AI and ethics in insurance: a new solution to mitigate proxy discrimination in risk modeling

Abstract

The development of Machine Learning is experiencing growing interest from the general public, and in recent years there have been numerous press articles questioning its objectivity: racism, sexism, …Driven by the growing attention of regulators on the ethical use of data in insurance, the actuarial community must rethink pricing and risk selection practices for fairer insurance. Equity is a philosophy concept that has many different definitions in every jurisdiction that influence each other without currently reaching consensus. In Europe, the Charter of Fundamental Rights defines guidelines on discrimination, and the use of sensitive personal data in algorithms is regulated. If the simple removal of the protected variables prevents any so-called ‘direct’ discrimination, models are still able to ‘indirectly’ discriminate between individuals thanks to latent interactions between variables, which bring better performance (and therefore a better quantification of risk, segmentation of prices, and so on). After introducing the key concepts related to discrimination, we illustrate the complexity of quantifying them. We then propose an innovative method, not yet met in the literature, to reduce the risks of indirect discrimination thanks to mathematical concepts of linear algebra. This technique is illustrated in a concrete case of risk selection in life insurance, demonstrating its simplicity of use and its promising performance.

Keywords Machine Learning AI & Ethics Discrimination Proxy discrimination Fairness Proxy discrimination

General introduction

1 Motivation and scope of this paper

In many sectors, Machine Learning models have been exposed as unintentionally discriminatory, leading to unfair decisions that can have drastic consequences. The insurance industry has always been under close scrutiny when it comes to the use of personal data and discrimination issues, but in the light of recent denunciations in all industries, the attention on fairness issues has grown.

Fairness is a complex philosophical matter, and there is no single definition for it. Researchers have managed to define it statistically, but the definition depends on underlying assumptions and ideologies. Furthermore, as of today, many methods have been proposed to come closer to some definitions of fairness, but none can ensure perfect fairness.

Regarding previous points, we wonder to what extent fairness can be approximated when applying a Machine Learning model to insurance mortality data, and more specifically to what extent proxy discrimination can be avoided. This thesis aims at illustrating the complexity of quantifying discrimination and finding a way to mitigate it. For this purpose, we propose a simple and promising method that relies on linear algebra to mitigate indirect discrimination.

All along the thesis, we have provided the reader with summaries and key points in the form of light blue frames.

2 Understanding key concepts and regulations around discrimination

2.1 The life insurance industry

Historically, life insurers have used classic statistical models to assess risks for their products, covering Mortality, Critical Illness111Critical illness insurance compensates insureds with a lump sum payment upon diagnosis in order to cover treatment costs Blyth (2022)., Disability, Longevity and Medical Expenses. But with the development of Machine Learning and the now richer than ever data sources, new techniques are becoming more and more popular. These methods imply new challenges for actuaries, mostly due to the richness of information and the complexity of algorithms.

2.1.1 Actuarial fairness

One of the challenges concerns the notion of equity, which has always been a key issue for insurers. ‘Actuarial fairness’ means that risky insureds should contribute more and pay a higher premium. Actuaries have to determine how to classify policyholders between risky and non-risky, and more specifically what attributes are good indicators of risk. They then rely on historical data to estimate losses Grari (2022). It is sometimes complicated to know if an attribute is directly related to risk or not. As we will see later on, there are country-specific regulations concerning the use of certain attributes for risk assessment.

2.1.2 Segmentation, pooling and adverse selection

Before insurance, the only way of hedging against risk was individual prudence. Pooling offered a new way to deal with uncertainty: losses were the collective responsibility of the pool. This created insurance solidarity with an understanding of fairness Frees and Huang (2021). Today, insurers offer contracts at large levels, counting on the compensation between policyholders who file claims and those who do not. In order to ask for premiums accordingly to a policyholder’s risk profile, insurers do a segmentation of the insureds Charpentier (2022). Segmentation consists in creating homogeneous classes and estimating the risk on average Barry and Charpentier (2022), so that premiums are adapted to the risk profile.

The pure premium is the expected loss of the insured over the coverage period. Since pooling is based on the law of large numbers, risks have to be homogeneous, which is why insurers need to classify the risks properly. The classification is based on observable factors, which should indicate what the risk is Grari (2022).

If groups are heterogeneous, policyholders could cross-subsidy. This leads to adverse selection: lower risks are asked to pay more than their expected loss because they are not classified in the right pool, so they are attracted by a competitor who will offer lower prices.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_segmentationpooling.png)

2.1.3 Risk modeling

Life insurers model biometric risks, which relate to human life conditions, and more specifically the duration until the occurrence of an event. In our case, we will be studying the mortality of cancer patients.

Individuals with cancer history are considered ‘aggravated risks’ and are often offered coverage with deterrent premiums, based on limited and imprecise criteria. But each cancer is specific and the evolution of treatment possibilities has tremendously increased survival odds in the past few years. At SCOR, the medical underwriting team is in charge of providing inclusive solutions for cancer patients. By using all available information about individuals, we can precisely estimate mortality rates thanks to Machine Learning models. These precise rates help insurers offer fair premiums to individuals with a history of cancer.

For cancer patients, insurers model the duration before death in the context of mortality or longevity products. Information about these individuals can also be used for critical illness products, to model the duration before the occurrence of a cancer. Once the R&D department has studied the rates linked to the covered condition, the pricing team takes over to put the add-on cover or product on the market. The underwriters can also benefit from the study to better assess risk profiles.

To do this modeling, we need to take into account a few constraints:

-

•

Underwriting constraints: the variables used by the model need to be available to the underwriter, i.e. be included in the medical file of the individual. Depending on the local legislation, models must not be discriminatory against certain population, so as a ‘solution’, some variables are simply deleted. The insurer also has business constraints as he is in a competitive market.

-

•

Medical constraints: the variables and the coefficients they are attributed need to be coherent with medical literature. For example, variables that are not medically relevant, such as the address, cannot be used by the model. Another example of variable coherence is if a larger tumor size implies a shorter life expectancy, it must be reflected by the model.

-

•

Modeling constraints: the variables must be statistically relevant, not too numerous nor strongly correlated with each other.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_constraintsvariables.png)

2.2 Fairness and bias

As we saw with the constraints of variable selection, depending on the local regulation, selected variables must not lead to discriminatory results. Fairness and bias is not a new subject in Machine Learning, but it has received increasing attention these past years, as numerous examples of unfair and biased outcomes were revealed in various fields. The most famous one is the COMPAS Recidivism Algorithm, which was proved biased against black defendants Larson et al. (2016). As actuaries use high dimensional data and complex models, to price contracts for example, they need to check that the outcomes are not biased. We need to define fairness and bias, see how it impacts insurance and find a method to detect it.

2.2.1 The need for fairness in insurance

Reputation

Fairness is a key issue in insurance, because actuaries need to explain to underwriters how their models work, so that in turn policy applicants can understand and trust the process to be fair. Insurance is not a well-seen sector in the public opinion and by the authorities in general, which is why fairness and transparency are crucial subjects.

Regulation

In the EU, the GDPR (General Data Protection Regulation) gives individuals the right to control their personal data, and specifically ‘the right not to be subject to a decision based solely on automated processing, including profiling, which produces legal effects concerning him or her or similarly significantly affects him or her’ GDPR.eu (b). This means that a human intervention is required in any automated decision process. Individuals also have a right to erasure, or ‘right to be forgotten’ GDPR.eu (a), which means that datasets might not be complete, independently of the collection process.

But there are specific regulations for the insurance sector. The French Supervisory Authority, the ACPR, requires appropriate data management, with ethical considerations such as fairness of processing and absence of discriminatory bias ACPR (2022).

In April 2021, the EU proposed the first-ever legal framework on Artificial Intelligence (AI), the AI Act. The proposal is to define four levels of risk, from unacceptable to none, concerning AI systems. Each category will be subject to requirements and specific obligations such as conformity assessments and registration in a database. It could become applicable as soon as the second half of 2024 Commission . Insurers do not know how they will be impacted by this new regulation, but if their AI systems are classified as risky, they will be under strict regulation.

All in all, there is a regulation stacking that needs to be understood. The real question is: which regulation will be predominant?

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_needfairness.png)

2.2.2 A multitude of points of view

Fairness is a relative notion that has many different definitions. A. Narayanan gave 21 definitions for fairness in classification tasks Narayanan (2018). It is a legal requirement, but also an ethical concept Charpentier (2022). Definitions can be categorized into individual or group fairness. Individual fairness aims to treat similar individuals similarly and group fairness treats different groups equally Mehrabi et al. (2019). But group fairness might appear unfair at the individual level and a generalization based on group membership may be wrong Binns (2019). There are therefore two opposite worldviews regarding fairness with respect to a specific task: We’re All Equal (WAE), meaning all groups have similar abilities, and What You See Is What You Get (WYSIWYG), meaning observations reflect similar abilities Bellamy et al. (2018). From this, many statistical definitions have been created to measure fairness for model outcomes, mostly for classification. We will study some of them in detail later on.

