The fiscal implications of stringent climate policy

Abstract

Stringent climate policy compatible with the targets of the 2015 Paris Agreement would pose a substantial fiscal challenge. Reducing carbon dioxide emissions by 95% or more by 2050 would raise 7% (1-17%) of GDP in carbon tax revenue, half of current, global tax revenue. Revenues are relatively larger in poorer regions. Subsidies for carbon dioxide sequestration would amount to 6.6% (0.3-7.1%) of GDP. These numbers are conservative as they were estimated using models that assume first-best climate policy implementation and ignore the costs of raising revenue. The fiscal challenge rapidly shrinks if emission targets are relaxed.

Keywords: climate policy

JEL codes: H20, Q54

url]http://www.ae-info.org/ae/Member/Tol_Richard

1 Introduction

Much has been written about how to reduce greenhouse gas emissions and how much that would cost (see Riahi et al., 2022, for a review of recent studies) but there is little about the implications for the public finances. This is an odd omission. Rapid emission reduction requires a major overhaul of the energy sector and energy-intensive activities (IEA, 2021). The energy transition will not just affect energy but everything it touches, including tax revenue and government spending. IEA (2022), for instance, reports that investment in the energy sector needs to double between 2020 and 2030, from 2% to 4% of GDP. This paper uses results from commonly-used integrated assessment models to study the impact of stringent climate policy on tax revenue and public expenditure, revealing the potential size of the carbon industry in the process.

The climate economics literature has focused on how best to reduce emissions (Dubash et al., 2022) and what that would cost (Riahi et al., 2022). Much attention has been paid to the technical feasibility of rapid emission reduction (Clarke et al., 2009) and to the required transition of energy, agriculture, and transport. The accompanying changes in the public sector have been largely ignored, with one exception, namely how to best use the revenues from a carbon tax (or permit auction). Using such revenue to reduce other taxes, which hold back economic growth or job creation, could result in a double dividend (Goulder, 1995) or, if the income distribution improves too, a triple dividend (van Heerden et al., 2006); Distefano and D’Alessandro (2023) explore a quadruple dividend, adding public debt to the mix.

The multiple-dividend literature is focused on the structure of tax revenue, but ignores its size. Indeed, for analytical clarity, these papers assume budget-neutrality. Belfiori and Rezai (2023) show that revamped consumption, energy, and income taxes can be a first-best policy, correcting the climate externality without an explicit Pigou tax. However, Tol (2012a) argues that stringent climate policy may well require an overall increase in tax revenue and so lead to an expansion of the state.

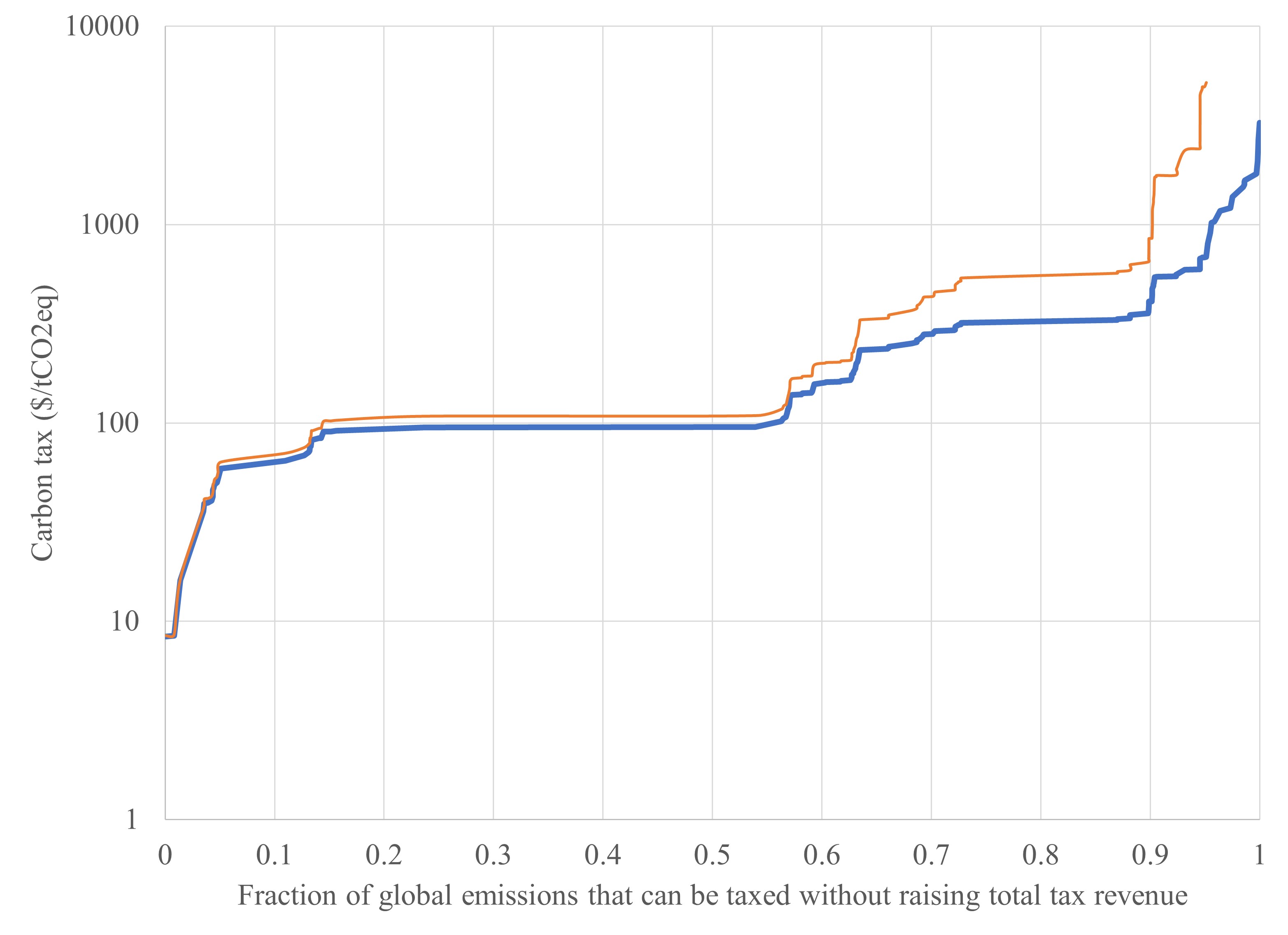

Tol (2012a) defines the Leviathan tax as that carbon tax whose revenue could replace the revenue of all other taxes combined.222Note that no assumptions are made on the desirable level of total tax revenue. Figure 1 shows the Leviathan tax for 2019. It is calculated as the greenhouse gas emission intensity of the economy—emissions over output—times the tax revenue as a share of GDP. Data are available from the World Bank for 145 countries. Figure 1 ranks these countries by their Leviathan tax, and plots this against their share in global emissions. The Central African Republic has the lowest Leviathan tax: A carbon tax of $8/tCO2eq would be budget-neutral if all other taxes are abolished. Sweden has the highest Leviathan tax: $3,263/tCO2eq. The global average is $242/tCO2eq

The Sixth Assessment Report of Working Group III of the Intergovernmental Panel on Climate Change (Riahi et al., 2022) reports that, according to the median model, a carbon tax of around $100/tCO2eq is needed in 2030 to have a good chance of meeting the 2target of the 2015 Paris Agreement. India’s Leviathan tax (for 2019) is $95/tCO2eq, China’s $96/tCO2eq, and Indonesia’s $102/tCO2eq. Stringent climate policy is therefore not just a technical and economic challenge, but a fiscal challenge too.

Fiscal problems would arise long before the Leviathan tax is reached. Besley and Persson (2013) show that fiscal capacity has grown slowly and that the structure of tax revenues has developed gradually. Rapid, massive change in tax collection is unprecedented and would be difficult, or so the historical record suggests. Climate policy would require two tax revolutions. First, taxes should shift to carbon from everything else to drive emissions to zero—and then taxes would have to shift back to maintain tax revenue.

