exampleExample \newsiamremarkremarkRemark \newsiamremarkhypothesisHypothesis \newsiamthmclaimClaim \headersStochastic th root approximation of a stochastic matrixF. Durastante, B. Meini

Stochastic th root approximation of a stochastic matrix: A Riemannian optimization approach††thanks: Submitted to the editors . \fundingThis work has been partially supported by: Spoke 1 “FutureHPC & BigData” of theItalian Research Center on High-Performance Computing, Big Data and QuantumComputing (ICSC) funded by MUR Missione 4 Componente 2 Investimento 1.4:Potenziamento strutture di ricerca e creazione di “campioni nazionali di R&S(M4C2-19 )” - Next Generation EU (NGEU); by the “INdAM – GNCS Project: Metodi basati su matrici e tensori strutturati per problemi di algebra lineare di grandi dimensioni” code CUP_E53C22001930001; and by the PRIN project “Low-rank Structures and Numerical Methods in Matrix and Tensor Computations and their Application” code 20227PCCKZ. The authors are member of the INdAM GNCS group.

Abstract

We propose two approaches, based on Riemannian optimization, for computing a stochastic approximation of the th root of a stochastic matrix . In the first approach, the approximation is found in the Riemannian manifold of positive stochastic matrices. In the second approach, we introduce the Riemannian manifold of positive stochastic matrices sharing with the Perron eigenvector and we compute the approximation of the th root of in such a manifold. This way, differently from the available methods based on constrained optimization, and its th root approximation share the Perron eigenvector. Such a property is relevant, from a modeling point of view, in the embedding problem for Markov chains. The extended numerical experimentation shows that, in the first approach, the Riemannian optimization methods are generally faster and more accurate than the available methods based on constrained optimization. In the second approach, even though the stochastic approximation of the th root is found in a smaller set, the approximation is generally more accurate than the one obtained by standard constrained optimization.

keywords:

Stochastic matrix, Matrix th root, Riemannian optimization, Markov chains, Embedding problem65C40, 65K05, 53B21, 65F60

1 Introduction

Discrete and continuous-time Markov chains are used to model a range of different time-evolving phenomena such as queueing models [9], physician’s estimate of prognosis under alternative treatment plans [5], synthetic DNA [3], rating agencies predicting the evolution of a firm’s rating in a given time interval [26, 25], studying diffusion and consensus on directed graphs [34] or the analysis of daily rainfall occurrence [20]. The evolution of a discrete-time Markov chain, with a finite number of states, is described in terms of an matrix , called transition matrix, whose -th entry represents the probability to go from state to state in one unit of time. The matrix is stochastic, i.e., belongs to the set

where , and the symbol “” represents the element-wise ordering; see [7, Chapter 8] for an introduction to finite Markov chains. For the Perron-Frobenius theorem, any stochastic matrix has a nonnegative Perron eigenvector, i.e., a nonnegative vector such that ; when is normalized so that , then is called steady state vector, or stationary distribution, for the matrix . If is irreducible, then the steady state vector has positive entries and is unique, moreover .

In many applications, the entries of the matrix are estimated through the analysis of historical series over long time intervals. Therefore, the unit time at which transitions occur is generally larger, compared with the characteristic time of the phenomenon to be analyzed. To know the transition probabilities in the typical time step of the phenomenon, it would therefore be necessary to investigate what happens in a fraction of a unit of time: for instance, which are the transition probabilities in a half-time unit? An attempt might be computing a matrix such that , or, in other terms, a square root of the transition matrix . More generally, we can inquire about any number of intermediate steps thus looking for a th root of , , . However, for the matrix to be descriptive of a Markov process, we need it to be itself a transition matrix, that is, should satisfy

Unfortunately, such does not exist in general [22], and several pathological cases can be readily produced, e.g., the th root may exist or not, it may exist and not be stochastic, and there can even be more than one stochastic th root. In some cases, we can exploit the fact that has more than one branch in the complex plane to define non-primary matrix functions by selecting different determinations of the function on repeated eigenvalues — see [21, Section 1.4] — and look for a non-primary stochastic matrix th root. Even with this added degree of freedom, stochastic th roots of a stochastic matrix might not exist.

The problem of the existence of a stochastic th root of a stochastic matrix is also strictly related to the so called embedding problem for Markov chains (see [33]). Indeed, a Markov chain with transition matrix is embeddable if and only if there exists a rate matrix such that . We recall that a rate matrix is a matrix with nonnegative off-diagonal entries, such that . It is immediate to verify that, if a Markov chain is embeddable, then is a stochastic th root of , for any . More precisely, in [27] it is shown that a Markov chain is embeddable if and only if the transition matrix is nonsingular and has stochastic th roots of any order . To this regard, in [33] a characterization of embeddable Markov chains is given in terms of infinite divisibility properties of nonnegative matrices. In practice, these conditions are difficult to verify and sufficient conditions for embeddability have been introduced for specific cases, as equal-input, circulant, symmetric or doubly stochastic matrices [4], small size matrices [13], or in other frameworks [15, 19, 22, 8].