Machine Learning is a statistical discrimination by nature, but it becomes objectionable when there is a systematic advantage for some privileged group. All definitions of fairness cannot be reconciled and cannot satisfy all aspects. There needs to be a legal study to provide an official definition of fairness and an associated metric.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_multitudepointsofview.png)

2.2.3 The different types of bias

Statistical fairness is strongly related to bias, which can be defined differently depending on the sector. In statistics, it is a systematic error in prediction outcomes Bellamy et al. (2018). For Machine Learning models, it can be introduced by users, come from the data or be amplified by algorithms. And it is a vicious circle, as algorithms learning from biased data give biased outcomes which will be fed into and amplified by future algorithms Mehrabi et al. (2019).

There are three types of biases that appear in classification problems Barry and Charpentier (2022):

-

•

Type 1: classes do not reflect the reality of the risk,

-

•

Type 2: classes reflect a correlation with risk that is non-causal,

-

•

Type 3: classes reflect a causal statistical reality, but are unacceptable because of ethical reasons.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_bias.png)

2.2.4 Unfair and fair discrimination

To better understand and scope the concept from a scientific point of view, we discussed with different lawyers specialized in data law. Those exchanges helped us focus on the different key concepts exposed below.

Legal definition

Discrimination is the difference in treatment between individuals in similar situations due to prohibited criteria. In France, the Penal Code pen defines these criteria in the Article 225-1:

‘their origin, their sex, their family situation, their pregnancy, their physical appearance, the particular vulnerability resulting from their economic situation, apparent or known to its author, their surname, their place of residence, their state of health, their loss of autonomy, their disability, their genetic characteristics, their morals, their sexual orientation, their gender identity, their age, their political opinions, their trade union activities, their ability to express themselves in a language other than French, their membership or non-membership, real or supposed, of an ethnic group, a nation, a so-called race or a determined religion’

These general prohibitions to fight against discrimination are supplemented by the French Insurance Code, and the Article L117-2 states that there can be absolutely no distinction between individuals based on:

-

•

age for access to insurance guarantees or termination of insurance benefits, with the exception of pricing for life insurance contracts with mortality tables;

-

•

pregnancy and motherhood for premium and benefit computation;

-

•

sex for premium and benefit computation, except for mandatory supplementary pension schemes.

The Article 16-13 of the Civil Code civ defines an absolutely prohibited criteria that is applicable to insurance:

‘No one may be discriminated against because of their genetic characteristics.’

Other criteria can be used if they are a justified business necessity, or to modulate premiums and guarantees.

The nature of insurance

As we saw in section 2.1.2, insurance is based on segmentation and pooling. It is about treating different risks differently. Classification and regression tasks are by definition a form of discrimination: the aim is to distinguish individuals based on a statistical similarity Barocas and Selbst (2016). This is a form of discrimination that is justified and deemed acceptable if it does not systematically put a protected group at a disadvantage.

Unfair discrimination

Discrimination is unfair when a certain group is treated unequally based solely on their affiliation to it Kamiran and Calders (2012). Direct discrimination happens when protected attributes are explicitly used to make the decision. Indirect discrimination happens when the treatment appears neutral and depends on non-protected attributes, but protected groups get treated unjustly Mehrabi et al. (2019). Harmful discrimination in insurance can happen at several stages: for the decision to insure, during the underwriting or marketing phases, to renew or cancel policies, for coverage offer or for pricing Frees and Huang (2021).

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_discrim.png)

2.2.5 Interpretability: a first step to tackling bias

Interpretability is the degree to which a human can understand the cause of a decision. Some models are directly interpretable and others, qualified as ‘black box’ models, need interpretability methods. As the need to explain Machine Learning models become more and more important, a new research field XAI, for eXplainable Artificial Intelligence, was created. Understanding why a model predicted specific outcomes is a first step in bias detection Molnar .

Interpretable models

Some models are directly interpretable because of their structure. Linear Regressions predict the target as a weighted sum of the feature inputs, but assume linear relationships. Generalized Additive Models take into account non linear effects. Decision trees and decision rules are easy to interpret and capture feature interaction.

Model-agnostic explanation methods

Global methods explain how features affect the prediction on average. Techniques include feature interaction detection, prediction function decomposition, feature importance measure and representative data points choice.

Local methods explain the individual predictions. Techniques include the description of how changing a feature changes the prediction, of which features anchor a prediction, of which features would need to be changed to change a prediction and of which individual features are attributed to a prediction.

Detecting bias

Having more information on which variables play an important role in predictions, which variables interact with each other and more generally what causes a prediction can help detect bias. The outcome might be biased if a protected attribute has a great importance in the prediction or if an important variable for the prediction has a strong correlation with a protected attribute. This can help find out where the bias actually comes from.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_interpretability.png)

2.3 The expression of fairness and bias in data

Feature selection is the process of choosing what attributes are observed and taken into account for analysis. They are necessarily a reduction of reality and fail to capture real-world phenomena Barocas and Selbst (2016). But obtaining sufficiently rich information is not always possible, and insurers have to rely on reductive data.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_expressionfairnessbias.png)

2.3.1 Sensitive variables

Insurers are not allowed to use all variables that are available to them, because they are viewed as protected or sensitive, and using them might lead to biased outcomes. The choice of which variables are allowed depends on regulators, but also on society as a whole, because it is both a legal and ethical concern. Often, attributes that are not under the control of individuals are not accepted. Attributes that change over time are accepted, because individuals are on both sides at different stages in their life. Acceptable variables should be good predictors of risk. If attributes are known to cause a risky event they are accepted Frees and Huang (2021).

Regulation

EU

The European Union has anti-discrimination legislation, in the Charter of Fundamental Rights, that applies to the insurance sector, but it can have the effect of restricting flexibility of risk management and raising costs and legal insecurity, which means that insurers offer less effective coverage. Lawmakers decide which factors are determining for risk assessment but they are not specialists. With these directives, insurers cannot perfectly prevent adverse selection and moral hazard, and as a consequence, consumers can end up penalized, paying higher premiums and deductibles Petkantchin (2010).

France

There is an evolving conflict between insurance and anti-discrimination standards: on the one hand, insurers classify risks and on the other, the law prohibits the differentiation of individuals based on criteria that deny equal dignity. Insurers can select risks as long as they demonstrate the objectivity and statistical foundations of the data they rely on to do so. The Insurance Code completely forbids discrimination based on pregnancy and motherhood, risk selection for supplementary pension and the use of genetic information Robineau (2010). In 2011, the EU court ruled that insurers offering different prices to men and women violated gender equality laws, and this affected car, term life, health insurance and annuities Kuschke (2012). This means that there is no possible discrimination on these criteria, even though there are some technical and pragmatic arguments for using them.

US

Recently, unfair discrimination has become closely connected to disparate impact (see section 2.4.1). It is a measure of how a practice affects a group more than another, even when it appears neutral. But as of 2009, no court had applied the disparate impact standard to evaluate insurance rates Miller (2009). Unfair discrimination in insurance is indeed not exactly equivalent to disparate impact. In State law, unfair discrimination happens when similar risks are treated differently for determining rates, coverage, benefits and terms and conditions of policies. Depending on States, certain factors are prohibited for risk classifications and in underwriting decisions. But laws are not as restrictive as one could believe: in fifteen States, it is only prohibited to use race as the only factor regarding a decision to issue or continue a policy and in four States there are no restrictions on the use of race for underwriting personal automobile insurance Stead (2020).

In July 2021, the governor of Colorado signed a Senate Bill on insurers’ use of external consumer data sen . Insurers in the State are prohibited from unfairly discriminating on several variables. Unfair discrimination is defined as including

‘the use of one or more external consumer data and information sources, as well as algorithms or predictive models using external consumer data and information sources, that have a correlation to race, color, national or ethnic origin, religion, sex, sexual orientation, disability, gender identity, or gender expression, and that use results in a disproportionately negative outcome for such classification or classifications, which negative outcome exceeds the reasonable correlation to the underlying insurance practice, including losses and costs for underwriting.’

This means that insurers using external consumer data in Colorado will need to provide a disparate impact analysis Krafcheck (2021), even though it is not a synonym for unfair discrimination. The following question is: will other States follow in the same direction as Colorado?

What are they?

Forbidden variables

in France are pregnancy, motherhood and genetic information in all processes. For car, term life, health insurance and annuities, gender is a forbidden variable. In the US, there are some rules that come from federal law: insurers cannot consider pre-existing health conditions or gender in the underwriting process, genetic information in coverage availability or premium charging, or housing practices that have a disparate impact on protected classes. There are no other federal laws regulating what criteria can be taken into account. Historically, States are responsible for regulating insurance discrimination. These regulations strongly depend on which State and insurance line are in question: nine States completely prohibit the use of race and national origin in all lines, 7 States religion, one State gender and five States sexual orientation. Louisiana explicitly allows the use of race for life insurance. No State completely bans the use of age, credit score, genetic testing or ZIP Code Avraham et al. (2013).

Sensitive variables

in France are those defined in the anti-discrimination law that are not forbidden, as we saw in section 2.2.4. They can only be used if statistical data proves their relevance and objectivity for risk analysis. Information on ethnicity, religion, sex, gender, sexual orientation, disability, and age can be viewed as sensitive. Less obvious sensitive variables include parenthood, military service, political party, socioeconomic status, or involvement in the criminal justice system.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_regulationdata.png)

2.3.2 Proxy variables

Proxies are unprotected variables that are strongly correlated to protected variables but also contain strong predictive information. Using proxy variables may result in indirect discrimination Barocas and Selbst (2016). Insurers seek good segmentation of risk and profit maximization, but this might lead to perpetuating inequalities in society if outcomes are biased because of the variables that are used for prediction.

