1

Template-Based Static Posterior Inference for Bayesian Probabilistic Programming

Abstract.

In Bayesian probabilistic programming, a central problem is to estimate the normalised posterior distribution (NPD) of a probabilistic program with score (a.k.a. observe) statements. Prominent approximate approaches to address this problem include Markov chain Monte Carlo (MCMC) and variational inference (VI), but neither of them is capable of generating guaranteed outcomes within a finite time limit. Moreover, most existing formal approaches that perform exact inference for NPD are restricted to programs with closed-form solutions to NPD or bounded loops/recursion. A recent work (Beutner et al., PLDI 2022) proposed an automated approach that derives guaranteed bounds for NPD over programs with unbounded recursion. However, as this approach requires recursion unrolling, it suffers from the path explosion problem. Furthermore, previous approaches do not consider score-recursive probabilistic programs that allow score statements inside loops, which is non-trivial and requires careful treatment to ensure the integrability of the normalising constant in NPD.

In this work, we propose a novel automated approach to derive bounds for NPD via polynomial templates, fixed-point theorems and Optional Stopping Theorem (OST). Our approach can handle probabilistic programs with unbounded while loops and continuous distributions with infinite supports. The novelties in our approach are three-fold: First, we use polynomial templates to circumvent the path explosion problem from recursion unrolling; Second, we derive a novel multiplicative variant of OST that addresses the integrability issue in score-recursive programs; Third, to increase the accuracy of the derived bounds via polynomial templates, we propose a novel technique of truncation that truncates a program into a bounded range of program values. Experiments over a wide range of benchmarks demonstrate that our approach is time-efficient and can derive bounds for NPD that are comparable with (or even tighter than) the recursion-unrolling approach (Beutner et al., PLDI 2022).

1. Introduction

In probabilistic programming, Bayesian statistical probabilistic programming adds specific statements for Bayesian reasoning into probabilistic programs. The principle of Bayesian probabilistic programming aims at first modelling probabilistic models as probabilistic programs and then analyzing the models through their program representation. Compared with traditional approaches (McIver and Morgan, 2004, 2005; Chakarov and Sankaranarayanan, 2013a; Chatterjee et al., 2016a) that specify an ad-hoc language, probabilistic programming languages (PPLs) (van de Meent et al., 2018) provide a universal framework to perform Bayesian inference. Unlike standard programming languages, PPLs have two specific constructs: sample and score (Borgström et al., 2016).111Sometimes observe is used instead of score (Gordon et al., 2014), which has the same implicit effect. The former construct allows drawing samples from a (prior) distribution, while the latter records the likelihood of observed data in the form of “score(weight)”.222The argument “weight” corresponds to the likelihood each time the data is observed. The universality of PPLs has the potential of enabling scientists and engineers to design and explore sophisticated probabilistic models easily: when using these languages, they no longer need to worry about developing custom inference engines for their models, which is previously a highly-nontrivial task that requires expertise in both statistics and machine learning. Thanks to its universality, Bayesian probabilistic programming has nowadays become an active research subject in both machine learning and programming language communities, and there have been an abundance of PPLs for Bayesian inference, such as Pyro(Bingham et al., 2019), WebPPL(Goodman and Stuhlmüller, 2014), Anglican(Tolpin et al., 2015), Church(Goodman et al., 2008), etc.

In this work, we consider the central problem of analyzing the normalised posterior distribution (NPD) in Bayesian inference over probabilistic programs. The general setting of this problem is that given a prior distribution over the latent variables of interest and the distribution of the probabilistic model represented by a probabilistic program, the task is to estimate the NPD by observing the evidence with the likelihood . Note that the problem can be generally solved by the Bayes’ rule , but the main difficulty to apply Bayes’ rule is that the normalising constant is usually intractable to compute.

In the literature, there are two classes of approaches to address the NPD problem. The first is the approximate approaches that estimate the NPD by random simulations, while the second is the formal approaches that aim at deriving guaranteed bounds for NPD. In approximate approaches, two dominant methods are Markov chain Monte Carlo (MCMC) (Gamerman and Lopes, 2006) and variational inference (VI) (Blei et al., 2017). Although approximate approaches can produce approximate results efficiently, they cannot provide formal guarantee within a finite time limit. Moreover, as shown in (Beutner et al., 2022), approximate approaches may produce inconsistent results between different simulation methods. In formal approaches, there is a large amount of previous works such as PSI (Gehr et al., 2016, 2020), AQUA (Huang et al., 2021), Hakaru (Narayanan et al., 2016) and SPPL (Saad et al., 2021), aiming to derive exact inference for NPD. However, these methods are restricted to specific kinds of programs, e.g., programs with closed-form solutions to NPD or without continuous distributions, and none of them can handle probabilistic programs with unbounded while-loops/recursion. Recently, Beutner et al. (Beutner et al., 2022) proposed an approach that infers guaranteed bounds for NPD and allows unbounded recursion. The main techniques in this approach are (i) the unrolling of every recursion in a probabilistic program to eliminate the appearance of recursion, (ii) the widening operator of abstract interpretation to eliminate the non-termination case in the unrolling and (iii) the interval semantics to handle continuous distributions.

Challenges and gaps.

In this work, we focus on developing formal approaches to derive bounds for NPD over probabilistic programs. In the previous formal approaches to address this problem, the most relevant work is Beutner et al. (2022), but it has the following drawbacks. The first is that this approach is based on recursion unrolling, and hence may cause path explosion. The second is that this approach cannot handle the situation where score statements with weight greater than appear inside a loop. In the sequel, we call such programs score-recursive, and show that score inside a loop may cause unbounded weights and integrability issues and thus requires careful treatment. Staton et al. (Staton et al., 2016) also noted that for a non-recursive -calculus with score, unbounded weights may introduce the possibility of “infinite model evidence errors”. To circumvent the second drawback, previous results (e.g., Borgström et al. (Borgström et al., 2016)) allow only -bounded weights, and no existing approaches can handle score-recursive programs whose weight of score can be greater than .

Template-based approaches.

To avoid the path explosion problem arising from the recursion unrolling method (Beutner et al., 2022), we consider the template paradigm (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2018, 2016a) that first sets up a numerical template for the bound function to be solved, then establishes constraints for the template which is derived from the underlying verification theory (e.g. fixed point theory, Optional Stopping Theorem, etc.), and finally solves the template based on the derived constraints to obtain a concrete bound function. Template-based approaches have been shown to be capable of synthesizing tight bounds for expectation and probabilistic properties over probabilistic programs (Wang et al., 2019, 2021b), and are time efficient since they can leverage highly optimized constraint solvers for linear, semidefinite, and convex programming, etc. Therefore, the template paradigm serves as a good candidate to address the NPD problem in Bayesian probabilistic programming. However, simply applying the template paradigm does not suffice by the following reasons:

-

•

The most accurate numerical template by far is polynomial template. However, polynomial template is tight only over a bounded region (see e.g. Weierstrass Approximation Theorem (Jeffreys, 1988)), and in general is not accurate over an unbounded region.

-

•

The common pattern for a template-based approach is to synthesize a single bound function via a single process of template solving. However, having a single template is not enough for synthesizing tight bounds for NPD, as different initial program inputs may need different bound functions to achieve tight bounds.

In this work, we have careful treatment to address the two weakness above. Our detailed contributions are as follows.

Our contributions.

In this work, we present the following contributions:

-

•

First, to circumvent the path explosion from loop unrolling (that corresponds to recursion unrolling in functional programs) in the previous work (Beutner et al., 2022), we propose a novel approach that uses polynomial templates (Chatterjee et al., 2016b, 2020; Wang et al., 2019), fixed-point theorems (Tarski, 1955) and Optional Stopping Theorem (OST) (Williams, 1991) to synthesize polynomial bounds for NPD.

-

•

Second, to address the integrability issue from score-recursive programs, we present a novel multiplicative variant of the classical OST to derive expectation bounds. This addresses the challenge of handling score-recursive probabilistic programs stated previously.

-

•

Third, to increase the accuracy of the derived bounds, we propose a novel truncation operation that truncates the probabilistic program of concern onto a bounded range of program values, which allows our algorithm to explore high-degree polynomials to improve the accuracy of the derived bounds. Moreover, we devise our algorithm in the way to synthesize multiple bounds for various initial program inputs to further improve the accuracy. The truncation operation and the synthesis of multiple bounds address the weakness of the existing template-based approaches in the literature.

-

•

Finally, experimental results show that our approach can handle a wide range of benchmarks including non-parametric examples such as Pedestrian (Beutner et al., 2022) and score-recursive examples such as phylogenetics (Ronquist et al., 2021). Compared with the previous approach (Beutner et al., 2022), our approach reduces the runtime by up to times, while deriving comparable or even tighter bounds for NPD.

Technical contributions.

Compared with the previous results on the use of template paradigm and OST, we propose a truncation operation (onto a bounded range of program values) that leverages the approximability of polynomials over a bounded region, and a multiplicative variant of OST that can handle score-recursive programs.

Limitations.

One limitation is that our approach has the combinatorial explosion that when the degree of the polynomial template increases, the time of the template solving increases exponentially. However, from our experimental results, a moderate choice of the degree (e.g., no more than ) suffices. Another is that for sampling statements with continuous distributions, our approach currently assumes polynomial density functions. However, with proper approximation via (piecewise) polynomials, our approach can handle any continuous density functions.