In the case where a stochastic th root does not exist, an alternative approach consists of finding an approximation which is a stochastic matrix. To this end, there are some methods available in the literature relying on optimization strategies, see, e.g., the code package in [29]. Given , the main approach consists in the computation of the solution of the following constrained optimization problem, where is the Frobenius norm (see [22, 14]):

-

(a)

find

Other, less used, strategies consist in

-

(b)

find

where is the principal th root of ;

-

(c)

find

for

where is the vector obtained by stacking the columns of the matrix , and set .

Formulations (a) and (b) deliver an approximation that is not, in general, a matrix-function of , while in (c) the approximation is a primary matrix function by construction. However, as pointed out in [22], there are situations where the stochastic th root exists but it is not a matrix-function of , therefore (c) does not compute such a stochastic th root. On the other hand, since is a function of , a nice feature of formulation (c) is that the output matrix shares with the steady state vector. If both and are irreducible, this implies that , i.e., the asymptotic behavior of the Markov chains with transition matrices and , respectively, is the same. From the modeling point of view, this is a desirable property, since we expect that doing time steps of different “lengths” should always bring us to the same limit.

In this paper, we propose to compute a stochastic approximation to a th root of the stochastic matrix by relying on a Riemannian optimization approach. Indeed, it is well known that the set of positive stochastic matrices is a Riemannian manifold, called multinomial manifold [18]. Therefore, the first approach that we propose is to solve problem (a) in this Riemannian optimization setting. However, as in standard constrained optimization, the computed matrix is a stochastic matrix that generally does not share with the steady state vector. To overcome this drawback, given a positive vector such that , we introduce the Riemannian manifold of positive stochastic matrices, having as steady state vector. Such Riemannian manifold can be seen as the generalization of the Riemannian manifold of doubly stochastic matrices, which corresponds to the special case where . In order to apply the Riemannian optimization algorithms, we give an expression to the tangent space, to the orthogonal complement and orthogonal projection, and to the Riemannian gradient and Hessian, by extending the analog properties valid for doubly stochastic matrices. To define a retraction from the tangent bundle to the manifold, we use a generalization of the Sinkhorn-Knopp algorithm. Hence, given an irreducible stochastic matrix with stationary distribution , we approximate its stochastic th root by solving (a) in the manifold . In implementing the optimization algorithms we need to solve several singular symmetric linear systems; in this regard, we provide a lower and an upper bound to the nonzero eigenvalues of the matrix, which give information on the convergence of Conjugate Gradient-like methods. Moreover, we propose some preconditioners to improve the convergence of iterative methods for the solution of such linear systems.

The new Riemannian manifold has been implemented in Matlab, in a format compatible with the Manopt library [11]. The code is available in the GIT repository github.com/Cirdans-Home/pth-root-stochastic.

The proposed methods have been tested on a variety of stochastic matrices , with different properties, in terms of size and embeddability. An application to finance, where represents the transitions in the credit classes [26, 25], has been treated in detail.

In the cases where we are not interested in preserving the steady state vector, the comparisons between constrained optimization algorithms, integrating together trust region and interior point techniques [12], and the Riemannian-based optimizers for formulation (a) on the multinomial manifold, show that the latter achieve smaller or equal residuals, and they are generally faster. When we are interested in preserving the steady state vector, the numerical experiments on the Riemannian manifold show that, in some cases, the approximation of the th root of has a higher residual with respect to the approximation in the manifold of positive stochastic matrices. This is expected, since the set is smaller than the set . However, in general, optimization methods in set provide an approximation having a stationary distribution far from the stationary distribution of . In the application to credit ranking in finance, the matrix is reducible, therefore we apply our method to the irreducible stochastic matrix , , which resembles the Page Rank matrix. From the numerical experiments, the approximation of the th root has a structure close to the reducible structure of , and the numerical values of its entries are very realistic, from a modeling point of view.

The paper is organized as follows. In Section 2 we recall the main definitions concerning Riemannian manifolds and Riemannian optimization. In Section 3 we recall the properties of the multinomial manifold of positive stochastic matrices and solve problem (a) in the framework of Riemannian optimization in such a manifold. In Section 4 we introduce the Riemannian manifold of stochastic matrices having a common steady state vector , and solve problem (a) in this manifold. We present the numerical experiments in Section 5 and draw conclusions in Section 6.

1.1 Notation

In the following, the symbols “” and “” represent the Hadamard (entry-wise) matrix division and multiplication, respectively. Given a vector – always denoted in bold face – the symbol “” denotes the diagonal matrix having the entries of on the main diagonal; for notational simplicity, we will also denote . If is a square matrix, then “” denotes the vector formed by the diagonal entries of , and its spectrum. The notation concerning Riemannian geometry will be introduced at the time of their use. If , is said to be nonnegative (positive), and we write (), if all its entries are nonnegative (positive).

2 Preliminaries on Riemannian optimization

We start by recalling some definitions concerning Riemannian manifolds and Riemannian optimization. The interested reader may find more details on this subject in [18, 2, 10].

Definition 2.1 (Embedded Manifold).

Let be a linear space of dimension . A non-empty subset of is a smooth embedded submanifold of of dimension if either

-

•

and is open in ;

-

•

for some and, for each , there exists a neighborhood of in and a smooth function such that

-

–

If , then if and only if ; and

-

–

, for the differential of at ;

such function is called a local defining function for at .

