A new class of nonparametric tests for second-order stochastic dominance based on the Lorenz P-P plot

Abstract

Given samples from two non-negative random variables, we propose a family of tests for the null hypothesis that one random variable stochastically dominates the other at the second order. Test statistics are obtained as functionals of the difference between the identity and the Lorenz P-P plot, defined as the composition between the inverse unscaled Lorenz curve of one distribution and the unscaled Lorenz curve of the other. We determine upper bounds for such test statistics under the null hypothesis and derive their limit distribution, to be approximated via bootstrap procedures. We then establish the asymptotic validity of the tests under relatively mild conditions and investigate finite sample properties through simulations. The results show that our testing approach can be a valid alternative to classic methods based on the difference of the integrals of the cumulative distribution functions, which require bounded support and struggle to detect departures from the null in some cases.

Keywords: Bootstrap, Lorenz curve, Stochastic order.

1 Introduction

The theory of stochastic orders deals with the problem of comparing pairs of random variables, or the corresponding distributions, with respect to concepts such as size, variability (or riskiness), shape, aging, or combinations of these aspects. The main notion in this context is generally referred to as the usual stochastic order or first-order stochastic dominance (FSD), which expresses the concept of one random variable being stochastically larger than the other (Shaked and Shantikumar, 2007). For this reason, FSD has important applications in all those fields in which “more” is preferable to “less”, clearly including economics. However, FSD is a restrictive criterion, and is rarely satisfied in real-world applications. This has pushed economic theorists to develop finer concepts, which formed the theory of stochastic dominance (SD), taking into account variability and shape, in addition to size (Hadar and Russell, 1969; Hanoch and Levy, 1969; Whitmore and Findlay, 1978; Fishburn, 1980; Muliere and Scarsini, 1989; Wang and Young, 1998). In this regard, the most commonly used SD relation is the second-order SD (SSD), expressing a preference for the random variable which is stochastically larger or at least less risky, therefore combining size and dispersion into a single preorder. This has applications in economics, finance, operations research, reliability, and many other fields in which decision-makers typically prefer larger or at least less uncertain outcomes.

Given a pair of samples from two unknown random variables of interest, statistical methods may be employed to establish whether such variables are stochastically ordered. In particular, we focus on a major problem in nonparametric statistics, that is testing the null hypothesis of dominance versus the alternative of non-dominance. About SSD, several procedures are available in the literature, some of which are described in the book of Whang (2019). We will now recall a few of these approaches. Davidson and Duclos (2000) proposed a test for SSD based on the distance between the integrals of the cumulative distribution functions (CDF). The problem with this test is that dominance is evaluated only on a fixed grid, which may lead to inconsistency. Barrett and Donald (2003) employed a similar approach, combined with bootstrap methods, to formulate a class of tests that are consistent under the assumption that the distributions under analysis are supported on a compact interval. Donald and Hsu (2016) leveraged a less conservative approach to determine critical values compared to Barrett and Donald (2003), avoiding the use of the least favourable configuration. Note that all the aforementioned papers deal more generally with finite-order SD, and then obtain SSD as a special case. Alternatively, other works focused on tests for the so-called Lorenz dominance, which is a scale-free version of SSD that applies to non-negative random variables. For example, Barrett et al. (2014) proposed a class of consistent tests for the Lorenz dominance that rely on the distance between empirical Lorenz curves. In this case, supports may be unbounded. Critical values are determined by approximating the limit distribution of a stochastic upper bound of the test statistic, similar to Barrett and Donald (2003). Sun and Beare (2021) used a different and less conservative bootstrap approach to improve the power of such tests, and established asymptotic properties under less restrictive distributional assumptions.

The main idea of this paper follows from noticing that some stochastic orders, including FSD, can be expressed and tested via the classic P-P plot, also referred to as the ordinal dominance curve (Hsieh and Turnbull, 1996; Schmid and Trede, 1996; Davidov and Herman, 2012; Beare and Moon, 2015; Tang et al., 2017; Beare and Clarke, 2022). Following a similar approach, we propose a new class of nonparametric tests for SSD between non-negative random variables, in which the test statistic is based on what we refer to as the Lorenz P-P plot (LPP), a kind of P-P plot based on unscaled Lorenz curves. More precisely, the LPP is obtained as the functional composition of the inverse unscaled Lorenz curve of one distribution and the unscaled Lorenz curve of the other. The key property of the LPP is that, under SSD, it does not exceed the identity function on the unit interval. Therefore, the LPP stands out as a promising tool for detecting deviations from the null hypothesis of SSD. Namely, any functional that quantifies the positive part of the difference between the identity and the LPP can be used to construct a test statistic. This gives rise to a whole class of tests, depending on the choice of the functional. The -values of such tests can then be computed via bootstrap procedures. In particular, we use a similar idea as in Barrett et al. (2014) to asymptotically bound the size of the test, and establish its consistency via the functional delta method. Note that the consistency of our family of tests is established without requiring a bounded support, which represents an advantage compared to classic methods based on integrals of CDFs. Moreover, our simulation studies show that our tests are often more reliable than the established KSB3 test by Barrett and Donald (2003), which may have problems detecting violations of the null hypothesis in some cases.

The LPP may also be used to define families of fractional-degree orders that are “between” FSD and SSD (or beyond SSD) by using a simple transformation. In this regard, we propose a method to define a continuum of SD relations, called transformed SD, in the spirit of the recent works by Müller et al. (2017), Lando and Bertoli-Barsotti (2020), and Huang et al. (2020). Interestingly, our tests can be easily adapted to this more general family of orders by simply transforming the samples through the same transformation used in the definition of transformed SD. In particular, FSD can be obtained as a limiting case, in which the empirical LPP of the transformed sample tends to the classic empirical P-P plot. This opens up the possibility of applying our class of tests to a wide family of stochastic orders.

The paper is organised as follows. Section 2 introduces the LPP and describes the idea behind the proposed family of tests. In Section 3, we propose an estimator of the LPP and study its properties. The empirical process associated with the LPP is investigated in Section 4, where we establish a weak convergence result that can be used to derive asymptotic properties of the tests. Namely, in Section 5, we establish bounded size under the null hypothesis and consistency under the alternative one, for both independent and paired samples. The extension to a family of fractional-degree orders is discussed in Section 6. In Section 7, we illustrate the finite sample properties of the tests through simulation studies, focusing on tests arising from sup-norm and integral-based functionals. Finally, Section 8 contains our concluding remarks. All the tables and proofs are reported in the Appendix.

2 Preliminaries

Throughout this paper, denotes a general CDF supported on the non-negative half line, with finite mean . In particular, we consider a pair of non-negative random variables and with CDFs and , respectively, and finite expectations. When and are absolutely continuous, we will denote their densities with and , respectively. Given that stochastic orders depend only on distribution functions, for any order relation we may write or interchangeably.

