White, J., 2014. Cyber-physical security challenges in manufacturing systems. Manufacturing Letters 2, 74–77. doi:10.1016/j.mfglet.2014.01.005.

- Woods et al. [2017] Woods, D., Agrafiotis, I., Nurse, J.R., Creese, S., 2017. Mapping the coverage of security controls in cyber insurance proposal forms. Journal of Internet Services and Applications 8, 1–13. doi:10.1186/s13174-017-0059-y.

- Woods and Böhme [2021] Woods, D.W., Böhme, R., 2021. SoK: Quantifying Cyber Risk, in: 2021 IEEE Symposium on Security and Privacy (SP), pp. 211–228. doi:10.1109/SP40001.2021.00053.

- Woods and Moore [2019] Woods, D.W., Moore, T., 2019. Does insurance have a future in governing cybersecurity? IEEE Security & Privacy 18, 21–27. doi:10.1109/MSEC.2019.2935702.

- Woods and Walter [2022] Woods, D.W., Walter, L., 2022. Reviewing estimates of cybercrime victimisation and cyber risk likelihood, in: 2022 IEEE European Symposium on Security and Privacy Workshops (EuroS&PW), IEEE. pp. 150–162. doi:10.1109/EuroSPW55150.2022.00021.

- Zhang et al. [2014] Zhang, L., Choffnes, D., Levin, D., Dumitraş, T., Mislove, A., Schulman, A., Wilson, C., 2014. Analysis of ssl certificate reissues and revocations in the wake of heartbleed, in: Proceedings of the 2014 Conference on Internet Measurement Conference, pp. 489–502. doi:10.1145/2663716.2663758.