Social and individual learning in the Minority Game

Abstract

We study the roles of social and individual learning on outcomes of the Minority Game model of a financial market. Social learning occurs via agents adopting the strategies of their neighbours within a social network, while individual learning results in agents changing their strategies without input from other agents. In particular, we show how social learning can undermine efficiency of the market due to negative frequency dependent selection and loss of strategy diversity. The latter of which can lock the population into a maximally inefficient state. We show how individual learning can rescue a population engaged in social learning from such inefficiencies.

Keywords: Financial markets, Individual learning, Minority Game, Self-organization, Social learning

1 Introduction

The Minority Game, inspired by the El Farol Bar problem [2], is a well-studied model of financial markets that exhibits self-organization of agents and phase transitions [8, 9, 10, 11, 31, 40]. It models a simplified market of buyers and sellers who use the history of past outcomes of the game to predict future ones. Agents have strategy tables that predict the future minority action based on the history of minority actions and thus give recommended actions. Using these strategy tables and given the history of minority actions, agents choose whether to buy or sell and succeed if their choice is the minority action of the population: the forces of supply and demand on prices being the intuition behind this. Since the size of the minority does not matter, there is an issue of efficiency in the market. The larger the minority, the more agents win in that round. Though a simplified model, the Minority Game is able to exhibit many qualitative behaviours of real markets [10, 16, 30].

There have been many extensions to the classic Minority Game, in particular the Evolutionary Minority Game [22, 27, 28, 29, 39]. In this framework, agents have an evolvable trait that determines whether or not they deviate from the strategies that the predictions of their strategy tables would recommend. The model has been extended in several ways, such as by incorporating a “genetic crossover” algorithm in which poorly performing agents can generate new strategies from their current strategies [36], and by setting the agents on networks [5, 13, 33, 42]. Evolution in the Minority Game on networks occurs by agents imitating neighbouring agents by copying their behaviours [12, 21, 26, 32, 33, 34, 35]. A variety of networks have been explored such as complete, random, regular, and scale-free networks. Imitation on these networks can be based on the payoffs of neighbours, and can lead to herding behaviour and thus high volatility [6].

Our goal here is to extend this line of research by further infusing ideas from social and individual learning [15, 38] into the Minority Game. Social learning is a mechanism of cultural transmission that has been well studied in biology and anthropology [25]. Through it, cultural traits, in our case financial strategies, can evolve in a population. Our framework thus fits under the novel field of social finance [24], which crosses the fields of finance with that of cultural evolution, the evolutionary study of social change [4, 7, 19]. It aims to understand markets through an ecological, evolutionary, and psychological view [1, 14, 20]. Social finance considers the ecology of investors: how they adopt beliefs and investment strategies from one another and how those impact market prices. Under the adaptive markets hypothesis [29], the change in investor behaviour is analogous to ecological and evolutionary processes in biology: through selection and adaptation, investors change their strategies in an evolving market.

Here, we explore the effects of the evolution of financial strategies in a framework of social finance. We do not consider the same evolving trait as in the Evolutionary Minority Game [22]. Rather, we consider the case where individuals can learn new strategy tables either via imitating their neighbours on a social network who have higher payoffs (i.e. social learning), or via creating novel strategy tables (i.e. individual learning). Such payoff-based social learning is well established in the literature on cultural evolution [23]. We show how social learning can undermine the efficiency of markets, and how individual learning can mitigate this effect.

2 Methods

Consider the classic Minority Game with an odd number of agents . Each agent has strategy tables, which are dictionaries with different combinations of memories of the last winning actions as keys and recommended actions as values: “1” or “-1” or, equivalently, “buy” or “sell”. Memory length is sometimes considered the “brain size” of agents, and each strategy table will thus have recommendations. Table 1 represents a strategy table with the key as a string of 1’s and -1’s and for memory length . Agents must choose one of their strategy tables and follow its recommendation independently of others’ actions each turn. During a turn of the game, all strategy tables earn virtual payoffs, which are payoffs an agent would have earned had they employed their recommendation. Agents will follow the recommendation of their strategy table with the greatest virtual payoff. Real payoffs are earned by agents who choose a specific recommendation from a strategy table and engage in it. At the end of each round, we count the number of buys and sells, and whichever side has more than of the total will be considered a losing strategy and the other strategy will be the winner. The real payoff of an agent with a losing strategy will be reduced by one, while the real payoff of an agent with a winning strategy will be increased by one. Virtual payoffs are calculated similarly: each strategy table earning them as if their recommendation that turn had been chosen. The game continues in this fashion for a number of turns, and agents may switch between different strategy tables as their virtual payoffs vary.