Name and surname

Accuracy of guessing the national origin of names varies significantly by the individual perception of national origin. Numerous characteristics matter, such as gender, popularity and the average level of educations of mothers who gave that name Gaddis (2017). A name depends on the culture of group, trends, the social level and time. With a name, you could identify the sex and the national origin of a person. You could also estimate the average age of people who have that name based on trends and popularity, but it would be difficult to infer the exact age Charpentier (2022).

Address

In the US, Black and Hispanic segregation and spacial isolation is still very active in some metropolitan areas Rugh and Massey (2014). This means that addresses are good proxies for ethnicity, and classifiers using this variable will exhibit discriminatory behavior Kamiran and Calders (2009). The term redlining comes from the 1930s when residential security maps were created to indicate which parts f a city were safe to invest in: neighborhoods outlined in red were the riskiest Martin and Varner (2017). From the 1960s, in the context of the struggle for Black Civil Rights, the use of redlining for risk classification was strongly criticized. The address is a non-causal variable, but it is strongly correlated with non-observable risk factors and with ethnicity Barry and Charpentier (2022).

There is a strong correlation between income and ethnicity and between income inequality and income segregation in the US. This is partly due to housing discrimination after World War II, forcing Black families with lower incomes to live in proximity in urban areas Reardon and Bischoff (2011). Addresses are therefore strongly correlated with income, which is strongly correlated with ethnicity.

Night lighting and wealth are correlated, and it is possible to approximately estimate how wealthy a neighborhood is from satellite imagery with a strong predictive power Jean et al. (2016). Address (and its associated satellite images) is a proxy for wealth.

With Google Street View, it is also possible to use the number and type of cars to infer wealth, ethnicity, education level and political preferences. It is also easy to detect the presence of handicap access ramps Hara et al. (2014) or a flag indicating national origins, political preferences or sexual orientations Charpentier (2022).

Occupation

Despite efforts for parity in the workplace, numerous occupations are still dominated by one of the two genders. In 2016 in a representative French region, sectors such as social working, healthcare and teaching are mostly feminine and industry, construction and transportation are mostly masculine. Another visible trend is that very feminine sectors tend to become even more so Faure (2020).

In 2018 in France, 18% of employees worked part-time, 78% of which were women DARES (2020). Knowing an individual works part-time means it is three times more likely that it is a woman.

Credit score

This variable cannot be measured directly, as it comes from the problem definition of creditworthiness. It is a non-arbitrary definition, not a given. The definition process can already itself be biased Barocas and Selbst (2016), as it relies on measurable attributes that are available. The choice of which variables to use can introduce discrimination. Credit scores also create a vicious circle in terms of poverty, and using this variable introduces a disparate impact on racial minorities and low-income households, who then have to pay a higher premium Charpentier (2022).

Face

With the boom of facial recognition softwares, there are numerous opportunities of application. It is now possible to use facial recognition tools for health assessment by using measurements and proportions of facial attributes. They may be considered biometric data, so there are ethical issues surrounding their use Boczar et al. (2021). Facial recognition can accurately predict gender and ethnicity, which raises moral questions.

Speech

The way an individual talks can indicate origin if he or she has difficulties with pronunciation, has a strong accent or speaks in a dialect. Linguistic profiling is the identification of an individual’s ethnicity based on how their voice sounds and using that information for discrimination Squires and Chadwick (2006).

Current Natural Language Processing tools are trained on traditional written sources, which are different from spoken language, and even more from dialectal spoken language. The latter are more likely to be incorrectly classified, so bias can arise, with an incorrect representation of ideas and opinions from minority groups Blodgett and O’Connor (2017).

Chatbots are rule-based, information retrieval or learning-based systems that are widely used today. In March 2016, a Microsoft chatbot was supposed to improve its small-talk capabilities by learning from conversations with human users. In less than a day, it was displaying racist and sexist abusive content Schlesinger et al. (2018). This shows that technical difficulties must be tackled in order to avoid such outcomes, especially when black box algorithms are used for treating voices.

In insurance, writing or speaking chatbots are used to report insurance claims. For example, Izzy Constat is a tool for amicable reports after a car accident. The chatbot asks for drivers’ identities and context and generates a sketch representing the incident Calvo (2022). What if this chatbot were biased against a group that had a specific dialect? This could result in understating the severity of impact and lower benefits.

Network

Who you know either gets you access to resources or makes you guilty by association. Recommendation systems are based on similarity between individuals, and if insurers had access to this kind of information, they could find customers and limit their financial risks. But this kind of practice may not be ethical, as people who are already marginalized can be even more affected Boyd et al. (2014).

There are many other variables with more or less predictive power that could be used as proxies for protected attributes. We will not be able to list them all, but the conclusion is that a study of their meaning and how they are linked to protected attributes is essential before using them as inputs in a prediction model.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_proxy.png)

2.4 How to measure fairness

Numerous metrics have been created to measure bias and fairness, the two notions not being distinct in most works. The general setting is the following:

-

•

is the set of n non-protected variables,

-

•

is the protected or sensitive variable,

-

•

is the true outcome,

-

•

is the predictor, classifier or regressor,

-

•

is the predicted outcome.

2.4.1 Binary classification

In the binary classification setting, 0. means the outcome is negative and means the outcome is positive. In this problem, it is possible to compute the confusion matrix between the true and predicted outcomes for each protected group, see table 1.

| Predicted outcome | |||

|---|---|---|---|

| Positive | Negative | ||

| True outcome | Positive | ||

| Negative | |||

TP: True Positive, FN: False Negative, FP: False Positive, TN: True Negative

The most common metrics in the literature are the following Alves et al. (2022).

Statistical parity

(or demographic parity) requires the likelihood of a positive outcome to be the same for all protected groups i.e. :

This is equivalent to having the same predicted acceptance rates AR for all protected groups:

Equalized odds

requires all protected groups to have the same probabilities of being correctly assigned a positive outcome and of being incorrectly assigned a positive outcome i.e. to have the same true and false positive rates i.e. :

This is equivalent to having the same true positive rates TPR and false positive rates FPR for all protected groups:

Remark: the true positive rate is also called recall or sensitivity.

Equal opportunity

is the same as equalized odds but only requires all protected groups to have the same probability of being correctly assigned a positive outcome i.e. requires the same true positive rates TPR for all protected groups:

Disparate Impact

is a popular metric in the US to measure bias. It is defined as the ratio in probability of favorable outcomes between groups and Bellamy et al. (2018):

It is a consequence of the statistical parity definition, in the case where the probabilities are non-null. A Disparate Impact of 1 would mean that the model is fair, lower than 1 that the model is unfair to group and above 1 that the model is unfair to group 0. This Disparate Impact is only defined in the case of a binary classification with a binary protected variable. Its estimation is not as easy as we could think, because of its definition as a ratio: we can have robust estimators for both probabilities, but the estimator of a ratio is not the ratio of estimators. This is why we decided not to use this fairness metric and to keep the original definition of statistical parity which is not as restrictive.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_fairnessmetrics.png)

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_cclmetrics.png)

2.4.2 Extension of the metrics to other settings

Most of these definitions can be extended to a multi-class classification () or a regression () setting: by defining a subset (respectively ) of values reflecting a positive (respectively negative) outcome, we adapt the definitions from the previous section:

This supposes that we can categorize every value of output as either positive or negative.

2.4.3 Model evaluation

We will compare models using the confusion matrix and metrics deriving from it:

-

•

The accuracy is the proportion of correct classifications among all classifications.

-

•

The true positive rate is the proportion of correct positive classifications among actual positive values.

-

•

The false positive rate is the proportion of wrong positive classifications among actual negative values. It is sometimes called the probability of false alarm.

-

•

The acceptance rate is the proportion of positive classifications among all classifications.

In order to evaluate a model, we need to take into account the facts that:

-

•

An acceptable accuracy threshold depends on the context of the prediction: do we need to be perfectly accurate in order for the decision to be accepted by society? Do mistakes cost a lot to the company? Furthermore, if there is a large class imbalance, accuracy is not the best metric as it can be very high while the model only fits the majority population.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_accuracy.png)

-

•

Missclassification errors are more or less acceptable depending on the context. For example, in a risk selection decision, underwriters want to select ‘good’ risks. It is generally more acceptable and less costly to falsely reject good risks than falsely accept bad risks.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_FPFN.png)

Simulated data

3 Simulated data

We will apply discrimination detection and correction methods to simulated data before tackling a real use case. The reason for this is that we wish to know the answer to the question ‘Is my prediction discriminatory towards a group?’ while knowing how the outcome was computed, so that we can look for a solution to a well-defined problem, instead of having to make assumptions.

We will begin by generating our data, which consists of two sensitive variables and , a set of non-protected variables , and a variable of interest 0. All variables can be correlated with each other, but depending on the country and its regulation, insurers are not always allowed to use the sensitive variables as explanatory variables, and sometimes, with the GDPR for example, cannot even collect the information. In this section, however, we will suppose that the variable is available, because it is the only way to measure discrimination.

