A Sampling-based Gittins Index Approximation

Abstract

A sampling-based method is introduced to approximate the Gittins index for a general family of alternative bandit processes. The approximation consists of a truncation of the optimization horizon and support for the immediate rewards, an optimal stopping value approximation, and a stochastic approximation procedure. Finite-time error bounds are given for the three approximations, leading to a procedure to construct a confidence interval for the Gittins index using a finite number of Monte Carlo samples, as well as an epsilon-optimal policy for the Bayesian multi-armed bandit. Proofs are given for almost sure convergence and convergence in distribution for the sampling based Gittins index approximation. In a numerical study, the approximation quality of the proposed method is verified for the Bernoulli bandit and Gaussian bandit with known variance, and the method is shown to significantly outperform Thompson sampling and the Bayesian Upper Confidence Bound algorithms for a novel random effects multi-armed bandit.

Keywords Stochastic Approximation Multi-Armed Bandits Optimal Stopping Bayesian Computation Markov Decision Processes

1 Introduction

The family of alternative bandit processes (FABP) is a well established problem in the field of Operations Research (Glazebrook (1983)). In short, an FABP is a problem in which the decision maker sequentially chooses one out of a finite collection of independent Markov reward processes (sometimes called arms) to evolve, and the goal is to optimize the total discounted reward. As initially proven in Gittins (1979), an index value can be determined based on the state of each bandit process, and the optimal policy is to choose the arm with the highest index value at each decision epoch. This index value, introduced as the dynamic allocation index, is now referred to as the Gittins index. As the Gittins index can be calculated separately based on the state of each bandit process, there is a large gain in computational efficiency for finding the optimal policy when compared to methods taking the states of all bandit processes into account (Puterman (1990)). Next to the family of alternative bandit processes, the Gittins index was also found to be the optimal solution to a number of other problems in operations research such as optimal scheduling and search problems (Aalto et al. (2011); Boodaghians et al. (2023)).

When, e.g., the total average reward is considered, or the Markov reward processes are no longer independent, the bandit problem becomes a restless bandit problem, where each arm evolves after an arm is chosen, instead of just that specific arm. Optimality of the Gittins index policy is no longer a guarantee in this case. When the condition of indexability is met, however, the policy choosing the largest Whittle index can provide a well-behaving heuristic for the problem under consideration (Weber and Weiss (1990); Glazebrook and Minty (2009); fryer2018two). The Whittle index has a definition similar to the Gittins index, and hence computation methods for the Gittins index work for the Whittle index as well.

Families of alternative bandit processes arise in various applications, such as job scheduling in queues, mining (or search) operations, advertisement, and Bayesian multi-armed bandit problems (Mahajan and Teneketzis (2008); Gittins et al. (2011)). The current paper will focus mainly on multi-armed bandit problems, with an application to clinical trials. Due to an increase in computational power and an increased focus on patient-centric medicine, research on treatment allocation in clinical trials using the Gittins index has gained popularity in the last decade (Villar et al. (2015a, b); Robertson et al. (2023)). In the multi-armed bandit problem, the decision maker is tasked with the choice to sample rewards from one out of a finite collection of unknown distributions at each decision epoch. In the Bayesian setting, each distribution is endowed with a prior. The resulting sequences of posterior distributions and posterior mean outcomes at each decision epoch then result in the separate Markov reward processes of an FABP. The Bayesian multi-armed bandit problem, popularized in Robbins (1952), was introduced in Thompson (1933) along with the approximate solution method now referred to as Thompson sampling, which was hence the first approximate solution method for the Bayesian multi-armed bandit problem (Slivkins (2019)).

This paper focuses on maximizing the Bayesian total expected discounted reward. When the regret under a multi-armed bandit problem is analyzed in the frequentist framework, many index-based approximate solution methods exist (Bubeck and Cesa-Bianchi (2012); Kuleshov and Precup (2014); Lattimore and Szepesvári (2020)), either based on frequentist or Bayesian approaches. in Lai et al. (1985), frequentist asymptotic lower bounds were found for the number of suboptimal choices made under a broad class of approximate solution methods. In the case of bounded rewards, the asymptotic regret upper bound equals this lower bound for e.g., approximate solution methods based on an upper confidence bound (UCB) for the expected reward (Lai (1987); Auer et al. (2002)), proving that these methods are asymptotically optimal in the frequentist framework. Many Bayesian approximate solution methods are asymptotically optimal and were shown to have excellent empirical frequentist performance (Kaufmann et al. (2012a); Kaufmann (2018); Lattimore and Szepesvári (2020)). In Lattimore (2016) it was shown that, in the frequentist framework, the Gittins index strategy with improper uniform prior for the mean yields an asymptotically optimal approximate solution method for the Gaussian model, outperforming other optimal Bayesian methods such as the Thompson sampling and Bayesian Upper Confidence Bound (Bayes-UCB).

There is a large amount of literature on calculating the Gittins index, starting with the Calibration method introduced in Gittins (1979). A survey covering most literature up to 2014 on offline and online algorithms to calculate the Gittins index for general countable state FABPs is provided in Chakravorty and Mahajan (2014). In Yao (2006), an approximation method for the Gittins index is derived in the Gaussian bandit with unknown mean and known variance. A numerical approximation for this bandit based on quadratic splines is described in Lattimore (2016). In Edwards (2019) the lack of general open source code for calculating the Gittins index is acknowledged, and methods and accompanying code, based on the Calibration method in Gittins (1979), are given to calculate the Gittins index for the Bernoulli and Gaussian bandit with known variance.

Calculation methods found in literature only work for countable state FABPs or are tailored to the Gaussian bandit with known variance. The calculation methods often revolve around the Bellman equation where it is assumed that the transition probabilities are known in closed form. First, when dealing with experimental data, the models can be much more complex and the assumption of known transition probabilities might not hold. For instance, the main types of outcome data encountered in clinical trials are categorical, continuous or event-times. Clearly only the first of these three is covered by considering a finite or countable state space, as continuous outcome data are often modeled using parameters on an uncountable parameter space. Second, in, e.g., latent variable modeling, the posterior distribution of the model parameters is often not known in closed form. Markov chain Monte Carlo approaches (Gilks et al. (1995)) provide a means to do (approximate) posterior inference in this case. Hence, the transition structure of the FABP is unknown, however one can still sample (approximately) from the Markov reward process. Another situation where the posterior is not available in closed form is when the prior being used in the Bayesian analysis is nonconjugate with respect to the likelihood. For instance, when a Bayesian experiment is performed for Gaussian data with possibly conflicting prior information, a nonconjugate Student’s t-distribution can be assumed as a prior distribution for the mean (Neuenschwander et al. (2020)). No method exists to accurately approximate the Gittins index in these settings.

To address the open problems listed above, a sampling-based Gittins index approximation (SBGIA) is introduced in this paper. The SBGIA can be calculated for any type of state space, also when there is access only to a simulator for future rewards. We first approximate the Gittins index using a truncation of the optimization horizon and support for the immediate rewards of the Markov chains. Second, we use a stochastic approximation procedure (Robbins and Monro (1951)) based on the optimal stopping value approximation introduced in Chen and Goldberg (2018) to find the root (i.e., the fair charge) of the prevailing charge formulation of the Gittins index, see, e.g., Weber (1992, Equation 2). As the SBGIA is sampling-based, samples from the (approximate) posterior reward distribution can be used to make decisions in the proposed algorithm.

The paper is organized as follows. Section 2 introduces the family of alternative bandit processes. Section 3 extends optimal stopping value approximation results from Chen and Goldberg (2018) to reward processes that are not restricted to be non-negative. In Section 4.1, based on convergence results provided in Chen and Goldberg (2018), we obtain finite-time convergence results for the SBGIA. In Section 4.2 we prove asymptotic convergence results for the stochastic approximation iterates. In Section 5 we show the performance of the SBGIA in several numerical simulation studies. Appendix A states the longer proofs of the theorems in the paper, and Appendix B summarises the notation used in the paper.

2 Family of alternative bandit processes

We consider independent Markov chains for , referred to as arms, each on a (shared) Borel space with underlying probability space . The (shared) transition kernel is denoted , where denotes the initial state of the Markov chain, and expectations w.r.t. are denoted . Let denote a -measurable reward function. See Lattimore and Szepesvári (2020, Chapter 35) for details on this setting.

Let be the set of policies, i.e., the mappings from the set of histories

| (1) |

to the unit--simplex of probability vectors over . A fixed policy induces a Markov chain , where is the number of times arm is chosen by the policy up to and including time . We denote the probability measure and expectation under this fixed policy by and . The objective is to find the optimal policy maximizing the total sum of discounted rewards for a discount factor :

| (2) |

We furthermore assume that the reward function for arm , with initial state , is discounted absolutely convergent in expectation under discount factor

Assumption 1.