| Memory (key) | Recommendation |

| 111 | 1 |

| 11-1 | -1 |

| 1-11 | 1 |

| 1-1-1 | 1 |

| -111 | 1 |

| -11-1 | -1 |

| -1-11 | -1 |

| -1-1-1 | 1 |

Here we explore an agent-based extension of this game with social and individual learning, akin to selection based on payoff differences and mutation in biology. After every turn, agents will learn socially or individually with probabilities and , respectively. Thus, with probability , an agent will be paired with a different randomly chosen agent to learn from. We consider the case where this imitation occurs across a social network. Specifically, we construct complete graphs and Erdős-Rényi random graphs where agents can only socially learn from agents with which they share an edge. To construct the Erdős-Rényi random graphs, a pair of agents is connected with probability , where is the mean node degree. Once the graph is constructed, we assume that it remains fixed throughout the game. Once a focal agent has been paired with one of its neighbours on the social network to learn from, we simulate social learning according to the Fermi rule:

| (1) |

where is the probability that the focal agent imitates a strategy table from its paired agent . More specifically, agent compares its worst strategy, the one with the lowest virtual payoff , with agent ’s best strategy, the one with the highest virtual payoff . is the sensitivity to the difference in payoffs between the agents. If imitation occurs, agent replaces its worst strategy table with agent ’ best strategy table along with copying the virtual payoff for that strategy. For individual learning, with probability , we randomly select an agent’s strategy table, irrespective of its virtual payoff, and replace it with a randomly chosen strategy table from the set of all possible strategy tables with the same memory length (note this set contains strategy tables). The new strategy table is initialized with a virtual payoff of zero.

| Parameter | Definition |

| control parameter | |

| mean node degree | |

| payoff differential sensitivity | |

| individual learning rate | |

| social learning rate | |

| memory length | |

| number of agents | |

| probability of connecting two agents | |

| strategy tables per agent |

is an important control parameter in Minority Games, since the macroscopic behaviour of the system depends on it [31]. Thus, we plot much of the outcomes of our simulations with respect to . In our simulations, we track key measures of the outcome of the game: the attendance, volatility, and entropy. The attendance is the number of “buys” agents make in a given turn minus the number of sells: it’s thus a measure of the collective actions of all agents. The volatility is the time average variance of the attendance after each round of the game normalized by the population size:

| (2) |

since the time average . It is an inverse measure of the efficiency of resource distribution in the game and thus our key measure of the efficiency of the market. The lower it is, the more efficient the system. If is greater than or less than one, the market is worse or better than a random toss of a fair coin. In addition to these measures, we evaluate the diversity of strategy tables in the population by calculating the Shannon entropy of the strategy tables:

| (3) |

where is the frequency of strategy table in the population. We track the average of these values over time and over multiple games. A summary of the parameters their default values and the variables tracked can be found in Table 2.