Let , for be the class of real-valued functions on the unit interval equipped with the norm , that is, for , and be the class of bounded real-valued functions equipped with the uniform norm . Moreover, let be the space of continuous real-valued functions on [0,1] also equipped with the uniform norm. Henceforth, “increasing” means “non-decreasing” and “decreasing” means “non-increasing”. Given a function , we denote with its positive part. If is increasing, denotes its right-continuos generalised inverse. Finally, denotes weak convergence, while denotes convergence in probability.

2.1 Stochastic dominance

We say that is larger than with respect to FSD, denoted as , if . Equivalently, if and only if for any increasing function . Within an economic framework, coherently with the expected-utility approach, one may assume that and represent monetary lotteries and is a utility function. Under this perspective, FSD represents all non-satiable decision-makers, that is all those with an increasing utility, and therefore can be seen as one of the strongest ordering principles. On the other hand, FSD has a limited range of applicability since, in real-world applications, CDFs often cross and hence distributions cannot be ordered using this criterion.

For this reason, weaker ordering relations have been introduced, among which the most important is the SSD. We say that is larger than with respect to SSD, denoted as , if . Equivalently, if and only if for any increasing and concave function . In economics, SSD generally represents all non-satiable and risk-averse decision-makers, expressing a preference for the random variable with larger values or smaller dispersion. For example, entails that and, in case of equality, and , where denotes the Gini coefficient. The above definitions may be generalised to -th order SD, denoted as , , and represented by the following integral inequality , where and , for .

Besides the classic definitions of SD discussed above, different notions — often including FSD and SSD as special or limiting cases — have been studied in the literature. Notable examples are the inverse SD (Muliere and Scarsini, 1989), which is based on recursive integration of the quantile function instead of the CDF, and coincides with classic SD at degrees 1 and 2, and also some fractional-degree SD relations that interpolate FSD and SSD (see, e.g., Müller et al., 2017), as discussed in more detail in Section 6.

2.2 The Lorenz P-P plot

The goal of this paper is to test the null hypothesis versus the alternative . This requires estimating some kind of distance between the situation of dominance and the situation of non-dominance. The classic solution (Davidson and Duclos, 2000; Barrett and Donald, 2003) is to construct test statistics based on an empirical version of the difference , which is expected to be large, at least at some point, if is false. However, the main issue with the usual definition of SSD, based on these integrated CDFs, is that these are unbounded in , so there are no uniformly consistent estimators for such integrals unless both distributions have bounded support. Not by chance, Barrett and Donald (2003) require that and have common bounded support , with finite, to derive consistent tests of stochastic dominance of order , including SSD. To avoid this limitation, we rely on an alternative but equivalent definition of SSD in terms of the unscaled Lorenz curve, which is always bounded. In particular, we observe that some stochastic orders may be alternatively expressed in terms of a Q-Q plot (Lando et al., 2023) or a P-P plot (Lehmann and Rojo, 1992). Similarly, SSD can be characterised by the modified P-P plot described below.

Let be the (left-continuous) quantile function of the CDF . The unscaled Lorenz curve of is defined as . The symbol is often used for the scaled version of the Lorenz curve, that is , while we use to denote the unscaled Lorenz curve, for the sake of simplicity. Also note that is increasing, convex and continuous in the unit interval. However, for technical reasons, we also let for . With this extension, the generalised inverse function is increasing, concave, and continuous in , while for .

Now, given the pair of CDFs and , consider the increasing continuous function

which takes values in , where denotes the minimum between two real numbers and . Letting , note that, if , then and for . Given some point , for , the graph of is a P-P plot with coordinates , which will be referred to as the Lorenz P-P plot (LPP). Within an economic framework, returns the probability given by to the average level of income corresponding to . In particular, if such a level cannot be reached under , we have . The LPP is scale-free, like the classic P-P plot; in particular, if and are multiplied by a positive scale factor, then remains unchanged.

To see how can be leveraged to characterize SSD, first recall that if and only if see, e.g., Shaked and Shantikumar (2007, Ch. 4). Such a relation can be equivalently expressed in terms of :

| (1) |

It is generally complicated to obtain an explicit expression of for parametric probabilistic models. Explicit calculations for the case of a Weibull versus a unit exponential distribution are provided in Example 1 below, while a graphical illustration is given in Figure 1. Differently, and more importantly for our testing purposes, the LPP can be computed quite easily in the empirical case, as discussed in Section 3.

Example 1.

Consider the Weibull distribution with , and the unit exponential distribution, , both supported on . In this case, the LPP has the following expression (see the Appendix for details):

where indicates the real part of a complex number, is the incomplete gamma function and is the Lambert function (Corless et al., 1996). Using the properties of SSD and the crossing conditions described in Shaked and Shantikumar (2007), it is easy to verify that if and only if and . Figure 1 shows the behaviour of when and .

2.3 Detecting deviations from SSD

Denote the identity function by . The representation of SSD in (1) can be leveraged to construct a test. In fact, is false if and only if is strictly positive at some point in the unit interval. Accordingly, departures from SSD can be detected by quantifying the positive part of the difference between and . This may be represented by some functional applied to the difference , with satisfying some desirable properties. In particular, we propose a family of test statistics obtained as empirical versions of the functionals

for , including

It can be shown that functionals of this type satisfy the following properties.

Proposition 1.

For every and for every ,

-

1.

If , then ;

-

2.

if , then ;

-

3.

if for some , then ;

-

4.

;

-

5.

, for any positive constant ;

-

6.

is convex.

-

7.

For any , .

Henceforth, we will denote simply by any general functional satisfying the above properties 1)–6). These properties determine a family of functionals which may be used to obtain consistent tests. In particular, properties 2) and 3) completely characterise SSD, in that if and only if , while if and only if . Differently, property 7) deals just with the class and shows that functionals of this kind measure the deviations from in a monotone way, that is, smaller (larger) values of downsize (emphasize) deviations, represented by the function . Proposition 1 generalises Lemma 2 of Barrett et al. (2014), which deals with the special cases of and . They introduced tests for the Lorenz dominance by applying to the difference between the (scaled) Lorenz curves, that is . One may extend their approach to SSD by considering (see, e.g., Zhuang et al., 2023). However, in this paper, we propose leveraging , which has some advantages over . For instance, is scale-free by properties of the LPP. On the contrary, if and are multiplied by a positive scale factor , then the difference between the unscaled Lorenz curves becomes . Moreover, whereas .

3 Estimation of the LPP

3.1 Sampling assumptions

Let and be i.i.d. random samples from and , respectively. As in Barrett et al. (2014), we will deal with two different sampling schemes: independent sampling and matched pairs. In the first scheme, the two samples and are independent of each other, and sample sizes and may differ. In contrast, in the matched-pairs scheme, and we have i.i.d. pairs drawn from a bivariate distribution with and as marginal CDFs. For both sampling schemes, we will consider the asymptotic regime in which , and . These assumptions are quite standard in the literature (see, e.g., Barrett and Donald, 2003) and imply that, as diverges, also goes to infinity with the same order.