Under Assumption 1, the in (2) is attained, and the optimal policy for the Markov decision process above is the policy choosing the arm with the highest Gittins index, see, e.g., Lattimore and Szepesvári (2020, Theorem 35.9). To specify this, let be the current state for arm in history , then

| (3) |

where is the set of stopping times in w.r.t. the filtration generated by the process starting from state . The Gittins index hence only depends on the current state for any arm . When ties occur in the above expression, i.e., the returns more than one value, the policy uniformly chooses an arm from the different choices of . Hence, under this choice, the Gittins index policy is a randomized Markov policy.

3 Preliminaries

This section extends the results on the optimal stopping value approximation introduced in Chen and Goldberg (2018) to reward processes that are not restricted to be non-negative, which are needed to develop our results. Section 4 translates these results to the setting of the family of alternative bandit processes.

3.1 Optimal stopping approximation

When considering the behavior of only one of the arms, the superscript is dropped from the state, filtration, and set of stopping times. Let , contain the realisations of up to time , and let be the smallest sigma algebra for which is measurable. For , let denote the set of integer-valued stopping times adapted to such that almost surely. We assume that is a Polish space, ensuring the existence of regular conditional probabilities for (e.g., Athreya and Lahiri (2006, Theorem 12.3.1)). Let for measurable real-valued functions . The random variable is assumed integrable (on the probability space for ) for all . The goal is to compute

| (6) |

The following two results extend Theorems 1 and 2 in Chen and Goldberg (2018) to remove the restriction that is non-negative. The proofs readily follow along the lines of the proofs in Chen and Goldberg (2018). Theorem 1 expresses (6) as an infinite sum. For bounded, Theorem 2 provides an error bound for truncation of the infinite sum.

Theorem 1 (Optimal stopping value representation).

where for all and

| (7) | ||||

| (8) |

Proof.

The proof follows the proof of Lemma 1 and Theorem 1 in Chen and Goldberg (2018) noting that, even though is not assumed non-negative in this case, the sequence remains a non-negative decreasing sequence of random variables for all . Hence still holds. ∎

Theorem 2 (Optimal stopping approximation).

Suppose almost surely for all for some such that , then

| (9) |

3.2 Simulation approximation

Following Chen and Goldberg (2018), the sum of expectations in (9) may be approximated via simulation. Let denote concatenation of the vectors and . Let be the all-ones vector in for all . For each index let be versions of such that if , and is independent of otherwise.

Let and for all . Recall (7) and (8), for all define the random processes

| (10) | ||||

| (11) |

where denotes the random variable conditioned on the event that the paths of the two processes and are equal up to time . After time they continue independently (as ). Note that this random variable is well defined as the regular conditional probabilities for exist (Section 3.1). The requirement if induces that the “right" partial paths of used at a lower level are used to construct values at higher level . To illustrate our notation and the relation between (7), (8) and (10), (11), note that equals

where , is the sigma algebra generated by , and the approximation is exact in the limit by the law of large numbers. Note that the process used to determine equals . Hence, corresponding to conditioning on above, in order to determine it is assumed that the history of the Markov process up to time is the same for all after which the processes continue independently.

Consider the following random variable projected on :

| (12) |

By the law of large numbers and Theorem 1, we have that

where indicates the element-wise limit for all .

Following Chen and Goldberg (2018), we may show that for every and we can choose a function , given implicitly in Algorithms and in Chen and Goldberg (2018, Pages 27 and 30), such that

This statement was shown in Chen and Goldberg (2018) for non-projected . However, the projection on can only reduce the error so the statement still holds for as defined in (12). Hence, choosing we have by Theorem 2 and the triangle inequality that

4 Gittins index approximation

This section first introduces our main method, which is a sampling-based method for Gittins index approximation. Section 4.1 develops finite-time bounds for the approximation, and Section 4.2 develops asymptotic convergence results.

Combining the results of Sections 2 and 3.1, we define for some such that

| (13) |

which is the argument in (5), scaled by for later convenience.

We now introduce our sampling-based Gittins index approximation.

Sampling-based Gittins index approximation (SBGIA)

-

•

Approximation I: truncation

Truncate the support of and the time horizon for the optimal stopping problem (4):(14) where the infimum is taken over the set of stopping times with, for a choice of ,

(15) where the minimum operator is denoted with . Note that only considers . Hence, using the stopped (bounded) process such that for all , in (14) can also be formulated as

(16) Boundedness of allows using the results stated in Section 3.1.

-

•

Approximation II: simulation

Highlighting the dependence on the state and current estimate only, we sample truncated to by sampling the respective processes , from the Markov kernel starting from state , needed to determine in (10), (11) and combining them in (12) such that(17) Using this sampling procedure, we approximate using stochastic approximation (Borkar (2008)), i.e., a stochastic root-finding procedure, starting from an initial point such that

(18) where are independent versions of , and is a possibly stochastic, predictable non-negative sequence of step-sizes in . We collect as our sampling-based approximation of the Gittins index , where is defined according to a certain (user-defined) stopping criterion (see Remark 2).

4.1 Finite-time error bounds

In this section, we first derive a truncation error bound for the first-stage approximation (Theorem 3). Subsequently, we couple the stochastic approximation iterates from the second-stage approximation to stochastic approximation iterates from a continuous increasing function (Lemma 1). Using a mean-squared error recursion result for these coupled sequences (Theorem 4), we then construct a confidence interval for the Gittins index in finite-time, where “finite-time” pertains to the number of stochastic approximation iterates (Theorem 5). Using finite-time bounds, we construct an -optimal policy for the family of alternative bandit processes (Theorem 6).

An upper bound on the error when approximating by the truncation-based index as defined in (14) is given in the following theorem, which holds for a general stopping time . A similar bound was given in Wang (1997) for a fixed truncation of the time horizon.

Theorem 3 (Truncation error bound).

Under Assumption 1 there is a unique real number attaining the supremum

In fact, is the unique root of

The infimum in the condition is attained for some .

Furthermore, with for , it holds that

Proof.

The complete proof can be found in Appendix A and is outlined here. The first two statements follow by showing that equals the Gittins index for the Markov process documenting the full history of up to and including each time with rewards , after which we can apply commonly known results for the Gittins index from Lattimore and Szepesvári (2020). Only the upper bound is non-trivial and mainly follows from bounding the difference between two optimal stopping values by the optimal stopping value of the difference and using the strong Markov property. ∎

We now give an error bound for the sampling-based approximation as defined in (18). Note that almost surely. Hence, according to Theorem 2 we have

Defining the functions

| (19) |

we have by (17) and by Jensen’s inequality

| (20) |

Using these results, we derive mean-squared error bounds for our approximation method. We do this by defining coupled stochastic approximation iterates based on the function that lie almost surely below and above the sequence defined in (18). As we do not have access to or even unbiased estimates of , these iterates cannot directly be simulated, but we can bound their distance to , and show finite-time convergence results for these sequences, which can then be used to derive finite-time convergence bounds for . To this end, let

| (21) |

which is a martingale difference sequence with respect to the natural filtration w.r.t. as (hence ) is bounded and

since is a function of .

Lemma 1.

Assume the step-size sequence is such that almost surely. For , we have

| (24) |

Proof.

Observe that , so that (24) is satisfied for .

Now assume for some . We have

where the second statement follows from (20), and the last statement follows as for any

| (25) |

which can easily be shown from the definition of , using the fact that the suprema are attained at unique stopping times.

Similarly, if for some , then . The proof is completed by induction. ∎

The next theorem gives the mean-squared error between either sequence and a limit point.

Theorem 4 (Mean-squared error recursion for coupled sequences).

For , initial point , and martingale difference sequence (21), let the sequence be defined as

Assume the step-size sequence is such that almost surely. Then for all

Proof.

Observe that by the assumption on we have (for ) so that the influence of the initial difference between and decays exponentially. The squared difference of the iterate and converges to a value that depends on the second moment of the martingale differences and the step-size sequence .

Different choices of step-size sequences yield different upper bounds on the rates of convergence. We examine two standard choices.

Example 1 (Constant step-size).

Let for all with . Let , and assume From the recursion for , we obtain that

Example 2 (Linear step-size).

In the above two examples, we see that we can choose the step-size sequence and stopping point such that is arbitrarily small. We can construct confidence intervals for using Chebyshev’s inequality:

Observe that is a strictly increasing surjective function on . We may therefore

| (26) |

We may now construct a finite-time confidence interval for the Gittins index for finite , which can be made arbitrary small by choosing large and small.

Theorem 5 (Finite-time confidence interval).

Let , be chosen according to (26). Then

| (27) |

which can be made arbitrarily small by suitable choice of and .

Let and be chosen such that , and

| (28) |

Then, with probability at least

| (29) |

Proof.

The confidence interval (29) can be used to construct an -optimal policy for any FABP. For this we first need to show that the values of are restricted to a closed bounded interval. The proof of this lemma can be found in Appendix A.

Lemma 2.

Let almost surely. We have almost surely that for all

For the family of alternative bandit processes, we can now define an -optimal policy, which we will denote the SBGIA policy (SBGIAP).

Theorem 6 (-optimal policy for FABP).

Proof.