Dowlatabadi (2000) was perhaps the first to warn about possible tax revolts (Burg, 2004, Keen and Slemrod, 2021) in the context of climate policy. One example is the 2018 protests by les gilets jeunes in France in response to a modest carbon tax on transport fuels (Stoll and Mehling, 2021). The carbon taxes needed to meet the Paris targets are not modest—and they will need to apply in countries that are not as used to high taxes as France is.

Throughout the paper, I write about climate policy as if a carbon tax were the sole policy instrument. The reason for this is that the models I rely on make this assumption. Although the optimal climate policy is a carbon tax, a uniform carbon tax, and nothing but a carbon tax (Tol, 2023b), the bulk of past and present climate policies rely on other instruments. There is no reason to assume future climate policy will be any different.

Some of the insights carry over. Cap-and-trade with auctioned permits behaves much like a carbon tax, the key difference being that permit prices fluctuate and taxes do not. The revenue of permit auctions can be used to reduce taxes.

If permits are grandparented instead of auctioned, climate policy is like a carbon tax (at the margin) plus lump-sum capital subsidies for the recipients of free permits. These capital subsidies pose no burden on the fiscal budget as the government costlessly creates the permits before giving them away. In this case, taxes cannot be reduced. Instead, the public sector expands.

Subsidies, another popular policy instrument, are negative taxes. Other taxes would need to go up substantially if subsidies are used to reduce emissions at the required scale.

Any technical standard has an equivalent tax (Baumol and Oates, 1971). If standards are the policy instrument of choice—as they often are—the tax burden calculated below is a measure of the changes needed in the economy. Fiscal implications would be indirect.

More troublesome than the assumption of a carbon tax is the assumption, again taken from the models I rely on, that climate policy will be cost-effective.333This paper shies away from a discussion of optimal climate policy targets, which are treated extensively elsewhere (Nordhaus, 1992, Tol, 1999, 2012b, 2023a). Current climate policy most definitely is not (e.g., Grimm et al., 2022). However, this strengthens the argument below. If cost-effective policy implies unrealistically large fiscal shocks, then sub-optimal policy (with the same emissions target) implies even larger shocks. Admittedly, without a carbon tax, those shocks may not be to the public finances; they will be to the economy instead.

2 Materials and methods

The IPCC AR6 scenario database contains projections of GDP, greenhouse gas emissions, carbon dioxide sequestration, and emission taxes for a range of ex-ante models and a range of scenarios with and without emission reduction targets. The database contains a host of variables on the structure of energy demand and supply, agriculture, land use, and so on. I here only use GDP, gross carbon dioxide emissions, gross carbon uptake, and carbon taxes. For most models, results are reported for 10-year intervals until 2100.

While generally well-structured, the database, unfortunately, does not match baseline and policy scenarios; this was added, manually, based on scenario names. Missing rows were replaced by missing observations. This then leads to the percentage reduction of GDP and emissions from baseline.

Total carbon tax revenue (subsidy) follows from multiplying gross carbon dioxide emissions (sequestration) with carbon taxes.

As highlighted by Riahi et al. (2022), the models in the database show a wide range of results. This is not a surprise, as the models have different structures and use different assumptions on economic growth, on relative prices, on technological change, on income, price and substitution elasticities, and on reserves, resources and potentials. Some models are computable general equilibrium models, others energy system models, and yet others are growth, econometric or new Keynesian models. All models have some foresight, many perfect foresight. The only commonality is that all models have been used to study future climate policy.

Note that I do not correct the IPCC database for reporting bias (Tavoni and Tol, 2010). This omission likely leads to an underestimate of the true cost of climate policy.

I follow Tol (2014) and compare these ex-ante models to the data, but where Tol (2014) relied on a fairly basic statistical analysis, I here use five advanced econometric studies of the efficacy of carbon pricing (Rafaty et al., 2020, Kohlscheen et al., 2021, Sen and Vollebergh, 2018, Metcalf and Stock, 2020, Best et al., 2020). These ex-post studies use different estimators and different samples, but they all study the effect of past climate policy on past emissions. The efficacy of a carbon tax is here defined as the percentage emission reduction per dollar per tonne of carbon dioxide carbon tax. This measure is reported by, or easily derived from the five econometric studies. It is also readily calculated from the data in the IPCC AR6 scenario database.

I use Bayesian statistics to assess the credibility of the different models. I use a non-informative prior. The results of the econometric models are the likelihood. Combined, this gives the posterior estimate of the tax efficacy. Alternatively, I shrunk the five estimates to a single, combined one (Goldberger, 1986). In a second step, as a prior, I assumed that each IPCC model is equally likely. The posterior likelihood of the tax efficacy implies a probability that an ex-ante model is able to reproduce observed climate policy as measured by the ex-post models.

While the methods are well-established, this is their first application to the fiscal implications of stringent climate policy.

3 Results

3.1 Model skill

Before discussing the key results, I need to establish which model is most credible. This is because the range of model range is so large. Some models find that climate policy is too cheap to meter, others that it would lead to economic ruin.

Table 1 shows the efficacy of a carbon price for the 24 models in the IPCC AR6 scenario database for which this information was available. Tax efficacy is the percentage CO2 emission reduction (from baseline) in 2030 divided by the carbon tax or permit price in the same year. (Recall that the models assume foresight.) Efficacy differs by three orders of magnitude from 0.0042%/$ for ices to 4.8%/$ for coffee.

At the bottom of 1, five econometric estimates of the same metric are shown (Rafaty et al., 2020, Kohlscheen et al., 2021, Sen and Vollebergh, 2018, Metcalf and Stock, 2020, Best et al., 2020). Three of these studies agree that a carbon price of $1/tCO2 would cut emissions by some 0.1%, higher than 2 of the 24 IPCC models and lower than 21. The other two econometric studies find that carbon pricing is more effective. The minimum and maximum differ by one order of magnitude.

The posterior mean, weighted average, or shrunk estimate is a reduction of 0.13% per dollar per metric tonne of carbon dioxide. This implies, assuming linearity, that a carbon tax of $792/tCO2 would fully decarbonize the world economy.

The short-run Leviathan tax is discussed in the introduction. It assumes that the imposed carbon tax does not affect emissions. Figure 1 also shows the long-run Leviation tax, using the central estimate of 0.13% emission reduction per dollar carbon tax. The Leviathan tax increases, but not sufficiently so that the IPCC’s $100/tCO2 carbon tax looks materially less problematic.

Only the imaclim model (Crassous et al., 2006, Sassi et al., 2010, Waisman et al., 2012, Bibas et al., 2015, Méjean et al., 2019) is close to the majority of the empirical evidence.444I have criticized this model for having so many distortions that it is hard to interpret the results. That said, the economy is full of distortions. Indeed, 95.5% of the posterior probability mass goes to imaclim. The posterior probability of gemini is 0.5%. The probabilities of the remaining models are very small.

3.2 The impact of stringent climate policy

Table 2 shows the main result. Twelve models in the IPCC AR6 database report scenarios that cut global carbon dioxide emissions by 95% or more in 2050. Table 2 shows the carbon price and the value of carbon capture and emissions, all averaged across the scenarios for each of the models. The carbon price is either the explicit carbon tax, the price of tradable permits, or the shadow price of the emissions constraint. The value of emissions is the total revenue of either a carbon tax or the auction of carbon permits. The value of carbon capture is either the total expenditure on carbon removal subsidies or the sum total spent on carbon offsets. Both values are given as a share of GDP.

The results vary widely. The most optimistic model is again the coffee model. As in Table 1, this model finds that a minimal carbon tax would completely decarbonize the economy. Revenues and expenditures are therefore small too. At the other extreme, dne21 has a carbon tax revenue of 3 times GDP, and on top spends 2 times GDP on carbon removal. One would hope this is a reporting error rather than a genuine result of what would be a mistaken model.