2. Preliminaries

We first review some basic concepts from probability theory (see standard textbooks such as (Pollard, 2002; Williams, 1991) for a detailed treatment), and then present the Bayesian probabilistic programming language and the normalised posterior distribution (NPD) problem. Throughout the paper, we denote by , and the sets of all natural numbers (including zero), integers, and real numbers, respectively.

2.1. Basics of Probability Theory

A measurable space is a pair , where is a nonempty set and is a -algebra on , i.e., a family of subsets of such that contains and is closed under complementation and countable union. Elements of are called measurable sets. A function from a measurable space to another measurable space is measurable if for all .

A measure on a measurable space is a mapping from to such that (i) and (ii) is countably additive: for every pairwise-disjoint set sequence in , it holds that . We call the triple a measure space. If , we call a probability measure, and a probability space. The Lebesgue measure is the unique measure on satisfying for all valid intervals in . For each , we have a measurable space and a unique product measure on satisfying for all .

The Lebesgue integral operator is a partial operator that maps a measure on and a real-valued function on the same space to a real number or infinity, which is denoted by or . The detailed definition of Lebesgue integral is somewhat technical, see (Rankin, 1968; Rudin et al., 1976) for more details. Given a measurable set , the integral of over is defined by where is the Iverson bracket such that if is true, and otherwise. If is a probability measure, then we call the integral as the expectation of , denoted by , or when the scope is clear from the context.

For a measure on , a measurable function is the density of with respect to if for all measurable , and is called the reference measure (most often is the Lebesgue measure). Common families of probability distributions on the reals, e.g., uniform, normal distributions, are measures on . Most often these are defined in terms of probability density functions with respect to the Lebesgue measure. That is, for each there is a measurable function that determines it: . As we will see, density functions such as play an important role in Bayesian inference.

Given a probability space , a random variable is an -measurable function . The expectation of a random variable , denoted by , is the Lebesgue integral of w.r.t. , i.e., . A filtration of is an infinite sequence such that for every , the triple is a probability space and . A stopping time w.r.t. is a random variable such that for every , the event {} is in .

A discrete-time stochastic process is a sequence of random variables in . The process is adapted to a filtration , if for all , is a random variable in . A discrete-time stochastic process adapted to a filtration is a martingale (resp. supermartingale, submartingale) if for all , and it holds almost surely (i.e., with probability ) that (resp. , ). See (Williams, 1991) for details. Applying martingales to qualitative and quantitative analysis of probabilistic programs is a well-studied technique (Chakarov and Sankaranarayanan, 2013a; Chatterjee et al., 2016a, 2017).

2.2. Bayesian Probabilistic Programming Language

The syntax of our probabilistic programming language (PPL) is given in Fig. 1, where the metavariables , and stand for statements, boolean expressions and arithmetic expressions, respectively. Our PPL is imperative with the usual conditional and loop structures (i.e., if and while), as well as the following new structures: (a) sample constructs of the form “” that sample a value from a prescribed distribution over and then assign this value to a sampling variable ; (b) score statements of the form “score()” that weight the current execution with a value expressed by (note that means the value of a probability density function w.r.t. at ); (c) probabilistic branching statements of the form “” that lead to the then part with probability and to the else part with probability . We also have sequential compositions (i.e., ";") and support return statements (i.e., return) that return the value of the program variable of interest. Note that are constants, and our language supports any distributions with continuous density functions and infinite supports, including but not limited to uniform and normal distributions.

Given a probabilistic program in our language, we distinguish two disjoint sets of variables in the program: (i) the set of program variables whose values are determined by assignments in the program (i.e., the expressions at the LHS of “:="); (ii) the set of sampling variables whose values are independently sampled from prescribed probability distributions each time they are accessed (i.e., each “" can be regarded as a sampling variable ).

Example 2.1.

Fig. 3 shows a Bayesian probabilistic program written in our PPL language. In this program, the set of program variables is , and the set of sampling variables is . Each time is executed, it samples a value uniformly from and then assigns the value to the variable . ∎

2.3. The Semantics of Our Programming Language

Let be a finite set of variables with an implicit linear order over its elements. A valuation on is a function that assigns a real value to each variable in . We denote the set of all valuations on by . For each , we denote the value of the -th variable (in the implicit linear order) in by , so that we can view each valuation as a real vector on . A program (resp. sampling) valuation is a valuation on (resp. ), respectively. For the sake of convenience, we fix the notations in the following way, i.e., we always use to denote a program valuation, and to denote a sampling valuation; we also write for the value of the return variable in .

Below we present the semantics for our programming language. Existing semantics in the literature are either measure-(Staton et al., 2016; Lee et al., 2020) or sampling-based (Mak et al., 2021; Beutner et al., 2022). To facilitate the development of our algorithm, we consider the transition-based semantics (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2016b) to our language and treat each probabilistic program as a weighted probabilistic transition system (WPTS). A WPTS extends a PTS (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2016b) with weights and an initial probability distribution.

Definition 2.2 (WPTS).

A weighted probabilistic transition system (WPTS) is a tuple

| (†) |

for which:

-

•

and are finite disjoint sets of program and resp. sampling variables.

-

•

is a finite set of locations with special locations . Informally, is the initial location and represents program termination.

-

•

is the initial probability distribution over with a finite support (denoted by ), while is a function that assigns a probability distribution to each . We call each an initial program valuation, and abuse the notation so that also denotes the independent joint distribution of all ’s ().

-

•

is a finite set of transitions where each transition is a tuple such that (i) is the source location of the transition, (ii) is the guard condition which is a predicate over variables , and (iii) each is called a weighted fork for which (a) is the destination location of the fork, (b) is the probability of this fork, (c) is an update function that takes as inputs the current program and sampling valuations and returns an updated program valuation in the next step, and (d) is a score function that gives the likelihood weight of this fork depending on the current program and sampling valuations.

In a WPTS, we use update and score functions to model the update on the program variables and resp. the likelihood weight when running a basic block of statements in a program, respectively. If there is no score statement in the block, then the score function is constantly . We always assume that a WPTS is deterministic and total, i.e., (i) there is no program valuation that simultaneously satisfies the guard conditions of two distinct transitions from the same source location, and (ii) the disjunction of the guard conditions of all the transitions from any source location is a tautology. The transformation from a probabilistic program into its WPTS can be done in a straightforward way (see e.g. (Chatterjee et al., 2018; Chakarov and Sankaranarayanan, 2013b)).

Example 2.3.

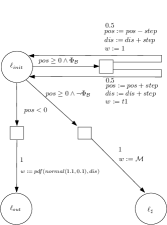

Fig. 3 shows the WPTS of the program in Fig. 3 which has two locations . The circle nodes represent locations and square nodes model the forking behavior of transitions. An edge entering a square node is labeled with the condition of its respective transition, while an edge entering a circle node stands for a fork, which is associated with its probability, update functions and score functions that marked by .333Here we omit the update functions if the values of program variables are unchanged. The value of is initialised to . An the initial probability distribution is determined by the joint distribution of where and observe the Dirac measures , and , respectively, e.g., the probability of the event “” equals . As simply receives values from a sampling variable, we neglect it in the WPTS.∎

We say that a WPTS is non-score-recursive if for all transitions in the WPTS with each fork (), we have that each score function is constantly (i.e., the multiplicative weight does not change) for every . Otherwise, the WPTS is score-recursive. Informally, a non-score-recursive WPTS has non-trivial score functions only on the transitions to the termination of a program, while a score-recursive WPTS has score statements in the execution of the program. For example, the WPTS of the program in Section 3.1 is non-score-recursive as the nontrivial (i.e., score values not equal to ) score statement only appears to the termination, while the WPTS of the program in Section 3.2 is score recursive since it has score statements inside the loop body. In the case of a non-score-recursive WPTS, we say that the WPTS is score-bounded by a positive real if for every in the WPTS with (), we have that whenever .

Given a program valuation and a predicate over variables , we say that satisfies (written as ) if holds when the variables in are substituted by their values in . A state is a pair where (resp. ) represents the current location (resp. program valuation), respectively, while a weighted state is a triple where is a state and represents the multiplicative likelihood weight accumulated so far.

Below we specify the semantics of a WPTS. Consider a WPTS in the form of († ‣ 2.2). The semantics of is formalized by the infinite sequence where each is the random weighted state at the th execution step of the WPTS such that (resp. , ) is the random variable for the location (resp. the random vector for the program valuation, the random variable for the multiplicative likelihood weight) at the th step, respectively. The sequence starts with the initial random weighted state such that is constantly , is sampled from the initial distribution and the initial weight is constantly set to 444This follows the traditional setting in e.g. (Beutner et al., 2022).. Then, given the current random weighted state at the th step, the next random weighted state is determined by: (a) If , then takes the same weighted state as (i.e., the next weighted state stays at the termination location ); (b) Otherwise, is determined by the following procedure:

-

•

First, since the WPTS is deterministic and total, we take the unique transition such that .

-

•

Second, we choose a fork with probability .