Note that (30) is possible due to (29). in Glazebrook (1982), it is shown that for any stationary policy

| (31) |

By our choice of we have by a union bound over for the events in (30) that for any time point

Combining Lemma 2 with the fact that yields for all , hence

Using this in the right-hand side of (31) scaled by gives

∎

4.2 Asymptotic convergence results

This section investigates convergence properties of the stochastic process defined in (18). In the previous section, we have shown that after a finite, known, amount of iterations, the iterates lie in an interval containing with high probability. The length of this interval depends on the choice of and . In this section, we let and be constants, not depending on , and investigate convergence and asymptotic normality of the iterates when goes to infinity, under different choices of the step-size sequence. First, we show that when the step-size sequence almost surely satisfies the Robbins-Monro conditions (Robbins and Monro (1951)), the stochastic approximation iterates converge almost surely (Theorem 7). Then, we show that if we instead take a constant step-size sequence, the iterates converge in mean-square to the set of roots (Theorem 8). Lastly, under stronger conditions, we show that we can construct an adaptive stochastic approximation procedure (Lai and Robbins (1979)), where a central limit theorem holds for the stochastic approximation iterates (Theorem 9). In the following, we let for fixed choices of , and define and as in (19), (21), respectively.

The sequence (18) relates to an Euler scheme for the first-order scalar autonomous ordinary differential equation (ODE) (Borkar (2008)),

| (32) |

This differential equation has as equilibrium points the roots of the function , provided that a root exists. We show that iteration scheme (18) satisfies the conditions stated in Borkar (2008, Chapter 2), hence almost surely the limiting behavior of the sample paths of the stochastic process (18) equals that of the solution to the above ODE. We then show that the ODE (32) always converges to an equilibrium point, irrespective of the starting point. It follows that the sample paths of (18) almost surely converge to a random variable such that .

To make this formal, we define an internally chain transitive invariant set corresponding to an ODE in accordance with the definition given in Borkar (2008).

Definition 1 (Internally chain transitive invariant set (Borkar (2008))).

We first show that is Lipschitz continuous.

Lemma 3.

The function is Lipschitz continuous in .

Proof.

We first prove by induction in that is Lipschitz continuous for all , starting with . From (10) and (13) it follows that is Lipschitz continuous with constant for all . Now assume that is Lipschitz continuous up to some for all . As the minimum, average, and sum of a finite set of Lipschitz continuous functions are Lipschitz continuous, we have by (11) that is also Lipschitz continuous for all possible . By induction we have that is Lipschitz continuous for all . Now, by (12)

Hence, as the expectation, maximum, minimum, and sum of Lipschitz continuous functions are Lipschitz continuous, we have that is Lipschitz continuous. ∎

Using this lemma, the next result follows.

Theorem 7 (Almost sure convergence of stochastic approximation iterates).

Proof.

We verify that assumptions (A1 - A4) in Borkar (2008, Chapter 2) are satisfied, from which the result follows by Borkar (2008, Chapter 2, Theorem 2):

-

(A1)

We have from Lemma 3 that is Lipschitz continuous.

-

(A2)

The Robbins-Monro conditions hold by assumption.

-

(A3)

The sequence defined by (21) is a bounded martingale difference sequence.

- (A4)

∎

The next corollary follows.

Corollary 1.

Proof.

From the proof of Lemma 2, we have for and for . Hence, if and if . From Lipschitz continuity of it then follows that no solution of (32) goes to infinity. Hence, by classification of solutions to a first-order scalar autonomous ODE, we know that each solution of (32) must converge to a (semi-)stable point contained in the set of roots of , which is non-empty and contained in by the above discussion. ∎

If the step-size sequence is constant, i.e., for all , the following result holds by Borkar (2008, Chapter 9, Theorem 3), which states that is close to in the limit in mean-square, but does not necessarily almost surely converge to a point in .

Theorem 8 (Convergence of stochastic approximation for constant step-size).

For a constant

Proof.

Remark 1.

In the above results, we have shown two convergence results under two different assumptions on the step-size sequence. Theorem 7 assumes that the Robbins-Monro conditions almost surely hold for the step-size sequence . This is a stronger condition than the one assumed in Section 4.1, where only was assumed for some bound . Under this stronger condition we were able to show that the stochastic process converges to a root of the function and based on a sample path alone, we can determine whether the sequence has converged or not. If we instead take a constant step-size sequence, we could only show that the limit of the stochastic process is close to , in terms of mean-squared difference. Often the rate of convergence is much higher for constant step-size sequences (Borkar (2008)).

The following lemma gives a recursive formula for the derivative which can be used for selection of the step-size in the adaptive stochastic approximation procedure (18).

Lemma 4.

If for all the cumulative distribution functions of starting from have finitely many jumps, then for all but finitely many points the function is differentiable with derivative

where , and

Proof.

The full proof can be found in Appendix A. The result might seem straightforward at first but the situation is more difficult due to the dependence of on . The result is obtained by showing continuity of for all but at most finitely many points, by giving a coinciding lower and upper bound for the derivative of whenever it exists and then using dominated convergence to show the derivative for the expected sum truncated to . ∎

The next theorem states that using Lemma 4 an adaptive stochastic approximation method can be designed with asymptotically optimal variance (Lai and Robbins (1979)).

Theorem 9 (Central limit theorem for stochastic approximation iterates).

Let be independent versions (in ) of , and

Let

Let be the set of points where is differentiable. If , then there is a unique point such that . If the derivative of exists at and , we have

| (34) |

Proof.

The full proof can be found in Appendix A. We first show that the sequence converges to a constant, by showing that satisfies the Robbins-Monro conditions almost surely and by applying Corollary 1. After this, we can apply the results in Lai and Robbins (1978), where we have to account for the fact that the residuals are not independent and identically distributed but bounded, and the function is only differentiable at all but finitely many points. ∎

Remark 2 (Step-size sequence and stopping criterion).

We propose to use the adaptive step-size sequence for the stochastic approximation sequence (18), and base the stopping criterion for the stochastic approximation sequence on the estimated radius of the confidence interval implied by (55). We stop the stochastic approximation procedure (18) when the estimated confidence radius based on Theorem 9 is small enough, i.e., when

| (35) |

with the level quantile of the standard normal distribution, and a pre-specified tolerance.

Remark 3.

When all values are large enough, we have by Theorem 2

| (36) | ||||

| (37) |

where we used As both and are continuous, negative at , positive at , and is increasing, we expect from (36) that the root of is an upper bound of the root of . As for , we furthermore expect that the root of decreases to the root of , and by (37) we expect that both roots coincide in the limit as . We furthermore have by (25) and (37) that, for large enough values of ,

| (38) |

hence the difference in the two roots is of order . In order to get an accurate SBGIA, we hence propose, for a fixed , to first increase all to large enough values such that the root of has converged. After convergence has occurred, we propose to increase and to repeat this procedure until the root has also converged in .

5 Application to Bayesian multi-armed bandits

We introduce the Bayesian multi-armed bandit in Section 5.1 as an application of the FABP. In Section 5.2, we consider outcome distributions from an exponential family. Subsequently, we present results for the SBGIA applied to two Bayesian bandits known from literature, the Bernoulli bandit and Gaussian bandit with known variance. In Section 5.3, we evaluate the performance of the SBGIAP for a novel Gaussian random effects bandit problem.

5.1 Bayesian multi-armed bandit

Consider distributions with support . Selecting distribution at time , results in a realisation of the random variable that has a known density w.r.t. a measure , where the unknown parameter lies in a parameter space (shared for all ). The random variables are assumed independent. We perform a Bayesian analysis, where the parameters are independent a priori and endowed with prior probability measure w.r.t. the Polish space . Given this probability measure on , we can determine the predictive distribution

| (39) |

A sample from this distribution then, in turn, generates a posterior distribution by Bayes’ rule, i.e.,

| (40) |

We can use the predictive distribution (39) and posterior updating rule (40) to determine Markov chains (arms), with states corresponding to (posterior) distributions on . The state space of each Markov chain is the space of probability measures on . Furthermore, we endow this state space with the sigma algebra , which is the smallest sigma field making all maps from to measurable. Then is a Borel space (Ghosal and Van der Vaart (2017, Chapter 3.1)). Each Markov chain has transition kernel

| (41) |

Our goal is to find a (Markov) policy to sequentially sample from one of the arms that maximizes the expected discounted sum of outcomes under the Bayesian model, i.e, to maximize

| (42) |

where is the posterior mean outcome for the current posterior . The equality in (42) follows from Assumption 1 and Fubini’s theorem. Letting for all , , and , we are in the setting of Section 2 with transition kernel (41) and reward function .

5.2 Gittins index approximation results

This section considers the FABP with distributions from an exponential family as detailed in Section 5.2.1. Specific results are presented for Bernoulli and Gaussian families in Sections 5.2.2 and 5.2.3.

For determining the SBGIA, we set and in (35) to estimate a asymptotic confidence interval for with radius . We compare the SBGIA with the Calibration method introduced in Gittins (1979), which is a combination of a bisection method and backward induction to obtain the value of the truncated optimal stopping problem in (4). The parameters of the Calibration method are set such that the approximation error is very small, so that we may consider these values to be the true Gittins index values.