Discarding the two outliers, carbon tax revenue ranges from 1 to 17% of GDP. This range is wide. A tax reform that brings in 1% of GDP by 2050 is feasible. Tax reforms at this scale happen regularly (Ortiz-Ospina and Roser, 2016). The high end of the range is more difficult. The global average tax revenue was 14% of GDP in 2019.555See World Bank. An expansion of the public sector by 3% in 30 years is doable. Reducing if not abolishing all other taxes would, of course, be an election winner—although taxes are rarely abolished (Seelkopf et al., 2021). However, as emissions approach zero, the tax base would get narrower and narrower and the carbon tax higher and higher, so that the fiscal system becomes increasingly distortionary. As emissions go to zero, so does carbon tax revenue—other taxes will have to be reintroduced, a politically more challenging prospect.666In GCAM, emissions fall to zero before 2050. Its fiscal transition is even faster. imaclim, the most credible model, has total carbon tax revenues at 7% of GDP in 2050, replacing “only” half of all other taxes (if government budget neutrality is assumed).

Total carbon removal subsidies, or payments for offsets, range from 0.3% (aim) to 7% (grape) of GDP. The model that compares best to the data, imaclim, is at the high end of this range. A subsidy that is a few tenths of a percent of GDP is no problem. Climate change has been a key concern of many people around the world for decades (Leiserowitz, 2006, Lee et al., 2015, Rettig et al., 2023)—the vocal protests of a small minority notwithstanding. Spending a small fraction of income on solving the climate problem should not be a problem. However, expenditure is much larger at the high end of the range, roughly equal to expenditures on health care. Public spending on health care is like motherhood and apple pie—we all rely on doctors and nurses to heal ourselves and our loved ones, and we all have friends and family who work in medicine and who deserve a decent salary. Carbon capture is very different. It solves a distant and abstract problem, rather than one that is close and obvious like ill-health. If climate policy is successful, there is not much of a problem to solve anymore, making it harder to continue to justify spending large sums of money. In order to keep costs down, carbon capture will be done where land is cheap—that is, where few people live—and heavily mechanized. Paying 7% of your income in taxes to keep grandma alive and your nurse friend in work is one thing. Paying 7% to a multinational company to suck carbon dioxide out of the air in a faraway country is something else.

3.3 Regional results

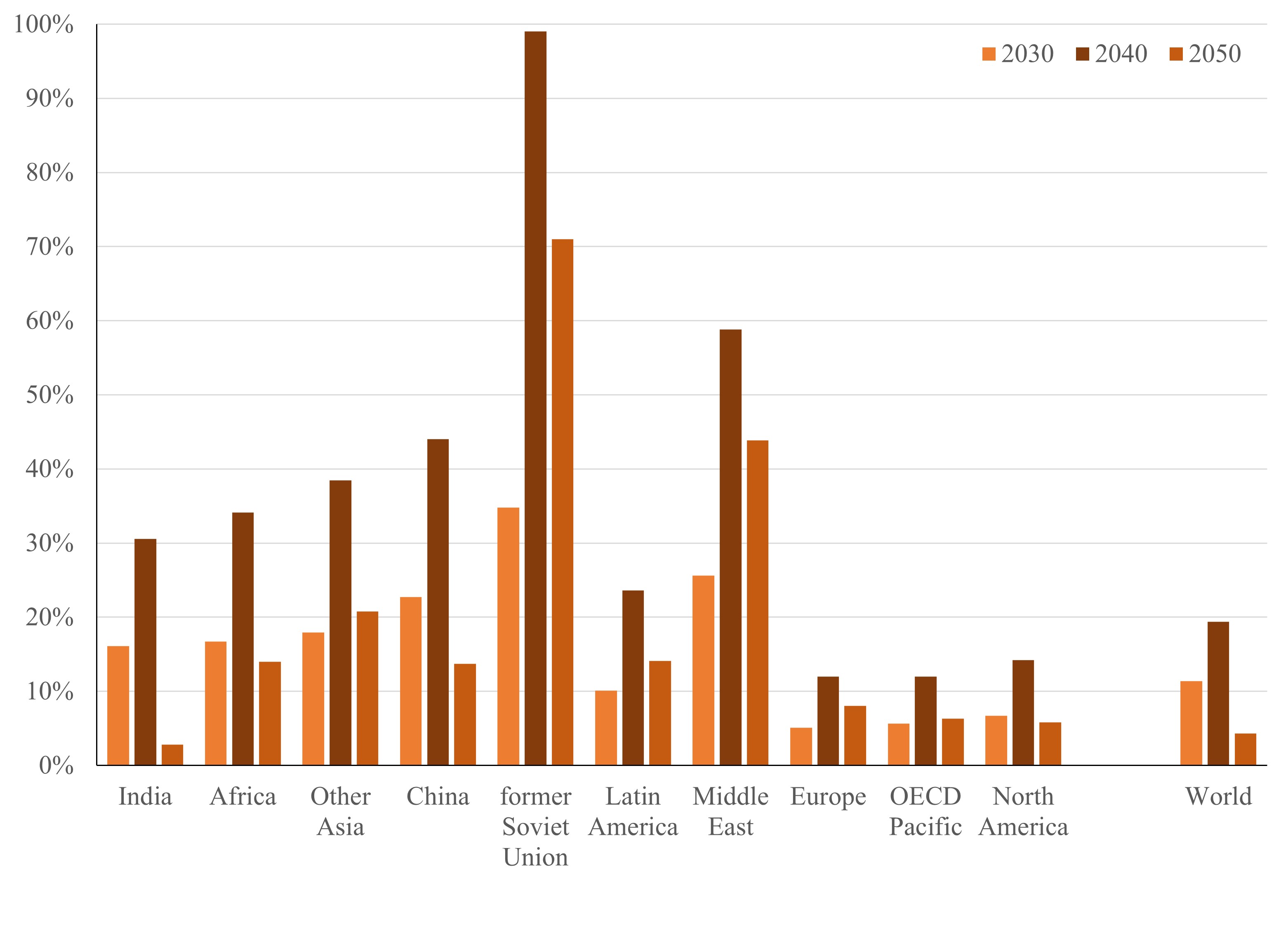

The above results are for the world as a whole. The models in the IPCC database also report regional results. I restrict the attention to imaclim and one particular scenario which reduces emissions by 94% in 2050. The carbon tax is $300/tCO2 in 2030, rising to $1,298/tCO2 in 2040 and $2,253/tCO2 in 2050. Figure 2 shows carbon tax revenue and sequestration subsidy, as a percentage of GDP, for 2030, 2040, and 2050.

Global carbon tax revenue is 4% of GDP in 2050, a reasonable number, but 11% in 2030 and 19% in 2040—underlining yet again the fiscal challenge posed by stringent climate policy.

The results in Figure 2 are ordered by per capita income in 2010. Carbon tax revenue is below the global average in the three richest regions, but above the global average in the seven poorest regions—with the exception of almost completely decarbonized India in 2050. The carbon tax revenue is very high in the carbon-intensive economies of the Middle East and the former Soviet Union.