3.2 Empirical LPP

The abovementioned random samples and yield the empirical CDFs

respectively. We denote the order statistics of rank from and with and , and their sample means with and , respectively. By the plugin method, the empirical counterparts of and are and , where for , is defined similarly, and is the inverse of . Coherently with our definition of , we let for . Note that coincides with the empirical unscaled Lorenz curve (Shorrocks, 1983), that is a piecewise linear function joining the points , , with .

Our definitions of and differ from the ones, based on step functions, in Csörgö et al. (2013):

where clearly . Note that and coincide at points , , and, likewise, and coincide at points , so these alternative empirical versions of and are clearly asymptotically equivalent.

According to the different empirical versions of and , we may obtain different estimators of . One may consider , which is a continuous piecewise linear function, or alternatively , which is a step function with jumps in the points , taking values in . In an economic framework, gives the relative frequency of observations from whose level of income is at most . Therefore, returns the relative frequency of observations from whose level of income is at most . Note that the value of at its “node” points does not generally coincide with the value of at its jump points. In this paper, we will use or as is more convenient, since the two are asymptotically equivalent. In fact, the sup-distance among and tends to zero as and diverge, as established in the following proposition.

Proposition 2.

For any , . Hence, as , .

In our asymptotic scenario, when we also have , hence the second part of Proposition 2 holds. Moreover, based on the strong uniform consistency of Lorenz curve estimators and their inverse functions (Goldie, 1977; Csörgö et al., 2013), we can prove the strong uniform consistency of and .

Proposition 3.

As , and a.s. and uniformly in .

4 Weak convergence of the LPP process

The empirical process associated with , henceforth referred to as the LPP process, may be useful to characterize the limit distribution of the test statistic under the null hypothesis of SSD. In this section, we study the asymptotic properties of such a process. Define the LPP process as

where , and let be the empirical counterpart of . For we know that when . In this case we have a.s., since also for and a.s. In other words, the interval contains no information. Accordingly, we are particularly interested in the asymptotic behaviour of restricted to , namely . Weak convergence of the LPP process can be derived under the following assumptions.

Assumption 1.

Both and are continuously differentiable with strictly positive density, and have a finite moment of order for some . Moreover, .

Assumption 2.

There exists some number such that .

The latter assumption does not represent a limitation in terms of applicability. In fact, if , one can apply the test to the shifted samples and , for some small , recalling that if and only if . In our simulations we set , obtaining results that are almost indistinguishable from those under . However, since the unscaled Lorenz curve is not translation invariant, the outcome of any test based on it (such as, e.g., Andreoli, 2018; Zhuang et al., 2023) may depend on the shift . Actually, in our experiments, we noted that larger values of may even improve the power of the test.

The following theorem establishes the weak convergence of under Assumptions 1–2, leveraging some recent results in Kaji (2018) that enable the derivation of the Hadamard differentiability of the map from CDFs to quantile functions. As discussed in Sun and Beare (2021, Section 2.4), this extends the applicability of earlier Hadamard differentiability conditions, based on stronger distributional assumptions such as bounded supports (Van der Vaart and Wellner, 1996, Lemma 3.9.23). Then, the weak convergence of follows by the functional delta method (Van der Vaart and Wellner, 1996, Sect. 3.9).

Let be a centered Gaussian element of with covariance function . Under the independent-sampling scheme, is the product copula, whereas, under the matched-pairs scheme, is the copula associated with the pair , . Now, let and . The random elements and are Brownian bridges that are independent under the independent-sampling scheme, but may be dependent under the matched-pairs one.

Theorem 1.

5 Asymptotic properties of the test

As discussed in Section 2.3, deviations from can be measured via the test statistic Intuitively, we reject if is large enough. However, since the null hypothesis is nonparametric, the main issue is how to determine the distribution of , or alternatively of an upper bound for , under . Following the approach of Barrett et al. (2014), it is easily seen that, under , the test statistic is dominated by , which therefore can be used to simulate -values or critical values via bootstrap, thus ensuring that the size of the test is asymptotically bounded by some arbitrarily small probability . By the continuous mapping theorem, is asymptotically distributed as , allowing us to derive large-sample properties of the test. The limit behaviour of under the null and the alternative hypotheses is established in the following lemma.

Lemma 1.

-

1.

Under , . Moreover, for any , the quantile of is positive, finite, and unique.

-

2.

Under , .

From a practical point of view, the limit distribution of under the null hypothesis may be approximated using a bootstrap approach, as discussed in the next subsection.

5.1 Bootstrap decision rule

Let us denote the bootstrap estimators of the empirical CDFs and as and , respectively:

where and are independent of the data and are drawn from a multinomial distribution according to the chosen sampling scheme. In particular, under the independent-sampling scheme, and are independently drawn from multinomial distributions with uniform probabilities over and trials, respectively. Under the matched-pairs scheme, we have drawn from the multinomial distribution with uniform probabilities over trials, which means that we sample (with replacement) pairs of data, from the pairs . Correspondingly, by applying the definitions in Section 2, we obtain the bootstrap estimators of the unscaled Lorenz curves, denoted with and , as well as the inverse , and we define . As is shown below, the random process has the same limiting distribution as . Therefore, bootstrap -values are determined by

and can be approximated, based on bootstrap replicates, by

where is the -th resampled realisation of . As usual, the test rejects if . The asymptotic behaviour of the test is addressed by the following proposition.

6 Extension to fractional-degree SD

An important topic in SD theory is represented by SD relations that are “between” FSD and SSD. This is motivated by the fact that FSD is a strong requirement, but, on the other hand, SSD corresponds to total risk-aversion, which is quite restrictive in some cases (Müller et al., 2017). There are different ways to define classes of orders that interpolate between FSD and SSD, and each leads to a different family of SD relations, typically parametrised by some real number that represents the strength of the dominance. The first attempt in this direction is ascribable to Fishburn (1980), who used fractional-degree integration to interpolate the classic -th order SD at all integer orders . More recently, Müller et al. (2017), Huang et al. (2020), and Lando and Bertoli-Barsotti (2020) proposed different parametrizations, with different interpretations and properties, which coincide with classic SD only at orders 1 and 2. In this section, we introduce a simple but very general family of fractional-degree orders, which have the advantage that they can be easily tested using the LPP method discussed earlier. Such a family can be defined as follows.

Let be the family of increasing absolutely continuous functions over the non-negative half line. Under an economic perspective, may be understood as a utility function, assigning values to monetary outcomes. For some , we say that dominates with respect to -transformed stochastic dominance (-TSD), and write , if . TSD has been studied by Meyer (1977), who denoted it as SSD with respect to , and by Huang et al. (2020), who focused on a particular parametric choice of . In fact, since -TSD represents SSD between the transformed random variables and , then it can be simply expressed through the LPP of and .

The behaviour of TSD clearly depends on the choice of . To understand this behaviour, let be two transformation functions defined on the same interval. Generalizing Chan et al. (1990), we say that is more convex than and write iff is convex. The following theorem shows that TSD can be equivalently expressed in terms of expected utilities, thus generalizing Theorem 1 of Huang et al. (2020).