5.2.1 Exponential families

Assume the data comes from a distribution belonging to an exponential family, i.e., for known functions we have

and

Now assume a conjugate prior for this model (Diaconis and Ylvisaker (1979)), with normalizing constant

Letting and , we have the following expression for the posterior

The vector is often referred to as the sufficient statistic, and as the effective number of observations, which is the sum of a prior number of observations and the actual number of observations for arm As the only random element in the posterior is , which we will assume to lie in , the Markov chain can be represented by the time-inhomogeneous Markov chain on the finite-dimensional state space with transition dynamics

| (43) |

The rewards are the posterior mean outcomes. As our goal is to maximize the expected discounted sum of outcomes under the Bayesian model, letting for all , , and , we are in the setting of Section 2 with the transition kernel implied by (43) and reward function .

5.2.2 Bernoulli bandit

We consider the case when are Bernoulli distributed with unknown success probability , i.e.,

which implies that the family of outcome distributions is an exponential family with

and the counting measure on the nonnegative integers. We assume a conjugate prior on each , hence and . In the following, we drop the superscript from notation as we consider results for a single arm only.

Observe that , hence for a fixed horizon the Markov reward process starting from is bounded. Thus, in Section 4 we can take , and the result of Theorem 3 holds without truncation of the support of the rewards. Using , and letting the Gittins index approximation after truncation be denoted by (as ), we have

| (44) |

hence for

| (45) |

For the rewards, we have

Starting from the rewards lie in the bounded interval up to a horizon for

which can be used in (13).

Table 1 shows the Gittins index values found under the SBGIA and the Calibration method for the Bernoulli bandit with . For the SBGIA and the Calibration method, we set , corresponding to a truncation error bound of according to (45). We set each and considered . For ease of comparison, Table 1 shows , the effective number of failures, as the second state variable. Table 1 shows the log computation time (in seconds), estimated bias (SBGIA minus Calibration), root-mean-squared error (RMSE), and average standard deviation over estimates for the SBGIA (calculated as the average deviation in the approximation over states for two independent simulation runs) for each considered value of . Using (38), the rightmost column of Table 1 shows an estimate of the limit as , found by performing ordinary least squares on the columns with the line .

Table 1 shows that the Gittins index is overestimated by the SBGIA for , which is in agreement with our expectation, as the expected minimum is always smaller than the minimum of the expectation over stopping times (see, e.g., Chen and Goldberg (2018)). When increases, the amount of overestimation decreases, and values of the SBGIA lie above the Gittins index computed by the Calibration method for any state and value of . It follows from Remark 3 that this behaviour should occur asymptotically when the values of go to infinity; the numerical results show that it also occurs for small values of . The estimate of the limit when , shown in the rightmost column of Table 1 has lowest bias and RMSE, indicating a correct assumption on the convergence rate. The computation time increases more than tenfold with each increase in , and for it is already about 100 times larger than the computation time of the Calibration method. The standard deviation over runs (SD) is quite low, around for all values of , indicating that the estimates are consistent over independent runs.

| General | Calibration | Est. limit | |||||

| 1 | 1 | 0.641 | 0.643 | 0.642 | 0.642 | 0.641 | |

| 1 | 2 | 0.443 | 0.447 | 0.446 | 0.445 | 0.442 | |

| 1 | 3 | 0.332 | 0.338 | 0.337 | 0.335 | 0.332 | |

| 1 | 4 | 0.263 | 0.270 | 0.268 | 0.267 | 0.264 | |

| 1 | 5 | 0.216 | 0.224 | 0.222 | 0.221 | 0.218 | |

| 1 | 6 | 0.183 | 0.191 | 0.189 | 0.188 | 0.185 | |

| 2 | 1 | 0.760 | 0.760 | 0.760 | 0.760 | 0.759 | |

| 2 | 2 | 0.590 | 0.592 | 0.591 | 0.591 | 0.590 | |

| 2 | 3 | 0.476 | 0.480 | 0.479 | 0.478 | 0.476 | |

| 2 | 4 | 0.398 | 0.402 | 0.401 | 0.400 | 0.398 | |

| 2 | 5 | 0.340 | 0.345 | 0.344 | 0.342 | 0.340 | |

| 2 | 6 | 0.296 | 0.301 | 0.300 | 0.299 | 0.297 | |

| 3 | 1 | 0.816 | 0.816 | 0.816 | 0.816 | 0.815 | |

| 3 | 2 | 0.671 | 0.673 | 0.673 | 0.672 | 0.671 | |

| 3 | 3 | 0.566 | 0.568 | 0.568 | 0.567 | 0.566 | |

| 3 | 4 | 0.487 | 0.490 | 0.489 | 0.489 | 0.487 | |

| 3 | 5 | 0.427 | 0.430 | 0.429 | 0.428 | 0.427 | |

| 3 | 6 | 0.379 | 0.383 | 0.382 | 0.381 | 0.379 | |

| 4 | 1 | 0.849 | 0.850 | 0.849 | 0.849 | 0.849 | |

| 4 | 2 | 0.725 | 0.726 | 0.725 | 0.725 | 0.724 | |

| 4 | 3 | 0.628 | 0.629 | 0.629 | 0.629 | 0.628 | |

| 4 | 4 | 0.552 | 0.554 | 0.554 | 0.553 | 0.552 | |

| 4 | 5 | 0.491 | 0.494 | 0.494 | 0.493 | 0.492 | |

| 4 | 6 | 0.443 | 0.446 | 0.445 | 0.444 | 0.443 | |

| 5 | 1 | 0.872 | 0.873 | 0.872 | 0.872 | 0.871 | |

| 5 | 2 | 0.762 | 0.763 | 0.763 | 0.762 | 0.762 | |

| 5 | 3 | 0.674 | 0.675 | 0.675 | 0.674 | 0.673 | |

| 5 | 4 | 0.602 | 0.604 | 0.603 | 0.603 | 0.602 | |

| 5 | 5 | 0.543 | 0.545 | 0.545 | 0.544 | 0.543 | |

| 5 | 6 | 0.494 | 0.497 | 0.496 | 0.496 | 0.495 | |

| 6 | 1 | 0.888 | 0.889 | 0.888 | 0.888 | 0.887 | |

| 6 | 2 | 0.790 | 0.791 | 0.791 | 0.791 | 0.790 | |

| 6 | 3 | 0.709 | 0.710 | 0.710 | 0.709 | 0.709 | |

| 6 | 4 | 0.641 | 0.643 | 0.642 | 0.642 | 0.641 | |

| 6 | 5 | 0.585 | 0.586 | 0.586 | 0.586 | 0.585 | |

| 6 | 6 | 0.537 | 0.539 | 0.538 | 0.538 | 0.537 | |

| CPUtime | 0.132 | 2.650 | 3.810 | 4.810 | |||

| Bias (x0.01) | 0.277 | 0.210 | 0.144 | 0.008 | |||

| RMSE (x0.01) | 0.342 | 0.264 | 0.189 | 0.071 | |||

| SD (x0.01) | 0.011 | 0.010 | 0.014 |

Table 2 shows the values of the SBGIA and the Calibration method for and , i.e., only the nested number of simulations for the SBGIA is increased. The CPU time, bias, RMSE, and standard deviations over two independent simulation runs are shown at the bottom of Table 2.

Table 2 shows that when increasing a smaller error (expressed in bias and RMSE) is attained for a lower computational cost in comparison to Table 1. The results in Table 2 hence agree with the proposal in Remark 3, as increasing the number of nested simulations leads to higher precision in less computation time.