-

•

Third, we obtain a sampling valuation by sampling each independently w.r.t the probability distribution

-

•

Finally, the value of the next random weighted state is determined as that of .

Given the semantics, a program run of the WPTS is a concrete instance of , i.e., an infinite sequence of weighted states where each is the concrete weighted state at the th step in this program run with location , program valuation and multiplicative likelihood weight . A state is called reachable if there exists a program run such that for some .

Example 2.4.

Consider the WPTS in Example 2.3. Consider an initial program valuation which means that the initial values of are , respectively. Then starting from the initial weighted state , a program run w.r.t the WPTS semantics above could be

Given an initial program valuation of a WPTS, one could construct a probability space over the program runs by their probabilistic evolution described above and standard constructions such as general state space Markov chains (Meyn and Tweedie, 2012). We denote the probability measure in the probability space by and the expectation operator by .

2.4. Normalised Posterior Distribution

Before presenting the central problem of Bayesian probabilistic programming, i.e., analyzing normalised posterior distribution with our WPTS models, we introduce some technical concepts.

Definition 2.5 (Termination).

The termination time of a WPTS is the random variable given by for every program run where . That is, is the number of steps a program run takes to reach the termination location . A WPTS is almost-surely terminating (AST) if for all initial program valuations .

Definition 2.6 (Expected Weights).

Given a WPTS in the form of († ‣ 2.2), a designated initial program valuation and a measurable subset , the expected weight is defined as .

By definition, we have that (resp. ) is the random vector (resp. variable) of the program valuation (resp. the multiplicative likelihood weight) at termination, respectively. Thus, is the expectation of that start from the state and end with . If , the restriction of can be removed.

Below we define the normalised posterior distribution (NPD) problem.

Definition 2.7 (Normalised Posterior Distribution).

Given a WPTS in the form of († ‣ 2.2), the normalised posterior distribution (NPD) of is defined by:

where is the unnormalised posterior distribution w.r.t. , , and is the normalising constant. The WPTS is called integrable if we have .

Interval Bounds for NPD.

In this work, we consider the automated interval-bound analysis for NPD of a WPTS. Formally, we aim to derive an interval for an integrable WPTS and any measurable sets as tight as possible such that .

To achieve interval bounds for NPD, below we introduce the construction of a new WPTS based on the original WPTS and a measurable set .

Construction of .

Consider a probabilistic program and its WPTS , given a measurable set , we construct a new program by adding a conditional branch of the form “if then score() fi” immediately after the termination of and obtain the WPTS of . Therefore, and have the same initial probability distribution and the same finite support . The following proposition shows that interval-bound analysis for NPD can be reduced to interval-bound analysis for expected weights in the form .

Proposition 2.8.

Given a WPTS in the form of († ‣ 2.2), a measurable set and the WPTS constructed as above, we have that for any . Furthermore, if there exist intervals such that and for any , then we have two intervals such that the unnormalised posterior distribution and the normalising constant . Moreover, if is integrable, i.e., , then we can obtain the NPD .555The interval bounds derived in this manner may be loose, but they are definitely correct. Note that by Definition 2.7, , , and .

The proof of Proposition 2.8 is relegated to Section A.5. In the following, we will develop approaches to obtain interval bounds for expected weights.

3. Motivating Examples

In this section, we present an overview of our novelties via two motivating examples, namely the Pedestrian example and the Phylogenetic model. The Pedestrian example is non-score-recursive and handled by our fixed-point approach, while the Phylogenetic model is score-recursive and addressed by our OST approach.

Before we go into the details of the examples, we first present the workflow of our approaches. Given a probabilistic program and a measurable set , the workflow of our approaches is shown in Fig. 4: First, our parser transforms the input program into its WPTS in the form of († ‣ 2.2); Second, our approaches perform a truncation operation (to be introduced in Section 4.3) that restricts the WPTS into the bounded range of program values so that whenever the program runs out of the range, our approaches directly have upper and lower bounds to over- and under-approximate the behaviour of the program outside the bounded range, the purpose of which is that a bounded range allows our approach to derive tight bounds via templates; Third, the truncated WPTS is further handled by our fixed-point or OST approach, depending on whether or not is score-recursive, to generate polynomial bounds for expected weights at the termination of the program; Fourth, the interval bounds for the NPD are calculated by the interval-bound analysis for expected weights. An illustration of our workflow is given in Fig. 4.

3.1. Pedestrian Random Walk

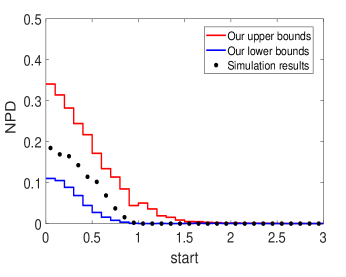

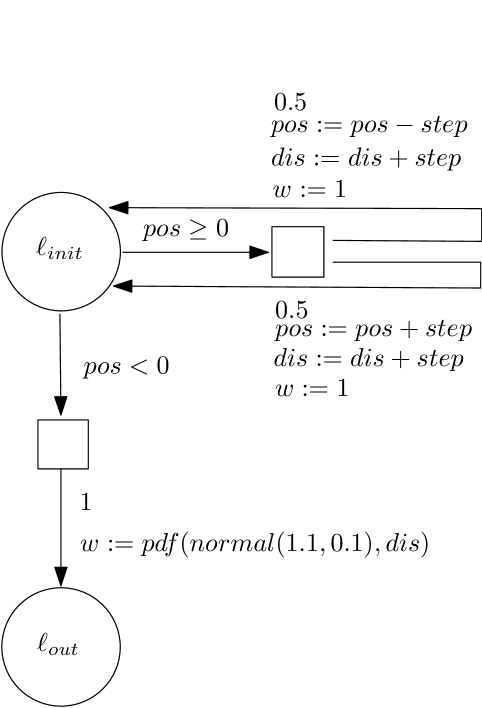

Consider the pedestrian random walk example (Mak et al., 2021) in Fig. 3. In this example, a pedestrian is lost on the way home, and she only knows that she is away from her house at most km. Thus, she starts to repeatedly walk a uniformly random distance of at most km in either direction of the road, until reaching her house. Upon she arrives, an odometer tells that she has walked km totally. However, this odometer was once broken and the measured distance is normally distributed around the true distance with a standard deviation of km. The question of this example is: what is the posterior distribution of the starting point? This example is modeled as a non-parametric probabilistic program whose number of loop iterations is unbounded. In the program, the variable represents the starting point, records the current position of the pedestrian, records the distance she walks in the next step, and records the total distance the pedestrian travelled so far. The probabilistic branch in the loop body specifies that the pedestrian walks either forward or backward, both with probability .

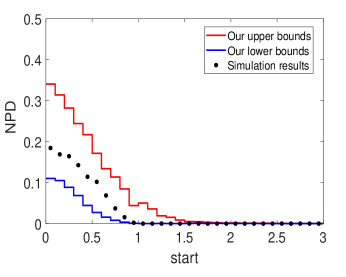

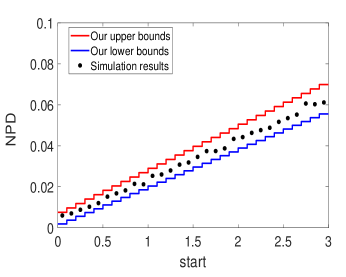

This program is non-score-recursive and was previously handled in (Beutner et al., 2022) by exhaustive recursion unrolling that has the path-explosion problem. To circumvent the path-explosion problem, in this work we propose a fixed-point theorem to establish constraints for this example, and solve the constraints by polynomial templates. To utilize the fact that polynomial approximation is usually accurate over a bounded range, during the solving of the polynomial templates, we restrict the behaviour of the program within a bounded range (e.g., ) and over-approximate the expected weights outside the bounded range by an interval (e.g. ). Note that here we omit the program variable as its value is determined once and has nothing to do with loop iterations. The solving of the polynomial template follows the previous approaches (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2018, 2016a) that consider linear/semidefinite programming. Our approach derives comparable bounds to the approach in Beutner et al. (2022) while our runtime is two-thirds of that of Beutner et al. (2022).