3 Results

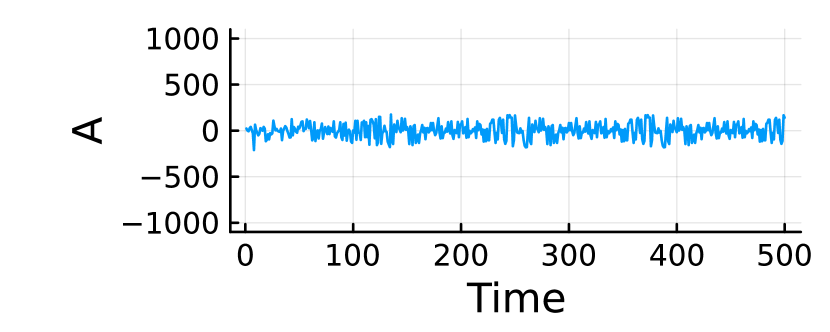

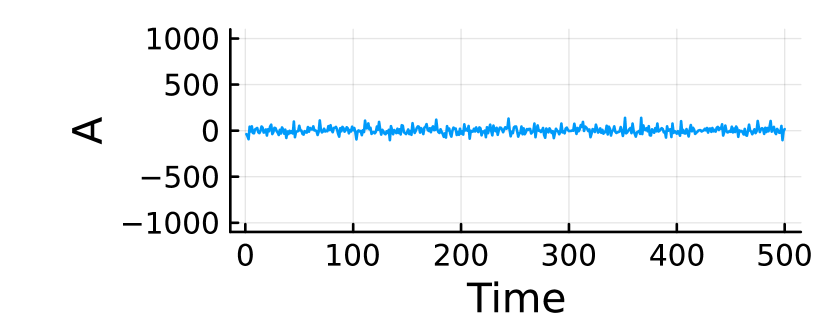

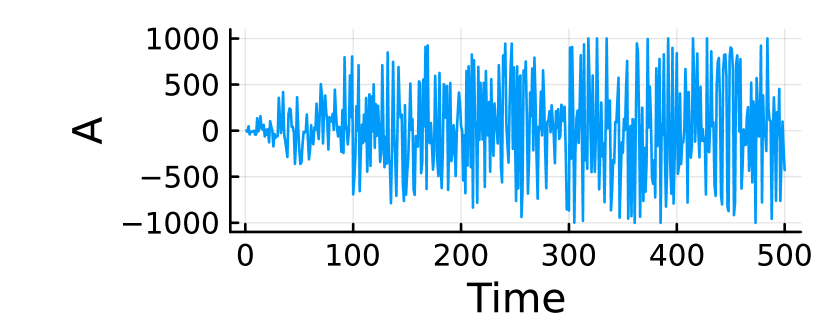

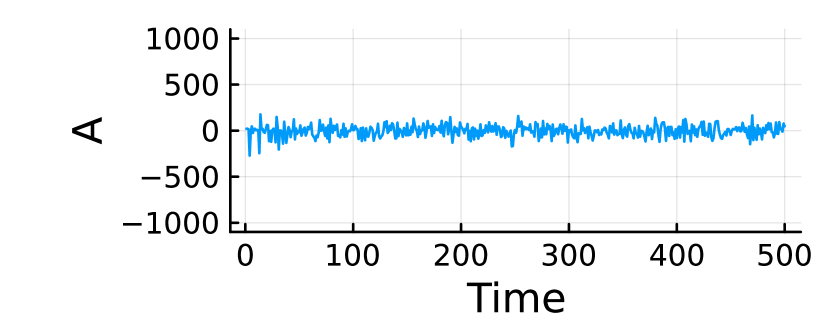

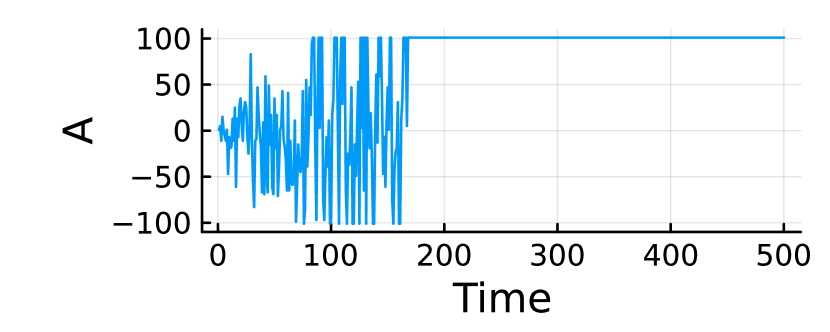

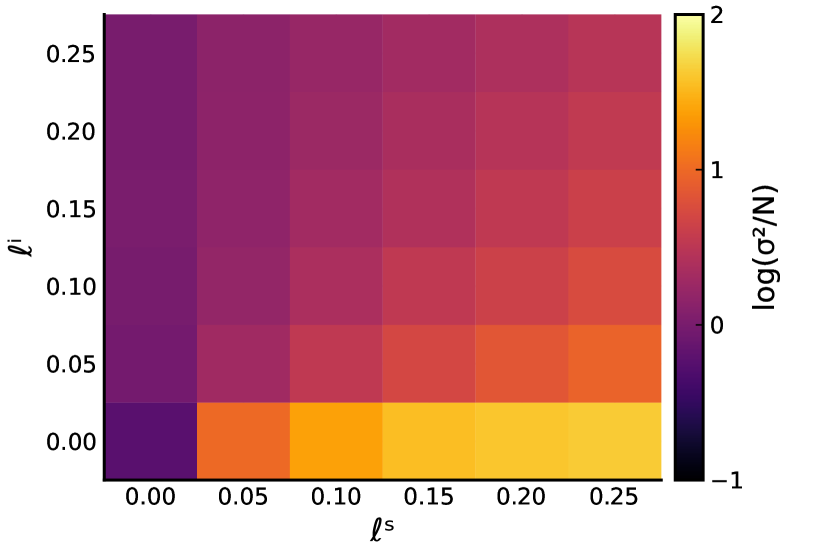

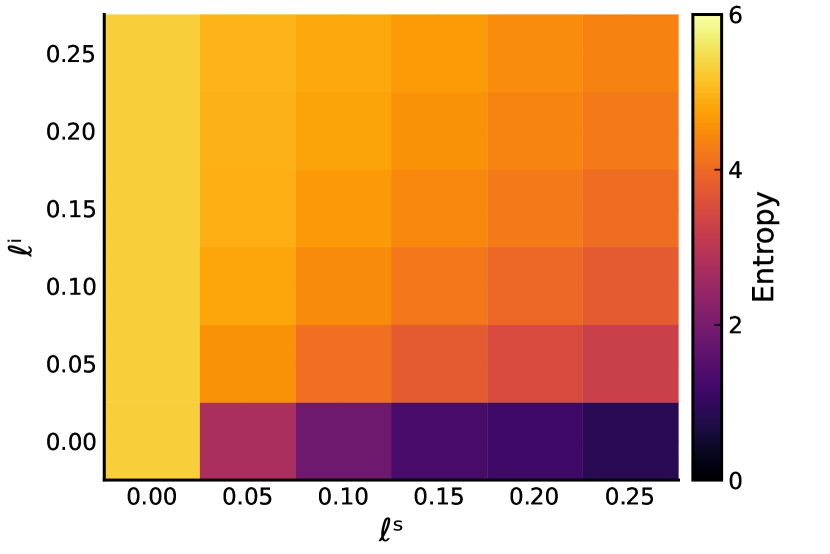

We begin our results by depicting several informative time series of the attendance in Figure 1. Social imitation on its own results in large swings in the population from buying to selling and thus a high volatility relative to the other cases. Because, payoffs are negative frequency dependent. A good strategy is readily imitated, which undermines its effectiveness. Social learning can also result in the population becoming locked into either buying or selling in which case no agent can ever win. Figure 1(e) is representative of this scenario. The population gets locked into always buying, since that is the only strategy recommendation agents have given a history of always buying. This phenomenon occurs because there is a crash in strategy table diversity as agents lose strategy tables by imitating others. Figure 2(b) depicts the entropy (diversity) of strategy tables at the end of a game given varying degrees of social and individual learning. We can observe a correlation between high volatility, low entropy, and high social learning. We also observe that individual learning can mitigate the negative effects of social learning, since individual learning fosters strategy table diversity.