| General | Calibration | |||||

| 1 | 1 | 0.641 | 0.642 | 0.642 | 0.642 | |

| 1 | 2 | 0.443 | 0.446 | 0.445 | 0.444 | |

| 1 | 3 | 0.332 | 0.337 | 0.334 | 0.333 | |

| 1 | 4 | 0.263 | 0.268 | 0.266 | 0.265 | |

| 1 | 5 | 0.216 | 0.222 | 0.220 | 0.219 | |

| 1 | 6 | 0.183 | 0.189 | 0.187 | 0.186 | |

| 2 | 1 | 0.760 | 0.760 | 0.760 | 0.760 | |

| 2 | 2 | 0.590 | 0.591 | 0.591 | 0.590 | |

| 2 | 3 | 0.476 | 0.479 | 0.478 | 0.477 | |

| 2 | 4 | 0.398 | 0.401 | 0.399 | 0.399 | |

| 2 | 5 | 0.340 | 0.344 | 0.342 | 0.341 | |

| 2 | 6 | 0.296 | 0.300 | 0.299 | 0.298 | |

| 3 | 1 | 0.816 | 0.816 | 0.816 | 0.816 | |

| 3 | 2 | 0.671 | 0.673 | 0.672 | 0.672 | |

| 3 | 3 | 0.566 | 0.568 | 0.567 | 0.566 | |

| 3 | 4 | 0.487 | 0.489 | 0.489 | 0.488 | |

| 3 | 5 | 0.427 | 0.429 | 0.428 | 0.428 | |

| 3 | 6 | 0.379 | 0.382 | 0.380 | 0.380 | |

| 4 | 1 | 0.849 | 0.849 | 0.849 | 0.849 | |

| 4 | 2 | 0.725 | 0.725 | 0.725 | 0.725 | |

| 4 | 3 | 0.628 | 0.629 | 0.629 | 0.628 | |

| 4 | 4 | 0.552 | 0.554 | 0.553 | 0.553 | |

| 4 | 5 | 0.491 | 0.494 | 0.493 | 0.493 | |

| 4 | 6 | 0.443 | 0.445 | 0.444 | 0.444 | |

| 5 | 1 | 0.872 | 0.872 | 0.872 | 0.872 | |

| 5 | 2 | 0.762 | 0.763 | 0.763 | 0.762 | |

| 5 | 3 | 0.674 | 0.675 | 0.674 | 0.674 | |

| 5 | 4 | 0.602 | 0.603 | 0.603 | 0.602 | |

| 5 | 5 | 0.543 | 0.545 | 0.544 | 0.544 | |

| 5 | 6 | 0.494 | 0.496 | 0.496 | 0.495 | |

| 6 | 1 | 0.888 | 0.888 | 0.888 | 0.888 | |

| 6 | 2 | 0.790 | 0.791 | 0.791 | 0.790 | |

| 6 | 3 | 0.709 | 0.710 | 0.709 | 0.709 | |

| 6 | 4 | 0.641 | 0.642 | 0.642 | 0.642 | |

| 6 | 5 | 0.585 | 0.586 | 0.585 | 0.585 | |

| 6 | 6 | 0.537 | 0.538 | 0.538 | 0.537 | |

| CPUtime | 0.132 | 3.810 | 3.950 | 4.170 | ||

| Bias (x0.01) | 0.210 | 0.113 | 0.059 | |||

| RMSE (x0.01) | 0.264 | 0.145 | 0.085 | |||

| SD (x0.01) | 0.010 | 0.016 | 0.013 |

Remark 4.

The length of the confidence interval for the Gittins index is in large part determined by the error bound for the optimal stopping value approximation given in Chen and Goldberg (2018). The contribution of the optimal stopping approximation is equal to (Theorem 5), which can be seen as the bias of approximating by . Here is the slope of in and is a bound for the error induced by the approximation method introduced in Chen and Goldberg (2018). The bound is similar to the radius of the confidence interval found under the Delta method when applied to sampled approximations to the truncated Gittins index , which would be proportional to . This implies that the bound could be sharp, given that the error bound is sharp. Note that rescaling in (13) would not alter this radius, increasing the range of linearly increases the error according to Theorem 2, yielding the same confidence radius. The results in Section 5.2 indicate that the bound can be made tighter. For instance, for , , and , an absolute bias of is seen in Table 1. We have , , hence to get the theoretical bound for the bias less than 0.001, we should at least have . Setting , following Chen and Goldberg (2018), we would need and to obtain a bias of for The main limiting factor in applying the theoretical bound in practice is hence the bound from Chen and Goldberg (2018) which could possibly be made more tight.

5.2.3 Gaussian bandit

Let be normally distributed with unknown mean , and known variance for each arm . By scaling the mean and outcomes by the (known) standard deviation, we can equivalently assume , which implies that the family of outcome distributions is an exponential family with, letting denote the standard normal density,

| (46) |

and the Lebesgue measure. We assume a prior on , hence , . In the following, we drop the superscript from notation as we consider results for a single arm only.

Observe from (46) that , hence

and

| (47) |

From Yao (2006) it holds that

It is hence sufficient to calculate the Gittins index for Gaussian rewards given that the initial sufficient statistic is zero. Observe from (47) that, starting from the initial state , the process is a Gaussian random walk starting at zero with normally distributed, zero-centered increments with variance .

Let the stopping time be defined as in (15) for fixed , and let , for fixed We then have by Kolmogorov’s inequality

We hence have . Note that

From Theorem 3, and as , it follows that

| (48) |

The truncation error in (48) is smaller than when, e.g.,

| (49) |

Values of and such that the above inequalities are satisfied can then be used in (13).

Table 3 shows the Gittins index values found under the SBGIA and the Calibration method for the Gaussian bandit with . For the SBGIA, we set , corresponding to a truncation error bound according to (48). For all states the value of was set to the lower bound in (49). We next set each and considered . The Gittins indices found under the Calibration method shown in Table 3 can also be derived from Gittins et al. (2011, Table 8.1). As we only consider , each state of the Gaussian bandit in Table 3 is denoted by . We show the log computation time at the bottom, as well as the bias, RMSE, and standard deviation in percentage points. The rightmost column of the table shows an estimate of the limit as , found by performing ordinary least squares on the columns with the line .

Table 3 shows that, as in Table 1, the Gittins index is overestimated for , and the values for the SBGIA, as well as the error measures, decrease in . The estimates for the Gaussian bandit show larger errors than those for the Bernoulli bandit. Possibly due to the continuity in the support of the rewards, which induces a larger variance in the sampled paths. The computation times for the Gaussian bandit are also approximately ten times larger than those for the Bernoulli bandit. The computation time shown in Table 3 is similar for , and increases tenfold when going from to . The computation time of the Calibration method is comparable to the computation time for , indicating that the Gaussian bandit with known variance is already a hard problem to solve under the Calibration method. The low average standard deviation in Table 3 indicates that the estimates are consistent over different runs. The estimates of the limits in the rightmost column again show a better quality than those for finite , often giving the value of the Gittins index with an error of 0.001 for

Table 4 shows values of the SBGIA obtained when setting and varying for the Gaussian bandit with unit variance. As in Table 2, it is seen that the errors decrease faster in for fixed than vice versa, in agreement with the proposal in Remark 3.

| General | Calibration | Est. limit | ||||

| 1 | 0.505 | 0.526 | 0.520 | 0.520 | 0.513 | |

| 2 | 0.308 | 0.329 | 0.323 | 0.320 | 0.312 | |

| 3 | 0.226 | 0.245 | 0.239 | 0.237 | 0.229 | |

| 4 | 0.179 | 0.196 | 0.191 | 0.188 | 0.180 | |

| 5 | 0.149 | 0.164 | 0.160 | 0.157 | 0.150 | |

| 6 | 0.128 | 0.142 | 0.138 | 0.135 | 0.128 | |

| 7 | 0.112 | 0.125 | 0.121 | 0.119 | 0.113 | |

| 8 | 0.100 | 0.112 | 0.108 | 0.106 | 0.101 | |

| 9 | 0.090 | 0.101 | 0.098 | 0.096 | 0.091 | |

| 10 | 0.082 | 0.092 | 0.089 | 0.087 | 0.083 | |

| 20 | 0.043 | 0.050 | 0.048 | 0.047 | 0.044 | |

| 30 | 0.029 | 0.034 | 0.033 | 0.032 | 0.030 | |

| 40 | 0.022 | 0.026 | 0.025 | 0.025 | 0.023 | |

| 50 | 0.018 | 0.021 | 0.020 | 0.020 | 0.018 | |

| CPUtime | 4.050 | 3.860 | 4.320 | 5.730 | ||

| Bias (x0.01) | 1.250 | 0.871 | 0.725 | 0.172 | ||

| RMSE (x0.01) | 1.380 | 0.970 | 0.818 | 0.263 | ||

| SD (x0.01) | 0.030 | 0.031 | 0.059 |

| General | Calibration | ||||

| 1 | 0.505 | 0.520 | 0.514 | 0.512 | |

| 2 | 0.308 | 0.323 | 0.317 | 0.316 | |

| 3 | 0.226 | 0.239 | 0.235 | 0.232 | |

| 4 | 0.179 | 0.191 | 0.188 | 0.185 | |

| 5 | 0.149 | 0.160 | 0.157 | 0.155 | |

| 6 | 0.128 | 0.138 | 0.135 | 0.133 | |

| 7 | 0.112 | 0.121 | 0.119 | 0.116 | |

| 8 | 0.100 | 0.108 | 0.107 | 0.104 | |

| 9 | 0.090 | 0.098 | 0.096 | 0.094 | |

| 10 | 0.082 | 0.089 | 0.088 | 0.085 | |

| 20 | 0.043 | 0.048 | 0.047 | 0.046 | |

| 30 | 0.029 | 0.033 | 0.032 | 0.031 | |

| 40 | 0.022 | 0.025 | 0.025 | 0.024 | |

| 50 | 0.018 | 0.020 | 0.020 | 0.019 | |

| CPUtime | 4.050 | 4.320 | 4.710 | 4.880 | |

| Bias (x0.01) | 0.871 | 0.644 | 0.437 | ||

| RMSE (x0.01) | 0.970 | 0.698 | 0.481 | ||

| SD (x0.01) | 0.031 | 0.015 | 0.010 |

5.3 Gaussian random effects bandit

This section compares the performance of a policy based on the SBGIA to that of policies Thompson sampling and Bayes-UCB in case each arm describes the posterior under a Gaussian random effects model. This multi-armed bandit model was not found in literature.