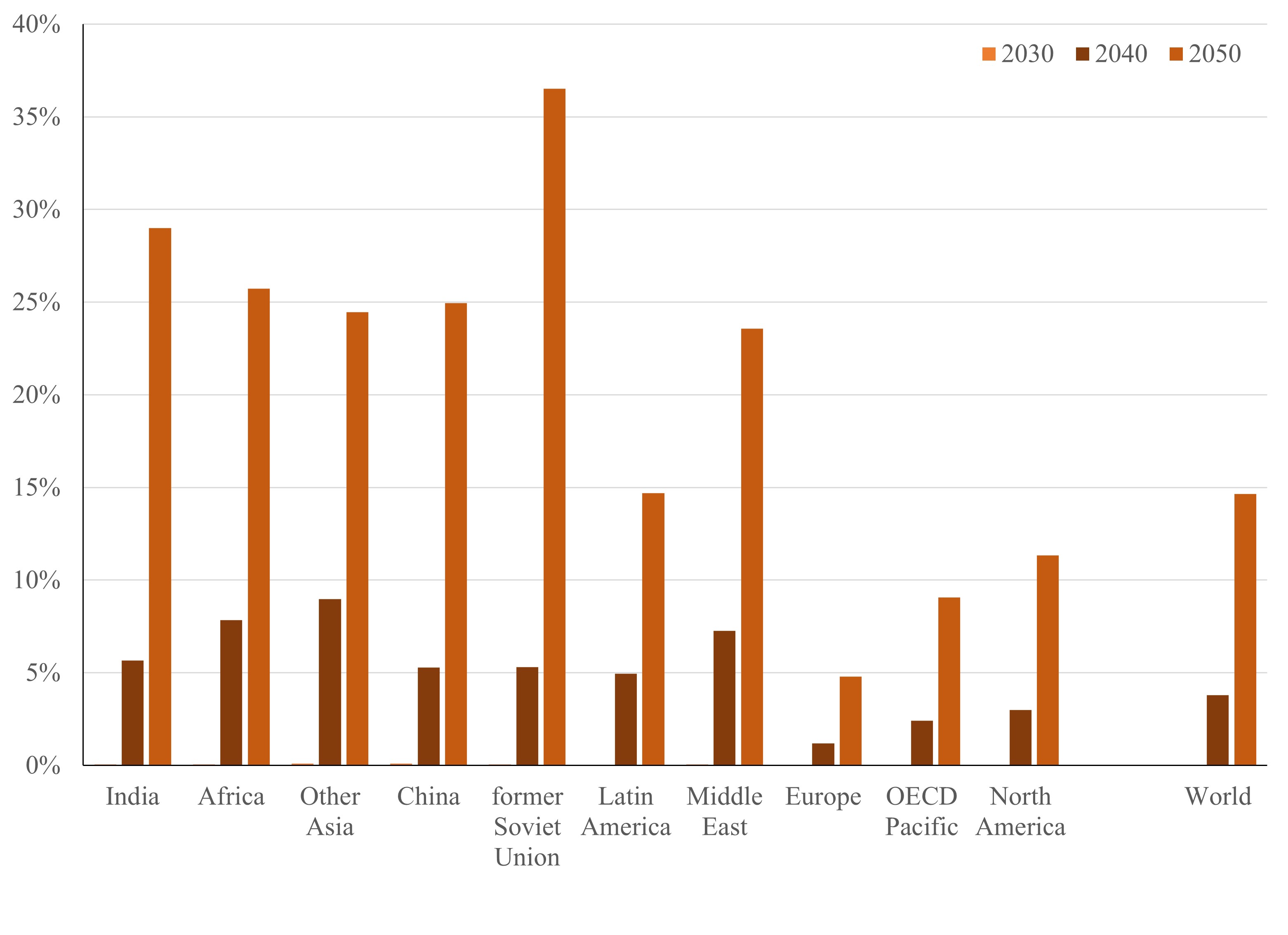

The bottom panel of Figure 2 shows the sequestration subsidies. The world total is 0.04% of GDP in 2030, rising to 3.8% in 2040 and 15% in 2050. As with tax revenues, the numbers are lower for the three rich regions and higher for the seven poor regions. Note, however, that it may well be that there will substantial transfers between regions. This is less likely with direct subsidies, more likely with tradable permits and offsets.

That said, Figure 2 highlights the scale of the activity. The sequestration sector would occupy almost 15% of the world economy, over 35% of the economy in the former Soviet Union.