To link with a real-life example, if we were in a pricing context for automobile insurance, could represent gender, marital status, the other variables such as age or car value and the claim occurrence. Gender is not the cause of an accident, but statistically we observe that gender and claim occurrence are correlated. Intuitively, we should not discriminate based on gender, because it would be unfair as it is a stereotype, but we do not have access to a ‘fairer’ variable, which could be driving behavior.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_whysimulated.png)

For simplification reasons, we will suppose that the protected variables and the outcome are binary. We will begin by giving the theoretical framework, then illustrate the simulation process with two variables, and finally create the dataset.

3.1 A reminder on statistical tools used to set the framework

In this section, we will pose important mathematical concepts that will help understand the observed effects on the fairness metric.

We want to generate the variables while controlling the relationship they have with each other. To do so, we will use the theory of copulas.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_reminderstattools.png)

Notations

First, we need to introduce some notations:

-

-

is a probability density function and the associated cumulative distribution function:

-

-

is the expected value and the variance

-

-

is the covariance matrix:

-

-

is the correlation matrix:

-

-

is the probability density function and the cumulative distribution function of a standard normal distribution

-

-

is the probability density function and the cumulative distribution function of a standard multivariate normal distribution

Probabilities Charpentier (2010)

Definition 1.

A d-dimensional real random vector is a standard normal random vector if all of its components are independent and follow a standard normal distribution.

Definition 2.

A d-dimensional real random vector follows a multivariate normal distribution if there exists a random k-vector , which is a standard normal random vector, a d-vector and a matrix of full rank such that 0.

We denote where is the mean vector and is the covariance matrix.

Definition 3.

The multivariate normal distribution is non-degenerate when the covariance matrix is positive definite, in which case it has the following density

where and is the determinant of 0.

Proposition 1.

For any univariate cumulative distribution function ,

Definition 4.

Set and two continuous random variables. and are independent if and only if 0.

Definition 5.

Set and two continuous random variables with finite variance. Pearson’s linear correlation coefficient is defined as

Remark: Pearson’s correlation coefficient is linear:

Proposition 2.

Remark: This proposition means that uncorrelated data is not independent in general. Furthermore, correlation does not imply causation, meaning that we cannot deduce a cause-and-effect relationship between variables solely based on their correlation. However, in the case of a multivariate normally distributed random vector, variables that are uncorrelated are independent.

Proposition 3.

Set and two random variables. For any measurable function such that is square-integrable,

Matrices Horn and Johnson (2013)

Definition 6.

A real symmetrical matrix is positive definite (respectively semi-definite) if and only if for any non zero real column vector , is positive (respectively non negative).

Proposition 4.

A matrix is positive definite (resp. semi-definite) if and only if all of its eigenvalues are positive (resp. non-negative).

Definition 7.

The Cholesky decomposition of a symmetrical real positive-definite matrix is a unique decomposition of the form where is a lower triangular matrix with real and positive diagonal entries.

Proposition 5.

If is positive definite (resp. semi-definite), it can be written as with a lower triangular matrix with a positive (resp. non negative) diagonal.

Remark: This is the unique (resp. non unique) Cholesky decomposition.

Proposition 6.

If a matrix can be eigendecomposed and all its eigenvalues are non null then it is invertible.

Copulas Charpentier (2010)

Copulas are used to study multi-hazard risks, ie random vectors 0. Most of the time, the marginal laws are known. Copulas are then used to get the joint law and model the dependence between variables Fermanian (2022).

Definition 8.

A d-dimensional copula is a cumulative distribution function whose margins are uniform on 0.

Theorem 1 (Sklar’s theorem).

For any multivariate cumulative distribution function with marginals , there exists a d-dimensional copula such that

If are all continuous, then is unique.

Definition 9.

The independence copula is defined as

Remark: We will note a random vector which has copula 0.

Definition 10.

For some correlation matrix , the n-dimensional Gaussian copula with parameter is defined as

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_gaussiancopula.png)

3.2 Simulation process

We will now see how to simulate copula models. It all relies on proposition 1. Our goal is to simulate , which is characterized by its marginal distributions and copula , chosen to be the Gaussian copula. The procedure is the following:

-

1.

Draw

-

2.

Compute

-

3.

Compute

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_simulation.png)

3.2.1 Illustration in dimension 2

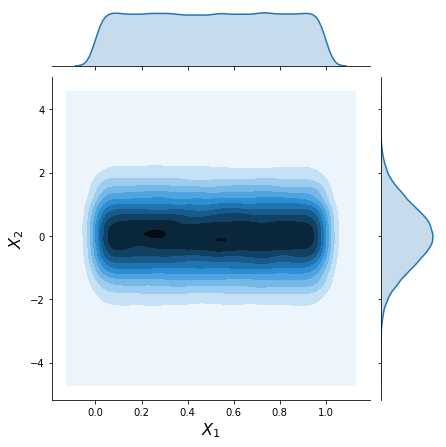

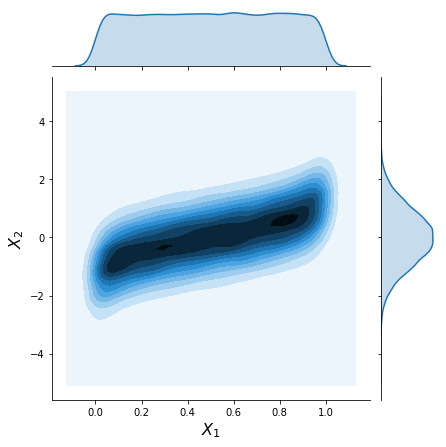

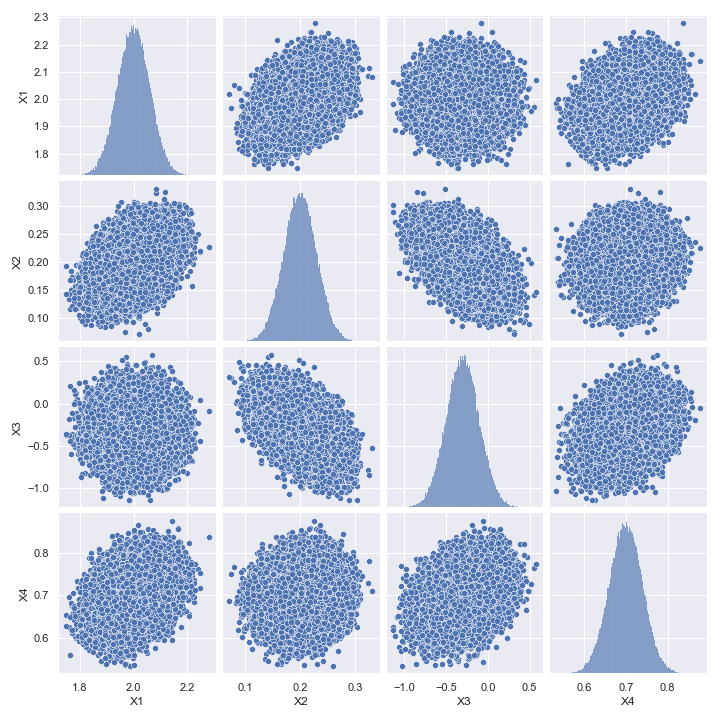

We will look at the results in dimension n=2 before creating our final dataset. This will allow us to give a visual illustration. First, we generate with and 0. Then, we compute 0.

The correlation between the is

because , 0. And the correlation between the is

First case:

and with

Then

In order to find the correlation between the , we need to compute:

And so,

| (1) |

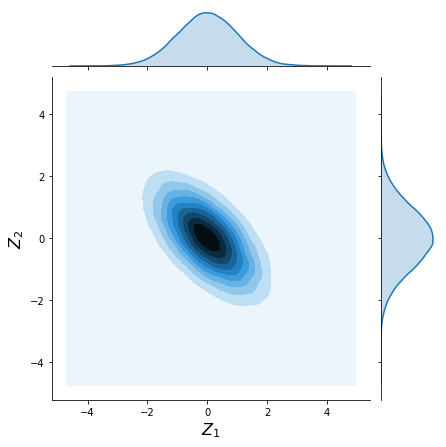

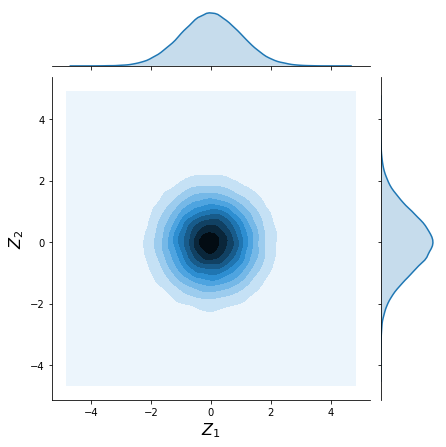

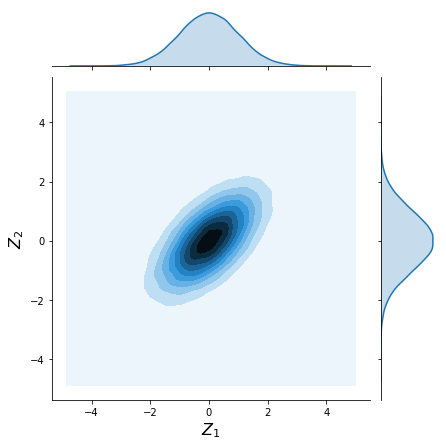

Illustration: We will take and 0.