Theorem 2.

if and only if , for every increasing utility such that

It is easy to see that, if and are twice differentiable, the condition is equivalent to , where is the Arrow-Pratt index of absolute risk aversion associated with the utility function . Moreover, the following general properties hold.

Theorem 3.

-

1.

If then ;

-

2.

if and only if .

Intuitively, the degree of convexity of the function determines the strength of the SD relation, and SSD is obtained by taking to be the identity function, whereas FSD is obtained when is infinitely “steep”.

Families of utility functions within can be obtained easily by composing the quantile function and the CDF of two absolutely continuous random variables. For example, one may consider the class of utility functions studied by Huang et al. (2020) and given by for . Since this paper deals with tests for non-negative random variables, we focus on a simpler choice, that is , with . Correspondingly, hereafter we denote the ordering relation with , thus yielding a continuum of SD relations that get stronger and stronger as grows. By Theorem 3, this order is characterised by those utility functions that have an Arrow-Pratt index larger than or equal to .

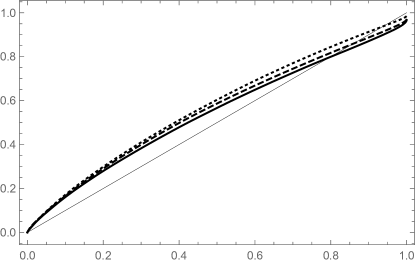

Since is equivalent to , a test for versus is readily obtained by applying our method to the LPP of the transformed random samples and . In particular, we consider the generalised LPP, given by , where and are the empirical (step-valued) unscaled Lorenz curves corresponding to the transformed samples , and . is a generalised P-P plot, in that it coincides with for . More interestingly, we prove that, as , tends to the classic P-P plot of the non-transformed samples, that is to , as depicted in Figure 2. In particular, one may always find some large enough such that the two P-P plots coincide, meaning that our tests may be also applied to FSD, expressed as . (tests for FSD based on the P-P plot have been studied, e.g., by Davidov and Herman (2012) and Beare and Clarke (2022)). In fact, this idea is coherent with the intuition that, for , the stochastic inequality reduces to , expressed as , as formally established in the following theorem.

Theorem 4.

-

1.

For , if and only if ;

-

2.

There exists some such that, for , the generalised LPP coincides with the classic P-P plot, that is, .

To test FSD as a limit case of TSD, one should choose a value of that ensures the result above. However, if is too large, computations may be difficult, depending on the precision of the software used. We recommend using , which corresponds to testing , for a good approximation of FSD.

7 Simulations

We perform numerical analyses to investigate the finite-sample properties of the proposed tests. In all simulations, we consider a significance level , and run experiments, with bootstrap replicates for each experiment. For simplicity, we set , so henceforth we will drop the subscript . Namely, we consider . The shift is set to , as discussed in Section 4. All computations have been performed in R, and the code is openly available at https://github.com/siriolegramanti/SSD.

In light of Proposition 2, instead of we use , which can be computed faster. Accordingly, we consider two different test statistics, namely and ; see Section 2.3. For , and can be rewritten, respectively, as

where . Our results are compared with those obtained from the tests of Barrett and Donald (2003), which represent the state of the art for SSD tests. In particular, Barrett and Donald (2003) propose three bootstrap-based tests, based on a least favourable configuration, denoted as KSB1, KSB2, and KSB3, which differ just for the bootstrap method employed to simulate the -values. We focus on KSB3 since it is based on the approach that is most similar to ours. Moreover, KSB3 seems to provide the best results compared to KSB1 and KSB2 as far as concerns SSD; see tables II-A and II-B of Barrett and Donald (2003). The -values of KSB3 were computed using a grid of evenly spaced values , where and are the smallest and the largest values in the pooled sample, respectively. As for the number of grid points, we set as in Barrett and Donald (2003), but we did not notice substantial differences in increasing .

Note that one pair of distributions gives rise to two different hypothesis tests. In fact, one may test versus , but also the reverse hypothesis test, denoted as versus . Except for the trivial case , if does not cross the identity we may have that is true while is false, or vice versa; differently, if crosses the identity, and are both false.

7.1 Size properties

To investigate the behaviour of the tests under the null hypothesis, we simulate samples from the Weibull family, denoted by , with CDF . Since the mean of a is , where , we let , for , and fix . All these distributions have mean 1, and in all these cases holds. Clearly, for we have , whereas the dominance of over becomes stronger, and more apparent, for larger values of .

The results in Tables 1, 2(a), 3(a) and 4(a) confirm that the proposed tests, both with and , behave as described in Proposition 4, part 1. Namely, the rejection rate tends to be bounded by under . More specifically, we observe that the rejection rate of the proposed tests tends to when (see Table 1), while it tends to 0 when strictly dominates (see Tables 2(a), 3(a) and 4(a)). The rejection rate for the KSB3 test by Barrett and Donald (2003) is also asymptotically bounded by but, when the dominance is stronger, it is still about for . For such a sample size, the rejection rate of both the proposed tests has already reached 0.

7.2 Power properties

We now investigate the behaviour of the tests under . In particular, we focus on cases in which is dominated by , so that should be rejected quite easily since is always below the identity. As we discuss in 7.2.1, the three tests considered behave quite similarly in such cases. We also focus on critical cases in which neither of the two distributions dominates the other, and therefore crosses the identity. In particular, the most critical situation for our class of tests is when is above the identity except for a small interval (see Figure 4(a)). The simulation results in 7.2.2 and 7.2.3 show that, in some of the most difficult cases, and KSB3 struggle to reject , whereas the proposed test stands out as the most reliable.

7.2.1 Weibull distribution

Using the same distributions as in Section 7.1, except for the case , we have that (strictly) and therefore . In these cases, is always above the identity. The results, reported in Tables 2(b), 3(b) and 4(b), show that the power of the tests increases with the sample size. In particular, seems to outperform for smaller sample sizes, while both the proposed and tests provide larger power compared to the KSB3 test by Barrett and Donald (2003).

7.2.2 Lognormal mixture vs. lognormal distribution

As a more critical example, we focus on a special case considered by Barrett and Donald (2003, Case 5). Here, is a mixture of lognormal distributions, namely , whereas . These CDFs cross multiple times, and also crosses the identity from below so that but also . In other words, both and are false. In the latter case, the null hypothesis is hard to reject, because crosses the identity from above, and it exceeds the identity just in a small subset of the unit interval. Note that Barrett and Donald (2003) just apply their test to versus , overlooking the reverse situation versus . As illustrated in Table 5, KSB3 seems to outperform our tests in detecting . In particular, exhibits quite a poor performance with the sample sizes considered (to increase its power up to 0.68, we need to reach ). Conversely, KSB3 has a really poor performance in rejecting , while the proposed and tests provide a large power in this critical setting.