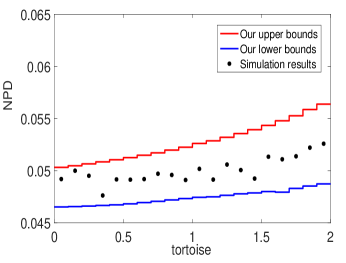

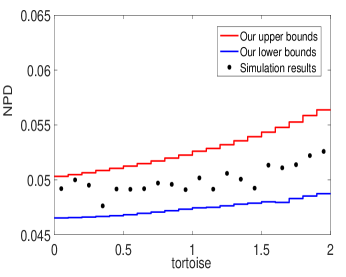

3.2. Phylogenetic Birth Model

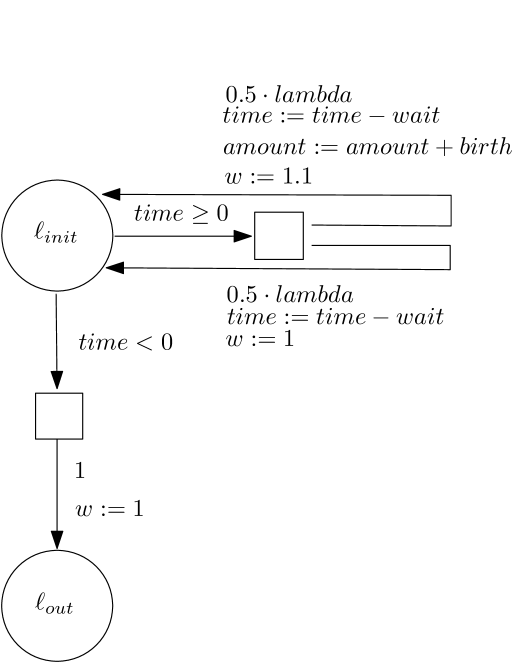

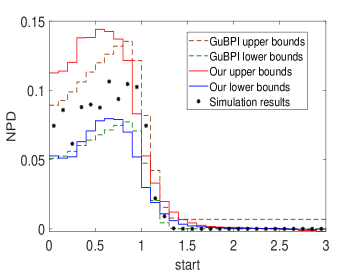

Consider a simplified version of the phylogenetic birth model (Ronquist et al., 2021) in Fig. 6, where a species arises with a birth-rate , and it propagates with a constant likelihood of at some time interval.666For simplicity, we assume constant weights that can be viewed as over-approximation for a continuous density function. This example is modelled as a probabilistic loop, where the variables stand for the birth rate of the species, the remaining propagation time, the current amount of the species and the propagation time to be spent, respectively. The variable is associated with a prior distribution, and the NPD problem is to infer its posterior distribution given the species evolution described by the loop. The WPTS of the program is given in Fig. 6.

This program cannot be handled by previous approaches (such as (Beutner et al., 2022; Gehr et al., 2020)) since it is a score-recursive program with an unbounded while loop and its score weight is greater than . To see why such a score-recursive program is nontrivial to tackle, consider a simple loop where in each loop iteration, the loop terminates directly with probability , and continues to the next loop iteration with the same probability. At the end of each loop iteration, a score command “score” is executed. It follows that the normalising constant in NPD is equal to , so that the infinity makes the posterior distribution invalid. One can observe that in this example the main problem lies at the fact that the scaling speed of the likelihood weight (i.e., ) is higher than that for program termination (i.e., ).

To tackle the difficulty of having scores greater than in a loop iteration, we propose a novel multiplicative variant of Optional Stopping Theorem (OST) that addresses score statements. Based on our OST variant, we apply truncation and polynomial template solving as in the non-score-recursive case. For example, we can restrict the behaviour of the program within a bounded range such as and , and over-approximate the expected weights outside the bounded range by an interval bound of polynomial functions derived from the same OST variant and polynomial-template method but without truncation. For the same reason as in Section 3.1, here we can safely omit the program variable . Our experimental result on this example shows that the derived bounds match the simulation result with samples.

4. Theoretical Approaches

In this section, we present our theoretical approaches for interval-bound analysis of expected weights in the form , namely the fixed-point approach, the OST approach. To obtain tight results, we also introduce the truncation operation.

4.1. The Fixed-Point Approach

We review some basic concepts of lattice theory. Given a partial order on a set and a subset an upper bound of is an element that is no smaller than every element of , i.e., Similarly, a lower bound for is an element that is no greater than every element of i.e. The supremum of denoted by , is an element such that is an upper-bound of and for every upper bound of we have Similarly, the infimum is a lower bound of such that for every lower-bound of we have We define and In general, suprema and infima may not exist.

A partially-ordered set is called a complete lattice if every subset has a supremum and an infimum. Given a partial order , a function is called monotone if for every in , we have

Given a complete lattice a function is called continuous if for every increasing chain in we have and cocontinuous if for every decreasing chain of elements of we have An element is called a fixed-point if Moreover, is a pre fixed-point if and a post fixed-point if . The least fixed-point of , denoted by is the fixed-point that is no greater than every fixed-point under Analogously, the greatest fixed-point of , denoted by , is the fixed-point that is no smaller than all fixed-points.

Theorem 4.1 (Kleene (Sangiorgi, 2011)).

Let be a complete lattice and be an continuous function. Then, we have

Analogously, if is cocontinuous, then we have

In this work, we apply the well-known Tarski’s fixed-point theorem.

Theorem 4.2 (Tarski (Tarski, 1955)).

Let be a complete lattice and a monotone function. Then, both and exist. Moreover, we have

Based on Theorem 4.2, we present our fixed-point approach for non-score-recursive WPTS’s. Below we fix a non-score-recursive WPTS in the form of († ‣ 2.2). Given a maximum finite value , we define a state function as a function such that for all , we have that . We denote the set of all state functions with maximum value by . We also use the usual partial order on that is defined in the pointwise fashion, i.e., for any , iff for all . It is straightforward to verify that is a complete lattice. For example, the top element (resp. the bottom element ) in the set is the constant function that maps every state to (resp. ), and the least upper bounds (resp. greatest lower bound) can be given via the pointwise infimum (resp. supremum), respectively.

To connect the complete lattice of state functions with expected weights (Definition 2.6), we define a special state function, called expected-weight function , by , and omit the subscript if it is clear from the context. Informally, is the expected weight of all program runs that start from without the restriction of the subset . In this work, we consider the following monotone function over the complete lattice .

Definition 4.3 (Expected-Weight Transformer).

Given a finite maximum value , the expected-weight transformer is the higher-order function such that for each state function and state , if is the unique transition that satisfies and for each , then we have that

| (1) |

Here the expectation is taken over a sampling valuation that observes the independent joint probability distributions of all the sampling variables .

Informally, given a state function , the expected-weight transformer computes the expected weight after one step of the WPTS execution. From the monotonicity of the Lebesgue integral (from the definition of expectation), we have that is monotone. Note that although the Lebesgue integral of a function usually requires measurability of the function, its preliminary definition is given via a supremum over simple functions not exceeding the function, and hence can be applied to all functions (including non-measurable functions) for which the monotonicity remains to be true. Therefore, we do not need to impose measurability here. In the following, we will omit the subscript in if it is clear from the context.

Definition 4.4 (Potential Weight Functions).

A potential upper weight function (PUWF) is a function that has the properties below:

-

(C1)

for all reachable states with , we have ;

-

(C2)

for all reachable states such that , we have .

Analogously, a potential lower weight function (PLWF) is a function that satisfies the conditions (C1’) and (C2), for which the condition (C1’) is almost the same as (C1) except for that “” is replaced with “”.

Informally, a PUWF is a state function that satisfies the pre fixed-point condition of ewt at non-terminating locations, and equals one at the termination location. A PLWF is defined similarly, with the difference that we use the post fixed-point condition instead.

The following result lays the backbone of our fixed-point approach.

Theorem 4.5.

Let be a non-score-recursive WPTS that is score-bounded by a positive real . If the WPTS has the AST property, then the expected-weight function ew is the unique fixed-point of the higher-order function ewt on the complete lattice .

Proof sketch..

Let . We first prove that the expected-weight function ew is the least fixed-point of the higher-order function ewt. Then we prove that the expected-weight transformer is both continuous and cocontinuous. Finally, according to Theorem B.1, we prove the uniqueness that , i.e., the fixed-point ew is unique. For the space limitation, we relegate the detailed proof for Theorem 4.5 to Appendix B.2. ∎

By a combination of Theorem 4.5 and Theorem 4.2, one has that it suffices to derive a pre fixed-point of ewt to obtain an upper bound for ew, and a post fixed-point to obtain a lower bound in the case of almost-sure termination of the program .

Theorem 4.6 (Fixed-Point Approach).

Let be a non-score-recursive WPTS that is score-bounded by a finite value . If the WPTS has the AST property, then (resp. ) for any PUWF (resp. PLWF) over and initial state , respectively.

Remark 1.

Notice that we always require a finite maximal value in our fixed-point approach. In general, our fixed-point approach cannot be applied to score-recursive Bayesian probabilistic programs, as in such a program a finite maximum weight may not exist.

4.2. The OST Approach

As stated in Remark 1, our fixed-point approach cannot handle score-recursive Bayesian probabilistic programs. To tackle score-recursive programs, we consider the adaption of Optional Stopping Theorem (OST) to our case. OST is a classical theorem in martingale theory that characterizes the relationship between the expected values initially and at a stopping time in a supermartingale. Below we first present the classical form of OST.

Theorem 4.7 (Optional Stopping Theorem (OST) (Williams, 1991)).

Let be a supermartingale adapted to a filtration , and be a stopping time w.r.t. the filtration . Then the following condition is sufficient to ensure that and :

-

•

, and

-

•

(bounded difference) there exists a constant such that for all , holds almost surely.

In our NPD problem, as the score statements accumulate weights in a multiplicative fashion, the classical OST cannot be applied since the bounded difference condition may be violated. To address this difficulty, we propose a novel variant of OST that tackles the multiplicative feature from score statements.

Theorem 4.8 (OST Variant).

Let be a supermartingale adapted to a filtration , and be a stopping time w.r.t. the filtration . Then the following condition is sufficient to ensure that and :

-

There exist integers and real numbers such that (i) for sufficiently large , and (ii) for all , holds almost surely.