In the Gaussian random effects bandit model, it is assumed that there an additional factor that induces heterogeneity within each of the distributions of choice. The factor induces multiple clusters to which the outcomes are assigned. Outcomes assigned to the same cluster have the same expected value, which deviates from the overall expected value for the distribution. As each deviation is induced by a common factor, the deviations are sampled from a common distribution. The assumed model is (hence) an independent mixed effects model (intercept and random effects) for the outcomes under each of the distributions.

For let be a vector denoting cluster assignment for outcome such that . We assume for all that

| (50) |

where, independently,

The set of model parameters for each arm hence consists of , and no parameters are shared between the arms. The process of cluster assignment is assumed predictable, i.e., all cluster assignments are known prior to assignment to the arm. The prior specification is as follows, we assume a normal prior on each , an inverse-gamma prior on each , and an prior on each .

The above data model and prior specification lead to an analytic expression for the full conditional distribution of each parameter, and hence an efficient Gibbs sampling procedure such as the one in Wang et al. (1993) can be constructed. This Gibbs sampling procedure can then be included in a sequential Markov chain Monte Carlo method (Chopin (2002)) in order to efficiently update approximations of the posterior distribution upon sampling a new observation . For the sequential Markov chain Monte Carlo method the set of observations leads to a collection of samples of particles and weights such that and, denoting with the Dirac measure at ,

| (51) |

Based on this approximation to the posterior, we consider three policies for the Bayesian multi-armed bandit:

-

•

SBGIAP: Determine the SBGIA by sampling future approximations to the posterior from the Markov chain that approximates (41) with transition kernel

where denotes the measure on approximate posteriors induced by a sequential Monte Carlo step using particles, given the current approximation to the posterior and the sampled outcome . The reward function for the Markov chain is given by the posterior mean under the empirical distribution

As in Theorem 6, the SBGIAP now chooses , where is determined as the -th iterate of (18) for a choice of . To decrease the numerical burden, the approximated posteriors in the SBGIAP are based on samples after sampling the first observation , by sampling particles to continue with from the initial distribution .

-

•

Thompson sampling (Thompson (1933)):

Sample and set Choose . -

•

Bayesian upper confidence bound (Bayes-UCB) (Kaufmann et al. (2012a)): Set

where is the empirical quantile given the samples and weights , and where is the total sample size of the experiment. Choose .

The total discounted rewards found under the policies are compared using a simulation study. We note that the policies Bayes-UCB and Thompson sampling, unlike the SBGIAP, are not tuned to a specific discount factor . Other Bayesian bandit policies tuned to a specific discount factor are not known from literature, and introducing them in the current paper would deviate attention from the SBGIAP. Policies Bayes-UCB and Thompson sampling have good performance guarantees for undiscounted reward (Kaufmann et al. (2012b, a)), hence in order to have a fair comparison, we compare the performance of the three policies when higher discount factors are used to determine the total discounted reward, while we tune the SBGIAP to . An outperformance over Bayes-UCB and Thompson sampling in terms of Bayesian total discounted reward (with discount factor ) is expected for the Gittins index policy, as it exactly maximizes this quantity. The SBGIA is however an approximation to the Gittins index, and hence outperformance for the SBGIAP in terms of the Bayesian total discounted reward is not guaranteed, furthermore there is no guarantee that a policy based on the Gittins index tuned to also outperforms other policies for other discount factors . Hence, it is interesting to compare the performance of the policy using a simulation study.

For the simulation study, we set , , , , , . In order to approximate the Bayesian total discounted reward, the parameters were sampled from the resulting prior distributions for each simulation. The sample size of the simulation study was set to , the number of clusters was set to 3, and the number of arms was set to . The cluster assignments were sampled uniformly for each arm . Given the sampled parameters and cluster assignments, the vector of observations were sampled according to model (50). Given the data and cluster assignments, a sequence of weights () and particles was generated for each arm using sequential Markov chain Monte Carlo sampling (starting with a sample from the prior) using 5 Gibbs sampler iterations in each Markov chain Monte Carlo step. Each algorithm then determined an interleaving of these independent Markov chain samples, where for the SBGIAP, we set , , each , , and . The above procedure, resulting in an interleaving of the sampled Markov chain for each algorithm described above, is then repeated independently 2500 times to approximate the Bayesian total discounted reward. This procedure took about 10 days on a computer with 32 cores.

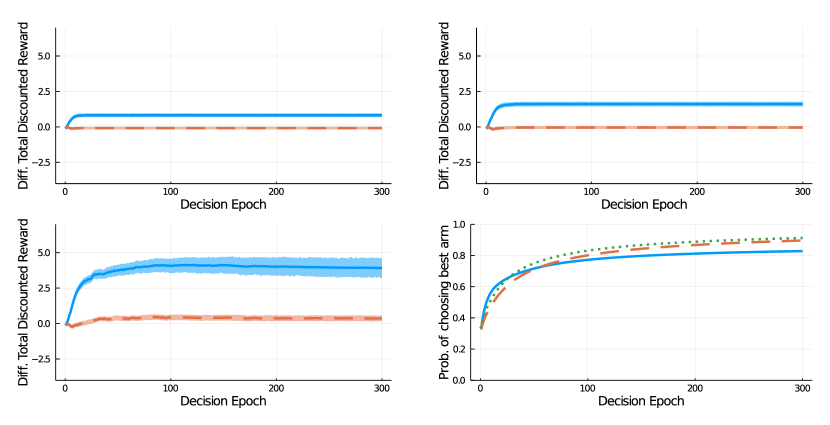

Figure 1 shows results for the SBGIAP with . Differences (averaged over 2500 simulations) between Bayesian total discounted reward for the SBGIAP vs. Bayes-UCB (solid, blue) and Thompson sampling vs. Bayes-UCB (dotted, red) are shown for discount factors , and , along with a point-wise bootstrapped confidence interval for the mean. The total discounted rewards at each decision epoch are calculated as the discounted sum of the expected rewards () from the initial decision epoch up to that time point.

Figure 1 shows that the SBGIAP significantly outperforms Bayes-UCB and Thompson sampling with a final difference in average total discounted reward of about 1, 2 and 4 for discount factors , and respectively.

The average (undiscounted) frequency of choosing the best arm is calculated as the frequency each algorithm chose at each decision epoch. It is seen that while the SBGIAP reaches a frequency of of optimal pulls early on, the other strategies end up at a higher frequency of optimal pulls. This might be a result of the low discount factor used for constructing the policy, indicating that short-term gains are preferred over long-term ones. The bottom-right graph is in line with the other graphs in Figure 1 as, when considering the sum of discounted rewards starting at the initial state, making good choices early on has a larger benefit than outperformance in the long run.

We conclude that with the SBGIAP, significant outperformance in terms of total discounted reward with respect to state-of-the-art policies can be attained for more complex models than usually considered in bandit literature.

6 Discussion and conclusion

In this paper, we have proposed the sampling-based Gittins index approximation (SBGIA). In Section 4, the SBGIA was introduced, and a general error bound was shown for the Gittins index obtained when truncating the horizon and support for the rewards using a stopping time, which can be viewed as an extension of the results presented in Wang (1997). Next, finite and asymptotic convergence results were shown for the SBGIA. Using the finite-time convergence result it is possible to obtain a confidence interval for the Gittins index which holds under a finite number of stochastic approximation samples. Next, it was shown in Theorem 6 that by making explicit choices for the width and safety level of this confidence interval, the policy choosing the largest Gittins index estimate is an -optimal policy for the Bayesian multi-armed bandit problem. For both the Bernoulli and Gaussian bandits, the SBGIA was seen to yield a good approximation to the Gittins index, increasing in quality with the number of nested simulations and the truncation parameter , and showing the best approximation when estimating the limit as goes to infinity. The results indicated that an efficient strategy for Gittins index approximation using SBGIA is to first increase the number of nested simulations, and then increase the truncation parameter , until no significant differences in the estimate are seen for both steps. The SBGIA can be applied even in cases where the actual transition kernel is unknown, but where samples from an approximation to the transition kernel can be generated. An example of this was seen in Section 5.3, where samples from the approximate posterior were generated using sequential Monte Carlo sampling. In this case, the SBGIAP was seen to outperform the state-of-the-art policies Bayes-UCB and Thompson sampling in terms of Bayesian total discounted reward.

The SBGIA can be applied to any family of alternative bandit processes. For example, to compute the Gittins index approximations in Section 5.2, only three things must be altered for each bandit, namely the transition kernel, the reward function, and calculation of the bounds In contrast, for the Calibration method, an additional requirement is that the reward support also has to be discretized and the change in state space leads to a reformulation of the backward induction step. The benefit of a method that works in general, is that there is more flexibility in the model choice when basing treatment allocation on the Gittins index, as there is no increased difficulty in implementing the calculation method when assuming a more elaborate model for the data. Another benefit is that less expert knowledge is necessary for Gittins index approximation. It might be an interesting idea to have a software library where practitioners only have to input functions that calculate, e.g., the posterior mean, after which the package calculates the SBGIA. It is furthermore useful to have a method that does not assume known transition probabilities, as in many real-life cases the posterior distribution cannot be calculated in closed form because of the high dimensionality of the model or when the assumed prior is nonconjugate.