7.2.3 Singh-Maddala Distribution

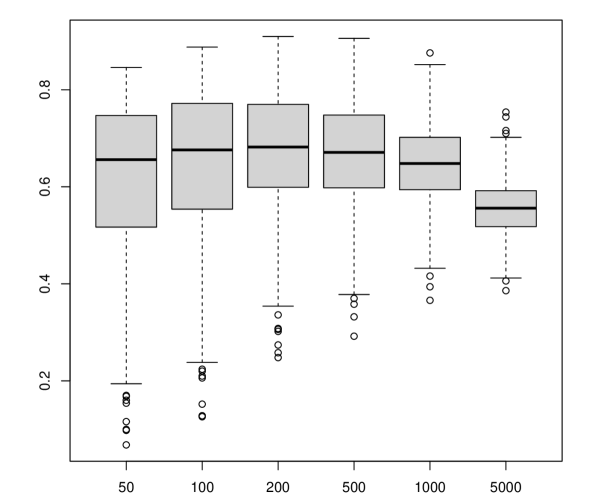

As a third case, let us consider the Singh-Maddala distribution, denoted as , with CDF . In all the following scenarios, the scale parameter is set to 1 and hence omitted, while the two shape parameters and vary. As in Section 7.2.2, we generate scenarios in which crosses the identity. In particular, we target the worst-case scenarios for our proposed tests, to investigate their limitations, by setting and , for . As shown in Figure 3, larger values of correspond to cases in which it is harder to detect the difference between and the identity, especially using . Tables 6(a), 7(a) and 8(a) show that KSB3 delivers larger power compared to our tests in such critical cases. In particular, while the performance of significantly improves for larger samples and lower , the power of is constantly close to 0, even for and . In light of part 7) of Proposition 1, this is due to the fact that downsizes the deviations from the null, which are hardly classified as “large”, at least with the sample sizes considered. Indeed, the -values of tend to decrease and to be less variable as grows, coherently with Proposition 4 (see Figure 4(a)). This suggests that the power of may eventually tend to 1 for larger samples. However, when applied to the reverse hypotheses and , the proposed tests and exhibit good performance, with rejection rates significantly increasing with ; see Tables 6(b), 7(b) and 8(b). On the contrary, KSB3 struggles to detect non-dominance and its power remains close to , even for large samples.

7.3 Paired samples

To simulate dependent samples we first draw a sample from a bivariate normal distribution, with standard marginals and correlation coefficient . Then, by transforming the data via the standard normal CDF , we obtain a dependent sample from a bivariate distribution with uniform marginals and . Finally, a dependent sample from a bivariate distribution with margins and is obtained as . In particular, we consider . As in the previous subsections, we compare our results with those of KSB3. Note that, although Barrett and Donald (2003) assume independence to prove the consistency properties of such a test, our simulations reveal that KSB3 exhibits a good performance even in the dependent case.

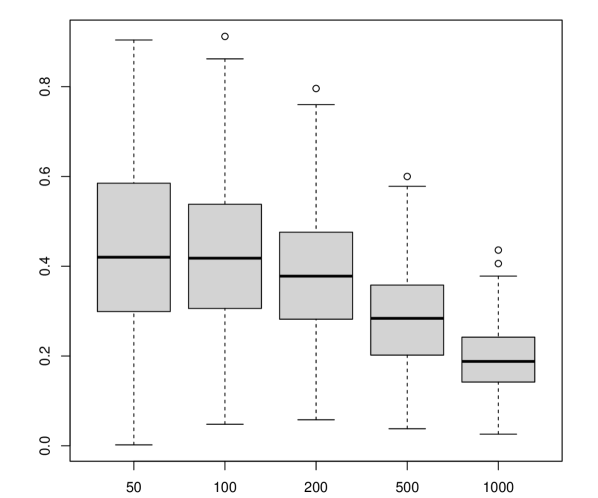

In this paired setting, we consider the same Singh-Maddala distributions as in Section 7.2.3, focusing on the cases and . The results, reported in Tables 9–14, confirm the ones reported in the previous tables, although it can be seen that a stronger dependence generally leads to larger rejection rates. Even , which was struggling with independent Singh-Maddala samples, shows a more evident decreasing trend in the empirical distribution of the -values when samples are paired (see Figure 4(b)).

7.4 Test for FSD

As discussed in Section 6, our methodology also allows to test TSD, including an approximation of FSD, obtained as with . We then apply the method described in Section 6 to the same Singh-Maddala distributions studied in Section 7.2.3. Since in these cases, SSD does not hold, we have that, a fortiori, the FSD null hypothesis, denoted as , is also false. This hypothesis can be tested using a sufficiently large value of , as discussed in Section 6. In particular, we set , which corresponds to approximating the FSD null hypothesis, , with . Our method is compared with the FSD version of the KSB3 test described in Barrett and Donald (2003). In contrast to the KSB3 test for SSD, this latter test may be shown to be consistent even in the case when the distributions have unbounded supports.

All the tests considered tend to provide a larger simulated power compared to the SSD case. This is logical since FSD is more stringent than SSD, and therefore, for the same pairs of distributions, it is easier to detect violations of FSD rather than of SSD. The results in Tables 15–17 show that KSB3 tends to provide larger power than our and tests under . On the contrary, under the reverse alternative , KSB3 exhibits a worse performance, also showing an unexpected behaviour, in that its rejection rates first increase and then decrease as grows.

8 Concluding remarks

In this paper, we proposed leveraging the LPP as a new tool to detect deviations from SSD in the case of non-negative random variables. The same approach can be used to test TSD, hence including FSD as a limit case. The asymptotic properties in Section 5 and the numerical results in Section 7 show that our family of tests can be a valid alternative to the established tests based on the difference between integrals of CDFs, such as the tests in Barrett and Donald (2003). In particular, the KSB3 test is outperformed by our proposed sup-based test in most of the cases analysed, sometimes with a remarkable gap.

Among the two tests proposed, our simulations reveal that the sup-based test is also overall more reliable than the integral-based , which has lower power in the most critical cases. However, both tests may be useful. In fact, in light of Proposition 1 part 7), and according to our numerical results in Section 7.2.3 and Section 7.2.2, performs better than when deviations from are subtle, while provides higher power than when deviations are more apparent. Therefore, in applications, it could be useful to use both tests and compare the -values. It is also worth noting that our proposed tests seem to improve in terms of power when the samples are dependent.

In general, the advantage of using the LPP instead of integrals of CDFs is that it can be approximated uniformly, which allows to establish asymptotic properties without requiring bounded support; moreover, the LPP has a different sensitivity in detecting violations of SSD, compared to other methods. Finally, the power of our tests may be improved further by combining the same proposed test statistics with different and less conservative bootstrap schemes. The latter represents an interesting direction for future work.