Our OST variant extends the classical OST with the relaxation that we allow the magnitude of the next random variable to be bounded by that of with a multiplicative factor , which corresponds to the multiplicative feature from score statements. The intuition of the theorem is that to cancel the effect of the multiplicative factor, we require in extra the exponential decrease in . The proof resembles (Wang et al., 2019, Theorem 5.2) and is relegated to Section B.3.

Below we show how our OST variant can be applied to handle score-recursive WPTS’s. Fix a WPTS in the form of († ‣ 2.2). In the rest of this subsection, we reuse the expected-weight transformer ewt defined in Definition 4.3 and potential weight functions given in Definition 4.4. The slight difference is that for the expected-weight transformer in the context of a score-recursive WPTS, we consider that the weight function before termination may not be constantly .

To apply our multiplicative OST variant, we impose a bounded update requirement as in (Wang et al., 2019). A WPTS has the bounded update property if there exists a constant such that for every reachable state , if is the unique transition with each fork such that , then we have that .

We apply our OST variant (Theorem 4.8) in a way similar to (Wang et al., 2019, Theorem 6.10 and Theorem 6.12) to obtain the main theorem for our OST-based approach. To be more precise, we construct a stochastic process from a PUWF (or the negative of a PLWF) and show that the stochastic process is a supermartingale and the condition is fulfilled. The statement of the theorem is as follows.

Theorem 4.9 (OST Approach).

Let be a score-recursive WPTS that has the bounded update property. Suppose that there exist real numbers and such that

-

(E1)

for sufficiently large , and

-

(E2)

for each score function wt in we have .

Then for any PUWF (resp. PLWF) over , we have that (resp. ) for any initial state , respectively.

Proof Sketch..

For the upper bounds, we define the stochastic process as where is the program state at the th step of a program run. Then we construct a stochastic process such that where is the weight at the th step of the program run. We consider the termination time of and prove that satisfies the prerequisites of our OST variant (Theorem 4.8). This proof depends on the assumption that has concentration and bounded update properties, and the score functions in are also bounded (Item 2, Theorem 4.9)). Then by applying Theorem 4.8, we obtain that . By (C2) in Definition 4.4, we have that . Thus, we have that . For the lower bounds, the proof is similar. The more detailed proof is relegated to Section B.4. ∎

4.3. Truncation over WPTS’s

In the following, we propose a truncation operation for a WPTS that restricts the value of every program variable in the WPTS to a prescribed bounded range. We consider that a bounded range for a program variable could be either (), or if the value of the program variable is guaranteed to be non-negative or non-positive.

To present our truncation operation, we define the technical notions of truncation and approximation functions. A truncation function is a function that maps every program variable to a bounded interval in that specifies the bounded range of the variable . We denote by the formula for a truncation function . An approximation function is a function such that each () is intended to be an over- or under-approximation of the expected weight outside the bounded range specified by . The truncation operation is given by the following definition.

Definition 4.10 (Truncation Operation).

Let be a WPTS in the form of († ‣ 2.2). Given a truncation function and an approximation function , the truncated WPTS w.r.t. and is defined as where is a fresh deadlock location and the transition relation is given by

| (‡) | |||

for which (a) we have () where id is the identity function and is the constant function that always takes the value , and (b) for a fork in the original WPTS we have if and otherwise.

Thus, the truncated WPTS is obtained from the original one by first restraining each transition to the bounded range and then redirecting to the fresh deadlock location all the situations jumping out of the bounded range and not going to the termination location. To make the truncated WPTS deterministic and total, we add the self-loop . Our main theorem shows that by choosing an appropriate approximation function in the truncation, one can obtain upper/lower approximation of the original WPTS.

Theorem 4.11.

Let be a WPTS in the form of († ‣ 2.2), a truncation function and an approximation function. Suppose that the following condition () holds:

-

()

for each fork in the truncated WPTS that is derived from some fork with the source location in the original WPTS (see sentence (b) in Definition 4.10), we have that for all such that the state is reachable and .

Then for all initial program valuations . Analogously, if it holds the condition () which is almost the same as () except for that “” is replaced with “”, then we have for all initial program valuations .

The theorem above states that if the approximation function gives correct bounds for the expected weights of the original WPTS outside the bounded range, then the bounds for the expected weights of the truncated WPTS are also correct bounds for the expected weights of the original WPTS. The detailed proof is relegated to Appendix C.

Example 4.12.

Recall the Pedestrian example in Fig. 3, here we make truncation to this example and generate its truncated WPTS. The truncation function is defined such that , , so . Following the truncation operation in () from Definition 4.10, we can obtain as shown in Fig. 7.∎

5. Algorithmic Approaches

In this section, we present algorithmic implementation of our theoretical approaches in Section 4. We first have some assumptions on the input probabilistic program:

-

•

To enable the exact calculation of the integrals over the probability density functions in a Bayesian probabilistic program possible, we assume that every probability density function in a sampling statement is a polynomial. Likewise, in score-recursive programs, we require that the probability density function in any score statement is polynomial. Our approach can handle non-polynomial density functions in sampling and score statements by having their polynomial approximations, for which we leave as a future work.

-

•

To capture all possible program executions, we assume that the input probabilistic program is accompanied with invariants (see e.g. (Chakarov and Sankaranarayanan, 2013a; Sankaranarayanan et al., 2004)) to over-approximate reachable states. We follow (Colón et al., 2003; Sankaranarayanan et al., 2004) to consider affine invariants. An affine invariant for a WPTS is a map that assigns to each location a (conjunctive) system of affine inequalities such that for all reachable states , every affine inequality in holds w.r.t the program values given in the program valuation .

We also present the high-level technical setting of our algorithms. Consider an input WPTS in the form of († ‣ 2.2). Recall the normalising constant in Definition 2.7. To tighten the interval bounds for , we split the set of initial program valuations into disjoint partitions such that and for any .777If , the set is not split. Our algorithms tackle each () separately to obtain polynomial interval bounds (where are polynomials) such that for all . It follows that the interval bound for can be derived by integrals of polynomial bounds over all ’s, that is,

| () |

Given a measurable set , the interval bounds for the unnormalised posterior distribution (in Definition 2.7) can be obtained analogously by deriving polynomial bounds for (see Proposition 2.8).

Below we present our algorithmic methods to deriving interval bounds for the normalising constant. The unnormalised posterior distribution can be derived in the same manner. Our algorithms are template-based and have the following stages:

Stage 1: Input. First, our algorithms receive a WPTS parsed from a Bayesian probabilistic program written in our PPL and an affine invariant for the WPTS as the basic input. Besides, the algorithms receive as auxiliary inputs a truncation function and two approximation functions that respectively fulfill the conditions (), () in the statement of Theorem 4.11. The truncation function is represented by the bounded intervals for each program variable, and the approximation functions are derived either from the score function at the termination of a non-score-recursive program or by applying our OST variant directly to a score-recursive program (without truncation). We also have two parameters , for which is the degree of our polynomial template and is the number of partitions for the set of initial program valuations (refer to ( ‣ 5)).

Moreover, if the program is non-score-recursive and its score function at the termination is non-polynomial, our algorithms take as extra inputs a (piecewise) polynomial approximation of and an error bound such that for all ( is the extended bounded range of program variables that derived from a one-step program run and the truncation function , which will be introduced in Step A1 below).

Stage 2: Partition and Truncation. Next, our algorithms fetch the set from the WPTS , partition it into disjoint subsets and construct a set such that each . Our algorithms then perform the truncation operation to w.r.t the input truncation function and approximation functions . To synthesize upper bounds for expected weights, we take the truncation w.r.t and to generate a truncated WPTS . For lower bounds, we generate the truncated WPTS .

Example 5.1.

Recall the Pedestrian example in Section 3.1 and its WPTS in Fig. 3. We derive an invariant simply from the loop guard so that and . The truncation function is defined such that and . We pick the constant approximation functions and to bound the expected weights beyond the truncated range, so that we obtain two truncated WPTSs and which are similar to that in Fig. 7. We also choose the algorithm parameters as and .888We choose here to exemplify our algorithms, the values of for this example are larger in the experiments. Since the program is non-score-recursive and its score function at the termination is non-polynomial (i.e., ), we choose a polynomial approximation of with the error bound . We obtain the set . Since the value of in is fixed, we partition uniformly into disjount subsets on the dimension , i.e., . We calculate the midpoints of the dimension for all ’s, and construct the set .∎

Stage 3: Template Solving. Then our algorithms establish -degree polynomial templates for and , and synthesize polynomial upper and lower bounds for the expected weights and for each initial program valuation in by solving the templates w.r.t the PUWF and PLWF constraints (i.e., (C1), (C2), (C1’) from Definition 4.4), respectively. The correctness of this stage follows from Theorem 4.6 and Theorem 4.9.

Note that Theorem 4.6 and Theorem 4.9 have prerequisites and we check these prerequisites in a succinct fashion as follows. For Theorem 4.6, we manually verify the AST property by the approaches of (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2016b), and check the score-bounded property by a direct manual inspection. For Theorem 4.9, we check the condition (E1) by approaches such as (Chatterjee et al., 2018; Wang et al., 2021b), the condition (E2) by a manual examination, and the bounded update property by simple check on whether the update value is bounded by a constant. The checking of the AST can be automated by template-based approaches (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2016b), and other simple prerequisites can be easily automated (via e.g. SMT solvers). We leave a fuller implementation that incorporate these features as a future work.