As specified by step 1, we first draw

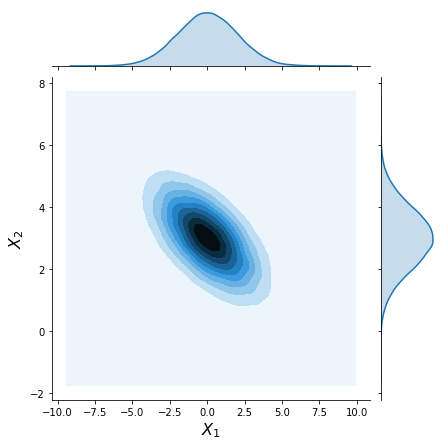

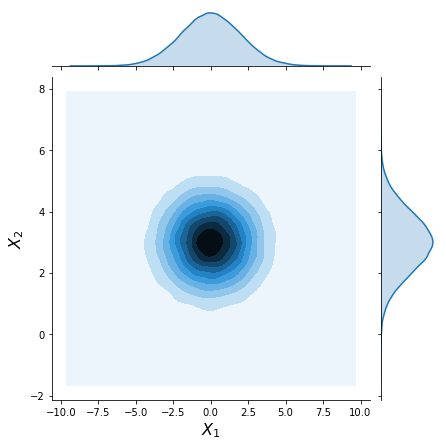

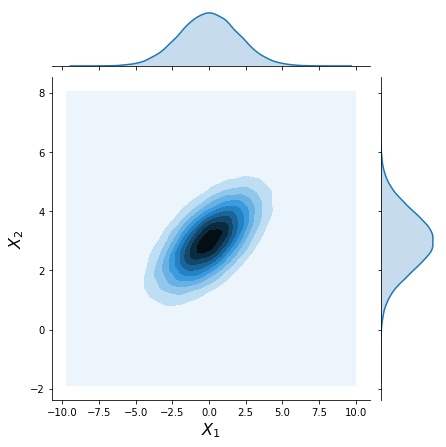

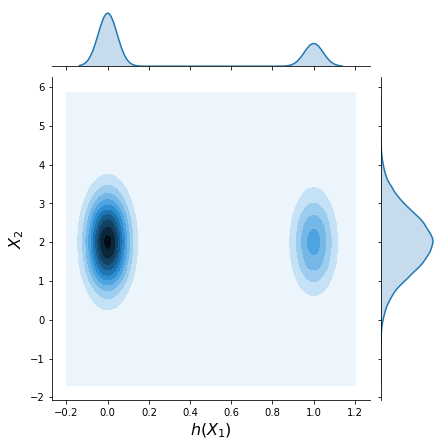

of size 0. We will follow the rest of the simulation process for three values of : , and , so as to compare the results for different correlations. Figure 1 represents the joint distribution of 0. We see that increasing the degree of correlation positively (resp. negatively) between the marginal distributions concentrates the joint distribution around the line (resp. ).

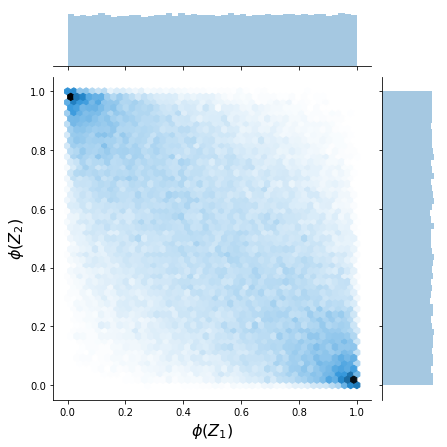

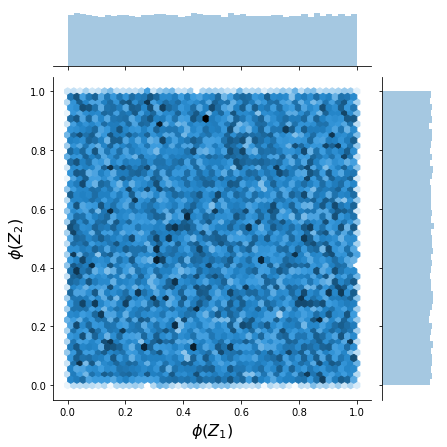

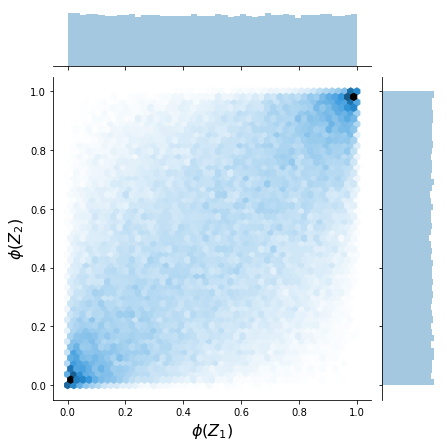

We then apply to and (step 2) and get their joint cumulative distribution, as plotted in figure 2. As , , , which is another formulation of proposition 1. So we get two uniform random variables that are correlated. Once again, the joint cumulative distribution concentrate around the line when the correlation varies.

We finally apply to to obtain , (step 3), as plotted in figure 3. We have the same conclusion as before on the correlation. We are well-aware that we could have directly generated a multivariate normal vector with the desired expected values and standard deviations, but this way allowed us to give an easy example of how to follow the simulation process.

We wrote down the values of the estimated Pearson correlation coefficients in table 2. As computed in equation 1, we have for the three values of 0.

| -0.6 | 0 | 0.6 | |

|---|---|---|---|

| -0.6018 | -0.0009 | 0.6005 | |

| -0.6018 | -0.0009 | 0.6005 |

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_dim2firstcase.png)

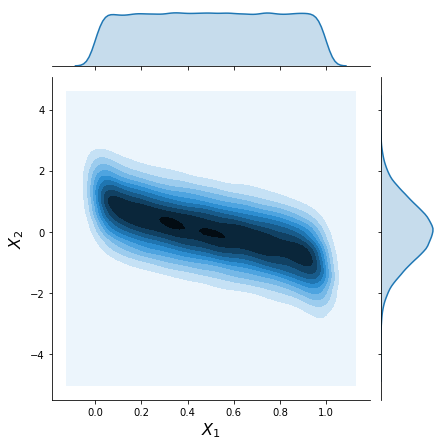

Second case:

and with

The computation of is not as direct as in the first case. As has a uniform distribution, we have

We can compute

because and so (consequence of proposition 1).

So we have

because of proposition 3, with square-integrable.

And , because

| (2) |

Proof.

By identification,

∎

So we have

We will do an integration by parts:

We can set

So

So we have

and because is a cumulative distribution function

so

So we have

and

because , as it is the integral on the entire support () of a probability density function (of the standard normal distribution). In the end,

| (3) |

To conclude, as , we almost keep the same correlation between and as between and , in the case where and 0.

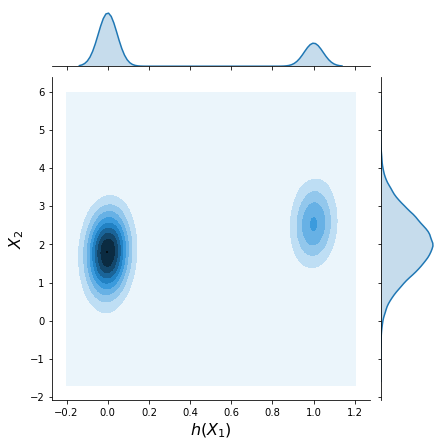

Illustration: We will take and 0. The joint distributions are plotted in figure 4. Like in the previous case, increasing the degree of correlation positively (respectively negatively) between the marginal distributions shifts the joint distribution on the line (respectively ).

We computed the estimated Pearson correlation coefficients between the simulated and , and and in table 3. As found with equation 3, for the three values of 0.

| -0.6 | 0 | 0.6 | |

|---|---|---|---|

| -0.5983 | -0.0031 | 0.6006 | |

| -0.586 | 0 | 0.586 | |

| -0.5838 | -0.0029 | 0.5874 |

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_dim2secondcase.png)

Third case:

and ,

As is not continuous, we are not under the assumptions of Sklar’s theorem (theorem 1), so the copula might not be unique.

We will place ourselves in the second case and simulate and with , then transform into a Bernoulli random variable using the function

We then have 0.

Proof.

By identification, with ∎

As the cumulative distribution function of a Bernoulli random variable is not invertible, we cannot go back to the generative copula from the set 0. In a sense, we have broken the correlation structure. But our transformation allows the computation of the correlation as a function of :

with

and

So

So we have

| (4) |

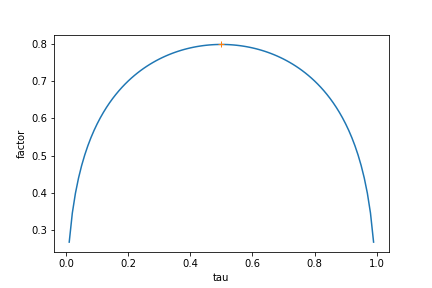

As the correlation coefficient is in ,

So has a minimal and maximal value:

Figure 5 represents for 0.

So for all 0.

Illustration: We will take and 0.