-

–

A tangent vector to at a point is defined as follows:

Definition 2.2 (Tangent vector, tangent bundle).

A tangent vector to a manifold at a point is a mapping from the set of smooth real-valued functions defined on a neighborhood of to such that there exists a curve on realizing the tangent vector , i.e., such that , and

see, e.g., Figure 1. The tangent space at is then the set of all tangent vectors to at a point . The tangent bundle is the manifold that assembles all the tangent vectors, i.e., the disjoint union .

To further characterize the tangent at a point in the case of an embedded manifold, such as the ones we are interested in, we also report the following result.

Theorem 2.3 ([10, Theorem 3.15]).

Let be an embedded submanifold of . Consider and the set from Definition 2.2. If is an open submanifold, then . Otherwise with any local defining function at .

A Riemannian manifold is a manifold equipped with a positive-definite inner product on its tangent space, i.e., , for any . Such a metric, called Riemannian metric, induces the norm , for any .

On the Riemannian manifold, we can define the minimization problem

| (1) |

where is a suitable smooth function.

2.1 Optimization methods

Optimization methods for solving (1) on Riemannian manifolds use local pull-back from the tangent spaces to the manifold to produce a sequence of iterates, which can be interpreted as iterates moving along specific curves on the manifold, see the representation in Figure 2.

What distinguishes the different algorithms is how the new point on the tangent space is determined. In general, it is possible to adapt the different classes of optimization methods in this new context, consider, e.g., first order methods, Newton and Quasi-Newton methods, or Trust-Region methods, see, [2, Chapters 6,7 and 8] for a complete discussion.

In order to define these methods, we need to recall some differential structures for functions taking values on the manifold. We denote by the directional derivative of given by:

Definition 2.4 (Affine connection).

An affine connection is a map that associates to each in the tangent bundle (Definition 2.2) the tangent vector satisfying for all , and smooth :

-

•

-

•

-

•

,

wherein the vector field acts on the function by derivation, that is

We call Levi-Civita connection the affine connection that preserves the Riemannian metric, i.e., the affine connection such that

-

•

,

-

•

, ,

where we are denoting with the Lie bracket

Definition 2.5 (Riemannian Gradient and Hessian).

The Riemannian gradient of at , denoted by , of a manifold is defined as the unique vector in that satisfies:

The Riemannian Hessian of at , denoted by , of a manifold is a mapping from into itself defined by:

where is the Riemannian gradient and is the Levi-Civita connection on .

Definition 2.6 (Retraction).

A retraction on a manifold is a smooth map from the tangent bundle , i.e., the disjoint union of the tangent spaces, onto . For all the restriction of to , denoted by , satisfies the following properties:

-

•

(centering);

-

•

The curve satisfies

To characterize retractions for embedded manifolds we will use the following result, that we report here for the sake of completeness.

Theorem 2.7 ([2, Proposition 4.1.2]).

Let be an embedded manifold of the Euclidean space and let be an abstract manifold such that . Assume that there is a diffeomorphism

where is an open subset of , with a neutral element satisfying

Under the above assumption, the mapping

where is the projection onto the first component, defines a retraction on the manifold for all and in the neighborhood of .

The general sketch of Newton’s method for solving (1) on a Riemannian manifold is synthesized in Algorithm 1. For other optimization methods, we refer to [2, Chapters 4,6–8].

3 Stochastic th root approximation via Riemannian optimization

Here we propose an approach based on Riemannian optimization, to numerically approximate the solution of problem (a).

Indeed, by following [18], we endow the set of stochastic matrices with positive entries, namely

with both a manifold structure (in the sense of Definition 2.1) and an intrinsic metric, making it a Riemannian manifold [18, 32], known as multinomial manifold. The solution of problem (a) is approximated within such a manifold.

On , we need to define the tangent space . By applying the definition, we find that if is a smooth curve such that and for any in a neighborhood of the origin, then the curve satisfies

thus while the opposite inclusion holds by comparing the number of degrees of freedom of the full space, and of the tangent space (see [18, Proposition 1] and Theorem 2.3), so that

Therefore, can be extended to be a Riemannian manifold by adding a positive-definite inner product on its tangent space at every point. This metric is given by the Fisher information metric

| (2) |

On the multinomial manifold , we can define the analogous of problem (a) as follows:

| (3) |

The two substantial differences with respect to the standard formulation are, on the one hand, the explicit request to have the elements of , on the other hand, the possibility of exploiting the Riemannian manifold structure to compute the solution of problem (3). Let us also stress that the constraint , needed for the definition of the metric, makes difficult obtaining general conditions of existence for the solution of (3). In the numerical experiments, we investigated cases in which the target matrix does not satisfy this constraint.

In particular, since the multinomial manifold is already defined in the MANOPT library [11],

to apply for instance the Riemannian version of the Trust Region optimization procedure, we can use a few lines of MANOPT code.