Below we present the detailed steps (Step A1 – A4) of our template solving.

Step A1. Consider the truncated WPTS (to derive an upper bound) or (to derive a lower bound). We denote the bounded range from the truncation function by . In this step, both of our algorithms compute an extended bounded range such that any program valuation from a one-step execution of the WPTS under any current program valuation in falls in . Formally, the extended bounded range satisfies that for every location , program valuation , transition , fork in and sampling valuation , we have that . Our algorithms determine the extended bounded range by examining the assignment statements in the truncated WPTS . The purpose to have a superset of the original bounded range is to reduce the runtime in the solving of the template, see Step A3 below.

Example 5.2.

Recall Example 5.1, the bounded range from the truncation function is denoted by . For or , the extended bounded range is given by .∎

Step A2. In this step, at each location , our algorithms set up a -degree polynomial template over the program variables . Each template is a summation of all monomials of degree no more than and each monomial is multiplied with a fresh unknown coefficient as a parameter to be resolved. For , our algorithms assume .

Example 5.3.

Recall Example 5.1, the algorithm parameter . For either or , we construct a -degree polynomial template at the location , i.e., where are unknown coefficients to be resolved, and let .∎

Step A3. In this step, our algorithms establish constraints for the templates ’s from (C1), (C1’) in Definition 4.4 (as (C2) is satisfied by the construction of in the previous step). For upper bounds on expected weights, our algorithms have the following relaxed constraints of (C1) to synthesize a PUWF over :

-

(D1)

For every location and program valuation , we have that .

-

(D2)

For every location and program valuation , we have that .

For lower bounds over , our algorithms have the relaxed PLWF constraints (D1’) and (D2’) which are obtained from (D1) and resp. (D2) by replacing “” with “” in (D1) and resp. “” with “” in (D2), respectively. We have that (D1) and (D2) together ensure (C1) since implies that for every location and program valuation . The same holds for (D1’) and (D2’).

Note that in (D1), the calculation of the value has the piecewise nature that different sampling valuations may cause the next program valuation to be within or outside the bounded range, and to satisfy or violate the guards of the transitions in the WPTS. In our algorithms, we have a fine-grained treatment for (D1) that enumerates all possible situations for a sampling valuation that satisfy different guards of the WPTS in the calculation of , for which we use an SMT solver (e.g., Z3 (De Moura and Bjørner, 2008)) to compute the situations. As for (D2), we use (D2) to avoid handling the piecewise feature in the computation of from within/outside the bounded range (i.e., the computation is a direct computation over a single-piece polynomial), so that the amount of computation of is reduced by ignoring the piecewise feature. The use of (D2) to reduce the computation is the aim of introducing an extended bounded range in Step A1. The same also holds for (D1’) and (D2’).

If is non-score-recursive and the score function at termination is non-polynomial, our algorithms replace in the expression with its polynomial approximation .

Example 5.4.

Recall Example 5.1–Example 5.3, the bounded range in (D1) is defined such that . Consider to derive upper bounds from . We make a fine-grained treatment for (D1) by splitting the range and enumerating all possible situations for the sampling valuation that the next program valuation satisfies or violates the loop guard “”. In detail, is split into and , where stands for the situation that with different sampling valuations the next program valuation may satisfy the loop guard (so that the next location is ) or violate the loop guard (so that the next location is directed to ), and stands for the situation that the next program valuation will definitely satisfy the loop guard and the next location is . For the non-polynomial score function at the termination of the example, we replace it with a polynomial approximation under the error bound .

We first show the PUWF constraints for . Recall that the program has two probabilistic branches with probability . When the current program valuation is in , we observe that

-

•

if the loop takes the branch , then the next value of remains to be non-negative and the loop continues, and

-

•

if the loop takes the branch , then it is both possible that the next value of satisfy or violate the loop guard, depending on the exact value of .

Then we have the constraint (D1.1) over that has expectation over a piecewise function on derived from whether the loop terminates in the next iteration or not, as follows:

-

(D1.1)

When the current program valuation is in , we observe that the next program valuation is guaranteed to satisfy the loop guard, and hence we have the constraint as follows:

-

(D1.2)

The range in (D2) is represented by the disjunctive formula . For the program valuation in , its next location is . Recall the constant approximation functions and . From (D2), we have two constraints from the disjunctive clauses in as follows:

-

(D2.1)

.

-

(D2.2)

.

For , the PLWF constraints (D1’.1) to (D2’.2) are obtained from the PUWF constraints above by replacing “” with “” and with . ∎

Step A4. In this step, for every initial program valuation in where ’s and are obtained from Stage 2, our algorithms solve the unknown coefficients in the templates ( via the well-established methods of Putinar’s Positivstellensatz (Putinar, 1993) or Handelman’s Theorem (Handelman, 1988). To be more detailed, our algorithms minimize (resp. maximize) the objective function for each in which subjects to the PUWF (resp. PLWF) constraints from the previous step to derive polynomial upper (resp. lower) bounds over (resp. ), respectively.

Note that the PUWF or PLWF constraints from Step A4 can be represented as a conjunction of formulas in the form where the set is defined by a conjunction of polynomial inequalities in the program variables and is a polynomial over whose coefficients are affine expressions in the unknown coefficients from the templates, and such formulas can be guaranteed by the sound forms of Putinar’s Positivstellensatz and Handelman’s Theorem. The application of Putinar’s Positivstellensatz results in semidefinite constraints and can be solved by semidefinite programming (SDP), while the application of Handelman’s Theorem is restricted to the affine case (i.e., every condition and assignment in the WPTS is affine) and leads to linear constraints and can be solved by linear programming (LP). We refer to Appendix C for the details on the application of Putinar’s Positivstellensatz and Handelman’s Theorem.

If the polynomial approximation is applied in the calculation of in Step A3, we show that the error of the final results will be bounded by the polynomial approximation error bound . See Theorem C.1 in the Appendix C.

Example 5.5.

Recall Example 5.1–Example 5.4, we have that and the set . Pick a point from , to synthesize the upper bound for as tight as possible, we solve the following optimization problem whose objective function is , i.e.,

| Subject to constraints (D1.1)–(D2.2) |

The lower bound for is solved by

| Subject to constraints (D1’.1)–(D2’.2) |

Although the constraints are universally quantified, the universal quantifiers can be soundly (but not completely) removed and relaxed into semidefinite constraints over the unknown coefficients ’s by applying Putinar’s Positivstellensatz, where we over-approximate all strict inequalities (e.g., ””) by non-strict ones (e.g., “”). Then we call a SDP solver to solve the two optimization problems and find the solutions of ’s, which will generate two polynomial bound functions such that and for all program valuation where the error bound . ∎

Stage 4: Integration. As a consequence of Stage 3, our algorithms obtain a group of concrete polynomial upper bound functions (resp. lower bound functions) (resp. ) for the expected weights (resp. ), respectively. Then our algorithms integrate these polynomial upper and lower bound functions to derive the upper and lower bounds for and , respectively. For , we have that

| (2) |

and the lower bound for is given by

| (3) |

If is non-score-recursive and the score function at termination is non-polynomial, our algorithms integrate the approximation error caused by polynomial approximation of to the two bounds, i.e, and , where is the volume of . In practice, to ensure the tightness of the interval bounds, we can control the amount of so that the approximation error is at least one magnitude smaller than the values of .

Theorem 5.6 (Soundness).

If our algorithms find valid solutions for the unknown coefficients of the templates, they return correct interval bounds for the normalising constant .

Proof Sketch..

By Theorem 4.6 (resp.Theorem 4.9), if the algorithms successfully find valid solutions for the unknown coefficients of the templates, we can obtain the polynomial upper bound (resp. lower bound ) for (resp. ), respectively. Then by Theorem 4.11, the polynomial upper bound is also the upper bound for and is the lower bound for . The same holds for the bounds if polynomial approximation of non-polynomial score functions happens. ∎

6. Experimental Results

In this section, we present the experimental valuation of our approach over a variety of benchmarks. First, we show that our approach can handle novel examples that cannot be addressed by other existing tools such as (Gehr et al., 2016, 2020; Huang et al., 2021; Narayanan et al., 2016). Then we compare our approach with the state-of-the-art tool GuBPI (Beutner et al., 2022). Finally, even though the problem of path probability estimations is not the focus of our work, we demonstrate that our approach can work well for this problem, and we also compare the performance of our approach with GuBPI.

We have implemented a parser from probabilistic programs to WPTS’s in F#, our algorithms in Matlab, and used the LP solver in Matlab (resp. Mosek (ApS, 2022)) for solving linear (resp. semidefinite) programming, respectively. All results were obtained on an Intel Core i7 (2.3 GHz) machine with 16 GB of memory, running MS Windows 10.

6.1. Experimental Setup

Below we clarify our experimental setting for the input programs with invariant, the input truncation and approximation functions and the polynomial approximation for the score statement at program termination in the non-score-recursive case.

Program Input. All the benchmarks in our experiments are of the form “” where are program statements without loops and is the loop guard which is a predicate over . We set two locations for all benchmarks, i.e., before while and after . Our algorithms also work for general programs with multiple locations. To reduce the influence from the choice of the invariant, we derive an invariant simply from the loop guard so that and .