3.4 Results for more lenient climate policy

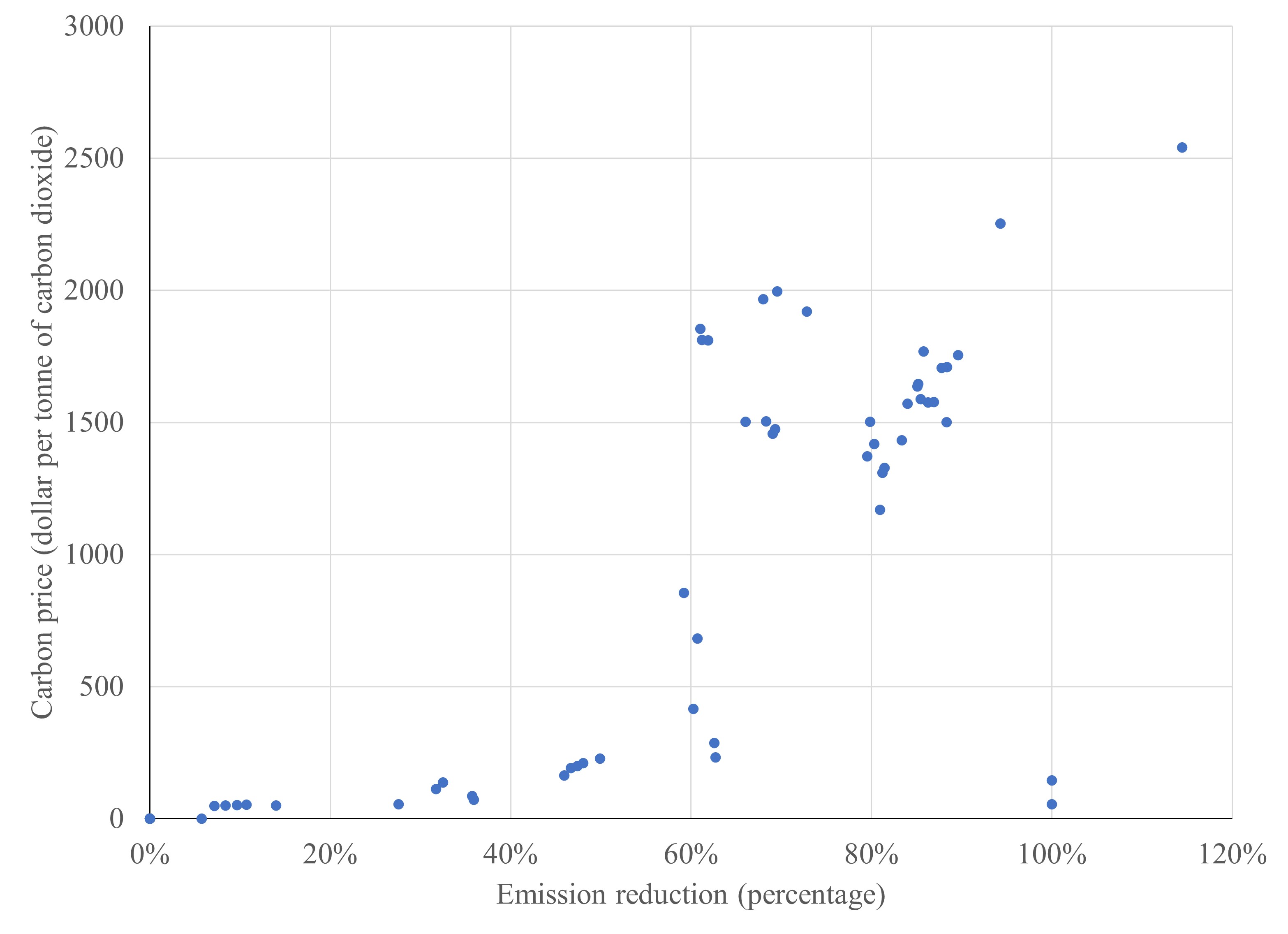

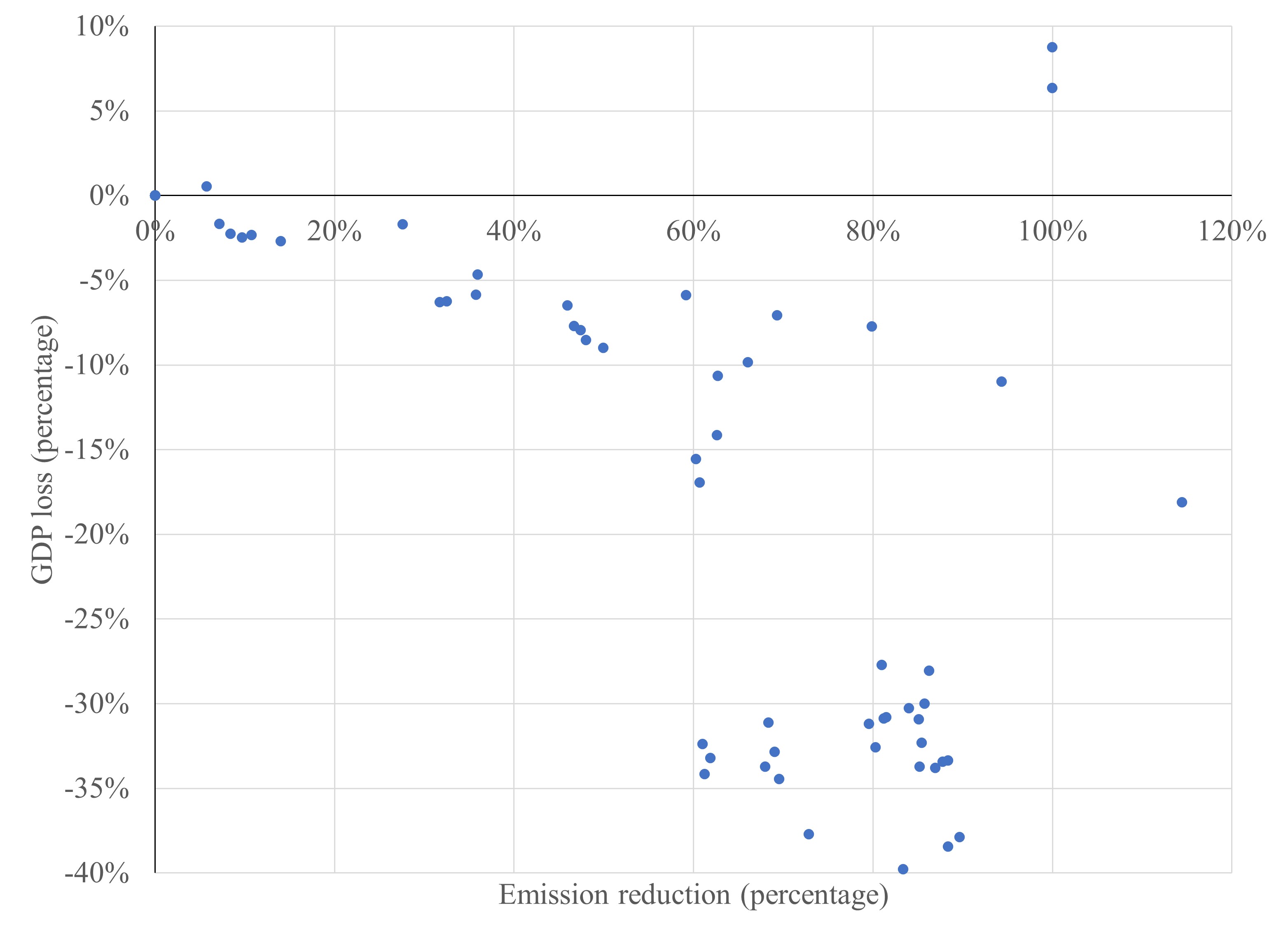

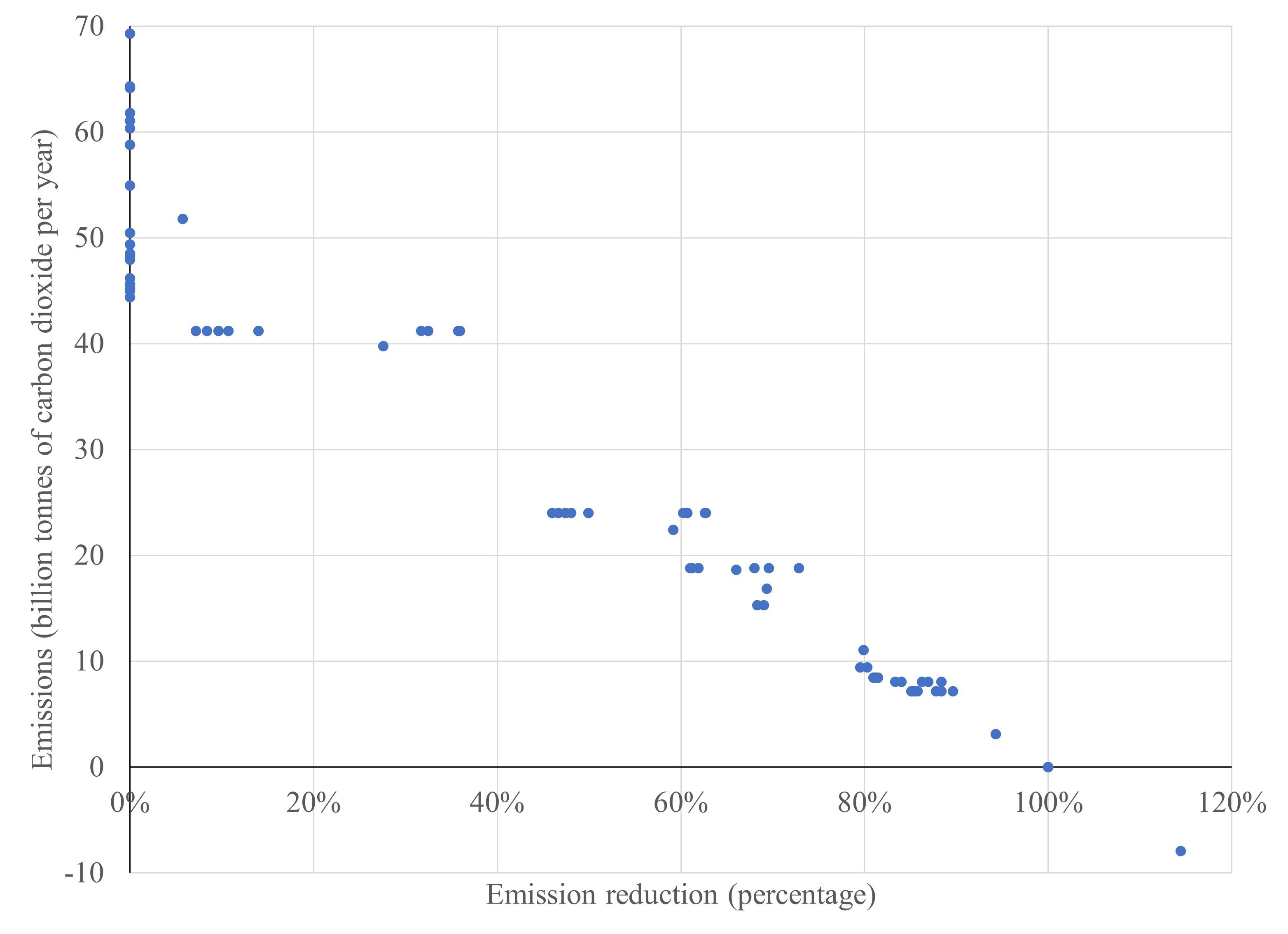

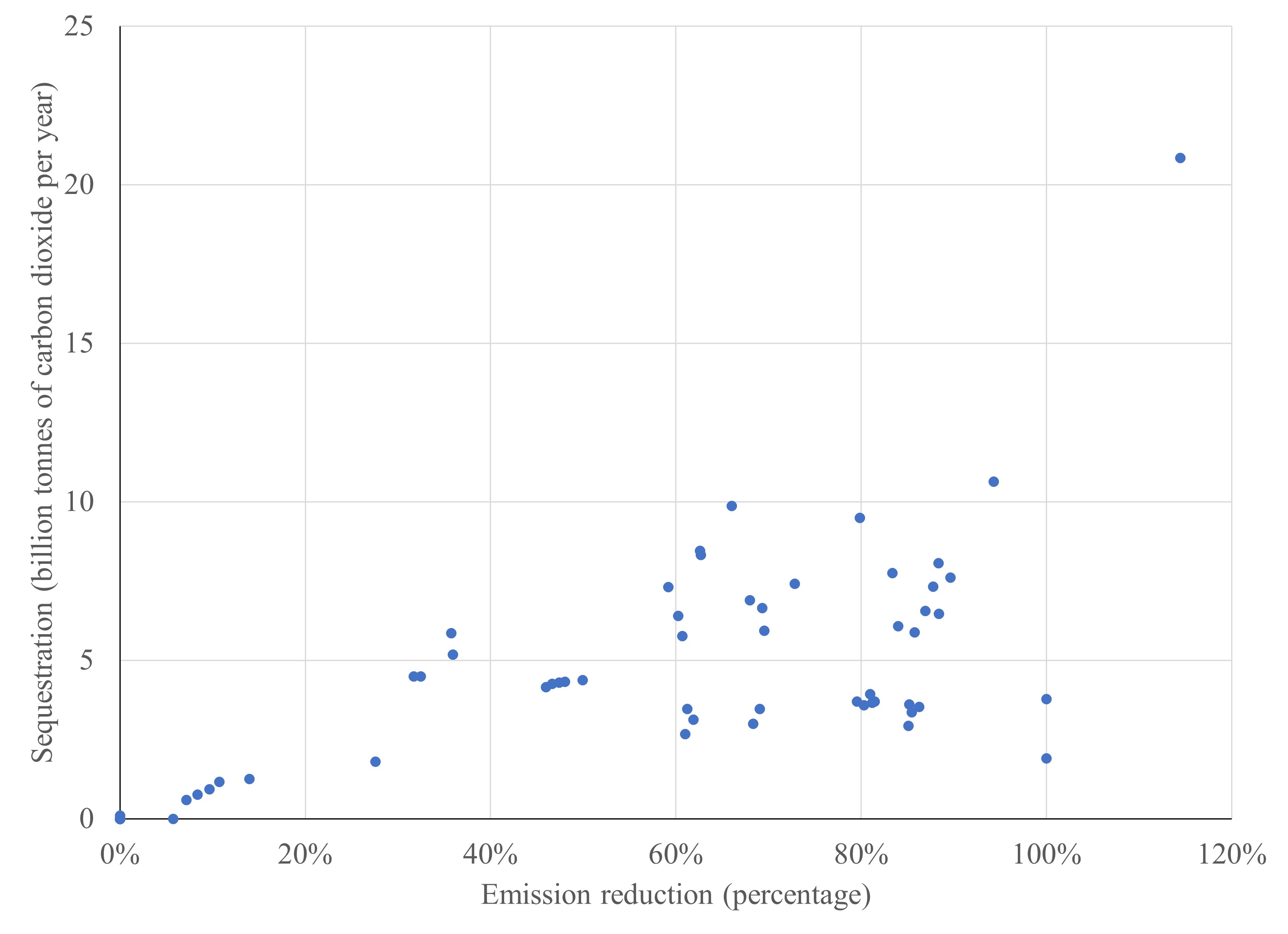

The above results are for very stringent climate policy. Cutting carbon dioxide emissions by 95% or more by 2050 is highly ambitious. The major fiscal implications highlighted above rapidly disappear for less stringent climate policy. This is because the fiscal implications are the product of carbon price and emissions. Take the subsidies for carbon dioxide removal first. A more lenient target would mean a lower volume at a lower price. The carbon tax revenue would fall too: Emissions would be higher but the carbon price lower; the former is linear, the latter exponential.

Figure 3 illustrates this for the imaclim model for 2050. The top left panel plots the carbon price against emission reduction from baseline. The carbon price inches up until emissions are halved and then starts rising very quickly. However, emissions, shown in the bottom left panel, continue to fall steadily. Sequestration, in the bottom right panel, similarly shows no profound non-linearity. The top right panel shows the drop in GDP, which accelerates around a 50% emission reduction. This accentuates carbon tax revenue and carbon sequestration expenditures relative to GDP.

4 Discussion and conclusion

Stringent climate policy would pose a substantial fiscal challenge. The global revenue of the carbon tax needed to meet the targets of the 2015 Paris Agreement would be larger than the revenue of all other taxes combined, while a very large subsidy would need to be paid to remove carbon dioxide from the atmosphere. Tax revenues are larger still in poor parts of the world. Climate policy by other means than taxes and subsidies would shift, perhaps hide, probably exacerbate the fiscal burden.

The fiscal challenge rapidly shrinks as the emission reduction target becomes less stringent. The policy implication is thus to adopt a more lenient climate policy—or rather, as the gap between nominal targets and actual climate policy had widened (UNEP, 2022), to adopt more realistic rhetoric.

The implications for research are more profound. Model results show a very large range for the costs of future climate policy. This is partly inevitable. The future is inherently uncertain. However, the skill of ex-ante models can be tested against over 30 years of experience with actual climate policy. This is here done with a single variable, tax efficacy, but these models generate many more variables, most of which are directly observed.

Even before testing their skills, two of the models in the IPCC database report patent nonsense. Either the database or the models need to be vetted better. The problems do not stop there. Many of the integrated assessment models used by the IPCC do not have a rich representation of the fiscal system—and none report this. Environmental regulation and general taxation interact (Sandmo, 1975). Ignoring prior tax distortions leads to unnecessarily expensive climate policy (Barrage, 2019). A tax is more distortionary as it rises and its base narrows—exactly what happens as emissions approach zero. Ignoring the excess burden in the climate policy endgame seems to be a crucial omission in integrated assessment models.