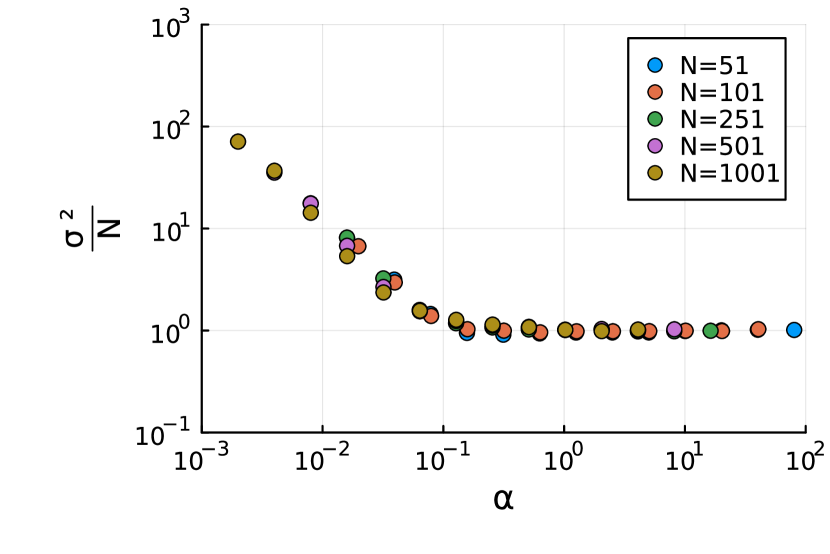

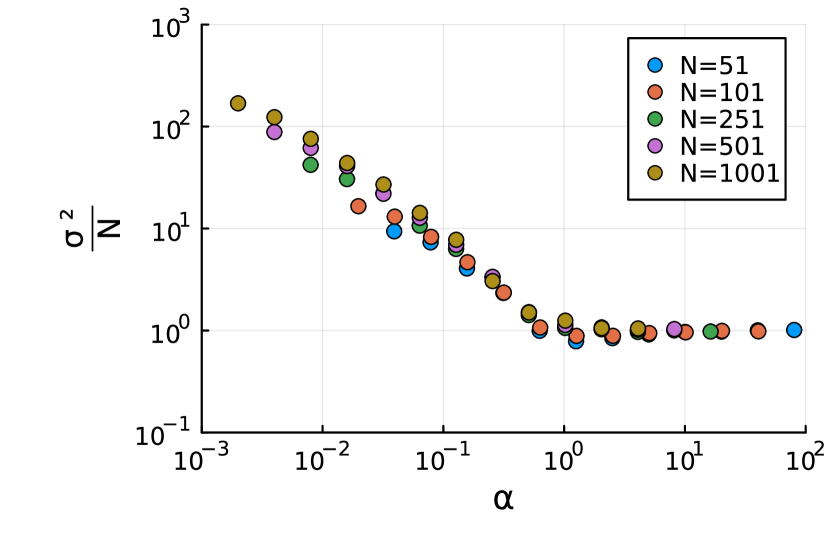

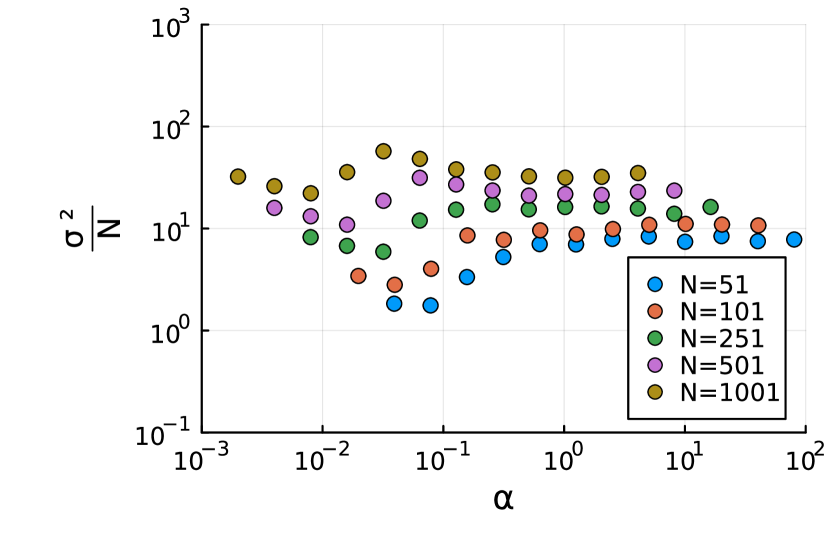

The normalized attendance variance or volatility is a key macroscopic observable of the system, and thus we plot it vs the control parameter in Figure 3. This figure compares a system with no individual or social learning, only individual learning, only social learning, and both individual and social learning. In the no individual learning or social learning case (Figure 3(a)), volatility, and thus the inefficiency of the system, decreases as we increase from a low level. The system then goes through a phase transition from a symmetric phase to an asymmetric phase around as has been uncovered in the literature [40], after which volatility increases and levels off. Thus, volatility reaches a minimum for an intermediate . However, there is no such minimum for the the Minority Game with individual learning (Figure 3(b)). Volatility simply decreases as increases and levels off at approximately . However, the decline is faster than when there is no such learning. Thus, for sufficiently low , individual learning can result in a more efficient market.