Partition of Initial Program Valuations. We partition the set of initial program valuations into disjoint subsets by splitting the quantity of one dimension uniformly.

Truncation Function. For the truncation function , we first restrict the range of all program variables to the domain satisfying the loop guard . That is, . Then we empirically specify a large enough bounded range over program variables that captures the major behaviour of the program. That is, for some constant . Finally, is defined by for all .

Approximation Functions. To derive the approximation functions , we consider two cases:

-

•

in the case that is non-score-recursive, are obtained as follows.

-

–

If the score function at termination is non-polynomial, we determine by bounds and also the monotonicity of the score function over the set (see definitions of in Step A1 in Section 5).

-

–

Otherwise, we directly use the polynomial score function as .

-

–

-

•

in the case that is score-recursive, are derived by using our OST approach in Section 4.2 but without truncation operation, i.e., by directly applying Theorem 4.9.

Polynomial Approximation. In the case that is non-score-recursive and the score function at termination is non-polynomial, there are two situations that polynomial approximation should be applied. The first is that is handled by polynomial approximation of it over the set , which will be later used in (D1) in Step A3 in Section 5. The second is that are determined by polynomial approximation of over the set , which will be used in (D2) in Step A3 in Section 5. Concretely, we apply polynomial interpolation to approximate the non-polynomial score function . That is, given an error bound we aim to find a polynomial approximation for such that for all program valuations (or ). The above operation can be easily extended to produce piecewise polynomial approximations if are split into multiple partitions. For the first situation, the approximation error caused by polynomial interpolation is taken into account when calculating interval bounds for NPD (see Theorem C.1 in Appendix C).

6.2. Results

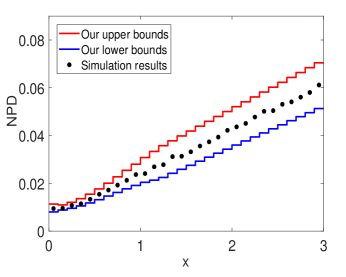

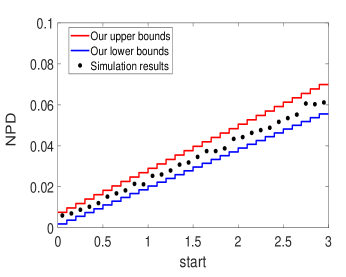

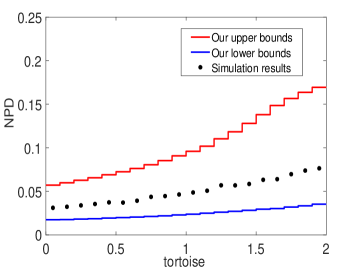

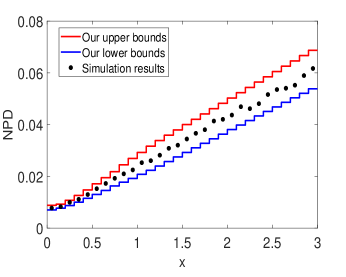

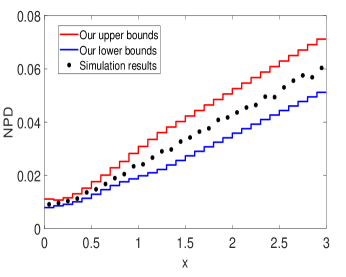

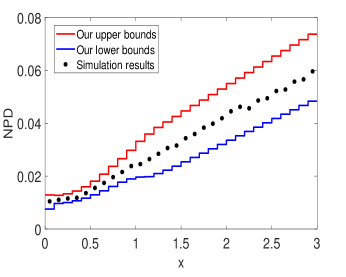

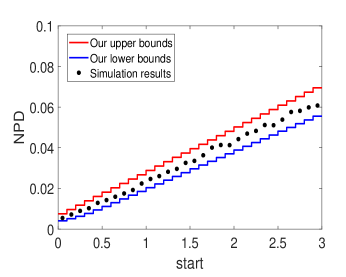

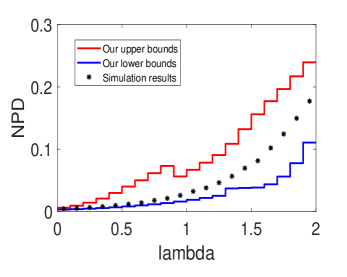

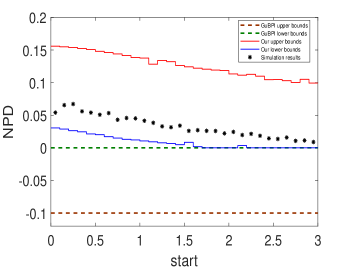

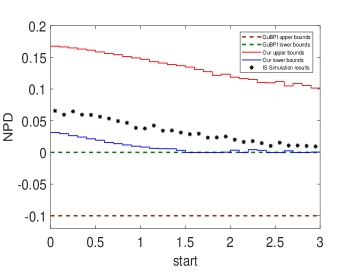

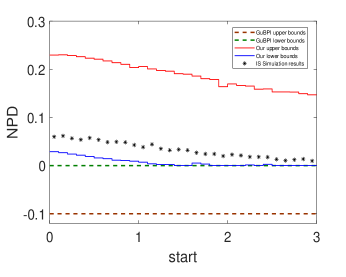

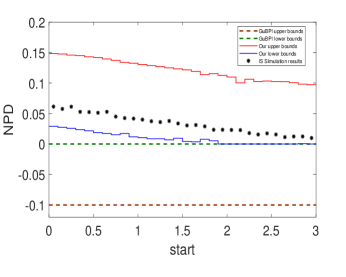

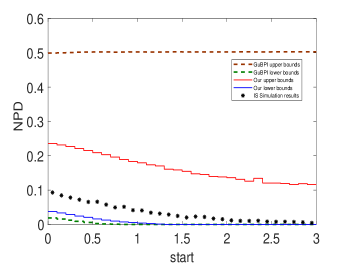

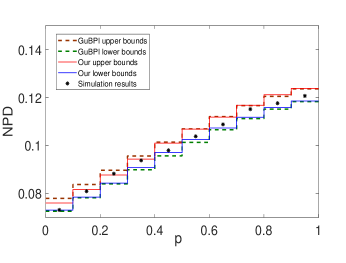

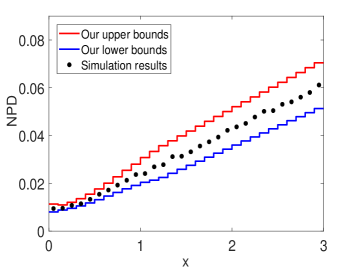

NPD - Novel Examples. We consider novel examples adapted from the literature, where all examples with prefix “Pd” or “RdWalk” are from (Beutner et al., 2022), the two “RACE” examples are from (Wang et al., 2021b), and the last example is from statistical phylogenetics (Ronquist et al., 2021) (see also Section 3). Concretely, the “RACE(V2)” and “BIRTH” examples are both score-recursive probabilistic programs with weights greater than , and thus their integrability condition should be verified by the existence of suitable concentration bounds (see Theorem 4.8); other examples are non-score-recursive probabilistic while loops with unsupported types of scoring by previous tools (e.g., polynomial scoring). Therefore, no existing tools w.r.t. NPD can tackle these novel examples. The results are reported in Table 1, where the first column is the name of each example, the second column contains the parameter of each example used in our approach (i.e., the degree of the polynomial template and the bounded range of program variables), the third column is the used solver, and the fourth and fifth columns correspond to the runtime of upper and lower bounds computed by our approach, respectively. We set the partition number . Our runtime is reasonable, that is, most examples can obtain tight bounds within seconds, and the simulation results by Pyro (Bingham et al., 2019) ( samples per case) match our derived bounds. Due to space limitation, we display part of the comparison in Fig. 9, see Appendix D for other figures.

| Benchmark | Parameters | Solver | Upper | Lower |

|---|---|---|---|---|

| Time (s) | Time (s) | |||

| Pd(v1) | , | SDP | ||

| Race(v1) | , | LP | ||

| Race(v2)* | , | LP | ||

| RdWalk(v1) | , | LP | ||

| RdWalk(v2) | , | LP | ||

| RdWalk(v3) | , | LP | ||

| RdWalk(v4) | , | LP | ||

| PdMB(v3) | , | LP | ||

| PdMB(v4) | , | LP | ||

| Birth* | , | LP |

-

*

It is a score-recursive probabilistic program with weights greater than .

-

•

The red and the blue lines mark the upper and lower bounds of our results; the black bold stars mark the simulation results; the brown and green dotted lines mark the upper and lower bounds generated by GuBPI (we denote by the infinity bounds).