Unlike tax distortions, tax revolts are unpredictable—but the probability of tax revolts varies systematically with observable variables (Dowlatabadi, 2000). Dynamic stochastic general equilibrium models are now regularly used to study climate policy (Cai and Lontzek, 2019, Van den Bremer and Van der Ploeg, 2021). It strikes me that tax revolts are a key stochastic element. Tax revolts may be more likely if the costs of climate policy are distributed in a way that is seen to be unfair (Chepeliev et al., 2021, Landis et al., 2021, Vandyck et al., 2021, Böhringer et al., 2022, Wu2022) and if assets are stranded and firms go bankrupt (Davis et al., 2010, Tong et al., 2019, van der Ploeg and Rezai, 2020, Semieniuk et al., 2022, Flora and Tankov, 2023).

All this complicates climate policy and makes it more expensive. Adding the analytically convenient but unrealistic assumption of first-best policy implementation, it appears that policy-makers are ill-advised by the IPCC and its choice of models. More importantly, current emission reduction targets may need to be relaxed.

References

- Barrage (2019) Lint Barrage. Optimal Dynamic Carbon Taxes in a Climate–Economy Model with Distortionary Fiscal Policy. The Review of Economic Studies, 87(1):1–39, 2019. URL https://doi.org/10.1093/restud/rdz055.

- Baumol and Oates (1971) W. J. Baumol and W. E. Oates. The use of standards and prices for the protection of the environment. Scandinavian Journal of Economics, 73(1):42–54, 1971.

- Belfiori and Rezai (2023) Elisa Belfiori and Armon Rezai. Optimal climate policy: Making do with the taxes we have. Technical report, Universidad Torcuato Di Tella, School of Business, Buenos Aires, 2023.

- Besley and Persson (2013) Timothy Besley and Torsten Persson. Chapter 2 - taxation and development. In Alan J. Auerbach, Raj Chetty, Martin Feldstein, and Emmanuel Saez, editors, Handbook of Public Economics, vol. 5, volume 5 of Handbook of Public Economics, pages 51–110. Elsevier, 2013. doi: https://doi.org/10.1016/B978-0-444-53759-1.00002-9.

- Best et al. (2021) R. Best, M. Hammerle, P. Mukhopadhaya, and J. Silber. Targeting household energy assistance. Energy Economics, 99, 2021. doi: 10.1016/j.eneco.2021.105311.

- Best et al. (2020) Rohan Best, Paul J. Burke, and Frank Jotzo. Carbon Pricing Efficacy: Cross-Country Evidence. Environmental & Resource Economics, 77(1):69–94, 2020. doi: 10.1007/s10640-020-00436-.

- Bibas et al. (2015) Ruben Bibas, Aurélie Méjean, and Meriem Hamdi-Cherif. Energy efficiency policies and the timing of action: An assessment of climate mitigation costs. Technological Forecasting and Social Change, 90(PA):137 – 152, 2015. doi: 10.1016/j.techfore.2014.05.003.