Appendix A: Tables

| KSB3 | |||

|---|---|---|---|

| 50 | 0.09 | 0.15 | 0.10 |

| 100 | 0.10 | 0.15 | 0.11 |

| 200 | 0.12 | 0.15 | 0.11 |

| 500 | 0.09 | 0.10 | 0.09 |

| 1000 | 0.08 | 0.09 | 0.09 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.08 | 0.10 | 0.12 |

| 100 | 0.04 | 0.06 | 0.11 |

| 200 | 0.03 | 0.02 | 0.10 |

| 500 | 0.02 | 0.00 | 0.11 |

| 1000 | 0.00 | 0.00 | 0.09 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.19 | 0.31 | 0.12 |

| 100 | 0.22 | 0.29 | 0.11 |

| 200 | 0.27 | 0.36 | 0.11 |

| 500 | 0.50 | 0.54 | 0.12 |

| 1000 | 0.72 | 0.72 | 0.18 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.04 | 0.05 | 0.12 |

| 100 | 0.04 | 0.02 | 0.13 |

| 200 | 0.02 | 0.00 | 0.12 |

| 500 | 0.01 | 0.00 | 0.11 |

| 1000 | 0.00 | 0.00 | 0.10 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.29 | 0.45 | 0.14 |

| 100 | 0.37 | 0.50 | 0.13 |

| 200 | 0.56 | 0.66 | 0.15 |

| 500 | 0.87 | 0.88 | 0.26 |

| 1000 | 0.99 | 0.99 | 0.48 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.03 | 0.03 | 0.12 |

| 100 | 0.02 | 0.00 | 0.12 |

| 200 | 0.01 | 0.00 | 0.11 |

| 500 | 0.01 | 0.00 | 0.11 |

| 1000 | 0.00 | 0.00 | 0.08 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.41 | 0.57 | 0.16 |

| 100 | 0.56 | 0.67 | 0.18 |

| 200 | 0.81 | 0.85 | 0.28 |

| 500 | 0.99 | 0.99 | 0.51 |

| 1000 | 1.00 | 1.00 | 0.88 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.25 | 0.17 | 0.43 |

| 100 | 0.43 | 0.15 | 0.59 |

| 200 | 0.58 | 0.10 | 0.74 |

| 500 | 0.89 | 0.08 | 0.98 |

| 1000 | 0.99 | 0.08 | 1.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.16 | 0.34 | 0.03 |

| 100 | 0.17 | 0.29 | 0.01 |

| 200 | 0.26 | 0.30 | 0.01 |

| 500 | 0.51 | 0.41 | 0.01 |

| 1000 | 0.84 | 0.68 | 0.02 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.02 | 0.00 | 0.38 |

| 100 | 0.04 | 0.00 | 0.52 |

| 200 | 0.05 | 0.00 | 0.63 |

| 500 | 0.11 | 0.00 | 0.88 |

| 1000 | 0.23 | 0.00 | 0.97 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.56 | 0.77 | 0.06 |

| 100 | 0.76 | 0.87 | 0.03 |

| 200 | 0.97 | 0.98 | 0.02 |

| 500 | 1.00 | 1.00 | 0.01 |

| 1000 | 1.00 | 1.00 | 0.03 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.07 | 0.01 | 0.51 |

| 100 | 0.10 | 0.01 | 0.66 |

| 200 | 0.16 | 0.00 | 0.83 |

| 500 | 0.44 | 0.00 | 0.96 |

| 1000 | 0.81 | 0.00 | 1.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.43 | 0.68 | 0.04 |

| 100 | 0.63 | 0.77 | 0.01 |

| 200 | 0.92 | 0.94 | 0.00 |

| 500 | 1.00 | 1.00 | 0.00 |

| 1000 | 1.00 | 1.00 | 0.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.16 | 0.05 | 0.64 |

| 100 | 0.24 | 0.03 | 0.79 |

| 200 | 0.45 | 0.01 | 0.92 |

| 500 | 0.85 | 0.01 | 0.99 |

| 1000 | 0.99 | 0.01 | 1.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.27 | 0.52 | 0.03 |

| 100 | 0.48 | 0.61 | 0.00 |

| 200 | 0.77 | 0.83 | 0.01 |

| 500 | 0.99 | 0.99 | 0.00 |

| 1000 | 1.00 | 1.00 | 0.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.05 | 0.01 | 0.45 |

| 100 | 0.04 | 0.00 | 0.54 |

| 200 | 0.08 | 0.00 | 0.68 |

| 500 | 0.17 | 0.00 | 0.90 |

| 1000 | 0.32 | 0.00 | 0.99 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.64 | 0.84 | 0.07 |

| 100 | 0.87 | 0.94 | 0.03 |

| 200 | 1.00 | 1.00 | 0.02 |

| 500 | 1.00 | 1.00 | 0.01 |

| 1000 | 1.00 | 1.00 | 0.04 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.04 | 0.01 | 0.49 |

| 100 | 0.05 | 0.00 | 0.59 |

| 200 | 0.09 | 0.00 | 0.74 |

| 500 | 0.20 | 0.00 | 0.94 |

| 1000 | 0.44 | 0.00 | 1.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.75 | 0.93 | 0.07 |

| 100 | 0.94 | 0.99 | 0.04 |

| 200 | 1.00 | 1.00 | 0.02 |

| 500 | 1.00 | 1.00 | 0.02 |

| 1000 | 1.00 | 1.00 | 0.06 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.03 | 0.00 | 0.58 |

| 100 | 0.08 | 0.00 | 0.70 |

| 200 | 0.13 | 0.00 | 0.87 |

| 500 | 0.32 | 0.00 | 0.99 |

| 1000 | 0.72 | 0.00 | 1.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.92 | 0.99 | 0.07 |

| 100 | 1.00 | 1.00 | 0.04 |

| 200 | 1.00 | 1.00 | 0.04 |

| 500 | 1.00 | 1.00 | 0.05 |

| 1000 | 1.00 | 1.00 | 0.15 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.19 | 0.05 | 0.70 |

| 100 | 0.28 | 0.02 | 0.80 |

| 200 | 0.51 | 0.01 | 0.92 |

| 500 | 0.88 | 0.01 | 0.99 |

| 1000 | 1.00 | 0.02 | 0.99 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.34 | 0.58 | 0.03 |

| 100 | 0.56 | 0.71 | 0.01 |

| 200 | 0.89 | 0.91 | 0.01 |

| 500 | 1.00 | 1.00 | 0.00 |

| 1000 | 1.00 | 1.00 | 0.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.21 | 0.05 | 0.76 |

| 100 | 0.38 | 0.01 | 0.85 |

| 200 | 0.64 | 0.01 | 0.95 |

| 500 | 0.96 | 0.01 | 0.99 |

| 1000 | 1.00 | 0.03 | 0.99 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.42 | 0.68 | 0.03 |

| 100 | 0.69 | 0.84 | 0.00 |

| 200 | 0.96 | 0.97 | 0.00 |

| 500 | 1.00 | 1.00 | 0.00 |

| 1000 | 1.00 | 1.00 | 0.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.28 | 0.04 | 0.86 |

| 100 | 0.57 | 0.01 | 0.93 |

| 200 | 0.85 | 0.02 | 0.98 |

| 500 | 1.00 | 0.02 | 0.99 |

| 1000 | 1.00 | 0.09 | 1.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.61 | 0.88 | 0.02 |

| 100 | 0.91 | 0.97 | 0.00 |

| 200 | 1.00 | 1.00 | 0.00 |

| 500 | 1.00 | 1.00 | 0.00 |

| 1000 | 1.00 | 1.00 | 0.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.11 | 0.14 | 0.24 |