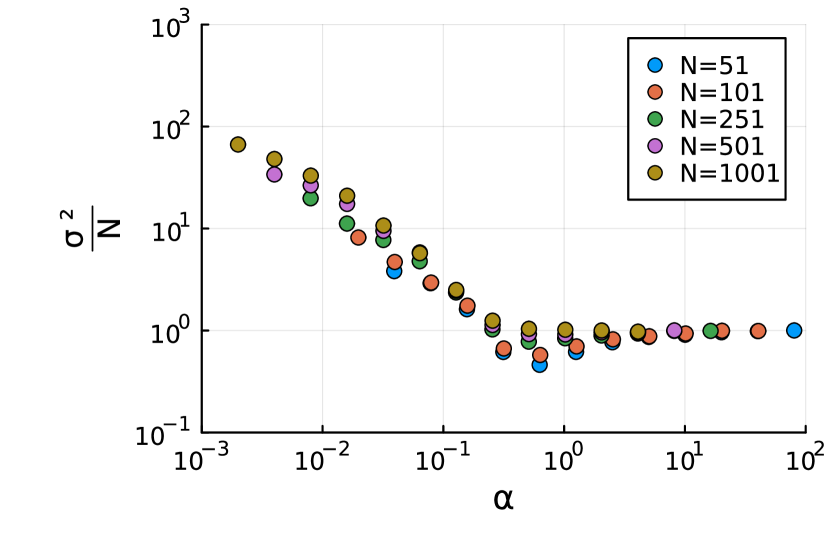

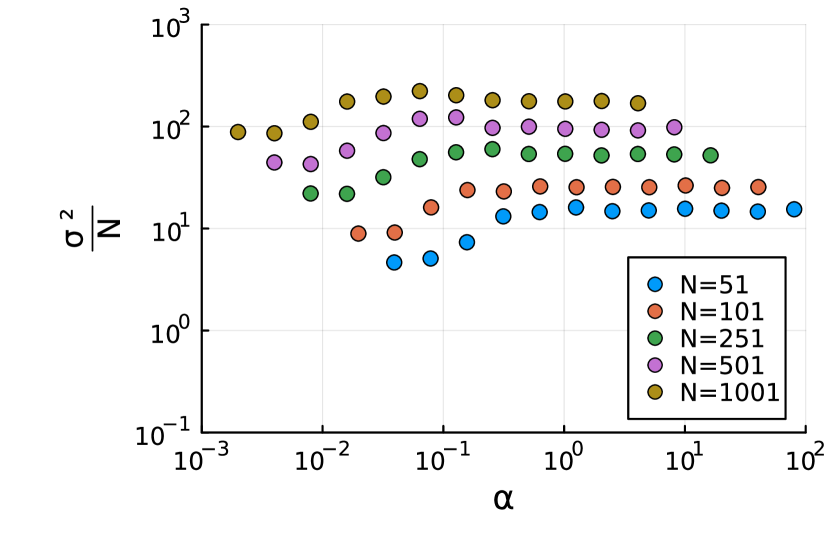

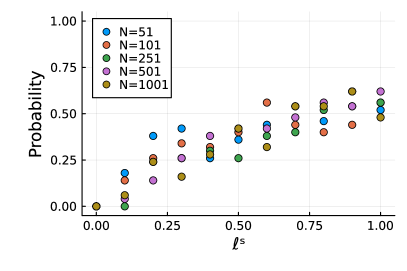

When there is only social learning (Figure 3(c)), we observe a separation of the volatilities by population size . Volatility decreases initially, but then increases before levelling off. Volatility is also much higher than when there is no individual or social learning and when there is individual learning, which aligns with the time series and heatmap results (Figures 1 and 2). Social learning results in high volatility, and this is worse the larger the population. The higher volatility from larger seems somewhat counter-intuitive, since a larger population should be more robust than a smaller one to loss of strategy diversity. However, this fact is the cause of the result. In the standard Minority Game, during a game. However, since the population can become locked into playing one strategy, volatility can go to zero in the long run for social learning as all agents make the same action every turn. This result is demonstrated in Figure 4, which plots the probability that the population becomes locked into either always buying or selling. For low learning rate , this probability increases as we decrease . The probabilities of becoming locked into a single action increase as . These probabilities for different become similar, since the outcome becomes noisier.

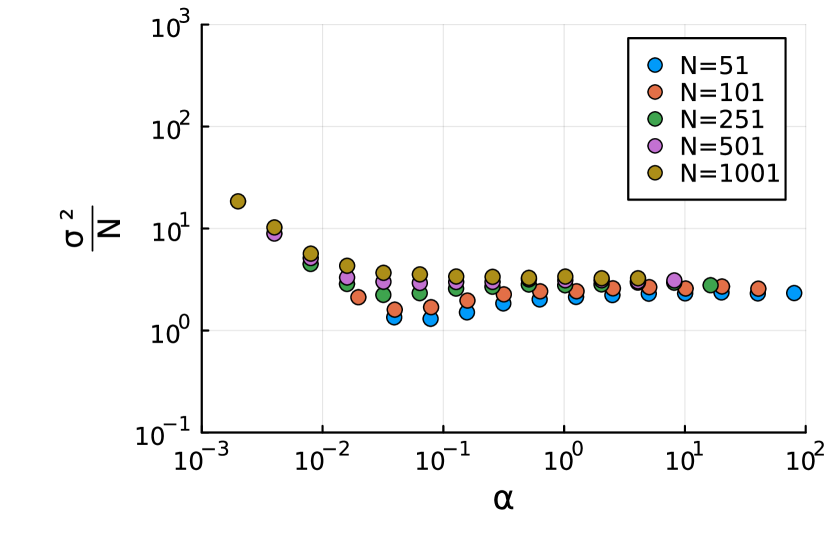

Though social learning can undermine efficiency in the market, allowing individuals to also learn individually can rescue it. Figure 3(d) depicts this case. When is low, volatility can be lower than the other three cases (Figures 3(a)-3(c)). Social learning here is improving agents’ strategy tables, and yet the negative frequency dependence and loss of diversity are being alleviated by the presence of individual learning. However, for higher , the cases with no individual and social learning and individual learning both have lower volatility.