- Böhringer et al. (2022) Christoph Böhringer, Xaquín García-Muros, and Mikel González-Eguino. Who bears the burden of greening electricity? Energy Economics, 105, 2022. doi: 10.1016/j.eneco.2021.105705.

- Burg (2004) David F. Burg. A World History of Tax Rebellions: An Encyclopedia of Tax Rebels, Revolts, and Riots from Antiquity to the Present. Routledge, London and New York, 2004.

- Cai and Lontzek (2019) Y. Cai and T. S. Lontzek. The social cost of carbon with economic and climate risks. Journal of Political Economy, 127(6):2684–2734, 2019. doi: 10.1086/701890.

- Chepeliev et al. (2021) Maksym Chepeliev, Israel Osorio-Rodarte, and Dominique van der Mensbrugghe. Distributional impacts of carbon pricing policies under the Paris Agreement: Inter and intra-regional perspectives. Energy Economics, 102:105530, 2021. URL https://www.sciencedirect.com/science/article/pii/S0140988321004084.

- Clarke et al. (2009) Leon Clarke, Jae Edmonds, Volker Krey, Richard Richels, Steven Rose, and Massimo Tavoni. International climate policy architectures: Overview of the EMF 22 international scenarios. Energy Economics, 31(S2):S64–S81, 2009. URL http://www.sciencedirect.com/science/article/B6V7G-4XHVH34-2/2/67f06e207a515adba42f7455a99f648e.

- Crassous et al. (2006) Renaud Crassous, Jean-Charles Hourcade, and Olivier Sassi. Endogenous structural change and climate targets modeling experiments with Imaclim-R. Energy Journal, 27(SPEC. ISS. MAR.):259 – 276, 2006.

- Davis et al. (2010) Steven J. Davis, Ken Caldeira, and H. Damon Matthews. Future CO2 emissions and climate change from existing energy infrastructure. Science, 329(5997):1330–1333, 2010. doi: 10.1126/science.1188566.

- Distefano and D’Alessandro (2023) Tiziano Distefano and Simone D’Alessandro. Introduction of the carbon tax in italy: Is there room for a quadruple-dividend effect? Energy Economics, 120, 2023. doi: 10.1016/j.eneco.2023.106578.

- Dowlatabadi (2000) H. Dowlatabadi. Bumping against a gas ceiling. Climatic Change, 46(3):391–407, 2000. doi: 10.1023/A:1005611713386.

- Dubash et al. (2022) Navroz K. Dubash, Catherine Mitchell, Elin Lerum Boasson, Mercy J. Borbor-Córdova, Solomone Fifita, Erik Haites, Mark Jaccard, Frank Jotzo, Sasha Naidoo, Patricia Romero-Lankao, Wei Shen, Mykola Shlapak, and Libo Wu. National and sub-national policies and institutions. In P. R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, and J. Malley, editors, Climate Change 2022: Mitigation of Climate Change—Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge, 2022.

- Flora and Tankov (2023) Maria Flora and Peter Tankov. Green investment and asset stranding under transition scenario uncertainty. Energy Economics, 124, 2023. doi: 10.1016/j.eneco.2023.106773.

- Goldberger (1986) Arthur S. Goldberger. Econometric Theory. Wiley, New York, 1986.

- Goulder (1995) L.H. Goulder. Environmental taxation and the double dividend: A reader’s guide. International Tax and Public Finance, 2(2):157–183, 1995. doi: 10.1007/BF00877495.

- Grimm et al. (2022) Veronika Grimm, Christian Sölch, and Gregor Zöttl. Emissions reduction in a second-best world: On the long-term effects of overlapping regulations. Energy Economics, 109, 2022. doi: 10.1016/j.eneco.2022.105829.

- IEA (2021) IEA. Net zero by 2050—a roadmap for the global energy sector. Technical report, International Energy Agency, Paris, 2021.

- IEA (2022) IEA. World energy outlook. Technical report, International Energy Agency, Paris, 2022.

- Keen and Slemrod (2021) Michael Keen and Joel Slemrod. Rebellion, Rascals, and Revenue: Tax Follies and Wisdom Through the Ages. Princeton University Press, Princeton, 2021.

- Kohlscheen et al. (2021) Emanuel Kohlscheen, Richhild Moessner, and Elod Takáts. Effects of carbon pricing and other climate policies on CO2 emissions. Working Paper 9347, CESifo, 2021. URL https://www.cesifo.org/en/publikationen/2021/working-paper/effects-carbon-pricing-and-other-climate-policies-co2-emissions.

- Landis et al. (2021) Florian Landis, Gustav Fredriksson, and Sebastian Rausch. Between- and within-country distributional impacts from harmonizing carbon prices in the EU. Energy Economics, 103:105585, 2021. URL https://www.sciencedirect.com/science/article/pii/S0140988321004540.

- Lee et al. (2015) Tien Ming Lee, Ezra M. Markowitz, Peter D. Howe, Chia-Ying Ko, and Anthony A. Leiserowitz. Predictors of public climate change awareness and risk perception around the world. Nature Climate Change, 5(11):1014 – 1020, 2015. doi: 10.1038/nclimate2728.

- Leiserowitz (2006) Anthony Leiserowitz. Climate change risk perception and policy preferences: The role of affect, imagery, and values. Climatic Change, 77(1-2):45 – 72, 2006. doi: 10.1007/s10584-006-9059-9.

- Méjean et al. (2019) Aurélie Méjean, Céline Guivarch, Julien Lefèvre, and Meriem Hamdi-Cherif. The transition in energy demand sectors to limit global warming to 1.5. Energy Efficiency, 12(2):441 – 462, 2019. doi: 10.1007/s12053-018-9682-0.

- Metcalf and Stock (2020) Gilbert E Metcalf and James H Stock. The macroeconomic impact of Europe’s carbon taxes. Working Paper 27488, National Bureau of Economic Research, 2020.

- Nordhaus (1992) William D. Nordhaus. An optimal transition path for controlling greenhouse gases. Science, 258:1315–1319, 1992.

- Ortiz-Ospina and Roser (2016) Esteban Ortiz-Ospina and Max Roser. Taxation. Our World in Data, 2016. https://ourworldindata.org/taxation.

- Rafaty et al. (2020) Ryan Rafaty, Geoffroy Dolphin, and Felix Pretis. Carbon pricing and the elasticity of CO2 emissions. Technical report, Energy Policy Research Group, University of Cambridge, 2020. URL http://www.jstor.org/stable/resrep30490.

- Rettig et al. (2023) Leonie Rettig, Lea Gärtner, and Harald Schoen. Facing trade-offs: The variability of public support for climate change policies. Environmental Science and Policy, 147:244 – 254, 2023. doi: 10.1016/j.envsci.2023.06.020.

- Riahi et al. (2022) Keywan Riahi, Roberto Schaeffer, Jacobo Arango, Katherine Calvin, Céline Guivarch, Tomoko Hasegawa, Kejun Jiang, Elmar Kriegler, Robert Matthews, Glen Peters, Anand Rao, Simon Robertson, Adam Mohammed Sebbit, Julia Steinberger, Massimo Tavoni, and Detlef van Vuuren. Mitigation pathways compatible with long-term goals. In P. R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, and J. Malley, editors, Climate Change 2022: Mitigation of Climate Change—Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press, Cambridge, 2022.

- Sandmo (1975) Agnar Sandmo. Optimal taxation in the presence of externalities. The Swedish Journal of Economics, 77(1):86–98, 1975. ISSN 00397318. URL http://www.jstor.org/stable/3439329.

- Sassi et al. (2010) Olivier Sassi, Renaud Crassous, Jean-Charles Hourcade, Vincent Gitz, Henri Waisman, and Céline Guivarch. IMACLIM-R: A modelling framework to simulate sustainable development pathways. International Journal of Global Environmental Issues, 10(1-2):5 – 24, 2010. doi: 10.1504/IJGENVI.2010.030566.