In Section 5.3, we evaluated the performance of the SBGIA policy (SBGIAP) for a novel random effects bandit problem. The SBGIAP was defined based on an approximation of the Markov chain describing the evolution of the posterior distribution, based on sequential Markov chain Monte Carlo. In future research, it would be interesting to investigate how finite-time convergence results for Markov chains (e.g., Rosenthal (1995)) can be used to construct finite-time error bounds for the SBGIA in these situations. In this paper, the SBGIA was evaluated for a number of Bayesian multi-armed bandit problems. In the case of Gaussian outcomes, the Gittins index was shown to result in near-optimal frequentist undiscounted regret (Lattimore (2016)). If this result is shown to hold in general, the confidence interval presented in Theorem 5 ensures that we have a method that can approximate, up to arbitrary precision, a near-optimal policy, in terms of undiscounted frequentist regret, for the multi-armed bandit problem.

References

- Aalto et al. [2011] S Aalto, U Ayesta, and R Righter. Properties of the Gittins index with application to optimal scheduling. Probability in the Engineering and Informational Sciences, 25(3):269–288, 2011.

- Athreya and Lahiri [2006] Krishna B Athreya and Soumendra N Lahiri. Measure theory and probability theory. Springer; New York, 2006.

- Auer et al. [2002] Peter Auer, Nicolo Cesa-Bianchi, and Paul Fischer. Finite-time Analysis of the Multiarmed Bandit Problem. Machine Learning, 47(2):235–256, 2002.

- Boodaghians et al. [2023] S Boodaghians, F Fusco, P Lazos, and S Leonardi. Pandora’s Box Problem with Order Constraints. Mathematics of Operations Research, 48(1):1–602, 2023.

- Borkar [2008] Vivek S Borkar. Stochastic approximation: a dynamical systems viewpoint. Cambridge University Press; Cambridge, 2008.

- Brown [1971] Bruce M Brown. Martingale central limit theorems. The Annals of Mathematical Statistics, 42(1):59–66, 1971.

- Bubeck and Cesa-Bianchi [2012] Sébastien Bubeck and Nicolo Cesa-Bianchi. Regret analysis of stochastic and nonstochastic multi-armed bandit problems. Foundations and Trends in Machine Learning, 5(1):1–122, 2012.

- Chakravorty and Mahajan [2014] Jhelum Chakravorty and Aditya Mahajan. Multi-armed bandits, Gittins index, and its calculation. Methods and Applications of Statistics in Clinical Trials: Planning, Analysis, and Inferential Methods, 2:416–435, 2014.

- Chen and Goldberg [2018] Y. Chen and D. Goldberg. Beating the curse of dimensionality in options pricing and optimal stopping. arXiv preprint, arXiv:1807.02227., 2018. Available at https://arxiv.org/abs/1807.02227v2, (accessed 8-6-2023).

- Chopin [2002] Nicolas Chopin. A sequential particle filter method for static models. Biometrika, 89(3):539–552, 2002.

- Chung [1954] Kai Lai Chung. On a stochastic approximation method. The Annals of Mathematical Statistics, 25(3):463–483, 1954.

- Diaconis and Ylvisaker [1979] Persi Diaconis and Donald Ylvisaker. Conjugate priors for exponential families. The Annals of Statistics, 7(2):269–281, 1979.

- Edwards [2019] James Edwards. Practical calculation of Gittins indices for multi-armed bandits. arXiv preprint arXiv:1909.05075, 2019. Available at https://arxiv.org/abs/1909.05075 (accessed 12-6-2023).

- Fisher [1986] Evan Fisher. An upper class law of the iterated logarithm for supermartingales. Sankhyā: The Indian Journal of Statistics, Series A, 48:267–272, 1986.

- Ghosal and Van der Vaart [2017] Subhashis Ghosal and Aad Van der Vaart. Fundamentals of nonparametric Bayesian inference. Cambridge University Press; Cambridge, 2017.

- Gilks et al. [1995] Walter R Gilks, Sylvia Richardson, and David Spiegelhalter. Markov chain Monte Carlo in practice. CRC press; Routledge, 1995.

- Gittins [1979] John Gittins. Bandit processes and dynamic allocation indices. Journal of the Royal Statistical Society. Series B (Methodological), 41(2):148–177, 1979.

- Gittins et al. [2011] John Gittins, Kevin Glazebrook, and Richard Weber. Multi-armed bandit allocation indices. John Wiley & Sons: Hoboken, 2011.

- Glazebrook [1982] Kevin D Glazebrook. On the evaluation of suboptimal strategies for families of alternative bandit processes. Journal of Applied Probability, 19(3):716–722, 1982.

- Glazebrook [1983] Kevin D Glazebrook. Optimal strategies for families of alternative bandit processes. IEEE Transactions on Automatic Control, 28(8):858–861, 1983.

- Glazebrook and Minty [2009] Kevin D Glazebrook and R Minty. A generalized Gittins index for a class of multiarmed bandits with general resource requirements. Mathematics of Operations Research, 34(1):26–44, 2009.

- Kaufmann [2018] Emilie Kaufmann. On Bayesian index policies for sequential resource allocation. The Annals of Statistics, 46(2):842–865, 2018.

- Kaufmann et al. [2012a] Emilie Kaufmann, Olivier Cappé, and Aurélien Garivier. On Bayesian upper confidence bounds for bandit problems. In Proceedings of the Fifteenth International Conference on Artificial Intelligence and Statistics, volume 22 of Proceedings of Machine Learning Research, pages 592–600, 2012a.

- Kaufmann et al. [2012b] Emilie Kaufmann, Nathaniel Korda, and Rémi Munos. Thompson Sampling: An Asymptotically Optimal Finite-Time Analysis. In Nader H. Bshouty, Gilles Stoltz, Nicolas Vayatis, and Thomas Zeugmann, editors, Algorithmic Learning Theory, pages 199–213. Springer; Berlin, Heidelberg, 2012b.

- Kuleshov and Precup [2014] Volodymyr Kuleshov and Doina Precup. Algorithms for multi-armed bandit problems. arXiv preprint arXiv:1402.6028., 2014. available at https://arxiv.org/abs/1402.6028 (accessed 8-6-2023).

- Lai and Robbins [1978] T L_ Lai and Herbert Robbins. Limit theorems for weighted sums and stochastic approximation processes. Proceedings of the National Academy of Sciences, 75(3):1068–1070, 1978.

- Lai and Robbins [1979] T L_ Lai and Herbert Robbins. Adaptive design and stochastic approximation. The Annals of Statistics, 7(6):1196–1221, 1979.

- Lai [1987] Tze Leung Lai. Adaptive treatment allocation and the multi-armed bandit problem. The Annals of Statistics, 15(3):1091–1114, 1987.

- Lai et al. [1985] Tze Leung Lai, Herbert Robbins, et al. Asymptotically efficient adaptive allocation rules. Advances in Applied Mathematics, 6(1):4–22, 1985.

- Lattimore and Szepesvári [2020] T. Lattimore and C. Szepesvári. Bandit algorithms. Cambridge University Press; Cambridge, 2020.

- Lattimore [2016] Tor Lattimore. Regret Analysis of the Finite-Horizon Gittins Index Strategy for Multi-Armed Bandits. In Vitaly Feldman, Alexander Rakhlin, and Ohad Shamir, editors, 29th Annual Conference on Learning Theory, volume 49 of Proceedings of Machine Learning Research, pages 1214–1245, 23–26 Jun 2016.

- Mahajan and Teneketzis [2008] Aditya Mahajan and Demosthenis Teneketzis. Multi-armed bandit problems. In A.O. Hero, D. Castañón, D. Cochran, and K. Kastella, editors, Foundations and Applications of Sensor Management, Signals and Communication Technology, chapter 6, pages 121–151. Springer: New York, 2008.

- Neuenschwander et al. [2020] B Neuenschwander, S Weber, H Schmidli, and A O’Hagan. Predictively consistent prior effective sample sizes. Biometrics, 76(2):578–587, 2020.

- Puterman [1990] Martin L Puterman. Markov decision processes. In D.P. Heyman and M.J. Sobel, editors, Handbooks in Operations Research and Management Science, volume 2, chapter 8, pages 331–434. Elsevier; Amsterdam, 1990.

- Robbins [1952] Herbert Robbins. Some aspects of the sequential design of experiments. Bulletin of the American Mathematical Society, 58(5):527–535, 1952.

- Robbins and Monro [1951] Herbert Robbins and Sutton Monro. A stochastic approximation method. The Annals of Mathematical Statistics, 22(3):400–407, 1951.

- Robertson et al. [2023] David S Robertson, Kim May Lee, Boryana C López-Kolkovska, and Sofía S Villar. Response-adaptive randomization in clinical trials: from myths to practical considerations. Statistical science, 38(2):185–208, 2023.