Indeed, given a stochastic matrix A} with \mintinlinematlabn = size(A,1), and given an integer

p}, it is sufficient to write \beginminted[bgcolor=bg,fontsize=]matlab manifold = multinomialfactory(n,n); problem.M = manifold; problem.cost = @(x) 0.5*cnormsqfro(mpower(x,p).’-A); problem = manoptAD(problem); options.tolgradnorm = 1e-7; [x, xcost, info, options] = trustregions(problem,[],options); Some attention is needed since in the multinomial manifold of the MANOPT library, matrices are column stochastic instead of row stochastic. The variable

x} contains an approximation to the solution of \eqrefeq:the_rewritten_problem. To illustrate the behavior of this approach, we consider the following example from [22, Fact 4.10].

Example 3.1.

Let us consider the matrix

having eigenvalues . This matrix is circulant and symmetric (and therefore doubly stochastic), and has only one stochastic square root, which is not a primary function, given by

This matrix is doubly stochastic and its eigenvalues are . Setting , an application of the optimization strategy produces

In this case the steady state vector of has an absolute difference with respect to the steady state vector of of , indeed this is mostly due to the fact that there exists a stochastic square root, which is also doubly stochastic, and the optimization method converges to such a matrix.

Example 3.2.

We consider the matrix Pajek/GD96_c from the SuiteSparse matrix collection as the adjacency matrix of an undirected graph normalized by the inverse of the sum of the row entries, then is a stochastic matrix, and we can apply the optimization strategy for . In this case, there doesn’t seem to be a stochastic square root matrix to converge to, since the residual of the optimization procedure is . Furthermore, as shown in Figure 3, the proposed approximation has a different stationary distribution with respect to , therefore the “half step” linked to it cannot converge to the same stationary state of the global system. For this reason, in the next section we will focus on the computation of an approximation of the root that preserves the stationary distribution.

4 Stochastic th root approximation preserving the stationary distribution

In this section we first introduce the manifold of positive stochastic matrices, having the same stationary distribution , . Then, given a stochastic matrix with stationary distribution , we approximate its stochastic th root on such a manifold. This way, the stochastic th root approximation of shares with the stationary distribution.

4.1 A new Riemannian manifold

Let be a positive vector such that , and define the set

i.e., is the set of positive stochastic matrices, having the same stationary distribution . After proving that is a manifold, the analogous of problem (a) is rewritten as:

By following the approach used in [18] for the manifold of doubly stochastic matrices, we may prove that is an embedded manifold of of dimension , since it is indeed generated by linearly independent equations. The following result characterizes the tangent space:

Lemma 4.1.

The tangent space to at is given by

| (4) |

Proof 4.2.

Let be any smooth curve such that and for in a neighborhood of the origin. By differentiating, we find

thus we have

To prove the opposite inclusion, we observe that the space is defined by independent equations. Since the whole space has size , then the dimension is given by which equals the size of the space of matrices with a given left- and right-eigenvector. Therefore, the set we defined has the same dimension as the tangent space, so that they coincide.

The manifold , endowed with the Fisher metric (2), is a Riemannian manifold. To use any optimization strategy we need an expression for the projection operator on the tangent space

For a and an , we can express the orthogonal projection by using the decomposition of any ambient vector into

| (5) |

Lemma 4.3.

The orthogonal complement of the tangent space has the expression

for some vectors .

Proof 4.4.

Let , for some vectors . Then

since for a we have and . Therefore, we have , , i.e., . To prove the opposite inclusion we use a dimensionality argument. Let us introduce the non-singular diagonal matrix and observe that

Then, the quantity on the right depends only on the first row and column of , since

Therefore, the dimension of the orthogonal complement of the tangent space has the correct dimension .

The above result allows us to give an expression for the orthogonal projection with respect to the scalar product induced by Fisher’s metric (2):

Proposition 4.5.

The orthogonal projection of a matrix –with respect to the scalar product induced by Fisher’s metric (2)–has the following expression:

where the vectors and are a solution to the following consistent linear system

| (6) |

Proof 4.6.

The formula for the orthogonal projection follows from Lemma 4.3. To find an expression for the vectors and , we use (5) and obtain

From Lemma 4.3, we find that

that is

i.e., in matrix form,

Similarly, by transposing (5), we obtain

From the properties of the Hadamard product, we find that

and

Therefore, we conclude that

so that the vectors and can be found as a solution of the linear system

The linear system is consistent with an affine space of solutions of dimension one, since

and

Let now be a smooth real function defined on the manifold, and denote by its euclidean gradient with respect to the euclidean metric. Then we can express the Riemannian gradient as follows.

Proposition 4.7 (Riemannian gradient).

The Riemannian gradient is expressed in terms of the Euclidean gradient as:

| (7) |

Proof 4.8.

We prove (7) by directly applying the Definition 2.5 of the Riemannian gradient. Indeed, the Riemannian gradient is the unique element of for which the directional derivative and the Riemannian metric satisfy the equation

| (8) |

Therefore if we find an element of for which (8) holds for all tangent vectors, then this is the Riemannian gradient. We start by writing the Euclidean gradient in terms of the directional derivative and the Euclidean scalar product as:

Restricting the previous to , and changing the inner product to the one induced by the Fisher metric (2) we find

To reach the conclusion we now need to apply again Lemma 4.3 and (5) to project the (scaled) Euclidean gradient

From this we find

having canceled out the second term by means of the definition of the orthogonal complement. Summarizing, we have thus shown that is a tangent vector that satisfies the condition (8), that permits us to conclude by the uniqueness of the Riemannian gradient that:

To implement Algorithm 1 we also need an expression for the Riemannian Hessian. From Definition 2.5, the Riemannian Hessian is related to the Levi-Civita connection, thus we first need a way of expressing the Levi-Civita connection for the metric (2).