- Seelkopf et al. (2021) L. Seelkopf, M. Bubek, E. Eihmanis, J. Ganderson, J. Limberg, Y. Mnaili, P. Zuluaga, and P. Genschel. The rise of modern taxation: A new comprehensive dataset of tax introductions worldwide. Review of International Organizations, 16(1):239–263, 2021. doi: 10.1007/s11558-019-09359-9.

- Semieniuk et al. (2022) G. Semieniuk, P.B. Holden, J.-F. Mercure, P. Salas, H. Pollitt, K. Jobson, P. Vercoulen, U. Chewpreecha, N.R. Edwards, and J.E. Viñuales. Stranded fossil-fuel assets translate to major losses for investors in advanced economies. Nature Climate Change, 12(6):532–538, 2022. doi: 10.1038/s41558-022-01356-y.

- Sen and Vollebergh (2018) Suphi Sen and Herman Vollebergh. The effectiveness of taxing the carbon content of energy consumption. Journal of Environmental Economics and Management, 92(C):74–99, 2018. doi: 10.1016/j.jeem.2018.08.01.

- Stoll and Mehling (2021) Christian Stoll and Michael A. Mehling. Climate change and carbon pricing: Overcoming three dimensions of failure. Energy Research & Social Science, 77:102062, 2021. ISSN 2214-6296. doi: https://doi.org/10.1016/j.erss.2021.102062. URL https://www.sciencedirect.com/science/article/pii/S2214629621001559.

- Tavoni and Tol (2010) M. Tavoni and Richard S. J. Tol. Counting only the hits? the risk of underestimating the costs of stringent climate policy: A letter. Climatic Change, 100(3):769–778, 2010. doi: 10.1007/s10584-010-9867-9.

- Tol (1999) Richard S. J. Tol. Kyoto, efficiency, and cost-effectiveness: Applications of FUND. The Energy Journal, (Special Issue):131–156, 1999. URL https://ideas.repec.org/a/aen/journl/1999si-a06.html.

- Tol (2012a) Richard S. J. Tol. Leviathan taxes in the short run. Climatic Change Letters, 113(3-4):1049–1063, 2012a.

- Tol (2012b) Richard S. J. Tol. A cost-benefit analysis of the EU 20/20/2020 package. Energy Policy, 49:288–295, 2012b. doi: 10.1016/j.enpol.2012.06.018.

- Tol (2014) Richard S. J. Tol. Ambiguity reduction by objective model selection, with an application to the costs of the EU 2030 climate targets. Energies, 7(11):6886–6896, 2014. URL https://www.mdpi.com/1996-1073/7/11/6886.

- Tol (2023a) Richard S. J. Tol. Social cost of carbon estimates have increased over time. Nature Climate Change, 2023a.

- Tol (2023b) Richard S. J. Tol. Climate economics: Economic analyses of climate, climate change, and climate policy (third edition). Edward Elgar, Cheltenham, 2023b.

- Tong et al. (2019) D. Tong, Q. Zhang, Y. Zheng, K. Caldeira, C. Shearer, C. Hong, Y. Qin, and S.J. Davis. Committed emissions from existing energy infrastructure jeopardize 1.5 climate target. Nature, 572(7769):373–377, 2019. doi: 10.1038/s41586-019-1364-3.

- UNEP (2022) UNEP. The closing window—climate crisis calls for rapid transformation of societies. Emissions Gap Report 2022, United Nations Environment Programme, Nairobi, 2022.

- Van den Bremer and Van der Ploeg (2021) Ton S. Van den Bremer and Frederick Van der Ploeg. The risk-adjusted carbon price. American Economic Review, 111(9):2782–2810, 2021. doi: 10.1257/aer.20180517.

- van der Ploeg and Rezai (2020) Frederick van der Ploeg and Armon Rezai. The risk of policy tipping and stranded carbon assets. Journal of Environmental Economics and Management, 100:102258, 2020. ISSN 0095-0696. URL https://www.sciencedirect.com/science/article/pii/S0095069618302481.

- van Heerden et al. (2006) Jan H. van Heerden, Reyer Gerlagh, James N. Blignaut, Mark Horridge, S. Hess, R. Mabugu, and M. Mabugu. Searching for triple dividends in south africa: Fighting co2 pollution and poverty while promoting growth. Energy Journal, 27(2):113–141, 2006.

- Vandyck et al. (2021) Toon Vandyck, Matthias Weitzel, Krzysztof Wojtowicz, Luis Rey Los Santos, Anamaria Maftei, and Sara Riscado. Climate policy design, competitiveness and income distribution: A macro-micro assessment for 11 EU countries. Energy Economics, 103:105538, 2021. URL https://www.sciencedirect.com/science/article/pii/S0140988321004151.

- Waisman et al. (2012) Henri Waisman, Céline Guivarch, Fabio Grazi, and Jean Charles Hourcade. The Imaclim-R model: Infrastructures, technical inertia and the costs of low carbon futures under imperfect foresight. Climatic Change, 114(1):101 – 120, 2012. doi: 10.1007/s10584-011-0387-z.

| model | # | mean | st.err. | prob. |

|---|---|---|---|---|

| coffee | 63 | 4.883% | 0.584% | 0.000 |

| aim | 123 | 1.103% | 0.352% | 0.000 |

| image | 81 | 0.802% | 0.128% | 0.000 |

| remind | 286 | 0.705% | 0.045% | 0.000 |

| witch | 142 | 0.646% | 0.028% | 0.000 |

| gcam | 47 | 0.612% | 0.082% | 0.000 |

| gem-e3 | 49 | 0.604% | 0.025% | 0.000 |

| message | 258 | 0.566% | 0.042% | 0.000 |

| poles | 134 | 0.544% | 0.046% | 0.000 |

| farm | 12 | 0.529% | 0.060% | 0.000 |

| prometheus | 6 | 0.442% | 0.065% | 0.000 |

| eppa | 4 | 0.373% | 0.040% | 0.000 |

| bet | 14 | 0.367% | 0.054% | 0.000 |

| grape | 17 | 0.331% | 0.042% | 0.000 |

| en-roads | 2 | 0.318% | 0.007% | 0.000 |

| dne21 | 34 | 0.317% | 0.030% | 0.000 |

| muse | 6 | 0.238% | 0.099% | 0.000 |

| c3iam | 4 | 0.228% | 0.008% | 0.000 |

| tiam-ucl | 5 | 0.225% | 0.051% | 0.000 |

| tiam-ecn | 58 | 0.202% | 0.028% | 0.000 |

| gemini | 5 | 0.165% | 0.051% | 0.005 |

| imaclim | 51 | 0.121% | 0.021% | 0.995 |

| env-linkages | 13 | 0.005% | 0.006% | 0.000 |

| ices | 6 | 0.004% | 0.001% | 0.000 |

| Average | 24 | 0.597% | 0.194% | |

| Weighted average | 24 | 0.009% | 0.001% | |

| Rafaty et al. (2020) | 0.110% | 1.779% | ||

| Metcalf and Stock (2020) | 0.125% | 0.013% | ||

| Kohlscheen et al. (2021) | 0.130% | 0.030% | ||

| Sen and Vollebergh (2018) | 0.730% | 0.640% | ||

| Best et al. (2021) | 2.960% | 0.987% | ||

| Weighted average | 0.126% | 0.012% |

| model | tax | sequestration | emissions |

|---|---|---|---|

| $/tCO2 | %GDP | %GDP | |

| coffee | 3 | -0.07 | 0.20 |

| aim | 119 | -0.29 | 1.73 |

| gem-e3 | 385 | -0.30 | 1.07 |

| gcam | 1720 | -0.31 | -4.21 |

| remind | 537 | -1.76 | 2.66 |

| image | 586 | -2.26 | 3.35 |

| message | 823 | -2.26 | 4.83 |

| witch | 1204 | -3.08 | 5.84 |

| poles | 4601 | -4.09 | 17.08 |

| imaclim | 913 | -6.56 | 7.41 |

| grape | 1196 | -7.09 | 20.58 |

| dne21 | 977 | -230.08 | 301.22 |