| 100 | 0.22 | 0.16 | 0.41 |

| 200 | 0.44 | 0.21 | 0.64 |

| 500 | 0.86 | 0.42 | 0.92 |

| 1000 | 1.00 | 0.82 | 0.95 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.03 | 0.29 | 0.19 |

| 100 | 0.10 | 0.38 | 0.19 |

| 200 | 0.31 | 0.53 | 0.14 |

| 500 | 0.92 | 0.92 | 0.05 |

| 1000 | 1.00 | 1.00 | 0.00 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.08 | 0.09 | 0.15 |

| 100 | 0.11 | 0.06 | 0.24 |

| 200 | 0.20 | 0.05 | 0.39 |

| 500 | 0.64 | 0.10 | 0.85 |

| 1000 | 0.96 | 0.29 | 0.97 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.08 | 0.44 | 0.32 |

| 100 | 0.19 | 0.56 | 0.44 |

| 200 | 0.52 | 0.80 | 0.52 |

| 500 | 0.99 | 0.99 | 0.39 |

| 1000 | 1.00 | 1.00 | 0.22 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.03 | 0.02 | 0.07 |

| 100 | 0.04 | 0.02 | 0.13 |

| 200 | 0.09 | 0.01 | 0.24 |

| 500 | 0.36 | 0.01 | 0.60 |

| 1000 | 0.77 | 0.02 | 0.92 |

| KSB3 | |||

|---|---|---|---|

| 50 | 0.10 | 0.59 | 0.47 |

| 100 | 0.30 | 0.70 | 0.63 |

| 200 | 0.74 | 0.91 | 0.78 |

| 500 | 0.99 | 1.00 | 0.78 |

| 1000 | 1.00 | 1.00 | 0.67 |

Appendix B: Proofs

Calculations of Example 1..

The unscaled Lorenz curve of is

while

It is well known (e.g. Goldie, 1977) that can be expressed as , with

Noting that for any , this function can be inverted using the Lambert function (Corless et al., 1996), that is . Accordingly,

Finally, by composition, we obtain the expression of in Example 1. ∎

Proof of Proposition 1..

-

1.

This follows from the properties of the norm.

-

2.

If then which implies and therefore by monotonicity of integrals.

-

3.

The proof is the same as in Lemma 2 of Barrett et al. (2014) and relies on the fact that .

-

4.

Minkowski’s inequality implies that, for some pair of functions , , so that , and similarly, , therefore, . Then

where the second inequality follows from the fact that, for every , .

-

5.

The proof follows from absolute homogeneity of the norm.

-

6.

Let . By convexity of the function , Minkowski’s inequality, and absolute homogeneity of the norm,

-

7.

This follows from basic properties of norms.

∎

Proof of Proposition 2..

can be expressed as

For the first summand, which is the difference between two step functions, we have for every , since for every . Moreover, for , while, within each interval , the difference is bounded above the height of the jumps of , that is, . For the latter summand, , since clearly is the linear interpolator of the jump points of the step function . Hence, the result follows. ∎

Proof of Proposition 3..

As proved in Theorem 10.1 and Theorem 13.2 of Csörgö et al. (2013), and converge strongly and uniformly to and , respectively. Since is uniformly continuous in and almost surely, we obtain that almost surely. Then, for every ,

Since both terms in the right-hand side converge to 0 with probability 1, we obtain that converges strongly and uniformly to in . By Proposition 2, for and , therefore the same property is satisfied by . ∎

Proof of Theorem 1..

Let be the space of maps with and , and the norm . As shown by Kaji (2018), under assumption i), the map , from CDFs to quantile functions, is Hadamard differentiable at , tangentially to the set of continuous functions in , with derivative map

The linear map coincides with its Hadamard derivative. Accordingly, by the chain rule (Van der Vaart and Wellner, 1996, Lemma 3.9.3), the composition map is also Hadamard differentiable at tangentially to , with derivative

Now, observe that

as shown in Lemma 5.1 of Sun and Beare (2021). Then, the functional delta method (Van der Vaart and Wellner, 1996, Theorem 3.9.13) implies the joint weak convergence

| (2) |

Now, consider the process , for . The LC is increasing and continuous on , therefore the inverse function is increasing and continuous on , moreover the derivative is strictly positive in the unit interval (note that assumption ii) entails that ). Then, by the inverse map theorem (Van der Vaart and Wellner, 1996, Lemma 3.9.20) the map is Hadamard-differentiable at , tangentially to the set of bounded functions on , with derivative

Since and , by (2) and the functional delta method, the above result implies

| (3) |

where is defined as

Now, consider the maps , and the composition map defined by . Recall that the Hadamard derivative of is , and is uniformly norm-bounded, since , therefore we can apply Lemma 3.2.27 of Van der Vaart and Wellner (1996), which establishes that is Hadamard differentiable at , tangentially to the set , where is the family of uniformly continuous functions on , with derivative

Now, since , using (3), the functional delta method and the Hadamard differentiability of the composition map give

which implies the statement since . ∎

Proof of Lemma 1..

Bear in mind that is a mean-zero Gaussian process since it is obtained by integrating and normalizing Gaussian processes. Under , , hence

where the last step follows from the continuous mapping theorem, since the map satisfies , where are continuous functions on the unit interval, as proved in Lemma 2 of Barrett et al. (2014). The quantile of the distribution of is positive, finite, and unique because is a mean zero Gaussian process, so the proof follows by the same arguments used in the proof of Lemma 4 in Barrett et al. (2014). Since, by Proposition 3, converges strongly and uniformly to , under we have . Finally, multiplying by , we obtain the second result. ∎

Proof of Proposition 4..

As proved in Lemma 5.2 of Sun and Beare (2021),

where denotes weak convergence conditional on the data a.s., see (Kosorok, 2008, p.20). The proof of Theorem 1 establishes the Hadamard-differentiability of the maps and , so that the functional delta method for the bootstrap implies

where denotes weak convergence conditional on the data in probability (see Kosorok, 2008, p.20). Using the Hadamard differentiability of the composition map , the functional delta method for bootstrap implies , which entails that by the continuous mapping theorem. The test rejects the null hypothesis if the test statistic exceeds the bootstrap threshold , but the weak convergence result implies . Hence, Lemma 1 yields the result. ∎

Proof of Theorem 2..

Integrating by substitution, we can see that if and only if , since , and similarly for . Hence, by setting , the proof follows from the classic characterisation of SSD, since , for any increasing concave function . ∎

Proof of Theorem 3..

Point 1) follows from the fact that implies , because the composition is concave by construction. The “only if” part of point 2) is trivial. The “if” part follows from the characterisation of FSD, taking into account that the equivalent condition of Theorem 2, that is, , for every , implies that such an inequality holds just for every increasing . Since any increasing function may be approximated by a sequence of functions in , we have . ∎

Proof of Theorem 4..