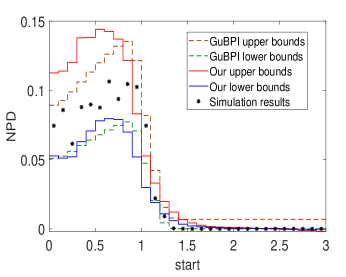

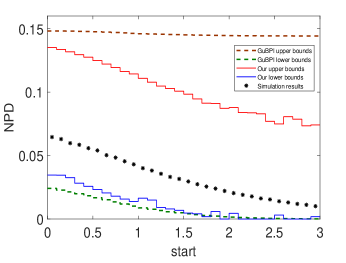

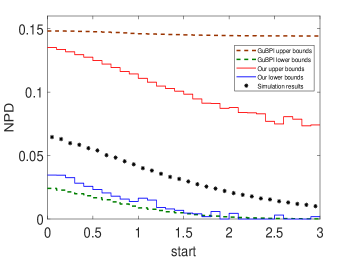

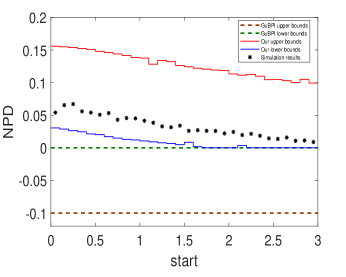

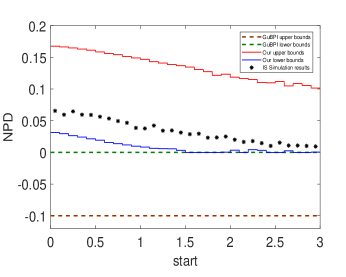

NPD - Comparision with GuBPI (Beutner et al., 2022). Since the parameters used in GuBPI and our approach are completely different, it is infeasible to compare the two approaches directly. Instead, we choose the parameters to our algorithms that can achieve at least comparable results with GuBPI. The main parameters are shown in Table 2 and we set the partition number . We consider the Pedestrian example “Pd” from (Beutner et al., 2022) (see also Section 3.1), and its variants. More concretely, we enlarged the standard deviation of the observed normal distribution to be for all other examples whose prefix name are “Pd”; for the four “PdBeta” examples, we also add different beta distributions in the loop bodies. The last example is from (Gehr et al., 2016). We report the results in Table 2 whose layout is similar to Table 1 except that the column “#” displays whether or not the bounds are trivial, i.e., . We also compare our results with GuBPI’s and simulation results ( samples per case), and show part of the comparison in Fig. 9, see Appendix D for other figures. Our runtime is up to 6 times faster than GuBPI while we can still obtain tighter or comparable bounds for all examples. Specifically, for the first example “Pd”, our upper bounds are a bit higher than GuBPI’s when the value of falls into (which is not suprising as the deviation of the normal distribution in this example is quite small, i.e., , and our approach constructs over-approximation constraints while GuPBI uses recursion unrolling to search for the feasible space exhaustively), but our lower bounds are greater than GuBPI’s, and our NPD bounds are tighter in the following.999When the value of approaches , our NPD bounds is close to zero, but the upper bounds may be lower than zero, which is caused by numerical issues of semi-definite programming. The problem of numerical issues is orthogonal to our work and remains to be addressed in both academic and industrial fields. For all variants of “Pd” where the deviation of the normal distrbution is enlarged, our NPD bounds are tighter than GuBPI’s, in particular, our upper bounds are much lower than GuBPI’s. For the four “PdBeta” examples, we also found that GuBPI produced zero-valued unnormalized lower bounds, thus its results w.r.t. NPD are trivial, i.e., . However, we can still produce non-trivial results and our runtime is at least 2 times faster than GuBPI.

| Benchmark | Our Tool | GuBPI | ||||

|---|---|---|---|---|---|---|

| Parameters | Solver | Time (s) | # | Time (s) | # | |

| Pd | , | SDP | ||||

| PdLD | , | LP | ||||

| PdBeta(v1) | , | LP | ||||

| PdBeta(v2) | , | LP | ||||

| PdBeta(v3) | , | LP | ||||

| PdBeta(v4) | , | LP | ||||

| PdMB(v5) | , | LP | ||||

| Para-recur | , | LP | ||||

-

*

marks the trivial bound , while marks the non-trivial ones.

Path Probability Estimation. We consider five recursive examples in (Beutner et al., 2022), which were also cited from the PSI repository (Gehr et al., 2016). Since all five examples are non-paramteric and with unbounded numbers of loop iterations, PSI cannot handle them correctly as mentioned in (Beutner et al., 2022). We estimated the path probability of certain events, i.e., queries over program variables, and report the results in Table 3. For the first three examples, we obtained tighter lower bounds than GuBPI and same upper bounds, while our runtime is at least 2 times faster than GuBPI. Moreover, we found a potential error of GuBPI. That is, the fourth example “cav-ex-5" in Table 3 is an AST program with no scores, which means its normalizing constant should be exactly one. However, the upper bound of the normailising constant obtained by GuBPI is smaller than (i.e., ). A stochastic simulation using samples yielded the results that fall within our bounds but violate those computed by GuBPI. Thus, GuBPI possibly omitted some valid program runs of this example and produces wrong results. All our results match the simulation results ( samples per case).

| Benchmark | Query | Our Tool | GuBPI | Simul | |||

|---|---|---|---|---|---|---|---|

| Parameters | Time (s) | Bounds | Time (s) | Bounds | |||

| cav-ex-7 | Q1 | ||||||

| Q2 | |||||||

| AddUni(L) | Q1 | ||||||

| Q2 | |||||||

| RdBox | Q1 | ||||||

| cav-ex-5 * | Q1 | ||||||

| Q2 | |||||||

| GWalk ** | Q1 | ||||||

| Q2 | |||||||

-

*

GuBPI’s result contradicts ours, and we found GuBPI produces wrong results for this example.

-

**

As we care about path probabilities, we compared bounds of unnormalized distributions for this example (the NPD can be derived in the same manner above).

7. Related Works

Below we compare our results with the most related work in the literature.

Static analysis in Bayesian probabilistic programming.

There are a lot of works on NPD inference for probabilistic programs, such as PSI (Gehr et al., 2016, 2020), AQUA (Huang et al., 2021), Hakaru (Narayanan et al., 2016) and SPPL (Saad et al., 2021). However, these methods are restricted to specific kinds of programs, e.g., programs with closed-form solutions to NPD or without continuous distributions, and none of them can handle probabilistic programs with unbounded while-loops/recursion. As far as we know, the most revelant work on static analysis of posterior distribution over unbounded loops/recursion is the approach (Beutner et al., 2022) that infers the bounds for posterior distributions by recursion unrolling and bounding the non-termination case via the widening operator of abstract interpretation. By unrolling recursion to arbitrary depth, this approach can achieve high precision on the derive bounds. However, a major drawback of this approach is that the recursion unrolling may cause path explosion. Our approach circumvents the path explosion problem by constraint solving. Another major drawback is that this approach cannot handle score-recursive programs as simply applying the approach to score-recursive programs leads to the trivial bound , and we address this issue by a novel OST variant.

MCMC and variational inference.

As mentioned previously, statistical approaches such as MCMC (Rubinstein and Kroese, 2016; Gamerman and Lopes, 2006) and variational inference (Blei et al., 2017) cannot provide formal guarantee on the bounds for posterior distributions in a finite time limit. In contrast, our approach has formal guarantee on the derived bounds.

Static analysis of probabilistic programs.

In recent years, there have been an abundance of works on static analysis of probabilistic programs. Most of them address fundamental aspects such as termination (Chakarov and Sankaranarayanan, 2013b; Chatterjee et al., 2016b; Fu and Chatterjee, 2019), sensitivity (Barthe et al., 2018; Wang et al., 2020), expectation (Ngo et al., 2018; Wang et al., 2019), tail bounds (Kura et al., 2019; Wang et al., 2021a; Wang, 2022), assertion probability (Sankaranarayanan et al., 2013; Wang et al., 2021b), etc. Compared with these results, we have:

-

•

Our work focuses on normalized posterior distribution in Bayesian probabilistic programming, and hence is an orthogonal objective.

- •

-

•

Our approach extends the classical OST as the previous works (Wang et al., 2019, 2021a) do, but we consider a multiplicative variant, while the work (Wang et al., 2019) considers only an additive variant, and the work (Wang et al., 2021a) considers a general extension through the uniform integrability condition and an implementation via polynomial functions, but does not have a detailed treatment for a multiplicative variant.

A very recent work (Batz et al., 2023) considers the synthesis of piecewise bounds for probabilistic programs. We focus on non-piecewise polynomial bounds and hence is orthognal. A promising future direction would be also to consider piecewise bounds in the NPD problem.

8. Conclusion

In this work, we considered the formal analysis of normalized posterior distribution in Bayesian probabilistic programming. Our contribution is a novel template-based approach that circumvents the the path explosion problem from loop/recursion unrolling and addresses score-recursive programs via a novel variant of Optional Stopping Theorem. A future direction would be to investigate whether our approach can be further improved by piecewise polynomials.

References

- (1)

- ApS (2022) MOSEK ApS. 2022. The MOSEK optimization toolbox for MATLAB manual. Version 10.0. http://docs.mosek.com/10.0/toolbox/index.html

- Barthe et al. (2018) Gilles Barthe, Thomas Espitau, Benjamin Grégoire, Justin Hsu, and Pierre-Yves Strub. 2018. Proving expected sensitivity of probabilistic programs. Proc. ACM Program. Lang. 2, POPL (2018), 57:1–57:29. https://doi.org/10.1145/3158145