Proposition 4.9 (Koszul formula, [2, Theorem 5.3.1]).

Theorem 4.10 (Riemannian Hessian).

The Riemannian Hessian can be obtained from the Euclidean gradient and the Euclidean Hessian by using the identity

where

and

Proof 4.11.

To obtain the first identity it is sufficient to use the Koszul formula (Proposition 4.9)

Then, we need to find an expression for . To find it, we denote ; from the properties of the Fréchet derivative we find that

Now we need an expression for , , and . Concerning , we have

To find an expression for and , we compute the derivative along the direction of both sides of the linear system

Therefore, we obtain

so that and can be computed by solving the linear system (with the same system matrix)

.

To complete the construction of the Riemannian optimization algorithm, we also need to define the retraction from the tangent bundle to the manifold (Definition 2.6). To obtain such a map, we apply a suitable modification of the generalized Sinkhorn-Knopp algorithm [30], which is based on the following theorem:

Theorem 4.12 (Sinkhorn generalization, [30, Theorem 2(a)-(b)]).

Let be a nonnegative matrix. Then for any vectors with nonnegative entries there exist diagonal matrices and such that

if and only if there exists a matrix such and , and having the same nonzero pattern as . Furthermore, if the matrix is positive, then and are unique up to a constant factor.

From the previous result, we can obtain the following generalization which allows us to obtain a matrix on the manifold through suitable diagonal scaling.

Proposition 4.13.

Let be a matrix with positive entries. Then there exist diagonal matrices and such that

Moreover, and are diagonal matrices such that and , where .

Proof 4.14.

Consider the matrix . By setting , according to Theorem 4.12 applied to , there exist diagonal matrices and such that and . Since diagonal matrices commute, from the first equality we obtain , so that ; from the second equality, we find that , i.e., .

The above result, combined with Theorem 2.7, provides an expression for the retraction to the manifold .

Theorem 4.15 (Retraction).

The map whose restriction to is given by:

| (9) |

is a well-defined retraction on in the sense of Definition 2.6 whenever is in a neighborhood of , i.e., whenever entry-wise.

Proof 4.16.

Since an embedded manifold, we apply Theorem 2.7, where the diffeomorphism is obtained by means of the extension of the Sinkhorn theorem given in Proposition 4.13. Since we deal with matrices with positive entries, the result in Proposition 4.13 is invariant with respect to the scaling and . Thus we can assume, without loss of generality, that the first diagonal element . Then, the map we need to construct is given by

Such satisfies all the requirements of Theorem 2.7. Indeed, both and are manifold as open subsets of the manifolds and , respectively. Furthermore, they satisfy the dimensionality relation since

Finally, the identity element of satisfies , and inherits the required regularity from the regularity of the matrix product. To build the projection in Theorem 2.7 we need the existence of the inverse map . This amounts to an application of the (modified) Sinkhorn-Knopp’s algorithm scaling the rows and the columns of the matrix. Observe that this is again a smooth map for the regularity of the matrix product. We have therefore proved that is a diffeomorphism. By Theorem 2.7, this means that is a retraction for in the neighborhood of , i.e., which can explicitly written in an element-wise sense as . Using the definition of and Lemma 4.1 the inverse map is the identity, since

hence, the canonical retraction is defined as .

To avoid the deterioration of the quality of the analogous retraction on in the presence of small modulus elements in the iterations of the Riemannian optimization algorithms, in [18] a modification based on the combination of the entry-wise exponential of a matrix and the Sinkhorn-Knopp’s algorithm (Theorem 4.12) is proposed. We adapt here such proposal to the manifold .

Theorem 4.17.

The map whose restriction to is given by:

| (10) |

is a first-order retraction on , where represents an application of the modified Sinkhorn-Knopp’s algorithm in Proposition 4.13, and the entry-wise exponential.

Proof 4.18.

We need to show Definition 2.6 is verified. The map (10) is centered, since for an

having selected in Proposition 4.13. To prove the local rigidity, we need to show that the curve satisfies

By definition

where the last equality follows from the first order Taylor expansion of the exponential

As in the proof of Theorem 2.7, we can now select small enough for having a matrix with all positive entries, and apply Proposition 4.13 to write

since we have , hence

We exploit now that (Lemma 4.1), and write

equivalently

The null space of is generated by the vector, equivalently , hence . Therefore, we have just proved that , and consequently

4.2 Computational issues

We have implemented this new Riemannian manifold in a format compatible with the Manopt library [11], i.e., we have produced a Matlab function that outputs a struct} variable whose fields implement the operation on the manifold, i.e., the \mintinlinematlabfunction with prototype

in which the optionsolve} contains options concerning the solution of the auxiliary linear systems, that can be selected when instantiating the manifold. The implementation is based on the \verb|multinomialdoublystochasticfactory.m| code by A. Douik and N. Boumal; see~\citeDouik8861409 and the relevant references in [11].