1. con be expressed as

| (4) |

Integrating by parts and by substitution, we obtain that, for both and ,

Hence,

by the Lebesgue dominated convergence theorem, recalling that as . Now, it is readily seen that if and only if for any , which implies the result.

2. Let and be ordered realisations from and , respectively. By properties of the power function, there exists some number such that, for , if and only if . In fact,

Accordingly, for any and , returns if , which coincides with the P-P plot . ∎

Funding

This research was supported by the Italian funds ex-MURST60%. T.L. was also supported by the Czech Science Foundation (GACR) under the project 20-16764S and by VŠB-TU Ostrava (SGS project SP2021/15).

Conflict of interest: None declared.

References

- Andreoli (2018) Andreoli, F., 2018. Robust inference for inverse stochastic dominance. Journal of Business & Economic Statistics 36, 146–159.

- Barrett and Donald (2003) Barrett, G.F., Donald, S.G., 2003. Consistent tests for stochastic dominance. Econometrica 71, 71–104.

- Barrett et al. (2014) Barrett, G.F., Donald, S.G., Bhattacharya, D., 2014. Consistent nonparametric tests for Lorenz dominance. Journal of Business & Economic Statistics 32, 1–13.

- Beare and Clarke (2022) Beare, B.K., Clarke, J.D., 2022. Modified Wilcoxon-Mann-Whitney tests of stochastic dominance. arXiv:2210.08892 .

- Beare and Moon (2015) Beare, B.K., Moon, J.M., 2015. Nonparametric tests of density ratio ordering. Econometric Theory 31, 471–492.

- Chan et al. (1990) Chan, W., Proschan, F., Sethuraman, J., 1990. Convex-ordering among functions, with applications to reliability and mathematical statistics. Lecture Notes-Monograph Series , 121–134.

- Corless et al. (1996) Corless, R.M., Gonnet, G.H., Hare, D.E., Jeffrey, D.J., Knuth, D.E., 1996. On the Lambert W function. Advances in Computational mathematics 5, 329–359.

- Csörgö et al. (2013) Csörgö, M., Csörgö, S., Horváth, L., 2013. An asymptotic theory for empirical reliability and concentration processes. volume 33. Springer Science & Business Media.

- Davidov and Herman (2012) Davidov, O., Herman, A., 2012. Ordinal dominance curve based inference for stochastically ordered distributions. Journal of the Royal Statistical Society: Series B (Statistical Methodology) 74, 825–847.

- Davidson and Duclos (2000) Davidson, R., Duclos, J.Y., 2000. Statistical inference for stochastic dominance and for the measurement of poverty and inequality. Econometrica 68, 1435–1464.

- Donald and Hsu (2016) Donald, S.G., Hsu, Y.C., 2016. Improving the power of tests of stochastic dominance. Econometric Reviews 35, 553–585.

- Fishburn (1980) Fishburn, P.C., 1980. Continua of stochastic dominance relations for unbounded probability distributions. Journal of Mathematical Economics 7, 271–285.

- Goldie (1977) Goldie, C.M., 1977. Convergence theorems for empirical Lorenz curves and their inverses. Advances in Applied Probability 9, 765–791.

- Hadar and Russell (1969) Hadar, J., Russell, W.R., 1969. Rules for ordering uncertain prospects. The American Economic Review 59, 25–34.

- Hanoch and Levy (1969) Hanoch, G., Levy, H., 1969. The efficiency analysis of choices involving risk. The Review of Economic Studies 36, 335–346.

- Hsieh and Turnbull (1996) Hsieh, F., Turnbull, B.W., 1996. Nonparametric and semiparametric estimation of the receiver operating characteristic curve. Annals of Statistics 24, 25–40.

- Huang et al. (2020) Huang, R.J., Tzeng, L.Y., Zhao, L., 2020. Fractional degree stochastic dominance. Management Science 66, 4630–4647.

- Kaji (2018) Kaji, T., 2018. Essays on asymptotic methods in econometrics. Ph.D. thesis. Massachusetts Institute of Technology.

- Kosorok (2008) Kosorok, M.R., 2008. Introduction to empirical processes and semiparametric inference. Springer.

- Lando et al. (2023) Lando, T., Arab, I., Oliveira, P.E., 2023. Transform orders and stochastic monotonicity of statistical functionals. Scandinavian Journal of Statistics 50, 1183–1200.

- Lando and Bertoli-Barsotti (2020) Lando, T., Bertoli-Barsotti, L., 2020. Distorted stochastic dominance: A generalized family of stochastic orders. Journal of Mathematical Economics 90, 132–139.

- Lehmann and Rojo (1992) Lehmann, E.L., Rojo, J., 1992. Invariant directional orderings. Annals of Statistics 20, 2100–2110.

- Meyer (1977) Meyer, J., 1977. Second degree stochastic dominance with respect to a function. International Economic Review , 477–487.

- Muliere and Scarsini (1989) Muliere, P., Scarsini, M., 1989. A note on stochastic dominance and inequality measures. Journal of Economic Theory 49, 314–323.

- Müller et al. (2017) Müller, A., Scarsini, M., Tsetlin, I., Winkler, R.L., 2017. Between first-and second-order stochastic dominance. Management Science 63, 2933–2947.

- Schmid and Trede (1996) Schmid, F., Trede, M., 1996. Testing for first-order stochastic dominance: a new distribution-free test. Journal of the Royal Statistical Society Series D: The Statistician 45, 371–380.

- Shaked and Shantikumar (2007) Shaked, M., Shantikumar, J.G., 2007. Stochastic Orders. Springer, New York.

- Shorrocks (1983) Shorrocks, A.F., 1983. Ranking income distributions. Economica 50, 3–17.

- Sun and Beare (2021) Sun, Z., Beare, B.K., 2021. Improved nonparametric bootstrap tests of Lorenz dominance. Journal of Business & Economic Statistics 39, 189–199.

- Tang et al. (2017) Tang, C.F., Wang, D., Tebbs, J.M., 2017. Nonparametric goodness-of-fit tests for uniform stochastic ordering. Annals of statistics 45, 2565.

- Van der Vaart and Wellner (1996) Van der Vaart, A., Wellner, J., 1996. Weak convergence and empirical processes: with applications to statistics. Springer Science & Business Media.

- Wang and Young (1998) Wang, S.S., Young, V.R., 1998. Ordering risks: Expected utility theory versus Yaari’s dual theory of risk. Insurance: Mathematics and Economics 22, 145–161.

- Whang (2019) Whang, Y.J., 2019. Econometric analysis of stochastic dominance: Concepts, methods, tools, and applications. Cambridge University Press.

- Whitmore and Findlay (1978) Whitmore, G., Findlay, M., 1978. Stochastic Dominance: An Approach to Decision-Making Under Risk. Heath, Lexington, MA.

- Zhuang et al. (2023) Zhuang, W., Yao, S., Qiu, G., 2023. Test of dominance relations based on kernel smoothing method. Journal of Nonparametric Statistics , 1–24.

Corresponding Author. Tommaso Lando, e-mail: tommaso.lando@unibg.it