Then (numeric computation) and

So

The joint distributions are plotted in figure 6. Like in the previous cases, increasing the degree of correlation positively (respectively negatively) between the marginal distributions shifts the joint distribution on the line (respectively ).

We computed the estimated Pearson correlation coefficients between the simulated and in table 4. We can see that for the three values of , as we computed in equation 4.

| -0.6 | 0 | 0.6 | |

|---|---|---|---|

| -0.455 | -0.001 | 0.455 | |

| -0.454 | 0.000 | 0.455 |

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_dim2thirdcase.png)

3.2.2 Illustration in dimension : creating the dataset

We can now create the simulated dataset. For simplicity reasons, we will suppose that we are in the setting of section 2.4.1, with two binary protected variables and a binary outcome. We have

For the choice of , there are constraints. It must be a square matrix and:

-

•

symmetrical, because

-

•

with a unity diagonal, because

-

•

all values must be in by definition of the correlation

-

•

positive semi-definite

-

•

invertible, otherwise the distribution is degenerate and does not have a density, as we saw in definition 3

In order to have an invertible and positive semi-definite matrix, it needs to be positive definite. Indeed, proposition 6 gives the equivalence between an invertible matrix and its eigenvalues being non null, and proposition 4 gives the equivalence between a positive definite (respectively semi-definite) matrix and its eigenvalues being positive (respectively positive or null).

Using proposition 5 (Cholesky decomposition), we will compute , choosing as a lower triangular matrix with a positive diagonal. That way we will have a square symmetrical, positive definite (so positive semi-definite and invertible) matrix.

We have

As we want the diagonal of to be unity, we need

The computation of the implies constraints on the values of the :

Finally, to set , we set values for the , check that the constraint above is verified, compute the accordingly and then 0. We also need to check that we have 0.

Finally, the procedure is:

-

•

set the matrix with the constraints mentioned above

-

•

compute

-

•

generate

-

•

set the parameters of the laws of

-

-

•

compute

Reminder:

-

Final dataset

We set and generated 100 datasets with the same parameters:

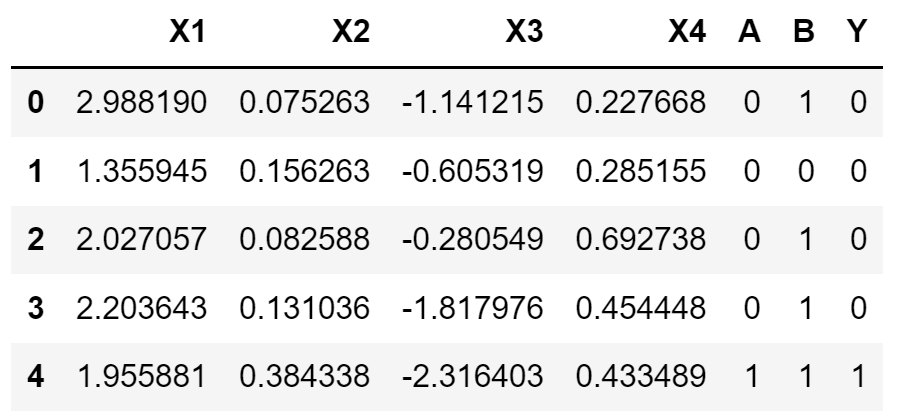

The reason for that is that we want to take into account the instability of results. Instability can come from the generative process: not all datasets will have the exact same variable distribution because of the limited sample size (100,00 lines here). It can also be caused later on by the train test split or sampling which depend strongly on the execution. Generating 100 datasets allows us to average and get confidence intervals on metrics and results. In reality, we often do not have access to the data generator so, to construct confidence intervals, we use bootstraping, which estimates the sampling distribution of statistics such as sample mean thanks to random sampling with replacement. Figure 7 shows the head of one of the datasets.

As mentioned previously, we will take advantage of having access to the data generation process. It means we can produce confidence intervals for every value: the mean of a variable, the number of observations of a certain class, the weights of the regression etc. This is the reason why we generated 100 datasets: we will look at the average and standard deviation over these datasets to produce the confidence interval of the value we are looking at. We gave a reminder on confidence intervals in appendix A.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_dimn.png)

3.3 Descriptive statistics

Before heading into applying methods, we need to prepare and explore our data. As we have built our datasets ourselves, we already know a lot about them.

3.3.1 Variable identification and univariate analysis

The explanatory variables are the , and , and the target variable is 0. As expected, we have 100,000 non-null values for each variable. The are continuous, and , and are categorical, taking values in 0.

X

By construction, the have means and standard derivations as defined in section 3.2.2, and it is verified by the computation of the sample means and standard derivations in table 5. We can notice that the confidence intervals are of size 0. This means that over our 100 datasets, we have a probability of 95% that they all have the means and standard deviations as defined in data generation process.

| i | 1 | 2 | 3 | 4 |

|---|---|---|---|---|

| mean | ||||

| std |

A

We computed it to follow a Bernoulli distribution of parameter , so we find as planned that

Table 6 gives the number of observations for each value of 0. By construction, as , there is an imbalance: about individuals have and individuals have 0. So the group imbalance ratio is

meaning there are 2.33 times more observations of than 0.

| A | Observations |

|---|---|

| 0 | |

| 1 |

B

We computed it to follow a Bernoulli distribution of parameter , so we find as planned that

Table 7 gives the number of observations for each value of 0. By construction, as , there is an imbalance: about individuals have and individuals have 0. So the group imbalance ratio is

meaning there are almost 9 times more observations of than 0.

| B | Observations |

|---|---|

| 0 | |

| 1 |

Y

We computed it to follow a Bernoulli distribution of parameter , so as expected

This results in an imbalance too: table 8 gives the number of observations for each value of , and the imbalance ratio is

meaning there are 4 times more observations of than 0.

| Y | Observations |

|---|---|

| 0 | |

| 1 |

Going back on imbalance

In real life, imbalance can be explained either by the way the data was collected or by the natural domination of one class. The collection of data can lead to an imbalance if the sampling is biased or if mistakes are made, for examples writing down the wrong labels on observations. In insurance, there are sampling biases: conclusions about risks only concern individuals who have been accepted at the underwriting stage. As underwriters aim at selecting ‘good’ risks, most of the time, the insurer’s portfolio will be very specific and predictions on claims frequency, for example, cannot be generalized to a different population.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_samplingbias.png)

3.3.2 Multivariate analysis

An important part of data exploration consists in studying the relationships between variables. To do so, we will analyze how they are correlated to each other. As a reminder, correlation is how linearly related two variables are, and is only the first order approximation of dependence, as seen previously.

Correlations with Y

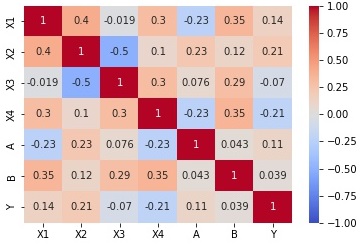

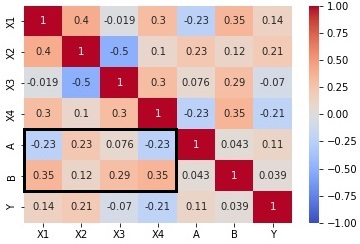

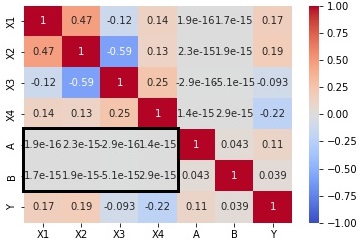

A heatmap of the correlations can help understand which variables are correlated with each other. Figure 8 shows the heatmap of correlations. The strongest positive correlations are colored in bright red and the strongest negative correlations are colored in bright blue. The strongest correlations to in absolute value are with , , , , , and then 0. This is coherent with the theoretical values of the correlation matrix in section 3.2.2.

Correlations with A

We saw in the previous paragraph that has the third strongest absolute value correlation to 0. It is also strongly correlated to the , as we see in figure 8. We noted in the previous section that there are imbalances in the number of observations for both and , and we see in table 9 that among group there is an imbalance in output values too. If we compute the imbalance ratio for the output, we get

meaning that within group , there are 4.86 times more observations of than and within group , there are 2.73 times more observations of than 0. In general there are a lot more outputs than ones, and when we zoom in on protected groups, the imbalance ratio is larger for group than for , meaning that the former has a larger proportion of outputs than the latter.

| Y=0 | Y=1 | |

|---|---|---|

| A=0 | ||

| A=1 |

Correlations with B

We saw that has the weakest absolute value correlation to , but it is still strongly correlated to the 0. Within groups, as for , there can be imbalances, as we see in table 10. The imbalance ratios by group are

meaning that within group , there are 5.53 times more observations of than and within group , there are 3.88 times more observations of than 0. The imbalance ratio is larger for group than for 0.

| Y=0 | Y=1 | |

|---|---|---|

| B=0 | ||

| B=1 |

Correlations between the

By construction the are related to each other, through the correlation matrix. Figure 9 gives the pairwise relationships between the , and the diagonal is their marginal distribution. We observe that is positively correlated with and , is negatively correlated with , and is negatively correlated with 0. Correlations between other variables are less obvious.

3.3.3 Outliers

As the were computed to follow normal distributions, and , and to take values in , we do not expect to have any outliers. This is verified in our datasets: there are no unexpected values for the and we have values of , and in 0.