For the computation of the various projections on the tangent space and for the computation of the Riemannian Hessian we have to solve several compatible singular linear systems of the form

| (11) |

To this purpose, we want to use an iterative method of the Krylov type to avoid assembling the block matrix. Since the system is symmetrical, an indication of the convergence properties can be obtained starting from the spectral properties of the matrix .

Proposition 4.19 (Spectral properties).

Given , the block matrix defined in (11) is such that

-

•

is similar to a singular M-matrix,

-

•

, for

and is such that ; moreover, if , then .

Proof 4.20.

The matrix

is a Z-matrix. Since , then is a singular M-matrix [7]. In particular, its eigenvalues have non negative real part [7]. On the other hand, since is symmetric, then its eigenvalues are real. Therefore the eigenvalues of are . Since is irreducible and , then the matrix is irreducible as well, therefore . Since

then , which implies

To obtain a lower-bound we use the eigenvalue interlacing Theorem [23, Theorem 4.3.6] for symmetric matrices. Indeed, by removing the -th column and row from we obtain a matrix whose eigenvalues are such that

Therefore, a lower bound to gives a lower bound to . For the moment, assume that . Since is a positive matrix, then is irreducible, therefore, by using the same arguments as for to show that , we deduce that . To give a positive lower bound to , consider the parametric similarity transformation for

where is the matrix obtained by removing the last column of the matrix . Let us call the -vector generating the diagonal matrix in the block, then we can estimate the smallest eigenvalue by Gershgorin Theorem [23, Chapter 6], that is, we can estimate by the intersection with the axis of the left-most circle. The circles for the first rows have center in and radii

whilst the circles for the last rows have center and radii . Thus we have

for

Observe now that, instead of removing the last row and column in , we can optimize the bound by selecting the column to which corresponds

and the corresponding

We can then solve the problem by solving the minimization problem

which is therefore equivalent to obtaining the positive root of the quadratic equation

The lower-bound is then given by

We can further elaborate on the above bound. Indeed, since , we obtain

so that

This latter inequality makes sense if .

In Section 5.2.1 we show, through some numerical experiments, the sharpness of the bounds given in the above proposition. The eigenvalue properties proved in Proposition 4.19 suggest different strategies to solve the linear system (11). Firstly, we can directly apply the Conjugate Gradient (CG) to the linear system, in fact, if the starting vector is not in the null space of the matrix, we do not undergo a breakdown; some preconditioning strategies are discussed in the sequel. Secondly, we can consider using the LSQR method on the system instead. To reduce the dimensionality of the problem, we can solve the system for the Schur complement with respect to the -block, i.e. we solve instead

| (12) |

The matrix in the above system is a symmetric irreducible singular M-matrix, therefore it is semidefinite, with a simple eigenvalue equal to 0. In both formulations (11) and (12), since the basis of the null space is known, we can consider the de-singularized version obtained through a rank 1 update of the matrix; so that, in small size problems, we can employ the -factorization to solve the associated linear systems. Specifically, for the -block formulation (11), this consists in solving the updated linear system

Indeed, we may easily observe that solves also the original linear system (11). It is worth to point out that linear systems with matrices of the kind , where is positive semi-definite and is low rank, arise in various applications (see for instance [6]). In our case the correction is rank-one, and it is made by an eigenvector of , so that the eigenvalues of the new matrix are the eigenvalues of the matrix , except for the eigenvalue 0 which is replaced by 1. Since, for Proposition 4.19, the upper bound on the eigenvalues of is , we expect that the rank one update does not modify conditioning of the linear system (11). For the Schur complement version (12), the updated system is given by

where . As in the previous case solves also the original linear system (11).

Moreover, the eigenvalues of the matrix in the above system are the eigenvalues of the matrix , except for the eigenvalue 0 which is replaced by . In order not to deteriorate the conditioning of the system, the parameter should be chosen between the smallest nonzero eigenvalue and the largest eigenvalue of the matrix . By using Gershgorin theorem, an upper bound to the spectral radius is given by , while a lower bound can be found by using the Cauchy interlacing theorem, as in the proof of Proposition 4.19, by bounding the smallest eigenvalue of a principal matrix. Therefore might be chosen as the arithmetic mean between these two bounds.

The different strategies can be selected through the optionsolve} variable in the definition phase of the manifold. Default values can be generated through the \mintinline[breaklines,breakanywhere]matlabinitoptions() function, i.e., optionsolve = initoptions()}. The user can select between the $2\times 2$-block formulation of the linear system (\mintinline[breaklines,breakanywhere]matlaboptionsolve.formulation = ”block”;) and the reduction to the Schur complement (optionsolve.formulation = "schur";}). In both cases the desingularization strategy via the rank-1 update can be activated (\mintinline[breaklines,breakanywhere]matlaboptions.correction = true;). The solution method for the linear systems can then be selected between the direct strategy (options.method = "direct";}), the CG (\mintinline[breaklines,breakanywhere]matlaboptions.method = ”cg”;), and the LSQR method ((