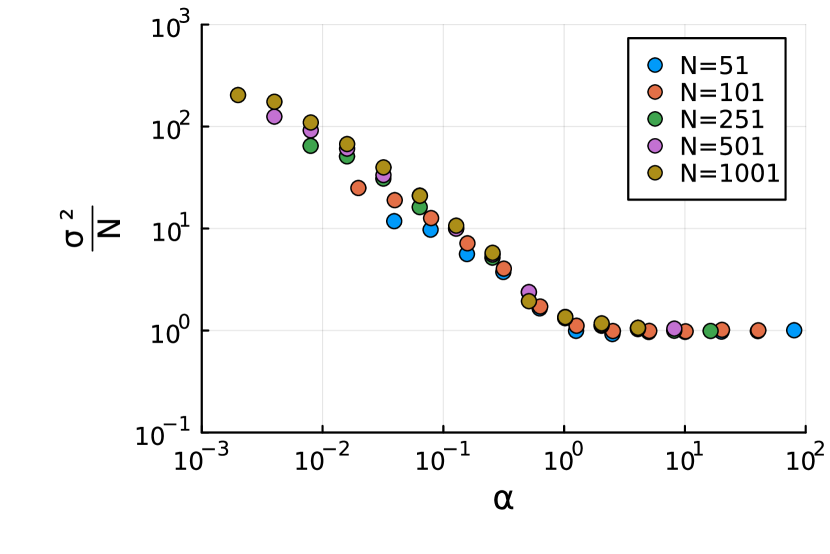

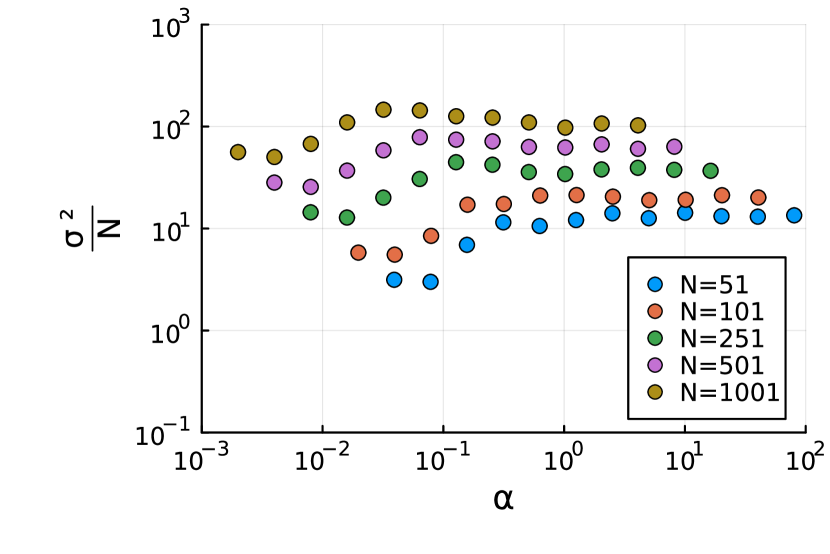

To explore the impact of further strategy tables per agent under social learning, we ran simulations for as depicted in Figure 5. Relative to the case where there is no individual or social learning, social learning has higher volatility. The difference, however, is less pronounced than it is when the number of strategy tables is smaller. Since there are more strategy tables per agent, diversity of strategy tables can be better maintained the greater . This, however, only somewhat mitigates the harm to the market by social learning.

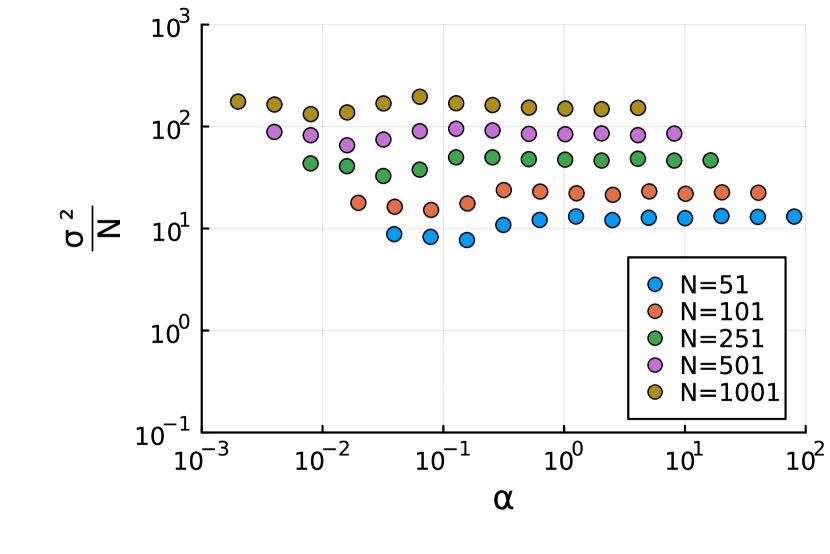

Figure 6 depicts the results for when there is only social learning and it occurs on a random graph. Even though the graph is not complete — in the cases plotted mean degree is quite low — the dynamics are still quite similar qualitatively to those of a complete graph. We surmise then that successful strategies can still spread through the population thereby undermining their efficacy and decreasing strategy table diversity in the population. Random graphs do suppress this effect to some degree as can be seen by comparing these figure to Figure 3(c), though not sufficiently to recover the case of no social learning (Figure 3(a)).