Discrimination mitigation applied to the simulated data

4 Discrimination mitigation applied to the simulated data

The goal of the section is to compare different pre-processing steps and see how they influence our fairness metrics. After this, we will apply a logistic regression model to the simulated explanatory variables predict the variable of interest. Appendix LABEL:appendix:logistic_regression gives a reminder on the logistic regression.

The reason why we chose the logistic regression is that it is interpretable, which is a major issue with Machine Learning, and an important characteristic to simplify our study on fairness. It also presents other advantages, such as its simplicity with a low number of parameters. The main drawback is that a lot of preprocessing must be done: we need to select variables that are not strongly correlated with each other, and to transform most continuous variables into categorical variables, or only their general effect will be captured by the coefficients. For this simulated dataset, we will keep all variables as there are only 5 of then, and they are very simple.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_choiceregression.png)

4.1 Regression model with no pre-processing step

In this section, we will simply predict the outcome with all the variables. We standardized the variables to have mean zero and standard deviation 1, then randomly separated the dataset into a train (80%) and a test dataset (20%), and applied a logistic regression model.

Table 11 gives confidence intervals of the weights of this logistic regression, their standard errors and the associated p-values. All variables have p-values below 0.05, so they are all significant to the model.

| Variable | Coefficient | Standard Error | P-value |

|---|---|---|---|

| Intercept | |||

| A | |||

| B |

Performance evaluation

-

•

We have 81.05% correct classifications on average. The accuracy acceptability depends on the business context. As we saw previously, if mistakes have a high cost then it might not be sufficient.

If there is a large class imbalance, accuracy is not the best metric as it can be very high while the model only fits the majority population. As a reminder, the output imbalance ratio is 0. So we cannot rely solely on accuracy to evaluate our model. -

•

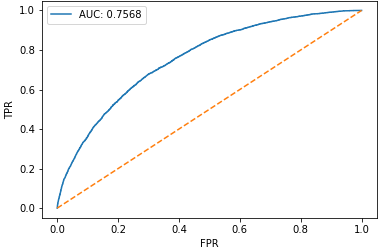

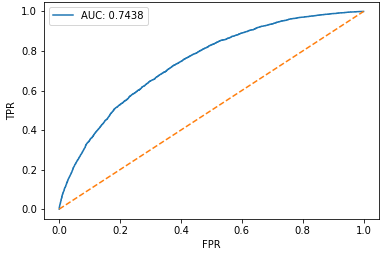

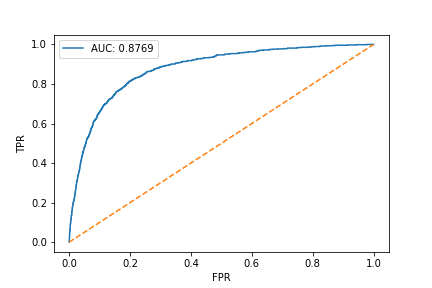

As a reminder, the ROC (Receiver Operating Characteristic) curve plots the true positive rate against the false positive rate for varying classification thresholds. A random classifier will exhibit a linear ROC curve as the one plotted in a dashed orange line (figure 10). Above that line, the model performs better than the random classifier, and below, worse. The perfect classifier has a ROC curve that is confined to the (0,1) point. Here, our model performs a lot better than the random classifier: the AUC (Area Under the ROC Curve) is of 0.7568.

| (%) | Global |

| Accuracy |

Fairness evaluation

We will compare fairness under all three definitions, first comparing the metrics between values of protected groups A and B (table 13), then between subgroups of combinations of A and B (table 14).

-

•

Statistical parity requires the same acceptance rates for all protected groups.

-

–

It is a lot higher for group than for group , by 8.26 points. So group is disadvantaged by the model under this definition.

-

–

It is higher for group than for group , by 3.47 points. So group is disadvantaged by the model under this definition.

-

–

Looking at subgroups, the most advantaged subgroup is for and the most disadvantaged is for 0. This shows that looking at combinations of protected variables reveals that groups with a certain combination of characteristics are even more disadvantaged.

-

–

-

•

Equal opportunity requires the same true positive rates for all protected groups.

-

–

It is higher for group , so group is disadvantaged by the model under this definition.

-

–

It is higher for group , although not by much, so group is disadvantaged by the model under this definition.

-

–

It is highest for subgroup and lowest for group 0.

-

–

-

•

Equalized odds requires the same true and false positive rates for both protected groups.

-

–

The false positive rate is higher for group than group 0. Group has lower true and false positive rates, so it is disadvantaged by the model under this definition.

-

–

The false positive rate is higher for group than 0. Group has lower true and false positive rates, so it is disadvantaged by the model under this definition.

-

–

The false positive rate is highest for subgroup and lowest for 0.

-

–

To conclude, the model is unfair and disadvantages groups and under all three fairness definitions, and the most disadvantaged subgroup is 0.

(%) Global A=0 A=1 Difference B=0 B=1 Difference AR TPR FPR

| (%) | A=0 | A=1 | ||

|---|---|---|---|---|

| B=0 | B=1 | B=0 | B=1 | |

| AR | ||||

| TPR | ||||

| FPR | ||||

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_simallvar.png)

4.2 Removing protected variables to avoid direct discrimination

When sensitive variables are omitted, models can still learn stereotypes, because sensitive information is embedded in datasets even if it is not intentional. Leaving out sensitive variables forces the correlated variables to take on a greater importance. This is the omitted variable bias Williams et al. (2018).

Removing sensitive attributes is problematic, because it becomes impossible to check for bias and discrimination. We cannot see if the most important variables for prediction are strongly correlated with a protected attribute or compute metrics. This is a problem related to data regulations: as we saw in section 2.2.1, the GDPR requires minimal data collection, but more data is needed to prove discrimination.

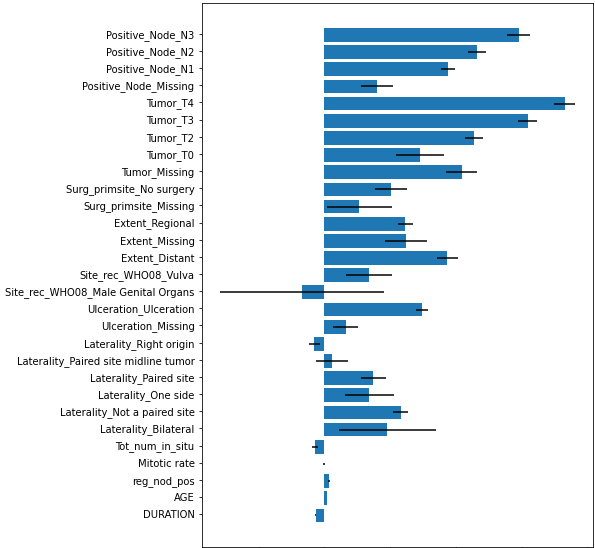

We will preprocess our data by removing the sensitive attributes, and , then predict the outcome with a logistic regression model. Table 15 gives the predicted weights of this logistic regression. As and are no longer used as explanatory variables, the weights of regression have changed. For example, the biggest change is for , which had a coefficient of 0.25 and now has a coefficient of 2.46. Remembering the correlation matrix, is correlated with A and B with relatively high Pearson correlation coefficients: -0.23 and 0.35 respectively. This can indicate that A and B will still indirectly play a part in the model predictions.

| With all variables | |||

|---|---|---|---|

| Variable | Coefficient | Standard Error | P-value |

| Intercept | |||

| A | |||

| B | |||

| Without protected variables | |||

| Variable | Coefficient | Standard Error | P-value |

| Intercept | |||

Performance evaluation

-

•

As we can see in table 17, the accuracy has only decreased by 0.01 on average, which is negligible, especially considering the width of the confidence interval.

-

•

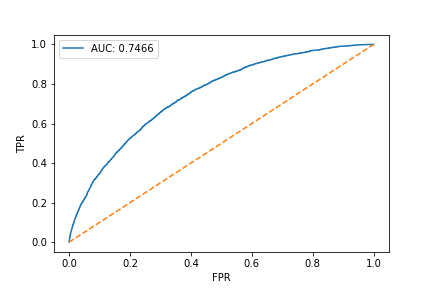

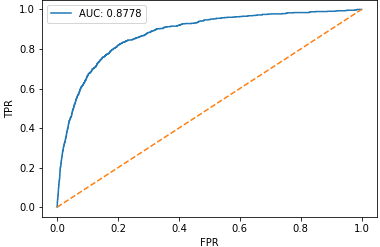

Looking at the ROC curve in figure 11, the model still performs quite well, and the AUC has decreased from 0.7568 to 0.7466 compared to the model using all variables.

| (%) | With all variables | Without protected variables |

|---|---|---|

| Accuracy |

Fairness evaluation

-

•

Acceptance rate

-

–

The global acceptance rate has slightly increased.

-

–

For groups A, the gap between acceptance rates has increased by more than one point. This was expected, as , strongly correlated with A, has taken on a great importance in the model prediction.

-

–

For groups B, the difference in acceptance rates has decreased.

-

–

Looking at protected subgroups, the most advantaged subgroups are the same as in the model with all variables: the most advantaged subgroup is and the most disadvantaged is 0. We now have a lower gap between acceptance rates for subgroups and and for and , which is coherent as acceptance rates between groups B are closer than previously.