options.method = "lsqr";}). All the options are case-insensitive. Additional debugging and tracing options can be enabled through this facility and are discussed in the code. To precondition the CG algorithm we start from an empirical observation, since the target matrix $X$ has to be stochastic we expect, as the dimension $n$ of the problem grows, to encounter a large number of small entries. This suggests using a \emphdiagonally compensated modified incomplete Cholesky [31, Section 10.3.5] directly on the system matrix. The diagonal compensation term, to avoid the presence of nonpositive pivots, can be taken to be . Another strategy consists in first scaling the system

and then recover

By calling , and observing that , we can use a truncated Neumann series as preconditioner, i.e.,

| (13) |

The two strategies can be selected by choosing options.method = "pcg";} or \mintinline[breaklines,breakanywhere]matlaboptions.method = ”pcg2”; respectively in the code. In both cases, the preconditioner must be regenerated anew at each outer iteration of the optimization method, i.e., whenever we move the tangent space.

The overall cost of the procedure is dominated by matrix-power operations needed for the computation of the objective function. Furthermore, we always need to store at least a dense matrix of the same size of the problem. All the proposed approaches for the solution of the auxiliary linear systems reduce the storage cost and require a number of operation that is less than cubic. The MATLAB implementation is expected to work on current standard computer for matrices of size up to few thousands.

5 Numerical Examples

In this section, we will compare the algorithms based on Riemannian optimization with the methods available in the literature. We will also validate the theoretical results discussed in Section 4.2 concerning the location of eigenvalues. Specifically, in Section 5.1 we compare the Riemannian optimization on the manifold with the methods based on constrained optimization available in the literature. Then, in Section 5.2 we test the new approach that preserves the stationary distribution, i.e., the Riemannian optimization routines on the manifold. Furthermore, we numerically investigate also the computational issues discussed in Section 4.2. Finally, in Section 5.3 we test our algorithms on an application in finance, where is the transition matrix of a Markov chain which represents the dynamics of the different credit ratings. The peculiarity of this problem is that is reducible, therefore its invariant distribution is not positive, so the manifold cannot be defined. The numerical examples have been executed on a Laptop with Intel® Core™ i7-8750H CPU @ 2.20GHz with 16 Gb of memory, and running MATLAB 2023a and Manopt v.7.1. Code and examples are available in the GitHub repository github.com/Cirdans-Home/pth-root-stochastic and can be reproduced.

5.1 Stochastic th root approximation via Riemannian optimization

In this section, we address the problem of the stochastic th root approximation via Riemannian optimization with the manifold described in Section 3. We compare the Riemannian algorithm with the interior point method implemented in the MATLAB routine fmincon}~\citeinteriorpoint. For the construction of the test matrices, we have prepared a generator of stochastic matrices of different classes matrixgenerator(n,p,seed,classes,numbers)} that produces matrices of which we want to approximate the stochastic $p$th root; the classes are described in the Table~\reftab:matrix-classes.

code. The routine also allows fixing the seed of the random number generator so that the set of matrices generated for equal parameters is always the same.| Name | Description | Size | Embeddability | Ref. |

|---|---|---|---|---|

| uniform stochastic | \mintedmatlab B = rand(n,n); D = diag(sum(B,2)); A = D\B; \endminted | unknown | ||

| th power of uniform stochastic | \mintedmatlab B = rand(n,n); D = diag(sum(B,2)); A = mpower(D\B,p); \endminted | yes | ||

| of intensity matrix | \mintedmatlab B = rand(n,n); B(1:1+n:end) = 0; D = diag(sum(B,2)); A = expm(B - D); \endminted | yes | ||

| K80 | \mintedmatlab b = rand(1); c = sqrt(b)-b; a = 1-b-2*c; A0= [a,b;a,b]; E = ones(2,2); A = [A0,c*E;c*E,A0]; \endminted | 4 | yes | [13] |

| \mintedmatlab b = 0.5*rand(1); c = (1-2*b)/2; a = 1-b-2*c; A0 = [a,b;a,b]; E = ones(2,2); A = [A0,c*E;c*E,A0]; \endminted | 4 | no | [13] | |

| Pei | \mintedmatlab I = eye(n,n); J = ones(n,n); alpha = rand(1)-(1/(n-1))^p; beta = (1-alpha)/n; A = alpha*I+beta*J; \endminted | yes | [28] |

To obtain the approximation we use the formulation (a) and generate stochastic test matrices for each class, where the dimension of the matrices with variable size is . As Riemannian optimization algorithms we consider the trustregions} algorithm~\citegenrtr and the rlbfgs} algorithm~\citeHuang2016. The trustregions} algorithm uses both the cost functional, its gradient, and an approximation of the Hessian. On the other hand, the \mintinlinematlabrlbfgs algorithm uses only the cost functional, and the gradient. To approximate Euclidean gradients and Hessian matrices we use automatic differentiation (AD) instead of defining them analytically. All methods are initialized from the same starting point generated as a random point on the manifold of stochastic matrices . We measure the quality of the obtained results in terms of the residual on the cost functional (a) and on the time necessary to carry out the optimization. We report the data in the form of a performance profile in Figure 4; see [17, Section 2] for the general usage of performance profiles to compare algorithms.