4 Discussion

Here we explored the effects of learning on the efficiency of financial markets as modelled by the Minority Game. The classic Minority Game already features learning, since agents learn which of their strategy tables performs the best. And, other forms of learning have been previously studied in the Minority Game such as searching behaviour in which individuals search for information from others [41]. In our model, however, agents can learn new strategy tables by either copying from others or invention. We find that social learning generally undermines efficiency in markets due to the negative frequency dependence of the payoffs of strategies. Good strategies are imitated, which undermines their efficacy. This type of “self-defeating ecosystem” has been observed previously in the Minority Game and other systems [3]. Similar results have also been observed due to herding behaviour, wherein agents imitate the most informed agent [6]. Social learning, however, can also be beneficial through the “wisdom of the crowds”. Maladaptive herding is generated by challenging tasks or when there is great uncertainty while the “wisdom of the crowds” emerges from other tasks [37]. Therefore, we would expect — and here we have observed — that social learning is harmful in the Minority Game as predicting the minority is a difficult task with high uncertainty.

There are many possible future directions this line of research could take. For one, we have assumed that agents know the true historic success of others’ strategy tables. This assumption can be justified by noting that an agent could evaluate the historic success of any strategy it copies via its own memory. However, we could relax this assumption. Previous research has incorporating beliefs into the Minority Game [43]. In an extension to our model, agents could incorrectly estimate the success of others’ strategies through biased beliefs. Another future direction is biased imitation. Biased transmission is the primary force in cultural evolution [17]. Though our network approach could be considered an example of this, explicitly modelling the prestige of information and agents, and how that affects imitation and the spread of strategies. Prestige processes are important in cultural transmission and can improve the quality of information spread [18]. However, in the Minority Game, this likely would undermine the efficiency of the market. A thorough study of prestige, financial gurus, and other factors biasing the spread of cultural traits applied to the Minority Game would be an interesting topic of future research.

Acknowledgments

This work was supported in part by the First Year Assistant Professor Award from the Council on Research and Creativity of Florida State University.

Code and data availability

Code to run numerical simulations is available at https://github.com/bmorsky/minority-games.

References

- [1] Erol Akçay and David Hirshleifer. Social finance as cultural evolution, transmission bias, and market dynamics. Proceedings of the National Academy of Sciences, 118(26):e2015568118, 2021.

- [2] W Brian Arthur. Inductive reasoning and bounded rationality. The American economic review, 84(2):406–411, 1994.

- [3] David Batten. Are some human ecosystems self-defeating? Environmental Modelling & Software, 22(5):649–655, 2007.

- [4] Robert Boyd and Peter J Richerson. Culture and the evolutionary process. University of Chicago press, 1988.

- [5] Enrique Burgos, Horacio Ceva, and Roberto PJ Perazzo. The evolutionary minority game with local coordination. Physica A: Statistical Mechanics and its Applications, 337(3-4):635–644, 2004.

- [6] Daniel Oliveira Cajueiro and Reinaldo Soares De Camargo. Minority game with local interactions due to the presence of herding behavior. Physics Letters A, 355(4-5):280–284, 2006.

- [7] Luigi Luca Cavalli-Sforza and Marcus W Feldman. Cultural transmission and evolution: A quantitative approach. Princeton University Press, 1981.

- [8] Damien Challet. Inter-pattern speculation: beyond minority, majority and $-games. Journal of Economic Dynamics and Control, 32(1):85–100, 2008.

- [9] Damien Challet, Alessandro Chessa, Matteo Marsili, and Yi-Cheng Zhang. From minority games to real markets. Quantitative Finance, 1(1):168–176, 2001.

- [10] Damien Challet, Matteo Marsili, and Yi-Cheng Zhang. Stylized facts of financial markets and market crashes in minority games. Physica A: Statistical Mechanics and its Applications, 294(3-4):514–524, 2001.

- [11] Damien Challet and Y-C Zhang. Emergence of cooperation and organization in an evolutionary game. Physica A: Statistical Mechanics and its Applications, 246(3-4):407–418, 1997.

- [12] Jiale Chen and Hongjun Quan. Effect of imitation in evolutionary minority game on small-world networks. Physica A: Statistical Mechanics and its Applications, 388(6):945–952, 2009.

- [13] Giorgio Fagiolo and Marco Valente. Minority games, local interactions, and endogenous networks. Computational Economics, 25:41–57, 2005.

- [14] J Doyne Farmer and Andrew W Lo. Frontiers of finance: Evolution and efficient markets. Proceedings of the National Academy of Sciences, 96(18):9991–9992, 1999.

- [15] Marcus W Feldman, Kenichi Aoki, and Jochen Kumm. Individual versus social learning: evolutionary analysis in a fluctuating environment. Anthropological Science, 104(3):209–231, 1996.