-

–

-

•

For true and false positive rates, we have the same conclusions as for the acceptance rates.

For groups A, the gaps between fairness metrics are wider when the protected variables are not used in the model, but for group B, they are smaller, although this phenomenon comes from the structure of the correlation matrix. The same groups remain disadvantaged.

To conclude, the performance metrics have not deteriorated too much compared to when using all variables. The fairness metrics are worse for groups A but better when looking at groups B. To conclude, simply ignoring the protected variables is not a solution.

With all variables (%) Global A=0 A=1 Difference B=0 B=1 Difference AR TPR FPR Without protected variables (%) Global A=0 A=1 Difference B=0 B=1 Difference AR TPR FPR

| With all variables | ||||

|---|---|---|---|---|

| (%) | A=0 | A=1 | ||

| B=0 | B=1 | B=0 | B=1 | |

| AR | ||||

| TPR | ||||

| FPR | ||||

| Without protected variables | ||||

| (%) | A=0 | A=1 | ||

| B=0 | B=1 | B=0 | B=1 | |

| AR | ||||

| TPR | ||||

| FPR | ||||

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_simnoprotected.png)

4.3 Transforming the non-protected variables to mitigate indirect discrimination

4.3.1 Theory

The idea

Focusing on the definition of fairness as statistical parity, we can view it as an independence condition. Statistical parity requires 0. Since we do not want or to impact the predicted output, the goal is firstly not to use them as explanatory variables and secondly to have explanatory variables that are independent of them. Dealing with independence is a complex problem, which is why we will tackle it on a linear level only - with correlation. We will try to obtain transformations of the variables uncorrelated with and , and we will then use them as inputs of a logistic regression model to predict 0.

Drawing inspiration from the Gram-Schmidt process (a reminder is given in appendix B), the idea is to view the variables as vectors in a n-dimensional space (n being the number of variables in our dataset) and the covariance between them as a scalar product. Let us set the theoretical framework.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_inspomethod.png)

Definition 11.

An inner product is a map

with a real vector space, that is symmetric, bilinear and positive-definite.

Proposition 7.

Set and real random variables with zero mean and finite variance. Their covariance

is an inner product (on the space of random variables with zero mean and finite variance).

Proof.

Set real random variables with zero mean and finite variance and 0. Then 0. We will check the three properties of the inner product:

-

•

symmetry:

-

•

bilinearity:

-

•

positive-definiteness:

and

∎

Definition 12.

Two vectors are orthogonal if their inner product is zero.

As covariance is an inner product on the space of random variables with zero mean and finite variance, two random variables of this space are orthogonal if their covariance is zero ie if their correlation is zero, because as we saw in definition 5,

and their variance is finite. So we have an interpretation of random variables of this space as vectors with an inner product.

Going back to the initial goal, we wanted a transformation of our variables that is uncorrelated to both and 0. With the framework we have set, it means that the transformed variables will be orthogonal to and to 0. Suppose the (non-orthogonal) basis of our vector space is the linearly independent set such that any vector Z of the space - which corresponds to the characteristic of one individual ie row of the dataset - can be uniquely written as a linear combination of the vectors of the basis:

Our goal is to find a change of basis that gives us the new basis 0. We will then be able to write

is called the transition matrix and its row is formed by the coordinates of :

Then, the change-of-basis formula gives in matrix form

So

Our goal is to have a new basis in which the non-sensitive vectors are orthogonal to the sensitive ones. For this reason, we impose the following constraints for the construction of the new basis:

-

1.

we do not want to transform the sensitive variables, so the first s vectors of the new basis will remain the same as in the old basis:

As a result,

with the identity matrix of size 0.

-

2.

the new non-sensitive vectors will be orthogonal to the sensitive vectors:

This is equivalent to: for all a system of equations with unknown variables (the ):(5) The rows of are the , so

For each row k of A, we are looking for the values of the 0. The previous constraints give for each row a system of equations, but we have unknown variables, so the system is underdetermined, with an infinite number of solutions. To simplify, we can set

Meaning that each non-sensitive vector of the new basis is written as a linear combination of itself and of the sensitive vectors of the old basis. This gives a transition matrix of the shape

We now have for each row, a system of linear equations and unknown variables. We need one more constraints in order to have a unique solution. An idea is to minimize the distance between the old and the new basis (non-sensitive) vectors:

As the distance is positive, it has a lower bound, so this problem has a solution. We have defined the inner product as the covariance between random variables with zero mean and finite variance, so the distance between two such random variables and is

So

As we had a system of linear equations and unknown variables, we can express as a combination of the other 0. So the minimization of this distance gives a unique solution with the previous constraints. To summarize, for each , we have the following minimization problem under constraints:

Solving the problem for every gives us the transition matrix 0. Then, with the coordinates of a vector in the base and in the base , we can write

Meaning that we will compute, for every observation, the transformation of each vector - corresponding to each individual - in the new basis.

Extreme-case scenarii

We can wonder what would happen in the extreme-case scenario in which the non-sensitive variables are already uncorrelated with the sensitive ones. Then, we do not need to transform the non-sensitive variables: We have for and and we have a minimal distance as 0.

The other extreme-case scenario is the one in which all the variables are the non-sensitive variables are perfectly (positively or negatively) correlated with the sensitive ones. Then it means that the non-sensitive variables are a linear function of the sensitive ones, and consequently, of each other. It is therefore impossible to have non-sensitive vectors uncorrelated with the sensitive ones. Fortunately, in reality, when we have our datasets, we only have samples of ‘true’ distributions, meaning that variables are never perfectly correlated with each other (except if a variables appears twice, but we can delete the duplicate). In the worst case, if the non-sensitive variables are very correlated to the non-sensitive ones, we will end up with transformed non-sensitive variables that have a very low variance, meaning that they will not explain the output very well.

4.3.2 Results

Transition matrix

The average transition matrix obtained on the 100 datasets is

This means that, on average,

Transformed variables

Figure 12 shows the correlations between variables before and after transforming the 0. We can see that the correlations between A (respectively B) and the have been reduced to zero, which was the goal of the procedure. Most correlations between other variables are close to before and after the change of basis, keeping the same signs and orders of magnitude. The most noticeable difference is that went from -0.019 to -0.12.

![[Uncaptioned image]](/html/2307.13616/assets/figures/encadres/cadre_simcorrmatrix.png)

Prediction

We then apply the baseline model to predict the output, using only the transformed non-sensitive variables as explanatory variables.

| Without protected variables | |||

|---|---|---|---|

| Variable | Coefficient | Standard Error | P-value |

| Intercept | |||

| Transformed variables | |||

| Variable | Coefficient | Standard Error | P-value |

| Intercept | |||

Performance evaluation

-

•

Table 20 gives the accuracy of the model. Compared to when simply deleting the protected variables, the accuracy decreases by only 0.23 points.

-

•

Figure 13 gives the ROC curve of the model. As a reminder, the AUC of the model without protected variables was of 0.7466. The AUC for the model with transformed variables has only decreased by 0.0028.

| (%) | Without protected variables | With transformed variables |

|---|---|---|

| Accuracy |

Fairness evaluation

-

•

Acceptance rate

-

–

The global acceptance rate has increased by 0.73 points on average, meaning that globally, more individuals get predicted the outcome with the model using the transformed variables compared to the model without protected variables.

-

–

For groups A: the difference in acceptance rates is now close to zero, which was the goal of the change of basis method. The reason why it is not exactly zero might come from the fact that we have approximated independence to correlation, so there might be some non linear dependence left between the transformed non-sensitive variables and A. It is interesting to note that the acceptance rate for group has decreased and for it has increased, and the advantageous position has shifted: the acceptance rate for group is now slightly lower than the one for group 0.

-

–

For groups B: the difference in acceptance rates is now null, meaning that there we have ie independence.

-

–

Looking at protected subgroups in figure 22, not all subgroups are treated fairly by the model as we have slight gaps between subgroups with and 0. The order of unfairness has also changed: now, the most disadvantaged subgroup is when it used to be the most advantaged one, and the most advantaged subgroup is when it used to be the most disadvantaged one.

-

–

-

•

True positive rate

-

–

The global true positive rate has decreased compared to the model without protected variables.

-

–

Groups A: as for the acceptance rate, the difference in true positive rates is now closer to zero, and the sign has changed, meaning that group now has a lower true positive rate than group 0.

-

–

Groups B: the difference in true positive rates is now very close to zero and has also changed signs.

-

–

As for the acceptance rate, the most advantaged subgroup now used to be the most disadvantaged and vice versa.

-

–

-

•

False positive rate

-

–

Globally, the false positive rate has also decreased.

-

–

Groups A: the difference in false positive rates has also decreased and changed signs.

-

–

Groups B: surprisingly, the difference in false positive rates has increased and changed signs.

-

–

Looking at subgroups, there has also been a shift in which subgroup is the most and least advantaged.

-

–

To conclude, looking at the variable A, we have almost reached statistical parity, and for B, we have. We are closer to equal opportunity, although there was a shift in the advantage. For equalized odds, we are closer to fairness when looking at variable A but not B, and we have for both a shift in the advantage. All in all, the change of basis method has achieved the removal of linear dependence between the protected and non protected variables. We can also draw the conclusion that all three fairness definitions are not compatible.