The results show that the Riemannian algorithms perform much better than their counterpart based on constrained optimization. Both the execution times and the residuals are practically always lower. Furthermore, no significant difference is observed between the use of the LBFGS and the trust-region algorithm, i.e., the two lines are practically overlapping and have little difference on an extremely low percentage of problems.

5.2 Stochastic th root approximation preserving the stationary distribution

In this section, we compare the two Riemannian optimization algorithms on the manifolds and , for the different test matrices from Table 5.1. Specifically, we compare the stationary distribution of the approximation obtained in the two manifolds, with the stationary distribution of , by using the same tolerance request on the gradient norm (1e-4}) and the same starting point for the optimization algorithm (\mintinlinematlabX0 = M.rand()) which, in this case, is the trustregions method.

and tolerance of the gradient of for a matrix generated from the classes in Table 5.1. The right panel reports the infinity norm error between and , i.e., . The dashed line represents the floating-point relative accuracy of MATLAB’s double-precision number.

5.2.1 Properties and solution of the associated linear systems

To validate the results of the bound given by the Proposition 4.19 we consider the test matrices from Table 5.1. Specifically, we first build the manifold associated with the stationary distribution for each matrix in the

class, then we generate a random point on that manifold and the associated block matrix needed for computing the projection on the tangent space associated with that point, i.e., the matrix in (6). Figure 6 reports the result of such an experiment.

Figure 6: Bound from Proposition 4.19 for the matrices built on the manifolds associated with the stationary distribution of the test matrices from Table 5.1. The vertical bars denote the bounds (red for the upper, blue for the lower), and the black dots are the numerically computed eigenvalues.

We observe that the upper bound is more accurate than the lower one.

As a second exploration, we consider the different solution strategies of associated linear systems discussed in Section 4.2. Let us first consider a case outside the optimization algorithm. That is, we generate the manifold , where is the stationary distribution associated with the out-degree random walk on the graphs from Figure 5.2.1.

’HB/gre_115’}]

5.3 The case of reducible Markov chains

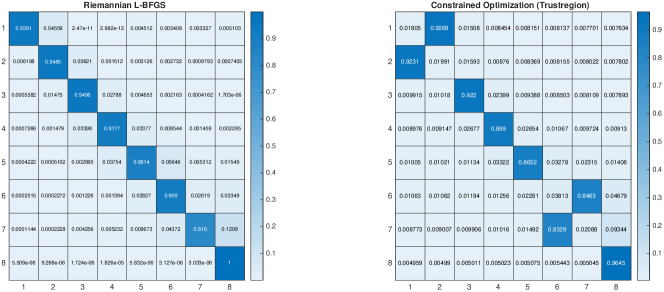

We consider here what is an edge case for our approach, i.e., when the chain is reducible due to the existence of two communication classes; in other words, to the case in which the stationary distribution . This case is motivated by the embedding problem for Markov models of the term structure of credit risk spreads [26]. The Markov chain modeling represents the dynamics of the different credit rating states, i.e., evaluations of the relative ability of an entity or obligation to meet financial commitments over time and examining the probability of transitioning in between these states. The different levels go from AAA, the lowest expectation of default risk, to D, for an issuer who has entered into bankruptcy and cannot recover from it. In Table 5.3 we report sample data from [26].

data(i,j)} & \textttAAA

AA

A

BBB

BB

B

CCC

D

AAA

0,891

0,0963

0,0078

0,0019

0,003

0

0

0

AA

0,0086

0,901

0,0747

0,0099

0,0029

0,0029

0

0

A

0,0009

0,0291

0,8894

0,0649

0,0101

0,0045

0

0,0009

BBB

0,0006

0,0043

0,0656

0,8427

0,0644

0,016

0,0018

0,0045

BB

0,0004

0,0022

0,0079

0,0719

0,7764

0,1043

0,0127

0,0241

B

0

0,0019

0,0031

0,0066

0,0517

0,8246

0,0435

0,0685

CCC

0

0

0,0116

0,0116

0,0203

0,0754

0,6493

0,2319

D

0

0

0

0

0

0

0

1

. (d) Entries of the approximated square roots

(d) Entries of the approximated square roots

6 Conclusions and future directions

In this paper, we have dealt with the problem of approximating the th root of a stochastic matrix with a stochastic matrix. In particular, by observing that stochastic matrices form a Riemannian manifold with respect to the Fisher metric, we have exploited several specific optimization algorithms which show better performance than their counterparts that use only constrained optimization. Furthermore, we have introduced a new Riemannian manifold—employing the same metric—on the set of stochastic matrices with fixed steady state. This allowed us to employ Riemannian optimization algorithms capable of obtaining approximations of stochastic th roots which also preserve such vector, i.e., such that the Markov chain induced by them has the same steady state. We have also shown that we can apply the proposed strategy to the case of non-reducible Markov chains through a perturbation technique.

In the future, we intend to study the geodetic structure of this new manifold to better characterize the obtained th root approximations, and to further investigate the solution of the associated computational problems, e.g., the solution of the linear systems needed to calculate the projections from the tangent plane to the manifold and the representation of the Riemannian Hessian, in order to further improve the computational efficiency of the proposed methods.

Acknowledgements

We thank the two anonymous reviewers whose comments allowed us to improve the presentation and clarity of the paper.

References