- Rosenthal [1995] J S Rosenthal. Convergence rates for markov chains. Siam Review, 37(3):387–405, 1995.

- Slivkins [2019] Aleksandrs Slivkins. Introduction to Multi-Armed Bandits. Foundations and Trends® in Machine Learning, 12(1-2):1–286, 2019.

- Thompson [1933] William R Thompson. On the likelihood that one unknown probability exceeds another in view of the evidence of two samples. Biometrika, 25(3–4):285–294, 1933.

- Villar et al. [2015a] S. S. Villar, J. Bowden, and J. Wason. Multi-armed bandit models for the optimal design of clinical trials: benefits and challenges. Statistical Science, 30(2):199–215, 2015a.

- Villar et al. [2015b] Sofía S. Villar, James Wason, and Jack Bowden. Response-adaptive randomization for multi-arm clinical trials using the forward looking Gittins index rule. Biometrics, 71(4):969–978, 2015b.

- Wang et al. [1993] CS Wang, JJ Rutledge, and D Gianola. Marginal inferences about variance components in a mixed linear model using Gibbs sampling. Genetics Selection Evolution, 25:41–62, 1993.

- Wang [1997] You-Gan Wang. Error bounds for calculation of the Gittins indices. Australian Journal of Statistics, 39(2):225–233, 1997.

- Weber [1992] Richard Weber. On the Gittins index for multiarmed bandits. The Annals of Applied Probability, 2(4):1024–1033, 1992.

- Weber and Weiss [1990] Richard Weber and Gideon Weiss. On an index policy for restless bandits. Journal of applied probability, 27(3):637–648, 1990.

- Yao [2006] Yi-Ching Yao. Some results on the Gittins index for a normal reward process. In Time Series and Related Topics, volume 52 of Lecture Notes–Monograph Series, pages 284–294. Institute of Mathematical Statistics, 2006.

Appendix A Proofs of theorems

Theorem 3.

Under Assumption 1 there is a unique real number attaining the supremum

In fact, is the unique root of

The infimum in the condition is attained for some .

Furthermore, with for , it holds that

Proof.

Let be a Markov chain with states . Let . The pair defines a Markov reward process as is a function of . As the filtrations and hence the set of stopping times generated by and are the same, we have

| (52) |

Note that as Assumption 1 holds for the Markov reward process defined by , it also holds for the Markov reward process defined by . Hence from Lattimore and Szepesvári [2020] there is an unique value for , denoted by , such that the left-hand side, hence the right-hand side of (52) is zero. As is a scaling of (52), the first two statements of the theorem are proven. From Lattimore and Szepesvári [2020], we also have that the supremum in (52) is attained for an unique stopping time , proving the third statement.

Now, we bound the approximation error from above (the lower bound holds trivially):

The second to last inequality above holds by the strong Markov property and as almost surely. The “positive part" of the Gittins index in the last term above comes from the fact that we can take in the seventh term. ∎

Theorem 4.

For , initial point , and martingale difference sequence (21), let the sequence be defined as

Assume the step-size sequence is such that almost surely. Then for all

Proof.

Let such that and are -measurable. Then, as for , we have

| (53) |

Now, by (25), letting we have

Hence

The last line above follows as , hence for all by the assumptions on and the maximum will be attained at the first argument if where and the maximum will be attained at the second argument if where . Then, continuing (53), we have:

To conclude, taking expectations, we have

where . ∎

Lemma 1.

Let almost surely. We have almost surely that for all

Proof.

Note that if it holds that irrespective of the path

For , we hence have irrespective of the path , that when

From this, we see that for

Hence for we have almost surely

Similarly, observe that almost surely if . Hence by (18) we have almost surely for all that

∎

Lemma 4.

If for all the cumulative distribution functions of starting from have finitely many jumps, then for all but finitely many points the function is differentiable with derivative

where , and

Proof.

First, we show by induction that for all , , random times and sets in (the smallest product sigma algebra measuring all versions ) we have

where , are random variables only depending on through the minimizers for .

For the result is immediately verified for and .

Second, we show that all but finitely many points we have

For and let be where every nested random time is replaced by the elements of consecutively, and let be defined similarly for , note that this makes deterministic.

For

The indicators above converge to when which has nonzero probability of being equal to one for at most finitely many points by the assumption. The direction can be shown by changing the first bound above to

and following the same steps as above.

Third, we show for points where all functions are continuous for that

| (54) |

Note that, by the second step above, the complement of this set is a subset of the set of jump points for the cumulative distribution functions of for all

We show the result by induction. Let , then we have for

By the choice of we have that the upper and lower bound almost everywhere almost surely converge to when . The case can be shown similarly.

Let the above statement hold up to , then for

Taking above we see that

Similarly, it can be shown that

Now, by the choice of , we know there is a random variable such that almost surely for all such that . Hence, for every sample path, for close enough to , we condition on above. From this it follows that almost surely

hence (54) holds. The case works similarly.

By induction it can be verified that the right-hand side of (54) is bounded for each .

We have for and

When by continuity and boundedness of the derivative the first term goes to

while the second term goes to zero by continuity (of ) and boundedness, where in both cases the dominated convergence theorem was used. ∎

Theorem 9.

Let be independent versions (in ) of , and

Let

Let be the set of points where is differentiable. If , then there is a unique point such that . If the derivative of exists at and , we have

| (55) |

Proof.

The first statement is trivial as has a positive derivative wherever the derivative is defined. We show the second statement by first verifying that the Robbins-Monro conditions hold almost surely, hence by Corollary 1 we have that converges almost surely to . As for a constant we have we have that almost surely. We verify that almost surely. Let and By the strong law of large numbers for martingales we have (by boundedness of ) that almost surely

| (56) |

Letting be such that for all we can choose and have an such that for all

We then conclude

Hence it follows by Corollary 1 that .

Now, if the derivative of at would not exist, hence almost surely for all we have and combined with the above result it follows that (with independently) almost surely by continuous mapping (noting that the set of discontinuity points of is restricted to a deterministic set). By boundedness we also have Similarly, it can be shown that which is deterministic. Hence and by (56) and continuous mapping we have

The result follows along the lines of Lai and Robbins [1978], with three additional remarks.

-

•

In order to use the representation (17) in Lai and Robbins [1978] the recursion of the stochastic approximation has to be truncated earlier, to make sure that the iterates remain in an interval around where is differentiable, so as to use the mean value theorem.

-

•

The martingale central limit theorem (Theorem 2 in Brown [1971]) can be used to show a central limit theorem result for the martingale , as the running mean of the quadratic variation process converges to a constant, we can show a central limit theorem result by just dividing by .

- •

∎

Appendix B Notation Table

| Symbol | Definition | Defined in |

| Markov chain/arm | Sec. 2 | |

| Time index | Sec. 2 | |

| Initial state of an arm | Sec. 2 | |

| Transition kernel and expectation for the Markov chains, conditional on initial state | Sec. 2 | |

| Set of histories | (1) | |

| Common reward function for the arms | Sec. 2 | |

| Policy and optimal policy (resp.) for the family of alternative bandit processes | Sec. 2 | |

| Total discounted absolute reward for sampling arm , starting from state | Sec. 2 | |

| Expectation operator under a fixed policy | Sec. 2 | |

| Discount factor | Sec. 2 | |

| Gittins index for state | Sec. 2 | |

| Natural filtration generated by and (resp.), including starting state | Sec. 2, 3.1 | |

| Set of stopping times w.r.t. or (resp.) | Sec. 2, 3.1 | |

| State of Markov chain/arm and general arm (resp.) at time | Sec. 2, 3.1 | |

| Stopping time, used to determine optimal stopping value | Sec. 2 | |

| Sampling horizon for optimal stopping value | Sec. 3.1 | |

| Set of stopping times adapted to and bounded by | Sec. 3.1 | |

| Measurable real-valued cost function | Sec. 3.1 | |

| Cost of an arm up to time | Sec. 3.1 | |

| Sec. 3.1 | ||

| Truncation point of number of nested expectations in optimal stopping approximation | Sec. 3.1 | |

| Sampling-based approximation of | Sec. 3.2 | |

| Number of simulated paths used to determine | Sec. 3.2 | |

| Sampling-based approximation of and | Sec. 3.2, 4 | |

| Stopping time, used to truncate the support of the rewards | (15) | |

| Upper and lower bound for reward support (resp.), induced by stopping time | Sec. 4 | |

| Constant, equal to | Sec. 4 | |

| Cost of an arm up to the minimum of time and | Sec. 4 | |

| Gittins index approximation found by truncation of horizon and reward support | (16) | |

| Stochastic approximation iterates for determining SBGIA | (18) | |

| Step-size sequence | Sec. 4 | |

| Sampling-based Gittins index approximation | Sec. 4 | |

| Expectation of | (19) | |

| Optimal stopping value | (19) | |

| Domain error bound, equal to | (20) | |

| Martingale difference sequence | (21) | |