- [16] Fernando F Ferreira, Gerson Francisco, Birajara S Machado, and Paulsamy Muruganandam. Time series analysis for minority game simulations of financial markets. Physica A: Statistical Mechanics and its Applications, 321(3-4):619–632, 2003.

- [17] Joseph Henrich. Cultural transmission and the diffusion of innovations: Adoption dynamics indicate that biased cultural transmission is the predominate force in behavioral change. American anthropologist, 103(4):992–1013, 2001.

- [18] Joseph Henrich and Francisco J Gil-White. The evolution of prestige: Freely conferred deference as a mechanism for enhancing the benefits of cultural transmission. Evolution and human behavior, 22(3):165–196, 2001.

- [19] Joseph Henrich and Richard McElreath. The evolution of cultural evolution. Evolutionary Anthropology: Issues, News, and Reviews: Issues, News, and Reviews, 12(3):123–135, 2003.

- [20] David Hirshleifer. Presidential address: Social transmission bias in economics and finance. The Journal of Finance, 75(4):1779–1831, 2020.

- [21] Shahar Hod and Ehud Nakar. Evolutionary minority game: The roles of response time and mutation threshold. Physical Review E, 69(6):066122, 2004.

- [22] Neil F Johnson, Pak Ming Hui, Rob Jonson, and Ting Shek Lo. Self-organized segregation within an evolving population. Physical Review Letters, 82(16):3360, 1999.

- [23] Jeremy Kendal, Luc-Alain Giraldeau, and Kevin Laland. The evolution of social learning rules: payoff-biased and frequency-dependent biased transmission. Journal of theoretical biology, 260(2):210–219, 2009.

- [24] Theresa Kuchler and Johannes Stroebel. Social finance. Annual Review of Financial Economics, 13:37–55, 2021.

- [25] Kevin N Laland. Imitation, social learning, and preparedness as mechanisms of bounded rationality. Bounded rationality: The adaptive toolbox, 233, 2001.

- [26] H Lavicka and F Slanina. Evolution of imitation networks in minority game model. The European physical journal. B, Condensed matter physics, 56(1):53–63, 2007.

- [27] Yi Li, Rick Riolo, and Robert Savit. Evolution in minority games.(i). games with a fixed strategy space. Physica A: Statistical Mechanics and its Applications, 276(1-2):234–264, 2000.

- [28] Yi Li, Rick Riolo, and Robert Savit. Evolution in minority games.(ii). games with variable strategy spaces. Physica A: Statistical Mechanics and its Applications, 276(1-2):265–283, 2000.

- [29] TS Lo, PM Hui, and NF Johnson. Theory of the evolutionary minority game. Physical Review E, 62(3):4393, 2000.

- [30] Matteo Ortisi and Valerio Zuccolo. From minority game to Black&Scholes pricing. Applied Mathematical Finance, 20(6):578–598, 2013.

- [31] Robert Savit, Radu Manuca, and Rick Riolo. Adaptive competition, market efficiency, and phase transitions. Physical Review Letters, 82(10):2203, 1999.

- [32] Lihui Shang and Xiao Fan Wang. A modified evolutionary minority game with local imitation. Physica A: Statistical Mechanics and its Applications, 361(2):643–650, 2006.

- [33] Lihui Shang and Xiao Fan Wang. Evolutionary minority game on complex networks. Physica A: Statistical Mechanics and its Applications, 377(2):616–624, 2007.

- [34] František Slanina. Social organization in the minority game model. Physica A: Statistical Mechanics and its Applications, 286(1-2):367–376, 2000.

- [35] František Slanina. Harms and benefits from social imitation. Physica A: Statistical Mechanics and its Applications, 299(1-2):334–343, 2001.

- [36] Marko Sysi-Aho, Anirban Chakraborti, and Kimmo Kaski. Intelligent minority game with genetic crossover strategies. The European Physical Journal B-Condensed Matter and Complex Systems, 34(3):373–377, 2003.

- [37] Wataru Toyokawa, Andrew Whalen, and Kevin N Laland. Social learning strategies regulate the wisdom and madness of interactive crowds. Nature Human Behaviour, 3(2):183–193, 2019.

- [38] Nicolaas J Vriend. An illustration of the essential difference between individual and social learning, and its consequences for computational analyses. Journal of economic dynamics and control, 24(1):1–19, 2000.

- [39] Wei-Song Yang, Bing-Hong Wang, Hong-Jun Quan, and Chin-Kun Hu. Strategy uniform crossover adaptation evolution in a minority game. Chinese physics letters, 20(10):1659, 2003.

- [40] Chi Ho Yeung and Yi-Cheng Zhang. Minority games. In Computational complexity theory, techniques, and applications, pages 1863–1879. Springer, 2012.

- [41] Wei Zhang, Yuxin Sun, Xu Feng, and Xiong Xiong. Evolutionary minority game with searching behavior. Physica A: Statistical Mechanics and its Applications, 436:694–706, 2015.

- [42] Xin-Jie Zhang, Yong Tang, Jason Xiong, Wei-Jia Wang, and Yi-Cheng Zhang. Dynamics of cooperation in minority games in alliance networks. Sustainability, 10(12):4746, 2018.

- [43] Li-Xin Zhong, Wen-Juan Xu, Ping Huang, Tian Qiu, Yun-Xin He, and Chen-Yang Zhong. Self-organization and phase transition in financial markets with multiple choices. Physica A: Statistical Mechanics and its Applications, 410:450–456, 2014.